Embed Size (px)

Citation preview

Presentation to Businesses in St.Lucia

Towards October1, 2012

• The Basic Concepts of VAT• Why VAT• Registration • Treatment for VAT• Charging VAT• Accounting for VAT• Penalties• Changes in Business Status

2

What is VAT• VAT is an indirect tax, payable on the importation of

taxable goods and on the domestic consumption oftaxable goods and services;

• VAT on imported services is payable to the Comptrollerof Inland Revenue twenty days (20) after the end of theperiod;

• VAT is a broad-based tax levied at the different stagesof the production/distribution chain, on the added valueto those goods and services.

3

• Reform and simplify indirect tax system

• Reform of direct tax system

• Increase revenue to meet government expenditure/commitments

4

Main Terms of VAT

• Output VATCharged by a registered taxpayer on taxable goods and services supplied.

• Input VATPaid by a registered taxpayer, on taxable imports (customs value) and on taxable domestic purchases.

• Tax Period Month to account for net VAT Due/Refundable.

(Output VAT – Input VAT)5

Main Terms of VAT

Taxable person• A taxable person can be - Sole Proprietor (individual),

Partnership, Limited Company, Public Limited Company (PLC), Local Authority (Gov’t Dept)or non-profit making body

Taxable Supplies• Taxable supplies are supplies in Saint Lucia in the

course or furtherance of a taxable activity, other than an exempt supply.

6

VAT RATES – goods and services

• A standard rate of fifteen percent (15%);

• A reduced rate of eight percent (8%) on goods and services provided by hotels until April 2013; and

• A rate of zero percent (0%)

Some goods and services are also exempt.

7

Zero Rated Supplies No VAT is charged (i.e. 0 percent) Registered taxpayers can claim allowable Input VAT Exports are always zero-rated

Exempt Supplies No VAT is charged Registered taxpayers cannot claim Input VAT

8

List of Zero Rated Supplies include:

• Fuel• Fresh Eggs• Uncooked pasta• Services to a non-resident• Electricity provided by Saint Lucia Electricity

Services Limited• Water provided by Saint Lucia Water & Sewerage

Company

9

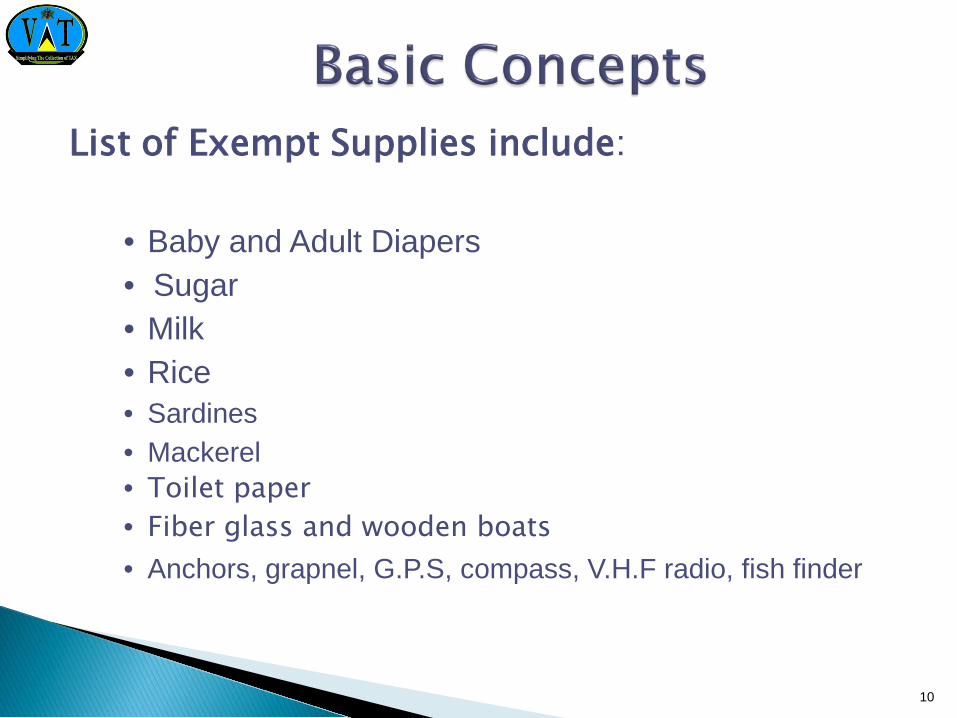

List of Exempt Supplies include:

• Baby and Adult Diapers• Sugar• Milk• Rice• Sardines• Mackerel• Toilet paper• Fiber glass and wooden boats• Anchors, grapnel, G.P.S, compass, V.H.F radio, fish finder

