Embed Size (px)

Citation preview

EXECUTIVE SUMMARY

Marketing products using visual merchandising system is an age-old practice but with growing growth

of retail industry, the art or arguably the science of Visual Merchandising has gone to occupy a

newfound fancy. There is a growing recognition of the need for an effective Visual Merchandising. But

even as it continues to grow, the understanding of Visual Merchandising impact and effectiveness is still in

its infancy. The shopping behaviour which governs the decision to buy is a function of three stimuli viz.,

visual, auditory and kinaesthetic; the visual stimulus is the easiest and most widely used tool for attracting

customers.

This project deals with components of visual merchandising, and a comparative analysis of six retail

lifestyle stores in Bangalore. The comparison has been made taking into account the components of

visual merchandising and rating each store on each of these components.

The methodology followed is questionnaire method with a total sample size of 150 respondents, 25

respondents from each store namely Lifestyle, Bangalore Central, Shoppers Stop, Globus, Westside and

Pantaloons. The data is tabulated and graphically represented through histograms, pie-charts, line graphs etc.

Findings and recommendations are listed at the end of this project.

RETAILING

Retailing consists of those business activities involved in the sales of goods and services to

consumers for their personal, family or household use. The field of retailing is both

fascinating and complex. It has enormous impact on the economy, in distribution, and its

relationship with companies that see goods and services to retailers for their resale or use.

Retailing is the final stage in the distribution process, it does not necessary have to include a

retailer. Manufacturers, importers, non-profit firms, and wholesalers,and other

organization are also considered as retailers when they sell goods and/or services to final

consumers. Competition in the retailing scene has intensified manifold for the past few

decades, generally as a consequence of new technologies, more sophisticated management

practices and industry consolidation. These trends have been especially pronounced in the

food industry.

There has been a significant amount of studies that examine the issues of retail channel management and

retail marketing strategies to tackle the fierce competition in existing retail channels in food industry. As in

all other industries, the ultimate decider of the eventual success of an alternative retail channel is the

CONSUMER.

Consumers refer to individuals who buy products and services for themselves or on behalf

on their households. They are invariably either users of these products or services or

responsible for the welfare and well being of those who are. Since consumers are extremely

crucial for retailers, an understanding of consumer behavior is an essential prerequisite of

successful retail marketing strategy and one of the most fundamental principles of in exerting

influence on consumer patronage decision process. Without customer focus, marketing

planning can easily be dominated by the actions of competitors or internal influences. The

success of a retailer depends on how well he/she selects, identifies and understands his

customers.

The feasibility of new retail channels is also highly dependent on retailers’ ability to select

the type of consumer segments to reach (mass markets, market segment, or multiple

segments), to identify the characteristics and needs of the specific target market and understanding

how consumers make decisions. According to Peter McGoldrick, the most successful examples of

innovation and evolution in retail formats are retailers that respond accurately and profitably to

previously unsatisfied needs.

TYPES OF RETAIL OUTLETS

The emergence of new sectors has been accompanied by changes in existing formats as well as the

beginning of new formats:

Hyper marts, typically 8,000 sq.ft and more

Large supermarkets, typically 3,500-5,000 sq. ft.

Mini supermarkets, typically 1,000-2,000 sq. ft.

Convenience stores, typically 750-1,000sq. ft.

Discount/shopping list grocery

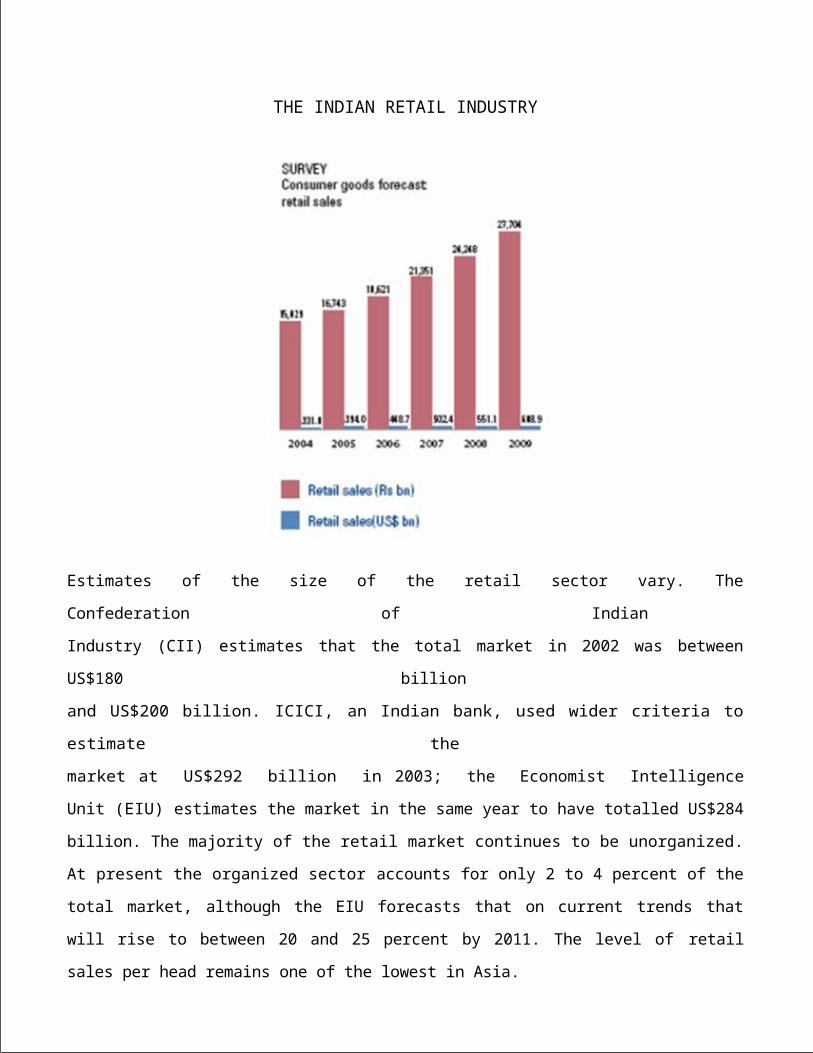

THE INDIAN RETAIL INDUSTRY

Estimates of the size of the retail sector vary. The Confederation of Indian

Industry (CII) estimates that the total market in 2002 was between US$180 billion

and US$200 billion. ICICI, an Indian bank, used wider criteria to estimate the

market at US$292 billion in 2003; the Economist Intelligence Unit (EIU) estimates the market in the

same year to have totalled US$284 billion. The majority of the retail market continues to be unorganized. At

present the organized sector accounts for only 2 to 4 percent of the total market, although the EIU forecasts

that on current trends that will rise to between 20 and 25 percent by 2011. The level of retail sales per head

remains one of the lowest in Asia.

For retailers, a critical issue is how fast and how far the consuming class will grow. This depends

both on the growth of personal disposable income, and the extent to which retailers succeed in reaching

lower down the income scale to reach potential consumers towards the bottom of the consumer pyramid.

This is a challenge that admits no easy solution, say companies. There is no point in going to a destitute

person and saying, here, I’ve got an aftershave lotion for you, says a senior manager at a leading consumer

product company.

You have got to find a relevant product, a needful product. The consumer market remains remarkably

undeveloped. Consumer goods penetration is very low compared to other emerging economies, and

consumer markets have the potential to grow rapidly in the coming decade.

According to a leading company that profiles household spending throughout

Asia, India still has a relatively narrow middle class, reflecting a lower proportion

of urban households compared to some Asian countries. It is estimated that around

70 percent of Indians live in the countryside, compared to around 60 percent of Chinese.

Indian consumers do not follow the consumption patterns seen in other Asian countries. As Indians

have grown richer, they have begun to spend more on vehicles, phones and eating out in restaurants,

according to recent research on consumption patterns. Indians discretionary spending is focused outside

the home; unlike other Asian consumers, they have tended not to greatly increase their spending on clothes,

personal care and household goods.

Consumption is moving out of the home, says a consumer goods producer. It’s

moving into lifestyle products, eating out, events, entertainment. And that is going

to continue. India is also unusual in its patterns of urbanization. The population

of cities has been rising in absolute terms and relative to rural population but at a

rather slow rate, unlike other Asian economies. By 2001, 28 percent of Indians

were living in towns, compared to 39 percent of Chinese and 83 percent of South

Koreans.

Some smaller Indian towns are actually shrinking as Indians congregate

increasingly in larger towns, which now account for more than three-quarters of

the urban population. India’s demographic advantage Increases in wealth,

improvements in life expectancy and increased access to birth control are reducing

fertility rates worldwide. The reduction is most marked in developing countries:

the World Bank’s population data shows that since the 1970s medical care and

birth control have dramatically reduced the number of children born per couple,

and dramatically increased the proportion of citizens living past retirement age.

India, however, is one of the handfuls of countries where the proportion of citizens

of working age is forecast to fall only slowly, and the overall labour force is

growing. A growing labour force both enables higher growth rates and creates an

Urgent political need for growth: according to the Asian Development Bank India will need to achieve

around eight percent average annual growth over the next two decades to create employment for all new

entrants to the workforce.

India’s forecast lower age dependency ratio over the next half-century means that public finances will

come under less strain than in most other countries, making infrastructural investment easier and

allowing the economy to continue growing well above the global trend.

According to the National Council of Applied Economic Research (NCAER), this

pro-growth demographic factor will be an important contributor to the expansion

of consumer markets in India. The NCAER forecasts that the number of

consumers driving growth will grow from 46 million households in 2003 to 124

million households in 2012, which will further drive increased volume in

consumer markets, while increased value will be driven by the fact that consumers are predominantly

young: 54 percent of Indians are under 25 years of age.

