Embed Size (px)

Citation preview

Marrying Your

Finances

The WII Group, LLC

Jeff Wilson II, CPA, CGMA, AFC

Personal Finance Counselor

Presented at Mt. EnnonBaptist Church

8 Keys to Effective Business

Partnerships

1. Commitment to a common mission

2. Unselfishness

3. Complimentary Communication

4. Ongoing Communication

5. Acceptance of Differences

6. Forgiveness

7. Fairness

8. Trust

“ There can be no freedom or

beauty about a home life that

depends on borrowing and debt.”

-Henrik Ibsen

Rule # 1

Financial responsibility means that youare accountable for your future

financial well-being and nobody else.

ACHIEVE

INVEST in Mutual Funds Stocks and Bonds Real Estate Retirement Plans

HANDLE the Credit Cards Installment loans Savings Account Education costs

Housing Expenses Transportation expenses

Insurance expenses

Income taxes ContingenciesMANAGE the

Long-term goals Short-term goals Organized financial records

Realistic budget Emergency savings fund

ESTABLISH

Checking Account Savings Account Money Market Account

Insurance protection

Employee benefits

Create a BASE

FOUNDATIONUse of regular income to provide basic lifestyle and savings

Financial Successful

House

Building a House of Love

Topic Areas

1. Financial Planning

2. Community vs. Common Law

3. Income Taxes

Financial Planning: The Process

1. Evaluate your financial condition

2. Define your financial goals

3. Develop a plan of action to achieve your goals

4. Implement your plan

5. Review your financial progress and make changes as appropriate (every 3 months)

Financial Planning: Evaluate your Financial Condition

1. Before the wedding , reveal everything in your financial closet (NO skeletons).

2. Order a free copy of your credit reports (www.annual creditreport.com)

3. Set preliminary financial goals both long and short (goals are likely to change after step #3)

4. Develop Personal Financial Statements (optional: with help of Financial Counselor or Financial Planner)

Create an Income Statement/Financial Portrait-(past)

Develop a Balance Sheet/Financial Portrait (present)

Household Budget Planner/Zero-Based Budget (future)

Financial Planning: Set Preliminary Financial Goals

Financial Plan Areas Long-term Goals and Objectives Short-term Goals and Objectives

For Spending

Evaluate and plan major purchase Purchase a new can in two years Begin saving $200 a month for a down payment of a car

Manage debt Keep installment debt under 10% of take-home pay Pay off charge cards at end of each month

For Risk Management

Medical costs Avoid late medical costs Maintain employer-subsidized medical insurance policy by paying $135monthly premium

Property and casualty losses Always have renters or homeowners insurance Make semiannual premium payment of $220 on renters insurance policy

Always have maximum automobile insurance coverage Make premium payments of $440 on automobile insurance policy

Liability losses Eventually buy $1 million liability insurance Rely on $100,000 policy purchased from same source as automobile insurance policy

Premature death Have adequate life insurance coverage for both Buy life insurance

Income loss from liability Buy sufficient disability insurance Rely on sick days and seek disability insurance through private insurance

For Capital Accumulation

Tax fund

Have enough money for taxes withheld from salaries

by both employers Confirm that employer withholding of taxes is sufficient.

Revolving savings fund

Always have sufficient cash in local accounts to meet

monthly budgets expenses Develop cash-flow calendar to ascertain needs. Keep all funds in interest earning accounts

Emergency fund

Build up monetary assets equivalent to three months

take home pay Put $150 per month into an emergency fund until is totals one month's take-home pay

