Embed Size (px)

Citation preview

Shaima Hasan, Sukuk Analyst, Thomson Reuters - Islamic Finance Ayman Hamza, Client Specialist, Thomson Reuters – Islamic Finance

“Thomson Reuters” Workshop: Deep Dive Sukuk

Oman Second Islamic Banking & Finance Conference

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

DEEP DIVE SUKUK WORKSHOP

OMAN SECOND ISLAMIC BANKING AND FINANCE CONFERENCE

MUSCAT - OMAN

Ayman Hamza, Client Specialist

Shaima Hasan, Sukuk Analyst

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

INTRODUCTION TO ISLAMIC FINANCE

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

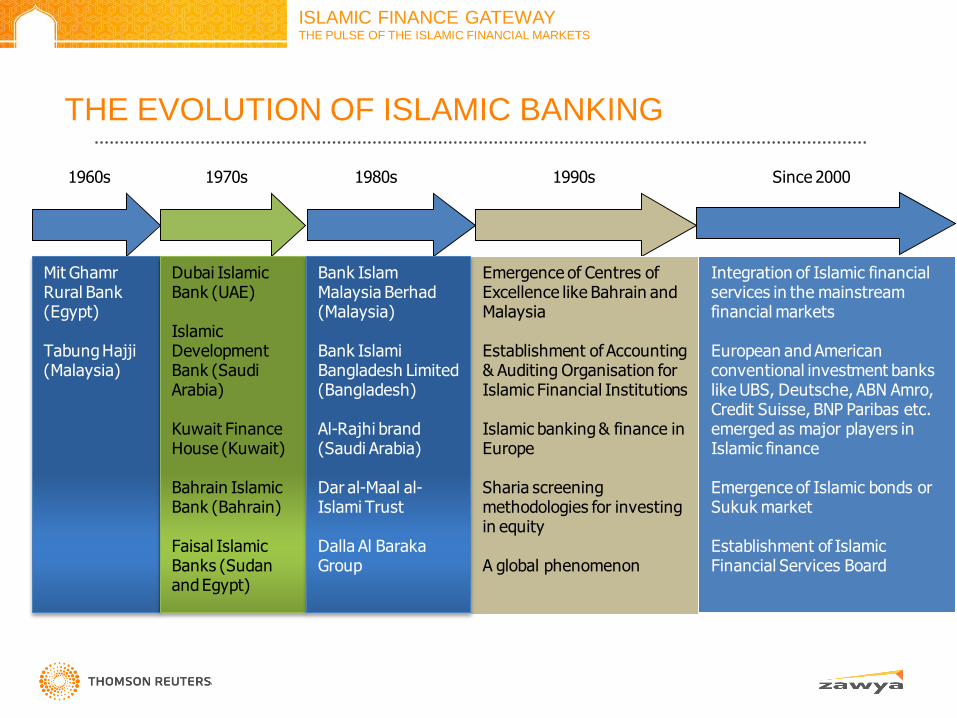

THE EVOLUTION OF ISLAMIC BANKING

1960s 1970s 1980s 1990s Since 2000

Emergence of Centres of Excellence like Bahrain and Malaysia

Establishment of Accounting & Auditing Organisation for Islamic Financial Institutions

Islamic banking & finance in Europe

Sharia screening methodologies for investing in equity

A global phenomenon

Integration of Islamic financial services in the mainstream financial markets

European and American conventional investment banks like UBS, Deutsche, ABN Amro, Credit Suisse, BNP Paribas etc. emerged as major players in Islamic finance

Emergence of Islamic bonds or Sukuk market

Establishment of Islamic Financial Services Board

Mit GhamrRural Bank (Egypt)

TabungHajji (Malaysia)

Dubai Islamic Bank (UAE)

Islamic Development Bank (Saudi Arabia)

Kuwait Finance House (Kuwait)

Bahrain Islamic Bank (Bahrain)

Faisal Islamic Banks (Sudan and Egypt)

Bank Islam Malaysia Berhad(Malaysia)

Bank IslamiBangladesh Limited (Bangladesh)

Al-Rajhi brand (Saudi Arabia)

Dar al-Maal al-Islami Trust

Dalla Al Baraka Group

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

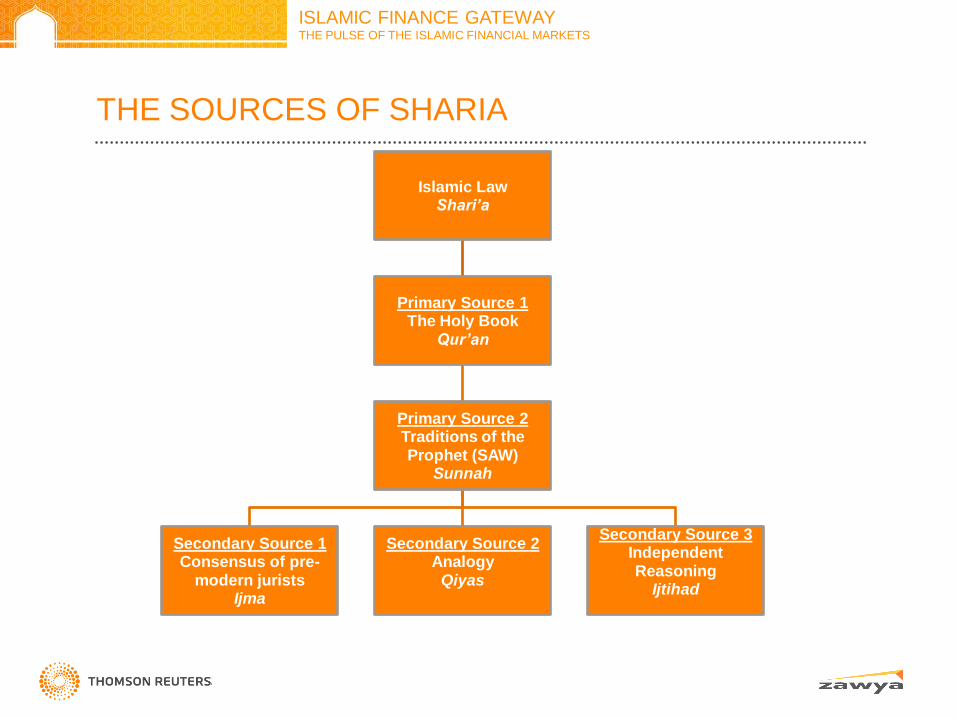

THE SOURCES OF SHARIA

Islamic Law Shari’a

Primary Source 1 The Holy Book

Qur’an

Primary Source 2 Traditions of the Prophet (SAW)

Sunnah

Secondary Source 1 Consensus of pre-

modern jurists Ijma

Secondary Source 2 Analogy

Qiyas

Secondary Source 3 Independent Reasoning

Ijtihad

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

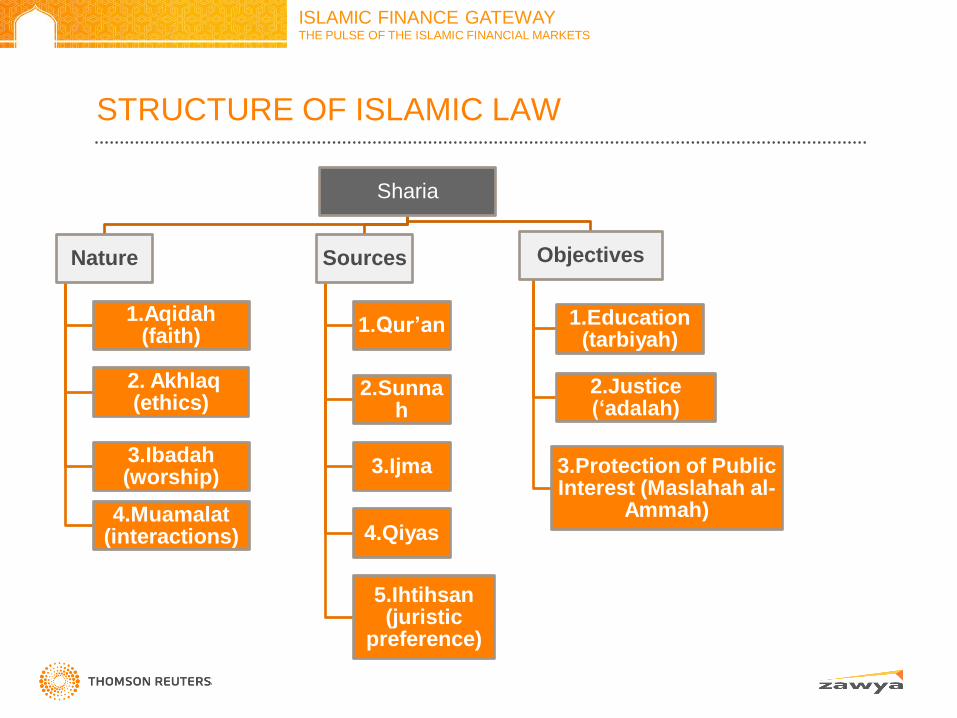

STRUCTURE OF ISLAMIC LAW

Sharia

Nature

1.Aqidah (faith)

2. Akhlaq (ethics)

3.Ibadah (worship)

4.Muamalat (interactions)

Sources

1.Qur’an

2.Sunnah

3.Ijma

4.Qiyas

5.Ihtihsan (juristic

preference)

Objectives

1.Education (tarbiyah)

2.Justice (‘adalah)

3.Protection of Public Interest (Maslahah al-

Ammah)

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

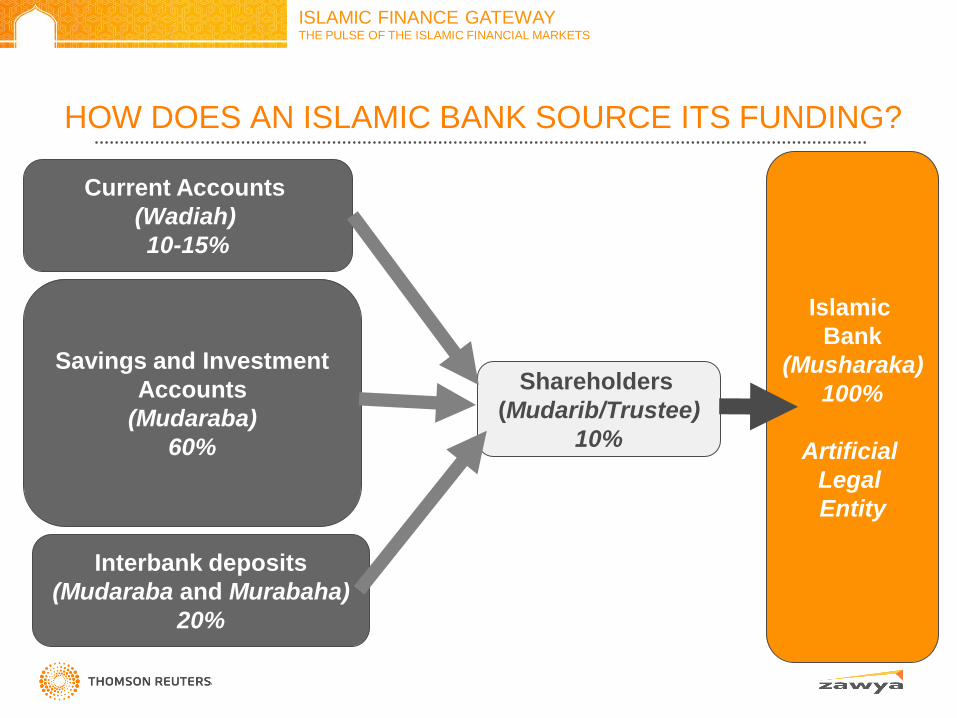

HOW DOES AN ISLAMIC BANK SOURCE ITS FUNDING?

