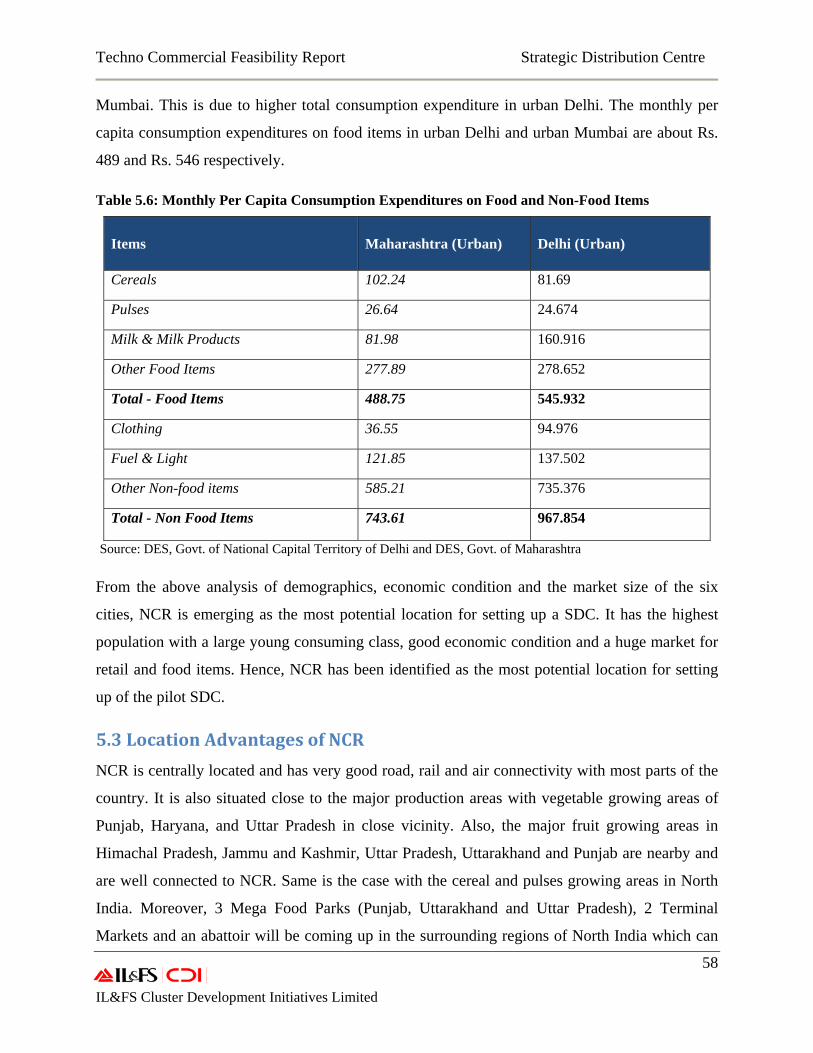

1

Strategic Distribution Centre

Techno‐Commercial Feasibility Report

Techno Commercial Feasibility Report Strategic Distribution Centre

2 IL&FS Cluster Development Initiatives Limited

Contents GLOSSARY ................................................................................................................................... 7

1. BACKGROUND ........................................................................................................................ 9

1.1 Status of Agro and Food Industry in India ................................................................................. 9 1.2 Food Processing Industry in India .............................................................................................. 10 1.3 Current Supply Chain and Distribution .................................................................................... 14 1.4 Current Logistics & Warehousing Scenario ............................................................................ 15 1.5 Changing Face of Indian Consumerism: Growth in Retail ................................................ 19 1.6 Changing Role of Warehousing .................................................................................................... 19 1.7 Mega Food Parks ................................................................................................................................ 25

2. OBJECTIVE AND METHODOLOGY ................................................................................... 26

2.1 Objective ....................................................................................................................................................... 26 2.2 Methodology ................................................................................................................................................ 26

3. MODERN DISTRIBUTION INFRASTRUCTURE: INDIAN SCENARIO ........................... 29

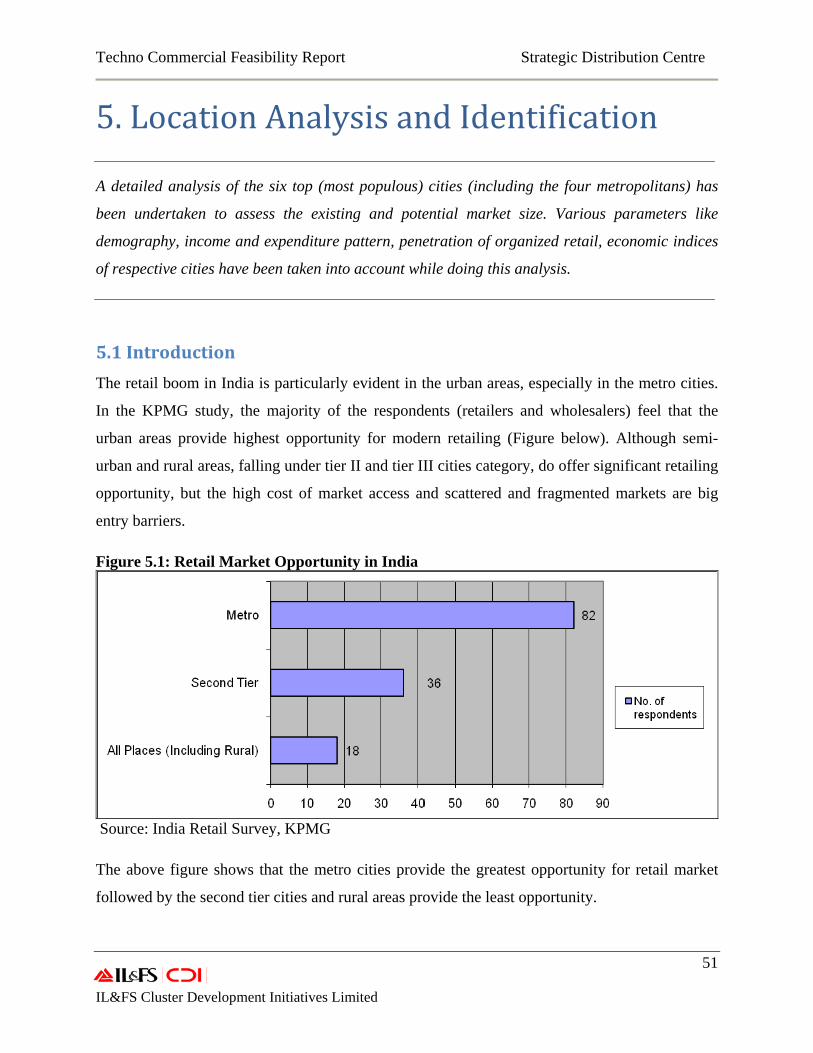

3.1 Introduction ................................................................................................................................................ 29 3.2 Analysis of Existing Value/Supply Chain ........................................................................................ 34 3.3 Staple Retailing .......................................................................................................................................... 39 3.4 Processed Food Retailing ...................................................................................................................... 40 3.5 Inefficiencies in Current Supply Chain ............................................................................................ 41 3.6 Challenges and Gaps ................................................................................................................................ 43 4.1 Concept .......................................................................................................................................................... 47 4.2 Potential Users of SDC ............................................................................................................................. 48 4.3 Benefits of SDC ........................................................................................................................................... 49

5. LOCATION ANALYSIS AND IDENTIFICATION ............................................................... 51

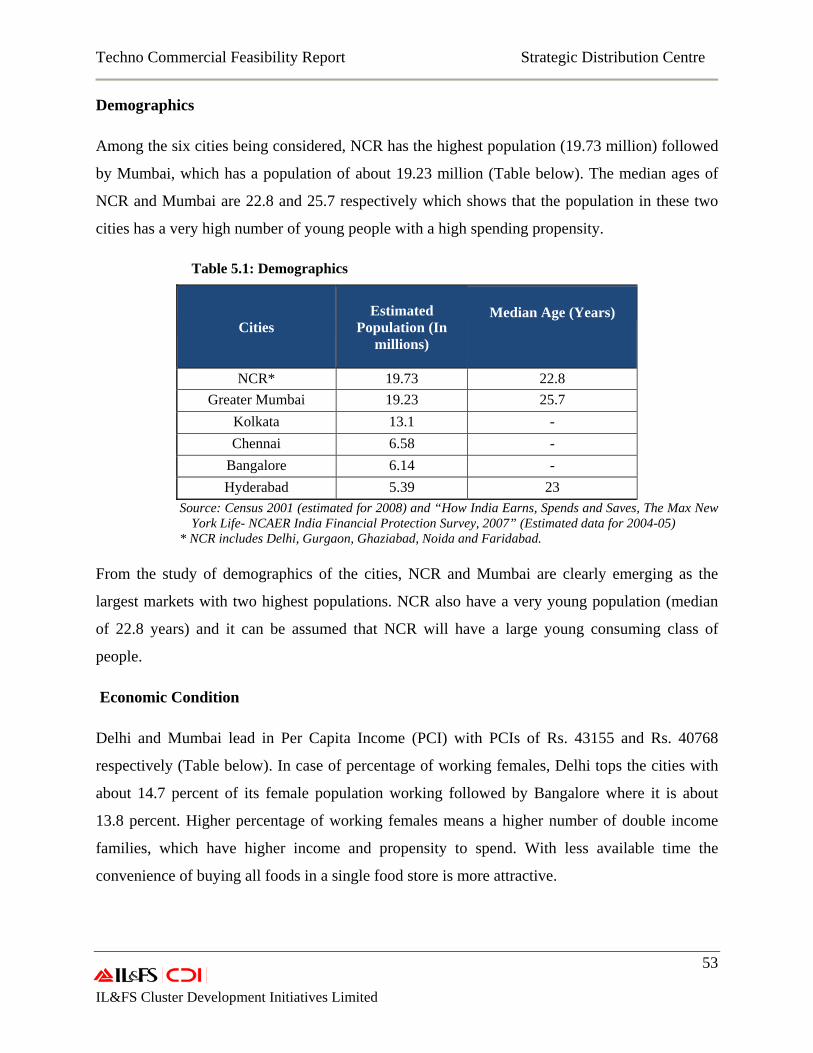

5.1 Introduction ................................................................................................................................................ 51 5.2 Comparison of Cities ................................................................................................................................ 52 5.3 Location Advantages of NCR ................................................................................................................ 58

6. PROPOSED SDC – NATIONAL CAPITAL REGION ........................................................... 60

6.1 Identified Sites ............................................................................................................................................ 60 6.2 Categories and Pattern of Food Consumption .............................................................................. 61

7. TECHNICAL DETAILS OF SDC ........................................................................................... 64

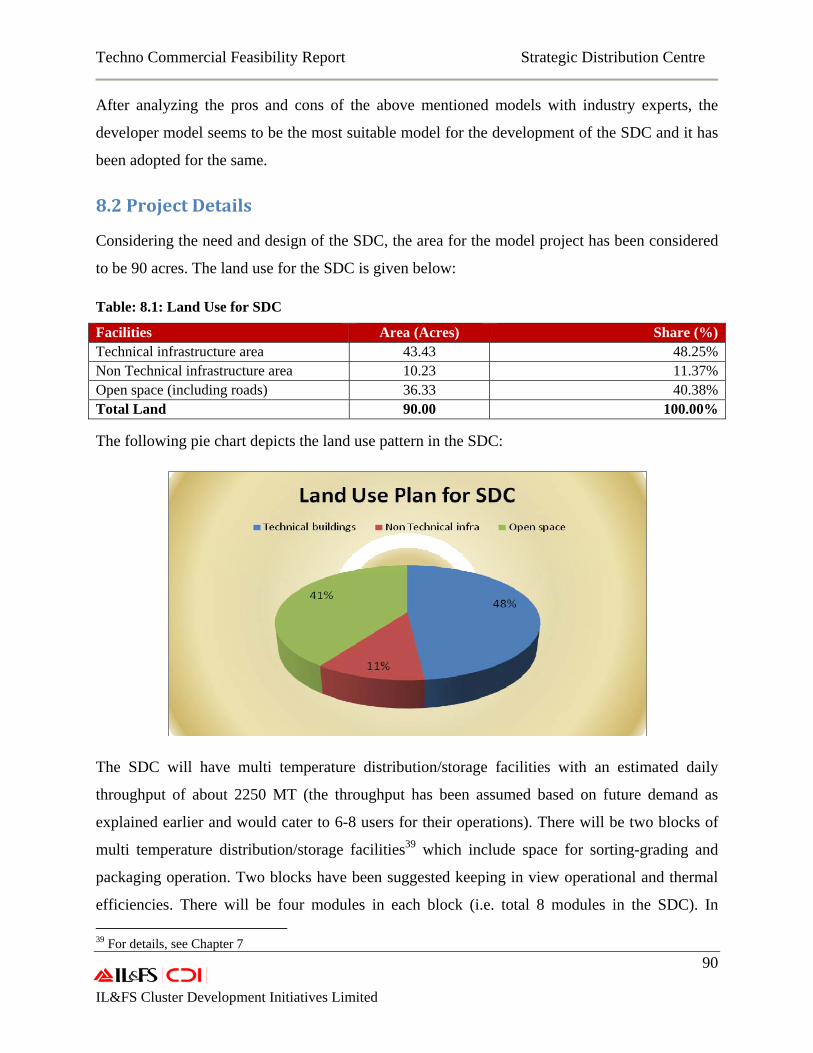

7.1 Product Categories ................................................................................................................................... 64 7.2 Operational Processes ............................................................................................................................. 65 7.3 Design of the SDC ...................................................................................................................................... 67 7.4 Modeling the SDC ...................................................................................................................................... 70 7.5 Case Study – A discount Supermarket Chain from the West .................................................. 82 7.6 Summary ....................................................................................................................................................... 86

8. FINANCIAL ANALYSIS ........................................................................................................ 87

Techno Commercial Feasibility Report Strategic Distribution Centre

3 IL&FS Cluster Development Initiatives Limited

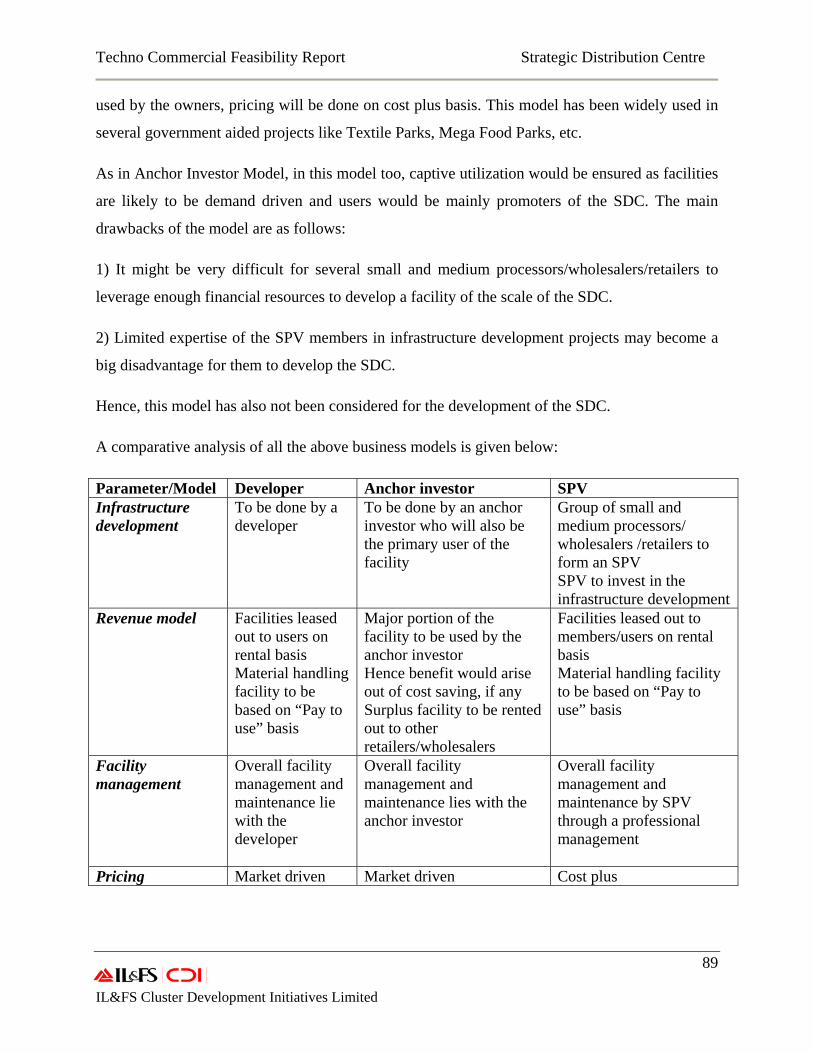

8.1 Business Model .......................................................................................................................................... 87 8.2 Project Details ............................................................................................................................................. 90 8.3 Project Cost .................................................................................................................................................. 92 8.4 Means of Finance ....................................................................................................................................... 96 8.5 Analysis of Business Plan....................................................................................................................... 97 8.6 Key Operating Assumptions ................................................................................................................. 98 8.7 Financial Performance .......................................................................................................................... 102 8.8 Sensitivity Analysis ................................................................................................................................ 104

ANNEXURE............................................................................................................................... 105

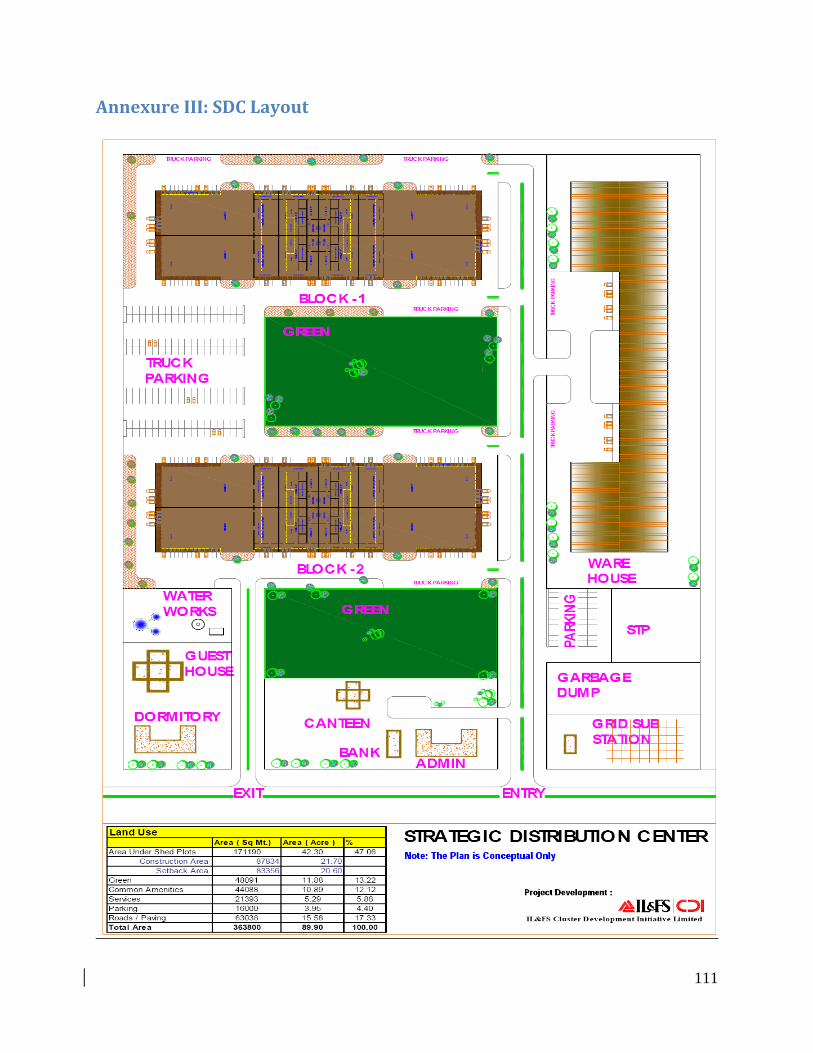

Annexure I: Scope of Work ......................................................................................................................... 105 Annexure II: Financial Tables .................................................................................................................... 107 Annexure III: SDC Layout ............................................................................................................................ 111 Annexure IV: SDC 3G Layout ..................................................................................................................... 112

Techno Commercial Feasibility Report Strategic Distribution Centre

4 IL&FS Cluster Development Initiatives Limited

Tables Table 1.1: Projected Food Consumption ..................................................................................................... 10 Table 1.2 : Growth Projections of Processed Food ................................................................................. 11 Table 3.1: Comparison between Traditional & Modern Supply Chain ........................................... 39 Table 3.2 Value Chain of Pigeon Pea ............................................................................................................. 40 Table 5.1: Demographics .................................................................................................................................... 53 Table 5.2: Per Capita Income and Percentage of Working Females ................................................ 54 Table 5.3: Salaried and Business/Professional HHs .............................................................................. 54 Table 5.4: Estimated Retail Space .................................................................................................................. 55 Table 5.5: Total Annual Expenditure on Food‐ Based on NSSO Survey‐2005‐06 ..................... 56 Table 5.6: Monthly Per Capita Consumption Expenditures on Food and Non‐Food Items .. 58 Table 6.1: Consumption of Food Items in Urban NCR ........................................................................... 62 Table 7.1: Growth Model of Volumes to be handled by SDC ............................................................... 71 Table 7.2: Parameters for Designing the SDC modules ......................................................................... 71 Table: 8.1: Land Use for SDC ............................................................................................................................. 90 Table 8.2: Details of Technical Infrastructure in the SDC .................................................................... 91 Table 8.3: Non technical facilities in the SDC ............................................................................................ 91 Table 8.4: Component Wise Project Cost of SDC ...................................................................................... 92 Table 8.5: Estimated Area and Construction Cost of SDC .................................................................... 93 Table 8.6: Machinery Cost ................................................................................................................................. 94 Table 8.7: Cost of Miscellaneous Assets and Utilities ............................................................................ 95 Table 8.8: Means of Finance .............................................................................................................................. 97 Table 8.9: Details of Power Load .................................................................................................................... 98 Table 8.10: Details of Manpower Costs ........................................................................................................ 99 Table 8.11: Depreciation Rates used for Assets in SDC ...................................................................... 101 Table:8.12 Rentals Assumption .................................................................................................................... 101 Table 8.13:Year wise Estimated Capacity Utilization of SDC ........................................................... 102 Table 8.14: Income Statement ....................................................................................................................... 102 Table 8.15 : Major Financial Indicators ..................................................................................................... 104 Table 8.16: Sensitivity Analysis of SDC ...................................................................................................... 104

Techno Commercial Feasibility Report Strategic Distribution Centre

5 IL&FS Cluster Development Initiatives Limited

Figures Figure1.1 Market Share of Unorganised Sector in Indian Food Processing Industry 11

