Embed Size (px)

Citation preview

Thursday, 8 June 2017

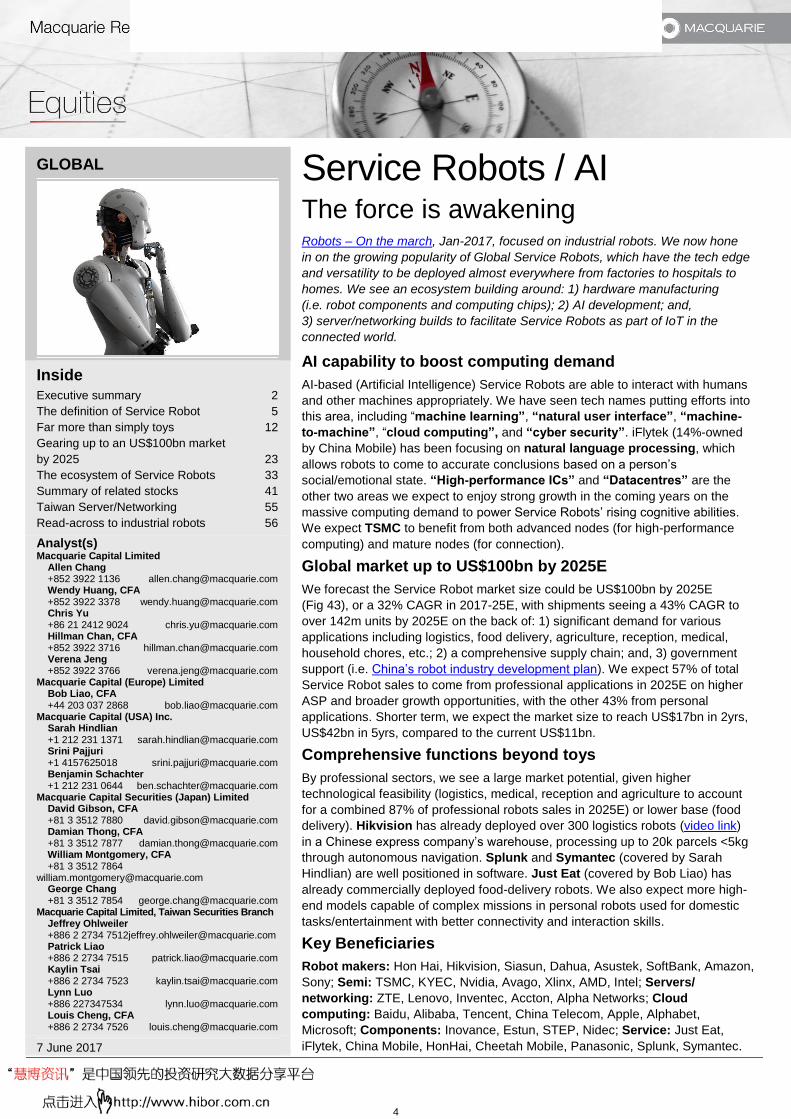

Service Robots / AI 4

The force is awakening Allen Chang

Robots – On the march, Jan-2017, focused on industrial robots. We now hone in on the growingpopularity of Global Service Robots, which have the tech edge and versatility to be deployed almosteverywhere from factories to hospitals to homes.

WH Group (Initiating coverage with Outperform) 5

Pigs can fly Linda Huang

We initiate coverage of WH Group with an Outperform rating and a target price of HK$9.90 based on15x FY18E PER, the company's peak cycle valuation. WH Group's share price has been under thepressure due to CDH Investment selling pressure, a pre-IPO investor.

Shuanghui (A-Share) (Initiating coverage with Outperform) 6

Dual engine to drive growth Linda Huang

We initiate coverage of Shuanghui with an Outperform rating and a target price of Rmb28.50 based on18x FY18E PER, the stock's peak cycle valuation. Shuanghui is China's leading vertical meatprocessing company with 18.8% packaged pork and 2.7% fresh pork market share.

Korea E&C 7

Turning cautious on property market James Hong

We are turning cautious on Korea's property market and this has implications for constructioncompanies. Korean construction companies should continue to enjoy strong earnings and cash inflowfrom the domestic housing business, but pre-sale volume and profitability, a function of property prices,is likely to slow down from late 2017.

LG Electronics (Outperform) 8

Flourishing, not floundering Daniel Kim

We ascertain LGE's earnings power to be real, but vastly understated in the market. Outperform.Quarterly OP growth on YoY basis to accelerate towards year-end.

Software & Robotics 9

JUST EAT (Outperform) 10

US Semiconductors 11

China Internet 12

The Future of Japanese Tech 13

SoftBank (Outperform) 14

Taiwan Server/Networking 15

Please refer to page 50 for important disclosures and analyst certification, or on our website www.macquarie.com/research/disclosures.