Current Accounts

(Wadiah)

10-15%

Savings and Investment

Accounts

(Mudaraba)

60%

Interbank deposits

(Mudaraba and Murabaha)

20%

Shareholders

(Mudarib/Trustee)

10%

Islamic

Bank

(Musharaka)

100%

Artificial

Legal

Entity

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

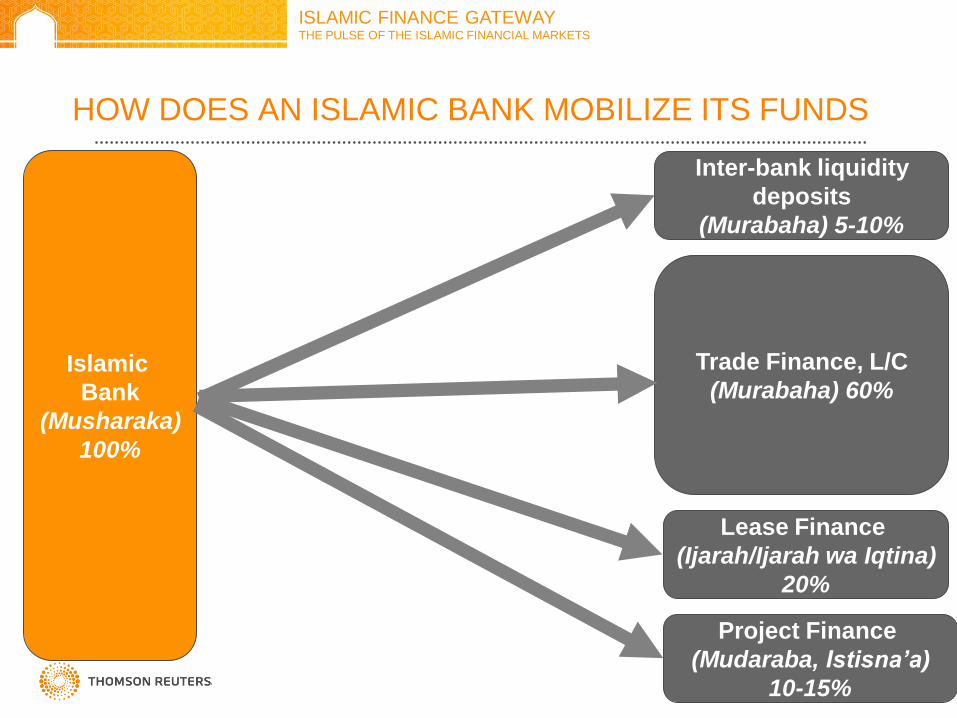

HOW DOES AN ISLAMIC BANK MOBILIZE ITS FUNDS

Islamic

Bank

(Musharaka)

100%

Inter-bank liquidity

deposits

(Murabaha) 5-10%

Trade Finance, L/C

(Murabaha) 60%

Lease Finance

(Ijarah/Ijarah wa Iqtina)

20%

Project Finance

(Mudaraba, Istisna’a)

10-15%

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

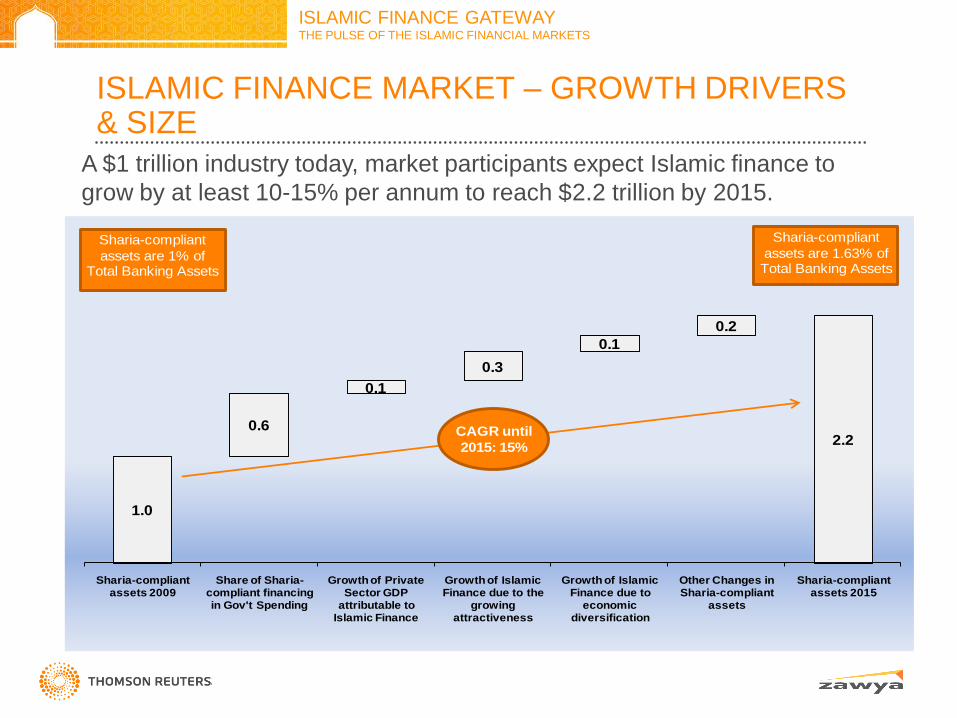

ISLAMIC FINANCE MARKET – GROWTH DRIVERS & SIZE

1.0

0.6

0.1

0.3

0.1

0.2

2.2

Sharia-compliant assets 2009

Share of Sharia-compliant financing in Gov't Spending

Growth of Private Sector GDP

attributable to Islamic Finance

Growth of Islamic Finance due to the

growing attractiveness

Growth of Islamic Finance due to

economic diversification

Other Changes in Sharia-compliant

assets

Sharia-compliant assets 2015

CAGR until

2015: 15%

Sharia-compliant

assets are 1% of Total Banking Assets

Sharia-compliant

assets are 1.63% of Total Banking Assets

A $1 trillion industry today, market participants expect Islamic finance to

grow by at least 10-15% per annum to reach $2.2 trillion by 2015.

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

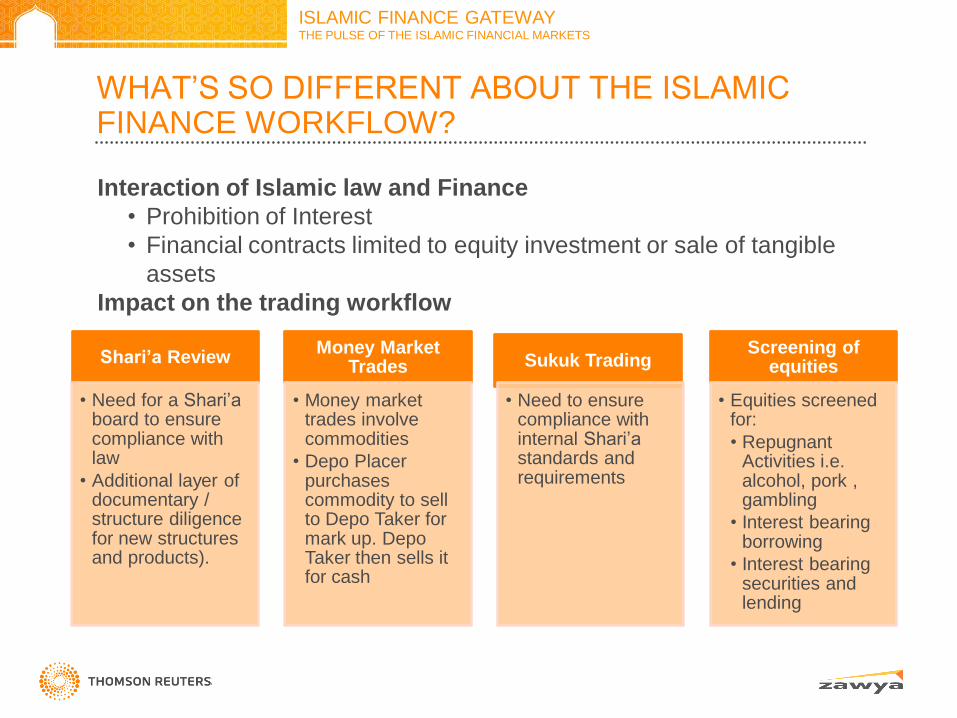

WHAT‟S SO DIFFERENT ABOUT THE ISLAMIC FINANCE WORKFLOW?

Interaction of Islamic law and Finance

• Prohibition of Interest

• Financial contracts limited to equity investment or sale of tangible

assets

Impact on the trading workflow

Shari’a Review

• Need for a Shari‟a board to ensure compliance with law

• Additional layer of documentary / structure diligence for new structures and products).

Money Market Trades

• Money market trades involve commodities

• Depo Placer purchases commodity to sell to Depo Taker for mark up. Depo Taker then sells it for cash

Sukuk Trading

• Need to ensure compliance with internal Shari‟a standards and requirements

Screening of equities

• Equities screened for:

• Repugnant Activities i.e. alcohol, pork , gambling

• Interest bearing borrowing

• Interest bearing securities and lending

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

ISLAMIC FINANCE INTERBANK MONEY MARKET

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

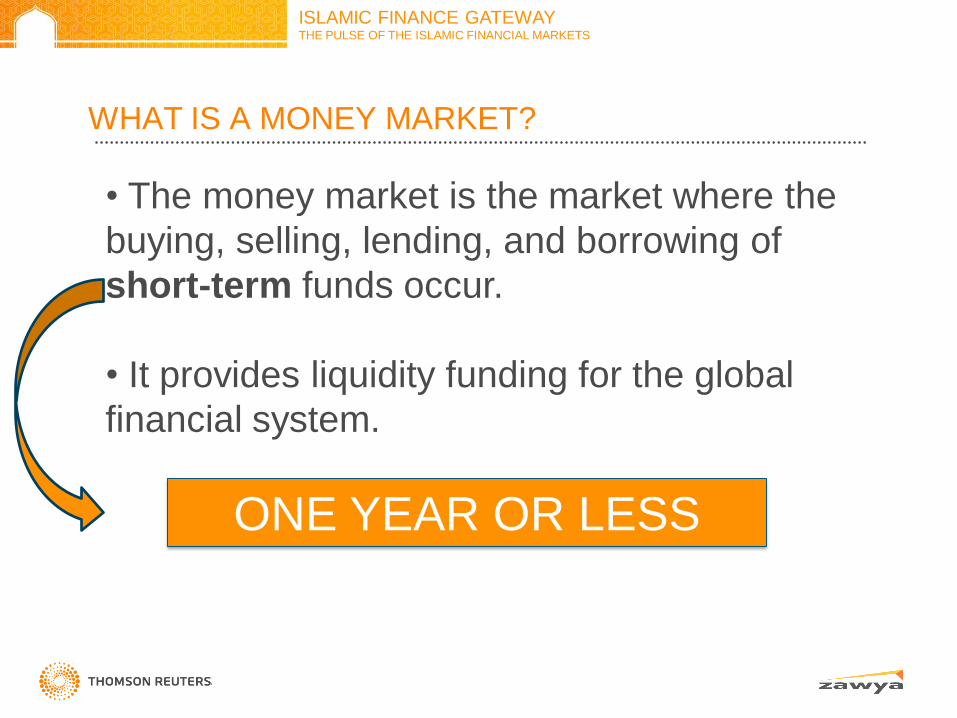

WHAT IS A MONEY MARKET?

• The money market is the market where the

buying, selling, lending, and borrowing of

short-term funds occur.

• It provides liquidity funding for the global

financial system.

ONE YEAR OR LESS

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

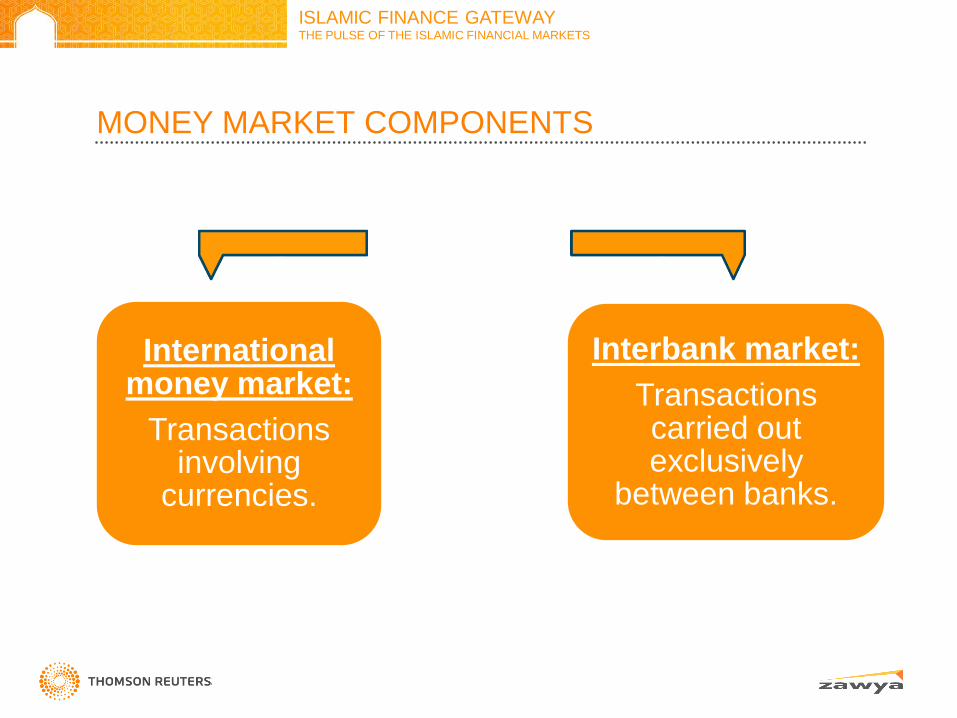

International money market:

Transactions involving

currencies.

Interbank market:

Transactions carried out exclusively

between banks.

