Embed Size (px)

Citation preview

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 1/24

English translation © 2009 M.E. Sharpe, Inc., rom the Russian text © 2009 “Vop-rosy ekonomiki.” “Ukraina: razdvoenie trans ormatsii,” Voprosy ekonomiki , 2009, no.3, pp. 125–42. A publication o the NP “Editorial Board o Voprosy ekonomiki” andthe Institute o Economics, Russian Academy o Sciences.

L Grigor’

ev is a Candidate o Economic Sciences, president o the oundation Insti-

Problems of Economic Transition , vol. 52, no. 7, November 2009, pp. 5–27.

© 2009 M.E. Sharpe, Inc. All rights reserved.ISSN 1061–1991/2009 $9.50 + 0.00.DOI 10.2753/PET1061-1991520701

L. G riGor’

ev , S. A GibALov , And M. S ALikhov

Ukraine: A Split Trans ormation

The Ukrainian economy (prior to the current crisis) achieved a limited recovery, but its prospects continue to be jeopardized by the split betweenthe industrial east, the agrarian west, and the Kyiv region, by failure to mod-ernize the crucial metallurgical sector, and by chronic political crisis.

As a rule, the success o trans ormation in Eastern Europe over the twenty

years since the all o the Berlin Wall is measured mainly in terms o degreeo political democratization and success in the creation o market institutions.But it is also important to take other criteria into account: the wel are o thepopulation undergoing “trans ormation,” the extent to which the intellectualpotential o a country has been preserved, and the adequate developmento human capital. By these criteria, the elites o countries with emergentmarkets have nothing special o which to boast. The situation o Ukraineis one o the most di cult rom the point o view o long-term prospects.In Ukraine everything remains ambiguous: democracy and political stale-mate; good conditions or development and comparatively limited results;success ul re orms and rampant corruption; the objective depth o regionaldevelopment; and interregional di erences in public opinion. A ter twodecades o trans ormation, the country and its leaders are unable to reach asocial compromise or ensure stable development in the broad sense.

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 2/24

6 PROBLEMS OF ECONOMIC TRANSITION

Ukraine is potentially a wealthy country; it perceives itsel and is perceived

by other countries as a political and economic power on the same level asTurkey and Poland. O all the “heirs” o the Soviet Union, Ukraine receivedone o the best collections o initial resources. The chie asset o the republicis an enterprising, hardworking, and educated population capable o producingliterally everything— rom ood to rockets. To a certain degree, the country hastried to emerge rom the trans ormational crisis by using a number o adaptivestrategies simultaneously. 1 Its eastern regions have striven to preserve industry,relying on signi cant competitive advantages such as cheap labor power andproximity to ports, while in Central and Western Ukraine labor migration toRussia and the European Union (EU) has become widespread. Like peoplein other post-Soviet states, Ukrainian citizens, acing the grave crisis o thetransition period, have managed to adapt to new realities.

Ukraine has objective advantages conducive to its development: a splendidclimate, ertile soils, a developed transportation in rastructure, ports, as wellas deposits o natural resources that are quite large by European standards.Finally, Ukraine is a transit country: like the Baltic states, it provides continen-tal Russia with an outlet to seaports and health spas; in addition, it provides

transit to the EU or Russian gas. Let us also note its developed chemical andmetallurgical industry, its research base, a number o manu acturing plants,and the nuclear energy sector (one o the largest in the world). Thus, initialconditions in the country at the start o the period o market trans ormationsappeared very avorable.

Unlike a number o countries o the ormer socialist “camp,” Ukrainedid not experience open civil conficts at the start o trans ormation in theearly 1990s. I market institutions had been created here in good time andsociopolitical stability maintained throughout the transition period, then thiswould have been a success story. However, despite the avorable startingconditions, the trans ormational crisis in Ukraine turned out to be one o the deepest in the ormer Soviet Union. This was caused by the split in thecountry, by di culties in solving the institutional problems o trans orma-tion, and by strong external pressure rom interest groups pursuing their ownspecial purposes.

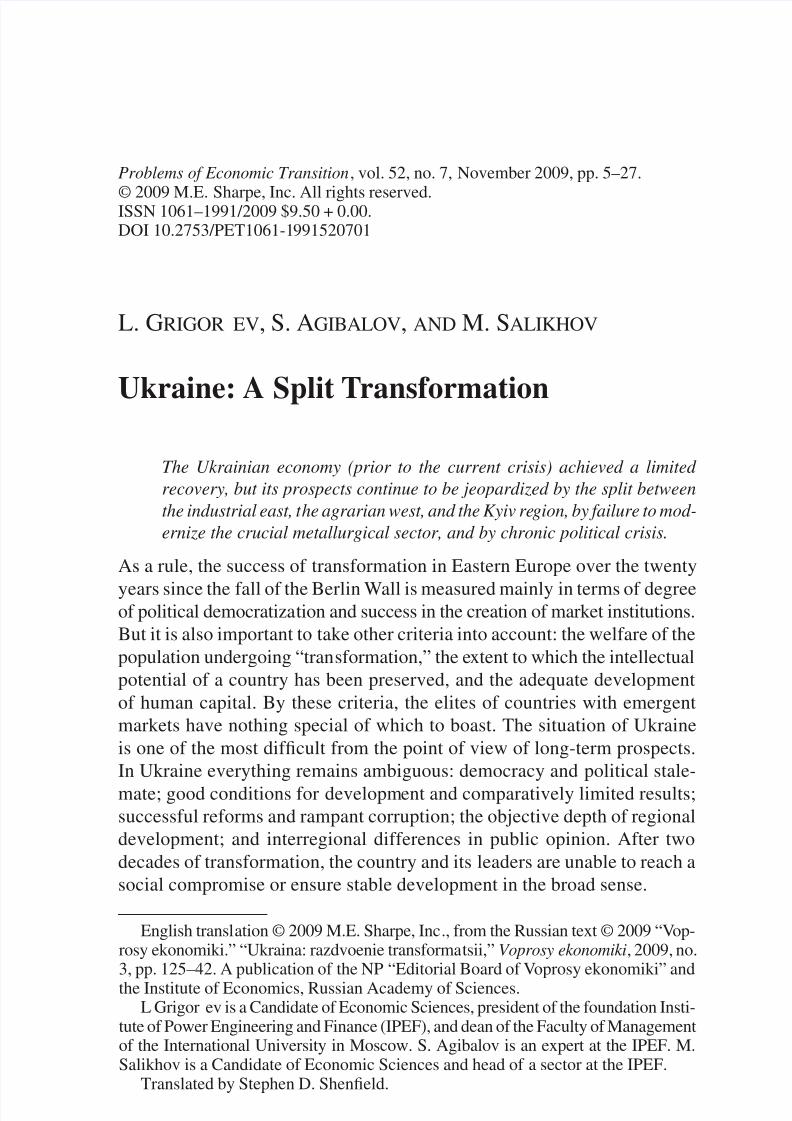

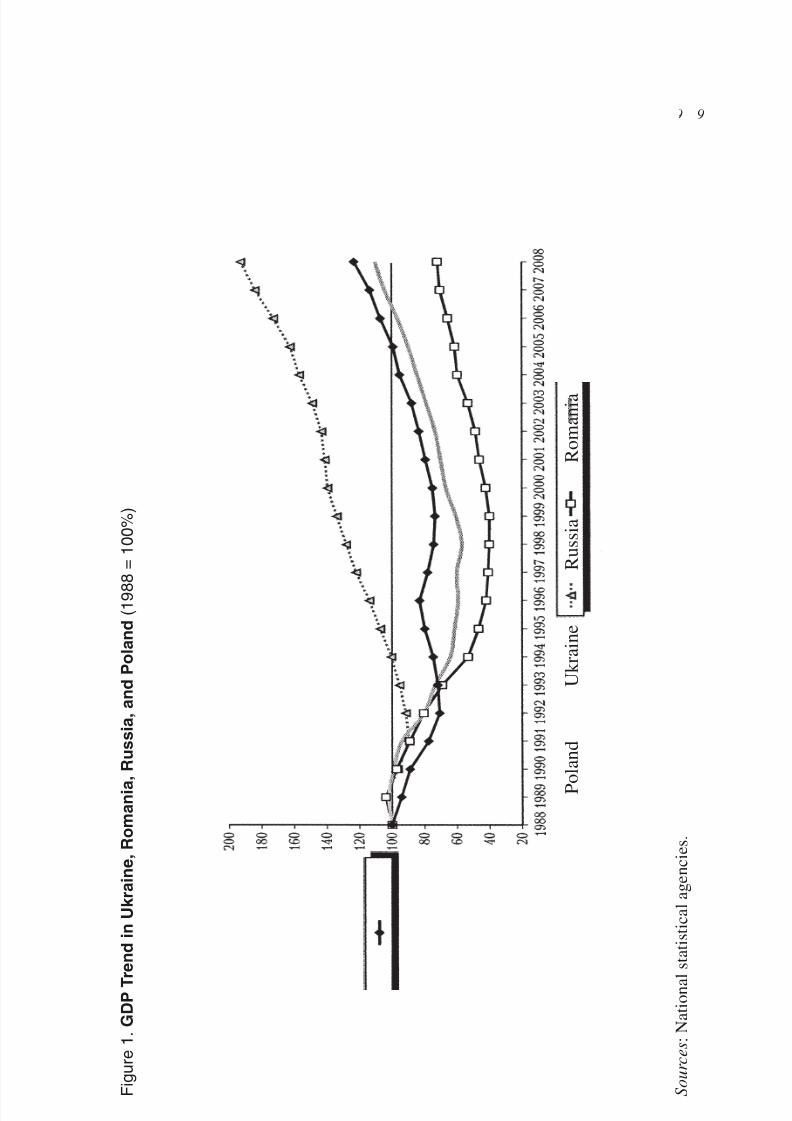

The deepest point o the crisis was reached in 1999, when a ter nine yearso continuous contraction the decline in the gross domestic product (GDP)reached 62 percent o the 1990 level—a much higher gure than in Russia,let alone the countries o Central and Eastern Europe (CEE). Since 2000 aneconomic recovery has begun in the country An e ective scal and monetary

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 3/24

NOVEMBER 2009 7

success ully, creating the conditions or an infow o capital—in particular,

o Russian capital. Until autumn 2008, the economy o Ukraine continuedto develop dynamically and in terms o rates o economic growth was oneo the leaders among East European economies and the large economies o the Commonwealth o Independent States (CIS). But this was accompaniedby unending political crisis and by successive external price shocks (positiveand negative); the questions o the price o imported gas and the conditions

or gas transit have remained throughout recent years instruments o domesticpolitical struggle. 2

Nevertheless, by the end o 2008 Ukraine’s GDP was still only slightlyover 70 percent o the 1990 level. Correspondingly, assuming that currentrates o growth are maintained, it will take until about 2015 to return to theprecrisis level. In essence, the country has lost the ruits o the labor o anentire generation. Now even this distant prospect is turning into a mirage: acrisis is un olding in Ukraine that threatens to wipe out the achievements o recent years.

