Embed Size (px)

Citation preview

Overview of Corporate Financial Statements

Or . . . What are all those numbers anyway?

Required Financial Statements

Financial Position at the end of the period;

Earnings for the period;

Cash flows during the period; and

Investments by and distributions to owners during the period.

The Accounting EquationThe Accounting Equation

AssetsAssets =

Resources owned by the firmowned by the firm with the potential to provide future economic future economic benefitsbenefits, as a result of past transactions or events.

The Accounting EquationThe Accounting Equation

AssetsAssets = LiabilitiesLiabilities

Creditors’ fixed claims on the assetsresulting from pastpast transactions and representing probable future probable future sacrifices sacrifices of economic benefits (resources).

The Accounting EquationThe Accounting Equation

AssetsAssets LiabilitiesLiabilities Owners’Equity

Owners’Equity= +

Owners’ residualresidual interest after all liabilities have been settled.

The Accounting EquationThe Accounting Equation

AssetsAssets LiabilitiesLiabilities Owners’Equity

Owners’Equity

CapitalStock

CapitalStock

RetainedEarnings

RetainedEarnings

= +

Earned Capital

Invested Capital

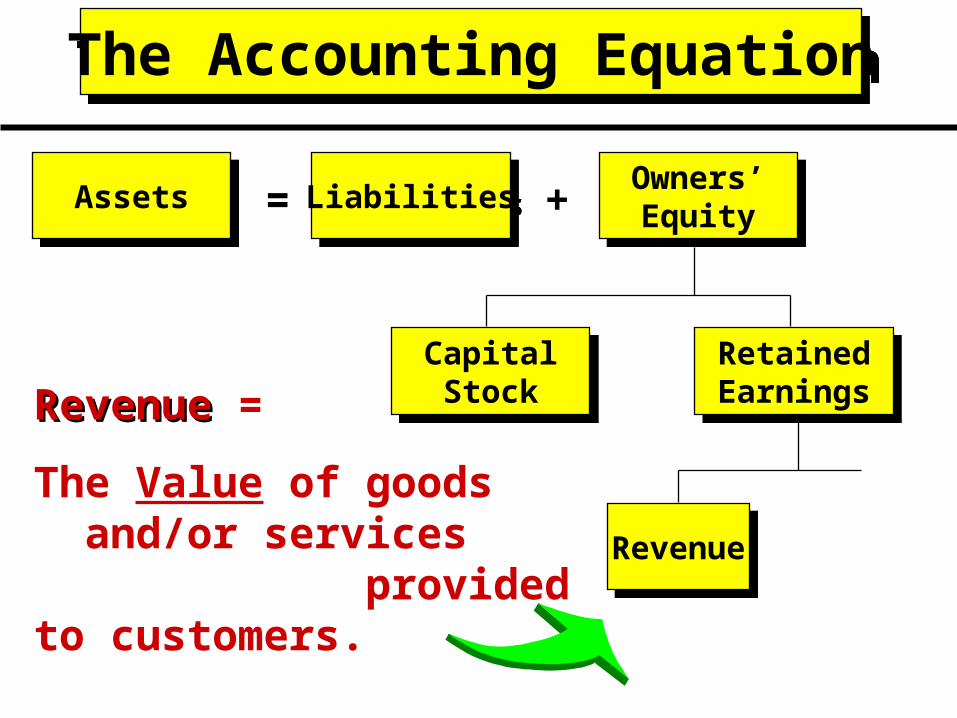

The Accounting EquationThe Accounting Equation

AssetsAssets LiabilitiesLiabilities Owners’Equity

Owners’Equity

CapitalStock

CapitalStock

RetainedEarnings

RetainedEarnings

RevenueRevenue

= +

RevenueRevenue =

The Value of goods and/or services provided to customers.

