Embed Size (px)

Citation preview

1

The macroeconomic significance of Household Lending demonstrated in

relation to a Stock-Flow Consistent model

Diarmid J G Weir

PhD student

University of Stirling

Email: [email protected]

Abstract

Post-Keynesian economic thought largely rejects utility maximisation by households, price equilibrium in the goods and labour markets, and firms’ profit maximisation subject to these given prices, as organising features of the monetary macroeconomy. This rejection is based on these features being at odds with the observable realities of economic institutions, such as money, banks and the distinct objectives of firms. An alternative framework is therefore required to explain the degree of economic order and predictability that does exist, and how policies might affect this order.

Wynne Godley and Marc Lavoie have built a series of macroeconomic models based on double-entry accounting, rigorous matching of stocks and flows across all sectors of the economy through integrated balance sheets and transaction matrices, along with the assumption of behavioural norms in terms of stock-flow ratios for households, firms and the government.

Godley and Lavoie introduce money into their models in three ways: government purchases, firms’ loans for production and household lending. In each case the formation of assets in the form of debt is matched by counterpart liabilities in the form of bank deposits. Godley and Lavoie explicitly claim that their transactions flow matrices set the monetary circuit – where private money is explicitly viewed as the result and counterpart of initial production loans (as described by Graziani, Parguez and others) – within a comprehensive accounting framework. As a consequence the supply of loans to firms and the holding of private money deposits by households and firms must always be equal.

In Godley and Lavoie’s models, however, money once created is primarily a portfolio asset that acts as a residual buffer for households. Godley and Lavoie do not explicitly trace, as the monetary circuit does, the return of monetary revenue to firms to repay their production loans and neither do they address the issue of how a monetary surplus is generated by firms to purchase capital goods.

I discuss the ways in which the monetisation of profits has been addressed in relation to the monetary circuit, drawing particularly on the work of Edward Nell who suggests a two-sector solution, and adapt some of Godley and Lavoie’s models to bring this issue into focus. In doing this additional restrictions are placed on firms, and I show the importance of household loans - as a source of money from outwith firms and outwith the productive sector – in providing firms with the flexibility to adjust prices to generate monetary and/or goods surpluses.

1. Introduction

This paper is part of a wider thesis in which I am investigating the role of the

Monetary Circuit Approach in understanding macroeconomic problems. The particular

problem of interest in this paper is the role of household debt. In the simple analysis of

this paper, this includes secured debt such as that acquired for home ownership or

2

unsecured debt such as credit cards. I start off by discussing the problems of addressing

macroeconomic problems created by the need to account for the co-ordination of so many

individual transactions, particularly if money is realistically to be included in its proper

role in the flow of these transactions. I therefore propose Stock-Flow Consistent models

as a starting point for consideration of macroeconomic problems. I point out with relation

to a specific very simple model of this type the issues raised by a strict Monetary Circuit

Approach and how these might be affected by the addition of household loans. Following

the technique of Godley and Lavoie (2007) I have run some computer simulations based

on the resulting equations and discuss the results.

2. The Problems of Macroeconomic Modelling

The study of the macroeconomy requires us to understand why there appear to be

persisting features in terms of institutions, rates of flow and levels of stocks in particular

sectors of the economy. If we cannot model their persistence we have little chance of

understanding the changes that take place from period to period. To bring about this

stability neoclassical economic models rely on regular behaviour by consumers, workers

and firms and more-or-less automatic equilibrium at the macroeconomic level of supply

and demand in the markets for consumption and capital goods and for labour.

There is much to debate in all of these assumptions. Theories about the behaviour

of consumers, workers and firms can be tested empirically, and has been, with much

evidence to suggest that consumers’ and workers’ behaviour is far from rational or

consistent (Camerer 2004) and that firms are unlikely to be pure profit maximisers

(Godley, Coutts and Nordhaus 1978). These facts create difficulties for the neoclassical

model, but can often be overcome, and all models of the economy must make some

assumptions about these behavioural functions. Much more problematic is the reliance on

3

equilibrium to close the model once the behavioural equations are in place. This assumes

that it is only reasonable and meaningful to analyse the economy with respect to points in

time where demand and supply are equal. Leaving aside whether this condition is

acceptable in a dynamic economy there are several serious problems that arise from the

attempt to establish equilibrium macroeconomic models from complex microeconomic

assumptions.

