Embed Size (px)

Citation preview

XBRL J

www.pwc.com

XBRL Japan

Standardize to Enhance: Process & Standardize to Enhance: Process & Controls, Analytical Insights, Economics

October 1, 2013

Discussion Topicsp

Trends

- Around the World

- Implications

- Analytical Insights

- Lessons Learned

Standardize to Empower Reporting Professionals: - Enhancing Reporting Process & Controls Agility, Effectiveness, Economics

Next Steps

PwC 2

TrendsTrends

PwC 3

Examples of More Granular Transparency / Insightsp f p y / g

“A comparison of Income, Revenue, and Taxes of p , ,various companies”

“Visual template representation - a comparison of unremitted taxes based on earnings made overseas”

“XBRL Data in Use - Accumulated values of key items”

PwC 4

Open Analytics at ACRA in Singaporep y g pEnhancing Analysis of Business Reports

PwC 5

Adoption is accelerating around the Worldp g

PwC 6

XBRL Around the World: Latin America

Panama – Banking Supervision

Brazil National Treasury: PublicPeru – Banking

Columbia (in development)

Brazil National Treasury: Public Sector Accounting and Fiscal Information System - 2014

gSupervision and Securities Regulation

Chile – Corporate Reporting and Uruguay – Central BankInsurance Regulation

Uruguay Central Bank(in development

Argentina – Central Bank

PwC 7

(in development)

XBRL Around the World: Europe

Finland – SBR (2014)Norway – Oslo Stock Exchange

p

Sweden

Belgium

D k

Lithuania

UK HMRC

Ireland Customs

Netherlands - SBR

Germany

Denmark

House

France – Central Bank Ukraine – Corporate

(

Poland – National Bank

Reporting (in development)

Spain

Switzerland

PwC 8

Turkey – SBR (2014)ItalyLuxembourg

Spain

XBRL Around the World: EU

Solvency IISolvency II

Basel II

Business Registers

CRD IV

PwC 9

XBRL Around the World: Asia and Oceana

China

Japan

Singapore

ThailandUAE

Korea

Singapore

Australia

India Indonesia Malaysia

Saudi Arabia

PwC 10

India Indonesia

Trends

‘Big Data’Migration from unstructured to structured information accelerating; driven largely Migration from unstructured to structured information accelerating; driven largely by economics and transparency demandExpansion of existing programs (e.g. Australia, Japan, Singapore, etc.)New regulatory territory adoption (e.g. Brazil, Malaysia, Russia, Saudi Arabia, etc.)New egu ato y te to y adopt o (e.g. a , a ays a, uss a, Saud ab a, etc.)New disclosure areas (e.g. Solvency II, CDR, WICI, CSR/GRI, Corp Actions, etc.)Assurance mandates on XBRL reports increasing (e.g. Netherlands, India, etc.)Alignment with other relevant standards (e g LEI RIXML ISO etc )Alignment with other relevant standards (e.g. LEI, RIXML, ISO, etc.)Internal applications at GL and sub-ledgers (e.g. Data Act, Brazil, companies, etc.)Emergence of new enabling software

P d i / Di l M / M iProduction / Disclosure Management / MappingConsumption / analytical applications

Standardized analytics enable collaboration among analysts / persistent analysis

PwC 11

And then there is the next thing.

Corp Actions – closing gap between Issuer & Investorp g g p

INVESTOR

LAWYERS, ADVISORS, LEAD MANAGERS, REGISTRARS, TRANSFER/FILING/INFORMATION/PUBLICATION AGENTS

REGULATORS, SHARE REGISTER, ANALYTICS COMPANY

ISSUERINVESTOR

FUND MANAGERS, FUND ADVISORS, INVESTMENT

EXCHANGE, WIRE SERVICES,

REFERENCE & TRADING DATA SERVICES

PwC 12

CENTRAL DEPOSITORY, CUSTODIANS, SUB‐CUSTODIANS, GLOBAL

CUSTODIANS, BROKER‐DEALERS

MANAGER INSTITUTION,

OFFSHORE INVESTORS

Standardization enhances Analytics (Social Analytics)y ( y )

Standardized Data, Formulas/Models, Relationships, Presentations

Deeper levels of analysis and insights as more data is immediately ‘reusable’

Enables collaboration by analysts on models (‘YouTube’ for modeling)

Shift in Time / Resources applied to:Accessing dataAccessing dataInputting data into analytical Inputting data into analytical applicationsapplicationsp g yp g y ppppCorrecting validation and input errorsCorrecting validation and input errorsPerforming analyticsPerforming analyticsAnalyzing analytical resultsAsking followAsking follow up questionsup questions

Migration from manual data lifting to intellectual efforts

Asking followAsking follow--up questionsup questionsAnalyzing answers to questionsMaking decisions

PwC 13

US SEC’s Analytics have been Standardized & Improvedy p

Here are examples of how the SEC has used standardized data and standardized analytics to enhance their risk assessment capabilities.

