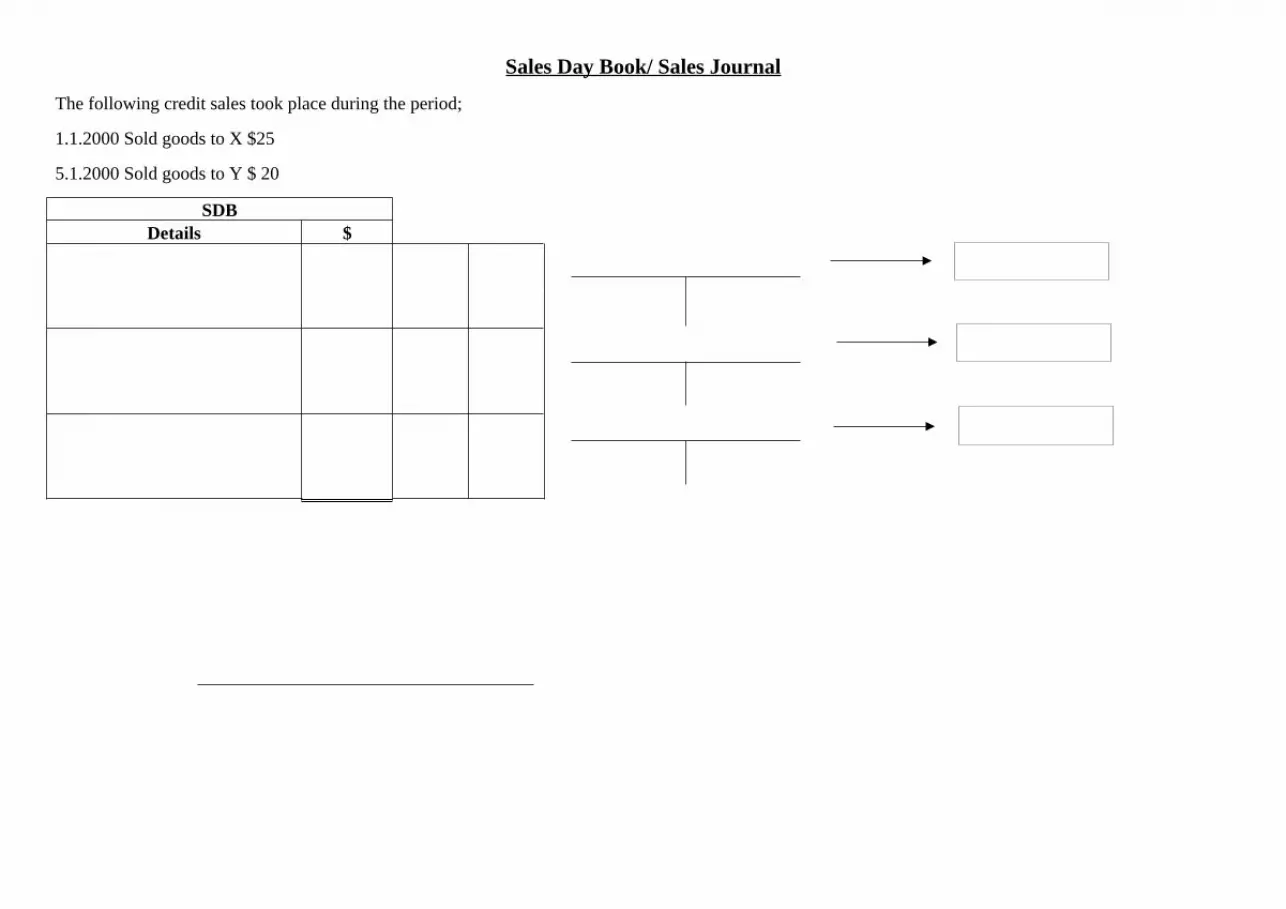

Sales Day Book/ Sales Journal

The following credit sales took place during the period;