The main issue is that it is very doubtful that macroeconomic aggregates can be

analysed using the type of representative agent analogy required by the neoclassical

microeconomic approach. By applying microeconomic theory that describes economic

relationships at the individual level and applies them by analogy to aggregate data,

expecting them to hold up assumes that the relationship between elements of the structure

will be preserved at higher levels. The logical requirement of consistent linear aggregation

restricts the functional form of the decision-making processes of representative agents’

(whether they are individuals or firms).

The reality of limited information, bounded rationality, diverse tastes and

endowments of individuals, along with differing technologies and goals on the part of

firms and with the presence of mediating institutions, macroeconomic externalities and

feedback from macro events mean that such constraints are too severe a limitation.

Without them rational choice-theoretic foundations have very few aggregative

consequences. As Colander (1996, p2) points out, the solution to a system of

simultaneous equations complex enough to describe the economy realistically with its

interdependencies at the level of individuals and individual firms has multiple equilibria

and complex dynamics, Thus a realistic neoclassical Walrasian micro model is consistent

with a wide range of phenomena at the macro level. The above analysis leaves us with the

4

problem of how to explain why the real world of the economy does not exhibit the chaotic

results anticipated.

Consistency of stocks and flows as used by Godley and Lavoie (2007) to build a

series of macroeconomic models may provide the answer to this and the further issues

that I outline in the following two sections

3. Matching Supply and Demand without Price Equilibrium

The market-clearing by price assumption of mainstream macroeconomic models is

widely challenged. Colander and van Ees (1996) go so far as state that the modern

economy is by no means ideally co-ordinated by the price mechanism, nor could it

conceivably be so co-ordinated. Godley and Lavoie (2007) describe the objection as

follows:

‘Excess demand leads to higher prices, which is assumed to reduce excess demand. This mechanism is put into effect within the period, before transactions are made. When transactions occur, as reflected in the transactions-flow matrix, supply and demand have already been equated through the price-clearing mechanism. We believe that such a market clearing mechanism, based on price variations, is only appropriate in the case of financial markets. In the case of goods and services markets, and in the case of the so-called labour market, we believe that the hypothesis of market-clearing equilibrium prices is wholly counterfactual, inappropriate and misleading.’ (Godley and Lavoie 2006 p64)

Eichner (1989 p246) also argues that price-clearing is the exception rather than a

rule in an advanced economy. It is only in commodity markets where individual sellers

are so numerous and lacking in market power that they are unable to exert any significant

influence on the price. When prices are given, the firm decides how much to produce and

then puts all of its output on the market at this price. Any imbalance between demand and

supply is then eliminated through an appropriate change in price. Eichner distinguishes

5

the firms in such markets by their direct control by a small number of owner-

entrepreneurs and the small number of plants which they control

By contrast, it is what Eichner terms ‘industrial markets’ that predominate in the

modern economy. In such markets, sellers are sufficiently few in number and with a well-

protected market position such that they can influence the market price directly. These

firms, therefore, can both decide on the quantity they will produce and the price at which

buyers will have to pay. Under these conditions, the firm sets the price and then sells

whatever quantity it can at that price. Thus when there is an imbalance between demand

and supply, the necessary adjustment occurs through the quantity variable rather than the

price variable. A decline in demand is experienced as a decline in sales rather than as a

weakening of the market leading to a fall in the industry price. Similarly, an increase in

demand is experienced as an increase in sales rather than a rise in price. Here there are no

organised market frameworks such as those that exist for shares or commodities, but

suppliers who create their own markets.

Relevant to Godley and Lavoie’s view then, is that the equality of income and

output seen in national accounts or flow of funds tables is not evidence of a real

equilibrium between investment and non-consumption, or income and output but arises

purely as a consequence of the definitions of profit and residual income; i.e.: any

discrepancy between what is earned by individuals and what is spent by them becomes

automatically matched by the gap between firms’ revenue and what they must pay out

(overwhelmingly, ultimately, as labour costs)

4. The Macroeconomic Role of Money

At the macro level, it is clear that money cannot be realistically introduced into a

framework resting on general equilibrium assumptions. As Clower and Howitt (1996)

6

point out – in general equilibrium there are no transaction costs to be alleviated by it since

these are ruled out by the presence of the Walrasian auctioneer.

