Embed Size (px)

Citation preview

LIFE BERMUDA LTD

TransExplorer index ul

protection accumulation

consumer guide

Contents

Advantages of Index Universal Life ..............................................................................................................4

About TransExplorer Index UL ......................................................................................................................5

Index Descriptions ........................................................................................................................................6

The S&P 500® Index1 ................................................................................................................................6

EURO STOXX 50® Index2 ..........................................................................................................................6

Hang Seng Index3 ......................................................................................................................................6

Premiums ..................................................................................................................................................... 7

Required Premium (RAP) .......................................................................................................................... 7

Premium Qualification Credit (PQC) ......................................................................................................... 7*Net Premiums are equal to gross premiums paid less applicable premium expense charges.

No-Lapse Guarantee ....................................................................................................................................8

No-Lapse Premium ...................................................................................................................................8

The Basic Interest Account and Index Account ............................................................................................9

How It works .............................................................................................................................................9

Basic Interest Account ..............................................................................................................................9

Index Account ...........................................................................................................................................9

Understanding Segments ...........................................................................................................................10

The Nuts and Bolts of the Index Crediting Strategy ...................................................................................13

Hypothetical Example of an Index Account calculation .............................................................................. 14

Transfers .....................................................................................................................................................15

Transfers to the Index Account ...............................................................................................................15

Transfers to the Basic Interest Account ..................................................................................................15

Automated Transfers from the BIA to the IA ...........................................................................................15

Policy Charges ............................................................................................................................................16

Premium Expense Charge ......................................................................................................................16

Monthly Deductions ................................................................................................................................16

Monthly Expense Charges Per Thousand ...............................................................................................16

Index Account Monthly Charges .............................................................................................................16

Surrender Charge ....................................................................................................................................16

Available Funds ...........................................................................................................................................18

Borrowing from the policy .......................................................................................................................18

Partial Surrenders ....................................................................................................................................18

AbouT TrAnsAmeriCA Life (bermudA) LTd.

Transamerica Life (Bermuda) Ltd. is a wholly owned subsidiary of Transamerica

Life Insurance Company—a company that has a heritage of helping families and

businesses secure their financial futures for more than a century.

Both Transamerica Life Bermuda and its parent company, Transamerica Life

Insurance Company (TLIC), are Aegon companies. Aegon N.V. is one of the

leading international life insurance, pension and asset management companies.

Headquartered in The Hague, the Netherlands, Aegon has businesses in over

20 markets in the Americas, Europe and Asia.

Transamerica Life Bermuda offers universal life insurance products designed

to meet long-term planning strategies--proceeds can be used to fund estate

taxes, create liquidity, and preserve wealth. Life insurance can bring needed

diversification to a portfolio. It is a predictable asset since the amount of the

policy death benefit is known, but it also serves as a non-correlated asset. This

means that despite occasional declines in the marketplace (affecting stocks and

bonds), the value held in a fixed life insurance policy may remain unaffected.

If you are looking for a policy that also offers potential cash value accumulation,

Transamerica Life Bermuda can offer the right product to help meet your needs.

TransExplorer indEx ul

4 5

from Transamerica Life (Bermuda) LTd.

About Transexplorer index uL SafEty and CaSh ValuE Growth TransExplorer Index UL is a flexible premium index universal life insurance policy that not only offers a

death benefit, but also the potential for greater cash value accumulation than a traditional life insurance

policy, without exposure to market declines.

indEx-BaSEd PErformanCEThe distinctive product design offers you the opportunity to allocate premiums to an Index Account

which uses three global financial indices (the S&P 500® Index, the EURO STOXX 50® Index and the

Hang Seng Index excluding dividend income) to determine the Index Interest. The Index Account uses

a one-year point-to-point crediting method.

no-laPSE GuarantEEThe product also offers a unique No-Lapse Guarantee for a period of the lesser of 30 years or through

the policy anniversary at the insured’s attained age 75, with a minimum of five years for all ages.

