Embed Size (px)

Citation preview

© Infosys Consulting 20181

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act)Infosys Point of View

April 2020

© Infosys Consulting 20182

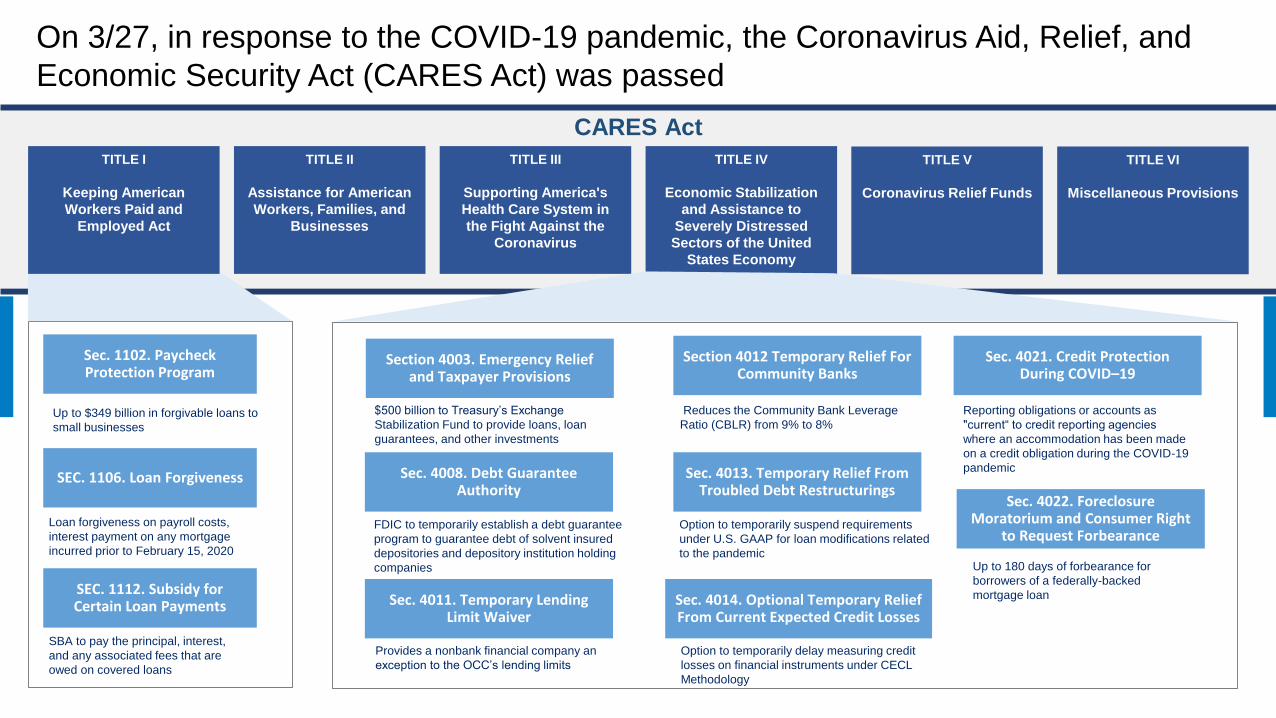

On 3/27, in response to the COVID-19 pandemic, the Coronavirus Aid, Relief, and

Economic Security Act (CARES Act) was passed

CARES Act

TITLE II

Assistance for American

Workers, Families, and

Businesses

TITLE III

Supporting America's

Health Care System in

the Fight Against the

Coronavirus

TITLE IV

Economic Stabilization

and Assistance to

Severely Distressed

Sectors of the United

States Economy

TITLE V

Coronavirus Relief Funds

TITLE VI

Miscellaneous Provisions

Sec. 4008. Debt Guarantee Authority

Sec. 1102. Paycheck Protection Program

Up to $349 billion in forgivable loans to

small businesses

SEC. 1106. Loan Forgiveness

SEC. 1112. Subsidy for Certain Loan Payments

Sec. 4013. Temporary Relief From Troubled Debt Restructurings

Sec. 4014. Optional Temporary Relief From Current Expected Credit Losses

Sec. 4021. Credit Protection During COVID–19

Sec. 4022. Foreclosure Moratorium and Consumer Right

to Request Forbearance

Sec. 4011. Temporary Lending Limit Waiver

Section 4003. Emergency Relief and Taxpayer Provisions

Section 4012 Temporary Relief For Community Banks

Loan forgiveness on payroll costs,

interest payment on any mortgage

incurred prior to February 15, 2020

SBA to pay the principal, interest,

and any associated fees that are

owed on covered loans

$500 billion to Treasury’s Exchange

Stabilization Fund to provide loans, loan

guarantees, and other investments

FDIC to temporarily establish a debt guarantee

program to guarantee debt of solvent insured

depositories and depository institution holding

companies

Provides a nonbank financial company an

exception to the OCC’s lending limits

Reduces the Community Bank Leverage

Ratio (CBLR) from 9% to 8%

Option to temporarily suspend requirements

under U.S. GAAP for loan modifications related

to the pandemic

Option to temporarily delay measuring credit

losses on financial instruments under CECL

Methodology

Reporting obligations or accounts as

"current“ to credit reporting agencies

where an accommodation has been made

on a credit obligation during the COVID-19

pandemic

Up to 180 days of forbearance for

borrowers of a federally-backed

mortgage loan

TITLE I

Keeping American

Workers Paid and

Employed Act

© Infosys Consulting 20183

The CARES Act authorizes more than $2 trillion to battle COVID-19 and its economic

effects on individuals and businesses

Corporations

Public Health &

Others

State & Local

Governments

Small Businesses

Individuals

$500 B $377 B $560 B $340 B $223 B• Backstop loans from the

Federal Reserve

• Loans and loan

guarantees

• Relief for airlines

• SBA Forgivable loans

(Paycheck Protection

Program)

