Embed Size (px)

Citation preview

© OLIVER WYMAN

The Changing U.S. Healthcare Landscape

Mike Lovdal, Emeritus Partner

1© OLIVER WYMAN

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1960 1970 1980 1990 2000 2010

Pe

rce

nta

ge

(%

)

Year

Total

Private

Public

U.S. Healthcare Expenditures

Percent of GDP

Source: Centers for Medicare and Medicaid Services, 2013

$2.81T

$1.56T

$1.25T

U.S. health spending: 5% of GDP in 1960, 17.5% in 2013

Demographicage wave

Declining population

health status andattitudes

New medical and therapeutic

technologies

Fee-for-service payment systems

Sense of healthentitlement

Projected

User = payer

2© OLIVER WYMAN

U.S. healthcare performance

…2nd highest risk of dying of noncommunicable diseases and 4th

highest risk of dying from communicable diseases…

… the United States ranked last among males and next to last among females for

life expectancy…

… the United States had the highest infant mortality rate of the 17 peer

countries…

3© OLIVER WYMAN

Patient Protection and Affordable Care Act (aka ACA)

4© OLIVER WYMAN

King v. Burwell: Supreme Court to rule on Obamacare subsidies based on ACA language ambiguity (“. . . established by the State”)

5© OLIVER WYMAN

Exchange status

Maryland

New

ConnRI

Mass

Federal Exchange

Federal Exchange

(state policy)

State SHOP/ Federally-

Facilitated Individual

State Exchange

Source: Mercer

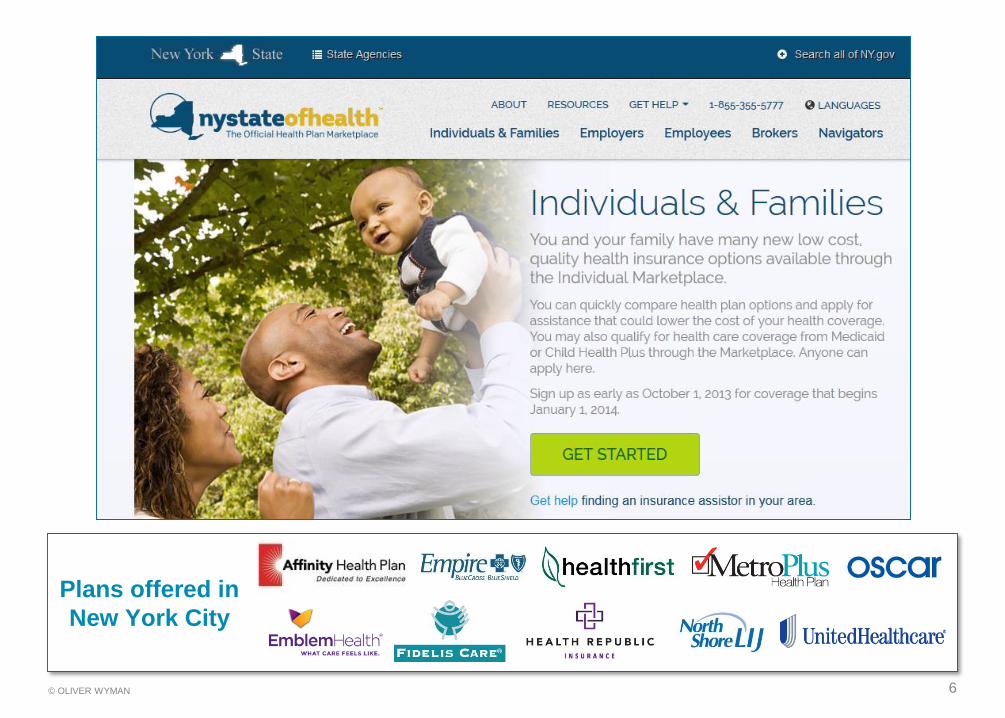

6© OLIVER WYMAN

Plans offered in

New York City

NOTES: Under discussion indicates executive activity supporting adoption of the Medicaid expansion. *AR, IA, MI, and PA have approved Section 1115 waivers; IN has a pending waiver to implement the expansion. The PA waiver is set to go into effect on January 1, 2015, but the newly-elected governor may opt for a state plan amendment. NH has submitted a waiver to continue their expansion via premium assistance. WI covers adults up to

100% FPL in Medicaid, but did not adopt the ACA expansion.

