Embed Size (px)

Citation preview

To identify service quality gaps in

banking sector: A comparative study of

public, private and foreign banks

2/28/2015 Indian Institute Of Social Welfare And Business Management By Mr.SAMIK DATTA And SENJUTI SARKAR

MBA Day 2013-15 Marketing (Major)/Finance (Minor)

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 1

Acknowledgment:

We, Ms. Senjuti Sarkar and Mr.Samik Datta, the students of marketing

specialization from Indian Institute of Social Welfare and Business Management

(IISWBM), Kolkata, want to take this opportunity to thank all those who have

extended their enthusiastic support in helping me to complete this endeavour.

This Dissertation of mine is concentrated on the fact of “Service Quality Gap

within public, private and foreign sector banks”. There are five major factors in

the “SERV QUAL” factors are there like tangibility, reliability, responsiveness,

assurance and empathy. In this process of research work I have tried to find out

the dependency of the total perceived service experience with respect to the five

“SERV QUAL” factors.

We would first like to convey our gratitude to the writer of the thesis, A Study on

customer Service Quality of Banks in India, Dr. Manasa Nagabhushanam, who is

also the Lead Researcher of Analyz Research Soultions Pvt. Limited for providing

us a platform from where the interest to work on this project has popped in my

mind. Many of the concepts have been an extension of her research work. Apart

from this I am thankful to our head of the department Dr. Tanima Ray Madam to

allow the opportunity to work on this project.

Thanking you in anticipation.

Date: 28/02/2015

Place: IISWBM, Kolkata

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 2

Institute certificate:

This is to certify that Mr. Samik Datta and Ms. Senjuti Sarkar, is a

bonafide student of the institute and has successfully completed his

dissertation project entitled ““Service Quality Gap within public, private and

foreign sector banks” for the fulfilment of the course MBA Day 2013-15

(Major: Marketing and Minor : Finance) from IISWBM, Kolkata.

---------------------------------------------

Prof. (Dr.) Tanima Roy

Head of the Department

MBA Day

IISWBM, Kolkata

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 3

Table of Contents

Abstract: ........................................................................................................... 4

Introduction: ..................................................................................................... 4

Role of banking sector in Indian Economy: .................................................... 5

Indian Banking Industry and Service Quality: ................................................. 7

Measuring service quality in banking sector: ................................................... 9

Objectives of the Study: ................................................................................... 11

Short-term objectives: ................................................................................... 11

Long-term objectives: ................................................................................... 11

Management Decision Problem: .................................................................. 11

Market Research Problem: ........................................................................... 11

Scope of the Study: .......................................................................................... 12

Limitations of the Study: ................................................................................. 13

Methodology of Study: .................................................................................... 13

A discussion about proper perceived service quality and shortfall in banking Industry with current examples: ....................................................................... 14

The current situations and 2013-2014 fiscal years: ......................................... 14

Research Statement and Data Collection: ......................................................... 17

Analysis of Data: ............................................................................................. 18

Primary Data Analysis: ................................................................................ 18

Recommendations and Conclusions:................................................................ 44

Further scope of extensive research: ................................................................. 45

Bibliography: ................................................................................................... 45

Appendix: ....................................................................................................... 45

Requisite documents: ................................................................................... 45

Questionnaire: ............................................................................................. 45

Response Sheets: .......................................................................................... 45

Important Table used for calculations: .......................................................... 45

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 4

Abstract:

Service quality is a comparison between expectations and performance. From

business administration view point , service quality is an achievement in customer service. It reflects at each service encounter. A customer's expectation for a

particular service is determined by, factors such as peer recommendations, personal needs and past experiences. The expected service and the perceived

service sometimes may not be equal, thus leaving a gap. The service quality model or the "GAP model" developed by the authors- Parasuraman, Zeithaml and Berry at Texas and North Carolina in 1985, highlights the main requirements for

delivering high service quality. It identifies "gaps" that cause unsuccessful delivery of service. Customers generally have a tendency to compare the service they

'experience' with the service they 'expect'. If the experience does not match the

expectation, there arises a gap.

Now in this process of finding the service quality gap we are actually trying to

realize that the five attribute have any effect on the total perceived quality or not. At the same time out motto is to find out how these five attribute dependency varies from one cluster of bank to another cluster, ranging from public to foreign

sector banks.

Therefore with this research we have tried to We will try to find out the service quality gap within the banking sectors. The comparison of the service quality gap

will be depicted between Public sector bank, private sector bank and foreign banks.

There will be also the analytical evidences that whether the five attributes like

tangibility, reliability, responsiveness, assurance and empathy has any effect to determine the overall service quality by the consumes or not.

Method of data collection is online. The data cleaning is done using methods of

mean replacement, clustering etc.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 5

Introduction:

Bank plays an important role in the economic development of a country. A

financial institution accepts deposits and channels those deposits into lending activities either directly or through capital markets. A bank connects customers

that have capital deficits to those customers with capital surpluses. The banking industry in India is facing certain challenges of quality service, customer

satisfaction, customer retention, customer loyalty; Quality service plays a major role in achieving customer satisfaction, and creating brand loyalty in banking sector.

Role of banking sector in Indian Economy:

The Government of India, after independence had to focus on many areas among

which one of the important tasks was economic development of the country. In this context, the industrial policy resolution in 1948 focused on mixed economy,

which played an active role in development of different sectors including banking and finance. A major step in this direction was the nationalization of banks in 1948. The Banking regulation Act was enacted which empowered the Reserve

Bank of India (RBI) to regulate, control and inspect the banks in India. In other words all the banks in India fell under jurisdiction of Reserve Bank of India under

the Banking Regulation Act.

The Government of India nationalized private banks in 1969 and later in 1980 in order to have better control over this sector. Government of India controls around

91% of the banking business in India. In early 1990‟s the prime minister of India P.V. Narshima Rao liberalized the sector by giving licence to small number of

private banks, which came to be known as new generation tech-savy banks. Among these banks were, Global Trust Bank (now Oriental Bank of Commerce), UTI (Now renamed as Axis Bank), ICICI Bank and HDFC Bank. The banking

sector of India constitutes government banks, private banks and foreign banks.

1. Mobilizing Saving for Capital Formation:

The commercial banks help in mobilizing savings through network of branch banking. People in developing countries have low incomes but the banks induce

them to save by introducing variety of deposit schemes to suit the needs of individual depositors. They also mobilize idle savings of the few rich. By

mobilizing savings, the banks channelize them into productive investments. Thus, they help in the capital formation of a developing country.

2. Financing Industry:

The commercial banks finance the industrial sector in a number of ways. They

provide short-term, medium-term and long-term loans to industry. In India they provide short-term loans. Income of the Latin American countries like

Guatemala, they advance medium-term loans for one to three years. But in Korea, the commercial banks also advance long-term loans to industry.

In India, the commercial banks undertake short-term and medium-term financing

of small scale industries, and also provide hire- purchase finance. Besides, they underwrite the shares and debentures of large scale industries. Thus they not only

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 6

provide finance for industry but also help in developing the capital market which is undeveloped in such countries.

3. Financing Trade:

The commercial banks help in financing both internal and external trade. The banks provide loans to retailers and wholesalers to stock goods in which they deal. They also help in the movement of goods from one place to another by providing

all types of facilities such as discounting and accepting bills of exchange, providing overdraft facilities, issuing drafts, etc. Moreover, they finance both

exports and imports of developing countries by providing foreign exchange facilities to importers and exporters of goods.

4. Financing Agriculture:

The commercial banks help the large agricultural sector in developing countries in

a number of ways. They provide loans to traders in agricultural commodities. They open a network of branches in rural areas to provide agricultural credit.

They provide finance directly to agriculturists for the marketing of their produce, for the modernisation and mechanization of their farms, for providing irrigation facilities, for developing land, etc.

They also provide financial assistance for animal husbandry, dairy farming, sheep breeding, poultry farming, pisciculture and horticulture. The small and marginal farmers and landless agricultural workers, artisans and petty shopkeepers in rural

areas are provided financial assistance through the regional rural banks in India. These regional rural banks operate under a commercial bank. Thus the

commercial banks meet the credit requirements of all types of rural people.