A prolonged transition

The basic causes o such a deep decline in Ukraine’s GDP during the 1990s areconnected both with initial conditions and with the policy conducted during thetransition period. The Ukrainian economy was marked by a serious structuralimbalance in avor o industry: at the time o the disintegration o the SovietUnion, the speci c weight o industry in the economy was greater in Ukrainethan in any other union republic. Inevitably, a considerable part o Ukraine’sindustry proved uncompetitive upon exposure to the global economy. A thirdo industrial output came rom the military-industrial complex, which instan-taneously lost most o its state orders. The result was that over the rst veyears o independence the volume o industrial output ell by more than 60percent. The rupture o established economic ties also played its part, inasmuchas the large economies o Russia and Ukraine were mutually complementaryto a higher degree than other pairs o ormer Soviet republics.

An ine ective government economic policy at the early stages o thetransition period ound expression, in particular, in substantial subsidies toloss-making industrial enterprises. So t budget constraints and cheap energygoods encouraged rent-seeking behavior on the part o property owners, im-peded restructuring, and weakened incentives to carry out e ective changes. 3 Structural re orms were held back by chaotic privatization (in particular by

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 4/24

8 PROBLEMS OF ECONOMIC TRANSITION

made an impact. It was precisely at this period that Ukrainian industry was

compelled to reorient itsel toward Western markets.The economic upswing since 2000 is attributable to several actors:

• rapid growth in Russia, the EU, and other countries that serve asUkraine’s main export markets and sources o income rom guestworkers ( Gastarbeiter );

• the weakness of the hryvnia, which helped to keep Ukrainian exportscompetitive;

• the availability of unused production capacities (as in Russia),

acilitating a rapid response to growing demand or traditional exportgoods;• competitiveness in terms of labor costs: real incomes and wages

in Ukraine were signi cantly lower than in Russia and in the CEEcountries;

• a prudent (until 2005) scal and monetary policy, thanks to whichinfation was brought down to an acceptable level; and

• reforms in power engineering and in agriculture that helped to revivethese sectors.

Commenting on the results o development o the Ukrainian economy,the World Bank noted: “Recent economic growth in Ukraine was based onundiversi ed, but strong export growth rom sectors controlled by nancialindustrial groups which operated through in ormal relations and specialprivileges.” 4

The recovery began in the manu acturing industry and trade in 1999. Theopening up o commodity markets as a result o devaluation stimulated pro-duction in industry, while the volume o money remittances by the millions

o Ukrainian guest workers abroad rose substantially (about two-thirds romRussia and one-third rom the EU).

The role played by savings sent home by Ukrainian migrant workers inthe development o the Ukrainian economy remains very important. Theseremittances support consumption and have a positive infuence on residen-tial construction. Statistics on money remittances are extremely limited, butaccording to general o cial estimates money trans ers, and in particularremittances, were quite signi cant even at the beginning o the 2000s. Netcurrent trans ers in this period were on the order o 4 percent o GDP. Thevolume o money remittances rom Russia continues to play a salient rolein the country’s economy: visible remittances alone (hidden remittances are

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 5/24

NOVEMBER 2009 9

G D P T r e n

d i n U k r a i n e ,

R o m a n i a , R

u s s i a , a n

d P o

l a n d ( 1 9 8 8 =

1 0 0 % )

a t i o n a l s t a t i s t i c a l a g e n c i e s .

P o l a n d

U k r a i n e

R u s s i a

R o m a n i a

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 6/24

10 PROBLEMS OF ECONOMIC TRANSITION

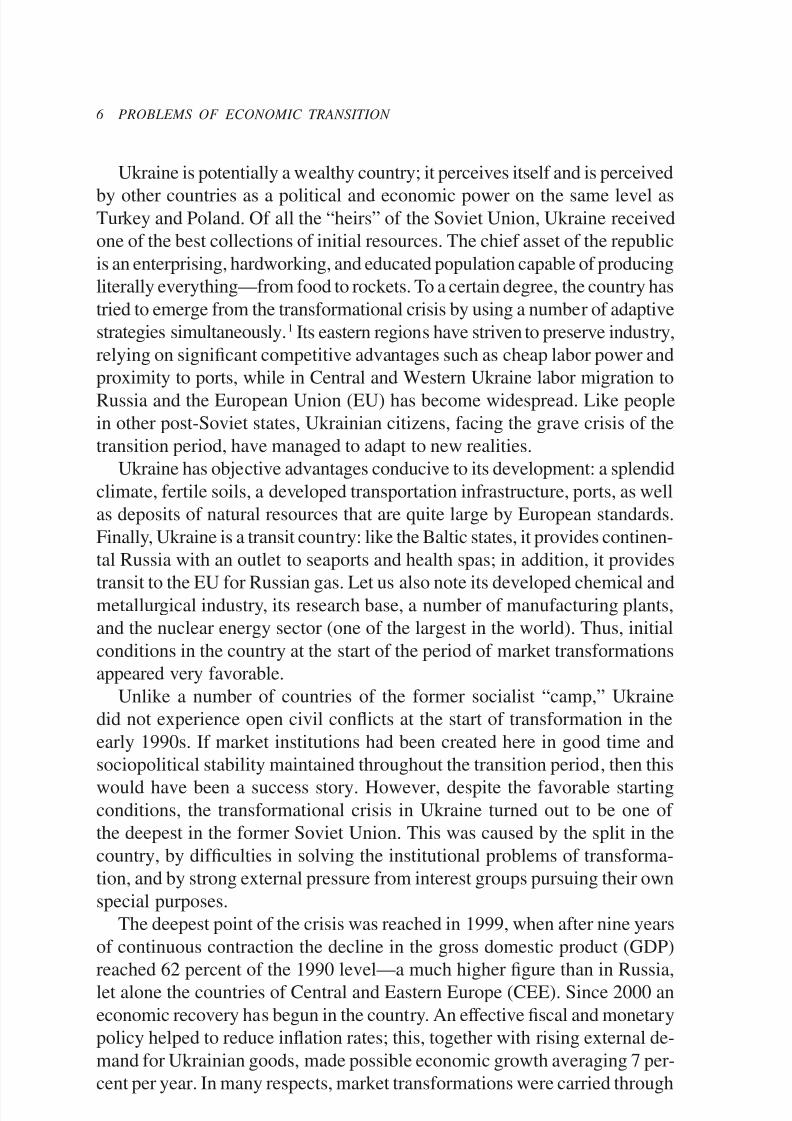

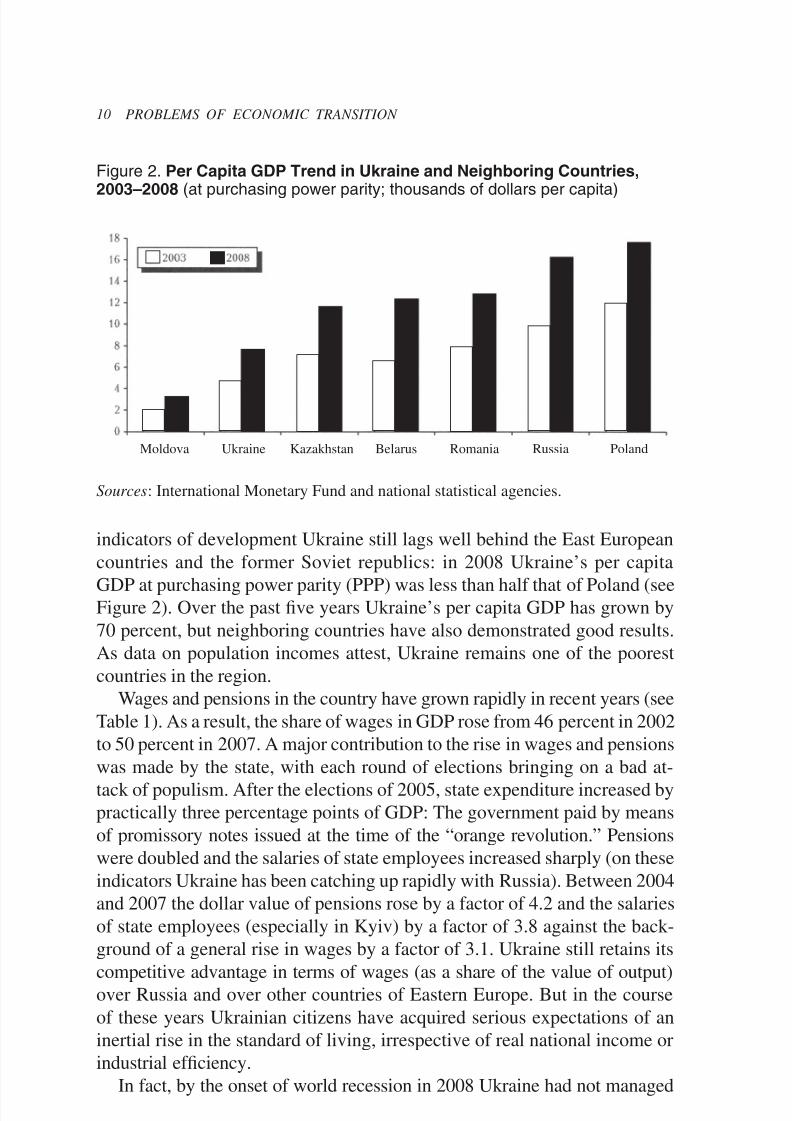

indicators o development Ukraine still lags well behind the East Europeancountries and the ormer Soviet republics: in 2008 Ukraine’s per capita

GDP at purchasing power parity (PPP) was less than hal that o Poland (seeFigure 2). Over the past ve years Ukraine’s per capita GDP has grown by70 percent, but neighboring countries have also demonstrated good results.As data on population incomes attest, Ukraine remains one o the poorestcountries in the region.

