Embed Size (px)

Citation preview

Workers Comp. Reserving - How and When Should

You Slice the Cake?

Mark J. Mahon, FCAS, MAAA

MBA, Inc.

CLRS - September 23, 2002

It’s Easy to Want the Data - Receiving It Is Not So Easy

To Start - Keep Things Simple

It’s Easy to Want the Data - Receiving It Is Not So Easy

To Start - Keep Things SimpleFollow the Client’s Operations

It’s Easy to Want the Data - Receiving It Is Not So Easy

To Start - Keep Things SimpleFollow the Client’s OperationsWhy Do You Want the Data?

It’s Easy to Want the Data - Receiving It Is Not So Easy

To Start - Keep Things SimpleFollow the Client’s OperationsWhy Do You Want the Data?Time Consuming and Expensive

Traumatic vs. Occupational Disease (Black Lung)

Coal Mine Compensation Rating Bureau of Pennsylvania.

Traumatic vs. Occupational Disease (Black Lung)

Comparison of OD to Traumatic Cumulative

Traumatic vs. Occupational Disease (Black Lung)

Comparison of OD to Traumatic Cumulative Long Report Time

Traumatic vs. Occupational Disease (Black Lung)

Comparison of OD to Traumatic Cumulative Long Report Time Claims take time to Adjudicate

Traumatic vs. Occupational Disease (Black Lung)

Comparison of OD to Traumatic Cumulative Long Report Time Claims take time to Adjudicate Lifetime Benefits

Traumatic vs. Occupational Disease (Black Lung)

Comparison of OD to Traumatic Cumulative Long Report Time Claims take time to Adjudicate Lifetime Benefits Low Frequency/High Severity

The OD System

Frequency times Severity.

The OD Frequency

IBNR Claims Uses Typical Accident Year Triangles Claims assigned to Year based on Last

Date of Exposure Claim Count Development used to

estimate IBNR Claims

OD Frequency

Three Pieces Known Claimants Receiving Benefits at

the valuation date (Awarded Claims) An Estimate of Pending Claims that will

be Awarded An Estimate of IBNR Claims that will be

Awarded

The OD Frequency

Awarded ClaimsREPORTED DATA TOTAL

TOTAL AWARDED AWARDED AWARDEDYEAR REPORTED AWARDED PENDING DENIED PENDING IBNR IBNR CLAIMS

1992 20 5 4 11 0.428 2.532 0.271 5.6991993 28 1 2 25 0.214 2.819 0.302 1.5161994 27 2 3 22 0.321 2.688 0.288 2.6091995 20 2 1 17 0.107 2.990 0.320 2.4271996 8 0 1 7 0.107 3.253 0.348 0.4551997 8 0 2 6 0.214 3.788 0.405 0.6191998 10 2 2 6 0.214 4.031 0.431 2.6451999 5 0 0 5 0.000 5.067 0.542 0.5422000 2 0 1 1 0.107 5.745 0.615 0.7222001 0 0 0 0 0.000 7.573 0.810 0.810

TOTAL 128 12 16 100 1.712 40.485 4.332 18.044

Award Ratio: Awarded/(Awarded plus Debied) = 12/(12+100) = 10.7%

The OD Frequency

New Federal Black Lung Legislation Increase in Reported Claims Increase in Awarded Claims

Retroactive

OD Severity

Life TablesLifetime BenefitsClaimant’s AgeAnnual BenefitsMarital StatusEscalation (State - No, Federal- Yes)

OD Severity

Life Tables used to Model Future Benefits

Mortality Probability Future FutureMiner's Table of Benefit Expected

Age Lives Payment Amount COLA Payment60 46,524 0.9884 $5,935 1.000 $5,86661 45,449 0.9651 5,935 1.030 5,90062 44,355 0.9414 5,935 1.061 5,92763 43,238 0.9171 5,935 1.093 5,94864 42,096 0.8923 5,935 1.126 5,960: : : : : :

105 39 0.0007 5,935 3.782 15106 25 0.0004 5,935 3.895 10107 16 0.0003 5,935 4.012 7108 10 0.0002 5,935 4.132 4109 6 0.0001 5,935 4.256 2110 0 0.0000 5,935 4.384 0

Total 149,977

OD Severity

Act 57 Only Claims Filed After Mid 1996 WC Benefits Reduced for Social Security WC Benefits Reduced for Pensions AMA Guidelines Made it Harder To