TSMC (Outperform) 16

Hon Hai (Outperform) 17

China Telecom (Outperform) 18

Hikvision (A-Share) (Outperform) 19

Lenovo (Outperform) 20

Asustek Computer (Outperform) 21

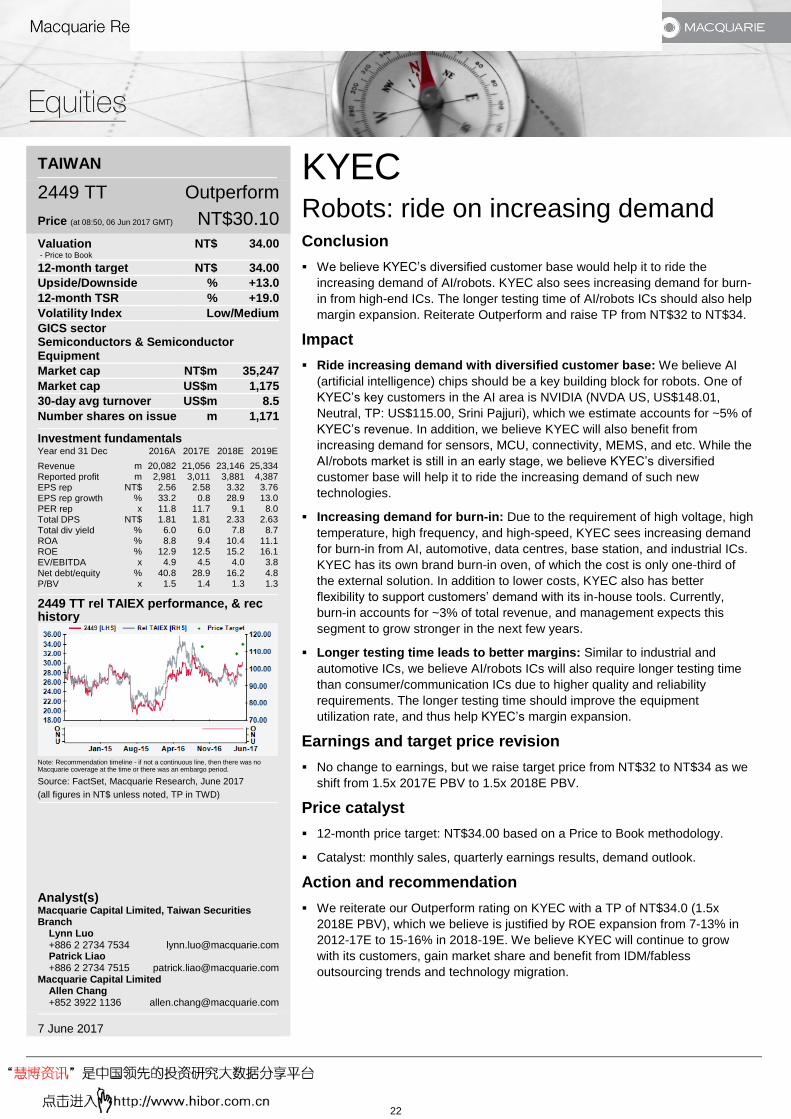

KYEC (Outperform) 22

Samsung C&T (Upgrade to Outperform) 23

Hyundai E&C (Outperform) 24

Daelim Industrial (Downgrade to Neutral) 25

Hyundai Development (Downgrade to Neutral) 26

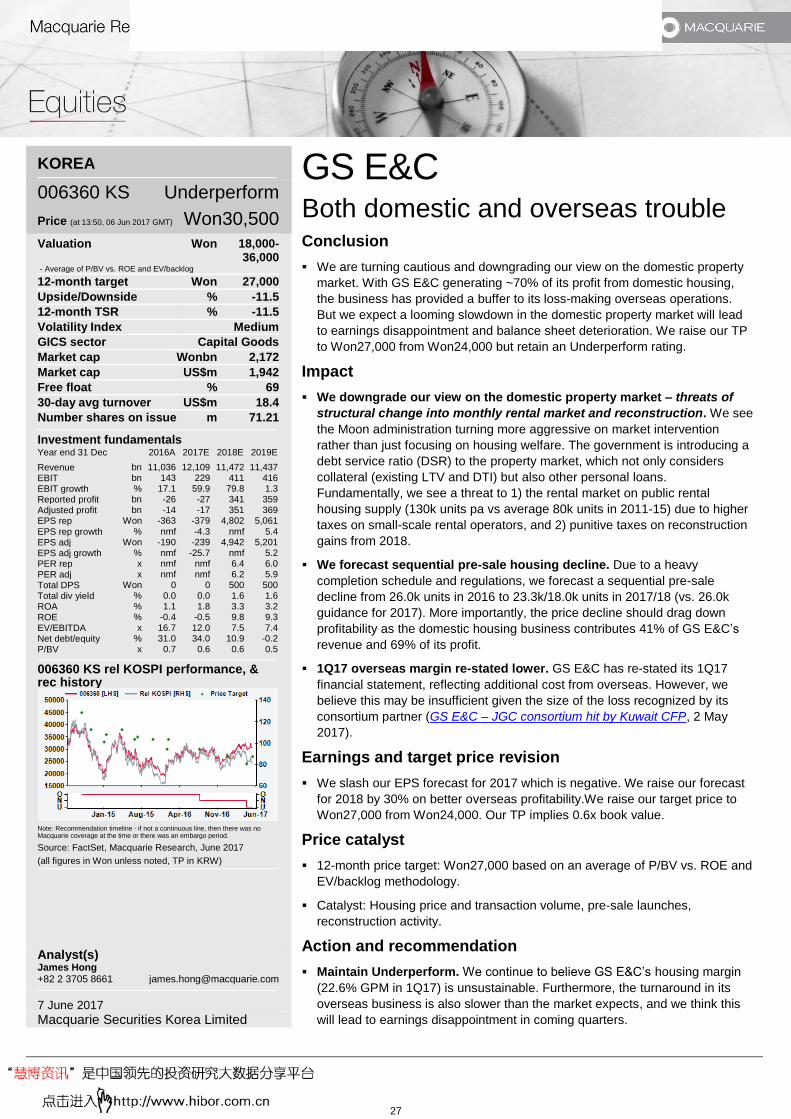

GS E&C (Underperform) 27

Brilliance China Automotive (Outperform) 28

Chongqing Changan Auto (B-Share) (Outperform) 29

Dongfeng Motor Group (Neutral) 30

Geely Automobile (Underperform) 31

Great Wall Motor Company (Outperform) 32

SAIC Motor (A-Share) (Outperform) 33

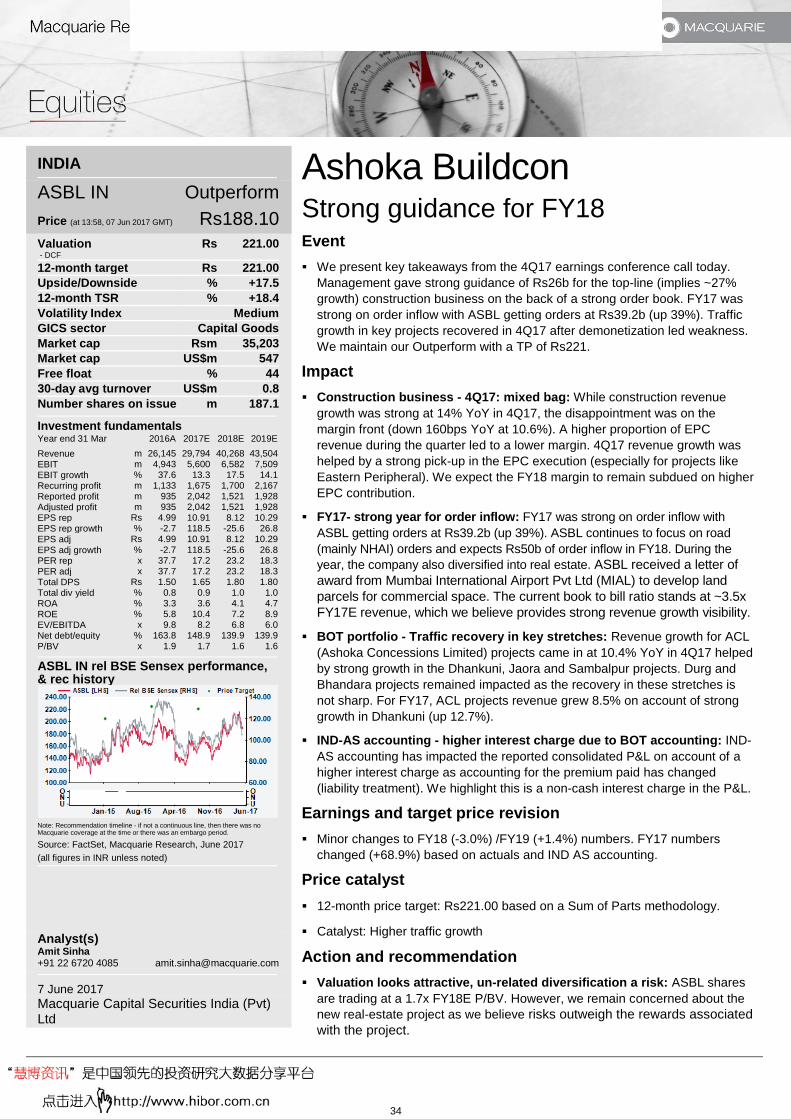

Ashoka Buildcon (Outperform) 34

BTS Growth Infrastructure Fund (Downgrade to Underperform) 35

Credit Saison (Neutral) 36

CUB (Outperform) 37

DeNA Co (Outperform) 38

Leshi Internet (A-Share) (Outperform) 39

2

Public Bank (Outperform) 40

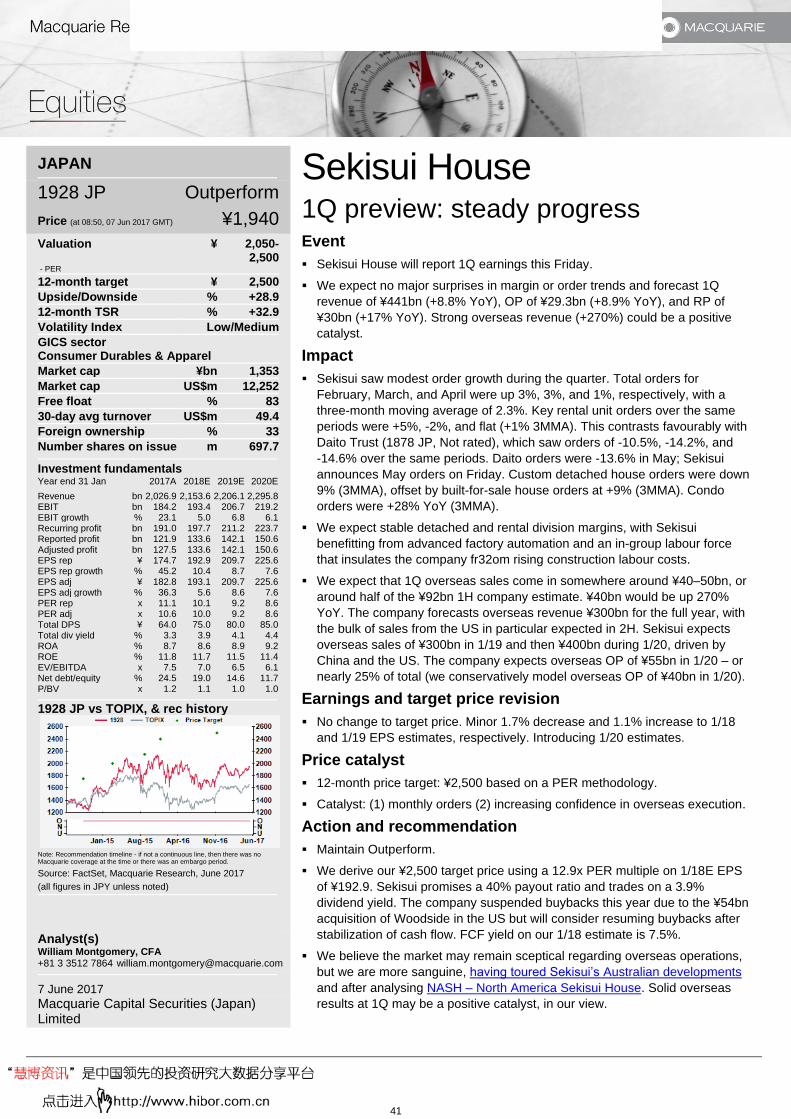

Sekisui House (Outperform) 41

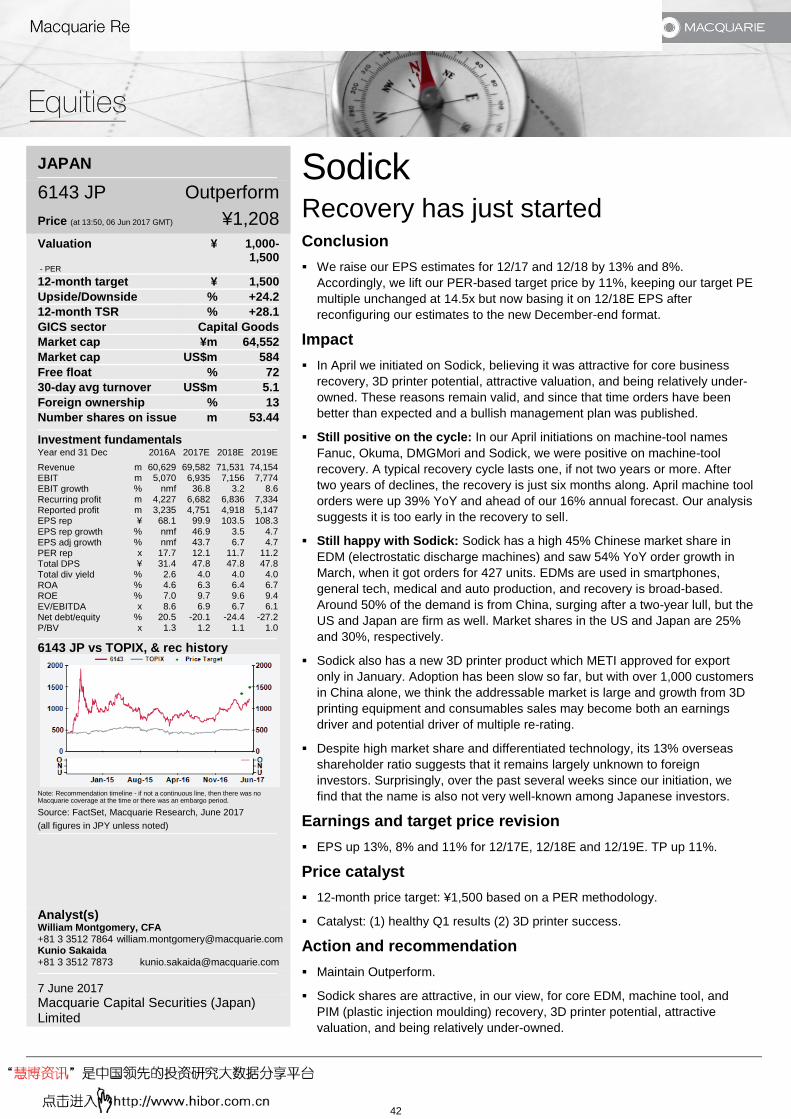

Sodick (Outperform) 42

Sumitomo Metal Mining (Neutral) 43

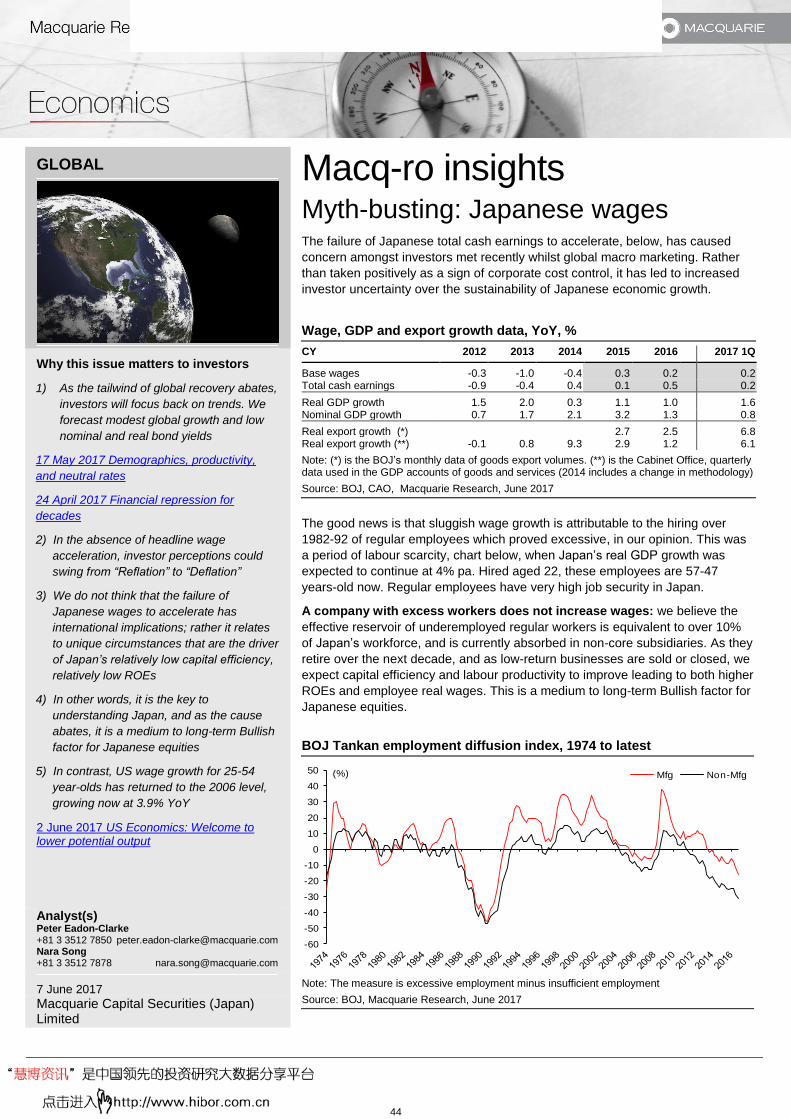

Macq-ro insights 44

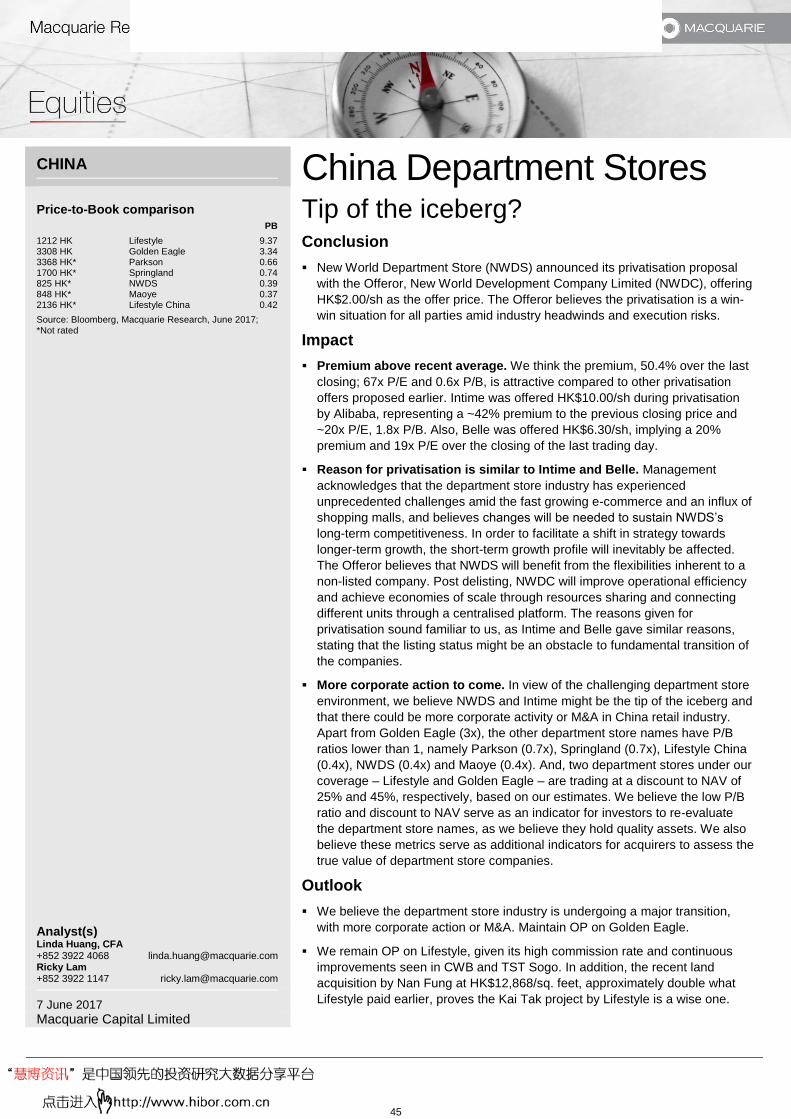

China Department Stores 45

India financials 46

Semiconductors Tracker 47

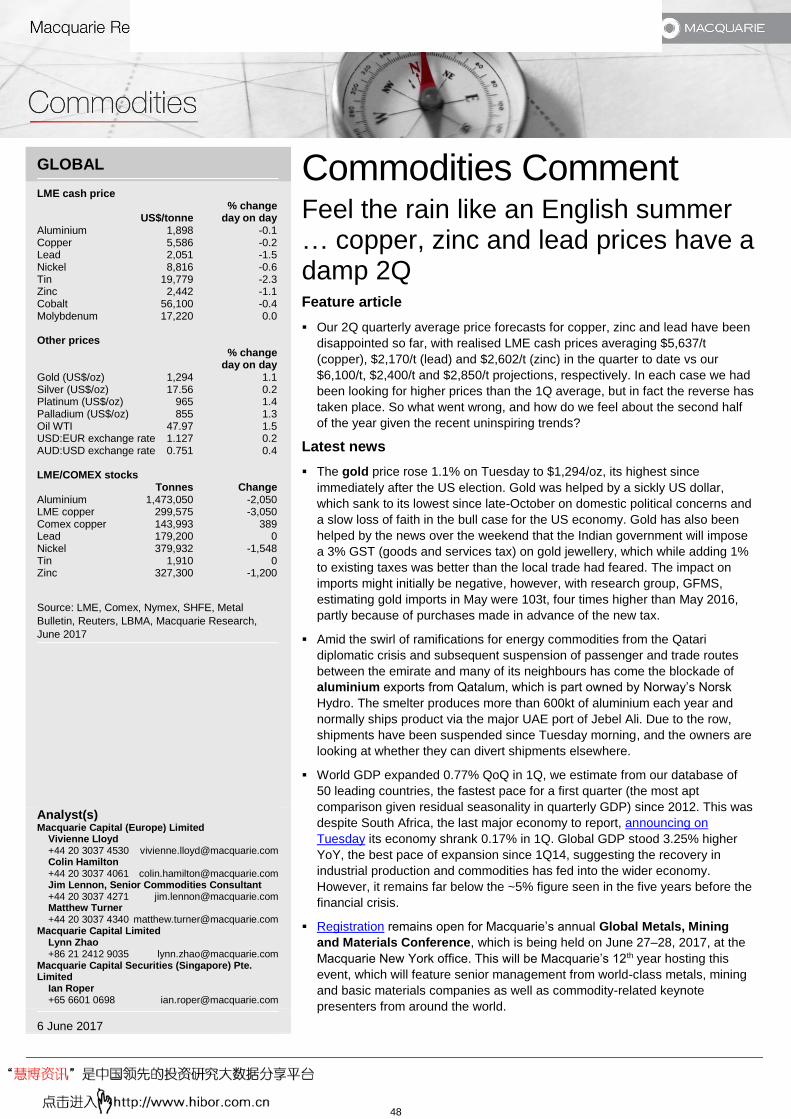

Macquarie Commodities Comment 48

Macquarie Commodities Comment 49

3

Please refer to page 144 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

GLOBAL

Inside

Executive summary 2

The definition of Service Robot 5

Far more than simply toys 12

Gearing up to an US$100bn market

by 2025 23

The ecosystem of Service Robots 33

Summary of related stocks 41

Taiwan Server/Networking 55

Read-across to industrial robots 56

Analyst(s) Macquarie Capital Limited Allen Chang +852 3922 1136 [email protected] Wendy Huang, CFA +852 3922 3378 [email protected] Chris Yu +86 21 2412 9024 [email protected] Hillman Chan, CFA +852 3922 3716 [email protected] Verena Jeng +852 3922 3766 [email protected] Macquarie Capital (Europe) Limited Bob Liao, CFA +44 203 037 2868 [email protected] Macquarie Capital (USA) Inc. Sarah Hindlian +1 212 231 1371 [email protected] Srini Pajjuri +1 4157625018 [email protected] Benjamin Schachter +1 212 231 0644 [email protected] Macquarie Capital Securities (Japan) Limited David Gibson, CFA +81 3 3512 7880 [email protected] Damian Thong, CFA +81 3 3512 7877 [email protected] William Montgomery, CFA +81 3 3512 7864 [email protected] George Chang +81 3 3512 7854 [email protected] Macquarie Capital Limited, Taiwan Securities Branch Jeffrey Ohlweiler +886 2 2734 [email protected] Patrick Liao +886 2 2734 7515 [email protected] Kaylin Tsai +886 2 2734 7523 [email protected] Lynn Luo +886 227347534 [email protected] Louis Cheng, CFA +886 2 2734 7526 [email protected]

7 June 2017

Service Robots / AI The force is awakening Robots – On the march, Jan-2017, focused on industrial robots. We now hone

in on the growing popularity of Global Service Robots, which have the tech edge

and versatility to be deployed almost everywhere from factories to hospitals to

homes. We see an ecosystem building around: 1) hardware manufacturing

(i.e. robot components and computing chips); 2) AI development; and,

3) server/networking builds to facilitate Service Robots as part of IoT in the

connected world.

AI capability to boost computing demand

AI-based (Artificial Intelligence) Service Robots are able to interact with humans

and other machines appropriately. We have seen tech names putting efforts into

this area, including “machine learning”, “natural user interface”, “machine-

to-machine”, “cloud computing”, and “cyber security”. iFlytek (14%-owned

by China Mobile) has been focusing on natural language processing, which

allows robots to come to accurate conclusions based on a person’s

social/emotional state. “High-performance ICs” and “Datacentres” are the

other two areas we expect to enjoy strong growth in the coming years on the

massive computing demand to power Service Robots’ rising cognitive abilities.

We expect TSMC to benefit from both advanced nodes (for high-performance

