Embed Size (px)

Citation preview

PREPARED AND PUBLISHED BY NON-US BROKER-DEALER(S): BNP PARIBAS - SINGAPORE (PI) THIS MATERIAL HAS BEEN APPROVED FOR U.S. DISTRIBUTION. ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES CAN BE FOUND AT APPENDIX ON PAGE 57

EQUITIES RESEARCH SINGAPORE TELECOMS

Picking the next potential outperformer

■ We have a non-consensus BUY rating on Starhub, and it is our top pick for the Singapore telecom sector. We initiate coverage on M1 with a HOLD rating on valuation grounds. We recommend HOLD for SingTel, given the absence of significant near-term catalysts.

■ We see substantial scope for Starhub to reverse its previous relative underperformance, following recent mobile tariff increases and accelerated LTE network deployment over the course of 2014. We are optimistic this will drive above-industry growth in 2015 and provide a re-rating catalyst for the stock.

■ We believe M1 will continue to benefit from improving mobile sector dynamics, but the related upside potential looks largely priced in. The increasingly assertive smaller operators could encroach on M1’s addressable broadband market, constraining earnings upside. Long term, we are concerned about the competitive impact of potential new mobile entrants.

Wei Shi Wu [email protected] +65 6210 1925

Our research is available on Thomson One, Bloomberg, TheMarkets.com, Factset and on http://eqresearch.bnpparibas.com/index. Please contact your salesperson for authorisation. Please see the important notice on the inside back cover.

10 OCTOBER 2014

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

To find out more about BNP Paribas Equities Research:

Visit : http://eqresearch.bnpparibas.com/ For ipad users : http://appstore.apple.com/BNPP-equities/

2

Picking the next potential outperformer

n Non-consensus BUY rating on Starhub (STH); initiate coverage of M1 at HOLD; SingTel HOLD

Recent weak operational trends have caused STH to be the worst performing Singapore telco ytd. We

think the market is still focusing on muted mobile trends and competitive pressures in broadband, and

that scope for an operational turnaround has been overlooked. The recent re-alignment of STH’s

businesses could reverse its operational underperformance, accelerate earnings growth and support

a re-rating. Our forecasts are up to 13% above consensus. We see limited upside potential for M1,

given emerging competition risks, and recommend HOLD for the yield. We also rate SingTel HOLD.

n Market expectations for STH seem low, but we see opportunities for a turnaround

We see significant opportunities from sector-wide mobile tariff increases, particularly STH’s most

aggressive re-pricing. With STH likely to catch up with competitors on LTE coverage by end-2014, we

believe a timely tariff increase could drive above-industry mobile gains in 2015. While M1 should

continue to benefit from improving mobile sector dynamics, intensifying broadband competition could

weigh on incremental growth. We anticipate relative stability for SingTel’s domestic operations, but

view competition in Australia as a persistent pressure point for Optus.

n STH is our top pick for its strong 2015 growth outlook and subsequent re-rating potential

While 2014 results will likely be fairly flat for STH, we expect an operational turnaround to drive the

fastest 2015 earnings growth in the sector and provide a re-rating catalyst. At about 10x 1-year

forward EV/EBITDA, STH is trading in line with M1 and at a slight premium to SingTel. But we view

STH’s improved near-term earnings profile as a differentiator. With expectations for M1 already fairly

high, we see limited scope for positive surprises and see further share price upside being constrained

by emerging competition risks. We rate SingTel a HOLD given a lack of near-term catalysts.

BNPP recommendations

Company BBG code Rating Share price Target price Upside/downside

StarHub Ltd STH SP BUY 4.09 4.75 +16.1%

M1 M1 SP HOLD 3.53 3.75 +6.1%

SingTel ST SP HOLD 3.80 3.94 +3.7%

Source: BNP Paribas

10 OCTOBER 2014

SECTOR REPORT

SINGAPORE TELECOMS

Wei Shi [email protected]+65 6210 1925

3

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Investment thesis

The Singapore mobile sector should continue to be buoyed

by improving data monetisation and moderating handset

subsidies. The recent sector-wide tariff increases, coupled

with ongoing LTE network expansion, should support ARPU

gains. STH could deliver above-industry growth in 2015,

having addressed both pricing and network deployment.

While residential broadband competition has been intense,

we see indications that pressure could ease in 2015,

potentially resulting in a slight sector recovery. On the other

hand, we expect competitive pressure to accelerate, in

particular, constraining the upside potential on M1.

Longer term, we have concerns about escalating mobile

competition, with smaller operators potentially entering the

market. Clearly, the success of new entrants is predicated

upon a number of regulatory/ commercial conditions being

met and the related challenges are well documented.

However, we think it would be hasty to dismiss the threat of

new operators from the outset. In the scenario of a more

crowded mobile market, we would favour operators with

established bundling strategies (e.g. SingTel, STH).

Stock recommendations

We have a non-consensus BUY rating on STH and it is our

top pick in the sector. Following a period of relative

operational underperformance, we believe growth could

accelerate in 2015, with the company having re-aligned its

mobile and fixed businesses.

With expectations for M1 already fairly high, we see limited

scope for positive surprises and therefore view further share

price upside as relatively constrained. We are also

concerned about potential competition risks over the longer-

term. However, we initiate coverage with a HOLD rating, for

the dividend yield.

We expect relative stability at SingTel’s Singapore

operations, but see competition as a persistent pressure

point for Optus. Associate contributions should be supported

by strong fundamentals, although FX remains a key risk. In

the absence of significant catalysts, we recommend HOLD.

Key risks

Key sector risks include more intense than expected

mobile/broadband competition, leading to margin erosion;

slower than expected data revenue gains, accelerated

competition around handset subsidies, and higher than

expected capex.

CONTENTS Executive summary ....................................................................... 5

Valuations ....................................................................................... 6

Relatively benign mobile market competition ......................... 7

Post-paid subscriber growth fairly stable; pre-paid should recover ............................................................................... 8

Strong momentum in mobile data monetisation should continue........................................................................................... 9

Roaming revenues showing signs of stabilising .................... 10

Recent tariff adjustments supportive of further ARPU expansion ...................................................................................... 11

Measured approach towards handset subsidies ................... 12

Potential longer-term competition risks in mobile .............. 13

Small players driving residential broadband competition . 15

Near-term pay-TV outlook is stable ......................................... 18

Sector revenue outlook .............................................................. 19

Sector EBITDA and margin outlook .......................................... 20

Sector capex outlook .................................................................. 21

Regional telco comps .................................................................. 22

Company reports ......................................................................... 23

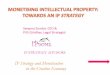

STH expected to deliver fastest revenue growth in 2015

Source: BNP Paribas estimates

Accelerated revenue growth should boost EBITDA gains for STH

Source: BNP Paribas estimates

7

5 4

4 5

4

(1)

6

5

(2)

(1)

0

1

2

3

4

5

6

7

2014E 2015E 2016E

(%) M1 SingTel STH

10

6 5

2

5 5

(0)

8

6

(2)

0

2

4

6

8

10

12

2014E 2015E 2016E

(%) M1 SingTel STH

4

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Executive summary

We are generally positive on Singapore’s mobile sector outlook and expect growth to

be supported by continued data monetisation (with a further near-term boost from

recent tariff increases), LTE network expansion and moderating handset subsidies.

Near-term competition among the major operators should remain relatively benign,

supporting continued revenue expansion and fairly stable margins. We see scope for

STH to recover from a position of relative weakness, as of the three incumbents it

has made the sharpest upward adjustments to tariffs (see Exhibit 15, p11) and has

accelerated LTE network deployment in recent months.

Following a period of relatively intense residential broadband price competition led by

smaller operators, we think things could get better. My Republic (not listed), one of

the smaller retail service providers (RSPs), is looking to expand its presence outside

of Singapore. We are cautiously optimistic that this company’s regional aspirations

could mean greater financial discipline and a more restrained pricing strategy

domestically. This would be positive for the entire sector, although it is possible any

rebound would be more pronounced for STH given its relative exposure to the

broadband (and pay-TV) sector.

However, we see enterprise broadband competition as potentially escalating, given

smaller RSPs (e.g. My Republic and Superinternet (not listed) are looking to

aggressively target the SME segment. Clearly, this would hurt SingTel, given its

relative dominance in this segment. But we believe the financial impact on SingTel

could be slight and fairly gradual. Likewise, there should be limited impact on STH,

especially given management’s recent shift in strategic focus away from SMEs

towards the corporate segment. We are, however, concerned that assertive action

from the smaller operators will limit potential upside for M1, given its greater overlap

with this group of operators.