PwC 14

Explicit Demand from Investorsp f

SIFMA Members

CFA Institute “The Irreversible Trend toward Greater Connectivity and Data in Financial Reporting”Recommendation: “The SEC should move forward with its 21st Century Disclosure

PwC 15

forward with its 21st Century Disclosure Project”

Examples of Poor Report Qualityp f p Q y

Examples of Report Quality Issues in Company Reports (2012 10ks):

Type XBRL Report CorrectFact Problem UFE $4 3B UFE $17 2B

"Quality means doing it right when no one is looking." – Henry Ford.

Fact Problem UFE $4.3B UFE $17.2BFact Problem Settlements -77910000 (dr) Settlements 77910000 (dr)Fact Problem Public Float $6.3 Quintillion

(17 zeros)Public Float $6.3B

(17 zeros)Fact Problem Accumulated

Amortization - $28.5B (cr)Accumulated Amortization $28.5B (cr)

Extension xxx Cash and Cash US GAAP Term: Cash andExtension Problem

xxx.Cash and Cash Equivalents

US GAAP Term: Cash and Cash Equivalents

Report Problem Net Cash Provided by Ops of $1 3B

Net Cash Provided by Opsof $1 0B

PwC 16

$1.3B of $1.0B

Learning’sg

Few like change / uncertaintyPerceptions drive reality – “No one is going to buy anything over the Internet”Perceptions drive reality No one is going to buy anything over the InternetRegulatory Mandate (Bad) …………… OR ……………. Supply Chain Standard (Good)Implementation approach dictates initial cost/benefit – perception

Bolt on adds cost/time OR Build in reduces cost/timeBolt-on adds cost/time………….OR ……………Build-in reduces cost/timeReview procedures need to address structures (not just presentation)

Process changes (and related benefits) follow the “Bell Curve”I d d fInvestor demand for

Structured disclosures is strongReport quality is high; however, actual report quality is poor

Enabling software Critical to benefit realization; most still early stage but maturingDevelopment based upon customer demand/request

PwC 17

There are many more supply chain applications (e.g. Corporate Actions, WICI, etc.) that are now emerging

Empowering Reporting ProfessionalsEmpowering Reporting Professionals

PwC 18

Perspective Question: What software application is p Q f ppmost commonly used by companies for reporting?

