Embed Size (px)

Citation preview

SCHOOL BOARD MEETINGAGENDA PACKET

FOR

April 11, 2017

THE SCHOOL BOARD OF HENDRY COUNTY,FLORIDA

Jon Basquin District 5Dwayne E. Brown, Vice Chairman District 1Sally Berg District 2Amanda Nelson District 3Stephanie Busin District 4

Paul K. Puletti, Superintendent

The mission of the Hendry County School District is to provide all students the opportunity to achieve at highacademic levels, equipping them to successfully pursue college or career goals.

Hendry County School BoardRegular Meeting

Tuesday, April 11, 20175.30 p.m.

School Board Sub-office, 475 E. Osceola Ave., Clewiston, FL

AGENDA ITEMS

1. CALL TO ORDER

2. INVOCATION AND PLEDGE

3. RECOGNITION - Jesus Almaraz-Argueta, CHS Student - 2016-17 Sunshine State ScholarAlternate

4. CITIZEN COMMENT ON AGENDA ITEMS

5. ITEMS FOR ACTION

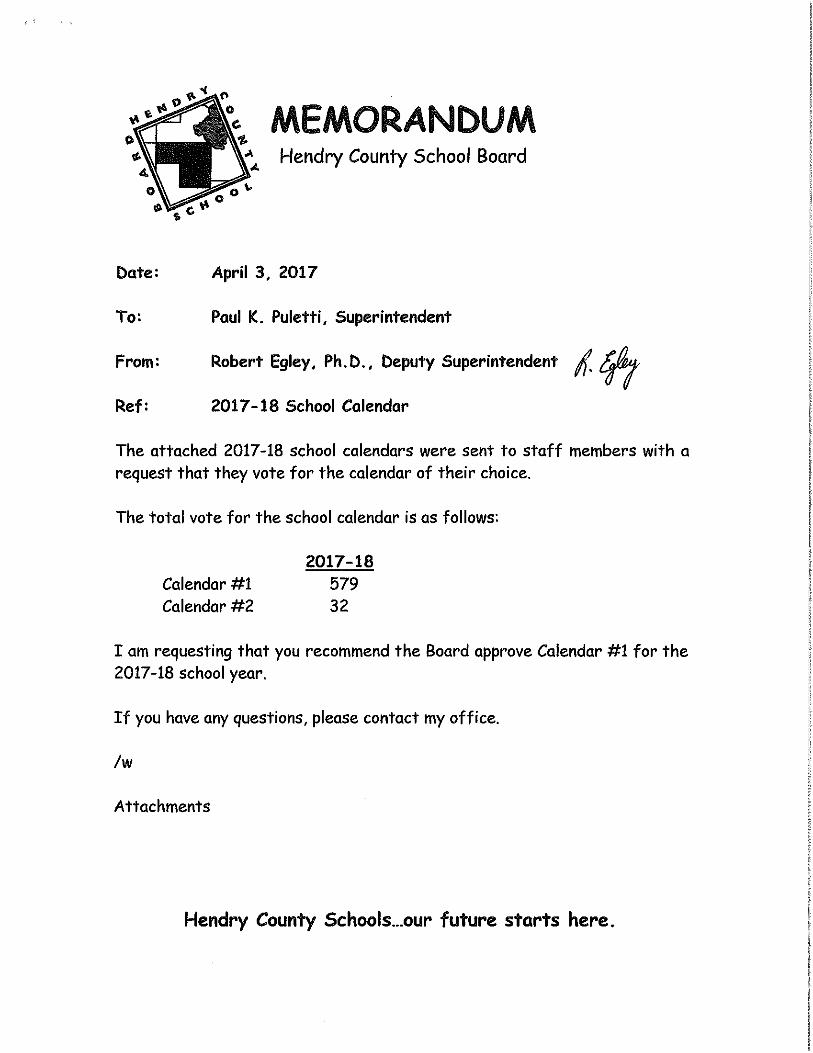

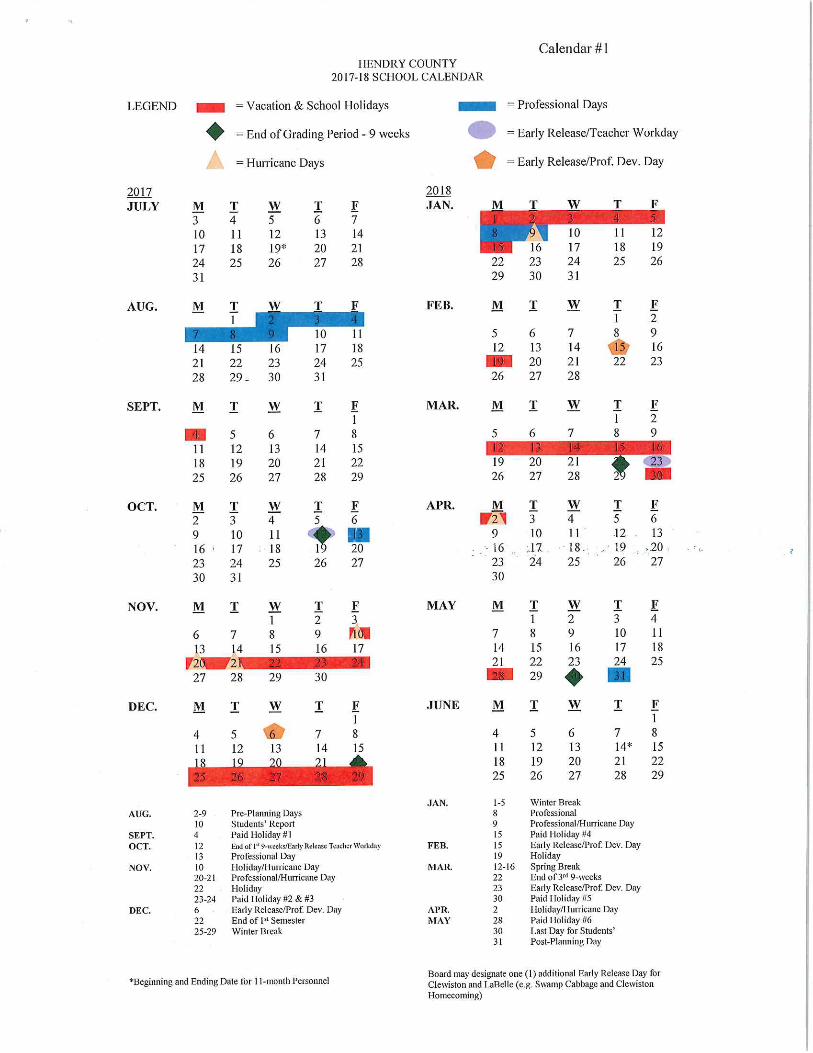

a. 2017-18 School Calendar

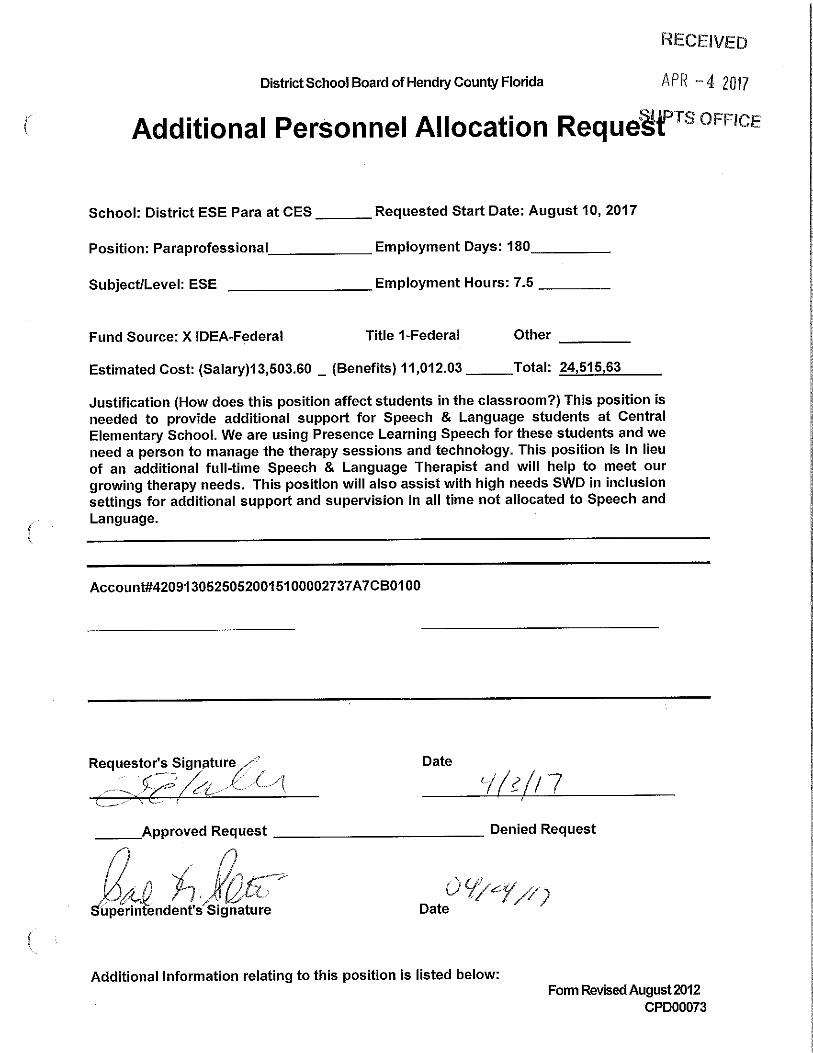

b. New Personnel Allocation Request

6. CONSENT AGENDA

a. Minutes – 3/28/17

b. Agreements –1) Amanda Rutledge - Agreement for Transportation (Aid in lieu) (Revised)2) Sodexo America, LLC - Second Amendment to Proposal Q15-002, Food Service Management

Company

c. Personnel Recommendations

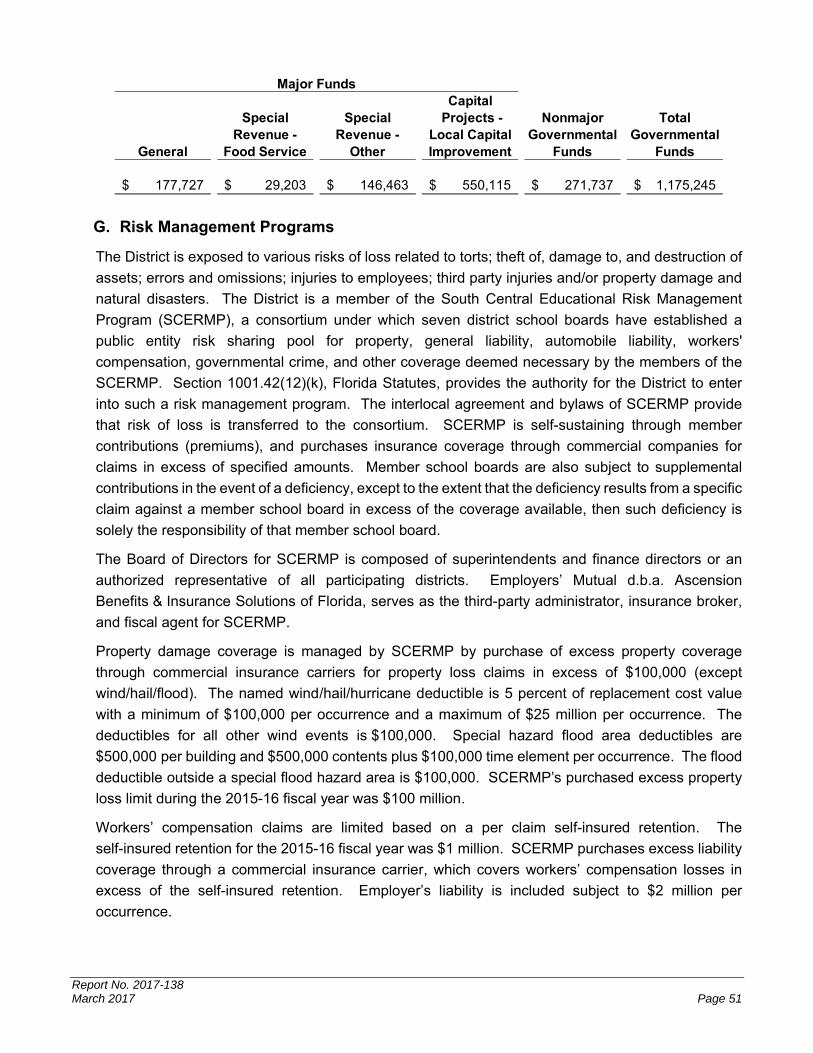

d. Financial Affairs –1) Approval of Purchases2) Bills (4/11/17)3) Internal Account Purchase Request4) Report No. 2017-138 - Hendry County School Board Financial & Federal Single Audit –

FY 6/30/16

7. BOARD MEMBER BUSINESSa. Dues & Feesb. Upcoming Board Meeting/Workshop Location Changes

8. ADJOURNMENT

N O T I C E1. Any person who desires to appeal any decision made by the School Board with respect to any matter considered at the above-noticed meeting will need a record of the proceedings, and for

such purposes may need to ensure that a verbatim record of the proceedings is made, such record includes the testimony and evidence upon which an appeal may be based.