We have slight concerns around escalating mobile competition over the longer term

(see p13-14). While we recognise the success of new entrants into a mature market

will be predicated upon a number of regulatory/commercial conditions being met, it

would be hasty to dismiss related threats from the outset. In a scenario of an

increasingly crowded mobile market, we would favour operators with strong bundling

strategies; this dovetails with our 12M relative preference for STH.

Stock recommendations

We recommend BUY on STH with a SGD4.75 TP, as our top pick in the Singapore

telecom sector, supported by our optimism that earnings growth will accelerate post

re-alignment of its businesses. We project the fastest 2015 earnings growth for STH

within the sector. Our BUY rating is a contrarian call and our FY14-16 forecasts are

up to 13% above Bloomberg consensus.

We like M1 for its nimbleness and technology focus, but rate it HOLD as we believe

related upside is largely priced in at current levels. Although M1 should deliver a

fairly strong finish to 2014, market expectations are already high and there is limited

scope for further positive surprises, in our view. We are also concerned increasing

broadband competition will crimp revenue upside for this company, while the

company’s less established bundling strategy vs peers renders it vulnerable to

longer-term mobile competition risks, in our opinion. Our TP is SGD3.75.

SingTel’s Singapore operations should continue to benefit from improving mobile

sector dynamics. However, we view competition as a persistent pressure point for

Optus and do not assume significant growth within the near term. Group underlying

net profit should be supported by robust fundamentals across SingTel’s key

associates, although FX remains a risk, with the SGD up y-y versus most associate

currencies during Apr-Sep. With SingTel’s stub PER trading in line with its long-term

average, we see few significant potential catalysts over the near term and

recommend HOLD with a SGD3.94 TP.

5

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Valuations

STH has been the worst performing Singapore telco over the past 12 months. We

believe this has been a function of the company’s fairly lacklustre operational

performance in recent quarters. Expectations for this company are low, with the

market focusing on muted mobile trends and competitive pressures in broadband.

But as we argue in this report, we think STH has re-aligned its businesses, which

could potentially drive accelerated growth and a subsequent re-rating of the stock.

On the other hand, we see limited scope for M1 to operationally surprise to the

upside, especially given potential competition risks. And given M1’s share price has

outperformed peers ytd, further share price upside potential looks constrained.

At current levels, STH is trading close to M1 in terms of 1-year forward P/E and

EV/EBITDA and at a premium to SingTel. But we project the fastest 2015 earnings

growth for STH and view this as a key differentiator and potential re-rating catalyst.

At current levels, all three Singapore telcos are offering fairly undifferentiated

dividend yields of approximately 5%. We flag SingTel and STH as having larger

headroom than M1 for potential dividend increases, relative to projected FCF (please

see respective company sections).

EXHIBIT 1: YTD relative share price performance EXHIBIT 2: 1-year forward dividend yield, by operator

Sources: Bloomberg; BNP Paribas Sources: Bloomberg; BNP Paribas

90

95

100

105

110

115

120

Ja

n-1

4

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Ju

n-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oc

t-1

4

M1 ST STH FSSTI

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0J

an

-11

Ap

r-1

1

Ju

l-1

1

Oc

t-1

1

Ja

n-1

2

Ap

r-1

2

Ju

l-1

2

Oc

t-1

2

Ja

n-1

3

Ap

r-1

3

Ju

l-1

3

Oc

t-1

3

Ja

n-1

4

Ap

r-1

4

Ju

l-1

4

(%) M1 ST STH

6

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Relatively benign mobile market competition

At 154% penetration (as at Jun 2014), the Singapore mobile sector is relatively

saturated. Singapore’s three-player structure in an addressable market of 5.5m

means it has one of the lowest populations per operator within the region, although

this is still above the ratio for Hong Kong.

EXHIBIT 3: Mobile population penetration, selected markets EXHIBIT 4: Population per operator, selected markets

As at June 2014 Sources: Telegeography; BNP Paribas

Note: Population as at 2013. Sources: Telegeography; BNP Paribas

Despite this, the competitive environment in Singapore is stable and fairly benign.

While growth has slowed with narrowing margins in recent years, this is more a

function of reduced profitability from data substitution than punitive price competition.

In fact, EBITDA margins are showing signs of improvements as the industry moves

towards more sustainable data pricing models.

EXHIBIT 5: Mobile subscriber share, by operator EXHIBIT 6: Sector EBITDA and EBITDA margin trends

Sources: Company data; BNP Paribas Sources: Company data; BNP Paribas

0

20

40

60

80

100

120

140

160

180

Ho

ng

Ko

ng

Sin

ga

po

re

Ma

lay

sia

Th

aila

nd

Ta

iwa

n

Ind

on

es

ia

Ja

pa

n

Ko

rea

(%)

0

5

10

15

20

25

30

35

40

Ho

ng

Ko

ng

Sin

ga

po

re

Ta

iwa

n

Ma

lay

sia

Ko

rea

Th

aila

nd

Ja

pa

n

Ind

on

es

ia

(m)

20

25

30

35

40

45

50

2008 2009 2010 2011 2012 2013

(%) M1 SingTel STH

32

33

34

35

36

37

38

39

40

2,900

2,950

3,000

3,050

3,100

3,150

3,200

3,250

3,300

2008 2009 2010 2011 2012 2013

(%)(SGD m) EBITDA (LHS) EBITDA margin (RHS)

7

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Post-paid subscriber growth fairly stable; pre-paid should recover

While post-paid subscriber growth has generally slowed, quarterly net adds remain

healthy, supported by increasing penetration of multiple/secondary SIMs. We expect

2H14 to be stronger than 1H14, driven by seasonality and the recent iPhone 6

launch. The pre-paid subscriber base has been impacted by regulatory reduction of

SIMs per user to three, from 10, effective Apr 2014. In response, some operators

have undertaken voluntary rationalisation of their pre-paid bases. We expect pre-

paid net adds to have remained weak in 3Q14, before stabilising or slightly

recovering in 4Q14.

EXHIBIT 7: Sector post-paid mobile net adds EXHIBIT 8: Sector pre-paid mobile net adds

Sources: Company data; BNP Paribas Sources: Company data; BNP Paribas

0

10

20

30

40

50

60

70

80

90

100

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

('000)

(200)

(150)

(100)

(50)

0

50

100

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

('000)

8

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Strong momentum in mobile data monetisation should continue

Following a general deceleration in revenue growth over the past few years, the

Singapore mobile sector is experiencing a slight revival, as better data monetisation

drives re-accelerated growth. With data economics now well understood by

operators, the relatively benign competitive landscape has provided scope for a

reduction in data allowances over the years and, more recently, an upward

adjustment in tariffs.

EXHIBIT 9: Sector mobile service revenue y-y chg EXHIBIT 10: Sector voice and data revenue split

Sources: Company data; BNP Paribas Sources: Company data; BNP Paribas

At the same time, increasing smartphone penetration, coupled with expanding LTE

network coverage, has driven accelerated data usage growth. For example, we

estimate 12% of post-paid subscribers in the sector exceeded their data allowances

in 2Q14, up significantly from 3% a year ago. For reference, excess data is charged

at SGD10.70 per GB, up from SGD5.35 per GB a year ago. As such, advanced data

revenue growth has been robust. We expect this trend will continue, supported by

operators’ rollout of LTE Advanced networks and associated demand for data

services. As an aside, it is worth noting that, over the past 12 months, STH appears

to have caught up with its competitors in terms of the proportion of subscribers

exceeding data allowances.

EXHIBIT 11: Data usage trends over past 12M EXHIBIT 12: Advanced data revenue trends

Sources: Company data; BNP Paribas Sources: Company data; BNP Paribas estimates

0

2

4

6

8

10

12

14

2006 2007 2008 2009 2010 2011 2012 2013

(%)

0

10

20

30

40

50

60

70

80

90

100

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

(%) Voice Data

0

10

20

30

40

50

60

70

M1 SingTel STH M1 SingTel STH

(%) % post-paid subscribers on tiered plans

% post-paid subscribers exceeding data allowance

2Q13 2Q14

0

5

10

15

20

25

30

35

0

50

100

150

200

250

300

350

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

(y-y %)(SGD m) Advanced data revenues (LHS)

Change (RHS)

9

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Roaming revenues showing signs of stabilising

So far, M1 has been the most successful in driving post-paid ARPU growth among

the Singapore telcos. Specifically, it is the only operator that has consistently grown

quarterly ARPUs over the past year. In our view, M1’s technology focus has been a

contributing factor to this trend – for instance, it was the first operator in Singapore to

roll out a nationwide 4G network.