• Emergency grants

• Relief for existing loans

• One-time direct cash

payments

• Extended unemployment

insurance benefits

• Student Loans

• Insurance Coverage

• Direct financial aid

• Community Development

Block Grants

• Education assistance

• Hospital and health-care

spending

• Food assistance

• Housing support

• Safety net

Direct and immediate impact on banks due to the Paycheck Protection Program (Sec 1102) accounting for

$349 billion and three other avenues of providing loans to small businesses

© Infosys Consulting 20184

These relief measures facilitated by Financial Institutions will directly or indirectly

impact origination, underwriting, servicing & fulfillment, risk and control functions

Lending Finance, Control & Reg Reporting Operations Mortgages

Customer Segmentation

Sales / Relationship

Management

Customer Lending Portal

Origination

Credit Underwriting

Limit Setting

Balance Sheet

Assessment

Credit Risk

Market Risk

FED, OCC, SEC, PRA

BASEL II, III, IV

BCBS 239

Sales Enablement

Training & Awareness

SOP Revisions

Capacity Planning &

Workforce Optimization

Lending Operations

KYC / Client Due

Diligence

Client Onboarding

Credit Facility Revision

Credit Facility Revision

Contract Optimization

Provisions to

accommodate

moratorium period

Re-computation of

Amortization Schedules

Enterprise Risk

Liquidity Risk

Stress Testing

Risk Reporting

Group Finance Reporting

IFRS9/ CECL

LCR/ NFRR

Credit Decisioning

Exposure Management

Credit Investigations

Asset Revaluation

Contract Optimization

Collateral Management

Collateral Management

Provisions made to

accommodate

moratorium period

Re-computation of

Amortization Schedules

Collateral Management

SHORT TERM IMPERATIVES

© Infosys Consulting 20185

Origination, underwriting, customer due diligence and reporting will require immediate

intervention

Consumer Lending Portal▪ Stand-up a portal to allow small businesses to apply for SBA paycheck protection loan

▪ Portal to be enabled to digitally collect relevant documentation for client onboarding

KYC / Client Due Diligence▪ Identify and define changes to KYC processes to support the modified requirements for loan applications

▪ Define a streamlined workflow for each stage of the CDD process

Credit Underwriting▪ Modifications to the underwriting and Risk Management processes / controls to support the loan

requirements based on the provisions of the Act

▪ Review of Risk models and portfolio management strategies to accommodate the new lending scenarios

Stress Testing & Regulatory Reporting▪ Stress testing scenario, portfolio impact and historical back-testing

▪ Identify and define critical reporting needs to fulfil regulatory requirements

Lending Operations▪ Determine target state documentation and processes to support faster turnaround of loan requests

Operations capacity planning and workflow management to address surge in demand

Credit Investigations▪ Ensure any federally backed mortgage loan may not initiate any foreclosure, eviction or credit reporting for

delayed or no mortgage payment

© Infosys Consulting 20186

The Paycheck Protection Program (PPP) will have the greatest impact on financial

institutions with enhancements needed across the lending value chain

Risk monitoring ServicingClosing & Loan

Funding

Credit

Underwriting

KYC / Client Due

Diligence / Loan Origination Collections

High High High Low Medium High Medium

Pro

ce

ss

Te

ch

no

log

y

• Define process and

workflows for

accepting new

requests

• Establish KYC

norms and

documentation

requirements for

PPP applications

• Define eligibility

requirements and

approval

methodology

• Identify documents

and checklist for

expedited loan

closing

• Define servicing

criteria and

determine changes

to existing terms

• Review changes to

risk monitoring

processes for PPP

loans and reporting

to SBA, as needed

• Identify impact to

existing Collections

process to support

PPP loans

• Stand-up external

portal for customers

• Enhance internal

systems to process

PPP specific

information

• Enhance / modify

KYC / CDD

workflows in the

systems to process

loan applications

• Build PPP specific

criteria into credit

decisioning and

pricing platforms

• Modify existing

workflows to

support expedited

loan closing and

booking

• Implement new

terms for customer

facing and internal

servicing systems

• Enhancements to

risk monitoring and

reporting systems

• Define new process

and workflows for

accepting new

requests

• Familiarize

customer facing

staff on eligibility

criteria and

requirements for

PPP loans

• Train KYC /

Operations team

and build

procedures on new

process for PPP

loans

• Train Front Office

teams on

communication to

customers on

approval terms and

requirements

• Communication to

employees,

customers and third

parties

• Train Operations

and Front Office

and Customer

Service teams on

new servicing terms

• Update internal

procedures and

communications for

risk monitoring

• Training and

communication to

internal and third-

party teams on

revised practices

Pro

ce

du

res

7

For example, banks will need to redesign or stand up portals to allow borrowers to sign up for SBA loans as part of the Paycheck Protection Program (PPP)

