Embed Size (px)

Citation preview

© Beta Educational Services, LLC, 2016.

Time Value of Money Effective Annual Return

Practice Question An investment returns 8% semiannually. What is its effective annual return?

Practice Question An investment returned 12% over 3 years. What was its effective annual return?

1

© Beta Educational Services, LLC, 2016.

Practice Question

Question Inflation = 2%. What is the nominal return that an investor would need to achieve a real return of 6%?

(a) 3.92%

(b) 6.00%

(c) 8.00%

(d) 8.12%

2

© Beta Educational Services, LLC, 2016.

Time Value of Money Effective Annual Return

Practice Question A $10,000 90-day treasury bill is currently priced at $9,850. Which comes closest to its effective annual return?

(a) 1.50%

(b) 3.30%

(c) 4.50%

(d) 6.30%

Practice Question What is the geometric average of the following returns?

25%, -10%, 8%, 2%

3

© Beta Educational Services, LLC, 2016.

Time Value of Money Time Weighted and Dollar Weighted Returns

Example Given the following information, compute the time-weighted and dollar-weighted returns.

4

Year ContributionsBeg. of Year

ValueEnd of Yr

2009 $700,0002010 +$50,000 $900,0002011 -$40,000 $1,000,000

© Beta Educational Services, LLC, 2016.

Time Value of Money Time Weighted and Dollar Weighted Returns

Example Given the following information, compute the time-weighted and dollar-weighted returns.

5

Year ContributionsEnd of Year

ValueEnd of Yr

2009 $45,000 $700,0002010 +$50,000 $900,0002011 -$40,000 $1,000,000

© Beta Educational Services, LLC, 2016.

Time Value of Money Bond Price and Savings

Practice Question What is the price of a 15-year, $1,000 bond that pays annual coupons of 5% and has a yield-to-maturity of 7%?

Practice Question An investor plans to save $25,000 a year, starting next year, for the next 20 years. He plans to invest the money in a fund that has a compounded annual return of 6%. If the S&P500 returns 7% and inflation is 3%, how much will the investor have in 20 years?

6

© Beta Educational Services, LLC, 2016.

Time Value of Money Real Rate of Return and Convertible Bond

Practice Question Emmett Brown saved $100,000 10 years ago in an investment that provided an annual return of 6%. Average annual inflation over the time period was 3%. What was his average annual real rate of return?

(a) 2.91%

(b) 6.00%

(c) 9.03%

Practice Question A 12-year $1,000 convertible bond that pays annual coupons of 6% is currently priced at $1,020. It has a YTM of 6.5% and is convertible into 40 shares of the company’s stock. The stock is currently price at $25. Compute the conversion premium.

(d) $0

(e) $20

(f) $40

(g) $60

7

© Beta Educational Services, LLC, 2016.

Interest Rate Risk Practice Question

Practice Question The current interest rate environment presents a yield curve that is increasing. Which of the following is the least risky investment?

(a) A

(b) B

(c) C

(d) D

Four Situational Investing

Bond Maturity CouponA 5 10%B 6 5%C 11 10%D 10 5%

8

© Beta Educational Services, LLC, 2016.

Asset and Liability Management Which Risk?

Practice Question A client has a target liability duration of 6. Her assets are invested in a portfolio of bonds with a duration of 8.4. Which of the following risk is more dominant?

(a) Market Risk

(b) Price Risk

(c) Reinvestment Risk

(d) Idiosyncratic Risk

(e) Interest Rate Risk

9

© Beta Educational Services, LLC, 2016.

Asset and Liability Management Which Risk?

Practice Question A client has a target liability duration of 10. Her assets are invested in a portfolio of bonds with a duration of 8.4. Which of the following risk is more dominant?

(a) Market Risk

(b) Price Risk

(c) Reinvestment Risk

(d) Idiosyncratic Risk

10

© Beta Educational Services, LLC, 2016.

Asset and Liability Management Immunizing

Practice Question A client has a target liability duration of 9. Which of the following allocation in the following bonds would have the client immunized?

(a) 80% in A and 20% in B

(b) 60% in A and 40% in B

(c) 40% in A and 60% in B

(d) 80% in A and 20% in B

11

Bond Duration

A 3

B 13

© Beta Educational Services, LLC, 2016.

Portfolio Theory Standard Deviation and Variance

Standard Deviation ~

Applications of standard deviation (and variance)

12

© Beta Educational Services, LLC, 2016.

Portfolio Theory and Computing Risk Standard Deviation and Variance

Practice Question Given the following information, compute the expected return and the standard deviation.

13

Probability Return0.6 0.20.3 0.050.1 -0.06

© Beta Educational Services, LLC, 2016.

Computing Risk Standard Deviation and Variance

Practice Question Given the following which comes closest to the variance of returns.