On the other hand, we believe the impact of roaming revenue decline (a function of

both decreasing volumes and tariffs) has been more pronounced for SingTel and

STH, reflecting their relative exposures to higher-end/corporate customers. We

estimate roaming accounts for 25-27% of SingTel’s mobile revenues and up to 15%

of STH’s mobile revenues. In comparison, M1’s roaming contribution is

approximately 10%. Coupled with generally decreasing voice and SMS, the roaming

revenue decline has effectively negated any positive impact from rising data usage

on SingTel’s and STH’s ARPUs.

EXHIBIT 13: Post-paid ARPU y-y chg, by operator EXHIBIT 14: Roaming contribution to mobile revenues

Sources: Company data; BNP Paribas Note: Estimated as at 2014 Sources: Company data; BNP Paribas estimates

Positively, recent management commentary across the three telcos suggests

roaming revenues could stabilise. There have been various initiatives to address

roaming usage decline – for example, through the introduction of daily cap plans. A

slight positive to the declining roaming trend is that inter-operator costs have also

come down, effectively holding associated margins steady.

(12)

(10)

(8)

(6)

(4)

(2)

0

2

4

6

8

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

(%) M1 SingTel STH

0

5

10

15

20

25

30

M1 STH SingTel

(%)

10

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Recent tariff adjustments supportive of further ARPU expansion

A significant positive is the recent upward tariff adjustments introduced by the telcos.

Specifically, post-paid mobile tariffs were raised by an average 3-5% across the

sector, effective September. This should support post-paid ARPU expansion over the

coming quarters.

STH has introduced the sharpest percentage tariff increases in the lower price plans

– a move we view positively. For instance, its new entry-level plan is priced 13%

above the previous plan. This compares with 5% and 8% price increases by M1 and

SingTel, respectively. Given the relative maturity of this market segment and the fact

that the new pricing levels are fairly comparable across all operators, the likelihood of

resulting subscriber churn from STH is low, in our view. In fact, we believe this could

drive faster near-term ARPU growth for STH versus its competitors.

EXHIBIT 15: Change in entry-level post-paid mobile tariffs EXHIBIT 16: Comparison of new entry-level post-paid plans

M1 SingTel STH

Price (SGD) 41 42.9 42.9

Talktime (mins) 200 200 150

SMS/MMS 1,000 1,000 1,000

Data (GB) 3 2 3

Wi-Fi (GB) n/a 2 n/a

Note: Slight adjustments in voice/SMS/data allowances in new price plans Sources: Company data; BNP Paribas

Note: SingTel also has a SGD27.90 plan, while M1 has a SGD28 plan Sources: Company data; BNP Paribas

Potential for STH to play catch up

In tandem with the price adjustments above, STH has also been addressing its

previous network issues. Specifically, the operator initially lagged competitors with its

LTE network rollout. We believe this could have contributed to STH’s less impressive

ARPU performance, especially versus M1. Recent feedback from management

suggests this issue could soon be resolved, with the company accelerating LTE

network deployment over the course of 2014. The company is targeting nationwide

LTE network coverage, offering 300Mbps, by end 2014. This would bring STH’s

network on a par with competitors, effectively eliminating STH’s previous

technological disadvantage. When considered within the context of higher tariffs, we

are optimistic this could accelerate ARPU gains for STH.

35

36

37

38

39

40

41

42

43

44

M1 SingTel STH

(SGD) Old New

+8% +13%

+5%

11

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Measured approach towards handset subsidies

We continue to see operator discipline around handset subsidies. The telcos have

selectively cut iPhone 6 handset subsidies, although the reductions are generally

slight. Regardless, we view this as indication that operators are taking an

increasingly measured approach towards subsidy-based competition, which should

be supportive of sector margins.

EXHIBIT 17: Average change in iPhone subsidies in past 12M, by price plans

Note: Tier 1 plans: SGD41-42.90; Tier 2 plans: SGD61-62.90; Tier 3 plans: SGD101-102.90; Tier 4 plans: SGD208-239.90; comprison based on iPhone 5S and iPhone 6 models Sources: Company data; Channelnewsasia, BNP Paribas

(8)

(6)

(4)

(2)

0

2

4

6

Tier 1 Tier 2 Tier 3 Tier 4

(%) 16GB 64GB

12

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Potential longer-term competition risks in mobile

The Infocomm Development Authority’s eagerness to facilitate greater competition in

mobile is well demonstrated. For example, spectrum was specifically set aside for

potential new entrants in the past two spectrum auctions, although there were

eventually no takers. Earlier this year, the IDA initiated a public consultation on the

potential entry of Mobile Virtual Network Operators (MVNOs). In response,

broadband retail service providers, My Republic and Superinternet, indicated their

interest in entering the mobile space.

The challenges surrounding the MVNO business case are well documented. Any

scepticism around a late new entrant into a highly penetrated mobile market with

three established players is also valid. However, we think it may be hasty to dismiss

the MVNO threat from the outset.

Market may not be too small to accommodate a fourth player

It is possible to construct an argument that the addressable market in Singapore is

too small to support four operators. After all, the launch of Virgin Mobile Singapore in

2001 and its subsequent exit from the market a year later may still be fresh in some

investors’ minds. But given the current landscape, we think there is merit in

considering the potential for a data-only fourth operator.

My Republic has indicated plans to offer basic mobile data access, subject to certain

commercial/regulatory conditions being met. Under this model, content and

applications (including voice) will be offered via third-party OTT platforms.

Management believes the company can realistically achieve 10% mobile market

share based on this framework.

In our view, it could be relatively easy for My Republic to cross-sell a mobile data

offering to its existing fixed broadband subscribers. A competitively-priced pure

access product could be attractive to an IT savvy, price sensitive user – a profile we

believe may be well represented in My Republic’s existing base.

Issues around wholesale access and spectrum

Clearly, any new entrant into the market would require some form of wholesale

access from incumbents, at least in the initial stages. The key issue is whether

mobile wholesale access should be regulated (as proposed by some of the smaller

operators), given the significant investments already made by the three incumbents.

In its response to the IDA’s consultation paper, My Republic indicated a wish to

acquire spectrum of its own. The 800 MHz and 900 MHz spectrum will be up for

renewal in March 2017. We do not rule out the possibility of My Republic obtaining

some spectrum when these become available. In the table below, we summarise the

status of selected spectrum bands that could become available within the next five

years.

EXHIBIT 18: Status of selected spectrum bands

Spectrum band Current assignments Amount of spectrum available Expiry of existing assigned uses

700 MHz Terrestrial broadcasting 90 MHz After Analogue Switch Off

800 MHz Trunked radio / short range devices / 2G To be determined 31 Mar 2017 (10 MHz for 2G)

900 MHz 2G / 3G / 4G Up to 50 MHz 31 Mar 2017

2.3 GHz Unassigned 50 MHz No existing uses

2.5 GHz (TDD) Partially assigned for WBA/4G 50 MHz 30 Jun 2015

Source: IDA

13

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Differentiated strategy and favourable regulations are key to MVNO success

There are few examples of successful MVNOs globally. Tesco Mobile (UK), Lyca

Mobile (UK), Virgin Mobile (UK and US) and TracFone (US) (all not listed) are among

those. The critical success factor for these MVNOs has been a differentiated and

niche strategy. For example, Lyca Mobile has a SIM-only product, offering the lowest

international calling rates to the Asian community. Similarly, TracFone has achieved

success in offering national/international calls at local rates.

Favourable regulatory conditions have also been a significant factor in the success of

MVNOs. For instance, the regulator in the EU (which hosts two-thirds of the world’s

MVNOs) closely monitors wholesale pricing offered by network providers to MVNOs.

Regulators in France and Hong Kong have facilitated MVNO entry by regulating

wholesale pricing, setting aside minimum network capacity for MVNOs and offering

incentives for network operators to host MVNOs. In line with global precedents, the

IDA has proposed that regulatory, spectrum, licence and voluntary conditions could

be introduced to encourage MVNO-hosting in Singapore.

