Embed Size (px)

Citation preview

RMK and CovarianceRMK and Covariance

Seminar on Risk and Return in Seminar on Risk and Return in ReinsuranceReinsurance

September 26, 2005September 26, 2005

Dave ClarkDave ClarkAmerican Re-Insurance CompanyAmerican Re-Insurance Company

This material is being provided to you for information only, and is not permitted to be further distributed without the express written permission of American Re. This material is not intended to be legal, underwriting, financial or any other type of professional advice. Examples given are for illustrative purposes only.

© Copyright 2005 American Re-Insurance Company. All rights reserved.

RMK FrameworkRMK Framework

Introduction:Introduction: A A Confusing Confusing List of TermsList of Terms Capital AllocationCapital Allocation Cost of CapitalCost of Capital Capital ConsumptionCapital Consumption Risk LoadRisk Load Risk / Reward trade-offsRisk / Reward trade-offs RMK ???RMK ???

RMK FrameworkRMK Framework

Introduction:Introduction: The RMK Framework sources The RMK Framework sources

RMK = Ruhm, Mango, KrepsRMK = Ruhm, Mango, Kreps

Mango:Mango: Capital Consumption: An AlternativeCapital Consumption: An Alternative

Methodology for Pricing ReinsuranceMethodology for Pricing ReinsuranceCAS Forum, Winter 2003CAS Forum, Winter 2003

Kreps:Kreps: Riskiness Leverage ModelsRiskiness Leverage ModelsPCAS 2005 – Originally circulated in bootleg version asPCAS 2005 – Originally circulated in bootleg version as

“ “A Risk Class with Additive Co-Measures”A Risk Class with Additive Co-Measures”

RMK FrameworkRMK Framework

Agenda:Agenda: Examples from Reinsurance PricingExamples from Reinsurance Pricing

Allocation of stop-loss premiumAllocation of stop-loss premium Multi-year profit commissionMulti-year profit commission

Example of “Capital Consumption”Example of “Capital Consumption” PropertiesProperties

The MathematicsThe Mathematics Problems & ChallengesProblems & Challenges

RMK FrameworkRMK Framework

Resource divided between individualsResource divided between individuals

Shared Resource:Shared Resource:

RMK FrameworkRMK Framework

Instead of the “capital allocation” problem Instead of the “capital allocation” problem we will start with two other examples in we will start with two other examples in which dollar amounts need to be allocated which dollar amounts need to be allocated in reinsurance applications.in reinsurance applications.

Example #1: A ceding company purchases Example #1: A ceding company purchases an aggregate “stop-loss” cover that an aggregate “stop-loss” cover that applies to all lines of business combined. applies to all lines of business combined. How should the cost of this reinsurance be How should the cost of this reinsurance be allocated to the individual lines of allocated to the individual lines of business?business?

RMK FrameworkRMK Framework

Example #2: A reinsurer has sold an Excess Example #2: A reinsurer has sold an Excess WC treaty with a profit commission that WC treaty with a profit commission that applies on a 3-year block. It is now the applies on a 3-year block. It is now the end of the second year and we want to end of the second year and we want to evaluate the “expected” profit commission evaluate the “expected” profit commission on the prospective third year. How do we on the prospective third year. How do we estimate the expected profit commission estimate the expected profit commission by year?by year?

RMK FrameworkRMK Framework

Example #3: Risk Measures and “Capital Example #3: Risk Measures and “Capital Consumption”Consumption”

Given an overall profit target, what is the Given an overall profit target, what is the fairest method for setting corresponding fairest method for setting corresponding profit targets for individual products?profit targets for individual products?

RMK FrameworkRMK Framework

Review Excel ExamplesReview Excel Examples

RMK FrameworkRMK FrameworkStrengths of the RMK Framework:Strengths of the RMK Framework:

Results are additive: business segments can be Results are additive: business segments can be defined any way you want and it will not affect the defined any way you want and it will not affect the answer.answer.

Risk measures by business segment are logically Risk measures by business segment are logically connected to the risk measure for the company in connected to the risk measure for the company in total.*total.*

Theory works for any correlation or dependence Theory works for any correlation or dependence structure in the losses: If you can simulate it, RMK structure in the losses: If you can simulate it, RMK will work!will work!

*This is why Kreps calls RMK “*This is why Kreps calls RMK “additive co-measuresadditive co-measures””

RMK FrameworkRMK FrameworkMathematicsMathematics

We will follow Kreps’ notation for describing We will follow Kreps’ notation for describing formulas for allocating the risk measure.formulas for allocating the risk measure.

),,( 321 xxxf

321 XXXY Assume that we have a Assume that we have a portfolio “Y”, made up of portfolio “Y”, made up of the sum of three the sum of three business segments: Xbusiness segments: X11, , XX22, and X, and X33..

These three segments do These three segments do not have to be not have to be independent or independent or identically distributed.identically distributed.

