Embed Size (px)

Citation preview

The "Checklist"> 10. Execution> Order scheduling

Order scheduling

Goal: find the optimal trading schedule for a parent order of size ∆hparent

ht−start

initial position

ht−end = h

t−start+ ∆hparent?

terminal position

where• tstart = “now”;• tend = “as soon as possible, considering the adverse impact of ourtrading”.

Going forward, we analyze order scheduling in volume time (1.104), see Table10.4, and we consider implicit the conditioning on the current information.

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L computation

Trading P&L decomposition

The trading P&L (10.5) in continuous volume time reads

Πh(·),qnow→qend = hqend (Pqend − pqnow )︸ ︷︷ ︸“no-trade” P&L

+∫ qendqnow

hq(pqnow − Pq)dq︸ ︷︷ ︸implementation shortfall

(10.22)

hqend = hqnow + ∆hparent

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L computation

Trading P&L decomposition

The trading P&L (10.5) in continuous volume time reads

Πh(·),qnow→qend = hqend (Pqend − pqnow )︸ ︷︷ ︸“no-trade” P&L

+∫ qendqnow

hq(pqnow − Pq)dq︸ ︷︷ ︸implementation shortfall

(10.22)

hqend = hqnow + ∆hparent = 0 liquidation (11.37)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L computation

Market impact P&L

The trading P&L (10.5) in continuous volume time reads

Πh(·),qnow→qend = hqend (Pqend − pqnow )︸ ︷︷ ︸“no-trade” P&L

+∫ qendqnow

hq(pqnow − Pq)dq︸ ︷︷ ︸implementation shortfall

(10.22)

hqend = hqnow + ∆hparent

⇓ Market impact model (10.16)

Market impact P&L

Πh(·),qnow→qend = hqend

∫ qend

qnow

b(qend − q)f(hq) dq + σhqendBqend−qnow︸ ︷︷ ︸“no-trade” P&L

−∫ qend

qnow

hqg(hq)dq −∫ qend

qnow

hq(∫ qqnow

b(q − s)f(hs) ds)dq − σ∫ qend

qnow

hqBq−qnow dq︸ ︷︷ ︸implementation shortfall

(10.23)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L evaluation

Market impact P&L: distribution

Πh(·),qnow→qend ∼ N (?, ?)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L evaluation

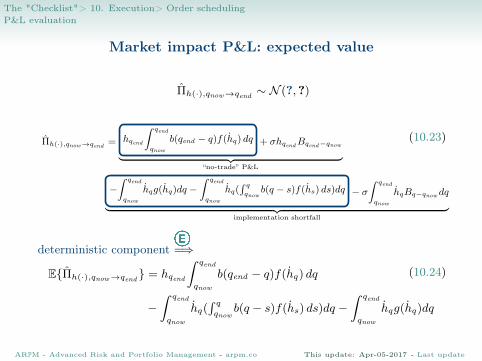

Market impact P&L: expected value

Πh(·),qnow→qend ∼ N (?, ?)

(10.23)Πh(·),qnow→qend = hqend

∫ qend

qnow

b(qend − q)f(hq) dq + σhqendBqend−qnow︸ ︷︷ ︸“no-trade” P&L

−∫ qend

qnow

hqg(hq)dq −∫ qend

qnow

hq(∫ qqnow

b(q − s)f(hs) ds)dq − σ∫ qend

qnow

hqBq−qnow dq︸ ︷︷ ︸implementation shortfall

deterministic component =⇒

E{Πh(·),qnow→qend } = hqend

∫ qend

qnow

b(qend − q)f(hq) dq

−∫ qend

qnow

hq(∫ qqnow

b(q − s)f(hs) ds)dq −∫ qend

qnow

hqg(hq)dq

(10.24)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L evaluation

Market impact P&L: variance

Πh(·),qnow→qend ∼ N (?, ?)

(10.23)Πh(·),qnow→qend = hqend

∫ qend

qnow

b(qend − q)f(hq) dq + σhqendBqend−qnow︸ ︷︷ ︸“no-trade” P&L

−∫ qend

qnow

hqg(hq)dq −∫ qend

qnow

hq(∫ qqnow

b(q − s)f(hs) ds)dq − σ

∫ qend

qnow

hqBq−qnow dq︸ ︷︷ ︸implementation shortfall

stochastic component =⇒ V{Πh(·),qnow→qend } = σ2∫ qendqnow

h2qdq (1)(10.25)

The variance is model-independent

• Trade at the end ⇒ large variance• Trade at the beginning ⇒ no variance

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L optimization

Two-step mean-variance optimization

Step 1: hλ (·) ≡ argmaxh(·)∈C

(E{Πh(·),qnow→qend } − λV{Πh(·),qnow→qend })