14

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Small players driving residential broadband competition

Unlike the mobile market, where competition has remained relatively benign so far,

the broadband sector has experienced deteriorating competition in recent years. The

emergence of new entrant retail service providers (RSPs) over the National

Broadband Network (NBN) has contributed to declining ARPUs across the sector.

My Republic noticeably disruptive

My Republic is a fibre broadband operator riding on the NBN. The company recently

secured SGD34m of funding from the telecommunications arm of Sinar Mas Group

(not listed) and Iliad (ILD FP; NR) founder, Xavier Niel, and has ambitions to enter

the mobile market in Singapore (we discuss this later in this report).

According to My Republic’s management, the company’s uniquely lean cost structure

has allowed it to be significantly competitive in its fibre broadband pricing. For

example, My Republic’s 1Gbps fibre plan, priced at SGD49.99, is at an almost 30%

discount to comparable plans offered by SingTel and STH. M1 recently launched a

SGD49 1Gbps plan in response, although this is for a limited promotional period. My

Republic’s pricing strategy has contributed to significant declines in broadband

ARPUs across the sector.

EXHIBIT 19: Selected fibre broadband plans (SGD), by operator

100Mbps 200Mbps 300Mbps 500Mbps 800Mbps 1Gbps

M1 29

39

49

My Republic

49.99

SingTel

49.9 59.9 79.9 69.9

STH 39.9

49.9 69.9

ViewQwest

65 89.95

149.95

Note: Shaded cells denote promotional pricing for limited period; ViewQwest (not listed) plans include Apple TV or ViewQwest TV Source: Company data

EXHIBIT 20: Broadband ARPU declines, by operator EXHIBIT 21: Sector broadband revenue trends

Sources: Company data; BNP Paribas Sources: Company data; BNP Paribas

STH more impacted by disruptive pricing so far

Disruptive pricing led by the smaller RSPs has disproportionately impacted STH. The

operator’s 2Q14 broadband revenues plunged 17% y-y, compared with a 9% decline

for SingTel and 14% increase for M1. We believe STH has had to respond to the

competition, in order to defend its legacy businesses. Consumer broadband

accounts for 10% of STH’s total revenues – the highest among the incumbents.

Furthermore, there is a need for STH to protect its pay-TV business, which is linked

to its broadband business by virtue of its hubbing strategy. It is not difficult to

understand STH’s broadband competitive strategy when we consider that broadband

and pay-TV together account for 26% of its revenues.

(25)

(20)

(15)

(10)

(5)

0

M1 SingTel STH

(%) ARPU decline vs 1 year ago ARPU decline vs 2 years ago

(12)

(10)

(8)

(6)

(4)

(2)

0

2

4

6

110

115

120

125

130

135

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

(y-y %)(SGD m) Broadband revenues (LHS)

Change (RHS)

15

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

EXHIBIT 22: Broadband revenues, by operator EXHIBIT 23: Revenue breakdown, by operator

Note: Comparable data not available for ST before 2Q12 Sources: Company data; BNP Paribas

Note: Broadband refers to consumer broadband revenues Sources: Company data; BNP Paribas

Near-term residential broadband competition could ease

We are cautiously optimistic that broadband competition could stabilise within the

near term and potentially ease going into 2015. Our recent checks with management

across the incumbents and smaller RSPs suggest limited near-term downside from

current pricing levels. In fact, we believe there may be attempts by operators to move

to a less competitive pricing regime, although this may not necessarily result in an

absolute tariff increase. Importantly, My Republic’s stated ambitions to expand its

business outside of Singapore (e.g. planned launches in New Zealand and Malaysia

over the next two years) could mean a less aggressive pricing strategy domestically.

Clearly, this would be positive for all three major operators. And just as disruptive

price competition has disproportionately impacted STH to the downside, it could be

argued that less aggressive pricing would have the greatest positive impact on STH.

Slight optimism around SME fibre take-up

The structural issues around enterprise access over the NBN are well flagged. But

we believe there is cause for some optimism. As part of the 2014 budget, the

government announced a number of initiatives targeted at accelerating ICT adoption

amongst SMEs. For example, there are plans to provide SMEs that tap qualifying

ICT-based productivity solutions with a 50% subsidy on their NBN subscriptions for

up to two years. In addition, the government will offer subsidies of up to SGD200k

per building to commercial building owners, as an offset to NBN installation charges.

While we are still not expecting a significant acceleration in SME fibre adoption within

the near term, the government’s initiatives are clearly a positive development.

SME competition likely to intensify

Building on its relative success in the residential broadband space, My Republic

launched an enterprise offering, aimed at the SME segment, earlier this year. The

company is targeting to grow enterprise to the current size of its residential business

within two years. This could potentially involve aggressive pricing, aimed at basic

users and value segments. Elsewhere, Superinternet is also looking to penetrate the

SME segment. The operator recently acquired an FBO licence and is selectively

rolling out its own fibre network to target SME customers.

Near-term impact on ST and STH may be relatively limited

Clearly, increased competition in the SME segment would hurt SingTel, given its

current dominance in this space. But given the relative complexity of enterprise

services, customer churn tends to be lower in this segment (versus residential) – a

point acknowledged by the challenger telcos. Even within the more price-sensitive

SME space, we expect market share erosion of incumbents’ bases will take time. In

addition, given the relatively low telco spend by SMEs, any negative financial impact

on SingTel is unlikely to be significant near term.

0

10

20

30

40

50

60

70

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

(SGD m) M1 SingTel STH

0

10

20

30

40

50

60

70

80

90

100

M1 SingTel STH

(%) Mobile Broadband Pay-TV Others

16

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

In view of intensifying competition, STH is shifting its focus away from SMEs (a

segment it initially identified as an opportunity), towards corporates. While there will

clearly be challenges targeting the corporate segment, there are indications STH has

gained some traction within this space in recent months. In any case, STH’s growing

focus on the corporate segment suggests competitive action by the smaller operators

should have a relatively subdued impact on the company.

We view M1 as most vulnerable in terms of potentially constrained upside

We do have concerns that increased assertiveness from the smaller RSPs could

potentially limit upside for M1. We recognise that M1 has the ability to offer enterprise

services of relative sophistication. But as a new entrant in the enterprise segment,

there could be a meaningful overlap between M1’s addressable market and that of

the other smaller operators. For this reason, among others, we do not share the

market’s optimism around M1.

17

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Near-term pay-TV outlook is stable

We have concerns around the long-term structural outlook of the pay-TV business.

The increasing emergence of OTT content sources suggests cord-trimming or cord-

cutting could become a growing threat to traditional pay-TV operators. But while our

projections do not assume meaningful near-term growth for this business, neither are

we expecting any significant revenue erosion over the next two to three years. In

reality, the pay-TV market in Singapore is flat, but signs of significant deterioration

are also absent. Recent ARPU trends have been, to some extent, supported by tariff

adjustments.

EXHIBIT 24: Pay-TV subscriber trends EXHIBIT 25: Pay-TV ARPU trends, by operator

Note: We believe subscriber growth in initial periods was boosted by take-up of dual STBs Sources: Company data; BNP Paribas

Sources: Company data; BNP Paribas

Important element of a strong bundling strategy

For major operators, pay-TV could be a competitive differentiator in an increasingly

crowded market. We view it as a retention strategy by incumbents to defend their

broadband businesses. As such, the bundling strategies adopted by STH and

SingTel should cushion the impact of aggressive price competition – a move

generally favoured by smaller new entrants. For this reason, M1 has also launched a

content service, branded MiBox, although this remains very niche.

Looking ahead, we believe a strong integrated/bundling strategy will become

increasingly important, especially if smaller operators enter the mobile market. From

this perspective and based on this measure, we favour STH and SingTel over M1 on

a medium-term horizon.

0

2

4

6

8

10

12

14

16

760

780

800

820

840

860

880

900

920

940

960

980

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

(y-y %)('000) Pay-TV subscribers (LHS) Change (RHS)

0

10

20

30

40

50

60

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

(SGD) STH SingTel

18

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Sector revenue outlook

Overall, we forecast accelerating sector revenue growth over 2014-15, supported by

growing mobile data usage, expanding LTE network coverage and further boosted by

the recent tariff increases. As highlighted above, we are optimistic STH will be able to

deliver above-industry growth in 2015, supported by its sharper mobile tariff

adjustments and accelerated LTE network expansion.