computing) and mature nodes (for connection).

Global market up to US$100bn by 2025E

We forecast the Service Robot market size could be US$100bn by 2025E

(Fig 43), or a 32% CAGR in 2017-25E, with shipments seeing a 43% CAGR to

over 142m units by 2025E on the back of: 1) significant demand for various

applications including logistics, food delivery, agriculture, reception, medical,

household chores, etc.; 2) a comprehensive supply chain; and, 3) government

support (i.e. China’s robot industry development plan). We expect 57% of total

Service Robot sales to come from professional applications in 2025E on higher

ASP and broader growth opportunities, with the other 43% from personal

applications. Shorter term, we expect the market size to reach US$17bn in 2yrs,

US$42bn in 5yrs, compared to the current US$11bn.

Comprehensive functions beyond toys

By professional sectors, we see a large market potential, given higher

technological feasibility (logistics, medical, reception and agriculture to account

for a combined 87% of professional robots sales in 2025E) or lower base (food

delivery). Hikvision has already deployed over 300 logistics robots (video link)

in a Chinese express company’s warehouse, processing up to 20k parcels <5kg

through autonomous navigation. Splunk and Symantec (covered by Sarah

Hindlian) are well positioned in software. Just Eat (covered by Bob Liao) has

already commercially deployed food-delivery robots. We also expect more high-

end models capable of complex missions in personal robots used for domestic

tasks/entertainment with better connectivity and interaction skills.

Key Beneficiaries

Robot makers: Hon Hai, Hikvision, Siasun, Dahua, Asustek, SoftBank, Amazon,

Sony; Semi: TSMC, KYEC, Nvidia, Avago, Xlinx, AMD, Intel; Servers/

networking: ZTE, Lenovo, Inventec, Accton, Alpha Networks; Cloud

computing: Baidu, Alibaba, Tencent, China Telecom, Apple, Alphabet,

Microsoft; Components: Inovance, Estun, STEP, Nidec; Service: Just Eat,

iFlytek, China Mobile, HonHai, Cheetah Mobile, Panasonic, Splunk, Symantec.

4

Please refer to page 30 for important disclosures and analyst certification, or on our website www.macquarie.com/research/disclosures.

HONG KONG

288 HK Outperform

Price (at 13:50, 06 Jun 2017 GMT) HK$7.58

Valuation HK$ 9.90 - PER

12-month target HK$ 9.90

Upside/Downside % +30.6

12-month TSR % +34.2

Volatility Index Low/Medium

GICS sector Food, Beverage & Tobacco

Market cap HK$m 111,055

Market cap US$m 14,253

Free float % 51

30-day avg turnover US$m 85.8

Number shares on issue m 14,651

Investment fundamentals Year end 31 Dec 2016A 2017E 2018E 2019E

Revenue m 21,534 21,408 22,354 23,596 EBIT m 1,665 1,826 2,041 2,154 EBIT growth % 6.9 9.7 11.8 5.6 Reported profit m 1,036 1,094 1,242 1,316 Adjusted profit m 1,036 1,094 1,242 1,316 EPS rep ¢ 7.1 7.5 8.5 9.0 EPS rep growth % 31.8 5.5 13.6 5.9 EPS adj ¢ 7.1 7.5 8.5 9.0 EPS adj growth % 31.8 5.5 13.6 5.9 PER rep x 13.8 13.0 11.5 10.8 PER adj x 13.8 13.0 11.5 10.8 Total DPS ¢ 3.4 3.5 4.0 4.2 Total div yield % 3.4 3.6 4.1 4.4 ROA % 11.9 13.5 14.4 14.0 ROE % 17.2 16.3 16.3 15.3 EV/EBITDA x 7.7 7.1 6.4 6.1 Net debt/equity % 24.7 11.1 -2.3 -12.0 P/BV x 2.3 2.0 1.8 1.6

Source: FactSet, Macquarie Research, June 2017

(all figures in USD unless noted, TP in HKD)

Analyst(s) Linda Huang, CFA +852 3922 4068 [email protected] Sunny Chow +852 3922 3768 [email protected]

7 June 2017 Macquarie Capital Limited

WH Group Pigs can fly We initiate coverage of WH Group with an Outperform rating and a target price

of HK$9.90 based on 15x FY18E PER, the company’s peak cycle valuation. WH

Group’s share price has been under the pressure due to CDH Investment selling

pressure, a pre-IPO investor. Post CDH’s recent divestment its stake is down to

3.24% and we believe the share price overhang has been removed.

WH Group’s China operations should rebound for the rest of the year and should

benefit long term from China’s consumption upgrading trend. The Smithfield

operation remains on the right track to deliver efficiency improvements. We

believe it is a good time to accumulate shares given its long-term growth outlook.