1.1.2000 Sold goods to X $25

5.1.2000 Sold goods to Y $ 20

SDBDetails $

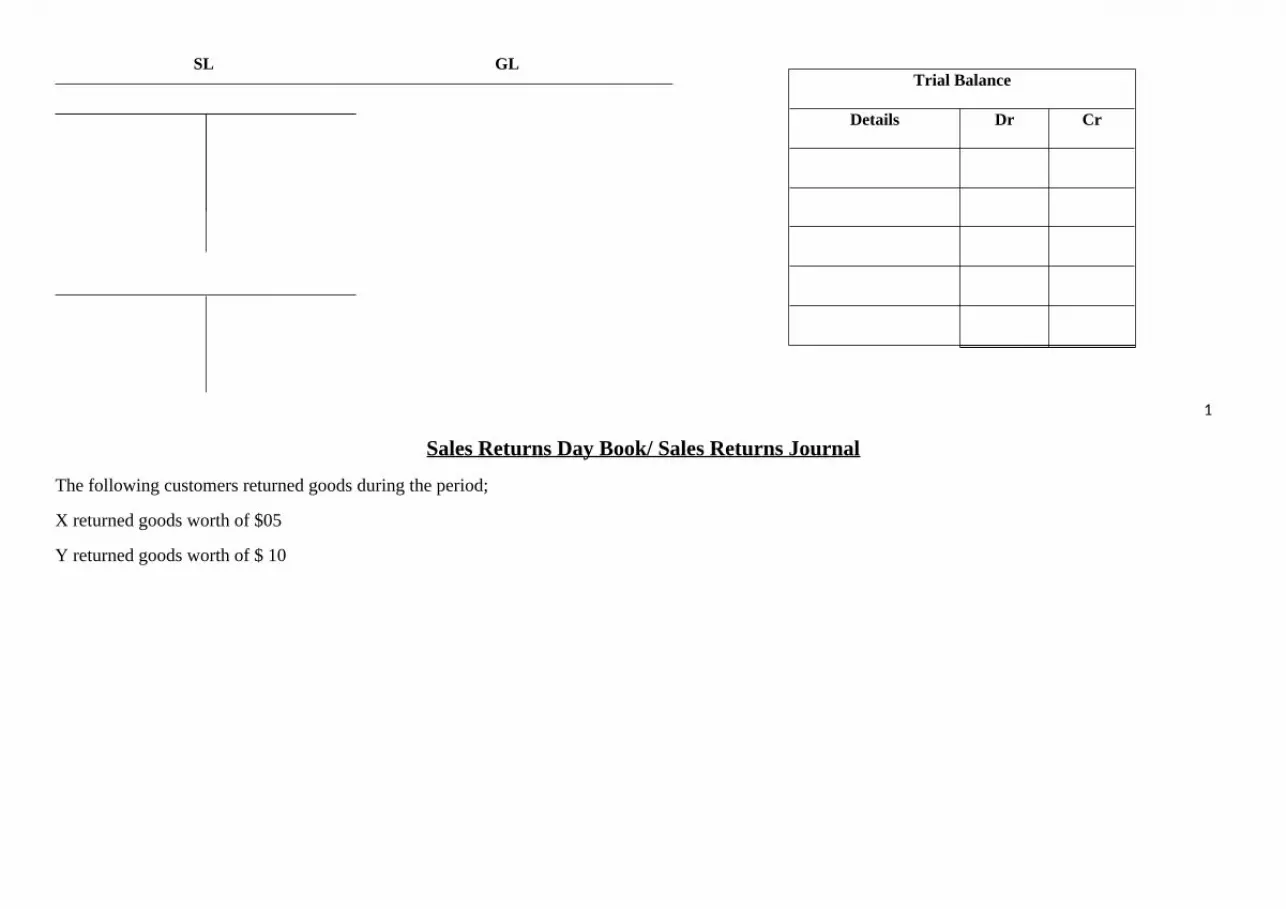

SL GL

Sales Returns Day Book/ Sales Returns Journal

The following customers returned goods during the period;

X returned goods worth of $05

Y returned goods worth of $ 10

1

Trial Balance

Details Dr Cr

SL GL

SRDBDetails $

Trial Balance

Details Dr Cr

Purchases Day Book/ Purchases Journal

The following credit Purchases took place during the period;

1.1.2000 Purchased goods from A $35

5.1.2000 Purchased goods from B $ 25

2

SDBDetails $

SL GL

Purchases Returns Day Book/ Purchases Returns Journal

The following customers returned goods during the period;

