Embed Size (px)

Citation preview

NEW ISSUE - BOOK-ENTRY ONLY RATINGS S&P:“AAA” (Insured)

S&P: “A” (underlying)

(See “CONCLUDING INFORMATION - RATINGS ON THE BONDS” herein)

In the opinion of Fulbright & Jaworski L.L.P., Los Angeles, California, Bond Counsel, under existing law interest on the Bonds is exempt from personal income taxes of the State of California and, assuming compliance with the tax covenants described herein, interest on the Bonds is excluded pursuant to section 103(a) of the Internal Revenue Code of 1986 (the “Code”) from the gross income of the owners thereof for federal income tax purposes and is not an item of preference under section 57(a) of the Code for purposes of the federal alternative minimum tax. See, however, “ LEGAL MATTERS - TAX MATTERS” herein regarding certain other tax considerations.

RIVERSIDE COUNTY STATE OF CALIFORNIA

$15,330,000* LAKE ELSINORE PUBLIC FINANCING AUTHORITY TAX ALLOCATION REVENUE BONDS (1999 SERIES C REFUNDING), 2010 SERIES A

Dated: Date of Delivery Due: September 1 as shown on the inside front cover.

The cover page contains certain information for quick reference only. It is not a summary of the issue. Potential investors must read the entire Official Statement to obtain information essential to making an informed investment decision. See “BONDOWNERS’ RISKS” herein for a discussion of special risk factors that should be considered in evaluating the investment quality of the Bonds.

Interest on the Bonds is payable semiannually on March 1 and September 1 of each year, commencing on September 1, 2010, until maturity or earlier redemption (see “THE BONDS - GENERAL PROVISIONS” and “THE BONDS - REDEMPTION” herein).

_____________________________________________________________________________________

The scheduled payment of principal of and interest on the Bonds when due will be guaranteed under a financial guaranty insurance

policy to be issued concurrently with the delivery of the Bonds by Assured Guaranty Corp. (see “SOURCES OF PAYMENT FOR THE

BONDS – BOND INSURANCE” herein).

_____________________________________________________________________________________

The information contained within this Official Statement was prepared under the direction of the Lake Elsinore Public Financing

Authority (the “Authority”) by the following firm serving as Financing Consultant to the Authority:

ROD GUNN ASSOCIATES, INC.

_____________________________________________________________________________________

MATURITY SCHEDULE (see inside cover)

____________________________________________________________________________

The Bonds are payable solely from the revenues pledged under the Indenture (the “Revenues”), consisting primarily of proceeds from the repayment of Loans with respect to three separate Redevelopment Projects and the Low and Moderate Income Housing Fund, as described herein, to be made by the Redevelopment Agency of the City of Lake Elsinore (the “Agency”) to the Authority and certain other funds held under the Indenture as described herein. The Loans are payable by the Agency solely from Tax Revenues or Housing Set-Aside Revenues (as defined herein) attributable to the Redevelopment Project to which such loan relates, as described herein, or with respect to the Housing Loan solely from Housing Set-Aside Revenues attributable to the Redevelopment Projects deposited into the Low and Moderate Income Housing Fund (see “SOURCES OF PAYMENT FOR THE BONDS” and “BONDOWNERS’ RISKS” herein).

A portion of the proceeds from the Bonds will be used, on the delivery date of the Bonds, to refund the Lake Elsinore Public Financing Authority Tax Allocation Revenue Bonds, 1999 Series C.

It is anticipated that the Bonds, in book-entry form, will be available for delivery through the facilities of The Depository Trust Company in New York, New York, on or about February 4, 2010 (see “APPENDIX H – DTC AND BOOK-ENTRY–ONLY SYSTEM”).

The date of the Official Statement is ___________.

___________________________ * Preliminary, subject to change.

PRELIMINARY OFFICIAL STATEMENT DATED JANUARY 20, 2010Th

is P

relim

inar

y O

ffici

al S

tate

men

t and

info

rmat

ion

cont

aine

d he

rein

are

sub

ject

to c

ompl

etio

n or

am

endm

ent w

ithou

t not

ice.

The

se s

ecur

ities

may

not

be

sold

nor

an

offe

r to

buy

be a

ccep

ted

prio

r to

the

time

the

Offi

cial

Stat

emen

t is

deliv

ered

in fi

nal f

orm

. U

nder

no

circ

umst

ance

s sh

all t

his

Prel

imin

ary

Offi

cial

Sta

tem

ent c

onst

itute

an

offe

r to

sell

or th

e so

licita

tion

of a

n of

fer t

o bu

y, n

or s

hall

ther

e be

any

sal

e of

thes

e se

curit

ies

in a

nyju

risdi

ctio

n in

whi

ch s

uch

offe

r, so

licita

tion

or s

ale

wou

ld b

e un

law

ful p

rior t

o re

gist

ratio

n or

qua

lific

atio

n un

der t

he s

ecur

ities

law

s of

any

suc

h ju

risdi

ctio

n.

i

$15,330,000* LAKE ELSINORE PUBLIC FINANCING AUTHORITY

TAX ALLOCATION REVENUE BONDS (1999 SERIES C REFUNDING),

2010 SERIES A

MATURITY SCHEDULE (Base CUSIP®** ____)

$6,240,000* Serial Bonds

Maturity Date September 1_

Principal Amount*

Interest _Rate_

Reoffering __Rate__

CUSIP® Suffix**

2010 $680,000 2011 300,000 2012 305,000 2013 310,000 2014 320,000 2015 325,000 2016 340,000 2017 345,000 2018 360,000 2019 375,000 2020 390,000 2021 400,000 2022 420,000 2023 435,000 2024 455,000 2025 480,000

$9,090,000* _____% Term Bonds due September 1, 2033, Price ___% CUSIP® Suffix** ____

___________________________ * Preliminary, subject to change. ** CUSIP® Copyright 2010. American Bankers’ Association. CUSIP® data herein is provided by Standard & Poor’s CUSIP® Service Bureau, a Division of The McGraw-Hill Companies, Inc. This data is not intended to create a database and does not serve in any way as a substitute for the CUSIP® Service Bureau. CUSIP® numbers are provided for convenience of reference only. The Authority and the Underwriter do not guarantee the accuracy of the CUSIP® data herein.

ii

LAKE ELSINORE PUBLIC FINANCING AUTHORITY LAKE ELSINORE, CALIFORNIA

AUTHORITY GOVERNING BOARD Daryl Hickman, Chairperson

Amy Bhutta, Vice-Chairperson Robert E. Magee, Board Member Thomas Buckley, Board Member

Melissa A. Melendez, Board Member ______________________________________________

CITY COUNCIL Melissa A. Melendez, Mayor Amy Bhutta, Mayor Pro Tem

Thomas Buckley, Council Member, Robert E. Magee, Council Member Daryl Hickman, Council Member

______________________________________________ AGENCY BOARD OF DIRECTORS

Robert E. Magee, Chairperson Thomas Buckley, Vice-Chairperson

Amy Bhutta, Board Member Melissa A. Melendez, Board Member

Daryl Hickman, Board Member ______________________________________________

CITY, AUTHORITY AND AGENCY STAFF Robert A. Brady, City Manager /Authority and Agency Executive Director

Barbara Leibold, City Attorney / Authority and Agency Counsel James R. Riley, CPA, Acting Director of Administrative Services / Authority and Agency Treasurer

Debora Thomsen, City Clerk / Authority and Agency Secretary ________________________________________

PROFESSIONAL SERVICES

Bond Counsel and Disclosure Counsel Fulbright & Jaworski L.L.P.

Los Angeles, California City Attorney

Leibold, McClendon & Mann, P.C. Laguna Hills, California Financing Consultant

Rod Gunn Associates, Inc. Huntington Beach, California

Trustee and Fiscal Agent Union Bank, N.A.

Los Angeles, California

Fiscal Consultant HdL Coren & Cone

Diamond Bar, California Underwriter

O’Connor & Company Securities, Inc. Newport Beach, California Underwriter’s Counsel

McFarlin & Anderson LLP Lake Forest, California

_______________________________________

FOR ADDITIONAL INFORMATION James R. Riley, CPA, City of Lake Elsinore (951) 674-3124

O’Connor & Company Securities, Inc. (949) 706-0444

iii

GENERAL INFORMATION ABOUT THE OFFICIAL STATEMENT

Use of Official Statement. This Official Statement is submitted in connection with the offer and sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part, for any other purpose. This Official Statement is not to be construed as a contract with the purchasers of the Bonds.

Estimates and Forecasts. When used in this Official Statement and in any continuing disclosure by the Agency, in any press release and in any oral statement made with the approval of an authorized officer of the Agency, the words or phrases “will likely result,” “are expected to,” “will continue,” “is anticipated,” “estimate,” “forecast,” “expect,” “intend,” and similar expressions identify “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended. Such statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forward-looking statements. Any forecast is subject to such uncertainties. Inevitably, some assumptions used to develop the forecasts will not be realized and unanticipated events and circumstances may occur. Therefore, there are likely to be differences between forecasts and actual results and those differences may be material. The information and expressions of opinion herein are subject to change without notice, and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, give rise to any implication that there has been no change in the affairs of the Agency or any other entity described or referenced herein since the date hereof. Neither the Authority nor the Agency plan to issue any updates or revisions to the forward-looking statements set forth in this Official Statement.

Limited Offering. No dealer, broker, salesperson or other person has been authorized by the Authority or the Agency to give any information or to make any representations in connection with the offer or sale of the Bonds other than those contained herein and if given or made, such other information or representation must not be relied upon as having been authorized by the Authority, the Agency or the Underwriter. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale.

Involvement of Underwriter. The Underwriter has submitted the following statement for inclusion in this Official Statement: The Underwriter has reviewed the information in this Official Statement in accordance with, and as a part of, its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information. The information and expressions of opinions herein are subject to change without notice and neither delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the Authority, the Agency or any other entity described or referenced herein since the date hereof. All summaries of the documents referred to in this Official Statement are made subject to the provisions of such documents and do not purport to be complete statements of any or all of such provisions.