Education

Maintain educational skills and credentials to remain

competitive Both take one graduate class per term

Savings Always have a nice sized savings balance

Investment

Own substantial shares of a conservative mutual fund

that will pay dividends equivalent to about 10% of

family income Start investing in a mutual fund before next year

Retirement

Retire at age 60 or earlier on income that is the same as

the take home-pay earned jest before retirement

Establish an IRA before next year. Contribute the maximum possible amount to employer-

sponsored retirement account

Estate planning Provide for surviving spouse Each spouse make a will

Financial Planning: Develop a Income Statement

Monthly Income Budget You

YOURS SPOUSE,

PARTNER, OR OTHER

CONTRIBUTING

MEMBER TOTAL

Employment (1) see notes 4,140.00$ -$ 4,140.00$

Overtime - - -

Child Support/Alimony (2) see notes - - -

Pension - - -

Interest - - -

Public Benefits (3) see notes - - -

Dividends - - -

Trust Payments - - -

Royalties - - -

Rents Received 1,250.00 - 1,250.00

Help from Friends or Relatives (HRSA loan repay)1,606.00 - 1,606.00

Other(List) 1,908.00 - 1,908.00

Total (MONTHLY) 8,904.00$ -$ 8,904.00$

MONTHLY INCOME BUDGET

Financial Planning: Develop a Income Statement

Monthly Income Budget You

YOURS SPOUSE,

PARTNER, OR OTHER

CONTRIBUTING

MEMBER TOTAL

EXPENSE TYPES (4) see notes

Payroll Deductions (5) see notes -$ -$ -$

Income Tax Withheld 175.00 - 175.00

Social Security - - -

FICA - - -

Wage Garnishments - - -

Credit Union - - -

Other - - -

Home Related Expenses 3,420.00$ -$ 3,420.00$

Mortgage or Rent (6) see notes 1,776.00 - 1,776.00

Second Mortgage - - -

Third Mortgage - - -

Real Estate Taxes (7) see notes - - -

Insurance (8) see notes 35.00 - 35.00

Condo Fees & Assessments 245.00 - 245.00

Mobile Home Lot Rent - - -

Home Maintenance/Upkeep - - -

Other 1,364.00 - 1,364.00

Utilities 379.00$ -$ 379.00$

Gas 60.00 - 60.00

Electric 90.00 - 90.00

Oil - - -

Water/Sewer - - -

Telephone: - - -

Land Line - - -

Cell 104.00 - 104.00

Cable TV 125.00 - 125.00

Internet - - -

Other - - -

MONTHLY EXPENSE BUDGET

Financial Planning: Evaluate Your Financial Condition

Financial Planning: Evaluate Your Financial Condition

Financial Planning: Financial Goals

Financial Plan Areas Long-term Goals and Objectives Short-term Goals and Objectives

For Spending

Evaluate and plan major purchase Purchase a new can in two years Begin saving $200 a month for a down payment of a car

Manage debt Keep installment debt under 10% of take-home pay Pay off charge cards at end of each month

For Risk Management

Medical costs Avoid late medical costs Maintain employer-subsidized medical insurance policy by paying $135monthly premium

Property and casualty losses Always have renters or homeowners insurance Make semiannual premium payment of $220 on renters insurance policy

Always have maximum automobile insurance coverage Make premium payments of $440 on automobile insurance policy

Liability losses Eventually buy $1 million liability insurance Rely on $100,000 policy purchased from same source as automobile insurance policy

Premature death Have adequate life insurance coverage for both Buy life insurance

Income loss from liability Buy sufficient disability insurance Rely on sick days and seek disability insurance through private insurance

For Capital Accumulation

Tax fund

Have enough money for taxes withheld from salaries

by both employers Confirm that employer withholding of taxes is sufficient.

Revolving savings fund

Always have sufficient cash in local accounts to meet

monthly budgets expenses Develop cash-flow calendar to ascertain needs. Keep all funds in interest earning accounts

Emergency fund

Build up monetary assets equivalent to three months

take home pay Put $150 per month into an emergency fund until is totals one month's take-home pay

Education

Maintain educational skills and credentials to remain

competitive Both take one graduate class per term

Savings Always have a nice sized savings balance

Investment

Own substantial shares of a conservative mutual fund

that will pay dividends equivalent to about 10% of

family income Start investing in a mutual fund before next year

Retirement

Retire at age 60 or earlier on income that is the same as

the take home-pay earned jest before retirement

Establish an IRA before next year. Contribute the maximum possible amount to employer-

sponsored retirement account

Estate planning Provide for surviving spouse Each spouse make a will

Prioritizing Savings and Retirement

• Contribute at a minimum 5% to 10% of salary to 401K, TSP, or 403-B retirement plans.

