Embed Size (px)

Citation preview

SIG Investment MeetingSIG Investment Meeting April 20,2010 April 20,2010

Financial Advisors Financial Advisors

Who are they?Who are they?

They go by various titles if they are not certified:

Financial advisor (adviser) Financial Analyst Financial Consultant Financial Planner Investment Consultants Wealth Managers

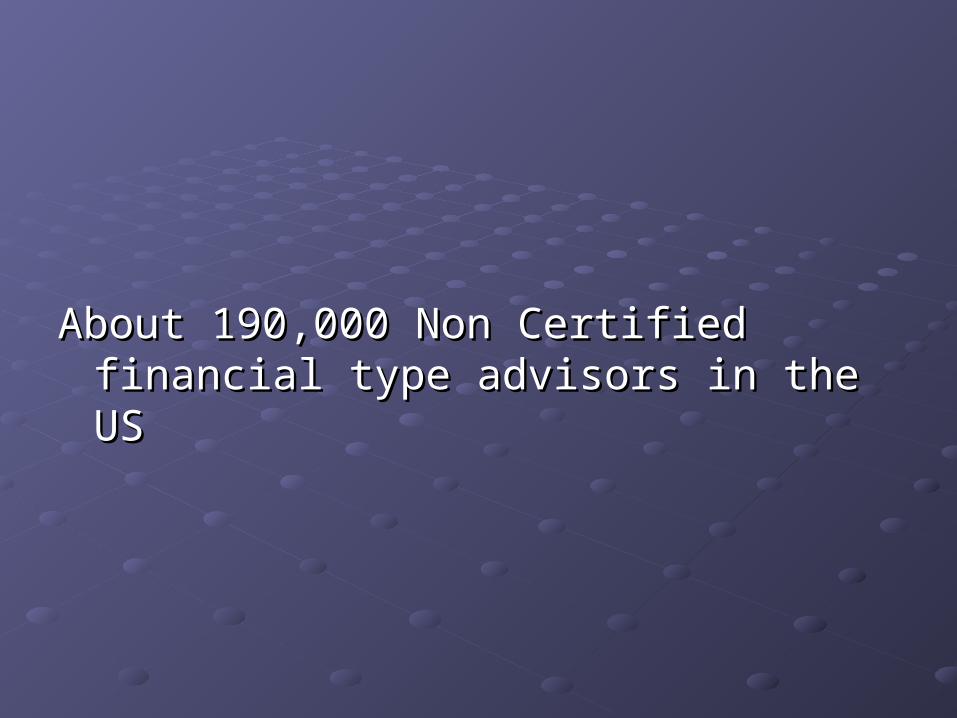

How many of these do you think are in the US?

About 190,000 Non Certified financial type About 190,000 Non Certified financial type advisors in the USadvisors in the US