5. Financing Consumer Activities:

People in underdeveloped countries being poor and having low incomes do not possess sufficient financial resources to buy durable consumer goods. The

commercial banks advance loans to consumers for the purchase of such items as houses, scooters, fans, refrigerators, etc. In this way, they also help in raising the

standard of living of the people in developing countries by providing loans for consumptive activities.

6. Financing Employment Generating Activities:

The commercial banks finance employment-generating activities in developing

countries. They provide loans for the education of young person‟s studying in engineering, medical and other vocational institutes of higher learning. They

advance loans to young entrepreneurs, medical and engineering graduates, and other technically trained persons in establishing their own business. A number of commercial banks in India is providing such loan facilities. Thus, the banks not

only help inhuman capital formation but also in increasing entrepreneurial activities in developing countries.

7. Help in Monetary Policy:

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 7

The commercial banks help the economic development of a country by faithfully following the monetary policy of the central bank. In fact, the central bank

depends upon the commercial banks for the success of its policy of monetary management in keeping with requirements of a developing economy.

Thus, the commercial banks contribute much to the growth of a developing

economy by granting loans to agriculture, trade and industry, by helping in physical and human capital formation and by following the monetary policy of

the country.

Indian Banking Industry and Service Quality:

There are varieties of services offered by Indian banking industries and most of

them are related to financial services. The modes of providing services are either B2B or B2C or B2G. The major services that bank can provide to its customers

are as follows:

Current Account

ATM Cards & Laser Cards

Savings account

Investments

Credit Card

Insurance

Mortgage

Online banking

Pension

Now we will discuss the effectiveness of these services in human life:

Current Account:

A Current Account is a common type of bank account which is used to store money, which is needed on a regular basis. It is a useful way to manage your

money in the short-term. It allows us to:

Receive money such as our salary or other types of income.

Withdraw cash by using our ATM (Automated Teller Machine) or Laser Card at the bank counter.

Pay for things using our Laser Card or by writing cheques

We can transfer money to other accounts.

Bank using the internet or the telephone.

We can pay bills.

Till date the current account service provided by Indian banks mostly in B2B

transactions.

Savings Account:

Savings accounts are a type of bank, building society, credit union or An post

account that is used for accumulating money. Funds saved can be for both short and long-term needs.

Short-term needs include things like holidays, weddings and short term

investments.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 8

Longer-term needs include things like saving for car purchase or a house. There are many different types of savings accounts available.

Generally speaking, savings accounts can be opened with a small sum of

money and you can save either regular amounts or lumps sums, or sometimes both.

A Savings Account accumulates interest which actually increases the fund

value. Interest rates can be either fixed or variable.

The Government charges DIRT (Deposit Interest Retention Tax) on the interest earned on savings. This tax is automatically taken from your account.

ATM Cards & Laser Cards:

ATM Cards are used to withdraw cash from our current or savings

account

We can use our ATM card abroad so long as our card has a Link logo on the back.

We can use our ATM card at any banks‟ ATM machines

Using cash Laser Cards (also known as Debit Cards) allow us to pay for

items at POS (Point of Sale) terminals in most shops, restaurants, and now even in some taxis.

Some retailers will give us the option of receiving “cash back”, the amount

of which is added to the transaction on our laser card.

Investments:

Investment involves purchasing a financial product or other item of some specified value with the expectation that the value of the item will increase over time. Simply put, investment means spending money in the hope of making more

money.

Investments can offer us a better return on our money in the longer-term compared to savings accounts. However, certain investments may carry a higher

level of risk.

Credit Card:

Credit cards are usually a “pay later” concept as they let us purchase an item and pay for it sometime in the future.

VISA, MasterCard, Maestro are the two main types of Credit Card in India.

Credit cards are mainly provided by banks, but some retailers and airlines also

provide their own credit cards.

According to financial rule in India a person must be 18 years or over to use a Credit Card.

Insurance:

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 9

Insurance is a form of risk management – you pay a set amount called a premium to an insurer and the insurer agrees to cover the costs associated with certain risks

that could be financially devastating if they were to happen. There are a number of different types of insurance including:

Car Insurance

By law if we have a car we must have third party insurance. Third party insurance

covers any injury or loss suffered by other people as a result of our driving. Comprehensive insurance is an “all inclusive” type of insurance that covers the

cost of repair or replacement if our car is stolen, damaged or destroyed and includes any loss suffered by Third parties.

Home Insurance

Some of the risks your home may be subject to include damage by fire or flooding,

burglary or someone injuring themselves on your property. Taking out insurance can cover you for some of these risks.

Travel Insurance

There are many risks associated with travel including damage or delay of luggage, cancelled flights, delayed or missed departure, loss or theft of money or passport

and illness or injury. Travel insurance can help compensate us in the eventuality of these things happening.

Health Insurance

Private health insurance helps us to cover medical or hospital expenses if we or

our family get sick, have and accident or need an operation.

Payment Protection insurance

Payment Protection insurance is designed to cover our repayments on a loan if we

suffer from an accident, illness, death or redundancy.

Mortgage:

Mortgage is a special type of loan offered by banks and building societies which enable people to buy properties. It‟s typically a big loan, paid back by the

borrower over 25 or 30 years, in monthly installments.

Some different types of Mortgages are:

Mortgage

This is the most common type of mortgage. The monthly repayment consists of

the original loan amount (or capital repayment) and the interest payment. At the beginning of the mortgage‟s life, most of the monthly repayment goes towards the interest. Towards the end, more of the monthly payment goes towards the capital

repayment.

Interest-only mortgage

With this type of mortgage the monthly repayment only covers the interest on the mortgage and not the capital. The original loan must be repaid in a lump sum

at the end of the mortgage term.

Measuring service quality in banking sector:

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 10

Service quality has been identified as a critical success factor for a organization to build their competitive advantage and increase their competitiveness. Pioneering

work by Parasuraman (1985) and led to a list of ten determinants (reliability; responsiveness; competence; access; courtesy; communication; credibility;

security; understanding the customer; and tangibles) of service quality as a result of their focus group studies with service providers and customers which subsequently resulted in the development. But among all these ten factors only

five are the main determinant of the quality and they are tangibility, reliability, responsiveness, assurance and empathy.

(1)Tangibles, which pertain to the physical facilities, equipment, personnel and communication materials; Parasuraman (1985) defined tangibility as the appearance of physical facilities, equipment, personnel, and written materials.

Ananth referred to tangibility in their study of private sector banks as modern looking equipment, physical facility, employees are well dressed and materials are

visually appealing.

(2)Reliability, which refers to the ability to perform the promised services dependably and accurately; Reliability depends on handling customers' services

problems; performing services right the first time; provide services at the promised time and maintaining error-free record. Furthermore, they stated reliability as the most important factor in conventional service .Reliability also

consists of accurate order fulfillment; accurate record; accurate quote; accurate in billing; accurate calculation of commissions; keep services promise. He also

mentioned that reliability is the most important factor in banking services

(3)Responsiveness, which refers to the willingness of service providers to help customers and provide prompt service; Responsiveness defined as the willingness

or readiness of employees to provide service. It involves timeliness of services. It is also involves understanding needs and wants of the customers, convenient

operating hours, individual attention given by the staff, attention to problems and customers. safety in their transaction.

(4)Assurance, which relates to the knowledge and courtesy of employees and

their ability to convey trust and confidence; Parasuraman et al. (1985) defined assurance as knowledge and courtesy of employees and their ability to inspire trust and confidence. According to Sadek et al. (2010), in British banks assurance

means the polite and friendly staff, provision of financial advice, interior comfort, eases of access to account information and knowledgeable and experienced

management team.

(5)Empathy, which refers to the provision of caring and individualized attention to customers; Parasuraman et al. (1985) defined empathy as the caring and

individual attention the firm provides its customers. It involves giving customers individual attention and employees who understand the needs of their customers

and convenience business hours. Ananth et al. (2011) referred to empathy in their

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 11

study on private sector banks as giving individual attention; convenient operating hours; giving personal attention; best interest in heart and understand customer.s

specific needs.