• Plan to save 8-10% of salary in savings; or have at least 6 months of households expenses in cash savings

• Ensure that all of you risks which you cannot save for are insured

• Begin planning for your child's education with your retirement in mind

• Avoid taking on “non mortgage debt” greater than 5% of your gross salary

• Avoid eating out during the month

Financial Planning: Develop A Plan of Action

Prioritizing Credit and Spending

• Avoid using credit cards for purchases that you don’t’ have the cash for

• Debts with collateral are almost always your highest priority debts

• Creditors making the most noise are not necessarily your most important creditor.

• Always pay family necessities first

• Do not move a debt up in priority because the creditor or collector threatens suit

Financial Planning: Develop A Plan of Action

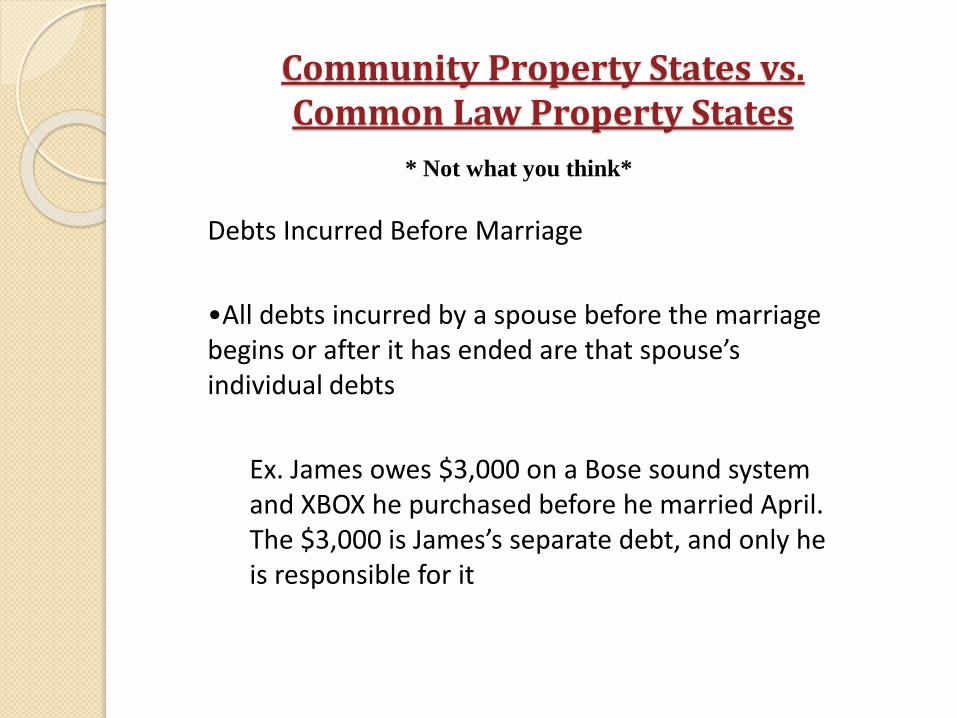

Community Property States vs. Common Law Property States

Who Owns that Debt or Property, when your married??