SECurity in thE form of GuarantEEd floorWith TransExplorer Index UL, you have the option of allocating net premiums to a Basic Interest Account,

an Index Account, or a combination of the two. Both account options offer the security of a guaranteed

minimum interest rate of 1.00%, which helps prevent market-based losses and preserve prior years’ gains.

Advantages of index universal Life Over the years, index universal life (IUL) products

have gained popularity due to their potential

for greater accumulation value. These products

include guaranteed minimum interest rates and

no exposure to market declines, thus preserving

policy accumulation value.

An IUL policy offers interest crediting based, in

part, on changes in one or more financial indexes.

An index account is credited with interest,

up to a specified Cap, that is potentially greater

than interest credited to traditional universal life

insurance. However, since interest amounts

credited to the index account are based, in part,

on changes in external indexes, there is greater

potential for interest volatility.

Note that even though the interest credited

to an index account may be affected by stock

indexes, an index universal life insurance

policy does not participate directly in any

stock, mutual funds, or investments.

There are additional factors that will affect your life

insurance decisions, but if you are looking for a

product with downside protection in the form

of a guaranteed minimum interest rate and access

to potentially higher policy accumulation values,

an index universal life insurance policy with an

index account based on global indexes may be

an option. This policy is not a short term savings

vehicle, nor is it ideal for short term insurance

needs. It is designed to be long-term in nature.

TransExplorer index ulValuE. PErformanCE. SECurity.

TransExplorer indEx ul

7

from Transamerica Life (Bermuda) LTd.

6

PremiumsrEquirEd PrEmium (raP)When the policy is purchased, you commit to a

Required Premium (RAP) which is the minimum

amount you need to pay each year for the first

five policy years. The RAP must be received

by Transamerica Life Bermuda by the policy

anniversary each year. If the RAP is not received

by the policy anniversary, the policy will enter its

grace period and will lapse if sufficient premium

is not paid.

PrEmium qualifiCation CrEdit (PqC)Transamerica Life Bermuda will credit your

policy with a Premium Qualification Credit (PQC)

if the full RAP is paid on or before each policy

anniversary during the five year RAP period.

Under this provision, the Company will add 2%

of the RAP amount directly to the accumulation

value at the beginning of the next policy year.

This bonus is payable in policy years two through

six and is separate from the interest crediting

strategies described below.

Important Note: If the RAP is paid after the policy

anniversary, no bonus will be paid. There is no

“catching-up” for earning the PQC.

1 S&P® is a registered trademark of Standard &

Poor’s Financial Services LLC (“S&P”) and Dow

Jones® is a registered trademark of Dow Jones

Trademark Holdings LLC (“Dow Jones”). The

foregoing trademarks have been licensed for

use by S&P Dow Jones Indices LLC. S&P® and

S&P 500® are trademarks of S&P and have been

licensed for use by S&P Dow Jones Indices LLC

and the Company. The S&P 500® index is a product

of S&P Dow Jones Indices LLC and has been

licensed for use by the Company. This policy is

not sponsored, endorsed, sold or promoted by

S&P Dow Jones Indices LLC, Dow Jones, S&P

or their respective affiliates and neither S&P Dow

Jones Indices LLC, Dow Jones, S&P nor their

respective affiliates make any representation

regarding the advisability of purchasing this policy.

2 The EURO STOXX 50® is the intellectual property

(including registered trademarks) of STOXX

Limited, Zurich, Switzerland, (the “Licensor”),

which is used under license. The TransExplorer

Index UL based on the Index is in no way

sponsored, endorsed, sold or promoted by the

Licensor and the Licensor shall have no liability

with respect hereto.

3 Please read the full disclaimer in the TransExplorer

Index UL policy regarding the Hang Seng Index in

relation to the policy.

index descriptions thE S&P 500® indEx1

The S&P 500® Index tracks 500 large cap common stocks actively traded in the United States, and is one

of the most well-known market benchmarks.