We expect WH Group net profit to grow by 5.6% and 13.6% in 2017 and 2018,

respectively. In addition to WH Group, we also initiate coverage of Shuanghui

(000895 CH, Rmb22.11, OP, TP: Rmb28.50) with an Outperform rating (LINK).

China growth drivers: premiumization, declining hog prices

WH Group’s China operations entity, Shuanghui, continues to promote low-

temperature products to catch up with the rising consumption upgrading trend.

We project low temperature product revenue contribution to the downstream

packaged meat business should pick up from 38% last year to 41% in 2017.

Meanwhile, margins are poised to expand at Shuanghui since China hog prices

have come down from a peak of Rmb21/kg in May 2016 to Rmb13/kg now. Its

fresh pork business should benefit from both volume and margin expansion. We

forecast the China operation will grow by 5.0% in 2017 to US$904m, accounting

for 43% of group operating profit.

US market riding efficiency improvements

The company kicked off its restructuring in 2015 and generated a rewarding

outcome as the US operating profit margin improved from 6.7% in 2015 to 8.4%

in 2016. The restructuring is ongoing as the company consolidates the brand

portfolio, while the SAP integration benefit should fully emerge in 2018. We

expect US OPM will further improve to 9.7% in 2018. For its fresh pork business,

profit growth should normalize from 2017 given that the China/US pork price gap

is narrowing.

Strong cash generation to lower gearing, higher payout and M&A

WH Group’s balance sheet keeps improving and we forecast it will see net cash

in 2018. This helps interest savings by US$50m/US$25m in 2017/2018,

respectively, contributing 2.8%/1.2% incremental profit growth in these two

years. The continuous strong cash generation ability offers dividend payout

upside while the cash could serve as the basis for future M&A. We expect it can

maintain a 50% payout, implying 4% dividend yield. Management will likely still

look for M&A opportunities to further strengthen its leading position in the global

animal protein market and ride emerging markets’ consumption upgrading trend.

The strong cash position can serve well as non-organic growth in the long run.

Risks

Food safety scandals; hog-related diseases; a US pork import ban into China.

5

Please refer to page 19 for important disclosures and analyst certification, or on our website www.macquarie.com/research/disclosures.

CHINA

000895 CH Outperform

Price (at 13:50, 06 Jun 2017 GMT) Rmb22.11

Valuation Rmb 28.50 - PER

12-month target Rmb 28.50

Upside/Downside % +28.9

12-month TSR % +35.0

GICS sector Food, Beverage & Tobacco

Market cap Rmbm

72,953

Market cap US$m 10,703

Free float % 22

30-day avg turnover US$m 34.6

Number shares on issue m 3,300

Investment fundamentals Year end 31 Dec 2016A 2017E 2018E 2019E

Revenue m 51,822 51,397 53,083 54,633 EBIT m 5,592 6,146 6,562 6,594 EBIT growth % 4.3 9.9 6.8 0.5 Reported profit m 4,405 4,810 5,217 5,349 Adjusted profit m 4,405 4,810 5,217 5,349 EPS rep Rmb 1.33 1.46 1.58 1.62 EPS rep growth % -13.7 9.2 8.5 2.5 EPS adj Rmb 1.33 1.46 1.58 1.62 EPS adj growth % -13.7 9.2 8.5 2.5 PER rep x 16.6 15.2 14.0 13.6 PER adj x 16.6 15.2 14.0 13.6 Total DPS Rmb 2.10 1.36 1.47 1.51 Total div yield % 9.5 6.1 6.7 6.8 ROA % 25.3 28.5 29.5 28.2 ROE % 28.4 32.7 33.3 32.5 EV/EBITDA x 10.8 10.0 9.4 9.3 Net debt/equity % -14.9 -17.4 -24.3 -24.6 P/BV x 5.1 4.8 4.5 4.3

Source: FactSet, Macquarie Research, June 2017

(all figures in Rmb unless noted)

Analyst(s) Linda Huang, CFA +852 3922 4068 [email protected] Sunny Chow +852 3922 3768 [email protected]

7 June 2017 Macquarie Capital Limited

Shuanghui (A-Share) Dual engine to drive growth We initiate coverage of Shuanghui with an Outperform rating and a target price

of Rmb28.50 based on 18x FY18E PER, the stock’s peak cycle valuation.

Shuanghui is China’s leading vertical meat processing company with 18.8%

packaged pork and 2.7% fresh pork market share. Shuanghui will accelerate its

earnings growth this year with fresh pork volume growth from lower pork prices,

margin expansion from the hog price correction and the long term consumption

upgrading trend.

Global meat processor companies valuation currently averages at 14x PER with

low-mid single digit profit growth (by taking out outliers), 20-25% ROE and 1.0-

1.5% dividend yield. Shuanghui stands out with 9.2% YoY FY17E net profit

growth, ~33% ROE and a 6% dividend yield. We strongly believe its high

valuation is justified and the market will rerate the stock.

Fresh pork benefits from volume growth and margin expansion

Based on MQ proprietary pork supply and demand model (p.13, Fig 26), we

expect China pork production to grow 2.0% YoY from 3.2%/3.4% decline

respectively in 205/2016 due to hog farmers’ healthy profit margin and rising hog

stock. China hog prices have peaked out at Rmb21/kg in May 2016 to Rmb13/kg

now. Shuanghui can benefit from the lower pork price as this can stimulate more

consumption demand. Shuanghui recorded 1.4% fresh pork volume growth in

1Q17 and it can achieve full year +10.2% YoY volume growth, implying strong

volume growth recovery for the rest of the year. Margin wise, given that pork

prices usually lag behind the hog price trend, we expect the company is in the

sweet spot with margin expansion. We project fresh pork GPM to expand 1.6ppt

YoY to 7% this year.

Premiumization is the right direction, though it takes time

In light of rising living standard and disposal income, Shuanghui concentrates on

low temperature package meat development and we expect a revenue

contribution from the downstream package meat business to pick up from 38%

last year to 41%. The company has a unique advantage of leveraging the

China/US pork price gap by importing US pork into China as the input cost.

Since WH Group acquired Smithfield in 2013, US imported pork as the raw

materials input has risen from 3% in 2014 to 16% in 2016. We believe this

effectively stabilizes the company’s downstream meat GPM even though the hog

price skyrocketed in 2016.

High dividend payout from the solid cash position and FCF

Shuanghui has very lean A/R turnover days less than one day, while inventory

turnover and A/P turnovers remain steady at ~30 days and ~20 days

respectively. We project the FCF yield at 6% and 8% for 2017/2018. Due to the

strong cash position and cash generation ability, the company has been

adopting the high payout policy. While the company has not committed a payout

ratio, we believe a 90% payout ratio is an achievable target. This implies a 6%

dividend yield.

Risks

Foods safety scandal; hog related disease; US pork import ban into China.

6

Please refer to page 27 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

KOREA

Annual pre-sale volume

Source: REPS, Company data, Macquarie Research, June 2017

Housing exposure (2018E)

Source: Company data, Macquarie Research, June 2017

Stocks for action Market cap TP

new TP

old

TSR

Company Ticker Rec (US$bn) (won) (won) (%)

Samsung Engineering

028050 OP 2.2 17k 17k 37.1

Samsung C&T 028260 OP 24.2 169k 165k 18.2

Hyundai E&C 000720 OP 4.7 53k 54k 13.1

Daelim Industrial

000210 N 2.8 100k 105k 9.9

HDC 012630 N 3.3 52k 70k 3.8

GS E&C 006360 UP 1.9 27k 24k -11.5

Source: Macquarie Research, June 2017

Changes in estimates

Ticker Chg in 17E EPS (%)

Chg in 18E EPS (%)

Samsung Engineering 028050 0.0 0.0

Samsung C&T 028260 -22.5 -19.4

Hyundai E&C 000720 -9.3 -4.1

Daelim Industrial 000210 31.3 -10.3

HDC 012630 -14.2 -31.0

GS E&C 006360 nmf 30.0

Source: Company data, Macquarie Research, June 2017

Samsung C&T 7 Hyundai E&C 11 Daelim Industrial 15 Hyundai Development 19 GS E&C 23

Analyst(s) James Hong +82 2 3705 8661 [email protected]

7 June 2017 Macquarie Securities Korea Limited

Korea E&C Turning cautious on property market Conclusion

We are turning cautious on Korea’s property market and this has implications

for construction companies. Korean construction companies should continue

to enjoy strong earnings and cash inflow from the domestic housing business,

but pre-sale volume and profitability, a function of property prices, is likely to

slow down from late 2017.

We downgrade Hyundai Development and Daelim Industrial to Neutral and

reiterate our Underperform rating on GS E&C. At the same time, we are

upgrading Samsung C&T to Outperform in view of its investment holdings.

Impact

We turn cautious on property market. The Moon administration is turning

more aggressive in market intervention rather than just housing welfare. It is

introducing debt service ratio (DSR) requirements, taking into account not

only collateral (such LTV and DTI, which are already taken into account) but

also other personal lending. This may hurt market sentiment, but not so much

fundamentals, as LTV and DTI are already low at 50%. Fundamentally, we

see a threat to the rental market and reconstruction, which we believe have

been the main drivers for structural changes in Korea’s property market.

Rental market threatened by public rental housing supply and taxes. The

new government is considering a bigger role in public housing: it plans to

increase annual construction of rental housing units from an annual average

of 80,000 over 2011-2015 to 130,000 by 2018. This should lower rental yield.

Furthermore, a temporary waiver on taxes levied on small-scale rental

business operators will expire at the end of 2018.

Reconstruction to peak out in 2017. We believe the current strength in the

Seoul metropolitan property market is due solely to one factor: developers

advancing their reconstruction activity in a bid to avoid taxes on excess gains

that are likely to be levied from 2018. Punitive taxes on reconstruction can

incentivize redevelopment or remodelling, where overall size of order to

construction companies is much smaller.

Construction companies remain bullish on Korean property market.

Managements of construction companies remain bullish as their underlying

profitability in housing business is still far above their long-term average. With

strong cash inflow expected till 2018 (as a result of successful pre-sale till

2016), construction companies are investing back into the housing business,

securing larger land banks. This, we believe, will cause a bigger downturn

once property prices start to contract, dragging down sustainable ROEs.

Outlook

We downgrade our ratings on construction companies with exposure to

housing—Hyundai Development and Daelim Industrial—to Neutral. We

cut volume and margin assumptions for their housing business order intake.

We are keeping Underperform rating on GS E&C, which has room to

disappoint from both domestic housing and overseas plant businesses.

We prefer Samsung Engineering and Samsung C&T. We upgrade

Samsung C&T to Outperform on investment holding value. We maintain

Outperform ratings on Samsung Engineering and Hyundai E&C.

-40%

-20%

0%

20%

40%

60%

0

100

200

300

400

500

600

200

8

200

9

201

0

2011

201

2

201

3

201

4

201

5

201

6

201

7E

201

8E

('000 units)

Seoul-metopolitan Provincial

YoY change (RHS)

53%

41%

31%

17%

6%

0%0%

10%

20%

30%

40%

50%

60%

HDev GS Daelim HEC SC&T SEng

(% revenue)

7

Please refer to page 14 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

KOREA

066570 KS Outperform

Price (at 06:41, 07 Jun 2017 GMT) Won85,300

Valuation Won 100,000 - Price to Book

12-month target Won 100,000

Upside/Downside % +17.2

12-month TSR % +17.8

Volatility Index Medium

GICS sector Consumer Durables & Apparel

Market cap Wonbn

15,422

Market cap US$m 14,115

Free float % 66

30-day avg turnover US$m 68.1

Number shares on issue m 180.8

Investment fundamentals Year end 31 Dec 2016A 2017E 2018E 2019E

Revenue bn 55,367 58,702 60,511 64,302 EBIT bn 1,338 2,837 3,047 3,169 EBIT growth % 12.2 112.1 7.4 4.0 Reported profit bn 126 1,805 1,955 1,971 Adjusted profit bn 77 1,741 1,761 1,650 EPS rep Won 699 9,984 10,810 10,897 EPS rep growth % -50.0 1,327.7 8.3 0.8 EPS adj Won 426 9,628 9,736 9,123 EPS adj growth % -68.2 2,160.6 1.1 -6.3 PER rep x 122.0 8.5 7.9 7.8 PER adj x 200.3 8.9 8.8 9.4 Total DPS Won 400 500 600 600 Total div yield % 0.5 0.6 0.7 0.7 ROA % 3.6 7.4 7.6 7.3 ROE % 0.7 13.9 12.7 10.8 EV/EBITDA x 5.4 4.1 4.1 4.1 Net debt/equity % 42.3 21.8 14.0 11.2 P/BV x 1.3 1.2 1.1 1.0

066570 KS rel KOSPI performance, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, June 2017

(all figures in Won unless noted, TP in KRW)

Analyst(s) Daniel Kim +82 2 3705 8641 [email protected] Ryan Kim +82 2 3705 8771 [email protected]

7 June 2017 Macquarie Securities Korea Limited

LG Electronics Flourishing, not floundering Event

We ascertain LGE’s earnings power to be real, but vastly understated in the

market. Outperform.

