Embed Size (px)

Citation preview

Session 177 OF, The Convergence of Capital Markets and Insurance

Moderator:

Erik J. Thoren, FSA, CERA, MAAA

Presenters: Prannoy Chaudhury, FSA, MAAA

Jean-Francois Lemay, FSA Erik J. Thoren, FSA, CERA, MAAA

SOA Antitrust Disclaimer SOA Presentation Disclaimer

Jean-Francois LemayCapital Markets Investment StructuresOct 26, 2016

Structures of Capital Market Investments in Insurance

2

Capital Markets• Capital Markets have used many different ways to

enter the life insurance space• Capital Markets may look at the insurance industry to:

• Access a risk that that is not correlated to other markets like mortality/longevity

• Access assets to manage• Or simply invest in an area where returns are thought to be

attractive• The ideal structure to enter the market will depend on

the goal and the specific situation of the capital provider

3

Direct Investment in an Onshore Insurer

4

Onshore Life Co

Capital Market$

• Requires onshore regulatory approval• Assets will be subject to onshore admitted asset

rules and RBC requirements• Arm’s length asset management contract

Asset Manager

OwnershipIMAReinsurance

Direct investment in an Offshore Reinsurer

5

Offshore Reinsurer Co

Capital Market$

• No onshore regulatory approval• Reinsurance will be done on a funds

Withhled / Modlco / Assets in trust basis.• Assets will be subject to onshore

admitted asset rules but Offshore Capital requirements

• Investment Management Agreement will be between the Onshore Life co and the Asset Manager.

Asset Manager

Onshore Life Co

OwnershipIMAReinsurance

Direct investment in an Offshore Reinsurer using a Sidecar

6

Offshore Sidecar

Capital Market$

• Added benefit of not having to manage the reinsurer and ability to select slice of risk

Asset Manager

Onshore Life Co

Offshore Reinsurer Co

OwnershipIMAReinsuranceManagement Agreement

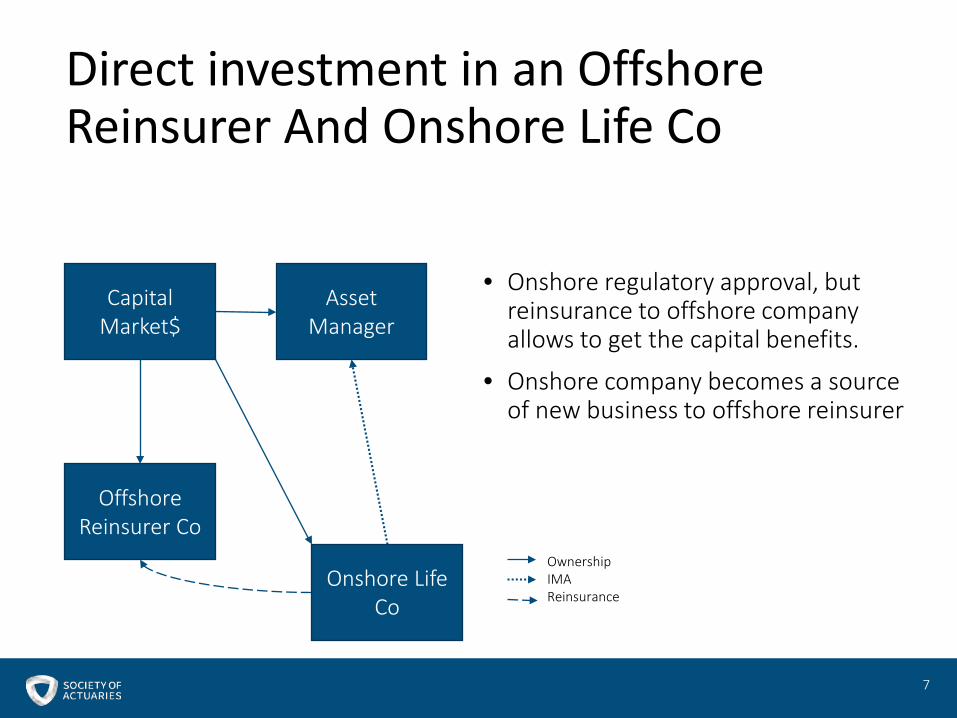

Direct investment in an Offshore Reinsurer And Onshore Life Co

7

Offshore Reinsurer Co

Capital Market$

• Onshore regulatory approval, but reinsurance to offshore company allows to get the capital benefits.