Euro Stoxx 50® indEx2

The EURO STOXX 50® Index is comprised of 50 large cap stocks from leading European blue-chip

companies. The stocks used in this index are selected from leading companies from countries in

the European Union.

hanG SEnG indEx3

Launched in 1969, the Hang Seng Index is one of the most recognized indicators of the performance

of the Hong Kong stock market.

TransExplorer indEx ul

9

from Transamerica Life (Bermuda) LTd.

8

The basic interest Account and index Account how it workSTransExplorer Index UL is designed for a variety of premium schedules. When premium payments are

made, a Premium Expense Charge of 6% is deducted from the premium payment. The net premium is

then applied to the policy’s Basic Interest Account (BIA), the Index Account (IA) or a combination of the

two, based on your allocation instructions.

You may choose to leave the premium in the BIA. If you do so, your policy will perform like a typical

universal life insurance policy, guaranteed to earn at least 1% annually.

For greater growth potential, you may allocate the premiums to the Index Account.

You may also choose to automate transfers from the BIA into the IA on a monthly or quarterly basis.

BaSiC intErESt aCCountThe portion of the policy’s accumulation value allocated to the BIA earns interest at rates declared by the

Company. The interest rate on the BIA will never be less than the guaranteed minimum interest rate of

1.00%. The Company will credit interest to the funds allocated to the BIA on a monthly basis. The value

of the BIA includes any interest earned since the previous monthly policy date.

The current interest rate applicable to the BIA is declared by the Company from time to time. The interest

rate credited to a particular premium depends on the date the premium is received at the Administrative

Office. Consequently, more than one interest rate is often applicable to different portions of the accumulation

value at the same time. Your annual statement itemizes the applicable interest rates. Interest is credited on

the initial premium as of the date the last offer letter requirement is received at the Administrative Office.

indEx aCCountFor greater growth potential, you may allocate premiums to the IA. Premiums can be paid quarterly,

semi-annually, or annually. In addition, you may request quarterly or monthly automated transfers from the

BIA to the IA. Each premium allocation or transfer from the BIA into the IA creates a separate one-year

IA Segment.

no-Lapse Guaranteeno-laPSE PrEmium Your policy comes with a No-Lapse Guarantee

which may prevent your policy from lapsing during

the No-Lapse Period, as long as you pay the

Minimum No-Lapse Premiums stated in the policy.

During the No-Lapse Period, as long as the

cumulative No-Lapse Premiums are paid (net of

loans, refunds, and partial surrenders) regardless

of how the policy performs, your policy’s Death

Benefit is guaranteed. However, by paying only

the minimum premium, you may be forgoing

the opportunity to potentially build up additional

accumulation value. If you take a cash withdrawal or

a loan, you may need to pay additional premiums

in order to keep the No-Lapse Guarantee in effect.

The No-Lapse Period is as follows:

Issue Ages 16 – 70: lesser of 30 years or until age 75

Issue Ages 71 – 85: 5 years

If the requirements of the No-Lapse Guarantee

are not met and the net cash value is not enough

to meet the monthly deductions and Index Account

Monthly Charges, a grace period will begin and

the policy will lapse at the end of the grace period

unless sufficient payment is made.

The No-Lapse Guarantee will terminate if the

cumulative No-Lapse Premium requirement is

not met by the policy anniversary each year.

There is no catch-up available to reinstate the

No-Lapse Guarantee.

Flexible Premium Payment

Owner Controlled

Net Premium Allocation Choices

Basic Interest Account (BIA) Credits interest at a

rate set by the Company.

Guarantees a minimum interest rate of 1%

Index Account (IA) Credited with interest based, in part,

on changes in three stock indexes.

Guarantees a minimum interest rate of 1%

from tranSamEriCa lifE (BErmuda) ltd.