Bond Insurer. The Assured Guaranty Corp. (“AGC”) makes no representation regarding the Bonds or the advisability of investing in the Bonds. In addition, AGC has not independently verified, makes no representation regarding, and does not accept any responsibility for the accuracy or completeness of this Official Statement or any information or disclosure contained herein, or omitted herefrom, other than with respect to the accuracy of the information regarding AGC supplied by AGC and presented under the heading “SOURCES OF PAYMENT FOR THE BONDS - BOND INSURANCE” and “APPENDIX F - SPECIMEN FINANCIAL GUARANTY INSURANCE POLICY.”

THE BONDS HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON AN EXEMPTION FROM THE REGISTRATION REQUIREMENTS CONTAINED IN SUCH ACT. THE BONDS HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER THE SECURITIES LAWS OF ANY STATE.

iv

TABLE OF CONTENTS INTRODUCTORY STATEMENT ............................1 THE AUTHORITY ......................................................1 Authorization and Formation ........................................1 Bond Authorization and Issuance..................................1 Financing Purpose of the Bonds ...................................2 THE AGENCY .............................................................2 Formation......................................................................2 Tax Allocation Financing ..............................................2 Housing Set-Aside Revenues ........................................2 Redevelopment Agency Project Area Boundaries.........3 THE REDEVELOPMENT PROJECTS.......................4 Redevelopment Project No. I........................................4 Formation......................................................................4 General Description. .....................................................4 Redevelopment Project No. II ......................................4 Formation......................................................................4 General Description. .....................................................4 Redevelopment Project No. III .....................................5 Formation......................................................................5 General Description ......................................................5 THE LOANS ................................................................5 Project No. I Loan ........................................................5 Authorization ................................................................5 Outstanding Bonded Indebtedness of

Redevelopment Project No. I .....................................6 Project No. II Loan .......................................................6 Authorization ................................................................6 Outstanding Bonded Indebtedness of

Redevelopment Project No. II....................................7 Project No. III Loan......................................................7 Authorization ................................................................7 Outstanding Bonded Indebtedness of

Redevelopment Project No. III ..................................7 The Housing Loan ........................................................7 Authorization ................................................................7 Outstanding Indebtedness of the Low and

Moderate Income Housing Fund................................8 SECURITY AND SOURCES OF REPAYMENT ........8 The Indenture................................................................8 The Loan Agreements ...................................................8 THE FINANCING PLAN ............................................8 Bond Insurance .............................................................8 The Refunding Program................................................8 REDEMPTION OF THE BONDS ...............................9 Mandatory Redemption from Optional Loan

Prepayments...............................................................9 Mandatory Sinking Payment Redemption.....................9 Mandatory Redemption upon Acceleration of the

Loans..........................................................................9 THE BONDS GENERAL PROVISIONS ....................9 Denominations ..............................................................9 Registration, Transfer and Exchange ............................9 Payment ........................................................................9 Notice..........................................................................10 LEGAL MATTERS ....................................................10

PROFESSIONAL SERVICES....................................10 FINANCIAL STATEMENTS.....................................11 CONTINUING DISCLOSURE..................................11 AVAILABILITY OF LEGAL DOCUMENTS............11

SELECTED ESSENTIAL FACTS .............................12 ESTIMATED SOURCES AND USES OF

FUNDS.......................................................................17 THE BONDS..............................................................17 THE LOANS..............................................................18

THE BONDS................................................................19 GENERAL PROVISIONS .........................................19 Repayment of the Bonds.............................................19 Transfer or Exchange of Bonds ..................................19 Bonds Mutilated, Lost, Destroyed or Stolen...............19 REDEMPTION ..........................................................20 Mandatory Sinking Payment Redemption ..................20 Mandatory Redemption from Optional Loan

Prepayments.............................................................20 Mandatory Redemption upon Acceleration of the

Loans .......................................................................20 Notice of Redemption; Rescission..............................20 Open Market Purchase of Bonds ................................21 Selection of Bonds for Redemption............................21 Effect of Redemption..................................................21 Partial Redemption .....................................................21 SCHEDULED DEBT SERVICE ON THE

BONDS....................................................................22 SCHEDULED DEBT SERVICE ON THE

LOANS....................................................................23 Redevelopment Project No. I Loan ............................23 Redevelopment Project No. II Loan ...........................24 Redevelopment Project No. III Loan..........................25 Housing Loan .............................................................26

SOURCES OF PAYMENT FOR THE BONDS........27 REPAYMENT OF THE BONDS ...............................27 The Bonds ..................................................................27 Reserve Fund ..............................................................27 REPAYMENT OF THE LOANS................................28 Tax Allocation Financing............................................28 In General ...................................................................28 Allocation of Taxes.....................................................28 Pledge of Tax Revenues or Housing Set-Aside

Revenues..................................................................29 Project No. I Loan ......................................................29 Project No. II Loan.....................................................29 Project No. III Loan....................................................29 Housing Loan .............................................................30 Alternative Method of Tax Apportionment

(“Teeter Plan”).........................................................30 ISSUANCE OF ADDITIONAL DEBT......................31 The Authority..............................................................31 The Agency.................................................................31 Subordinate Debt ........................................................32 BOND INSURANCE.................................................33

v

The Insurance Policy ..................................................33 The Insurer..................................................................33

BONDOWNERS’ RISKS............................................35 THE BONDS..............................................................35 General........................................................................35 No Liability of the Authority to the Owners................35 No Effective Acceleration on Default .........................35 Enforceability of Remedies.........................................35 Bond Insurer Default ..................................................35 Investment of Funds....................................................36 Secondary Market .......................................................36 THE LOANS ..............................................................36 Risk Factors Relating to the Reduction of Tax

Increment Revenues .................................................36 General........................................................................36 Reduction in Inflationary Rate. ...................................37 Assessment Appeals. ...................................................38 Proposition 8 Adjustments ..........................................38 Levy and Collection....................................................39 Property Owner Bankruptcy .......................................39 Risk Factors Related to Real Estate Market

Conditions................................................................39 Development Risks .....................................................39 Current Real Estate Market Conditions ......................39 Adjustable Rate and Unconventional Mortgage

Structures .................................................................40 Risk Factors Related to Natural and Man-Made

Disasters...................................................................41 Risk Factors Relating to the Loans and the

Redevelopment Law.................................................41 Loans are a Limited Obligation...................................41 Redevelopment Plan Limitations on Tax Revenues

.................................................................................41 Risk Factors Related to Bankruptcy of the

Authority and the Agency ........................................42 Risk Factors Related to State Budget Legislation .......42 Risk Factors Related to Assumptions and

Projections of Tax Revenues....................................44 PROPERTY TAXATION IN CALIFORNIA............45

CONSTITUTIONAL AMENDMENTS AFFECTING TAX INCREMENT REVENUES.....45

IMPLEMENTING LEGISLATION ...........................45 CONSTITUTIONAL CHALLENGES TO

PROPERTY TAX SYSTEM....................................46 PROPERTY TAX COLLECTION

PROCEDURES........................................................46 SUPPLEMENTAL ASSESSMENTS..........................46 TAX COLLECTION FEES ........................................47 UNITARY PROPERTY TAX .....................................47 BUSINESS INVENTORY AND

REPLACEMENT REVENUE.................................47 PROPOSITION 87 .....................................................47 FUTURE INITIATIVES.............................................48

THE AUTHORITY .....................................................49 GENERAL..................................................................49 AUTHORIZATION....................................................49 The Bonds...................................................................49

The Loans ...................................................................49 AUTHORITY FINANCIAL STATEMENTS.............49 DEBT SERVICE PAYMENTS ON THE LOANS

AND DEBT SERVICE COVERAGE ON THE AUTHORITY BONDS............................................50

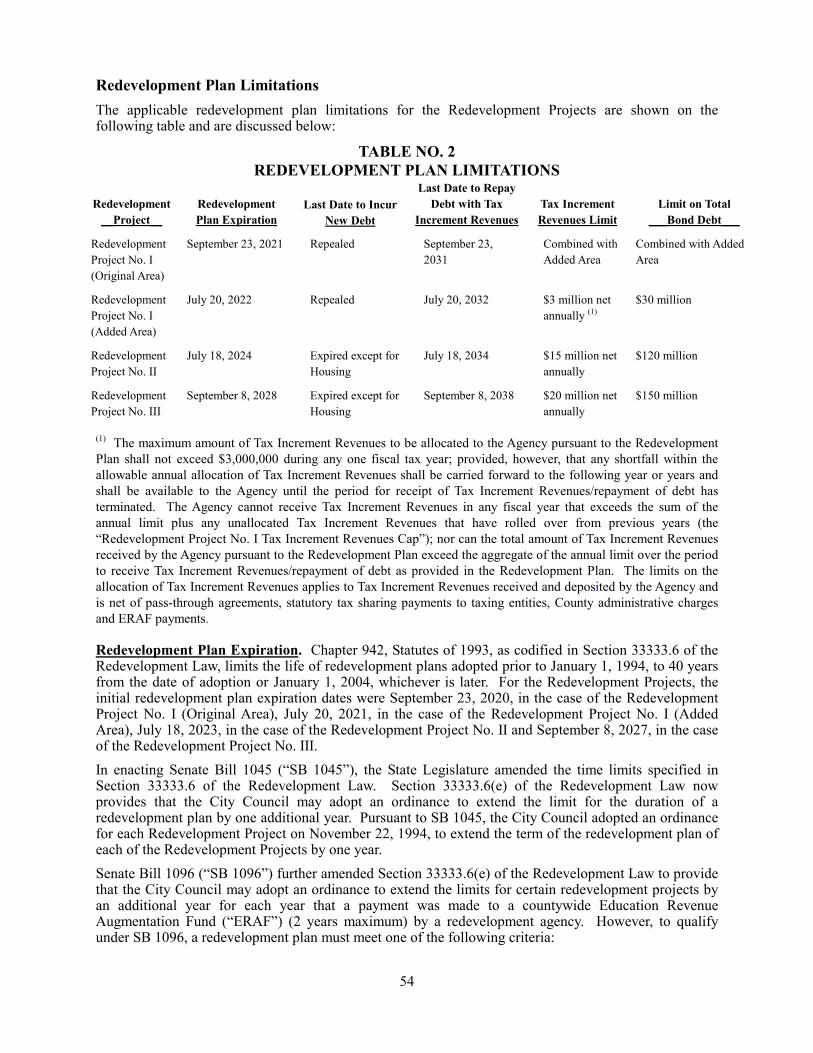

THE AGENCY ............................................................52 GOVERNMENT ORGANIZATION .........................52 AGENCY POWERS ..................................................53 REDEVELOPMENT PLANS....................................53 General .......................................................................53 Amended and Restated Redevelopment Plans............53 Redevelopment Plan Limitations................................54 Redevelopment Plan Expiration .................................54 Receipt of Tax Increment Time Limits .......................55 Time Limit on Incurring Indebtedness........................55 Limitation on the Amount of Tax Increment