Figure 1.2 Targets for Food Processing Industry in India 14

Figure 1.3: Composition of Warehousing in India 16

Figure 1.4 : Composition of Cold Storage Operators in India 17

Figure 1.5: Storage Conditions in Grain Warehouse 17

Figure 1.6: Cost Elements of Logistics in India 18

Figure 1.7: Retail Visibility 22

Figure 2.1 : Methodology Adopted by IL&FS CDI 28

Figure 3.1: Income Pyramid w.r.t. Population in India 31

Figure 3.2: Category wise Expenditure Pattern 32

Figure 3.3: Typical Supply Chain in F&V 35

Figure 3.4: Supply Chain of F&V in Azadpur Mandi 36

Figure 3.5: Supply Chain of Banana from Jalgaon to Azadpur Mandi 36

Figure 3.6: Model I: Procurement through APMC Market Yards 37

Figure 3.7: Model II: Direct Procurement from Growers 37

Figure 3.8 Value Chain of Pea from Jalandhar to Azadpur Mandi 38

Figure 3.9: Typical Supply Chain of Staples 39

Figure 3.10: Supply Chain for Processed Food Products 41

Figure 3.11: Picture of a typical warehouse operations in India 42

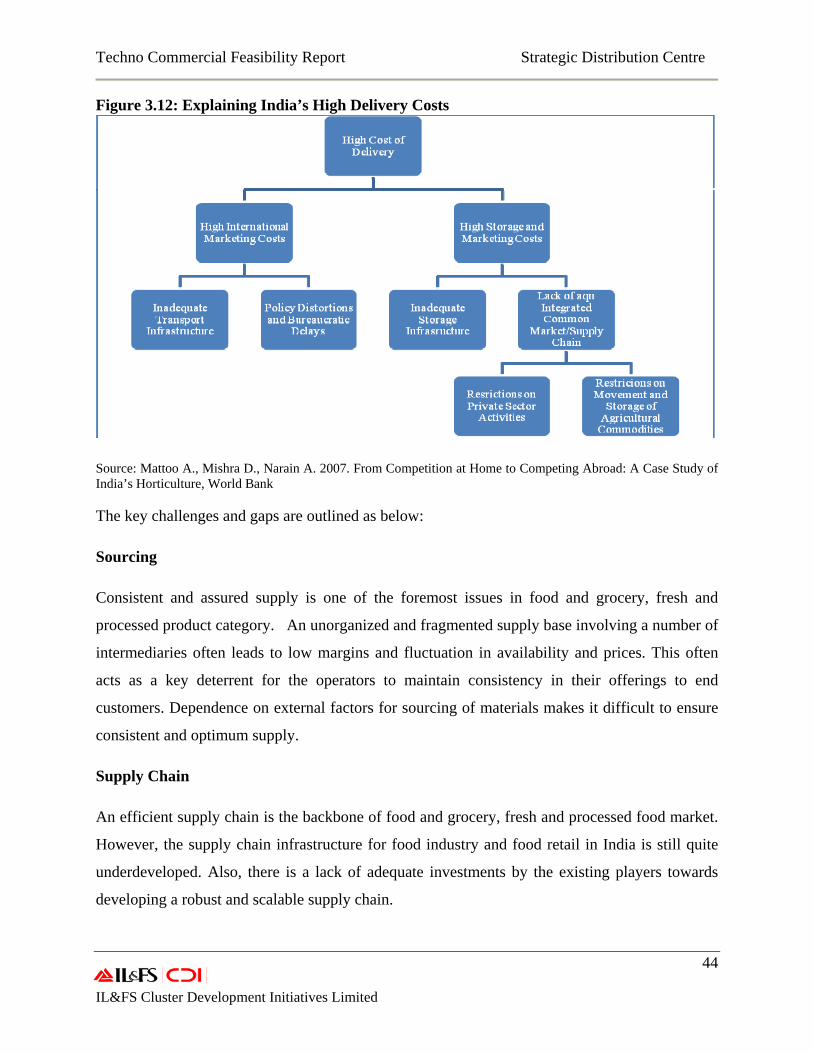

Figure 3.12: Explaining India’s High Delivery Costs 44

Figure 5.1: Retail Market Opportunity in India 51

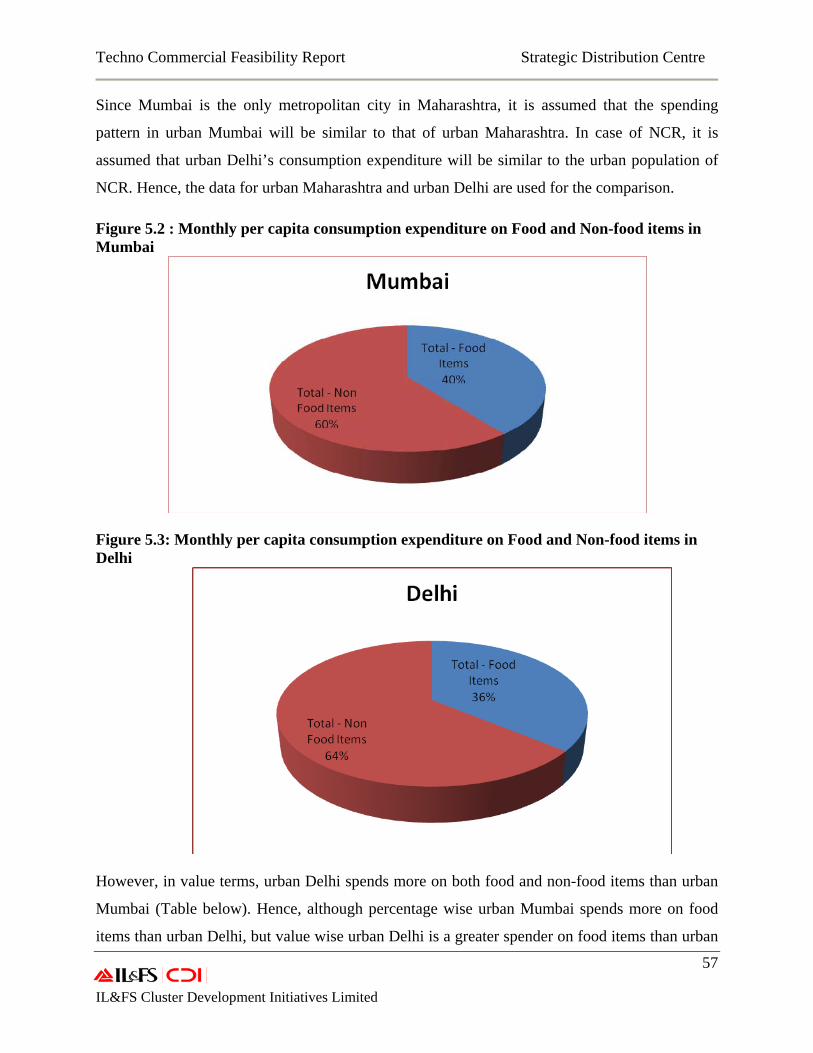

Figure 5.2 : Monthly per capita consumption expenditure on Food and Non-food items in Mumbai 57

Techno Commercial Feasibility Report Strategic Distribution Centre

6 IL&FS Cluster Development Initiatives Limited

Figure 5.3: Monthly per capita consumption expenditure on Food and Non-food items in Delhi 57

