Embed Size (px)

Citation preview

The convergence of re/insurance and capital markets

The ART market(Alternative Risk Transfer)

Big picture• Risks being transferred

– Catastrophic (cat) risk• $1 trillion of assets at risk

– Reinsurance risk• Driven by insurance cycle

• The vehicles– Cat bonds– Sidecars, collateralized Re– Industry loss warranties

• The rewards– High returns– Low correlations with

financial markets

End of 2012: $15.5b2013 to date: $1.95b

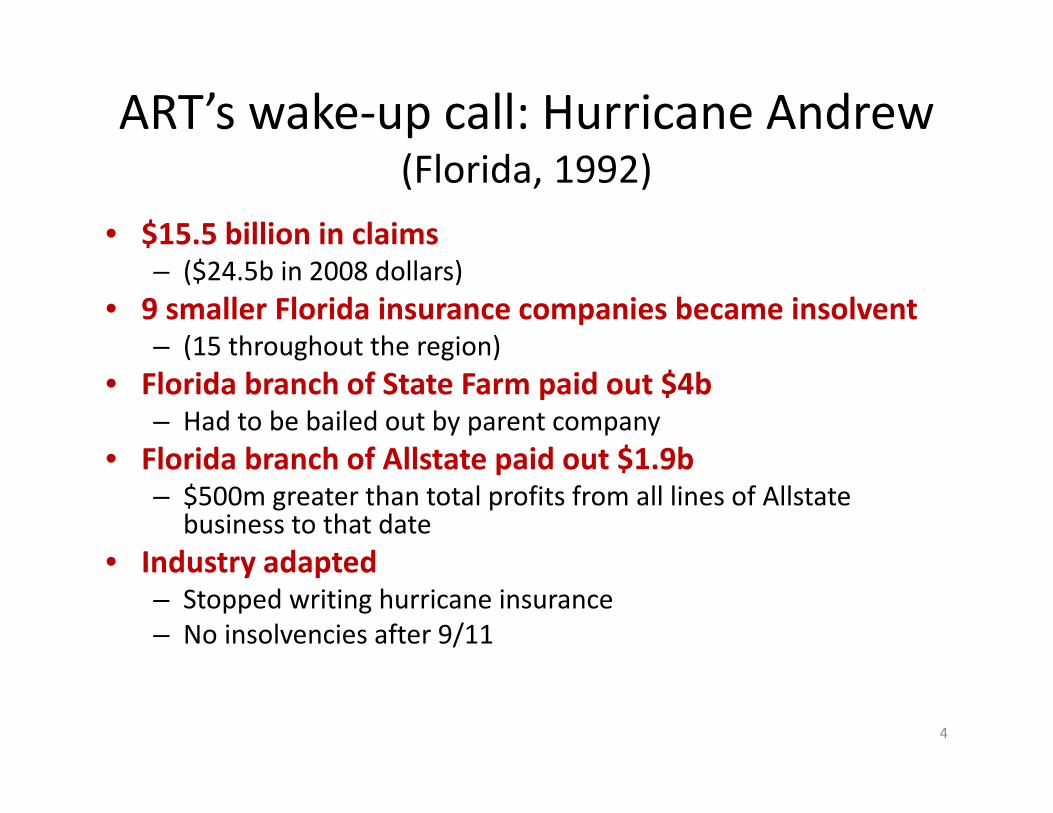

ART’s wake‐up call: Hurricane Andrew(Florida, 1992)

• $15.5 billion in claims– ($24.5b in 2008 dollars)

• 9 smaller Florida insurance companies became insolvent– (15 throughout the region)

• Florida branch of State Farm paid out $4b– Had to be bailed out by parent company