SOURCE: “Status of State Action on the Medicaid Expansion Decision,” KFF State Health Facts, updated December 17, 2014.http://kff.org/health-reform/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act/

State Medicaid expansion decisions

WY

WI*

WV

WA

VA

VT

UT

TX

TN

SD

SC

RI

PA*

OR

OK

OH

ND

NC

NY

NM

NJ

NH*

NVNE

MT

MO

MS

MN

MI*

MA

MD

ME

LA

KYKS

IA*

IN*IL

ID

HI

GA

FL

DC

DE

CT

COCA

AR*AZ

AK

AL

Adopted (28 States including DC)

Adoption under discussion (7 States)

Not Adopting At This Time (16 States)

Healthy Indiana Plan – a consumer-directed plan for low-income individuals. The Governor has requested to use the state-run plan in place of traditional Medicaid expansion

Coordinated Care Organizations –innovative experiment with managing Medicaid populations in coordinated care organizations

Accountable Care Entities – ACOs for Medicaid

Private Option – uses federal funds to purchase private coverage for low income residents

8© OLIVER WYMAN

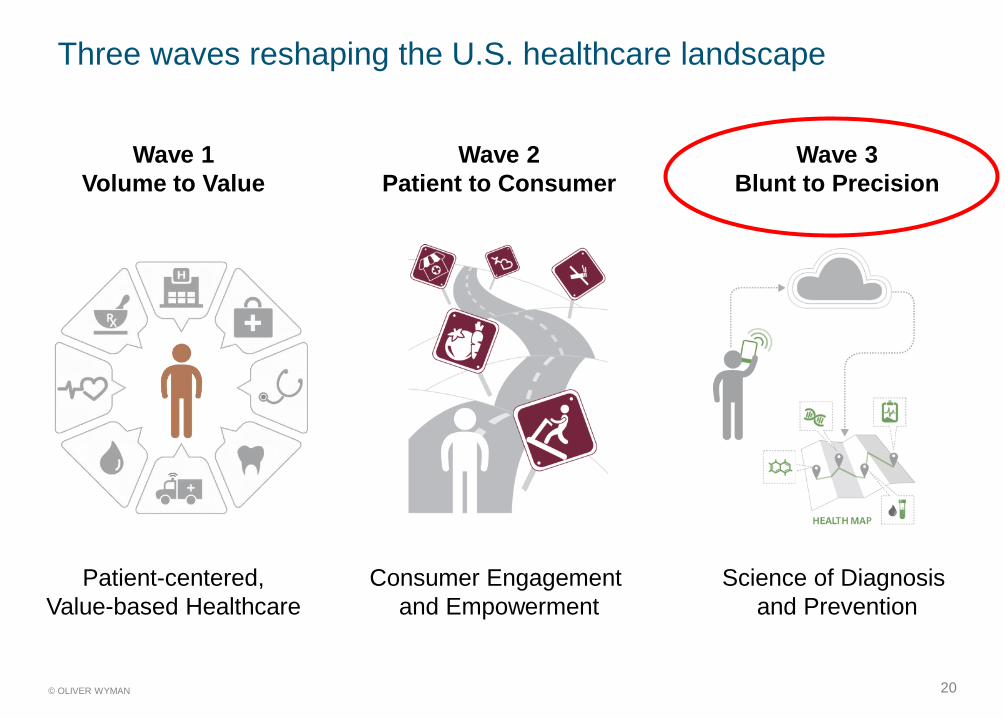

Patient-centered,

Value-based Healthcare

Consumer Engagement

and Empowerment

Science of Diagnosis

and Prevention

Three waves reshaping the U.S. healthcare landscape

Wave 1

Volume to Value

Wave 2

Patient to Consumer

Wave 3

Blunt to Precision

9© OLIVER WYMAN

How will the three waves impact your Community Heath Center’s business model?

Served Populations Revenue Models

Strategic Control Scope

Value Proposition

What revenue models will

we use to capture value

from serving these

consumers?

What consumer (aka patient)

segments (aka populations)

are we serving?

How will we protect our

consumer base and sustain

our value proposition?

What is our unique and

differentiated value

proposition relative to

competitors?

What value chain positions

and what assets and

partners do we need?

Wave 1

Volume to Value

Wave 2

Patient to Consumer

Wave 3

Blunt to Precision

Patient-centered,

Value-based Healthcare

Consumer Engagement

and Empowerment

Science of Diagnosis

and Prevention

10© OLIVER WYMAN

Patient-centered,

Value-based Healthcare

Consumer Engagement

and Empowerment

Science of Diagnosis

and Prevention

Three waves reshaping the U.S. healthcare landscape

Wave 1

Volume to Value

Wave 2

Patient to Consumer

Wave 3

Blunt to Precision

11© OLIVER WYMAN

Team-Based

Population

Health

IT

Interoperability

Predictive Care

Patient

Personalization

Patients First

Philosophy

Targeted

Engagement /

Management

Holistic Care Fast Analytics

Evidenced-

Based

Real-Time

Monitoring

Accessible and

Available

Patient-Centered

Care Core Principles

Wave 1: Patient-centered . . .