For their part companies repeatedly point to the demographic outlook as the most

positive factor in the long-term growth forecast for consumer markets. Policy is

positive at the moment, but demographics are a very important factor, says a

senior manager at a leading consumer product company. Who knows, tomorrow

we may have a communist government, but demographics is something the

government can’t do anything about, so that is a guaranteed positive.

India has sometimes been called a nation of shopkeepers. This epithet has its roots in the huge number of

retail enterprises in India, which totalled over 12 million in 2003. About 78% of these are small family

businesses utilising only household labour. India's retail sector appears underdeveloped not only by the

standards of industrialized countries but also in comparison with several other emerging markets in Asia

and elsewhere. There are only 14 companies that run department stores and two with hypermarkets.

Retail sales now accounts for 44 per cent of the GDP.

Food sales accounts for 63 per cent of the total retail sales, growing to 10 lakh crores from

3.81 lakh crores in 1996.

The organized retail food and grocery sector constitutes the largest opportunity for growth and account for

2% of total sales at present.

Urbanization, working spouses, increasing household disposable incomes and convenience of one stop shop

with good ambience drive growth of retailing in India.

Government policy

There has been vigorous opposition to foreign direct investment (FDI) in

retailing from small traders who fear that foreign retailing companies

would take away their business, lead to the closure of many small trading

businesses and result in considerable unemployment, but the

government has barred FDI in retailing since 1997. Hence, at present,

foreign retailers can only enter the retailing sector through franchising

agreements.

Organizational characteristics

Given the traditional and underdeveloped state of the Indian retail sector,

the organizational characteristics of retail enterprises are rudimentary.

Most of them belong to independent enterprises in the form of small

family businesses.

Cooperatives have been present in India for several decades, spurred by

the encouragement given by the Indian Government, which viewed the

cooperative movement as an integral component of its erstwhile

socialist policies. However, since the 1990s, there has been a reduction

in government support for cooperatives. In 2002, there were about

35,000 outlets run by cooperatives.

Economic liberalization, competition and foreign investment since the 1990s led to a

proliferation of brands with both foreign and Indian companies

acquiring a strong brand equity for their products. Hence, franchising

emerged as a popular mode of retailing. Sales of franchises grew at a

rapid pace of 14% per annum over the review period. In 2002, there

were over 5,000 franchised outlets.

The other major retailing organisation format is multiples, better known

as "chain stores" in

India. In 2002, there were about 1,800 chain stores. Among the various

organizational

formats, sales of chain stores grew at the fastest pace, with sales growth during the review period averaging 24% per year.

India represents an economic opportunity on a massive scale, both as a global base and as a

domestic market. Regulatory controls on foreign direct investment (FDI) have relaxed

considerably in recent years. However, while retailing currently remains closed to FDI, this is

an area of ongoing debate. This means that foreign retailers and consumer goods

manufacturers can only participate in the retail market through indirect access strategies, such

as wholesaling, franchising or licensing, or by having a manufacturing base in India, or in

businesses upstream of retailing. However, the Indian government has indicated in 2005 that

liberalization of direct investment in retailing is under active consideration. Price

controls

have been progressively liberalized since 1992, but a small number of items remain

fully

controlled. There are also extensive controls on packaging, labelling and

certification.

Estimates of the size of the retail sector vary, with recent calculations putting the annual

value of Indian retailing anywhere between US$180 billion and US$292 billion in 2003.

The retail sector is largely made up of what is known in India as the unorganized sector.

This sector consists of small family-owned stores, located in residential areas, with a shop

floor of less than 500 square feet. At present the organized sector (everything other than

these small family-owned businesses) accounts for only 2 to 4 percent of the total market

although this is expected to rise by 20 to 25 percent by 2010.

Many of the companies surveyed believe that the potential size of this market

is underestimated. They consider that there are considerable opportunities for

organized retailers in the kind of rural territories that many companies have failed to

address. A critical issue is how fast and how far the consuming class will grow. This

depends both on the growth of personal disposable income and the extent to which

organized retailers succeed in reaching lower down the income scale to reach potential

consumers towards the bottom of the consumer pyramid.

Companies expect retail growth in the coming five years to be stronger than GDP growth,

driven by changing lifestyles and by strong income growth, which in turn will be supported

by favorable demographic patterns. The structure of retailing will also develop rapidly.

Shopping malls are becoming increasingly common in large cities, and

announced

development plans project at least 150 new shopping malls by 2011. The number of

department stores is growing much faster than overall retail, at an annual 24 percent.

Supermarkets have been taking an increasing share of general food and grocery trade over the

last two decades.

Consumer credit will also grow, assisted by the likely fall in retail lending rates and

more efficient and consumer-friendly lending practices. Distribution continues to improve,

but it still remains a major inefficiency.

Poor quality of infrastructure, coupled with poor quality of the distribution sector, results in

logistics costs that are very high as a proportion of GDP, and inventories which have to be

maintained at an unusually high level. Marketing and advertising are of increasing interest

and concern to consumer companies. Indian consumers are becoming

increasingly

sophisticated and knowledgeable about products; media channels that allow companies

to

communicate with consumers are growing in diversity and reach. Foreign brands remain very

powerful in India, especially in clothing and personal care products, but increasingly brands

have to be associated with value. Advertising is becoming a bigger part of the marketing

mix

ñ companies are concerned about identifying consumer insights and the profusion of media

channels.

Food and beverage offer the greatest organized retail growth opportunities, say companies.

The main growth opportunity in the segment is in processed foods: rapid growth in the

processed food segment is already apparent, changing lifestyles and food habits are resulting

in the rapid expansion of branded food outlet and cafe chains. Gemstones and jewellery

represent the most significant specialist segment of Indian retailing. Organized jewellery

retailers are increasingly offering brand solutions to the demand for quality and value, as

consumers move away from traditional retail settings reliant on family retailers.

All companies agree: Indian consumer markets are changing fast, with rapid growth in

disposable incomes, the development of modern urban lifestyles, and the emergence of the

kind of trend-conscious consumers that India has not seen in the past. Indians are travelling

abroad a lot more, says a representative of an industry association. They get exposed to

what is happening in other markets, they bring back new attitudes and preferences.

But with those changes, companies are adamant that while there are growth opportunities

for

consumer companies, there are few easy pickings. You canít sell junk in India, says a

senior manager in a leading fashion company. it is not like worldwide fashion, where people

might wear a garment three or four times and then discard it. In India you have to

give

value.

Companies are also increasingly keen to bring organized retailing to unvisited arts of

the economy. We think the best opportunities are in rural markets, says a leading shoe

retailer. Our whole strategy is to penetrate the rural market. Distribution remains the

biggest challenge companies face, not least because India’s transport infrastructure

remains weak. Understanding the consumer, understanding the marketing

environment, these are challenges, but distribution is the biggest issue, says a personal

care products company. A leading watch and jewellery company agrees: Distribution and

marketing is a huge cost in Indian consumer markets. It’s a lot easier to cut

manufacturing costs than it is to cut distribution and marketing costs.

Companies expect that the next cycle of change in Indian consumer markets will be the

arrival of foreign players in consumer retailing. Although FDI remains highly restricted in

retailing, most companies believe that will not be for long. The very fact that politicians

have left the issue open leads us to think the restrictions are going to be reviewed, says a

leading sportswear manufacturer. And if retailing is liberalized, say companies, growth will

be boosted, but so will competition. Says a leading shoe retailer: Indian companies know

Indian markets better, but foreign players will come in and challenge the locals by sheer cash

power, the power to drive down prices. That will be the coming struggle.

VISUAL MERCHANDISING

Visual Merchandising is defined as selling a product through a visual medium. It is

arranging items for display and thereby turning a passive looker into an active buyer,

through use of color, texture, composition and visual communication.

EVOLUTION OF VISUAL MERCHANDISING

Visual merchandising is not a newfound tool; it has been around since selling started. When a

vegetable vendor arranges the best of his produce on to for people to touch and feel them, or

when the jeweler puts the best of his pieces on the glass panels for passerbyís to see, itís

visual merchandising at work. Starting from the 1800ís it became associated with retail

industry. The Victorian era made window displays popular and the Great Exhibition of 1851

in London established the prominence of display over the items while commercializing the

practice. In due course visual merchandising became an inalienable part of the fashion and

retail industry.

As far as the term Visual Merchandising is concerned, it became widespread only in 1970

even though it was coined during the 1940s. From the late 1800s till the 1920s, visual

merchandisers were known as window trimmers. By the late 1920s, the window trimmers

were referred to as display men, just as advertising industry called its people ad men. The

industry is evolving and entering new domains, Visual Merchandising is increasingly

perceived as a part of the overall brand communication process.

COMPONENTS OF VISUAL MERCHANDISING

STORE IMAGE

Image can be described as the overall look of a store and the series of mental pictures and

feelings it evokes within the beholder. For the retailer, developing a powerful image provides the

opportunity to embody a single message, stand out from the competition and be

remembered.

As a rule, image is the foundation of all retailing efforts. While store layout, presentation,

signing, displays and events can all change to reflect newness and excitement from week to

week, season to season, they must always remain true to the underlying store image. The

following elements combine to form a distinctive image that not only reaches out and grabs

the customer's attention, but also makes a positive impression within those precious few

seconds. Image forms the solid foundation for the remaining components of Maximizing

Store Impact

STORE DESIGN

Store design plays a crucial role in branding: it reflects and reinforces the corporate image. It

tangiblizes what the retailer claims to be. The sights, sounds, smells and other any other

aspect should therefore reflect what the retailer brand is about and what its attributes are.

Different types of store design are

Grid: it contains long gondolas (a free standing block of shelves used to display goods in a

supermarket) of merchandise and aisles in repetitive pattern.