Borrower Application form from Treasury (As of 4/3)

8

Similarly, banks will need to build or modify apps to submit Paycheck Protection Program loan information to the SBA

Lender Application form from Treasury (As of 4/3)

© Infosys Consulting 20189

How can Infosys assist

Establish & execute CARES Act Program

Office

Assess Bank Technology impact & implement

Assess readiness & implement Regulatory

changes

▪ Define work streams

▪ Prioritize implementation

▪ Initiate implementation and track progress

▪ Establish & track dependencies

▪ Review and ensure implementation

completeness

▪ Inventory and assess impact on process,

systems, controls and identify gaps

▪ Develop heat map

▪ Develop requirements, create

implementation plan, identify

dependencies

▪ Validate implementation with Business

stakeholders

▪ Review impact on balance sheet, capital

requirement etc.

▪ Assess impact to existing regulatory

reports and new reporting requirements

▪ Review impact on data assets

▪ Build new data channels

▪ Automate report generation

© Infosys Consulting 201810

Establish & execute CARES Act Program Office

Bank technology impact assessment &

implementation

Assess readiness & implement Regulatory

impact

CARES Act Offering Details

PMO Work Streams Impacted Systems Impacted Reg Areas

Client

Onboarding &

KYC

Third Party

Management

Client

Onboarding

Finance &

Reporting

Credit &

Underwriting

Risk

Monitoring &

Collections

Loan

Origination

Portal

Client

Onboarding &

KYC / CDD

Loan

Underwriting

AccountingLoan

Operations

Risk

Management &

Monitoring

CECL

Methodology &

Reporting

Credit

Agencies

Reporting

Regulatory

Interpretation

Data

Availability &

Readiness

Assessment

Business

Rules

Definition &

Validation

Reporting

Framework

Impact

Analysis

© Infosys Consulting 201811

Infosys has experience across the banking value chain including specific areas of

impact to help you navigate the CARES Act journey

Large Regulatory Programs

Top Global Bank

Dodd Frank Reform and Volcker Rule Implementation

50+ Rules analysis (CFTC, SEC rules and Volcker Rule)

20+ Business, Technology, Operations workstreams

Large Insurance Company

California Consumer Privacy Act (CCPA)End to end ownership of implementing the regulation with compliance of

Jan 1, 2020

7 work-streams from client requests to updating privacy notices.

Manage product vendor to streamline client request portal

Program Management

Top Global Bank

PMO for Intermediate Holding CompanyDriving planning and tracking execution, and running Steering committee.

Created consolidated plan, elaborated key requirements, test strategy

Leverage Infosys’s templates as accelerators

Leading financial advisoryBuild Portfolio Management Competency to handle technology

investment portfolio.

70 interdependent projects and $240 million in IT spend

Client Onboarding & KYC

Large global bank

Reimagine and standardize KYC application across the

globe.Catering to 3+ million clientsImplemented across 90+ countries

Top 5 US bank

Digitized and standardized client onboarding experience

across Wholesale Banking60+% reduction in customer onboarding cycle time from 30+ days to 11

days

Defined consistent, streamlined process for 6 lines of business within

Wholesale Banking

Credit Underwriting

Top credit card issuer

Current state assessment for credit underwriting processDesign thinking led approach to identify gaps and prioritization followed by

tactical & strategic recommendations

Large regional bank

Customer Experience for Mortgage Servicing, design New

On-Demand Information Platform

Implement multiple decision science use cases across business banking

and omni-channel.

Lending & Mortgage

Super regional bank

Transformed CRM for Loan OfficersLeveraged design thinking, rapid prototyping and implemented journeys in

salesforce CRM. Persona based training.

The combination of desirable design and training led to a 100% adoption

Large regional bank

Digital Borrower Experience implementationDesigned customer experience and launched LOB’s first mobile customer

engagement platform in 4 months employing Design Thinking.

Increased customer satisfaction, reduced customer call volumes, and

introduced new ways of working at the bank.

Regulatory Reporting

One of the largest global financial institutions

Risk Finance Data Integration for Regulatory ReportingProgram awarded best data management initiative on the street

The warehouse acquired over 90% of the bank’s balance sheet across

100+ countries.

Wall Street Major

Respond to OCCs MRALaid down tenets of the program for all the regulatory reporting

programs at the bank

Reports included Basel, CCAR and other US reg reports

© Infosys Consulting 201812

Infosys Consulting Contacts

Rajesh Menon

Managing Partner Financial Services and Insurance

Infosys Consulting

Phone: +1 (201) 739 4112

Email: [email protected]

Debashis Pradhan

Partner Financial Services and Insurance

Infosys Consulting

Phone: +1 (201) 919 1883

Email: [email protected]