12© OLIVER WYMAN

Team-Based

Population

Health

IT

Interoperability?

Predictive Care

Patient

Personalization

Patients First

Philosophy

Targeted

Engagement /

Management

Holistic Care Fast Analytics

Evidenced-

Based

Real-Time

Monitoring

Accessible and

Available

Patient-Centered

Care Core Principles

Report to Congress

April 2015

Report on Health Information Blocking

The Office of the National Coordinator for

Health Information Technology (ONC)

. . . The federal government has

invested over $28 billion to

accelerate the development and

adoption of health IT . . .

. . . Current economic and market

conditions create business

incentives for some persons and

entities to exercise control over

electronic health information in

ways that unreasonably limit its

availability and use . . .

. . . Information blocking not only

interferes with effective health

information exchange but also

negatively impacts many important

aspects of health and health care.

One hurdle . . .

13© OLIVER WYMAN

Future: FFV

Partial Population

• Frail elder

• Poly-chronic

Full Population

• Pediatric

• All-risks

• Oncology

• Diabetes

• Asthma

• Chronic renal

• Orthopedics

• CV surgery

• General surgery

Today: FFS

Transactional

Models

Episodic

Care

Models

Condition

Care

Models

Population

Care

ModelsTransactional

Models

Episodic

Care

Models

Condition

Care

Models

Population

Care

Models

Wave 1: Patient-centered and value-based care

14© OLIVER WYMAN

75%Healthy

Independent

5%Complex /

Polychronic

20%Early State

Chronic

20%

45%ER visits,

overutilization, cost variation,

noncompliance

35%Infections,

complications, rehospitalizations

Wave 1: Patient-centered, value-based care

15© OLIVER WYMAN

HHS January 26, 2015 announcement

“HHS has set a goal of tying 30% of traditional, or fee-for-service, Medicare payments

to quality or value through alternative payment models, such as Accountable Care

Organizations (ACOs) or bundled payment arrangements by the end of 2016, and tying

50% of payments to these models by the end of 2018 . . .

. . . This is the first time in the history of the Medicare program that HHS has set

explicit goals for alternative payment models and value-based payments.”

16© OLIVER WYMAN

Reactions to HHS announcement

“We encourage the Administration to fully evaluate and improve on the delivery system reforms currently in place . . . Moreover, we need to phase in changes in a thoughtful manner tailored to the specific needs of individual communities.

We look forward to learning more from HHS on the details and metrics of this program.”

"Physicians have many ideas for redesigning and improving the delivery of high-quality patient care in this country . . .

We look forward to hearing more details behind the percentages HHS put forward as well as their plans to reach these percentage targets.”

“Advancing a patient-centered health system requires a fundamental

transformation in how we pay for and deliver care. Health plans have been

on the forefront of implementing payment reforms . . .

We are excited to bring these experiences and innovations to this new

collaboration.”

17© OLIVER WYMAN

$1T to value-based healthcare (in some form) by 2017

$0

$0.5 TN

$1.0 TN

$1.5 TN

$2.0 TN

$2.5 TN

$3.0 TN

$3.5 TN

$4.0 TN

2010 2015 2020 2025

Managed Medicaid: $268 B

MA

$1.5 T

Duals

$578 B

Innovative Employers

$1.2 T

Individuals & Exchange

$231 B

Value market by funding source

2010-2025

$3.7T in 2025

(70% of total spend)

TIPPING POINT:

FFV tops 30% of total market

18© OLIVER WYMAN

The transition is already underway, with 500+ ACOs currently in the market and hundreds of additional pilots on the way

Legend

Medicare / Medicaid

Private

Both

Prep activity only

Updated as of January 2014. Sources: News releases, company websites, Dartmouth Atlas PCSAs, Claritas, Oliver Wyman analysis

1. ACOs defined as providers participating in Pioneer ACO, Medicare Shared Savings, a Medicaid ACO, PGP Transition, or in a shared savings/risk arrangement with a commercial payer; Prep

activity defined as participation in a learning collaborative or providers preparing to become an ACO

19© OLIVER WYMAN

Accountable Care ... ... Organizations

• High quality care

• Efficient delivery

• Coordination of activities

• Measurable results

• Patient-centric

• Whose “Organization”

– Hospital?

– Doctor?

– Payer?

– Population Health Manager?

Where will the trillion $ migrate?

– Community Health Center?