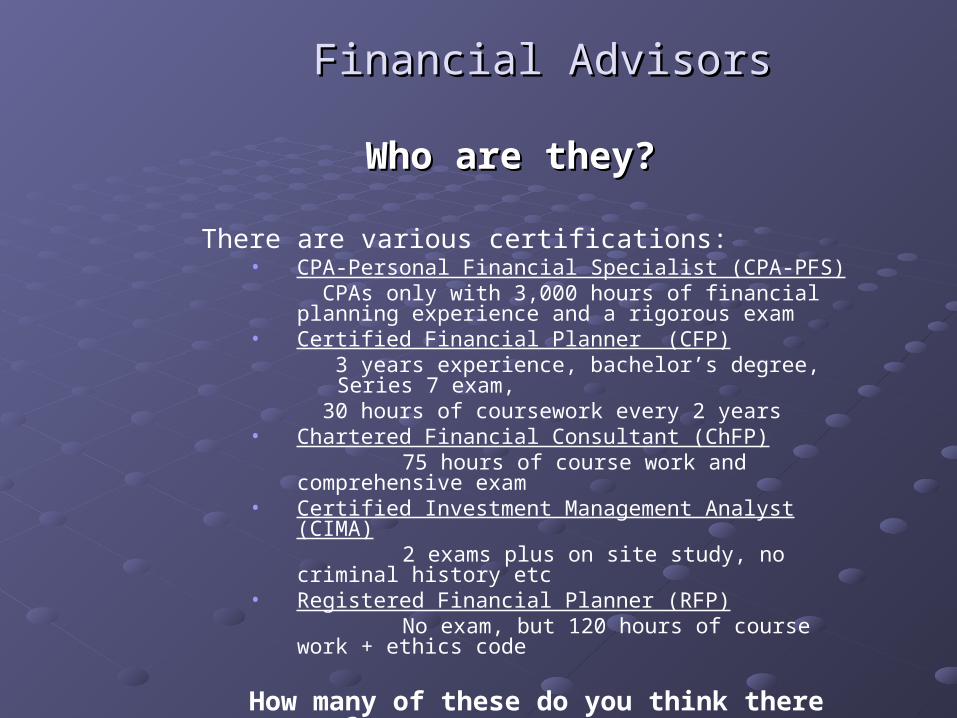

Financial AdvisorsFinancial Advisors

Who are they?Who are they?

There are various certifications:• CPA-Personal Financial Specialist (CPA-PFS)

CPAs only with 3,000 hours of financial planning experience and a rigorous exam

• Certified Financial Planner (CFP) 3 years experience, bachelor’s degree, Series 7 exam, 30 hours of coursework every 2 years

• Chartered Financial Consultant (ChFP) 75 hours of course work and comprehensive exam• Certified Investment Management Analyst (CIMA) 2 exams plus on site study, no criminal history etc• Registered Financial Planner (RFP) No exam, but 120 hours of course work + ethics code

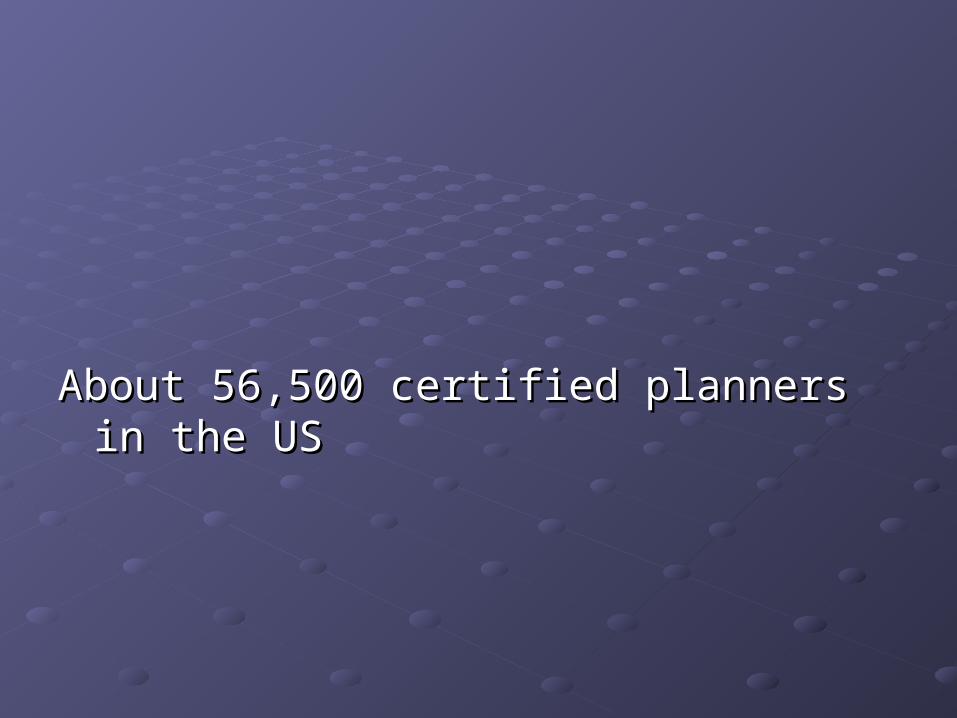

How many of these do you think there are?

About 56,500 certified planners in the USAbout 56,500 certified planners in the US

Financial AdvisorsFinancial Advisors

Who are they?Who are they?