RMK FrameworkRMK FrameworkMathematicsMathematics

Kreps’ notation continued:Kreps’ notation continued:

Define a risk measure Define a risk measure RR, which is based on the , which is based on the total losses to the portfolio.total losses to the portfolio.

dyyfyLyR y )()(

Amount by which Amount by which an actual loss an actual loss exceeds the exceeds the average.average.

The “Leverage” or The “Leverage” or pain associated pain associated with the loss with the loss amount.amount.

RMK FrameworkRMK FrameworkMathematicsMathematics

Kreps’ notation continued:Kreps’ notation continued:

We then introduce a simplified notation.We then introduce a simplified notation.

dFyLyR y )(

wherwheree

321321 ),,( dxdxdxxxxfdF

RMK FrameworkRMK FrameworkMathematicsMathematics

Kreps’ notation continued:Kreps’ notation continued:

The overall risk-load is allocated as follows.The overall risk-load is allocated as follows.

dFyLyR y )(

Changes Changes to…to…

dFyLxR kkk )(

RMK FrameworkRMK FrameworkMathematicsMathematics

Kreps’ notation continued:Kreps’ notation continued:

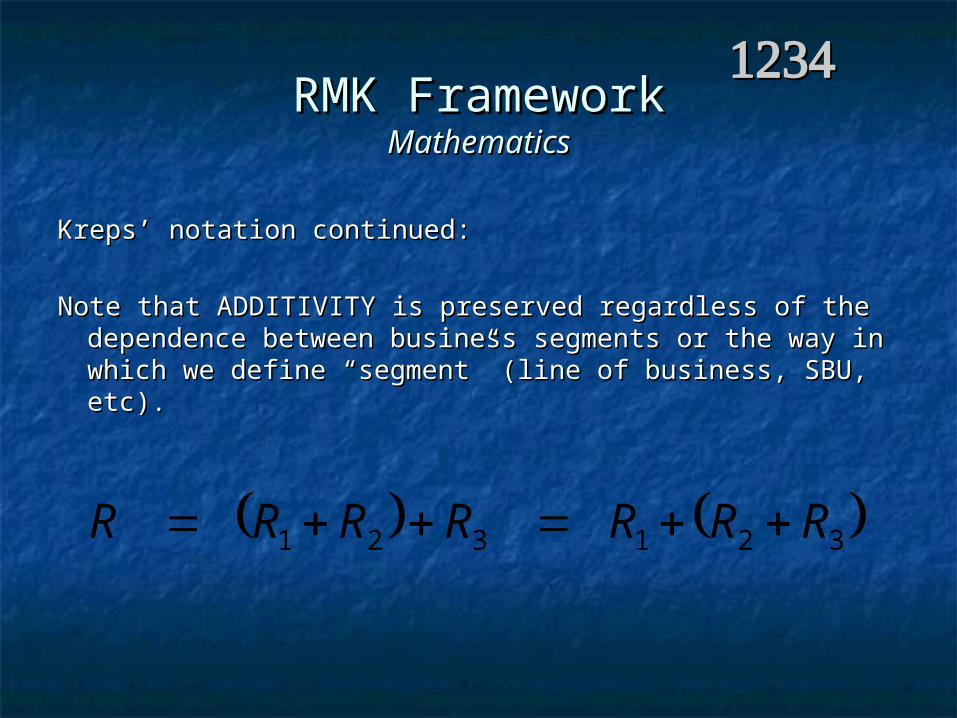

Note that ADDITIVITY is preserved regardless of the Note that ADDITIVITY is preserved regardless of the dependence between business segments or the way in dependence between business segments or the way in which we define “segment” (line of business, SBU, etc).which we define “segment” (line of business, SBU, etc).

321321 RRRRRRR

RMK FrameworkRMK FrameworkMathematicsMathematics

The Leverage Ratio The Leverage Ratio L(y)L(y) is a “pain” is a “pain” function:function:

If (y-If (y-μμyy) is ) is negativenegative::no capital used, no capital used, L(y)L(y)=0; there is no “pain”=0; there is no “pain”

If (y- If (y- μμyy) is ) is smallsmall but positive: but positive:some capital is consumed, some capital is consumed, L(y)L(y)>0>0

If (y- If (y- μμyy) is ) is largelarge::capital is consumed, solvency is imperiledcapital is consumed, solvency is imperiled

If (y- If (y- μμyy) is ) is hugehuge (a multiple of capital): (a multiple of capital):L(y)L(y) stops growing, since we no longer care if we stops growing, since we no longer care if we are are dead many times overdead many times over

RMK FrameworkRMK FrameworkMathematicsMathematics

Kreps shows that virtually all of the common Kreps shows that virtually all of the common proposals for risk measures can be proposals for risk measures can be formulated in terms of a leverage ratio formulated in terms of a leverage ratio L(y) L(y) ::