In Clower and Howitt’s words: ‘[T]he problem of accounting for monetary

exchange is just the problem of explaining why the firms that make markets do not

routinely deal in direct barter of goods for goods.’ (Clower and Howitt 1996, p26) They

do not go on to detail these explanations, but I would tentatively suggest they are as

follows:

1. They do not have to, because money is introduced into the economy in

the process of acquiring loans to pay for wages or investment goods.

2. Firms need to acquire money to repay debts

3. They can dispose of their products more easily if they are willing to

exchange them for money, since

a. It is easier for consumers to buy on impulse – what they are foregoing

the do not yet have and so cannot value

b. Firms can facilitate (or even provide directly themselves) credit for

consumers to make purchases

Under a credit-based system of money an increase in the amount of money in

circulation occurs as an endogenous response whenever one of the non-financial sectors

uses loans to finance outlays. There is then a circular flow of these funds among the

various sectors of the economy. This flow occurs alongside the flow of produced goods to

consumption and a flow in the opposite direction of labour from households to firms. The

strict accounting of these flows is the distinguishing feature of the Monetary Circuit

Approach as described by for example Graziani (2003).

7

Eichner (1986) describes the significance of this. If there is a change in one

sector’s financial position without an increase in the overall amount of funds in

circulation, i.e.: its gross savings have increased relative to tangible investment this can

only be at the expense of some other sector. On the other hand, if there is a change in the

overall amount of funds in circulation, subsequent to a payment made that has been

financed by a loan from a bank, the sector making the payment will have both increased

its financial liabilities (in the form of the loan) and increased its financial assets (in the

form of additional deposits). Following the payment some further physical or financial

asset is acquired – it being on this basis that the loan was likely to have been made in the

first instance. Thus no intrinsic limitation on the amount of funds in circulation exists.

5. Monetisation of Macroeconomic Models

To understand the role played by lending or a flow of money from a particular

source, as I wish to do in this paper we must understand that we are dealing with a

monetary economy i.e.: an economy where virtually all transactions of significance are

carried out using money, and so for those transactions to take place money must be in the

hands of the purchaser of a real good immediately preceding that purchase. This only

makes sense if transactions are considered sequentially in the way that the monetary

circuit approach does. The real economy consists of overlapping transactions and circuits

which have started at different times, so it may seem unhelpful to isolate individual

circuits. But unless we do this it is difficult to analyse how the flow of money – where it

comes from and where it goes - affects the economy. In Nell’s words:

An account of why money is held does not explain how money is used. An account of the demand by individual agents for (real) cash balances (the average demand over a period) tells us nothing about the sources and destinations of inflows or about their regularity. The approach assumes that balances are attributable to individual decisions, based on preferences, and does not consider the way agents interact with each other as they

8

carry out their duties according to their institutional roles. (Nell 2004, p174-5)

In particular, the problem of accounting for the flow of a particular sum of money

arises each time there is an increase in the firm’s financial input that is converted into an

additional profit. While we can account for a greater than one for one productive increase

by a firm’s position on an increasing returns portion of its production function, no such

explanation can suffice to account for an incremental increase in monetary profit.

Nell asks how a sum of money exchanged against all the goods and services

produced in the economy, can be put into circulation as capital to buy inputs and then

return as a larger sum to allow profits to be extracted from revenue. Nell rightly

distinguishes between productivity; the transformation of a larger set of outputs from

given real inputs; and the increase in a sum of money where money is not itself

productive. Nell’s explanation proceeds from the establishment of a two-sector model.

The first sector is that of the equipment sector, the second that of the consumer sector.

This recognizes, as do circuitists such as Graziani (2003) that ultimately, the

overwhelming expense of the productive sector as a whole is spent on labour; even of

course that of the mining and extractive sector. In the case of two sectors, it can be

postulated that the consumer goods sector earns its profits in the form of the wages paid to

the employees of the equipment sector, since these must be paid to the consumer sector to

acquire the means of support. Thus the consumer sector borrows to pay its wage bill, but

can pay for its supply of equipment goods with the money received in payment from the

workers of the equipment goods sector. The problem is thus solved arithmetically, since

the initial finance borrowed by the capital goods sector to pay its wage bill passes through

both sectors before returning to the equipment goods sector to allow it to repay its debt.