11

Instead of crediting interest at a rate declared

in advance as in the BIA, at the end of each IA

Segment year, the Company determines the Index

Interest to be credited based, in part, on the

performance of the S&P 500® Index, the EURO

STOXX 50® Index and the Hang Seng Index,

excluding dividend income. The Index Interest

Rate cannot be greater than the Cap* declared

by the Company and will never be less than the

guaranteed minimum interest rate of 1.00%.

Each Index Segment earns a rate of interest

based, in part, on the one-year, point-to-point

performance of the underlying financial indexes.

As of each IA Segment Anniversary, the Index

Interest Rate will be applied to that Segment’s

average month-end value to calculate the Index

Interest to be credited to that IA Segment.

If you have not submitted transfer instructions

with the Company, the values of the ending

Segment, plus any interest credited at the

Segment Anniversary, will renew into a new

Segment in the Index Account.

* The Cap is the maximum Index Interest Rate

that can be used to determine the Index Interest

credited to that Segment. A Cap rate is declared

for each Segment on its Beginning Monthly Date.

The Cap can vary from Segment to Segment and

from Segment year to Segment year.

undErStandinG SEGmEntS • Segments are components of the Index Account

to which net premiums and/or transfers of

accumulation values are allocated.

• There are up to 12 Segments for each policy

year, and each Segment begins on a Monthly

Policy Date.

• Each Segment lasts for 12 months and ends

on the Segment Anniversary.

• The value of the Index Account is the sum of

its Segment values and any amount pending*

application to that Segment.

* Premiums designated for the IA but received at the

Bermuda Office on dates other than the Monthly

Policy Date are held until they are allocated.

While held, they earn the guaranteed minimum

interest rate of 1.00% until they are allocated to

the next Segment.

TransExplorer indEx ul

10

TransExplorer indEx ul

13

from Transamerica Life (Bermuda) LTd.