20© OLIVER WYMAN

Patient-centered,

Value-based Healthcare

Consumer Engagement

and Empowerment

Science of Diagnosis

and Prevention

Three waves reshaping the U.S. healthcare landscape

Wave 1

Volume to Value

Wave 2

Patient to Consumer

Wave 3

Blunt to Precision

21© OLIVER WYMAN

Wave 3: Science of diagnosis and prevention

$100M

$10M

$1M

$100K

$10K

$1K

$100Co

st

to S

eq

uen

ce a

Wh

ole

Gen

om

e

2001 2005 2009 2013 2017 2021 2025

1. Source: National Human Genome Research Institute

2001

First human genome

sequenced for ~$95M

Today

Human genome

sequencing costs ~$1 -2K

2020 ?

High throughput

technology lowers cost to

~$100 / genome

22© OLIVER WYMAN

23© OLIVER WYMAN

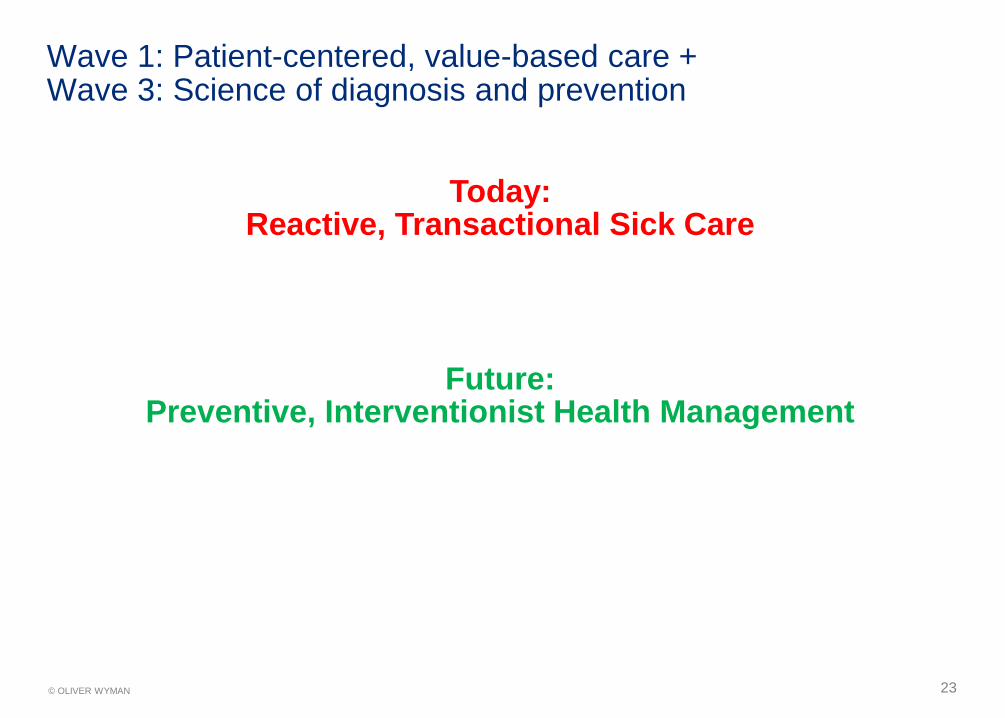

Future: Preventive, Interventionist Health Management

Today: Reactive, Transactional Sick Care

Wave 1: Patient-centered, value-based care + Wave 3: Science of diagnosis and prevention