1 SAP1. SAP2. Oracle3. Hyperion4. Fujitsu5. BAAN6. IBM Cognos6. IBM Cognos7. JD Edwards8. Microsoft Dynamics

Offi9. Office

PwC 19

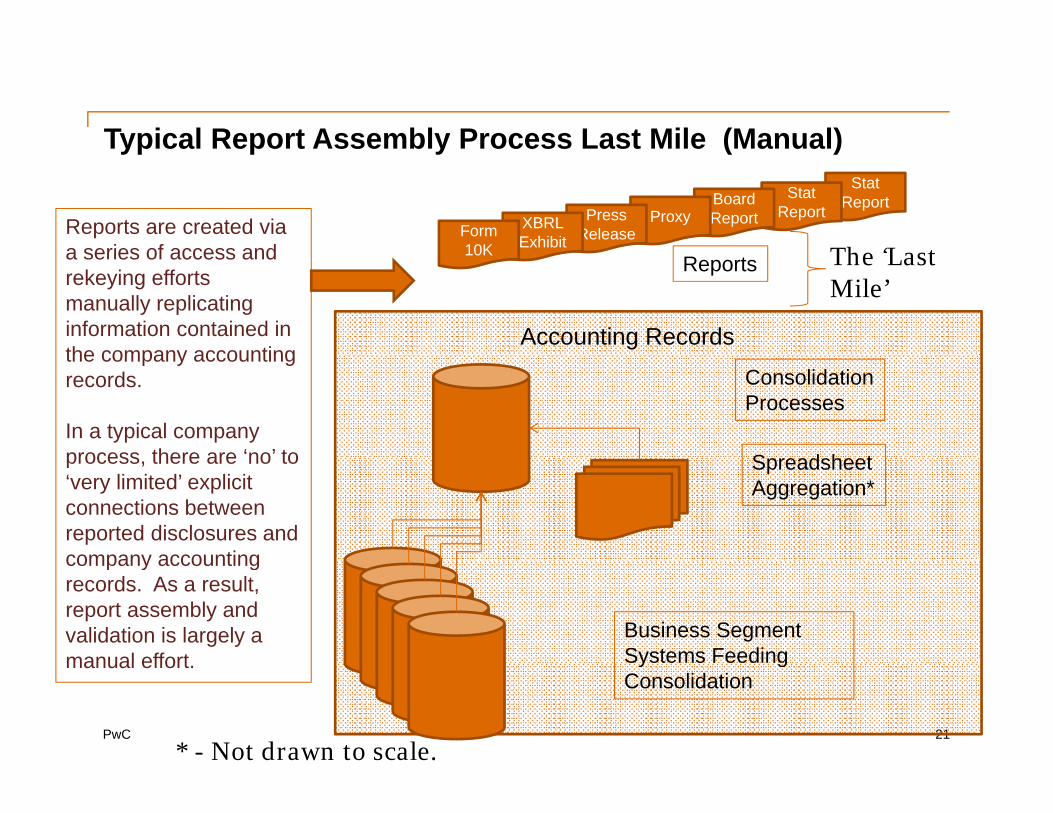

Common Report Assembly Manual Processesp y

While companies have significant investments in ERP and consolidation application, the ‘last mile’ of report assembly and review pp , p yprocesses and controls are highly manual. ‘Last Mile’ process steps that are commonly manual include:• Spreadsheet Aggregation p gg g• Report Assembly from disparate sources• Report Validation

N ti T t G ti• Narrative Text Generation• Review Processes via emailing of Office docs• Benchmarking / Peer & Best Practice Assessments• References from disclosures to relevant standards, regulations, key

accounting policies & memos• Tagging of completed reports with XBRL taxonomy elements

PwC 20

Tagging of completed reports with XBRL taxonomy elements

Typical Report Assembly Process Last Mile (Manual)Stat

ReportStat Report

Reports are created via a series of access and

Board ReportProxyPress

ReleaseXBRL Exhibit

Form 10K

yp p y ( )

The ‘Last Reports

Accounting Records

a series of access and rekeying efforts manually replicating information contained in the company accounting

10K The Last Mile’

ConsolidationProcesses

S d h t

the company accounting records.

In a typical company process there are ‘no’ to Spreadsheet

Aggregation*process, there are no to ‘very limited’ explicit connections between reported disclosures and company accounting

Business Segment Systems Feeding

company accounting records. As a result, report assembly and validation is largely a manual effort

PwC 21

y gConsolidation

manual effort.

* - Not drawn to scale.

Typical Report Assembly Process Last Mile (Manual)Stat

ReportStat Report

Reports are created via a series of access and

Board ReportProxyPress

ReleaseXBRL Exhibit

Form 10K

yp p y ( )

Reports

Accounting Records

a series of access and rekeying efforts manually replicating information contained in the company accounting

10K

ConsolidationProcesses

S d h t

the company accounting records.

In a typical company process there are ‘no’ to Spreadsheet

Aggregation*process, there are no to ‘very limited’ explicit connections between reported disclosures and company accounting

Business Segment Systems Feeding

company accounting records. As a result, report assembly and validation is largely a manual effort

PwC 22

y gConsolidation

manual effort.

* - Not drawn to scale.

スライド 22

RMW2 this is the same as the prior slide; just with the excel worksheets expanded for effect.R M Willis, 2013/09/27

Outsourcing may be common: But control is importantg y p

$19B$19B

"Earlier this morning RR Donnelley, the financial printer, informed us that they h d f l d d f h h hhad filed our draft 8K earnings statement without authorization. We have ceased trading on NASDAQ while we work to finalize the document. Once it's finalized we will release our earnings, resume trading on NASDAQ and hold our earnings call as normal at 1:30 PM PT," the company said.

PwC 23

earnings call as normal at 1:30 PM PT, the company said.

Many CFO’s Moving to Build – in XBRLy g

60 00%

70.00%

Bowne / RR DONNELLEYAnd the market share decline over the past 2 years for the major

40.00%

50.00%

60.00% years for the major outsourcing vendor reflects this transition.