10

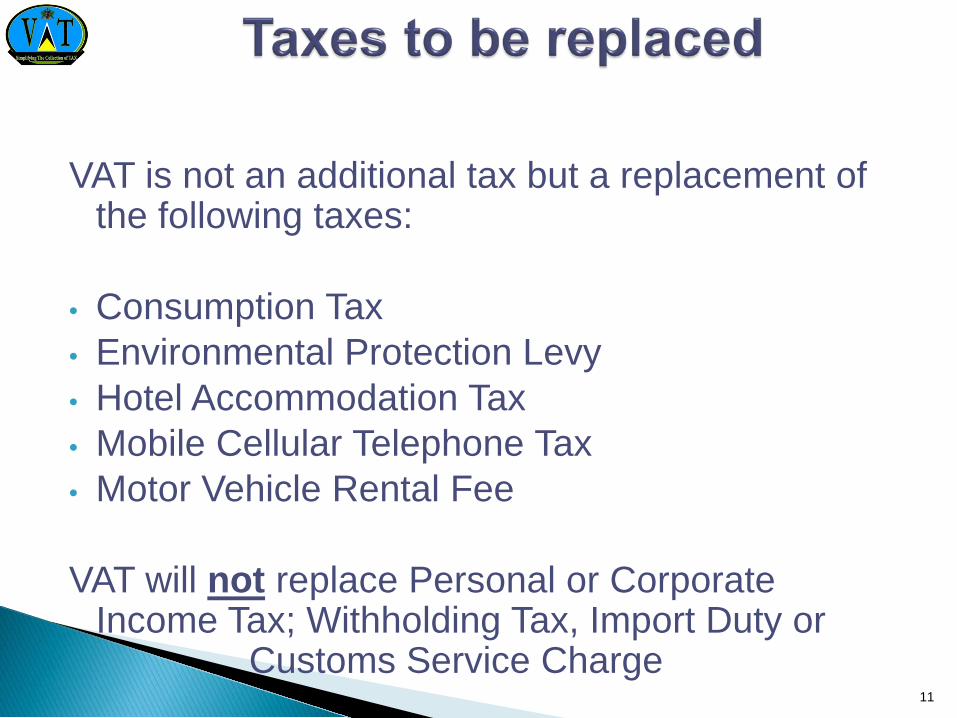

VAT is not an additional tax but a replacement of the following taxes:

• Consumption Tax• Environmental Protection Levy• Hotel Accommodation Tax• Mobile Cellular Telephone Tax• Motor Vehicle Rental Fee

VAT will not replace Personal or Corporate Income Tax; Withholding Tax, Import Duty or

Customs Service Charge11

THRESHOLD• The threshold for registration is EC $ 180,000.00

minimum gross annual sales of taxable supplies (goods and services).

• A REGISTRATION CERTIFICATE will be issued which should be prominently displayed in the business. Additional certificates will be issued if the business has more than one location/branch.

• Voluntary registration is also available for businesses whose taxable supplies are below the threshold.

12

Except where specifically exempted, VAT must be charged by registered businesses in the services sector trading in taxable supplies.

Exempt Services include the following:Financial ServicesMedical ServicesReligious ServicesVeterinary ServicesEducation Services/Supplies

13

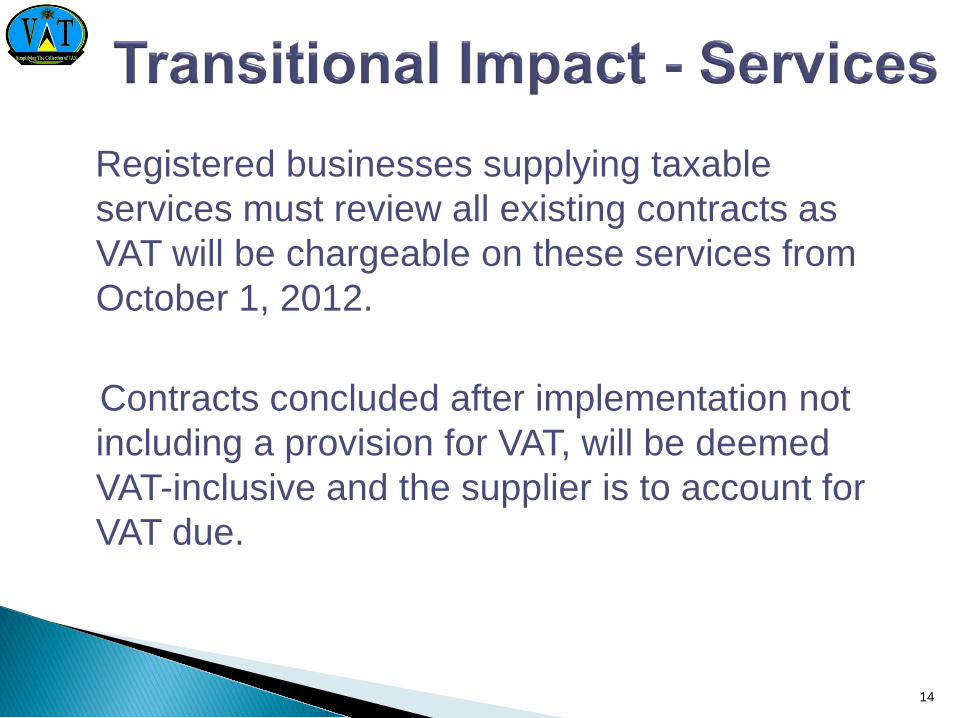

Registered businesses supplying taxable services must review all existing contracts as VAT will be chargeable on these services from October 1, 2012.

Contracts concluded after implementation not including a provision for VAT, will be deemed VAT-inclusive and the supplier is to account for VAT due.

14

As at the 1st of October 2012, any duty free concessions relating to Consumption tax and Environmental protection levy tax will no longer exist and VAT will prevail.

15

As at the 1st of October 2012, any stock held where Consumption tax and Environmental protection levy tax has been previously paid, VAT will be added on where the goods are to be treated as taxable goods as per the VAT Act 2012.

16

• Raw materials in stock as at 1st October 2012 where consumption tax and environmental levy tax has not been paid; will be treated as free of taxes (Manufacturers)

• Once these raw materials are issued to production, VAT is charged on the sale of the final product.(Output VAT)

17

Taxable goods being imported into Saint Lucia will need to be re-priced as there may be significant differences in the cost price once Consumption Tax and Environmental Protection Levy is replaced by VAT.