Figure 5.4: Food Production and Processing Areas around NCR 59

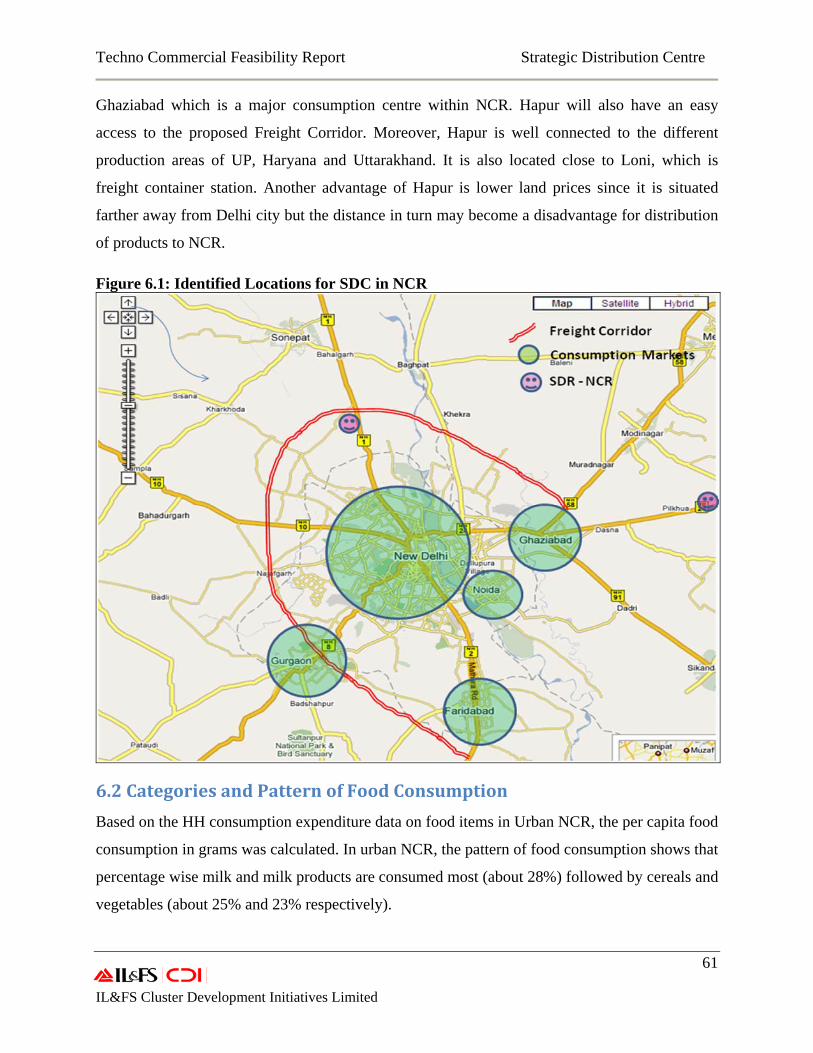

Figure 6.1: Identified Locations for SDC in NCR 61

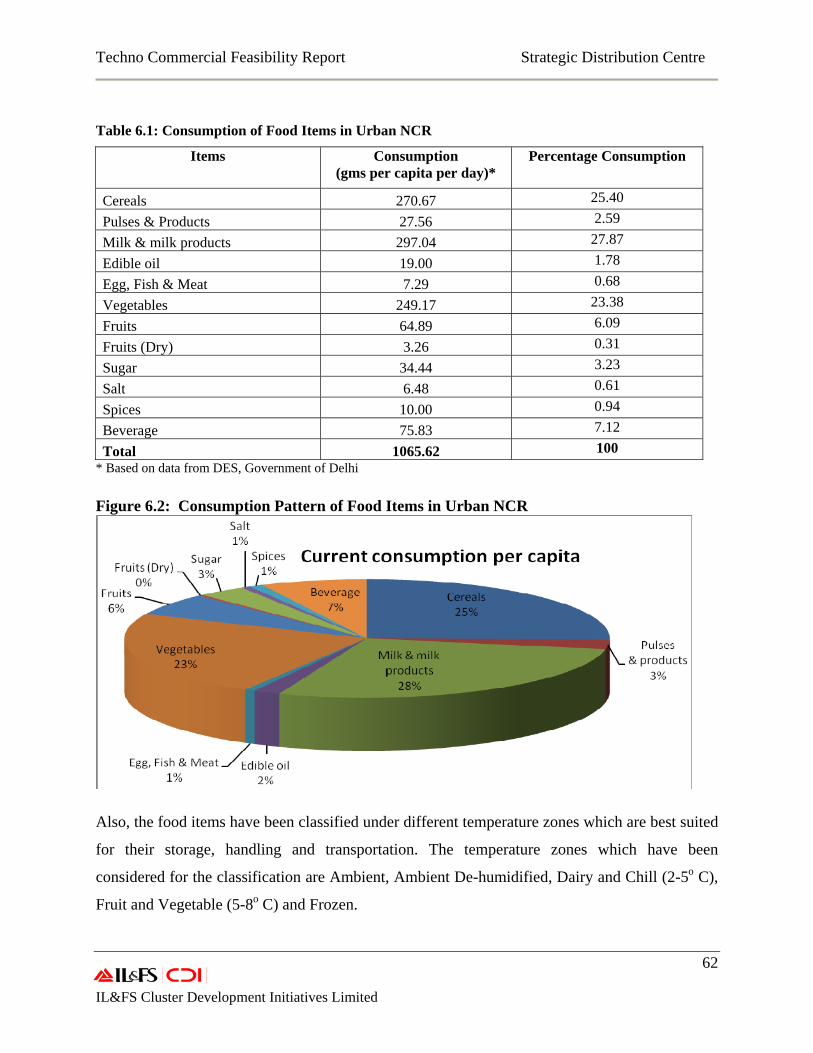

Figure 6.2: Consumption Pattern of Food Items in Urban NCR 62

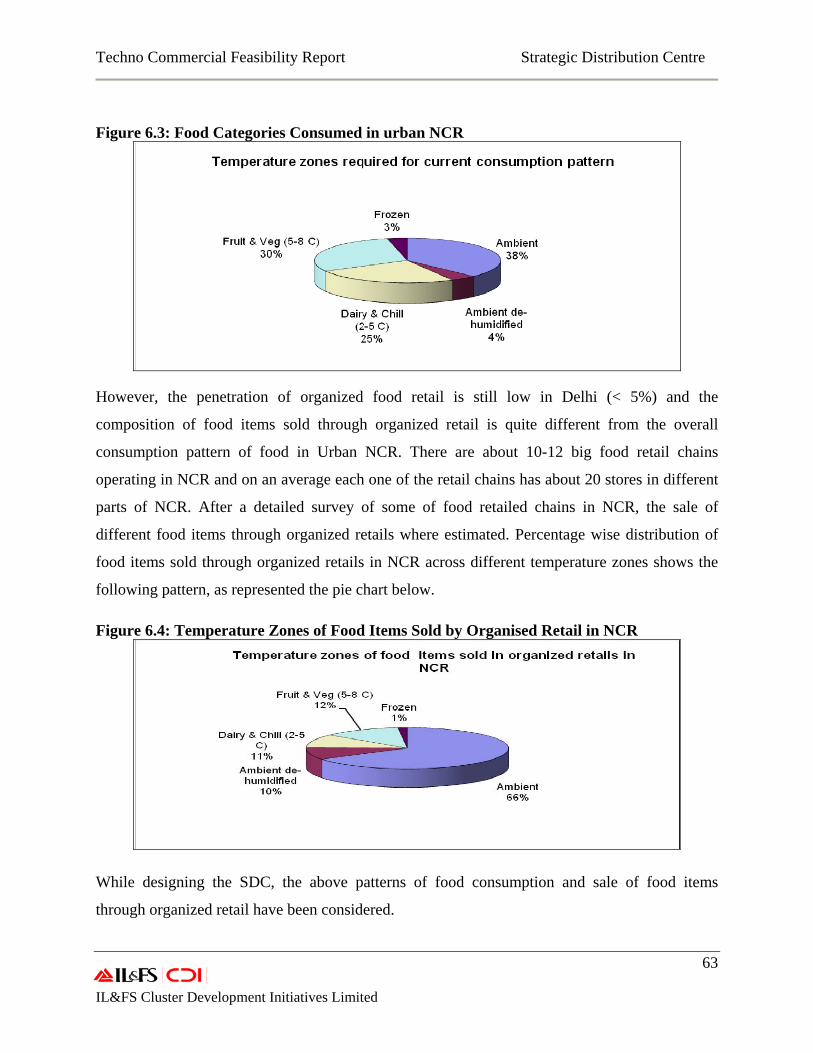

Figure 6.3: Food Categories Consumed in urban NCR 63

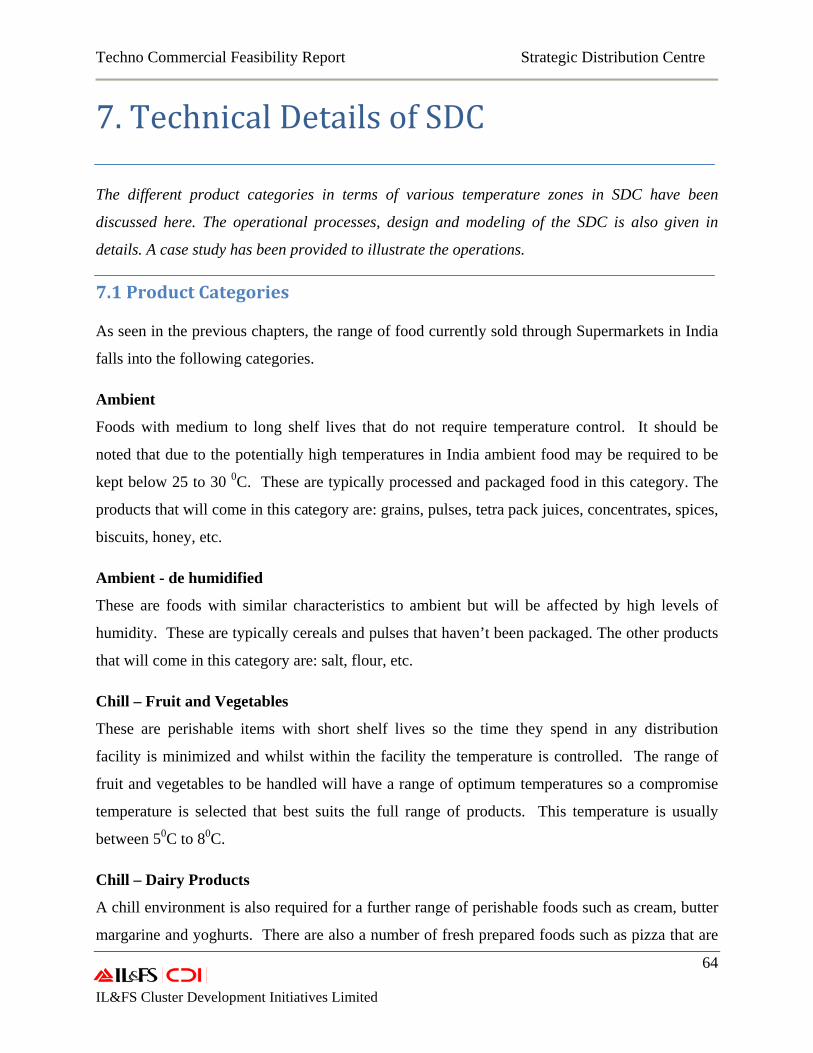

Figure 6.4: Temperature Zones of Food Items Sold by Organised Retail in NCR 63

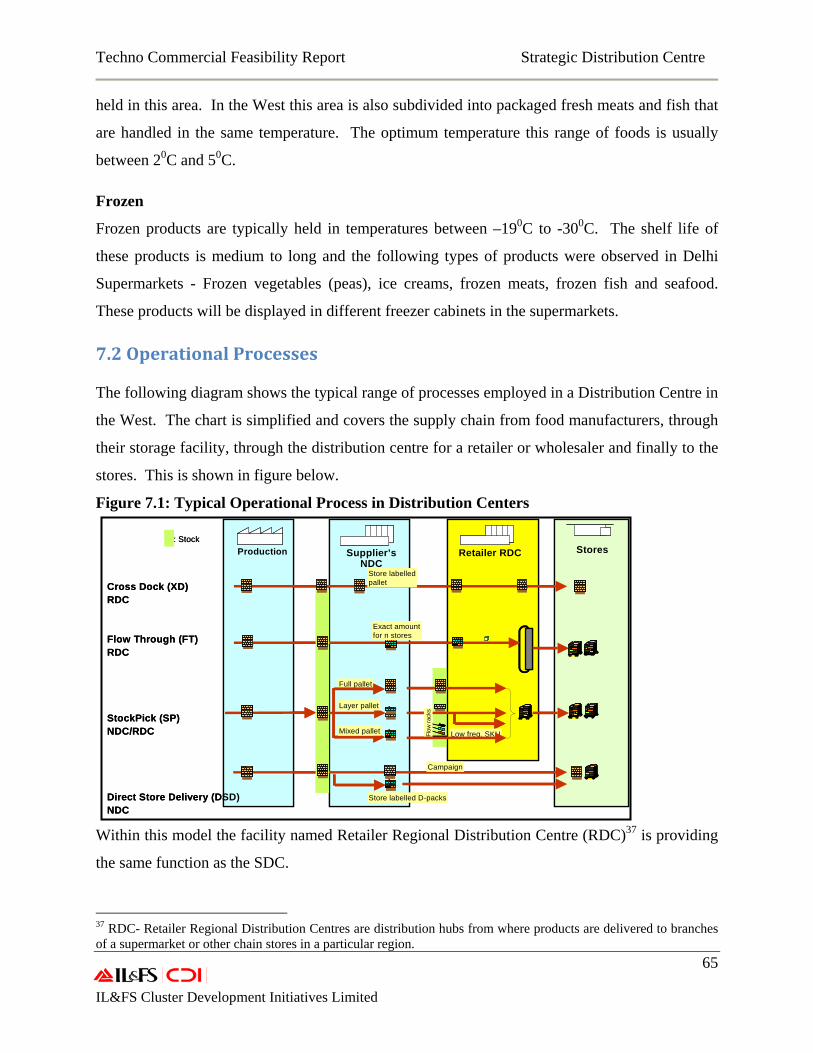

Figure 7.1: Typical Operational Process in Distribution Centers 65

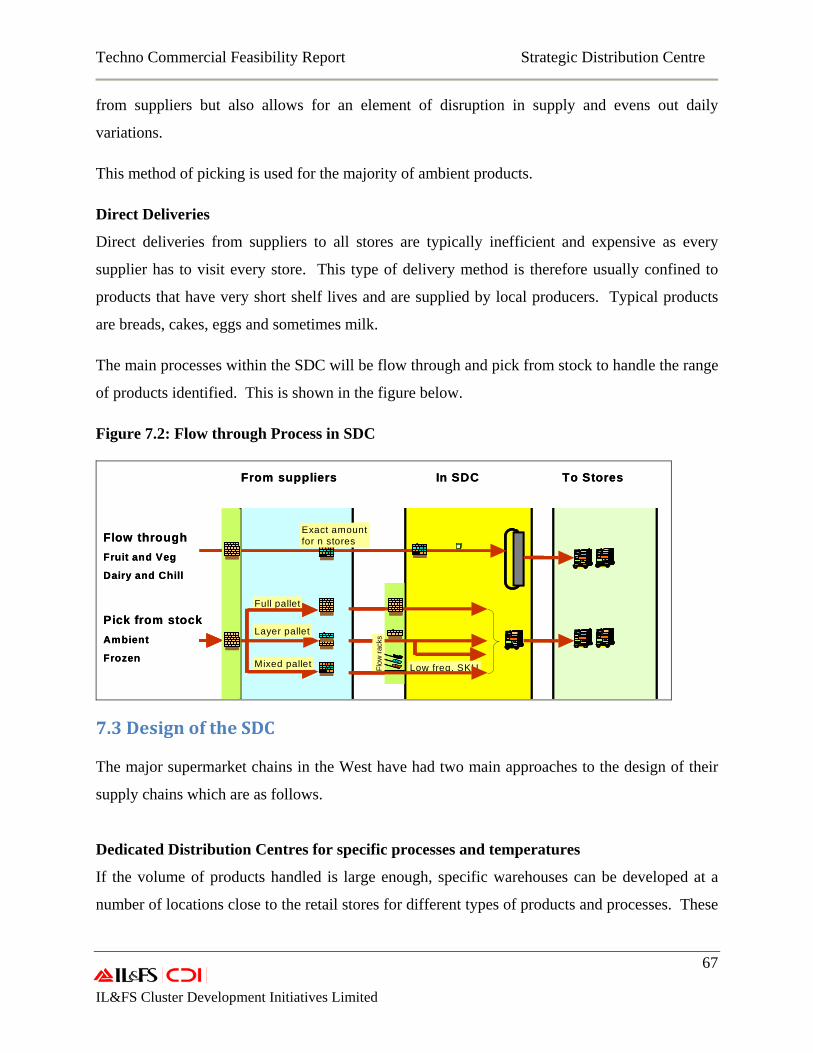

Figure 7.2: Flow through Process in SDC 67

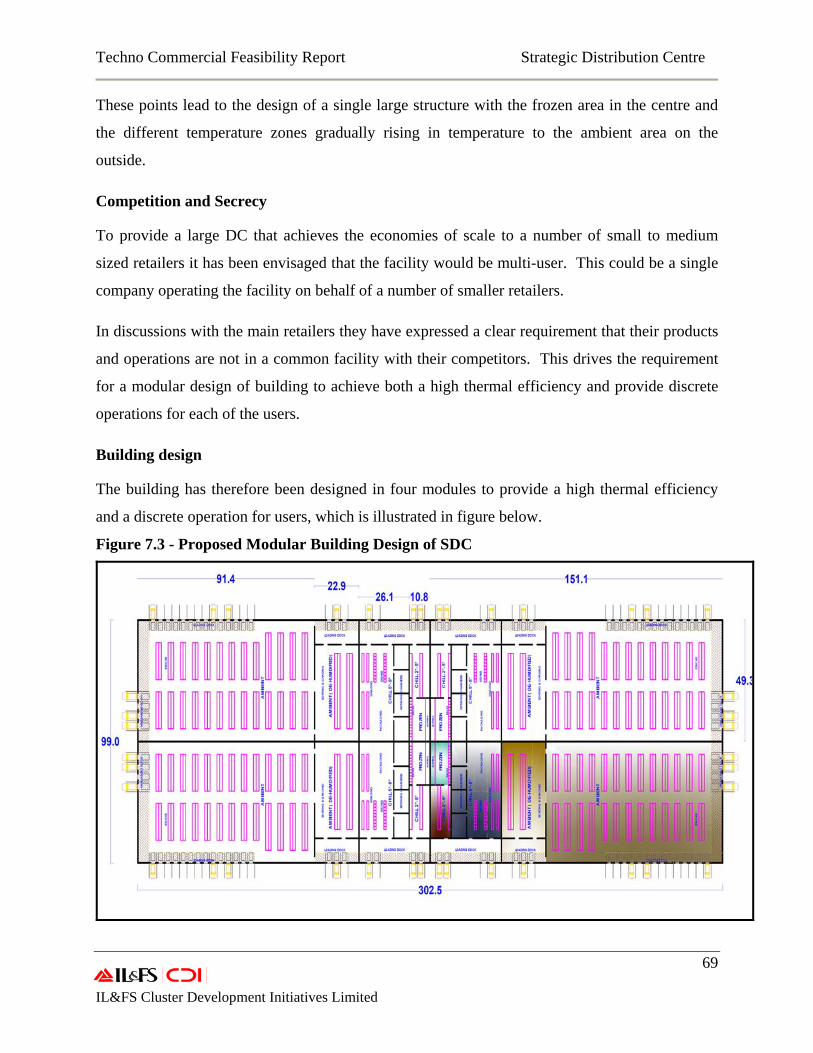

Figure 7.3 - Proposed Modular Building Design of SDC 69

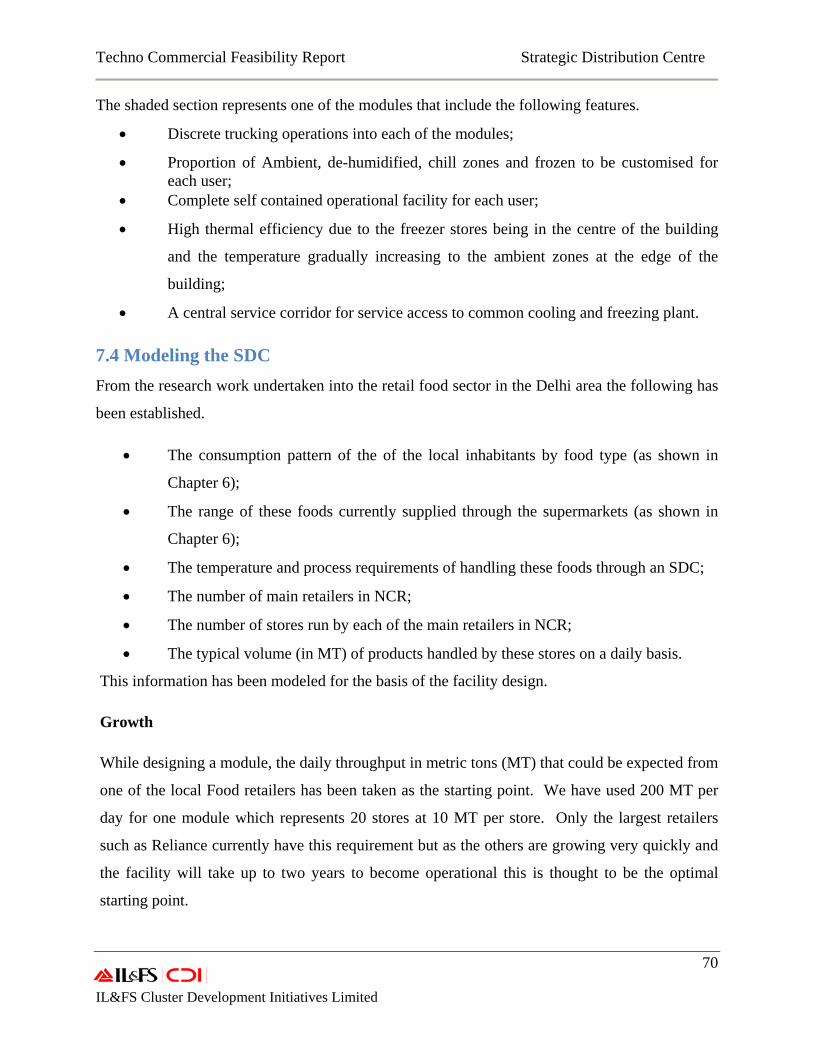

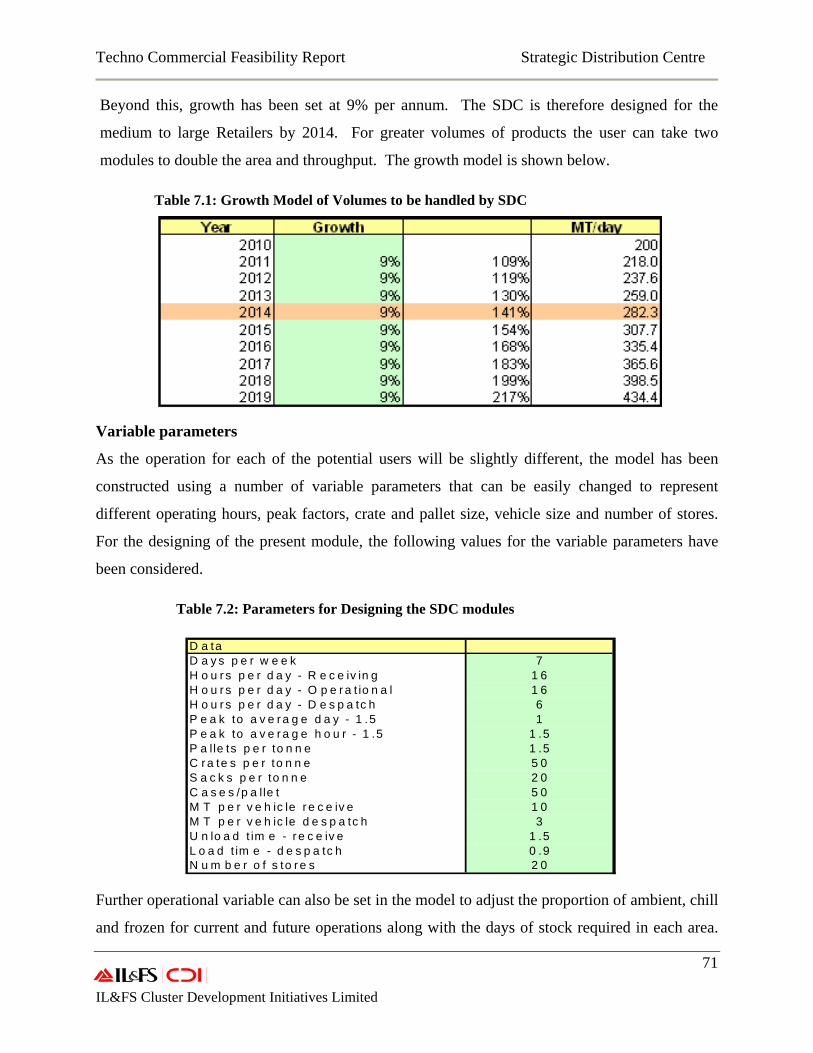

Figure 7.4: Model for a Single Module of the SDC. 72

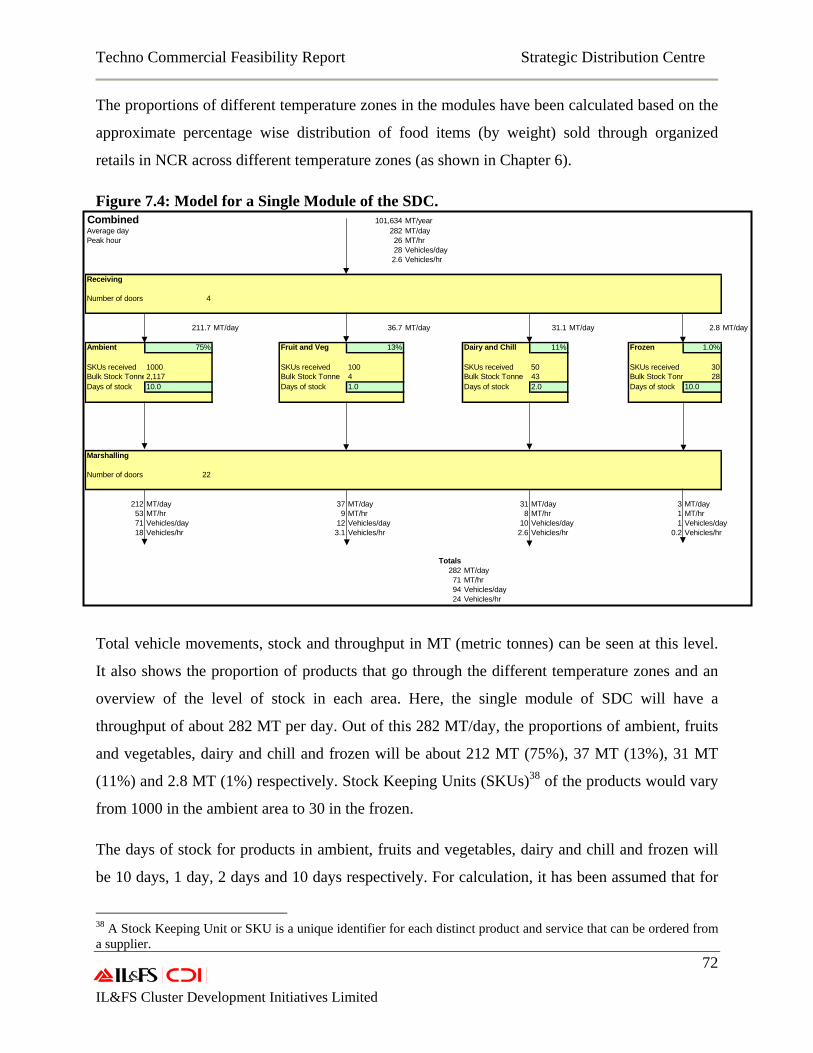

Figure 7.5: Size and Layout of SDC Module: 73

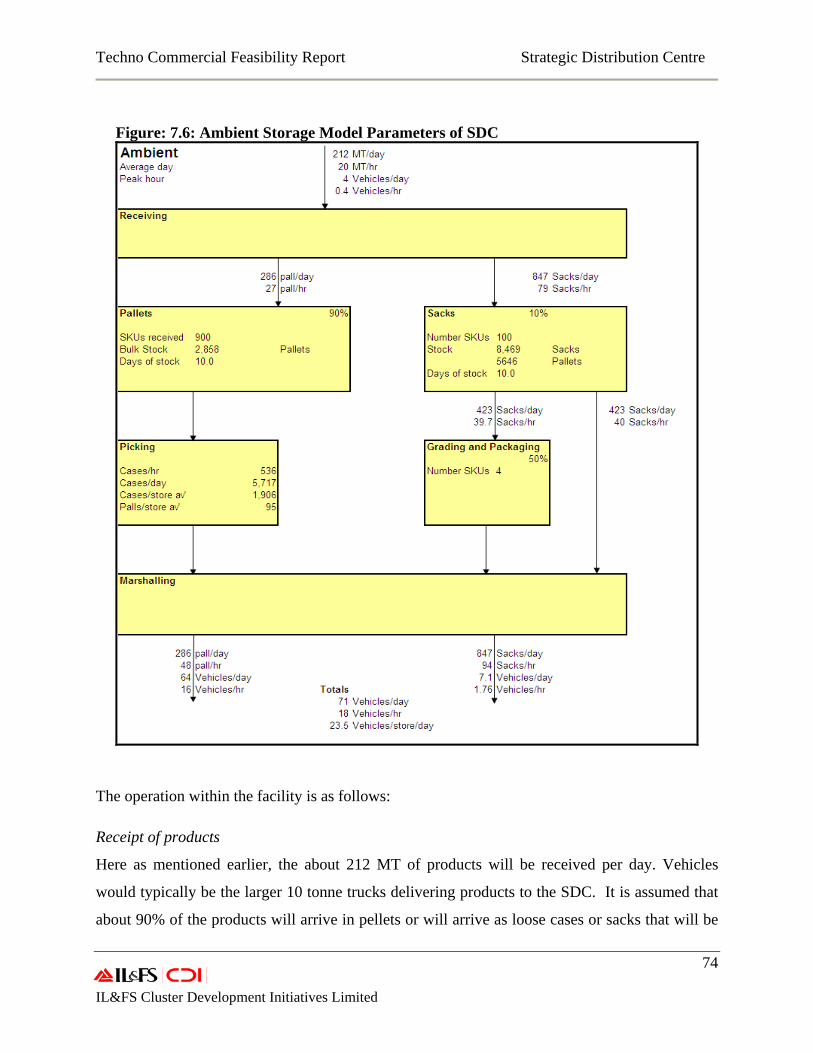

Figure: 7.6: Ambient Storage Model Parameters of SDC 74

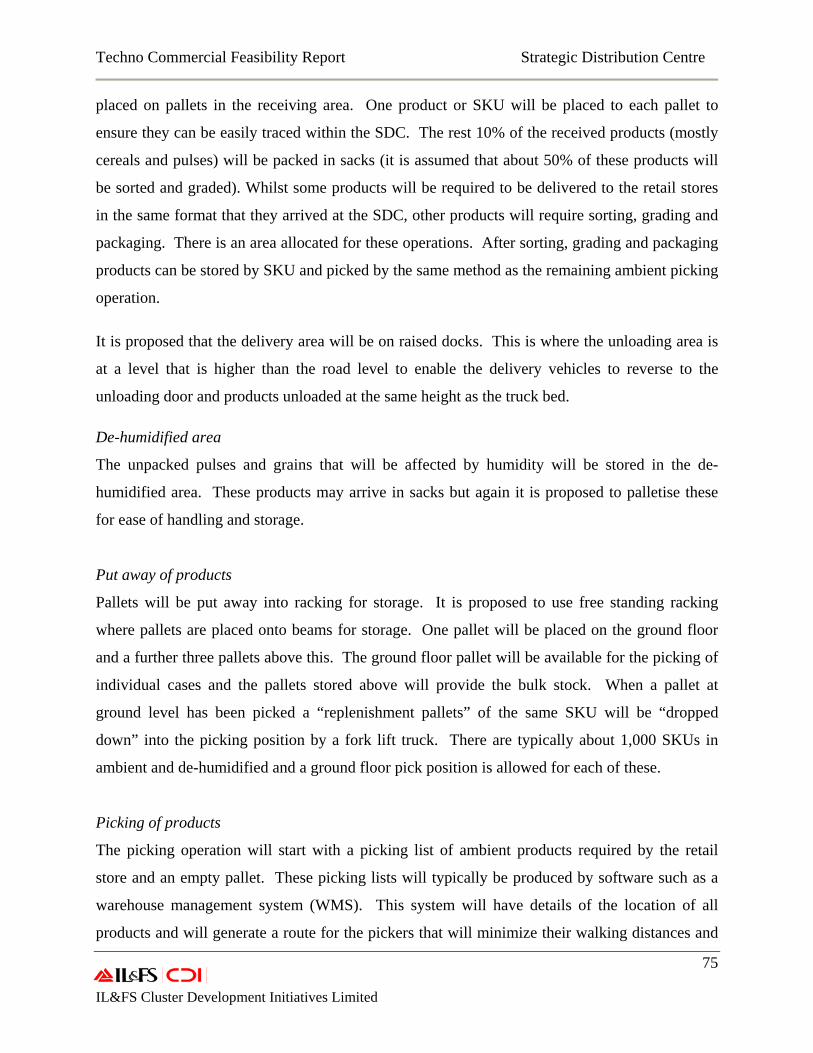

Table: 7.7: Layout of Ambient Area 76

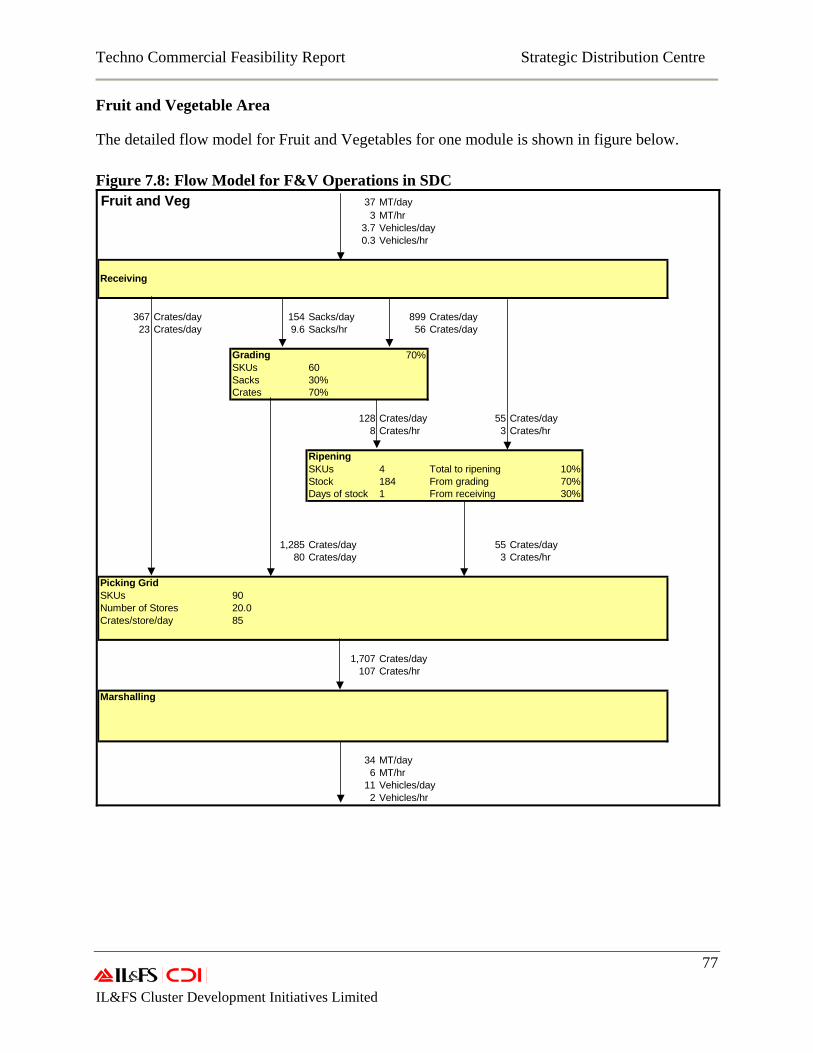

Figure 7.8: Flow Model for F&V Operations in SDC 77

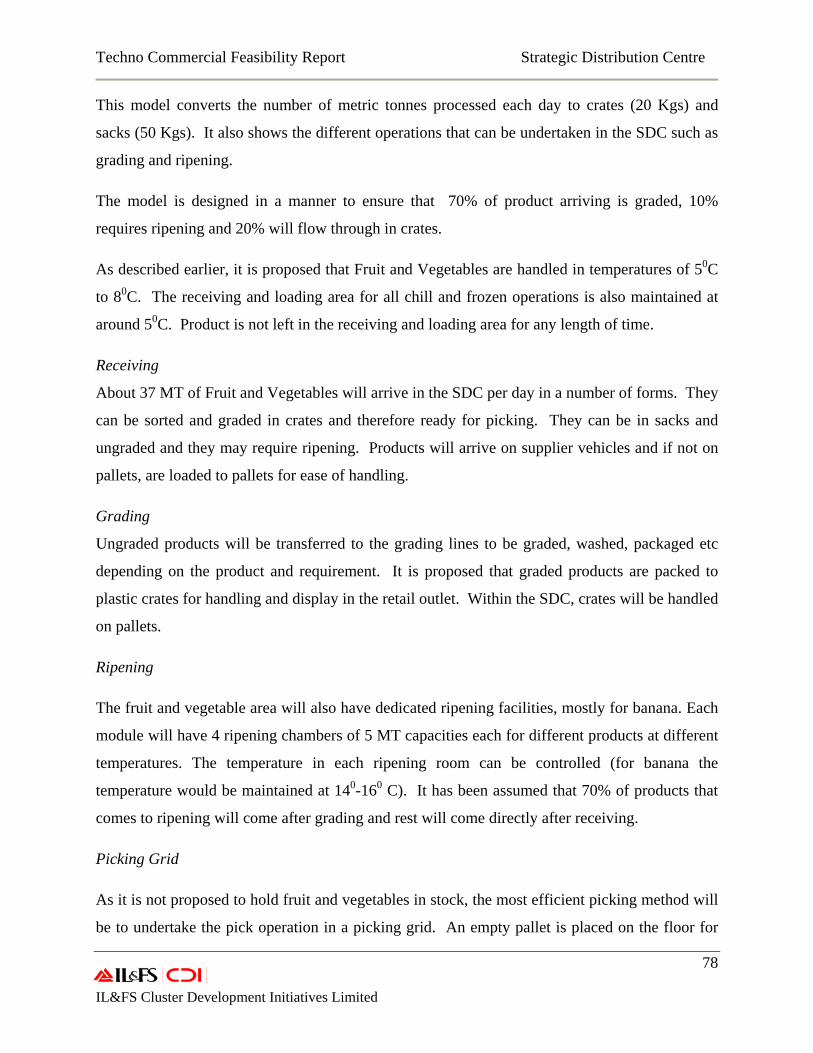

Figure 7.9: Layout of Chill and Frozen Sections Operational Flows 79

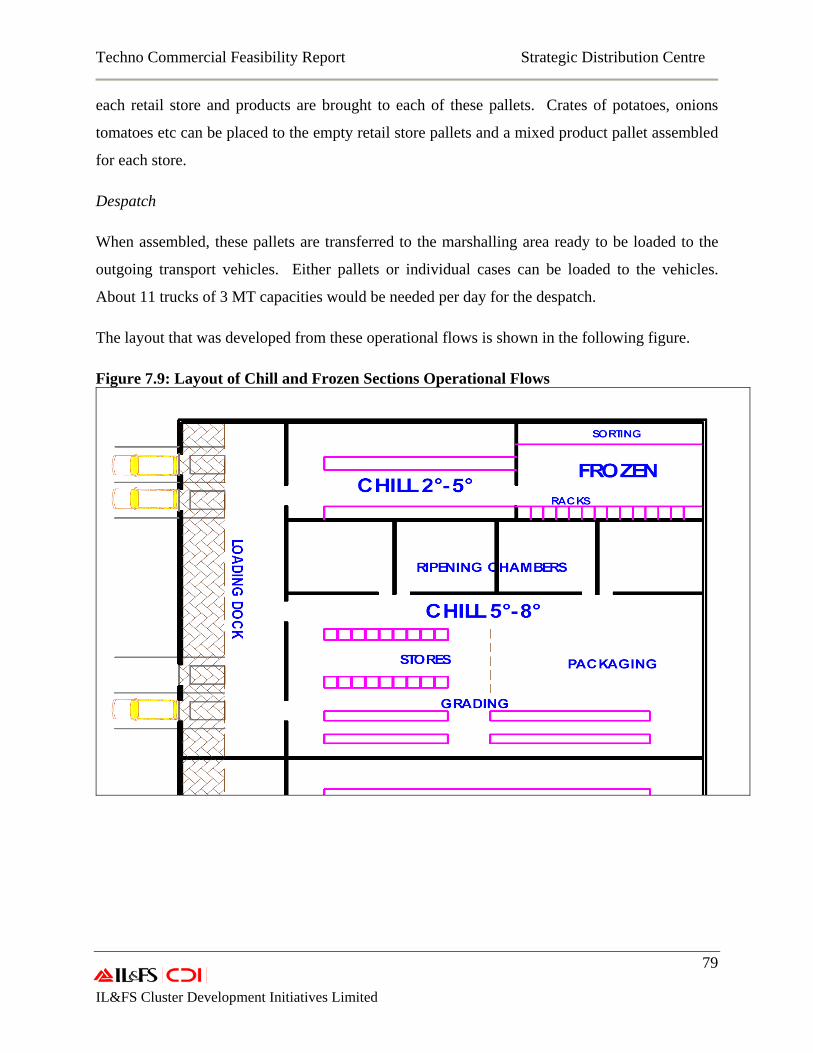

Figure 7.10 : Dairy and Chill Operations Module 80

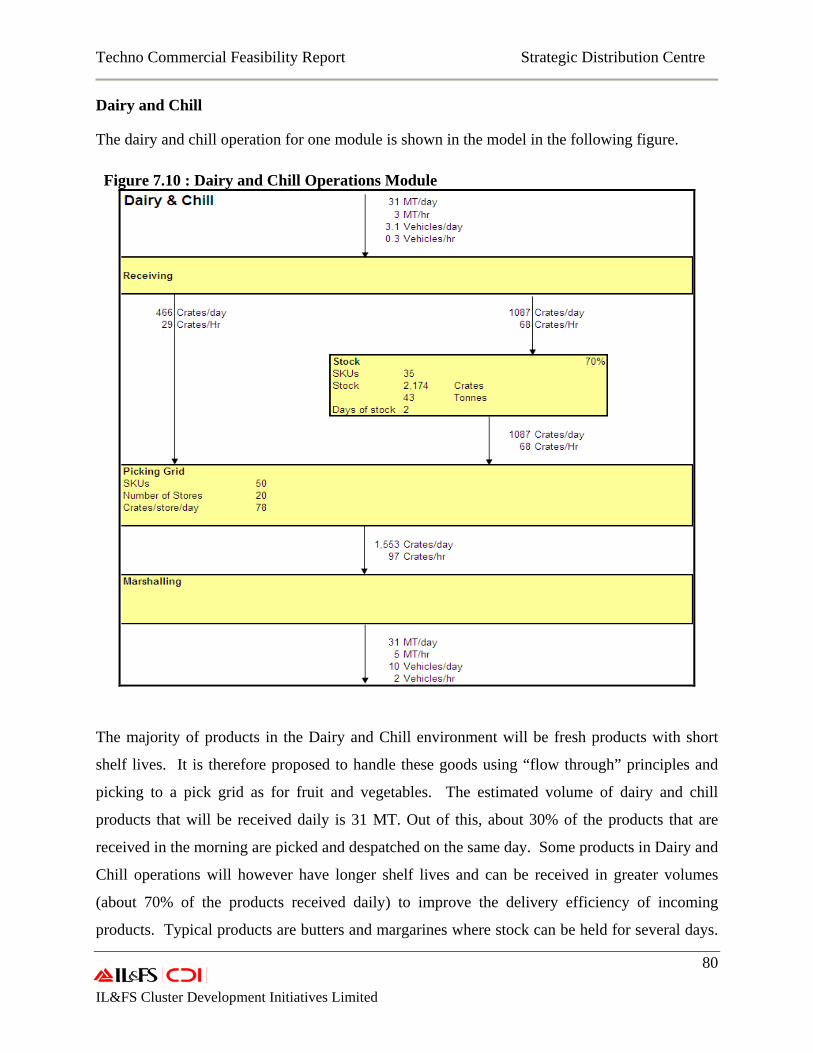

Figure 7.11: Model of Frozen Operations: 81

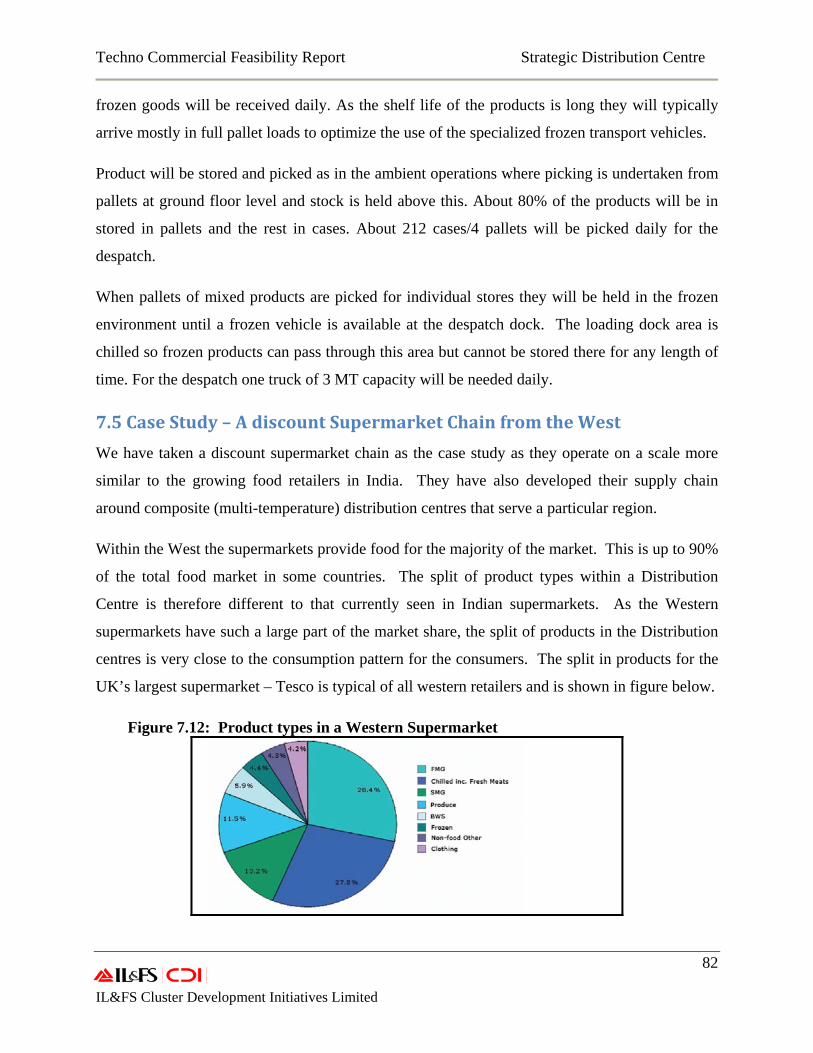

Figure 7.12: Product types in a Western Supermarket 82

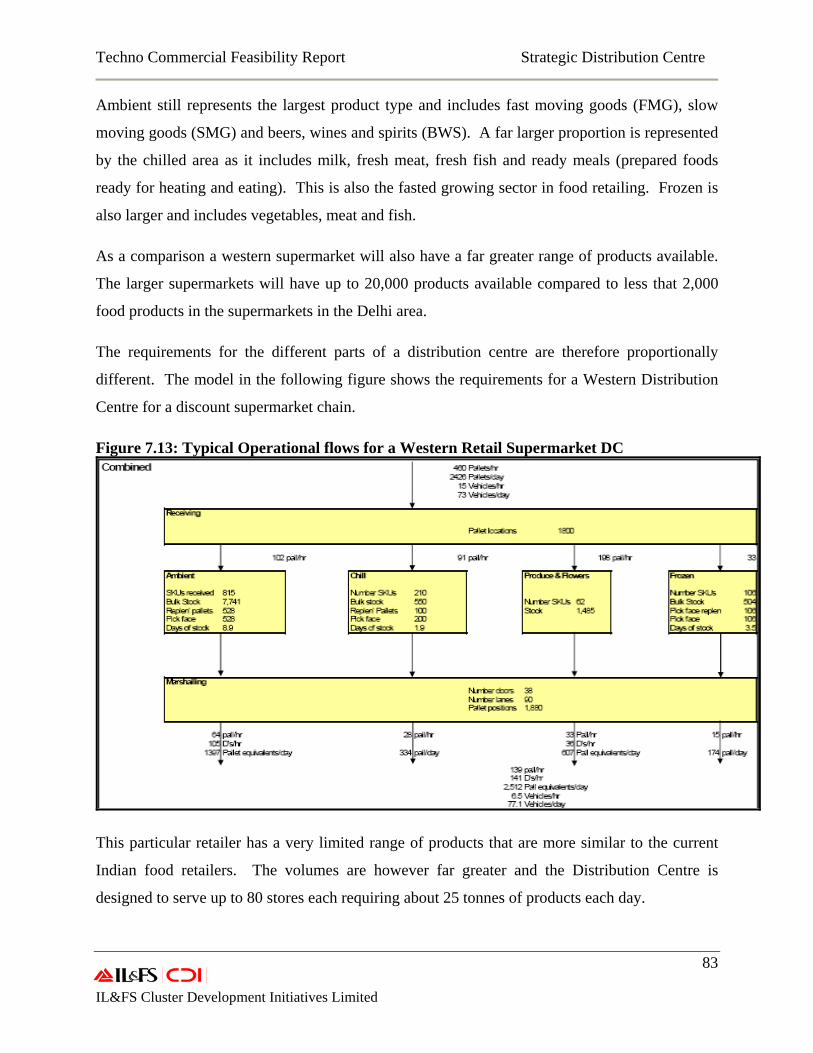

Figure 7.13: Typical Operational flows for a Western Retail Supermarket DC 83

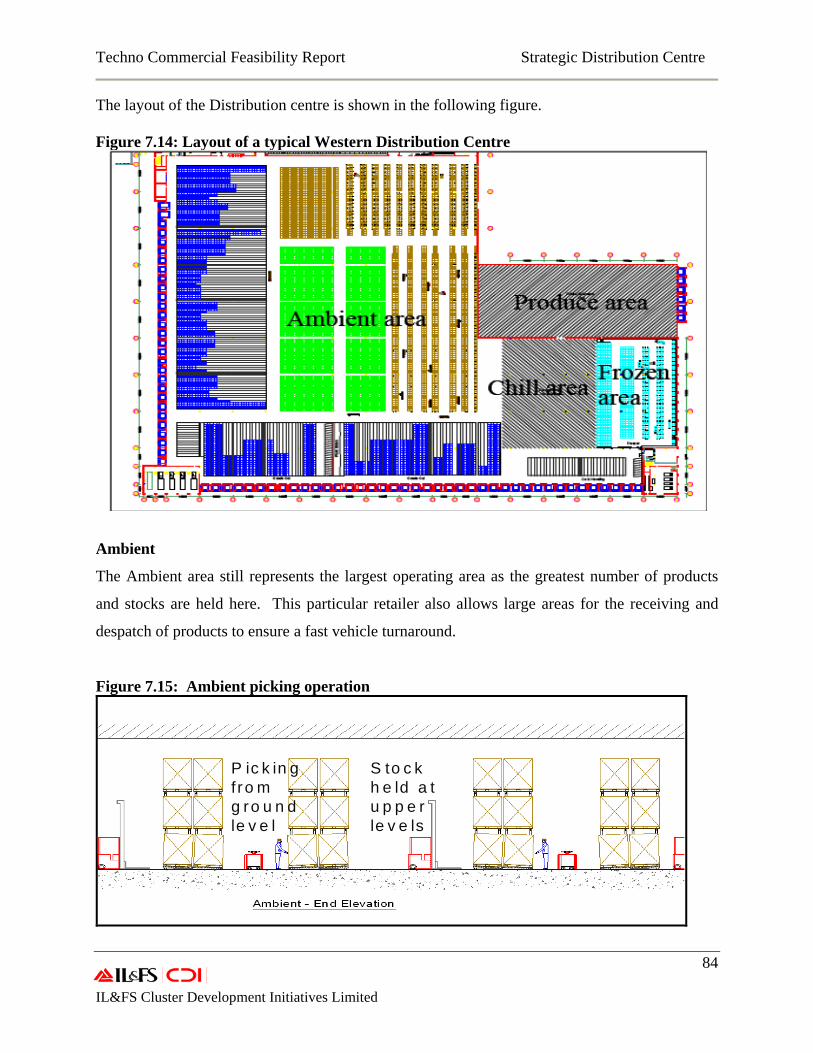

Figure 7.14: Layout of a typical Western Distribution Centre 84

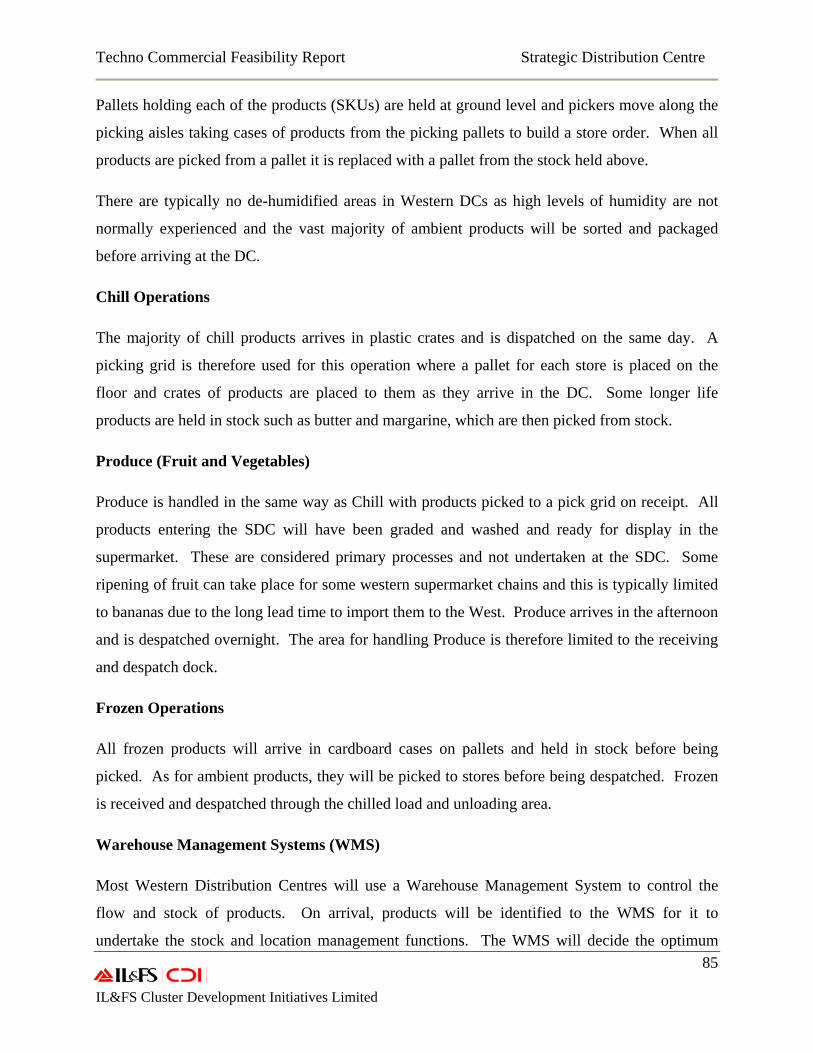

Figure 7.15: Ambient picking operation 84

Techno Commercial Feasibility Report Strategic Distribution Centre

7 IL&FS Cluster Development Initiatives Limited

Glossary 3PL – Third Party Logistics

% - percent

bn - billion

APMC – Agriculture Produce Marketing Committee

BWS – Beer, Wine and Spirits

CA – Commission Agent

CAGR – Compounded Annual Growth Rate

CWC – Central Warehousing Corporation

CNF – Carrying and Forward Agent

DC – Distribution Center

DES - Directorate of Economics and Statistics

DMI – Directorate of Marketing and Inspection, Government of India

DSCR – Debt Service Coverage Ratio

DSD – Direct Store Delivery

F&B – Food & Beverages

FCI – Food Corporation of India

FICCI – Federation of Indian Chambers of Commerce and Industry

FMCG – Fast Moving Consumer Goods

FT – Flow Through

GDP – Gross Domestic Product

HH - Households

IIM – Indian Institute of Management

INR – Indian Rupees

IRR – Internal Rate of Return

Techno Commercial Feasibility Report Strategic Distribution Centre

8 IL&FS Cluster Development Initiatives Limited

KWH – Kilo Watt Hour

LPH – Litre Per Hour

MFP – Mega Food Parks

MFPI/MoFPI – Ministry of Food Processing Industries

MPCE – Monthly Per Capita Consumption Expenditure

MT – Metric Tonnes

NCAER – National Council of Applied Economic Research

NCR – National Capital Region

OGP – Oilseeds, Grains and Pulses

PFCE – Per Capita Private Final Consumption Expenditure

PTC – Price to Consumer

RBI – Reserve Bank of India

RDC – Regional Distribution Center

SEZs – Special Economic Zones

SDC – Strategic Distribution Center