Impact

Quarterly OP growth on YoY basis to accelerate towards year-end. We

estimate OP will rise 33%YoY to Won779bn in 2Q17, despite the likely bigger

losses in Handset division. Higher losses in Handset, in our view, are not

alarming, as the company made a strategic decision to spend on marketing.

3Q17 OP, we estimate, will be more than 2x the year-ago period’s.

Home Appliance: moving up the value ladder + globally synchronized

economic recovery. LGE’s premium brand strategy seems to be paying off,

while the module approach helps keep costs low. Its new products (electricity

dryer and air-purifier) are well-received by local consumers, who are

increasingly aware of fine-dust and air quality issues. LGE’s household

appliances command better margins than global peers’ (Electrolux and

Whirlpool).

Emerged as the leader in premium TV segment. We expect LGE to grow

the proportion of premium models—OLEDs and UHD TVs—from 50% in 2016

to 70% in 2017. We believe the TV segment’s annual profit of over Won1.0tr

is sustainable in light of rising high-end TV sales and the likely stabilizing, if

not falling, LCD TV panel prices. Notably, Consumer Report in the US rated

eight of LG’s OLED TV models among the top 10 TVs.

Earnings growth story is beyond 2017. The Handset division targets to cut

losses by Won1.0tr this year, thanks not only to the absence of one-off

expenses but also lower overhead cost. More importantly, sales of premium

phones (G and V series) should normalize from 2018, improving the

prospects of a turnaround. Moreover, VC (vehicle component) division should

have critical mass next year big enough to cover its investment burden. That

should set its earnings growth story well on course to continue in 2018.

Earnings and target price revision

We have fine-tuned our above-consensus 2017/18 OP forecasts.

No change in target price of Won100,000, or 1.2x 2018E book-value.

Price catalyst

12-month price target: Won100,000 based on a Price to Book methodology.

Catalyst: 2Q17 earnings release. Potential turnaround in Handset division

Action and recommendation

Despite the strong rally year to date (68% versus KOSPI’s 17%), we see more

upside to the share price in light of the prevailing scepticism in the market.

LGE’s PE of 9x looks attractive for its historic trading range and its global

peers. Based on SOTP (sum-of-the-part) valuation, LGE looks more under-

valued, even if we assign zero value to its MC and VC divisions and gives 12x

PE multiple to HA/HE profits. SOTP-based fair value suggests Won130,000.

Outperform.

8

Please refer to page 28 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

NORTH AMERICA

Inside

Robotics Rising – $100bn CY25e TAM 2

Microsoft Executive Summary,

Valuation, Risks and Estimates 7

Splunk Executive Summary,

Valuation, Risks and Estimates 14

Symantec Executive Summary,

Valuation, Risks and Estimates 21

Analyst(s) Sarah Hindlian +1 212 231 1371 [email protected] Frederick Havemeyer +1 212 231 1830 [email protected] David Yueh +1 212 231 8079 [email protected]

7 June 2017 Macquarie Capital (USA) Inc.

Software & Robotics Robotics Rising – $100bn CY25e TAM In conjunction with our colleagues in Asia who are evaluating a growing

trend of robotics usage and mining through the emerging trend of Service

Robots, we examine the potential impact of rising demand for this

technology on software spending and the companies within our coverage

that stand to benefit. In our broader Macquarie thematic report on the

Service Robot industry, we forecast it will represent a very large and

difficult to ignore ~$100bn TAM by CY’25e, with a 32% CY’17-CY’25 CAGR.

Service Robots Moving Beyond Factory Floors – Generating Data, More Robust AI Software & Services

Compared to Industrial Robots, Service Robots have embedded AI (Artificial

Intelligence) to enable reactions according to the environment or users’

behaviours. Service Robots are also required to understand users’ preferences

and expectations, accumulating the data to facilitate capabilities through time

(aka machine learning). Robotics and AI have long been synonymous and the

focus of innumerable science fiction stories and hyperbolic reports in the media,

and robots are not a new phenomenon. However, Service Robots are

increasingly more than just clumsy machines operating in production lines. We

believe that the progressively substantial data being generated by robots

enables software vendors to provide products and services that leverage this

data to generate value by optimizing and orchestrating operations, and

improving artificial intelligence models.

Artificial Intelligence, IoT and Cloud-Scale Data Analytics

AI software is a foundational technology for Service Robots, enabling a wide

range of capabilities from understanding human speech to recognizing images.

Unlike other robots, Service Bots require advanced software to operate. Like

other robots, Service Bots will increasingly be generating data that needs to be

analyzed and interpreted. We believe that the expanding Service Robot

ecosystem is best viewed as a fundamental component of the larger IoT

landscape as internet-connected Service Robots interface with the cloud to

benefit from cloud-scale AI capabilities, while we expect that the vast quantities

of data generated by Service Robots will require large scale big data ingestion

and analytics capabilities.

Picks for the Rise of the Machines – MSFT, SPLK & SYMC

We consider the rise of robots to be tied to three investment areas: 1) bots will

create more data to be used for better software applications which will require

scale cloud services and robust data models; 2) bots are likely to need

sophisticated software, which we expect hardware vendors to have to develop;

and 3) bots will require more security to prevent against attacks. We note that

Microsoft (MSFT US, US$72.28, Neutral, TP: US$66.00) is well positioned to

benefit with its portfolio of AI services, IoT device management, data analytics,

and cloud-based ML models. We expect Splunk (SPLK US, US$62.56,

Outperform, TP: US$74.00) to benefit from increasing quantities of machine data

generated by fleets of robots that require data aggregation, correlation and

analysis. We think the demand for security for service robots and IoT devices in

general should benefit Symantec (SYMC US, US$30.07, Outperform, TP:

US$36.00) given the company’s robust security portfolio, which includes a suite

of customizable embedded IoT security solutions.

9

Please refer to page 7 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

UNITED KINGDOM

JE/ LN Outperform

Price (at 00:39, 03 Jun 2017 GMT) £6.70

Valuation £ 7.30 - DCF (WACC 8.5%, beta 1.2, ERP 5.5%, RFR 2.0%, TGR 2.5%)

12-month target £ 7.30

12-month TSR % +9.0

GICS sector Software & Services

Market cap £m 4,548

Market cap US$m 5,867

30-day avg turnover £m 25.6

Number shares on issue m 679.3

Investment fundamentals Year end 31 Dec 2016A 2017E 2018E 2019E

Revenue m 375.7 494.9 586.0 673.6 EBITDA m 115.3 163.8 223.6 280.4 EBITDA growth % 93.1 42.1 36.5 25.4 EPS adj £ 0.15 0.17 0.25 0.26 PER adj x 45.5 39.0 27.0 25.4 EV/EBITDA x 38.3 27.8 20.4 16.3

JE/ LN vs FTSE 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, June 2017

(all figures in GBP unless noted)

Analyst(s) Macquarie Capital (Europe) Limited Bob Liao, CFA +44 203 037 2868 [email protected] Macquarie Capital Limited Allen Chang +852 3922 1136 [email protected] Chris Yu +86 21 2412 9024 [email protected]

7 June 2017

JUST EAT I, Deliver Event

We are optimistic on delivery robots. Delivery robots are already commercially

deployed, they are technically capable and practical and they are expected to

be lower cost and more efficient that human delivery. We forecast global

delivery robot shipments rise from 600 in 2017 to 185,900 shipments in 2022.

We believe adoption of robot delivery services would increase Just Eat’s

market share, profitability and addressable market.

Impact

Delivery robots could be economically disruptive. Starship, a leading delivery

robot provider, is targeting a price of only £1, €1 or €1 per delivery, well below

the cost of human delivery services. In addition, Starship estimates that a van

with eight robots can more than double traditional delivery capacity.

We believe such economics could allow Just Eat to level the playing field

against its competitors with human logistics networks. Just Eat could

eventually match or better competitors’ human delivery services with efficient,

integrated and cost competitive robot delivery services.

We believe low cost robot delivery services should also increase Just Eat’s

margins with branded and chain restaurants and allow it to target previously

uneconomic customers, thereby expanding its addressable market.

Delivery robots are already being rolled out. Just Eat’s robot delivery service

has progressed beyond trials and the company now has tens of robots in

operation with plans to roll out across Britain.

Robots from Starship, a leading supplier used by Just Eat, have driven

132,000 miles and encountered over three million people without incident.

Delivery robots are backed by impressive individuals and companies. Starship

was founded by Skype co-founders Ahti Heinla and Janus Friis in 2014 and

Mercedes Benz has invested $17m in the company.

Earnings and target price revision

We raise our long term forecasts, DCF valuation and target price to £7.30

from £6.70.

Price catalyst

12-month price target: £7.30 based on a DCF methodology.

Catalyst: Interim results on 27 July

Action and recommendation

Digital takeaway is the most underpenetrated of all vertical marketplaces that

we cover and Just Eat is the clear market leader, in our view, in many of the

most attractive takeaway markets in the world. As a result, we expect the

company to readily sustain double digit revenue growth and higher profit

growth over the next few years. We reiterate our Outperform

recommendation.

10

Please refer to page 3 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

UNITED STATES

Analyst(s) Srini Pajjuri +1 4157625018 [email protected]

7 June 2017 Macquarie Capital (USA) Inc.

US Semiconductors Implications from Service Robot Growth Nearly 150m unit opportunity by 2025

Macquarie’s global technology team published a detailed report on the emerging

trend of Service Robots (see Service Robots – The Force is Awakening). We

expect the service robot market size to approach 150m units by 2025, which

should drive incremental demand for the semiconductor industry. While robot

unit growth will help IC demand, the ecosystem and infrastructure needed to

facilitate these robots is another driver. In particular, we believe semiconductor

components that enable artificial intelligence (AI/ML), connectivity, and sensing

are well positioned. AI/ML is already driving strong growth at NVIDIA, and we

expect AMD, Broadcom, Intel, and Xilinx to also benefit from this trend in the

coming years.

Machine Learning is compute-intensive

AI-based Service Robots with cognitive capabilities could make it possible to

automate many tasks that were long regarded as impossible for machines to

perform. Initial focus for the industry is on training neural networking models that

enable cognitive capability in machines. Deep learning, which is an advanced

form of machine learning, is highly compute-intensive and is already driving

significant innovation in the semiconductor market. Graphics processing units

(GPUs) with their massively parallel computing capability currently dominate

deep learning applications on the training front. We expect GPUs to maintain

their lead in training AI models while FPGAs, custom ASICs, and CPUs appear

better suited for on-field inferencing tasks.

Analog, sensing, and connectivity ICs will also benefit

Similar to today’s consumer drones, service robots will have the ability to sense,

perceive, communicate, move (or fly), and control. In most cases, these

machines will be untethered, requiring a portable power source. We expect IC

vendors that supply 5G, WiFi, image processing, sensing, motor control, and

battery management components to be the key beneficiaries. While the Semi

content will likely be lower than that of a self-driving car, the Service Robot unit

opportunity could be much bigger given their applicability across industries

including medical, agriculture, transportation, military, and entertainment.