2. This is a formal notification to the public, that written information associated with the meeting is available in alternate formats upon request, i.e., large print, Braille, etc., and auxiliary aids areavailable upon request, i.e., assistive learning device systems, sign language interpreters, etc. All services are available upon a 72 hour advanced notice. Please contact county personnel at 863/902-4244.

RECOGNITION

Jesus Almaraz-Argueta, CHS Student – Selected as the 2016-17 Sunshine StateScholar Alternate

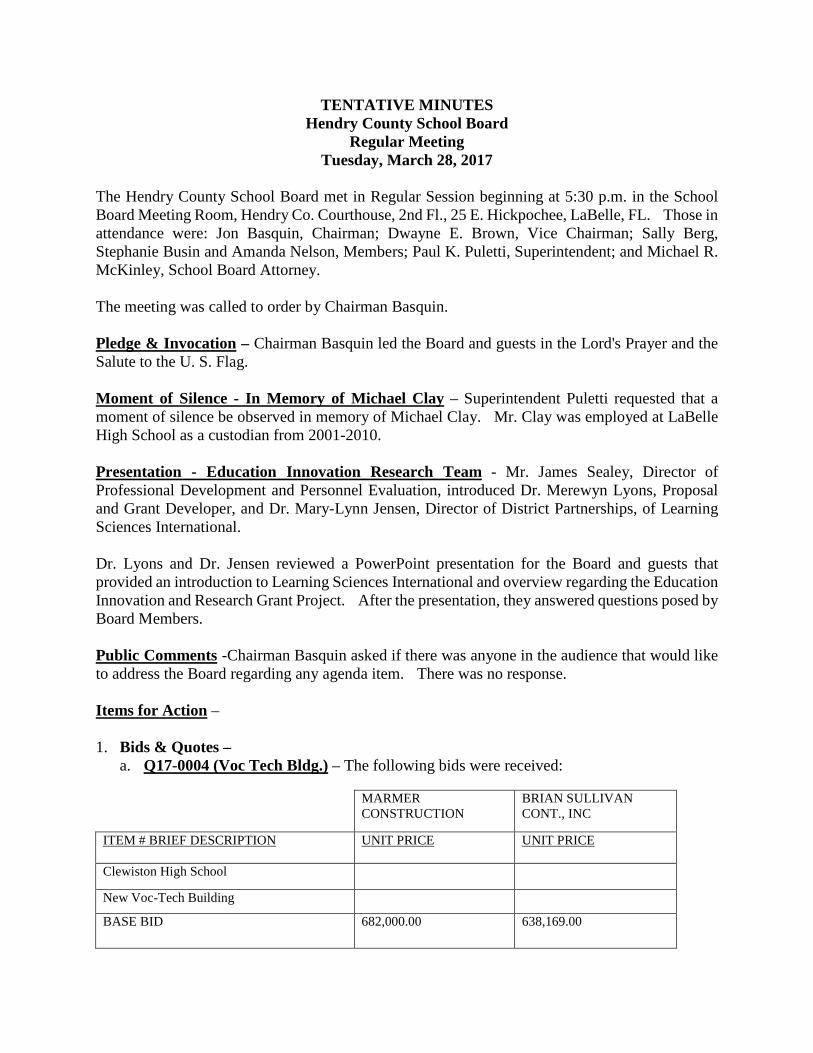

TENTATIVE MINUTESHendry County School Board

Regular MeetingTuesday, March 28, 2017

The Hendry County School Board met in Regular Session beginning at 5:30 p.m. in the SchoolBoard Meeting Room, Hendry Co. Courthouse, 2nd Fl., 25 E. Hickpochee, LaBelle, FL. Those inattendance were: Jon Basquin, Chairman; Dwayne E. Brown, Vice Chairman; Sally Berg,Stephanie Busin and Amanda Nelson, Members; Paul K. Puletti, Superintendent; and Michael R.McKinley, School Board Attorney.

The meeting was called to order by Chairman Basquin.

Pledge & Invocation – Chairman Basquin led the Board and guests in the Lord's Prayer and theSalute to the U. S. Flag.

Moment of Silence - In Memory of Michael Clay – Superintendent Puletti requested that amoment of silence be observed in memory of Michael Clay. Mr. Clay was employed at LaBelleHigh School as a custodian from 2001-2010.

Presentation - Education Innovation Research Team - Mr. James Sealey, Director ofProfessional Development and Personnel Evaluation, introduced Dr. Merewyn Lyons, Proposaland Grant Developer, and Dr. Mary-Lynn Jensen, Director of District Partnerships, of LearningSciences International.

Dr. Lyons and Dr. Jensen reviewed a PowerPoint presentation for the Board and guests thatprovided an introduction to Learning Sciences International and overview regarding the EducationInnovation and Research Grant Project. After the presentation, they answered questions posed byBoard Members.

Public Comments -Chairman Basquin asked if there was anyone in the audience that would liketo address the Board regarding any agenda item. There was no response.

Items for Action –

1. Bids & Quotes –a. Q17-0004 (Voc Tech Bldg.) – The following bids were received:

MARMERCONSTRUCTION

BRIAN SULLIVANCONT., INC

ITEM # BRIEF DESCRIPTION UNIT PRICE UNIT PRICE

Clewiston High School

New Voc-Tech Building

BASE BID 682,000.00 638,169.00

March 28, 2017Page 2

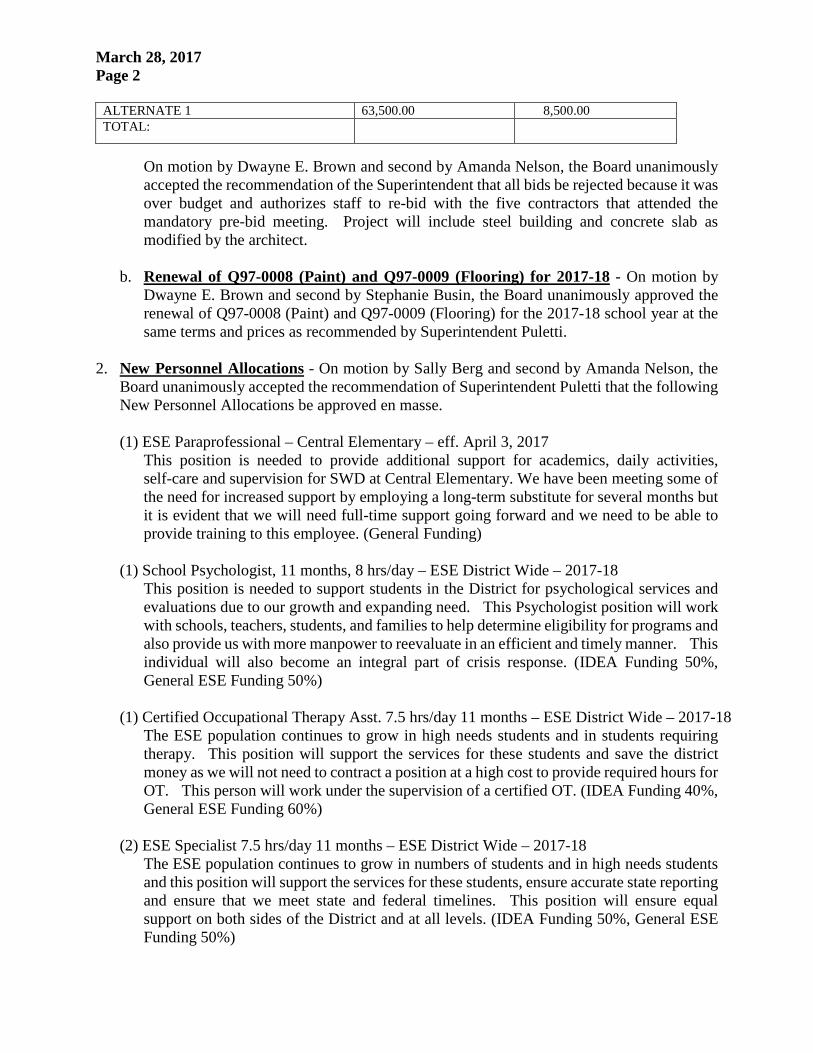

On motion by Dwayne E. Brown and second by Amanda Nelson, the Board unanimouslyaccepted the recommendation of the Superintendent that all bids be rejected because it wasover budget and authorizes staff to re-bid with the five contractors that attended themandatory pre-bid meeting. Project will include steel building and concrete slab asmodified by the architect.

b. Renewal of Q97-0008 (Paint) and Q97-0009 (Flooring) for 2017-18 - On motion byDwayne E. Brown and second by Stephanie Busin, the Board unanimously approved therenewal of Q97-0008 (Paint) and Q97-0009 (Flooring) for the 2017-18 school year at thesame terms and prices as recommended by Superintendent Puletti.

2. New Personnel Allocations - On motion by Sally Berg and second by Amanda Nelson, theBoard unanimously accepted the recommendation of Superintendent Puletti that the followingNew Personnel Allocations be approved en masse.

(1) ESE Paraprofessional – Central Elementary – eff. April 3, 2017This position is needed to provide additional support for academics, daily activities,self-care and supervision for SWD at Central Elementary. We have been meeting some ofthe need for increased support by employing a long-term substitute for several months butit is evident that we will need full-time support going forward and we need to be able toprovide training to this employee. (General Funding)

(1) School Psychologist, 11 months, 8 hrs/day – ESE District Wide – 2017-18This position is needed to support students in the District for psychological services andevaluations due to our growth and expanding need. This Psychologist position will workwith schools, teachers, students, and families to help determine eligibility for programs andalso provide us with more manpower to reevaluate in an efficient and timely manner. Thisindividual will also become an integral part of crisis response. (IDEA Funding 50%,General ESE Funding 50%)

(1) Certified Occupational Therapy Asst. 7.5 hrs/day 11 months – ESE District Wide – 2017-18The ESE population continues to grow in high needs students and in students requiringtherapy. This position will support the services for these students and save the districtmoney as we will not need to contract a position at a high cost to provide required hours forOT. This person will work under the supervision of a certified OT. (IDEA Funding 40%,General ESE Funding 60%)

(2) ESE Specialist 7.5 hrs/day 11 months – ESE District Wide – 2017-18The ESE population continues to grow in numbers of students and in high needs studentsand this position will support the services for these students, ensure accurate state reportingand ensure that we meet state and federal timelines. This position will ensure equalsupport on both sides of the District and at all levels. (IDEA Funding 50%, General ESEFunding 50%)

ALTERNATE 1 63,500.00 8,500.00TOTAL:

March 28, 2017Page 3

(1) VPK Paraprofessional – Montura Site 2017/2018This position will provide teacher and student support for Pre-K in a remote section ofHendry County. This position will allow the district to open a 2nd Pre-K site in Montura.(VPK Funds – Title 1)

(1) VPK Teacher – Montura Site 2017/2018This position will provide quality instruction and will increase access to Pre-K in a remotesection of Hendry County. This position will allow the district to open a 2nd Pre-K site inMontura. (VPK Funds – Title 1)

Consent Agenda - On motion by Dwayne E. Brown and second by Amanda Nelson, the Boardunanimously accepted the recommendation of the Superintendent that the following ConsentAgenda Items be approved en masse.