EXHIBIT 26: Sector revenue trends EXHIBIT 27: Total revenue y-y chg, by operator

Note: 2014E refers to FY15E for SingTel; refers to domestic operations for SingTel Sources: Company data; BNP Paribas estimates

Note: 2014E refers to FY15E for SingTel; refers to domestic operations for SingTel Sources: Company data; BNP Paribas estimates

(1)

0

1

2

3

4

5

6

7,800

8,000

8,200

8,400

8,600

8,800

9,000

9,200

9,400

9,600

9,800

2011 2012 2013 2014E 2015E 2016E

(y-y %)(SGD m) Sector revenues (LHS) Change (RHS)

(8)

(6)

(4)

(2)

0

2

4

6

8

10

2011 2012 2013 2014E 2015E 2016E

(%) M1 SingTel STH

19

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Sector EBITDA and margin outlook

We expect gradual expansion in the sector’s EBITDA margin beyond 2014, driven by

continued improvements in data monetisation and moderating handset subsidies. A

potential downside risk to our margin assumptions is a spike in mobile and/or

broadband competition, leading to escalated marketing costs across the sector.

EXHIBIT 28: Sector EBITDA trends EXHIBIT 29: EBITDA y-y chg, by operator

Note: 2014E refers to FY15E for SingTel; refers to domestic operations for SingTel. Sources: Company data; BNP Paribas estimates

Note: 2014E refers to FY15e for SingTel; refers to domestic operations for SingTel. Sources: Company data; BNP Paribas estimates

36.0

36.5

37.0

37.5

38.0

38.5

39.0

39.5

2,000

2,200

2,400

2,600

2,800

3,000

3,200

3,400

3,600

3,800

4,000

2011 2012 2013 2014E 2015E 2016E

(%)(SGD m)Sector EBITDA (LHS)

Sector EBITDA margin (RHS)

(6)

(4)

(2)

0

2

4

6

8

10

12

14

2011 2012 2013 2014E 2015E 2016E

(%) M1 SingTel STH

20

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Sector capex outlook

We project sustained increases in sector capex over 2014-15, driven by operators’

LTE network expansion and spectrum payments due end-2014. Beyond 2015, we

forecast a slight dip in sector capex, although this should generally remain at

relatively elevated levels.

EXHIBIT 30: Sector capex outlook

Note: 2014E refers to FY15E for SingTel; refers to domestic operations for SingTel Sources: Company data; BNP Paribas estimates

13.0

13.5

14.0

14.5

15.0

15.5

0

200

400

600

800

1,000

1,200

1,400

1,600

2011 2012 2013 2014E 2015E 2016E

(%)(SGD m) Sector capex (LHS) Capex/sales (RHS)

21

Singapore Telecoms Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Regional telco comps

EXHIBIT 31: Regional telco comps

Name BBG code Price Mkt cap ----------- P/E ----------- ------ EV/EBITDA ------ ----------- P/BV ----------- -------- Div yield --------

FY14E FY15E FY14E FY15E FY14E FY15E FY14E FY15E

(LC) (USD m) (x) (x) (x) (x) (x) (x) (%) (%)

China Mobile* 941 HK 94.95 249,495 14.3 14.0 4.5 4.1 1.8 1.7 3.0 3.1

China Telecom* 728 HK 4.70 49,045 16.0 13.7 3.9 3.7 1.0 1.0 2.2 2.5

China Unicom* 762 HK 11.70 36,073 18.2 15.8 3.5 3.4 1.0 0.9 2.2 2.5

Taiwan Mobile* 3045 HK 93.60 10,541 17.0 18.8 9.7 9.3 4.5 4.7 5.9 5.3

Chunghwa* 2412 TT 91.40 23,342 19.3 19.3 8.8 8.6 2.0 2.0 4.9 4.7

Far Eastone* 4904 TT 60.60 6,501 17.5 17.8 7.5 7.1 2.7 2.8 6.2 6.2

Hutchison* 215 HK 3.04 1,889 18.7 17.2 7.6 7.5 1.3 1.3 4.0 4.4

SmarTone* 315 HK 10.40 1,403 20.4 19.7 4.2 4.6 3.4 3.3 2.9 4.3

HKT Trust* 6823 HK 9.31 9,089 24.1 20.0 8.5 7.6 1.8 1.8 5.2 5.8

CITIC Telecom* 1883 HK 2.99 1,291 13.3 11.3 8.0 7.4 1.4 1.3 4.5 5.1

SingTel* ST SP 3.80 47,739 16.4 15.3 8.8 8.3 2.4 2.3 4.6 4.9

StarHub* STH SP 4.09 5,557 19.5 17.4 10.2 9.4 71.5 44.2 4.9 4.9

M1* M1 SP 3.53 2,589 18.2 17.1 10.1 9.6 7.6 7.0 4.4 4.7

Advanced Info ADVANC TB 226.00 20,732 16.3 13.9 9.1 8.3 13.8 12.9 6.1 7.3

DTAC DTAC TB 103.50 7,562 16.0 14.0 6.9 6.2 7.5 7.4 6.6 7.5

Axiata Group AXIATA MK 7.04 18,612 20.3 18.4 8.8 8.3 2.8 2.7 3.8 4.3

DiGi.Com DIGI MK 5.85 14,020 22.3 21.1 13.6 12.9 63.6 61.6 4.4 4.7

Maxis Bhd MAXIS MK 6.47 14,969 23.1 21.9 12.3 12.0 10.8 11.8 4.9 5.1

TM T MK 6.83 7,720 25.1 22.8 7.4 7.1 3.4 3.3 3.7 3.9

Indosat ISAT IJ 3,850 1,719 19.1 17.0 3.8 3.7 1.2 1.2 2.5 2.8

Telkom Indonesia TLKM IJ 2,800 23,186 16.4 15.2 6.2 5.9 3.7 3.4 4.3 4.8

XL Axiata EXCL IJ 6,075 4,259 38.5 22.3 7.3 6.4 3.2 2.9 1.0 2.0

Globe Telecom* GLO PM 1,650 4,898 18.1 15.3 7.0 6.6 5.2 5.0 5.4 5.9

PLDT* TEL PM 3,044 14,709 17.5 16.3 8.9 8.7 4.8 4.8 5.7 6.1

Bharti Airtel* BHARTI IN 404.95 26,526 30.5 23.6 7.2 6.4 2.5 2.3 0.2 0.5

Idea Cellular* IDEA IN 160.40 9,453 21.3 23.2 7.9 7.3 2.6 2.3 - -

Reliance Comm* RCOM IN 104.85 4,128 25.2 24.9 8.1 7.1 0.8 0.8 - -

KT Corp* 030200 KS 35,250 8,532 (19.2) 11.1 5.8 4.0 0.8 0.7 - 1.4

LG Uplus* 032640 KS 11,950 4,837 20.7 11.5 4.6 4.0 1.2 1.2 2.5 2.9

SK TELECOM* 017670 KS 281,000 21,033 11.5 9.4 4.9 4.3 1.5 1.3 3.3 3.3

NTT Docomo* 9437 JP 1,717.50 69,544 13.1 12.2 4.8 4.7 1.2 1.1 3.7 3.9

KDDI* 9433 JP 6,549.00 54,492 11.4 10.7 5.1 4.9 1.6 1.5 2.8 3.0

Softbank* 9984 JP 7,233.00 80,560 13.6 11.4 7.2 6.6 2.8 2.2 0.6 0.7

Note: As at 9 October 2014 close Sources * BNP Paribas estimates; all others (Not rated) are Bloomberg consensus estimates

22

Risks emerging n Potential upside largely priced in – initiate at HOLD, SGD3.75 TP

We like M1 for its nimbleness and technology focus, and expect

healthy mobile gains on the back of data growth. However, we view

related upside as largely priced in at current levels. Longer term, we

see vulnerabilities as smaller operators encroach on M1’s

addressable market in broadband and potentially mobile.

n Mobile momentum may taper; potential competition risks

Operationally, M1 has been the best performing Singapore telco over

the last year, as its mobile focus positions it well to ride the data

wave. But, after several quarters of robust mobile gains, we believe

incremental growth could start to taper. We view M1 as potentially

the most vulnerable to intensifying mobile competition, given its less-

established bundling strategy.

n Assertive smaller operators could limit broadband upside

We accept that the NBN offers significant fixed-line opportunities for

M1. However, we are concerned the increasingly assertive behaviour

of smaller new entrants could limit the upside for M1. With My

Republic (not listed) and Superinternet (not listed) looking to

aggressively target the SME market, we have reservations about

growth momentum for M1 in this segment.

n Relative share price outperformance likely to narrow

M1 has been the best performing Singapore telco stock in the past 12

months, reflecting its strong mobile operational performance in recent

quarters. With mobile momentum potentially tapering and emerging

competition risks, we see limited upside potential from current levels,

and M1’s relative outperformance to peers may narrow.