• Onshore company becomes a source of new business to offshore reinsurer

Asset Manager

Onshore Life Co

OwnershipIMAReinsurance

Direct investment in an Offshore Reinsurer And Onshore Life Co - stacked

8

Offshore Reinsurer Co

Capital Market$

• Offshore reinsurer can be used for third party reinsurance.

• Stacked structure allows offshore reinsurer to have a greater capital base.

Asset Manager

Onshore Life Co

Onshore Life Co

OwnershipIMAReinsurance

Some Tax Efficiencies…

9

Offshore Re (Cayman/BDA)

Capital Market$

• Benefit from have multiple jurisdictions:

• Irish/953(d) will have no FET

• Cayman may have more flexible capital rules and no FIT.

Asset Manager

Onshore Life Co

Onshore Life Co

Offshore Re (Ireland/953d)

OwnershipIMAReinsuranceManagement Agreement

Some More Capital Efficiencies

10

Offshore Re (Cayman)

Capital Market$

• Solvency II friendly jurisdictions for European business.

Asset Manager

Onshore Life Co

Onshore Life Co (US)

Offshore Re (Ireland/953d)

Onshore Life Co (Europe)

Offshore Re(Bermuda/Ilse

of Man/PR)

OwnershipIMAReinsurance

Cell Company Structure

11

Offshore Re (Cayman)

Capital Market$

• Each deal is collateralized and immune to default of other cells

Asset Manager

Onshore Life Co

Offshore Re (Ireland/953d)

Onshore Life Co (Europe)

Offshore Re(Bermuda/Ilse

of Man)

Cell/PIC

Cell/PIC

Cell/PIC

Onshore Life Co (US)

Onshore Life Co (US)

Onshore Life Co (US)

OwnershipIMAReinsurance

Complete the circle and reinvest in the capital markets

12

Offshore Re (Cayman)

Capital Market$

Asset Manager

Onshore Life Co

Offshore Re (Ireland/953d)

Onshore Life Co (Europe)

Offshore Re(Bermuda/Ilse

of Man)

Cell/PIC

Cell/PIC

Cell/PIC

Onshore Life Co (US)

Onshore Life Co (US)

Onshore Life Co (US)

Capital Markets – Other points of entry

• Longevity swap• Cat bond• Premium finance

13

Presented by:

Prannoy Chaudhury, FSA, MAAA Consulting Actuary, Milliman Inc.

Society of Actuaries - Annual Meeting (Session 177)

October 26, 2016

XXX / AXXX Reserve Financing

2

Agenda

Introduction to XXX / AXXX reserve financing

Common solutions to financing XXX / AXXX strain

Hot topic: AG 48

Role of actuaries in reserve financing transactions

3

Introduction to XXX / AXXX Reserve Financing

Many banks and reinsurers are willing to finance the excess of statutory over ‘economic’ reserves

The definition of economic reserves has historically been a negotiated deal term that for XXX/AXXX financing deals has often been GPV determined with best estimate assumptions. The graph below shows how XXX economic and excess reserves can vary over time.

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Statutory

Excess

Economic

4

Why do most large stock life insurers and reinsurers use reserve financing?