Even this leaves the equipment goods sector without profit, so that no increase in the

production of equipment can take place. Nell’s solution to this problem is that the capital

9

goods sector is further subdivided so that each subdivision provides the profit for another

until we reach the machine tools sector. It is Nell’s argument that this sector makes its

own capital goods and so does not require a monetary surplus.

There are several possible objections to Nell’s approach. Firstly while it is true

that arithmetically, the double use of capital goods firms’ wages as the profits of

consumer goods firms partially solves the profits problem, it is not clear that it solves it

economically. The practical sequence of events is presumably (assuming that capital

goods firms need no raw materials, or already have access to them without expenditure)

that some proportion at least of capital goods (and in the case of a factory this is not

enough) must be produced and be ready for use before the consumer goods firm can

commence operations. This implies that the capital goods firm has borrowed its wage bill,

and paid its workers, but as yet no revenue has accrued to the consumer goods firm as it

has produced no output at this stage. In all probability, the consumer goods firm must

borrow the sum it must pay the capital goods firm for its output. However this loan

returns quickly to the bank, before the consumer goods firm commences output and the

workers of both sets of firms start acquiring it in return for their wages. Of course there

will be variations, with some capital goods firms prepared to wait until consumer goods

firms have made their monetary surplus before being paid. The difference between these

scenarios is that the consumer goods firms will have to pay interest on their loan for

acquiring the capital goods. Nell would dismiss this as a bridging loan that he regards of

little importance (Nell 2004, p179), yet a high enough interest rate on this loan or

unwillingness on the part of banks to advance it may prevent production taking place.

A second consideration is that in the real economy it is much more difficult to

distinguish ‘capital goods’ and ‘consumer goods’ firms. Construction firms may build

dwelling houses and factories; food manufacturers may supply supermarkets and plant

10

canteens. Because of this the sequence of production is not as clear-cut as Nell suggests.

Because of this we cannot be sure that money can always complete the double circulation

necessary to ensure that the consumer goods firms have their monetary surplus when their

wage-bill loans come due. Thirdly Nell’s conception of the machine tools sector that

‘makes its own capital goods’ seems somewhat far-fetched. It is unlikely that machine

tools firms actually build their own factories!

Lastly, it is an empirical fact (Corbett and Jenkinson 1997) that firms do not

generally spend their profits in the same period as they acquire them, and they may indeed

accumulate funds for several periods before making a major investment

6. The Stock-Flow Consistent Approach as an Organising Framework

Godley and Lavoie (2006) have attempted to replace the organising power of

equilibrium, utility maximisation and profit maximisation with a different framework

based on rigorous stock-flow accounting, the conscientious matching of stocks and flows

and the assumption of stable ‘stock-flow’ norms. Using this framework they have

constructed a series of macroeconomic models of increasing complexity. Godley and

Lavoie claim that within broad parameter limits the response of their models can be

reliably traced in simulations.

The arguments in favour of stock-flow norms as an organising principle for

macroeconomic behaviour are largely laid out in Godley and Cripps (1983). Here the

authors argue that these norms are a better approximation to actual behaviour than, for

example, utility maximisation; that they are more predictable, and so allow the co-

ordination of behaviour that is seen in the actual economy; and that they allow

straightforward linking from individual to aggregate behaviour.

11

For firms, the existence of cost-plus pricing combined with a quantity response to

changes in demand means that sales are equal to effective demand since the firm has

finished goods to act as buffer. Transactions in each period have results from stocks at the

end of the period and these stock variables are critical. They also emphasise the

importance of money creation by government purchasing and of production loans to firms

by banks. There are important roles for various buffers (residuals) for each sector – whose

quantities depend on other decisions that have been taken previously. Their modelling

largely follows the arguments of Eichner (1987) in his incomplete outline of a more

empirically-based approach to macroeconomics.

Godley and Lavoie point out (2007) that individual welfare maximisation is not

consistent with firms having an independent existence with distinct motivations, because

optimum prices, output and employment are decided for them by the location of aggregate

demand and supply schedules. They object that when households and firms are

amalgamated into a single sector, as they usually are in neoclassical models, the problem

of co-ordination between consumption and production is assumed away. Moreover, the

fact that there is no time element to production, and no excess demand or supply in these

models means that there is no place for loans or credit money, and thus no role for banks.

