Embed Size (px)

Citation preview

Power & UtilitiesNewsletter

Q1 2014

1© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

• Electricity baseload prices in Continental Europe have continued their trendof low values (around 30€/MWh), high volatility and low differential vs peakprices.

• Prices in the UK have slightly decreased to around 40€/MWh, with lowervolatility and low differential vs peak

• Gas border prices in Europe have stabilised around 12 USD/MMBTU, wellabove Henry Hub levels (4 USD/MMBTU)

• Coal continues to decline in price, reaching 70-80 USD/t• As a result, spark spreads are negative across Continental Europe (close to

zero in the UK), while dark spreads are only marginally positive

• Electricity baseload prices in Continental Europe have continued their trendof low values (around 30€/MWh), high volatility and low differential vs peakprices.

• Prices in the UK have slightly decreased to around 40€/MWh, with lowervolatility and low differential vs peak

• Gas border prices in Europe have stabilised around 12 USD/MMBTU, wellabove Henry Hub levels (4 USD/MMBTU)

• Coal continues to decline in price, reaching 70-80 USD/t• As a result, spark spreads are negative across Continental Europe (close to

zero in the UK), while dark spreads are only marginally positive

• The EU launched a new energy policy framework for 2030 emphasizingenergy competitiveness vs other regions

• Germany has launched the Electricity reform (100% renewable target by 2050), while defining new Grid Development Plan and reserve capacity needs until 2018

• Spain completing its regulatory reform, with new Electricty Law approved and new regulation defined for networks and renewables/cogen

• UK implementing RIIO regulation, setting new rules for retailers and preparing auctions for new capacity builds

• The U.S. continues exploring the possibility of further opening the export of LNG

• The EU launched a new energy policy framework for 2030 emphasizingenergy competitiveness vs other regions

• Germany has launched the Electricity reform (100% renewable target by 2050), while defining new Grid Development Plan and reserve capacity needs until 2018

• Spain completing its regulatory reform, with new Electricty Law approved and new regulation defined for networks and renewables/cogen

• UK implementing RIIO regulation, setting new rules for retailers and preparing auctions for new capacity builds

• The U.S. continues exploring the possibility of further opening the export of LNG

• Positive quarter in share price evolution for most European utilities, exceptfor UK-centered players (SSE, Centrica).

• Best performers include EDP, Enel and their renwablres subsidiaries• Valuation levels have widened, with EV/EBITDA now ranging from 3,4 (RWE)

to 10,1 (National Grid)• Debt levels of major players have moderated, with credit rating maintained

in all cases except Centrica (downgraded in late December)

• Positive quarter in share price evolution for most European utilities, exceptfor UK-centered players (SSE, Centrica).

• Best performers include EDP, Enel and their renwablres subsidiaries• Valuation levels have widened, with EV/EBITDA now ranging from 3,4 (RWE)

to 10,1 (National Grid)• Debt levels of major players have moderated, with credit rating maintained

in all cases except Centrica (downgraded in late December)

• M&A activity has remained strong in Q1 2014, driven by deleveraging of major players

• Largest deals have included:o The sale of RWE Dea to LetterOne Group (1.7 €bn)o The acquisition of Tennet Offshore by Copenhagen Infrastructure

Partners (2,1 €bn)o EDF selling its 50% stake in Dalkia to Veolia Environnement (1,5

€bn)

• M&A activity has remained strong in Q1 2014, driven by deleveraging of major players

• Largest deals have included:o The sale of RWE Dea to LetterOne Group (1.7 €bn)o The acquisition of Tennet Offshore by Copenhagen Infrastructure

Partners (2,1 €bn)o EDF selling its 50% stake in Dalkia to Veolia Environnement (1,5

€bn)