Most competitors price term life and universal life assuming debt-like financing costs for excess reserveso Results in better pricing for consumers

Reserve financing frees up surplus that can be used to improve RBC ratios, finance sales growth, or invest in acquisitions

The nature and structure of reserve financing utilized can impact rating agency views of an insurer’s capital adequacy, financial flexibility or enterprise risk management

5

Key steps in a XXX/AXXX transaction

Insurer identifies a particular block of XXX/AXXX business for reserve financing

Insurer receives proposals from financing providers (and selects one)

Insurer creates a Captive Reinsurer to which the chosen block of XXX/AXXX business will be ceded

Insurer works with its state of domicile and the Captive’s state of domicile regulator to receive approval (e.g., the transaction structure is presented along with the Captive’s pro-forma)

6

Common Solutions to Financing XXX / AXXX Strain

Structured reinsurance (3rd party)

Funded solutions (involving captive surplus note issuance)

Letters of credit (“LOC”)

Credit Linked Notes (“CLN”)

Other forms of collateral acceptable to the cedant’s regulator

7

Financing Structure: Non-recourse LOC

Popular since 2010

Some banks have additional features (with extra boxes and arrows) to differentiate their solutions

Most non-recourse LOCs to date have been “conditional”, whereby a draw is only permitted after economic reserve assets, and the Captive’s surplus assets are depleted

Bank

Captive Reinsurer

Reinsurance Premiums

Reinsurance Claims

Cash Drawn on LOC if needed

Life Insurer or Professional

Reinsurer

LOC Fees

8

Financing Structure: Credit Linked Note (“CLN”)

SPV

Captive Reinsurer

Reinsurance Premiums

`CLN

interest & principalLife Insurer or

Professional Reinsurer

Surplus Note interest & principal

Financing Provider

Fee=Surplus Note interest – CLN interest

SPV’s CF shortfall

Popular since 2012

Captive issues a Surplus Note bought by the SPV, and Captive buys the credit linked note (“CLN”) with a lower coupon

In good times, the coupon difference is paid to financing provider as a fee

In bad times, financing provider covers SPV’s CF shortfall

Reinsurance Claims

9

Key reserve financing market development: AG 48

Applicable for new transactions effective after 12/31/2014

One must determine Actuarial Method Reserves (“AMR”) that now replaces the ‘Economic Reserve’

o AMR is based on VM-20 (PBR) guidelines

o Interesting insights gained from AG 48 transactions regarding a PBR world.

AMR must be backed by ‘Primary Securities’ (cash, bonds etc.)

Excess of AMR, up to Statutory Reserve, can be backed by ‘Other Securities’ (LOC, CLN asset, etc.)

XXX/AXXX Statutory Reserves

AMR Economic Reserves

Mezzanine Layer = (AMR - Economic Reserves)

Excess of XXX/AXX Statutory Reserves over

AMR

10

Role of Actuaries in Reserve Financing Transactions

Develop actuarial projectionso Review experience studies to determine best estimate assumptions

o If working for a bank or other provider of financing, advise on key risk factors for the block of business.

Analyze financing proposalso Quantitative: for e.g., impact of the different transactions on the distributable

earnings of the Insurer

o Qualitative: regulatory approval, rating agency view of the transaction

Develop deal modelo Based on the terms of the chosen transaction structure (documented across a

number of legal documents), develop a deal model that incorporates items such as the Captive’s priority of payments

o Help determine the Captive’s capitalization and dividend thresholds.

THIS DOCUMENT SHOULD NOT BE REPRODUCED IN ANY FORM WITHOUT PRIOR WRITTEN APPROVAL

The convergence of capital markets and insurance –secured financeErik Thoren, CFA, FSAOctober 26, 2016

USP0221

Agenda

• Capital markets overview

• Why secured finance?

• What is secured finance?

• What else do I need to consider?

• Summary

USP0221

Capital markets overviewInsurers have been living in a tough environment

Source: Bloomberg, as of October 2016.

Chart 1: 10-year global government yields Chart 2: Spread between 2- and 10-year yields

Chart 3: US credit spreads• Tough environment yield over the past decade

• Can you find higher returns using alternatives to debt?– Move into alternative investments (i.e., PE, hedge

funds, real estate equity) is not a panacea

• Where else can you search for yield?– Extend duration– Lower credit quality– Less liquidity

USP0221

Capital markets overviewCredit and liquidity risks in the marketplace

For illustrative purposes only.

