Embed Size (px)

Citation preview

The State of Natural Gas SupplyAPPA/NGSA Joint Meeting

September 30, 2010Chicago, IL

1

A Decade Makes A DifferenceThen

• Shale known but uneconomic

• Storage rates regulated

• Four LNG ports, not all active

• “Associated” gas dominates

• 63-year supply

• Incomplete price transparency

• Limited means to respond to sudden demand changes

Now

• Burgeoning production

• Market-based storage rates

• Eight-plus active LNG ports

• Shale gas replacing associated gas

• 100-year supply

• Most transparent fuel market in the world

• Highly market-responsive supply

#2

3

Decade of Growing Natural Gas Infrastructure

# 4

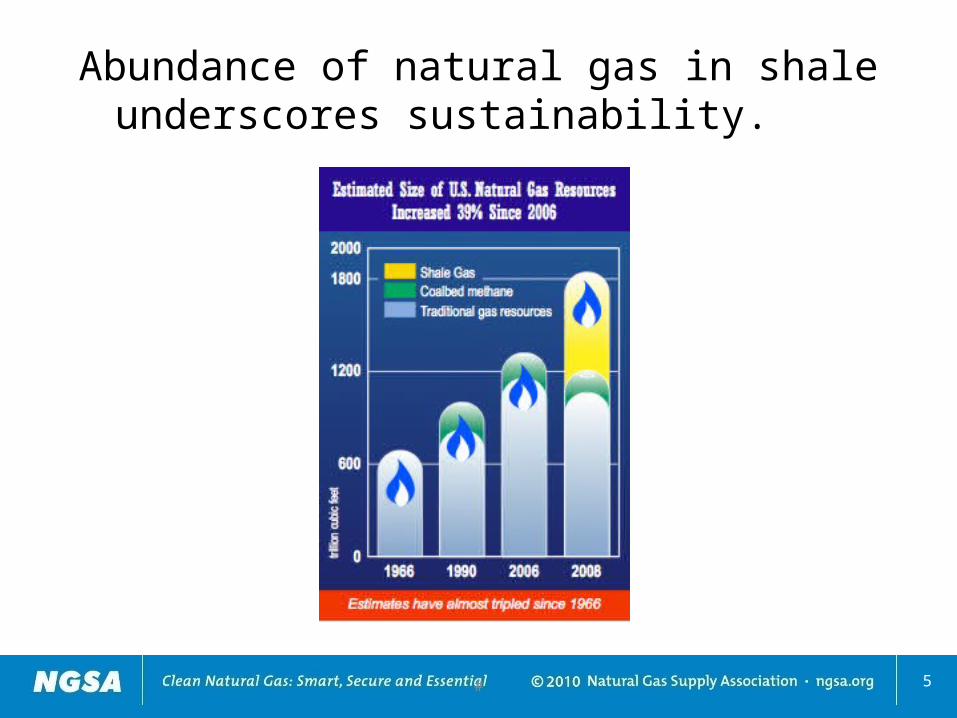

Abundance of natural gas in shale underscores sustainability.

5# 5

How Shale Produces Natural Gas

#

6SouSource: Energy Tomorrow

# 6

# 7

8# 8

Cha

nges

in p

rice

Source: CME Group, a CME/Chicago Board of Trade Company

Ebb and Flow of Commodity PricesNatural Gas 2002-2010

Source: CME Group, a CME/Chicago Board of Trade Company

Ebb and Flow of Commodity PricesNatural Gas compared to Crude Oil & Coal 2002-2010

Ebb and Flow of Commodity PricesNatural Gas compared to other Major Commodities

2002-2010

Source: CME Group, a CME/Chicago Board of Trade Company

Natural Gas MythsMYTH #1 –”There’s not enough natural gas to meet demand from

manufacturers and electrics” – U.S. supply up 40 percent since 2006 due to shale – 100-year supply with potential to grow

MYTH #2 – “Offshore drilling ban will hurt natural gas customers”– Most GOM gas production located in shallow water and excluded from ban

MYTH # 3 – “Heavy-handed regulation of shale could stop its production”– States are heavily invested in shale production – 50,000 jobs created in 2009 in

Pennsylvania alone

MYTH #4 – “Natural gas is vulnerable to Middle East policies”– Between 1 and 3 percent of U.S. demand is met by LNG imports– 75 percent of those imports are from Trinidad & Tobago, remainder from Norway, Algeria,

Egypt, Nigeria and Qatar.

13

Final Thoughts

• Entire gas industry significantly expanded since 2000

• “Fracking” issue real, but manageable• Competitive market has dampened price

volatility• “Dash to Gas” issue overstated• U.S. enjoys most robust, transparent, and

reliable natural gas industry in world