PRICES AND MARGINSPRICES AND MARGINS REGULATORY NEWSREGULATORY NEWS

CAPITAL MARKETSCAPITAL MARKETS M&AM&A

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

2© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

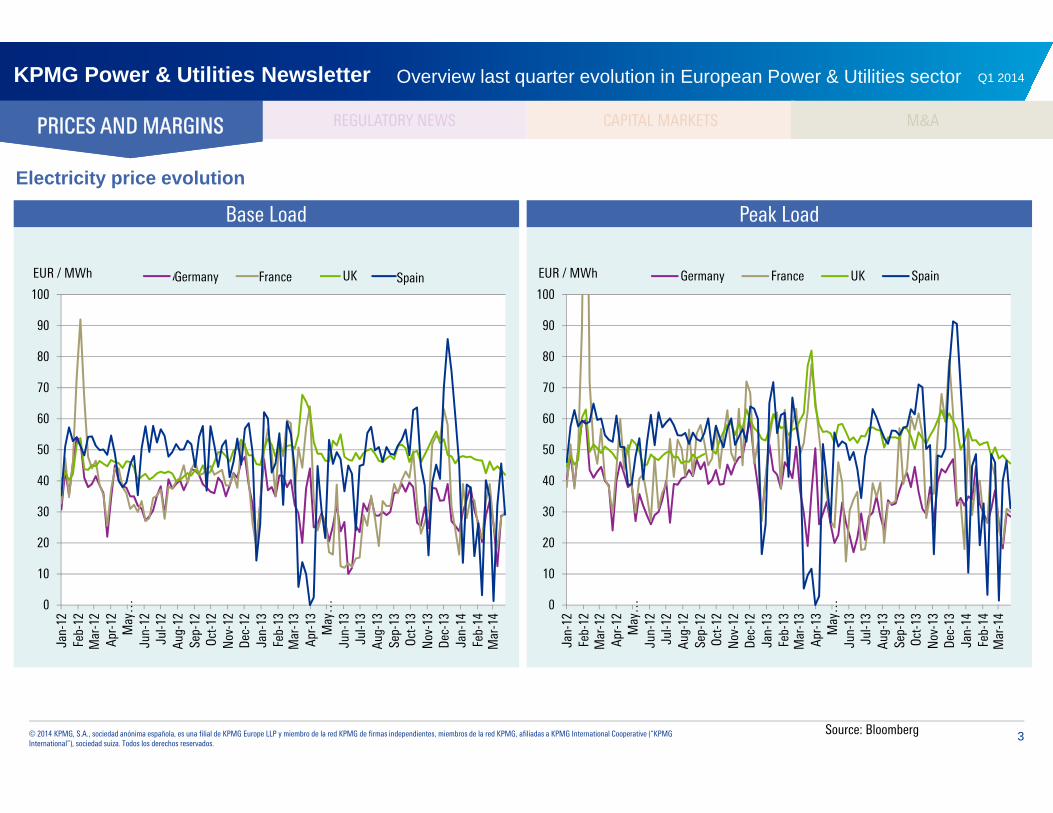

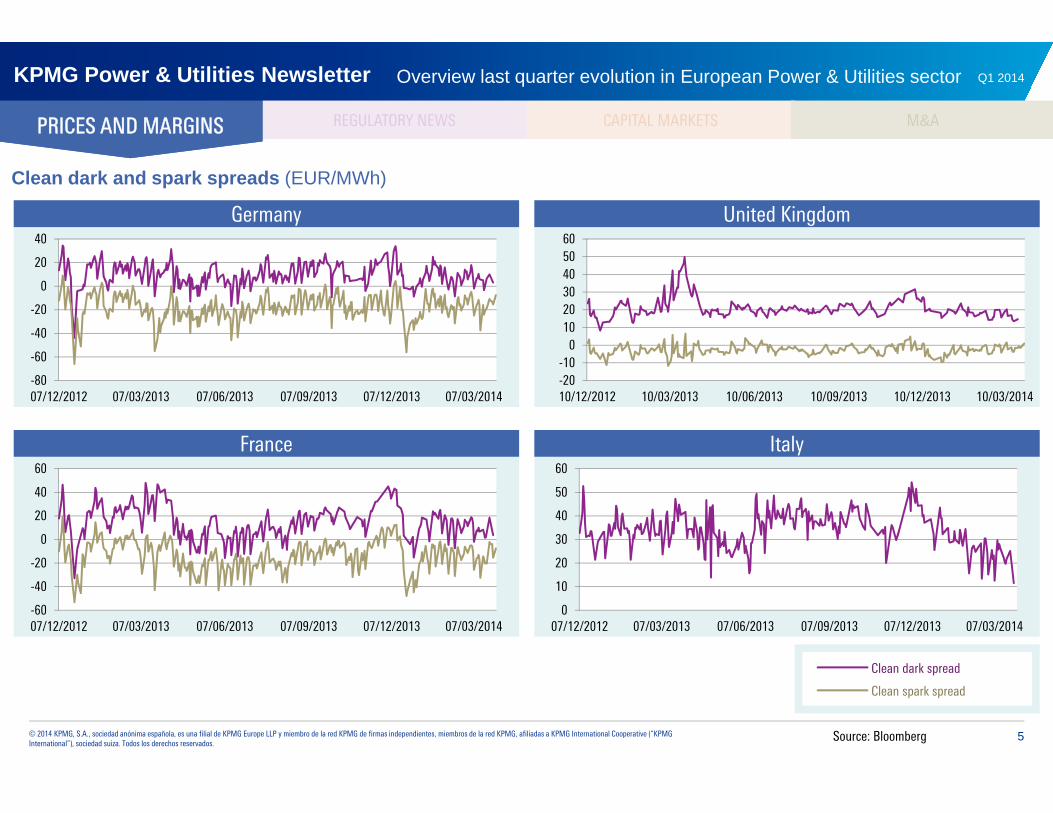

•Electricity baseload prices in Continental Europe have continued their trend of lowvalues (around 30€/MWh), high volatility and low differential vs peak prices.

•Prices in the UK have slightly decreased to around 40€/MWh, with lower volatility and low differential vs peak

•Gas border prices in Europe have stabilised around 12 USD/MMBTU, well above Henry Hub levels (4 USD/MMBTU)

•Coal continues to decline in price, reaching 70-80 USD/t

•As a result, spark spreads are negative across Continental Europe (close to zero in theUK), while dark spreads are only marginally positive

•Electricity baseload prices in Continental Europe have continued their trend of lowvalues (around 30€/MWh), high volatility and low differential vs peak prices.

•Prices in the UK have slightly decreased to around 40€/MWh, with lower volatility and low differential vs peak

•Gas border prices in Europe have stabilised around 12 USD/MMBTU, well above Henry Hub levels (4 USD/MMBTU)

•Coal continues to decline in price, reaching 70-80 USD/t

•As a result, spark spreads are negative across Continental Europe (close to zero in theUK), while dark spreads are only marginally positive