20.00%

30.00% RR DONNELLEY

0.00%

10.00%

q1 q2 q3 q4 q1 q2 q3 q4

PwC 24

2011 2011 2011 2011 2012 2012 2012 2012

Transition to ‘built-in’ approach ppLowers Cost/time while enhancing control

There is a history lesson here for financial executives with respect to supply chain standardization: Almost 40 years ago, grocery store managers initially had inventory clerks apply the UPC/bar code to products when they stocked the shelves (at the very end of the supply h i ) Thi l ‘b l ’ d f h l h i h chain). This manual ‘bolt-on’ end of the supply chain approach gave

way to the automated application of the UPC/bar code at the very beginning of the supply chain; thereby enabling automation of inventory management sales processes and consumer buying pattern inventory management, sales processes, and consumer buying pattern insights and a $17B annual cost reductions. Financial Executives may follow a similar path via the adoption of XBRL initially bolting on to existing manual processes and XBRL initially bolting-on to existing manual processes and subsequently targeting the broad range of highly manual report assembly and review processes and controls outlined on the earlier slide

PwC 25

slide.

Disclosure Management – Streamlining the Last Mile

Stat ReportStat

ReportMapping relationships between company report writer systems

New Relationships

Board ReportProxyPress

ReleaseXBRL Form

g g

p y p yand the company report are explicit and access, reuse and some validation processes are automated within the built-in

Accounting Records

ReleaseExhibitForm 10K Reports

application. These explicit relationships now can exist between source system accounting records and

Disclosure Management Apps

ConsolidationProcesses

Spreadsheet

gcompany reports.

Disclosure Management process controls are critical and Spreadsheet

Aggregation

Business Segment

process controls are critical and may include: application access controls; control over mappings (both incoming and outgoing); log of changes; report

PwC 26

Business Segment Systems Feeding Consolidation

log of changes; report versioning controls and audit trail; and others.

Disclosure Management Process Enhancementsg

‘Last Mile’ process steps that are automated and streamlined via effective Disclosure Management application implementation include:

• Spreadsheet Assembly is automated ‘pulling’ data from disparate source systems

• Report Assembly (& updating) is automated pulling data from disparate tsystems

• Report Validation is built into the DM application• Some Narrative Text Generation is automated

25% to 50% cost and time enhancements

• Review Processes are collaborative and provide a ‘topical’ view• Benchmarking / Peer & Best Practice Assessments are automatically loaded in

context of the company disclosures (e.g. Income taxes)• References explicitly link from reporting concepts to standards, regulations,

key accounting memos, and company policies• Virtual Reporting Service Center useful across all reporting types

PwC 27

• XBRL Reports are a by-product of report assembly and review

Disclosure Management Articlesg

“Disclosure Management: Streamlining the Last Mile” -Outlines general process enhancements enabledg p

“How to Differentiate Disclosure Management Features”

“Grocery Store Managers & Financial Executives: Bolt-on or Built-in to Realize Process Benefits?”

PwC 28

Next StepsNext Steps

PwC 29

Next Steps for Producersp f

Enhance review of report structures to ensure report quality

Use Disclosure Management to Standardize Reporting Processes & Controls- Apply the standardized reporting processes & controls across all content silos

(e.g. Company reports, Corp Actions, IR, Internal, etc.)(e.g. Co pa y epo ts, Co p ct o s, , te a , etc.)- Migrate reporting content silos towards a Virtual Service Center- Use Disclosure Management to enable process effectiveness and

Prioritize internal ERP instances for Standardization to enhance internal transparency

‘Robocop’ for your internal GRC IA BI WICI etcRobocop for your internal GRC, IA, BI, WICI, etc.

PwC 30

Next Steps for Consumersp f

Communicate demand for high quality structured disclosures

Use freely available granular disclosures to enhance:- Timeliness / persistence of analysis

Insights from more granular analysis- Insights from more granular analysis- Number of companies analyzed- Cost of analysis

Standardize formulas / models to enhance: - Institutional management of analytical intellectual property- Institutional transparency of how, where and when analytics are applied

PwC 31

Thank youThank you

This publication has been prepared for general guidance on matters of interest only, and does i f i l d i Y h ld h i f i i d i hi not constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PwC, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information

t i d i thi bli ti f d i i b d it contained in this publication or for any decision based on it.

© 2013. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers LLP which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.