MONEY MARKET COMPONENTS

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

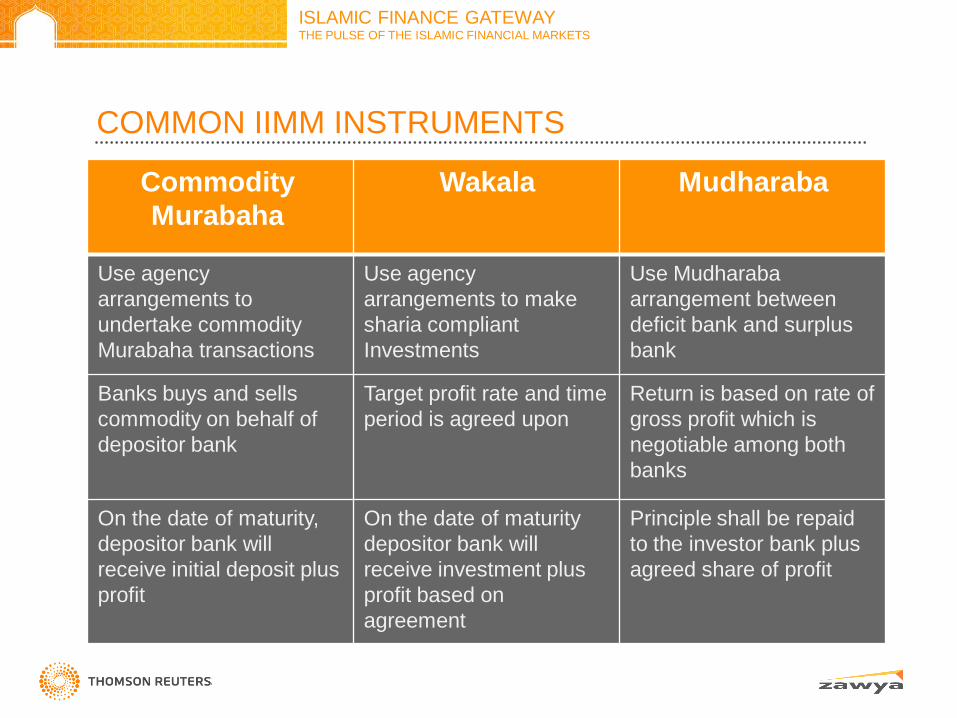

COMMON IIMM INSTRUMENTS

Commodity

Murabaha

Wakala Mudharaba

Use agency

arrangements to

undertake commodity

Murabaha transactions

Use agency

arrangements to make

sharia compliant

Investments

Use Mudharaba

arrangement between

deficit bank and surplus

bank

Banks buys and sells

commodity on behalf of

depositor bank

Target profit rate and time

period is agreed upon

Return is based on rate of

gross profit which is

negotiable among both

banks

On the date of maturity,

depositor bank will

receive initial deposit plus

profit

On the date of maturity

depositor bank will

receive investment plus

profit based on

agreement

Principle shall be repaid

to the investor bank plus

agreed share of profit

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

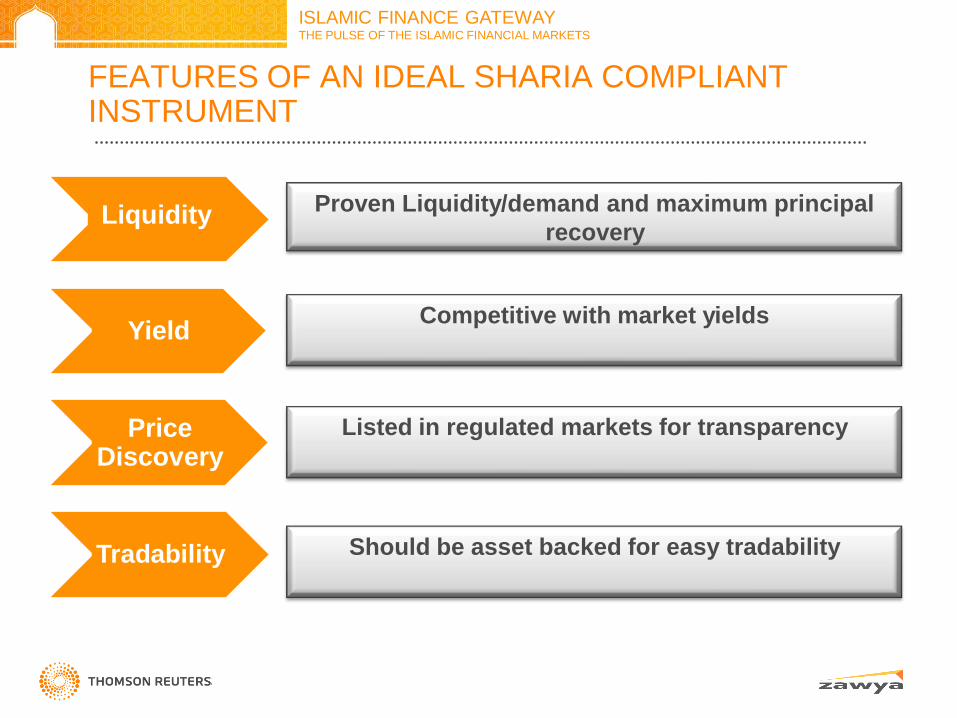

FEATURES OF AN IDEAL SHARIA COMPLIANT INSTRUMENT

Liquidity Proven Liquidity/demand and maximum principal

recovery

Yield Competitive with market yields

Price Discovery

Listed in regulated markets for transparency

Tradability Should be asset backed for easy tradability

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

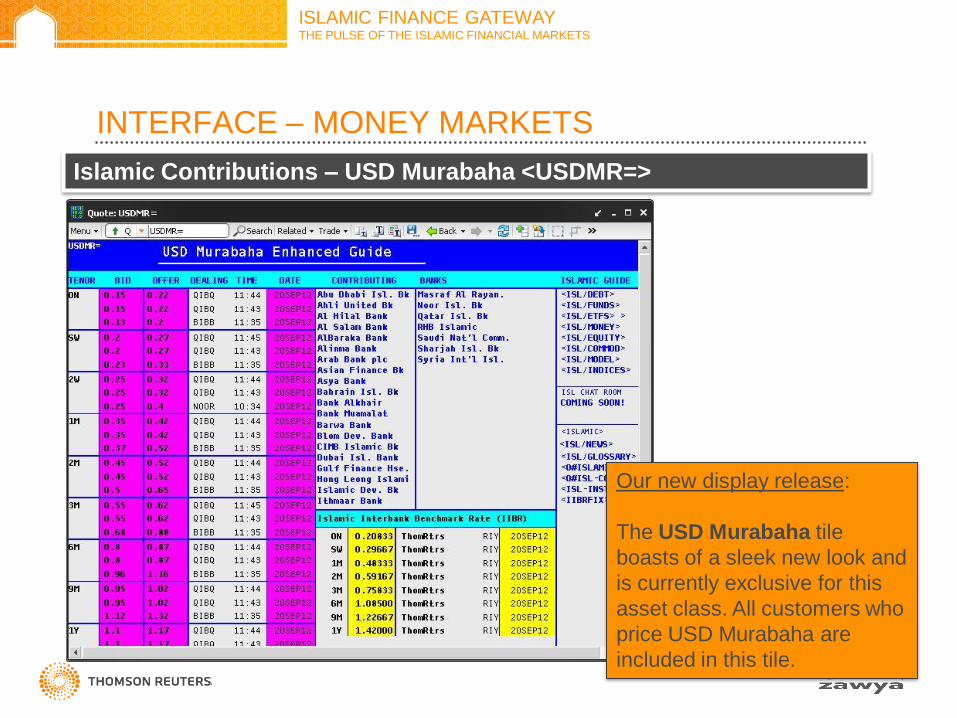

INTERFACE – MONEY MARKETS

Islamic Contributions – USD Murabaha <USDMR=>

Our new display release:

The USD Murabaha tile

boasts of a sleek new look and

is currently exclusive for this

asset class. All customers who

price USD Murabaha are

included in this tile.

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

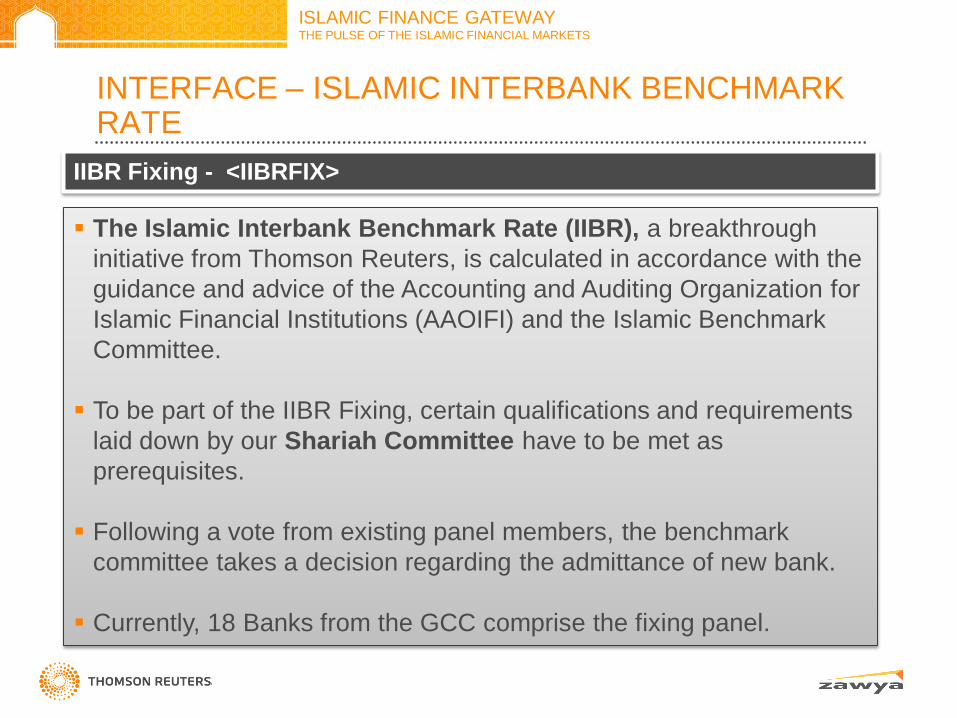

INTERFACE – ISLAMIC INTERBANK BENCHMARK RATE

IIBR Fixing - <IIBRFIX>

The Islamic Interbank Benchmark Rate (IIBR), a breakthrough

initiative from Thomson Reuters, is calculated in accordance with the

guidance and advice of the Accounting and Auditing Organization for

Islamic Financial Institutions (AAOIFI) and the Islamic Benchmark

Committee.

To be part of the IIBR Fixing, certain qualifications and requirements

laid down by our Shariah Committee have to be met as

prerequisites.

Following a vote from existing panel members, the benchmark

committee takes a decision regarding the admittance of new bank.

Currently, 18 Banks from the GCC comprise the fixing panel.

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

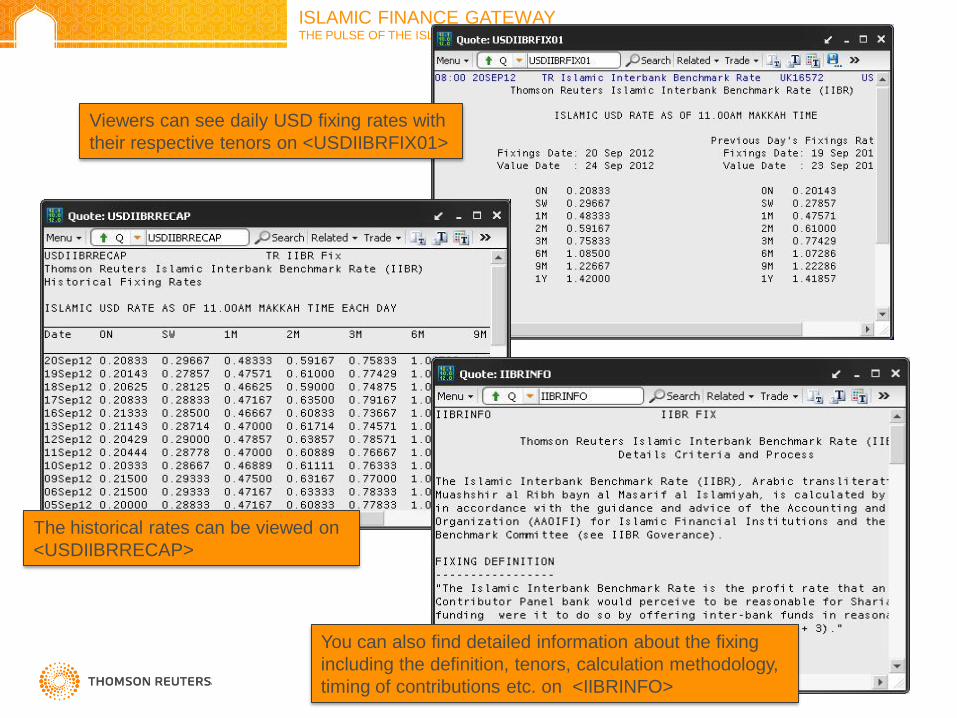

You can also find detailed information about the fixing

including the definition, tenors, calculation methodology,

timing of contributions etc. on <IIBRINFO>

The historical rates can be viewed on

<USDIIBRRECAP>

Viewers can see daily USD fixing rates with

their respective tenors on <USDIIBRFIX01>

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

WHAT IS SUKUK?