When re-pricing, please be mindful that the dollar value mark up should be replaced and not the percentage mark up. (see example)

18

Example of transitional pricingPre VAT

EC$Item importedCost of 100 Items $2,071.25Insurance & freight $ 375.00Customs Value $2,446.25

Import Duty @ 30% 733.88 (2446.25x 30%)Consumption tax @ 15% 477.02 (2446.25+733.88) x15%Environmental Protection Levy @ 1.5% 36.69 (2446.25x1.5%)Service Charge @5% 122.32 (2446.25x5%) Total Cost of Item 3,816.16 Mark up @50% 1,908.08Selling Price 5,724.24Selling price per unit (5,724.24/100) 57.24

19

Example of transitional pricing Post VAT

EC$Customs Value 2,446.25Import duty @ 30% 733.88Service Charge @ 5% 122.32Cost Price excl. VAT 3,302.45

VAT @ 15% (payable to Customs) 495.36 (Input VAT on importation)

Re Pricing for VAT method 1 method 2Cost Price excl. of VAT 3,302.45 3,302.45Mark up @ 50% 1,651.23 (dollar value) 1,908.08Selling price 4,953.68 5,210.53

VAT @15% 743.05 781.58Sales Price incl of VAT 5,696.73 5,992.11

20

Method 1By using the percentage mark up of 50%; There was a reduction in the dollar value mark up amount. There was a reduction in sales price

Method 2 The dollar mark up used was the same as pre VAT The sales price increase by $2.68 a 4.47% increase

Method 1 provides for a sales price reduction at the expense of the business. The mark up has been reduced due to the fact that the existing percentage rate mark up was used on the new lower cost, thus reducing the amount the company may require to operate and cover its overheads cost and any surplus funds for development.

Method 2 does not provide for a sales price reduction, but maintains the same dollar mark up despite the fact that cost has reduced, the new percentage mark up to be used for future under the VAT is now 57.78% , this allows the company to maintain the mark up required for the purpose of covering all overhead costs, and a profit margin.

21

Importation Full Domestic AccountingTo Customs To Inland Revenue Department

$9 + $6 + $3 + $12 Total VAT = $30

Output $15Input -$9

Returns $6

Output $18Input -$15

Returns $3

Output $30Input -$18

Returns $12Importer Wholesaler Retailer Consumer

Cost: $60Mark-up: $40

VAT: $15Sell for: $115

Cost: $100Mark-up: $20

VAT: $18Sell for: $138

Cost: $120Mark-up: $80

VAT: $30Sell for: $230

Cost :$230(VAT Incl. $30)

Each supplier is registered and accounts for the VAT through his monthly returns

22

23

Receipt of goods Full Domestic AccountingTo Customs To Inland Revenue Department

Nil Nil Total VAT = $0

The $ 3000 representsInput VAT on business expenses.(Rent, supplies)

Output VAT $ 0Input VAT $ 3000Due from IRD $ 3000

Shopkeeper Export Consumer

NB Goods are being received into the shop –warehousing principles apply - no taxes

Cost: $6000Mark-up: $4000VAT: $ 0Sell for: $10000

Cost :$10000(VAT Incl. $0)

Shopkeeper is registered and accounts for the VAT through his monthly returns

Mix Supply

Occurs where a taxable person or persons are making both taxable and exempt supplies for a tax period.

The amount of input tax allowed as a deduction for the tax period is the amount of input tax in respect of supplies and imports received which are directly allocable to the making of taxable supplies.

All input tax on supplies made by the taxable person, that are directly allocable to exempt supplies will not be allowed for deduction.

Where activities are put together to form a package which is sold as one product, but the activities which make up the package comprise of taxable and exempt activities (mix supply) the treatment of the final product supplied is dependant on which activity is most dominant within the package.

24

Mix Supply Example

The formula for apportionment in a mixed supply activity is:A X B/CWhere A is the input tax paid that cannot be directly allocated;B is the taxable supplies; andC is the total supplies.

The following example details the apportionment of input VAT paid during a tax period.

EX. Total supplies – $10,000; taxable supplies - $8,000; input VAT not directly allocable – $1,000.

Workings –: 1,000 X 8,000/10,000 = 800 (allowable input VAT)

NB. Directly allocable input tax should not be apportioned; where the taxable supplies exceed ninety percent (90%), all input tax is allowable.

25

Second hand rule

Where an item is purchased in Saint Lucia new, and resold in Saint Lucia; under the VAT Act, the item is classified as a second hand item and treated as such.

26

Second hand rule continued………

Input tax deduction on second hand items;

Second hand goods acquired in Saint Lucia during the tax period by a registered person from a person, registered or not registered, in a transaction not subject to tax if the goods are taxable at a positive rate under this Act and are acquired for the purpose of making taxable supplies;

Input VAT is calculated as follows;An amount equal to seventy percent of the tax fraction of the lesser of-

The amount paid, orThe fair market value, including tax,

27

Second hand rule continued……..

Input tax deduction on second hand items for related parties;

Second hand goods acquired in Saint Lucia during the tax period by a registered person from a related person, registered or not registered, in a transaction not subject to tax if the goods are taxable at a positive rate under this Act and are acquired for the purpose of making taxable supplies but not more than the tax imposed on the supply of the goods to the related person;

Input VAT is calculated as follows;An amount equal to seventy percent of the tax fraction of the lesser of-

The amount paid, orThe fair market value, including tax, 28

Second hand rule continued……..