While consumes comes to the banks these are the basic qualities they always look for. Now in general as per the general perseverance of the customer the

perceptions are as follows:

For Public Sector Banks, the domains of tangibles are very poor, banks are reliable, and responsiveness is optimal, assurance is high and empathy is least.

For Private Sector Banks, the domains of tangibles are very high, reliability is at

the low ebb, and responsiveness is high, assurance is optimal and empathy is extraordinary.

For Foreign Banks, the domains of tangibles are very high, reliability is high, and

responsiveness is very quick, assurance is maximum and empathy is up to the mark.

Objectives of the Study:

Short-term objectives:

The short term objective of this research paper is:

To find out the factors that has an impact on the perceived qualities of the

services in different clusters of banking sectors within India.

To find out the Strength, Weakness, Opportunities and Threat of different banking cluster one with respect to another.

To investigate the all the policies of different banking and how the different

clusters of banks implement these policies while delivering their services.

Long-term objectives:

To establish best service qualities barring the different clusters.

To reduce competitive rivalry and increase the service dependencies between the different clusters of banks.

To induce healthy competition with respect to best service delivery between all the clusters.

Management Decision Problem:

What are the service gaps in the banking Industry?

Market Research Problem:

What are the pot holes in the service process of Public sector Banks in India?

What are the deficient alongside the service provided by Private Sector Banks in India?

What are the service quality gaps for foreign sector bank in India?

What are the challenges Foreign banks are facing while penetrating Indian soil?

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 12

Scope of the Study:

This study can be incorporated to study or research the following domains, like:

1. A comparative study between Indian Public, Private and Foreign sector

banks:

The dissertation project can give a comparative idea that that how the individual banks are performing in intra and inter group

banking market.

Suppose someone needs a comparative analysis between the service quality between two market leaders like SBI and ICICI bank or

Canara Bank and HDFC bank, and then the information of this study will be helpful.

The threat that the public, nationalized and private sector banks are

facing due to the presence of foreign sector banks.

The nascent sectors of Indian banking industry.

Scope of market penetration for all the clusters of banks.

2. Current status of Indian Banking industry:

Introduction of Liberalization Privatization and Globalization (LPG) in

Indian economy has affected almost all the sectors and industries of the economy. Indian banking industry is no exception to that. The net result of

such policy initiatives has been increased competition at the marketplace. The fight for customers has got intensified. Literatures establish a direct

link between service quality and marketing performance of banks thus concluding that loyal customer base can only be created through superior service. Hence effectiveness of service quality of banks is largely being

tested to forecast the marketing performances of the banks. It has also been seen that degree and effectiveness of service quality has been said to be

different in case of public and private sector bank.

This study will clarify the process like followings:

Test of Tangibility

1. Does the bank have modern looking equipment?

2. Are the bank's receptions desk employees neat appearing?

Test of Reliability

1. When the bank promises to do something by a certain time, it does so

2. When you have a problem, the bank is sympathetic and reassuring

3. Are the employees in the bank area polite with you?

Test of responsiveness:

1. Do the Employees in the bank give your prompt service?

2. Are employees in the bank always willing to help you?

Test of Assurance:

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 13

1. Does the behavior of employees in the bank instill trust in you?

2. Do you feel safe in your transactions with the bank?

3. Do the employees in the bank have the knowledge to answer your

questions?

Test of Empathy:

1. Do the employees of the bank understand your specific needs?

2. Does the bank have operating hours convenient to all its customers?

3. Does the bank have your best interest at heart?

3. Where will you invest to get the best return?

Which bank should you use for the purpose of investment?

What does the consumer feel for, prior to investing in a bank?

How others are feeling about the service quality of the three clusters of banks

4. Customer Relationship Management and its realistic analysis using the

banking clusters in India.

Approaches and service delivery pattern of all the clusters towards the banking sector.

Limitations of the Study:

The Study is based on the response of only forty two responses.

The post data cleaning sample size is 31.

Some people have answered in biased way.

The survey is based on online survey method only.

Diversified responses.

Very short response time.

Short Duration of research work (only 30 days).

Lack of capital (both financial and resource).

Methodology of Study:

Defining the research problem, here the aim was to find out the condition

of banking sectors which deals in the consumer service.

The first objective of knowing the current market scenario is studied using

the methodology of taking responses from the consumers.

The secondary data from the websites and the informations and contact

numbers of the big players of the sector in and around Kolkata was one of

the prime methodologies of primary data collection.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 14

From the collected data of the sector and it is client market clusters are

made divided and the required graphical representations are made.

After that each cluster of public, private and foreign banks perceived and

expected qualities are calculated using regression analysis.

The guidelines and rules of RBI are used to find out the expected amount

of credit need of individual organization.

A discussion about proper perceived service quality and shortfall in

banking Industry with current examples:

India is a country where the whole industry depends upon the banking sector.

Most of the capital requirement and capital budgeting is done by the banks under

the guidance of RBI. With the potential to become the fifth largest banking industry in the world by 2020 and third largest by 2025 according to KPMG-CII

report, India‟s banking and financial sector is expanding rapidly. The Indian Banking industry is currently worth Rs. 81 trillion (US $ 1.31 trillion) and banks

are now utilizing the latest technologies like internet and mobile devices to carry out transactions and communicate with the masses. The Indian banking sector consists of 26 public sector banks, 20 private sector banks and 43 foreign banks

along with 61 regional rural banks (RRBs) and more than 90,000 credit cooperatives.

Factors promoting growth of Banking and Financial Services

The Banking Laws (Amendment) Bill that was passed by the Parliament in 2012 allowed the Reserve Bank of India (RBI) to make final guidelines on issuing new bank licenses. Moreover, the role of the Indian Government in expanding the

banking sector is noteworthy. It is expected that the new guidelines issued by RBI will curb practices of impish borrowers and streamline the loan system in the

country. In the coming time, India could see a rise in the number of banks in the country, a shift in the style of operation, which could also evolve by incorporating

modern technology in the industry.

Another emerging trend witnessed by the banking sector is the use of social media platform like Facebook to attract customers. In September 2013 ICICI bank launched a Facebook bill payment and fund transfer service called „Pockets‟ for

customer convenience.

According to a report by Zinnov, a Globalization and Market Expansion firm, „IT adoption in BSFI sector in India‟, the Information Technology Industry spend in

BFSI vertical is expected to reach USD 3.5 billion by Financial Year 2014. The study also highlighted „the growing maturity of Indian BFSI organizations in IT

adoption, as technology is seen as a driver of business value. Technology firms have great potential to explore in the BFSI sector, which contributes to eight per

cent of India's Gross Domestic Product.‟

The current situations and 2013-2014 fiscal years:

Global growth did not recover as expected across most major developed and

rapid-growth economies in 2013-14. During the year gone by, the central bankers

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 15

across the globe took decisive steps to restore confidence in markets and broader economy. In Europe, the banking situation improved in part due to the long-term

refinancing operations of the European Central Bank (ECB), which helped ensure there was plenty of liquidity in the system. In the US, the picture was more upbeat

but still mixed. And although businesses and consumers started to borrow again, credit growth remained tepid. The global economic environment broadly strengthened, and is expected to improve further, with much of the growth

impetus emanating from advanced economies. There was acute financial volatility in emerging market economies, and increases in the cost of capital which

dampened investments and weighed on growth.

The banking sector, being the barometer of the economy, is reflective of the macro-economic variables. While the Indian economy is yet to catch strength, the

Indian banking system continues to deal with improvement in asset quality,

execution of prudent risk management practices and capital adequacy.

The Reserve Bank of India (RBI) maintained a status quo in interest rate since

January 2014. However, despite the retail inflation softening in recent periods, it'll be a little while before the Central Bank would opt for rate cut.

Indian banking industry, with total asset size of Rs 81 trillion (USD 1.34 trillion),

is expanding continuously but on a cautious note. The fact that the industry is plagued by bad loans, the lenders have chosen to go slow in terms of credit off take. Fiscal 2014 saw a combination of various external and internal events that

kept markets turbulent, interest rates high and investor confidence low, resulting in shrinking investment and GDP growth.