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

SUKUK IS…

An Islamic Investment instruments, comes from the word “Sak” which means a financial certificate. Sukuk are always linked to the underlying assets (tangible or intangible), which gives a partial ownership in the assets

Sukuk refer to securitization, a process in which ownership of the underlying assets is transferred to a large number of investors

Sukuk can be structured in a number of ways, depending on the underlying assets and the business purpose.

While majority of the Sukuk issued to date have utilized “Ijara” or “Musharaka” structures based on real estate as the underlying asset.

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

..HENCE THE OBJECTIVES OF SUKUK ARE…

Raise capital in a Sharia-compliant style

Expand the investor base

Offering investment opportunities

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

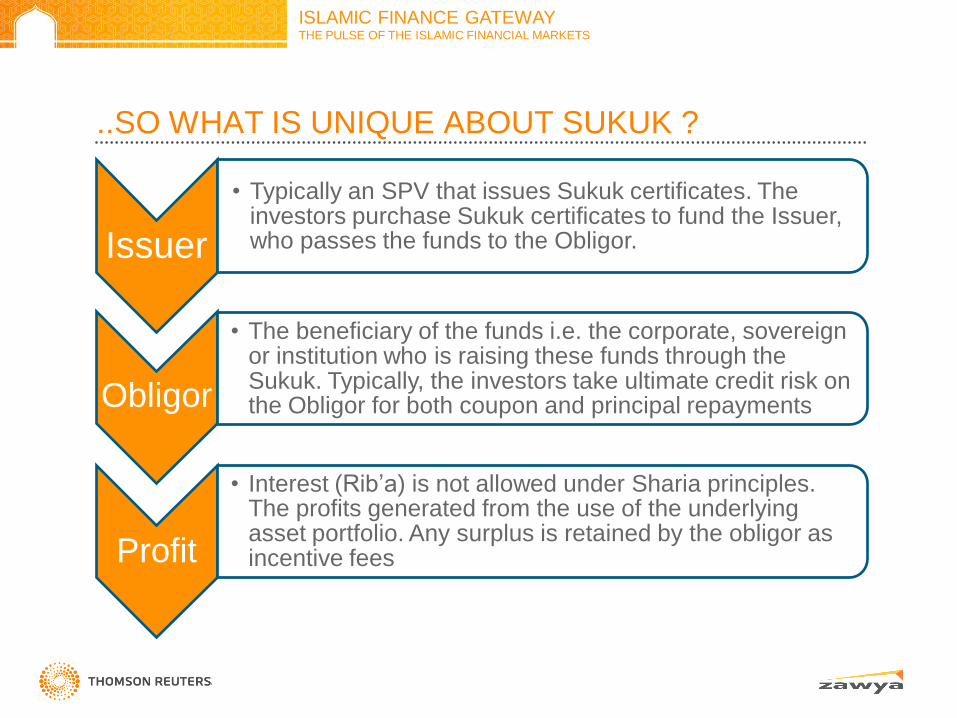

..SO WHAT IS UNIQUE ABOUT SUKUK ?

Issuer

• Typically an SPV that issues Sukuk certificates. The

investors purchase Sukuk certificates to fund the Issuer, who passes the funds to the Obligor.

Obligor

• The beneficiary of the funds i.e. the corporate, sovereign or institution who is raising these funds through the Sukuk. Typically, the investors take ultimate credit risk on the Obligor for both coupon and principal repayments

Profit

• Interest (Rib‟a) is not allowed under Sharia principles. The profits generated from the use of the underlying asset portfolio. Any surplus is retained by the obligor as incentive fees

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

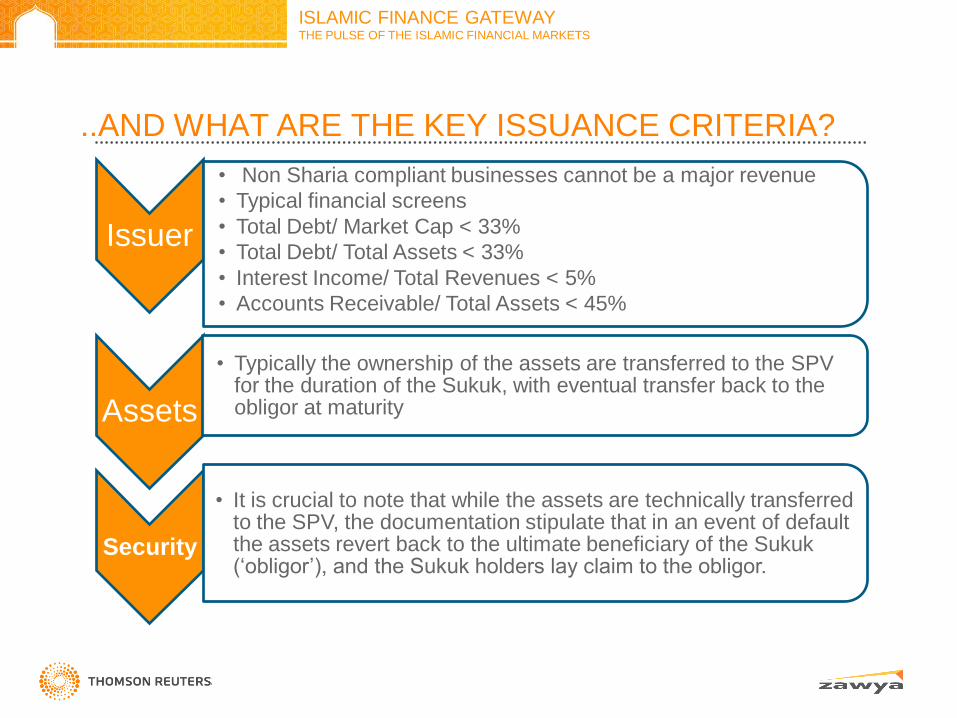

..AND WHAT ARE THE KEY ISSUANCE CRITERIA?

Issuer

• Non Sharia compliant businesses cannot be a major revenue

• Typical financial screens

• Total Debt/ Market Cap < 33%

• Total Debt/ Total Assets < 33%

• Interest Income/ Total Revenues < 5%

• Accounts Receivable/ Total Assets < 45%

Assets

• Typically the ownership of the assets are transferred to the SPV

for the duration of the Sukuk, with eventual transfer back to the obligor at maturity

Security

• It is crucial to note that while the assets are technically transferred to the SPV, the documentation stipulate that in an event of default the assets revert back to the ultimate beneficiary of the Sukuk („obligor‟), and the Sukuk holders lay claim to the obligor.

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

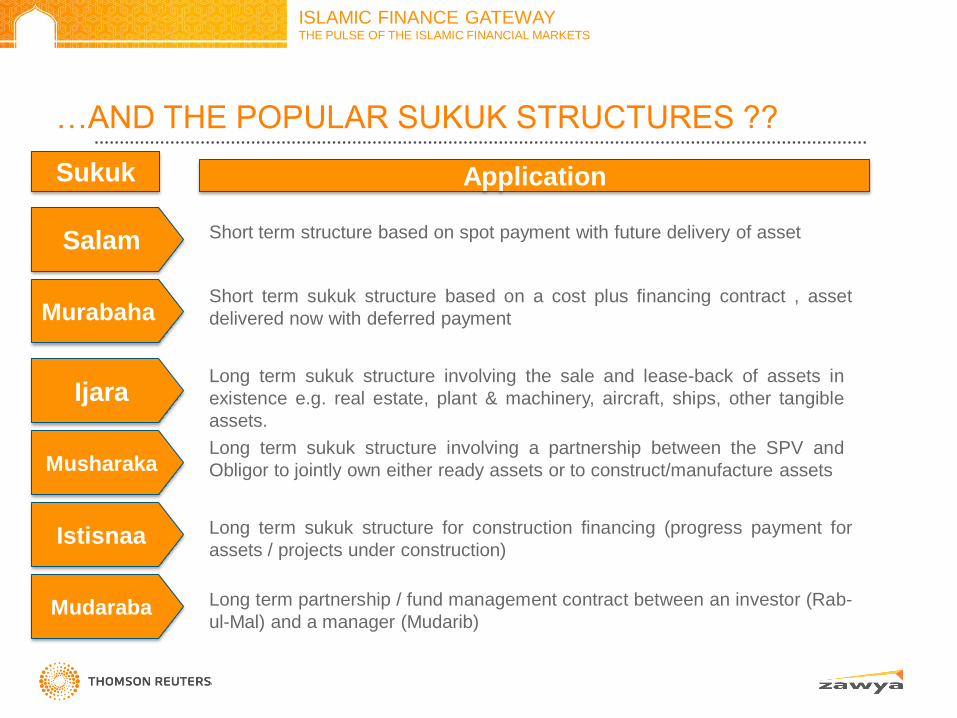

• Sukuk Application

Salam Short term structure based on spot payment with future delivery of asset

Long term sukuk structure involving the sale and lease-back of assets in

existence e.g. real estate, plant & machinery, aircraft, ships, other tangible

assets.

Long term sukuk structure involving a partnership between the SPV and

Obligor to jointly own either ready assets or to construct/manufacture assets

Long term sukuk structure for construction financing (progress payment for

assets / projects under construction)

…AND THE POPULAR SUKUK STRUCTURES ??

Mudaraba

Murabaha

Ijara

Musharaka

Istisnaa

Short term sukuk structure based on a cost plus financing contract , asset

delivered now with deferred payment

Long term partnership / fund management contract between an investor (Rab-

ul-Mal) and a manager (Mudarib)

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

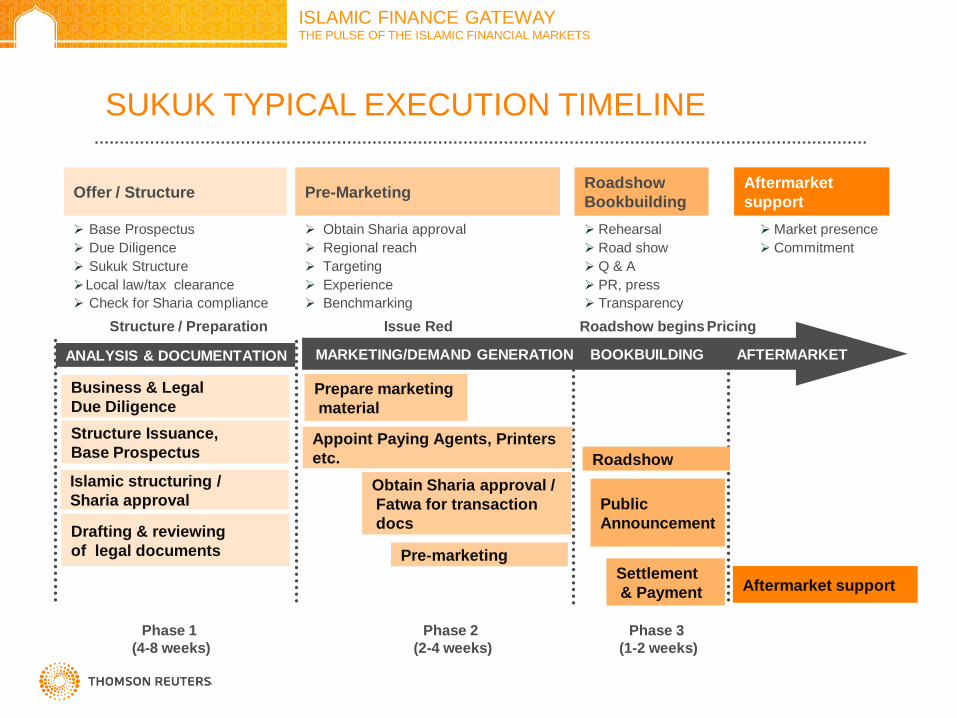

Offer / Structure Pre-Marketing Roadshow

Bookbuilding

Aftermarket

support

Base Prospectus

Due Diligence

Sukuk Structure

Local law/tax clearance

Check for Sharia compliance

Obtain Sharia approval

Regional reach

Targeting

Experience

Benchmarking

Rehearsal

Road show

Q & A

PR, press

Transparency

Market presence

Commitment

ANALYSIS & DOCUMENTATION MARKETING/DEMAND GENERATION BOOKBUILDING AFTERMARKET

Pre-marketing

Roadshow

Aftermarket support

Structure / Preparation Issue Red Roadshow begins Pricing

Phase 1

(4-8 weeks)

Phase 2

(2-4 weeks)

Appoint Paying Agents, Printers

etc.