Input tax deduction on Second hand goodsTax fraction being 15/115ExampleXYZ Autos Advertises sale of a second hand dump truck on 20/10/13Market value at 20/10/13 – EC$15,000.00Costs incurred to bring to sale – EC$1,200XYZ advertises dump truck for sale at-EC$17,000.00 (amount paid)

As per the Act Use the lesser of Amount paid Market valueAmount advertised 17,000.00Less costs incurred (1,200.00)

15,800.00 Lesser of: use market value

Selling price excluding VAT EC$15,000.00VAT charged (70%x15/115) = 9.13% 1,369.50

29

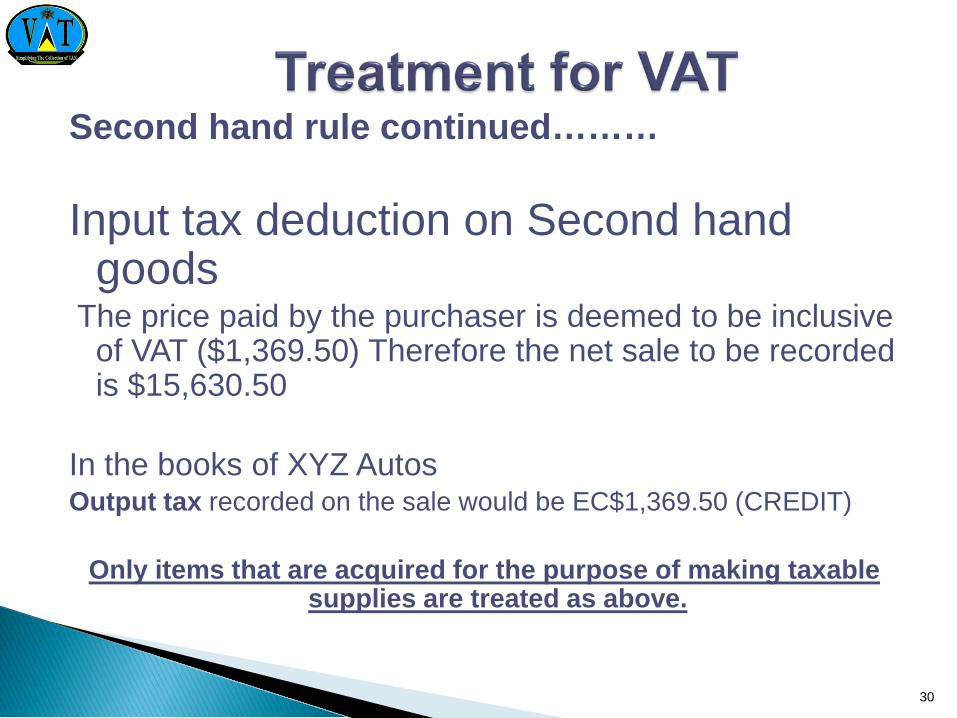

Second hand rule continued………

Input tax deduction on Second hand goods

The price paid by the purchaser is deemed to be inclusive of VAT ($1,369.50) Therefore the net sale to be recorded is $15,630.50

In the books of XYZ Autos Output tax recorded on the sale would be EC$1,369.50 (CREDIT)

Only items that are acquired for the purpose of making taxable supplies are treated as above.

30

Bad Debt\Recovery

Where a person grants supplies on credit the VAT is still due on these supplies. VAT liability is not affected by non-collection of payment for the supplies made during the tax period. The Act makes provision for relief to be granted where the tax was paid on a supply that has proven to be uncollectible.

Bad Debt relief will be granted at the discretion of the Comptroller where:

Reasonable efforts have been made by the supplier to recoup the outstanding debt.Evidence to show reasonable efforts is available ( credit control function)The debt is minimum 6 months oldProvisions have been made for bad debt in the accounts and the debt has been written off.