NVDA, AVGO, INTC, XLNX, and AMD are key beneficiaries

The service robot eco-system is coming together with advances in machine

learning software and robotics engineering. Initial investments are focused on

training models that perform human-like tasks (such as facial and voice

recognition). The AI/ML semiconductor market is still relatively small today but

NVIDIA’s early success shows that IC companies with right exposure could see

a significant benefit. We expect GPUs to dominate the training side of machine

learning in the near term. Once the models are trained, the compute intensity

needed to “infer” from data goes down significantly. We believe FPGAs, CPUs,

and custom ASICs are better suited for inferencing tasks as a result. While

NVDA should continue to benefit from this trend, our top pick in US Semis is

AVGO due to its dominant franchises in connectivity and cloud infrastructure,

growing exposure toAdvanced Micro Devices AI/ML, and attractive valuation.

11

Please refer to page 3 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

CHINA/UNITED STATES

Baidu’s driverless car

Source: Company data, June 2017

Alibaba’s AI applications

Source: Company data, June 2017

Companies mentioned:

Baidu, BIDU US, US$187, N, TP: US$189

Alibaba, BABA US, US$125, OP, TP: US$142

Tencent, 700 HK, HK$274, OP, TP: HK$304

Cheetah Mobile, CMCM US, US$12, OP, TP: US$11.5

Kingsoft, 3888 HK, HK$21, OP, TP: HK$28.5

Softbank, 9984 JP. ¥8,949, OP, TP: ¥10,900

Analyst(s) Wendy Huang, CFA +852 3922 3378 [email protected] Hillman Chan, CFA +852 3922 3716 [email protected] Joe Yu +852 3922 1160 [email protected] Ivy Luo +852 3922 1507 [email protected]

7 June 2017 Macquarie Capital Limited

China Internet Embracing AI and robotics Baidu focuses its future on AI

Chinese leader in the AI space. Baidu, as China’s largest search engine, has

seen its investment in AI accelerate since hiring Dr. Lu Qi as the new Chief

Operating Officer in Jan 2017. It currently operates four research labs

(Augmented Reality, AI, Deep Learning, and Big Data) across Beijing and Silicon

Valley. Some of its AI technology, such as speed and image recognition, is

world-leading. The AI has been applied to Search, Duer (similar to Siri),

Autonomous Driving, Cloud and other products. Driverless cars are

approaching the commercialization stage. Among the AI-enabled products

within Baidu, driverless cars present the best growth and commercialization

opportunities. It has merged its L3 (eyes off) and L4 (mind off) autonomous

driving business into a single group (IDG) which is now led by Lu Qi. Baidu

launched the “Apollo Project” in April 2017 to open its autonomous driving

platforms (hardware + software + cloud) to car manufacturers to develop

autonomous vehicles. Baidu has already partnered with local OEMs incl. Cherry,

BYD and BAIC Motor. In terms of development timeline, Baidu plans to share its

technology for simple urban road conditions by the end of 2017, with the ultimate

goal of being fully autonomous on highways and open city roads by 2020.

Alibaba embeds AI across businesses

Empowering e-Commerce and cloud. Alibaba is building up AI on large-scale

computing power and data, and is exploring the potential to embed AI into

various business lines. For its core e-commerce, Alibaba is applying AI

algorithms to shopping experience, to upgrade supply chain management, and

to improve logistics efficiency; Alibaba Cloud is introducing AI services to

healthcare and manufacturing companies; and Alibaba’s affiliate Ant Financial is

working on face-recognition technology to secure e-payments. Cooperation

with business partners. In addition, Ant Financial acquired EyeVerify in Sep

2015 for its biometric authentication technology. EyeVerify checks identities

through eye-vein patterns and creates digital eye print IDs. Alibaba has also

established Alibaba Robotics, a joint venture with SoftBank, to operate the

Pepper robot business in China. Softbank has sold 10,000 Pepper robots in the

Japanese market. In China, Pepper will be powered by Alibaba’s YunOS

operating system and will help scan traveller ID cards and print boarding passes.

Tencent playing catch-up on AI

Boosting AI lab and R&D capabilities. Among BAT, Tencent started relatively

late in the field of AI. But it has been boosting its R&D talents since 2016.

Tencent recently opened an artificial intelligence research facility in Seattle, US,

to be led by former Microsoft scientist Yu Dong. This will strengthen its AI

capabilities in addition to the existing AI lab of about 50+ researchers and 200+

engineers in Shenzhen. Voice, AI open source and cloud collaboration.

Tencent launched its Alexa-like AI voice assistant Dingdang in Apr 2017.

Tencent will integrate Dingdang into its apps and ecosystem with services

including weather, news, music and LBS. Further, Tencent plans to open source

its AI computing platform called Angel with a focus on machine learning

techniques. Tencent applies them internally in areas such as video streaming

and social ads. In terms of Tencent Cloud, its offering comes with AI services

including face detection and optical character recognition, and Tencent recently

adopted NVIDIA Tesla for AI cloud computing.

Artificial Intelligence Algorithms

Smart Product Search and

Recommendation

Smart Customer

Service - Ali Assistant

Pervasive Personalization

Smart Supply Chain

Smart Logistics

12

Please refer to page 9 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

JAPAN

Hitachi’s EMIEW3 customer service / hospitality robot

Source: Hitachi, June 2017

Honda’s Miimo lawn mower

Source: Honda, June 2017

The Future of Japanese Tech - and drones:

A largely untapped opportunity (11 Aug 2016)

The Future of Japanese Tech - Japan’s

leadership in Energy Storage (17 Mar 2016)

Analyst(s) Macquarie Capital Securities (Japan) Limited Damian Thong, CFA +81 3 3512 7877 [email protected] William Montgomery, CFA +81 3 3512 7864 [email protected] David Gibson, CFA +81 3 3512 7880 [email protected] George Chang +81 3 3512 7854 [email protected] Macquarie Capital Limited Allen Chang +852 3922 1136 [email protected]

7 June 2017

The Future of Japanese Tech Service robot opportunity is still latent Conclusion

Japan’s service robot market has yet to meet the hope and hype of the past

two decades, despite extensive work done in academia and at companies.

But a combination of new innovations and growing unmet need (e.g. in

logistics and infrastructure inspection) may yet drive a breakthrough. The

growth of the market may be spurred by the entry of foreign firms.

Impact

Still a latent opportunity: Back in 2013, METI/NEDO projected that Japan’s

domestic service robot market would grow from ¥60bn in 2011 to ¥373.3bn in

2015, ¥1,024.1bn in 2020 and ¥2,646.2bn in 2025. Thus far, this seems over-

optimistic. Even the home-use vacuum cleaning robot amounts to only

<¥20bn/year now. High-profile hospitality robots like Toshiba’s trilingual Junko

Chihira, Hitachi’s EMIEW3 (being tested at Haneda Airport), and Softbank’s

Pepper are mainly used for public relations, with novelty value but limited

commercial impact – though Panasonic’s HOSPI does try to strike a balance

between novelty and usefulness (in the transporting of items in hospitals).

Consumer-oriented service robot market to expand: iRobot suggests that

the vacuum cleaner market is only 1/5th penetrated by robotic products. We

expect the service robot market to grow in tandem with the development of

the Internet-of-Things. Highlighting the importance of Japan – the world’s

leading robotic vacuum cleaner producer iRobot launched its Japan direct-

sales operation in April 2017 by absorbing the assets of its distributor.

Other major opportunities are likely to be in “near-industrial” and

labour-saving applications. These include logistics/ecommerce fulfilment,

infrastructure maintenance, and security. Examples include Hitachi’s Racrew

shelf-moving robot (which has orders e.g. from MonotaRO) and Alsok’s

Reborg-X security robot. Such robots address the needs created by Japan’s

growing labour shortages, which are likely to be aggravated by a 27%

shrinkage of the working-age population over the next 30 years.

There will also be growing deployment of robotic devices in healthcare

settings. Cyberdyne’s exoskeleton systems, while not strictly speaking

robots, use comparable technology to help health care professionals with load

carrying, and to provide patients with therapeutic benefit. The PARO

therapeutic robot seal has been marketed globally to nursing homes.

Ongoing policy support: The Japanese government has not stopped trying

to spur innovation and commercialisation of service robots. In 2015, METI

released a “New Robot Strategy”; a key tenet is that “society and structure

must undergo a transformation to take full advantage of robots” to create a

“robot barrier-free society”. Supportive factors would include technological

advances (e.g. better sensors, AI), standardisation and regulatory changes.

Thematic relevance: We do not expect Japan’s big tech conglomerates to

visibly benefit from service robots in the next 3-5 years, but the theme is likely

to be increasingly prominent at many firms – e.g. at Panasonic (6752 JP,

¥1,471, Outperform, TP: ¥1,580) and its Connected Solutions and appliances

businesses. Growth in service robots may benefit tech/parts suppliers ranging

from large firms like Nidec (6594 JP, ¥11,785, Outperform, TP: ¥12,500) to

emerging unlisted firms like Mujin and 3D Media. The listed firm most exposed

to healthcare applications is Cyberdyne (7779 JP, ¥1,533, Not Rated).

13

Please refer to page 5 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

JAPAN

9984 JP Outperform

Price (at 13:51, 02 Jun 2017 GMT) ¥8,995

Valuation ¥ 10,900 - Sum of Parts

12-month target ¥ 10,900

Upside/Downside % +21.2

12-month TSR % +21.7

Volatility Index Medium

GICS sector Telecommunication Services

Market cap ¥bn 9,900

Market cap US$m 89,183

Free float % 74

30-day avg turnover US$m 610.1

Number shares on issue m 1,101

Investment fundamentals Year end 31 Mar 2017A 2018E 2019E 2020E

Revenue bn 8,901.0 9,053.5 9,230.5 9,417.0 EBIT bn 1,026.0 1,136.4 1,231.2 1,277.7 EBIT growth % 12.9 10.8 8.3 3.8 Recurring profit bn 712.5 1,032.3 1,220.8 1,424.9 Reported profit bn 1,426.3 660.8 782.1 916.4 EPS rep ¥ 1,276 600 711 833

EPS rep growth % 218.2 -53.0 18.4 17.2 PER rep x 7.0 15.0 12.7 10.8 PER adj x 7.0 15.0 12.7 10.8 Total DPS ¥ 44 44 44 44 Total div yield % 0.5 0.5 0.5 0.5 ROA % 4.5 4.5 4.8 4.8 ROE % 46.1 17.0 17.1 17.1 EV/EBITDA x 7.8 7.4 6.8 6.4 Net debt/equity % 283.6 239.7 193.2 150.9

P/BV x 2.8 2.4 2.0 1.7

9984 JP vs TOPIX, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, June 2017

(all figures in JPY unless noted)

Analyst(s) David Gibson, CFA +81 3 3512 7880 [email protected] Aya Haruyama +81 3 3512 7867 [email protected]

7 June 2017 Macquarie Capital Securities (Japan) Limited

SoftBank Pepper Time Conclusion

We examine Softbank Robotics, which has plans beyond the well-known

Pepper for service robots. The division is not profitable yet despite selling 20k

Peppers as of Feb-17 but is an important part of the long-term vision for robot

services, especially for the elderly (given Japan’s ageing population).

Impact

Pepper, the emotive robot: Softbank, with Aldebaran Robotics, launched

Pepper, the company’s first humanoid robot, in June 2014. Pepper is

designed to analyse expressions and voice tones, but not as a functional

robot for domestic use. Rather it was intended ‘to make people happy’,

enhance people’s lives and facilitate relationships. Pepper identifies emotions

using four inputs—sight, hearing, touch and recognition of person—and uses

a cloud-based AI computer to figure out those emotions, and responds via

communication. As of June 2016 10k Peppers were sold and the number

reached 20k by Feb 2017, according to the Nikkei. The majority robots sold

are used for business needs such as a receptionist or a greeting robot in

stores. The business version sells for around US$18k for 3yrs (hardware +

subscription) and includes software development to match the corporate

needs. As of Feb 2017 over 2,000 firms have installed Pepper, according to

the Nikkei. The retail version sells for around US$10k for 3yrs with access to

300 apps including the ability for children to program the robot. In Dec 2015

production increased to 1,300 per month. Yano research estimates the Japan

domestic communication robot market will expand from US$22m now to

US$80m in 2020.