Public

Announcement

Settlement

& Payment

Phase 3

(1-2 weeks)

Drafting & reviewing

of legal documents

Business & Legal

Due Diligence

Structure Issuance,

Base Prospectus

Prepare marketing

material

Islamic structuring /

Sharia approval Obtain Sharia approval /

Fatwa for transaction

docs

SUKUK TYPICAL EXECUTION TIMELINE

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

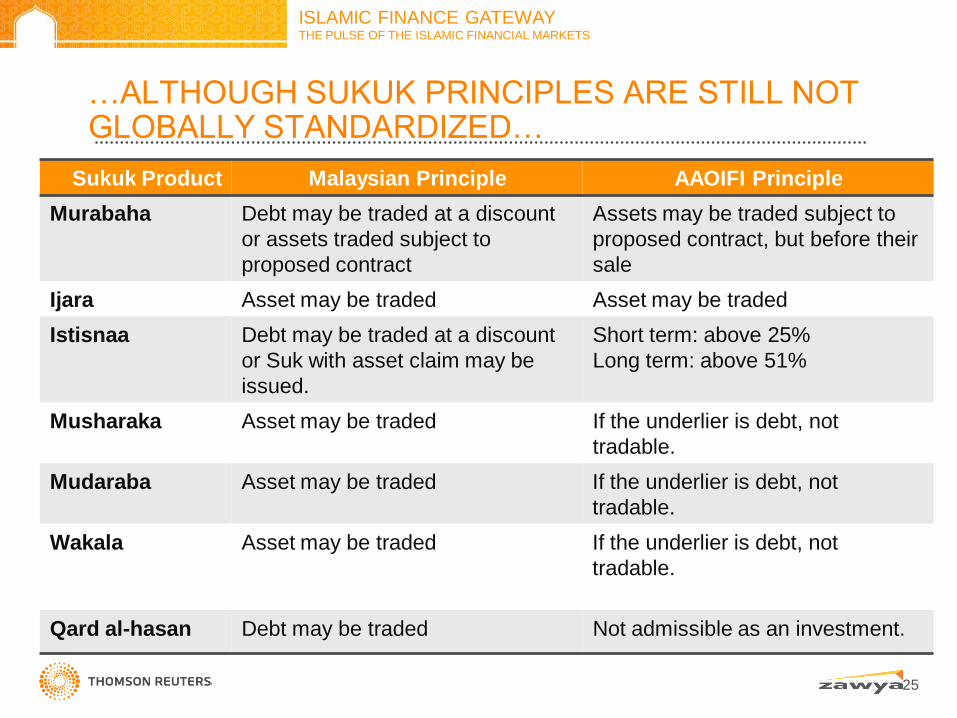

…ALTHOUGH SUKUK PRINCIPLES ARE STILL NOT GLOBALLY STANDARDIZED…

Sukuk Product Malaysian Principle AAOIFI Principle

Murabaha Debt may be traded at a discount

or assets traded subject to

proposed contract

Assets may be traded subject to

proposed contract, but before their

sale

Ijara Asset may be traded Asset may be traded

Istisnaa Debt may be traded at a discount

or Suk with asset claim may be

issued.

Short term: above 25%

Long term: above 51%

Musharaka Asset may be traded If the underlier is debt, not

tradable.

Mudaraba Asset may be traded If the underlier is debt, not

tradable.

Wakala Asset may be traded If the underlier is debt, not

tradable.

Qard al-hasan Debt may be traded Not admissible as an investment.

25

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

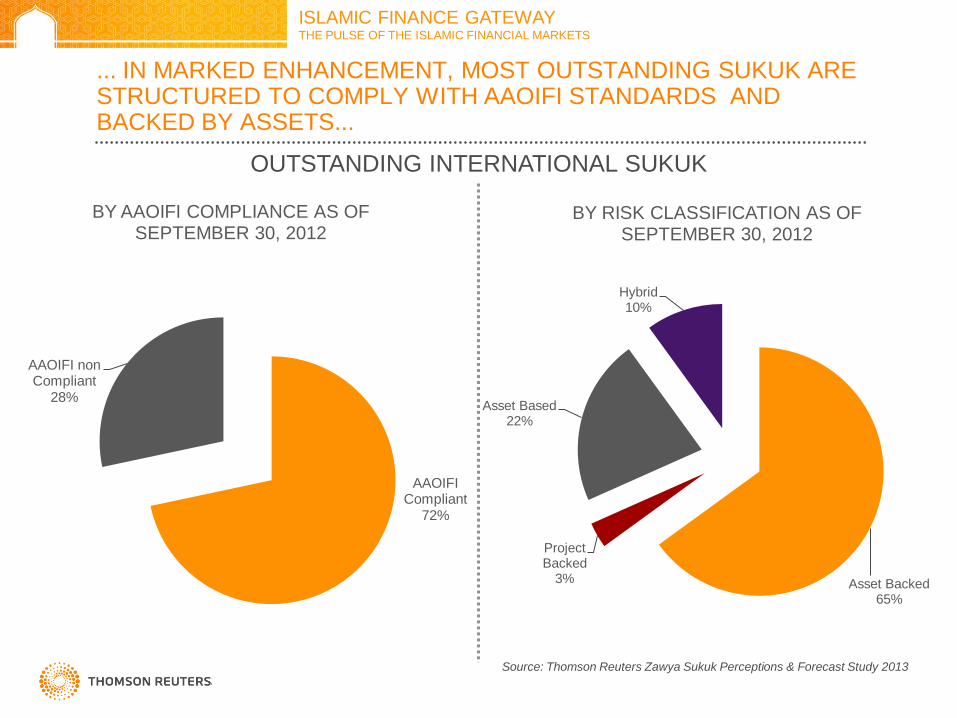

... IN MARKED ENHANCEMENT, MOST OUTSTANDING SUKUK ARE STRUCTURED TO COMPLY WITH AAOIFI STANDARDS AND BACKED BY ASSETS...

Asset Backed 65%

Project Backed

3%

Asset Based 22%

Hybrid 10%

BY RISK CLASSIFICATION AS OF SEPTEMBER 30, 2012

AAOIFI Compliant

72%

AAOIFI non Compliant

28%

BY AAOIFI COMPLIANCE AS OF SEPTEMBER 30, 2012

Source: Thomson Reuters Zawya Sukuk Perceptions & Forecast Study 2013

OUTSTANDING INTERNATIONAL SUKUK

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

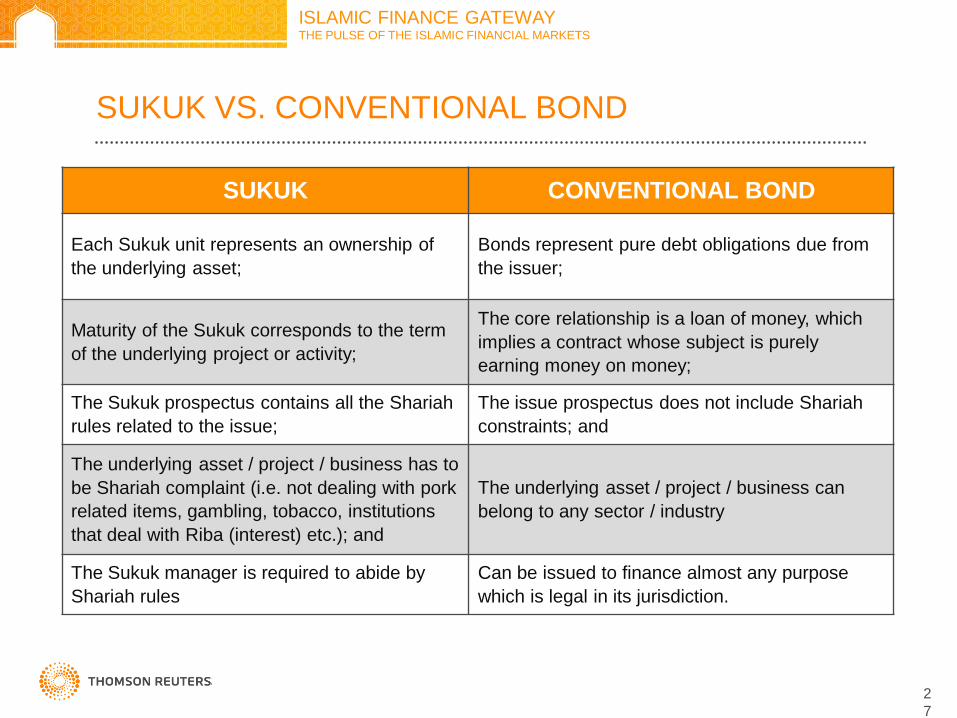

SUKUK VS. CONVENTIONAL BOND

SUKUK CONVENTIONAL BOND

Each Sukuk unit represents an ownership of

the underlying asset;

Bonds represent pure debt obligations due from

the issuer;

Maturity of the Sukuk corresponds to the term

of the underlying project or activity;

The core relationship is a loan of money, which

implies a contract whose subject is purely

earning money on money;

The Sukuk prospectus contains all the Shariah

rules related to the issue;

The issue prospectus does not include Shariah

constraints; and

The underlying asset / project / business has to

be Shariah complaint (i.e. not dealing with pork

related items, gambling, tobacco, institutions

that deal with Riba (interest) etc.); and

The underlying asset / project / business can

belong to any sector / industry

The Sukuk manager is required to abide by

Shariah rules

Can be issued to finance almost any purpose

which is legal in its jurisdiction.

2

7

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

LET’S VIEW KEY HISTORICAL TRENDS...

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

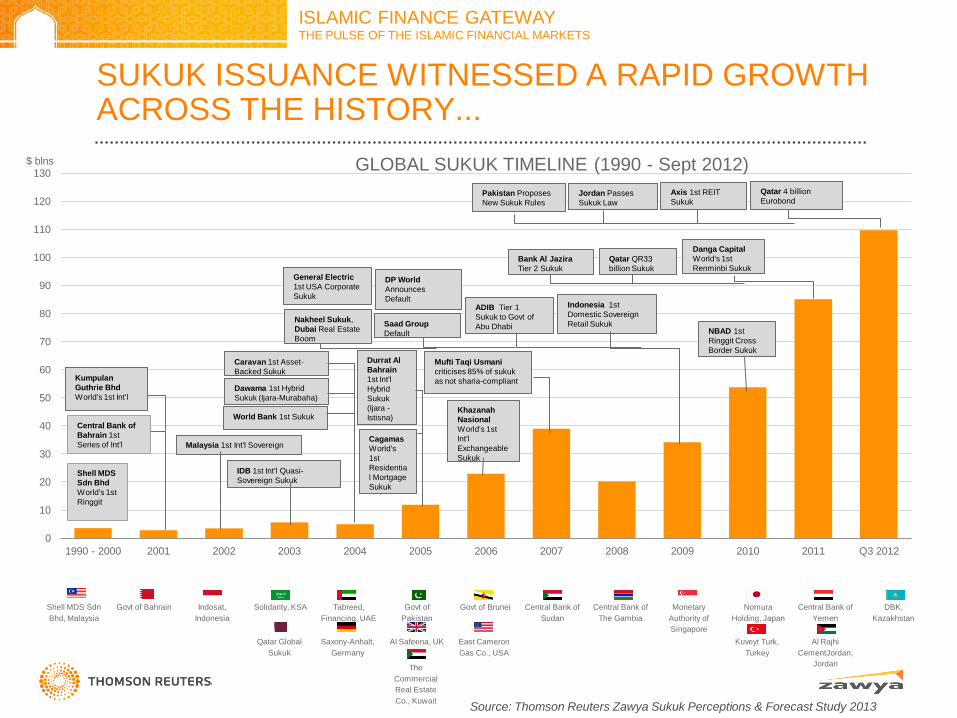

SUKUK ISSUANCE WITNESSED A RAPID GROWTH ACROSS THE HISTORY...