VarianceVariance Standard DeviationStandard Deviation Value at Risk Value at Risk (VaR)(VaR) Conditional DownsideConditional Downside (TVaR or “tail value at (TVaR or “tail value at

risk”)risk”)

RMK FrameworkRMK FrameworkMathematicsMathematics

Kreps’ notation and covariance:Kreps’ notation and covariance:

Alternative formulation (from Ruhm & Mango):Alternative formulation (from Ruhm & Mango):

yxCovR kk ,

)(, yLxCovR kk

yyyL )(This implies that ifThis implies that if

Then a covariance Then a covariance allocation results:allocation results:

RMK FrameworkRMK FrameworkMathematicsMathematics

Conditions for RMK to reproduce covariance:Conditions for RMK to reproduce covariance:

yVar

yxCovRR k

k

,

yVarR

(1) If the portfolio risk measure is variance(1) If the portfolio risk measure is variance

(2) If there is a linear relationship between expected (2) If there is a linear relationship between expected losses, then for losses, then for anyany leverage ratio: leverage ratio:

ymbyXE k ]|[

yVar

yxCovRR k

k

,

OrOr……

RMK FrameworkRMK FrameworkMathematicsMathematics

Conditions for RMK to reproduce covariance:Conditions for RMK to reproduce covariance:

This second condition is EXACTLY met whenThis second condition is EXACTLY met when

1.1. All business segments write identical policies (even All business segments write identical policies (even if they have different commission percents)if they have different commission percents)

2.2. All business segments take different shares of a poolAll business segments take different shares of a pool

3.3. All business segments are drawn from certain All business segments are drawn from certain multivariate distributionsmultivariate distributions

We can also find cases when it is APPROXIMATELY We can also find cases when it is APPROXIMATELY met…met…

RMK FrameworkRMK FrameworkMathematicsMathematics

Loss Distributions for which RMK = covariance:Loss Distributions for which RMK = covariance:

Examples:Examples: Elliptical DistributionsElliptical Distributions

Normal, Student-t, Logistic, etcNormal, Student-t, Logistic, etc Additive Form of Exponential FamilyAdditive Form of Exponential Family

Normal, Poisson, Gamma, Inverse GaussianNormal, Poisson, Gamma, Inverse Gaussian Note “Additive” = closed-under-convolutionNote “Additive” = closed-under-convolution

Other…Other…

RMK FrameworkRMK FrameworkMathematicsMathematics

Generalized Pareto (a.k.a. Beta of Second Kind)Generalized Pareto (a.k.a. Beta of Second Kind)

x

x

x

x

x

x

dx

dxxf

)(

)()(

1

yx

yx

yx

yx

yx

yx

dydx

dydxyxf

)(

)()(),(

11

Bivariate Generalized Pareto (common Bivariate Generalized Pareto (common and and ))

xdx

RMK FrameworkRMK FrameworkMathematicsMathematics

General Principle, informally stated:General Principle, informally stated:

Covariance allocation is a linear Covariance allocation is a linear approximation to any arbitrary riskapproximation to any arbitrary risk

co-measure.co-measure.

Note: subject to conditions such as all variances Note: subject to conditions such as all variances existing, and the risk measure being on a “central” existing, and the risk measure being on a “central” basis (x-basis (x-μμ).).

RMK FrameworkRMK FrameworkMathematicsMathematics

Condition for RMK to approximate covariance:Condition for RMK to approximate covariance:

0

500

1,000

1,500

2,000

0 1,000 2,000 3,000 4,000 5,000

All Lines Combined

Lin

e 1

RMK FrameworkRMK FrameworkMathematicsMathematics

0

500

1,000

1,500

0 1,000 2,000 3,000 4,000 5,000

All Lines Combined

Lin

e su

bje

ct t

o S

top

L

oss

Condition when RMK does NOT approximate covariance:Condition when RMK does NOT approximate covariance:

RMK FrameworkRMK FrameworkMathematicsMathematics

Condition when RMK does NOT approximate covariance:Condition when RMK does NOT approximate covariance:

0

500

1,000

1,500

2,000

0 1,000 2,000 3,000 4,000 5,000

All Lines Combined

Ca

tas

tro

ph

e L

os

s

RMK FrameworkRMK Framework

Problems & Challenges:Problems & Challenges:

Two hurdles:Two hurdles: Calibration down to individual Calibration down to individual

contract level will probably always be contract level will probably always be an approximation.an approximation.

More work needed on theory for More work needed on theory for including the time value of money.including the time value of money.

RMK FrameworkRMK Framework

Questions & DiscussionQuestions & Discussion

David R. ClarkDavid R. Clark

““Reinsurance Applications of the RMK Framework”;Reinsurance Applications of the RMK Framework”;

Spring 2005 Spring 2005 CAS ForumCAS Forumwww.casact.org/pubs/forum/05spforumwww.casact.org/pubs/forum/05spforum