Racetrack: also known as loop. It provides a major aisle to facilitate customer traffic that has

access to the storeís multiple entrances.

Free Form: also known as boutique; arranges fixtures and aisles asymmetrically.

Visual merchandising creates a connection between the companyís image and the look

of the store.

EXTERIOR DESIGN

STORE NAME

An effective store name sets the tone and provides a store's identification by conjuring up an

image in the customer's mind. An effective name is consistent with both the product mix and the

store atmosphere.

VISUAL TRADEMARK

An identifiable trademark adds a visual image to the memory recall of a store name, by

combining words and pictures, color, shape, typeface, texture and/or style to make it stand

out.

STOREFRONT

Storefront is also an important element, which adds to the store image like the exterior

architecture, signing and window displays.

EXTERIOR ARCHITECTURE

A store's exterior look is often referred to as the architecture, and comprises aspects such as

building materials, architectural style and detail, colors and textures. These elements give a

lasting first impression to the consumer. It is important that the exterior look and ìfeelî right to the

shopper.

STORE SIGN

The store sign is a vital element of the storefront and also an important component of Visual

Merchandising it helps in identifying the store In realizing the value of a strong storefront sign,

many retailers are employing new design techniques which include projecting or

cantilevering the store sign beyond the lease line, adding motion, or using three-dimensional

lettering and unique lighting applications to add depth to the sign.

WINDOWS DISPLAY AND FLOORING

A store's exterior windows or glass storefront provide an additional opportunity to reach out

and grab the passing customer. Windows are integral in creating a positive impression since

they offer an opportunity to begin telling the store's unique merchandise story. The flooring

and the number of floors a retail outlet has, also make an important impact on the consumers.

INTERIOR DESIGN ELEMENTS

The elements of interior design can be used to create an image that matches the desired

customer profile.

FIXTURES

A major consideration in developing an appropriate store design involves the use of fixtures. They

are used to display merchandise, to help sell, to guard it and to provide a storage space for it.

They should be attractive and focus customersí attention and interest on the

merchandise.

DISPLAYS

Displays play an important role in a retail store. An attractive and informative display can help

sell goods. There are several principles that help ensure this effectiveness. They are achieving

balance, provide dominant point, create eye movement etc.

MERCHANDISE PRESENTATION TECHNIQUE

Merchandise Presentation technique is one of the most important component of Visual

Merchandising. The following are the different presentation techniques:

Idea-Oriented Presentation: a method of presenting merchandise based on a specific idea

or image of the store.

Style/Item Presentation: organizing stock by style or item

Color Presentation: A major role in a display is that of the color and lighting.

Aesthetic and innovative use of them can lure customers to visit more aisles than they

usually do and spend more time there.

Price- lining: is the technique when retailers offer a limited number of predetermined price

points within a classification.

Vertical Merchandising: merchandise is presented vertically suing walls and high gondolas

Tonnage Merchandising: here large quantities of merchandise are displayed together to

enhance and reinforce a storeís price image

Frontal Presentation: here the retailer exposes its much of the product as possible to catch

the customerís eye

Fixtures: the primary purposes of fixtures are to efficiently hold and display merchandise.

COLOR

The psychological effect of color continues to be important to retailers. Color probably more than

any other factor except price, is the ìstopperî that catches the consumerís attention. Intelligent

use of color is important in store design.

LIGHTING

Proper lighting is one of the most important considerations in retail outlet. Today lighting has

become a display medium. It is an integral part of the storeís interior and exterior design.

Lighting is used to highlight merchandise, sculpt space and capture a mood or feeling that

enhances the storeís image.

CEILINGS

Ceiling represents a potentially important element of interior design. Ceiling heights, color and

material used will influence the store look.

FLOORING

Flooring choices are important because the coverings can be used to separate departments;

muffs noise in high-traffic areas and strengthen the store image.

SHELVING

The material used for shelving as well as its design must be compatible with the

merchandising strategy and the overall image desired. Music and scent in the retail outlet can

influence consumer behavior to a large extent.

Dos and Don’ts in Visual Merchandising

Dos

Window display should be changed weekly or fortnightly to ensure freshness. The display

and layout should differentiate the store from competition. Colors and design should be

characteristic of the brand image.

Impulse purchase items (perfumes, watch straps, gifts) should be close to the entry and exit

doors for non-serious or causal customers would like to browse the whole store. Their

purchase is not pre-planned and because these impulse purchase items are relatively cheaper they

might buy them in a whim. Also when customers wait at the billing counter the people

accompanying the buyer may snoop around and make a purchase too.

Use symbols as directions.

Control movement and crowd ñ aim of the design.

Distance between the aisles should facilitate the easy for movement shoppers.

Doníts

Avoid too many floors

Racks shouldnít be too high, especially in bookstores because customers might not be able to

reach the books.

Lighting shouldnít be poor and at the same time shouldnít be very bright. Shadows are

essential for that added effect.

The display shouldnít be contrast to the section in which it is. It also shouldnít be

unaesthetic.

The whole point of visual merchandising is to help companies to communicate the brand

message so that consumers can make better-informed choices. Consumers increasingly shop by

what attracts their eye, whether it is perfume, a sandwich or chocolates.

NEED AND IMPORTANCE OF THE STUDY

Marketing products using visual merchandising system is an age-old practice but

with growing growth of retail industry, the art or arguably the science of Visual

Merchandising has gone to occupy a newfound fancy. There is a growing

recognition of the need for an effective Visual Merchandising. But even as it

continues to grow, the understanding of Visual Merchandising impact and

effectiveness is still in its infancy.

The shopping behavior which governs the decision to buy is a function of three stimuli viz.,

visual, auditory and kinesthetic; the visual stimulus is the easiest and most widely used tool for

attracting customers. Although Visual Merchandising has long been an important part of

retailing (clothing, house-wares, etc.) it is not as well known or accepted within the food

industry. While there is substantial amount of research on each of the components of visual

merchandising, a holistic approach towards visual merchandising involving the consumersí

perceptions has not attracted much of research effort, particularly in using the ëGESTALTí

approach to visual merchandising. This is the vital gap in the current research and this has

prompted to take up research investigation in this field.

COMPANY PROFILES

Pantaloon is the company's departmental store and part of life style retail format. In fact,

RIL took its very initial steps in the retail journey by setting up the first Pantaloon store

in Kolkata in 1997. In a short time Pantaloon has been able to carve a special place for it

self in the hearts and minds of the aspirational Indian customers. The company has depth

of offering for both men and women at affordable prices. A striking characteristic of

Pantaloon has been the strength of its private label programme. John Miller, Ajile.

Scottsvile, Lombard, Annabelle are some of the successful brands created by the

company. With 13 stores across the country and an ever-increasing stable of private

brands, Pantaloon - in the coming years is poised to become a leading fashion

trendsetter.

From a humble beginning in 1987, Pantaloon as today evolved as a leading manufacturer-

retailer in the country with 16 Pantaloon stores and 21 hypermarkets(Big Bazaar), 33

Food Bazaars, 3 central, 2 Fashion Station, 2 aLL and 1 MeLa store operational across

the country. It has been a remarkable journey for PRIL as its evolved from a

manufacturing to a completely integrated player controlling the entire value chain.

During its evolution the company achieved various milestone and demonstrated

innovativeness and leadership by pioneering concepts that has now become industry

standards.

Vision:

To be a Global Retailer in India and Maintain No.1 position in the Indian Market in the

Department Store Category.

Positioning

Shoppersí Stop is positioned as a family store delivering a complete shopping experience

defined by its mission, vision and values.

1991: Shoppers' Stop launches at Andheri

Setting up shop in 1991 with its flagship store in Andheri, Mumbai, Shoppersí Stop is a

member of the K. Raheja Corp. of Companies. Shoppersí Stop is the first retail venture by

the K. Raheja Corp. Promoted by Mr. Chandru L. Raheja, Mr. Ravi C. Raheja and Mr. Neel

C. Raheja, the K. Raheja Corp. have been leaders in the construction business for over 48

years.

With its wide range of merchandise, exclusive shop-in-shop counters of international

brands and world-class customer service, Shoppersí Stop brought international standards of

shopping to the Indian consumer providing them with a world class shopping

experience.

India ñ 2000 & BeyondÖ

Expanding its operations to Bangalore, Hyderabad, Jaipur, Delhi, Chennai, Mumbai

(Andheri, Bandra, Chembur, Kandivli, Mulund), Pune, Gurgaon and Kolkata, Shoppersí

Stop is today recognised as Indiaís premier shopping destination. With a customer entry of

about 50,000 customers a day, a national presence with over 6,00,000 square feet of retail

space and stocking over 250 brands of garments and accessories, Shoppersí Stop has

clearly become a one stop shop for all customers.

Customer Profile

Shoppersí Stopís core customers represent a strong SEC A skew. They fall between the

age group of 16 years to 35 years, the majority of them being families and young couples

with a monthly household income above Rs. 20000 and an annual spend of Rs.15000. A

large number of Non - Resident Indians visit the shop for ethnic clothes in the

international environment they are accustomed to.

Range of merchandiseÖ

The stores offer a complete range of apparel and lifestyle accessories for the entire

family. From apparel brands like Provogue, Color Plus, Arrow, Leviís, Scullers, Zodiac to

cosmetic brands like Lakme, Chambor, Le Teint Ricci etc., Shoppersí Stop caters to every

lifestyle need. Shoppers' Stop retails its own line of clothing namely Stop, Life , Kashish,

Vettorio Fratini and DIY. The merchandise at Shoppersí Stop is sold at a quality and price

assurance backed by its guarantee stamp on every bill.

Their motto: ìWe are responsible for the goods we sellî.