0

10

20

30

40

50

60

70

80

90

100

110

120

130

1990 - 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Q3 2012

$ blns GLOBAL SUKUK TIMELINE (1990 - Sept 2012)

Kumpulan

Guthrie Bhd

World's 1st Int'l

Malaysia 1st Int'l Sovereign

IDB 1st Int'l Quasi-

Sovereign Sukuk

Caravan 1st Asset-

Backed Sukuk

Dawama 1st Hybrid

Sukuk (Ijara-Murabaha)

World Bank 1st Sukuk

Cagamas

World's

1st

Residentia

l Mortgage

Sukuk

Durrat Al

Bahrain

1st Int'l

Hybrid

Sukuk

(Ijara -

Istisna)

Khazanah

Nasional

World's 1st

Int'l

Exchangeable

Sukuk

Nakheel Sukuk,

Dubai Real Estate

Boom

Saad Group

Default

DP World

Announces

Default

Mufti Taqi Usmani

criticises 85% of sukuk

as not sharia-compliant

Indonesia 1st

Domestic Sovereign

Retail Sukuk

ADIB Tier 1

Sukuk to Govt of

Abu Dhabi

Danga Capital

World's 1st

Renminbi Sukuk General Electric

1st USA Corporate

Sukuk

NBAD 1st

Ringgit Cross

Border Sukuk

Qatar QR33

billion Sukuk

Bank Al Jazira

Tier 2 Sukuk

Pakistan Proposes

New Sukuk Rules

Jordan Passes

Sukuk Law

Axis 1st REIT

Sukuk

Qatar 4 billion

Eurobond

Shell MDS

Sdn Bhd

World's 1st

Ringgit

Central Bank of

Bahrain 1st

Series of Int'l

Shell MDS Sdn

Bhd, Malaysia

Govt of Bahrain

Indosat,

Indonesia

Solidarity, KSA

Tabreed,

Financing, UAE

Govt of

Pakistan

Govt of Brunei

Central Bank of

Sudan

Central Bank of

The Gambia

Monetary

Authority of

Singapore

Nomura

Holding, Japan

Central Bank of

Yemen

DBK,

Kazakhstan

Qatar Global

Sukuk

Saxony-Anhalt,

Germany

Al Safeena, UK

East Cameron

Gas Co., USA

Kuveyt Turk,

Turkey

Al Rajhi

CementJordan,

Jordan

The

Commercial

Real Estate

Co., Kuwait Source: Thomson Reuters Zawya Sukuk Perceptions & Forecast Study 2013

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

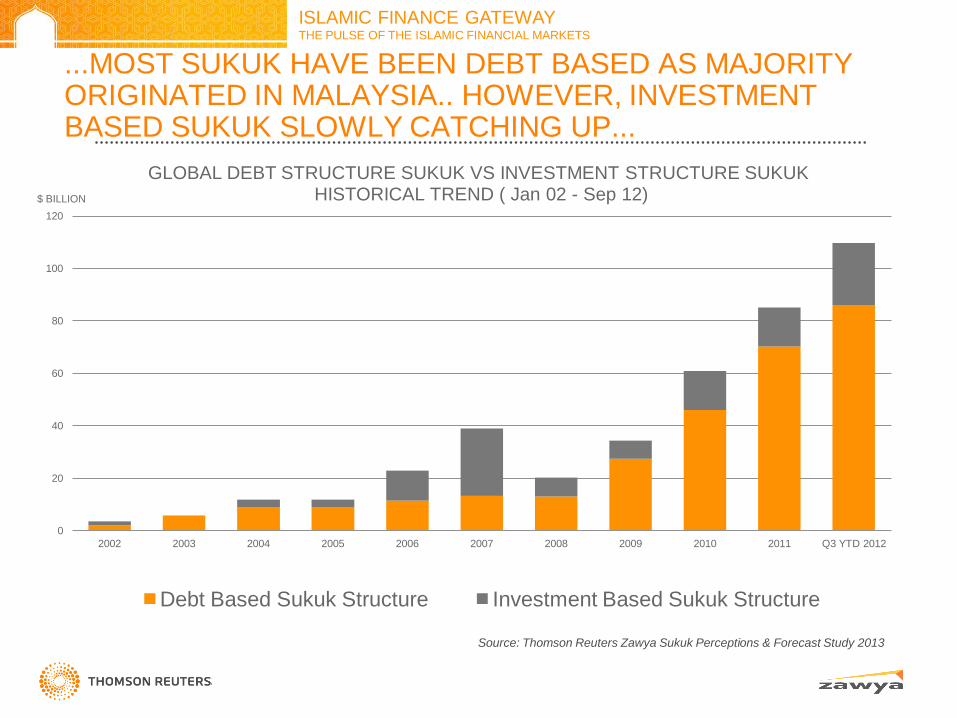

...MOST SUKUK HAVE BEEN DEBT BASED AS MAJORITY ORIGINATED IN MALAYSIA.. HOWEVER, INVESTMENT BASED SUKUK SLOWLY CATCHING UP...

Source: Thomson Reuters Zawya Sukuk Perceptions & Forecast Study 2013

0

20

40

60

80

100

120

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Q3 YTD 2012

$ BILLION

GLOBAL DEBT STRUCTURE SUKUK VS INVESTMENT STRUCTURE SUKUK HISTORICAL TREND ( Jan 02 - Sep 12)

Debt Based Sukuk Structure Investment Based Sukuk Structure

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

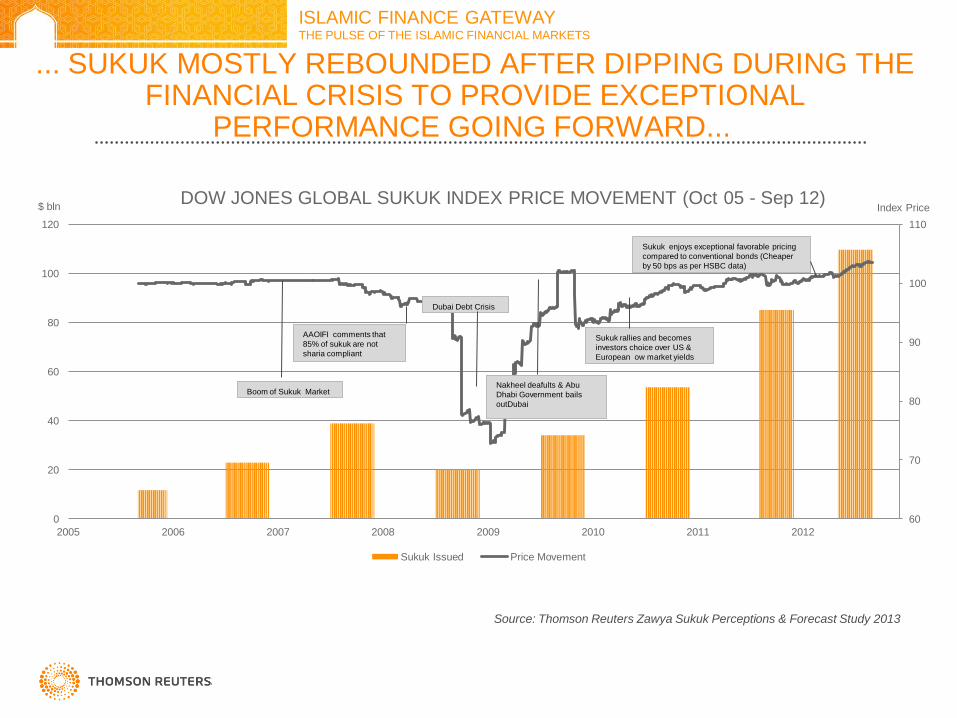

60

70

80

90

100

110

0

20

40

60

80

100

120

2005 2006 2007 2008 2009 2010 2011 2012

Index Price $ bln DOW JONES GLOBAL SUKUK INDEX PRICE MOVEMENT (Oct 05 - Sep 12)

Sukuk Issued Price Movement

Boom of Sukuk Market

Dubai Debt Crisis

Sukuk rallies and becomes

investors choice over US &

European ow market yields

Nakheel deafults & Abu

Dhabi Government bails

outDubai

Sukuk enjoys exceptional favorable pricing

compared to conventional bonds (Cheaper

by 50 bps as per HSBC data)

AAOIFI comments that

85% of sukuk are not

sharia compliant

... SUKUK MOSTLY REBOUNDED AFTER DIPPING DURING THE FINANCIAL CRISIS TO PROVIDE EXCEPTIONAL

PERFORMANCE GOING FORWARD...

Source: Thomson Reuters Zawya Sukuk Perceptions & Forecast Study 2013

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

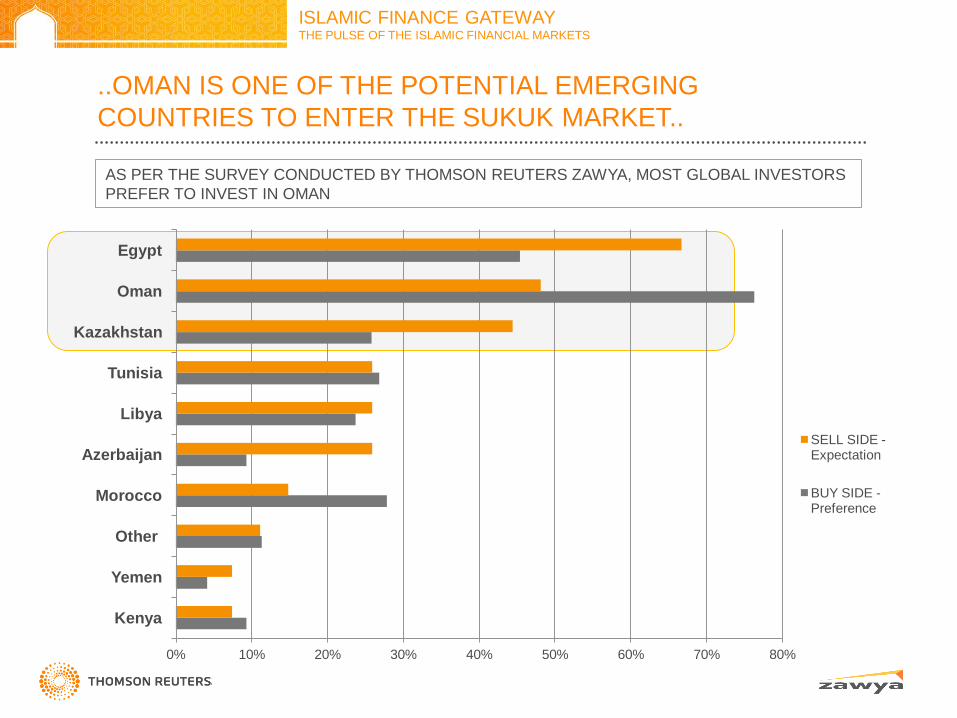

AS PER THE SURVEY CONDUCTED BY THOMSON REUTERS ZAWYA, MOST GLOBAL INVESTORS

PREFER TO INVEST IN OMAN

..OMAN IS ONE OF THE POTENTIAL EMERGING

COUNTRIES TO ENTER THE SUKUK MARKET..

0% 10% 20% 30% 40% 50% 60% 70% 80%

Kenya

Yemen

Other

Morocco

Azerbaijan

Libya

Tunisia

Kazakhstan

Oman

Egypt

SELL SIDE - Expectation

BUY SIDE - Preference

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

WILL SUPPLY MEET DEMAND?

DEMAND AND SUPPLY EQUILIBRIUM ANALYSIS

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

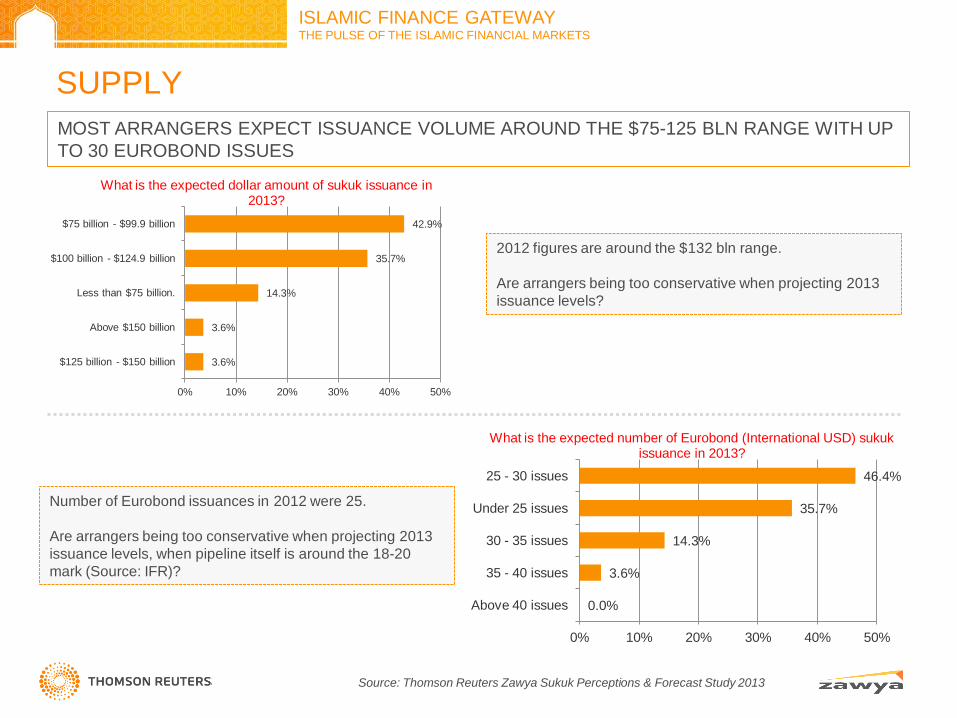

SUPPLY

3.6%

3.6%

14.3%

35.7%

42.9%

0% 10% 20% 30% 40% 50%

$125 billion - $150 billion

Above $150 billion

Less than $75 billion.

$100 billion - $124.9 billion

$75 billion - $99.9 billion

What is the expected dollar amount of sukuk issuance in 2013?

0.0%

3.6%

14.3%

35.7%

46.4%

0% 10% 20% 30% 40% 50%

Above 40 issues

35 - 40 issues

30 - 35 issues

Under 25 issues

25 - 30 issues

What is the expected number of Eurobond (International USD) sukuk issuance in 2013?

2012 figures are around the $132 bln range.

Are arrangers being too conservative when projecting 2013

issuance levels?

Number of Eurobond issuances in 2012 were 25.

Are arrangers being too conservative when projecting 2013

issuance levels, when pipeline itself is around the 18-20

mark (Source: IFR)?