(a) 32

(b) 27

(c) 12

(d) 5

Returns8%11%-3%4%

14

© Beta Educational Services, LLC, 2016.

Portfolio Theory and Computing Risk Value at Risk

Value at Risk

Practice Question A fund has a daily average return of .03% and standard deviation of 1.6%. What is the 95% VaR?

(a) -1.43%

(b) -2.02%

(c) -2.61%

(d) -3.70%

V aR = Avg � Z↵�

Zα = 1.28 for 90%Zα = 1.65 for 95%Zα = 2.33 for 99%

15

© Beta Educational Services, LLC, 2016.

Computing Risk Annualizing Standard Deviation

The quarterly standard deviation is 5%. Compute the annual standard deviation.

The monthly standard deviation of Fund XYZ is 6%. Compute the annual standard deviation.

16

© Beta Educational Services, LLC, 2016.

Portfolio Theory and Computing Risk Value at Risk

Practice Question A fund has an annual standard deviation of 20%. At what critical level is a monthly VaR of 7.39%?

(a) 68%

(b) 90%

(c) 95%

(d) 99%

17

© Beta Educational Services, LLC, 2016.

Portfolio Theory and Computing Risk Value at Risk

Practice Question A fund has a daily standard deviation of 1%. What is the critical value of a 30-day VaR of 7.01?

(a) 68%

(b) 90%

(c) 95%

(d) 99%

18

© Beta Educational Services, LLC, 2016.

Portfolio Theory Semi Deviation - Semi Variance

Semi Deviation

Applications of semi deviation (and semi variance)

Question: Which of the following is more appropriate to measure the downside

(a) Standard Deviation

(b) Correlation

(c) Semi Deviation

19

(a) Variance

(b) CoVariance

(c) Semi Variance

© Beta Educational Services, LLC, 2012.

Portfolio Theory Correlation - Covariance

Correlation

Applications of correlation (and covariance)

20

© Beta Educational Services, LLC, 2016.

Portfolio Theory Correlation and Covariance

Practice Question Given the following information, compute the correlation between the S&P 500 and MSCI FM.

21

Asset Return Std DeviationMSCI FM 0.09 0.22S&P 500 0.08 0.16

Covariance between SP500&MSCI FM = .0176

© Beta Educational Services, LLC, 2012.

Portfolio Theory Beta

Beta

Applications of Beta

22

© Beta Educational Services, LLC, 2016.

Portfolio Theory Beta

Practice Question Given the following information, compute the beta of MSCI FM to the S&P 500.

23

Asset Return Std DeviationMSCI FM 0.09 0.22S&P 500 0.08 0.16

Covariance between SP500&MSCI FM = .0176

© Beta Educational Services, LLC, 2016.

Benchmarking and Attribution Tracking Error

Tracking Error ~ Volatility of Excess Return

Applications of Tracking Error

© Beta Educational Services, LLC, 2012.

Portfolio Theory Return, Duration, Beta

Compute the Return of the Portfolio (Rp)

Compute the Duration of the Portfolio (Dp)

Compute the Beta of the Portfolio (βp)

Compute standard deviation of the portfolio (σp).

Asset Weights Return Duration Beta Std Dev

A 0.8 0.2 20 2 0.2

B 0.2 0.1 10 1 0.1

25

© Beta Educational Services, LLC, 2016.

Computing Risk Standard Deviation of a Portfolio

Practice Question The correlation between the two assets is .30, compute the return and the standard deviation of the portfolio.

Asset Weights Return Std DeviationAsset A 0.8 0.04 0.08Asset B 0.2 0.08 0.16

26

© Beta Educational Services, LLC, 2016.

Computing Risk Standard Deviation of a Portfolio

Practice Question What is the standard deviation of a portfolio that is equally weighted between the S&P 500 and the MSCI FM?

27

Asset Return Std DeviationMSCI FM 0.09 0.22S&P 500 0.08 0.16

Covariance between SP500&MSCI FM = .0176

© Beta Educational Services, LLC, 2016.

Portfolio Theory The Opportunity Set

When correlation = 1, there is no advantage to diversification

When correlation = -1, we can create a risk free asset

28

7.5%

8.5%

9.5%

0% 4.4% 8.8% 13.2% 17.6% 22%

Asset Return Std DeviationS&P 500 0.08 0.16

MSCI FM 0.09 0.22

S&P 500

MSCI FM

© Beta Educational Services, LLC, 2016.

Portfolio Theory The Optimal Portfolio29

4%

6.75%

9.5%

0% 4.4% 8.8% 13.2% 17.6% 22%

Corr. = .5

Asset Return Std DeviationS&P 500 0.08 0.16

MSCI FM 0.09 0.22

MSCI FM40% S&P 500

60%

S&P 500

MSCI FM

© Beta Educational Services, LLC, 2016.