M1 fibre broadband ARPU

Source: M1 Ltd

40

42

44

46

48

50

52

54

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

(SGD)

10 OCTOBER 2014

INITIATION 10 SINGAPORE SINGAPORE / WIRELESS TELECOMMUNICATION SERVICES

M1 LTD M1 SP

HOLD

TARGET PRICE SGD3.75

CLOSE SGD3.53

UP/DOWNSIDE +6.1%

SGD %

HOW WE DIFFER FROM CONSENSUS MARKET RECS

TARGET PRICE (%) (0.3) POSITIVE 11

EPS 2014 (%) 3.9 NEUTRAL 10

EPS 2015 (%) 3.7 NEGATIVE 3

Wei Shi Wu [email protected] +65 6210 1925

KEY STOCK DATA

YE Dec (SGD m) 2013A 2014E 2015E 2016E

Revenue 1,008 1,074 1,126 1,172

Rec. net profit 160 180 192 203

Recurring EPS (SGD) 0.17 0.19 0.21 0.22

EPS growth (%) 8.3 11.4 6.3 5.9

Recurring P/E (x) 20.3 18.2 17.1 16.2

Dividend yield (%) 5.9 4.4 4.7 5.0

EV/EBITDA (x) 11.1 10.1 9.6 9.1

Price/book (x) 8.3 7.6 7.0 6.5

Net debt/Equity (%) 49.4 50.9 39.0 39.8

ROE (%) 43.1 43.5 42.7 41.6

Share price performance 1 Month 3 Month 12 Month

Absolute (%) (4.6) (0.8) 3.5

Relative to country (%) (2.1) (0.4) 0.2

Next results October 2014

Mkt cap (USD m) 2,583

3m avg daily turnover (USD m) 2.3

Free float (%) 39

Major shareholder Axiata Investments (29%)

12m high/low (SGD) 3.83/3.17

3m historic vol. (%) 16.6

ADR ticker -

ADR closing price (USD) -

Issued shares (m) 930

Sources: Bloomberg consensus; BNP Paribas estimates

(2)

3

8

13

3.00

3.20

3.40

3.60

3.80

4.00

Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

(%)(SGD) M1 Ltd Rel to Straits Times Index

23

M1 Ltd M1 SP Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Investment thesis

M1’s mobile focus suggests it is most sensitive to improving mobile sector dynamics, including better data monetisation and declining handset subsidies. This has supported the company’s recent operational outperformance. While we are still generally positive on the sector’s near-term mobile outlook, it is possible incremental growth for M1 could start to taper, following several quarters of robust gains.

Within broadband, we have concerns that increasingly assertive smaller operators will encroach upon M1’s addressable market, effectively limiting potential upside for this company. We recognise M1’s scale and service sophistication offer some differentiation from the smaller operators, but among the major telcos, its competitive positioning would be closest to the smaller operators.

Over the longer term, M1’s less established bundling strategy vs peers increases its vulnerability to potential new mobile entrants, in our view.

Catalyst

Expected near-term robust mobile performance and the dividend yield should provide share price support. But over the longer-term, competition risks could narrow the relative share price performance versus peers.

Risks to our call

Key downside risks: Accelerated mobile competition, leading

to market share and/or ARPU erosion; more intense than

expected broadband competition, leading to slower revenue

gains; accelerated handset costs, leading to lower margins;

higher than expected capex.

Key upside risks: More benign than expected competition,

leading to accelerated revenue growth; faster than expected

data usage increase, driving mobile ARPU gains; lower than

expected capex; accelerated shareholder returns.

Company background Key assumptions

M1 is a Singapore telecoms company, offering mobile,

broadband and IDD services.

FY13 FY14E FY15E FY16E

(%) (%) (%) (%)

Mobile revenue growth 6.1 4.9 6.4 5.4

EBITDA margin 31.0 32.0 32.3 32.6

Source: M1 Ltd; BNP Paribas estimates

Principal activities, revenue split FY14 Earnings sensitivity

----------- FY14E ----------- ----------- FY15E -----------

Bear Base Bull Bear Base Bull

(%) (%) (%) (%) (%) (%)

Mobile revenue growth 3.9 4.9 5.9 5.4 6.4 7.4

EPS change (1)

2 (3)

3

EBITDA margin 30.0 32.0 33.0 30.3 32.3 33.3

EPS change (10)

5 (10)

5

Key executives Source: BNP Paribas estimates

Title

Karen Kooi Lee Wah CEO

Raymond Yeo Eng Ann CFO

Lee Kok Chew CCO

Patrick Michael Scodeller COO and CTO

http://www.m1.com.sg

Key earnings drivers include mobile revenue growth and

EBITDA margin.

We estimate a 1ppt change in mobile revenue growth rate

changes our FY15E EPS by 3%.

We estimate a 1ppt change in our EBITDA margin

projection changes our FY15E EPS by 5%.

Mobile (62.88%)

International call services(8.76%)

Fixed services (6.59%)

Handset sales (21.77%)

24

M1 Ltd M1 SP Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Initiate coverage with a HOLD rating and TP of SGD3.75

We like M1 for its technological focus and ability to respond quickly to competition.

We also recognise M1’s mobile focus positions it well to ride the mobile data wave.

However, we think related upside has largely been priced in. We do not share the

market’s apparent enthusiasm around M1’s fixed broadband opportunities, as

accelerated competitive pressures in the SME segment could limit incremental gains

for this company, in our view. Furthermore, we do not think the market has fully

accounted for the potential risks of increased competition in the mobile segment.

M1 has been the best performing Singapore telco ytd. With market expectations

already fairly high, we see limited scope for further upside at current valuations.

However, the supportive dividend yield limits the downside risk.

Mobile: Riding the data wave, but longer-term risks loom

M1 has been the best performing Singapore telco in the mobile sector. It is the only

operator in the market that has consistently grown post-paid ARPU in the past few

quarters. This could be attributed to the company’s technological focus. In addition,

the operator has been relatively cushioned from the impact of reduced roaming, as

this has always been a small part of M1’s business. Increasing data demand

(supported by ongoing LTE Advanced network rollout) and better data monetisation

should continue to drive healthy ARPU gains for M1. This should offset the negative

impact of M1’s post-paid subscriber share erosion.

EXHIBIT 1: M1 post-paid net adds and sub share EXHIBIT 2: M1 post-paid ARPU trends

Sources: M1 Ltd; BNP Paribas Sources: M1 Ltd; BNP Paribas

We expect the pre-paid segment will continue to be impacted by rationalisation of the

base, following the regulator’s reduction of SIMs per user. Furthermore, industry-

wide issues such as increasing Wi-Fi offload, reduced IDD volumes and relatively

weak tourist arrivals could limit pre-paid revenue gains near term.

24.5

25.0

25.5

26.0

26.5

27.0

0

2

4

6

8

10

12

14

16

18

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

(%)('000)Post-paid net adds (LHS)

Post-paid sub share (RHS)

(12)

(10)

(8)

(6)

(4)

(2)

0

2

4

6

8

49

50

51

52

53

54

55

56

57

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

(y-y %)(SGD) Post-paid ARPU (LHS) Change (RHS)

25

M1 Ltd M1 SP Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

EXHIBIT 3: M1 pre-paid net adds and sub share EXHIBIT 4: M1 pre-paid ARPU trends

Sources: M1 Ltd; BNP Paribas Sources: M1 Ltd; BNP Paribas

Longer-term competition risks to consider

We are not convinced the market has fully considered the potential longer-term risks

of increased mobile sector competition. Clearly, there are significant challenges for a

new mobile operator in a mature market, but in our view, these are not

insurmountable. Should the mobile market become more crowded, we would favour

operators with strong bundling strategies. Based on this measure alone, M1 appears

potentially the most vulnerable of the incumbents.