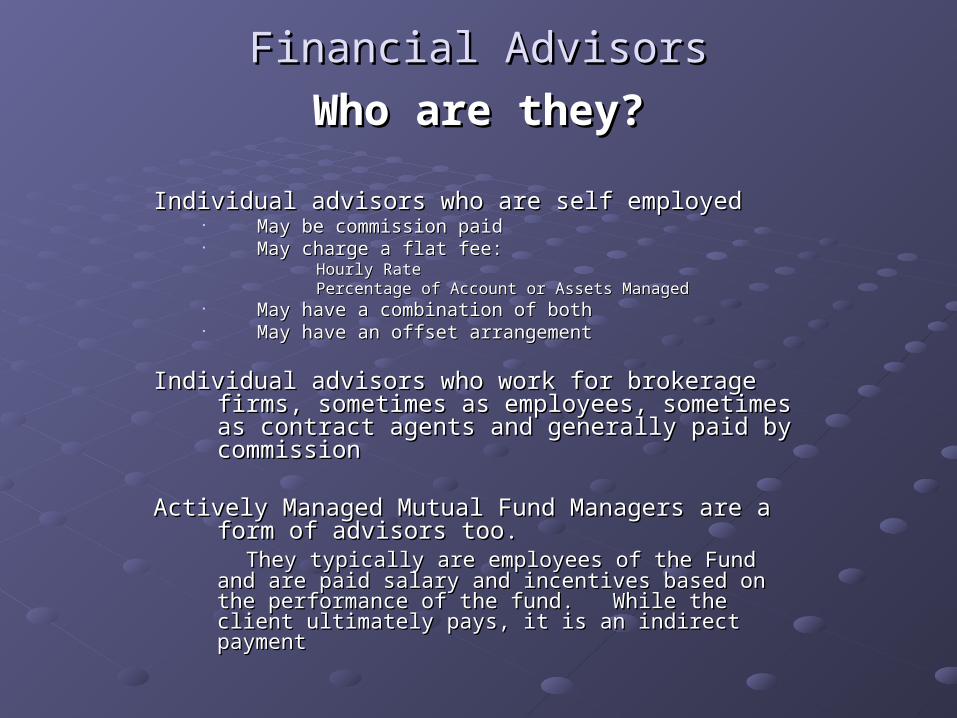

Individual advisors who are self employedIndividual advisors who are self employed• May be commission paidMay be commission paid• May charge a flat fee:May charge a flat fee:

Hourly RateHourly Rate Percentage of Account or Assets ManagedPercentage of Account or Assets Managed

• May have a combination of bothMay have a combination of both• May have an offset arrangementMay have an offset arrangement

Individual advisors who work for brokerage firms, sometimes Individual advisors who work for brokerage firms, sometimes as employees, sometimes as contract agents and as employees, sometimes as contract agents and generally paid by commissiongenerally paid by commission

Actively Managed Mutual Fund Managers are a form of Actively Managed Mutual Fund Managers are a form of advisors too.advisors too. They typically are employees of the Fund and are paid They typically are employees of the Fund and are paid salary and incentives based on the performance of the fund. salary and incentives based on the performance of the fund. While the client ultimately pays, it is an indirect paymentWhile the client ultimately pays, it is an indirect payment

Financial AdvisorsFinancial Advisors

Who are they?Who are they?