Achieve PT Disability Status

The OD Reserve

Three Pieces>Known Awarded Claims: Sum of Each Claimant’s future payments

from severity model>Pending Claims: Pending Claims x Award Ratio x Average

Severity of Pending Claims>IBNR Claims: IBNR Claims x Award Ratio x Average

Severity of Awarded and Pending Claims

OD System - Concluding Remarks

Lifetime Payments/Long Tail

OD System - Concluding Remarks

Lifetime Payments/Long TailRelatively Few Claims

OD System - Concluding Remarks

Lifetime Payments/Long TailRelatively Few ClaimsParallels Actual Process

OD System - Concluding Remarks

Lifetime Payments/Long TailRelatively Few ClaimsParallels Actual ProcessReviewed by Interested Parties

OD System - Concluding Remarks

Lifetime Payments/Long TailRelatively Few ClaimsParallels Actual ProcessReviewed by Interested PartiesExpensive

OD System - Concluding Remarks

Lifetime Payments/Long TailRelatively Few ClaimsParallels Actual ProcessReviewed by Interested PartiesExpensiveIs This Really the Only Way to Make

Estimates?

Traumatic - Indemnity vs. Medical

Very Common SplitAlso Breakdown Medical into Medical

Only and Medical on IndemnityDifferent

Development Inflation Law Changes

Tail Factor -Inverse Power Curve

Form: ldf = 1 + a*(time+c)^(b)Transformation: ln(Ldf-1) = ln(a) + b*ln(time+c) Fitted Fitted

Period Ldf time c ln(Ldf-1) ln(time+c) Data points: 12:24 to 60-72 ln(Ldf-1) Ldf12:24 1.902 1 3 -0.103 1.386 Regression Statistics -0.248 1.78124:36 1.290 2 3 -1.238 1.609 R-Square 96.4% -0.955 1.38536:48 1.233 3 3 -1.457 1.792 Observations 5 -1.533 1.21648:60 1.144 4 3 -1.938 1.946 a 4.147 -2.021 1.13360:72 1.085 5 3 -2.465 2.079 b -3.170 -2.445 1.087

72:84 6 3 2.197 -2.818 1.06084:96 7 3 2.303 -3.152 1.043

96:108 8 3 2.398 -3.454 1.032108:120 9 3 2.485 -3.730 1.024120:132 10 3 2.565 -3.983 1.019

: : : : : :240:252 20 3 3.135 -5.792 1.003

Possible Tail Factors: 6-10 1.1896-15 1.2516-20 1.277

Tail Factor -Relate to Larger Body

A. Relationship of Company Z to IndustryLoss Development Factors Relationship

Company Z Insurance Industry Company Z Period Factor Period Factor to Industry12-24 1.902 12-24 1.351 140.8%24-36 1.290 24-36 1.091 118.2%36-48 1.233 36-48 1.040 118.6%48-60 1.144 48-60 1.024 111.7%60-72 1.085 60-72 1.017 106.7%