Broadband: Smaller new entrants may limit upside

The market has been excited about M1’s potential broadband opportunities on the

back of the National Broadband Network (NBN). We recognise that the potential

upside is material, given this represents a new revenue stream for M1. In addition,

the ability to offer fixed-line services significantly enhances M1’s long-term

competitive positioning. The company has been registering robust growth in fixed

network services, albeit from a low base.

EXHIBIT 5: M1 fibre broadband subscriber trends EXHIBIT 6: M1 fixed network services revenue trends

Note: Subscriber share based on SingTel’s and STH’s reported broadband subscribers. Sources: M1 Ltd; BNP Paribas

Sources: M1 Ltd; BNP Paribas

However, we are concerned that the increasingly assertive smaller new entrants will

limit further upside for M1. Clearly, M1’s scale and integrated suite of offerings

represent a material differentiator from smaller operators. But positioning-wise, it

would be closest amongst the incumbents to the challenger telcos. My Republic and

Superinternet have stated their intention to aggressively penetrate SMEs – a

segment previously identified by M1’s management as a key opportunity area. We

believe this could erode M1’s addressable market, with any related price competition

limiting revenue upside.

23.0

23.5

24.0

24.5

25.0

25.5

26.0

26.5

27.0

(120)

(100)

(80)

(60)

(40)

(20)

0

20

40

60

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

(%)('000) Pre-paid net adds (LHS)

Pre-paid sub share (RHS)

(25)

(20)

(15)

(10)

(5)

0

5

10

15

20

25

0

2

4

6

8

10

12

14

16

18

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

(y-y %)(SGD) Pre-paid ARPU (LHS) Change (RHS)

0

1

2

3

4

5

6

7

8

9

0

10

20

30

40

50

60

70

80

90

100

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

(%)('000) Fibre broadband subs (LHS)

Broadband sub share (RHS)

0

10

20

30

40

50

60

70

80

90

0

2

4

6

8

10

12

14

16

18

20

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

(y-y %)(SGD m) Fixed network services revenues (LHS)

Change (RHS)

26

M1 Ltd M1 SP Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Revenue forecasts

We expect robust FY14 revenue growth, supported by mobile and reflecting recent

trends. The deceleration in FY15 revenue growth is mainly due to our anticipation of

lower handset sales.

EXHIBIT 7: Revenue forecasts

FY11 FY12 FY13 FY14E FY15E FY16E

(SGD m) (SGD m) (SGD m) (SGD m) (SGD m) (SGD m)

Mobile 587 607 644 676 719 758

International call services 125 116 114 94 87 80

Fixed services 38 48 62 71 82 91

Handset sales 314 305 188 234 238 243

Total revenues 1,065 1,077 1,008 1,074 1,126 1,172

Change (y-y %)

1.1 (6.4) 6.6 4.8 4.1

Sources: M1 Ltd; BNP Paribas estimates

Opex forecasts

We forecast FY14 opex growth of 5%, driven largely by handset costs. The opex

outlook is largely predicated on M1’s ability to manage handset costs/subsidies.

EXHIBIT 8: Opex forecasts

FY11 FY12 FY13 FY14E FY15E FY16E

(SGD m) (SGD m) (SGD m) (SGD m) (SGD m) (SGD m)

Handset costs 366 385 284 309 318 325

Traffic expenses 65 64 70 66 67 67

Wholesale costs of fixed services 21 25 31 35 41 46

Other cost of sales 41 41 39 40 44 46

Staff costs 97 97 109 113 119 124

Advertising and promotion 27 22 25 27 29 32

Others 142 143 140 142 146 151

Total opex 757 778 697 732 764 791

Change (y-y %)

2.7 (10.3) 5.0 4.3 3.6

Sources: M1 Ltd; BNP Paribas estimates

Key financial forecasts

We anticipate M1 will deliver robust EBITDA gains in FY14, supported by strong

mobile momentum and sustained margin improvements. But while we believe further

margin expansion beyond FY14 is possible, we project a deceleration in such gains,

reflecting greater competitive intensity in the enterprise broadband segment.

FY14 and FY16 capex will be impacted by spectrum payments (for the spectrum

acquired in the 2013 auction). But otherwise, we see few reasons for any significant

capex spike within the foreseeable future.

27

M1 Ltd M1 SP Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

EXHIBIT 9: Key financial forecasts

FY11 FY12 FY13 FY14E FY15E FY16E

(SGD m) (SGD m) (SGD m) (SGD m) (SGD m) (SGD m)

Revenues 1,065 1,077 1,008 1,074 1,126 1,172

Change (y-y %)

1.1 (6.4) 6.6 4.8 4.1

EBITDA 310 300 312 344 364 382

Change (y-y %)

(3.3) 4.2 10.2 5.7 5.1

EBITDA margin 29.1 27.8 31.0 32.0 32.3 32.6

Net profit 164 146 160 180 192 203

Change (y-y %)

(10.6) 9.4 12.2 6.8 5.9

Capex 124 123 125 170 129 193

Change (y-y %)

(1.4) 2.0 36.0 (23.8) 49.0

Capex/sales 11.7 11.4 12.4 15.8 11.5 16.5

Sources: M1 Ltd; BNP Paribas estimates

BNP Paribas versus consensus

We are slightly ahead of Bloomberg consensus in our forecasts; we believe, due to

our more optimistic mobile assumptions.

EXHIBIT 10: BNPP versus consensus estimates

---------------- FY14E ------------- --------------- FY15E------------- ---------------- FY16E -------------

BNPP Cons Var BNPP Cons Var BNPP Cons Var

(SGD m) (SGD m) (%) (SGD m) (SGD m) (%) (SGD m) (SGD m) (%)

Revenues 1,074 1,040 3 1,126 1,076 5 1,172 1,100 7

EBITDA 344 332 4 364 350 4 382 362 6

EBITDA margin (%) 32.0 31.9

32.3 32.5

32.6 32.9

Net profit 180 173 4 192 185 4 203 195 4

Sources: Bloomberg consensus estimates; BNP Paribas estimates

Dividend outlook

We assume an 80% dividend payout over FY14-16, in line with management

guidance. Based on our current projections, dividend/FCF increases sharply in FY16,

due to the expected spectrum payments.

EXHIBIT 11: M1 dividend outlook

Source: BNP Paribas estimates

70

80

90

100

110

120

130

15

15

16

16

17

17

18

18

FY14E FY15E FY16E

(%)(SGD cents/share) DPS (c/share) (LHS) Div/FCF (RHS)

28

M1 Ltd M1 SP Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Valuations

At current levels, M1 is trading >1SD above its five-year historical average P/E and

EV/EBITDA. We think there is limited scope for significant share price upside,

especially in view of potential competition risks.

EXHIBIT 12: P/E EXHIBIT 13: EV/EBITDA

Sources: Bloomberg; BNP Paribas Sources: Bloomberg; BNP Paribas

We value M1 using DCF analysis, based on 7.4% WACC (2.4% risk free rate, 5.6%

equity risk premium, 5% cost of debt) and 0% terminal growth rate to reflect the long-

term growth nature of the Singapore telecoms market. Our SGD3.75 TP implies

about 18x FY15 P/E and 10x FY15 EV/EBITDA.

EXHIBIT 14: M1 DCF valuation

2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E

(SGD m) (SGD m) (SGD m) (SGD m) (SGD m) (SGD m) (SGD m) (SGD m) (SGD m) (SGD m)

EBIT 237 251 260 273 280 287 295 304 313 320

Less: Tax (40) (43) (44) (46) (48) (49) (50) (52) (53) (54)

Add: Depreciation 126 131 138 142 147 151 154 157 161 167

Less: Capex (129) (193) (128) (126) (123) (119) (122) (125) (128) (131)

Less: Chg in WC (1) (1) (0) (1) (1) (0) (0) (0) (1) (1)

FCF 193 146 225 242 256 270 277 284 292 301

NPV FCF 1,657

NPV TV 2,010

EV 3,667

FY15E net debt (183)

Equity value 3,485

Target price (SGD) 3.75

Note: We use outstanding share base of 930m shares Source: BNP Paribas estimates

Risks to our recommendation and estimates

Key downside risks: Accelerated mobile competition, leading to market share and/or

ARPU erosion; more intense than expected broadband competition, leading to

slower revenue gains; accelerated handset costs, leading to lower margins; higher

than expected capex.