Portfolio Theory The Efficient Frontier

The Efficient Frontier

MEAN VARIANCE OPTIMIZATION

30

© Beta Educational Services, LLC, 2016.

Portfolio Theory The Efficient Frontier

Practice Question Which of the following is not on the efficient frontier?

(a) A

(b) B

(c) C

(d) D

31

Asset Return Std DeviationA 0.08 0.14B 0.13 0.24C 0.14 0.22D 0.11 0.16

© Beta Educational Services, LLC, 2016.

Portfolio Theory and CAPM Diversification Graph

Total Risk = Market Risk + NonMarket Risk

Practice Question Which of the following is more appropriate for a portfolio that goes from 60 stocks to 15?

(a) Its systematic risk has increased.(b) Its systematic risk has decreased.(c) Its unsystematic risk has increased.(d) Its unsystematic risk has decreased.

StandardDeviation

# of securities in a portfolio

32

© Beta Educational Services, LLC, 2016.

CAPM Summarizing the Theory

Stdev

E(R

)

Beta

E(R

)

Market Market

33

© Beta Educational Services, LLC, 2016.

CAPM Practice Question

Practice Question Which of the following statements is or are true? According to CAPM, a security is overpriced if _____

i. It has a negative alpha.

ii. Its return is lower than the market return

iii. It has a positive alpha.

iv. Its return is greater than the market return

(a) i only

(b) i and ii only

(c) iii only

(d) iii and iv only

34

© Beta Educational Services, LLC, 2016.

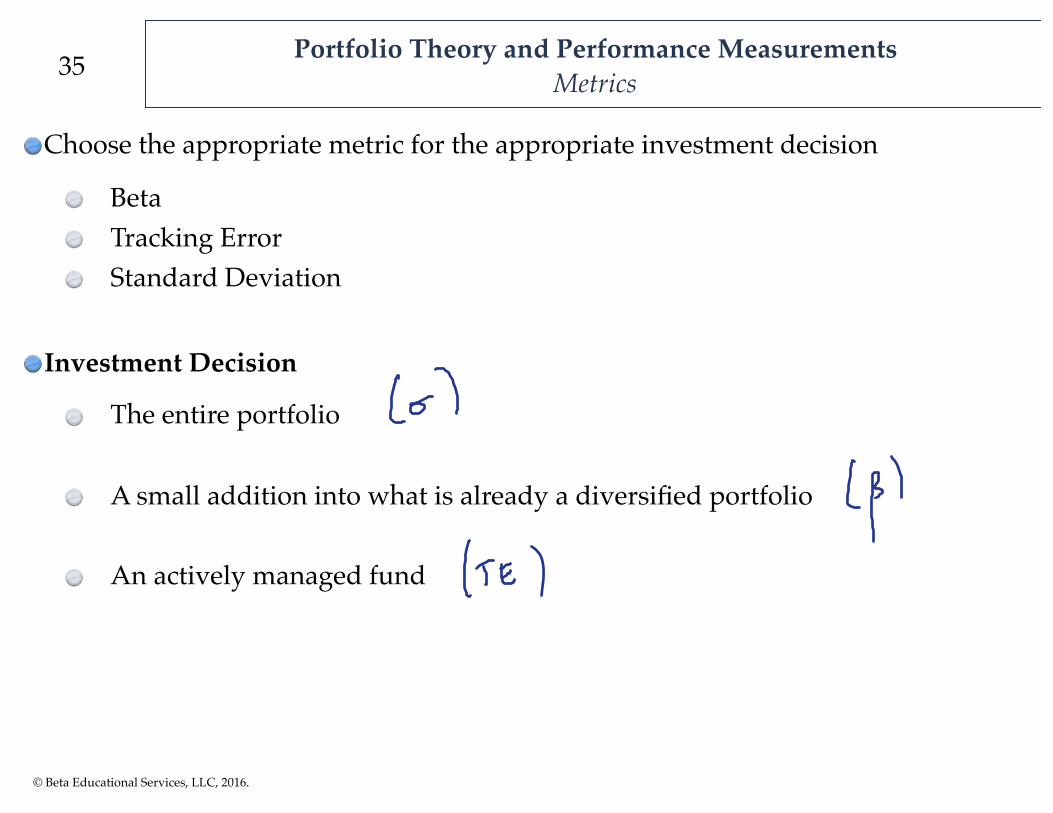

Portfolio Theory and Performance Measurements Metrics

Choose the appropriate metric for the appropriate investment decision

BetaTracking ErrorStandard Deviation

Investment Decision

The entire portfolio

A small addition into what is already a diversified portfolio

An actively managed fund

35

© Beta Educational Services, LLC, 2016.