Receipts ...................................................................55 Limit on the Amount of Bonded Indebtedness ...........56 AGENCY FINANCIAL ADMINISTRATION...........56 Annual Budget............................................................56 Agency Accounting Records and Financial

Statements................................................................56 Annual Financial Report.............................................57 Filing of Statement of Indebtedness............................57

THE REDEVELOPMENT PROJECTS ...................59 REDEVELOPMENT PROJECT NO. I......................59 General Description....................................................59 Assessed Value by Land Use ......................................59 Top Ten Taxable Property Owners .............................60 Redevelopment Project No. I Aerial Views ................61 REDEVELOPMENT PROJECT NO. II ....................64 General Description....................................................64 Assessed Value by Land Use ......................................64 Top Ten Taxable Property Owners .............................65 Redevelopment Project No. II Map............................66 REDEVELOPMENT PROJECT NO. III ...................70 General Description....................................................70 Assessed Value by Land Use ......................................70 Top Ten Taxable Property Owners .............................71 Redevelopment Project No. III Aerial ........................72

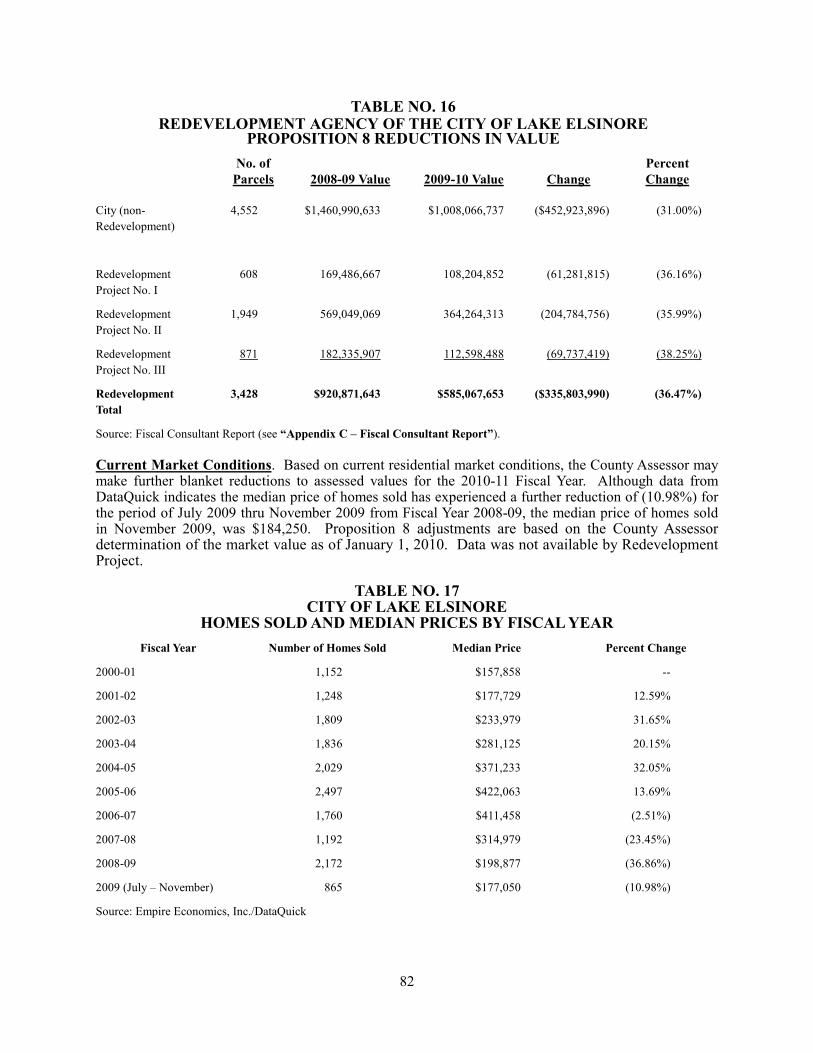

TAX INCREMENT REVENUES...............................76 HISTORICAL TAXABLE VALUATIONS ................76 Value of Residential Parcels .......................................78 ASSESSMENT APPEALS.........................................79 General .......................................................................79 Base Year Appeals ......................................................79 Redevelopment Project No. I......................................79 Redevelopment Project No. II ....................................80 Redevelopment Project No. III ...................................80 Proposition 8 Adjustments..........................................81 General. ......................................................................81 Prior Proposition 8 Adjustments.................................81 Current Market Conditions .........................................82 TRANSFERS OF OWNERSHIP ...............................83 Redevelopment Project No. I......................................83 Redevelopment Project No. II ....................................83 Redevelopment Project No. III ...................................83

vi

DELINQUENCIES.....................................................83 FORECLOSURES......................................................83 Redevelopment Project No. I......................................84 Redevelopment Project No. II ....................................84 Redevelopment Project No. III ...................................85 PASS-THROUGH AGREEMENTS AND

STATUTORY PAYMENTS .....................................85 Pass-Through Agreements ..........................................85 Statutory Tax Sharing..................................................88 County Property Tax Collection Reimbursement........89 HOUSING SET-ASIDE..............................................90 FUTURE DEVELOPMENT IN THE

REDEVELOPMENT PROJECTS...........................90 PROJECTED TAX REVENUES AND DEBT

SERVICE COVERAGE...........................................92 Projected Tax Revenues and Housing Set-Aside

Revenues ..................................................................92 Debt Service Coverage Based Upon Projected

Tax Revenues ...........................................................93 LEGAL MATTERS .....................................................98

ENFORCEABILITY OF REMEDIES........................98 APPROVAL OF LEGAL PROCEEDINGS................98 TAX MATTERS .........................................................98 ABSENCE OF LITIGATION...................................100

CONCLUDING INFORMATION ...........................101 RATINGS ON THE BONDS ...................................101 UNDERWRITING ...................................................101 EXPERTS .................................................................101 FINANCIAL STATEMENTS OF THE AGENCY...101 THE FINANCING CONSULTANT.........................102 FORWARD-LOOKING STATEMENTS..................102 ADDITIONAL INFORMATION .............................102 REFERENCES .........................................................102 EXECUTION ...........................................................103

APPENDIX A............................................................ A-1 SUMMARY OF THE INDENTURE....................... A-1 APPENDIX B.............................................................B-1 SUMMARY OF THE LOAN AGREEMENTS .......B-1

FORM OF LOAN AGREEMENT............................B-1 FORM OF HOUSING FUND LOAN

AGREEMENT.......................................................B-1

APPENDIX C ............................................................C-1 FISCAL CONSULTANT REPORT .........................C-1 APPENDIX D ............................................................D-1 AGENCY AUDITED FINANCIAL

STATEMENTS FOR FISCAL YEAR ENDING JUNE 30, 2009 ........................................................D-1

APPENDIX E.............................................................E-1 FORM OF CONTINUING DISCLOSURE

AGREEMENT........................................................E-1 APPENDIX F............................................................. F-1 SPECIMEN FINANCIAL GUARANTY

INSURANCE POLICY.......................................... F-1 APPENDIX G FORM OF OPINION OF BOND

COUNSEL.............................................................. G-1 APPENDIX H ........................................................... H-1 DTC AND BOOK-ENTRY-ONLY SYSTEM......... H-1

vii

VICINITY MAP

1

OFFICIAL STATEMENT

$15,330,000* LAKE ELSINORE PUBLIC FINANCING AUTHORITY

TAX ALLOCATION REVENUE BONDS (1999 SERIES C REFUNDING), 2010 SERIES A

This Official Statement which includes the cover page and appendices (the “Official Statement”) is provided to furnish certain information concerning the sale by the Lake Elsinore Public Financing Authority (the “Authority”) of its Tax Allocation Revenue Bonds (1999 Series C Refunding), 2010 Series A (the “Bonds”), in the aggregate principal amount of $15,330,000.*

INTRODUCTORY STATEMENT This Introductory Statement contains only a brief description of this issue and does not purport to be complete. The Introductory Statement is subject in all respects to more complete information in the entire Official Statement and the offering of the Bonds to potential investors is made only by means of the entire Official Statement and the documents summarized herein. Potential investors must read the entire Official Statement to obtain information essential to make an informed investment decision (see “BONDOWNERS’ RISKS” herein).

THE AUTHORITY Authorization and Formation The Authority is a joint exercise of powers authority organized and existing under and by virtue of the Joint Exercise of Powers Act, constituting Articles 1 through 4 (commencing with Section 6500) of Chapter 5, Division 7, Title 1 of the Government Code of the State (the “Joint Powers Act”). The City of Lake Elsinore (the “City”), pursuant to Resolution No. 89-32, adopted on July 25, 1989, and the Redevelopment Agency of the City of Lake Elsinore (the “Agency”), pursuant to Resolution No. 89-4, adopted on July 25, 1989, formed the Authority by the execution of a joint exercise of powers agreement (see “THE AUTHORITY” herein).

Bond Authorization and Issuance Pursuant to the Joint Powers Act, the Authority is authorized, among other things, to issue revenue bonds to provide funds to acquire local obligations issued by local agencies or to make loans to local agencies to finance or refinance public capital improvements, such revenue bonds to be repaid from the repayment of the local obligations so acquired by the Authority or repayment of a loan, such as the Loans (the “Loans”) described herein (see “INTRODUCTORY STATEMENT – THE LOANS” and “INTRODUCTORY STATEMENT – SECURITY AND SOURCES OF REPAYMENT” below). The Bonds are being issued pursuant to the Indenture, as defined herein (see “APPENDIX A – SUMMARY OF THE INDENTURE”). The Bonds are being sold to the Underwriter pursuant to, and subject to the terms and conditions of, the Purchase Contract, by and among the Underwriter, the Authority and the Agency (the “Purchase Contract”). The Indenture and the Purchase Contract were approved by the Authority pursuant to a resolution, adopted on November 10, 2009. It is anticipated that the Bonds, in book-entry form, will be available for delivery through the facilities of The Depository Trust Company, on or about February 4, 2010 (see “APPENDIX H – DTC AND BOOK-ENTRY-ONLY SYSTEM”).