1. Minutes - 2/14/17 & 2/28/17

2. Agreements & Contracts -a. Presence Learning - Amendment to Master Services Agreement (ESE Dept.)b. Presence Learning - Amendment to Master Services Agreement (ESE Dept.)c. Early Learning Coalition of Southwest Florida - State of Florida Statewide Voluntary

Prekindergarten Provider (2017-18)(Fed. Prog.)d. Victoria Stem - Title 1 Instructional Tutoring Contract (Fed. Prog.)e. Blue Cross and Blue Shield of Florida, Inc. - Accounting & Retention Agreement

3. Hendry County School District Student Acceptable Use Policy (AUP) and TechnologyFee - Removed from Consent Agenda

4. Personnel RecommendationsSuspension with Pay – InstructionalLouisa McLymont – CMS Teacher, eff. 3/9/17

Retirement and Termination of Participation in the FRS Deferred Retirement Option ProgramKathleen Crosby – WES Teacher, eff. 6/1/17 pmHernan Serra – CHS Teacher, eff. 6/1/17 pmFrederick S. Parantha – LES Teacher, eff. 6/1/17 pm

Enrollment for Participation in the FRS Deferred Retirement Option ProgramDebbie Foutch – Media Specialist – UES, eff. 2/1/17Jim Foutch – Teacher – LES, eff. 2/1/17Mary J. Gaskins – Custodian – COES, eff. 2/1/17Bessie Gregory – ESE Paraprofessional – UES, eff. 3/1/17Jovita Williamson – Technology Specialist – IT, eff. 3/1/17

Termination – InstructionalSvetlana Siber – Spch/Lang Pathologist, eff. 3/1/17 (released during probationary period)

March 28, 2017Page 4

Termination – SupportLory J. Ehlers – Food Service Manager, eff. 3/10/17 pm (released during probationary period)

Termination – Non-InstructionalAnna Pereiro – Pre-K Para @ WES eff. 2/16/17 (released during probationary period)

Retirement – InstructionalMegan Greenleaf – LHS Media Specialist, eff. 6/30/17Brent Ringler – LHS Teacher, eff. 6/1/17 pmLynne Pellerin – LHS Teacher, eff. 5/12/17 pmFrederick Parantha – LES Teacher, eff. 6/1/17Joan Basquin – LES Teacher, eff. 6/1/17Steven Hein – LHS Teacher, eff. 6/1/17 pm

Resignation – Instructional -Jessica DuPree – CHS Teacher, eff. 3/17/17Kaleigh Limper – CHS Teacher, eff. 6/1/17 pmJacquelyn Galbraith – CHS Teacher, eff. 6/1/17 pmSaeed Azan – CHS Teacher, eff. 6/1/17 pmTaylor Galarneau – EES Teacher, eff. 6/2/17 pm

Resignation – Non-InstructionalAmber Delorme – LaBelle Van Driver, eff. 2/17/17Rena Bach – LHS, Custodian, eff. 3/24/17Lucille Suchomski – LaBelle Bus Attendant, eff. 3/2/17Samantha Kozinski – EES – Para, eff. 6/2/17 pm

Transfer – Non-InstructionalFaviola Luna – from LMS Clerk Typist to Finance Account Clerk, eff. 4/4/17Ashley Allison – from Finance Account Clerk to Secretary to Deputy Superintendent,

eff. 2/24/17

Change in Designation – AdministrationJohn Klinger – LMS, from Dean to 11 month Assistant Principal, eff. 3/6/17

Change in Designation – InstructionalLaura Lofton – LHS, from Reading Teacher to Media Specialist, eff. 17/18 School Year

Change in Designation – Non-InstructionalTiffany Lara – Clew. Bus Attendant, from 6.25 hrs/day to 4 hrs/day (route time decrease)Jesenia Williams – LaBelle, from full time Van Attendant to full time Van Driver, eff. 3/6/17Idelsis Villatoro – Clew. Bus Attendant, from 6.25 hrs/day to 5.5 hrs/day, eff. 3/6/17

Leave of Absence – InstructionalMelinda Krause – WES Teacher, eff. 2/17/17 through 4/4/17 (Maternity)

March 28, 2017Page 5

Marc Waddell – CHS – Teacher, extended Medical Leave, eff. 5/31/2016 through 6/1/2017(Medical)

Leave of Absence – Non-InstructionalMaria Dominguez – School Nurse – Maternity Leave eff. 12/15/16 through 3/1/17

(requesting Family Medical Leave)Jessica Langs – Clew. Bus Driver – Extension of Maternity Leave eff. 2/27/17 through

3/17/17

Appointment – InstructionalDenisesha Thorpe – WES Pre-K Teacher, eff. 2/21/17

Appointment - Non-InstructionalSkylar Bell – COES ESE Para, eff. 2/13/17 (New Allocation)Krishendath Dookram – LMS Custodian, eff. 2/21/17Victoria Ortiz – WES ESE Pre-K Para, eff. 2/27/17Daion Banks – WES Custodian, eff. 3/20/17Jimesha Smith – WES ESE Pre-K Para, eff. 2/27/17Nathan Snow – LHS Custodian, eff. 3/27/17Ashley Campbell – COES – ESE Para, eff. 2/27/17

Appointment Teacher Temporary Part time for Deaf HHDeborah Finley – ESE – eff. 2/6/17 through 6/30/17

Appointment Substitute Bus DriversTonya Whitehead - eff. 2/23/17Ronnie Rawls – eff. 3/20/17Ronnie Rawls – Trainee, eff. 1/23/17Lydia Maldonado - eff. 3/22/17

Additional days/hoursMeloni Timgren - 31.5 hrs. for driving/after schoolMark Duda - ESE Attendant for After School Program eff. 2/7/17Rene Ibarra – LaBelle Trans. – 6.5 hrs. due to bus driver shortage, eff. PR 19

Supplements 2016/2017Michael Willis – ADD – Football Spring Training, Asst. Coach, 90% - CHSManny Gomez – ADD – Football Spring Training, Head Coach, 10% and Asst. Coach, 10%

each - CHSCharles Roth – ADD – Baseball JV, Asst. Coach – CHSSteve Barnes – DELETE – Baseball JV, Asst. Coach – CHSChris Barraza – ADD – Softball, Head Coach – CHSSamantha Ortiz – DELETE – Softball, Head Coach – CHSManny Gomez – ADD – Softball, Asst. Coach – CHSChris Barraza – DELETE – Softball, Asst. Coach – CHSJenine Hannam – ADD – Softball, Asst. JV Coach – CHS

March 28, 2017Page 6

Melissa Padilla – DELETE – Softball, Asst. JV Coach – CHSNora Ramirez – ADD – Sunshine Club – CHSJoaquin Barbara Llanes – ADD – Tennis, Head Coach – CHSCurtis Midget – ADD – Track, Head Coach Boys and Girls (10% each), Track Asst. Coach

Boys and Girls (10% each) - CHSBrad Garrett – CHANGE – Track, Head Coach, from 100% to 90% - CHSMichael Willis – CHANGE – Track, Asst. Coach, from 100% to 90% - CHSZach Threlkeld – CHANGE – Track, Head Coach, from 100% to 90% - CHSWill Davis – CHANGE – Track, Asst. Coach, from 100% to 90% - CHSTiffany Groves – DELETE – Beta Club, 50% - CHSIan Stone – ADD – Beta Club, 50 % - CHSSteve Barnes – DELETE – Football Spring Training, 90% -CHSDiana Weiss – DELETE – Sunshine Club – CHS

Summer Boot Camp – LHS/CHS 2017Dustin LedfordDavid LeeDavid TippettJoaquin Barbara-Llanes

Writing Boot Camp - SAI Fund – EES, eff. 2/25/17Amanda Howard Ivette PorthMaggie Pennington Tammy MitchellDanielle Dasher Catisia WilliamsKristin Mann

Summer School –CHS- 2017Steven BarnesTameka WebberBrent JohnsonWillie Lee

Summer Driver’s Ed –LHS/CHS 2017Ronald DunbarDave BlakeMichael WillisRyan Petersmark

Science After School – SAI Funding – EES eff. 3/2/17Ivette Porth Danielle DasherCatisia Williams Caitlyn SayersKaren Richardson

4th Grade After School Program - SAI Funds – COES eff. 3/27/17 to 4/27/17Kimberly StittHeidi Dana

March 28, 2017Page 7

Reading Endorsement Bonus (Title II Funds)Blanca Aguirre – COES

After School Tutorial Reading – LHS – SAI FundJohnathan WilliamsChristel Williams

Best and Brightest Teacher Scholarship Program 16-17Kristina Andrews Daphne Arreola Susan BonnoyerEricka Burke Alexandria Collins Kevin FarmerDenise Gibson Megan Greenleaf Tiffany GrovesJessica Hendricks-Pickles Lauren Kinard Taylor LucasJulie McGirt Catherine McVay Ivette PorthRebecca Pratt Magdalene Solomonides Laurie Steinke

HCSB Approval for ECET2 Professional DevelopmentJason AdamsTammy BassJose RoquettTina Wills

5. Correspondence & Reports -a. Donations

1) $50.00 from Liolia Olvera and Gustavo Castro to LaBelle Elementary School to beused for student field trips.

6. Financial Affairs –a. Approval of Purchases

1) 1712616, MCM Paint & Flooring, Clewiston, FL in the amount of $75,000.00 forpainting and flooring district wide.

2) 1712622, Center for Educational Leadership, Seattle, WA in the amount of $62,675.00for Consultant fees for orientation for studio and resident teachers and ILTwalkthroughs and virtual support.

3) 1712642, Learning Sciences International, Blairsville, PA in the amount of $22,000.00for Marzano leadership training.

4) 1712660, Franklin Covey Client Sales, Inc., Salt Lake City, UT in the amount of$22,961.54 for consultation fees and 7 habits signature participant kit and an annualmembership.

5) 1712724, MCM Paint & Flooring, Clewiston, FL in the amount of $47,497.00 forpainting and flooring district wide.

6) 1712891, Howard Technology Solutions, Laurel, MS in the amount of $21,840.00 for84 Chromebook Celerons, 84 White glove services, 84 Console, 84 Belkin mouse, 84headphones and 84 one year warranties.

7) 1712895, Howard Technology Solutions, Laurel, MS in the amount of $37,008.00 for144 ASUS Chromebook Celerons, 144 White Glove services, 144 Google Chrome OS

March 28, 2017Page 8

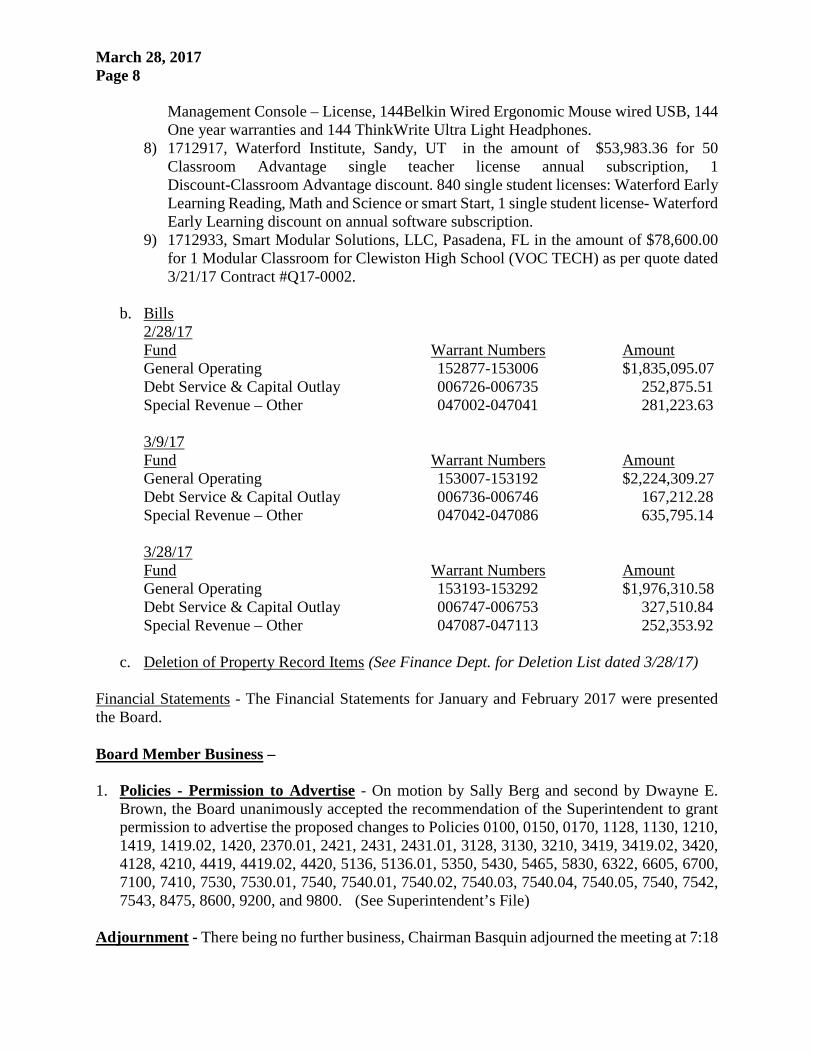

Management Console – License, 144Belkin Wired Ergonomic Mouse wired USB, 144One year warranties and 144 ThinkWrite Ultra Light Headphones.

8) 1712917, Waterford Institute, Sandy, UT in the amount of $53,983.36 for 50Classroom Advantage single teacher license annual subscription, 1Discount-Classroom Advantage discount. 840 single student licenses: Waterford EarlyLearning Reading, Math and Science or smart Start, 1 single student license- WaterfordEarly Learning discount on annual software subscription.

9) 1712933, Smart Modular Solutions, LLC, Pasadena, FL in the amount of $78,600.00for 1 Modular Classroom for Clewiston High School (VOC TECH) as per quote dated3/21/17 Contract #Q17-0002.

b. Bills2/28/17Fund Warrant Numbers AmountGeneral Operating 152877-153006 $1,835,095.07Debt Service & Capital Outlay 006726-006735 252,875.51Special Revenue – Other 047002-047041 281,223.63

3/9/17Fund Warrant Numbers AmountGeneral Operating 153007-153192 $2,224,309.27Debt Service & Capital Outlay 006736-006746 167,212.28Special Revenue – Other 047042-047086 635,795.14

3/28/17Fund Warrant Numbers AmountGeneral Operating 153193-153292 $1,976,310.58Debt Service & Capital Outlay 006747-006753 327,510.84Special Revenue – Other 047087-047113 252,353.92

c. Deletion of Property Record Items (See Finance Dept. for Deletion List dated 3/28/17)

Financial Statements - The Financial Statements for January and February 2017 were presentedthe Board.