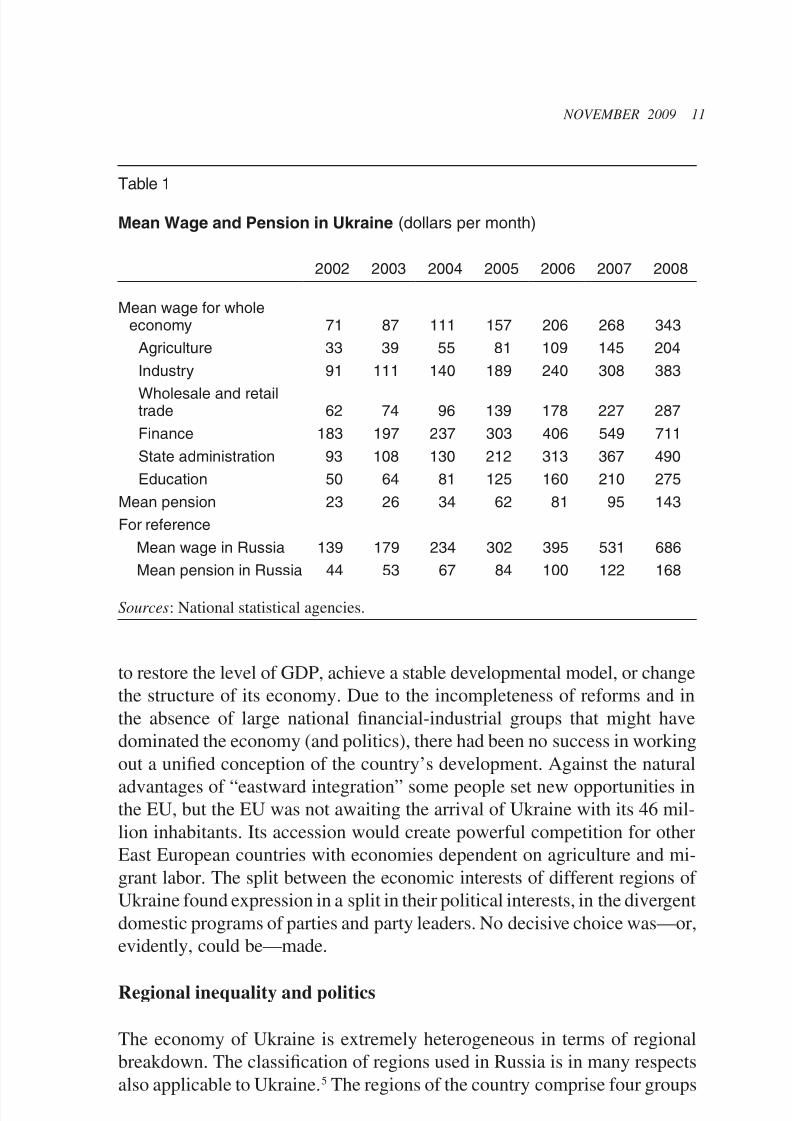

Wages and pensions in the country have grown rapidly in recent years (seeTable 1). As a result, the share o wages in GDP rose rom 46 percent in 2002to 50 percent in 2007. A major contribution to the rise in wages and pensionswas made by the state, with each round o elections bringing on a bad at-tack o populism. A ter the elections o 2005, state expenditure increased bypractically three percentage points o GDP: The government paid by meanso promissory notes issued at the time o the “orange revolution.” Pensionswere doubled and the salaries o state employees increased sharply (on theseindicators Ukraine has been catching up rapidly with Russia). Between 2004and 2007 the dollar value o pensions rose by a actor o 4.2 and the salarieso state employees (especially in Kyiv) by a actor o 3.8 against the back-ground o a general rise in wages by a actor o 3.1. Ukraine still retains itscompetitive advantage in terms o wages (as a share o the value o output)over Russia and over other countries o Eastern Europe. But in the courseo these years Ukrainian citizens have acquired serious expectations o an

Figure 2. Per Capita GDP Trend in Ukraine and Neighboring Countries,

2003–2008 (at purchasing power parity; thousands of dollars per capita)

Moldova Ukraine Kazakhstan Belarus Romania Russia Poland

Sources : International Monetary Fund and national statistical agencies.

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 7/24

NOVEMBER 2009 11

to restore the level o GDP, achieve a stable developmental model, or changethe structure o its economy. Due to the incompleteness o re orms and inthe absence o large national nancial-industrial groups that might havedominated the economy (and politics), there had been no success in workingout a uni ed conception o the country’s development. Against the natural

advantages o “eastward integration” some people set new opportunities inthe EU, but the EU was not awaiting the arrival o Ukraine with its 46 mil-lion inhabitants. Its accession would create power ul competition or otherEast European countries with economies dependent on agriculture and mi-grant labor. The split between the economic interests o di erent regions o Ukraine ound expression in a split in their political interests, in the divergentdomestic programs o parties and party leaders. No decisive choice was—or,evidently, could be—made.

Regional inequality and politics

Table 1

Mean Wage and Pension in Ukraine (dollars per month)

2002 2003 2004 2005 2006 2007 2008

Mean wage for wholeeconomy 71 87 111 157 206 268 343

Agriculture 33 39 55 81 109 145 204Industry 91 111 140 189 240 308 383

Wholesale and retailtrade 62 74 96 139 178 227 287Finance 183 197 237 303 406 549 711State administration 93 108 130 212 313 367 490Education 50 64 81 125 160 210 275

Mean pension 23 26 34 62 81 95 143For reference

Mean wage in Russia 139 179 234 302 395 531 686Mean pension in Russia 44 53 67 84 100 122 168

Sources : National statistical agencies.

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 8/24

12 PROBLEMS OF ECONOMIC TRANSITION

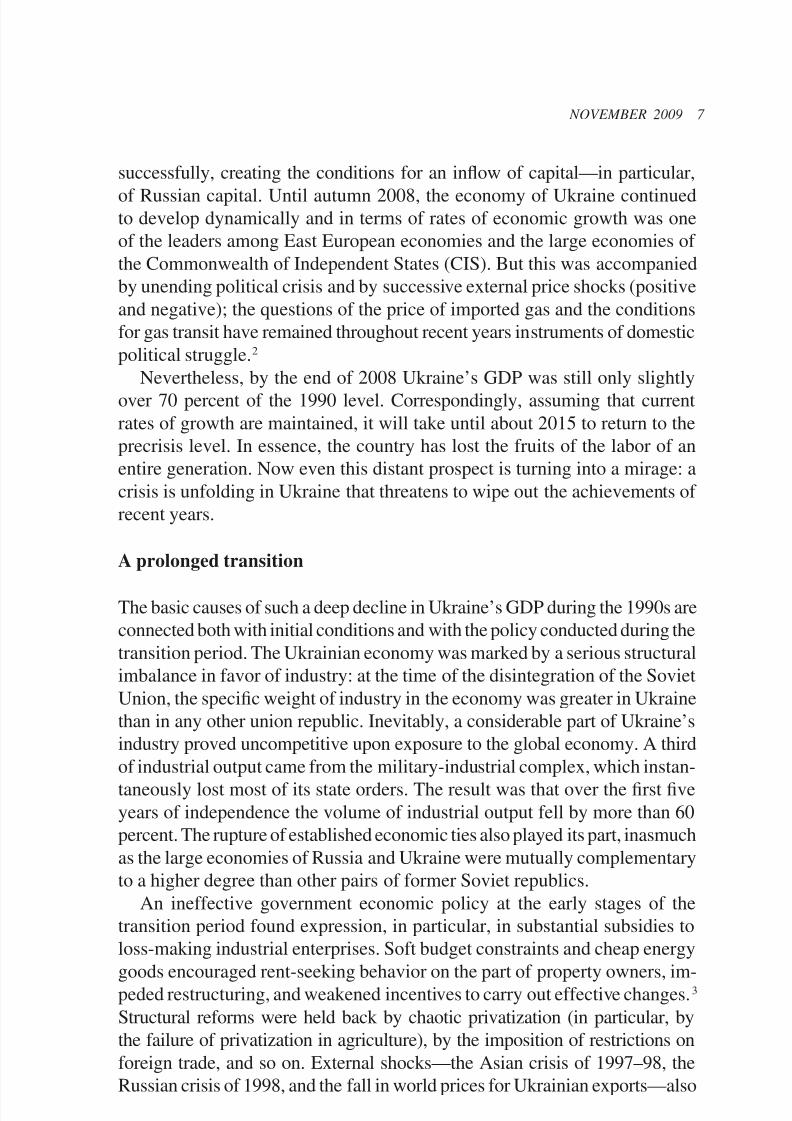

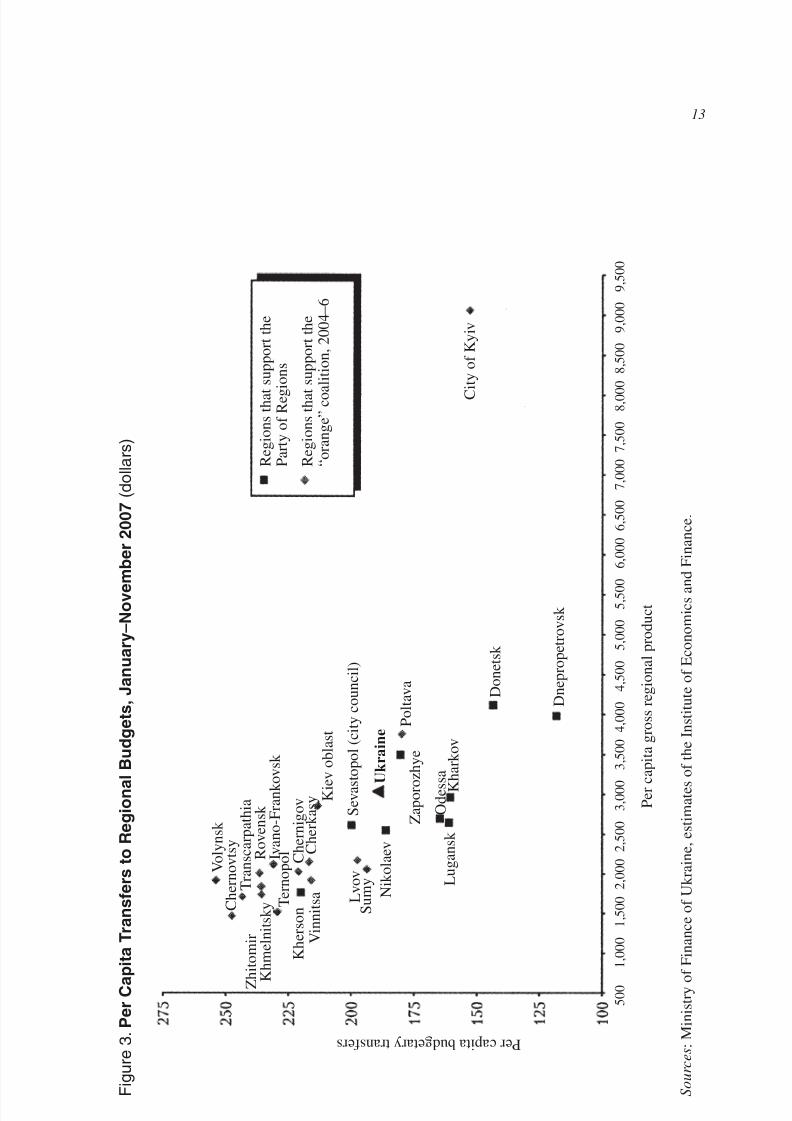

similar to those in Russia: the capital (Kyiv); regions o developed industry;