It is anticipated that the Authority will issue other series of bonds. Each series will be separately secured under the terms of an indenture for such other series of bonds. The Authority is not authorized to issue any additional bonds under the Indenture secured by repayment of the Loans except for refunding purposes. However, the Authority may in the future loan money to the Agency, which loan may be payable on a parity with the Loans (see “SOURCES OF PAYMENT FOR THE BONDS – ISSUANCE OF ADDITIONAL DEBT” herein). ___________________________ * Preliminary, subject to change.

2

Financing Purpose of the Bonds Pursuant to Resolution No. PFA 99-3, adopted by the Authority on September 14, 1999, the Authority issued its Tax Allocation Revenue Bonds, 1999 Series C (the “Authority 1999C Bonds”) in the principal amount of $14,180,000 of which $13,170,000 remains outstanding. On the date of delivery of the Bonds, a portion of the proceeds of the Bonds, together with certain other funds, will be used to redeem the Authority 1999C Bonds (see “- THE FINANCING PLAN - The Refunding Program” below). The Bonds are also being issued:

1. To provide funds to make the Loans on the date of delivery of the Bonds; 2. To fund the Reserve Fund (see “SOURCES OF PAYMENT FOR THE BONDS - REPAYMENT OF THE BONDS - Reserve Fund” herein); and 3. To pay the expenses of the Authority in connection with the issuance of the Bonds.

(see “ESTIMATED SOURCES AND USES OF FUNDS” and “SOURCES OF PAYMENT FOR THE BONDS – REPAYMENT OF THE BONDS” herein).

THE AGENCY Formation The Agency is a public body, corporate and politic, existing under and by virtue of the Community Redevelopment Law of the State, constituting Part 1 of Division 24 (commencing with Section 33000) of the Health and Safety Code of the State (the “Redevelopment Law”). The Agency was activated in July 1980. The City Council of the City (the “City Council”), at the same time, declared itself to be the members of the Agency and appointed the City Manager to be the Agency’s Executive Director (see “THE AGENCY” herein). The Agency is comprised of 3 Redevelopment Projects: (i) the Rancho Laguna Redevelopment Project No. I (“Redevelopment Project No. I”); (ii) the Rancho Laguna Redevelopment Project No. II (“Redevelopment Project No. II”) and (iii) the Rancho Laguna Redevelopment Project No. III (“Redevelopment Project No. III”). Collectively Redevelopment Project No. I, Redevelopment Project No. II and Redevelopment Project No. III are referred to herein as the “Redevelopment Projects” (see map entitled “Project Area Boundaries” below).

Tax Allocation Financing The Redevelopment Law provides a means for financing redevelopment projects based upon an allocation of taxes collected within a redevelopment project. The taxable valuation of a redevelopment project last equalized prior to adoption of the redevelopment plan, or base roll, is established and, except for any period during which the taxable valuation drops below the base year level, the taxing agencies within the redevelopment project thereafter receive the taxes produced by the levy of the then current tax rate upon the base roll. Taxes collected upon any increase in taxable valuation over the base roll (except such portion generated by rates levied to pay voter-approved bonded indebtedness on or after January 1, 1989, for the acquisition or improvement of real property) are allocated to a redevelopment agency (the “Tax Increment Revenues”) and may be pledged by a redevelopment agency to the repayment of any indebtedness incurred in financing or refinancing a redevelopment project. Redevelopment agencies themselves have no authority to levy property taxes and must look specifically to the allocation of taxes produced as above indicated.

Housing Set-Aside Revenues In accordance with Section 33334.2 of the Redevelopment Law, not less than twenty percent (20%) of all taxes which are allocated to the Agency from the Redevelopment Projects (see “Tax Allocation Financing” above) are required to be deposited in a low and moderate income housing fund (the “Low and Moderate Income Housing Fund”) to be used by the Agency for purposes of improving, increasing and preserving the City’s supply of housing for persons and families of low or moderate income (including the payment of indebtedness issued or incurred for such purposes) (the “Housing Set-Aside Revenues”). The Housing Set-Aside Revenues are calculated at 20% of gross Tax Increment Revenues within each of the Redevelopment

PROJECT AREA NO. 2AREA B

PROJECT AREA NO. 3PARCEL NO. 1

PROJECT AREANO. 2

AREA D

PROJECT AREA NO. 2 AREA A

PROJECT AREA NO. 1

PROJECT AREA NO. 2AREA C

Lake \ Elsinore

PROJECT AREA NO. 3PARCEL NO. 3

PROJECT AREA NO. 3PARCEL NO. 4

PROJECT AREA NO. 3PARCEL NO. 2

AREA NO.1 ORIGINAL

AREA NO.1

AREA NO.2

AREA NO.3

CITY OF LAKE ELSINOREREDEVELOPMENT AGENCY

PROJECT AREA BOUNDARIES

Prepared By:City of Lake Elsinore GISMay, 2006Data Sources:County of Riverside GIS,City of Lake Elsinore GISStateplane NAD83

3

Redevelopment Agency Project Area Boundaries

4

Projects; therefore the amount of Housing Set-Aside Revenues is not affected by payments under any tax sharing agreements or any statutory pass-through requirements.

THE REDEVELOPMENT PROJECTS

Redevelopment Project No. I

Formation. The original Redevelopment Plan (as defined herein) for Redevelopment Project No. I was adopted by Ordinance No. 607 on September 23, 1980, and, thereafter, has been amended four times: by Ordinance No. 624, adopted on July 20, 1981, to add territory; by Ordinance No. 987 on November 22, 1994, to conform limits to Assembly Bill 1290 (AB1290); by Ordinance No. 1249 on February 26, 2008, to repeal the debt establishment limit as provided by Senate Bill 211 (SB211), to extend the effectiveness date and time limit to repay debt and collect tax increment revenues as provided by Senate Bill 1045 (SB1045) and to make certain technical corrections; and by Ordinance No. 1260 on April 28, 2009, to adopt an Amended and Restated Redevelopment Plan (as defined herein). The Amended and Restated Redevelopment Plan (i) reflects changes in the Community Redevelopment Law that impose additional requirements and restrictions not reflected in the original text, (ii) incorporates all prior amendments, (iii) updates the land use provisions, (iv) clarifies and restates the time limits and financial limits, and (v) improves the format and presentation of the text and the project areas maps.

General Description. The 1,910-acre Redevelopment Project No. I is divided between two non-contiguous areas of the City (see “THE REDEVELOPMENT PROJECTS – REDEVELOPMENT PROJECT NO. I” herein for a description of Redevelopment Project No. I). Redevelopment Project No. I generally consists of three areas in terms of land use (see map entitled “Redevelopment Agency Project Area Boundaries” above). The first area is adjacent to, and southerly of, Interstate 15. Major land uses include the Lake Elsinore Outlet Center, the Central Business Park, and 2 retail centers that include Target and Home Depot. The second area includes the central business district and governmental offices. The third area is a commercial district near the municipal baseball stadium. Redevelopment Project No. I also includes several small non-contiguous areas at the western end of Lake Elsinore. 648.37 acres of the 1,910 acres within Redevelopment Project No. I are vacant. In terms of total taxable value, residential uses comprise 35.65% of the assessed value, commercial uses comprise 25.18% of the assessed value, industrial uses comprise 19.84% of the assessed value and vacant land comprises 10.94% of the assessed value within Redevelopment Project No. I.

Redevelopment Project No. II

Formation. The Redevelopment Plan for Redevelopment Project No. II was adopted by Ordinance No. 671 on July 18, 1983, and, thereafter, has been amended three times: by Ordinance No. 987 on November 22, 1994, to conform time limits to AB1290; by Ordinance No. 1249 on February 26, 2008, to repeal the debt establishment limit for affordable housing debt as provided by SB211, to extend the effectiveness date and time limit to repay debt and collect tax increment revenues as provided by SB1045, and to make certain technical corrections; and by Ordinance No. 1261 on April 28, 2009, to adopt an Amended and Restated Redevelopment Plan. The Amended and Restated Redevelopment Plan (i) reflects changes in the Community Redevelopment Law that impose additional requirements and restrictions not reflected in the original text, (ii) incorporates all prior amendments, (iii) updates the land use provisions, (iv) clarifies and restates the time limits and financial limits, and (v) improves the format and presentation of the text and the project areas maps.

General Description. Redevelopment Project No. II has an area of 4,859 acres in three non-contiguous areas. The first area runs parallel on both sides of Interstate 15, extending in each direction from Railroad Canyon Road, a major arterial highway (see map entitled “Redevelopment Agency Project Area Boundaries” above). This area includes the City Shopping Center, anchored by a 126,000 square foot Wal-Mart. This area also includes two major subdivisions, Summerhill and Tuscany Hills. Summerhill includes 428 completed single family homes. Tuscany Hills is a planned community, ultimately consisting of 2,000 homes. 1,020 homes have been constructed and occupied. The second area includes the municipal baseball stadium area and the Summerly Planned Community, which is located in both Redevelopment Project No. II

5

and Redevelopment Project No. III. Approximately 833 single family homes are planned in the first phase of the Summerly Planned Community. The Summerly Planned Community is in the early development stages. The third area is located at the west end of Lake Elsinore and is developed with commercial and single family homes. Of the 4,859 acres within Redevelopment Project No. II, 2,398.13 are vacant. In terms of total taxable value, residential uses comprise 60.25% of the assessed value, commercial uses comprise 19.64% of the assessed value, industrial uses comprise 4.3% of the assessed value and vacant land comprises 11.51% of the assessed value within Redevelopment Project No. II (see “THE REDEVELOPMENT PROJECTS – REDEVELOPMENT PROJECT NO. II” herein for a description of Redevelopment Project No. II).