31

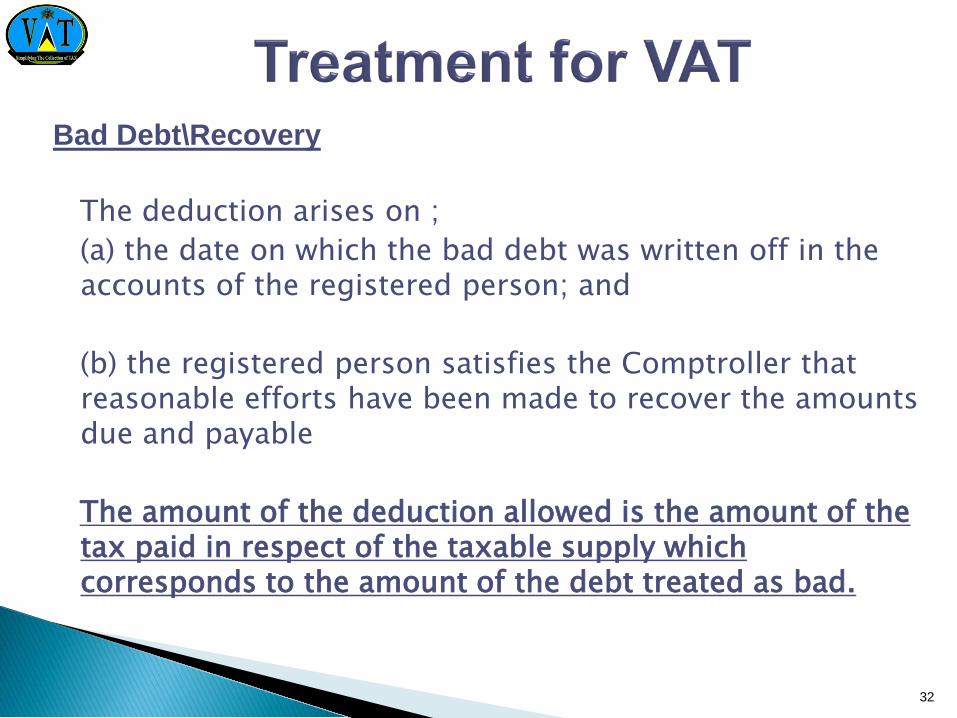

Bad Debt\Recovery

The deduction arises on ;(a) the date on which the bad debt was written off in the accounts of the registered person; and

(b) the registered person satisfies the Comptroller that reasonable efforts have been made to recover the amounts due and payable

The amount of the deduction allowed is the amount of the tax paid in respect of the taxable supply which corresponds to the amount of the debt treated as bad.

32

Time Of Supply

A supply of goods or services occurs on the earliest of the date on which:

The goods are delivered to the recipient or madeavailable or the performance of the services iscompleted;

An invoice for the supply is issued by the supplier; or

Any consideration for the supply is received by thesupplier.

33

Time Of Supply

Credit Agreements• Supply occurs on the date of commencement of the

agreement

Lay-a-way agreement• Supply occurs when the goods are delivered to the

recipient.

34

Time Of SupplyExample 1• Taxpayer A visits Taxpayer B’s warehouse on the 29/08/13 and pays

for the goods to be delivered to his place of business at a later date, an invoice is remitted to taxpayer A, dated 29/08/13 . The goods are delivered to Taxpayer A on the 02/09/13.

Supply took place on 29/08/13

Example 2 Taxpayer A requests a management report on credit from Taxpayer B

on 20/08/13, the report is delivered on 29/08/13. Invoice follows via post 5 days after the delivery date. Payment for these goods are made on 30/09/13.

Supply took place on 29/08/13

35

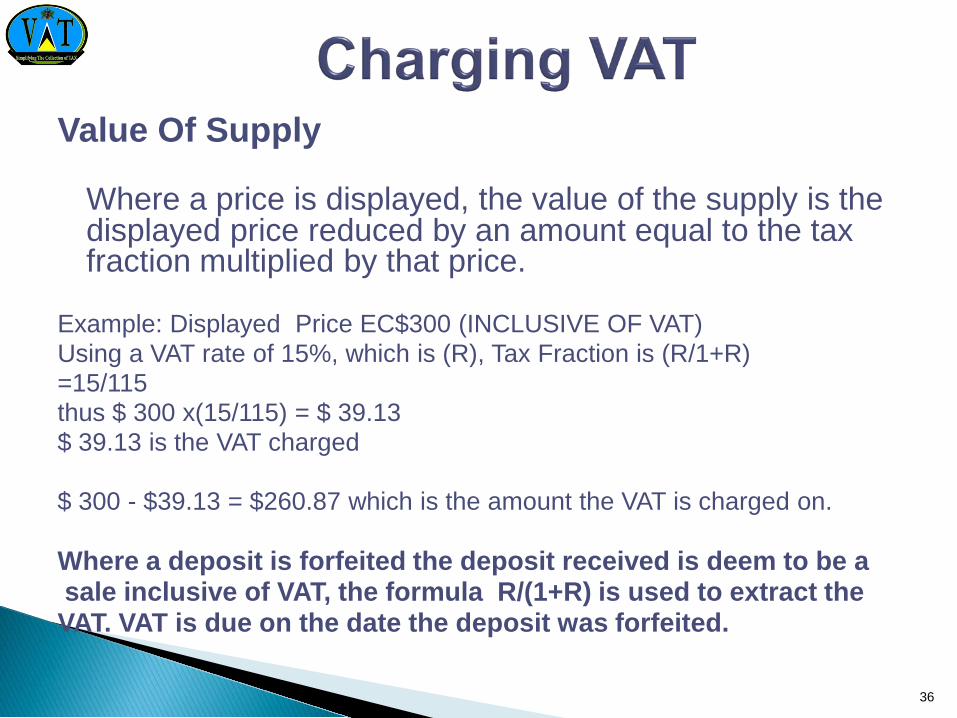

Value Of Supply

Where a price is displayed, the value of the supply is the displayed price reduced by an amount equal to the tax fraction multiplied by that price.

Example: Displayed Price EC$300 (INCLUSIVE OF VAT) Using a VAT rate of 15%, which is (R), Tax Fraction is (R/1+R) =15/115thus $ 300 x(15/115) = $ 39.13$ 39.13 is the VAT charged

$ 300 - $39.13 = $260.87 which is the amount the VAT is charged on.

Where a deposit is forfeited the deposit received is deem to be asale inclusive of VAT, the formula R/(1+R) is used to extract the VAT. VAT is due on the date the deposit was forfeited.

36

A registered taxpayer must:

• Issue a Tax Invoice to another registered taxpayer when a taxable supply is made.

•Issue a Sales Receipt when a supply is made to an unregistered business or final consumer.

•Display VAT-inclusive prices of goods and services

•Display VAT Registration Certificate prominently at all business locations

.