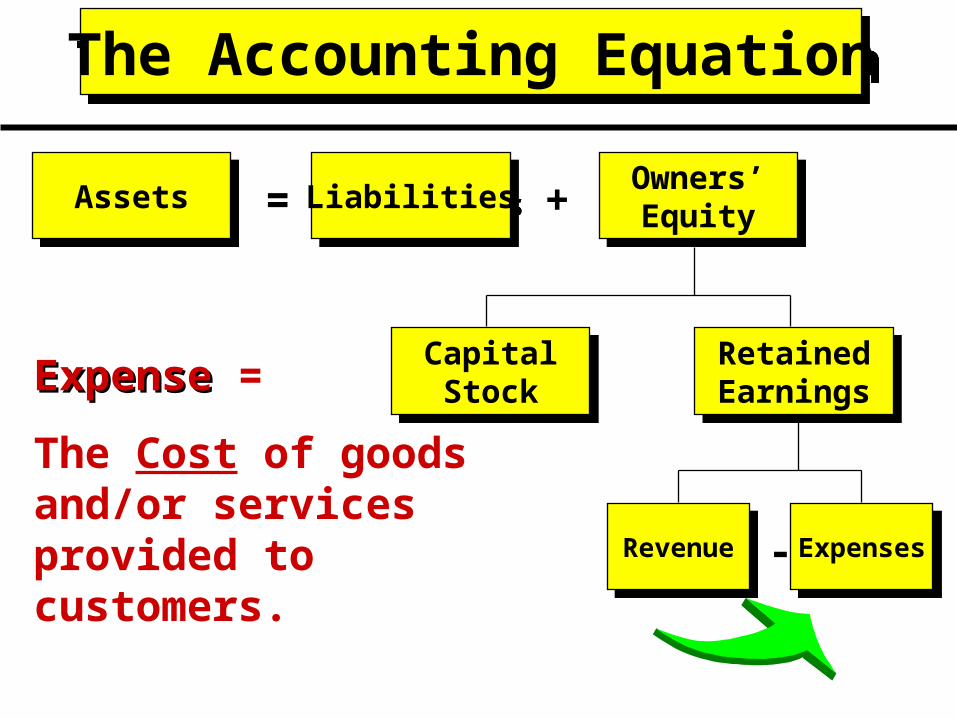

The Accounting EquationThe Accounting Equation

AssetsAssets LiabilitiesLiabilities Owners’Equity

Owners’Equity

CapitalStock

CapitalStock

RetainedEarningsRetainedEarnings

ExpensesExpensesRevenueRevenue

= +

-

ExpenseExpense =

The Cost of goods and/or services provided to customers.

The Accounting EquationThe Accounting Equation

AssetsAssets LiabilitiesLiabilities Owners’Equity

Owners’Equity

CapitalStock

CapitalStock

RetainedEarnings

RetainedEarnings

ExpensesExpensesRevenueRevenue

= +

NetIncome

NetIncome

-

=

Net IncomeNet Income =

Net Value added to the firm

The Financial Statements

Financial Statements

We will illustrate the “set” of financial statements by examining Sourdough Alaska, Inc. 2001 and 2002 financial statements.Sourdough Alaska is a fictitious company

but it will provide us with an opportunity to examine the individual statements.

The Balance Sheet

AKA: Statement of Financial Position . . .

The Balance Sheet . . .

A Balance sheet lists a firm’s

assets,

liabilities, and

owners’ equity

at a given point in time. That is, it is a snapshot of the financial position of a firm at a specific point in time.

2002 2001 AmountPercentIncrease/Decrease

$1,2007,0008,000

450$16,650

6,5006,0003,000

15,500$32,150

$2,600($1,400)(53.8%)4,0009,750

150$16,500

6,5006,0001,500

14,000$30,500

3,000($1,750)

300$150

000

1,5001,500

$1,650

75.0%(17.9%)200.0%

0.9%

0.0%0.0%

100.0%10.7%5.4%

Current Assets Cash Accounts Rec. Net Inventory Prepaid Expenses Total Current Assets

Property and Equipment Land Buildings, Net Equipment, Net Total Prop. & Equip.TOTAL ASSETS

ASSETS

Sourdough Alaska, Inc.Balance Sheet

Sourdough Alaska, Inc.Balance Sheet

1,000 600 400 66.7%

2002 2001 AmountPercentIncrease/Decrease

500$7,750

7,00014,750

1,8006,0003,100

10,9006,500

17,400$32,150

450 50 11.1%$6,050 $1,700 28.1%

8,00014,050

1,8006,0003,100

10,9005,550

16,450$30,500

(1,000)700

00

000

950950

$1,650

(12.5%)5.0%

0.0%0.0%0.0%0.0%

17.1%5.8%5.4%

Notes Payable Total Curr LiabilitiesLong Term Liabilities Bonds Payable, 6%TOTAL LIABILITIESSTKHOLDERS EQUITYPref. Stock, $100 Par, 6%Common Stock, $10 ParAdditional Paid in Cap. Total Paid In CapitalRetained EarningsTOTAL SETOTAL LIAB & EQUITY

$6,250 $5,000 $1,250 25.0% Accrued Payables Accounts Payable

LIABILITIESLIABILITIES

Current Liabilities

Current Assets . . .

