Embed Size (px)

Citation preview

October 28,2016 Missouri Department of Revenue

Presented by: Cindy Doss

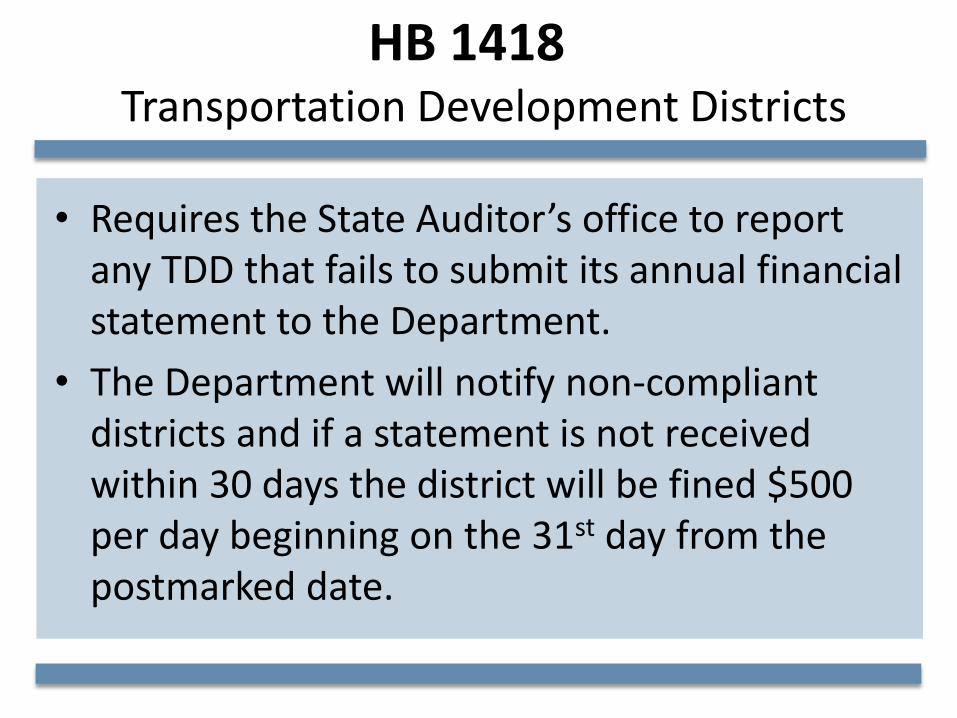

HB 1418

• Requires the State Auditor’s office to report any TDD that fails to submit its annual financial statement to the Department.

• The Department will notify non-compliant districts and if a statement is not received within 30 days the district will be fined $500 per day beginning on the 31st day from the postmarked date.

Transportation Development Districts

HB 1434 Tax Increment Financing Commission

• Specifies that a recommendation by a TIF commission in select counties must be approved by a majority of commissioners, not a tie vote.

• Limits authority of any municipality in select counties to include actions which the economic activity taxes generated to not exceed costs association with demolition and clearing and grading of land.

• Adds transparency language for TIF commissions.

HB 1434 Tax Increment Financing Commission

• Prohibits the adoption of any tax increment financing from superseding, altering, or reducing the sheltered workshop levy.

• Requires the governing body of a municipality to submit a report of each plan and project in existence on December 31 to the Department by November 15 each year. Any municipality that does not comply within 60 days after notification from the Department will be prohibited from adopting any new TIF plan for five years.

Continued

HB 1435 Sales Tax Refund Claims

Clarifies that the limitations on sales tax refund claims will not apply for a refund claim filed by a purchaser that originally paid the tax to a vendor or seller, the claim is for use tax remitted by the purchaser, or an additional refund claim is filed by a person legally obligated to remit the tax because of certain changes in information.

HB 1561 Local Sales Tax

• Changes the distribution formula beginning January 1, 2017, so that municipalities in Group B must receive at least 50 percent of the amount of taxes generated within the municipalities based on the location where the sales were deemed consummated.

• In no event will the city or county receive less than the amount they received in 2014.

• Authorizes Cedar County to impose a local sales tax for the purpose of funding public libraries.

HB 1582 - Withholding Tax Returns

• Changes the amount of withholding required to file an annual withholding tax return to less than $100 in each of the four preceding quarters if the employer is not otherwise required to file a withholding return on a quarterly or monthly basis.