The key words that prevails the service quality in Indian Banking cluster:

Supply: The process of liquidity is controlled by Reserve Bank of India(RBI).

Demand: India is a growing economy and demand for credit is high through it could be cyclical.

Barrier to entry: The main barrier to entry is licensing requirement, investment in technology and branch network, capital and regulatory requirements.

Bargaining power of supplies: This power is high during periods of tight

liquidity. Trade union in public sector banks can be anti-reforms and orchestrate strikes.

Bargaining power of customers: For good creditworthy borrowers bargaining

power is high due to the availability of large number of banks.

Competition: High- There is public sector banks, private sector and foreign banks along with non-banking finance companies competing in similar business

segments. Plus the RBI is all set to issue new banking licenses soon.

The Achievements and Agendas of Financial Year '14:

India's underlying economic growth trends remained weak during FY14. High and persistent inflation remained a key macroeconomic challenge facing India throughout the FY14.

During the year, the operating environment for the banking system continued to be challenging with persistent high inflation, muted growth, slowdown in credit

off-take, concerns over higher non-performing assets and a high incidence of restructured assets.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 16

Against the backdrop of a slowdown in the domestic economy and tepid global recovery, the growth of Indian banking sector too remained under pressure in

FY14. That said, the deposit and credit growth was marginally better than that in FY13. The growth in deposits of scheduled commercial banks (SCBs) at 14.6% in

FY14 was marginally better than the growth at 14.2% in the previous financial year. However, this growth came on the back of the liberal policy adopted by the RBI towards non-resident Indian deposits. The credit growth at 14.3% in FY14

too was marginally better than that at 14.1% in FY13. As a part of monetary transmission, base rate of major banks inched up from 9.70%-10.25% in April

2013 to 10.0% -10.25% in March 2014, while deposit rates were readjusted from 7.5%-9.00% to 8.0%-9.25% in the same period.

In FY14, private sector lenders experienced significant growth in credit cards and personal loan businesses.

Owing to elevated inflation levels, the banks were compelled to offer

attractive interest rates on their term deposits so as to protect their liability franchise. The higher deposit rates coupled with lower credit off take impacted the

net interest income and thereby the earnings profile of commercial banks. Additionally, the macroeconomic challenges and poor repayment capacity of

borrower's deteriorated the banks' asset quality further in FY14. Consequently, the restructured assets moved north during the year. However, despite the challenging environment, few banks with prudent risk management systems and the ones with

robust cash recovery delivered a sound performance during FY14.

The aggregated profit after tax (PAT) of PSBs declined by 27% YoY during FY14. The gross NPAs of banks (PSBs + private) increased over the last

one year from 3.3% to 3.9% as on March 2014. Restructured advances of the PSBs remain at elevated levels of 6.2% as on March 31, 2014. Private sector banks

were able to hold on good asset quality as reflected in their gross NPAs of 1.8% as on March 2014. Banks started reporting capital adequacy as per Basel III norms

since June 2013. The Tier 1 capital of PSBs stood at around 8.6% as on March 31, 2014 as against the required Tier 1 capital of 6.5%, while that of private sector banks was well above the norms around 12.8%. Return on net worth for PSBs

dropped to single digit in FY14. (data taken from: RBI, ET and

www.equitymaster.com)

Prospects of FY 2015-16

While the medium term prospects point towards an improving growth scenario, given the improved macroeconomic fundamentals it is highly likely that there will

only be a modest economic recovery in FY15.

o That said, the Indian economy is now on the threshold of a major

transformation, with expectations of policy initiatives by the change in guard at the Centre. Positive business sentiments, improved

consumer confidence and more controlled inflation should help boost the economic growth. With a new and stable Government in

place now, a clear revival in the investment climate is sure to come.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 17

o Higher spending on infrastructure, speedy implementation of projects and continuation of reforms will provide further impetus to

growth. A moderate recovery is likely to be seen in FY15 and the real GDP is expected to grow by 5.3%-5.5%. While the CPI

inflation is expected to remain an important challenge for India, it should witness a downward trajectory during the major part of FY15

o The worst seems to be over for the Indian banking industry, as there will be increased clarity on macroeconomic and political fronts

during FY15. On the positive side, liquidity remains steady, inflation is expected to move downwards for the major part of

FY15 and the RBI is in full control to manage any volatility. Macroeconomic improvements and potential for post-election

reforms should see a gradual reduction in stressed loans on lower

slippages and higher recoveries. Recovery in macroeconomic environment and expected revival in economic growth will help to

mitigate risks and resolve problems of asset quality. o Not just that, the banking industry may see more participants and

greater healthy competition. Two new banks have already received licences from the RBI i.e. IDFC and Bandhan Group, which apart from providing impetus to financial inclusion, is expected to

intensify competition in the banking sector in the medium term. In addition, by postponing the implementation of Basel III capital

norm by one year, RBI has given some breathing space to banks struggling with stressed margins and lower profitability on account

of increase in NPAs. The RBI's new norms will further encourage banks to identify potential bad loans and take corrective actions.

o The overall credit growth may revive marginally at 14-15% in FY15; private sector banks may continue to outpace PSBs in credit growth. Overall (PSBs + private banks) gross NPAs could remain at

4-4.2% by FY15 as against 3.9% in FY14. o Banks need to raise capital of Rs. 1.8-2 trillion over the next two

years (FY15-FY16); of which 45-50% may be issued in the form of additional Tier 1, 35-40 % through Tier II and balance through

common equity. However, if there are no seekers for additional Tier 1 capital instruments, Indian banks may need to mop up Rs. 1-1.3 trillion common equity capital over the next two years as

mentioned by a rating agency report.

Research Statement and Data Collection:

We will try to find out the service quality gap within the banking sectors. The comparison of the service quality gap will be depicted between Public sector bank,

private sector bank and foreign banks.

There will be also the analytical evidences that whether the five attributes like tangibility, reliability, responsiveness, assurance and empathy has any effect to

determine the overall service quality by the consumes or not.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 18

Method of data collection is online. The data cleaning is done using methods of mean replacement, clustering etc.

Analysis of Data:

There were six major questions that is being asked in the questionnaire and those

are:

The rating (1 to 5) the respondent want to provide for the “Total perceived or

experienced service quality” which he/she experienced while dealing with

public, private or foreign sector banks individually.

The rating (1 to 5) the respondent want to provide regarding the quality for the

“perceived or experienced with respect to Tangibility” which he/she experienced

while dealing with public, private or foreign sector banks individually.

The rating (1 to 5) the respondent want to provide regarding the quality for the

“perceived or experienced with respect to Reliability” which he/she experienced while dealing with public, private or foreign sector banks individually.

The rating (1 to 5) the respondent want to provide regarding the quality for the

“perceived or experienced with respect to Responsiveness” which he/she experienced while dealing with public, private or foreign sector banks individually.

The rating (1 to 5) the respondent want to provide regarding the quality for the

“perceived or experienced with respect to Assurance” which he/she experienced while dealing with public, private or foreign sector banks individually.

The rating (1 to 5) the respondent want to provide regarding the quality for the

“perceived or experienced with respect to Empathy” which he/she experienced while dealing with public, private or foreign sector banks individually.

There was also another format of question where the respondents have to tell us

their total expectation from the service received from any particular cluster of banks in a scale rating of 5.

Primary Data Analysis:

We have divided our analysis in four different strata.

1. The Analysis of the data collected for the public sector banks.

A. The descriptive analysis of the collected data using descriptive

statistics

B. The Inferential analysis of the collected data using inferential statistics.

2. The Analysis of the data collected for the private sector banks.

A. The descriptive analysis of the collected data using descriptive

statistics

B. The Inferential analysis of the collected data using inferential statistics.

3. The Analysis of the data collected for the foreign sector banks.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 19

A. The descriptive analysis of the collected data using descriptive statistics.

B. The Inferential analysis of the collected data using inferential

statistics.