Key upside risks: More benign than expected competition, leading to accelerated

revenue growth; faster than expected data usage increase, driving mobile ARPU

gains; lower than expected capex; accelerated shareholder returns.

7

9

11

13

15

17

19

21

Se

p-0

9

Ja

n-1

0

Ma

y-1

0

Se

p-1

0

Ja

n-1

1

Ma

y-1

1

Se

p-1

1

Ja

n-1

2

Ma

y-1

2

Se

p-1

2

Ja

n-1

3

Ma

y-1

3

Se

p-1

3

Ja

n-1

4

Ma

y-1

4

(x)

+1 SD

+2 SD

-1 SD

-2 SD

5-yr avg.

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

Se

p-0

9

Ja

n-1

0

Ma

y-1

0

Se

p-1

0

Ja

n-1

1

Ma

y-1

1

Se

p-1

1

Ja

n-1

2

Ma

y-1

2

Se

p-1

2

Ja

n-1

3

Ma

y-1

3

Se

p-1

3

Ja

n-1

4

Ma

y-1

4

(x)

+1 SD

+2 SD

-1 SD

-2 SD

5-yr avg.

29

M1 Ltd M1 SP Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Financial statements M1 Ltd

Profit and Loss (SGD m) Year Ending Dec 2012A 2013A 2014E 2015E 2016E

Revenue 1,077 1,008 1,074 1,126 1,172

Cost of sales ex depreciation (778) (697) (732) (764) (791)

Gross profit ex depreciation 299 311 342 362 380

Other operating income 1 2 2 2 2

Operating costs 0 0 0 0 0

Operating EBITDA 300 312 344 364 382

Depreciation (111) (115) (121) (126) (131)

Goodwill amortisation 0 0 0 0 0

Operating EBIT 189 197 223 237 251

Net financing costs (6) (5) (6) (6) (6)

Associates 0 0 0 0 0

Recurring non operating income 0 0 0 0 0

Non recurring items 0 0 0 0 0

Profit before tax 183 193 216 231 245

Tax (37) (33) (37) (39) (42)

Profit after tax 146 160 180 192 203

Minority interests 0 0 0 0 0

Preferred dividends 0 0 0 0 0

Other items 0 0 0 0 0

Reported net profit 146 160 180 192 203

Non recurring items & goodwill (net) 0 0 0 0 0

Recurring net profit 146 160 180 192 203

Per share (SGD)

Recurring EPS * 0.16 0.17 0.19 0.21 0.22

Reported EPS 0.16 0.17 0.19 0.21 0.22

DPS 0.15 0.21 0.16 0.17 0.17

Growth

Revenue (%) 1.1 (6.4) 6.6 4.8 4.1

Operating EBITDA (%) (3.3) 4.2 10.2 5.7 5.1

Operating EBIT (%) (7.0) 4.5 12.8 6.6 5.7

Recurring EPS (%) (11.1) 8.3 11.4 6.3 5.9

Reported EPS (%) (11.1) 8.3 11.4 6.3 5.9

Operating performance

Gross margin inc depreciation (%) 17.5 19.4 20.5 20.9 21.2

Operating EBITDA margin (%) 27.8 31.0 32.0 32.3 32.6

Operating EBIT margin (%) 17.5 19.6 20.7 21.1 21.4

Net margin (%) 13.6 15.9 16.7 17.0 17.3

Effective tax rate (%) 20.1 16.9 17.0 17.0 17.0

Dividend payout on recurring profit (%) 90.9 120.7 80.1 80.1 80.1

Interest cover (x) 34.3 43.8 36.6 38.5 41.5

Inventory days 16.2 16.2 15.3 15.9 15.9

Debtor days 62.4 58.8 54.1 57.5 57.7

Creditor days 106.3 112.3 107.5 109.9 110.3

Operating ROIC (%) 25.6 26.5 28.9 29.4 29.7

ROIC (%) 21.8 23.0 25.4 26.0 26.4

ROE (%) 43.6 43.1 43.5 42.7 41.6

ROA (%) 15.4 16.7 18.2 18.4 18.6

*Pre exceptional, pre-goodwill and fully diluted

Revenue By Division (SGD m) 2012A 2013A 2014E 2015E 2016E

Mobile 607 644 676 719 758

International call services 116 114 94 87 80

Fixed services 48 62 71 82 91

Handset sales 305 188 234 238 243

Sources: M1 Ltd; BNP Paribas estimates

30

M1 Ltd M1 SP Wei Shi Wu

BNP PARIBAS 10 OCTOBER 2014

Financial statements M1 Ltd

Cash Flow (SGD m) Year Ending Dec 2012A 2013A 2014E 2015E 2016E

Recurring net profit 146 160 180 192 203

Depreciation 111 115 121 126 131

Associates & minorities 0 0 0 0 0

Other non-cash items 10 3 4 2 2

Recurring cash flow 267 278 305 321 337

Change in working capital 8 24 (15) (1) (1)

Capex - maintenance (123) (126) (170) (129) (193)

Capex - new investment 0 0 0 0 0

Free cash flow to equity 152 176 120 190 143

Net acquisitions & disposals 0 0 0 0 0

Dividends paid (132) (136) (144) (154) (163)

Non recurring cash flows 1 4 0 0 0

Net cash flow 21 43 (24) 37 (20)

Equity finance 10 22 0 0 0

Debt finance (31) (22) 0 0 0

Movement in cash (1) 43 (24) 37 (20)

Per share (SGD)

Recurring cash flow per share 0.29 0.30 0.33 0.34 0.36

FCF to equity per share 0.17 0.19 0.13 0.20 0.15

Balance Sheet (SGD m) Year Ending Dec 2012A 2013A 2014E 2015E 2016E

Working capital assets 235 195 228 239 249

Working capital liabilities (253) (235) (257) (270) (280)

Net working capital (18) (40) (29) (31) (32)

Tangible fixed assets 630 649 698 701 762

Operating invested capital 612 609 668 670 730

Goodwill 0 0 0 0 0

Other intangible assets 99 88 88 88 88

Investments 0 0 0 0 0

Other assets 0 0 0 0 0

Invested capital 711 697 756 758 818

Cash & equivalents (12) (55) (31) (67) (48)

Short term debt 272 0 0 0 0

Long term debt * 0 250 250 250 250

Net debt 260 195 219 183 202

Deferred tax 103 107 107 107 107

Other liabilities 0 0 0 0 0

Total equity 348 395 430 468 509

Minority interests 0 0 0 0 0

Invested capital 711 697 756 758 818

* includes convertibles and preferred stock which is being treated as debt

Per share (SGD)

Book value per share 0.38 0.43 0.46 0.50 0.55

Tangible book value per share 0.27 0.33 0.37 0.41 0.45

Financial strength

Net debt/equity (%) 74.7 49.4 50.9 39.0 39.8

Net debt/total assets (%) 26.6 19.8 21.0 16.7 17.7

Current ratio (x) 0.5 1.1 1.0 1.1 1.1

CF interest cover (x) 28.7 40.1 20.8 31.9 24.6

Valuation 2012A 2013A 2014E 2015E 2016E

Recurring P/E (x) * 22.0 20.3 18.2 17.1 16.2

Recurring P/E @ target price (x) * 23.3 21.5 19.3 18.2 17.2

Reported P/E (x) 22.0 20.3 18.2 17.1 16.2

Dividend yield (%) 4.1 5.9 4.4 4.7 5.0

P/CF (x) 12.0 11.7 10.7 10.2 9.7

P/FCF (x) 21.1 18.5 27.2 17.3 23.0

Price/book (x) 9.3 8.3 7.6 7.0 6.5

Price/tangible book (x) 12.9 10.6 9.6 8.6 7.8

EV/EBITDA (x) ** 11.6 11.1 10.1 9.6 9.1

EV/EBITDA @ target price (x) ** 12.3 11.7 10.7 10.1 9.6

EV/invested capital (x) 4.9 5.0 4.6 4.6 4.3

* Pre exceptional, pre-goodwill and fully diluted ** EBITDA includes associate income and recurring non-operating income

Sources: M1 Ltd; BNP Paribas estimates

31

No significant near-term catalysts n Transfer coverage and maintain HOLD on limited catalysts

We expect relative stability in SingTel’s Singapore operations,

supported by improving mobile sector dynamics. However, sustained

competitive pressures in Australia could limit near-term upside for

Optus. While the fundamental outlook for associates is strong, FX