Redevelopment Project No. III

Formation. The Redevelopment Plan for Redevelopment Project No. III was adopted by Ordinance No. 815 on September 8, 1987, and, thereafter, has been amended three times: by Ordinance No. 987 on November 22, 1994, to conform time limits to AB1290; by Ordinance No. 1249 on February 26, 2008, to repeal the debt establishment limit for affordable housing debt as provided by SB211 and to extend the effectiveness date and time limit to repay debt and collect tax increment revenues as provided by SB1045, and to make certain technical corrections; and by Ordinance No. 1262 on April 28, 2009, to adopt an Amended and Restated Redevelopment Plan. The Amended and Restated Redevelopment Plan (i) reflects changes in the Community Redevelopment Law that impose additional requirements and restrictions not reflected in the original text, (ii) incorporates all prior amendments, (iii) updates the land use provisions, (iv) clarifies and restates the time limits and financial limits, and (v) improves the format and presentation of the text and the project areas maps.

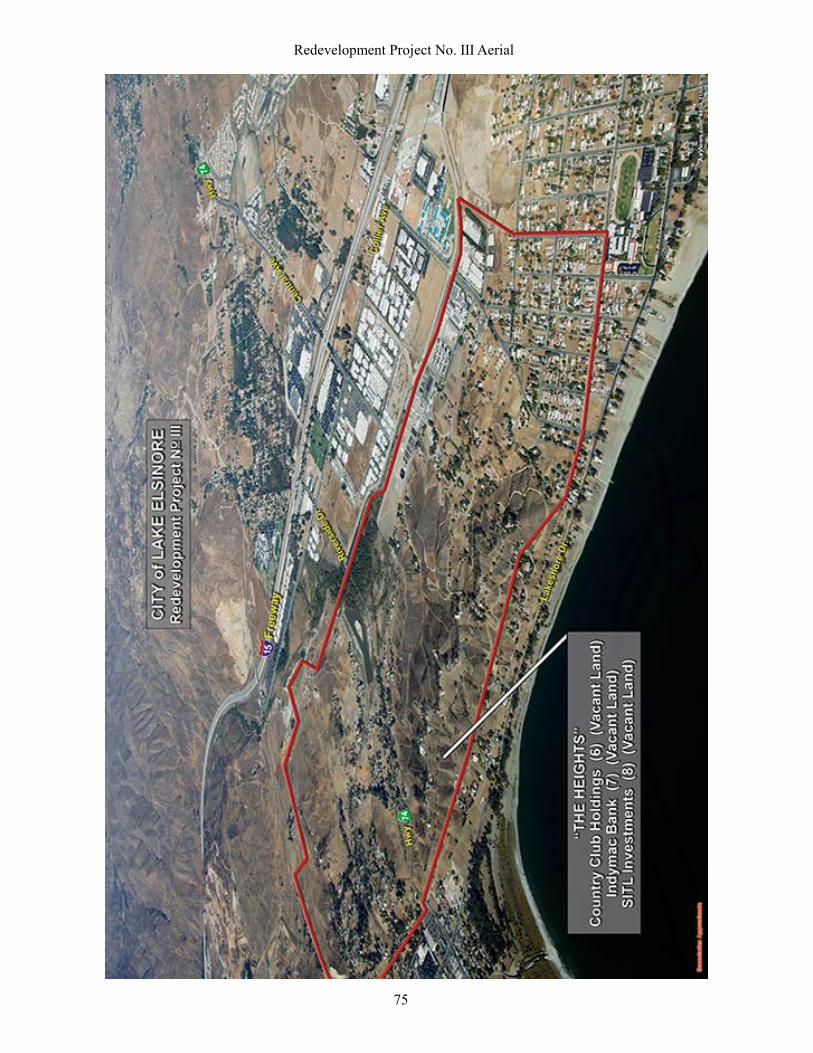

General Description. Redevelopment Project No. III, as shown on the map “Redevelopment Agency Project Area Boundaries” above, consists of four (4) non-contiguous parcels of land.

PARCEL 1 is in the Summerly Specific Plan area adjacent to the southeasterly shore line of Lake Elsinore (the “Lake”) and some of the commercial operations adjacent to and associated with the municipal airport facility. Parcel 1 contains approximately 1,886 acres. PARCEL 2 is adjacent to the municipal airport facility and is used for agricultural purposes and a five (5) acre commercial site. Parcel 2 contains approximately 84.5 acres. PARCEL 3 is generally referred to as “the Avenues.” This area is characterized by older single family residential units, many of which have been converted to multiple family units, on partially developed roadways. Parcel 3 contains approximately 466 acres. PARCEL 4, know as “the Heights,” is also a residential area. The roads are generally unpaved. The area is dominated by steep slopes. Parcel 4 contains approximately 1,104 acres.

1,151.73 acres of the 3,541 acres within Redevelopment Project No. III are vacant. In terms of taxable value, residential uses comprise 67.12% of the assessed value, commercial uses comprise 2.55% of the assessed value, industrial uses comprise 0.32% of the assessed value and vacant land comprises 26.52% of the assessed value within Redevelopment Project No. III (see “THE REDEVELOPMENT PROJECTS – REDEVELOPMENT PROJECT NO. III” herein for a description of Redevelopment Project No. III).

THE LOANS The proceeds of the Bonds will be loaned to the Agency pursuant to the Project No. I Loan (the “Project No. I Loan”), the Project No. II Loan (the “Project No. II Loan”), the Project No. III Loan (the “Project No. III Loan”), and the Housing Loan (the “Housing Loan”). Collectively, the Project No. I Loan, the Project No. II Loan, the Project No. III Loan and the Housing Loan are referred to herein as the “Loans.”

Project No. I Loan Authorization. The Authority will be making the Project No. I Loan to the Agency with respect to the Redevelopment Project No. I in the amount of $3,035,000.* The Agency authorized the Project No. I Loan by resolution, adopted on November 10, 2009. The Agency has pledged a lien on Redevelopment Project

6

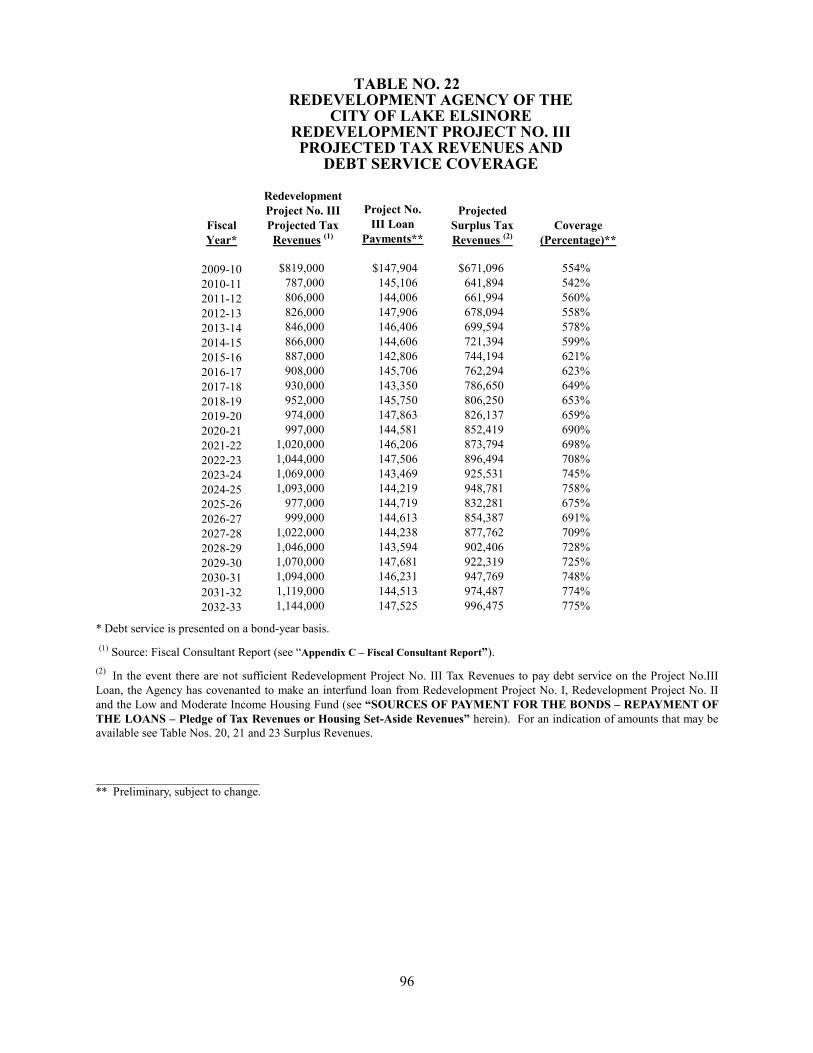

No. I Tax Revenues to the repayment of the Project No. I Loan. “Redevelopment Project No. I Tax Revenues” consist of Tax Increment Revenues from the Agency’s Redevelopment Project No. I, excluding (i) amounts required to be deposited into the Agency’s Low and Moderate Income Housing Fund, (ii) the SB 2557 County Administrative fees and collection charges and (iii) amounts required to be paid pursuant to certain Pass-Through Agreements and Statutory Tax Sharing (as these terms are defined herein) (see “SOURCES OF PAYMENT FOR THE BONDS,” “BONDOWNERS’ RISKS” and “TAX INCREMENT REVENUES” herein). The pledge of Redevelopment Project No. I Tax Revenues is on a subordinate basis with any payments required under the Agency’s Loan Agreement, dated as of January 1, 1999, with respect to Redevelopment Project No. I (the “Project No. I 1999A Loan”) and relating to the Lake Elsinore Public Financing Authority Tax Allocation Revenue Bonds, 1999 Series A (see “Outstanding Bonded Indebtedness of Redevelopment Project No. I” below). Debt service on the Project No. I Loan and the Project No. I 1999A Loan is estimated to be covered by Redevelopment Project No. I Tax Revenues initially by a ratio of approximately 2.24 to 1* and after the annual Redevelopment Project No. I Tax Revenue Cap is reached, as described herein, by a ratio of 1.51 to 1.* In addition, in the event there are not sufficient Redevelopment Project No. I Tax Revenues to pay debt service on the Project No. I Loan, the Agency has covenanted to make an interfund loan from Redevelopment Project No. II, Redevelopment Project No. III and the Low and Moderate Income Housing Fund (see “SOURCES OF PAYMENT FOR THE BONDS – REPAYMENT OF THE LOANS – Pledge of Tax Revenues or Housing Set-Aside Revenues” herein). For an indication of amounts that may be available see Table Nos. 21, 22 and 23 Surplus Revenues herein.