Board Member Business –

1. Policies - Permission to Advertise - On motion by Sally Berg and second by Dwayne E.Brown, the Board unanimously accepted the recommendation of the Superintendent to grantpermission to advertise the proposed changes to Policies 0100, 0150, 0170, 1128, 1130, 1210,1419, 1419.02, 1420, 2370.01, 2421, 2431, 2431.01, 3128, 3130, 3210, 3419, 3419.02, 3420,4128, 4210, 4419, 4419.02, 4420, 5136, 5136.01, 5350, 5430, 5465, 5830, 6322, 6605, 6700,7100, 7410, 7530, 7530.01, 7540, 7540.01, 7540.02, 7540.03, 7540.04, 7540.05, 7540, 7542,7543, 8475, 8600, 9200, and 9800. (See Superintendent’s File)

Adjournment - There being no further business, Chairman Basquin adjourned the meeting at 7:18

March 28, 2017Page 9

p.m.

________________________________ _____________________________Paul K. Puletti, Superintendent Jon Basquinand Secretary to the Board Chairman of the Board

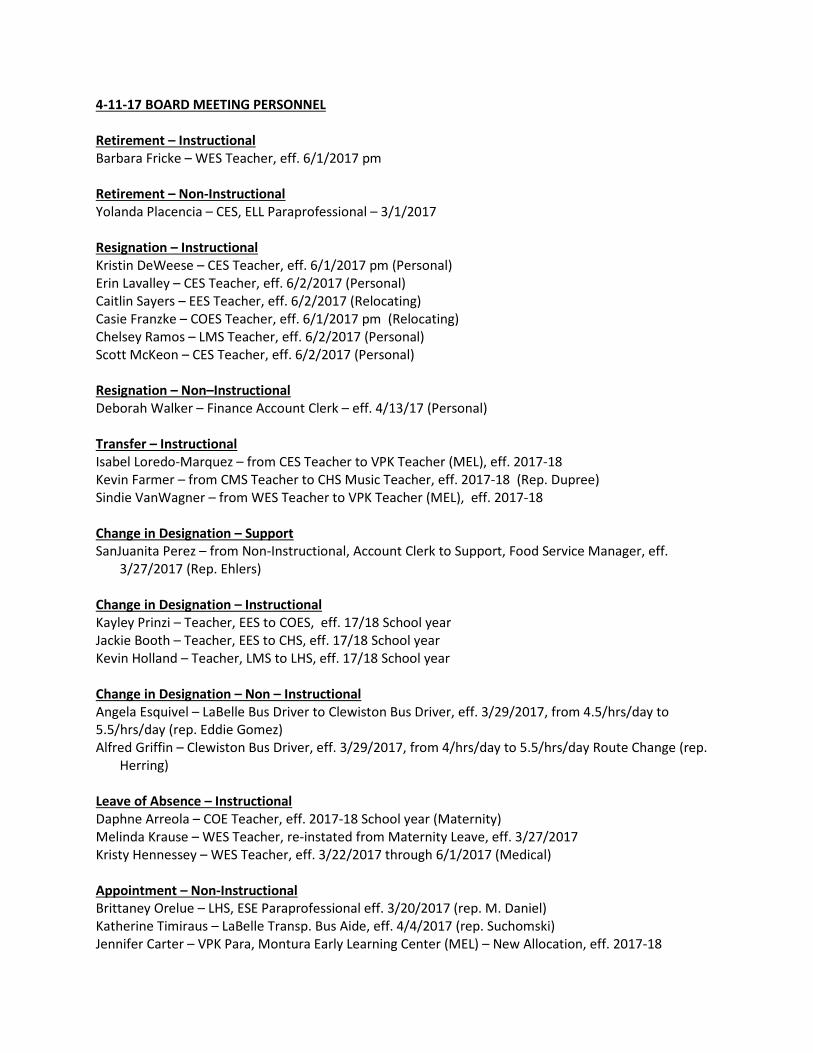

4-11-17 BOARD MEETING PERSONNEL

Retirement – InstructionalBarbara Fricke – WES Teacher, eff. 6/1/2017 pm

Retirement – Non-InstructionalYolanda Placencia – CES, ELL Paraprofessional – 3/1/2017

Resignation – InstructionalKristin DeWeese – CES Teacher, eff. 6/1/2017 pm (Personal)Erin Lavalley – CES Teacher, eff. 6/2/2017 (Personal)Caitlin Sayers – EES Teacher, eff. 6/2/2017 (Relocating)Casie Franzke – COES Teacher, eff. 6/1/2017 pm (Relocating)Chelsey Ramos – LMS Teacher, eff. 6/2/2017 (Personal)Scott McKeon – CES Teacher, eff. 6/2/2017 (Personal)

Resignation – Non–InstructionalDeborah Walker – Finance Account Clerk – eff. 4/13/17 (Personal)

Transfer – InstructionalIsabel Loredo-Marquez – from CES Teacher to VPK Teacher (MEL), eff. 2017-18Kevin Farmer – from CMS Teacher to CHS Music Teacher, eff. 2017-18 (Rep. Dupree)Sindie VanWagner – from WES Teacher to VPK Teacher (MEL), eff. 2017-18

Change in Designation – SupportSanJuanita Perez – from Non-Instructional, Account Clerk to Support, Food Service Manager, eff.

3/27/2017 (Rep. Ehlers)

Change in Designation – InstructionalKayley Prinzi – Teacher, EES to COES, eff. 17/18 School yearJackie Booth – Teacher, EES to CHS, eff. 17/18 School yearKevin Holland – Teacher, LMS to LHS, eff. 17/18 School year

Change in Designation – Non – InstructionalAngela Esquivel – LaBelle Bus Driver to Clewiston Bus Driver, eff. 3/29/2017, from 4.5/hrs/day to5.5/hrs/day (rep. Eddie Gomez)Alfred Griffin – Clewiston Bus Driver, eff. 3/29/2017, from 4/hrs/day to 5.5/hrs/day Route Change (rep.

Herring)

Leave of Absence – InstructionalDaphne Arreola – COE Teacher, eff. 2017-18 School year (Maternity)Melinda Krause – WES Teacher, re-instated from Maternity Leave, eff. 3/27/2017Kristy Hennessey – WES Teacher, eff. 3/22/2017 through 6/1/2017 (Medical)

Appointment – Non-InstructionalBrittaney Orelue – LHS, ESE Paraprofessional eff. 3/20/2017 (rep. M. Daniel)Katherine Timiraus – LaBelle Transp. Bus Aide, eff. 4/4/2017 (rep. Suchomski)Jennifer Carter – VPK Para, Montura Early Learning Center (MEL) – New Allocation, eff. 2017-18

4-11-17 BOARD MEETING PERSONNEL – Page 2

Juliette Cruz – VPK Para, MEL – New Allocation, eff. 2017-18Gabriela Salazar Sanchez – VPK Para, MEL – New Allocation, eff. 2017-18

Appointment – Hospital/Homebound 2016-17Mercedes NunezJacob Walk

Appointment - Substitute Van Driver/Van Attendant/Bus AttendantSandra Cabrera – eff. 4/3/2017Cynthia Biggs – eff. 3/6/2017 (Sub Van/Bus Attendant)

Additional days/hoursRene Ibarra – 6.5 hours driving/bus repair, PR#20Meloni Timgren – 30.25 hours driving/After school, PR#18Melissa Luna – 1.25 hours – for Parent Teacher Conferences, eff. 2/16/2017Cruz Martinez – 1.25 hours – for Parent Teacher Conferences, eff. 2/16/2017Nona Timmons – Bus Driver – LaBelle Migrant Homeless After-School Program, eff. 3/24/2017Deanna Cherry – Bus Driver – Part-time mower, eff. 4/4/2017

Supplements 2016/2017Kevin Farmer – ADD – Band Director, CHSTy Marshall – CHANGE – Baseball, Asst. Coach, from 100% to 25% - LHSRicky Bass – ADD – Baseball, Asst. Coach, 75% - LHSBrent Burnside – ADD – Football Spring Training, Asst. Coach, 50% - LHSCudjoe London – DELETE – Football Spring Training, Asst. Coach - LHS

3rd Grade After-School Program – SAI Funds – COES – Extended through 3/27/17Nicole KusnierzCarrie McKinleyHanna Officer

Avid Tutors – SAI Funds – CHS- eff. 3/30/17Marizel PerezLiliaesther Delgado Lopez

SLP Technology Para Sub – CES – eff. 3/20/17Renee Martin

Professional Development Stipend for SIM Training 2016 – LHS/LMSEusyher Mendoza Taynika ArtacheJoy Bridwell Laura LoftonStuart Friesen Sara ChildersAnn Daniel Alana AndersonCarole Schroeder Haili MarottiJoel Reinking Ashley CorbittLea Burnside Jimmy Norman

4-11-17 BOARD MEETING PERSONNEL- Page 3

Summer School – LHS – 2017Claude Cadet Kristina AndrewsHeidi Lederer Maria Nancy Rodriguez

Math Tutoring – SAI Funds – LMS eff. 3/21/2017Tracie Smith-Murphy Natalia RoseBret Mayo Douglas KnittFaye Reed Veronica Gil

Civics Tutoring Services – SAI Funds - LMS eff. 3/27/2017Ashley CorbittJoel Reinking

Science Boot Camp – SAI Funds – eff. 4/29/2017Maranda Berner Stefanie CurtisKristin DeWeese Meredith KaneSofia Kirstein Claudia LozanoJalyce Morris

Math Boot Camp – SAI Funds – eff. 4/22/2017Alice Bradberry Jessica Cirino-Lan Stefanie CurtisKristin DeWeese Sofia Kirstein Claudia LozanoJalyce Morris Mark vanTol

Summer School – Federal Programs – eff. 06/05/2017Kris Cottrell Sandra Van Wagner Rebecca Caudill LozanoPamela R. Cooper Shannon Angel Jacqueline MorenoBlanca Aguirre Kristen Walker Crystal RobbinsAngela St. John Debbie Foutch Michael MillerSydney Thacker Elvira Garcia-Rodriguez Kim StittStella Luckey Susan Smith Rachel KirklandNicole Kusnierz Theresa Barber Cathy CharneskiWendy O’Ferrell Melanie Holt Kevin LutkenhausRuss Bell Jose Marquez Joel ReinkingBlanca Gongora Chelsa Skipper Laura LoftonDustin Ledford Reyna Garza Margie PulettiIngrid Gutierrez Kathleen Crawford Maggie PenningtonAdam Pennington Kristin Mann Amanda Howard (EES)Shawn Grooms Yesenia Zamora Catisia WilliamsLillian Ramos Sherry Irey Danielle DasherRushie Osby Susana Kettler Maranda BernerDeborah Panton April White Danielle JeanSamuel Thomas Vermell White Kevin FarmerGlenna Shelnut Samantha Ortiz Melissa LunaMarion Willis Richard Talada Tamarra ParrishFlora Talada Hope Escobar George Wedeles

4-11-17 BOARD MEETING PERSONNEL- Page 4

Linda Butler-Mosley Tracy Owens Irma AlanizJanet Hamilton Chasity Poling Isabelle LoredoCindie Van Wagner Judy Morales Lil MendozaErlinda Brown Odalys Burke Nora GarciaMargarita Pruitt Patty Sutton Adriana SotoGracie Garcia Rosa Perez

FINANCIAL AFFAIRS

1) Approval of Purchases (See Attached)

2) Bills (4/11/17) (See Attached)

3) Internal Account Purchase Order (See Attached)

a) EES – Universal Studios, Orlando, FL in the amount of $10,576.00 foradmission/dining cards for 5th grade field trip.