Performance Measurements Summarizing

Standard Deviation - Sharpe and M2

Beta - Alpha, Treynor

Semi Deviation - Sortino Ratio

Tracking Error - Information Ratio

Measure of Risk Investment SituationBeta Marginal addition to a well-diversified portfolio

Standard Deviation All eggs in one basket, or the whole portfolioSemi Deviation Downside RiskTracking Error Active versus Passive

36

© Beta Educational Services, LLC, 2016.

Performance Measurements M2

Practice Question Evaluate the MSCI FM vs the S&P 500 using M2.

Asset Return Std Deviation BetaS&P 500 0.08 0.16 1

MSCI FM 0.09 0.22 0.36TBill 0.04 0

37

© Beta Educational Services, LLC, 2016.

Performance Measurements M2

Evaluating the MSCI FM vs the S&P 500 using M2.

Asset Return Std Deviation BetaS&P 500 0.08 0.16 1

MSCI FM 0.09 0.22 0.36TBill 0.04 0

38

4%

6.75%

9.5%

0% 4.4% 8.8% 13.2% 17.6% 22%

S&P 500MSCI FM

Stdev

Ret

urn

© Beta Educational Services, LLC, 2012.

Assess Equity Markets US-Denominated Return

Example A client invested $200,000 in a Euro-denominated fund a year ago when

the exchange rate was $1.14 per €. The current exchange rate is $1.25 per €, what

was her US-denominated return if she had a 15% euro-denominated return?

39

© Beta Educational Services, LLC, 2012.

Assess Equity Markets US-Denominated Return

Example A client invested $150,000 in a Japanese stock. The original exchange rate

was 84 Yen per USD. It is presently 78 Yen per USD. What must have been her

yen-denominated return if she currently has $160,000?

40

© Beta Educational Services, LLC, 2012.

Assess Equity Markets International Investing

Practice Question You expect an inflationary environment in the United States.

Which of the following is the least appropriate investment?

(a) International Equity Fund

(b) Commodities

(c) Long Term Treasuries

(d) REITs

41

© Beta Educational Services, LLC, 2012.

Assess Equity Markets Protecting Your Purchasing Power of Money

Which of the following may be best to hedge your US inflation risk, thereby protecting your purchasing power of money?

(a) A domestic equity fund

(b) A domestic bond fund

(c) A diversified international fund, where the currency risks have been hedged

(d) A diversified international fund, where the currency risks have not been hedged

42

© Beta Educational Services, LLC, 2016.

Investment Choices

Practice Question You expect the dollar to weaken vs. the Euro, which of the following would be the more appropriate choice(s)?

i) European Stocks

ii) ADR on European Stocks

iii) US Stocks

iv) Emerging Market Stocks

a) i) only

b) i) and iv) only

c) i) and ii) only

d) ii) only

43

© Beta Educational Services, LLC, 2016.

Investment Choices

Practice Question Which of the following is more appropriate in a taxable account, as opposed to tax deferred?

i. REITs

ii. Zero Coupon Corporates

iii. High Yield Bonds

iv. Stocks

44

© Beta Educational Services, LLC, 2012.

Benchmarking and Attribution The Link Between Sharpe Ratios and Information Ratios

Information Ratio = Excess Return over Tracking Error (vs a benchmark)

Lets make the benchmark the treasury bill

45

Ret (Bench)

Risk (Bench)

Ret (Fund) -

Risk (Fund) -

Excess Return

Tracking Error

© Beta Educational Services, LLC, 2016.

Benchmarking and Attribution Tracking Error

Practice Question Given the following information, compute the tracking error of the fund.

46

Fund Return Bench Return6% 5%-2% -3%-1% -5%12% 9%

© Beta Educational Services, LLC, 2016.

Practice Question

Practice Question

47

Asset Stdev Beta Sharpe Sortino SemiDevA 0.25 1.10 0.40 0.22 0.08B 0.28 0.90 0.27 0.21 0.13C 0.22 1.02 0.19 0.19 0.14D 0.20 0.88 0.32 0.18 0.11

© Beta Educational Services, LLC, 2016.

Space for Additional Questions

Practice Question Compute the P/E Ratio of the portfolio.

48

Asset No. of Shares Price EarningsA 1,000 $10 $1B 2,000 $50 $2

© Beta Educational Services, LLC, 2016.

Space for Additional Questions49

© Beta Educational Services, LLC, 2016.

Space for Additional Questions50

© Beta Educational Services, LLC, 2016.

Space for Additional Questions51

© Beta Educational Services, LLC, 2016.

Space for Additional Questions52

© Beta Educational Services, LLC, 2016.

Space for Additional Questions53

© Beta Educational Services, LLC, 2016.

Space for Additional Questions54

© Beta Educational Services, LLC, 2016.

Space for Additional Questions55

5

6

7