Customer Rewards ñ The First Citizen

Shoppersí Stopís customer loyalty program is called The First Citizen. The program

offers its members an opportunity to collect points and avail of innumerable special

benefits. Currently, Shoppersí Stop has a database of over 2.5 lakh members who

contribute to nearly 50% of the total sales of Shoppersí Stop.

International Affiliations

Shoppersí Stop is the only retailer from India to become a member of the prestigious

Intercontinental Group of Departmental Stores (IGDS). The IGDS consists of 29

experienced retailers from all over the world, which include established stores like

Selfridges (England), Karstadt (Germany), Shanghai No. 1 (China), Matahari (Indonesia),

Takashimaya (Japan), C K Tang (Singapore), Manor (Switzerland) and Lamcy Plaza

(Dubai). This membership is restricted to one member organization per country/region.

The Company:

Strong, Competitive, Innovative, Adaptive

History:

Launched in January 1998, Globus is a part of the Rajan Raheja group. The company

opened its first store in 1999 at Indore followed by the launch of its second store in

Chennai (T-Nagar). Soon to follow was another in Chennai located in Adyar. The

flagship store in Mumbai was opened on 1st November 2001 followed by a swanky new

outlet in New Delhi in South Extension Part

The sixth & seventh stores are in Bangalore in Koramangala & Richmond Road

respectively. The Eighth store in Ghaziabad at Shipra Mall followed by the ninth, tenth and

eleventh in Kalaghoda, Mumbai, Thane and Ghaziabad and the twelfth store at

Kanpur. Coming soon to Ahmedabad.

Mission:

Achieve customer delight by offering quality products and services through a

process of continuous innovation and adaptation.

Build a dynamic team of committed and passionate employees through sustained

learning and grooming.

Develop mutually beneficial relationships with our business partners.

Employ cost-effective processes and thereby create a strong organization.

Infrastructure:

Globus Stores Pvt. Ltd. was formed to contribute in the revolution sweeping the retail

industry. Globus promises to bring about a perceptible change in the way apparel and

lifestyle retailing has been carried so far.

Towards this end, modern international technology has been brought in and heavy

investments have been made in investing and acquiring the best, tried and tested

processes and procedures of operation.

Research & Design

Production & Merchandising

Marketing & Brand Development

Service

Human resources

Administering policies & procedures

Future:

Globus combines state of art international information technology, the highest quality

human resources and sustained financial commitment to realize the long term vision. We

are rapidly expanding and the target is to have an additional 100 fashion stores by the end

of 2008.

Style, affordable prices, quality ó these are the factors that have shaped Westsideís

success story in the retail fashion stores business. Launched in 1998 in Bangalore, the

Westside chain has, ever since, been setting the standards for other fashion retailers to

follow.

The Westside story really began in 1997, when the Tatas sold Lakme, their cosmetics

business, to Hindustan Lever and acquired the Britain-based Littlewoods retail chain. A new

entity called Trent Limited emerged from this move and Littlewoods was renamed

Westside. Today Westside has seven outlets, one each in Bangalore, Hyderabad,

Chennai, Mumbai, Pune, New Delhi and Kolkata.

Westside stands out from the competition for a variety of reasons. One is that a majority

of the brands the chain stocks and sells are its own, unlike retailers who store multiple

labels. About 90 per cent of Westsideís offerings are home-grown, and they cater to

different customer segments. The other 10 per cent includes toys, cosmetics and lingerie.

According to Himanshu Chakrawarti, Trentís general manager, this arrangement has many

advantages. "Being a brand retailer, we are able to develop our style and image in a manner

whereby customers can build a relationship with us," he says. "We also have the flexibility of

pricing and are able to fulfil the promise of affordable style." Price is crucial in the Indian

retail scenario and Westsideís focus on this factor is part of the reason it increased sales in

October-December 2001 by a whopping 71 per cent over the same period the previous

year.

Repeat customers, those who keep coming back to Westside, are another vital element in

the chain being a winning proposition. Simone Tata, Trentís chairperson, puts that down

to giving customers something to come back for: "We have something new every week." Mr

Chakrawarti adds that "ultimately itís the products and their quality that makes

customers return again and again".

Visit a Westside store and Mr Chakrawartiís words are clearly confirmed. Each outlet

blends products, ambience, customer service and facilities to create a standout shopping

experience. The stores are spacious (10,000 to 20,000 square feet each), designed to look

and feel international, and products are displayed attractively. The Westside outlets in

Mumbai and Hyderabad have an additional drawing card: Taj CafÈs that serve delicious

pastries, sandwiches and coffee.

Westside has recently expanded its range of merchandise by offering outfits from some of

Indiaís best-known fashion designers, among them Wendell Rodericks, Anita Dongre,

Krishna Mehta and Mona Pali. This is an interesting marketing shift, since it means

moving away from the chainís only-our-own-brands concept.

What was the idea behind the move? According to Mrs Tata, it is Westsideís response to the

increasing demand in India for designer lines. She says: "Designer wear is really an

aspiration product, and it is highly priced. We wanted to offer an affordable selection for

weddings and parties, but since this is still a very small segment we felt it was better to

bring in established designers rather than do it ourselves."

The designers create collections exclusively for the store, and the prices for these are

hardly eye-popping (the Wendell Rodericks range starts at Rs 600). Westside has

managed to obtain this exclusivity at a lower price because it has multiple outlets.

"Designer wear for us is really, to use the phrase, ëthe cherry on the cakeí," adds Mrs

Tata.

Facing the challenge

The greatest challenge for Westside in its quest for a place in the retail sun is not the

competition from similar organised players, but from the unorganised sector (98 per cent of

Indiaís retail garment industry operates in the unorganised sector). According to Mr

Chakrawarti, the task at hand is to get people who usually shop with unorganised players to

visit organised stores such as Westside.

The general perception in India is that organised retailers are far more expensive than

unorganised ones. Westsideís response to this dogmatic view has been to connect price to

quality. "We had to get customers to realise that they were getting the latest style at very

good prices, and in a comfortable environment," says Mr Chakrawarti.

The other challenge for Westside is that the retail fashion business in the country is

becoming increasingly crowded with new players, Indian and foreign. Among the new

entrants have been Wills Sport, Raymonds (Be), Globus, Nike, Crocodile, Mango and,

the latest, Marks & Spencer. But this does not perturb Mr Chakrawarti, who says itís

ironic that while Marks & Spencer is actually a value-for-money brand abroad, it has

positioned itself in India as a high-style clothier, selling at prices way above that of its

competitors.

Customers are what everyone is after, and it is they that Westside is concentrating on.

Continuing research and surveys have helped the chain build on customer loyalty.

"Weíve learned enormously through the years," says Mrs Tata. "It is absolutely essential to

listen to customers ó what they want in terms of style and price, and to understand the

demographics of it all. Itís continuous learning."

An example of this commitment to customers is in the small matter of Westside tailoring

its products to suit particular regions. The chain learnt that customers in south India tend

to be smaller in size than their counterparts in the north, and in some cities women rarely

wear sleeveless dresses. Knowing these facts has helped Westside get the right balance in

terms of products and the people they are intended for.

An assured return-and-exchange policy reinforces customer confidence in the chain. No

questions are asked and a bill is not necessary. "We can do this only because it is our own

merchandise," says Mr Chakrawarti. "Many-brand stores are governed by the exchangeand-

return policy of the various labels they sell."

Bangalore Central

Bangalore Central, Indiaís First and Biggest Seamless Mall in the heart of Bangalore City is

ready to redefine and revolutionise the shopping experience in India. Bangalore

Central, owned by Pantaloon Retail (India) Limited, the leading retailer in India, is

located in the cityís nerve centre, MG Road.

Located in the heart of the city, Bangalore Central houses over 300 brands across

categories, such as apparels, footwear and accessories for women, men, children, infant

basics, apart from a whole range of Music, Books, Coffee Shop, Food Court, Super

Market (Food Bazaar), Fine Dining Restaurant, Pub and Discotheque. The mall also has a

separate section for services such as Travel, Finance, Investment, Insurance,

Concert/Cinema Ticket Booking, Bill Payments and other miscellaneous services.

Bangalore Central also houses Central Square ñ a dedicated space for product launches,

impromptu events, daring displays, exciting shows and art exhibitions.

Bangalore Central conceptualised with a theme and tagline that says ìShop, Eat and

Celebrateî has several unique features. Centralized Billing, Customer friendly

environment and Indiaís first live Radio Central ñ an in-house radio station are only some of

the many things that the retail giant Pantaloons has in the offing for Bangalore

Centralís customers.

Bangalore Central helps the brands in unleashing the complete potential of a brand.

Bangalore Central, because of its seamless nature offers direct walk-ins to the brand. The

consumer gets to experience the brand in a setting that is classy, uniform and bereft of

boundaries. The brands at the Mall have the facility to organize in-store brand

promotions

/ launches / schemes and in turn strengthen their image and branding. The brands are also

laid out in such a way that it is easy for the customers to locate and access a category in

which all the related brands are showcased together. This means that once a customer

walks in to the category, all the brands get the customerís attention.

Commenting on the unique format of Bangalore Central Mall, Mr. Kishore Biyani,

Managing Director, Pantaloon Retail (India) Limited said, ìBangalore Central is based on

the concept of a Seamless Mall with the objective to provide world-class retail experience to

customers and brands. We are extending the retail experience beyond just shopping to

ìShop, Eat and Celebrateî, the spirit that symbolises affluent India. Pantaloons has

always been the pioneers in the retail market and with Central we are hoping to create

new benchmarks in mall managementî

Mr. Muralidharan, Head, Pantaloon Malls, said, ìWith malls mushrooming, our

competitive edge comes from the amount of experience and expertise that Pantaloons has in

retail management, and a keen understanding of consumer needs. With Bangalore

Central, we have not only created a truly world class mall, but have also created a

ëparadigm shiftí in the retail segment, that will be tough to emulate.î

ìAt Bangalore Central, both our customers and the brands have an added advantage as

compared to the large format malls. The well planned and laid out floor with interiors,

common billing, space for individual branding and uniform categorising of various

brands at the mall will assure them consistent footfalls, giving them opportunities to

convert the walk-ins into purchases.î he further added.