• Beginning January 1, 2018, employers with 250 or more employees must file their Form W-2s electronically to the state unless a waiver is granted for the federal requirement by the IRS.

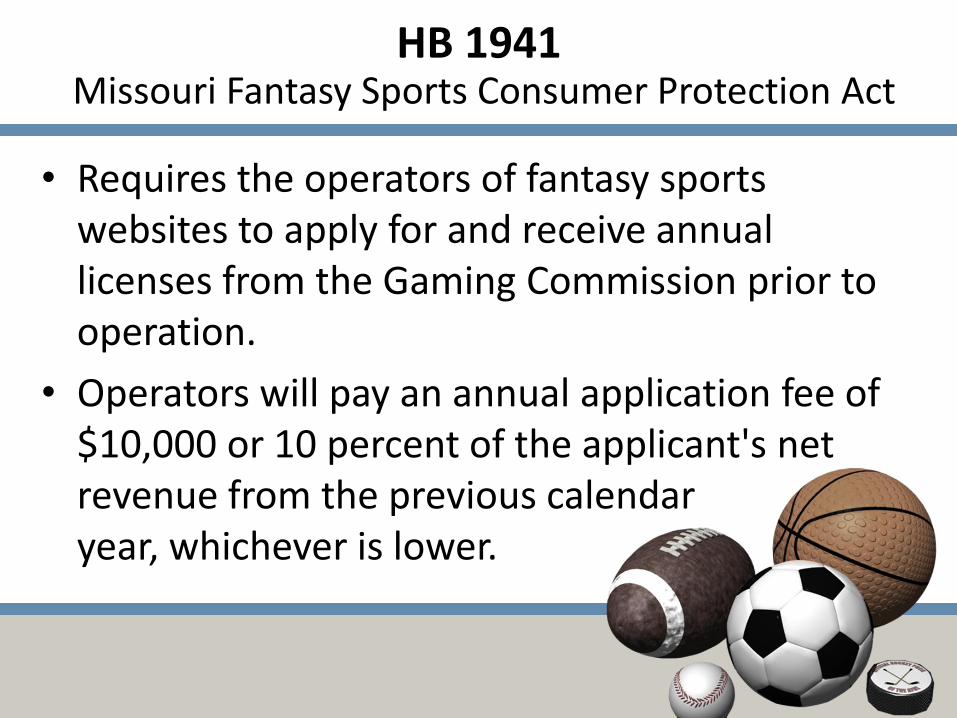

• Requires the operators of fantasy sports websites to apply for and receive annual licenses from the Gaming Commission prior to operation.

• Operators will pay an annual application fee of $10,000 or 10 percent of the applicant's net revenue from the previous calendar year, whichever is lower.

HB 1941 Missouri Fantasy Sports Consumer Protection Act

• Operators will be required to remit an annual operation fee of eleven and one-half (11.5) percent of the operator’s net revenues from the previous calendar year to be placed in the Gaming Proceeds for Education Fund created in Section 313.822.

• Licensed operators must verify certain required information and conduct and pay for an annual independent audit to ensure compliance with this bill.

• The Commission oversees all licensed operators and has certain investigatory, licensing, and rule-making powers under these provisions.