4. Comparative study of public, private and foreign sectors banks.

The Analysis of the data collected for the public sector banks:

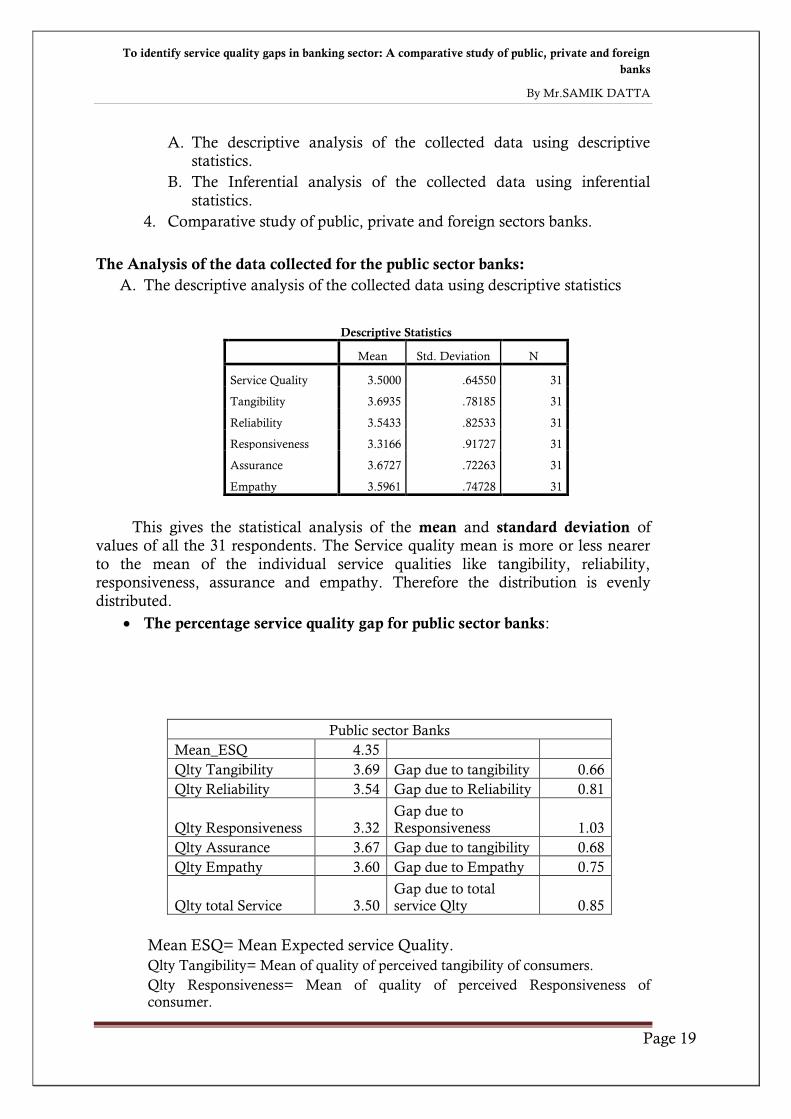

A. The descriptive analysis of the collected data using descriptive statistics

Descriptive Statistics

Mean Std. Deviation N

Service Quality 3.5000 .64550 31

Tangibility 3.6935 .78185 31

Reliability 3.5433 .82533 31

Responsiveness 3.3166 .91727 31

Assurance 3.6727 .72263 31

Empathy 3.5961 .74728 31

This gives the statistical analysis of the mean and standard deviation of values of all the 31 respondents. The Service quality mean is more or less nearer

to the mean of the individual service qualities like tangibility, reliability, responsiveness, assurance and empathy. Therefore the distribution is evenly

distributed.

The percentage service quality gap for public sector banks:

Public sector Banks

Mean_ESQ 4.35

Qlty Tangibility 3.69 Gap due to tangibility 0.66

Qlty Reliability 3.54 Gap due to Reliability 0.81

Qlty Responsiveness 3.32 Gap due to Responsiveness 1.03

Qlty Assurance 3.67 Gap due to tangibility 0.68

Qlty Empathy 3.60 Gap due to Empathy 0.75

Qlty total Service 3.50 Gap due to total service Qlty 0.85

Mean ESQ= Mean Expected service Quality.

Qlty Tangibility= Mean of quality of perceived tangibility of consumers.

Qlty Responsiveness= Mean of quality of perceived Responsiveness of consumer.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 20

Qlty Assurance= Mean of quality of perceived Assurance of consumer.

Qlty Empathy= Mean of quality of perceived Empathy of consumer.

Qlty total Service= Mean of quality of perceived total Service of consumer.

Analysis of the service quality gap with respect to the age range of the

respondants:

We have taken the age range of the respondents ranging between:

15 years to 25 years

26 years to 40 years

41 years to 60 years

More than 60 years

On the other hand the service quality gap has been catehories as:

Maximum ranging data is 0.50 and minimum ranging data is -2.0.

High = The service quality is satisfactory ( gap ranging from 0 to 0.50).

Medium= The service quality is optimum ( gap ranging from 0.0 to -1.00).

Low = The service quality is dis-satisfactory ( gap ranging from -1.00 to -

2.00).

The representation is as follows:

Age range

15-25 26-40 41-60

61-

above

Service

Quality

Gap

High 1 0 1 0 2

Medium 3 6 1 0 10

Low 2 11 5 1 19

6 17 7 1 31

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 21

Graph: 1

Analysis of the service quality gap with respect to the income group range of the respondants:

We have taken the income range of the respondents ranging between: > Rs.60,000 Per Annum Rs.60,001 to Rs. 2,00,000 Per Annum

Rs. 2,00,001 to Rs. 4,00,000 Per Annum Rs. 4,00,001 to Rs. 8,00,000 Per Annum

More than 8,00,001 Per Annum On the other hand the service quality gap has been catehories as:

Maximum ranging data is 0.50 and minimum ranging data is -2.0.

High = The service quality is satisfactory ( gap ranging from 0 to 0.50).

Medium= The service quality is optimum ( gap ranging from 0.0 to -1.00).

Low = The service quality is dis-satisfactory ( gap ranging from -1.00 to -2.00).

The representation is as follows: Graph: 2

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 22

The result we can conclude from the graphs are as follows:

Graph1 : The people within the age range 26-40, who are mostly professional

people, they have expericened low service qulaity and therefore for public sector

banks there is a big gap between the perceived and expected quality of service.

Same conclusion for age range of 41-60 years.

Graph 2 : As a whole the inference is most of the consumers irrespective of the

income level ladged a negative perceived value again the service quality, therefore, for all kind of Income range public sector banks are providing least

satisfactory services.

B. The Inferential analysis of the collected data using inferential statistics.

I. Correlation Matrix:

II. Variables Entered/Removed

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 23

Model

Variables Entered Variables

Removed

Method

1

Empathy,

Assurance,

Responsiveness,

Tangibility,

Reliablityb

. Enter

a. Dependent Variable: Service Quality

b. All requested variables entered.

III.

Model Summaryb

Model R R Square Adjusted R

Square

Std. Error of the Estimate

1 .971a .942 .931 .16985

a. Predictors: (Constant), Empathy, Assurance, Responsiveness, Tangibility, Reliability

b. Dependent Variable: Service Quality

This part gives the information that whatever regression model we are creating that has

94.2 % reliability. That means with this sample data we can explain 94.2% of the model.

IV.

The ANNOVA table also defines that the mean of the regression and residual are

not equal. So going with the dependency relationship.

V. The Linear Regression co-efficient:

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 24

Now this is the linear regression coefficients and the t-test significance representation. Interpreting the results we can get the following conclusions:

The regression equation contains in Y axis or dependable variable as

“Total experienced service quality” of the consumers and the independent X axis variables are: Tangibility, reliability, responsiveness, assurance,

empathy qualities as per the consumer response. Now, we will examine whether there is at all any dependency between the five variables over the

„service quality‟ that the consumers are getting.

Analysing the result we can infer that except tangibility all the other attribute have the significance level less than 0.05, so those

attributes have effect on the experienced service quality level.

The regression equation would be:

Y =.182+.112X1+.208X2+.222X3+ .222X4+.172X5

X1= the experienced Service quality due to tangibility.

X2= the experienced Service quality due to reliability.

X3= the experienced Service quality due to responsiveness.