REGULATORY NEWS CAPITAL MARKETS M&APRICES AND MARGINSPRICES AND MARGINS

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

3© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

Electricity price evolution

REGULATORY NEWS CAPITAL MARKETS M&A

Base Load Peak Load

Source: Bloomberg

PRICES AND MARGINSPRICES AND MARGINS

0

10

20

30

40

50

60

70

80

90

100

Jan-

12Fe

b-12

Mar

-12

Apr-

12M

ay…

Jun-

12Ju

l-12

Aug-

12Se

p-12

Oct-1

2N

ov-1

2De

c-12

Jan-

13Fe

b-13

Mar

-13

Apr-

13M

ay…

Jun-

13Ju

l-13

Aug-

13Se

p-13

Oct-1

3N

ov-1

3De

c-13

Jan-

14Fe

b-14

Mar

-14

EUR / MWh Alemania Francia UK EspañaGermany France Spain

0

10

20

30

40

50

60

70

80

90

100

Jan-

12Fe

b-12

Mar

-12

Apr-

12M

ay…

Jun-

12Ju

l-12

Aug-

12Se

p-12

Oct-1

2N

ov-1

2De

c-12

Jan-

13Fe

b-13

Mar

-13

Apr-

13M

ay…

Jun-

13Ju

l-13

Aug-

13Se

p-13

Oct-1

3N

ov-1

3De

c-13

Jan-

14Fe

b-14

Mar

-14

EUR / MWh Germany France UK Spain

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

4© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

NOVEDADES REGULATORIAS MERCADOS DE CAPITALES M&A

Crude Oil

Source: Bloomberg; BAFA, World Bank

Coal: South African, Colombian and Australian export price Monthly Price

Carbon price – EU ETS Gas prices: US (H.Hub), EU (border prices), NBP

Fuel price evolution

0

20

40

60

80

100

120

140

2011

M01

2011

M03

2011

M05

2011

M07

2011

M09

2011

M11

2012

M01

2012

M03

2012

M05

2012

M07

2012

M09

2012

M11

2013

M01

2013

M03

2013

M05

2013

M07

2013

M09

2013

M11

2014

M01

2014

M03

US D

olla

rs p

er M

etric

Ton

Colombian Australian South African

REGULATORY NEWS CAPITAL MARKETS M&A

80859095

100105110115120125130

$ / bblAverage Brent Dubai WTI

NBPEUR

02468

1012

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14 0

2468

10121416

2009

M01

2009

M06

2009

M11

2010

M04

2010

M09

2011

M02

2011

M07

2011

M12

2012

M05

2012

M10

2013

M03

2013

M08

2014

M01

($/mmbtu) United States Europe

0

20

40

60

80

100

120GBP

PRICES AND MARGINSPRICES AND MARGINS

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

5© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

NOVEDADES REGULATORIAS MERCADOS DE CAPITALES M&A

Clean dark and spark spreads (EUR/MWh)

Germany

Source: Bloomberg

United Kingdom

France Italy

REGULATORY NEWS CAPITAL MARKETS M&A

0

10

20

30

40

50

60

07/12/2012 07/03/2013 07/06/2013 07/09/2013 07/12/2013 07/03/2014-60

-40

-20

0

20

40

60

07/12/2012 07/03/2013 07/06/2013 07/09/2013 07/12/2013 07/03/2014

-20-10

0102030405060

10/12/2012 10/03/2013 10/06/2013 10/09/2013 10/12/2013 10/03/2014-80

-60

-40

-20

0

20

40

07/12/2012 07/03/2013 07/06/2013 07/09/2013 07/12/2013 07/03/2014

Clean dark spread

Clean spark spread

PRICES AND MARGINSPRICES AND MARGINS

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

6© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

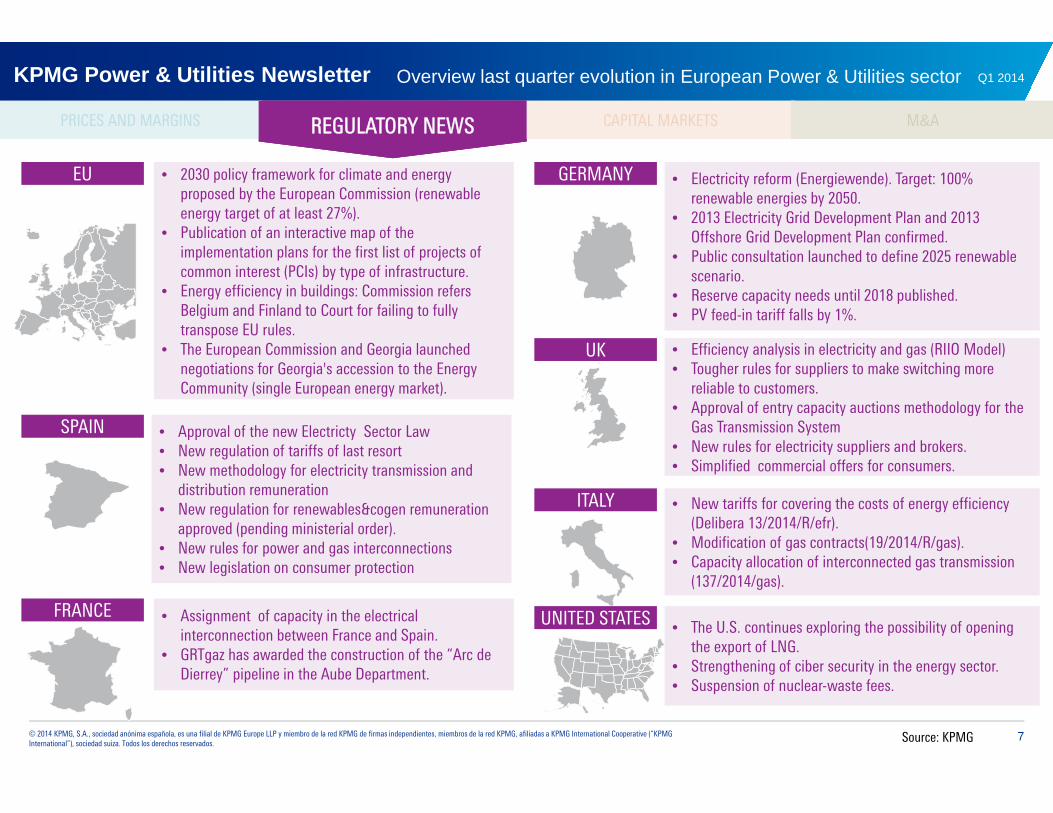

•The EU launched a new energy policy framework for 2030 emphasizing energycompetitiveness vs other regions

•Germany has launched the Electricity reform (100% renewable target by 2050), while defining new Grid Development Plan and reserve capacity needs until 2018

•Spain completing its regulatory reform, with new Electricty Law approved and new regulation defined for networks and renewables/cogen

•UK implementing RIIO regulation, setting new rules for retailers and preparing auctions for new capacity builds

•The U.S. continues exploring the possibility of further opening the export of LNG

•The EU launched a new energy policy framework for 2030 emphasizing energycompetitiveness vs other regions

•Germany has launched the Electricity reform (100% renewable target by 2050), while defining new Grid Development Plan and reserve capacity needs until 2018

•Spain completing its regulatory reform, with new Electricty Law approved and new regulation defined for networks and renewables/cogen

•UK implementing RIIO regulation, setting new rules for retailers and preparing auctions for new capacity builds

•The U.S. continues exploring the possibility of further opening the export of LNG

MERCADOS DE CAPITALES M&APRECIOS Y MÁRGENES NOVEDADES REGULATORIASNOVEDADES REGULATORIASPRICES AND MARGINS REGULATORY NEWSREGULATORY NEWS CAPITAL MARKETS M&A

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

7© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

MERCADOS DE CAPITALES M&APRECIOS Y MÁRGENES

Q1 2014

NOVEDADES REGULATORIASNOVEDADES REGULATORIAS

Source: KPMG

PRICES AND MARGINS REGULATORY NEWSREGULATORY NEWS CAPITAL MARKETS M&A

• The U.S. continues exploring the possibility of opening the export of LNG.