What next for Pepper - AI: Softbank Robotics’ main goal is to upgrade the

software using the experience of the already sold Peppers and thus make the

service robot smarter.

Nao and Romeo in the family: Softbank spent US$100m in 2013 to acquire

Aldebaran, which is now called Softbank Robotics. Aldebaran was established

in 2005 in France but had previously begun developing its robot Nao in 2004.

Nao replaced Sony’s Aibo in the RoboCup Standard Platform League for

robotic soccer competition in 2007. Nao is designed as an interactive

companion robot (58cm tall) and has clocked 10k sales to date. Romeo is still

under development and is intended to be a “genuine personal assistant and

companion” for the elderly. The robot is 140cm tall and is designed to perform

such tasks as opening doors, climbing stairs and reaching to objects on a

table. Romeo is not commercially available yet.

Earnings and target price revision

No change.

Price catalyst

12-month price target: ¥10,900 based on a Sum of Parts methodology.

Catalyst: Vision Fund details, Indian e-commerce deals

Action and recommendation

Maintain Outperform.

14

Please refer to page 2 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

TAIWAN

Global tier-one service provider capex trends

Source: Bloomberg, Macquarie Research, June 2017

Datacenter switch revenue by speed

Source: IDC, Macquarie Research, June 2017

Analyst(s) Kaylin Tsai +886 2 2734 7523 [email protected] Jeffrey Ohlweiler +886 2 2734 7512 [email protected]

7 June 2017 Macquarie Capital Limited, Taiwan Securities Branch

Taiwan Server/Networking Rising back-end support demand Conclusion

We believe service robots that receive information, analyse/communicate with

clouds, and react with solutions, will serve as a new source of demand for

back-end support from datacentre server/networking. With increasing

intelligence of robots and devices, there will be more AI (artificial

intelligence)/deep-learning specialized hardware in datacenters.

Impact

Both quantity and quality expansion from hyperscale datacenters:

Driven by new services (eg. video streaming, live casting, etc) and operations

shifting to public clouds, global tier-one service providers (including Google,

Facebook, Amazon, Microsoft, etc) capex expansion is expected to grow at a

12% CAGR for 2016-2019E, according to Bloomberg consensus estimates.

And aside from a quantity expansion, AI/Deep Learning functionality has been

addressed which can be found in the comments from chipset supplier Nvidia

(growing GPU penetration in cloud and hyperscale) and ODM Inventec (some

AI server projects in 2017).

Datacenter connections also need to be upgraded: With increasing data

traffic from new services or information that we didn’t keep track of before,

datacenters are upgrading their bandwidth from 1G/10G to 40G/100G from

2015-16 to accommodate larger flow of data. The trend can be found in the

revenue growth of Accton, a leading high-speed datacentre switch provider.

Its revenue has grown 19% in 2016 and 44% YoY in 2017 YTD (Jan-Apr).

Get smart and get connected: In order to get more information from the

surroundings for the robot to perform its services, there will be more “things”

becoming connected in various communication standards, such as home

appliances, home security systems, etc. And the trend will benefit networking

players such as Alpha Networks and Wistron NeWeb.

Stock implication

In the Taiwan server space, our top pick is Inventec (2356 TT, NT$23.60,

Outperform, TP: NT$25.70, Jeffrey Ohlweiler) given high server sales

exposure, attractive valuation, high dividend yield and also other non-server

growth drivers (eg. AirPods).

For Taiwan Networking space, our top pick is Accton Technology (2345 TT,

NT$71.00, Outperform, TP: NT$73.00, Kaylin Tsai) which is a true beneficiary

datacenters turning to purchase white-box and high-speed switches. We also

like Alpha Networks (3380 TT, NT$26.85, Outperform, TP: NT$27.60, Kaylin

Tsai), which has significantly expanded its OPM by streamlining operations.

-

10

20

30

40

50

60

2013 2014 2015 2016 2017F 2018F 2019F

(US$bn)

Google Facebook Amazon Microsoft

Alibaba Baidu Tencent

01234567

(US$bn)

<1G 10G 40G 100G

15

Please refer to page 5 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

TAIWAN

2330 TT Outperform

Price (at 10:49, 06 Jun 2017 GMT) NT$210.50

Valuation NT$ 228.00 - PER

12-month target NT$ 228.00

Upside/Downside % +8.3

12-month TSR % +11.7

Volatility Index Low

GICS sector Semiconductors & Semiconductor Equipment

Market cap NT$bn 5,458

Market cap US$m 182,602

Free float % 93

30-day avg turnover US$m 168.0

Number shares on issue m 25,930

Investment fundamentals Year end 31 Dec 2016A 2017E 2018E 2019E

Revenue bn 947.9 974.2 1,103.7 1,192.7 Reported profit bn 334.2 341.9 393.7 427.2 EPS rep NT$ 12.89 13.19 15.18 16.48

EPS rep growth % 9.0 2.3 15.1 8.5 PER rep x 16.3 16.0 13.9 12.8 Total DPS NT$ 7.00 7.12 8.20 8.90 Total div yield % 3.3 3.4 3.9 4.2 ROA % 21.3 19.8 21.0 20.6 ROE % 25.6 23.6 24.6 23.9 EV/EBITDA x 8.4 8.0 7.3 6.9 Net debt/equity % -21.0 -22.7 -26.0 -29.2 P/BV x 3.9 3.6 3.2 2.9

2330 TT rel TAIEX performance, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, June 2017

(all figures in NT$ unless noted, TP in TWD)

Analyst(s) Macquarie Capital Limited, Taiwan Securities Branch Patrick Liao +886 2 2734 7515 [email protected] Lynn Luo +886 2 2734 7534 [email protected] Macquarie Capital Limited Allen Chang +852 3922 1136 [email protected]

7 June 2017

TSMC Robots: driving demand for ICs Conclusion

We expect robots will not only drive the demand for TSMC’s advanced nodes

(for high-performance computing), but also matured nodes (for connection).

We believe TSMC’s technology leadership, variety of offering, and solid

execution will keep it the major beneficiary of the emerging robot market.

Reiterate Outperform and raise target price from NT$215 to NT$228.

Impact

Advanced nodes to support high-performance computing: We believe

robots will require HPC (high-performance computing)/AI [artificial

intelligence]) chips based on TSMC’s advanced nodes. TSMC also views

HPC as one of three key growth platforms in the next few years. We note that

one of the key customers in this area is Nvidia, which we estimate accounts

for 5-7% of TSMC’s revenue. We believe TSMC’s technology leadership will

make it the key beneficiary of the increasing HPC/AI demand.

Matured nodes to support connection: We expect robots will also drive the

demand for 40nm and above matured technologies with sensors, MCU,

connectivity, and power management ICs. In addition to the chips in robots,

we believe silicon content will also increase in other devices to interact and

connect with the robots. We believe TSMC’s continued improving efficiency

and variety of technologies positions it well for the market. We note one of the

key customers in this area is Broadcom, which we estimate accounts for 5-7%

of TSMC’s revenue. Fanuc is also a TSMC customer for machine controller IC.

Higher quality and reliability requirement: Although the robot demand

volume is still small for the whole semiconductor market, it will require better

quality and reliability comparing with consumer and communication products.

Therefore, we believe TSMC’s solid execution and track record will keep it in

leading position in this emerging market.

Earnings and target price revision

No change to earnings, but we raise target price from NT$215 to NT$228, as

we shift from 15x 2H17-1H18 P/E to 15x 2018 P/E.

Price catalyst

12-month price target: NT$228.00 based on a PER methodology.

Catalyst: Monthly sales, quarterly results/guidance, customer demand, and

progress of advanced technologies

Action and recommendation

We reiterate our Outperform rating with a target price of NT$228 (15x 2018

PER). We are optimistic on TSMC’s sales and EPS growth over 2017-19,

estimating 11% and 12% CAGRs, respectively. We believe TSMC’s continued

sales and EPS growth will lead to share price upside.

16

Please refer to page 5 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

TAIWAN

2317 TT Outperform

Price (at 13:50, 06 Jun 2017 GMT) NT$105.00

Valuation NT$ 150.00 - PER

12-month target NT$ 150.00

Upside/Downside % +42.9

12-month TSR % +49.1

Volatility Index Low

GICS sector Technology Hardware & Equipment

Market cap NT$bn 1,820

Market cap US$m 60,486

Free float % 88

30-day avg turnover US$m 113.9

Number shares on issue m 17,329

Investment fundamentals Year end 31 Dec 2016A 2017E 2018E 2019E

Revenue bn 4,358.7 4,814.3 5,273.0 5,709.2 EBITDA bn 251.6 306.5 343.2 383.1 EBITDA growth % -4.4 21.8 12.0 11.6 EBIT bn 188.3 249.2 285.4 324.9 EBIT growth % -1.9 32.3 14.5 13.8 Reported profit bn 148.7 201.3 231.3 265.5

EPS rep NT$ 8.52 11.54 13.26 15.21 EPS rep growth % 0.9 35.4 14.9 14.8 PER rep x 12.3 9.1 7.9 6.9 Total DPS NT$ 4.30 6.10 7.00 8.04 Total div yield % 4.1 5.8 6.7 7.7 ROA % 7.7 9.3 9.9 10.3 ROE % 14.3 17.7 18.3 18.2 EV/EBITDA x 6.0 4.8 4.4 3.9 Net debt/equity % -24.8 -28.5 -31.7 -40.1

P/BV x 1.7 1.5 1.4 1.1

2317 TT rel TAIEX performance, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, June 2017

(all figures in NT$ unless noted, TP in TWD)

Analyst(s) Allen Chang +852 3922 1136 [email protected] Verena Jeng +852 3922 3766 [email protected] Chris Yu +86 21 2412 9024 [email protected]

7 June 2017 Macquarie Capital Limited

Hon Hai Service robots: in APP and hardware Conclusion

Hon Hai has been aggressively expanding its robots business, from industry

robots (Foxbot) in 2010 to service robots (Pepper) in 2014. The company has

been increasing its investment in AI after acquiring Sharp in April 2016.

Despite limited revenue contribution in the near term, we expect AI to support

Hon Hai’s valuation as it has a more diversified portfolio and is moving up the

value chain. Maintain Outperform with PT of NT$150 (13x 2017E PE).

Impact

Hon Hai in Pepper, more than manufacturing: Hon Hai is the sole

electronics manufacturing services (EMS) provider for Pepper; however,

its contribution goes beyond assembly, to hardware design (incl. finger

movements) and B2B software apps to, for example, department stores,

3C tech malls, telecom retail stores, and financial institutions. Hon Hai is also

working on B2C apps, initially targeting education and recreation (Fig 1-2).

Pepper, among the world’s first personal companion robots: Pepper,

Hon Hai-made humanoid robot, is designed to simulate human interactions

through a range of voice inflections and ‘expressions’, aided by sophisticated

facial recognition. Apart from Hardware, Hon Hai also developed APPs to

improve Pepper’s interaction with people, such as helping run a coffee shop

(greeting customers, recommending coffee based on stored customer

preferences, etc).

Sharp’s service robots: Sharp’s service robots include AI smartphone

RoBoHoN (Fig 3) and robot vacuum cleaner Cocorobo (Fig 4). RoBoHoN can

be voice-controlled and is equipped with facial recognition, enabling it to

better interact with users. Like Pepper, RoBoHoN can simulate some human

actions (eg dancing) to attract more commercial clients, especially in retail

sales and nursing care sectors. Sharp is also developing AI-featured home

assistant robots for home energy consumption management and surveillance.

Hon Hai’s recent investments in AI and Big Data: Hon Hai has been

aggressively investing in AI and big data, eg: 1) Hike (a chat app in India similar

to WhatsApp): Hon Hai invested US$75m in Aug 2016, and Hike has over

100m subscribers in India; 2) Beijing Megvii Tech: Hon Hai invested US$20m

in Sep 2016. Megvii develops facial recognition and machine vision; and;

3) TetraVue: Hon Hai was the main investor in the A-round US$10m financing

in Feb 2017. TetraVue develops 3D Flash LIDAR for autonomous driving.