Goods returned to A worth of $15

Goods returned to B worth of $ 10

3

Trial Balance

Details Dr Cr

SL GL

4

SRDBDetails $

Trial Balance

Details Dr Cr

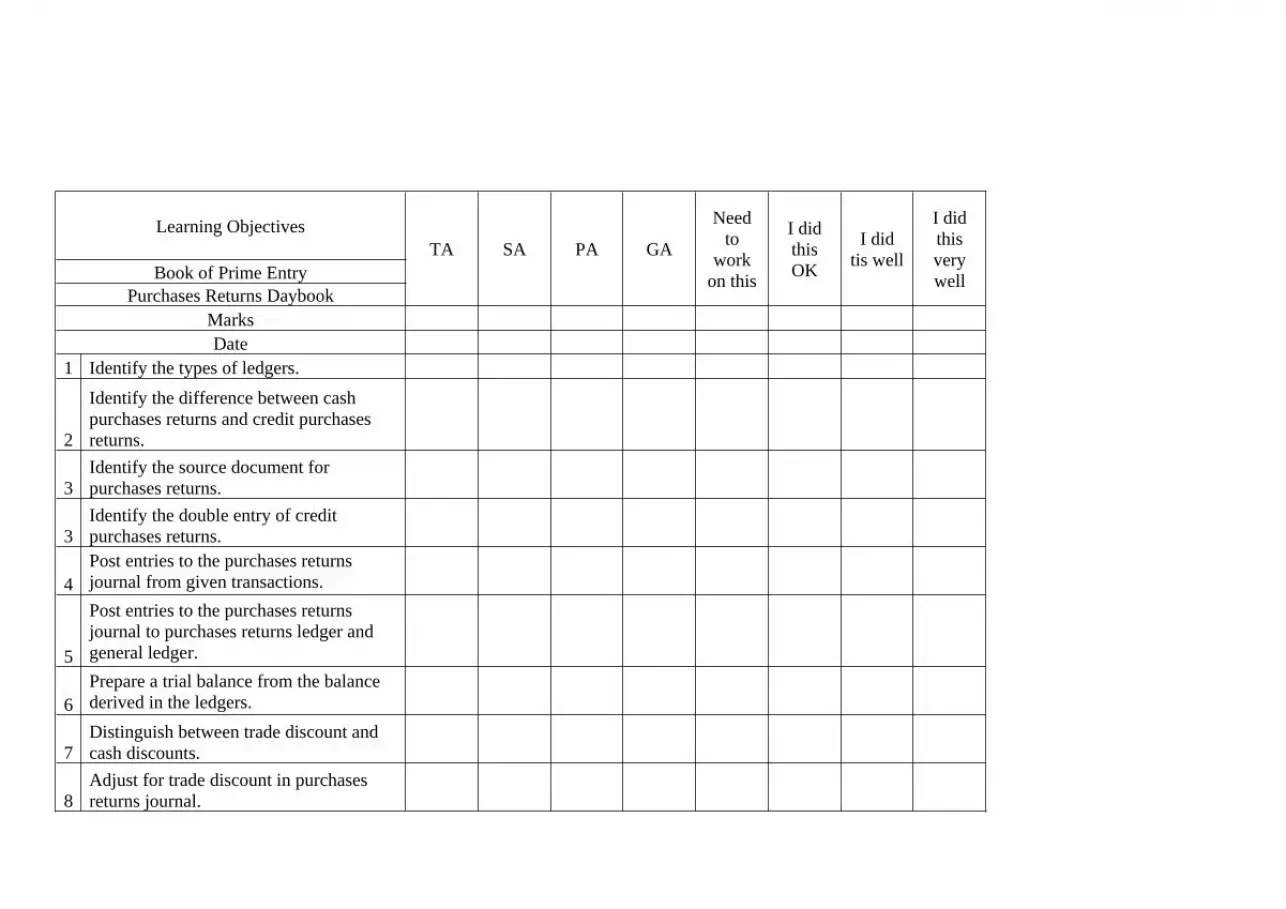

TA - Teacher Assessment

SA - Student Assessment

PA - Peer Assessment

GA - Group Assessment

4

Learning ObjectivesTA SA PA GA

Need to

work on this

I did this OK

I did tis well

I did this very wellBook of Prime Entry

Purchases Returns DaybookMarks Date

1 Identify the types of ledgers.

2

Identify the difference between cash purchases returns and credit purchases returns.

3Identify the source document for purchases returns.

3Identify the double entry of credit purchases returns.

4Post entries to the purchases returns journal from given transactions.

5

Post entries to the purchases returns journal to purchases returns ledger and general ledger.

6Prepare a trial balance from the balance derived in the ledgers.

7Distinguish between trade discount and cash discounts.

8Adjust for trade discount in purchases returns journal.

9Adjust for cash discount in trade payable and discount received account.