coastal regions; and poor agrarian regions (in western and central ukraine).From 2000 onward, the capital developed at an advanced rate: its average

annual rate o economic growth in 2000–2007 was 12.7 percent. No otherregion o Ukraine was able to boast o such a tempo. The GRP o the easternindustrial regions increased on average by 7.1 percent per year, while thewestern agrarian regions and the central regions grew even more slowly—atan average rate o 7.0 percent per year. Taking the crisis year o 1998 as abaseline, the economy both o the western regions and o the industrial regionso eastern Ukraine grew by a actor o 1.7. But Kyiv was ar ahead: here thecorresponding growth actor was 2.6.

During the crisis years o the 1990s, the depth o the economic declinevaried rom region to region. The large industrial centers su ered the most:the output o many industrial products ell to a small raction o its previouslevel. The region o the capital was a ected by the crisis to a lesser degree.By 2008 Kyiv had returned to the precrisis level in terms o the gross regionalproduct (GRP), while both the western and the eastern regions still have along way to go in this direction, with output at only 64 percent and 67 percent,

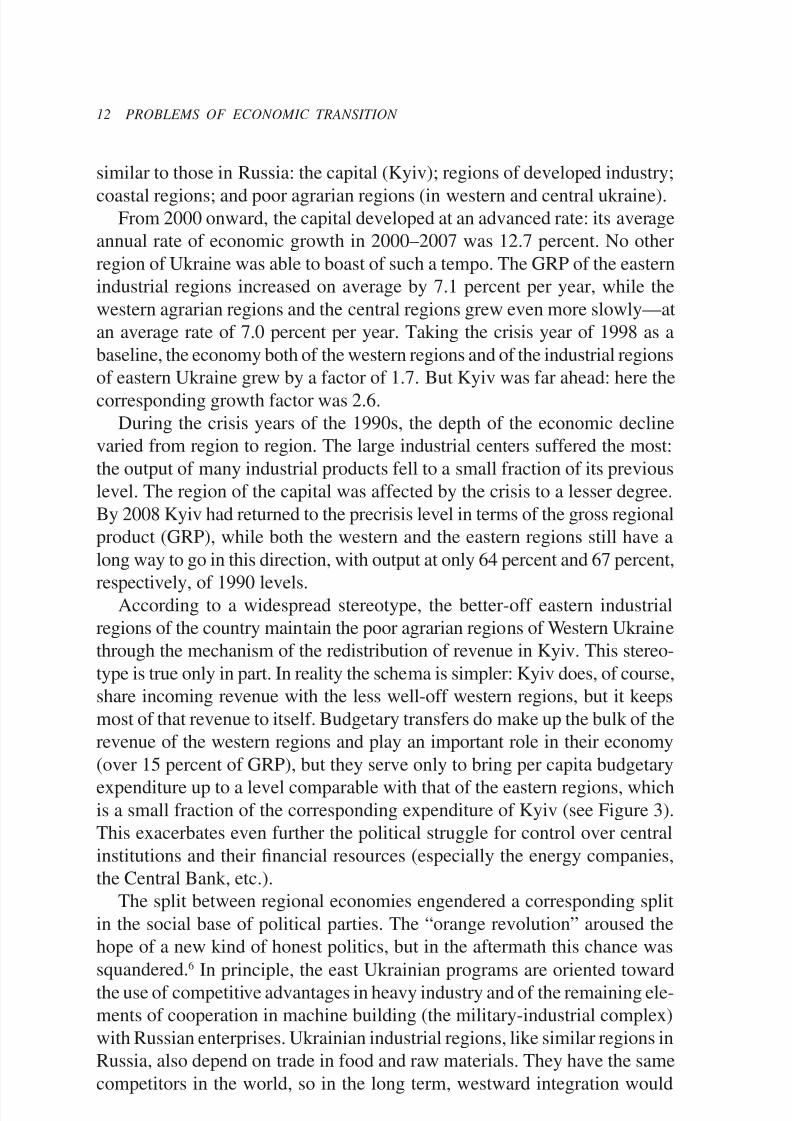

respectively, o 1990 levels.According to a widespread stereotype, the better-o eastern industrialregions o the country maintain the poor agrarian regions o Western Ukrainethrough the mechanism o the redistribution o revenue in Kyiv. This stereo-type is true only in part. In reality the schema is simpler: Kyiv does, o course,share incoming revenue with the less well-o western regions, but it keepsmost o that revenue to itsel . Budgetary trans ers do make up the bulk o therevenue o the western regions and play an important role in their economy(over 15 percent o GRP), but they serve only to bring per capita budgetaryexpenditure up to a level comparable with that o the eastern regions, whichis a small raction o the corresponding expenditure o Kyiv (see Figure 3).This exacerbates even urther the political struggle or control over centralinstitutions and their nancial resources (especially the energy companies,the Central Bank, etc.).

The split between regional economies engendered a corresponding splitin the social base o political parties. The “orange revolution” aroused thehope o a new kind o honest politics, but in the a termath this chance wassquandered. 6 In principle, the east Ukrainian programs are oriented towardthe use o competitive advantages in heavy industry and o the remaining ele-ments o cooperation in machine building (the military-industrial complex)

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 9/24

NOVEMBER 2009 13

P e r

C a p

i t a T r a n s f e r s

t o R e g

i o n a l B u

d g e t s ,

J a n u a r y – N o v e m

b e r

2 0 0 7 ( d o

l l a r s )

P e r c a p i t a g r o s s r e g i o n a l p r o d u c t

R e g i o n s

t h a t s u p p o r t t h e

P a r t y o f

R e g i o n s

R e g i o n s

t h a t s u p p o r t t h e

“ o r a n g e ” c o a l i t i o n ,

2 0 0 4 – 6

V o l y n s k

C h e r n o v t s y

Z h i t o m i r

K h m e l n i t s k y

K h e r s o n

V i n n i t s a T

r a n s c a r p a t h i a

R o v e n s k

I v a n o - F r a n k o v s k

T e r n o p o l C h e r n i g o v

C h e r k a s y K i e

v o b l a s t

L v o v

S u m y

N i k o l a e v

U k r a

i n e

Z a p o r o z h y e

S e v a s

t o p o l ( c i t y c o u n c i l )

P o l t a v a

O d e s s a

L u g a n s k

K h a r k o v

D o n e t s k

D n e p r o p e t r o v s k

C i t y o f

K y i v

in i s t r y o f F i n a n c e o f

U k r a i n e , e s t i m a t e s

o f t h e I n s t i t u t e o f

E c o n o m

i c s a n d

F i n a n c e .

5 0 0

1 , 0 0 0 1 , 5 0 0 2 , 0 0 0 2 , 5 0 0 3 , 0 0 0

3 , 5 0 0 4 , 0 0 0 4 , 5 0 0 5 , 0 0 0 5 , 5 0 0 6 , 0 0 0 6 , 5 0 0 7 , 0 0 0 7 , 5 0 0 8 , 0 0 0 8 , 5 0 0 9 , 0 0 0 9 , 5 0 0

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 10/24

14 PROBLEMS OF ECONOMIC TRANSITION

mean completing the deindustrialization o Ukraine: all niches o any com-

plexity on the EU’s markets or machine-building products ( or armaments,in particular) are already occupied by the Czech Republic and by other moredeveloped countries o CEE.

The program or integrating Western and Central Ukraine into the worldeconomy is in no way di erent in nature rom the integration o the agrar-ian areas o Latvia, Poland, Romania, and Bulgaria. In essence, this meansdevaluing old assets and human capital and making a new start on the basiso agriculture and migrant labor under conditions o the sharpest quality com-petition with EU countries and cost competition with developing countries(especially taking into account liberalization within the ramework o theWorld Trade Organization).

The poor compatibility o two such di erent programs implies the poorcompatibility o the uture position o the respective nancial and politicalelites. The acute problems associated with use o the Russian language, entryinto NATO, and relations with Russia merely conceal the pro ound conficto interests. O course, or the west Ukrainian elite to maintain its controlover the general policy o the country (over Kyiv) it requires external support,