12

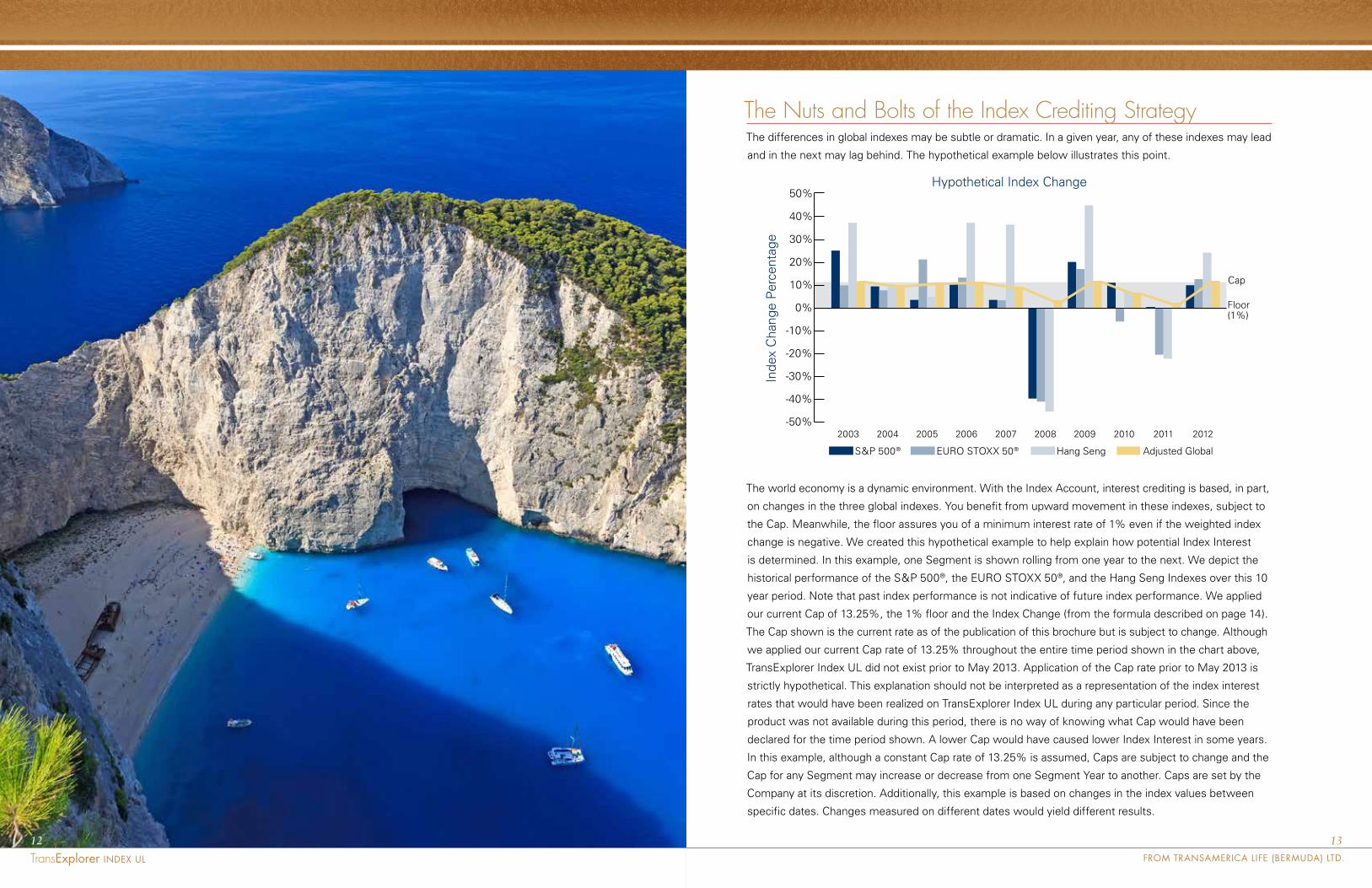

The nuts and bolts of the index Crediting strategyThe differences in global indexes may be subtle or dramatic. In a given year, any of these indexes may lead

and in the next may lag behind. The hypothetical example below illustrates this point.

The world economy is a dynamic environment. With the Index Account, interest crediting is based, in part,

on changes in the three global indexes. You benefit from upward movement in these indexes, subject to

the Cap. Meanwhile, the floor assures you of a minimum interest rate of 1% even if the weighted index

change is negative. We created this hypothetical example to help explain how potential Index Interest

is determined. In this example, one Segment is shown rolling from one year to the next. We depict the

historical performance of the S&P 500®, the EURO STOXX 50®, and the Hang Seng Indexes over this 10

year period. Note that past index performance is not indicative of future index performance. We applied

our current Cap of 13.25%, the 1% floor and the Index Change (from the formula described on page 14).

The Cap shown is the current rate as of the publication of this brochure but is subject to change. Although

we applied our current Cap rate of 13.25% throughout the entire time period shown in the chart above,

TransExplorer Index UL did not exist prior to May 2013. Application of the Cap rate prior to May 2013 is

strictly hypothetical. This explanation should not be interpreted as a representation of the index interest

rates that would have been realized on TransExplorer Index UL during any particular period. Since the

product was not available during this period, there is no way of knowing what Cap would have been

declared for the time period shown. A lower Cap would have caused lower Index Interest in some years.

In this example, although a constant Cap rate of 13.25% is assumed, Caps are subject to change and the

Cap for any Segment may increase or decrease from one Segment Year to another. Caps are set by the

Company at its discretion. Additionally, this example is based on changes in the index values between

specific dates. Changes measured on different dates would yield different results.

-40%

-30%

-50%

-20%

-10%

0%

10%

20%

30%

50%

40%

Adjusted GlobalS&P 500® EURO STOXX 50® Hang Seng

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Cap

Floor(1%)

Hypothetical Index Change

Inde

x C

hang

e Pe

rcen

tage

TransExplorer indEx ul

15

from Transamerica Life (Bermuda) LTd.