SKU – Stock Keeping Units

SMG – Slow Moving Goods

SPV – Special Purpose Vehicle

SWC – State Warehousing Corporations

Sq ft - Square Feet

UK – United Kingdom

US$ - US Dollars

USA – United State of Amercia

WMS – Warehouse Management System

Techno Commercial Feasibility Report Strategic Distribution Centre

9 IL&FS Cluster Development Initiatives Limited

1. Background Despite India's inherent potential to emerge as a Global Food Basket, the existing supply chain

and distribution network has been the key constraint to this. Absence of infrastructure is causing

the loss of a whopping Rs.33, 000 crore per annum in the forms of wastages and value losses. It

is also a major deterrent for the retail sector to enable them to offer the best quality products at

competitive prices. The changing role of warehousing demands modern logistics and distribution

centres.

1.1 Status of Agro and Food Industry in India

The presence of diverse agro climatic conditions of around 20 agro-climatic regions and nearly

46 out of 60 soil types along with long sunshine hours and day length round the year as also 52

per cent of total cultivable land areas against 11 per cent globally has helped India become one

of the key food producers in the world. Today, India is the largest producer of milk in the world,

and is likely to become the second largest dairy products producer in the coming years, second

largest producer of fruits and vegetables, third largest producer food grains, third largest output

of fish and has the largest number of livestock in the world.

The Indian food market in 2008 is estimated at over US$ 182 billion1 of which the retail food

sector accounted for around US$ 70 billion and the processed food market accounted for 32 per

cent. A McKinsey & Company study suggests that the Indian food market is expected to reach

US$ 344 billion in 2025 at a compound annual growth rate (CAGR) of 4.1 per cent. McKinsey &

Company further estimate that the retail food sector in India is likely to grow from around US$

70 billion in 2008 to US$ 150 billion by 2025 and will account for a large chunk of the world

food industry, which is likely to grow to US$ 400 billion from US$ 175 billion. A survey by

FICCI suggests that India's food and beverages (F&B) sector is expected to touch Rs 4,660-

billion mark by the March 2009, growing at 9% rate.

The outlook of growth of the food consumption in the year 2010 and 2015 is provided in the

table below:

1 'India Food Report 2008' by Research and Markets

Techno Commercial Feasibility Report Strategic Distribution Centre

10 IL&FS Cluster Development Initiatives Limited

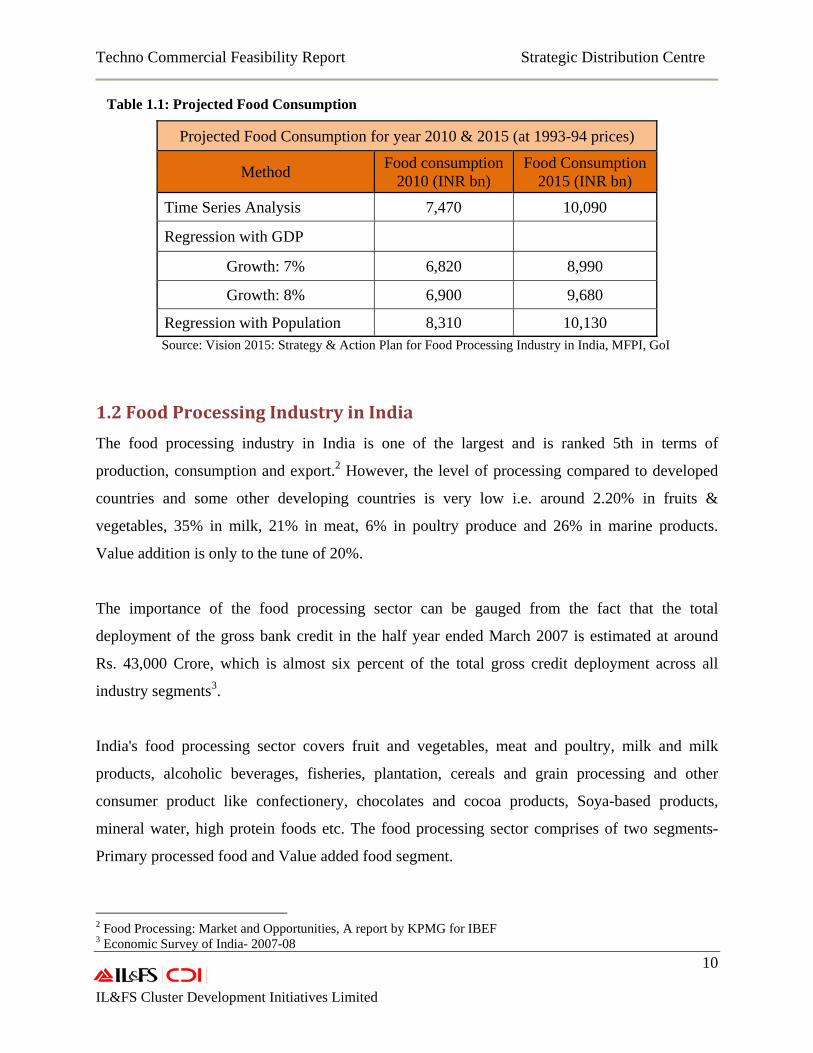

Table 1.1: Projected Food Consumption

Projected Food Consumption for year 2010 & 2015 (at 1993-94 prices)

Method Food consumption2010 (INR bn)

Food Consumption 2015 (INR bn)

Time Series Analysis 7,470 10,090

Regression with GDP Growth: 7% 6,820 8,990

Growth: 8% 6,900 9,680

Regression with Population 8,310 10,130 Source: Vision 2015: Strategy & Action Plan for Food Processing Industry in India, MFPI, GoI

1.2 Food Processing Industry in India The food processing industry in India is one of the largest and is ranked 5th in terms of

production, consumption and export.2 However, the level of processing compared to developed

countries and some other developing countries is very low i.e. around 2.20% in fruits &

vegetables, 35% in milk, 21% in meat, 6% in poultry produce and 26% in marine products.