(10.26)set of constraints

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L optimization

Two-step mean-variance optimization

Step 1: hλ (·) ≡ argmaxh(·)∈C

(E{Πh(·),qnow→qend } − λV{Πh(·),qnow→qend })

(10.26)set of constraints

Full execution requirement

C : {{hq}q∈[qnow ,qend ) such that∫ qendqnow

hqdq = ∆hparent} (10.27)

Full execution

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L optimization

Two-step mean-variance optimization

Step 1: hλ (·) ≡ argmaxh(·)∈C

(E{Πh(·),qnow→qend }−λV{Πh(·),qnow→qend }) (10.26)

set of constraints

Full execution requirement

C : {{hq}q∈[qnow ,qend ) such that∫ qendqnow

hqdq = ∆hparent} (10.27)

Full execution

Step 2: h∗ (·) ≡ argmaxλ

satis(hλ (·)) (10.29)

best trajectory index ofsatisfaction (7a.5)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

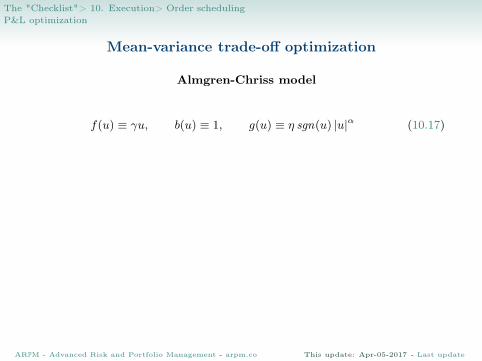

The "Checklist"> 10. Execution> Order schedulingP&L optimization

Mean-variance trade-off optimization

Almgren-Chriss model

f(u) ≡ γu, b(u) ≡ 1, g(u) ≡ η sgn(u) |u|α (10.17)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L optimization

Mean-variance trade-off optimization

Almgren-Chriss model

market impact function

f(u) ≡ γu , b(u) ≡ 1, g(u) ≡ η sgn(u) |u|α (10.17)

positive

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L optimization

Mean-variance trade-off optimization

Almgren-Chriss model

market impact decay kernel

f(u) ≡ γu, b(u) ≡ 1 , g(u) ≡ η sgn(u) |u|α (10.17)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L optimization

Mean-variance trade-off optimization

Almgren-Chriss model

slippage

f(u) ≡ γu, b(u) ≡ 1, g(u) ≡ η sgn(u) |u|α (10.17)

positive α = 1

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L optimization

Mean-variance trade-off optimization

Almgren-Chriss model

f(u) ≡ γu, b(u) ≡ 1, g(u) ≡ η sgn(u) |u|α (10.17)

• full execution requirement (10.27)

• total liquidation (11.37), i.e. hqend = 0

The solution of the mean-variance trade-off (10.26) is

hλ(q) = hqnow

sinh(√

λησ(qend − q))

sinh(√

λησ(qend − qnow ))

(10.30)

• the trajectories {hλ(·)}λ are monotonically decreasing from hqnow to 0

• ληdetermines the speed of trading

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L optimization

Mean-variance trade-off optimization

Almgren-Chriss model

f(u) ≡ γu, b(u) ≡ 1, g(u) ≡ η sgn(u) |u|α (10.17)

• full execution requirement (10.27)

• partial liquidation, i.e. hqend 6= 0

The solution of the mean-variance trade-off (10.26) is

hλ(q) = (hqnow − hqend )sinh(

√λησ(qend − q))

sinh(√

λησ(qend − qnow ))

+ hqend (10.31)

• the trajectories {hλ(·)}λ are monotonically decreasing from hqnow to• λ

ηdetermines the speed of trading

hqend

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L optimization

Trading trajectories in the Almgren-Chriss model

• volume time interval: [0, 1)

• initial position: hqnow = 100

• final position: hqend = 90

• "daily" parameters: η = 0.135, σ = 1.57

• λ = 0, 0.3, 1, 5

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

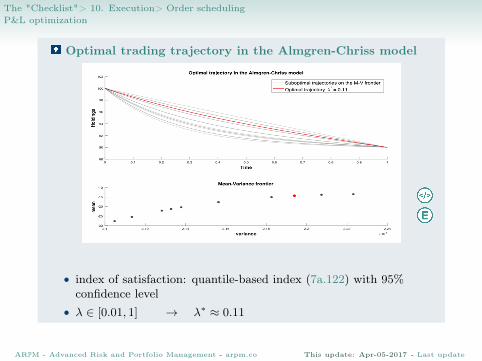

The "Checklist"> 10. Execution> Order schedulingP&L optimization

Optimal trading trajectory in the Almgren-Chriss model

• index of satisfaction: quantile-based index (7a.122) with 95%confidence level

• λ ∈ [0.01, 1] → λ∗ ≈ 0.11

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L quasi-optimal distribution