24© OLIVER WYMAN

Patient-centered,

Value-based Healthcare

Consumer Engagement

and Empowerment

Science of Diagnosis

and Prevention

Three waves reshaping the U.S. healthcare landscape

Wave 1

Volume to Value

Wave 2

Patient to Consumer

Wave 3

Blunt to Precision

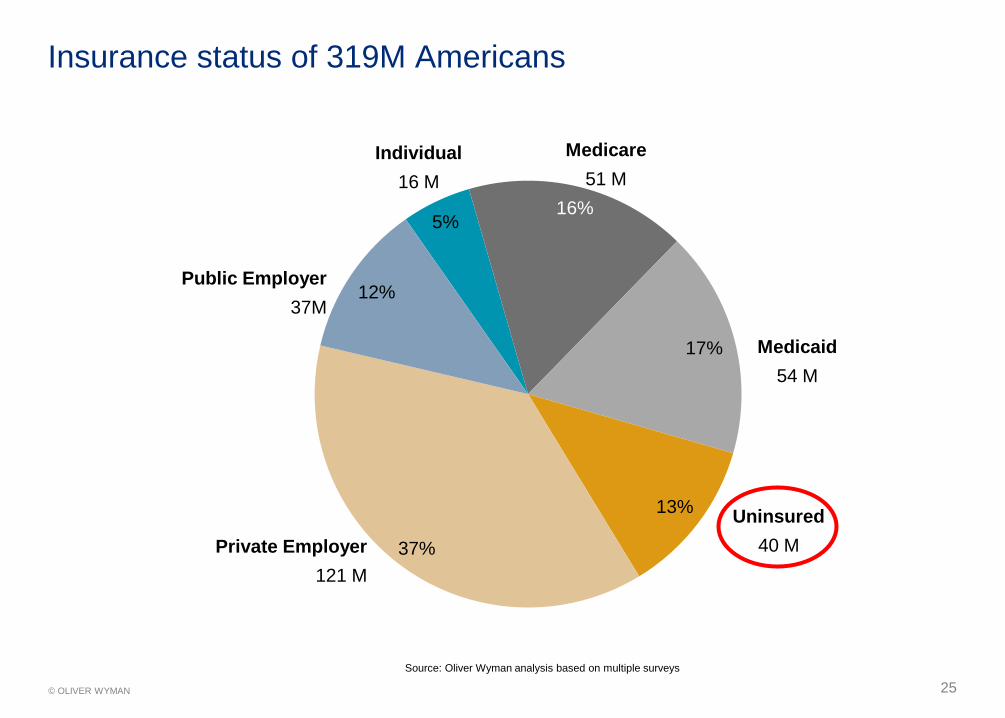

25© OLIVER WYMAN

Public Employer

37M

Individual

16 M

Medicare

51 M

Medicaid

54 M

Uninsured

40 MPrivate Employer

121 M

Source: Oliver Wyman analysis based on multiple surveys

5%16%

17%

13%

37%

12%

Insurance status of 319M Americans

26© OLIVER WYMAN

Medicare Vouchers and /or

Medicaid Block Grants are Adopted

More Employers Move to

Defined Contribution

But what if . . .

Active Employees

Retired Employees

27© OLIVER WYMAN

Public Employer

37M

Individual

16 M

Medicare

51 M

Medicaid

54 M

Uninsured

40 MPrivate Employer

121 M

Source: Oliver Wyman analysis based on multiple surveys

5%16%

17%

13%

37%

12%

Here comes the healthcare consumer! Changes to Medicare

(e.g., proposals for vouchers for

buying private insurance) = +51 M?

Changes to

Medicaid (e.g.,

block grants to

states) = +54 M?

Employers dropping

health coverage or

moving to defined-

contribution health

plans = +158 M?

Entry of the uninsured

through ACA penalties

+ exchange subsidies

= +40 M?

28© OLIVER WYMAN

Old World: Patients and members

Sick

At-Risk

Healthy

Provider

Payer

29© OLIVER WYMAN

New World: Consumer-centricity

Family Status

Employment

Education

Geography

Income Level

Social Network

Tech-savviness

Pref. Channels

Ambitions

Gender

Culture

Age

30© OLIVER WYMAN

Voice of the U.S. Healthcare Consumer

“We want to understand how to improve our health and live longer and better.”

“We want to be able to make informed decisions about health services.”

“We want simple, secure personal health information and tools.”

“We want to be able to stretch our dollars beyond the benefit plan.”

“We want anytime and anywhere access to convenient care.”

31© OLIVER WYMAN

“We want to understand how to improve our health and live longer and better.”

“We want to be able to make informed decisions about health services.”

“We want simple, secure personal health information and tools.”

“We want to be able to stretch our dollars beyond the benefit plan.”

“We want anytime and anywhere access to convenient care.”

Voice of the U.S. Healthcare Consumer

Source: IFTF, Centers for Disease Control and Prevention, Health and Health Care, 2010, The Forecast, The Challenge.

“We want to understand how to improve our health and live longer and better.”

Behavior 50%

Genetics 20%

Environment 20%

Access to care 10%

Drivers of health status

3333© Oliver Wyman

A B C ’ S

Aspirin

~60% compliance1

Blood Pressure

Control

(~50% compliance)2

Cholesterol

Control

(~50% compliance)3

Smoking

Cessation

(~30% compliance)4

1. Source: 1) Lip, Gregory. Shantsila, Eduard. “Aspirin Resistance’ or treatment non-compliance? Which is to blame for Cardiovascular Complications?” Journal of Translational Medicine, 2008. 2) Ahmed, Calhoun. “Apparent Resistant Hypertension and Medication Compliance.” Nature commentary of Hypertension Research, 2011. 3) Medscape Today: Lipid lowering therapy: Strategies for Improving Compliance: Improving Patient Compliance 4) Lightwood. “Smoking Cessation in heart failure-it is never too late. Journal of the

American College of Cardiology. 200

“We want to understand how to improve our health and live longer and better.”