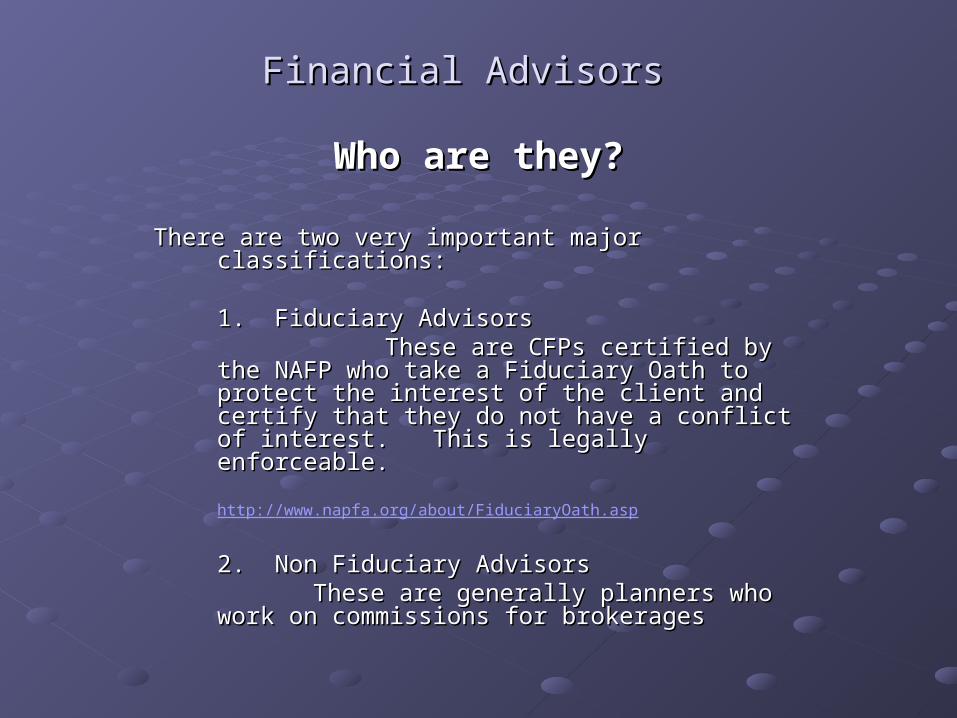

There are two very important major classifications:There are two very important major classifications:

1. Fiduciary Advisors1. Fiduciary Advisors These are CFPs certified by the NAFP who These are CFPs certified by the NAFP who

take a Fiduciary Oath to protect the interest of the take a Fiduciary Oath to protect the interest of the client and certify that they do not have a conflict of client and certify that they do not have a conflict of interest. This is legally enforceable.interest. This is legally enforceable.

http://www.napfa.org/about/FiduciaryOath.asp

2. Non Fiduciary Advisors2. Non Fiduciary AdvisorsThese are generally planners who work on These are generally planners who work on

commissions for brokeragescommissions for brokerages

Financial AdvisorsFinancial Advisors

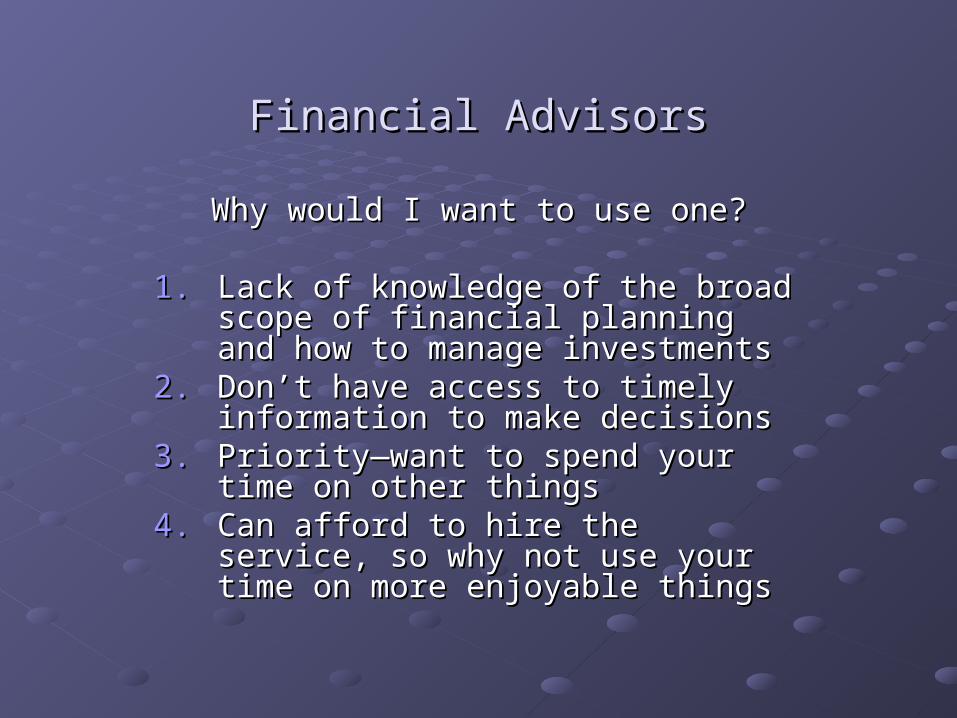

Why would I want to use one?Why would I want to use one?