HB 1941 Missouri Fantasy Sports Consumer Protection Act

Continued

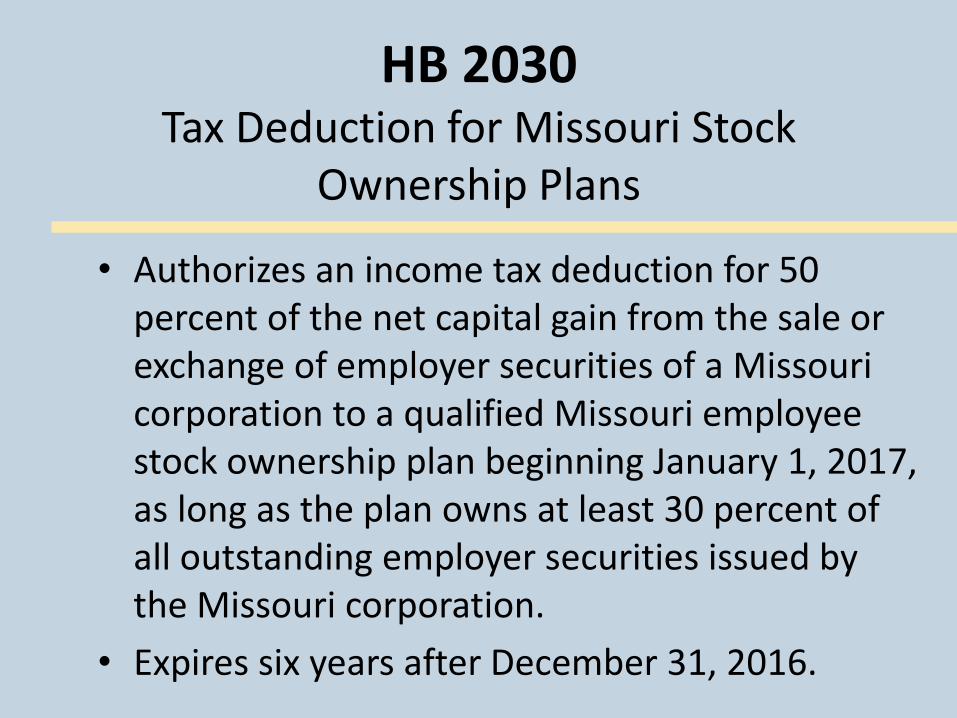

HB 2030 Tax Deduction for Missouri Stock

Ownership Plans

• Authorizes an income tax deduction for 50 percent of the net capital gain from the sale or exchange of employer securities of a Missouri corporation to a qualified Missouri employee stock ownership plan beginning January 1, 2017, as long as the plan owns at least 30 percent of all outstanding employer securities issued by the Missouri corporation.

• Expires six years after December 31, 2016.

HB 2140 Task Force of Fair, Local Taxation

• Authorizes a taxing jurisdiction to hold a vote, no later than November 2018, on whether to impose a local sales tax on vehicle titling on purchases from a source other than a licensed Missouri dealer after such tax was repealed.

• Creates the Missouri Task Force on Fair, Nondiscriminatory Local Taxation to review the disparity in taxation that resulted from several issues. The task force must submit a report of its findings to the Governor and General Assembly by December 31, 2017.

SB 572 Municipalities

4

• Changes minimum standards for municipalities in St. Louis County, nuisance abatement ordinance regulation changes.

• Specifies that the state is not liable for the debts of a municipality that is financially insolvent.

• Establishes disincorporation procedures for third class cities, charter cities, and home rule cities. Decreased the number of signatures required on a petition to disincorporate a fourth class city, town, or village.

• Prohibits a municipal judge from serving on more than five municipal courts.

• Changes the definition of court costs, reduces the maximum allowable fine for minor traffic violations to $250.

• Adds municipal ordinance violations and amended charges to the calculation limiting the percentage of annual general operating revenue that can come from fines and court costs for minor violations and to provisions in municipal court cases.

Continued

SB 572 Municipalities

SB 641 Deduction for Agricultural Disaster

• Creates an income tax deduction for payments received as part of a program that compensates agricultural producers who have suffered a loss due to disaster or emergency.

• Authorizes the deduction for tax years on or after 2014.

SB 665 Modifies Provisions Relating to Agriculture

4

• Re-authorizes the existing Qualified Beef Tax Credit until 2021 and limits credits up to $15,000 per year per taxpayer for no more than three years. Limits the amount of tax credits issued under this credit and the Meat Processing Facility Investment Tax Credit to $2 million per calendar year.

• Creates the Meat Processing Facility Investment Tax Credit between the years of 2017 and 2021.

• Modifies the Agricultural Product Utilization Contributor Tax Credit and New Generation Cooperative Incentive Tax Credit to only allow the credits to be carried forward up to four years, removes the carry back provision, and extends the expiration date to December 31, 2021.

• Modifies the Motor Fuel per barrel inspection fee to not exceed four cents per barrel from 2017 to 2021 and shall not exceed five cents per barrel from 2022 and thereafter.

SB 732 Modifies Provisions Relating to Public Safety

Authorizes Liberty and North Kansas City to impose a sales tax of up to 0.5 percent for the purpose of improving public safety of the city subject to voter approval.