X4= the experienced Service quality due to assurance.

X5= the experienced Service quality due to empathy.

Y= Experienced Service Quality.

Apart from this, within unstandardized coefficients all the B values are greater than standard error value, which signifies there is a better interdependency between the Y and X value and also intra data X

relations are there. And of course the with 94.2% reliable model.

Therefore we can conclude that there is direct effect of tangibility, reliability, responsiveness, assurance and empathy over the service quality.

Now the standardise residual and service quality forms a histogram which gives rise to a normal distribution, which signifies the accuracy of the data set.

The graph is depicted below:

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 25

DESCRIPTIVE STATISTICS OF SERVICE GAP:

Now we will perform an MANNOVA test to prove that there is interdependencies between all

the five factors and total experienced service quality.

MANNOVA Table:

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 26

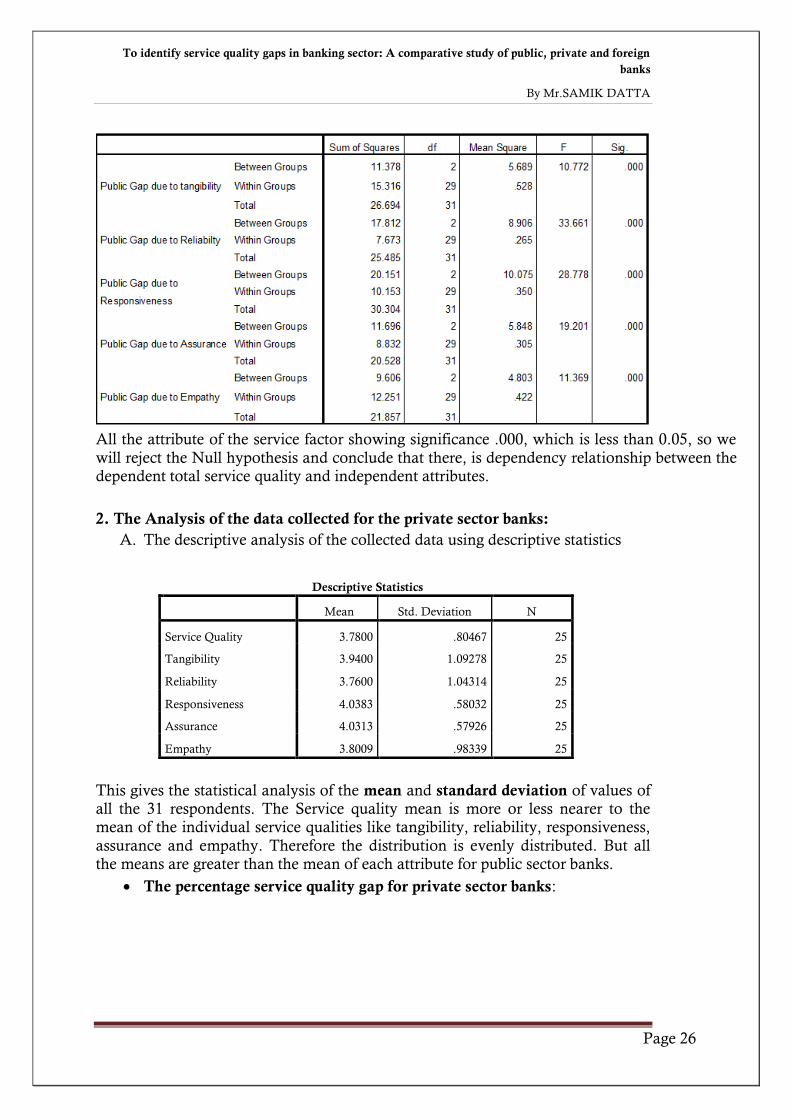

All the attribute of the service factor showing significance .000, which is less than 0.05, so we

will reject the Null hypothesis and conclude that there, is dependency relationship between the dependent total service quality and independent attributes.

2. The Analysis of the data collected for the private sector banks:

A. The descriptive analysis of the collected data using descriptive statistics

Descriptive Statistics

Mean Std. Deviation N

Service Quality 3.7800 .80467 25

Tangibility 3.9400 1.09278 25

Reliability 3.7600 1.04314 25

Responsiveness 4.0383 .58032 25

Assurance 4.0313 .57926 25

Empathy 3.8009 .98339 25

This gives the statistical analysis of the mean and standard deviation of values of all the 31 respondents. The Service quality mean is more or less nearer to the mean of the individual service qualities like tangibility, reliability, responsiveness,

assurance and empathy. Therefore the distribution is evenly distributed. But all the means are greater than the mean of each attribute for public sector banks.

The percentage service quality gap for private sector banks:

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 27

Private sector Banks

Mean_ESQ 4.37

Qlty Tangibility 3.78 Gap due to tangibility -0.43

Qlty Reliability 3.94 Gap due to Reliability -0.61

Qlty Responsiveness 3.76 Gap due to Responsiveness -0.33

Qlty Assurance 4.04 Gap due to tangibility -0.34

Qlty Empathy 4.03 Gap due to Empathy -0.57

Qlty total Service 3.80 Gap due to total service Qlty -0.59

Mean ESQ= Mean Expected service Quality.

Qlty Tangibility= Mean of quality of perceived tangibility of consumers.

Qlty Responsiveness= Mean of quality of perceived Responsiveness of consumer.

Qlty Assurance= Mean of quality of perceived Assurance of consumer.

Qlty Empathy= Mean of quality of perceived Empathy of consumer.

Qlty total Service= Mean of quality of perceived total Service of consumer.

Analysis of the service quality gap with respect to the age range of the respondants:

We have taken the age range of the respondents ranging between:

15 years to 25 years

26 years to 40 years

41 years to 60 years

More than 60 years

On the other hand the service quality gap has been catehories as:

Maximum ranging data is 0.0 and minimum ranging data is -2.0.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 28

High = The service quality is satisfactory ( gap ranging from 0 to 0.50).

Medium= The service quality is optimum ( gap ranging from 0.0 to -1.00).

Low = The service quality is dis-satisfactory ( gap ranging from -1.00 to -2.00).

The representation is as follows:

Graph: 1

Income Category

<60,000

60,001 INR -

2,00,000 INR

2,00,001 INR -

4,00,000 INR

4,00,001 INR -

8,00,000 INR

Above 8,00,000

Service category

Highly Satisfied

0.00% 0.00% 0.00% 0.00% 0.00%

Satisfied 20.00% 8.00% 12.00% 12.00% 12.00%

Dis-satisfied 8.00% 4.00% 4.00% 12.00% 8.00%

Analysis of the service quality gap with respect to the income group range of the respondants:

We have taken the income range of the respondents ranging between: > Rs.60,000 Per Annum

Rs.60,001 to Rs. 2,00,000 Per Annum Rs. 2,00,001 to Rs. 4,00,000 Per Annum Rs. 4,00,001 to Rs. 8,00,000 Per Annum

More than 8,00,001 Per Annum On the other hand the service quality gap has been catehories as:

Maximum ranging data is 0.50 and minimum ranging data is -2.0.

High = The service quality is satisfactory ( gap ranging from 0 to 0.50).

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 29

Medium= The service quality is optimum ( gap ranging from 0.0 to -1.00).

Low = The service quality is dis-satisfactory ( gap ranging from -1.00 to -

2.00). The representation is as follows: Graph: 2

Age Category

15-25 years

26-40 Years

41-60 Years

Above 60 years

Service category

Highly Satisfied 0.00% 0.00% 0.00% 0.00%

Satisfied 20.00% 40.00% 0.00% 4.00%

Dis-satisfied 0.00% 24.00% 12.00% 0.00%

The result we can conclude from the graphs are as follows:

Graph1 : The Distribution of satisfied consumer are uniform.Except the salary

range of 4,00,000 to 8,00,000 within all other income categories the frequency of satisfied people is greater than unsatisfied people. There is no highly satisfied

people dealing with private sector banking.

Graph 2 : The people within the age range 26-40, who are mostly professional people, they have expericened satisfactory service qulaity and therefore for

public sector banks there is a littele gap between the perceived and expected

quality of service. But conclusion for age range of 41-60 yearsis different, for these sample of people the service qulaity gap for the strata of people is high.