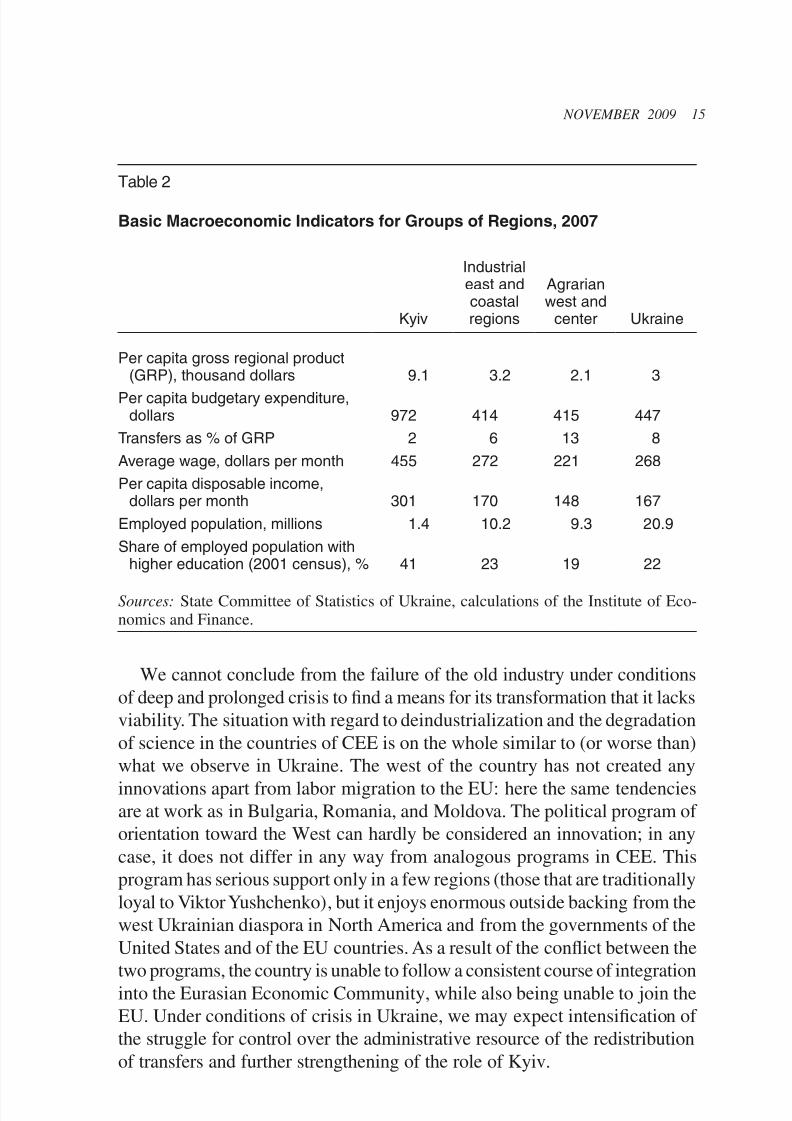

because countries with a market economy are usually dominated by elitesrom the more developed donor–regions.The gap in level o economic development between the eastern and the

western regions refects the initial con guration o the assets inherited rom theSoviet period (see Table 2). 7 This situation was exacerbated by an enormousoutfow o population, especially rom agrarian areas. Here as in Russia, indus-trial regions ace a di cult and uncertain uture in the post-Soviet period.

We are not in ull agreement with the conclusions drawn by the author o one work devoted to analysis o the situation in Ukraine:

Ukrainian regionalism is more complex than the historically evolved op-position between the east and the west. The east and the west represent thepolitical “poles” o Ukraine, while in all elections without exception thestruggle is waged primarily or the center. However, the roles played bythe west and the east in Ukrainian politics cannot be reduced to a mattero territorial demarcation. They can be analyzed in the context o center–periphery relations in the process o post-Soviet state building. The (pre-dominantly agrarian) west o Ukraine then appears as the political center

o the country, as the zone o its political innovations. At the same time,the Ukrainian east, where the main economic potential o the country wasconcentrated despite its very high level o urbanization and industrializa

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 11/24

NOVEMBER 2009 15

We cannot conclude rom the ailure o the old industry under conditionso deep and prolonged crisis to nd a means or its trans ormation that it lacksviability. The situation with regard to deindustrialization and the degradationo science in the countries o CEE is on the whole similar to (or worse than)what we observe in Ukraine. The west o the country has not created anyinnovations apart rom labor migration to the EU: here the same tendenciesare at work as in Bulgaria, Romania, and Moldova. The political program o orientation toward the West can hardly be considered an innovation; in anycase, it does not di er in any way rom analogous programs in CEE. Thisprogram has serious support only in a ew regions (those that are traditionallyloyal to Viktor Yushchenko), but it enjoys enormous outside backing rom thewest Ukrainian diaspora in North America and rom the governments o theUnited States and o the EU countries. As a result o the confict between thetwo programs, the country is unable to ollow a consistent course o integrationinto the Eurasian Economic Community, while also being unable to join theEU Under conditions o crisis in Ukraine we may expect intensi cation o

Table 2

Basic Macroeconomic Indicators for Groups of Regions, 2007

Kyiv

Industrialeast andcoastalregions

Agrarianwest and

center Ukraine

Per capita gross regional product(GRP), thousand dollars 9.1 3.2 2.1 3

Per capita budgetary expenditure,dollars 972 414 415 447

Transfers as % of GRP 2 6 13 8Average wage, dollars per month 455 272 221 268Per capita disposable income,

dollars per month 301 170 148 167Employed population, millions 1.4 10.2 9.3 20.9Share of employed population with

higher education (2001 census), % 41 23 19 22

Sources: State Committee o Statistics o Ukraine, calculations o the Institute o Eco-nomics and Finance.

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 12/24

16 PROBLEMS OF ECONOMIC TRANSITION

“New” growth on the basis o old assets

The long-term growth potential o the Ukrainian economy consists in thegradual improvement o the quality o products supplied to EU markets andin the partial return o labor power in the context o the modernization o industry oriented toward the East. But this requires substantial oreign (Rus-sian) investment, or which conditions, due to the permanent political crisis,have been ar rom ideal. As a result, the upswing has taken place mainly onthe basis o old assets.

At the beginning o 2006, Ukraine ran up against the rst appreciable risein the prices o imported energy resources. It became obvious that this wasnot a one-time phenomenon, but rather a mani estation o a tendency orcontinued rise in prices. Ukrainian industry had received a clear signal thatit must expand investment in raising the energy e ciency o production. In2006 and 2007, investment in manu acturing industry increased by 23 percentand 32 percent, respectively. Let us note that many declarations and publi-cations that appeared in the run-up to the next round o negotiations on thecost o imported natural gas contained extremely negative assessments o the

consequences o higher gas prices or Ukrainian industry and or the coun-try’s economy as a whole. At the beginning o 2006, pessimistic assessmentswere given by the World Bank and the International Monetary Fund (IMF),and also by well-known Ukrainian research companies. These assessments,o course, were o an “orange” character and were not borne out. The WorldBank later admitted that Ukraine had demonstrated extraordinary resiliencein the ace o higher costs or imported natural gas. 9

The rapid development o the country in the 2000s led to perceptiblechanges in the structure o its economy. Thus, at the start o the decade, whenUkraine had only just begun to recover a ter prolonged crisis, the share o agriculture in GDP exceeded 16 percent, as it does in the majority o poor andunderdeveloped states. This was a consequence o contraction o the sectoro market and nonmarket services. Trans ormations in the ormer union re-publics were accompanied, as a rule, by a considerable weakening o the roleo the state. As a result, in the structure o GDP the greatest reductions took place in expenditure on social needs and education, in the share o nonmarketservices nanced mostly by the state. Ukraine, despite the di cult situationin the 1990s, managed to maintain unding o the state’s social unctions at acomparatively high level. Even in 2001 education accounted or 4.9 percent o GDP while the corresponding gure or Russia at the same time was no more

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 13/24

NOVEMBER 2009 17

The upswing in the Ukrainian economy in the 2000s took place on the oun-dation o ormerly Soviet industry, inasmuch as it was based on the restorationo trading ties with Russia against the background o a general acceleration inthe development o the world economy; this enabled Ukraine to increase itsexports o industrial goods. The embryonic condition o the sector o marketservices (a legacy o the planned economy) and the rapid growth in populationincomes predetermined the rapid development o this sector.

As a result, substantial shi ts took place in the structure o the Ukrainianeconomy. The share o agriculture remains high even by the standards o the majority o East European countries, although it declined by practicallyhal . The speci c weight o industry in GDP increased, mainly thanks to thedynamic growth o the manu acturing sector. In contrast to more developedcountries, in Ukraine it is precisely industrial production that remains the“locomotive” o economic development. Comparatively new kinds o activityare emerging or the country— or example, the production o automobilesand other means o transportation Over a third o annual investment in xed

Table 3

Change in Structure of the Ukrainian Economy, 2001–2007: Shares ofAdded Value (in %)

2001 2007

Agriculture, hunting, forestry 16.1 7.3Industry 30.2 31.0Mining 4.6 4.6

Manufacturing 19.4 22.6Production and distribution of electricity, gas, and water 6.1 3.9Construction 4.0 4.9Services 49.8 57.0Trade, automobile repairs, and so on 12.2 14.1Transportation and communications 13.4 10.6Education 4.9 5.6Health care and social assistance 3.3 3.5Other forms of economic activity 16.0 23.1

Source: State Committee o Statistics o Ukraine.

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 14/24

18 PROBLEMS OF ECONOMIC TRANSITION

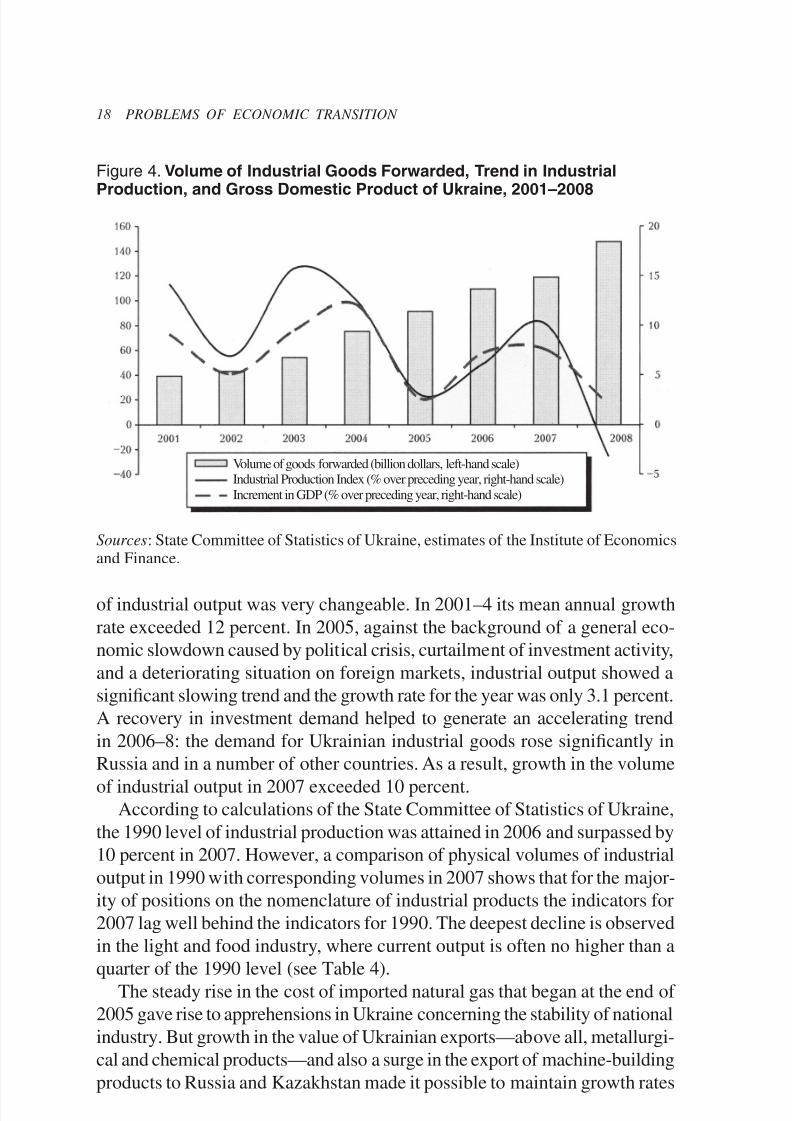

o industrial output was very changeable. In 2001–4 its mean annual growthrate exceeded 12 percent. In 2005, against the background o a general eco-nomic slowdown caused by political crisis, curtailment o investment activity,and a deteriorating situation on oreign markets, industrial output showed asigni cant slowing trend and the growth rate or the year was only 3.1 percent.A recovery in investment demand helped to generate an accelerating trendin 2006–8: the demand or Ukrainian industrial goods rose signi cantly inRussia and in a number o other countries. As a result, growth in the volume