MOST ARRANGERS EXPECT ISSUANCE VOLUME AROUND THE $75-125 BLN RANGE WITH UP

TO 30 EUROBOND ISSUES

Source: Thomson Reuters Zawya Sukuk Perceptions & Forecast Study 2013

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

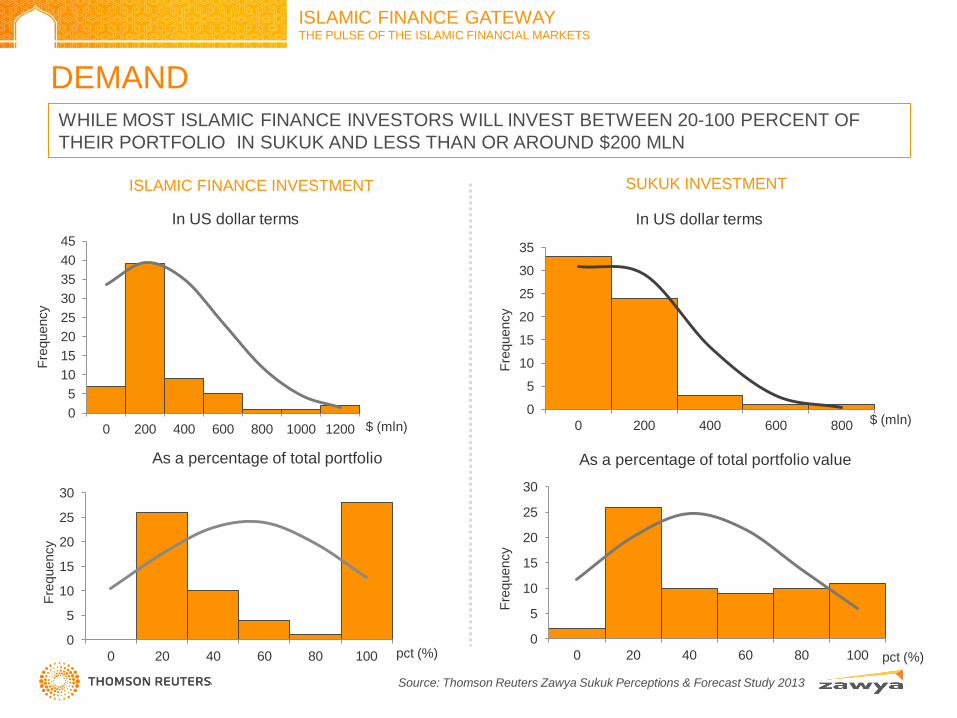

DEMAND

WHILE MOST ISLAMIC FINANCE INVESTORS WILL INVEST BETWEEN 20-100 PERCENT OF

THEIR PORTFOLIO IN SUKUK AND LESS THAN OR AROUND $200 MLN

0

0.0002

0.0004

0.0006

0.0008

0.001

0.0012

0

5

10

15

20

25

30

35

40

45

0 200 400 600 800 1000 1200

Fre

quency

$ (mln)

In US dollar terms

0

0.002

0.004

0.006

0.008

0.01

0.012

0

5

10

15

20

25

30

0 20 40 60 80 100

Fre

quency

pct (%)

As a percentage of total portfolio

ISLAMIC FINANCE INVESTMENT SUKUK INVESTMENT

0

0.0002

0.0004

0.0006

0.0008

0.001

0.0012

0.0014

0.0016

0.0018

0

5

10

15

20

25

30

35

0 200 400 600 800

Fre

quency

$ (mln)

In US dollar terms

0

0.002

0.004

0.006

0.008

0.01

0.012

0.014

0

5

10

15

20

25

30

0 20 40 60 80 100

Fre

quency

pct (%)

As a percentage of total portfolio value

Source: Thomson Reuters Zawya Sukuk Perceptions & Forecast Study 2013

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

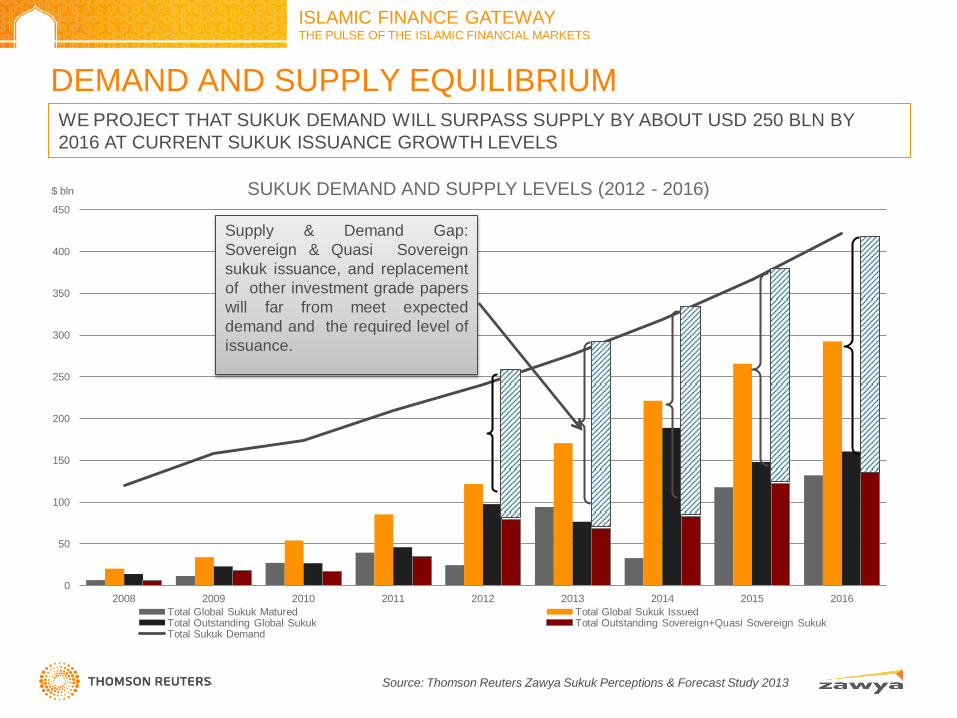

DEMAND AND SUPPLY EQUILIBRIUM

0

50

100

150

200

250

300

350

400

450

2008 2009 2010 2011 2012 2013 2014 2015 2016

$ bln SUKUK DEMAND AND SUPPLY LEVELS (2012 - 2016)

Total Global Sukuk Matured Total Global Sukuk Issued Total Outstanding Global Sukuk Total Outstanding Sovereign+Quasi Sovereign Sukuk Total Sukuk Demand

Supply & Demand Gap:

Sovereign & Quasi Sovereign

sukuk issuance, and replacement

of other investment grade papers

will far from meet expected

demand and the required level of

issuance.

WE PROJECT THAT SUKUK DEMAND WILL SURPASS SUPPLY BY ABOUT USD 250 BLN BY

2016 AT CURRENT SUKUK ISSUANCE GROWTH LEVELS

Source: Thomson Reuters Zawya Sukuk Perceptions & Forecast Study 2013

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

SOME EXAMPLES ….

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

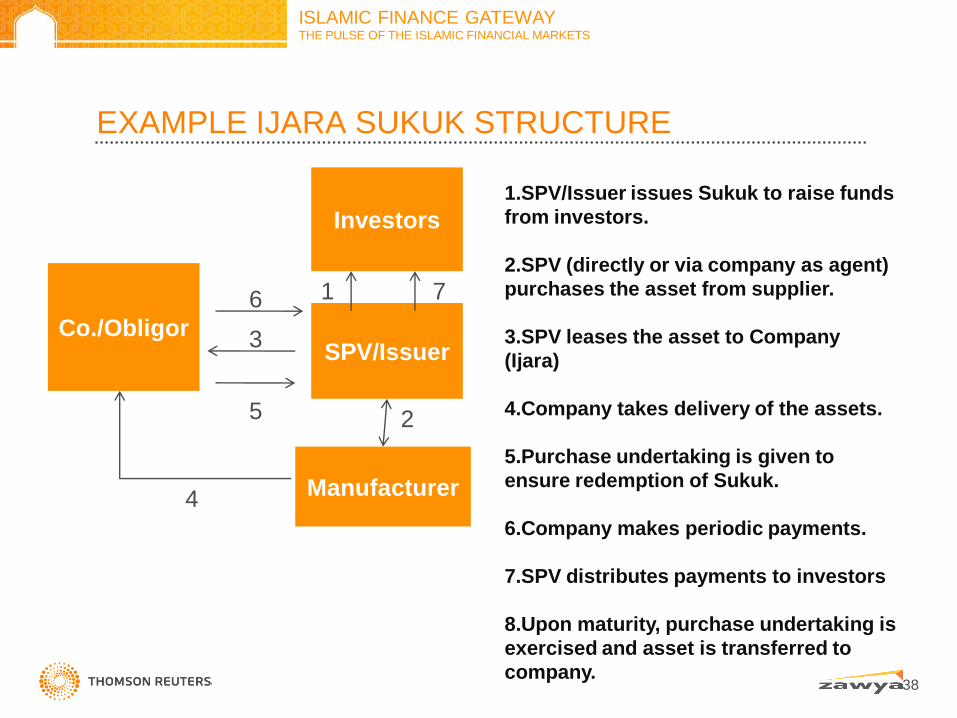

EXAMPLE IJARA SUKUK STRUCTURE

38

Investors

SPV/Issuer

Manufacturer

Co./Obligor

7

5

4

2

3

1 6

1.SPV/Issuer issues Sukuk to raise funds

from investors.

2.SPV (directly or via company as agent)

purchases the asset from supplier.

3.SPV leases the asset to Company

(Ijara)

4.Company takes delivery of the assets.

5.Purchase undertaking is given to

ensure redemption of Sukuk.

6.Company makes periodic payments.

7.SPV distributes payments to investors

8.Upon maturity, purchase undertaking is

exercised and asset is transferred to

company.

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

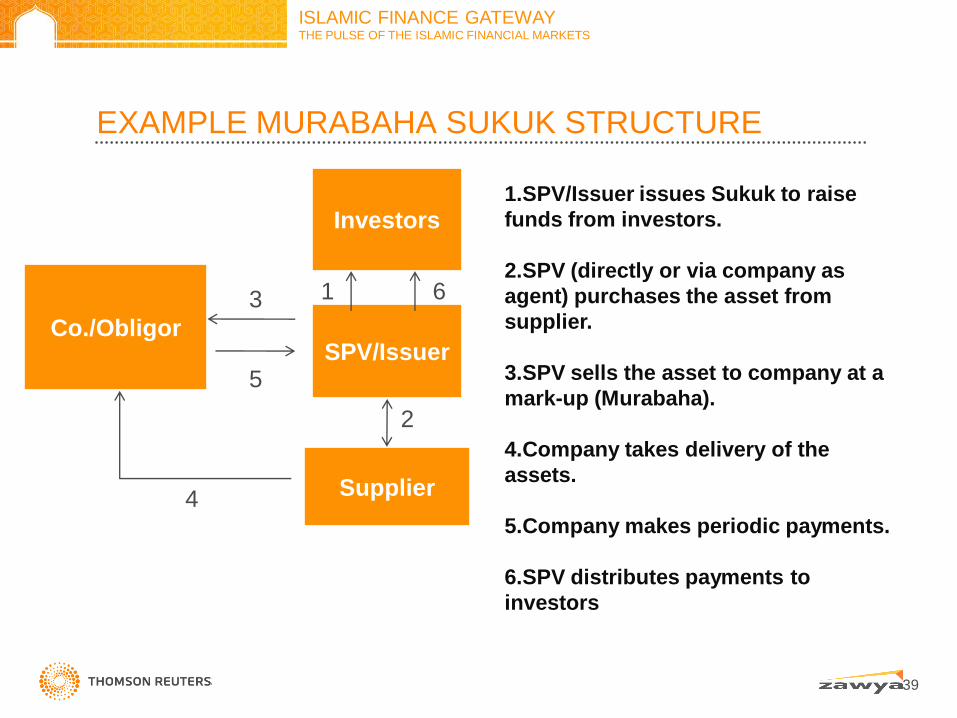

EXAMPLE MURABAHA SUKUK STRUCTURE

39

Investors

SPV/Issuer

Supplier

Co./Obligor

6

5

4

2

3 1

1.SPV/Issuer issues Sukuk to raise

funds from investors.

2.SPV (directly or via company as

agent) purchases the asset from

supplier.

3.SPV sells the asset to company at a

mark-up (Murabaha).

4.Company takes delivery of the

assets.

5.Company makes periodic payments.