About Bangalore Central

Sprawling over 1 lakh 20 thousand sq. ft. area, Bangalore Central has everything a family

would need, for a complete shopping experience. The 6 storied Seamless Mall has

specific areas dedicated to women, men, children, infants, food and beverages, home

appliances and furnishing, toys, play area for children among others.

Bangalore Central is the first of the chain of Central Malls by Pantaloon Retail (India)

Ltd. Central would be opening up their second mall in Hyderabad and third in Pune,

called Hyderabad Central and Pune Central respectively, followed by more in other parts of

the country.

LIFESTYLE

Lifestyle has revolutionised retailing in India by offering a truly international shopping

experience, to become the preferred must-stop for discerning shoppers with a youthful,

vibrant, spicy lifestyle. Launched in 1999 in Chennai, Lifestyle today is one of India's

largest professional retailers with over 325,000 sq. ft. of shopping space across Chennai,

Hyderabad, Bangalore, Gurgaon and Mumbai. With the widest choice of stylish yet

affordable merchandise for the entire family and their home, in a world-class,

shopperfriendly layout, it is one of the most desired shopping destinations in India.

Not surprisingly, Lifestyle's retailing model has also received corporate admiration

by winning the 'Most Respected Company in the Indian Retail Sector' and the 'Most

Admired Large Format Retail Company' awards in India.

Business World-IMRB Most Respected Company Awards Survey has rated Lifestyle as the

Most Respected Company in the retail sector in 2003 and 2004. Lifestyle has also been

awarded the ICICI - KSA Technopak Award for Retail Excellence in 2005 and more

recently the Lycra Images Fashion Awards for the Most Admired Large Format Retailer

of the Year in 2006

Lifestyle is part of the Landmark Group, a Dubai-based retail chain. With over 30 yearsí

experience in retailing, the group has become the foremost retailer in the Gulf. Positioned as

a trendy, youthful and vibrant brand that offers customers a wide variety of

merchandise at an exceptional value for money, Lifestyle India began operations in 1998

with its first store in Chennai in 1999.

RESEARCH DESIGN

STATEMENT OF THE TOPIC

Visual merchandising in select retail units in Bangalore city - a comparative study

OBJECTIVES OF THE STUDY

To understand the dynamics of visual merchandising

To capture the perceptions of consumers towards visual merchandising.

To make appropriate recommendations for an effective visual merchandising

To make a comparative analysis of six different lifestyle stores in Bangalore.

SCOPE OF THE STUDY

This study is limited to a comparative analysis confined to these six lifestyle stores in

Bangalore city only. Further more it covers only the aspects or components of visual

merchandising.

RESEARCH METHODOLOGY

Primary data was collected using the structured questionnaire. A sample size of 150

respondents were chosen through random sampling technique. 25 respondents in each

store were asked to fill the questionnaire.

Construction of questionnaire:

The questionnaire was used as the respondents had to give a specific answer to the

questions. This also made it easier for the respondents to give their opinion without too

much time.

Personal interaction with the consumers at the store and observation techniques were also

used.

Secondary data was collected from various articles published in magazines, internet,

company brochures and publications.

Sample Size: 150 (25 in each store)

Sampling technique: Random Sampling

Limitations of the study:

The project had to be done keeping in mind a time frame.

The study is limited to the stores in Bangalore city only. Branches outside Bangalore are not

taken into account.

DATA ANALYSIS

How important is the ambience of the store while shopping?

Respondents

Very Imp 66

Imp 72

Neither imp nor unimp 7

Not imp 2

Not at all imp 3

150

Importance of ambience while shopping

5%1%2%

Very Imp

44%

48%

Imp

Neither imp nor unimp

Not imp

Not at all imp

Inference: Here we can see that 44% of people feel the ambience is extremely important,

while 48% feel it is important. Hence, retailers should prioritize ambience at the top

while designing the store.

How probable are you to purchase a product without pre planning?

Respondents

Very probable 31

Probable 23

Not probable 37

Not at all probable 59

150

Probability of purchasing without pre -planning

21%

39%

15%

25%

Very probable

Probable

Not probable

Not at all probable

Inference: 36% of the people feel that they might buy a product without pre-planning.

This accentuates the importance of visual merchandising in boosting sales.

Which type of store design would you prefer?

Respondents

Grid 76

Race track 38

Free form 36

150

Rating on dress code

Pantaloons 3.12

Globus 2.92

Westside 2.96

Shoppers Stop 3.16

Lifestyle 3.64

Bangalore Central 3.72

0 1 2 3 4

Inference: This graph shows that out of 150 respondents, 76 prefer the grid type of store

design. The reason for the same is to avoid confusion and free movement from one aisle to

another.

Do you agree that the window display (for the sake of VM) should be changed

weekly or fortnightly to ensure fresh display?

Respondents

Totally agree 82

Somewhat agree 38

Neither agree nor

disagree 12

Somewhat disagree 11

Totally disagree 7

150

Opinion of respondents on window display changes

7% 5% Totally agree

8% Somew hat agree

Neither agree nor disagree55%

25% Somew hat disagree

Totally disagree

Inference: Most of the respondents feel that the display should be changed

weekly/fortnightly to avoid monotony to regular customers.

Do you agree that the impulse items like perfumes watches, socks, ties, gift items

and accessories should be close to the entry and exit doors for non-serious customers

and casual customers so that they can browse the whole store?

Respondents

Totally agree 69

Somewhat agree 23

Neither agree nor

disagree 15

Somewhat disagree 15

Totally disagree 28

150

Display of impulse items at entry and exits

Totally disagree 28

Somew hat disagree 15

Neither agree nor disagree 15

Somew hat agree 23

Totally agree 69

0 10 20 30 40 50 60 70

Inference: Most of the respondents feel that impulse items should be placed close to entry

and exit doors to facilitate easy accessibility to such impulse products.

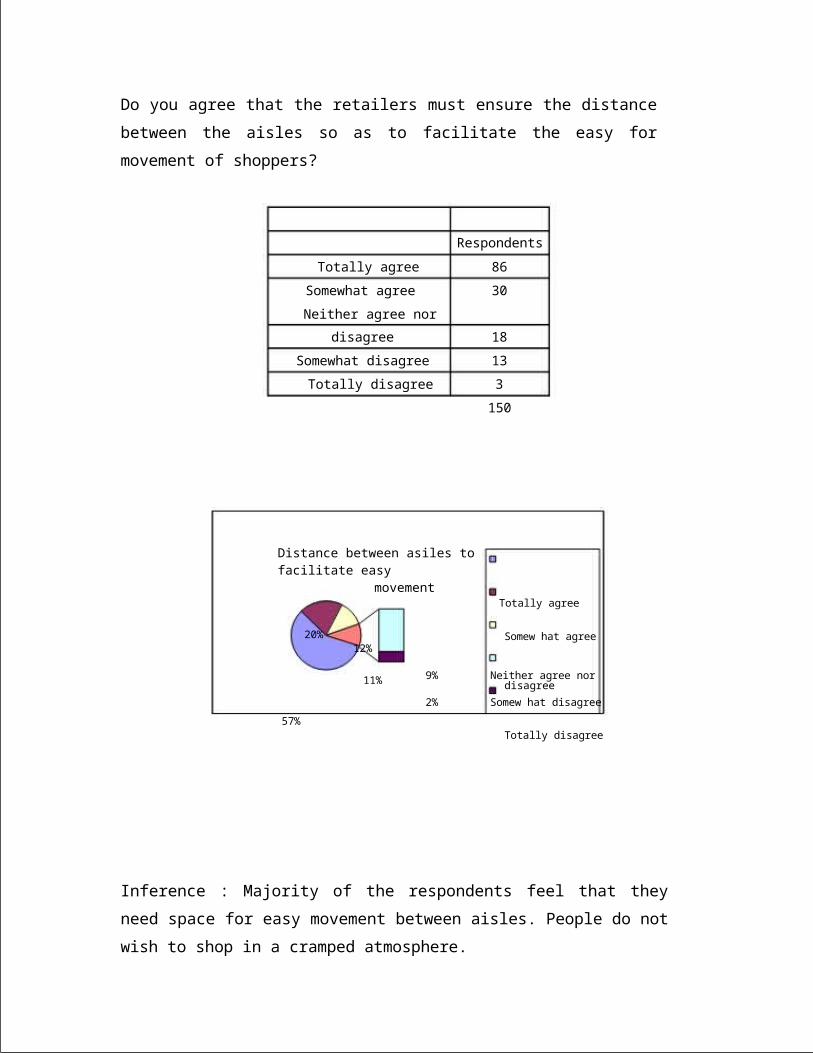

Do you agree that the retailers must ensure the distance between the aisles so as to

facilitate the easy for movement of shoppers?

Respondents

Totally agree 86

Somewhat agree 30

Neither agree nor

disagree 18

Somewhat disagree 13

Totally disagree 3

150

Distance between asiles to facilitate easy movement

Totally agree

20%12%

11%

57%

Somew hat agree

9% Neither agree nordisagree

2% Somew hat disagree

Totally disagree

Inference : Majority of the respondents feel that they need space for easy movement

between aisles. People do not wish to shop in a cramped atmosphere.

Do you agree that the retailers should avoid too many floors because shoppers would be

tired?