• Florida branch of Allstate paid out $1.9b– $500m greater than total profits from all lines of Allstate

business to that date• Industry adapted

– Stopped writing hurricane insurance– No insolvencies after 9/11

4

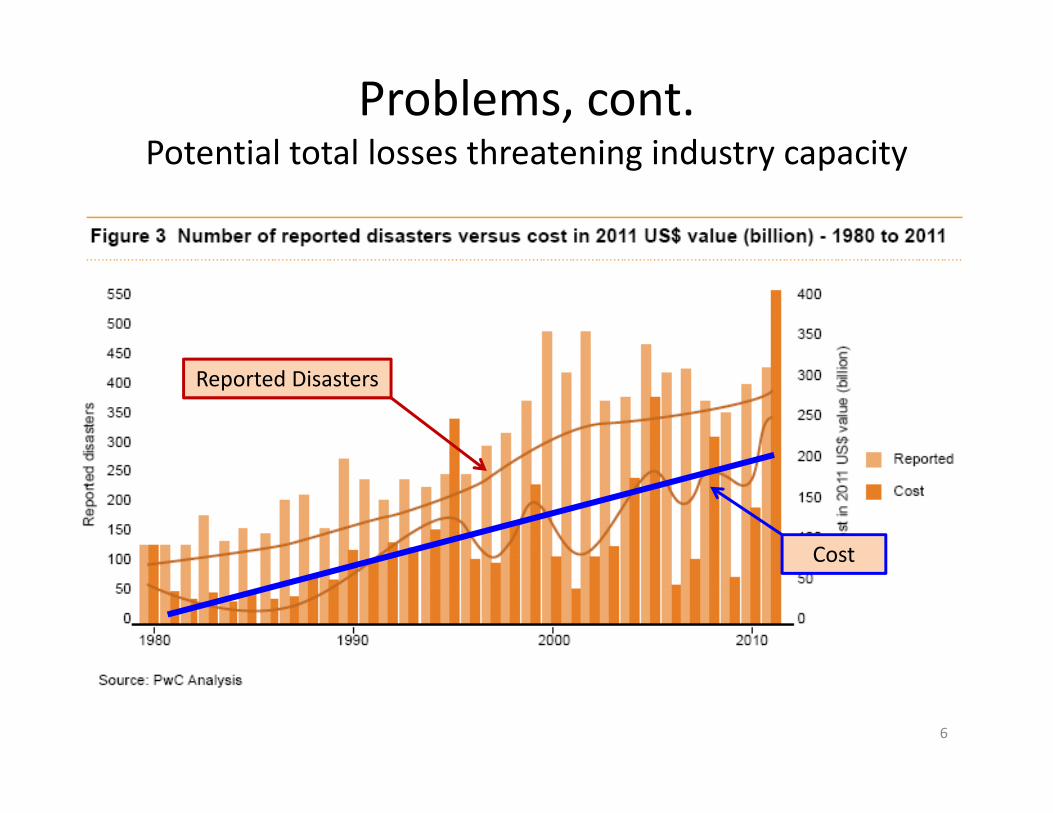

Difficulty created by catastrophic losses: Ambiguous risk

• Low mean losses• High maximum losses• Infrequent (1/6) in any single location– No way to pool risk for regional carriers