• Strengthening of ciber security in the energy sector.• Suspension of nuclear-waste fees.

• New tariffs for covering the costs of energy efficiency (Delibera 13/2014/R/efr).

• Modification of gas contracts(19/2014/R/gas).• Capacity allocation of interconnected gas transmission

(137/2014/gas).

• Electricity reform (Energiewende). Target: 100% renewable energies by 2050.

• 2013 Electricity Grid Development Plan and 2013 Offshore Grid Development Plan confirmed.

• Public consultation launched to define 2025 renewable scenario.

• Reserve capacity needs until 2018 published.• PV feed-in tariff falls by 1%.

• 2030 policy framework for climate and energy proposed by the European Commission (renewable energy target of at least 27%).

• Publication of an interactive map of the implementation plans for the first list of projects of common interest (PCIs) by type of infrastructure.

• Energy efficiency in buildings: Commission refers Belgium and Finland to Court for failing to fully transpose EU rules.

• The European Commission and Georgia launched negotiations for Georgia's accession to the Energy Community (single European energy market).

• Efficiency analysis in electricity and gas (RIIO Model)• Tougher rules for suppliers to make switching more

reliable to customers.• Approval of entry capacity auctions methodology for the

Gas Transmission System• New rules for electricity suppliers and brokers. • Simplified commercial offers for consumers.

• Assignment of capacity in the electrical interconnection between France and Spain.

• GRTgaz has awarded the construction of the “Arc de Dierrey” pipeline in the Aube Department.

EU

• Approval of the new Electricty Sector Law• New regulation of tariffs of last resort• New methodology for electricity transmission and

distribution remuneration• New regulation for renewables&cogen remuneration

approved (pending ministerial order).• New rules for power and gas interconnections• New legislation on consumer protection

SPAIN

FRANCE

GERMANY

UK

ITALY

UNITED STATES

Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

8© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

MERCADOS DE CAPITALES M&APRICES AND MARGINS

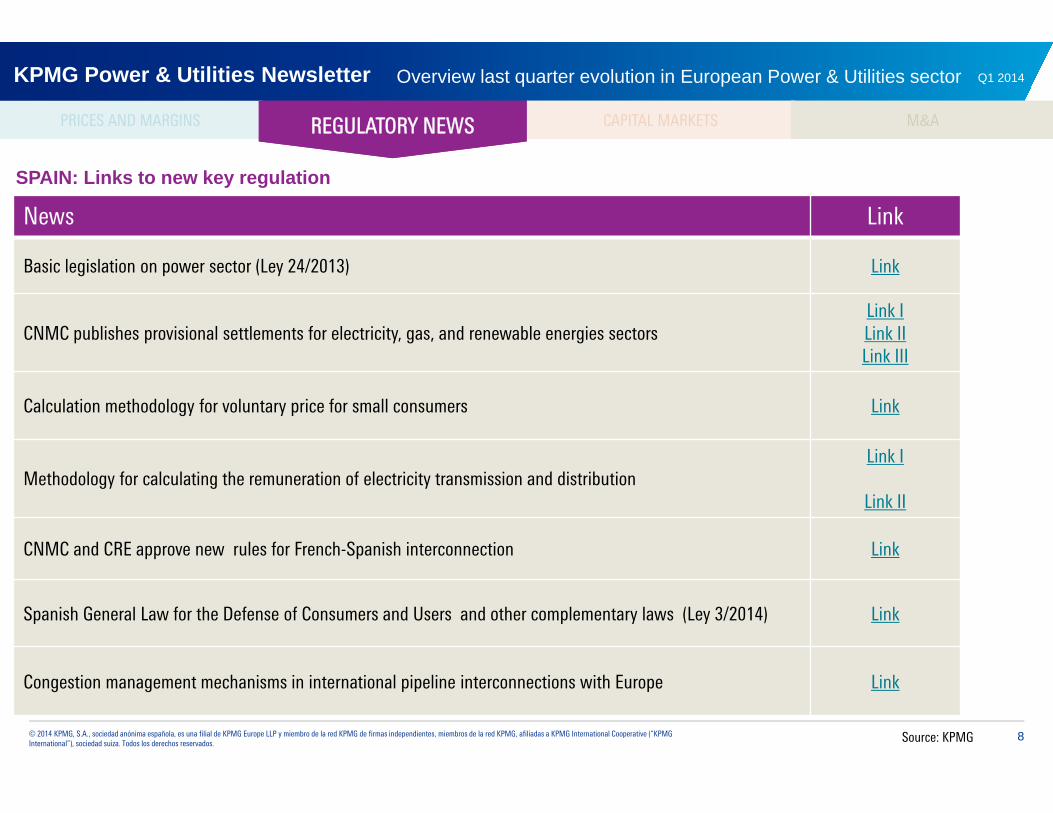

SPAIN: Links to new key regulation

News Link

Basic legislation on power sector (Ley 24/2013) Link

CNMC publishes provisional settlements for electricity, gas, and renewable energies sectorsLink ILink IILink III

Calculation methodology for voluntary price for small consumers Link

Methodology for calculating the remuneration of electricity transmission and distributionLink I

Link II

CNMC and CRE approve new rules for French-Spanish interconnection Link

Spanish General Law for the Defense of Consumers and Users and other complementary laws (Ley 3/2014) Link

Congestion management mechanisms in international pipeline interconnections with Europe Link

CAPITAL MARKETS M&AREGULATORY NEWSREGULATORY NEWS

Source: KPMG

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

9© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

•Positive quarter in share price evolution for most European utilities, except for UK-centered players (SSE, Centrica).

•Best performers include EDP, Enel and their renwablres subsidiaries

•Valuation levels have widened, with EV/EBITDA now ranging from 3,4 (RWE) to 10,1 (National Grid)

•Debt levels of major players have moderated, with credit rating maintained in all cases except Centrica (downgraded in late December)

•Positive quarter in share price evolution for most European utilities, except for UK-centered players (SSE, Centrica).