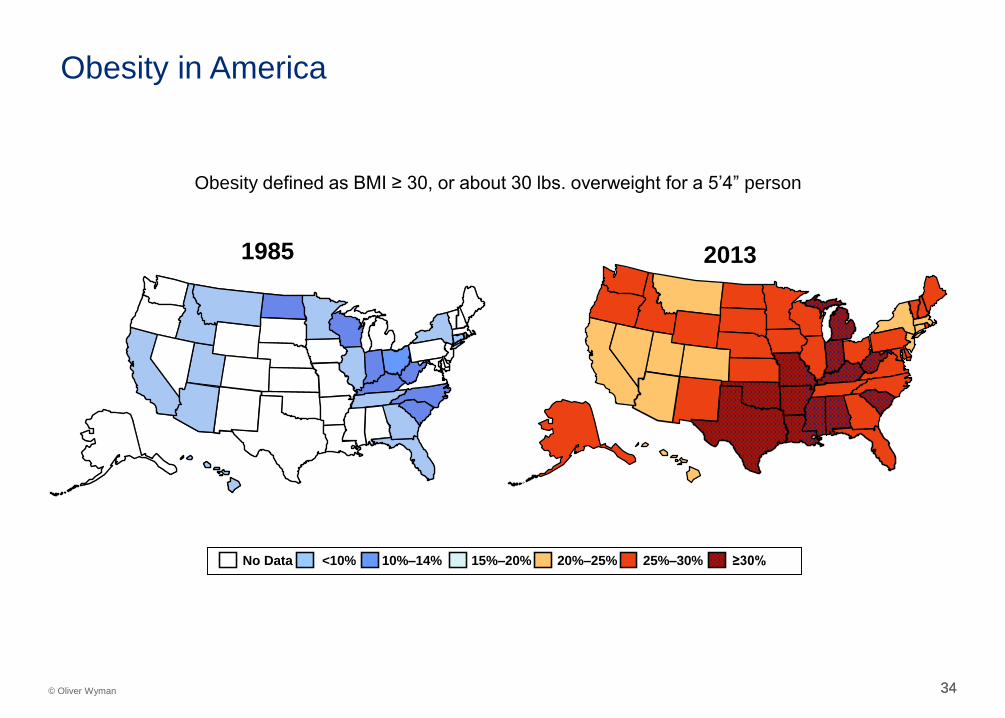

34© Oliver Wyman 34

1985

Obesity defined as BMI ≥ 30, or about 30 lbs. overweight for a 5’4” person

2013

No Data <10% 10%–14% 15%–20% 20%–25% 25%–30% ≥30%

Obesity in America

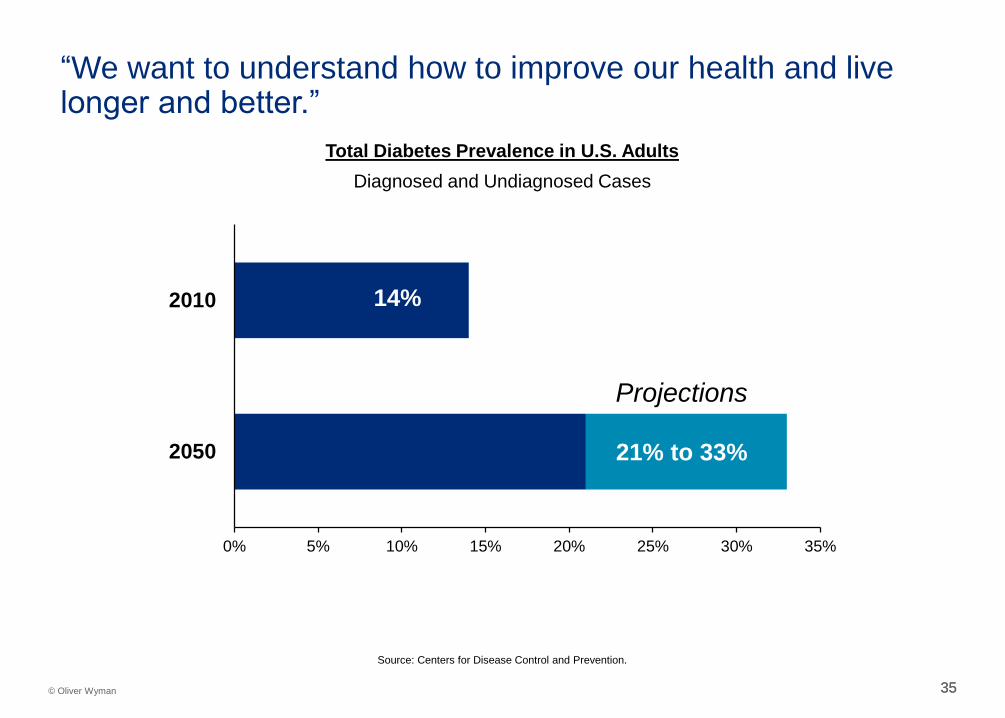

3535© Oliver Wyman

0% 5% 10% 15% 20% 25% 30% 35%

2010

2050

Source: Centers for Disease Control and Prevention.