B. The Inferential analysis of the collected data using inferential statistics.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 30

Now, using different hypothesis we will try to draw some inferential or conclusive decision about the gathered sample and perception about the

private banking.

We will use:

Linear Regression Analysis, for finding out whether there is at all any dependencies between the dependent variable, i.e. the total experienced or

perceived service quality and the independent variables, all the attribute qualities.

MANOVA, to found out the inter dependencies between the independent

attribute variables and the dependent variables.

Descriptive statistics to identify the mean, median, mode and skewness.

We will start with linear regression model, where the correlation table gives us the

idea about the inter-dependencies between each of the attribute variables.

This table signifies:

Tangibility and reliability is weakly co-related.

Tangibility and responsiveness is highly co-related.

Tangibility and Assurance is highly co-related.

Tangibility and Empathy is highly co-related

Reliability and responsiveness is weakly co-related.

Reliability and Assurance is highly co-related.

Reliability and empathy is weakly co-related.

Responsiveness and Assurance is very highly co-related.

Responsiveness and empathy is weakly co-related.

Assurance and Empathy is weakly co-related.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 31

Linear regression model Summary:

Model Summaryb

Model R R Square Adjusted R

Square

Std. Error of the

Estimate

1 .772a .596 .515 .56033

a. Predictors: (Constant), Empathy, Reliability, Responsiveness,

Tangibility

b. Dependent Variable: Service Quality

This part gives the information that whatever regression model we are creating that has

59.6 % reliability. That means with this sample data we can explain 59.6 % of the model.

Therefore, the model of regression is not apt for this sample of data.

noANOVAa

Model Sum of Squares df Mean Square F Sig.

1

Regression 9.261 4 2.315 7.374 .001b

Residual 6.279 20 .314

Total 15.540 24

a. Dependent Variable: Service Quality

b. Predictors: (Constant), Empathy, Reliablity, Responsiveness, Tangibility

As the significance is <0.05, so the ANNOVA table also defines that the mean of the

regression and residual are not equal. Therefore, we will go the conclusion of the

dependency relationship of the dependent and independent variable.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 32

Now this result of linear regression is quite interesting, this result signifies that for the

given sample assurance has no impact on the total perceived service quality by the

consumer. Now this is the linear regression coefficients and the t-test significance representation. Interpreting the results we can get the following conclusions:

The regression equation contains in Y axis or dependable variable as

“Total experienced service quality” of the consumers and the independent X axis variables are: Tangibility, reliability, responsiveness, assurance,

empathy qualities as per the consumer response. Now, we will examine whether there is at all any dependency between the five variables over the

„service quality‟ that the consumers are getting.

Analysing the result we can infer that except tangibility all the other

attribute have the significance level less than 0.05, so those

attributes have effect on the experienced service quality level.

The regression equation would be:

Y =-.388-0.225X1+.231X2+.849X3+ .0X4+.199X5

X1= the experienced Service quality due to tangibility.

X2= the experienced Service quality due to reliability.

X3= the experienced Service quality due to responsiveness.

X4= the experienced Service quality due to assurance.

X5= the experienced Service quality due to empathy.

Y= Experienced Service Quality.

Apart from this, within unstandardized coefficients all the B values

of reliability, responsiveness, empathy are greater than standard error value, along with this tangibility has negative relationship with

perceived quality, which signifies there is a better interdependency between the Y and X value for reliability, responsiveness, empathy

and also intra data X relations are there. And of course the with 59.4% reliable model.

Therefore we can conclude that there is direct effect of reliability,

responsiveness, and empathy over the service quality.

Now the standardise residual and service quality forms a histogram which gives rise to a normal distribution, which signifies the accuracy of the data set.

Descriptive statistics for the service Gap:

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 33

3. Analysis of the data collected for the foreign sector banks.

A. The descriptive analysis of the collected data using descriptive statistics.

Descriptive Statistics

Mean Std. Deviation N

Service Quality 4.2935 .58534 31

Tangibility 3.9532 .76452 31

Reliability 3.9067 .72801 31

Responsiveness 3.7857 .75907 31

Assurance 3.7698 .60012 31

Empathy 3.8257 .64942 31

This gives the statistical analysis of the mean and standard deviation of values of all the 31 respondents. The Service quality mean is more or less nearer to the

mean of the individual service qualities like tangibility, reliability, responsiveness, assurance and empathy. Therefore the distribution is evenly distributed. But all

the means are greater than the mean of each attribute for public sector banks and private sector banks.

The percentage service quality gap for private sector banks:

Private sector Banks

Mean_ESQ 4.84

Qlty Tangibility 3.95 Gap due to tangibility -0.89

Qlty Reliability 3.91 Gap due to Reliability -0.39

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 34

Mean

ESQ= Mean Expected service Quality.

Qlty Tangibility= Mean of quality of perceived tangibility of consumers.

Qlty Responsiveness= Mean of quality of perceived Responsiveness of consumer.

Qlty Assurance= Mean of quality of perceived Assurance of consumer.

Qlty Empathy= Mean of quality of perceived Empathy of consumer.

Qlty total Service= Mean of quality of perceived total Service of consumer.

Analysis of the service quality gap with respect to the age range of the respondants:

We have taken the age range of the respondents ranging between:

15 years to 25 years

26 years to 40 years

41 years to 60 years

More than 60 years

On the other hand the service quality gap has been catehories as:

Maximum ranging data is 0.1 and minimum ranging data is -2.0.

High = The service quality is satisfactory ( gap ranging from 0 to 0.50).

Medium= The service quality is optimum ( gap ranging from 0.0 to -1.00).

Low = The service quality is dis-satisfactory ( gap ranging from -1.00 to -2.00).

The representation is as follows:

Qlty Responsiveness 3.79 Gap due to Responsiveness

-1.05

Qlty Assurance 3.77 Gap due to tangibility -1.07

Qlty Empathy 3.83 Gap due to Empathy -1.01

Qlty total Service 4.29 Gap due to total service Qlty

-0.55

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 35

Graph: 1

Analysis of the service quality gap with respect to the income group range

of the respondants: We have taken the income range of the respondents ranging between:

> Rs.60,000 Per Annum Rs.60,001 to Rs. 2,00,000 Per Annum

Rs. 2,00,001 to Rs. 4,00,000 Per Annum Rs. 4,00,001 to Rs. 8,00,000 Per Annum

More than 8,00,001 Per Annum On the other hand the service quality gap has been catehories as:

Maximum ranging data is 0.50 and minimum ranging data is -2.0.

High = The service quality is satisfactory ( gap ranging from 0 to 0.50).

Medium= The service quality is optimum ( gap ranging from 0.0 to -1.00).

Low = The service quality is dis-satisfactory ( gap ranging from -1.00 to -2.00). The representation is as follows:

Graph: 2

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 36

Age Category

Service category

as a percentage of

Age Category

15-25

years

26-40

Years

41-60

Years

Above 60

years

Highly

Satisfied 0.00% 3.23% 3.23% 0.00%

Satisfied 9.68% 29.03% 16.13% 0.00%

Dis-

satisfied 9.68% 22.58% 3.23% 3.23%

The result we can conclude from the graphs are as follows:

Graph1 : The Distribution of satisfied consumer are uniform.Except the salary range of 4,00,000 to 8,00,000 within all other income categories the frequency of satisfied people is greater than unsatisfied people. There is no highly satisfied

people dealing with private sector banking.

Graph 2 : The people within the age range 26-40, who are mostly professional people, they have expericened satisfactory service qulaity and therefore for

public sector banks there is a littele gap between the perceived and expected

quality of service. But conclusion for age range of 41-60 yearsis different, for these sample of people the service qulaity gap for the strata of people is high.

B. The Inferential analysis of the collected data using inferential statistics.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 37

Now, using different hypothesis we will try to draw some inferential or conclusive decision about the gathered sample and perception about the private banking.

We will use:

• Linear Regression Analysis, for finding out whether there is at all any dependencies between the dependent variable, i.e. the total experienced or perceived service quality and the independent variables, all the attribute

qualities.

