Embed Size (px)

Citation preview

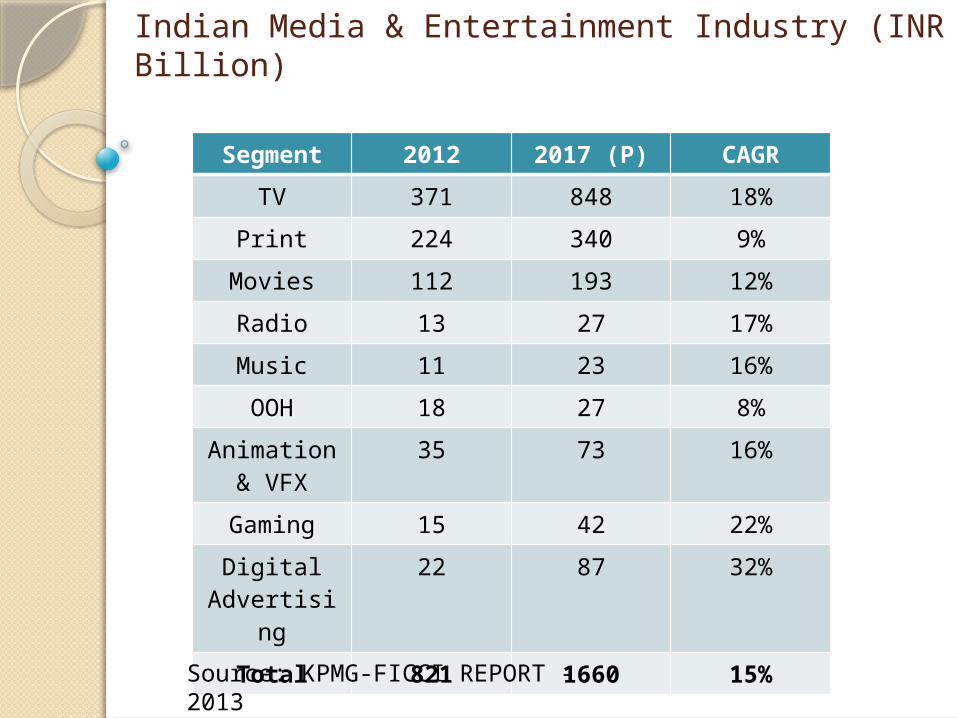

Indian Media & Entertainment Industry (INR Billion)

Segment 2012 2017 (P) CAGR

TV 371 848 18%

Print 224 340 9%

Movies 112 193 12%

Radio 13 27 17%

Music 11 23 16%

OOH 18 27 8%

Animation & VFX

35 73 16%

Gaming 15 42 22%

Digital Advertising

22 87 32%

Total 821 1660 15%

Source: KPMG-FICCI REPORT - 2013

Indian M&E Industry Size – 2012 (INR 821 Billion)

TV45%

Print27%

Radio1%

OOH, 2.5%

Music1%

Movies

14%

An-ima-tion &

VFX4% Gaming

2%Digital Advertis-

ing, 2.5%TVPrintRadioOOHMusicMoviesAnimation & VFXGamingDigital Advertising

Source: KPMG FICCI REPORT - 2013

Indian M&E Industry Size – 2017 (P) (INR 1660 Billion)

Source: KPMG FICCI REPORT - 2013

TV51%

Print20%

Radio, 2%

OOH2%

Music1%

Movies12%

Anim-ation & VFX

4%

Gam-ing, , 3%

Digital Advertising, , 4% TV

PrintRadioOOHMusicMoviesAnimation & VFXGamingDigital Advertising

Segment USD Billion CAGR %

Movie Entertainment 103 4.9

TV -Networks & Distribution 480 7.5

Music 40 2.3

Radio & Out-of-Home 99 5.2

Gaming 50 9.1

Business Information 110 5.8

Print 317 2.1

Theme Parks andAmusement Parks

30 4.6

Casino and OtherRegulated Gaming

144 7.2

Sports Entertainment 123 5.2

Total 1496 6.4

Global Media & Entertainment Industry Size

Source- PWC Report

Source- PWC Report

Global Media & Entertainment Industry

Movies7%

TV- Networks & Dist32%

Music3%

Radio & OOH7%

Gaming3%

Business Info.7%

Print21%

Theme & Amusement

Parks2%

Casinos10%

Sports Entertainment8%

% Share

Top M&E marketsNation USD Billion

1 USA 503

2 Japan 186

3 China 120

4 Germany 96

5 UK 82

6 France 72

7 Italy 45

8 Canada 42.6

9 Brazil 42.2

10

South Korea 37

11

Australia 35

12

Spain 28

India 12.6Source: PWC Report

Indian Advertising Industry Revenue (INR billion)