• Frequent (5/6) from global perspective– Global capacity insufficient

5

Problems, cont.Potential total losses threatening industry capacity

6

Reported Disasters

Cost

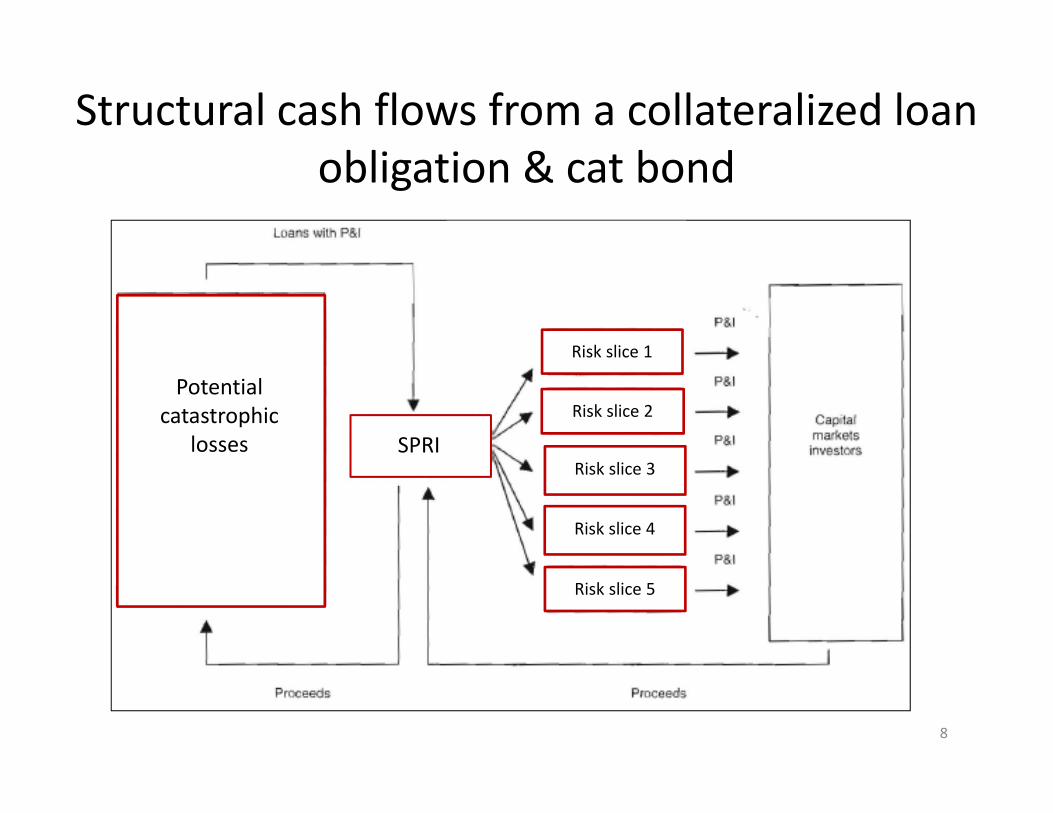

Structural cash flows from a collateralized loan obligation & cat bond

7

Structural cash flows from a collateralized loan obligation & cat bond

8

Potential catastrophic

losses SPRI

Risk slice 1

Risk slice 2

Risk slice 3

Risk slice 4

Risk slice 5

9

Triggers

10

Cat bond structure

11

Catastrophe strikesNo catastrophe strikes

12

CAT bond yields, Nov. 2012

13

Why they are popular• Issuers

– Use SPR• Capture tax and accounting benefits associated with traditional reinsurance

• Investors– Prefer SPR

• Isolates investment risk from business and credit risk of insurer

– Value near zero correlation with other asset classes

• Insureds– Fully collateralized

• Little or no counterparty risk

14

Why they are popular• Issuers

– Use SPR• Capture tax and accounting benefits associated with traditional reinsurance

• Investors– Prefer SPR

• Isolates investment risk from business and credit risk of insurer

– Value near zero correlation with other asset classes

• Insureds– Fully collateralized

• Little or no counterparty risk

15

Investors by category

16

Seeking reinsurance exposure but with higher returns

Sidecars

17

Self insurance and captives enter

ILS enter

Low returns

The beginning: 9/11

• Huge re/insurer losses• Market hardens

• Hedge funds entered reinsurance business–BUT couldn’t get out!