Consist of cash and other assets the firm expects to convert into cash within one year or the operating cycle, whichever is longer.

A firm’s operating cycle is the average time from when materials are purchased to when sales of finished goods or services yield cash.

Current Assets . . .

Are listed in order of liquidity; that is, how easily they can be converted into cash.

A typical order would be:

Cash and cash equivalents

Marketable securities

Receivables

Inventory

2002 2001 AmountPercentIncrease/Decrease

$1,2007,0008,000

450$16,650

6,5006,0003,000

15,500$32,150

$2,600($1,400)(53.8%)4,0009,750

150$16,500

6,5006,0001,500

14,000$30,500

3,000($1,750)

300$150

000

1,5001,500

$1,650

75.0%(17.9%)200.0%

0.9%

0.0%0.0%

100.0%10.7%5.4%

Current Assets Cash Accounts Rec. Net Inventory Prepaid Expenses Total Current Assets

Property and Equipment Land Buildings, Net Equipment, Net Total Prop. & Equip.TOTAL ASSETS

ASSETS

Sourdough Alaska, Inc.Balance Sheet

Sourdough Alaska, Inc.Balance Sheet

Noncurrent Assets . . .

Consist of those assets that do not meet the definition of a current asset.

Noncurrent assets include . . .

Long-term receivables;

Investments;

Property, plant and equipment; and

Purchased intangible assets

2002 2001 AmountPercentIncrease/Decrease

$1,2007,0008,000

450$16,650

6,5006,0003,000

15,500$32,150

$2,600($1,400)(53.8%)4,0009,750

150$16,500

6,5006,0001,500

14,000$30,500

3,000($1,750)

300$150

000

1,5001,500

$1,650

75.0%(17.9%)200.0%

0.9%

0.0%0.0%

100.0%10.7%5.4%

Current Assets Cash Accounts Rec. Net Inventory Prepaid Expenses Total Current Assets

Property and Equipment Land Buildings, Net Equipment, Net Total Prop. & Equip.TOTAL ASSETS