Learning ObjectivesTA SA PA GA

Need to

work on this

I did this OK

I did tis well

I did this very wellBook of Prime Entry

Purchases DaybookMarks Date

1 Identify the types of ledgers.

2Identify the difference between cash purchases and credit purchases.

3Identify the source document for credit purchases.

3Identify the double entry of credit purchases.

4Post entries to the purchases journal from given transactions.

5

Post entries to the purchases journal to purchases ledger and general ledger.

6Prepare a trial balance from the balance derived in the ledgers.

7Distinguish between trade discount and cash discounts.

8Adjust for trade discount in purchases journal.

9Adjust for cash discount in trade payable and discount received account.

Learning ObjectivesTA SA PA GA

Need to

work on this

I did this OK

I did tis well

I did this very wellBook of Prime Entry

Sales DaybookMarks Date

1 Identify the types of ledgers.

2Identify the difference between cash sales and credit sales.

3Identify the source document for credit sales.

4 Identify the double entry of credit sales.

5Post entries to the sales journal from given transactions.

6Post entries to the sales journal to sales ledger and general ledger.

7Prepare a trial balance from the balance derived in the ledgers.

8Distinguish between trade discount and cash discounts.

9Adjust for trade discount in sales journal.

10

Adjust for cash discount in trade receivables and discount allowed account.

Learning ObjectivesTA SA PA GA

Need to

work on this

I did this OK

I did tis well

I did this very wellBook of Prime Entry

Sales Returns DaybookMarks Date

1 Identify the types of ledgers.

2Identify the difference between cash sales returns and credit sales returns.

3Identify the source document for sales returns.

3Identify the double entry of credit sales returns.

4Post entries to the sales returns journal from given transactions.

5

Post entries to the sales returns journal to sales returns ledger and general ledger.

6Prepare a trial balance from the balance derived in the ledgers.

7Distinguish between trade discount and cash discounts.

8Adjust for trade discount in sales returns journal.

9

Adjust for cash discount in trade receivables and discount allowed account.

http://keydifferences.com/difference-between-trade-discount-and-cash-discount.html

Date Details Dr Cr Date Details Dr Cr

Trade receivables balances are as follows for the year 2003;

Trade Receivable Date Credit Sales

$

Date Sales Returns Date Total due Discount

Allowed

Payment

received by

cheque

Aleen 1.1.2003 2,500 5.1.2003 500 15.1.2003

Aleena 5.1.2003 4,000 6.1.2003 300 10.1.2003

Maheen 10.1.2003 500 12.1.2003 100 30.1.2003

The company policy is to provide 10 % cash discount for the payments made within 20 days.

Guidelines;

1. Carefully go through the table and understand the information provided.2. Calculate the total due of each of the trade receivable.3. From the date of sale identify the customers those who are eligible for a cash discount.4. Provide cash discount for identified trade receivables.5. Identify how much each trade receivable will pay by cheque.6. Recall the double entry for the following;

a. Credit salesb. Sales returnsc. Discount allowed d. Cash/ bank received from the trade receivables

7. Post entries in the above sequence8. Balance off the accounts ( do not balance off the cash ledger)

Credit sales Sales returns Discounts allowed Cash/ bank received from trade receivables

Date Details Amount $ Date Details Amount $

Date Details Amount $ Date Details Amount $

Date Details Amount $ Date Details Amount $

Date Details Amount $ Date Details Amount $

Date Details Amount $ Date Details Amount $

1.1.2000 Sameera a trade payable balance is $ 5,000

2.1.2000 Credit purchases from Sameera $ 12,000. Allow trade discount of 10 %

5.1.2000 Purchases returns to Sameera $ 1,000

10.1.2000 Paid cash to Sameera for the outstanding balance on 1.1.2000 with cash discount of 5%.

7.1.2000 Credit purchases from Sameera $ 2,000. Allow 10 % trade discount.

8.1.2000 Returns goods worth $500 to Sameera .

10.1.2000 Paid cash to Sameera for the outstanding balance with cash discount of 5%.

PDB

Date Details $ $

2.1.2000 Sameera 12,000

T.D 12,000 x10/100 [1,200] 10,800

7.1.2000 Sameera 2,000

T.D 2,000 x10/100 [200] 1,800

12,600

PRDB

Date Details $ $

Sales Ledger

Date Details Amount $ Date Details Amount $

General Ledger

Purchases

Date Details Amount $ Date Details Amount $

Purchases Returns Account

Date Details Amount $ Date Details Amount $

Cash/ Bank Account

Date Details Amount $ Date Details Amount $

Recommended