Joined mainstream ART market in 2005 after Katrina, Rita & Wilma

Statistics• Total insured cat losses ≈

$83.4 billion• U.S. portion ≈ $73–79 billion• Models failed

Effects on reinsurance• Models revised

– Predict greater losses

• Capital requirements raised on cat losses

• Ratings agencies changed way they assessed cat risk

,

Record Capital Model Rating agencylosses erosion revisions reassessments

Need for newSidecars

capital fast

20

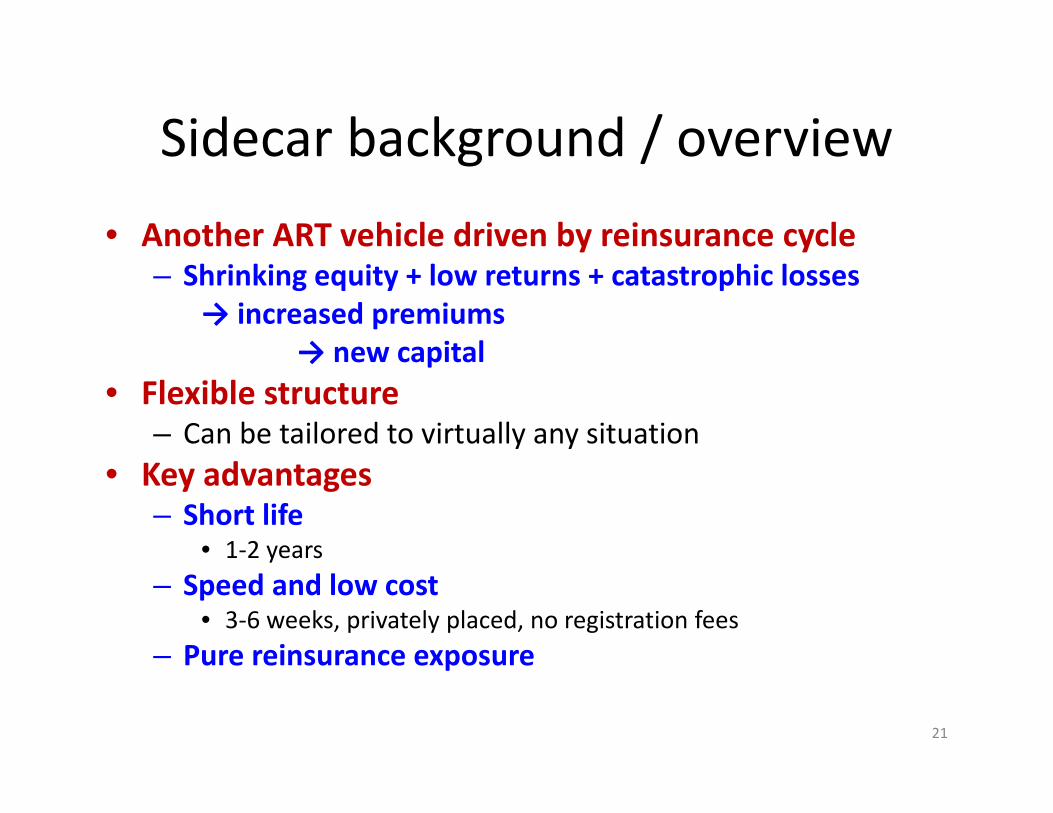

Sidecar background / overview• Another ART vehicle driven by reinsurance cycle

– Shrinking equity + low returns + catastrophic losses→ increased premiums

→ new capital• Flexible structure

– Can be tailored to virtually any situation• Key advantages

– Short life• 1‐2 years

– Speed and low cost• 3‐6 weeks, privately placed, no registration fees

– Pure reinsurance exposure

21

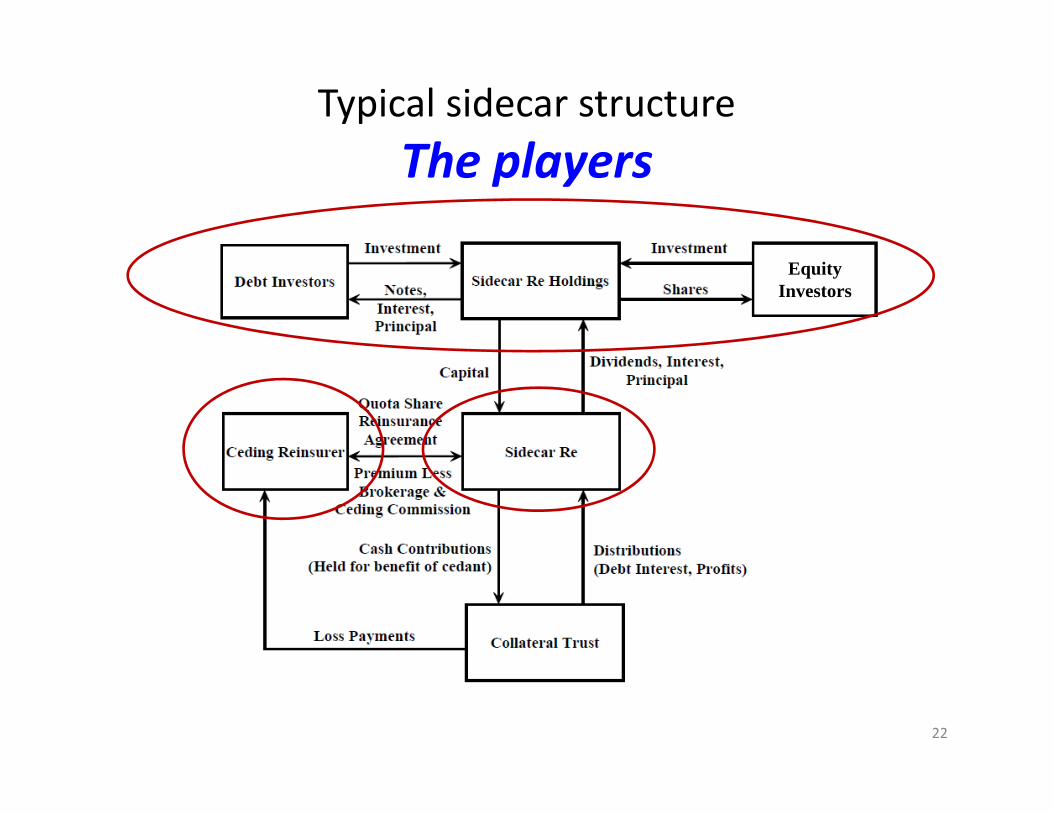

Typical sidecar structureThe players

Equity Investors

22