4) Report No. 2017-138 – Hendry County School Board Financial & Federal Single Audit –FY Ended 6/30/16 (See Attached)

BOARD MEETINGApril 11, 2017

2016/2017Purchase Orders

FINANCIAL AFFAIRS-

1. 1712990, Curriculum Associates, North Billerica, MA in the amount of $232,060.00for I-Ready Diagnostic Math and Reading per student license for 8 sites. I-Ready Mathand Reading for K-8 Teacher Toolbox for I-Ready site license for 8 sites. I-Ready Mathand Reading for K-8 for site license for 8 sites. I-Ready Diagnostic and Instruction Prof.Dev. On site practicing with add on leadership sessions. (Federal)

2. 1713031, AVID Center, San Diego, CA in the amount of $17,272.00 for one AVIDweekly subscription for CHS for 2017-18. One AVID membership fees for CHS for2017-18. One AVID weekly subscription for CMS for 2017-18. One AVID membershipfee for CMS for 2017-18. One AVID weekly subscription for LHS for 2017-18. OneAVID membership for LHS for 2017-18. One AVID weekly subscription for LMS for2017-18. One AVID membership fee for LMS for 2017-18.(General)

3. 1713104, CenturyLink, e/mail, LA in the amount of $25,000.00 for Smartnet Support.(General)

CURRICULUM ASSOCIATES 1712990P.O. Box 2001North Billerica, MA 01862-0901

03/29/17420-9141-5-000-5100-6920-000-2127B-7CB01-00420-9141-5-000-6400-3100-000-2127B-7CB01-00

1 I-Ready Diagnostic Math and Reading per student 58,243.00 58,243.00License – 1 Year – 8 sites1 I-Ready Math and Reading K-8 Teacher Toolbox 90,147.00 90,147.00For I-Ready Site License – 1 Year – 8 sites1 I-Ready Math and Reading K-8 Teacher Toolbox 59,670.00 59,670.00For I-Ready Site License – 1Year – 8 Sites1 I-Ready Diagnostic and Instruction Prof. Dev. On Site 24,000.00 24,000.00Practicing (1) and Advanced (7) User Packages. (Allsessions up to 6 hrs.) with Add on Leadership Session (Upto 3 hours)LABELLE MIGRANT - HENDRY COUNTY SCHOOL $****232,060.00

AVID CENTER 17130319246 Lightwave Ave., Suite 200San Diego, CA 92123

04/03/17100-9105-5-000-5100-6920-000-00000-17075-00100-9105-5-000-5100-3100-000-00000-17075-00

1 AVID Weekly Subscription for Clewiston High School 519.00 519.00for 2017-181 AVID Membership Fees Clewiston High School for 3,799.00 3,799.002017-181 AVID Weekly Subscription for Clewiston Middle School 519.00 519.00for 2017-181 AVID Membership fees for Clewiston Middle School 3,799.00 3,799.00for 2017-181 AVID Weekly Subscription for LaBelle High School 519.00 519.00for 2017-181 AVID Membership fees for LaBelle High School for 3,799.00 3,799.002017-181 AVID Weekly Subscription for LaBelle Middle School 519.00 519.00for 2017-181 AVID Membership fees for LaBelle Middle School 3,799.00 3,799.00for 2017-18INSTRUCTION – HENDRY COUNTY SCHOOLS $****17,272.00

CENTURYLINKAcct. Executive/Ed Spece/mail: After Ord., LA 71211-4786

04/06/17100-9350-5-000-8200-3100-000-00000-00000-00

1 Smartnet Support 25,000.00 25,000.00INFORMATION TECHNOLOGY-HENDRY CO. SCHOOLS $****25,000.00

APRIL 11, 2017

FUND BEG. ENDINGCHECK CHECKNUMBER NUMBER AMOUNT

I GENERAL OPERATING 153293 - 153456 $2,033,899.47

II & III DEBT SERV. & CAPT. OUT 6754 - 6764 $ 290,179.22

IV SPECIAL REV. – OTHER 047114 - 047167 $ 280,066.40

TOTAL: $2,604,145.09

Sherrill F. Norman, CPA

Auditor General

Report No. 2017-138

March 2017

HENDRY COUNTY

DISTRICT SCHOOL BOARD

For the Fiscal Year Ended

June 30, 2016

Finan

cial and Fed

eral Single Audit

The Auditor General conducts audits of governmental entities to provide the Legislature, Florida’s citizens, public entity

management, and other stakeholders unbiased, timely, and relevant information for use in promoting government

accountability and stewardship and improving government operations.

The team leader was Cesar A. Mayorga and the audit was supervised by Deirdre F. Waigand, CPA.

Please address inquiries regarding this report to Micah E. Rodgers, CPA, Audit Supervisor, by e-mail at

[email protected] or by telephone at (850) 412-2905.

This report and other reports prepared by the Auditor General are available at:

www.myflorida.com/audgen

Printed copies of our reports may be requested by contacting us at:

State of Florida Auditor General

Claude Pepper Building, Suite G74 ∙ 111 West Madison Street ∙ Tallahassee, FL 32399-1450 ∙ (850) 412-2722

Board Members and Superintendent

During the 2015-16 fiscal year, Paul K. Puletti served as Superintendent of the Hendry County

Schools and the following individuals served as School Board Members:

District No. Dwayne E. Brown, Chair to 11-16-15 1 Dr. Sally Berg, Chair from 11-17-15, Vice Chair to 11-16-15

2

John Benkert 3 Stephanie Busin 4 Jon Basquin, Vice Chair from 11-17-15 5

HENDRY COUNTY DISTRICT SCHOOL BOARD

TABLE OF CONTENTS

Page No.

SUMMARY ........................................................................................................................................ i

INDEPENDENT AUDITOR’S REPORT

Report on the Financial Statements .............................................................................................. 1

Other Reporting Required by Government Auditing Standards .................................................... 3

MANAGEMENT’S DISCUSSION AND ANALYSIS ........................................................................... 4

BASIC FINANCIAL STATEMENTS

Statement of Net Position ............................................................................................................. 13

Statement of Activities ................................................................................................................... 14

Balance Sheet – Governmental Funds ......................................................................................... 16

Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Position .................................................................................................. 18

Statement of Revenues, Expenditures, and Changes in Fund Balances – Governmental Funds ....................................................................................... 20

Reconciliation of the Governmental Funds Statement of Revenues, Expenditures, and Changes in Fund Balances to the Statement of Activities ....................................................................................................... 22

Statement of Net Position – Proprietary Fund ............................................................................... 23

Statement of Revenues, Expenses, and Changes in Fund Net Position – Proprietary Fund ................................................................................................... 24

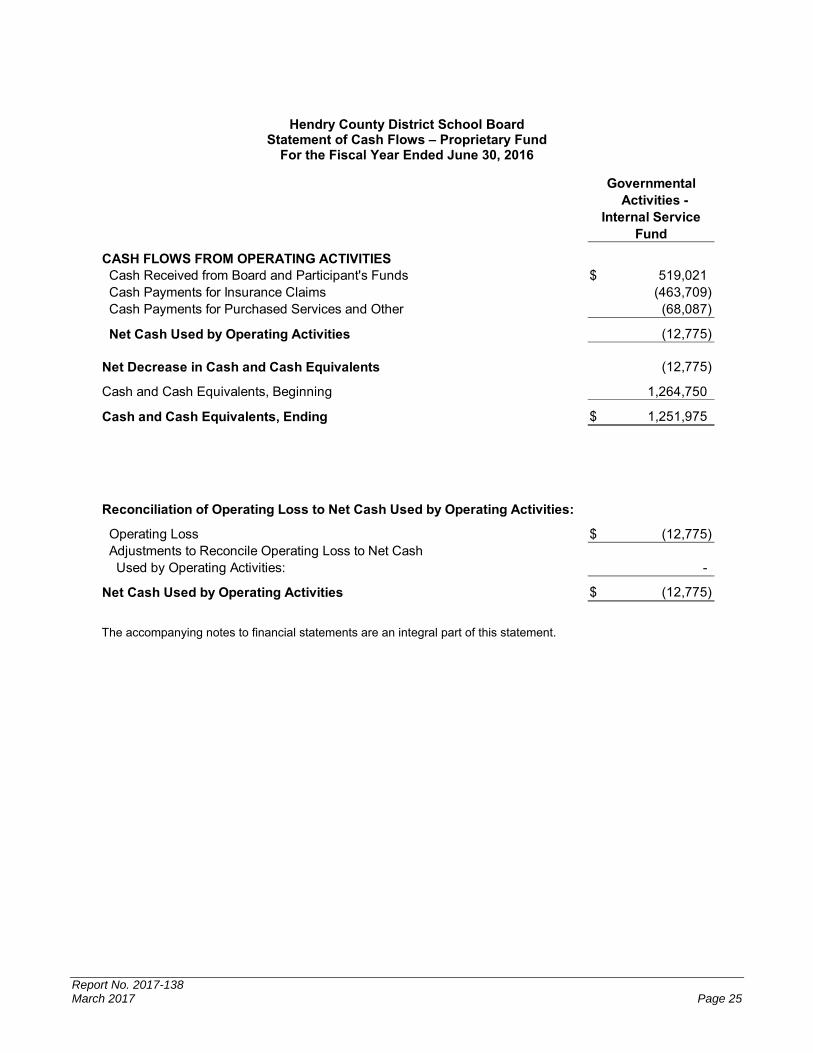

Statement of Cash Flows – Proprietary Fund ............................................................................... 25

Statement of Fiduciary Net Position – Fiduciary Funds ................................................................ 26

Statement of Changes in Fiduciary Net Position – Fiduciary Funds ............................................. 27

Notes to Financial Statements ...................................................................................................... 28

OTHER REQUIRED SUPPLEMENTARY INFORMATION

Budgetary Comparison Schedule – General and Major Special Revenue Funds ........................ 58

Schedule of Funding Progress – Other Postemployment Benefits Plan ....................................... 60

Schedule of the District’s Proportionate Share of the Net Pension Liability – Florida Retirement System Pension Plan ................................................................................................ 60

Schedule of District Contributions – Florida Retirement System Pension Plan ............................ 60

Schedule of the District’s Proportionate Share of the Net Pension Liability – Health Insurance Subsidy Pension Plan ................................................................................................. 61

Schedule of District Contributions – Health Insurance Subsidy Pension Plan .............................. 61

Notes to Required Supplementary Information ............................................................................. 61

HENDRY COUNTY DISTRICT SCHOOL BOARD

TABLE OF CONTENTS (CONTINUED)

Page No.

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS ............................................................ 64

INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS ............................................. 66

INDEPENDENT AUDITOR’S REPORT ON COMPLIANCE FOR EACH MAJOR FEDERAL PROGRAM AND REPORT ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY THE UNIFORM GUIDANCE .......................................................... 68

SCHEDULE OF FINDINGS AND QUESTIONED COSTS ................................................................ 71

PRIOR AUDIT FOLLOW-UP ............................................................................................................. 72

SUMMARY SCHEDULE OF PRIOR AUDIT FINDINGS .................................................................... 72

Report No. 2017-138 March 2017 Page i

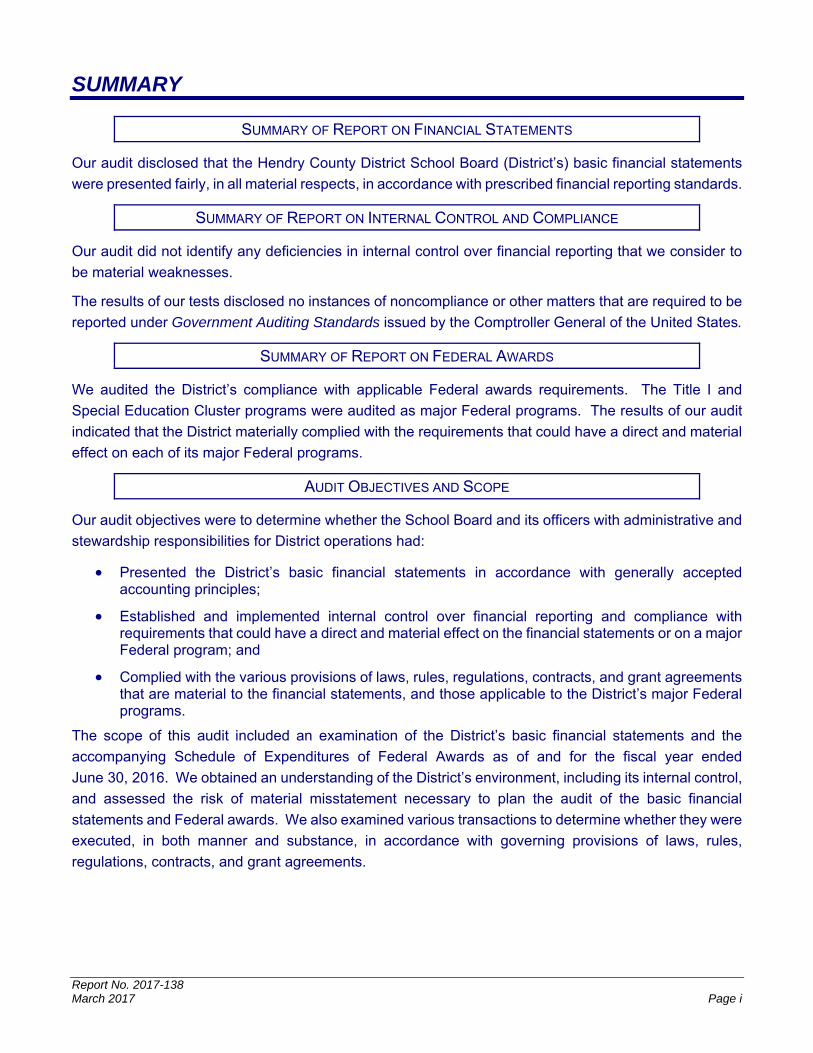

SUMMARY

SUMMARY OF REPORT ON FINANCIAL STATEMENTS

Our audit disclosed that the Hendry County District School Board (District’s) basic financial statements

were presented fairly, in all material respects, in accordance with prescribed financial reporting standards.

SUMMARY OF REPORT ON INTERNAL CONTROL AND COMPLIANCE

Our audit did not identify any deficiencies in internal control over financial reporting that we consider to

be material weaknesses.

The results of our tests disclosed no instances of noncompliance or other matters that are required to be

reported under Government Auditing Standards issued by the Comptroller General of the United States.

SUMMARY OF REPORT ON FEDERAL AWARDS

We audited the District’s compliance with applicable Federal awards requirements. The Title I and

Special Education Cluster programs were audited as major Federal programs. The results of our audit

indicated that the District materially complied with the requirements that could have a direct and material

effect on each of its major Federal programs.

AUDIT OBJECTIVES AND SCOPE

Our audit objectives were to determine whether the School Board and its officers with administrative and

stewardship responsibilities for District operations had:

Presented the District’s basic financial statements in accordance with generally accepted accounting principles;

Established and implemented internal control over financial reporting and compliance with requirements that could have a direct and material effect on the financial statements or on a major Federal program; and

Complied with the various provisions of laws, rules, regulations, contracts, and grant agreements that are material to the financial statements, and those applicable to the District’s major Federal programs.