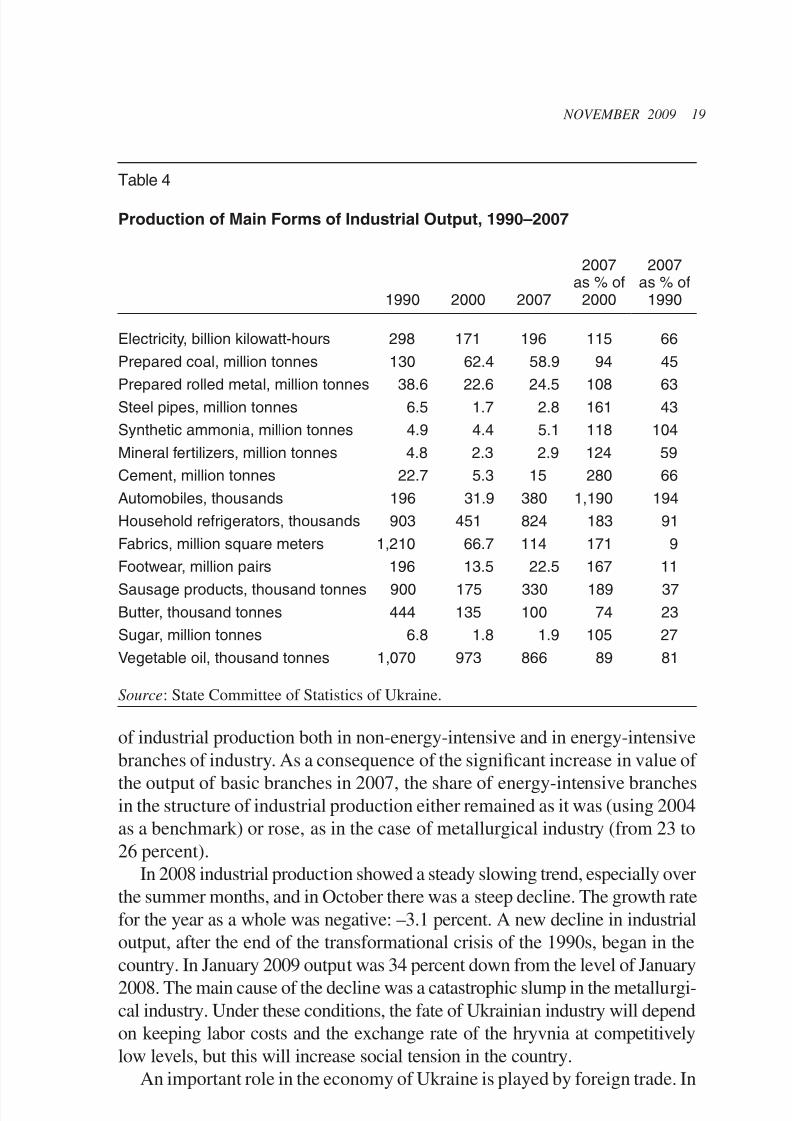

o industrial output in 2007 exceeded 10 percent.According to calculations o the State Committee o Statistics o Ukraine,

the 1990 level o industrial production was attained in 2006 and surpassed by10 percent in 2007. However, a comparison o physical volumes o industrialoutput in 1990 with corresponding volumes in 2007 shows that or the major-ity o positions on the nomenclature o industrial products the indicators or2007 lag well behind the indicators or 1990. The deepest decline is observedin the light and ood industry, where current output is o ten no higher than aquarter o the 1990 level (see Table 4).

The steady rise in the cost o imported natural gas that began at the end o 2005 gave rise to apprehensions in Ukraine concerning the stability o national

Figure 4. Volume of Industrial Goods Forwarded, Trend in Industrial

Production, and Gross Domestic Product of Ukraine, 2001–2008

Volume o goods orwarded (billion dollars, le t-hand scale)Industrial Production Index (% over preceding year, right-hand scale)Increment in GDP (% over preceding year, right-hand scale)

Sources : State Committee o Statistics o Ukraine, estimates o the Institute o Economicsand Finance.

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 15/24

NOVEMBER 2009 19

o industrial production both in non-energy-intensive and in energy-intensivebranches o industry. As a consequence o the signi cant increase in value o

the output o basic branches in 2007, the share o energy-intensive branchesin the structure o industrial production either remained as it was (using 2004as a benchmark) or rose, as in the case o metallurgical industry ( rom 23 to26 percent).

In 2008 industrial production showed a steady slowing trend, especially overthe summer months, and in October there was a steep decline. The growth rate

or the year as a whole was negative: –3.1 percent. A new decline in industrialoutput, a ter the end o the trans ormational crisis o the 1990s, began in thecountry. In January 2009 output was 34 percent down rom the level o January2008. The main cause o the decline was a catastrophic slump in the metallurgi-cal industry. Under these conditions, the ate o Ukrainian industry will depend

Table 4

Production of Main Forms of Industrial Output, 1990–2007

1990 2000 2007

2007as % of

2000

2007as % of

1990

Electricity, billion kilowatt-hours 298 171 196 115 66Prepared coal, million tonnes 130 62.4 58.9 94 45

Prepared rolled metal, million tonnes 38.6 22.6 24.5 108 63Steel pipes, million tonnes 6.5 1.7 2.8 161 43Synthetic ammonia, million tonnes 4.9 4.4 5.1 118 104Mineral fertilizers, million tonnes 4.8 2.3 2.9 124 59Cement, million tonnes 22.7 5.3 15 280 66Automobiles, thousands 196 31.9 380 1,190 194Household refrigerators, thousands 903 451 824 183 91Fabrics, million square meters 1,210 66.7 114 171 9Footwear, million pairs 196 13.5 22.5 167 11

Sausage products, thousand tonnes 900 175 330 189 37Butter, thousand tonnes 444 135 100 74 23Sugar, million tonnes 6.8 1.8 1.9 105 27Vegetable oil, thousand tonnes 1,070 973 866 89 81

Source : State Committee o Statistics o Ukraine.

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 16/24

20 PROBLEMS OF ECONOMIC TRANSITION

2007 oreign trade turnover exceeded 78 percent o GDP—a act that shows

how open the country is to the world economy.The most important article in Ukraine’s exports is errous metals. Through-

out recent years the situation on the metals market has been very avorable orUkraine. Ever since the Ukrainian economy started to recover in 1999, metalprices have mostly risen, raising the value o Ukrainian exports. Between2001 and 2007, exports o errous metals and o items made out o themincreased rom $5.6 billion to $19.8 billion, while their share in total exportsrose rom 35 percent to 40 percent. Other very important articles o exportare equipment and means o transportation. In nominal terms, the value o these exports increased rom $1.9 billion to $6.8 billion.

Throughout recent years, Russia has remained the key market or theexport o Ukrainian equipment. In 2007 Russia accounted or over hal o Ukrainian exports o machinery, equipment, and means o transportation. Theother large importers o Ukrainian equipment are Belarus and Kazakhstan.In 2007 the share o machinery, equipment, and means o transportation inthe total volume o Ukrainian exports reached 14 percent. It was preciselyin the “orange” year o 2005 and in the ollowing two years that Ukraine’s

share o Russia’s imports rose sharply—to 26 percent—as a consequenceo the strongly competitive position o Ukrainian producers (in particular,o Ukrainian suppliers o metals and o machinery and equipment). Underthese conditions, internal political obstacles blocked the natural integrationo Ukraine into the Eurasian Economic Community. As the cyclical slump inthe EU deepens, Ukrainian goods will ace stronger competition there, whiletotal remittances rom guest workers in the EU and Russia will decline.

Investment growth in 2007 and the rise in population incomes acilitateddynamic growth in imports o machinery and equipment and o automobiles.Since 2005 imports o these categories o goods have increased by $9 billion.At the same time, the speci c weight o imports rom Russia has declined.The share o machinery and equipment in the total volume o imports rose

rom 3 percent in 2001 to 18.3 percent in 2007.Russia remains Ukraine’s biggest trading partner. Although the actor o

the Soviet legacy must be taken into consideration here, in many respectsRussian–Ukrainian trade relations have taken shape during the period o eco-nomic growth in both countries. The basis o Ukraine’s imports rom Russiais energy resources, which account or about 60 percent o the total value o Ukraine’s imports rom our country. The structure o Ukraine’s exports toRussia is more diversi ed and goods with high added value make up a larger

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 17/24

NOVEMBER 2009 21

Ukrainian economy. First o all, it should be noted that although physical

volumes o imported energy goods have contracted the cost o imports hasincreased, and this has had a negative impact on the country’s balance o trade.When the prices o energy goods began to rise the cost o imports rom Russiaincreased by $5 billion, while Ukrainian exports increased by $7 billion overthe same period. As a result, the de cit in Ukraine’s bilateral trade with Rus-sia has gradually decreased in recent years. In 2008 the trend in exports wasagain ahead o the corresponding indicator or imports; the trade de cit orthe year was a little over $4 billion, which was less than in 2004–6. Growthin Russian demand or the products o Ukrainian industry compensated orlosses due to the increased cost o imported energy resources.