Their argument is that on the contrary, in a modern industrial economy, firms have a

separate existence with a distinct set of objectives such as to make profits for growth-

maximising investment. Since firms operate under imperfect competition and increasing

returns, they must decide for themselves how much to produce and how many workers to

employ, what pieces to charge, how much to invest and how to obtain finance. It is then

the pricing decision of firms rather than the marginal productivity of capital and labour

that determines the distribution of the national income between wages and profits. And

thus, since production really is a time-consuming process and expectations are frequently

12

falsified resulting in persistent excess demands and supplies, there is a systemic need for

loans from outside the production sector if the firm wishes to continue expansion.

An important further point that Godley and Lavoie raise is that sales of investment

goods give rise to receipts in the business sector, which receipts must themselves arise

from the business sector – which is itself doing the investing. Thus they implicitly

recognise an issue of profits that we will come back to in this paper.

7. Godley and Lavoie’s Bank-Money World (BMW) Model

Although Godley and Lavoie’s models subsequently become more complex, I

have chosen to base my analysis in this paper on a version of a very simple model, but

one that does introduce the concept of private bank with firms requiring to borrow fixed

capital. I start by analyzing this model and adapting it to conform with the monetary

circuit view, or in Nell’s expression monetising it (Nell 2004). This model conforms to

the general principles described above, consisting of households, production firms and

banks, but no government sector. There is a single financial asset, money deposits held by

households, and only fixed capital expenditures are considered. Godley and Lavoie define

a transaction matrix for their model as shown in Table 1 below.

13

Table 1 Transactions-flow matrix of Model BMW

Production Firms Banks

Households Current Capital Current Capital ∑

Consumption -C +C 0

Investment +I -I 0

[Production] [Y] 0

Wages +WB -WB

Depreciation allowances -AF +AF 0

Interest on loans -rl-1.L-1 + rl-1.L-1 0

Interest on deposits +rm-1.M-1 - rm-1.M-1 0

Change in loans +∆L -∆L 0

Change in deposits -∆M +∆M 0

∑ 0 0 0 0 0 0

Here components of the National Income and Product Accounts are arranged as

transactions between the sectors above the first horizontal line. Below this line are the

changes in financial assets and liabilities that correspond to the Flow of Funds Account.

All columns and rows sum to zero, since all transactions must have an issuer and a

receiver. In this model Godley and Lavoie assume an instantaneous quantity adjustment

process, so that the variables in the matrix represents both quantities supplied and those

demanded.

14

By using these equalities and particular behavioural functions, Godley and Lavoie

complete their model and run computer simulations to show the consequences of varying

some of the parameters. Analysing this matrix, it is important to realize that to the extent

that firms can pay out the quantity AF without borrowing, depends on a transfer of

investment funds from the capital account to current expenditure. This leaves open the

question of where these funds come from. Godley and Lavoie’s model does not start from

the zero position and so cannot account for any increase in investment of the sort Eichner

believes to be essential for survival. (See Eichner 1987, p360.)

Godley and Lavoie claim that their transactions flow matrix ‘sets the monetary

circuit…within a comprehensive accounting framework’ (2006, p47), but this is not

strictly correct. The general assumption of the monetary circuit approach is that initial

finance for firms comes in the form of a loan for the wage bill (see e.g.: Graziani 2003,

p27) The flow of money arising from this loan must then be specifically traced through

the series of transactions that follow until it is back in the hands of firms allowing the

initial loan to be repaid. This is done in Table 2, where I have added a line (Line 5)

representing the purchase of equities by households from firms, providing a route for

firms to access funds not used for consumption by households.

15

Table 2 Phased Circuit Flow in Adapted BMW Model

Circuit Phase

Households Firms Banks Households’

Balances Firms’

Balances Firms’ Loans Outstanding

1 Initial Loan -WB 0 WB WB

2 Wages +WB -WB WB 0 WB

[Production] [Y]

3 Consumption -C +C S C WB

4 First Partial Loan

Repayment -C +C S 0 S=WB-C

5 Equity Purchase -E +E S-E E S

6 Second Partial

Loan Repayment -E +E M 0 M=WB-C-E

7 Interest on loans -rl-1.L-1 +rl-1.L-1 ? ?

8 Depreciation allowances

-AF ? ?