•Best performers include EDP, Enel and their renwablres subsidiaries

•Valuation levels have widened, with EV/EBITDA now ranging from 3,4 (RWE) to 10,1 (National Grid)

•Debt levels of major players have moderated, with credit rating maintained in all cases except Centrica (downgraded in late December)

PRICES AND MARGINS REGULATORY NEWS M&ACAPITAL MARKETSCAPITAL MARKETS

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

10© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

PRICES AND MARGINS REGULATORY NEWS M&A

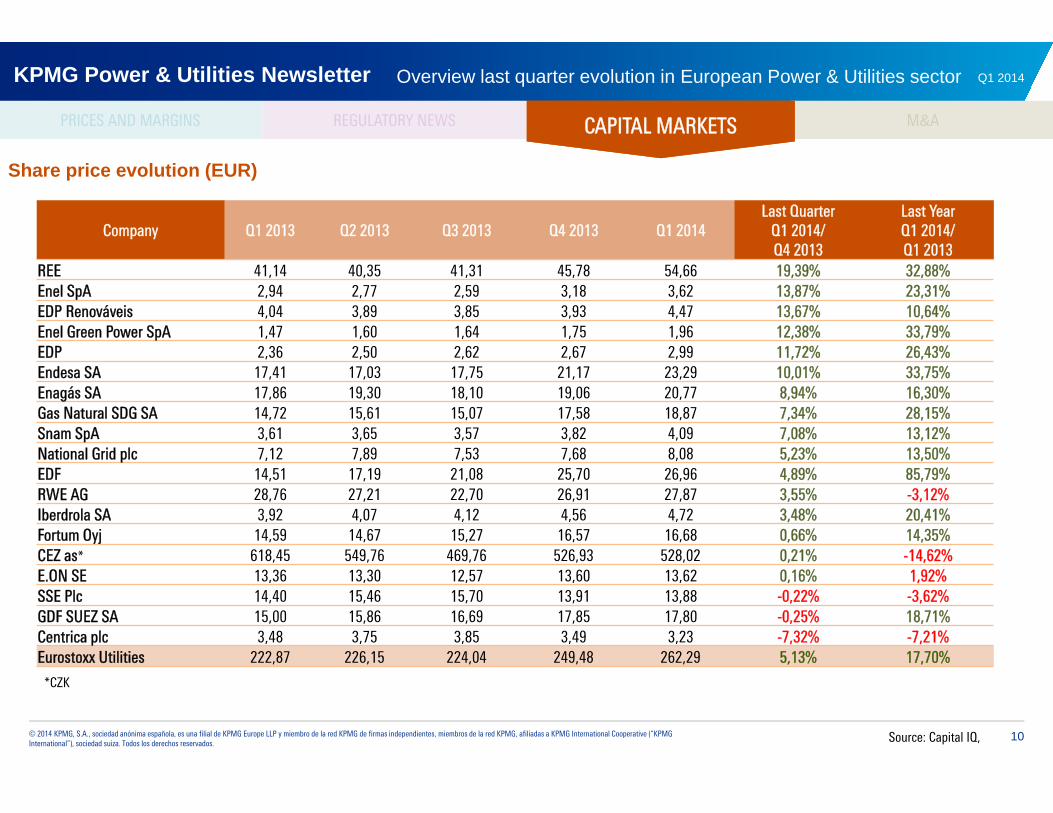

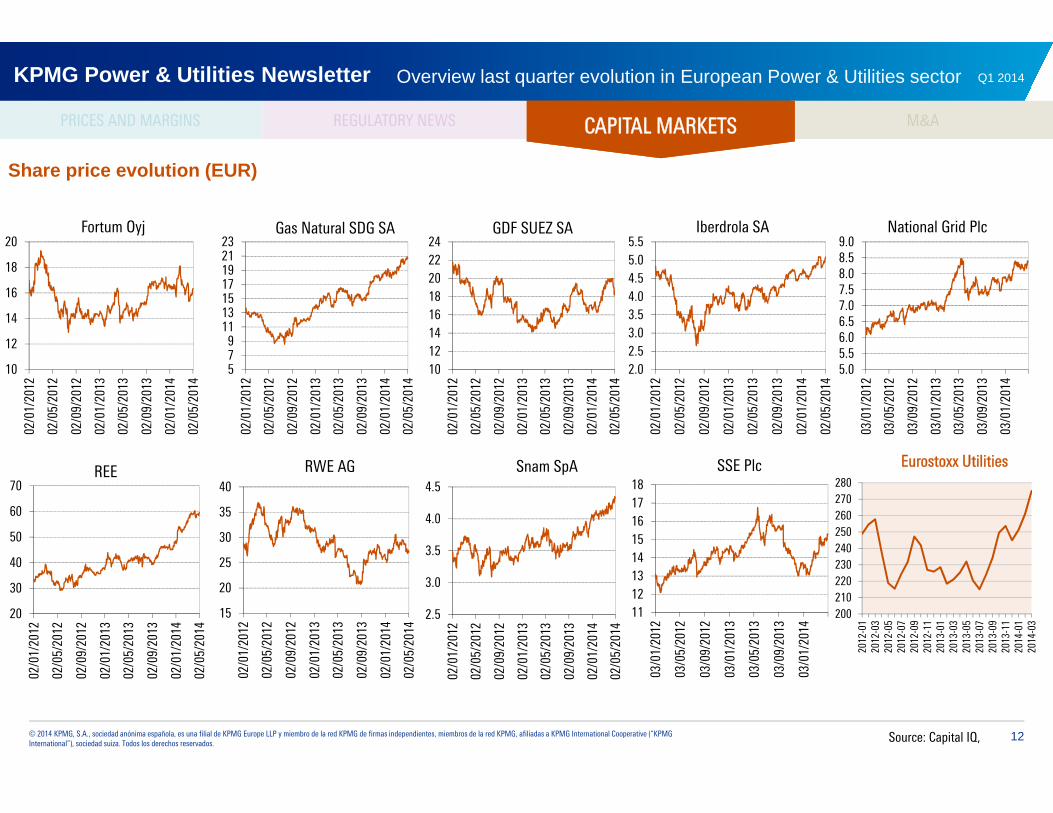

Share price evolution (EUR)