37

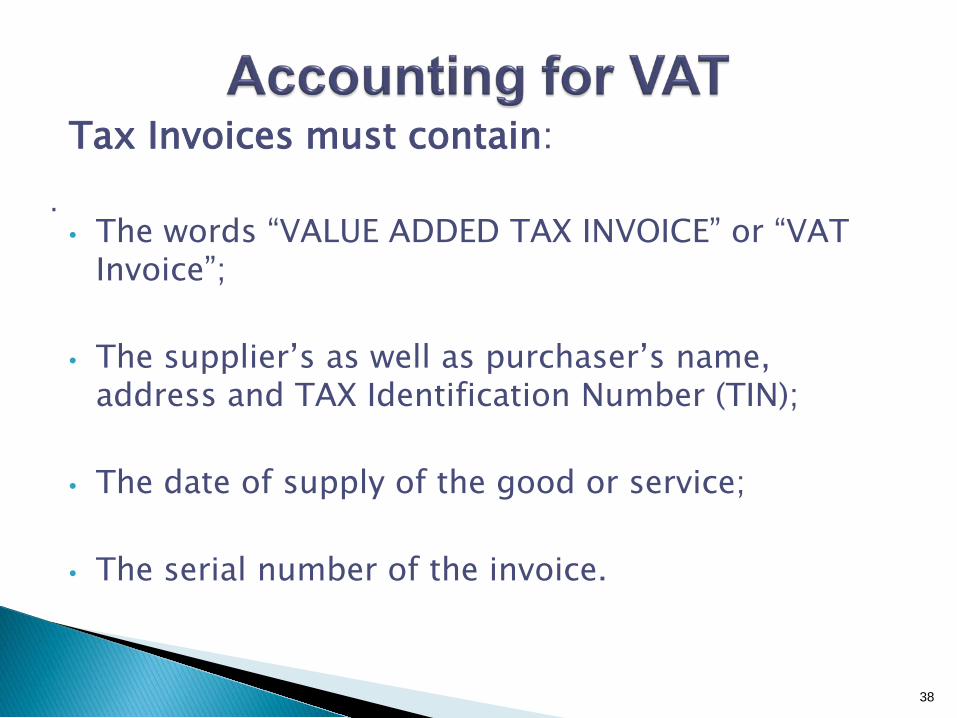

Tax Invoices must contain:

• The words “VALUE ADDED TAX INVOICE” or “VAT Invoice”;

• The supplier’s as well as purchaser’s name, address and TAX Identification Number (TIN);

• The date of supply of the good or service;

• The serial number of the invoice.

38

.

Tax Invoice

For each description, a registered person must include on the Tax Invoice;

Extent of the services Charge made, excluding VAT Rate of VAT Total Charge made, excluding VAT Each rate of VAT charged with the amount charged at

each such rate Rate of any cash discount offered Total VAT payable

39

VAT INVOICE INVOICE NO. 174 DATE: 11/11/2012

RADIO SUPPLIES LTD TIN - 9182021 ANY ROAD, CASTRIES

SOLD TO: A N OTTEN LTD TIN – 1234522 HIGH ROAD, CASTRIES

_____________________________________________________________________________________QTY DESCRIPTION/PRICE AMOUNT EXC. VAT VAT RATE VAT_____________________________________________________________________________________

6 RADIOS @ 25.20 151.20 15% 22.684 RECORD PLUGS @ 23.60 94.40 15% 14.166 LAMPS @ 15.55 93.30 15% 14.00

50.84

SUB-TOTAL 338.90TAX 50.84TOTAL 389.74

40

VAT INVOICE

41

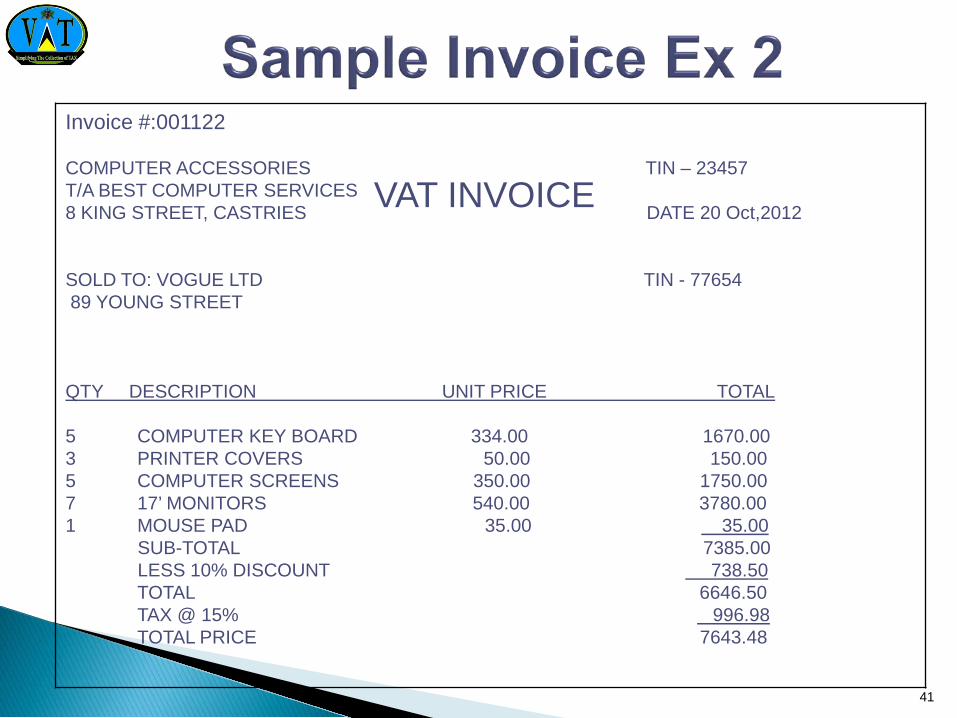

Invoice #:001122

COMPUTER ACCESSORIES TIN – 23457T/A BEST COMPUTER SERVICES8 KING STREET, CASTRIES DATE 20 Oct,2012

SOLD TO: VOGUE LTD TIN - 77654 89 YOUNG STREET

QTY DESCRIPTION UNIT PRICE TOTAL

5 COMPUTER KEY BOARD 334.00 1670.003 PRINTER COVERS 50.00 150.005 COMPUTER SCREENS 350.00 1750.007 17’ MONITORS 540.00 3780.001 MOUSE PAD 35.00 35.00