ASSETS

Sourdough Alaska, Inc.Balance Sheet

Sourdough Alaska, Inc.Balance Sheet

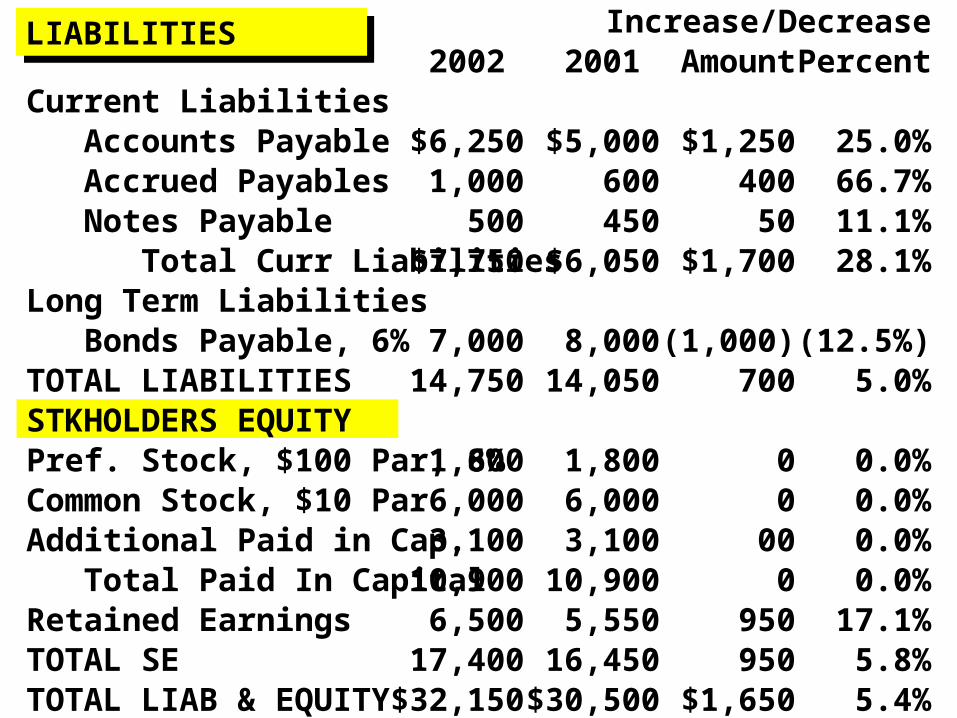

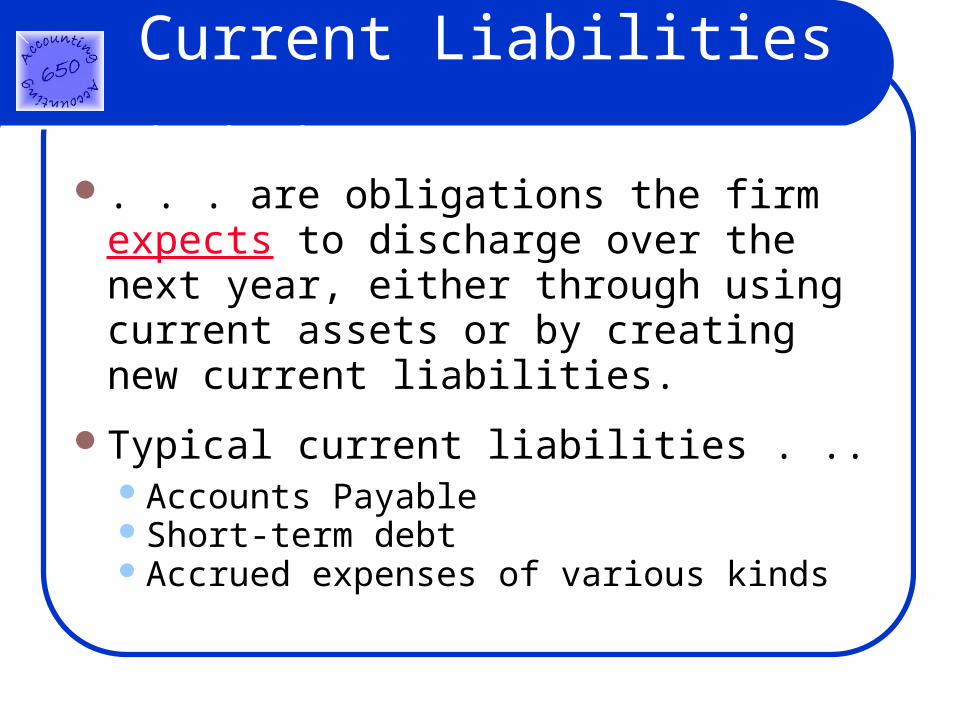

Current Liabilities . . .

. . . are obligations the firm expects to discharge over the next year, either through using current assets or by creating new current liabilities.

Typical current liabilities . ..Accounts PayableShort-term debtAccrued expenses of various kinds

1,000 600 400 66.7%

2002 2001 AmountPercentIncrease/Decrease

500$7,750

7,00014,750

1,8006,0003,100

10,9006,500

17,400$32,150

450 50 11.1%$6,050 $1,700 28.1%

8,00014,050

1,8006,0003,100

10,9005,550

16,450$30,500

(1,000)700

00

000

950950

$1,650

(12.5%)5.0%

0.0%0.0%0.0%0.0%

17.1%5.8%5.4%

Notes Payable Total Curr LiabilitiesLong Term Liabilities Bonds Payable, 6%TOTAL LIABILITIESSTKHOLDERS EQUITYPref. Stock, $100 Par, 6%Common Stock, $10 ParAdditional Paid in Cap. Total Paid In CapitalRetained EarningsTOTAL SETOTAL LIAB & EQUITY