14%

21% to 33%

Projections

Total Diabetes Prevalence in U.S. Adults

Diagnosed and Undiagnosed Cases

“We want to understand how to improve our health and live longer and better.”

3636© Oliver Wyman

“We want to understand how to improve our health and live longer and better.”

“We want to be able to make informed decisions about health services.”

“We want simple, secure personal health information and tools.”

“We want to be able to stretch our dollars beyond the benefit plan.”

“We want anytime and anywhere access to convenient care.”

Voice of the U.S. Healthcare Consumer

37© OLIVER WYMAN

No

Coordination of

Care

Hard to fit

patients in

schedule

Lack resources to

manage chronic

illnesses

DoctorsWait weeks

to see doctor

Too many

patients, too little

time

No time or $ to

talk end of life

Emotionally

attached

Byzantine

billing

More billing

staff than

nurses

Hard to be

ideal doc

Professional

frustration

Miss

Appointments

Problems go

unnoticed

Can’t

Drive

Complicated

referrals

15-20

medications

Patient

Expensive

hospitalization

Multiple

specialistsConflicting

treatmentsNo holistic

care

Emergency?

Call 911

Expensive

co-pays

No end-of-life

plan

Health

Plan

Redundant

treatment

Hard to find

quality docs

Costly

senior

care

Risk of

adverse

selection

death spiral

Need to

minimize

costs Staff

focused on

costs, not

preventionSmall

margin for

Medicare

patients Denial of

coverage

Healthcare hassle map

38© OLIVER WYMAN

22% 41%

40%

24%

14%

24%32%

40%Finding

information

Enrolling in

a plan

Figuring out

premium costs

Learning about

resources

(e.g. Gym discounts)

Getting information

about vision, dental,

etc.

Understanding

what I have to pay

for care

Comparing

health plans

Understanding

what is covered

Hassle Map for finding health insurance coverage

3939© Oliver Wyman

“We want to understand how to improve our health and live longer and better.”

“We want to be able to make informed decisions about health services.”

“We want simple, secure personal health information and tools.”

“We want to be able to stretch our dollars beyond the benefit plan.”

“We want anytime and anywhere access to convenient care.”

Voice of the U.S. Healthcare Consumer

40© OLIVER WYMAN

?Will consumers opt-in

to the cloud or will

privacy concerns

drive “in-pocket”

alternatives

“We want simple, secure personal health information and tools.”

41© OLIVER WYMAN

Healthcare-Focused Social Media

“We want simple, secure personal health information and tools.”

42© OLIVER WYMAN

Tech Times | October 6 2014, 9:17 AM

“We want simple, secure personal health information and tools.”

Easy-to-use, affordable

technology to track patients and

their health conditions remotely

Reflexion Health uses Kinect for Windows to bring physical therapy to patients’ homes

“We want simple, secure personal health information and tools.”

44© OLIVER WYMAN

“We want simple, secure personal health information and tools.”

Google’s Glucose Tracking Contact LensInstant Heart Rate Monitor

Lens measures glucose levels in tears,

potentially relieving millions of diabetics from the

burden of having to prick their fingers to draw

their blood as many as 10 times a day

App uses the camera lens to monitor heart

rate by detecting changes in color in the

user’s fingertip

“We want simple, secure personal health information and tools.”

46© OLIVER WYMAN

“We want to understand how to improve our health and live longer and better.”

“We want to be able to make informed decisions about health services.”

“We want simple, secure personal health information and tools.”

“We want to be able to stretch our dollars beyond the benefit plan.”

“We want anytime and anywhere access to convenient care.”

Voice of the U.S. Healthcare Consumer

47© OLIVER WYMAN

“We want to be able to stretch our dollars beyond the benefit plan.”

Do you think your doctor should discuss the cost of recommended medical treatment

with you ahead of time, or don’t you think that is necessary?

80%

18%

2%

Should discuss

Not necessary

No opinion

Should discuss

Source: CBS / NYT poll

48© OLIVER WYMAN

Disparities in healthcare prices have captured media attention

49© OLIVER WYMAN

The transparency revolution has already reshaped other consumer-facing service industries

50© OLIVER WYMAN

Innovators are driving and monetizing transparency

51© OLIVER WYMAN

“The lack of price transparency in health care threatens

to erode public trust in our healthcare system . . .

The time for price transparency in health care is now.”

The definitive statement on transparency

52© OLIVER WYMAN

You will be rated . . .

Cost

Experience

Access Quality Winning in the Future

You will be rated by several sources, crowd-sourced and B2C

Sources of Medical Ratings

54© OLIVER WYMAN

“We want to understand how to improve our health and live longer and better.”

“We want to be able to make informed decisions about health services.”

“We want simple, secure personal health information and tools.”