14

Transfers tranSfErS to thE indEx aCCountYou may transfer a portion of the funds from the Basic Interest Account into the Index Account on any

monthiversary date by making a request in writing using the form “Request for Change in Allocation

Percentage or Transfer of Funds Between Account Options.”

Transfers may be requested in either a dollar amount or as a percentage of the current BIA value.

The amounts transferred to the IA will be included in the Segment that will be created on the next

monthly policy date.

tranSfErS to thE BaSiC intErESt aCCount A transfer of funds from the Index Account into the Basic Interest Account will only be allowed on the

Segment Anniversary. A transfer request must be made in writing using the “Request for Change in

Allocation Percentage or Transfer of Funds Between Account Options” form, and must be received by

the Bermuda office before the IA Segment Anniversary date.

There is no charge to process transfers between accounts.

automatEd tranSfErS from thE Bia to thE iaTo help reduce exposure to market volatility, you may allocate your net premiums to the BIA and

request automated transfers of a specified amount from the BIA to the IA on a quarterly or monthly

basis. Automated transfers must be requested in writing using the Automated Transfer form. On the

form, you will specify an amount to be transferred and a frequency (monthly or quarterly) for the

transfers from the BIA to the IA.

The transferred amount will be moved into a new IA Segment on the monthiversary following the transfer.

On the date of an automated transfer, if the accumulation value in the BIA is not sufficient to complete

the transfer, the transfer will not occur, although transfers will continue to be processed on subsequent

monthly or quarterly scheduled dates. The automated transfer feature will continue until you terminate it.

hyPothEtiCal ExamPlE of an indEx aCCount CalCulation

how it workS:At the end of each Index Account Segment year, the Company determines whether any Index Interest

will be credited for the Segment year just ended. The amount of Index Interest credited at the end of

the Segment year depends on the average Segment month-end values, the weighted change in the

values of the indexes, and the applicable Cap. Monthly deductions and Index Account Monthly Charges

along with policy owner transactions such as loans or withdrawals will reduce the average Segment

month-end value on which the Index Interest is calculated. Index Interest is only credited at the end of

a Segment year.

Index InterestThe Index Account uses a weighted average to calculate Index Interest. To determine the Index Interest Rate, the percentage change in each Index is multiplied by its corresponding weighting to arrive at the Index Change percentage. The Index Change percentage is then compared to the Cap, and the lower of the two (subject to the guaranteed minimum interest rate of 1.00%) is credited to the average Segment month-end value at the end of the Segment year.

Index Weighting ExplainedTo arrive at the weighted index change percentage, we apply the following factors:

50% to the percentage change in the S&P 500® or the EURO STOXX 50®, whichever is higher

30% to the percentage change in the S&P 500® or the EURO STOXX 50®, whichever is lower

20% to the percentage change in the Hang Seng Index

1%Floor

Index changes may be positive or negative.

However, you have the security of knowing you wioll never be credited

less than the guaranteed minimum interest rate.

Hypothetical Example

IndexIndex

ChangeWeight

Weighted Index Change Percentage

EURO STOXX 50® 6% 50% (6% x 50%) - 3%

S&P 500® 5% 30% (5% x 30%) - 1.5%

Hang Seng 7% 20% (7% x 20%) - 1.4%

Total 5.9%

Index Account Segment Calculation

Index Change X Weight =Weighted Index

Change Percentage

13.25%CapThe Cap is the maximum percentage of index change your index account can be credited.

TransExplorer indEx ul

16

from Transamerica Life (Bermuda) LTd.

17

Policy ChargesPrEmium ExPEnSE CharGEA charge of 6% is deducted from each premium

payment on a current and guaranteed basis.

monthly dEduCtionSEach month, the Company subtracts from the

accumulation value a monthly deduction (MD).