The scope of this audit included an examination of the District’s basic financial statements and the

accompanying Schedule of Expenditures of Federal Awards as of and for the fiscal year ended

June 30, 2016. We obtained an understanding of the District’s environment, including its internal control,

and assessed the risk of material misstatement necessary to plan the audit of the basic financial

statements and Federal awards. We also examined various transactions to determine whether they were

executed, in both manner and substance, in accordance with governing provisions of laws, rules,

regulations, contracts, and grant agreements.

Report No. 2017-138 Page ii March 2017

AUDIT METHODOLOGY

We conducted our audit in accordance with auditing standards generally accepted in the United States

of America; applicable standards contained in Government Auditing Standards, issued by the Comptroller

General of the United States; and Title 2 U.S. Code of Federal Regulations Part 200, Uniform

Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards.

Report No. 2017-138 March 2017 Page 1

Phone: (850) 412-2722 Fax: (850) 488-6975

Sherrill F. Norman, CPA Auditor General

AUDITOR GENERAL STATE OF FLORIDA Claude Denson Pepper Building, Suite G74

111 West Madison Street Tallahassee, Florida 32399-1450

The President of the Senate, the Speaker of the House of Representatives, and the Legislative Auditing Committee

INDEPENDENT AUDITOR’S REPORT

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, each major fund,

and the aggregate remaining fund information of the Hendry County District School Board, as of and for

the fiscal year ended June 30, 2016, and the related notes to the financial statements, which collectively

comprise the District’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in

accordance with accounting principles generally accepted in the United States of America; this includes

the design, implementation, and maintenance of internal control relevant to the preparation and fair

presentation of financial statements that are free from material misstatement, whether due to fraud or

error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We did not

audit the financial statements of the school internal funds, which represent 17 percent of the assets and

86 percent of the liabilities of the aggregate remaining fund information. In addition, we did not audit the

financial statements of the Hendry Public Schools Foundation, Inc. (Foundation), which represent less

than 1 percent of the assets, 0 percent of the liabilities, 3 percent of the revenues, and 2 percent of the

expenses/expenditures of the aggregate remaining fund information. Those statements were audited by

other auditors whose reports have been furnished to us, and our opinion, insofar as they relate to the

amounts included for the school internal funds and the Foundation, is based solely on the reports of the

other auditors. We conducted our audit in accordance with auditing standards generally accepted in the

United States of America and the standards applicable to financial audits contained in Government

Auditing Standards, issued by the Comptroller General of the United States. Those standards require

Report No. 2017-138 Page 2 March 2017

that we plan and perform the audit to obtain reasonable assurance about whether the financial statements

are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in

the financial statements. The procedures selected depend on the auditor’s judgment, including the

assessment of the risks of material misstatement of the financial statements, whether due to fraud or

error. In making those risk assessments, the auditor considers internal control relevant to the entity’s

preparation and fair presentation of the financial statements in order to design audit procedures that are

appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness

of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes

evaluating the appropriateness of accounting policies used and the reasonableness of significant

accounting estimates made by management, as well as evaluating the overall presentation of the

financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for

our audit opinions.

Opinions

In our opinion, based on our audit and the reports of other auditors, the financial statements referred to

above present fairly, in all material respects, the respective financial position of the governmental

activities, each major fund, and the aggregate remaining fund information of the Hendry County District

School Board, as of June 30, 2016, and the respective changes in financial position and, where

applicable, cash flows thereof for the fiscal year then ended in accordance with accounting principles

generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that MANAGEMENT’S

DISCUSSION AND ANALYSIS, the Budgetary Comparison Schedule – General and Major Special

Revenue Funds, Schedule of Funding Progress – Other Postemployment Benefits Plan, Schedule

of the District’s Proportionate Share of the Net Pension Liability – Florida Retirement System

Pension Plan, Schedule of District Contributions – Florida Retirement System Pension Plan,

Schedule of the District’s Proportionate Share of the Net Pension Liability – Health Insurance

Subsidy Pension Plan, Schedule of District Contributions – Health Insurance Subsidy Pension

Plan, and Notes to Required Supplementary Information, as listed in the table of contents, be

presented to supplement the basic financial statements. Such information, although not a part of the

basic financial statements, is required by the Governmental Accounting Standards Board who considers

it to be an essential part of financial reporting for placing the basic financial statements in an appropriate

operational, economic, or historical context. We have applied certain limited procedures to the required

supplementary information in accordance with auditing standards generally accepted in the United States

of America, which consisted of inquiries of management about the methods of preparing the information

and comparing the information for consistency with management’s responses to our inquiries, the basic

financial statements, and other knowledge we obtained during our audit of the basic financial statements.

Report No. 2017-138 March 2017 Page 3

We do not express an opinion or provide any assurance on the information because the limited

procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Supplementary Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively

comprise the District’s basic financial statements. The accompanying SCHEDULE OF EXPENDITURES

OF FEDERAL AWARDS, as required by Title 2 U.S. Code of Federal Regulations Part 200, Uniform

Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, is presented

for purposes of additional analysis and is not a required part of the basic financial statements.

The accompanying SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS is the responsibility of

management and was derived from and relates directly to the underlying accounting and other records

used to prepare the basic financial statements. Such information has been subjected to the auditing

procedures applied in the audit of the basic financial statements and certain additional procedures,

including comparing and reconciling such information directly to the underlying accounting and other

records used to prepare the basic financial statements or to the basic financial statements themselves,

and other additional procedures in accordance with auditing standards generally accepted in the United

States of America. In our opinion, the accompanying SCHEDULE OF EXPENDITURES OF FEDERAL

AWARDS is fairly stated, in all material respects, in relation to the basic financial statements as a whole.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued a report dated March 9, 2017,

on our consideration of the District’s internal control over financial reporting and on our tests of its

compliance with certain provisions of laws, rules, regulations, contracts, and grant agreements and other

matters included under the heading INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL

OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN

AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT

AUDITING STANDARDS. The purpose of that report is to describe the scope of our testing of internal

control over financial reporting and compliance and the results of that testing, and not to provide an

opinion on internal control over financial reporting or on compliance. That report is an integral part of an

audit performed in accordance with Government Auditing Standards in considering the District’s internal

control over financial reporting and compliance.

Respectfully submitted, Sherrill F. Norman, CPA Tallahassee, Florida March 9, 2017

Report No. 2017-138 Page 4 March 2017

MANAGEMENT’S DISCUSSION AND ANALYSIS

The management of the Hendry County District School Board has prepared the following discussion and

analysis to provide an overview of the District’s financial activities for the fiscal year ended June 30, 2016.

The information contained in the Management’s Discussion and Analysis (MD&A) is intended to highlight

significant transactions, events, and conditions and should be considered in conjunction with the District’s

financial statements and notes to financial statements found immediately following the MD&A.

FINANCIAL HIGHLIGHTS

Key financial highlights for the 2015-16 fiscal year are as follows:

As of June 30, 2016, the assets and deferred outflows of resources exceed the liabilities and the deferred inflows of resources by $35.6 million.

In total, net position decreased $3 million, which represents a 7.7 percent decrease over the 2014-15 fiscal year.

General revenues total $62.5 million, or 92.7 percent of all revenues. Program specific revenues in the form of charges for services, operating grants and contributions, and capital grants and contributions total $4.9 million, or 7.3 percent of all revenues.

Expenses total $70.3 million. Only $4.9 million of these expenses was offset by program specific charges, with the remainder paid from general revenues.

At the end of the current fiscal year, the fund balance of the General Fund totals $10.1 million, which is $0.9 million less than the prior fiscal year balance. The General Fund total assigned and unassigned fund balances was $3.8 million, or 7.3 percent of total General Fund revenues.

Total long-term liabilities increased by $9.8 million, or 35.9 percent, mainly because the District’s net pension liability increased.

OVERVIEW OF FINANCIAL STATEMENTS

The basic financial statements consist of three components: (1) government-wide financial statements;

(2) fund financial statements; and (3) notes to financial statements. This report also includes

supplementary information intended to furnish additional details to support the basic financial statements.

Government-wide Financial Statements

The government-wide financial statements provide both short-term and long-term information about the

District’s overall financial condition in a manner similar to those of a private-sector business. The

statements include a statement of net position and a statement of activities that are designed to provide

consolidated financial information about the governmental activities of the District presented on the

accrual basis of accounting. The statement of net position provides information about the District’s

financial position, its assets, liabilities, and deferred inflows/outflows of resources, using an economic

resources measurement focus. Assets plus deferred outflows of resources, less liabilities and deferred

inflows of resources, equals net position, which is a measure of the District’s financial health. The

statement of activities presents information about the change in the District’s net position, the results of

operations, during the fiscal year. An increase or decrease in net position is an indication of whether the

District’s financial health is improving or deteriorating.

Report No. 2017-138 March 2017 Page 5

The government-wide statements present the District’s activities in the following categories:

Governmental activities – This represents most of the District’s services, including its educational programs: basic, vocational, adult, and exceptional education. Support functions such as transportation and administration are also included. Local property taxes and the State’s education finance program provide most of the resources that support these activities.

Blended component units – The District presents two separate legal entities in this report, which are the Hendry Public Schools Foundation, Inc. (Foundation) and the Hendry County School Board Leasing Corporation (Leasing Corporation). The Foundation is a not-for-profit corporation organized and operated as a direct-support organization under Section 1001.453, Florida Statutes. The Leasing Corporation was formed to facilitate financing for the acquisition of facilities and equipment for the District. Based on generally accepted accounting principles, as discussed in the notes to financial statements, these two entities have been included as an integral part of the primary government.

Fund Financial Statements

Fund financial statements are one of the components of the basic financial statements. A fund is a

grouping of related accounts that is used to maintain control over resources that have been segregated

for specific activities or objectives. The District uses fund accounting to ensure and demonstrate

compliance with finance-related legal requirements and prudent fiscal management. Certain funds are

established by law while others are created by legal agreements, such as bond covenants. Fund financial

statements provide more detailed information about the District’s financial activities, focusing on its most

significant or “major” funds rather than fund types. This is in contrast to the entitywide perspective

contained in the government-wide statements. All of the District’s funds may be classified within one of

the broad categories discussed below.

Governmental Funds: Governmental funds are used to account for essentially the same functions

reported as governmental activities in the government-wide financial statements. However, unlike the

government-wide financial statements, governmental fund financial statements focus on near-term

inflows and outflows of spendable resources, as well as on balances of spendable resources available

at the end of the fiscal year. Such information may be useful in assessing a government’s near-term

financing requirements.

Because the focus of governmental funds is narrower than that of the government-wide financial

statements, it is useful to compare the information presented for governmental funds with similar

information presented for governmental activities in the government-wide financial statements. By doing

so, readers may better understand the long-term impact of the government’s near-term financing

decisions. Both the governmental funds balance sheet and the governmental funds statement of

revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this

comparison between governmental funds and governmental activities.

The governmental funds balance sheet and statement of revenues, expenditures, and changes in fund

balances provide detailed information about the District’s most significant funds. The District’s major

funds are the General Fund, Special Revenue – Food Service Fund, Special Revenue – Other Fund, and

Capital Projects – Local Capital Improvement Fund. Data from the other governmental funds are

combined into a single, aggregated presentation.

Report No. 2017-138 Page 6 March 2017

The District adopts an annual appropriated budget for its governmental funds. A budgetary comparison

schedule has been provided for the General and major Special Revenue Funds to demonstrate

compliance with the budget.

Proprietary Fund: Proprietary funds may be established to account for activities in which a fee is

charged for services. The internal service fund is used to report activities that provide goods and services

to support the District’s other programs and functions through user charges. The District uses the internal

service fund to account for self-insurance activity for dental employee benefits. Since these services

predominantly benefit governmental functions, the internal service fund has been included within

governmental activities in the government-wide financial statements.

Fiduciary Funds: Fiduciary funds are used to report assets held in a trustee or fiduciary capacity for the

benefit of external parties, such as student activity funds. Fiduciary funds are not reflected in the

government-wide statements because the resources are not available to support the District’s own

programs. In its fiduciary capacity, the District is responsible for ensuring that the assets reported in

these funds are used only for their intended purposes.

The District uses a private-purpose trust fund to account for the activities of the Foundation, which is a

separate not-for-profit corporation organized to receive, hold, invest, and administer property and to make

expenditures to or for the benefit of public prekindergarten through postsecondary education.

The District uses agency funds to account for resources held for student activities and groups.

Notes to Financial Statements

The notes provide additional information that is essential for a full understanding of the data provided in

the government-wide and fund financial statements.

Other Information

In addition to the basic financial statements and accompanying notes, this report also presents required

supplementary information concerning the District’s net pension liability and its progress in funding its

obligation to provide other postemployment benefits to its employees.

GOVERNMENT-WIDE FINANCIAL ANALYSIS

As noted earlier, net position over time may serve as a useful indicator of a government’s financial health.