Respondents

Totally agree 31

Somewhat agree 36

Neither agree nor

disagree 28

Somewhat disagree 29

Totally disagree 26

150

Opinion on reduction of floors

3640 31 Totally agree

28 29 2630 Somew hat agree

20 Neither agree nor disagree

10 Somew hat disagree

0 Totally disagreeRespondents

Inference: One look at the graph tells us that there is no significant preference with

respect to number of floors. As long as the stores have escalators, shoppers donít mind

moving up and down.

Do you agree that the racks in the stores should not be too high?

Respondents

Totally agree 88

Somewhat agree 34

Neither agree nor

disagree 11

Somewhat disagree 8

Totally disagree 9

150

Racks should not be too high

Totally disagree

9 Somewhat disagree8

Respondents 11 Neither agree nor34 disagree

88 Somewhat agree

0 50 100 Totally agree

Inference: Respondents feel that racks should be low and accessible to view and touch the

product.

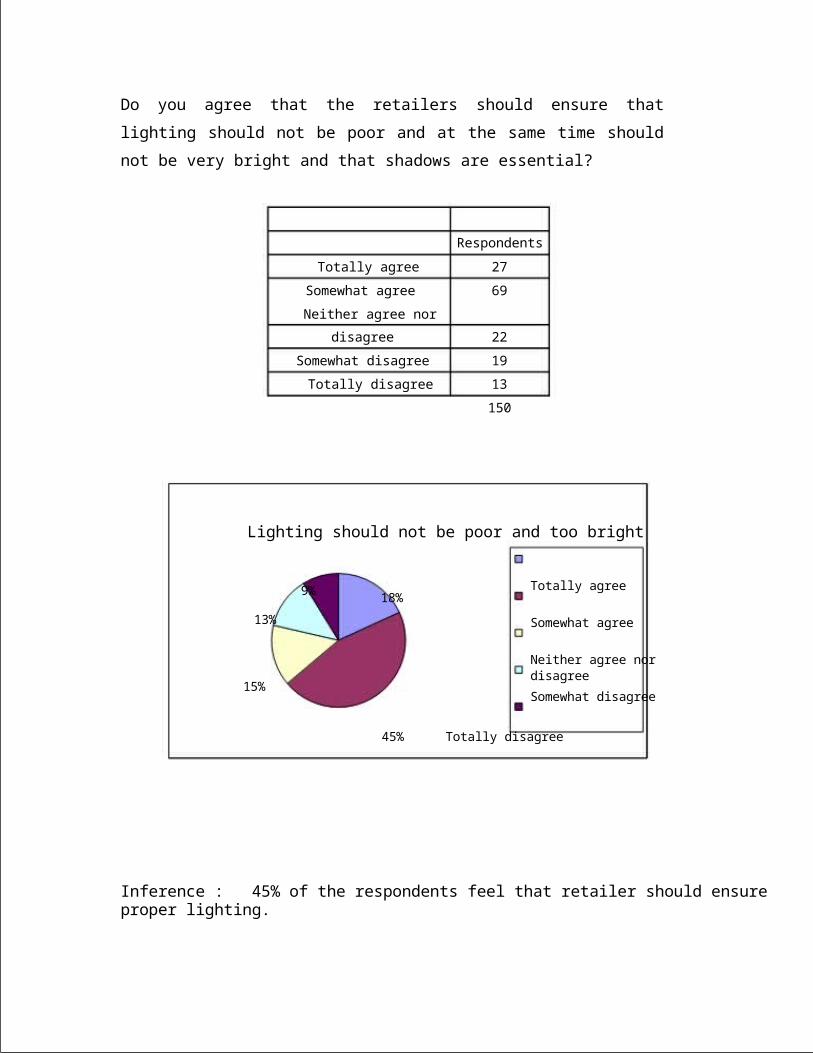

Do you agree that the retailers should ensure that lighting should not be poor and at the

same time should not be very bright and that shadows are essential?

Respondents

Totally agree 27

Somewhat agree 69

Neither agree nor

disagree 22

Somewhat disagree 19

Totally disagree 13

150

Lighting should not be poor and too bright

9%

13%

15%

Totally agree18%

Somewhat agree

Neither agree nordisagree

Somewhat disagree

45% Totally disagree

Inference : 45% of the respondents feel that retailer should ensure proper lighting.

Do you agree that the VM should be powerful enough to enable that the customers to

visit as many aisles as possible?

Respondents

Totally agree 93

Somewhat agree 26

Neither agree nor

disagree 14

Somewhat disagree 9

Totally disagree 8

150

VM should be powerful enough to makecustomers visit all aisles

100

80

60

40

20

0Respondents

Totally agree

Somewhat agree

Neither agree nor disagree

Somewhat disagree

Totally disagree

Inference : Most of the respondents feel that visual merchandising should be powerful

enough so that customers visit maximum number of aisles. Ultimately a retailer would

want his shoppers to visit as many aisles as possible. Visual merchandising is a powerful

tool for the same.

Do you agree that the exposure through VM is a significant variable in consumer

decision-making?

Respondents

Totally agree 79

Somewhat agree 47

Neither agree nor

disagree 6

Somewhat disagree 7

Totally disagree 11

150

Importance of VM in purchase decision

7%5%

4%

53%

31%

Totally agree

Somewhat agree

Neither agree nor disagree

Somewhat disagree

Totally disagree

Inference : Most of the respondents feel that visual merchandising play an important role in

consumer buying decision. Hence it is vital to ensure that all components of visual

merchandising are given utmost importance.

Do you agree that VM is not just physical, architectural exercise, it must encompass

aesthetics, the customers' desires and the business?

Respondents

Totally agree 84

Somewhat agree 37

Neither agree nor

disagree 12

Somewhat disagree 6

Totally disagree 11

150

VM is not just physical, architectural exercise, it

must encompass

4%

8%

25%

7% Totally agree

Somewhat agree

Neither agree nor

56% disagreeSomewhat disagree

Totally disagree

Inference : Most of the respondents feel that visual merchandising is done to suit their

needs, wants and preferences.

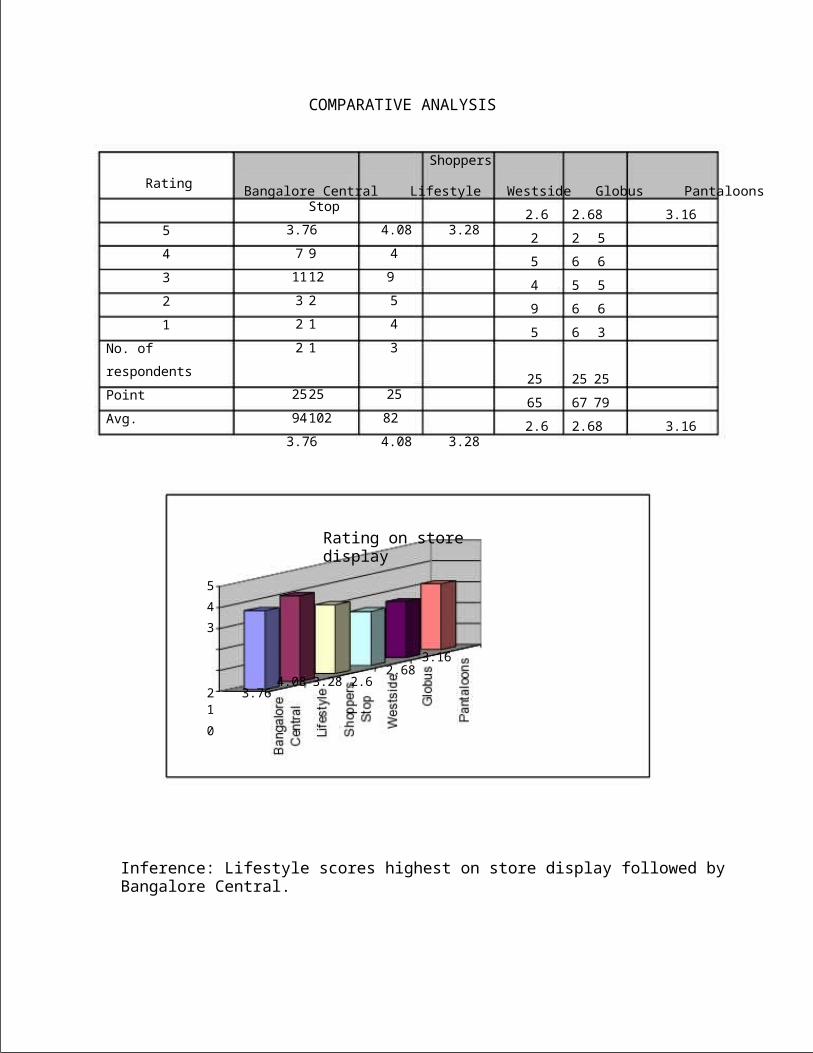

COMPARATIVE ANALYSIS

Shoppers

Rating

5

4

3

2

1

No. of

respondents

Point

Avg.

5

4

3

Bangalore Central Lifestyle Stop

3.76 4.08 3.28

7 9 4

1112 9

3 2 5

2 1 4

2 1 3

2525 25

94102 82

3.76 4.08 3.28

Rating on store display

3.162.68

Westside Globus Pantaloons

2.6 2.68 3.16

2 2 5

5 6 6

4 5 5

9 6 6

5 6 3

25 25 25

65 67 79

2.6 2.68 3.16

4.08 3.28 2.62 3.761

0

Inference: Lifestyle scores highest on store display followed by Bangalore Central.