Value addition is only to the tune of 20%.

The importance of the food processing sector can be gauged from the fact that the total

deployment of the gross bank credit in the half year ended March 2007 is estimated at around

Rs. 43,000 Crore, which is almost six percent of the total gross credit deployment across all

industry segments3.

India's food processing sector covers fruit and vegetables, meat and poultry, milk and milk

products, alcoholic beverages, fisheries, plantation, cereals and grain processing and other

consumer product like confectionery, chocolates and cocoa products, Soya-based products,

mineral water, high protein foods etc. The food processing sector comprises of two segments-

Primary processed food and Value added food segment.

2 Food Processing: Market and Opportunities, A report by KPMG for IBEF 3 Economic Survey of India- 2007-08

Techno Commercial Feasibility Report Strategic Distribution Centre

11 IL&FS Cluster Development Initiatives Limited

At present the food processing sector employs about 13 million people directly and about 35

million people indirectly. As per Index of Industrial production, food products sector grew at 6.8

per cent during 2007-08. In 2005-06, food processing sector contributed about 14% of

manufacturing GDP with a share of Rs 2,80,000 Crores. Of this, the unorganized sector

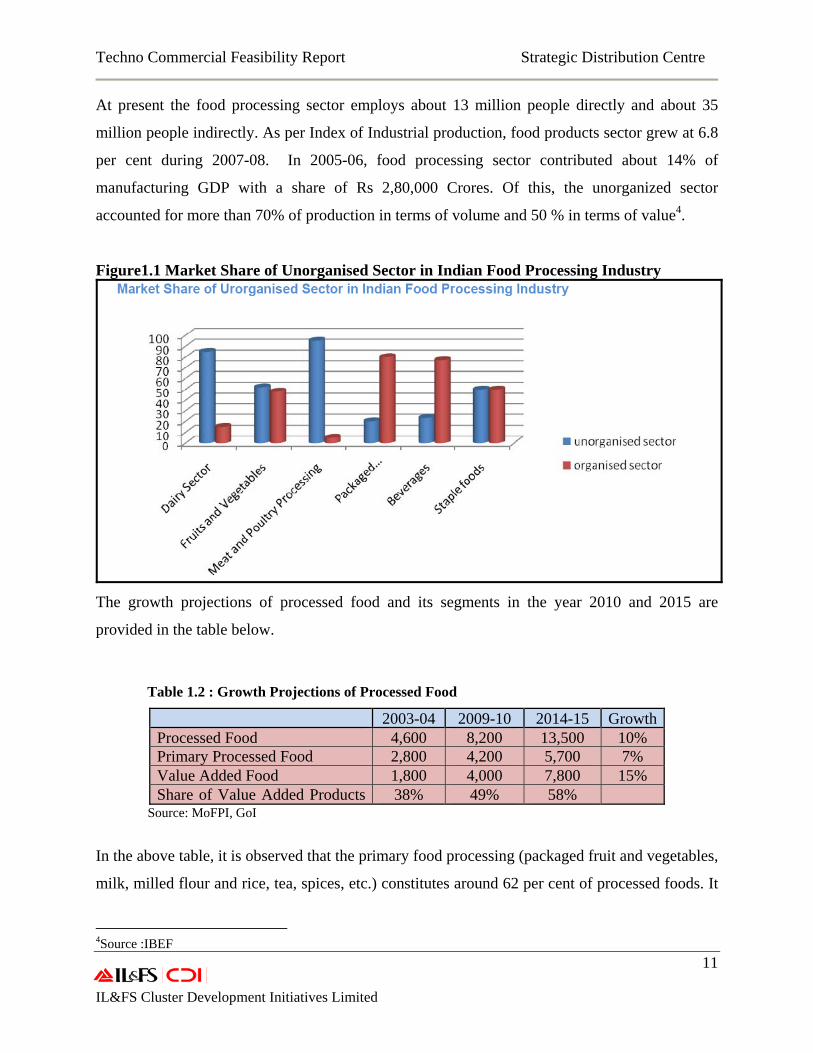

accounted for more than 70% of production in terms of volume and 50 % in terms of value4.

Figure1.1 Market Share of Unorganised Sector in Indian Food Processing Industry

The growth projections of processed food and its segments in the year 2010 and 2015 are

provided in the table below.

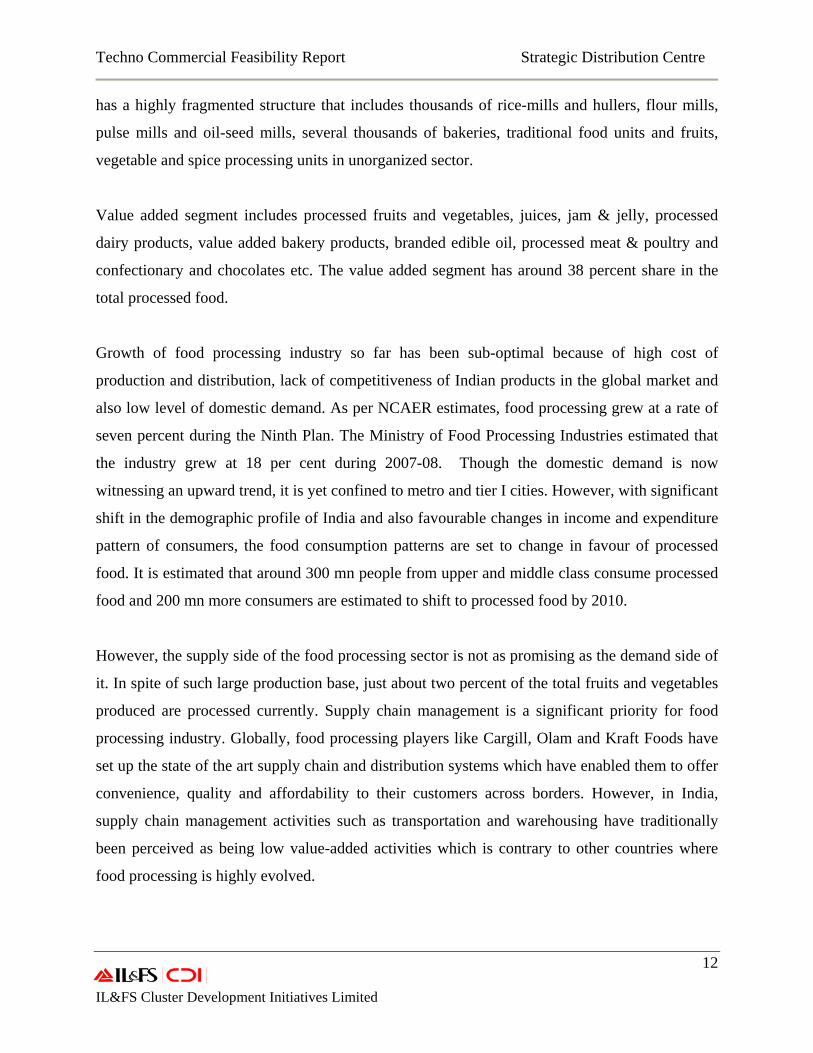

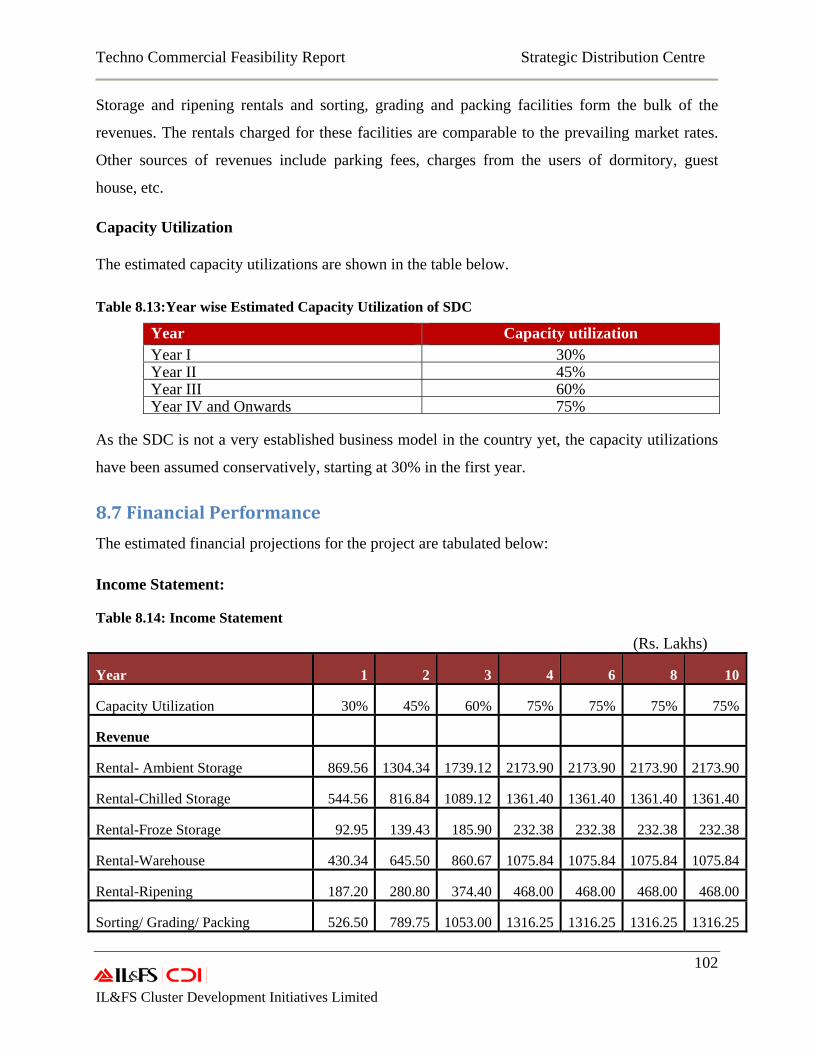

Table 1.2 : Growth Projections of Processed Food

2003-04 2009-10 2014-15 GrowthProcessed Food 4,600 8,200 13,500 10% Primary Processed Food 2,800 4,200 5,700 7% Value Added Food 1,800 4,000 7,800 15% Share of Value Added Products 38% 49% 58%

Source: MoFPI, GoI

In the above table, it is observed that the primary food processing (packaged fruit and vegetables,

milk, milled flour and rice, tea, spices, etc.) constitutes around 62 per cent of processed foods. It

4Source :IBEF

Techno Commercial Feasibility Report Strategic Distribution Centre

12 IL&FS Cluster Development Initiatives Limited

has a highly fragmented structure that includes thousands of rice-mills and hullers, flour mills,

pulse mills and oil-seed mills, several thousands of bakeries, traditional food units and fruits,

vegetable and spice processing units in unorganized sector.

Value added segment includes processed fruits and vegetables, juices, jam & jelly, processed

dairy products, value added bakery products, branded edible oil, processed meat & poultry and

confectionary and chocolates etc. The value added segment has around 38 percent share in the

total processed food.

Growth of food processing industry so far has been sub-optimal because of high cost of

production and distribution, lack of competitiveness of Indian products in the global market and

also low level of domestic demand. As per NCAER estimates, food processing grew at a rate of

seven percent during the Ninth Plan. The Ministry of Food Processing Industries estimated that

the industry grew at 18 per cent during 2007-08. Though the domestic demand is now

witnessing an upward trend, it is yet confined to metro and tier I cities. However, with significant

shift in the demographic profile of India and also favourable changes in income and expenditure

pattern of consumers, the food consumption patterns are set to change in favour of processed

food. It is estimated that around 300 mn people from upper and middle class consume processed

food and 200 mn more consumers are estimated to shift to processed food by 2010.

However, the supply side of the food processing sector is not as promising as the demand side of

it. In spite of such large production base, just about two percent of the total fruits and vegetables

produced are processed currently. Supply chain management is a significant priority for food

processing industry. Globally, food processing players like Cargill, Olam and Kraft Foods have

set up the state of the art supply chain and distribution systems which have enabled them to offer

convenience, quality and affordability to their customers across borders. However, in India,

supply chain management activities such as transportation and warehousing have traditionally

been perceived as being low value-added activities which is contrary to other countries where

food processing is highly evolved.

Techno Commercial Feasibility Report Strategic Distribution Centre

13 IL&FS Cluster Development Initiatives Limited

The current structure of the Indian food processing industry itself is a major deterrent for the

growth of the sector. The unorganized sector constitutes for almost two-third of the food

processing units and mostly includes small flour and rice mills, and various small and medium

size units for products like pickles & papads, chutneys, jam, jelly, ketchups, juices etc. However,

this segment suffers from low efficiency due to lack of modern technology, inadequate logistics

and distribution facilities and market linkages for forward distribution and access to credit.

Recently, the sector is gradually seeing the entry of organized players. However, it still accounts

for only 25 percent of the total food processing units.5 The key impediments behind the slow

growth of the size of organized sector has been identified as the lack of processing, storage,

packaging and distribution infrastructure for food items including fresh produce. Lack of such

facilities also results in huge wastages of perishable (including fruits and vegetables) estimated at

about 35 percent, the value of which is a Rs. 33, 000 Crore annually.6 A developed food

processing industry supported by adequate distribution and logistics network would not only

assist to reduce the wastages, but would also fetch increased income to stakeholders including

growers.

As per the estimates by MFPI, India requires an investment of US$ 28 billion to bring the level

of processing to 10-12 per cent by 2012. The Ministry of Food Processing has introduced several

fiscal incentives to strengthen the infrastructure and supply chain integration to promote the food

processing industry. Last but not the least, the food processing sector has immense employment

generation potential. An investment of one million in the food processing sector generates 1.8

direct jobs and 6.4 indirect jobs.

The Vision – 2015 prepared by the Ministry of Food Processing Industries envisages

• increasing processing level of perishables from 6 to 20%,

• increase in value addition from the present level of 20 to 34% and

• increased share in global trade from 1.6 to 3%,

5 FAIDA/MFPI, GoI 6 Working Group Report, XI FYP, MoFPI

Techno Commercial Feasibility Report Strategic Distribution Centre

14 IL&FS Cluster Development Initiatives Limited

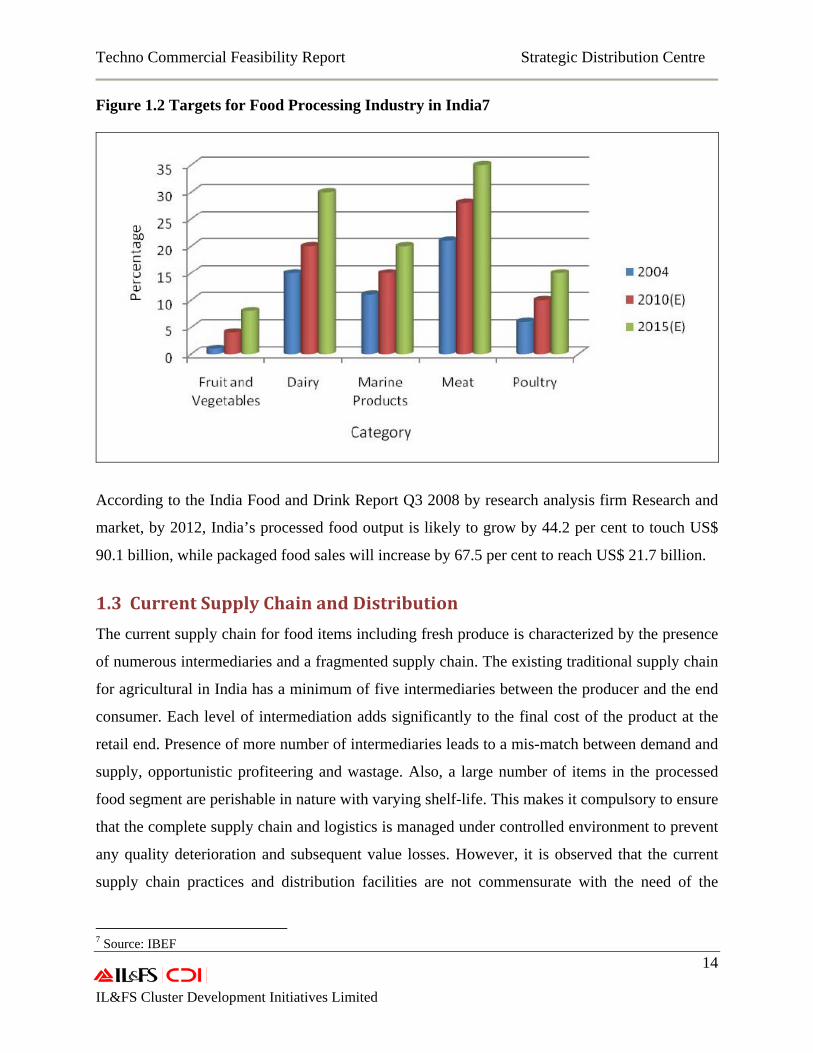

Figure 1.2 Targets for Food Processing Industry in India7

According to the India Food and Drink Report Q3 2008 by research analysis firm Research and

market, by 2012, India’s processed food output is likely to grow by 44.2 per cent to touch US$

90.1 billion, while packaged food sales will increase by 67.5 per cent to reach US$ 21.7 billion.

1.3 Current Supply Chain and Distribution The current supply chain for food items including fresh produce is characterized by the presence

of numerous intermediaries and a fragmented supply chain. The existing traditional supply chain

for agricultural in India has a minimum of five intermediaries between the producer and the end

consumer. Each level of intermediation adds significantly to the final cost of the product at the

retail end. Presence of more number of intermediaries leads to a mis-match between demand and

supply, opportunistic profiteering and wastage. Also, a large number of items in the processed

food segment are perishable in nature with varying shelf-life. This makes it compulsory to ensure

that the complete supply chain and logistics is managed under controlled environment to prevent

any quality deterioration and subsequent value losses. However, it is observed that the current

supply chain practices and distribution facilities are not commensurate with the need of the

7 Source: IBEF

Techno Commercial Feasibility Report Strategic Distribution Centre

15 IL&FS Cluster Development Initiatives Limited

processing industry. The inefficiencies in the system adversely affect the stakeholders’ income

and also make products less competitive.

A recent World Bank Study mentions that the “vastness of India, with large distances between

growing and consuming regions lead to high domestic transportation costs, and high wastage

when commodities are moved, due in large part to poor infrastructure and the lack of cold

storage infrastructure. For example in Apples - the major apple producing areas of the country

are located in the north and northeastern parts of India, and most apple trade happens through

Delhi. Domestically grown apples are much cheaper than foreign apples in markets located near

these regions. However the high cost of transporting and marketing these in the southern and

western regions leads to very high prices in these markets, rendering domestic production

uncompetitive. Apple prices in Chennai are almost 70 per cent higher than those in Delhi.” In

India various studies have estimated wastages at about 35% in case of fruits and vegetables, the

value of which is approximately Rs.33,000 Crore annually

A developed food processing industry would not only reduce the wastages, but would also

increasingly fetch remunerative income to farmers which is another problem before the

agriculture sector at present. A FIICCI –KPMG survey has highlighted some of the long-pending

demands of the industry like income tax exemption of agriculture and farm produce, cold storage

and processing of fruit and vegetables from April 2007 to March 2012. The survey said that

"The setting up of cold chain and other modernised technology for upgrading of storage handling

and transportation should be granted infrastructure status and a 10-year tax holiday should be

provided to it".

1.4 Current Logistics & Warehousing Scenario The market size of Indian logistics sector in 2007 is estimated at US$ 9.75 billion and is growing

at a CAGR of 7 percent. Logistics cost in India is 13 percent of GDP as compared to 11 percent

in Europe and 9 percent in U.S.A. The organized logistics market has a meager 6 percent share

though it is projected to become a US$ 15 billion industry by 2011.8 The higher spending on

warehousing and logistics is largely attributed to inadequate infrastructure facilities throughout

8 GATI-Logistics Industry Report

Techno Commercial Feasibility Report Strategic Distribution Centre

16 IL&FS Cluster Development Initiatives Limited

the country. Warehousing, packaging and transportation accounts for 24 percent of the total

logistics cost, while transportation alone accounts for almost 40 percent.9

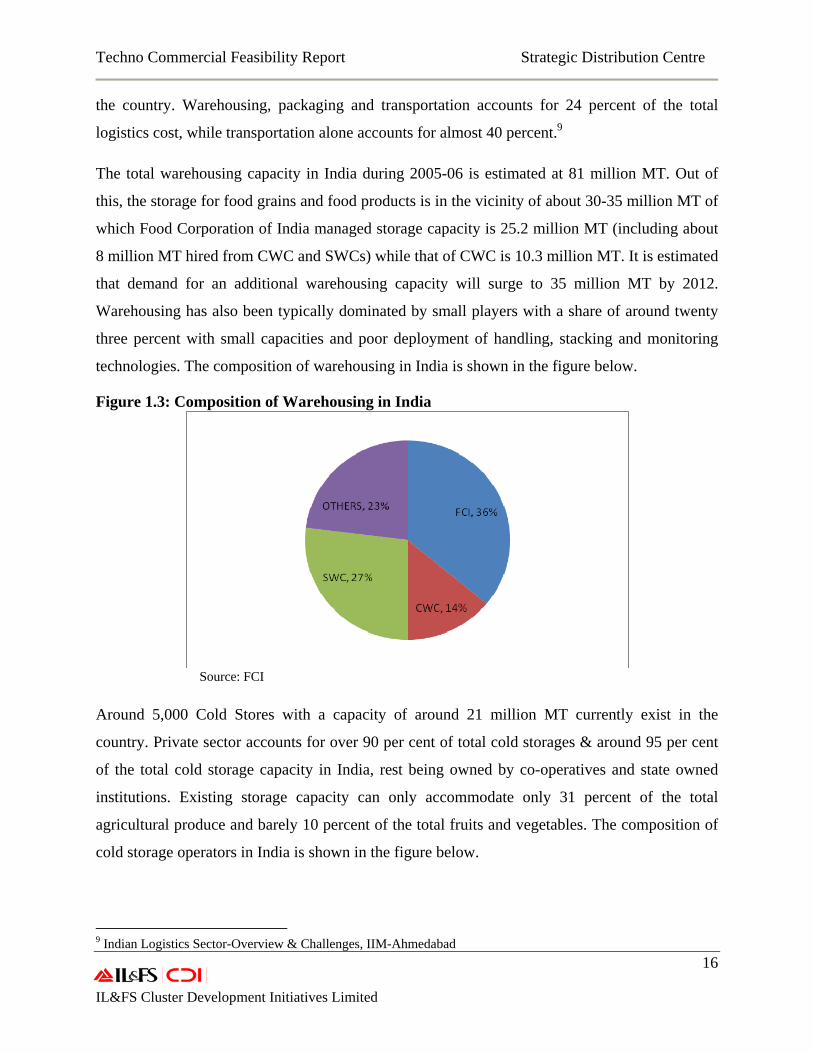

The total warehousing capacity in India during 2005-06 is estimated at 81 million MT. Out of

this, the storage for food grains and food products is in the vicinity of about 30-35 million MT of

which Food Corporation of India managed storage capacity is 25.2 million MT (including about

8 million MT hired from CWC and SWCs) while that of CWC is 10.3 million MT. It is estimated

that demand for an additional warehousing capacity will surge to 35 million MT by 2012.