1.1. Lack of knowledge of the broad scope of Lack of knowledge of the broad scope of financial planning and how to manage financial planning and how to manage investmentsinvestments

2.2. Don’t have access to timely information Don’t have access to timely information to make decisionsto make decisions

3.3. Priority—want to spend your time on Priority—want to spend your time on other thingsother things

4.4. Can afford to hire the service, so why not Can afford to hire the service, so why not use your time on more enjoyable thingsuse your time on more enjoyable things

Financial AdvisorsFinancial Advisors

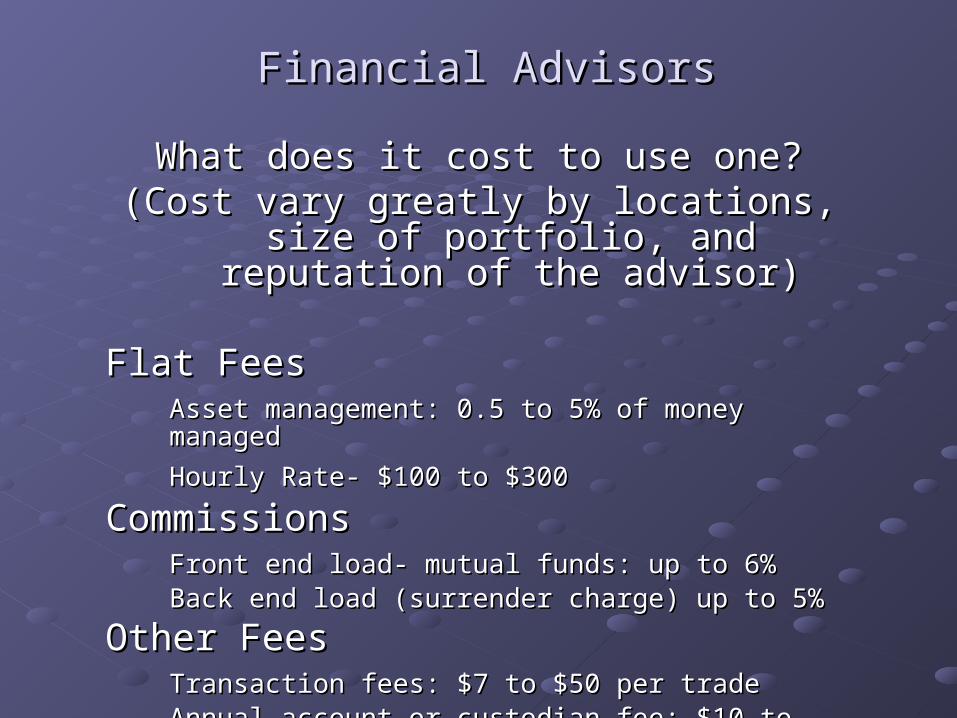

What does it cost to use one?What does it cost to use one?(Cost vary greatly by locations, size of (Cost vary greatly by locations, size of

portfolio, and reputation of the advisor)portfolio, and reputation of the advisor)

Flat FeesFlat FeesAsset management: 0.5 to 5% of money managedAsset management: 0.5 to 5% of money managed

Hourly Rate- $100 to $300Hourly Rate- $100 to $300

CommissionsCommissionsFront end load- mutual funds: up to 6%Front end load- mutual funds: up to 6%Back end load (surrender charge) up to 5%Back end load (surrender charge) up to 5%

Other FeesOther FeesTransaction fees: $7 to $50 per tradeTransaction fees: $7 to $50 per tradeAnnual account or custodian fee: $10 to $50 per yearAnnual account or custodian fee: $10 to $50 per year

Financial AdvisorsFinancial Advisors

What do the do, i.e. what is the What do the do, i.e. what is the scope of their services?scope of their services?