CAPITAL MARKETSCAPITAL MARKETS

*CZK

Source: Capital IQ,

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

Company Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014Last Quarter

Q1 2014/Q4 2013

Last YearQ1 2014/Q1 2013

REE 41,14 40,35 41,31 45,78 54,66 19,39% 32,88%Enel SpA 2,94 2,77 2,59 3,18 3,62 13,87% 23,31%EDP Renováveis 4,04 3,89 3,85 3,93 4,47 13,67% 10,64%Enel Green Power SpA 1,47 1,60 1,64 1,75 1,96 12,38% 33,79%EDP 2,36 2,50 2,62 2,67 2,99 11,72% 26,43%Endesa SA 17,41 17,03 17,75 21,17 23,29 10,01% 33,75%Enagás SA 17,86 19,30 18,10 19,06 20,77 8,94% 16,30%Gas Natural SDG SA 14,72 15,61 15,07 17,58 18,87 7,34% 28,15%Snam SpA 3,61 3,65 3,57 3,82 4,09 7,08% 13,12%National Grid plc 7,12 7,89 7,53 7,68 8,08 5,23% 13,50%EDF 14,51 17,19 21,08 25,70 26,96 4,89% 85,79%RWE AG 28,76 27,21 22,70 26,91 27,87 3,55% -3,12%Iberdrola SA 3,92 4,07 4,12 4,56 4,72 3,48% 20,41%Fortum Oyj 14,59 14,67 15,27 16,57 16,68 0,66% 14,35%CEZ as* 618,45 549,76 469,76 526,93 528,02 0,21% -14,62%E.ON SE 13,36 13,30 12,57 13,60 13,62 0,16% 1,92%SSE Plc 14,40 15,46 15,70 13,91 13,88 -0,22% -3,62%GDF SUEZ SA 15,00 15,86 16,69 17,85 17,80 -0,25% 18,71%Centrica plc 3,48 3,75 3,85 3,49 3,23 -7,32% -7,21%Eurostoxx Utilities 222,87 226,15 224,04 249,48 262,29 5,13% 17,70%

11© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

PRICES AND MARGINS REGULATORY NEWS M&ACAPITAL MARKETSCAPITAL MARKETS

Share price evolution (EUR)

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

10

15

20

25

30

35

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

EDF

2.52.72.93.13.33.53.73.94.1

03/0

1/20

12

03/0

5/20

12

03/0

9/20

12

03/0

1/20

13

03/0

5/20

13

03/0

9/20

13

03/0

1/20

14

Centrica Plc

300

400

500

600

700

800

90002

/01/

2012

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

CEZ a.s (*CZK)

11

13

15

17

19

21

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

E.ON

2.02.53.03.54.04.55.05.5

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

EDP Renováveis

1.0

1.5

2.0

2.5

3.0

3.5

4.0

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

EDP

0.50.70.91.11.31.51.71.92.12.3

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

Enel Green Power SpA

1.5

2.0

2.5

3.0

3.5

4.0

4.5

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

Enel SpA

1012141618202224

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

Enagás SA

10

15

20

25

30

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

Endesa SA

12© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

PRICES AND MARGINS REGULATORY NEWS M&A

Share price evolution (EUR)