9 Investment -I ? ?

We can see that after the second partial loan repayment, made possible by the

introduction of equities into the model, firms have no remaining funds for paying interest

on their wage-bill loans, for replenishing depreciation or for new investment, and in fact

they remain in debt to the banks. As the model stands they can only invest by the

counterfactual method of acquiring new loans for the whole of any new investment

(Corbett and Jenkinson 1997). No monetary profit can be made. From the steady state of

the original BMW model any increase in output entails an increase in target investment

for the next period that cannot be achieved without further loans. If the firm relies on

borrowing for investment, then there is an increasing interest and debt burden which is

likely to limit long-run expansion.

16

In Godley and Lavoie’s BMW model there is a transfer each period from firms’

capital to current accounts – offset in whole or in part by a transfer in the opposite

direction. If the offset is not complete, the difference is made up by an increase in loans

and so by a positive ∆L. In this way the appearance of a surplus each period – in fact if

there is any positive investment, this must arise from an increase in loans for firms, so that

there is only loan funding of investment. If we consider a start from a point of zero

capital, all capital must be funded by loans, and any new investment results in an increase

in loans.

If there is no other source of money, then a growing economy requires a loan that

increases each period by more than new investment because of interest on the wage-bill

loan and any investment loan. Firms are also vulnerable to increases in deposits held by

individuals as this will reduce further their ability to pay interest in any period. This

severely limits the flexibility of firms to accumulate funds until they are ready to make

capital investments, and so reduces their discretion to grow as required.

In Nell’s two-sector model - since profits are immediately paid to firms for capital

goods – all profits return to firms and allow the debt that created it to be repaid; but if

consumer goods firms do not purchase capital goods immediately – and we are accepting

the reality that they need not and often do not, spending some time in accumulating

profits before enacting an investment expansion – then there is an outstanding debt burden

for the firms sector that cannot be repaid, and so additional interest must also be paid. As

long as capital goods are not purchased this outstanding debt persists. Interest payments

form the income of banks and my also be accumulated, thus depleting the quantity of

money available.

17

8. Rewriting the Godley and Lavoie BMW model to account for the Monetary

Circuit

Table 3 Transactions-flow matrix of Adapted Model BMW

Households Firms Banks ∑

Consumption -C +C 0

Investment -I 0

[Production] [Y] 0

Wages +WB -WB 0

Equity Purchases -E +E 0

Depreciation allowances -DA 0

Interest on loans -rl-1.L-1 + rl-1.L-1 0

Change in loans +∆L -∆L 0

Change in deposits -∆M +∆M 0

∑ 0 0 + rl-1.L-1 0

I have altered the BMW transactions matrix (Table 3) to reflect the rigorousness of

the Monetary Circuit approach. In this new model the real output Y of firms is assumed,

according to Circuit Theory, to be equivalent to the wage bill WB,

Y WB= . (1)

Tracing out the flow in Table 3, we can see the total loan requirement for firms L

if they are to enter the next period without un-repaid debts, and desire to invest a positive

sum:

18

1 1 1 1 1. . ( )l lL L WB C r L r WB I DA E E− − − − −= + − + + + + − − . (2)

where C is consumption, r the real net interest rate on loans, I the level of investment and

DA the amount firms require to spend to compensate for depreciation of their capital

equipment. I have added the interest that must also be paid on the current wage-bill loan.

If households have access to a supply of bank loans H then their disposable

income is given by

YD WB H= + . (3)

out of which consumption takes place according to

0 1 2.C WB Hα α α= + + . (4)

where α0 is an autonomous element to consumption, α1 is the propensity to consume out of

wage income and α2 is the propensity to consume out of the current loan. M is the quantity

of money deposits held in that period, and varies according to

1 ( )M M YD Cγ−= + − . (5)

The quantity of new money deposits depends on an uncertainty parameter γ operating on

the residual income remaining once consumption has been determined. The rest of

unconsumed income is used to purchase equities, so that

1 ( )E E YD C YD Cγ−= + − − − (6)

Money holdings are responsive to uncertainty about the future. If this uncertainty

increases, then money holdings will increase and ceteris paribus purchase of equities will

decrease. Households’ demand for loans is given by

19

.H WBε= . (7)

Firms’ investment behaviour is given by

0 1 1I K DAβ β −= + + . (8)

where β0 is an autonomous element to investment, β1 a constant proportion of capital

accumulated in the previous period. This is to concord with Eichner’s view that firms aim

to keep up with general market expansion, but must also expand their market share if they

are not to be outstripped by firms newly entering the market.