• MANOVA, to found out the inter dependencies between the independent attribute variables and the dependent variables.

• Descriptive statistics to identify the mean, median, mode and skewness.

We will start with linear regression model, where the correlation table gives us the

idea about the inter-dependencies between each of the attribute variables.

This table signifies:

Tangibility and reliability is highly co-related.

Tangibility and responsiveness is highly co-related.

Tangibility and Assurance is highly co-related.

Tangibility and Empathy is highly co-related

Reliability and responsiveness is highly co-related.

Reliability and Assurance is highly co-related.

Reliability and empathy is highly co-related.

Responsiveness and Assurance is very highly co-related.

Responsiveness and empathy is highly co-related.

Assurance and Empathy is highly co-related.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 38

And therefore, due to high inter dependency between the variables and the regression model is not a sound one.

Linear regression model Summary:

Model Summary

Model R R Square Adjusted R

Square

Std. Error of the

Estimate

1 .428a .183 .020 .57954

a. Predictors: (Constant), Empathy, Tangibility, Responsiveness,

Assurance, Reliability

b. Dependent Variable: Service Quality

This part gives the information that whatever regression model we are creating that has 18.3 % reliability. That means with this sample data we can explain 59.6

% of the model.

Therefore, the model of regression is not apt for this sample of data.

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1

Regression 1.882 5 .376 1.121 .375b

Residual 8.397 25 .336

Total 10.279 30

a. Dependent Variable: Service Quality

b. Predictors: (Constant), Empathy, Tangibility, Responsiveness, Assurance, Reliablity

Now this result of linear regression is quite interesting, this result signifies that for

the given sample assurance has no impact on the total perceived service quality by the consumer.

Now this is the linear regression coefficients and the t-test significance

representation. Interpreting the results we can get the following conclusions:

• The regression equation contains in Y axis or dependable variable as “Total experienced service quality” of the consumers and the independent X axis

variables are: Tangibility, reliability, responsiveness, assurance, empathy qualities as per the consumer response. Now, we will examine whether there is at all any

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 39

dependency between the five variables over the „service quality‟ that the consumers are getting.

analysing the result we can infer that except tangibility all the other

attribute have the significance level less than 0.05, so those attributes have effect on the experienced service quality level.

the regression equation would be:

Y =-3.065-.138X1 -.437X2-.061X3 -.476X4+1.155X5

X1= the experienced Service quality due to tangibility.

X2= the experienced Service quality due to reliability.

X3= the experienced Service quality due to responsiveness.

X4= the experienced Service quality due to assurance.

X5= the experienced Service quality due to empathy.

Y= Experienced Service Quality.

Apart from this, within unstandardized coefficients all the B values of

reliability, responsiveness, empathy are greater than standard error value, along with this tangibility has negative relationship with perceived quality, which signifies there is a better interdependency between the Y and X value for

reliability, responsiveness, assurance, empathy and also intra data X relations are there. And of course the with 18.1 % reliable model.

Therefore we can conclude that there is there is no direct effect of tangibility ,

reliability, responsiveness, and empathy over the service quality.

Now the standardise residual and service quality forms a histogram which gives rise to a normal distribution, which signifies the accuracy of the data set.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 40

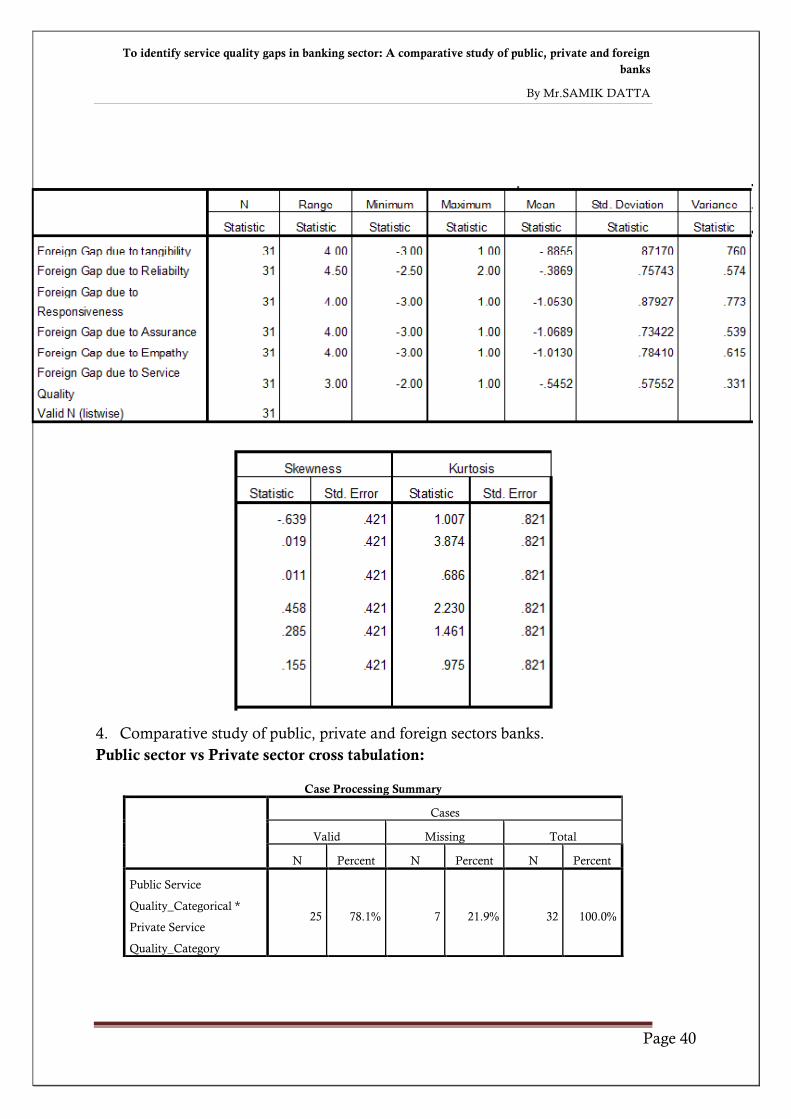

4. Comparative study of public, private and foreign sectors banks.

Public sector vs Private sector cross tabulation:

Case Processing Summary

Cases

Valid Missing Total

N Percent N Percent N Percent

Public Service

Quality_Categorical *

Private Service

Quality_Category

25 78.1% 7 21.9% 32 100.0%

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 41

Public Service Quality_Categorical * Private Service Quality_Category Crosstabulation

Count

Private Service Quality_Category Total

Bad Service Average Service Good Service

Public Service

Quality_Categorical

Bad Service 3 5 2 10

Medium Service 6 3 4 13

High Service 0 2 0 2

Total 9 10 6 25

Chi-Square Tests

Value df Asymp. Sig. (2-

sided)

Pearson Chi-Square 4.968a 4 .291

Likelihood Ratio 5.742 4 .219

Linear-by-Linear Association .000 1 .987

N of Valid Cases 25

a. 8 cells (88.9%) have expected count less than 5. The minimum expected

count is .48.

The H0 is accepted. The two variables are independent to each other. So the

service quality doesn‟t depend each other.

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA

Page 42

Public sector Bank and Foreign Bank:

Case Processing Summary

Cases

Valid Missing Total

N Percent N Percent N Percent

Public Service

Quality_Categorical *

Foreign Service

Quality_Category

31 96.9% 1 3.1% 32 100.0%

Public Service Quality_Categorical * Foreign Service Quality_Category Crosstabulation

Count

Foreign Service Quality_Category Total

Bad service Average Service Good Service

Public Service

Quality_Categorical

Bad Service 1 6 4 11

Medium Service 2 6 10 18

High Service 0 1 1 2

Total 3 13 15 31

Chi-Square Tests

Value df Asymp. Sig. (2-

sided)

Pearson Chi-Square 1.522a 4 .823

Likelihood Ratio 1.723 4 .787

Linear-by-Linear

Association .476 1 .490

N of Valid Cases 31

To identify service quality gaps in banking sector: A comparative study of public, private and foreign

banks

By Mr.SAMIK DATTA