72-Ult 72-Ult 1.076

Average of Latest 3: 112.3%Trended: 104.5%

B. Possible Tail Factors Company Z Industry Tail Relationship Tail

Average -1 1.076 112.3% 1.210Average -2 1.076 104.5% 1.120

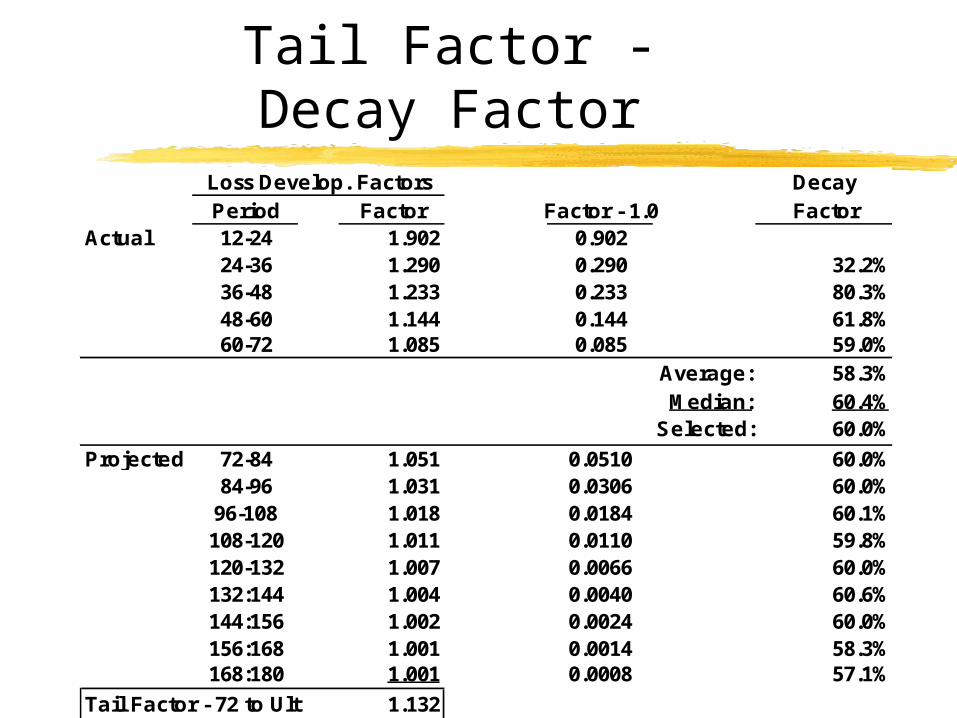

Tail Factor -Decay Factor

Loss Develop. Factors DecayPeriod Factor Factor - 1.0 Factor

Actual 12-24 1.902 0.90224-36 1.290 0.290 32.2%36-48 1.233 0.233 80.3%48-60 1.144 0.144 61.8%60-72 1.085 0.085 59.0%

Average: 58.3%Median: 60.4%

Selected: 60.0%

Projected 72-84 1.051 0.0510 60.0%84-96 1.031 0.0306 60.0%

96-108 1.018 0.0184 60.1%108-120 1.011 0.0110 59.8%120-132 1.007 0.0066 60.0%132:144 1.004 0.0040 60.6%144:156 1.002 0.0024 60.0%156:168 1.001 0.0014 58.3%168:180 1.001 0.0008 57.1%

Tail Factor - 72 to Ult 1.132

Traumatic Losses By Injury Type

Death, Permanent Total, Permanent Partial and Temporary Claims

Traumatic Losses By Injury Type

Death, Permanent Total, Permanent Partial and Temporary Claims

Proportion of Losses by Injury Type Act 57 Impacts Largest Claims Severity Subsequent to Law Change

should be Smaller

Traumatic Losses By Injury Type

Permanent Total Claim Count Development

Accident YearReport 1989 1990 1991 1992 1993 1994 1995 1996 1997 199812 mos. 1 2 2 3 1 3 2 4 2 224 mos. 4 5 4 5 3 6 5 5 636 mos. 8 9 12 7 8 7 9 1048 mos. 13 14 13 9 10 12 1360 mos. 15 16 18 10 12 1272 mos. 15 17 19 10 1386 mos. 16 16 19 1096 mos. 16 17 19108 mos. 16 17120 mos. 16

Traumatic Losses By Injury Type

PT Count Development after Act 57Accident Year

Report 1989 1990 1991 1992 1993 1994 1995 1996 1997 199812 mos. 1 2 2 3 1 3 2 0 0 024 mos. 4 5 4 5 3 6 1 0 136 mos. 8 9 12 7 8 7 1 048 mos. 13 14 13 9 8 7 260 mos. 15 16 18 10 8 672 mos. 15 17 17 9 686 mos. 16 16 15 896 mos. 14 12 14108 mos. 12 10120 mos. 11

Traumatic Losses By Injury Type

Act 57 Also made it Easier to Settle Claims Fewer Claims Being Reported as PT Retroactive - Existing PT’s Settled and

Reclassified

Traumatic Losses By Injury Type

Reserve Estimation – Be Careful Incurred Loss Triangles Double Count

Impact of Settlements Understating Reserve Need

Paid Triangles Overstate Reserve Need

Traumatic Losses By Injury Type

Safety Program Impact Drop in Number of Injuries Shift to less Severe Accidents

Losses in Higher Layers

Be Careful - Reserves in Higher Layers may be Inadequate

Loss Development Under Estimates Higher Layers in Most Recent AY Immature years don’t yet have any big losses Change in claims handling Historically there are no Higher Layer Losses

in layer but because of new severe classes or inflation new losses are expected

Losses in Higher Layers

Latest Years’ Lower than HistoricalPolicy Period

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Losses Limited to $250,000Ultimate 9,735 14,422 12,928 11,955 14,434 11,442 6,006 11,462 7,185 8,152

Gross LossesUltimate 10,995 15,410 14,141 12,907 15,822 11,862 6,697 12,231 7,615 8,542