$6,250 $5,000 $1,250 25.0% Accrued Payables Accounts Payable

LIABILITIES

Current Liabilities

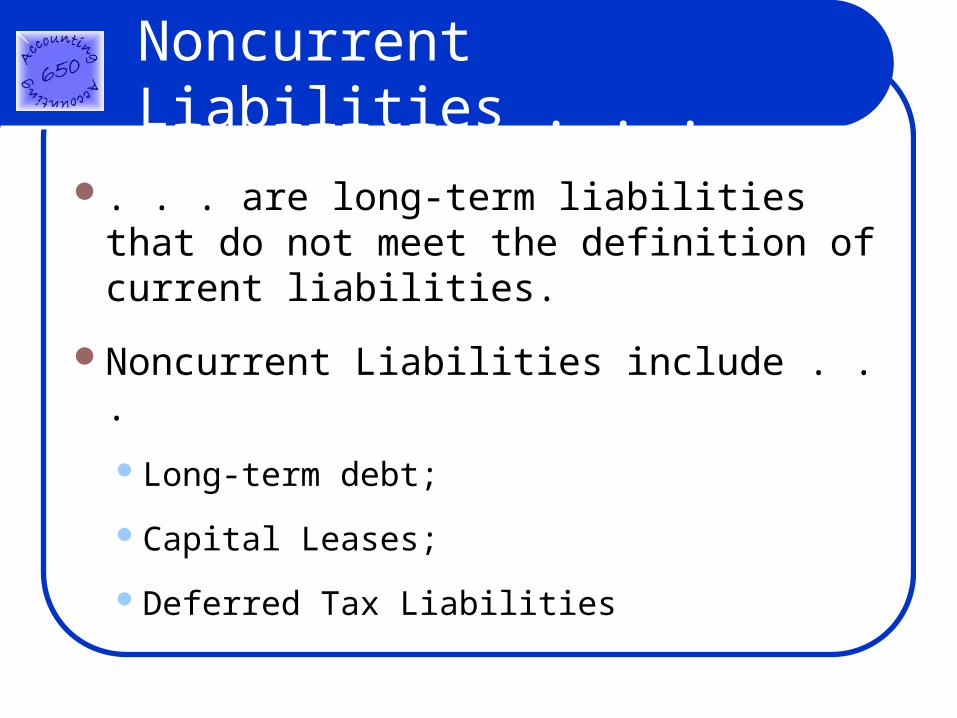

Noncurrent Liabilities . . .

. . . are long-term liabilities that do not meet the definition of current liabilities.

Noncurrent Liabilities include . . .

Long-term debt;

Capital Leases;

Deferred Tax Liabilities

1,000 600 400 66.7%

2002 2001 AmountPercentIncrease/Decrease

500$7,750

7,00014,750

1,8006,0003,100

10,9006,500

17,400$32,150

450 50 11.1%$6,050 $1,700 28.1%

8,00014,050

1,8006,0003,100

10,9005,550

16,450$30,500

(1,000)700

00

000

950950

$1,650

(12.5%)5.0%

0.0%0.0%0.0%0.0%

17.1%5.8%5.4%

Notes Payable Total Curr LiabilitiesLong Term Liabilities Bonds Payable, 6%TOTAL LIABILITIESSTKHOLDERS EQUITYPref. Stock, $100 Par, 6%Common Stock, $10 ParAdditional Paid in Cap. Total Paid In CapitalRetained EarningsTOTAL SETOTAL LIAB & EQUITY

$6,250 $5,000 $1,250 25.0% Accrued Payables Accounts Payable

LIABILITIES

Current Liabilities

Owners’ Equity . . .

Typically has three major components:

Contributed Capital

Common and preferred stock at par value

Additional paid-in capital

Retained Earnings

Treasury Common or Preferred Stock

1,000 600 400 66.7%

2002 2001 AmountPercentIncrease/Decrease

500$7,750

7,00014,750

1,8006,0003,100

10,9006,500

17,400$32,150

450 50 11.1%$6,050 $1,700 28.1%

8,00014,050

1,8006,0003,100

10,9005,550

16,450$30,500

(1,000)700

00

000

950950

$1,650

(12.5%)5.0%

0.0%0.0%0.0%0.0%

17.1%5.8%5.4%

Notes Payable Total Curr LiabilitiesLong Term Liabilities Bonds Payable, 6%TOTAL LIABILITIESSTKHOLDERS EQUITYPref. Stock, $100 Par, 6%Common Stock, $10 ParAdditional Paid in Cap. Total Paid In CapitalRetained EarningsTOTAL SETOTAL LIAB & EQUITY

$6,250 $5,000 $1,250 25.0% Accrued Payables Accounts Payable

LIABILITIES

Current Liabilities

The Income Statement

AKA: Statement of Operations . . .