Robust schedulingAlmgren-Chriss model

f(u) ≡ γu, b(u) ≡ 1, g(u) ≡ η sgn(u) |u|α (10.17)

α generic⇓

Πh(·),qnow→qend = γ2

(h2qend − h

2qnow )− η

∫ qend

qnow

|hq|α+1dq

+ σhqendBqend−qnow − σ∫ qend

qnow

hqBq−qnow dq

Market impactP&L

(10.32)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L quasi-optimal distribution

Robust schedulingAlmgren-Chriss model

f(u) ≡ γu, b(u) ≡ 1, g(u) ≡ η sgn(u) |u|α (10.17)

α generic⇓

Πh(·),qnow→qend = γ2

(h2qend − h

2qnow )− η

∫ qend

qnow

|hq|α+1dq

+ σhqendBqend−qnow − σ∫ qend

qnow

hqBq−qnow dq

Market impactP&L

(10.32)

Postulated power execution strategy

hq ≡ hqnow + (q − qnowqend − qnow

)β∆hparent , for q ∈ [qnow , qend ] (10.34)

∆hparent ≡ hqend− hqnow

• the trajectory h(·) is monotonically decreasing from hqnow to hqend• β is the acceleration parameter and satisfies β ∈ ( α

1+α, 1]

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L quasi-optimal distribution

Robust schedulingAlmgren-Chriss model

f(u) ≡ γu, b(u) ≡ 1, g(u) ≡ η sgn(u) |u|α (10.17)

α generic⇓

Πh(·),qnow→qend = γ2

(h2qend − h

2qnow )− η

∫ qend

qnow

|hq|α+1dq

+ σhqendBqend−qnow − σ∫ qend

qnow

hqBq−qnow dq

Market impactP&L

(10.32)

Postulated power execution strategy

hq ≡ hqnow + (q − qnowqend − qnow

)β∆hparent , for q ∈ [qnow , qend ] (10.34)

⇒ E{Πh(·),qnow→qend } = γ2

(h2qend − h

2qnow )︸ ︷︷ ︸

permanent impact

− ηξ|∆hparent |1+α(qend − qnow )−α︸ ︷︷ ︸temporary impact

(10.36)

ξ ≡ βα+1/(β + βα − α) > 0

• Execute faster (β = 0+) ⇒ lower expected value• Execute slower (β = 1) ⇒ higher expected value

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L quasi-optimal distribution

Robust schedulingAlmgren-Chriss model

f(u) ≡ γu, b(u) ≡ 1, g(u) ≡ η sgn(u) |u|α (10.17)

α generic⇓

Πh(·),qnow→qend = γ2

(h2qend − h

2qnow )− η

∫ qend

qnow

|hq|α+1dq

+ σhqendBqend−qnow − σ∫ qend

qnow

hqBq−qnow dq

Market impactP&L

(10.32)

Postulated power execution strategy

hq ≡ hqnow + (q − qnowqend − qnow

)β∆hparent , for q ∈ [qnow , qend ] (10.34)

⇒ E{Πh(·),qnow→qend } = γ2

(h2qend − h

2qnow )︸ ︷︷ ︸

permanent impact

− ηξ|∆hparent |1+α(qend − qnow )−α︸ ︷︷ ︸temporary impact

(10.36)

ξ ≡ βα+1/(β + βα − α) > 0

• Execute faster (β = 0+) ⇒ lower expected value• Execute slower (β = 1) ⇒ higher expected value

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update

The "Checklist"> 10. Execution> Order schedulingP&L quasi-optimal distribution

Robust schedulingAlmgren-Chriss model

f(u) ≡ γu, b(u) ≡ 1, g(u) ≡ η sgn(u) |u|α (10.17)

α generic⇓

Πh(·),qnow→qend = γ2

(h2qend − h

2qnow )− η

∫ qend

qnow

|hq|α+1dq

+ σhqendBqend−qnow − σ∫ qend

qnow

hqBq−qnow dq

Market impactP&L

(10.32)

Postulated power execution strategy

hq ≡ hqnow + (q − qnowqend − qnow

)β∆hparent , for q ∈ [qnow , qend ] (10.34)

⇒ V{Πh(·),qnow→qend } = σ2(qend − qnow )(h2qnow + 2hqnow

∆hparent

β+1+ (∆hparent )2

2β+1) (10.37)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Apr-05-2017 - Last update