Ratio of Gross to $250k12.9% 6.9% 9.4% 8.0% 9.6% 3.7% 11.5% 6.7% 6.0% 4.8%

Five Year Dollar Weighted Average: 9.1% 9.1% 9.1% 9.1% 9.1%Selected Ratio: 6.4% 11.5% 9.1% 9.1% 9.1%

Restated Gross Ultimate Losses: 12,175 6,697 12,510 7,842 8,897 Losses Limited to $250k times [Selected Ratio plus 1.0]

Losses in Higher Layers

Immature Years have No LossesPolicy Period

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Case Incurred Losses XS $250,0001,100 840 1,000 730 700 240 350 320 0 0

Excess Loss Development Factor1.145 1.176 1.213 1.304 1.411 1.750 1.974 2.403 2.900 4.500

Ultimate Losses XS $250,0001,260 988 1,213 952 988 420 691 769 0 0

Restated Ultimate Lossses (Five Year Average): 800 800

Losses in Higher Layers

Use Industry Statistics to Fill-in Excess Losses Payroll x Loss Cost x Excess Loss Factor As AY matures rely on actual data more

and moreFor Insurers Do Gross, Ceded and

Net Separately

Losses By Business Segment

Many Self-Insureds have Different Operating Units E.g., Construction vs. Shipbuilding Financial Data Already Split Usually Easy to get Actuarial Data as

Coding already there

Losses By Business Segment

Many Self-Insureds have Different Operating Units E.g., Construction vs. Shipbuilding Financial Data Already Split Usually Easy to get Actuarial Data as

Coding already thereData by Jurisdiction

USL&H Benefits Higher than State Benefits

Combining DataIncreases Credibility for Companies with

Sparse Data

Combining DataIncreases Credibility for Companies with

Sparse DataProvides a Guide to Overall Level

Combining DataIncreases Credibility for Companies with

Sparse DataProvides a Guide to Overall LevelUse Combined Data as Minimum as

usually the Sum of the Slices are greater than the Total Less Variation in Total Smaller Slice with Tail muted by Larger Slice

without Tail Shifting Losses to Longer Tail Slice

Keeping Score

Purpose of Slices - Improve Reserve Estimation Accuracy

Keep Tabs on your Estimates - Keep A Scorecard

Ultimate Losses Valued as of: ChangesPolicy 3-31-97 to 3-31-98 to 3-31-99 toYear 3-31-97 3-31-98 3-31-99 3-31-00 3-31-98 3-31-99 3-31-00

1993 12,399 12,100 12,600 11,928 (299) 500 (672)1994 11,355 11,800 11,800 12,000 445 0 2001995 13,027 13,500 13,700 14,000 473 200 3001996 11,061 10,300 10,900 11,100 (761) 600 2001997 6,563 6,500 5,900 6,000 (63) (600) 100

Subtotal 54,405 54,200 54,900 55,028 (205) 700 128

1998 9,400 9,400 10,600 10,800 0 1,200 2001999 - - 8,450 7,500 7,200 - - (950) (300)2000 - - - - 7,400 7,700 - - - - 3002001 - - - - - - 7,800 - - - - - -

Subtotal 9,400 17,850 25,500 33,500 0 250 200

Total 63,805 72,050 80,400 88,528 (205) 950 328

Keeping Score

Keeping Score

Keep Score of Your Estimates

Workers Comp. Reserving - How and When Should

You Slice the Cake?

Mark J. Mahon, FCAS, MAAA

MBA, Inc.

CLRS - September 23, 2002

![Shortest Paths Algorithm Design and Analysis 2015 - Week 7 ioana/algo/ Bibliography: [CLRS] – chap 24 [CLRS] – chap 25](https://img.dokumen.tips/doc/110x75/56649cb95503460f94981232/shortest-paths-algorithm-design-and-analysis-2015-week-7-httpbigfootcsuptroioanaalgo.jpg)

![EECS 3101 Prof. Andy Mirzaian. STUDY MATERIAL: [CLRS] chapter 34 [CLRS] chapter 34 2](https://img.dokumen.tips/doc/110x75/56649cc25503460f9498aa35/eecs-3101-prof-andy-mirzaian-study-material-clrs-chapter-34-clrs-chapter.jpg)

![Algoritmer og Datastrukturer 1 Merge-Sort [CLRS, kapitel 2.3] Heaps [CLRS, kapitel 6]](https://img.dokumen.tips/doc/110x75/56814de0550346895dbb4b06/algoritmer-og-datastrukturer-1-merge-sort-clrs-kapitel-23-heaps-clrs.jpg)