Capital accumulates according to

1K K I DA−= + − . (9)

Depreciation allowances are determined according to

1.DA Kδ −= . (10)

The interest on bank loans is given by

l lr r= . (11)

Since the firm desires to achieve a monetary surplus only, and does not wish to

have unsold goods remaining, we can monitor this according to

( ) /X pY C p= − . (12)

where X is the real quantity of goods manufactured in that period and left unsold.

20

9. Results of simulations of the Circuit constrained model

I have constructed a computer simulation based on the model given above and

using plausible parameters. To ease interpretation, an initial arbitrary wage-bill and thus

planned output by the firm of €100 is chosen. The initial parameters are as follows:

Autonomous component of consumption α0 = 25,

Propensity to consume out of wages α1 = 0.73,

Propensity to consume out of loans α2 = 0.9,

Autonomous component of investment β0 = 0,

Capital increment to investment β1 = 0,

Loan demand parameter ε = 0,

Deposit holding ratio (Uncertainty parameter) γ = 0.5,

Rate of depreciation of capital δ =0.05,

Net interest rate on loans lr = 0.0,

Price level p = 1.

Simulations run using this new model over 5 and then 10 periods with these

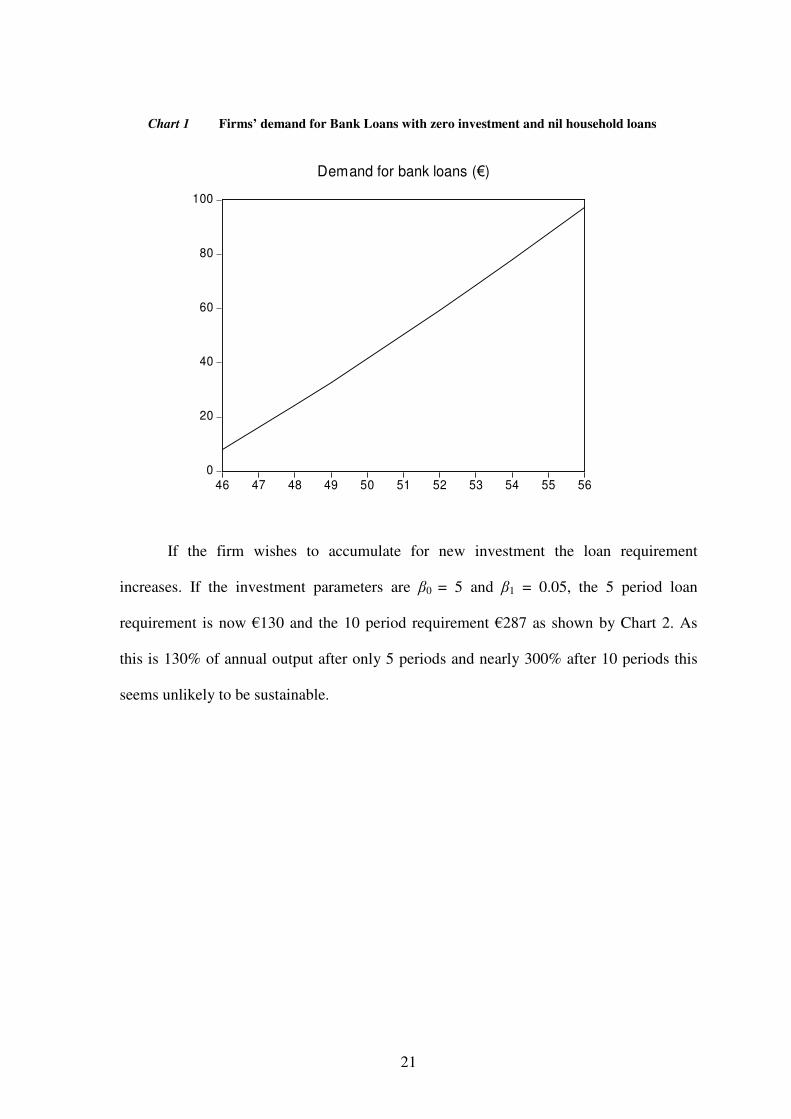

parameters now show that even with zero growth in output or disposable income, and

with no investment the level of current loans required by firms to avoid failing to repay

wage-bill loans increases year on year, €50 after 5 periods, and €97 after 10 periods. (See

chart 1)

21

Chart 1 Firms’ demand for Bank Loans with zero investment and nil household loans

0

20

40

60

80

100

46 47 48 49 50 51 52 53 54 55 56

Demand for bank loans (€)

If the firm wishes to accumulate for new investment the loan requirement

increases. If the investment parameters are β0 = 5 and β1 = 0.05, the 5 period loan

requirement is now €130 and the 10 period requirement €287 as shown by Chart 2. As

this is 130% of annual output after only 5 periods and nearly 300% after 10 periods this

seems unlikely to be sustainable.