“With your shield or on it”—the Ukrainian metallurgicalindustry *

The metallurgical industry is o critical importance or the Ukrainian economy.Ukraine is one o the world’s leading producers o metallurgical products. In2007 it produced 43 million tonnes o steel and was the eighth largest steel

producer in the world with a market share o 3.2 percent. Metallurgical prod-ucts account or 40 percent o the value o all Ukrainian exports. In 2008 theexport o metals brought Ukraine $27.6 billion. In addition, this sector is o major importance as an employer and as a consumer o goods and services.

The ourth quarter o 2008 was a very bad time or the world metallurgicalindustry. Demand or consumer durables—above all, or automobiles— elleverywhere; this and the collapse o the building industry led to a large-scaleworldwide slump in the metallurgical industry. The main producers signi -cantly reduced their output, but nowhere did the all in production have sucha great impact on the general state o the economy as it did in Ukraine. ByNovember 2008 output in the metallurgical industry was down to practicallyhal o its level in November 2007. As a result, output or the year was 11percent below the level o the preceding year. Output in related sectors—theproduction o iron ore and coking coal— ell in corresponding measure. Therewas a decline in the volume o reight carried on rail transportation, wherethe output o the metallurgical and mining industry accounts or 40 percento the total load. The overall result was a all in industrial production in 2008o 3.1 percent.

Support or this industry is a key task in preventing a general slump in theeconomy The government is trying to compensate or the reduction in exports

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 18/24

22 PROBLEMS OF ECONOMIC TRANSITION

by increasing domestic consumption. Proposals have been made sharply to

increase expenditure on the building objects o in rastructure and on regionaldevelopment with a view to stimulating demand rom machine building andconstruction. Such measures will hardly bring success because the domesticmarket is too small to expand consumption substantially, while 70 percent o the output o metallurgical industry was exported.

Another problem is the insu ciency o nancial resources or large-scalegovernment programs. It is not obvious whether the economy o the country,which means in act its citizens, should be expected to pay the price or the tech-nological backwardness o the metallurgical industry. Russia and Ukraine are theonly countries in the world that still make wide use o the open hearth urnace(Siemens–Martin process), which is much less energy-e cient than the oxygenconverter or the electric arc urnace. But while in Russia the proportion o steelsmelt in open hearth urnaces has declined in recent years, in Ukraine it has evenincreased somewhat and be ore the crisis stood at a level o about 45 percent.

In the period rom 2005 to mid-2008, when conditions were avorable,Ukrainian metal producers ailed to undertake adequate e orts to modernizetheir industry. They did not draw signi cant conclusions rom the experience

o 2005, when Ukraine su ered a serious external shock caused by a reduc-tion in the physical volume o metal exports due to the commissioning o large-scale production capacities in China.

It is characteristic that throughout recent years there should have been lessinvestment in the xed capital o the metallurgical complex, which accounts

or about one-quarter o the total volume o industrial output, than in oodindustry, which accounts or only one-sixth o total industrial output. Theextremely avorable situation on the metals market made it possible or theindustry to continue using the old technology. A ter the rst rise in the priceso imported natural gas, practically all o Ukraine’s metallurgical companiesannounced large-scale plans to modernize production, but no correspondinggrowth in investment ollowed. Moreover, the rise in steel prices enabledthem even to expand smelting in the energy-intensive open hearth urnaces.The sharp all in metal prices and the contraction o demand exerted a healthyinfuence on Ukraine’s metallurgical complex. At the beginning o December2008, eighteen o the twenty-two open hearth urnaces and ten o the twenty-one blast urnaces in Donetsk oblast ceased operating, while seven o the eightoxygen converters continue to unction.

One o the measures taken by the government in support o the industry wasto abolish the 12 percent surcharge on natural gas or metallurgical rms It is

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 19/24

NOVEMBER 2009 23

allow metal producers to switch to a di erent source o energy—in particular,

coal. But in any case this transition will take at least ve years.It is rather di cult to reequip and modernize enterprises when the price

o pro led iron is so high ($1,350 per tonne): the trans er price is more thansu cient to cover all costs and permits the use o all available capacity. Butit will be equally di cult to take decisions about modernization when thespeculative bubble bursts and the price alls to a raction o its current level:the prospects or uture demand are cloudy at best, and Ukraine will hardlymanage to compete in terms o e ciency with European producers. Simplesolutions are there ore chosen: workers are laid o , wages are cut, and pressureis exerted on suppliers. At least one actor a ecting production costs—energyprices—will become much more important or Ukrainian rms in 2009. Theprice o natural gas, which be ore 2006 was o little practical importance, hasincreased by more than 50 percent since the start o 2009 to over $300 perthousand cubic meters, not including the cost o delivery. Taking into accountthe sharp devaluation o the hryvnia, the price o gas is becoming a seriousproblem or consumers. The golden rain that poured down on Ukrainian metalproducers in 2007 and in the rst hal o 2008 enables them to nance large-

scale investment programs, and it is precisely now that they must act to raisethe e ciency o production. Otherwise, i prices continue to all, Ukrainemay lose its place among the world’s ten largest metal producers.

Economic crisis and political confict

The current crisis in Ukraine has turned out to be a major one. The nationalcurrency has been devalued by 50 percent; Ukraine’s GDP, according to ourestimate, ell by more than 10 percent in the ourth quarter o 2008 alone.The confict over gas in January 2009 developed against the background o two very grave crises—the economic crisis and the preelectoral crisis—thatalmost paralyzed the leadership o the country. Ukraine entered 2009 in a stateo pro ound crisis, with a population tired o permanent political confict andthe situation approaching a stalemate.

The confict o January 2009—unpleasant or all the parties involved—overthe transit o Russian gas to the EU and gas prices or Ukraine developedagainst the background o a rapid decline in production, exports, and budget-ary revenue. By all estimates, Ukraine consumes a disproportionately largeamount o energy due to the speci c structure o the economy and to the lowe ciency o production 10 Gas consumption is also higher than in Europe

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 20/24

24 PROBLEMS OF ECONOMIC TRANSITION

processes. Apparently, Ukrainian institutions were unable to pay or gas in

autumn 2008 because the corresponding unds had gone into the state budget.The repayment o debts (without penalty) in accordance with the contract o December 30 while simultaneously breaking o negotiations, the judicial an-nulment (without hearings and during the holiday) o the international transitcontract o January 5, the withdrawal rom negotiations or ten days, and thetemporary re usal to supply “technical gas” or transit (in accordance with therati ed Energy Charter) make the legal position o Ukraine in this confict veryshaky. Had any other country or even Ukraine treated a contracting party “not

rom Russia” in similar ashion, European courts would readily have ound itguilty. In “our” case everything is colored by politics. This confict providedan occasion or the consolidation o all interest groups in the EU that seek torevive nuclear energy and the coal industry, activate e orts to diversi y sourceso the supply o energy resources and ensure energy security, and so on.

Obviously the prolonged political crisis was not conducive to economicgrowth, but the costs associated with it were more than covered by exportearnings. Temporary stability was secured by high prices or basic Ukrainianexport goods (metals and ertilizers) and by growing demand or machinery

and equipment in Russia and in a number o other post-Soviet countries.Growth in population incomes stimulated the development o the servicesand construction sectors and brought an infow o oreign capital. At the sametime, the legal situation or Western capital in the country remained di cult,while Russian capital continued in addition to ace political obstacles.

The massive fight o capital in autumn 2008 that a ected Ukraine togetherwith other developing economies, in conjunction with problems in the bankingsystem, led to drastic devaluation o the national currency. The collapse o Prominvestbank, the sixth largest bank in Ukraine, caused widespread panicamong depositors, and as a result the banking system lost 10 percent o itsdeposits in the space o a ew days. The withdrawn unds were used to acquire

oreign currency. In the context o the political struggle and the “carve-up” o government agencies among the parties, blame or the all o the hryvnia waslaid on the “Yushchenko team” and on the Central Bank o Ukraine.

The main blows or the Ukrainian economy were the all in world demandand prices or metals and the all in demand rom the CIS or equipment. InNovember and December 2008, exports to Russia declined by practically 30percent. The current crisis will continue to have a negative impact on the worldeconomy: in January 2009, even Japanese exports were 45 percent down romthe level o January 2008 The situation or Ukrainian exports can there ore