MD rates are applied to the net amount at risk,

which is the difference between the death benefit

of the policy and the accumulation value at the

beginning of each month. Monthly deductions

cover cost factors that include, but are not limited

to, the cost of insurance, the costs of riders, and

any charges for substandard class ratings.

Monthly deduction rates vary based on the insured’s

issue age, underwriting status, sex, region, and

the policy’s duration.

The current MD rates are guaranteed for the first

five policy years, and are zero after the policy

anniversary at the insured’s age 111.

After the initial guarantee period, the MD rates will

never be greater than the guaranteed rates printed in

each issued policy. Guaranteed MD rates continue

to the anniversary at the insured’s age 121.

monthly ExPEnSE CharGES PEr thouSandMonthly expense charges per thousand will be

deducted monthly. On a current basis, this charge

will be assessed during the first eight policy years.

On a guaranteed basis, this charge will be assessed

until the policy anniversary at the insured’s age

121. The rate for this charge is based on the

insured’s issue age, sex, underwriting class,

region, and the policy’s duration.

indEx aCCount monthly CharGEThe Index Account Monthly Charge is 0.06%

(0.72% per year) of the Index Account Value.

This charge is taken in all years until the policy

anniversary at the insured’s age 111.

SurrEndEr CharGE Company-imposed surrender charges decrease

each year and disappear entirely after the 10th

policy anniversary for all risk classes. Surrenders

and withdrawals will affect the policy value, net

cash value, and the death benefit.

TransExplorer indEx ul

18

Available fundsBorrowinG from thE PoliCy You may borrow any amount up to the policy’s cash value less any outstanding loans (known as “net

cash value”) and less any loan interest due. Policy loans are taken from the Basic Interest Account first

until it is exhausted, then pro rata from the Index Account Segments. Amounts removed from a Segment

due to loans will reduce the Index Interest that may otherwise be earned as of a Segment Anniversary.

Interest earned on values securing policy loans will be credited monthly to the BIA.

The rate of interest charged on the policy loan is 4% in arrears. You will be billed annually for the interest

on any Loan Balance. If you do not pay the loan interest, it will be added to your loan subject to available

values, and interest will be compounded.

You may repay the loan at any time. If there is any outstanding Loan Balance at the time of death of the

insured, the Loan Balance will be deducted from the death benefit paid to the beneficiary.

Loans must be requested in writing, except for loan interest capitalization or if the Automatic Premium

Loan provision is exercised.

Partial SurrEndErS or withdrawalS You may also withdraw amounts from the policy’s net cash value subject to face amount minimums. Partial

surrenders or withdrawals are subject to Company-imposed surrender charges and may reduce the death

benefit of the policy. Additionally, during the Required Premium Period, withdrawals may be limited.

Partial surrenders and surrender charges will be withdrawn from the Basic Interest Account first, then

pro rata from the Index Account Segments. Amounts removed from a Segment due to partial surrenders

will reduce the Index Interest that may otherwise be earned as of a Segment Anniversary.

Surrender Charges vary by issue age, gender, region, and underwriting class. The surrender charges

grade down over 10 years and end after the 10th policy year.

tranSamEriCa lifE (BErmuda) ltd.BErmuda adminiStratiVE offiCE P.o. Box 2274hamilton hm JxBermudafax: (441) 278-8559Email: [email protected]

TransExplorer Index UL (Policy Form No.IUL07) is a non-participating, flexible

premium index universal life insurance policy issued by Transamerica Life

(Bermuda) Ltd., incorporated in Hamilton, Bermuda. Insurance eligibility and

premiums are subject to underwriting. In the event of suicide during the first

two policy years, death benefits are limited only to the return of premiums paid.

This product guide provides highlights only. Please see the policy contract for details, including conditions and limitations.

TLB 326BM 0513LIFE BERMUDA LTD