22

Chart 2 Firms demand for bank loans with positive investment and nil household loans

0

50

100

150

200

250

300

46 47 48 49 50 51 52 53 54 55 56

Demand for bank loans (€)

We might anticipate that in this situation the firm will increase its price to acquire

increased revenue. If there is a 5% price increase, equivalent to raising the p parameter to

0.05 and keeping the other parameters the same as in the last simulation what we see is an

unchanged loan requirement, but now an increased in period by period unsold goods from

a real value of €2 to €6.7 annually. So on its own raising the price is of no benefit to

firms.

If, however, we make ε a positive value we can introduce a quantity of household

loans. For the final simulation demonstrated here, all other parameters remain as the

previous simulation, but now the loans parameter is ε = 0.075. Firms are now receiving

from households more than they pay out in their wage bill and this has the effect of

reducing the level of loans required for firms to €85 at the 5 year period and $200 at the

10 year period if investment is continued at the same level (See Chart 3). The level of

unsold goods is now only €0.7 annually. Thus the facility for households to acquire loans

23

reduces the level of loans firms require and so we can show how household loans can

provide the funds firms need to monetize their revenue and achieve a monetary surplus.

Chart 3 Firms’ demand for bank loans with positive investment and positive household loans

0

40

80

120

160

200

240

46 47 48 49 50 51 52 53 54 55 56

Demand for bank loans (€)

10. Conclusion

The equations derived in this paper and the simulations run from them

demonstrate in a very simple, and admittedly simplistic, way the potential importance of

household loans to the abilities of firms to maintain sustainable growth for themselves and

the economy as a whole. This may have important implications for the stability of

economies where the level of household loans is very high. I intend to work with more

complex and realistic Stock-Flow Consistent models, and complement them with more

comprehensive monetary flow elements to extend this analysis.

24

11. References

Camerer C. F. 2004. ‘Prospect Theory in the Wild: Evidence from the Field’; In Advances

in Behavioural Economics, Camerer, C. F., Loewenstein G. and Rabin M., eds.

Princeton University Press: Princeton N.J.

Clower R. and Howitt P. 1996. ‘Taking markets seriously: groundwork for a Post

Walrasian macroeconomics’. In Beyond Microfoundations: Post Walrasian

macroeconomics. Colander D., ed. Cambridge University Press: Cambridge U.K.

Colander D. 1996. ‘Overview’; In Beyond Microfoundations: Post Walrasian

macroeconomics. Colander D., ed. Cambridge University Press: Cambridge U.K.

Colander D. and van Ees H. 1996. ‘Post Walrasian macroeconomic policy’; In Beyond

Microfoundations: Post Walrasian macroeconomics. Colander D., ed. Cambridge

University Press: Cambridge U.K.

Corbett, J. and T. Jenkinson. 1997. ‘How is Investment Financed? A study of Germany,

Japan, the United Kingdom and the United States.’ The Manchester School

Supplement. pp69-93.

Coutts, K., Godley, W. and Nordhaus, W. 1978. Industrial pricing in the United

Kingdom. Cambridge University Press: Cambridge U.K.

Eichner A. 1987. The Macrodynamics of Advanced Market Economies. M.E. Sharpe:

Armonk N.Y.

Godley W. and Cripps F. 1983. Macroeconomics. Fontana Paperbacks: Oxford U.K.

Godley W. and Lavoie M. 2007. Monetary Economics: An integrated approach to credit,

money, income, production and wealth. Palgrave Macmillan: Basingstoke U.K.

Graziani A. 2003. The Monetary Theory of Production. Cambridge University Press:

Cambridge U.K.

Nell, E. 2004. ‘Monetising the Classical Equations: a theory of circulation’. Cambridge

Journal of Economics, 28, pp173-203