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 21/24

NOVEMBER 2009 25

o national industry. Thanks to the growth o population incomes, the purchase

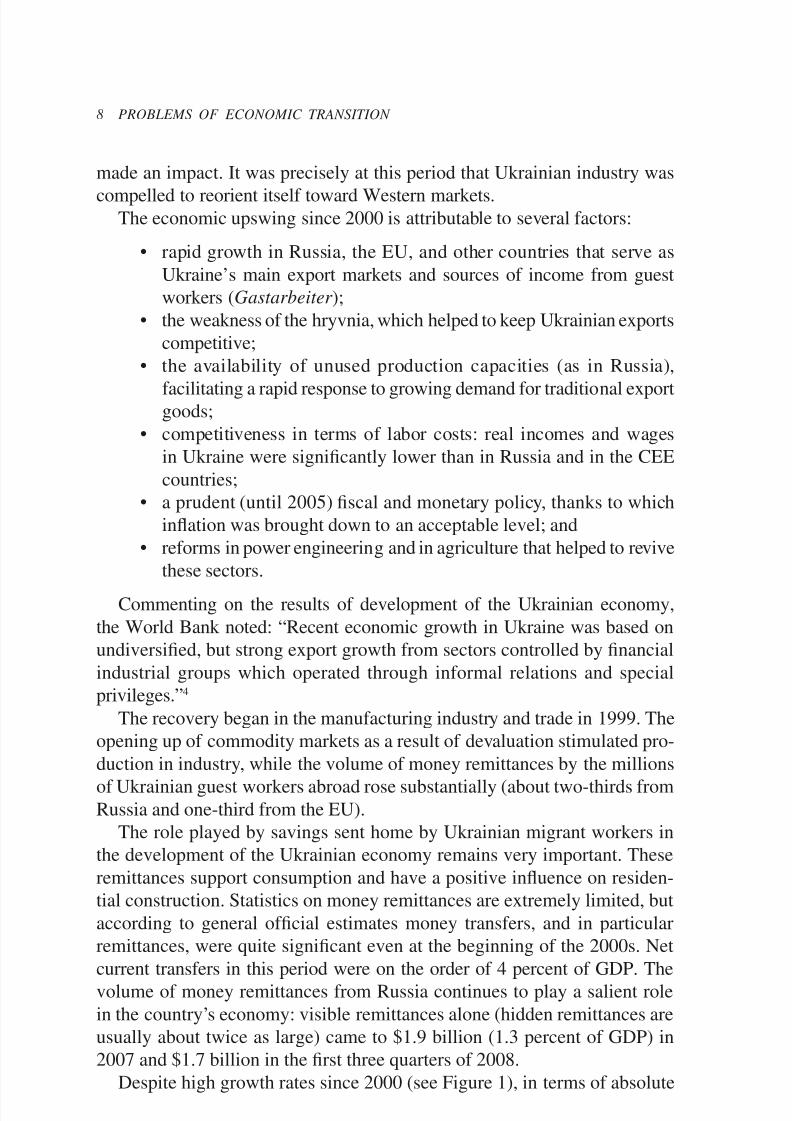

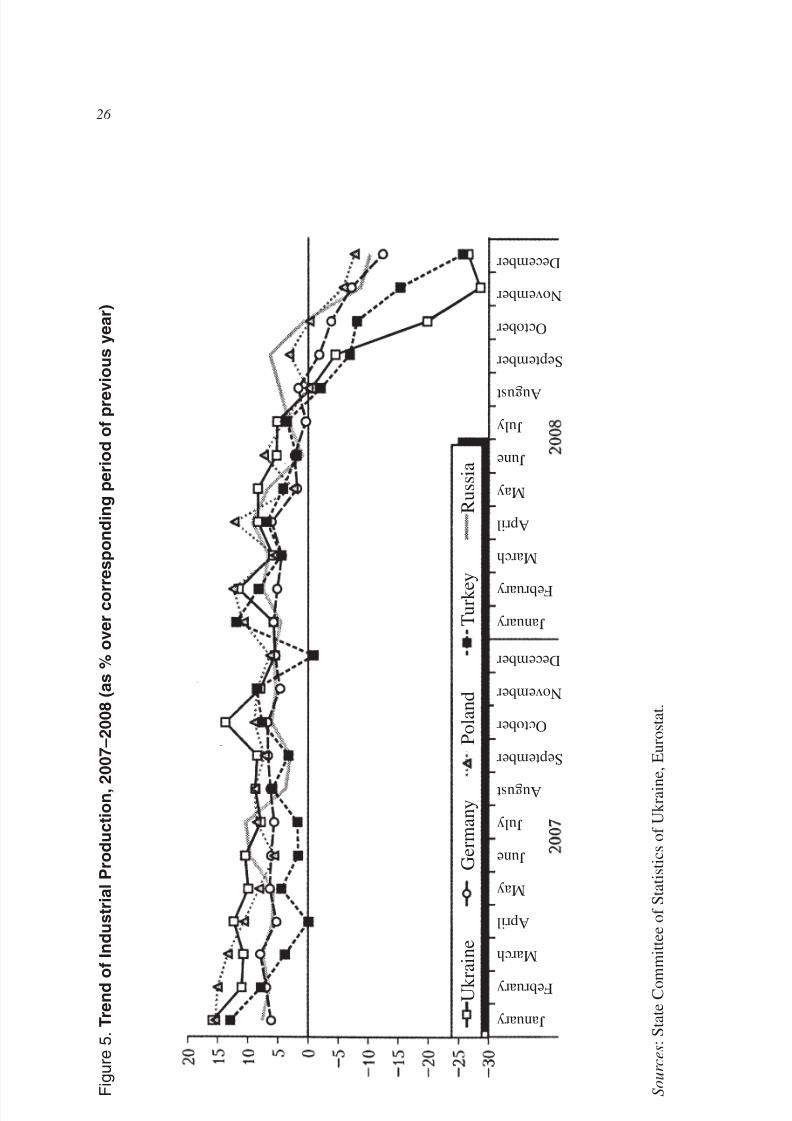

o an automobile has become a ordable or many households; assemblyproduction o oreign automobiles has been established in the country. Foodindustry has undergone serious modernization over the past ew years; a build-ing materials industry has in act been created; the transportation and commu-nications sector has developed; but the core o the Ukrainian economy—themetallurgical industry—has remained predominantly export-oriented. As aresult, the country has entered the crisis with its old problems unresolved:energy-intensive and ine cient metallurgical and machine building capacities“tied” to export to the CIS; and this has had an inevitable impact on the deptho the decline in industrial production (see Figure 5). The old problems havebeen joined by new ones—in particular, a large oreign debt ($42 billion)accumulated by the banks (a disease common to all the countries o EasternEurope), which in recent years have actively sought external nancing.

The latest news rom Ukraine gives grounds or serious alarm. The scalcrisis threatens to lead to de ault on the oreign debt. On February 25, 2009,Standard & Poor’s Rating Services lowered the sovereign rating o the countryto CCC+, which is seven rungs below investment grade (ratings o B and above)

and implies the possibility o de ault.* This may have a negative impact on newagreements over gas, inasmuch as devaluation has made gas much more expen-sive in terms o the national currency while budgetary revenues are alling.

The country aces presidential elections in January 2010 and the politicalelite is paralyzed by the struggle or power: to back away rom programs andde ned positions in oreign and domestic policy means to lose votes and utureo ces.11 Parties and leaders o parliamentary ractions nd it quite impossibleto resolve upon the budgetary cuts and banking re orm that the IMF requiresas conditions or the release o the second tranche o its loan, equal to $16billion. In the context o a worldwide recession and credit reeze, no othersources o supplementary budget nancing are in sight.

To appeal to Russia or aid in a preelectoral year would be a di cult stepor the Party o the Regions and the Yulia Tymoshenko Bloc to take because it

could be used against them in the election campaign. It is a practically impos-sible step or the Yushchenko team, taking into consideration the whole patterno their policy in 2007–9: support or the church schism, implementation o programs related to NATO accession, revision o history, restrictions on useo the Russian language, assistance to Georgia in the confict o August 2008,and the gas confict o January 2009.

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 22/24

26 PROBLEMS OF ECONOMIC TRANSITION

January

F e b r u a r y

M a r c h

A p r i l

M a y

J u n e

J u l y

A u g u s t

S e p t e m b e r

O c t o b e r

N o v e m b e r

D e c e m b e r

J a n u a r y

F e b r u a r y

M a r c h

A p r i l

M a y

J u n e

J u l y

A u g u s t

S e p t e m b e r

O c t o b e r

N o v e m b e r

D e c e m b e r

T r e n d o

f I n d u s t r i a l P r o

d u c t i o n ,

2 0 0 7 – 2 0 0 8 ( a s %

o v e r c o r r e s p o n

d i n g p e r i o

d o

f p r e v i o u s y e a r )

ta t e C o m m

i t t e e o f

S t a t i s t i c s o f

U k r a i n e ,

E u r o s t a t .

U k r a i n e

G e r m a n y

P o l a n d

T u r k e y

R u s s i a

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 23/24

NOVEMBER 2009 27

For almost two decades the country has been unable to adopt a single

program o development, orm a single elite, or reconstruct the economy. Theworld crisis has already shown itsel a strict examiner o the governments o leading countries, o the international nancial organizations, and o orumso political leaders. For Ukraine it represents a test o the survival o nationalindustry and o the possibility o integration into the world economy as ademocratic country at a medium level o development. Objective reality hascompelled all countries o the ormer socialist “camp” to pursue this goal.

Notes

1. See L.M. Grigor’

ev and M.R. Salikhov, GUAM. Piatnadtsat ’

let spustia (Mos-cow: Regnum, 2007); L. Grigor

’

ev, S. Kondrat’

ev, and M. Salikhov, “Trudnyi vykhodiz trans ormatsionnogo krizisa (sluchai Gruzii),” Voprosy ekonomiki , 2008, no. 10.

2. For an analysis o the rst confict over gas, see L.M. Grigor’

ev and M.R.Salikhov, “Ukraina—rost i gaz,” Ekonomicheskoe obozrenie IEF , January 2006. Onthe nature o the second confict, see S. Pirani, J. Stern, and K. Ya mava, The Russo-Ukrainian Gas Dispute of January 2009: A Comprehensive Assessment (Ox ordInstitute or Energy Studies, 2009) [www.ox ordenergy.org/pd s/nt27.pd ].

3. O. Babanin, V. Dubrovskiy, and O. Ivaschenko, Ukraine: The Lost Decade . . .and a Coming Boom? (Kyiv, 2002).

4. “Country Assistance Strategy Progress Report for Ukraine,” World Bank ReportNo. 32250-UA, May 19, 2005, p. 20.

5. See L. Grigor’

ev, N. Zubarevich, and Iu. Urozhaeva, “Stsilla i Kharibdaregional

’

noi politiki,” Voprosy ekonomiki , 2008, no. 2 [translated as “The Scylla andCharybdis o Regional Policy,” Problems of Economic Transiation, vol. 51, no. 12(April 2009), pp, 58–77].

6. See I. Bunin, “‘Oranzhevaia’ revoliutsiia,” Strategiia Rossii , 2006, no. 9,pp. 61–68.

7. A similar imbalance in regional development underlay the voluntary “divorce”

o the Czech Republic and Slovakia, but Czechoslovakia did not have such a dominantand uni ying capital as Kyiv, nor did it have traditions o separate statehood.

8. See V.Ia. Gel’

man, “Ukraina— ragmentirovannoe prostranstvo,” in SSSR posleraspada , ed. O.L. Marganiia (Moscow: Ekonomicheskaia shkola, 2007).

9. World Bank, “Ukraine: The Impact o Higher Natural Gas and Oil Prices,” Decem-ber 6, 2005; World Bank, “Ukraine Economic Update,” November 2006; InternationalMonetary Fund, “Ukraine—2006. Article IV Consultation,” October 24, 2006.

10. See, in particular S. Pirani, “Ukraine: A Gas Dependent State,” in Russian and CIS Gas Markets and Their Impact on Europe, ed. Pirani (Ox ord University Press

or the Ox ord Institute or Energy Studies, 2009), pp. 93–132.

11. A sad joke by one o the leaders o Ukraine: the political struggle in the countryhas come to resemble “a struggle or an exchange o cabins on the Titanic .”

8/6/2019 Ukraine Regional Differences Integration to Read

http://slidepdf.com/reader/full/ukraine-regional-differences-integration-to-read 24/24

Copyright of Problems of Economic Transition is the property of M.E. Sharpe Inc. and its content may not be

copied or emailed to multiple sites or posted to a listserv without the copyright holder's express written

permission. However, users may print, download, or email articles for individual use.