CAPITAL MARKETSCAPITAL MARKETS

Source: Capital IQ,

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

5 7 9

11 13 15 17 19 21 23

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

Gas Natural SDG SA

10 12 14 16 18 20 22 24

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

GDF SUEZ SA

2.02.53.03.54.04.55.05.5

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

Iberdrola SA

5.05.56.06.57.07.58.08.59.0

03/0

1/20

12

03/0

5/20

12

03/0

9/20

12

03/0

1/20

13

03/0

5/20

13

03/0

9/20

13

03/0

1/20

14

National Grid Plc

10

12

14

16

18

20

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

Fortum Oyj

20

30

40

50

60

70

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

REE

15

20

25

30

35

40

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

RWE AG

2.5

3.0

3.5

4.0

4.5

02/0

1/20

12

02/0

5/20

12

02/0

9/20

12

02/0

1/20

13

02/0

5/20

13

02/0

9/20

13

02/0

1/20

14

02/0

5/20

14

Snam SpA Eurostoxx Utilities

11 12 13 14 15 16 17 18

03/0

1/20

12

03/0

5/20

12

03/0

9/20

12

03/0

1/20

13

03/0

5/20

13

03/0

9/20

13

03/0

1/20

14

SSE Plc

200210220230240250260270280

2012

-01

2012

-03

2012

-05

2012

-07

2012

-09

2012

-11

2013

-01

2013

-03

2013

-05

2013

-07

2013

-09

2013

-11

2014

-01

2014

-03

13© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

PRECIOS Y MÁRGENES NOVEDADES REGULATORIAS M&A

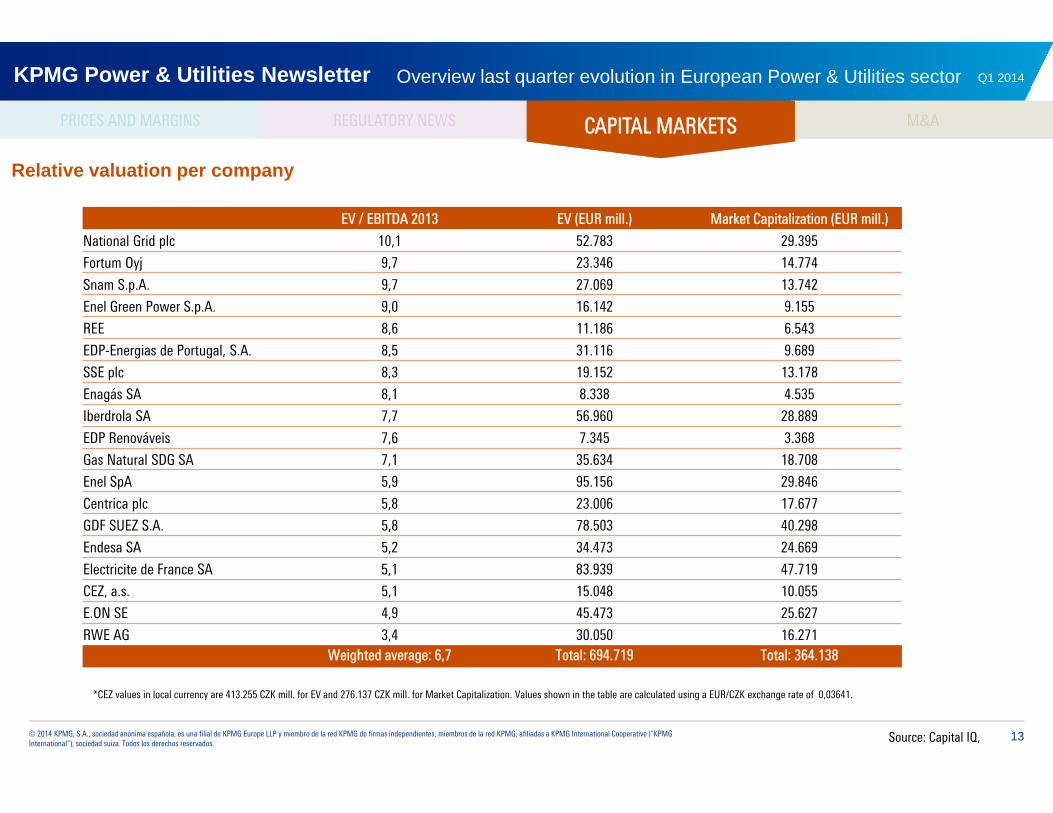

Relative valuation per company

PRICES AND MARGINS REGULATORY NEWS M&ACAPITAL MARKETSCAPITAL MARKETS

Source: Capital IQ,

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

*CEZ values in local currency are 413.255 CZK mill. for EV and 276.137 CZK mill. for Market Capitalization. Values shown in the table are calculated using a EUR/CZK exchange rate of 0,03641.

EV / EBITDA 2013 EV (EUR mill.) Market Capitalization (EUR mill.)

National Grid plc 10,1 52.783 29.395

Fortum Oyj 9,7 23.346 14.774

Snam S.p.A. 9,7 27.069 13.742

Enel Green Power S.p.A. 9,0 16.142 9.155

REE 8,6 11.186 6.543

EDP-Energias de Portugal, S.A. 8,5 31.116 9.689

SSE plc 8,3 19.152 13.178

Enagás SA 8,1 8.338 4.535

Iberdrola SA 7,7 56.960 28.889

EDP Renováveis 7,6 7.345 3.368

Gas Natural SDG SA 7,1 35.634 18.708

Enel SpA 5,9 95.156 29.846

Centrica plc 5,8 23.006 17.677

GDF SUEZ S.A. 5,8 78.503 40.298

Endesa SA 5,2 34.473 24.669

Electricite de France SA 5,1 83.939 47.719

CEZ, a.s. 5,1 15.048 10.055

E.ON SE 4,9 45.473 25.627

RWE AG 3,4 30.050 16.271Weighted average: 6,7 Total: 694.719 Total: 364.138

14© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

PRECIOS Y MÁRGENES NOVEDADES REGULATORIAS M&A

Leverage and credit ratings

Source:Capital IQ; S&P; Moody’s; Fitch.

PRICES AND MARGINS REGULATORY NEWS M&ACAPITAL MARKETSCAPITAL MARKETS

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

Net Debt/ EBITDA Rating S&P Date Rating Moody’s Date Rating Fitch Date EDP-Energias de Portugal, S.A. 5,0 BB+ 01-feb-12 Ba1 13-nov-13 BBB- 15-abr-2014 (rating watch maintained)

Snam S.p.A. 4,8 BBB+ 11-jul-13 Baa1 18-feb-14 - -

National Grid plc 4,5 A- 24-ago-07 Baa1 13-dic-13 BBB 12-dic-2013 (rating affirmed)

Iberdrola SA 3,8 BBB 28-nov-12 Baa1 13-dic-13 BBB+ 25-mar-2014 (rating affirmed)

EDP Renováveis 3,7 - - - - - -

Enagás SA 3,7 BBB 15-oct-12 Baa2 14-feb-14 A- 30/04/2014 (rating affirmed)

REE 3,6 BBB 15-oct-12 - - A- 30/04/2014 (rating affirmed)

Fortum Oyj 3,3 A- 27-nov-12 A2 15-jul-05 A- 06-dic-2013 (rating affirmed)

Enel Green Power S.p.A. 3,3 - - - - -

Gas Natural SDG SA 3,1 BBB 17-dic-10 Baa2 11-dic-13 BBB+ 10-ene-2014 (rating affirmed)

Enel SpA 3,0 BBB 11-jul-13 Baa2 12-dic-13 BBB+ 15-abr-2014 (rating affirmed)

SSE plc 2,6 A- 21-ago-09 A3 22-sep-09 A- 30-sep-2013 (rating affirmed)

GDF SUEZ S.A. 2,0 A 22-jul-08 A1 04-feb-11 - -

Electricite de France SA 1,9 A+ 17-ene-12 Aa3 14-ene-09 A+ 12-dic-2013 (rating affirmed)

E.ON SE 1,8 A- 27-jul-12 (P)A3 21-jun-13 A- 23-abr-2014 (rating affirmed)

CEZ, a.s. 1,6 A- 02-oct-06 A2 27-mar-14 A- 17-abr-2014 (rating affirmed)

RWE AG 1,4 BBB+ 27-jul-12 Baa1 21-jun-13 BBB+ 12-dic-2013 (rating affirmed)

Centrica plc 1,3 A- 29-may-09 A3 05-feb-13 A- 16-dic-2013 (rating downgrade)

Endesa SA 0,5 BBB 13-jul-13 - 12-dic-13 BBB+ 15/04/2014 (rating affirmed )