SB 765 Modifies Provisions Relating to Political Subdivisions

Extends the authority of regional jail districts to collect a sales tax of up to 0.5 percent until September 30, 2028, and allows the Department to make refunds.

SB 794 Tax Exemption for Medical Equipment

Creates a sales tax exemption for all sales, rentals, parts, and repairs of durable medical equipment as well as for parts for certain types of health care- related equipment.

SB 814 Military Income Tax Deduction

After January 1, 2016, any income earned as compensation for being active duty of the armed forces may be deducted from the person’s Missouri adjusted gross income regardless of a where the service member is stationed.

SB 823 Modifies Provisions Relating to Sales Tax

• Creates a State and Local sales tax exemption for internet use or access.

• Provides that a property operated as a bed and breakfast with six or fewer rooms is classified as residential property for tax purposes as long as the owner resides there.

• Provides that the Department shall not notify taxpayers before August 28, 2017, regarding the ruling on IBM Corporation v. Director of Revenue holding that tax exemptions for production/manufacturing do not apply to production of intangible products like computer data.

• Lowers the cap to two times the average monthly tax liability for bonding requirements for sales licenses and releases taxpayers after one year of satisfactory tax compliance.

SB 861 Modifies Provisions Relating to Transportation Facilities

• Creates the Advanced Industrial Manufacturing Zones Act to authorize port authorities located in Missouri to establish these zones. Creates the Port Authority AIM Zone Fund to approve any projects, disperse money in the fund, and submit an annual budget for the collected funds to Department of Economic Development.

• Authorizes an income tax deduction equal to 50 percent of the expenses associated with eliminating a business unit located outside Missouri and reestablishing that unit within the state. Tax deductions under this section are capped at $5 million on a first come, first served basis.

• Creates three types of income tax deductions for entities transporting cargo through water port facilities and airports in Missouri administered by Department of Economic Development.

• Provides that all demolition costs in St. Louis County associated with a former automobile manufacturing plant are an allowable cost for tax credits so long as the redevelopment will create at least 250 new jobs or retain at least 300 jobs.

Continued

SB 861 Modifies Provisions Relating to Transportation Facilities

4

SB 919 Modifies Provisions Relating to Liquor • Allows a brewer to lease portable

refrigeration unites to retail licensees at a value equal to the cost of the unit to the brewer beginning January 1, 2017.

• Changes the requirements for applicants seeking to renew a liquor license to provide the statement of no tax due. Requires a licensee to file the statement within 20 days of issuance from the Department.

Exempts Instructional Classes from Sales Tax

• Provides that the definition of “sale at retail” does not include amounts paid for instructional classes in places of recreation.

• Imposes a four percent tax on the amounts paid to or in places of recreation, excluding amounts paid for instructional classes.

SB 1025

Tax Forms and Changes

• Due date for 2016 Individual Income Tax and Property Tax Credit returns is April 18, 2017.