Cre

dit r

isk

Liquidity

Mid-market private debtMezzanine, second lien

Distressed debt

High yield bondsBroadly syndicated bank loans

Residential and consumerCommercial real estate loans

Secured corporatesInvestment grade bonds

Lower Higher

Higher

Lower

Securedfinance

USP0221

High yieldInvestment grade

+340bp

Why secured finance?Complexity and illiquidity premium creates a potential attractiverisk-adjusted return

As of June 30, 2016. The spreads shown are for illustrative purposes only.

0

50

100

150

200

250

300

350

400

450

500

550

600

650

700

750

AAA A BBB BB

Spre

ad o

ver 3

mon

th L

ibor

(bp)

Representative secured finance universe Investment grade corporate bonds

USP0221

Why secured finance?Regulation has created opportunities to extract illiquidity/complexity

• Increasing regulation has reduced bank lending

• Leading to wider secured credit spreads

• Long term investors (insurers) can provide an alternative source of finance to borrowers

• Illiquid secured finance provides an interesting opportunity for insurers

– Risk/reward opportunities are compelling – no need to sacrifice credit quality while seeking additional return

Source: Bloomberg, TRACE and Morgan Stanley, as of June 30, 2014.

Analysis of bank balance sheet asset base

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2006 2008 2009 2011 2012 2014

Yoy

Cha

nge

Assets

USP0221

• Secured finance refers to lending that is secured against a single asset or portfolio of assets

• Typically, investors provide capital in return for interest and principal payments

• Investments can be structured with different credit and cash flow timing characteristics– e.g., senior investment grade tranches (e.g., AAA, AA or A) with a

supporting junior ranking tranche (e.g., BB), where principal of most senior tranches paid off first

What is secured finance?Introduction

For illustrative purposes only.

Examples of collateral include:• Residential mortgages• Commercial real estate

loans• Corporate loans• Auto loans• Credit card debt

Senior loan

Junior loan/equity

Collateral pool (e.g., mortgage

loans)

Interest and principal from

mortgages

Interest frommortgages

Principal frommortgages

Losses

Debt (e.g., 60%)

Equity (e.g., 40%)

Priority of payments

USP0221

What is secured finance?Collateral and liquidity characteristics

For illustrative purposes only.

• Prime residential mortgage backed securities (RMBS)

• Auto loans (ABS)

• Credit card debt (ABS)

Residential and consumer

• Mortgage warehouse

• Bridge lending

• Auto/credit card warehouse

Commercial real estate Secured corporate

Liqu

id

• Office

• Retail

• Hotel

• Corporate loan warehouse

• SME warehouse

• Collateralized loan obligations (CLO)

• Whole business securitizations (WBS)

• Collateralized mortgage backed securities (CMBS)

Illiq

uid

USP0221

What is secured finance?The trade-off between ‘liquid’ and illiquid

For illustrative purposes only.

Securities Loans

Origination Public market Proprietary channels

Underwriting and valuation

PublicLoan-level underwriting

Private informationLoan-level underwriting

Structuring None (structuring is already done so your decision is “take it or leave it”)

Negotiate deal terms and security package

Trading Public tradable market Limited liquidity, hold to maturity ore.g., sell to syndicate/ club member

More Liquid Less Liquid

USP0221

• Are we able to?

– What are our ALM considerations?

– How much liquidity can we sell?

– Are they permitted?

• Do we want to?

– What is my risk appetite?

– What are my collateral and structure preferences?

– How much will we allocate?

• How can we?

– How familiar are we with investing in these assets?

– What are we able to access?

– Should we do this in-house or hire an external manager?

What else do I need to consider?