SUB-TOTAL 7385.00LESS 10% DISCOUNT 738.50TOTAL 6646.50TAX @ 15% 996.98TOTAL PRICE 7643.48

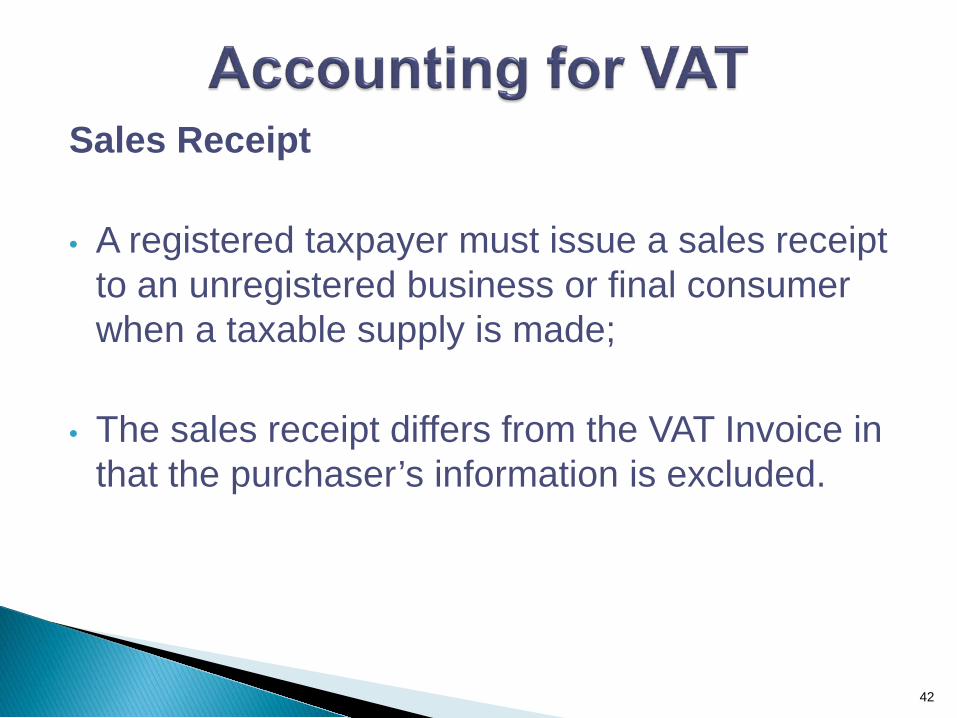

Sales Receipt

• A registered taxpayer must issue a sales receipt to an unregistered business or final consumer when a taxable supply is made;

• The sales receipt differs from the VAT Invoice in that the purchaser’s information is excluded.

42

SALES RECEIPT Sales Receipt NO. 101067 DATE: 11/09/2012

THE PERFUMERY PLUS LTD TIN - 9195521 MISTIQ ROAD, CASTRIES

______________________________________________________________________________QTY DESCRIPTION/PRICE AMOUNT EXC. VAT VAT RATE VAT______________________________________________________________________________

6 BOTTLES - COLOGNE @ 225.20 1,351.20 15% 202.681 CAMERAS @ 523.60 523.60 15% 78.543 BOTTLES – WHISKEY @ 133.66 400.98 15% 60.15

341.37

SUB-TOTAL 2,275.78 TAX 341.37TOTAL 2,617.15

43

SALES RECEIPT Sales Receipt NO. 101067 DATE: 11/12/2012

EVERY THING GOES LTD TIN - 19145THE LANE, GROS ISLET

______________________________________________________________________________QTY DESCRIPTION/PRICE AMOUNT EXC. VAT VAT RATE VAT______________________________________________________________________________1O LBS RICE @ 5.80 58.00 E 0.005 TINS MILK @ 3.45 34.50 E 0.001 CT FRESH EGGS @ 6.00 6.00 Z 0.006 BTLS WATER @ 2.00 12.00 15% 1.801 BTL PEPPER @ 9.00 9.00 15% 1.351 BTL WHISKEY @ 50.00 50.00 15% 7.50

10.65

SUB-TOTAL 169.50 TAX 10.65TOTAL 180.15

44

Keeping Records

It is important that a VAT registered business maintain complete, accurate and up to date records. This includes details of all supplies, purchases and expenses as well as a VAT Account.

Records should be kept, in English, in Saint Lucia for six(6) years after the end of the tax period to which they relate.