Outstanding Bonded Indebtedness of Redevelopment Project No. I. Pursuant to an Indenture of Trust, dated as of January 1, 1999, the Authority issued its Tax Allocation Revenue Bonds, 1999 Series A Bonds (the “Authority 1999A Bonds”) in the aggregate principal amount of $33,450,000, of which $28,255,000 currently remains outstanding. Proceeds of the Authority 1999A Bonds were loaned, in part, by the Authority to the Agency pursuant to a Project No. I Loan Agreement, dated as of January 1, 1999 (the “Project No. I 1999A Loan Agreement”). The loan pursuant to the Project No. I 1999A Loan Agreement (the “Project No. I 1999A Loan”) was in the principal amount of $18,420,000, of which $15,255,000 currently remains outstanding. The Project No. I 1999A Loan matures on September 1, 2030.

Project No. II Loan Authorization. The Authority will be making the Project No. II Loan to the Agency with respect to the Redevelopment Project No. II, in the amount of $5,465,000.* The Agency authorized the Project No. II Loan by resolution, adopted on November 10, 2009. The Agency has pledged a lien on Redevelopment Project No. II Tax Revenues to the repayment of the Project No. II Loan. “Redevelopment Project No. II Tax Revenues” consist of Tax Increment Revenues from the Agency’s Redevelopment Project No. II, excluding (i) amounts required to be deposited into the Agency’s Low and Moderate Income Housing Fund, (ii) the SB 2557 County Administrative fees and collection charges and (iii) amounts required to be paid pursuant to certain Pass-Through Agreements (as this term is defined herein) (see “SOURCES OF PAYMENT FOR THE BONDS,” “BONDOWNERS’ RISKS” and “TAX INCREMENT REVENUES” herein). The pledge of Redevelopment Project No. II Tax Revenues is on a parity basis with any payments required under the Agency’s Loan Agreement, dated as of January 1, 1999, with respect to Redevelopment Project No. II (the “Project No. II 1999A Loan”) and relating to the Authority 1999A Bonds (see “Outstanding Bonded Indebtedness of Redevelopment Project No. II” below). Debt service on the Project No. II Loan and the Project No. II 1999A Loan is estimated to be covered by Redevelopment Project No. II Tax Revenues by a ratio of approximately 2.62 to 1.* In addition, in the event there are not sufficient Redevelopment Project No. II Tax Revenues to pay debt service on the Project No. II Loan, the Agency has covenanted to make an interfund loan from Redevelopment Project No. I, Redevelopment Project No. III and the Low and Moderate Income Housing Fund (see “SOURCES OF PAYMENT FOR THE BONDS – REPAYMENT OF THE LOANS – Pledge of Tax Revenues or Housing Set-Aside Revenues” herein). For an indication of amounts that may be available see Table Nos. 20, 22 and 23 Surplus Revenues herein. ___________________________ * Preliminary, subject to change.

7

Outstanding Bonded Indebtedness of Redevelopment Project No. II. Proceeds of the Authority 1999A Bonds were also loaned, in part, by the Authority to the Agency pursuant to a Project No. II Loan Agreement, dated as of January 1, 1999 (the “Project No. II 1999A Loan Agreement). The loan pursuant to the Project No. II 1999A Loan Agreement (the “Project No. II 1999A Loan”) was in the principal amount of $15,030,000, of which $13,000,000 currently remains outstanding. The Project No. II 1999A Loan matures on September 1, 2030.

Project No. III Loan Authorization. The Authority will be making the Project No. III Loan to the Agency with respect to the Redevelopment Project No. III in the amount of $2,060,000.* The Agency authorized the Project No. III Loan by resolution, adopted on November 10, 2009. The Agency has pledged a lien on Redevelopment Project No. III Tax Revenues to the repayment of the Project No. III Loan. “Redevelopment Project No. III Tax Revenues” consist of Tax Increment Revenues from the Agency’s Redevelopment Project No. III, excluding (i) amounts required to be deposited into the Agency’s Low and Moderate Income Housing Fund, (ii) the SB 2557 County Administrative fees and collection charges and (iii) amounts required to be paid pursuant to certain Pass-Through Agreements (as this term is defined herein) (see “SOURCES OF PAYMENT FOR THE BONDS,” “BONDOWNERS’ RISKS” and “TAX INCREMENT REVENUES” herein). Debt service on the Project No. III Loan is estimated to be covered by Redevelopment Project No. III Tax Revenues by a ratio of approximately 5.42 to 1. In addition, in the event there are not sufficient Redevelopment Project No. III Tax Revenues to pay debt service on the Project No. III Loan, the Agency has covenanted to make an interfund loan from Redevelopment Project No. I, Redevelopment Project No. II and the Low and Moderate Income Housing Fund (see “SOURCES OF PAYMENT FOR THE BONDS – REPAYMENT OF THE LOANS – Pledge of Tax Revenues or Housing Set-Aside Revenues” herein). For an indication of amounts that may be available see Table Nos. 20, 21 and 23 Surplus Revenues herein. Outstanding Bonded Indebtedness of Redevelopment Project No. III. Redevelopment Project No. III will not have any other Bonded indebtedness after the closing date for the Bonds.

The Housing Loan Authorization. The Authority will be making a loan to the Agency with respect to the Low and Moderate Income Housing Fund (see “Housing Set-Aside Revenues” above), in the amount of $4,770,000.* The Agency authorized the Housing Loan by resolution, adopted on November 10, 2009. The Agency has pledged Housing Set-Aside Revenues to the repayment of the Housing Loan. The pledge of Housing Set-Aside Revenues is on a parity basis with any payments required under the Agency’s housing loan incurred in 1995 (the “1995 Housing Loan”) relating to the Lake Elsinore Public Financing Authority Tax Allocation Revenue Bonds, 1995 Series A. The term “Housing Set-Aside Revenues” means all amounts required to be deposited by the Agency in the Low and Moderate Income Housing Fund of the Agency in any Fiscal Year (as defined in the Indenture) pursuant to Section 33334.3 of the Redevelopment Law (see “INTRODUCTORY STATEMENT – THE AGENCY - Housing Set-Aside Revenues” above), which amounts are derived from the taxes annually allocated to the Agency with respect to the Redevelopment Projects pursuant to Article 6 of Chapter 6 (commencing with Section 33670) of the Redevelopment Law and Section 16 of Article XVI of the Constitution of the State and as provided in the redevelopment plans (see “INTRODUCTORY STATEMENT – THE AGENCY - Tax Allocation Financing” above and “SOURCES OF PAYMENT FOR THE BONDS,” “BONDOWNERS’ RISKS” and “TAX INCREMENT REVENUES” herein). Debt service on the Housing Loan and the 1995 Housing Loan is estimated to be covered by Housing Set-Aside Revenues by a ratio of approximately 2.98 to 1.* In addition, in the event there are not sufficient Housing Set-Aside Revenues to pay debt service on the Housing Loan, the Agency has covenanted to make an interfund loan from Redevelopment Project No. I, Redevelopment Project No. II and Redevelopment Project No. III (see “SOURCES OF PAYMENT FOR THE BONDS – REPAYMENT OF THE LOANS – Pledge of Tax Revenues or Housing Set-Aside Revenues” herein). For an indication of amounts that may be available see Table Nos. 20, 21 and 22 Surplus Revenues herein. ___________________________ * Preliminary, subject to change.

8

Outstanding Indebtedness of the Low and Moderate Income Housing Fund. Pursuant to an Indenture of Trust, dated as of December 1, 1995, the Authority issued its 1995 Housing Bonds in the aggregate principal amount of $13,345,000, of which $10,065,000 currently remains outstanding. Proceeds of the 1995 Housing Bonds were loaned by the Authority to the Agency pursuant to a Loan Agreement, dated as December 1, 1995 (the “1995 Housing Loan”). The 1995 Housing Loan matures on September 1, 2025.

SECURITY AND SOURCES OF REPAYMENT The Indenture The Bonds are secured under an Indenture of Trust, dated as of February 1, 2010 (the “Indenture”), by and between the Authority and Union Bank, N.A., Los Angeles, California, as trustee (the “Trustee”) (see “APPENDIX A - SUMMARY OF THE INDENTURE”). The proceeds of the Bonds will be loaned by the Authority to the Agency pursuant to the Loans. The Bonds are payable from loan payments to be made to the Authority under the Loans, from amounts in the Reserve Fund created under the Indenture and from certain funds and accounts created under the Indenture, and from investment earnings thereon (see “SOURCES OF PAYMENT FOR THE BONDS” and “BONDOWNERS’ RISKS” herein). The Bonds are limited obligations of the Authority. The Bonds do not constitute a debt or liability of the City, the State of California (the “State”) or of any political subdivision thereof, other than the Authority. The Authority shall be obligated to pay the principal of the Bonds, and the interest thereon, only from the funds described herein, and neither the faith and credit nor the taxing power of the City, the State or any of its political subdivisions is pledged to the payment of the principal of or the interest on the Bonds. The Authority has no taxing power.

The Loan Agreements The Loans are to be made and secured pursuant to the Loan Agreements (the “Loan Agreements”) authorized by Resolution No. 2009-15 of the Agency, adopted on November 10, 2009. A description of the Loan Agreements is set forth in “APPENDIX B - SUMMARY OF THE LOAN AGREEMENTS.” The Loans are made in accordance with the laws of the State, and particularly the Community Redevelopment Law of the State, constituting Part 1 of Division 24 (commencing with Section 33000) of the Health and Safety Code of the State.

The Loans are limited obligations of the Agency. The Loans do not constitute a debt or liability of the State or of any political subdivision thereof, other than the Agency. The Agency shall be obligated to pay the principal of the Loans, and the interest thereon, only from the funds described herein, and neither the faith and credit nor the taxing power of the City, the State or any of its political subdivisions is pledged to the payment of the principal of or the interest on the Loans. The Agency has no ad valorem taxing power.