USP0221

• More opportunity exists now for insurers as a result of bank deleveraging

• Reach for yield does not have to come at the cost of increased credit risk

• Secured finance provides an interesting opportunity for insurers:

– Enhanced yield vs. investment grade corporate bonds by extracting illiquidity and complexity premium

– Most insurers familiar with or already invest in ‘liquid’ secured finance types

– Illiquid assets may be particularly attractive due to increase yield and protection

• There are a lot of decisions to make along the way

Summary

Important disclosures

Past performance is not a guide to future performance. The value of investments and any income from them will fluctuate and is not guaranteed (this may partly be due to exchange rate changes) and investors may not get back the amount invested. Transactions in foreign securities may be executed and settled in local markets. Performance comparisons will be affected by changes in interest rates. Investment returns fluctuate due to changes in market conditions. Investment involves risk, including the possible loss of principal. No assurance can be given that the performance objectives of a given strategy will be achieved. The information contained herein is for your reference only and is being provided in response to your specific request and has been obtained from sources believed to be reliable; however, no representation is made regarding its accuracy or completeness. This document must not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or otherwise not permitted. This document should not be duplicated, amended, or forwarded to a third party without consent from Insight. This is a marketing document intended for professional clients only and should not be made available to or relied upon by retail clients.

Investment advisory services in North America are provided through four different investment advisers registered with the Securities and Exchange Commission (SEC), using the brand Insight Investment: Cutwater Asset Management Corp. (CAMC), Cutwater Investor Services Corp. (CISC), Insight North America LLC (INA) and Pareto Investment Management Limited (PIML). The North American investment advisers are associated with other global investment managers that also (individually and collectively) use the corporate brand Insight Investment and may be referred to as “Insight” or “Insight Investment”. The investment adviser providing these advisory services is Cutwater Investor Services Corp. (CISC), an investment adviser registered with the SEC, under the Investment Advisers Act of 1940, as amended, and is also registered with the Commodity Futures Trading Commission (CFTC) as a Commodity Trading Advisor and Commodity Pool Adviser. Registration with either the SEC or the CFTC does not imply a certain level of skill or training. You may request, without charge, additional information about Insight. Moreover, specific information relating to Insight’s strategies, including investment advisory fees, may be obtained from CISC’s Form ADV Part 2A, which is available without charge upon request.

Unless otherwise stated, the source of information is Insight. Any forecasts or opinions are Insight’s own at the date of this document (or as otherwise specified) and may change. Material in this publication is for general information only and is not advice, investment advice, or the recommendation of any purchase or sale of any security. Insight makes no implied or expressed recommendations concerning the manner in which an account should or would be handled, as appropriate investment strategies depend upon specific investment guidelines and objectives and should not be construed to be an assurance that any particular security in a strategy will remain in any fund, account, or strategy, or that a previously held security will not be repurchased. It should not be assumed that any of the security transactions or holdings referenced herein have been or will prove to be profitable or that future investment decisions will be profitable or will equal or exceed the past investment performance of the securities listed. Telephone calls may be recorded.Insight does not provide tax or legal advice to its clients and all investors are strongly urged to consult their tax and legal advisors regarding any potential strategy or investment. Insight does not provide tax or legal advice to its clients and all investors are strongly urged to consult their tax and legal advisors regarding any potential strategy or investment.

Insight and MBSC Securities Corporation are subsidiaries of BNY Mellon. MBSC is a registered broker and FINRA member. BNY Mellon is the corporate brand of The Bank of New York Mellon Corporation and may also be used as a generic term to reference the Corporation as a whole or its various subsidiaries generally. Products and services may be provided under various brand names and in various countries by subsidiaries, affiliates and joint ventures of The Bank of New York Mellon Corporation where authorized and regulated as required within each jurisdiction. Unless you are notified to the contrary, the products and services mentioned are not insured by the FDIC (or by any governmental entity) and are not guaranteed by or obligations of The Bank of New York Mellon Corporation or any of its affiliates. The Bank of New York Mellon Corporation assumes no responsibility for the accuracy or completeness of the above data and disclaims all expressed or implied warranties in connection therewith.© 2016 Insight Investment. All rights reserved.