Income Statement . . .

Summarizes the firm’s operating activities over a given period of time.

An income statement always begins by reporting revenue

Key expenses are then subtracted from revenues to yield operating income

$55,000$52,000 $3,000 5.8%38,000

$17,000

$7,5006,300

$13,800

$3,200436

$2,7641,106

$1,658

36,000$16,000

$7,0006,000

$13,000

$3,000435

$2,5651,026

$1,539

2,000$1,000

$500300

$800

$2001

$19980

$119

5.6%6.3%

7.1%5.0%6.2%

6.7%0.2%7.8%7.8%

7.8%

SalesCost of Goods SoldGross Margin

Operating Expenses: Selling Expenses Administrative Exp.Total Operating Expense

Net Operating IncomeInterest ExpenseNet Income Before Taxes Income Taxes

Net Income

2002 2001 AmountPercentIncrease/DecreaseSourdough Alaska, Inc.

Income StatementSourdough Alaska, Inc.

Income Statement

Income Statement . . .

Immediately following operating income:

Nonoperating income,

Income tax expense,

Effects of discontinued operations,

Extraordinary items,

Income Statement . . .

Immediately following operating income:

Cumulative effects of changes in accounting principles

Net Income

For Example

Let’s briefly examine the Bridgeport Let’s briefly examine the Bridgeport Corporation Income Statement for the Corporation Income Statement for the year ended December 31, 2002.year ended December 31, 2002.

Bridgeport CorporationIncome Statement

For the Year Ended December 31, 2002

Bridgeport CorporationIncome Statement

For the Year Ended December 31, 2002

Sales $2,000,000

Gross Profit $800,000

Income from operations $350,000

Operating Expenses

Selling

Administrative 450,000170,000

$280,000

Cost of Goods Sold 1,200,000

Bridgeport CorporationIncome Statement

For the Year Ended December 31, 2002

Bridgeport CorporationIncome Statement

For the Year Ended December 31, 2002

Income From Operations $350,000

Other Revenue (Expense)

Loss on sale of machinery (50,000)1

Inc. From Continuing Opns. BT

Income Tax on Continuing Operations

Income From Continuing Operations

$300,000

120,000

$180,000

2

Bridgeport CorporationIncome Statement

For the Year Ended December 31, 2002

Bridgeport CorporationIncome Statement

For the Year Ended December 31, 2002

Income From Continuing Operations $180,000

Earnings From Sunrise Division operations, less applicable taxes ($110,000 - $44,000)

Loss on disposal of Sunrise facilities, less tax savings ($250,000 - $100,000)

Income Before Extraordinary Item

66,000

(150,000)

$96,000

3

Bridgeport CorporationIncome Statement

For the Year Ended December 31, 2002

Bridgeport CorporationIncome Statement

For the Year Ended December 31, 2002

Income Before Extraordinary Item $96,000

Extraordinary Item Flood loss, less tax savings ($60,000 - $24,000) (36,000)

4

Cumulative effect on prior years of a change in accounting principle, less applicable taxes ($25,000 - $10,000)

Net Income

15,000

$75,000

5

The Statement of Cash Flows

Where the cash came from . . . and Where the cash went . . .

Statement of Cash Flows

A statement of cash flows subdivides the change in a firm’s cash balance over the period into three categories . . .

operating activities

investing activities, or

financing activities

Statement of Cash Flows

Is used extensively by creditors who are interested in . .

The extent to which the firm will be able to meet interest payments on its current and potential future debt; and

The firm’s liquidity, solvency, and financial flexibility.

Statement of Cash Flows

Is used extensively by investors, who are interested in . . .

The firm’s ability to pay future dividends from future operating cash flows; and

The firm’s liquidity, solvency, and financial flexibility.