6.SPV distributes payments to

investors

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

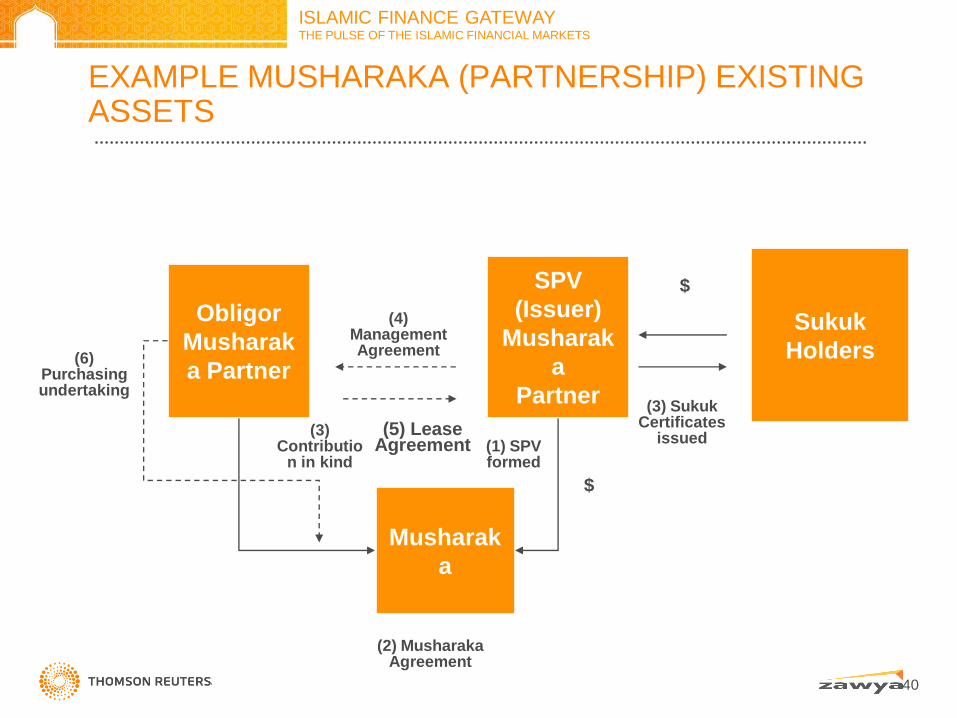

EXAMPLE MUSHARAKA (PARTNERSHIP) EXISTING ASSETS

40

(2) Musharaka Agreement

(4) Management Agreement

(3) Sukuk Certificates

issued

$

Obligor

Musharak

a Partner

SPV

(Issuer)

Musharak

a

Partner

Sukuk

Holders

Musharak

a

(3) Contributio

n in kind

$

(1) SPV formed

(5) Lease Agreement

(6) Purchasing undertaking

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

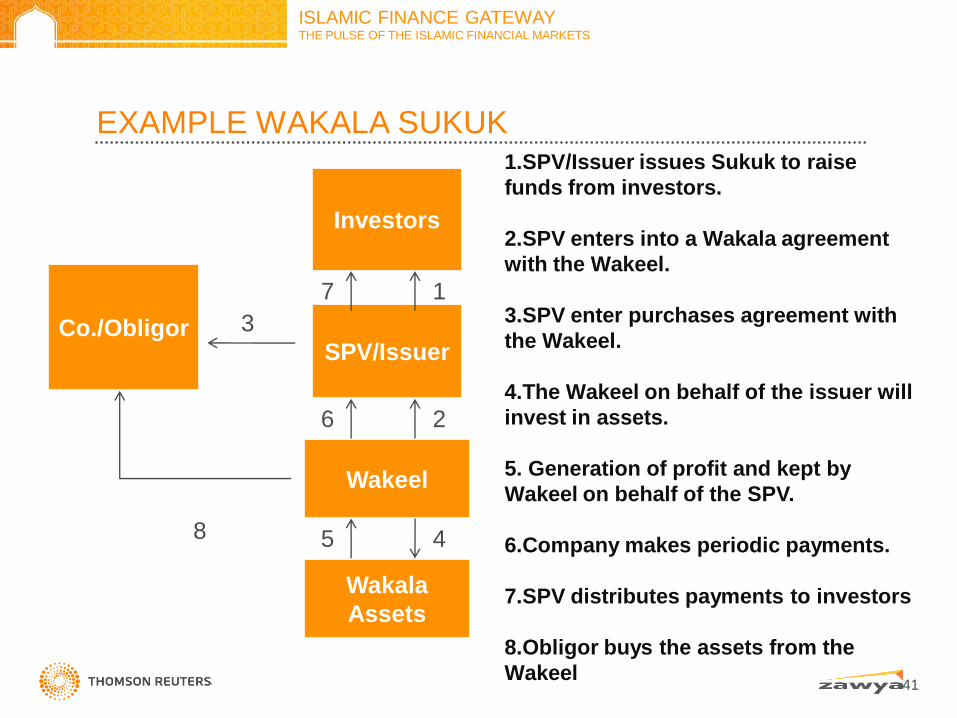

EXAMPLE WAKALA SUKUK

41

Investors

SPV/Issuer

Wakeel

Co./Obligor

7

6

5

2

4

1

1.SPV/Issuer issues Sukuk to raise

funds from investors.

2.SPV enters into a Wakala agreement

with the Wakeel.

3.SPV enter purchases agreement with

the Wakeel.

4.The Wakeel on behalf of the issuer will

invest in assets.

5. Generation of profit and kept by

Wakeel on behalf of the SPV.

6.Company makes periodic payments.

7.SPV distributes payments to investors

8.Obligor buys the assets from the

Wakeel

Wakala

Assets

3

8

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

SUKUK ANALYSIS STRUCTURE…

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

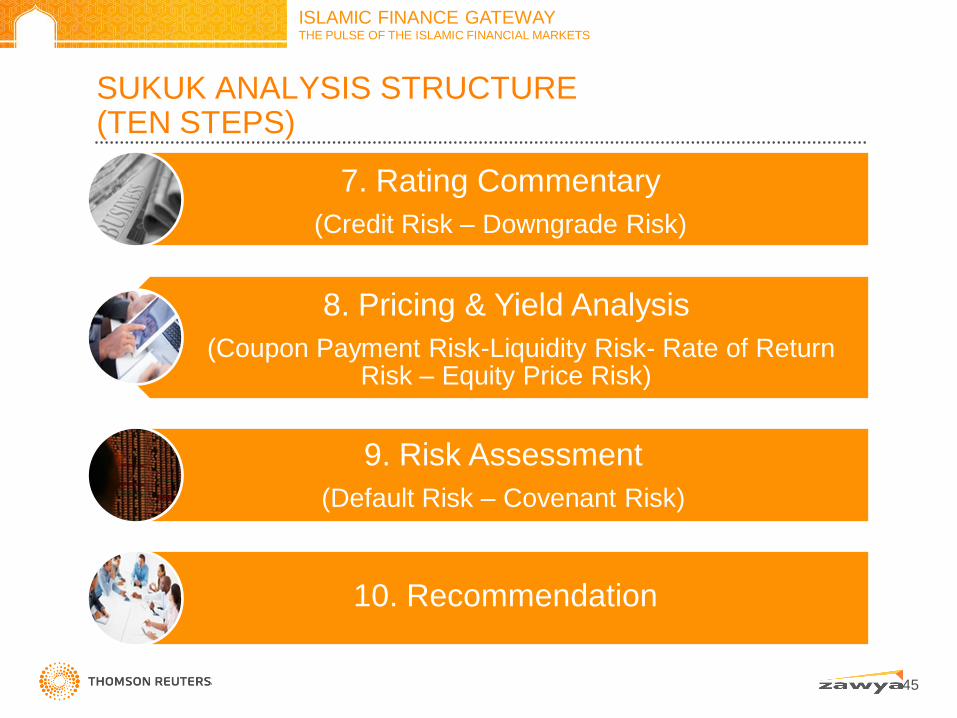

SUKUK ANALYSIS STRUCTURE (TEN STEPS)

43

1. Sukuk Overview

2. Sukuk Issuer Background

(Counterparty Risk – Credit Risk – Operational Risk-Supply Risk)

3. Country Outlook

(Country Risk- systemic Risk-Currency Risk-

Regulation Risk)

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

SUKUK ANALYSIS STRUCTURE (TEN STEPS)

44

4. Industry Outlook

(Regulation Risk – Competitor Risk – Market Risk)

5. Sukuk Structure

(SPV Risk – Asset Quality Risk – Pre-Settlement Risk)

6. Financial Commentary

(Operational Risk – Company Liquidity Risk)

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

SUKUK ANALYSIS STRUCTURE (TEN STEPS)

45

7. Rating Commentary

(Credit Risk – Downgrade Risk)

8. Pricing & Yield Analysis

(Coupon Payment Risk-Liquidity Risk- Rate of Return Risk – Equity Price Risk)

9. Risk Assessment

(Default Risk – Covenant Risk)

10. Recommendation

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

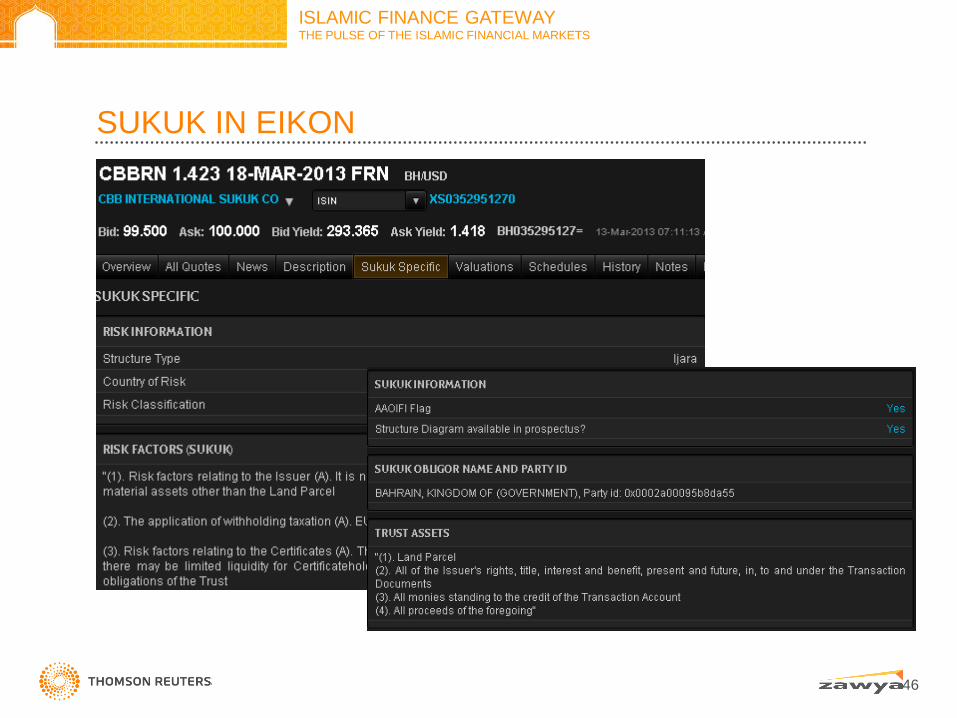

SUKUK IN EIKON

46

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

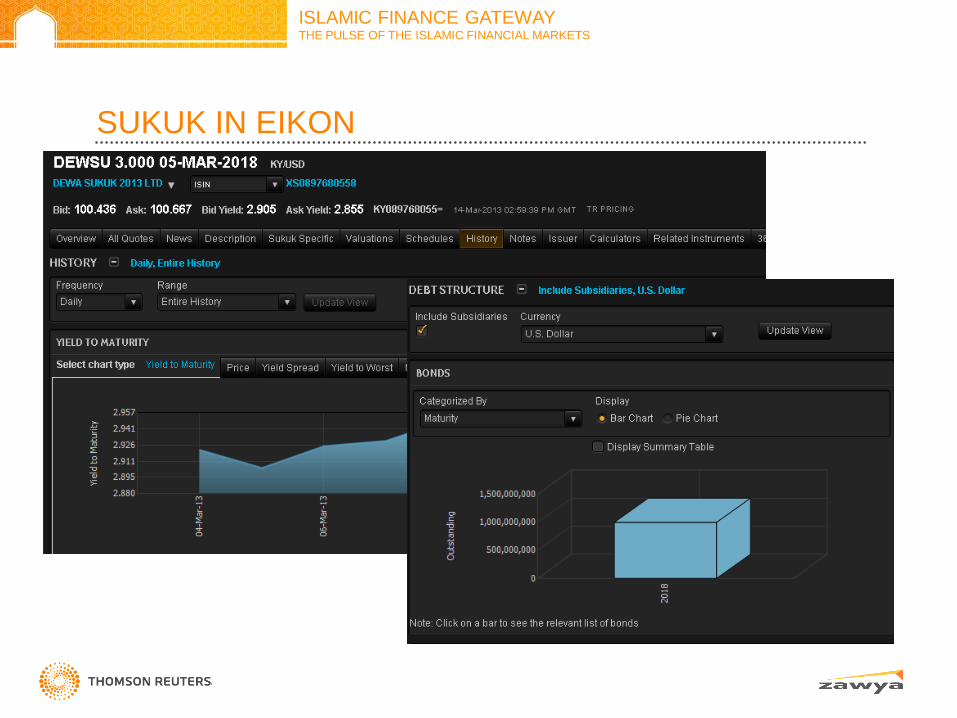

SUKUK IN EIKON

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

JOIN THE IFG COMMUNITY: ONLINE.THOMSONREUTERS.COM/IFG

REACH US: [email protected]

FIND OUT WHAT WE DO: FINANCIAL.THOMSONREUTERS.COM/ISLAMICFINANCE

THE RIGHT INFORMATION IN THE RIGHT HANDS LEADS

TO AMAZING THINGS

ISLAMIC FINANCE GATEWAY THE PULSE OF THE ISLAMIC FINANCIAL MARKETS

THANK YOU

QUESTIONS ?