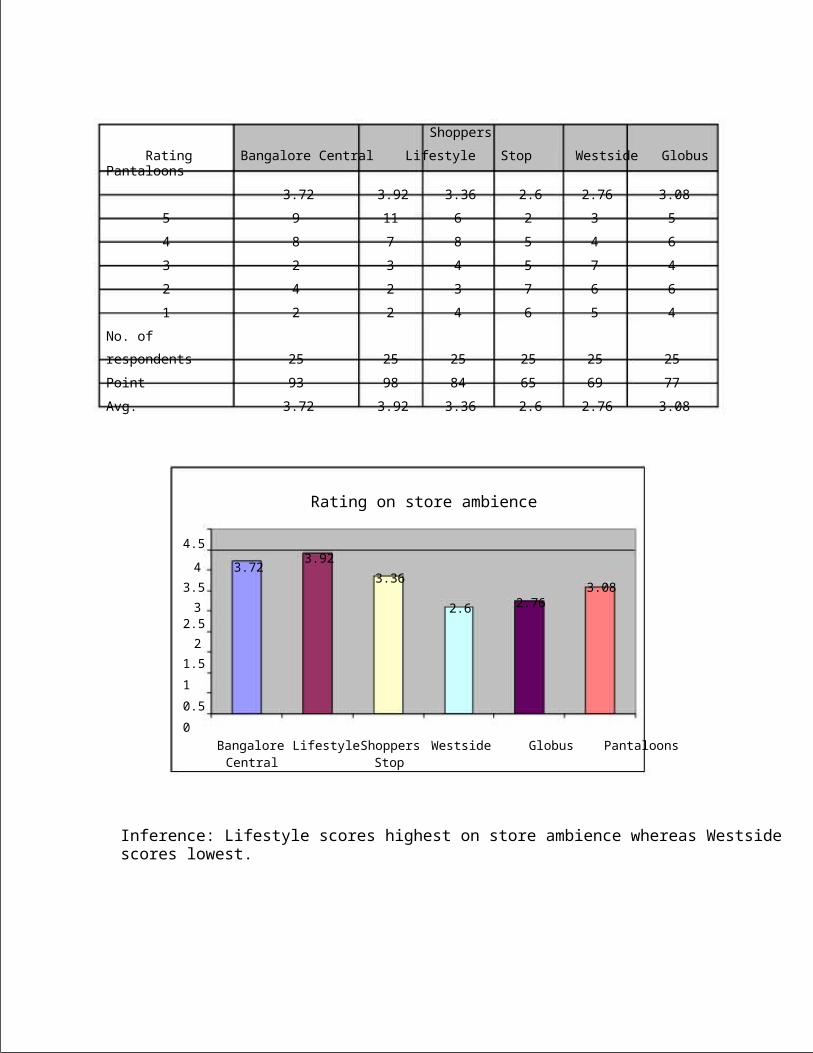

Shoppers

Rating Bangalore Central Lifestyle Stop Westside Globus Pantaloons

3.72 3.92 3.36 2.6 2.76 3.08

5 9 11 6 2 3 5

4 8 7 8 5 4 6

3 2 3 4 5 7 4

2 4 2 3 7 6 6

1 2 2 4 6 5 4

No. of

respondents 25 25 25 25 25 25

Point 93 98 84 65 69 77

Avg. 3.72 3.92 3.36 2.6 2.76 3.08

Rating on store ambience

4.5

4 3.723.92

3.53.36

3.08

3 2.6 2.76

2.5

2

1.5

1

0.5

0

Bangalore Lifestyle Shoppers Westside Globus PantaloonsCentral Stop

Inference: Lifestyle scores highest on store ambience whereas Westside scores lowest.

Bangalore Shoppers

Rating Central Lifestyle Stop Westside Globus Pantaloons

3.52 3.76 3.32 2.56 2.84 2.96

5 5 7 5 2 3 4

4 11 10 8 5 6 6

3 3 4 6 6 5 4

2 4 3 2 4 6 7

1 2 1 4 8 5 4

No. of

respondents 25 25 25 25 25 25

Point 88 94 83 64 71 74

Avg. 3.52 3.76 3.32 2.56 2.84 2.96

Rating on store planning and design

4 2.962.84 Bangalore Central

3 3.32 2.563.76 Lifestyle

2 3.52 Shoppers Stop

1 Westside

0 Globus1 Pantaloons

Inference: Lifestyle scores highest on store planning and design followed by Bangalore

Central whereas Westside scores lowest among all.

Shoppers

Rating Bangalore Central Lifestyle Stop Westside Globus Pantaloons

3.72 3.68 3.44 2.64 2.8 3.24

5 7 8 6 3 4 5

4 10 9 9 5 6 5

3 4 3 3 4 5 6

2 2 2 4 6 3 7

1 2 3 3 7 5 4

No. of

respondents 25 25 25 25 23 27

Point 93 92 86 66 70 81

Avg. 3.72 3.68 3.44 2.64 2.8 3.24

Rating on store windows

43.5

32.5

21.5

10.5

0

3.723.68

3.443.24

2.64 2.8

S1

Inferences: Bangalore Central scores highest among all on store windows.

Bangalore Shoppers

Rating Central Lifestyle Stop Westside Globus Pantaloons

3.64 3.36 3.16 2.76 3 2.88

5 8 6 5 4 5 4

4 7 7 7 5 4 6

3 4 6 5 4 7 4

2 5 2 3 5 4 5

1 1 4 5 7 5 6

No. of

respondents 25 25 25 25 25 25

Point 91 84 79 69 75 72

Avg. 3.64 3.36 3.16 2.76 3 2.88

Rating on flooring

Pantaloons 2.88

Globus 3

Westside 2.76

Shoppers Stop 3.16

Lifestyle 3.36

Bangalore Central 3.64

0 0.5 1 1.5 2 2.5 3 3.5 4

Inference: Among the six retailers flooring of Bangalore Central is rated highest.

Bangalore

Rating Central

3.4

5 5

4 9

3 4

2 5

1 2

No. of

respondents 25

Point 85

Avg. 3.4

Pantaloons

Globus

Westside

Shoppers Stop

Lifestyle

Bangalore Central

0

Shoppers

Lifestyle Stop

3.76 3.48

87

86

56

34

12

25 25

94 87

3.76 3.48

Rating on store signs

1 2

Westside Globus Pantaloons

2.92 3 3.24

4 4 5

6 6 8

4 6 5

6 4 2

5 5 5

25 25 25

73 75 81

2.92 3 3.24

3.24

3

2.92

3.48

3.76

3.4

3 4

Inference: On store signs respondents feel Lifestyle is the best and most informative.

Shoppers

Rating Bangalore Central Lifestyle Stop Westside Globus Pantaloons

3.68 3.96 3.28 2.96 2.96 3.12

5 6 9 5 6 5 6

4 11 10 8 5 4 5

3 4 3 4 3 7 4

2 2 2 5 4 3 6

1 2 1 3 7 6 4

No. of respondents 25 25 25 25 25 25

Point 92 99 82 74 74 78

Avg. 3.68 3.96 3.28 2.96 2.96 3.12

Rating on store design

Pantaloons 3.12

Globus 2.96

Westside 2.96

Shoppers Stop 3.28

Lifestyle 3.96

Bangalore Central 3.68

0 0.5 1 1.5 2 2.5 3 3.5 4

Inference: Lifestyle scores highest on store design followed by Bangalore Central

whereas Globus and Westside scores lowest among all.

Bangalore Shoppers

Rating

5

4

3

2

1

No. of

respondents

Point

Avg.

3.4

1

Central Lifestyle Stop Westside Globus Pantaloons

3.4 3.92 3.28 2.96 2.88 3.16

7 8 6 3 4 5

6 11 5 5 6 7

5 3 7 9 3 4

4 2 4 4 7 5

3 1 3 4 5 4

25 25 25 25 25 25

85 98 82 74 72 79

3.4 3.92 3.28 2.96 2.88 3.16

Rating on fixture & hardware

4

3.16 3

2.883.92 3.28 2.96 2

1

0 Bangalore CentralLifestyle

Shoppers Stop

Westside

Globus

Pantaloons

Inference: In terms of fixture and hardware respondents feel that Lifestyle is best among

all.

Bangalore Shoppers

Rating

5

4

3

2

1

No. of

respondents

Point

Avg.

4.54

3.5

Central Lifestyle Stop Westside Globus Pantaloons

3.6 3.36 3.92 2.92 3.08 3.24

6 6 8 3 5 6

8 7 9 6 7 5

7 5 6 7 3 7

3 4 2 4 5 3

1 3 0 5 5 4

25 25 25 25 25 25

90 84 98 73 77 81

3.6 3.36 3.92 2.92 3.08 3.24

Rating on props & decorative items

3.923.6 3.36

3 2.92 3.08 3.24

2.5 2 1.5 1 0.5 0

Bangalore Lifestyle Shoppers Westside Globus PantaloonsCentral Stop

Inference: Respondents rate Shoppers Stop highest in terms of props and decorative

items.

Bangalore

Rating Central

3.76

5 8

4 9

3 4

2 2

1 2

No. of

respondents 25

Point 94

Avg. 3.76

5432 3.76 3.9210

Bangalore LifestyleCentral

Shoppers

Lifestyle Stop

3.92 3.2

9 4

10 8

2 6

3 3

1 4

25 25

98 80

3.92 3.2

Rating on with colors

3.2 2.84

Shoppers WestsideStop

Westside Globus Pantaloons

2.84 2.68 3.24

3 2 5

5 5 6

6 8 5

7 3 8

4 7 1

25 25 25

71 67 81

2.84 2.68 3.24

2.68 3.24

Globus Pantaloons

Inference: Lifestyle scores highest on colors followed by Bangalore Central.