Warehousing has also been typically dominated by small players with a share of around twenty

three percent with small capacities and poor deployment of handling, stacking and monitoring

technologies. The composition of warehousing in India is shown in the figure below.

Figure 1.3: Composition of Warehousing in India

Source: FCI

Around 5,000 Cold Stores with a capacity of around 21 million MT currently exist in the

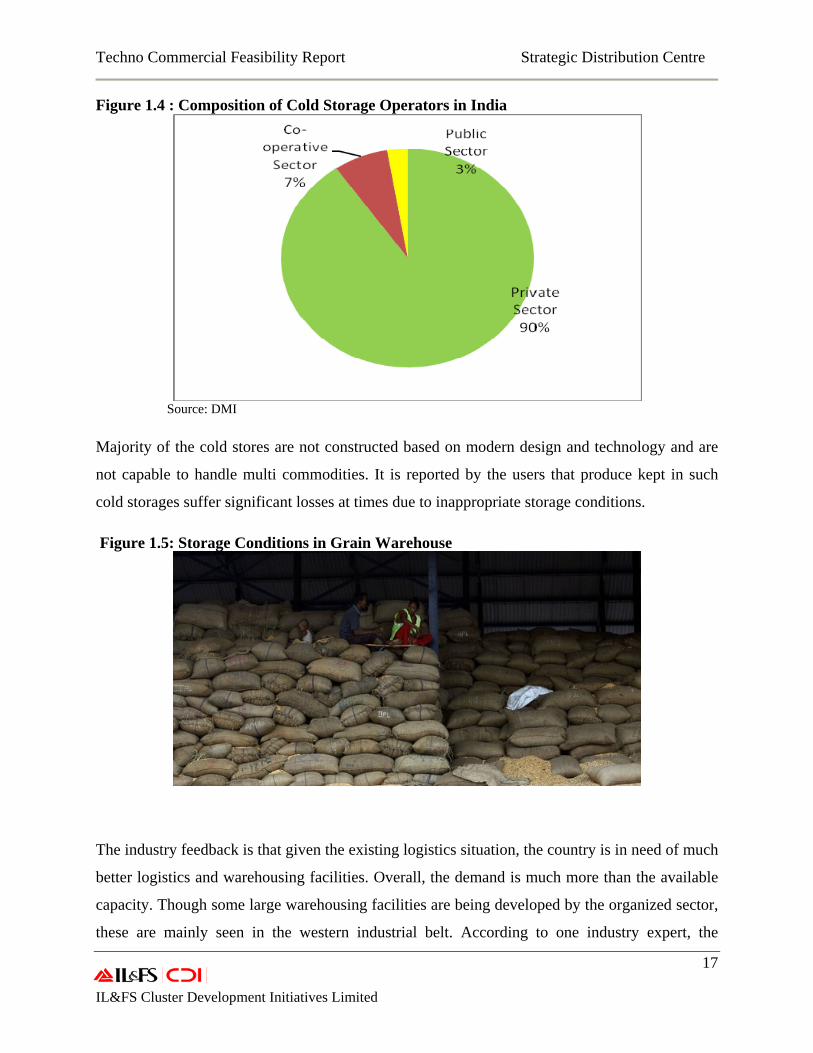

country. Private sector accounts for over 90 per cent of total cold storages & around 95 per cent

of the total cold storage capacity in India, rest being owned by co-operatives and state owned

institutions. Existing storage capacity can only accommodate only 31 percent of the total

agricultural produce and barely 10 percent of the total fruits and vegetables. The composition of

cold storage operators in India is shown in the figure below.

9 Indian Logistics Sector-Overview & Challenges, IIM-Ahmedabad

Techno Commercial Feasibility Report Strategic Distribution Centre

17 IL&FS Cluster Development Initiatives Limited

Figure 1.4 : Composition of Cold Storage Operators in India

Source: DMI

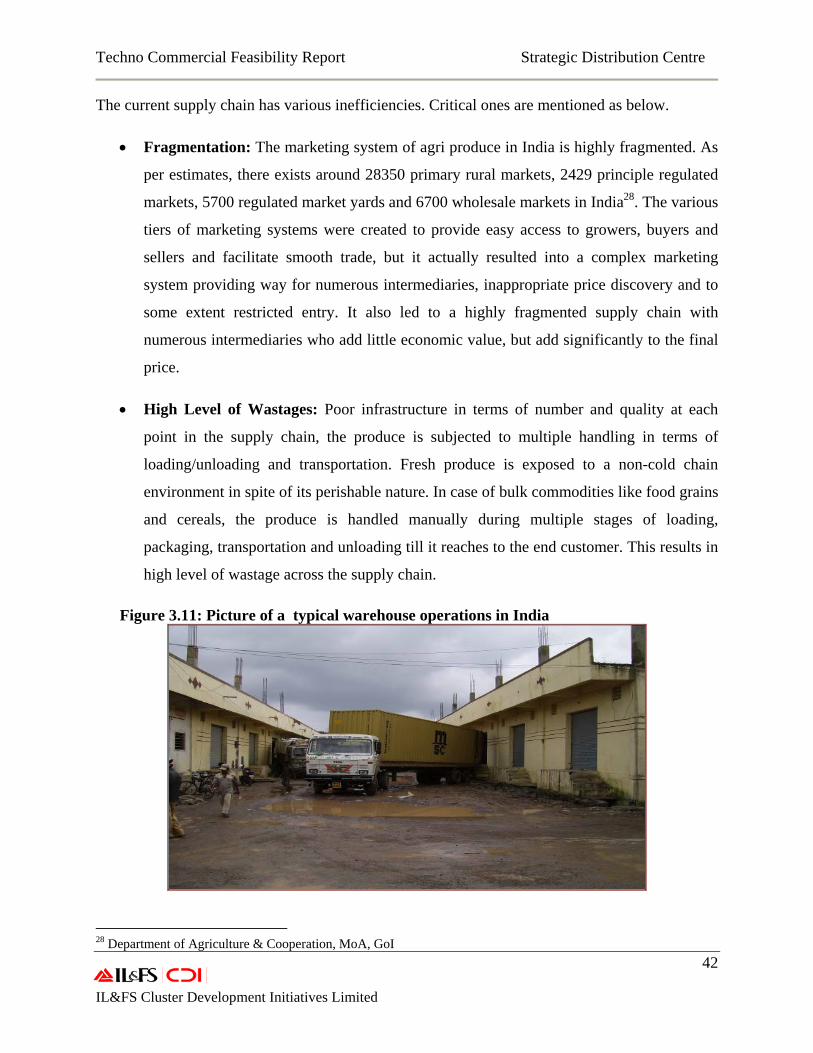

Majority of the cold stores are not constructed based on modern design and technology and are

not capable to handle multi commodities. It is reported by the users that produce kept in such

cold storages suffer significant losses at times due to inappropriate storage conditions.

Figure 1.5: Storage Conditions in Grain Warehouse

The industry feedback is that given the existing logistics situation, the country is in need of much

better logistics and warehousing facilities. Overall, the demand is much more than the available

capacity. Though some large warehousing facilities are being developed by the organized sector,

these are mainly seen in the western industrial belt. According to one industry expert, the

Techno Commercial Feasibility Report Strategic Distribution Centre

18 IL&FS Cluster Development Initiatives Limited

warehousing market in the country is 3,922 million sq. ft and is growing at 31% but the supply is

miniscule with limited quality warehouses in the country.

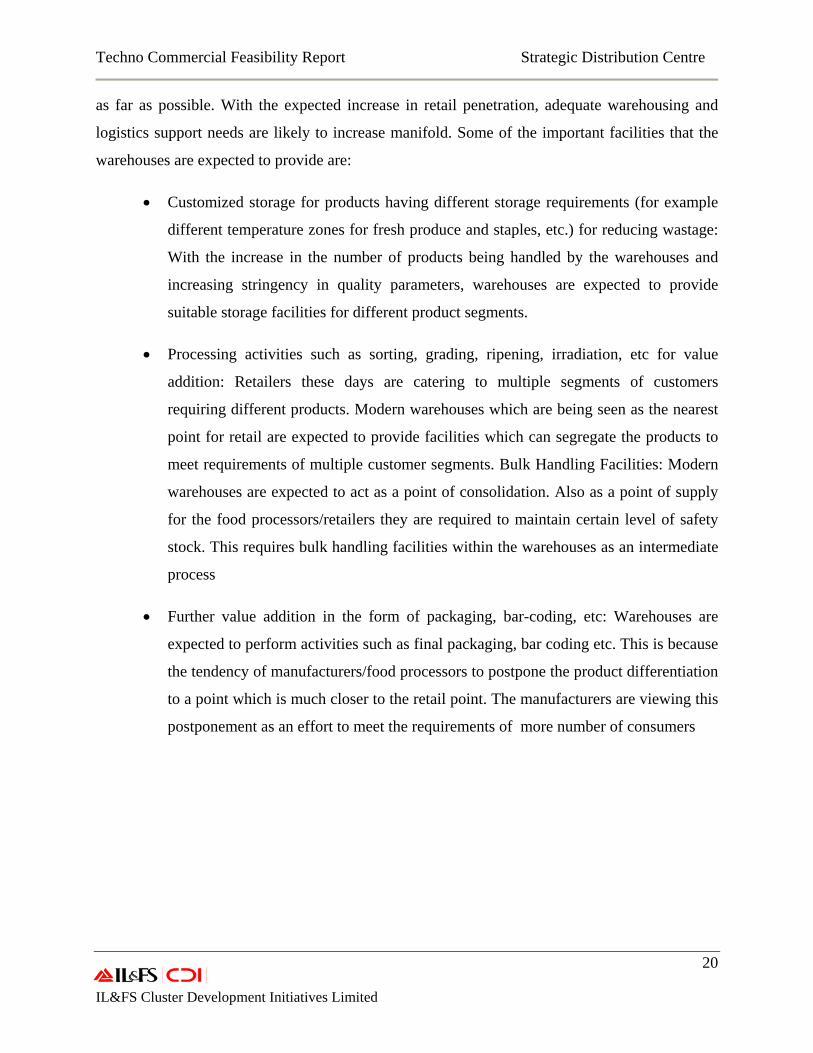

The relative value of costs of various elements of the logistics in India is shown in the figure

below.

Figure 1.6: Cost Elements of Logistics in India

Source: Indian Logistics Sector-Overview & Challenges, IIM-Ahmedabad

It is observed that on an average, warehousing packaging transportation and losses during the movement together account for almost sixty six percent of the total logistic cost followed by inventory and other costs.

3PL Usages in Distribution and Logistics

The third party logistics (3PL) is a highly evolved sector in developed countries with a state-of-

the-art distribution and logistics management systems. It has been reported that logistics in

developed countries is mostly outsourced to a third party who is responsible for complete

logistics on behalf of the companies engaged in the business of retail and distribution. In India,

3PL is still in a nascent phase, though growing at a rate of 20 percent per annum and has been

observed to have strong correlation with the growth of retail. Level of outsourcing is to the

extent of 26 percent in the organized retail supply chain and the share of 3PL in the same is

estimated at around 30 percent10. With regional food & grocery retail players entering in the rest

of the country, their logistics strategy and needs are transforming very significantly with this

nationwide expansion. It is expected that as the retail grows, the organized segment is likely to

10 Technopak- Supply Chain Challenges in the India Retail Sector, January 2008

Techno Commercial Feasibility Report Strategic Distribution Centre

19 IL&FS Cluster Development Initiatives Limited

outsource their distribution and logistics subject to an assurance of benchmark quality and

reliable services. The current challenge before the existing distribution and logistics operators is

to meet the specific needs of retail in terms of need based replenishments, robust supply chain

information systems, value additions such as packaging and bar-coding and increased control

over stock losses. These challenges can only be met by putting in place the state-of-the-art

modern distribution and warehousing systems which can handle multi commodities from

manufacturing to retail.

1.5 Changing Face of Indian Consumerism: Growth in Retail India’s economic growth has accelerated in the last two decades. This has led to a surge in the

spending power of the customers. Based on the rise in income levels, the shape of the country’s

income pyramid has changed dramatically due to fattening of a burgeoning middle class. It is

estimated that India’s middle class will swell by over ten times from its current size of 50 million

to 583 million by 2025. With these changes in incomes, the expenditure pattern is also

witnessing paradigm shift. Food and beverages alone contributes about 42 percent of private

consumption expenditure11. With the rising convenience needs of dual income families, the

demand for processed food products is also growing. The robust growth in economy and

favourable changes in demographics has spurred the evolution of retail. The growth of retail

which so far is largely limited to metro and tier I cities is likely to enter in tier II cities. The retail

sector is estimated to grow at a CAGR of 8.6 percent from US$ 300 bn in 2006 to US$ 453 bn by

2011. Organized retail revenues are expected to increase from an estimated US$ 12.9 billion in

2005-06 to more than US$ 43.8 billion by 2010-11.12 The growth in retail will influence

significant changes in the distribution and logistics sector. The logistics sector, currently engaged

in providing warehousing and transport services, is expected to provide the holistic solution to

the supply chain needs of the retail.

1.6 Changing Role of Warehousing Changing customer requirements have ushered in changes in the traditional role (which involves

mostly storage functions) of warehouses. Warehouses today are expected to play a much more

important role than storage only. The most critical parameter for the retail to succeed is to reach

11 Economic Survey of India 2007-08 12 Retail: Shopping Goes Hyper, Edelweiss, 2008

Techno Commercial Feasibility Report Strategic Distribution Centre

20 IL&FS Cluster Development Initiatives Limited

as far as possible. With the expected increase in retail penetration, adequate warehousing and

logistics support needs are likely to increase manifold. Some of the important facilities that the

warehouses are expected to provide are:

• Customized storage for products having different storage requirements (for example

different temperature zones for fresh produce and staples, etc.) for reducing wastage:

With the increase in the number of products being handled by the warehouses and

increasing stringency in quality parameters, warehouses are expected to provide

suitable storage facilities for different product segments.

• Processing activities such as sorting, grading, ripening, irradiation, etc for value

addition: Retailers these days are catering to multiple segments of customers

requiring different products. Modern warehouses which are being seen as the nearest

point for retail are expected to provide facilities which can segregate the products to

meet requirements of multiple customer segments. Bulk Handling Facilities: Modern

warehouses are expected to act as a point of consolidation. Also as a point of supply

for the food processors/retailers they are required to maintain certain level of safety

stock. This requires bulk handling facilities within the warehouses as an intermediate

process

• Further value addition in the form of packaging, bar-coding, etc: Warehouses are

expected to perform activities such as final packaging, bar coding etc. This is because

the tendency of manufacturers/food processors to postpone the product differentiation

to a point which is much closer to the retail point. The manufacturers are viewing this

postponement as an effort to meet the requirements of more number of consumers

Techno Commercial Feasibility Report Strategic Distribution Centre

21 IL&FS Cluster Development Initiatives Limited

Growth in retail sector and agro–processing industries has multiplied the need for this sort of

modern warehousing cum distribution centers.

While emphasis is being given to the supply side of the distribution chain the other aspect of the

distribution chain i.e. creation of demand is being neglected. The absence of an organized

distribution chain is hampering the growth of the food processing industry in India as distribution

is not being seen as a force to create more demand. Absence of an efficient distribution system is

acting as a bottleneck in creating large scale demand for the value added processed food items.

This is also limiting the export potential for Indian processed food items. A modern warehousing

cum distribution center helps the food processors, mainly, in overcoming this bottleneck. More

specifically it can perform the following functions

• Creating more retail visibility for the food items

• Increasing handling efficiency for catering the needs of export market

It may also help the processors in sourcing raw material for their units. The demand side

functions that a modern warehousing cum distribution center can perform are detailed below:

Retail Visibility: Production and distribution are interdependent and grow together. Due to

decentralized distribution system of food items including that of processed foods the landed cost

of items at the point of retail is increasing which in turn is reducing the willingness of the

retailers to store a variety of products subsequently affecting the off-take of the products. On the

other hand the food processors are not investing in large scale production as they don’t see the

retail space for their products.

Small scale production of processed/value added food items is increasing the cost of the

production and subsequently affecting the price of the product. All these are leading to a scenario

of small scale production, lesser retail space confined to a very small geographical area and a

cost which is not affordable by the masses. The scenario, pictorially, is depicted below.

Techno Commercial Feasibility Report Strategic Distribution Centre

22 IL&FS Cluster Development Initiatives Limited

Figure 1.7: Retail Visibility

There is a latent demand for the processed/value added food items on account of changing

demographics such as higher disposable income along with more increasing expenditure for food

items, more number of working couple looking for convenience in food preparation, etc. and

modern distribution chains with large retailers and wholesalers targeting different market

segments exploit the market more effectively. Changing demographics and subsequent changes

in food retail have been explained later.

This requires the presence of the items in the neighbourhood shops, more visibility and an

affordable price. This will be possible only when there is large scale production which is linked

to a streamlined distribution system. A modern warehousing cum distribution center can go a

long way in streamlining the present day distribution structure thus encouraging the food

processing industry to reach the mass market with large scale production with an affordable

price.

Efficiency for export market:

India produces a variety of fruits and vegetables which command good market demand in the

overseas market. Also, the popularity of Indian culinary is growing in these markets. Hence India

is considered to be a supplier base for foreign retailers. But Indian products are not price

competitive in comparison to some other countries even though the cost of production is lower in

Techno Commercial Feasibility Report Strategic Distribution Centre

23 IL&FS Cluster Development Initiatives Limited

India. This is mainly attributed to the suppliers and the distribution channels which are small and

unorganized and have in-built inefficiency.

Source: Study conducted by MoFPI, GoI

To cater to the export market the distribution chain must be able to handle volumes and be able

to maintain stringent quality parameters throughout the chain. Most of the issues mentioned

above in the box can be addressed by a modern warehousing cum distribution center. The center

can handle large volumes of a number of items thus giving the importer a scope to choose his

product. It can maintain stringent quality parameters through in-house infrastructure. It can act as

an intermediate infrastructure between farm gate and import point through provision of storage

and other primary processing facilities. Above all it may re-define the supply chain and use

information technology to improve the overall efficiency of the existing supply chain. In short, it

will help the food processors in reaching out to the export market.

A benchmarking study targeted at US and Australia shows that Indian exporters enjoy tremendous advantages in the supply of food products and raw materials to the large retail chains in the developed countries. The cost advantage of Indian food articles has been estimated up to 35% since the Indian farm gate prices are cheaper. The use of information technology in the supply chain is also cheaper in India. The major barriers to export are marketing issues and quality standards.

This will require focused attention on the following:

While the country and the cost factors have been rated as good in case of India, the weak links are factors related to supply of products and provision of services. In respect of transportation bottlenecks and communication infrastructure, Indian manufacturers still face considerable risks

As far as supply chain is concerned, lack of variety of sourceable items quality guarantees and ethical standards constitute weak points

Facilities in respect of in-house research, cold storage and product testing and flexibility of shifting to new varieties as well as length of the supply chain are other areas which need to be addressed.

Techno Commercial Feasibility Report Strategic Distribution Centre

24 IL&FS Cluster Development Initiatives Limited

Raw Material Handling Facility:

The modern warehousing cum distribution center is also expected to deal with fresh fruits and

vegetables for catering to the needs of the fresh market segment. While the produce fit for fresh

segment can directly go to the retail markets, processors can source the rest of the produce fit for

processing

Thus in the changing scenario a modern warehousing cum distribution center is expected to cut

down the costs involved in procurement and distribution besides improving efficiency of the

distribution chain. A modern warehousing cum distribution center is seen as a marketing

infrastructure that would support agricultural growth as well as growth of the processed food

market.

Through these functions a modern warehousing cum distribution center is expected to overcome

following inefficiencies:

Higher cost of sales and distribution

Distribution and marketing is a huge cost in Indian consumer markets leading to overall

inefficiency. Various studies and reports have pointed out that in the current context in Indian

markets; distribution remains the biggest challenge in the supply chain of food items. High

logistics costs and higher level of inventories, which are to be maintained due to the nature (such

as seasonality and shelf life) of the products involved is increasing the final price of the products

thus reducing the consumer benefit. However, this higher price is not resulting in better price

realization for producers due to overall in-efficiency in the supply chain. This is also hampering

the overall growth of food market. A modern warehousing cum distribution center in place may

help to improve the current status of food supply chain.

Frequent stock outs

One of the major challenges in distribution is that demand changes quickly, but supply takes

longer to change. Surges in demand strain the capacity of supply chain and distribution,

compelling it to handle much more throughput than its capacity. Traditional distribution systems

have not been able to reduce these problems due to the lack of capacity in consolidating the

Techno Commercial Feasibility Report Strategic Distribution Centre

25 IL&FS Cluster Development Initiatives Limited

produce. This results in frequent stock outs for the retailers. The stock-out levels among Indian

retailers is in the range of 10 to 15 percent.13 The cost of these stock-outs is very high for the

retailers especially in the case of organized retailers. This also results in price fluctuations in

consumer price as there is a mismatch between the supply and demand of food products. This

has necessitated the establishment of modern warehousing cum distribution centers nearer to

consumption markets.

1.7 Mega Food Parks Ministry of Food Processing has launched the scheme to set up thirty Mega Food Parks (MFP) at

various locations across the country under 11th Five Year Plan. Ten of the proposed thirty MFPs

are likely to become operational in next 2-3 years. Such parks, once in place, are expected to

spur food processing in the country. Finished products from the MFPs will need to be supported

by strategic distribution networks before reaching out to the end customers. Most of such

processed products shall require an ambient condition for storage and appropriate handling

facility during warehousing. In addition to the Mega Food Park Scheme, there are other

initiatives such as the integrated cold chain, initiatives by the State Governments to promote food

processing industry, etc. which are expected to generate demand for specialized storage facilities

and the distribution network specific to food products in the country.

The distribution centres will act as hubs for distribution of food products for the domestic retail

segment including super markets as well as for exports of processed foods. The Ministry of Food

Processing Industries (MoFPI) proposes to facilitate the establishment of Strategic Distribution

Centres (SDCs) which will form the nerve centres of the various supply chain networks

including cold chain networks supporting the Mega Food Parks which are to be set up in the

country under the 11th five year plan scheme.