Earnings and target price revision

No change.

Price catalyst

12-month price target: NT$150.00 based on a PER methodology.

Catalyst: 2Q17 results

Action and recommendation

Maintain Outperform.

17

Please refer to page 5 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

HONG KONG

728 HK Outperform

Price (at 13:50, 06 Jun 2017 GMT) HK$3.81

Valuation HK$ 4.70 - DCF

12-month target HK$ 4.70

Upside/Downside % +23.4

12-month TSR % +26.4

Volatility Index Low

GICS sector Telecommunication Services

Market cap HK$m 308,352

Market cap US$m 39,571

Free float % 99

30-day avg turnover US$m 23.4

Number shares on issue m 80,932

Investment fundamentals Year end 31 Dec 2016A 2017E 2018E 2019E

Revenue bn 352.3 369.7 388.7 406.7 EBITDA bn 95.1 100.7 105.7 110.5 EBITDA growth % 1.1 5.9 5.0 4.5 EBIT bn 27.2 29.9 33.0 34.2 EBIT growth % 2.9 10.0 10.4 3.3 Reported profit bn 18.0 20.0 22.3 21.1

EPS rep Rmb 0.22 0.25 0.28 0.26 EPS rep growth % -10.2 11.1 11.7 -5.7 PER rep x 14.9 13.5 12.0 12.8 Total DPS Rmb 0.09 0.09 0.11 0.10 Total div yield % 2.8 2.8 3.2 3.0 ROA % 4.2 4.5 4.9 4.9 ROE % 5.8 6.2 6.7 6.1 EV/EBITDA x 3.6 3.4 3.3 3.1 Net debt/equity % 23.7 23.2 20.7 16.7

P/BV x 0.9 0.8 0.8 0.8

728 HK rel HSI performance, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, June 2017

(all figures in Rmb unless noted, TP in HKD)

Analyst(s) Allen Chang +852 3922 1136 [email protected] Verena Jeng +852 3922 3766 [email protected] Chris Yu +86 21 2412 9024 [email protected]

7 June 2017 Macquarie Capital Limited

China Telecom IoT leadership to drive growth in 5G age Conclusion

As we highlighted in March (Telecom Connecting World; 5G Era), we believe

China Telecom has built strong capabilities in emerging services such as

Internet data centres and cloud computing, Smart Family (IPTV), Internet

finance, big data, and Internet+ (specialized apps). We expect China

Telecom’s lead in fixed-line broadband and fibre infrastructure and its strong

enterprise client base to better support its growth in the coming 5G era.

Impact

Leader in IDC and cloud computing (Fig 1): China Telecom’s IDC and

cloud computing revenue rose 28% in 2016 to Rmb15.9bn, which is 2x as

large as China Unicom’s and 32x as large as China Mobile’s. We attribute

China Telecom’s leadership in this business to its dominant market share in

the fixed-line market and its higher broadband speeds. We expect the

company’s revenue from IDC and cloud computing to grow 30% in 2017.

Leader in Smart Family (IPTV) (Fig 2): China Telecom’s IPTV revenue rose

24% to Rmb4.8bn in 2016, contributing 1.4% of the year’s revenue. The

company’s IPTV subscribers increased by 21m in 2016 to 61m, or 50% of its

fixed-line broadband subscribers. Over 70% of IPTV subscribers in China are

on China Telecom’s service, based on 2016 data. IPTV can provide not only

TV content, but also educational content for children, and serve as a portal for

family conferences.

Strong fixed-line broadband subs with higher ARPU (Fig 3~4): China

Telecom has leading market share in fixed-line broadband subscribers, with

44% market share as of April 2017, followed by China Mobile (30%) and

China Unicom (26%). The company also enjoys higher ARPU in the fixed-line

broadband business, at Rmb54 in 2016, vs China Mobile’s Rmb32 and China

Unicom’s Rmb49. We attribute the higher ARPU to its higher speeds, with

25% of subscribers using >100Mbps bandwidth and 24% using 50–100Mbps.

Earnings and target price revision

No change.

Price catalyst

12-month price target: HK$4.70 based on a DCF methodology.

Catalyst: 2Q17 results

Action and recommendation

Maintain Outperform.

18

Please refer to page 5 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

CHINA

002415 CH Outperform

Price (at CLOSE#, 06 Jun 2017) Rmb28.62

Valuation Rmb 30.00 - PER

12-month target Rmb 30.00

Upside/Downside % +4.8

12-month TSR % +7.3

Volatility Index Medium

GICS sector Technology Hardware & Equipment

Market cap Rmbm 264,134

Market cap US$m 38,837

Free float % 39

30-day avg turnover US$m 158.7

Number shares on issue m 9,229

Investment fundamentals Year end 31 Dec 2016A 2017E 2018E 2019E

Revenue m 31,924 45,065 63,021 86,874 EBITDA m 8,509 12,691 17,890 25,070 EBITDA growth % 25.3 49.1 41.0 40.1 EBIT m 8,269 12,371 17,471 24,521 EBIT growth % 24.6 49.6 41.2 40.4 Reported profit m 7,422 11,015 15,696 21,994

EPS rep Rmb 1.22 1.19 1.70 2.38 EPS rep growth % 89.7 -2.2 42.5 40.1 PER rep x 23.4 24.0 16.8 12.0 Total DPS Rmb 0.37 0.54 0.84 1.17 Total div yield % 1.3 1.9 2.9 4.1 ROA % 23.1 26.9 30.7 34.0 ROE % 34.1 40.7 46.3 50.6 EV/EBITDA x 29.2 19.8 14.1 10.0 Net debt/equity % -48.5 -43.2 -38.0 -34.0

P/BV x 9.7 7.7 6.1 4.6

002415 CH rel CSI 300 performance, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, June 2017

(all figures in Rmb unless noted, TP in CNY)

Analyst(s) Allen Chang +852 3922 1136 [email protected] Verena Jeng +852 3922 3766 [email protected] Chris Yu +86 21 2412 9024 [email protected]

7 June 2017 Macquarie Capital Limited

Hikvision (A-Share) Logistics and parking service robot Conclusion

As we highlighted in April, Hikvision disclosed its emerging business (Ezviz

Smart Home, Robot, Drones, Automotive electronics) results, with revenues

of Rmb648m in 2016, or 2% of total revenues and 39% GM. Among the

emerging businesses, Ezviz Smart Home was the main contributor, implying a

limited revenue contribution from Robot. However, we are positive on the

company’s extension into robotics, which, we expect to support valuation in

the long run, given the diversified product portfolio.

Impact

Hikvision’s robot products include robots for sorting, for logistics and for

parking. Management guides to gross margin of robots to be higher than the

company’s blended gross margin of 40%, supporting the company’s gross

margin in the long term.

Parking robots – parking within 2 mins (Fig 1): The parking robot is

capable of a 3-ton load and equipped with in-house sensors for route planning

as well as collision avoidance. The automated parking system is able to

coordinate 500 parking robots with each vehicle retrieving task being

completed within 2 minutes, according to management. Hikvision’s parking

robots are currently in trial operations in a town near Shanghai.

Intelligent storage system Crossroad: In Feb 2016, the company launched

intelligent storage system, Crossroad, which consists of storage robot, robot

scheduling system (RCS) and intelligent warehouse management system

(iWMS). Crossroad leverages Hikvision’s expertise in video analysis and

management, targeting to increase storage efficiency.

Storage robot in Crossroad (Fig 2): The square shaped robot is developed

in-house with two wheels and a maximum operating speed of 1.0 meters per

second, maximum load capacity of 500kg, independent positioning and

navigation, automatic obstacle avoidance and self-charging.

Robot scheduling system (RCS) & Intelligent warehouse management

system (iWMS) in Crossroad: RCS is the crucial part of Crossroad, in

charge of allocating tasks among storage robots, monitoring operations and

battery status of the robots and providing prompt alarm to human staff to

ensure Crossroad runs smoothly. iWMS conducts data analysis with video

surveillance network and instant operation overview to optimize warehouse

management and enhance storage space utilization.

Earnings and target price revision

No change to net income. EPS for 2017-19E adjusted by -34% on share

count update. New PT at Rmb30, based on an unchanged 25x 2017E PER

(vs. Rmb45 previously).

Price catalyst

12-month price target: Rmb30.00 based on a PER methodology.

Catalyst: 2Q17 results

Action and recommendation

Maintain Outperform.

19

Please refer to page 5 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

HONG KONG

992 HK Outperform

Price (at 13:50, 06 Jun 2017 GMT) HK$5.07

Valuation HK$ 7.50 - PER

12-month target HK$ 7.50

Upside/Downside % +47.9

12-month TSR % +53.2

Volatility Index Medium

GICS sector Technology Hardware & Equipment

Market cap HK$m 56,321

Market cap US$m 7,228

Free float % 62

30-day avg turnover US$m 48.1

Number shares on issue m 11,109

Investment fundamentals Year end 31 Mar 2017A 2018E 2019E 2020E

Revenue m 43,035 44,389 46,136 50,554 EBITDA m 1,408 1,258 1,309 1,455 EBITDA growth % 111.1 -10.7 4.1 11.1 EBIT m 666 1,019 1,097 1,264 EBIT growth % nmf 53.0 7.7 15.2 Reported profit m 535 814 899 1,068

EPS rep ¢ 4.9 7.4 8.2 9.7 EPS rep growth % nmf 52.0 10.5 18.8 PER rep x 13.4 8.8 8.0 6.7 Total DPS ¢ 3.4 3.4 3.4 3.4 Total div yield % 5.3 5.2 5.2 5.2 ROA % 2.6 3.6 3.7 4.1 ROE % 30.4 18.3 15.8 15.6 EV/EBITDA x 5.2 5.9 5.7 5.1 Net debt/equity % 6.9 -20.0 -36.7 -45.6

P/BV x 1.9 1.4 1.1 1.0

992 HK rel HSI performance, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, June 2017

(all figures in USD unless noted, TP in HKD)

Analyst(s) Allen Chang +852 3922 1136 [email protected] Verena Jeng +852 3922 3766 [email protected] Chris Yu +86 21 2412 9024 [email protected]

7 June 2017 Macquarie Capital Limited

Lenovo AI-featured devices, Big Data, Cloud Conclusion

Lenovo’s enterprise (data centre) business was around 9% of FY2017

revenues, mainly focused on hyper-scaled and hyper-converged servers. We

are positive on Lenovo’s role in the future IoT era, given the company has a

comprehensive devices portfolio to form big data and to provide cloud

services to their devices users, and has hyper-scaled and hyper-converged

servers to run super computing for their enterprise clients.

Impact

AI-featured devices to form Big Data: Lenovo has a comprehensive

devices portfolio, including PC (leading brand with global market share at 20-

22%), smartphone (newly transitioned to high-end models), and smart home

facilities (smart assistant, smart storage), which could form Big Data and

enable Lenovo to provide cloud services to their devices users.

Lenovo AI-featured Smart Assistant (Fig 1): As we highlighted in Jan

(report link, CES 2017: AR, VR, Smart Home, Jan 5), the company

showcased its Smart assistant and Smart storage. The Smart Assistant is an

AI-featured speaker box, equipped with voice recognition, and can play music,

conduct web searches, support online shopping, create lists, etc. Voice

commands can be up to 5 meters away given eight 360-degree far-field

microphones in the device.

Private cloud services (Fig 2): Lenovo’s private cloud services could be

connected by multiple devices. It is an app in Windows OS, equal to a 100GB

hard drive, supporting printing, editing, and synchronizing. The private cloud

services also provide multiple “one-key” functions, such as copying photos to

cloud, printing files in cloud, and moving all data to new devices.

Enterprise (data centre) business outlook: Lenovo’s enterprise business is

under transition, with PTI margin at -11.6% in FY2017, mainly because of

rising components costs and continuous investments in China market (ex:

sales rep, channels, etc.). Management is confident it can improve profitability

in FY2018 given the previous opex investments and the company’s rising

partnership in hyper-converged market.

Earnings and target price revision

No change.

Price catalyst

12-month price target: HK$7.50 based on a PER methodology.

Catalyst: FY1Q18 results

Action and recommendation

Maintain Outperform.

20