W. T. Grant Co.W. T. Grant Co.“Retailing With A Difference”

A Classic Example . . .

The W. T. Grant Co.

The W. T. Grant Company was the nation’s largest retailer when it filed for protection under Chapter XI of the bankruptcy act on October 2, 1975.

Four months later the company was liquidated.

What Happened?

Chain of Events . . .

1906: First store opened

1928: Public stock offering

1950: Had 500 stores

1963: W. T. Grant retired

1969: Opened 410 new stores

1973: Stock sold at 20 times earnings

Chain of Events . . .

1974: Borrowed $600 million

1974: Stock price was at $2 from a high of $71

1974: Hired new president

1975: Opened 6 new stores

1975: Closed 107 stores and laid off 7,000 employees

Chain of Events . . .

Oct. 1975: Chairman, Senior VP and all outside directors resigned - FILED FOR CHPT 11 BANKRUPTCY.

Feb. 1976: Judge ordered liquidation in 60 days

Apr. 1976: Company adjudicated as a bankrupt.

40

20

-20

0

-40

-100

Millions of Dollars

19681966 1970 1972 1974

Net Income

Working Capital Provided By Operations

Cash Flow Provided by Operations

W. T. Grant CompanyW. T. Grant Company

The Statement of Cash Flows

Where Does It Fit In?

The Income Statement

Focuses on the results of operations and reveals a firm’s revenues and expenses for a given accounting period.

The Balance Sheet . . .

Discloses information on the economic resources, financial obligations, and stock-holders’ equity of a business enterprise at a specific point in time.

Inherent Limitations

Neither the Balance Sheet nor the Income Statement disclose specific events or transactions that occurred during the period.

What caused the change?

1. Purchase $25,000 of Equipment?

The Balance Sheet doesn’t say!

Examine Two Balance SheetsExamine Two Balance Sheets

Property Plantand Equipment

2001$50,000

Property Plantand Equipment

2001$50,000

Property Plantand Equipment

2002$75,000

Property Plantand Equipment

2002$75,000

Difference$25,000

Difference$25,000

2. Sell/Buy with net change of $25,000?

P.S.: The Income Statement doesn’t either!

The Statement of Shareholder’s Equity

Statement of Shareholders’ Equity

. . . details the changes in shareholders’ equity accounts from one period to the next.

Financial Statement Articulation

Or . . . How do the financial statements fit together?

Income Statement Notes

Statement of Cash

Flows

Balance Sheet

Statement of Owners

Equity

Financial Statement ArticulationFinancial Statement Articulation

Statement of Cash

Flows

Statement of Owners

Equity

Balance Sheet

Income Statement

Notes

Financial Statement ArticulationFinancial Statement Articulation

Financial Statement ArticulationOr, How the Financial Statements Fit Together

Financial Statement ArticulationOr, How the Financial Statements Fit Together

Balance Sheetas of

12/31/01

Balance Sheetas of

12/31/01

Income StatementFor Period Ending

12/31/02

Income StatementFor Period Ending

12/31/02

Balance Sheetas of

12/31/02

Balance Sheetas of

12/31/02

Statement of Cash FlowsFor Period Ending

12/31/02

Statement of Cash FlowsFor Period Ending

12/31/02

Notes to the Financial Statements

Or . . . Helping us to read between the lines . . .

Notes to the Financial Statements

Notes are valuable to many different user groups because of the wealth of information they provide about the firm’s:

Operating activities,

Investing activities, and

Financing activities

Notes to the Financial Statements

Some is information that is not formally recognized in the financial statements, but is either . . .

Mandated by the FASB to be disclosed in notes, or

Is voluntarily disclosed by the firm.

Notes to the Financial Statements

Note #1

It is crucial that the reader carefully scrutinize note 1 with a view to under-standing management’s objectives as revealed through its choices in accounting methods.

Management objectives may not always agree with investor objectives.

Notes to the Financial Statements

The sophisticated reader can use the notes to adjust the stated information in the firm’s financial statements . . .

to make adjustments based on his or her own analysis of such off-financial statement items.

![[2] Reports AntWhere AnyWay](https://img.dokumen.tips/doc/110x75/577dae321a28ab223f901ee6/2-reports-antwhere-anyway.jpg)