MD, DC, VA are all Common law property states

Community Property – in most situations husband and wife act as a “community” acquiring property and incurring debt as unit

Common Law States – the assumption is that property acquired by the spouses together and held in both names is marital property, while all other is separate

* Not what you think*

* Not what you think*

• Community Property- Community property is liable for all joint debts (debts incurred for the benefit of the community)

• Who Owes the Debts – If you live in a common law property state, who owes what debt depends on when the debt was incurred and in some instances what the debt was for

Community Property States vs. Common Law Property States

* Not what you think*

Debts Incurred Before Marriage

•All debts incurred by a spouse before the marriage begins or after it has ended are that spouse’s individual debts

Ex. James owes $3,000 on a Bose sound system and XBOX he purchased before he married April. The $3,000 is James’s separate debt, and only he is responsible for it

Community Property States vs. Common Law Property States

* Not what you think*

Debts Incurred During Marriage

•All debts incurred by the spouses jointly during the marriage are joint debts. All debts incurred by one spouse during the marriage and before permanent separation are separately owed by that spouse unless any of the following is true:

1. The creditor looked to both spouses or considered both spouses credit information before approving credit

2. The debt was incurred for family necessities, such as food, clothing, or shelter

3. The debt was incurred for medical purposes (in some but not all common law states)

Community Property States vs. Common Law Property States

Income Taxes for Married Couples

Income Taxes

Seven Tax Tips for Recently Married Taxpayers

• Notify the Social Security Administration Report any name change to the Social Security Administration so your name and Social Security number will match when you file your next tax return. File a Form SS-5, Application for a Social Security Card, at your local SSA office. The form is available on SSA’s website at www.ssa.gov, by calling 800-772-1213 or at local offices.

• Notify the IRS if you move If you have a new address you should notify the IRS by sending Form 8822, Change of Address. You may download Form 8822 from www.IRS.gov or order it by calling 800–TAX–Form(800–829–3676 ).

• Notify the U.S. Postal Service You should also notify the U.S. Postal Service when you move so it can forward any IRS correspondence or refunds.

• Notify your employer Report any name and address changes to your employer(s) to make sure you receive your Form W-2, Wage and Tax Statement, after the end of the year.

Income Taxes

• Check your withholding If both you and your spouse work, your combined income may place you in a higher tax bracket. You can use the IRS Withholding Calculator available on www.irs.gov to assist you in determining the correct amount of withholding needed for your new filing status. The IRS Withholding Calculator will give you the information you need to complete a new Form W-4, Employee's Withholding Allowance Certificate. You can fill it out and print it online and then give the form to your employer(s) so they withhold the correct amount from your pay.

• Select the right tax form Choosing the right individual income tax form can help save money. Newly married taxpayers may find that they now have enough deductions to itemize on their tax returns. Itemized deductions must be claimed on a Form 1040, not a 1040A or 1040EZ.

• Choose the best filing status A person’s marital status on Dec. 31 determines whether the person is considered married for that year. Generally, the tax law allows married couples to choose to file their federal income tax return either jointly or separately in any given year. Figuring the tax both ways can determine which filing status will result in the lowest tax, but usually filing jointly is more beneficial.

Income Taxes for Married Couples

Disadvantages of Married Filing Separately

Earned Income Credit

Child Care credit (unless spouses lived apart for last six months)

Education Credits

Lost Credits

Lost Education Benefits Student loan interest deduction

Tuition and fees deduction

Savings bond interest exclusion

Standard Deduction If one spouse itemizes deductions, the other must also itemize ( that

is, cannot claim the standard deduction)

Taxable Social Security A greater percentage of Social Security benefits may be taxable

unless the spouses lived apart for the entire year

IRA deduction and contributions phased out

Spousal IRA rules do not apply

IRAs

Net Capital loss deduction is limited to $1,500 per spouseCapital Losses

Sale of Home Gain exclusion is limited to $250,000 per spouse

In addition to the exemption phasing out, some high income

taxpayers must add an amount back to AMTI.

AMT Exemption

Income Taxes for Married Couples

QUESTIONS, COMMENTS, OR CONCERNS?

Contact Information: Jeff Wilson II, CPA, AFCEmail: [email protected] address: http://www.wiicpas.com