Since such Distribution Centres do not exist in the country, the MoFPI has commissioned a study

to explore the feasibility of setting up a SDC in the country (Scope of Work in the Annexure I).

13 IL&FS CDI Field study

Techno Commercial Feasibility Report Strategic Distribution Centre

26 IL&FS Cluster Development Initiatives Limited

2. Objective and Methodology

The techno-commercial feasibility study of a Strategic Distribution Center (SDC) involves

detailed conceptualization of market, geographic and demographic conditions along with the

supply chain solutions and costs, a detailed location analysis, adoption of a scientific method to

arrive at the design and layout and detailed financial analysis.

2.1 Objective

The broad objective of the assignment is

“To assess the techno-commercial feasibility of a Strategic Distribution Center (SDC”

Specific objectives of this techno-commercial feasibility study are as follows:

• To find out a potential location (city) for a pilot SDC • To identify suitable sites where SDC can be established • To study the existing supply chain and its inefficiencies in the catchment areas of the

SDC • To analyze the existing infrastructure and related gaps in the SDC location • To suggest facilities that can be provided through SDC • To estimate the throughput that can be handled by the SDC • To develop a scientific design and layout for the SDC • To suggest scientific operational processes in the SDC • To suggest viable business models for the SDCs in consultation with the stakeholders • To analyze the financial viability of the SDC

2.2 Methodology

The following methodology is being adopted to establish the techno-commercial feasibility of a

Strategic Distribution Center (SDC):

Conceptualization

Intensive one-to-one discussions were carried out with a number of organized retailers,

wholesalers, exporters and other industry representatives and Government officials to develop a

Techno Commercial Feasibility Report Strategic Distribution Centre

27 IL&FS Cluster Development Initiatives Limited

detailed concept of the SDC. This was aimed at understanding the requirement of the industry

and also their views on the need for the SDC.

Location analysis

After conceptualizing the SDC the next task was to find out a suitable location for the pilot

facility. Demographic, socio-economic and market related information was gathered for major

cities of India through intensive secondary research. Cities were compared with respect to the

above-mentioned parameters to arrive at the two most suitable locations for the SDC.

An intensive field based study was carried out to choose the best among the two. The field based

study included components such as assessment of the food market, estimate of throughput,

assessment of infrastructure, etc. Details of the location analysis are provided in Chapter-5.

Assessment of the supply chain and estimation of throughput

An assessment of the supply chain was carried out in the catchment area of the SDC to find out

supply chain and inventory management related gaps. A major aim of the assessment was to

finalize the facilities to be provided in the SDC.

Similarly an estimate of marketed food items in the SDC location was undertaken to arrive at the

capacities of the SDC and its facilities. This was also helpful in developing the design and layout

of the pilot SDC.

Site selection

An analysis of the infrastructure in and around the potential SDC location was undertaken to

arrive at a couple of the most suitable sites for the SDC. Infrastructures such as road, railway

network, availability of power and water, etc were assessed during this process.

Other issues such as availability of labour, traffic congestion, ease with which local retailers can

access the SDC were also analyzed in detail. Availability and cost of land was also taken into

consideration while selecting potential sites.

Developing design and layout

After estimating the throughput that the SDC can handle per day and assessing the nature of the

goods, a scientific design of the SDC was developed. Details of the design, its underlying

principles and layout of the SDC is given in Chapter-7

Techno Commercial Feasibility Report Strategic Distribution Centre

28 IL&FS Cluster Development Initiatives Limited

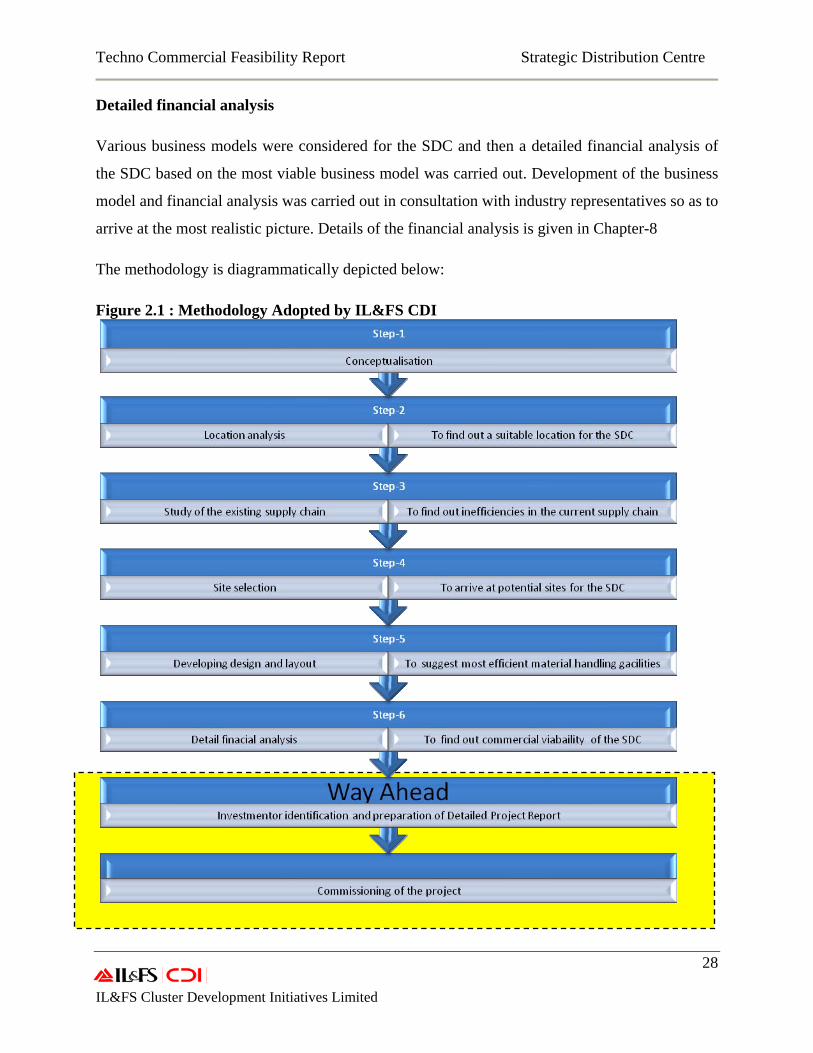

Detailed financial analysis

Various business models were considered for the SDC and then a detailed financial analysis of

the SDC based on the most viable business model was carried out. Development of the business

model and financial analysis was carried out in consultation with industry representatives so as to

arrive at the most realistic picture. Details of the financial analysis is given in Chapter-8

The methodology is diagrammatically depicted below:

Figure 2.1 : Methodology Adopted by IL&FS CDI

Techno Commercial Feasibility Report Strategic Distribution Centre

29 IL&FS Cluster Development Initiatives Limited

3. Modern Distribution Infrastructure: Indian Scenario

There has been a significant favourable shift of several demographic and economic factors in

India over the last decade. A strong 9 percent GDP growth, backed by changing consumer

behaviour in favour of increased discretionary spend, has set the stage for a handsome 8.6

percent growth in the retail space over 2007-10. It has, in addition, also called for a demand for

a paradigm shift in the Indian food distribution and logistics which will be quite different from

the current food supply chain in India, which is highly fragmented and characterized by the

presence of multiple intermediaries leading to low value realization and high wastages. The

produce is subjected to multiple handling which leads to quality deterioration and low

acceptance in the consumer market. This is further aggravated by the lack of appropriate

storage, distribution network and logistics.

3.1 Introduction

Current Indian Economy

India is the world 4th largest economy on purchasing power parity basis. India’s GDP for 2006-

07 is estimated to be US$ one trillion. At the moment India is the second fastest growing major

economy in the world, with a GDP growth rate of about 9 percent in 2006–2007.14

The economic development has significantly paced up during the last five years between 2002

and 2007. The rate of growth in per capita income as measured by per capita GDP at market

prices (constant 1999-2000 prices) grew by an annual average rate of 3.1 per cent during 1980-

81 to 1991-92. It accelerated marginally to 3.7 per cent per annum during the next 11 years

from1992-93 to 2002-03. Since then, there has been a sharp acceleration in the growth of per

capita income, almost doubling to an average of 7.2 per cent per annum (2003-04 to 2007-08).

This means that average income has doubled in a decade instead of after a generation. The

growth rate of per capita income in 2007-08 is projected to be 7.2 per cent, the same as the

14 The Economy Assessment and Prospects, RBI, August, 2008

Techno Commercial Feasibility Report Strategic Distribution Centre

30 IL&FS Cluster Development Initiatives Limited

average of the five years to the current year. Per capita private final consumption expenditure

(PFCE) has also increased in line with per capita income. The growth in PFCE has almost

doubled to 5.1 per cent per year during the subsequent five years from 2003-04 to 2007-08, with

the current year’s growth expected to be 5.3 per cent, marginally higher than the five year

average.15

With rising income levels, household consumption has increased manifold, with the emergence

of a redefined middle class. Growth in service sector has been the driving factor behind this. The

country is on the brink of becoming an economic powerhouse and gaining huge attention by

global players as an excellent investment destination.

High economic growth has led to increased disposable income for the Indian middle class, which

currently comprises of 22 percent of population and estimated to reach 32 percent by 2010.

Accordingly, disposable incomes are set to rise at an average of 8.5 percent by 2015.16 Indians

with an ability to spend over US$ 30, 000 per annum on PPP basis accounts for around 3 percent

of the country’s total population and amounts to 20 million people17.

Consumption and Spending Patterns

India possesses the advantage of having a large young population. It is estimated that around 35

percent of India’s population is under 14 years of age and more than 60 percent of the population

is estimated to constitute the working age group.18 Two-third of the population is under 35 years,

with a median age of 24 years, as opposed to USA, China and Japan with median ages of 35, 30

and 41 years respectively. The large population of working age group forms a wide consumer

base.19

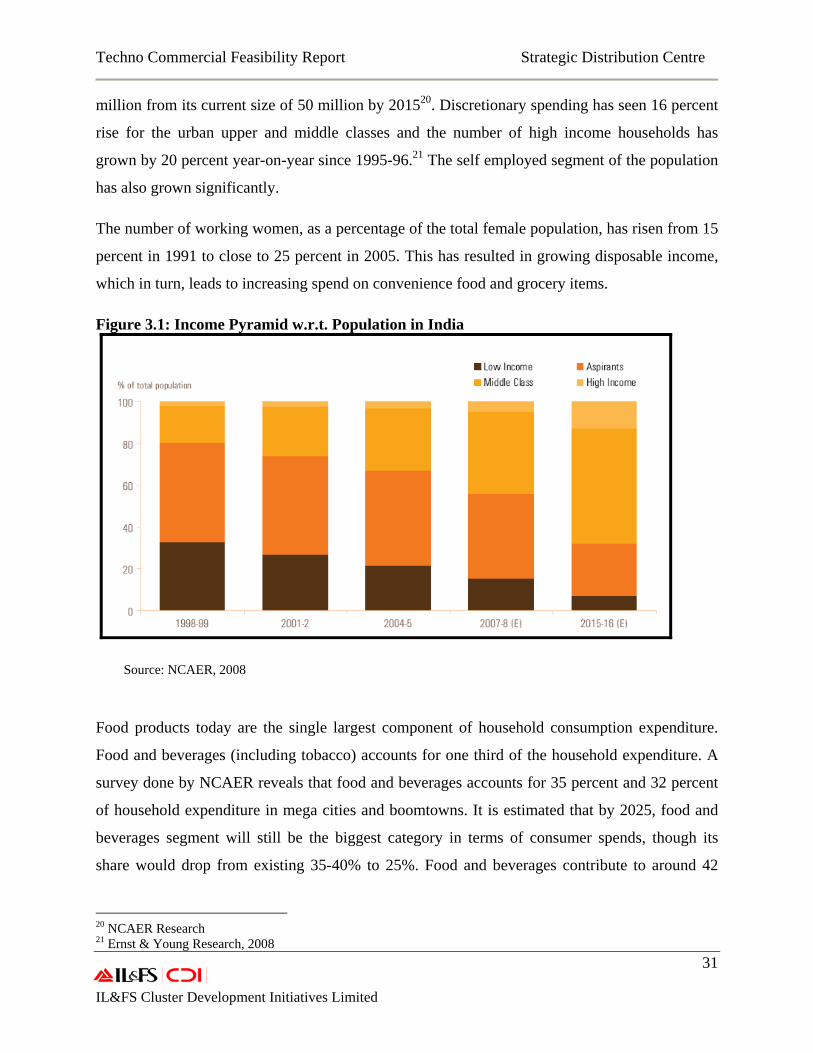

Rapidly changing demographic profiles and increased disposable income are changing the face

of Indian consumers. The swelling middle class is redefining the consuming pattern with a shift

towards branded products. With the country’s income pyramid changing rapidly, a definite shift

is observed from saving to spending attitude. The middle class is estimated to reach a size of 582

15 Economic Survey of India, 2007-08 16 Ernst & Young Research, 2008 17 Mckinsey Research, 2007 18 Retail: Market and Opportunities, A report by Ernst & Young, 2008 19 Retail: Shopping Goes Hyper, Edelweiss, 2008

Techno Commercial Feasibility Report Strategic Distribution Centre

31 IL&FS Cluster Development Initiatives Limited

million from its current size of 50 million by 201520. Discretionary spending has seen 16 percent

rise for the urban upper and middle classes and the number of high income households has

grown by 20 percent year-on-year since 1995-96.21 The self employed segment of the population

has also grown significantly.

The number of working women, as a percentage of the total female population, has risen from 15

percent in 1991 to close to 25 percent in 2005. This has resulted in growing disposable income,

which in turn, leads to increasing spend on convenience food and grocery items.

Figure 3.1: Income Pyramid w.r.t. Population in India

Source: NCAER, 2008

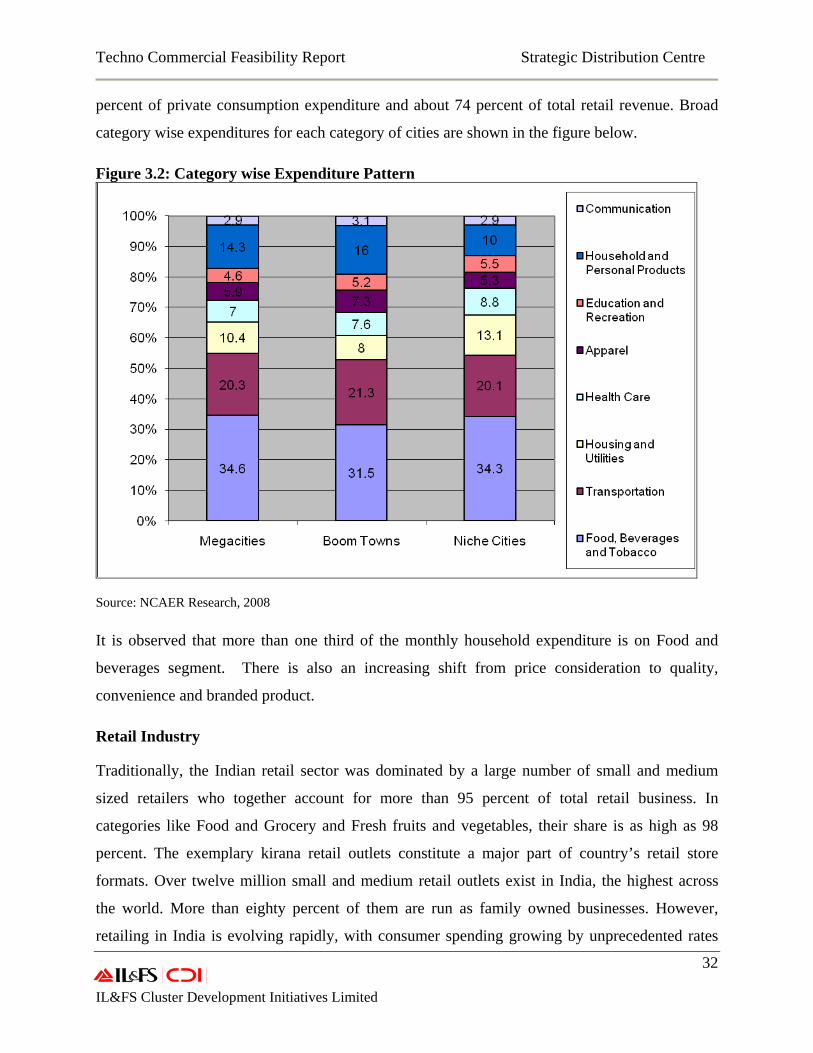

Food products today are the single largest component of household consumption expenditure.

Food and beverages (including tobacco) accounts for one third of the household expenditure. A

survey done by NCAER reveals that food and beverages accounts for 35 percent and 32 percent

of household expenditure in mega cities and boomtowns. It is estimated that by 2025, food and

beverages segment will still be the biggest category in terms of consumer spends, though its

share would drop from existing 35-40% to 25%. Food and beverages contribute to around 42

20 NCAER Research 21 Ernst & Young Research, 2008

Techno Commercial Feasibility Report Strategic Distribution Centre

32 IL&FS Cluster Development Initiatives Limited

percent of private consumption expenditure and about 74 percent of total retail revenue. Broad

category wise expenditures for each category of cities are shown in the figure below.

Figure 3.2: Category wise Expenditure Pattern

Source: NCAER Research, 2008

It is observed that more than one third of the monthly household expenditure is on Food and

beverages segment. There is also an increasing shift from price consideration to quality,

convenience and branded product.

Retail Industry

Traditionally, the Indian retail sector was dominated by a large number of small and medium

sized retailers who together account for more than 95 percent of total retail business. In

categories like Food and Grocery and Fresh fruits and vegetables, their share is as high as 98

percent. The exemplary kirana retail outlets constitute a major part of country’s retail store

formats. Over twelve million small and medium retail outlets exist in India, the highest across

the world. More than eighty percent of them are run as family owned businesses. However,

retailing in India is evolving rapidly, with consumer spending growing by unprecedented rates

Techno Commercial Feasibility Report Strategic Distribution Centre

33 IL&FS Cluster Development Initiatives Limited

and with increasing number of domestic and global companies investing in this sector. These

players have been defined under the organized retail segment within the retail sector. The size of

Indian Retail Industry was estimated at US$ 311.7 billion in 2006, accounting for almost 39

percent of GDP. In 2006, organized retail stood at US$ 12.9 billion, implying a share of 4% of

the total retail revenue.22

Organized retail in India is currently undergoing a metamorphosis and is expected to scale up to

meet global standards in the next five years. The sector is rapidly evolving due to significant

shift in factors ranging from demographics to economics to social. Led by the rising purchasing

power, changing consumption patterns, increased access to information and communication

technology and improving infrastructure, the retail market is all set to observe a sea change at

both back as well as the front end. The most significant period of growth was recorded during

2000 to 2006, when the sector revenues increased by about 93.5 percent translating to CAGR of

13.3 percent. Organized retail revenues are expected to increase from an estimated US$ 12.9

billion in 2005-06 to more than US$ 43.8 billion by 2009-10.23

Though the retail market has been dominated by unorganized players and depicts rural biasness,

the entry of domestic and international organized players is set to change the scenario. The share

of organized retail, currently at only 4 percent, is expected to reach to a market share of 10

percent by 2010. Apart from increasing presence in metro and tier I cities, organized retail is also

looking at tier II cities to scale up their operations. Today, top eight cities (four metros, Pune,

Ahmedabad, Bangalore and Hyderabad) together account for almost 80 percent of the total

organized retail. This is also the reason behind almost all the players strongly focusing on these

cities for scaling up the business. Further to this, the tier II cities are also poised to contribute

significantly to future expansion plans of the organized retail.

Food Retail

Food Retail industry in India is currently estimated at US$ 161.7 billion and it has grown at a

CAGR of 3.96% between 2000 and 2005.24 Within this, organized food retail grew from US$

391 million in 2002 to US$ 1, 624 million in 2007 with a CAGR of about 33 percent. The

22 Retail-Market & Opportunity 2008, A report by Ernst & Young 23 Retail: Shopping Goes Hyper, Edelweiss, 2008 24 Industry Insight-Indian Food Retailing, Cygnus, 2008

Techno Commercial Feasibility Report Strategic Distribution Centre

34 IL&FS Cluster Development Initiatives Limited

organized segment, though small at present, is growing fast. Food production is expected to

double in the next ten years and the consumption of value added food products is expected to

grow at a much faster pace.

Food retail in India is primarily characterized by different type of products retailed rather than

different retail formats in operation. The food and beverages segment alone accounts for the

largest share of revenue of the total retail market, followed by apparels and clothing. This

category has the highest consumer demand across all income levels, consumer groups and

various retail formats. According to Edelweiss and Mckinsey Research, it is estimated that food

market size will reach US$ 334 billion by 2025 with a CAGR of around 4 percent.

Out of the total retail revenue of US$ 311 billion in 2006, food and beverages contribute US$

231 billion, which forms about 74 % of the total revenue. Retail sector revenue is estimated to

reach US$ 460.6 billion by 2010-11 with the organized retail projected revenue of US$ 43.8

billion25. It is envisaged that modern retail will adapt and absorb some of the traditional formats

in subsequent years. Also, with the rural retail constituting the largest share of total retail

revenues, the existing players are now looking at rural market to tap the opportunity. A few

players like ITC Limited, Godrej and DSCL have already started the venture under the brand

name of Choupal Sagaar, Aadhaar and Hariyali Kisaan Bazaar respectively.