45

Keeping Records

A taxable person must maintain, in Saint Lucia and in English:

Original VAT invoices, Sales Receipts, VAT Credit notes and VAT debit notes received

A copy of all VAT invoices, VAT credit notes and VAT debit notes issued

Customs documentation relating to imports and exports

Accounting records relating to taxable activities carried on; and

Any other records as may be prescribed by Regulations

46

Keeping Records Annual Accounts including profit and loss accounts Bank statements and paying in slips Cash books and other account books Cheque book stubs duly completed Credit and debit notes issued or received Import and Export documentation Order and delivery books & records Purchases and sales books Purchase invoices and sales invoices A record of daily gross takings( e.g. cash register/till rolls) VAT account Any other relevant business correspondence

47

Keeping Records

Records may be kept manually, or computerized, however:

The figures that are used in the completion of the VAT return must be easy to find;

Invoices relating to the VAT return preparation should be filed in Chronological order (per month and invoice number order);

A VAT file should be kept with all working papers relating to the preparation of the VAT return.

48

The VAT Account is a summary of :

• The totals of the output VAT and input VAT for each tax period.

• It provides a link between the business records and the VAT return.

The information from the VAT Account can be used to complete the VAT return.

49

The VAT AccountExample:THE BUSINESS APPROACH LIMITED, ACCOUNT, October 1 – 30, 2012

INPUT VAT $ OUTPUT VAT $

VAT on imports 20 000 VAT on sales 50 000VAT on local purchases 10 000 VAT on goods - personal use 200VAT on business inputs 1 000 VAT on bad debts recovered 500VAT on services 3 000 VAT on credit notes received 300VAT on bad debt w/off 300VAT on credit notes given 100

TOTAL INPUT VAT 34 400 TOTAL OUTPUT VAT 51 000LESS: TOTAL INPUT VAT 34 400

NET VAT PAYABLE 16 600

50

Completing the Returns

• A VAT return is due and tax payable withintwenty-one calendar days after the end of theperiod in which you are reporting; i.e. Tax PeriodOctober 1- 30, 2012, is due by November 21,2012

• The totals on the return include total supplies ofservices; purchases and imports; input andoutput VAT; adjustments for bad debts as well ascredit and debit notes.

51

VAT Payable/Refunds

• An amount is due and payable where the Output VAT exceeds the Input VAT for a tax period;

• Where the Input VAT exceeds the Output VAT, a credit is available for carry forward for a period of three months, after which a claim may be made for a refund;

• Where more than fifty percent of taxable supplies is zero-rated (exports), a claim for refund can be made immediately on filing;

• A claim for a refund must be made within three years after the period to which it relates.

52

Non-compliance

Penalties will be applied for non-compliance with the VAT Act including:

• Failure to register;• Failure to display Registration Certificate;• Failure to provide invoices/sales receipts;• Failure to keep proper records;• Failure to pay net VAT due on time;• Failure to file VAT returns on time.

53

A person who —(a) issues a false VAT invoice or false sales receipt;(b) uses a false taxpayer identification number;(c) fails to provide a tax invoice, sales receipt, tax credit

note, or tax debit note;Is liable to a penalty of five thousand dollars for the first instance, ten thousand dollars for the second instance, fifteen thousand dollars for the third instance and twenty-five thousand dollars for the fourth and any subsequent instance.

54

Non-compliance A person who, for two or more consecutive or non-consecutive tax

periods, fails to file returns within the time and in the manner prescribed under the Act commits an offence and is liable on summary conviction to a fine not exceeding fifty thousand dollars (EC$50,000.00) or to imprisonment for a term not exceeding three years or to both.

Tax payable under the VAT Act which is not paid by the date upon which it becomes due and payable bears interest at the rate of one point two five per cent(1.25%) per month or part of a month for the period during which it remains unpaid.

A person who fails to file a return within the time required under this Act is liable to a penalty of two hundred and fifty dollars per month or part of the month, for the period during which the return remains unfiled.

55

56

A taxable person shall notify the Comptroller :

1. If he ceases to carry on a taxable activity/ies. (notify in writing within 5 working days)

2. If his taxable supplies fall below the threshold (only after the expiration of 2 years from the date of registration).

The Comptroller will cancel the registration with effect from the last calendar day of the tax period during which all such taxable activities ceased….

The taxable person must indicate whether or not he intends to carry on any taxable activity within 12 months from that date. (Comptroller will not cancel if taxable activity will resume within 12 months from the date).

57

The Comptroller will not cancel the registration if there are reasonable grounds to believe that the person will carry on taxable activity within 12 months from that date.

Comptroller may cancel registration if a taxable person:

1. Is not carrying on a taxable activity 2. was not required or entitled to apply for registration 3. has no fixed place of abode or business 4. has not kept proper accounting records relating to any business

activity carried on 5. has not submitted regular and reliable tax returns as required.

Notification of Change

A registered taxpayer must notify the IRD in writing within twenty-one days (21) days of:

(a) Any change in the particulars of the business provided in the application for registration; or(b)The closure of the business.

Examples of changes in particulars of registration include: Change of name or trade name or address; Change of place of business; Change of constitution; Change of nature of principal activity; or Any change in circumstances if the person ceases to operate or

closes on a temporary basis.

58

VAT Implementation Project Bridge StreetCastries468-1420vatcoordinator@vat.gov.lcvatinfo.vat.gov.lcwww.vat.gov.lc

![KINEO Street Legal price-list 2017 ... · KINEO Street Legal price-list 2017_00 Complete wheels retail price incl VAT[Euro]inside EU description disc carriers ... Ducati Hypermotard](https://img.dokumen.tips/doc/110x75/5ae06ce77f8b9ab4688d5429/kineo-street-legal-price-list-2017-street-legal-price-list-201700-complete.jpg)