While the common impression is While the common impression is that the advisors tell you how that the advisors tell you how to invest your money, those to invest your money, those with certifications take a much with certifications take a much more comprehensive more comprehensive approach.approach.

Financial AdvisorsFinancial Advisors

What do the do, i.e. what is the scope What do the do, i.e. what is the scope of their services?of their services?

The professionals will want to thoroughly understand you The professionals will want to thoroughly understand you entire personal situation as it reflects on your finances: entire personal situation as it reflects on your finances: age, income, assets/investments, debts, goals, time age, income, assets/investments, debts, goals, time frames, estate planning, possible inheritances, frames, estate planning, possible inheritances, temperament, fears, prejudices.temperament, fears, prejudices.

He / she will want to coordinate with your other professional He / she will want to coordinate with your other professional consultants such as attorneys, insurance agents and consultants such as attorneys, insurance agents and CPAs.CPAs.

He / she will want to match up your back ground with an He / she will want to match up your back ground with an investment plan that will satisfy you and give you a investment plan that will satisfy you and give you a comfortable feeling about your financial security.comfortable feeling about your financial security.

Financial AdvisorsFinancial Advisors

What do the do, i.e. what is the scope What do the do, i.e. what is the scope of their services?of their services?

The financial plan will probably include a detailed allocation The financial plan will probably include a detailed allocation of your investments as matched up with your personal of your investments as matched up with your personal situation, but also will Include a complete situation, but also will Include a complete accumulation / arrangement of your key records: accumulation / arrangement of your key records: Pension and retirement, insurance, property, marriage Pension and retirement, insurance, property, marriage and divorce, Social Security,tax, property insurance, and divorce, Social Security,tax, property insurance, military, cemetery lots and instructions, safe-deposit military, cemetery lots and instructions, safe-deposit and bank accounts, life insurance, loan agreements, and bank accounts, life insurance, loan agreements, credit cards etccredit cards etc

Normally the Advisors will want to meet at least annually to Normally the Advisors will want to meet at least annually to take in to account any changes in your situation as it take in to account any changes in your situation as it affects your plan and investments.affects your plan and investments.

Financial AdvisorsFinancial Advisors

What do they do?What do they do?

Recently an article in Barron's gave a list of the top 100 Advisors in Recently an article in Barron's gave a list of the top 100 Advisors in the US and described the investment actions that the top 10 the US and described the investment actions that the top 10 were recommending to their clients:were recommending to their clients:

Their comments:Their comments: They don’t buy the PIMCO concept of the “new They don’t buy the PIMCO concept of the “new

normal”normal” Asset allocation and diversification still appliesAsset allocation and diversification still applies The big thing is to avoid mistakes and protect capitalThe big thing is to avoid mistakes and protect capital The fast recovery is over, now it will be slow The fast recovery is over, now it will be slow

and steadyand steady Return to hedge funds and away from bondsReturn to hedge funds and away from bonds Large cap dividend payers are better than bonds nowLarge cap dividend payers are better than bonds now Use fund managers going forward now instead of stock Use fund managers going forward now instead of stock

pickerspickers

Financial AdvisorsFinancial Advisors

How can you find an Advisor?How can you find an Advisor?

First decide which type of advisor you want to deal First decide which type of advisor you want to deal with.with.

For a Fiduciary Advisor, the NAPFA has a guide for For a Fiduciary Advisor, the NAPFA has a guide for this: this: http://findanadvisor.napfa.org/Home.aspx/Search

They are listed about where ever you want to look: They are listed about where ever you want to look: phone books, on line etc.phone books, on line etc.

Perhaps the best way is to get a referral by a satisfied Perhaps the best way is to get a referral by a satisfied client.client.

Financial AdvisorsFinancial Advisors

How can you find an Advisor?How can you find an Advisor?