The following is a summary of the District’s net position as of June 30, 2016, compared to net position as

of June 30, 2015:

Report No. 2017-138 March 2017 Page 7

Net Position, End of Year

6-30-16 6-30-15

Current and Other Assets 19,280,874$ 19,062,062$ Capital Assets 50,700,806 51,568,384

Total Assets 69,981,680 70,630,446

Deferred Outflows of Resources 6,773,876 5,349,031

Long-Term Liabilities 37,256,195 27,423,972 Other Liabilities 700,941 348,057

Total Liabilities 37,957,136 27,772,029

Deferred Inflows of Resources 3,162,514 9,614,309

Net Position: Net Investment in Capital Assets 47,433,827 47,799,478 Restricted 7,865,140 6,899,055 Unrestricted (Deficit) (19,663,061) (16,105,394)

Total Net Position 35,635,906$ 38,593,139$

GovernmentalActivities

The largest portion of the District’s net position is investment in capital assets (e.g., land; buildings;

furniture, fixtures, and equipment), less any related debt still outstanding. The District uses these capital

assets to provide services to students; consequently, these assets are not available for future spending.

Although the investment in capital assets is reported net of related debt, the resources used to repay the

debt must be provided from other sources, since the capital assets cannot be used to liquidate these

liabilities.

The restricted portion of the District’s net position represents resources that are subject to external

restrictions on how they may be used. The deficit unrestricted net position was the result, in part, of

accruing $6.2 million in compensated absences payable, $2.8 million in other postemployment benefit

obligations, and $23.5 million in net pension liability.

The key elements of the changes in the District’s net position for the fiscal years ended June 30, 2016,

and June 30, 2015, are as follows:

Report No. 2017-138 Page 8 March 2017

Operating Results for the Fiscal Year Ended

6-30-16 6-30-15

Program Revenues: Charges for Services 275,237$ 635,354$ Operating Grants and Contributions 4,150,258 3,695,251 Capital Grants and Contributions 463,977 291,059 General Revenues: Property Taxes, Levied for Operational Purposes 10,480,934 10,447,529 Property Taxes, Levied for Capital Projects 2,764,034 2,706,244 Grants and Contributions Not Restricted to Specific Programs 48,589,841 46,555,044 Unrestricted Investment Earnings 106,471 83,929 Miscellaneous 521,409 1,061,978

Total Revenues 67,352,161 65,476,388

Functions/Program Expenses: Instruction 37,543,129 35,260,138 Student Support Services 2,662,400 2,320,291 Instructional Media Services 851,255 776,571 Instruction and Curriculum Development Services 1,602,820 1,385,392 Instructional Staff Training Services 945,030 921,441 Instruction-Related Technology 531,623 420,840 Board 666,914 618,452 General Administration 1,397,246 1,088,710 School Administration 4,041,794 3,817,068 Facilities Acquisition and Construction 1,834,567 1,589,649 Fiscal Services 669,461 653,868 Food Services 4,360,555 3,734,391 Central Services 356,352 349,247 Student Transportation Services 2,776,973 2,815,243 Operation of Plant 4,275,891 4,215,172 Maintenance of Plant 1,621,377 1,404,262 Administrative Technology Services 1,250,034 989,723 Unallocated Interest on Long-Term Debt 97,588 49,129 Unallocated Depreciation Expense 2,777,300 2,797,667 Loss on Disposal of Capital Assets 47,085 45,497

Total Functions/Program Expenses 70,309,394 65,252,751

Change in Net Position (2,957,233) 223,637

Net Position - Beginning 38,593,139 60,096,277 Adjustment to Beginning Net Position (1) - (21,726,775)

Net Position - Beginning, as Restated 38,593,139 38,369,502

Net Position - Ending 35,635,906$ 38,593,139$

GovernmentalActivities

Note: (1) The adjustment to beginning net position was due to the implementation of Governmental Accounting Standards Board Statement No. 68, which was a change in accounting principle that required employers participating in cost-sharing multiple-employer defined benefit pension plans to report the employers' proportionate share of the net pension liability of the defined benefit pension plans.

Report No. 2017-138 March 2017 Page 9

The largest revenue source is the State of Florida (61 percent). Revenues from State sources for current

operations are primarily received through the Florida Education Finance Program (FEFP) funding formula

which is accounted for as grants and contributions not restricted. The FEFP formula utilizes student

enrollment data, and is designed to maintain equity in funding across all Florida school districts, taking

into consideration the District’s funding ability based on the local property tax base. Grants and

contributions not restricted increased by $2 million, or 4.4 percent from an increase in State funding per

student and an increase in enrollment. Operating Grants and Contributions increased by $0.5 million, or

12.3 percent due to the first year of participation in the community eligibility provision for food service.

Instruction expenses represent 53.4 percent of total governmental expenses in the 2015-16 fiscal year.

Instruction expenses increased by $2.3 million, or 6.5 percent from the previous year due mainly to an

increase in instructional positions. Instruction-related technology increased by 26.3 percent due to a

large purchase of computers; general administration expenses increased by 28.3 percent resulting from

an increase in terminal leave payments; and administrative technology services increased by

26.3 percent because of an increase in information technology staff.

FINANCIAL ANALYSIS OF THE DISTRICT’S FUNDS

Governmental Funds

The focus of the District’s governmental funds is to provide information on near-term inflows, outflows,

and balances of spendable resources. Such information is useful in assessing the District’s financing

requirements. Specifically, unassigned fund balance may serve as a useful measure of a government’s

net resources available for discretionary use as it represents the portion of fund balance that has not

been limited to a particular purpose by an external party, the District, or a group or individual delegated

authority by the Board to assign resources for particular purposes.

The total fund balances of governmental funds decreased by $0.1 million during the fiscal year to

$17.4 million at June 30, 2016. Approximately 17.9 percent of this amount is unassigned fund balance

($3.1 million), which is available for spending at the District’s discretion. The remainder of the fund

balance is nonspendable, restricted, committed, or assigned to indicate that it is: (1) not in spendable

form ($0.1 million), (2) restricted for particular purposes ($7.9 million), (3) committed for particular

purposes ($5.6 million), or (4) assigned for particular purposes ($0.7 million).

Major Governmental Funds

The General Fund is the District’s chief operating fund. At the end of the current fiscal year, assigned

fund balance is $0.7 million and unassigned fund balance is $3.1 million, while the total fund balance is

$10.1 million. As a measure of the General Fund’s liquidity, it may be useful to compare the total assigned

and unassigned fund balances to General Fund total revenues. The total assigned and unassigned fund

balance is approximately 7.3 percent of the total General Fund revenues, while total fund balance

represents approximately 19.4 percent of total General Fund revenues.

Total fund balance decreased by $0.9 million during the fiscal year. The key factor impacting the change

in fund balance is that total expenditures increased by $2.1 million, or 4.1 percent, due mainly to an

increase in staff and other costs.

Report No. 2017-138 Page 10 March 2017

The Special Revenue – Food Service Fund expenditures exceeded revenues by $0.2 million. This may

be compared to last fiscal year’s results in which the Special Revenue – Food Service Fund revenues

exceeded expenditures by $0.4 million. The funding was mainly used for food and supplies.

The Special Revenue – Other Fund has total revenues and expenditures of $7.5 million each. The

funding was mainly used for instruction. Because grant revenues attributed to the grants accounted for

in this fund are not recognized until expenditures are incurred, this fund generally does not accumulate

a fund balance. Activity in the Special Revenue – Other Fund was substantially unchanged.

The Capital Projects – Local Capital Improvement (LCI) Fund has total fund balance of $1.9 million. This

fund is restricted for the acquisition, construction, and maintenance of capital assets. The fund balance

decreased in the current fiscal year primarily due to prior year resources being used to finance current

fiscal year expenditures. It should be noted that approximately $0.6 million has been encumbered for

LCI projects.

Proprietary Fund

The District’s proprietary fund financial statements provide the same type of information reported in the

government-wide financial statements, but in more detail. Unrestricted net position of the Internal Service

Fund decreased by less than $0.1 million during the 2015-16 fiscal year to $1.2 million at June 30, 2016.

This decrease occurred primarily because of increases in dental claims.

GENERAL FUND BUDGETARY HIGHLIGHTS

During the 2015-16 fiscal year, the District amended its General Fund budget several times, which

resulted in a decrease in total budgeted revenues of $0.3 million, or 0.5 percent. At the same time, final

appropriations are greater than the original budgeted amounts by $1.1 million. Budget revisions occurred

primarily from changes in estimated State funding levels and corresponding adjustments to planned

expenditures to ensure maintenance of an adequate fund balance.

Actual revenues are in line with the final budgeted amounts while actual expenditures are $2.2 million, or

4 percent, less than final budgeted amounts. The variance in expenditures was primarily due to continued

cost containment measures implemented by the District. The actual ending fund balance exceeded the

estimated fund balance contained in the final amended budget by $2.3 million.

CAPITAL ASSETS AND LONG-TERM DEBT

Capital Assets

The District’s investment in capital assets for its governmental activities as of June 30, 2016, is

$50.7 million (net of accumulated depreciation). This investment in capital assets includes land;

construction in progress; improvements other than buildings; buildings and fixed equipment; furniture,

fixtures, and equipment; motor vehicles; and computer software. The total decrease in capital assets for

the current fiscal year was approximately 1.7 percent.

Additional information on the District’s capital assets can be found in Notes I.F.4. and II.C. to the financial

statements.

Report No. 2017-138 March 2017 Page 11

Long-Term Debt

At June 30, 2016, the District has total long-term debt outstanding of $4.8 million, composed of

$1.7 million of bonds payable and $3.1 million of certificates of participation payable. During the current

fiscal year, the District issued the Revenue Bond Series 2015 for $1.5 million and refunded the Revenue

Bond Series 1997 for $0.2 million. The retirement of debt was $0.5 million.

State school bonds outstanding at June 30, 2016, totaling $0.2 million, are secured by a pledge of the

District’s portion of the State-assessed motor vehicle license tax. The State’s full faith and credit is also

pledged as security for these bonds. Revenue bonds of $1.5 million are secured by pari-mutuel tax

proceeds. The District’s certificates of participation are not secured by specified revenue sources.

Additional information on the District’s long-term debt can be found in Notes I.F.4. and II.H. to the financial

statements.

OTHER MATTERS OF SIGNIFICANCE

Employer contributions to the Florida Retirement System increased for regular employees from

7.26 percent to 7.52 percent of payroll for the 2016-17 fiscal year.

Housing prices are expected to increase the taxable assessed property value for the 2016-17 fiscal year

resulting in increased property tax revenues.

REQUESTS FOR INFORMATION

This report is designed to provide a general overview of the District’s finances for all those with an interest

in the District’s finances. Questions concerning information provided in the MD&A or other required

supplementary information, and financial statements and notes thereto, or requests for additional

financial information should be addressed to the Superintendent, Hendry County District School Board,

25 East Hickpoochee Avenue, LaBelle, Florida 33935.

Report No. 2017-138 Page 12 March 2017

THIS PAGE INTENTIONALLY LEFT BLANK

Report No. 2017-138 March 2017 Page 13

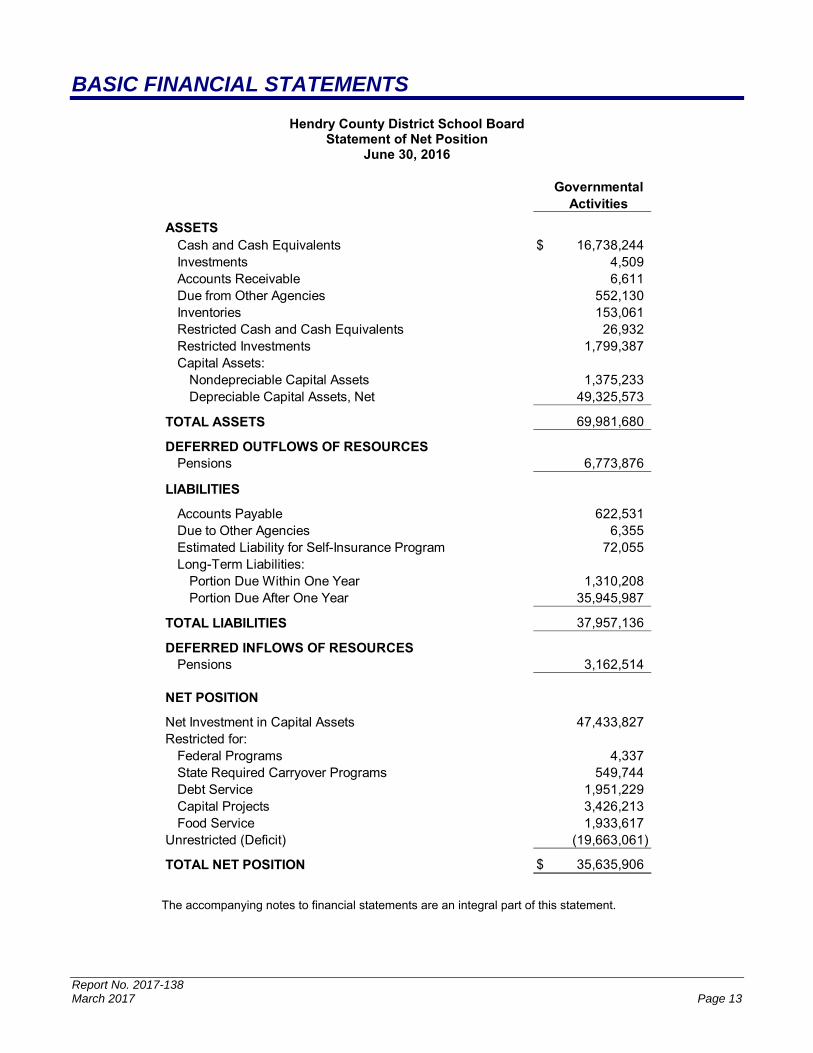

BASIC FINANCIAL STATEMENTS

Hendry County District School Board Statement of Net Position

June 30, 2016

GovernmentalActivities

ASSETSCash and Cash Equivalents $ 16,738,244 Investments 4,509 Accounts Receivable 6,611 Due from Other Agencies 552,130 Inventories 153,061 Restricted Cash and Cash Equivalents 26,932 Restricted Investments 1,799,387 Capital Assets:

Nondepreciable Capital Assets 1,375,233 Depreciable Capital Assets, Net 49,325,573

TOTAL ASSETS 69,981,680

DEFERRED OUTFLOWS OF RESOURCESPensions 6,773,876

LIABILITIES

Accounts Payable 622,531 Due to Other Agencies 6,355 Estimated Liability for Self-Insurance Program 72,055 Long-Term Liabilities:

Portion Due Within One Year 1,310,208 Portion Due After One Year 35,945,987

TOTAL LIABILITIES 37,957,136

DEFERRED INFLOWS OF RESOURCESPensions 3,162,514

NET POSITION

Net Investment in Capital Assets 47,433,827 Restricted for:

Federal Programs 4,337 State Required Carryover Programs 549,744 Debt Service 1,951,229 Capital Projects 3,426,213 Food Service 1,933,617

Unrestricted (Deficit) (19,663,061)

TOTAL NET POSITION $ 35,635,906

The accompanying notes to financial statements are an integral part of this statement.

Report No. 2017-138 Page 14 March 2017

Hendry County District School Board Statement of Activities

For the Fiscal Year Ended June 30, 2016

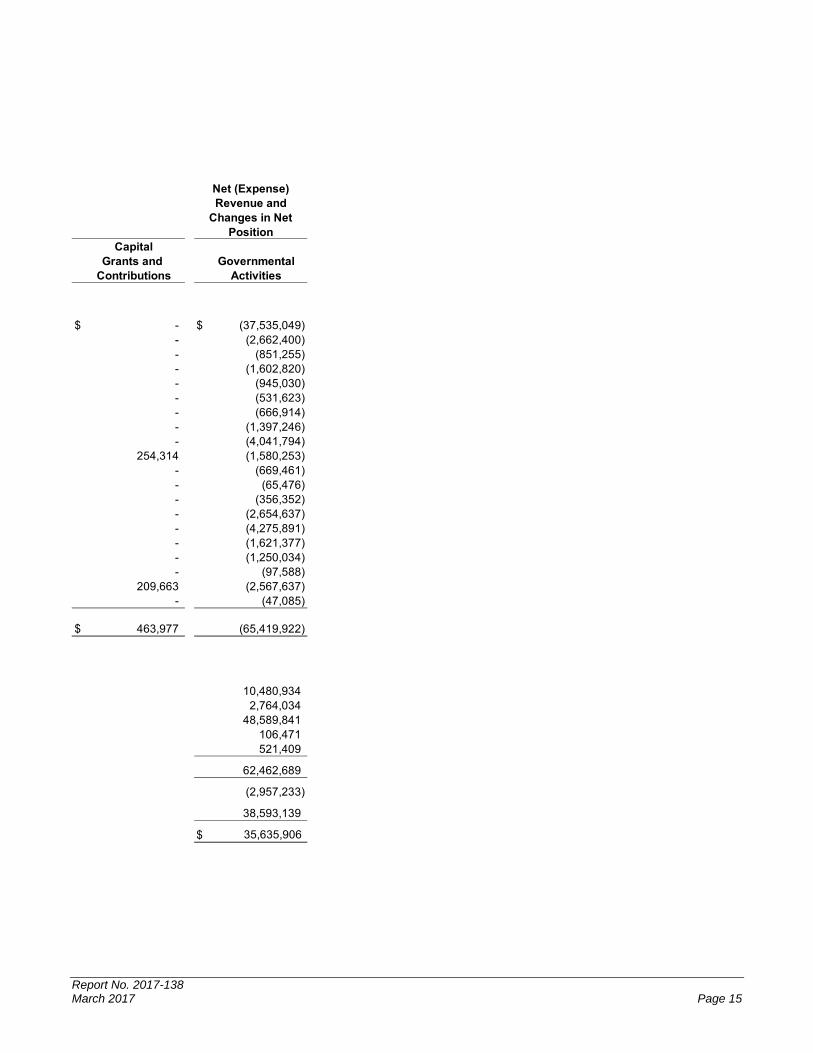

Charges Operatingfor Grants and

Expenses Services ContributionsFunctions/Programs

Governmental Activities:Instruction $ 37,543,129 $ - $ 8,080 Student Support Services 2,662,400 - - Instructional Media Services 851,255 - - Instruction and Curriculum Development Services 1,602,820 - - Instructional Staff Training Services 945,030 - - Instruction-Related Technology 531,623 - - Board 666,914 - - General Administration 1,397,246 - - School Administration 4,041,794 - - Facilities Acquisition and Construction 1,834,567 - - Fiscal Services 669,461 - - Food Services 4,360,555 152,901 4,142,178 Central Services 356,352 - - Student Transportation Services 2,776,973 122,336 - Operation of Plant 4,275,891 - - Maintenance of Plant 1,621,377 - - Administrative Technology Services 1,250,034 - - Unallocated Interest on Long-Term Debt 97,588 - - Unallocated Depreciation Expense 2,777,300 - - Loss on Disposal of Capital Assets 47,085 - -

Total Governmental Activities $ 70,309,394 $ 275,237 $ 4,150,258

General Revenues:Taxes: Property Taxes, Levied for Operational Purposes Property Taxes, Levied for Capital ProjectsGrants and Contributions Not Restricted to Specific ProgramsUnrestricted Investment EarningsMiscellaneous

Total General Revenues

Change in Net Position

Net Position - Beginning

Net Position - Ending

Program Revenues

The accompanying notes to financial statements are an integral part of this statement.

Report No. 2017-138 March 2017 Page 15

CapitalGrants and Governmental

Contributions Activities

$ - $ (37,535,049) - (2,662,400) - (851,255) - (1,602,820) - (945,030) - (531,623) - (666,914) - (1,397,246) - (4,041,794)

254,314 (1,580,253) - (669,461) - (65,476) - (356,352) - (2,654,637) - (4,275,891) - (1,621,377) - (1,250,034) - (97,588)

209,663 (2,567,637) - (47,085)

$ 463,977 (65,419,922)

10,480,934 2,764,034

48,589,841 106,471 521,409

62,462,689

(2,957,233)

38,593,139

$ 35,635,906

Net (Expense) Revenue and

Changes in Net Position

Report No. 2017-138 Page 16 March 2017

Hendry County District School Board Balance Sheet – Governmental Funds

June 30, 2016

Special Revenue - Special Revenue -General Food Service Other

Fund Fund Fund

ASSETS Cash and Cash Equivalents $ 9,862,158 $ 1,791,154 $ 5,042 Investments - - - Accounts Receivable 6,611 - - Due from Other Funds 265,866 129,897 29 Due from Other Agencies 12,268 93,810 444,187 Inventories 153,061 - - Restricted Cash and Cash Equivalents - - - Restricted Investments - - -

TOTAL ASSETS $ 10,299,964 $ 2,014,861 $ 449,258

LIABILITIES, DEFERRED INFLOWS OF RESOURCES, AND FUND BALANCESLiabilities:

Accounts Payable $ 210,828 $ 75,317 $ 55,085 Due to Other Funds 29 5,927 389,836 Due to Other Agencies 6,355 - -

Total Liabilities 217,212 81,244 444,921

Deferred Inflows of Resources:Unavailable Revenue - Capital Outlay and Debt Service - - -

Fund Balances:Nonspendable:

Inventories 153,061 - - Restricted for:

Federal Programs - - 4,337 State Required Carryover Programs 549,744 - - Debt Service - - - Capital Projects - - - Food Service - 1,933,617 -

Total Restricted Fund Balance 549,744 1,933,617 4,337 Committed for:

Economic Stabilization 5,570,090 - - Assigned for:

Emergency Fund 518,876 - - Purchases on Order 177,727 - -

Total Assigned Fund Balance 696,603 - - Unassigned Fund Balance 3,113,254 - -

Total Fund Balances 10,082,752 1,933,617 4,337

TOTAL LIABILITIES, DEFERRED INFLOWS OF RESOURCES,AND FUND BALANCES $ 10,299,964 $ 2,014,861 $ 449,258

The accompanying notes to financial statements are an integral part of this statement.

Report No. 2017-138 March 2017 Page 17

Capital Projects - Other TotalLocal Capital Governmental Governmental

Improvement Fund Funds Funds

$ 2,043,619 $ 1,784,296 $ 15,486,269 - 4,509 4,509 - - 6,611 - - 395,792 - 1,865 552,130 - - 153,061 - 26,932 26,932 - 1,799,387 1,799,387

$ 2,043,619 $ 3,616,989 $ 18,424,691

$ 188,240 $ 93,061 $ 622,531 - - 395,792 - - 6,355

188,240 93,061 1,024,678

- 1,865 1,865

- - 153,061

- - 4,337 - - 549,744 - 1,951,229 1,951,229

1,855,379 1,570,834 3,426,213 - - 1,933,617

1,855,379 3,522,063 7,865,140 -

- - 5,570,090 -

- - 518,876 - - 177,727 - - 696,603 - - 3,113,254

1,855,379 3,522,063 17,398,148

$ 2,043,619 $ 3,616,989 $ 18,424,691

Report No. 2017-138 Page 18 March 2017

Hendry County District School Board Reconciliation of the Governmental Funds Balance Sheet

to the Statement of Net Position June 30, 2016

Total Fund Balances - Governmental Funds $ 17,398,148

50,700,806

1,179,920

Deferred Outflows Related to Pensions $ 6,773,876

Deferred Inflows Related to Pensions (3,162,514) 3,611,362

1,865

Certificates of Participation Payable $ (3,068,200) Bonds Payable (1,698,779) Other Postemployment Benefits Payable (2,808,621) Compensated Absences Payable (6,185,889) Net Pension Liability (23,494,706) (37,256,195)

Net Position - Governmental Activities $ 35,635,906

Amounts reported for governmental activities in the statement of net position are different because:

Internal service funds are used by management to charge the costs of certain activities, such asinsurance, to individual funds. The assets and liabilities of the internal service funds are includedin governmental activities in the statement of net position.

Long-term liabilities are not due and payable in the fiscal year and, therefore, are not reported asliabilities in the governmental funds. Long-term liabilities at year-end consist of:

Capital assets, net of accumulated depreciation, used in governmental activities are not financialresources and, therefore, are not reported as assets in the governmental funds.

The deferred outflows of resources and deferred inflows of resources related to pensions areapplicable to future periods and, therefore, are not reported in the governmental funds.

A portion of capital outlay and debt service revenue is not available to pay current periodexpenditures and, therefore, is reported as unavailable revenue in the governmental fund

The accompanying notes to financial statements are an integral part of this statement.

Report No. 2017-138 March 2017 Page 19

THIS PAGE INTENTIONALLY LEFT BLANK

Report No. 2017-138 Page 20 March 2017

Hendry County District School Board Statement of Revenues, Expenditures, and Changes in

Fund Balances – Governmental Funds For the Fiscal Year Ended June 30, 2016

Revenues

Intergovernmental:Federal Through State and Local $ 394,502 $ 4,088,162 $ 7,462,613 State 40,402,912 54,016 -

Local:Property Taxes 10,480,934 - - Charges for Services - Food Service - 152,901 - Miscellaneous 609,224 44,410 - Total Local Revenues 11,090,158 197,311 -

Total Revenues 51,887,572 4,339,489 7,462,613

Expenditures

Current - Education:Instruction 32,014,536 - 4,863,654 Student Support Services 2,050,689 - 570,310 Instructional Media Services 820,690 - 12,639 Instruction and Curriculum Development Services 715,577 - 876,525 Instructional Staff Training Services 86,426 - 852,443 Instruction-Related Technology 345,866 - - Board 662,714 - - General Administration 1,214,982 - 164,617 School Administration 3,956,693 - - Facilities Acquisition and Construction 13,100 - 350 Fiscal Services 658,474 - - Food Services - 4,360,555 - Central Services 350,321 - - Student Transportation Services 2,651,257 - 83,869 Operation of Plant 4,241,866 - - Maintenance of Plant 1,595,793 - - Administrative Technology Services 1,235,613 - -

Fixed Capital Outlay:Facilities Acquisition and Construction - - - Other Capital Outlay 151,683 134,501 41,965