Typical sidecar structureThe players

Reinsurance companyCreated to assume underwriting risk from ceding (re)insurer

Constrained Special purpose entity that attaches to sponsor

Adds capacity Limited purposeFinite life

Re(insurer) championing the sidecar

Sole clientService provider

Assumes underwriting and claims settlement of sidecar

Receives feesReceives additional fees tied to profits

Capital market institutions seeking pure reinsurance exposure

Directly underwrite specific risksHedge funds, investment banks, private equity

High risk appetiteSeeking high returns

Equity Investors

23

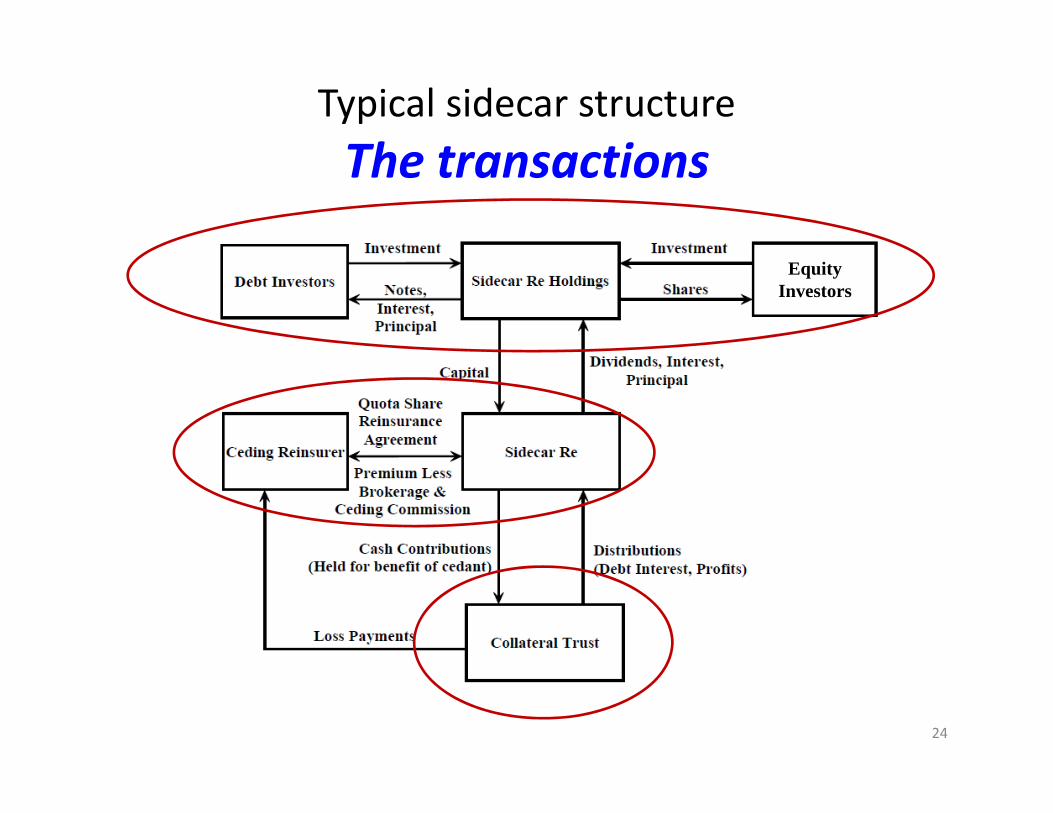

Typical sidecar structureThe transactions

Equity Investors

24

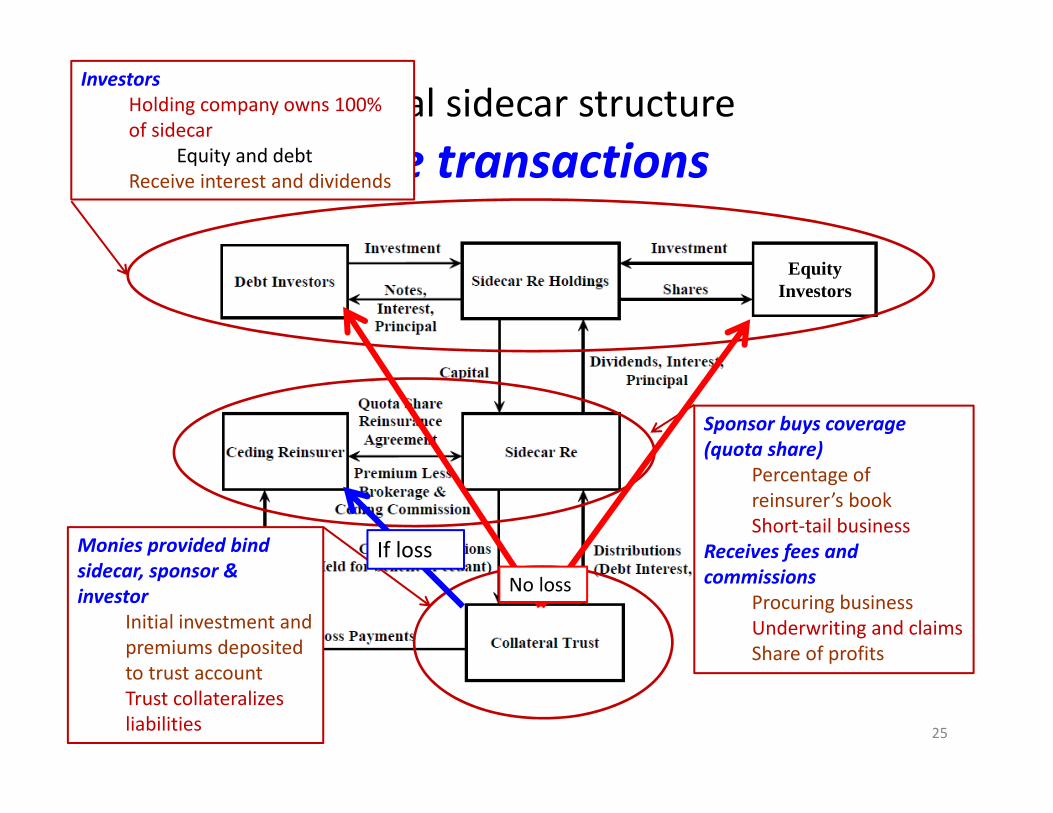

Typical sidecar structureThe transactions

Sponsor buys coverage (quota share)

Percentage of reinsurer’s bookShort‐tail business

Receives fees and commissions

Procuring businessUnderwriting and claimsShare of profits

InvestorsHolding company owns 100% of sidecar

Equity and debtReceive interest and dividends

Equity Investors

Monies provided bind sidecar, sponsor & investor

Initial investment and premiums deposited to trust accountTrust collateralizes liabilities

If lossNo loss

25

Newer developments

• Collateralized reinsurance (similar to sidecars)– Direct access to cat exposure

• No fees, etc.

• “Rent‐a‐sidecar”• Swiss Re sponsoring its own sidecar

– Putting in $100 million, seeking another $150‐200 million

• Aon → Lloyd’s → Berkshire Hathaway sidecar

Summary

• Cat bonds• Long‐term (3‐5 year) catastrophic coverage• In hard markets, cost effective• Issued by insurers, reinsurers, states, countries

• Sidecars– Provide just‐in‐time capital– Direct access to reinsurance exposure w/o balance sheet risk

– Finite, quota‐share agreement

27

Questions?

My thanks to Swiss Re, Munich Re, and PwC for many of the graphics in this slide deck. The latest reports are available free of charge from their respective websites.