Bangalore

Rating Central

3.56

5 6

4 10

3 3

2 4

1 2

No. of

respondents 25

Point 89

Avg. 3.56

4

3.5

3

2.5

2

1.5

1

0.5

0

Shoppers

Lifestyle Stop

3.88 3.28

8 5

11 8

2 4

3 5

1 3

25 25

97 82

3.88 3.28

Rating on lighting

Westside Globus Pantaloons

2.92 3 3.32

3 4 6

5 6 7

9 5 4

3 6 5

5 4 3

25 25 25

73 75 83

2.92 3 3.32

Bangalore Central

Lifestyle

Shoppers Stop

Westside

Globus

Pantaloons

Bangalore Lifestyle Shoppers Westside Globus PantaloonsCentral Stop

Inference: Respondents feel that lighting of Lifestyle is best when compared to the other

five.

Bangalore Shoppers

Rating Central Lifestyle Stop Westside Globus Pantaloons

3.72 3.64 3.16 2.96 2.92 3.12

5 9 8 6 3 4 4

4 8 7 5 6 7 6

3 3 5 4 7 3 7

2 2 3 7 5 5 5

1 3 2 3 4 6 3

No. of

respondents 25 25 25 25 25 25

Point 93 91 79 74 73 78

Avg. 3.72 3.64 3.16 2.96 2.92 3.12

Rating on dress code

Pantaloons 3.12

Globus 2.92

Westside 2.96

Shoppers Stop 3.16

Lifestyle 3.64

Bangalore Central 3.72

0 1 2 3 4

Inference: Respondents feel that dress code of Bangalore Central is most appropriate in

comparison to the other five.

Bangalore Central Lifestyle Shoppers Stop Westside Globus Pantaloons

3.64 3.80 3.34 2.80 2.91 3.17

Store Display 3.76 4.08 3.28 2.6 2.68 3.16

Ambience 3.72 3.92 3.36 2.6 2.76 3.08

Store

Planning and

Design 3.52 3.76 3.32 2.56 2.84 2.96

Store

Windows 3.72 3.68 3.44 2.64 2.8 3.24

Flooring 3.64 3.36 3.16 2.76 3 2.88

Displays 3.8 4.16 3.32 2.8 3.28 3.44

Signs 3.4 3.76 3.48 2.92 3 3.24

Space Design 3.68 3.96 3.28 2.96 2.96 3.12

Fixture and

Hardware 3.4 3.92 3.28 2.96 2.88 3.16

Props and

Decorative

Items 3.6 3.36 3.92 2.92 3.08 3.24

Colors 3.76 3.92 3.2 2.84 2.68 3.24

Lighting 3.56 3.88 3.28 2.92 3 3.32

Dress Code 3.72 3.64 3.16 2.96 2.92 3.12

Cumulative

Score 47.28 49.4 43.48 36.44 37.88 41.2

Average 3.64 3.80 3.34 2.80 2.91 3.17

Average Rating

4.00 3.64 3.80

3.50

3.00

2.50

2.00

1.50

1.00

0.50

0.00

Bangalore LifestyleCentral

3.34 3.17

2.80 2.91

Shoppers Westside Globus PantaloonsStop

Inference: Based on the thirteen parameters we arrive at the average rating for each store.

Lifestyle is rated highest and follows the best practices of visual merchandising.

Lifestyle: Out of thirteen parameters Lifestyle got top rating in nine. Currently it is

practicing the best visual merchandising techniques. The respondents are extremely

satisfied with Lifestyle in terms of visual merchandising. But there is an area for

improvement in store windows, flooring, props, decorative items and appropriateness of

dress code.

Bangalore Central: Bangalore Central is a close second behind Lifestyle. In terms of

store windows, flooring and appropriateness of dress code, it is rated number one by

respondents. It requires marginal improvement in most of the areas mentioned to beat

Lifestyle. Overall respondents were satisfied.

Shoppers Stop: Shoppers Stop comes third just behind Bangalore Central. Shoppers

Stop could improve on fixtures to display its line of apparel more effectively. Shirts were

displayed on shelves in Lifestyle which were more attractive than hangars used in

Shoppers Stop.

Pantaloons: Pantaloons could improve on flooring which is not appealing when

compared to the other five stores. Store display could also be improved. Most of the

parameters were given an average rating by the respondents.

Globus: Window display is virtually non existent. The only attractive feature of this store is

a hoarding of brand ambassador ìSoha Ali Khanî at the entrance of the store.

Westside: The interesting thing about Westside is that while going up the escalator,

strategic placement of gift items hits you in the face. This feature is unique to Westside.

However it needs improvement in all other areas of Visual Merchandising.

FINDINGS AND RECOMMENDATIONS

The ambience of the store is a very important element in Visual Merchandising as it

influences consumers in purchase decision. A customer is highly influenced by the look

and feel of the store. The minute he/she walks in, an image of the store is formed. This

image is extremely important to the retailer if he wants to bag a new customer. Hence the

ambience is to be given utmost importance. A retailer needs to hire a good interior

decorator and if possible use ergonomics while designing a store.

Visual merchandising will lead to impulse purchase of the product. Visual merchandising

is used to attract shoppers to view the product more closely. Effective visual

merchandising is essential to attract shoppers enticing them to make a purchase. Effective

visual merchandising should also be supported by good sales staff to close deals with

shoppers.

Visual Merchandising enhances the pleasure of shopping experience.

Store windows can be used effectively to entice people on the streets to walk into the

store.

Promotions, props and decorative items are huge attractions with regard to visual

merchandising. Unfortunately, stores use these tools only during festivals and

anniversaries.

CONCLUSION

This project has helped me understand the importance and significance of visual

merchandising and its impact on consumer buying behavior. It has given me exposure to

the practical side of retailing and at the same time enhanced my knowledge by applying

theory learnt in class to practice.

Visual merchandising when used effectively is no doubt, a powerful tool to entice

customers in making a purchase decision. Retailers can attract more customers and

increase sales by proper use of visual merchandising techniques.

BIBLIOGRAPHY

BOOKS:

Retail Management By Ron Hasty & James Reardon

Marketing Management - Philip Kotler

Research Methodology ñ Cooper and Schindler

JOURNALS AND MAGAZINES :

4 Ps

Business World

Business Today

ANNEXURES

I am a student of Christ University, Bangalore, pursuing BBA Program. As a part of the BBA curriculum, I have taken up a research project on VISUAL MERCHANDISING IN RETAIL UNITS. In this connection, I need some information. Below is the questionnaire. Kindly give your responses to the questions in the questionnaire. I sincerely assure your responses will be kept strictly confidential and shall only be used for academic purpose. I shall greatly appreciate your cooperation in completing my research project.

Mr. Sandipan Sarkhel

Visual Merchandising is defined as selling a product through a visual medium. It is

arranging items for display and thereby turning a passive looker into an active buyer, through use of

color, texture, composition and visual communication.

1 How often do you visit the store?

Weekly

Fortnightly

Monthly

Others (please specify)

2 How important is the ambience of the store while shopping?

Very important

Important

Neither important nor unimportant

Not important

Not at all important

3 How pleased are you with store display?

Very pleased

Pleased

Neither pleased nor displeased

Displeased

Very displeased

4 How appealing is the lighting, choice of colors, and material in the store?

Very appealing

Appealing

Neither appealing nor unappealing

Not appealing

Not at all appealing

5 How appropriate is the dress code of the staff?

Very appropriate

Appropriate

Neither Appropriate nor inappropriate

Not appropriate

Not at all appropriate

6 How would you rate the store on the following aspects?

Ambience

Store planning and

design

Store windows

Flooring

Displays

Signs

Space design

Fixture and hardware

Props and decorative

items

Colors

Lighting

Excellent Very Good Good Average Poor

7 How probable are you to purchase a product without pre planning?

Very probable

Probable

Not probable

Not at all probable

8 How informative are the signs in the store?

Very informative

Informative

Not informative

Not at all informative

9 Do you agree that different stores that cater to different customers need to

be different in their internal design?

Totally agree

Somewhat agree

Neither agree nor disagree

Totally disagree

Somewhat disagree

10 Do you agree that the visual merchandising help retailers to communicate retail

brand message so that the customers can make better informed choices?

Totally agree

Somewhat agree

Neither agree nor disagree

Somewhat disagree

Totally disagree

11 Which type of store design would you prefer?

Grid

Race track

Free-form

12 Do you agree that the window display (for the sake of VM) should be changed

weekly or fortnightly to ensure fresh display?

Totally agree

Somewhat agree

Neither agree nor disagree

Totally disagree

Somewhat agree

13 Do you agree that the impulse items like perfumes watches, socks, ties, gift items

and accessories should be close to the entry and exit doors for non-serious customers

and casual customers so that they can browse the whole store?

Totally agree

Somewhat agree

Neither agree nor disagree

Totally disagree

Somewhat agree

14 Do you agree that the retailers must ensure control movement and crowd in terms of

strategic positions of the exit doors?

Totally agree

Somewhat agree

Neither agree nor disagree

Totally disagree

Somewhat disagree

15 Do you agree that the retailers must ensure the distance between the aisles so as to

facilitate the easy for movement of shoppers?

Totally agree

Somewhat agree

Neither agree nor disagree

Totally disagree

Somewhat disagree

16 Do you agree that the retailers should avoid too many floors because shoppers would

be tired?

Totally agree

Somewhat agree

Neither agree nor disagree

Totally disagree

Somewhat disagree

17 Do you agree that the racks in the stores should not be too high?

Totally agree

Somewhat agree

Neither agree nor disagree

Totally disagree

Somewhat disagree

18 Do you agree that the retailers should ensure that lighting should not be poor and at

the same time should not be very bright and that shadows are essential?

Totally agree

Somewhat agree

Neither agree nor disagree

Totally disagree

Somewhat disagree

19 Do you agree that the store display should not be contrast to the section in which

it is and should not be unaesthetic?

Totally agree

Somewhat agree

Neither agree nor disagree

Totally disagree