You also need to how to avoid Bernie Madoff and You also need to how to avoid Bernie Madoff and

Robert Stanford type AdvisorsRobert Stanford type Advisors.. http://www.napfa.org/userfiles/file/Worried About Your Advisor.pdf

What are other ways to avoid getting scammed?What are other ways to avoid getting scammed?

Financial AdvisorsFinancial Advisors

How can you find an Advisor?How can you find an Advisor?

To avoid getting scammed:To avoid getting scammed:If you choose to work with an advisor there are several ways to avoid this

1.You can just 1.You can just pay a flat fee for a financial planpay a flat fee for a financial plan which will tell you how to make your which will tell you how to make your investments and then you make the investments your self through various investments and then you make the investments your self through various brokerages or investment houses such as Schwab, Vanguard, Fidelity.brokerages or investment houses such as Schwab, Vanguard, Fidelity.

2 Never use an Advisor that handles your money directly. When you write a check, 2 Never use an Advisor that handles your money directly. When you write a check, the payee should be the broker (Scott Trade, Schwab etc) not the advisor. the payee should be the broker (Scott Trade, Schwab etc) not the advisor.

3. There are two types of ways to authorize an Advisor to invest your money: a. Non 3. There are two types of ways to authorize an Advisor to invest your money: a. Non Discretionary-You place the tradesDiscretionary-You place the trades

b. Discretionary-you delegate all decisions tob. Discretionary-you delegate all decisions to the plannerthe planner

Choose Non Discretionary.Choose Non Discretionary. 4. If you allow an Advisor to use discretionary authority, then get regular reports from 4. If you allow an Advisor to use discretionary authority, then get regular reports from

the broker that do not get routed through the Advisor.the broker that do not get routed through the Advisor.

Financial AdvisorsFinancial Advisors

What’s Best thing to Do?What’s Best thing to Do?

1. If you are still in your career and building your retirement portfolio, 1. If you are still in your career and building your retirement portfolio, paying for a comprehensive Financial plan is a good idea. paying for a comprehensive Financial plan is a good idea.

It will point out omissions, mistakes, and give good It will point out omissions, mistakes, and give good counsel on strategy pertinent for your stage of life, family counsel on strategy pertinent for your stage of life, family obligations, and current wealthobligations, and current wealth

Then the implementation of the plan would depend on Then the implementation of the plan would depend on the factors mentioned before: Your knowledge of investments, the factors mentioned before: Your knowledge of investments,

2. If you are retired, the opportunity to structure your financial 2. If you are retired, the opportunity to structure your financial situation does not have as many options but a plan may still be situation does not have as many options but a plan may still be instructive if you have never had one. instructive if you have never had one.

If you have basic knowledge of investments, and keep informed, If you have basic knowledge of investments, and keep informed, you can probably achieve similar results with out paying the fee.you can probably achieve similar results with out paying the fee.

According to Malkiel, et al, buying index funds will out perform According to Malkiel, et al, buying index funds will out perform the actively managed funds 75% of the time. The S & P index the actively managed funds 75% of the time. The S & P index outperforms the average managed fund by 2%.outperforms the average managed fund by 2%.

Financial AdvisorsFinancial AdvisorsHmmmm—Another way?Hmmmm—Another way?

A thought:A thought: A CFP who charges based on the asset base, does so with the A CFP who charges based on the asset base, does so with the

incentive to make your asset base bigger so that he makes more incentive to make your asset base bigger so that he makes more money. I wonder at the justification for associating his pay on money. I wonder at the justification for associating his pay on the asset base.the asset base.

Perhaps a better way for the client would be to pay him a higher fee Perhaps a better way for the client would be to pay him a higher fee based on what performance he achieves for your portfolio above based on what performance he achieves for your portfolio above what an allocation between equity and fixed income would earn if what an allocation between equity and fixed income would earn if invested in Index funds.invested in Index funds.

If he doesn’t out perform the index, he doesn’t get paid.If he doesn’t out perform the index, he doesn’t get paid.

Problem is he may make long shots.Problem is he may make long shots.

Financial AdvisorsFinancial Advisors

The EndThe End