THE FINANCING PLAN Bond Insurance The scheduled payment of principal of and interest on the Bonds when due will be guaranteed under a financial guaranty insurance policy (the “Insurance Policy”) to be issued concurrently with the delivery of the Bonds by Assured Guaranty Corp. (“AGC” or the “Bond Insurer”) (see “SOURCES OF PAYMENT FOR THE BONDS - BOND INSURANCE,” “BONDOWNERS’ RISKS – THE BONDS - Bond Insurer Default” and “CONCLUDING INFORMATION - RATINGS ON THE BONDS” herein and “APPENDIX F –SPECIMEN FINANCIAL GUARANTY INSURANCE POLICY”).

The Refunding Program Pursuant to an Indenture of Trust, dated as of November 1, 1999, between the Authority and Union Bank, N.A., Los Angeles, California, as trustee (the “Prior Indenture”), the Authority issued its 1999C Bonds in the aggregate principal amount of $14,180,000 of which $13,170,000 currently remains outstanding. The Authority 1999C Bonds were used to acquire loans made by Redevelopment Project No. I (the “Project No. I

9

1999C Loan”), Redevelopment Project No. II (the “Project No. II 1999C Loan”), Redevelopment Project No. III (the “Project No. III 1999C Loan”) and the Low and Moderate Income Housing Fund (the “1999 Housing Loan”). Collectively, the Project No. I 1999C Loan, the Project No. II 1999C Loan, the Project No. III 1999C Loan and the 1999 Housing Loan are referred to herein as the “1999C Loans.” On the Date of Delivery, a portion of the proceeds of the Bonds, together with certain other funds, will be deposited in trust with Union Bank, N.A., Los Angeles, California, as escrow holder (the “Escrow Bank”) pursuant to an Escrow Deposit and Trust Agreement, dated as of February 1, 2010, between the Authority and the Escrow Bank (the “Escrow Agreement”). The deposit will be in an amount sufficient to pay interest on the Authority 1999C Bonds through and including March 22, 2010, and to pay the redemption price with respect to the remaining Authority 1999C Bonds on March 22, 2010. The lien of the Authority 1999C Bonds created by the Prior Indenture, including, without limitation, the pledge of Revenues pursuant to the Prior Indenture, will be discharged, terminated and of no further force and effect. Upon such redemption, the 1999C Loans will be canceled.

REDEMPTION OF THE BONDS Mandatory Redemption from Optional Loan Prepayments The Bonds are subject to mandatory redemption from optional prepayments under the respective Loan prior to maturity, in whole or in part, on a pro rata basis and by lot within a maturity, on September 1, 2019, and on any date thereafter, at a redemption price equal to the principal amount thereof, plus accrued interest to the date of redemption, as described herein (see “THE BONDS - REDEMPTION – Mandatory Redemption From Optional Loan Prepayments” herein).

Mandatory Sinking Payment Redemption The Bonds maturing September 1, 2033, are subject to mandatory sinking payment redemption, without premium, prior to their maturity date, in part by lot on September 1 in each year commencing September 1, 2026, from mandatory sinking payments under the Indenture (see “THE BONDS - REDEMPTION – Mandatory Sinking Payment Redemption” herein).

Mandatory Redemption upon Acceleration of the Loans The Bonds are also subject to mandatory redemption, without premium, prior to maturity, in whole or in part, on any date, from amounts credited toward the payment of principal of the respective Loan coming due and payable solely by reason of acceleration of the respective Loan (see “THE BONDS - REDEMPTION - Mandatory Redemption upon Acceleration of the Loans ” herein).

THE BONDS GENERAL PROVISIONS Denominations The Bonds will be issued in the minimum denomination of $5,000 each or any integral multiple thereof (see “THE BONDS - GENERAL PROVISIONS” herein).

Registration, Transfer and Exchange The Bonds will be issued in fully-registered form without coupons. Any Bond may, in accordance with its terms, be transferred or exchanged, pursuant to the provisions of the Indenture (see “THE BONDS - GENERAL PROVISIONS - Transfer or Exchange of Bonds” herein). When delivered, the Bonds will be registered in the name of The Depository Trust Company, New York, New York (“DTC”), or its nominee. DTC will act as securities depository for the Bonds. Individual purchases of Bonds will be made in book-entry form only in the principal amount of $5,000 or any integral multiple thereof. Purchasers of beneficial interests in the Bonds will not receive certificates representing their ownership interests in Bonds purchased (see “APPENDIX H – DTC AND BOOK-ENTRY–ONLY SYSTEM”).

Payment Principal of the Bonds and any premium upon redemption will be payable in each of the years and in the amounts set forth on the inside cover page hereof upon surrender at the corporate trust office of the Trustee

10

in Los Angeles, California. Interest on the Bonds will be paid by check of the Trustee mailed by first-class mail on the Interest Payment Date (as defined in the Indenture) to the person entitled thereto (except as otherwise described herein for interest paid to an account in the continental United States of America by wire transfer as requested in writing no later than the applicable Record Date (as defined in the Indenture) by owners of $1,000,000 or more in aggregate principal amount of Bonds) (see “THE BONDS - GENERAL PROVISIONS” herein). Initially, interest on and principal and premium, if any, of the Bonds will be payable when due by wire of the Trustee to DTC which will in turn remit such interest, principal and premium, if any, to DTC’s Direct Participants (as defined herein), which will in turn remit such interest, principal and premium, if any, to Beneficial Owners (as defined herein) of the Bonds (see “APPENDIX H – DTC AND BOOK-ENTRY-ONLY SYSTEM”).

Notice Notice of any redemption will be mailed by first-class mail by the Trustee at least thirty (30) but no more than sixty (60) days prior to the date fixed for redemption to the registered owners of any Bonds designated for redemption and to the Securities Depositories and one or more Information Services provided in the Indenture. Neither failure to receive such notice nor any defect in the notice so mailed will affect the sufficiency of the proceedings for redemption of such Bonds or the cessation of accrual of interest on the redemption date (see “THE BONDS - REDEMPTION - Notice of Redemption; Recission” herein). The Authority shall have the right to rescind any optional redemption by written notice to the Trustee on or prior to the date fixed for redemption. Any notice of optional redemption shall be cancelled and annulled if for any reason funds will not be or are not available on the date fixed for redemption for the payment in full of the Bonds then called for redemption, and such cancellation shall not constitute an Event of Default under the Indenture.

LEGAL MATTERS The legal proceedings in connection with the issuance of the Bonds are subject to the approving opinion of Fulbright & Jaworski L.L.P., Los Angeles, California, as Bond Counsel. Such opinion, and certain tax consequences incident to the ownership of the Bonds, including certain exceptions to the tax treatment of interest, are described more fully under the heading “LEGAL MATTERS” herein. Certain legal matters will be passed on for the City and the Agency by Leibold, McClendon & Mann, P.C., Laguna Hills, California, as City Attorney and Agency Counsel and by Fulbright & Jaworski L.L.P., Los Angeles, California, as Disclosure Counsel. Certain legal matters will be passed on for the Underwriter by McFarlin & Anderson LLP, Lake Forest, California.

PROFESSIONAL SERVICES Union Bank, N.A., Los Angeles, California, will serve as Trustee under the Indenture. The Trustee will act on behalf of owners of the Bonds (the “Bondowners”) for the purpose of receiving all moneys required to be paid to the Trustee, to allocate, use and apply the same, to hold, receive and disburse the Revenues and other funds held under the Indenture, and otherwise to hold all the offices and perform all the functions and duties provided in the Indenture to be held and performed by the Trustee. Rod Gunn Associates, Inc., Huntington Beach, California, Financing Consultant (the “Financing Consultant”), advised the Authority as to the financial structure and certain other financial matters relating to the Bonds and assisted the Authority and the Agency with the preparation of this Official Statement. HdL Coren & Cone, Diamond Bar, California (the “Fiscal Consultant”), prepared the Fiscal Consultant Report containing certain background information on the Agency and the Redevelopment Projects, including the projection of Tax Increment Revenues and Housing Set-Aside Revenues used in sizing and structuring the Bonds. See “APPENDIX C - FISCAL CONSULTANT REPORT” for more complete information regarding Tax Revenues and Housing Set-Aside Revenues. Fees payable to Bond Counsel, Disclosure Counsel, Underwriter’s Counsel and the Financing Consultant are contingent upon the sale and delivery of the Bonds.