Segment 2012 2017(P) CAGR

TV 125 240 14%

Print 150 248 10.6%

Radio 13 27 16.6%

OOH 18 27 8.4%

Digital Advertising

22 87 32%

Total 328 629 14%

Source: KPMG FICCI REPORT - 2013

Indian Advertising Industry Revenue

TV38%

Print46%

Radio4%

Di-gital7%

OOH5%

Advt. Revenue - 2012

TV38%

Print39%

Radio4%

Di-gita

l14% OOH

4%

Advt. Revenue - 2017

Segment Advertising Pay

Print 79 % 21 %

TV 43 % 57 %

Film 1 % 99 %

Internet 27 % 73 %

Music & Home Video

- 100 %

OOH 100 % -

Radio 100% -

Total 40% 60%

Advertising v/s Pay Revenues for Indian M&E industry

Source-The Indian Media Business – Vanita Kohli, Khandekar

# Country Population

(Crs)Internet

Users (Crs)

Penetration(%

Population)

Users% World

1 China 134 54 40 % 22%

2 United States 31 25 78 % 10%

3 India 120 14 11 % 6 %

4 Japan 13 10 79 % 4 %

5 Brazil 19 8.9 46 % 4 %

6 Russia 14 6.8 48 % 3 %

7 Germany 8 6.7 83 % 3 %

8 Indonesia 25 5.5 22 % 2 %

9 United Kingdom

6.3 5.3 83 % 2 %

10 France 6.5 5.2 80 % 2 %

TOP 10 COUNTRIES WITH HIGHEST INTERNET USERS

Source: www.internetworldstats.com

Common Terms used in MEA sector

Content ARPU (Avg. Revenue Per User) Subscriber base Cable Digitization (DAS) Viewership TRP (TAM rating) GRP (TAM rating) Circulation v/s readership (IRS / NRS / ABC ratings) Subscriber base Listenership Sq. Cm rate TVC (Television Commercial) Spot rate / air-time rate Traditional Media (Print, Television, Films) New Media (Internet, Mobiles, Gaming)

Key figures about Indian M&E industry

14.6 crs TV households73 crs TV viewers.12 crs Cable & Satellite (C&S)

households623 channels82,000 news papers30-35 crs newspaper readers 13.7 crs internet users15.9 crs radio listeners1000 Indian films released every year

Key figs about Indian M&E industry

Mission Impossible: Ghost Protocol and The Adventures Of Tintin: The Secret Of The Unicorn released in India before they did in the U.S.

Digital sales of music contributes 42% of total revenues of the music industry in India and its share will be almost 80% by 2015

77 crs mobile phones , 55 crs active mobile subscribers and 8 crs mobile internet users

More than 35 million Indians are logged on to some kind of social network

India has the 2nd highest number of Facebook users and 3rd highest number of internet users.

Key figures about Indian M&E industry

Average time spent watching television is 2.55 hrs / day. One of the highest in the world.

Advertising spends across all media to cross Rs 629 billion by 2017

40 million DTH households 107 million copies of newspapers circulated daily

accounting for than 20% of all dailies in the world.

Indian film industry is pegged at 112 billion INR and produces more movies than Hollywood every year

4 billion movie tickets sold across 12,500 screens

The India Story 80% cinema screens are now digitized and 100% will be digitized

by 2015. 1000 Crs Box-Office mark not far DAS for TV digitization; Phase-1 completed in 4 metros and Phase

–II in 38 cities under process. Govt. has announced new Radio licensees in 294 cities India is still largely a traditional media market with new media co-

existing as an add-on distribution platform Regional Markets remain key centers of growth across print, TV

and films. India is a language driven market due to increasing literacy in

regional languages. Revenue models still advertising dependent as compared to

global standards and hence susceptible to economic downturns. Piracy and transparency across value chain a concern Indian content being consumed worldwide albeit gradually eg:

Zee TV in 169 countries, Chennai Express released in 35 countries

Can India reach the Un-Reached !!!