3.2 Analysis of Existing Value/Supply Chain

One of the most serious challenges faced by the retail sector (both traditional and organized) is to

overcome the constraints of current supply chain and logistics system. In India, about 60 percent

of food quality is lost in the supply chain from the farm to the final consumer. 35 to 40 percent of

the total production of fresh fruits and vegetables is wasted in India. Consumers actually end up

paying approximately about 35 percent more because of wastage as well as multiple intermediate

handling in the current supply chain.26 The farmer in India gets around 30 percent of what the

consumer pays at the retail store. One of the most critical challenges in the retail sector in India

is poor supply chain and logistics management. The importance can be understood by the fact

that the logistics management cost component in India is as high as 7 -10 percent against the

global average of 4-5 percent of the total retail price. 25 Retail: Market and Opportunities, A report by Ernst & Young, 2008 26 Vision 2015, MoFPI, 2007

Techno Commercial Feasibility Report Strategic Distribution Centre

35 IL&FS Cluster Development Initiatives Limited

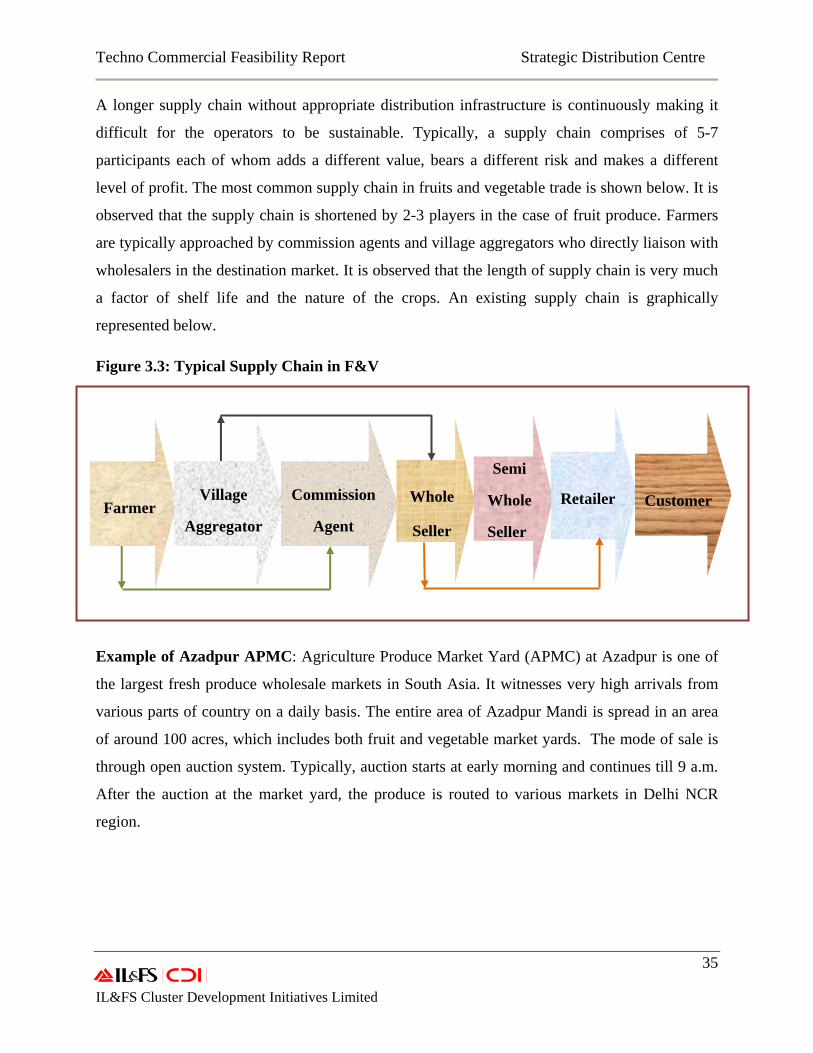

A longer supply chain without appropriate distribution infrastructure is continuously making it

difficult for the operators to be sustainable. Typically, a supply chain comprises of 5-7

participants each of whom adds a different value, bears a different risk and makes a different

level of profit. The most common supply chain in fruits and vegetable trade is shown below. It is

observed that the supply chain is shortened by 2-3 players in the case of fruit produce. Farmers

are typically approached by commission agents and village aggregators who directly liaison with

wholesalers in the destination market. It is observed that the length of supply chain is very much

a factor of shelf life and the nature of the crops. An existing supply chain is graphically

represented below.

Figure 3.3: Typical Supply Chain in F&V

Example of Azadpur APMC: Agriculture Produce Market Yard (APMC) at Azadpur is one of

the largest fresh produce wholesale markets in South Asia. It witnesses very high arrivals from

various parts of country on a daily basis. The entire area of Azadpur Mandi is spread in an area

of around 100 acres, which includes both fruit and vegetable market yards. The mode of sale is

through open auction system. Typically, auction starts at early morning and continues till 9 a.m.

After the auction at the market yard, the produce is routed to various markets in Delhi NCR

region.

Farmer

Village

Aggregator

Commission

Agent

Whole

Seller

Semi

Whole

Seller

Retailer

Customer

Techno Commercial Feasibility Report Strategic Distribution Centre

36 IL&FS Cluster Development Initiatives Limited

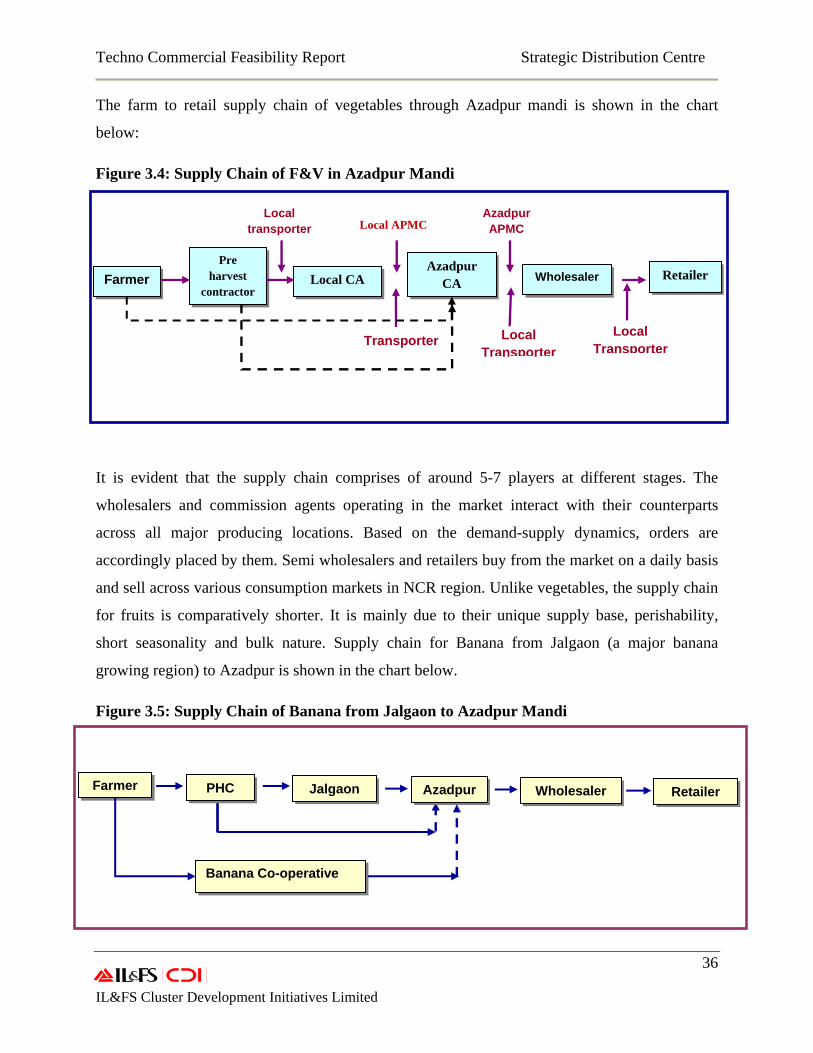

The farm to retail supply chain of vegetables through Azadpur mandi is shown in the chart

below:

Figure 3.4: Supply Chain of F&V in Azadpur Mandi

It is evident that the supply chain comprises of around 5-7 players at different stages. The

wholesalers and commission agents operating in the market interact with their counterparts

across all major producing locations. Based on the demand-supply dynamics, orders are

accordingly placed by them. Semi wholesalers and retailers buy from the market on a daily basis

and sell across various consumption markets in NCR region. Unlike vegetables, the supply chain

for fruits is comparatively shorter. It is mainly due to their unique supply base, perishability,

short seasonality and bulk nature. Supply chain for Banana from Jalgaon (a major banana

growing region) to Azadpur is shown in the chart below.

Figure 3.5: Supply Chain of Banana from Jalgaon to Azadpur Mandi

Farmer PHC Jalgaon Azadpur

Banana Co-operative

Wholesaler Retailer

Farmer Pre

harvest contractor

Local CA Azadpur

CA Wholesaler

Transporter

Retailer

Local transporter Local APMC

Azadpur APMC

Local Transporter

Local Transporter

Techno Commercial Feasibility Report Strategic Distribution Centre

37 IL&FS Cluster Development Initiatives Limited

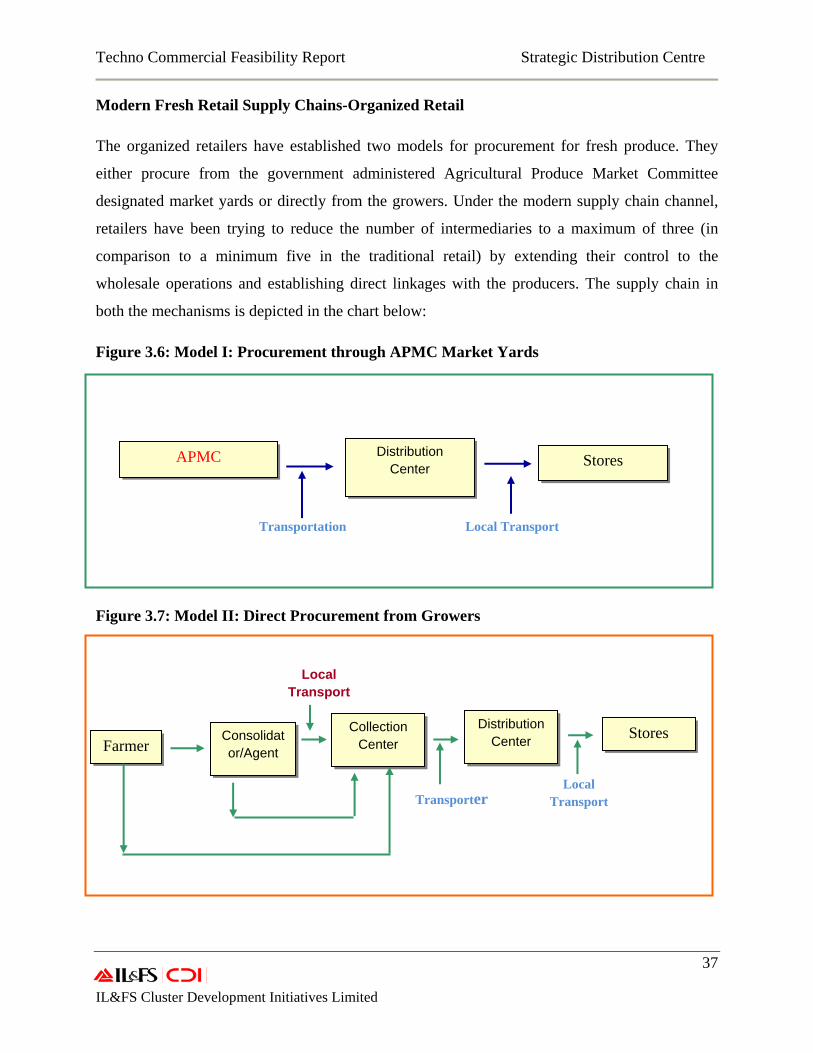

Modern Fresh Retail Supply Chains-Organized Retail

The organized retailers have established two models for procurement for fresh produce. They

either procure from the government administered Agricultural Produce Market Committee

designated market yards or directly from the growers. Under the modern supply chain channel,

retailers have been trying to reduce the number of intermediaries to a maximum of three (in

comparison to a minimum five in the traditional retail) by extending their control to the

wholesale operations and establishing direct linkages with the producers. The supply chain in

both the mechanisms is depicted in the chart below:

Figure 3.6: Model I: Procurement through APMC Market Yards

Figure 3.7: Model II: Direct Procurement from Growers

APMC Distribution Center Stores

Transportation Local Transport

Farmer Consolidator/Agent

Local Transport

Collection Center

Distribution Center Stores

Local Transport Transporter

Techno Commercial Feasibility Report Strategic Distribution Centre

38 IL&FS Cluster Development Initiatives Limited

In case of direct procurement from growers, the organized retailers have set up farm proximate

collection centers where the produce is aggregated and then, directly transported to respective

distribution centers. The produce is sorted, graded, and packed at the distribution centers and

then transported to retail stores. Distribution centers also have the facilities like cold storage,

ripening chamber and deep freeze storage.

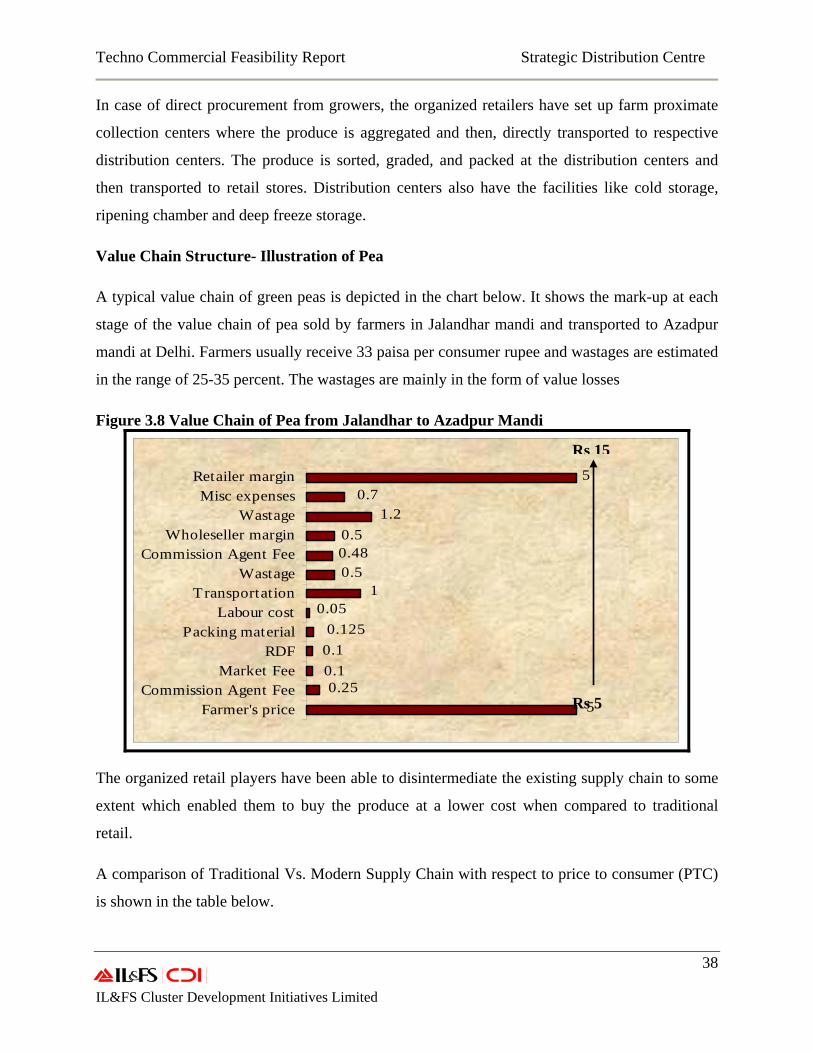

Value Chain Structure- Illustration of Pea

A typical value chain of green peas is depicted in the chart below. It shows the mark-up at each

stage of the value chain of pea sold by farmers in Jalandhar mandi and transported to Azadpur

mandi at Delhi. Farmers usually receive 33 paisa per consumer rupee and wastages are estimated

in the range of 25-35 percent. The wastages are mainly in the form of value losses

Figure 3.8 Value Chain of Pea from Jalandhar to Azadpur Mandi

5

5

0.71.2

0.50.480.5

10.05

0.1250.10.10.25

Farmer's priceCommission Agent Fee

Market FeeRDF

Packing materialLabour cost

TransportationWastage

Commission Agent FeeWholeseller margin

WastageMisc expenses

Retailer margin

The organized retail players have been able to disintermediate the existing supply chain to some

extent which enabled them to buy the produce at a lower cost when compared to traditional

retail.

A comparison of Traditional Vs. Modern Supply Chain with respect to price to consumer (PTC)

is shown in the table below.

Rs 15

Rs 5

Techno Commercial Feasibility Report Strategic Distribution Centre

39 IL&FS Cluster Development Initiatives Limited

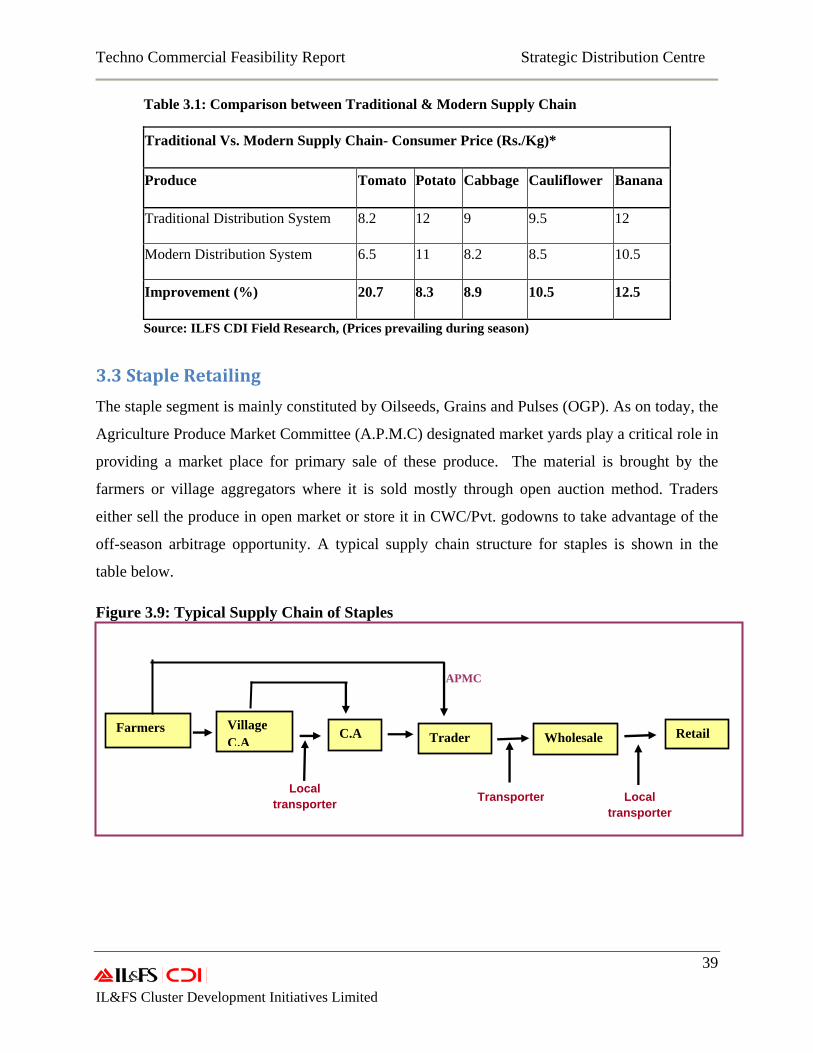

Table 3.1: Comparison between Traditional & Modern Supply Chain

Source: ILFS CDI Field Research, (Prices prevailing during season)

3.3 Staple Retailing

The staple segment is mainly constituted by Oilseeds, Grains and Pulses (OGP). As on today, the

Agriculture Produce Market Committee (A.P.M.C) designated market yards play a critical role in

providing a market place for primary sale of these produce. The material is brought by the

farmers or village aggregators where it is sold mostly through open auction method. Traders

either sell the produce in open market or store it in CWC/Pvt. godowns to take advantage of the

off-season arbitrage opportunity. A typical supply chain structure for staples is shown in the

table below.

Figure 3.9: Typical Supply Chain of Staples

Traditional Vs. Modern Supply Chain- Consumer Price (Rs./Kg)*

Produce Tomato Potato Cabbage Cauliflower Banana

Traditional Distribution System 8.2 12 9 9.5 12

Modern Distribution System 6.5 11 8.2 8.5 10.5

Improvement (%) 20.7 8.3 8.9 10.5 12.5

TransporterLocal

transporter

Farmers Village C.A

C.A Trader Wholesale Retail

APMC

Local transporter

Techno Commercial Feasibility Report Strategic Distribution Centre

40 IL&FS Cluster Development Initiatives Limited

A typical value chain (during the season) for Tuar (a.k.a Pigeon Pea) is shown in the table below.

Table 3.2 Value Chain of Pigeon Pea

Source: ILFS CDI Research- Based on prevailing prices during 2006-07

There are at least 4-6 intermediaries involved and the produce is subjected to multiple handling

at various stages in the supply chain. The trader in the market yard typically operates with a

margin of 4-6 percent. It is estimated that staples suffer wastages of 15-20 percent in the value

chain, most of which is due to poor warehousing and storage and inadequate distribution of the

material. Organized retail buys in bulk from the traders and aggregates the stock at their

distribution centers, where the bulk stock is repacked in various SKUs and further shipped to the

retail stores.

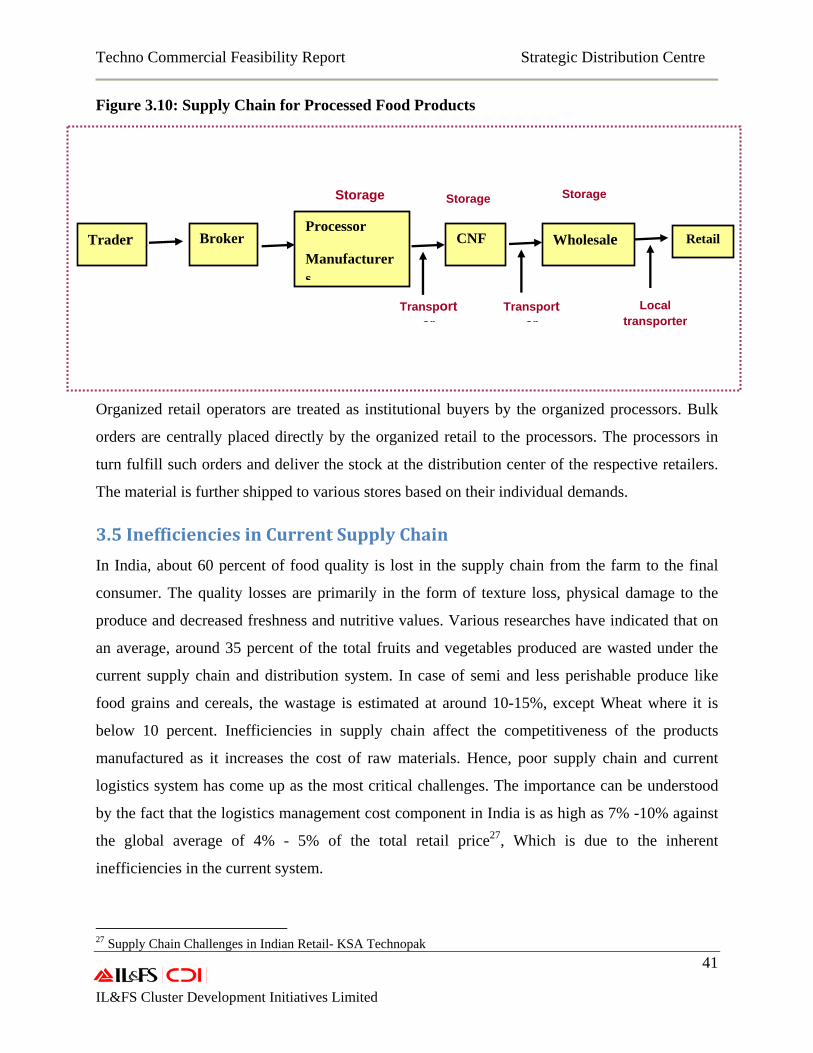

3.4 Processed Food Retailing

The processors mostly source their raw material from the suppliers, who are none other than the

traders. The interaction between the supplier and the processors also happens through a broker

who charges a fixed brokerage for his services. The finished products are sold through the typical

CNF-Wholesale-Retail channel or the institutional sales channel. The supply chain structure for

processed food products is shown in the picture below.

Player Expenses (Rs./Kg) Mark Up/Qt.

Farmer Price 25 Rs.2500/Qt.

Rs.2988/Qt