Average: 2,9

15© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

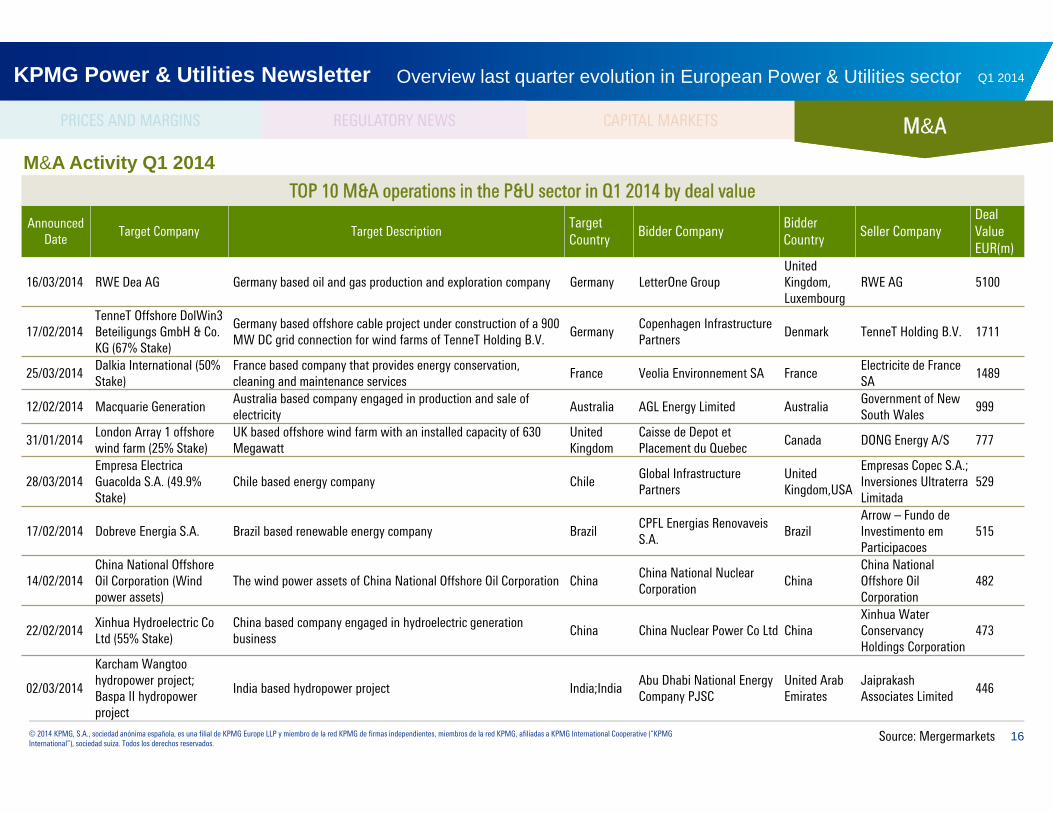

•M&A activity has remained strong in Q1 2014, driven by deleveraging of majorplayers

•Largest deals have included:

The sale of RWE Dea to LetterOne Group (5,1 €bn)

The acquisition of Tennet Offshore by Copenhagen Infrastructure Partners(1,7 €bn)

EDF selling its 50% stake in Dalkia to Veolia Environnement (1,5 €bn)

•M&A activity has remained strong in Q1 2014, driven by deleveraging of majorplayers

•Largest deals have included:

The sale of RWE Dea to LetterOne Group (5,1 €bn)

The acquisition of Tennet Offshore by Copenhagen Infrastructure Partners(1,7 €bn)

EDF selling its 50% stake in Dalkia to Veolia Environnement (1,5 €bn)

PRECIOS Y MÁRGENES NOVEDADES REGULATORIAS CAPITAL MARKETS M&AM&APRICES AND MARGINS REGULATORY NEWS

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

16© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

PRECIOS Y MÁRGENES NOVEDADES REGULATORIAS CAPITAL MARKETS

M&A Activity Q1 2014

Source: Mergermarkets

M&AM&APRICES AND MARGINS REGULATORY NEWS

Q1 2014Overview last quarter evolution in European Power & Utilities sectorKPMG Power & Utilities Newsletter

AnnouncedDate

Target Company Target DescriptionTarget Country

Bidder CompanyBidderCountry

Seller CompanyDealValueEUR(m)

16/03/2014 RWE Dea AG Germany based oil and gas production and exploration company Germany LetterOne GroupUnitedKingdom,Luxembourg

RWE AG 5100

17/02/2014TenneT Offshore DolWin3 Beteiligungs GmbH & Co.KG (67% Stake)

Germany based offshore cable project under construction of a 900 MW DC grid connection for wind farms of TenneT Holding B.V.

GermanyCopenhagen InfrastructurePartners

Denmark TenneT Holding B.V. 1711

25/03/2014Dalkia International (50% Stake)

France based company that provides energy conservation, cleaning and maintenance services

France Veolia Environnement SA FranceElectricite de France SA

1489

12/02/2014 Macquarie GenerationAustralia based company engaged in production and sale of electricity

Australia AGL Energy Limited AustraliaGovernment of New South Wales

999

31/01/2014London Array 1 offshore wind farm (25% Stake)

UK based offshore wind farm with an installed capacity of 630 Megawatt

UnitedKingdom

Caisse de Depot et Placement du Quebec

Canada DONG Energy A/S 777

28/03/2014Empresa ElectricaGuacolda S.A. (49.9% Stake)

Chile based energy company ChileGlobal InfrastructurePartners

United Kingdom,USA

Empresas Copec S.A.; Inversiones UltraterraLimitada

529

17/02/2014 Dobreve Energia S.A. Brazil based renewable energy company BrazilCPFL Energias RenovaveisS.A.

BrazilArrow – Fundo de Investimento em Participacoes

515

14/02/2014China National Offshore Oil Corporation (Wind power assets)

The wind power assets of China National Offshore Oil Corporation ChinaChina National Nuclear Corporation

ChinaChina National Offshore Oil Corporation

482

22/02/2014Xinhua Hydroelectric Co Ltd (55% Stake)

China based company engaged in hydroelectric generation business

China China Nuclear Power Co Ltd ChinaXinhua Water Conservancy Holdings Corporation

473

02/03/2014

Karcham Wangtoohydropower project; Baspa II hydropower project

India based hydropower project India;IndiaAbu Dhabi National Energy Company PJSC

United ArabEmirates

JaiprakashAssociates Limited

446

TOP 10 M&A operations in the P&U sector in Q1 2014 by deal value

© 2014 KPMG, S.A., sociedad anónima española, es una filial de KPMG Europe LLP y miembro de la red KPMG de firmas independientes, miembros de la red KPMG, afiliadas a KPMG International Cooperative (“KPMG International”), sociedad suiza. Todos los derechos reservados.

KPMG, el logotipo de KPMG y “cutting through complexity” son marcas registradas o comerciales de KPMG International.

La información aquí contenida es de carácter general y no va dirigida a facilitar los datos o circunstancias concretas de personas o entidades. Si bien procuramos que la información que ofrecemos sea exacta y actual, no podemos garantizar que siga siéndolo en el futuro o en el momento en que se tenga acceso a la misma. Por tal motivo, cualquier iniciativa que pueda tomarse utilizando tal información como referencia, debe ir precedida de una exhaustiva verificación de su realidad y exactitud, así como del pertinente asesoramiento profesional.

kpmg.es