11

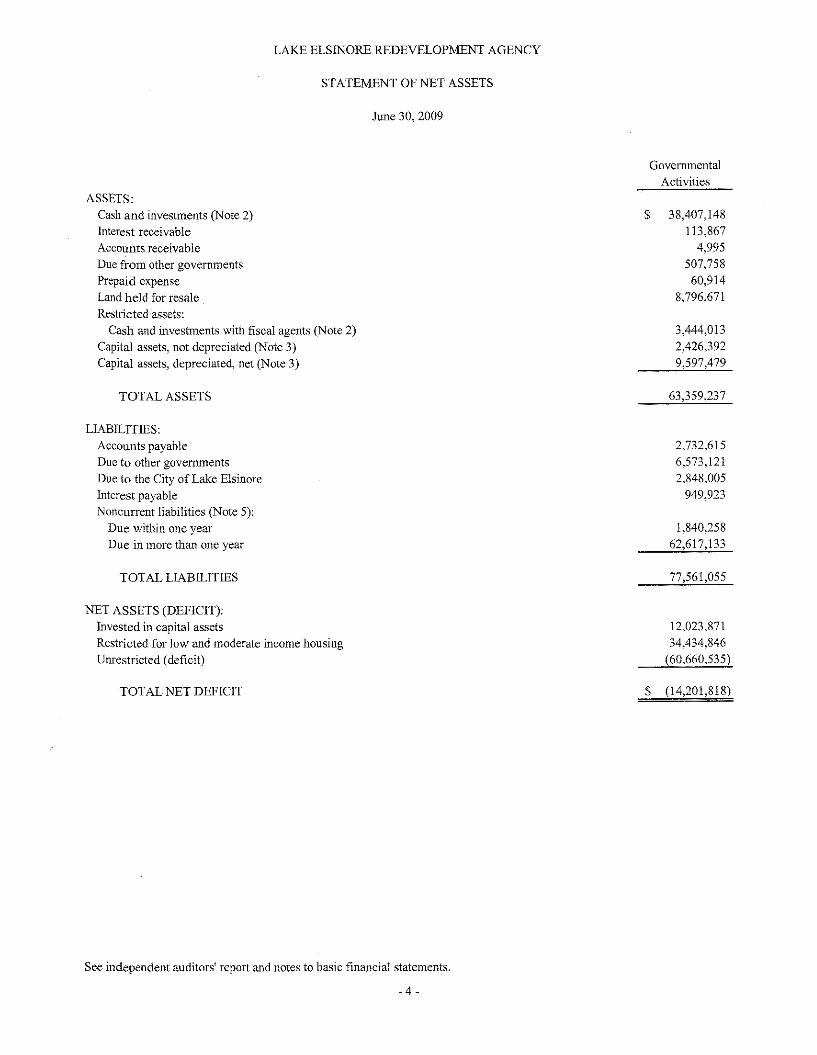

FINANCIAL STATEMENTS The Agency’s financial statements for the fiscal year ended June 30, 2009, are attached hereto as “APPENDIX D” and have been audited by Diehl, Evans & Company, LLP, Certified Public Accountants & Consultants, Irvine, California. The Agency’s audited financial statements are public documents and are included within this Official Statement without the prior approval of the auditor. The auditor has not performed any post-audit of the financial condition of the Agency. The Agency represents that there have been no material adverse changes in its financial position since June 30, 2009.

CONTINUING DISCLOSURE The Agency has undertaken all responsibilities for any required continuing disclosure to Bondowners as described below. The Authority shall have no liability to the Bondowners or any other person with respect to such disclosures provided by the Agency. The Agency will covenant to provide annually certain financial information and operating data relating to the Redevelopment Projects by not later than February 15 of each year, commencing February 15, 2011, and to provide the audited financial statements of the Agency for the fiscal year ending June 30, 2010, and for each subsequent fiscal year when they are available (together, the “Annual Report”), and to provide notices of the occurrence of certain other enumerated events. The Annual Report and the notice of material events will be filed by the Trustee, acting as dissemination agent, on behalf of the Agency with the Municipal Securities Rulemaking Board (“MSRB”) in an electronic format as prescribed by the MSRB. The specific nature of the information to be contained in the Annual Report or the notices of material events and certain other terms of the continuing disclosure obligation are summarized in “APPENDIX E - FORM OF CONTINUING DISCLOSURE AGREEMENT.”

The Agency has not previously failed to comply with any undertaking to provide any required continuing disclosure.

AVAILABILITY OF LEGAL DOCUMENTS The summaries and references contained herein with respect to the Indenture, the Loan Agreements, the Bonds, the Loans and other statutes or documents do not purport to be comprehensive or definitive and are qualified by reference to each such document or statute, and references to the Bonds are qualified in their entirety by reference to the form thereof included in the Indenture. Copies of the documents described herein are available for inspection during the period of initial offering of the Bonds at the offices of the Underwriter, O’Connor & Company Securities, Inc., 620 Newport Center Drive, Suite 1100, Newport Beach, California, 92660 (949) 706-0444. Copies of these documents may be obtained after delivery of the Bonds from the City at 130 S. Main Street, Lake Elsinore, California 92530, telephone (951) 674-3124.

12

SELECTED ESSENTIAL FACTS The following summary does not purport to be complete. Reference is hereby made to the complete Official Statement in this regard.

THE BONDS Principal Amount of Bonds: $15,330,000* Additional Bonds: No Additional Bonds are authorized to be

secured by the Loans except bonds issued to refund the Bonds. However, the Agency is authorized to issue additional indebtedness secured by the Tax Revenues or Housing Set-Aside Revenues on a parity with the Loans, and the Authority may issue bonds to acquire the additional indebtedness of the Agency. When and if issued, the Bonds and such additional bonds of the Authority would be secured by separate indebtedness of the Agency which in turn, will be secured by the same Tax Revenues or Housing Set-Aside Revenues on a parity with each other (see “SOURCES OF PAYMENT FOR THE BONDS – ISSUANCE OF ADDITIONAL DEBT” herein).

First Optional Redemption Date: September 1, 2019, at 100% of principal amount (see “THE BONDS - REDEMPTION – Mandatory Redemption From Optional Loan Prepayments” herein).

Primary Source of Revenues for Repayment: The Bonds are repayable from Revenues, as defined herein, which primarily consist of repayment of the Loans (see “SOURCES OF PAYMENT FOR THE BONDS” and “BONDOWNERS’ RISKS” herein).

Priority: All the Bonds are equally secured by a first pledge of and lien on the Revenues as described herein (see “SOURCES OF PAYMENT FOR THE BONDS – REPAYMENT OF THE BONDS” and “BONDOWNERS’ RISKS”).

Debt Service Coverage from Repayment of the Loans (see “THE AUTHORITY – DEBT SERVICE PAYMENTS ON THE LOANS AND DEBT SERVICE COVERAGE ON THE AUTHORITY BONDS” herein):

100%

THE LOANS Project No. I Loan

Principal Amount of the Project No. I Loan: $3,035,000*

Outstanding Principal Amount of the Project No. I 1999A Loan:

$15,255,000

___________________________ * Preliminary, subject to change.

13

Additional Loans: Additional indebtedness on a parity with the Project No. I Loan is permitted subject to certain conditions (see “SOURCES OF PAYMENT FOR THE BONDS – ISSUANCE OF ADDITIONAL DEBT” herein). No additional indebtedness senior to the Project No. I Loan is allowed (other than to refund the Project No. I 1999A Loan). Subordinate debt is permitted.

Primary Source of Revenues for Repayment of the Project No. I Loan:

Redevelopment Project No. I Tax Revenues on a subordinate basis to the Project No. I 1999A Loan (see “TAX INCREMENT REVENUES” herein).

Priority: The Agency has pledged a lien on Redevelopment Project No. I Tax Revenues, on a subordinate basis to the Project No. I 1999A Loan (see “SOURCES OF PAYMENT FOR THE BONDS” and “BONDOWNERS’ RISKS” herein).

Minimum Ratio of Estimated Redevelopment Project No. I Tax Revenues in any Fiscal Year to Maximum Annual Debt Service on the Project No. I Loan and the Project No. I 1999A Loan:

Initially 224%,* after the Redevelopment Project No. I Tax Increment Revenues Cap is reached, as described herein, 151%* (see “TAX INCREMENT REVENUES - PROJECTED TAX REVENUES AND DEBT SERVICE COVERAGE” herein).

Interfund Loans: In the event there are not sufficient Redevelopment Project No. I Tax Revenues to pay debt service on the Project No. I Loan, the Agency has covenanted to make an interfund loan from Redevelopment Project No. II, Redevelopment Project No. III and the Low and Moderate Income Housing Fund (see “SOURCES OF PAYMENT FOR THE BONDS – REPAYMENT OF THE LOANS – Pledge of Tax Revenues or Housing Set-Aside Revenues” herein). For an indication of amounts that may be available see Table Nos. 21, 22 and 23 Surplus Revenues herein.

Project No. II Loan

Principal Amount of the Project No. II Loan: $5,465,000*

Outstanding Principal Amount of the Project No. II 1999A Loan:

$13,000,000

Additional Loans: Additional indebtedness on a parity with the Project No. II Loan and the Project No. II 1999A Loan is permitted subject to certain conditions (see “SOURCES OF PAYMENT FOR THE BONDS – ISSUANCE OF ADDITIONAL DEBT” herein). Subordinate debt is permitted.

___________________________ * Preliminary, subject to change.

14

Primary Source of Revenues for Repayment of the Project No. II Loan :

Redevelopment Project No. II Tax Revenues on a parity basis with the Project No. II 1999A Loan. (see “TAX INCREMENT REVENUES” herein).

Priority: The Agency has pledged a lien on Redevelopment Project No. II Tax Revenues, on a parity basis with the Project No. II 1999A Loan (see “SOURCES OF PAYMENT FOR THE BONDS” and “BONDOWNERS’ RISKS” herein).

Minimum Ratio of Estimated Redevelopment Project No. II Tax Revenues in any Fiscal Year to Maximum Annual Debt Service on the Project No. II Loan and the Project No. II 1999A Loan:

262%* (see “TAX INCREMENT REVENUES - PROJECTED TAX REVENUES AND DEBT SERVICE COVERAGE” herein).

Interfund Loans: In the event there are not sufficient Redevelopment Project No. II Tax Revenues to pay debt service on the Project No. II Loan, the Agency has covenanted to make an interfund loan from Redevelopment Project No. I, Redevelopment Project No. III and the Low and Moderate Income Housing Fund (see “SOURCES OF PAYMENT FOR THE BONDS – REPAYMENT OF THE LOANS – Pledge of Tax Revenues or Housing Set-Aside Revenues” herein). For an indication of amounts that may be available see Table Nos. 20, 22 and 23 Surplus Revenues herein.

Project No. III Loan

Principal Amount of the Project No. III Loan: $2,060,000*

Additional Loans: Additional indebtedness on a parity with the Project No. III Loan is not permitted (see “SOURCES OF PAYMENT FOR THE BONDS – ISSUANCE OF ADDITIONAL DEBT” herein). Subordinate debt is permitted.

Primary Source of Revenues for Repayment of the Project No. III Loan:

Redevelopment Project No. III Tax Revenues on a senior lien basis (see “TAX INCREMENT REVENUES” herein).

Priority: The Agency has pledged a lien on Redevelopment Project No. III Tax Revenues, on a senior lien basis (see “SOURCES OF PAYMENT FOR THE BONDS” and “BONDOWNERS’ RISKS” herein).

Minimum Ratio of Estimated Redevelopment Project No. III Tax Revenues in any Fiscal Year to Maximum Annual Debt Service on the Project No. III Loan:

542%* (see “TAX INCREMENT REVENUES - PROJECTED TAX REVENUES AND DEBT SERVICE COVERAGE” herein).

___________________________ * Preliminary, subject to change.

15