“We want to be able to stretch our dollars beyond the benefit plan.”

“We want anytime and anywhere access to convenient care.”

Voice of the U.S. Healthcare Consumer

55© OLIVER WYMAN

Retailer clinics

Total rooftops:

7,800 8,582 4,987 2,638 1,801

Ratio: 1 : 9 1 : 21 1 : 38 1 : 19 1 : 26

4,587

1 : 153

~30~70

~140~130

~400

~900

0

100

200

300

400

500

600

700

800

900

Source: Company Websites and Annual Reports

“We want anytime and anywhere access to convenient care.”

56© OLIVER WYMAN © OLIVER WYMAN

Urgent Care in New York City

Source: Company Websites

40 locations in NY today,

9 more planned (3 in New Jersey)

“We want anytime and anywhere access to convenient care.”

57© OLIVER WYMAN

“We want anytime and anywhere access to convenient care.”

58© OLIVER WYMAN

“We want anytime and anywhere access to convenient care.”

59© OLIVER WYMAN

“We want to understand how to improve our health and live longer and better.”

“We want to be able to make informed decisions about health services.”

“We want simple, secure personal health information and tools.”

“We want to be able to stretch our dollars beyond the benefit plan.”

“We want anytime and anywhere access to convenient care.”

“We want help with caregiving.”

“We want to live independently.”

Voice of the U.S. Healthcare Consumer

The voice of specific segments

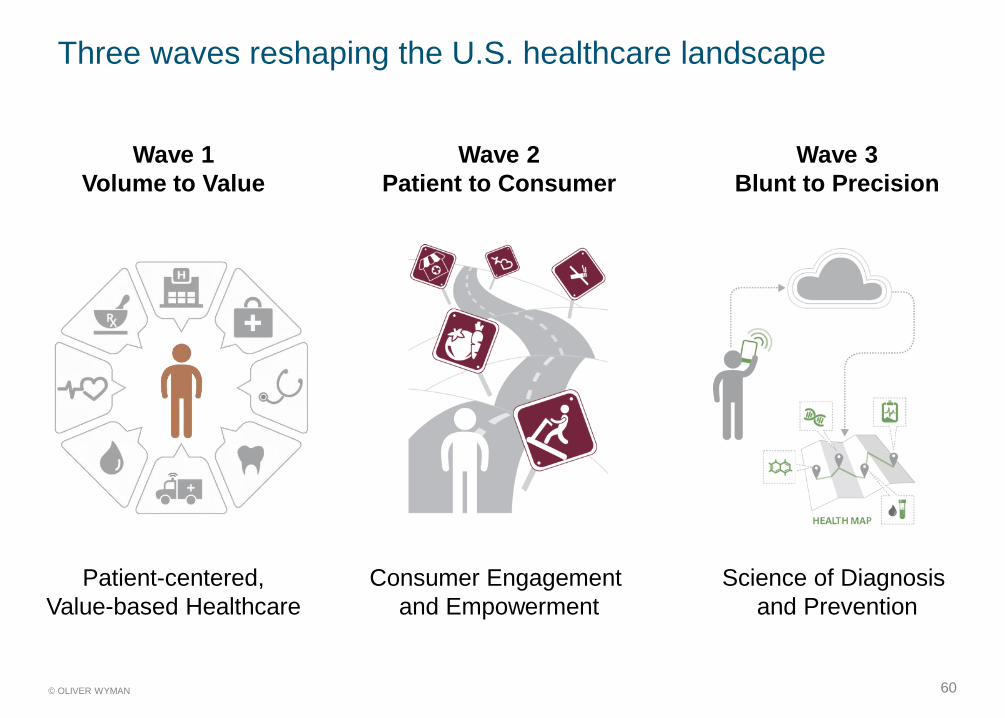

60© OLIVER WYMAN

Patient-centered,

Value-based Healthcare

Consumer Engagement

and Empowerment

Science of Diagnosis

and Prevention

Three waves reshaping the U.S. healthcare landscape

Wave 1

Volume to Value

Wave 2

Patient to Consumer

Wave 3

Blunt to Precision

61© OLIVER WYMAN

How will the three waves impact your Community Heath Center’s business model?

Served Populations Revenue Models

Strategic Control Scope

Value Proposition

What revenue models will

we use to capture value

from serving these

consumers?

What consumer (aka patient)

segments (aka populations)

are we serving?

How will we protect our

consumer base and sustain

our value proposition?

What is our unique and

differentiated value

proposition relative to

competitors?

What value chain positions

and what assets and

partners do we need?

Wave 1

Volume to Value

Wave 2

Patient to Consumer

Wave 3

Blunt to Precision

Patient-centered,

Value-based Healthcare

Consumer Engagement

and Empowerment

Science of Diagnosis

and Prevention