How to segment a diverse audience base and create customized content for each segment to ensure relevance with-out losing economies of scale ?

Is there possibility of further zoning/ going hyper-local to create localized content?

How do we engage the multi-tasking youth of today who experiences content on varied distribution platforms but forms a low ARPU segment ?

How to leverage increasing penetration of mobile phones and increased band-width connectivity through 3G/4G technology?

How to create content which has a global appeal for international markets?

Major CompaniesPrintBennett Coleman & Co (The Times of India)HT Media (Hindustan Times)Telegraph (ABP group)Dainik BhaskarDainik JagranDeccan HeraldDeccan ChronicleGujarat SamacharRajasthan PatrikaNavbharat TimesMaharashtraTimes

TVColors ( Viacom 18 Group)MTV (Viacom 18 Group)Star TVABP NewsZee GroupSony (Multi Screen Media & Sony Group)SAB TVLife OKUTV (Movies/Bindaas/Action)Disney (Walt Disney Group)Cartoon Network (Turner Broadcasting/Time Warner)ESPN (Walt Disney Group)Ten Sports (Zee Group)ETV (Eanadu Group)DiscoveryNat GeoFox Traveler

Film Entertainment Disney UTV Eros Entertainment Reliance Big Entertainment Yashraj Films Viacom 18 Fox Star Studios Sony Pictures Entertainment Warner Bros PVR Inox Shemaroo Entertainment Aamir Khan Productions Red Chillies Entertainment Dharma Production Vidhu Vinod Chopra Films Vishesh Films

Music & Home VideoSaregama (RPG Group)BIG Music,Home Video & Games

(Reliance Entertainment)Moser Baer Entertainment LtdShemaroo Entertainment LtdErosYashraj FilmsT-Series

Gaming (PC /Console)MicrosoftSonyElectronic ArtsActivisionNintendoTake 2SegaUbisoftVivendi

Indian Licensees• Milestone Interactive•BIG Music, Home Video & Games• WWE CD-ROMs

Gaming (Mobile/On-line)Indiagames (UTV)Dhruva InteractiveTrine GamesMaujMobile2winIbiboZapakHungama

Animation/VFX/Post ProductionToonz AnimationPentamedia GraphicsUTV ToonsCrest AnimationPrime FocusTata ElxsiShemaroo EntertainmentBIG Animation

RadioRadio Mirchi (Times Group)Fever 104 (HT Media)Big 92.7 (Reliance

Entertainment)Radio City Red FM

OOHLakshyaBright OutdoorBIG StreetOOH Digital Media Co.TDITimes OOH

Digital AdvertisingGoogle-adwordsFacebookRediffYahoo

DTH playersTata Sky (Tata + Sky

Broadcasting)Dish (Zee Group)AirtelBIG TVVideocon D2H

Value Chain Presence

Indian Company/

Group

Film Prod / Dist.

Music /Home Video Label

Film Exhibition

Content Aggregation

Retail Stores Gaming On-line

Satellite Channel Print Radio

Theme Parks

Times Group

UTV

Eros

Network 18

Reliance (ADAG)

Yashraj Films

Shemaroo

Moser Baer

PVR

RPG Group

HT Media

Hungama Mobile/ Mauj

Zee Group

Value Chain Presence

International Company/Group

Film Production

Theatrical Distribution

Music/ Home Video Label Gaming

Film Exhibition

Theme Parks Merchandise

TV Production/ Channel

Warner Bros.

Disney

20th Century Fox

Sony (Entertainment Div)

Viacom

Universal Studios

Fox Star Studios

Wanda/AMC

Key TrendsDigital technology continues to

revolutionalise media distributionMedia on the go- Proliferation of New age

Media DevicesRegional Markets becoming increasingly

attractiveDigital advertising offers cost effective

targeted advertising options to advertisersM&E industry still dependent largely on

advertising revenues due to low ARPU (Average Revenue Per User)

![Hal Berger Pet Industry [Reduce File Size]](https://img.dokumen.tips/doc/110x75/54e838c34a7959d76d8b4c72/hal-berger-pet-industry-reduce-file-size.jpg)