Tax Forms and Changes

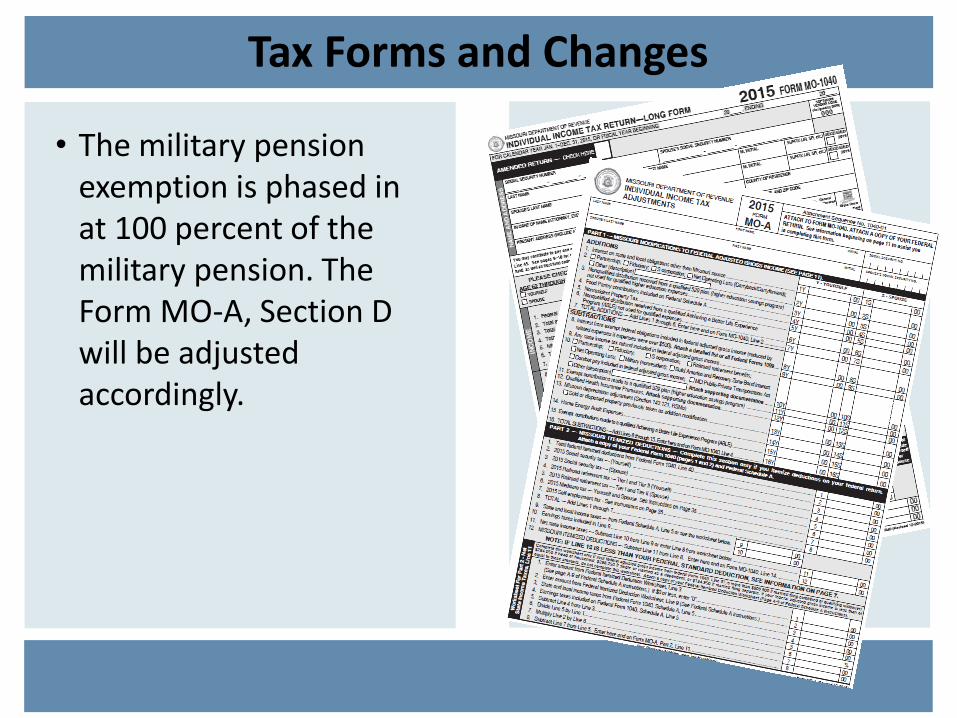

• The military pension exemption is phased in at 100 percent of the military pension. The Form MO-A, Section D will be adjusted accordingly.

Tax Forms and Changes

• Added a new line 18 to the MO-104O for the Military Income Deduction.

• Added new line 19 on the MO-1040 for the Bring Jobs Home Deduction.

Tax Forms and Changes

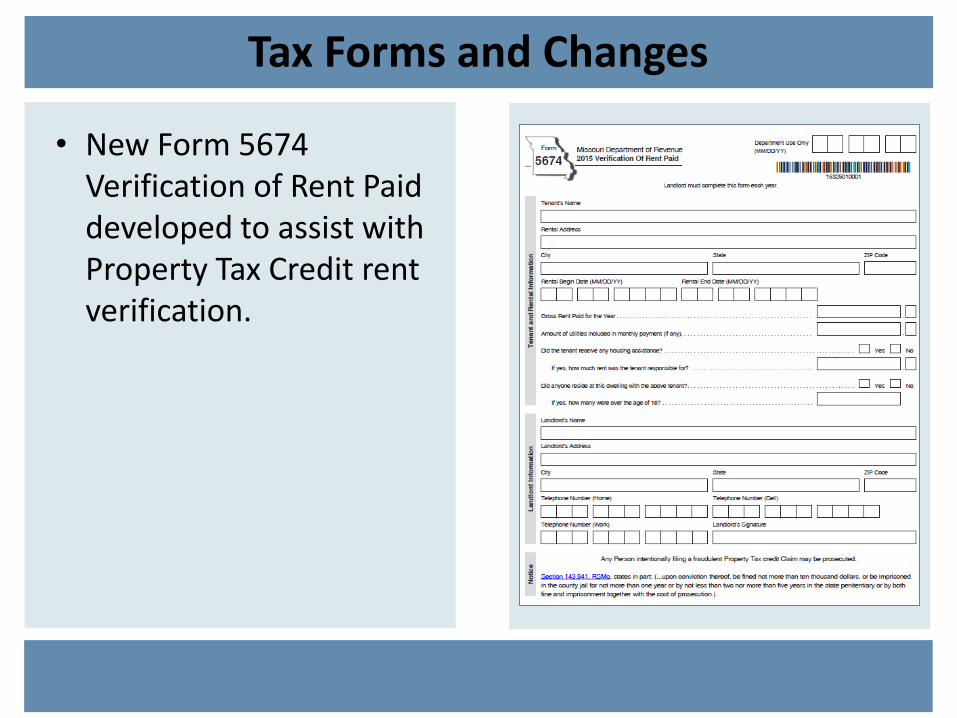

• New Form 5674 Verification of Rent Paid developed to assist with Property Tax Credit rent verification.

Tax Forms and Changes

For 2014 and 2015 the Department will need: •Amended Form 1040 • Form MO-AGDR • Form 1099 (that

indicates your agriculture payment)

• Federal Schedule F • Federal Schedule K-1 (if

applicable) • Write “AG DISASTER” at

the top of the Form MO-1040

• Form MO-AGDR Agriculture Disaster Relief will be available soon on the Department website for taxpayers who received agriculture payments as a result of a disaster or emergency included in Federal Income.

Tax Forms and Changes

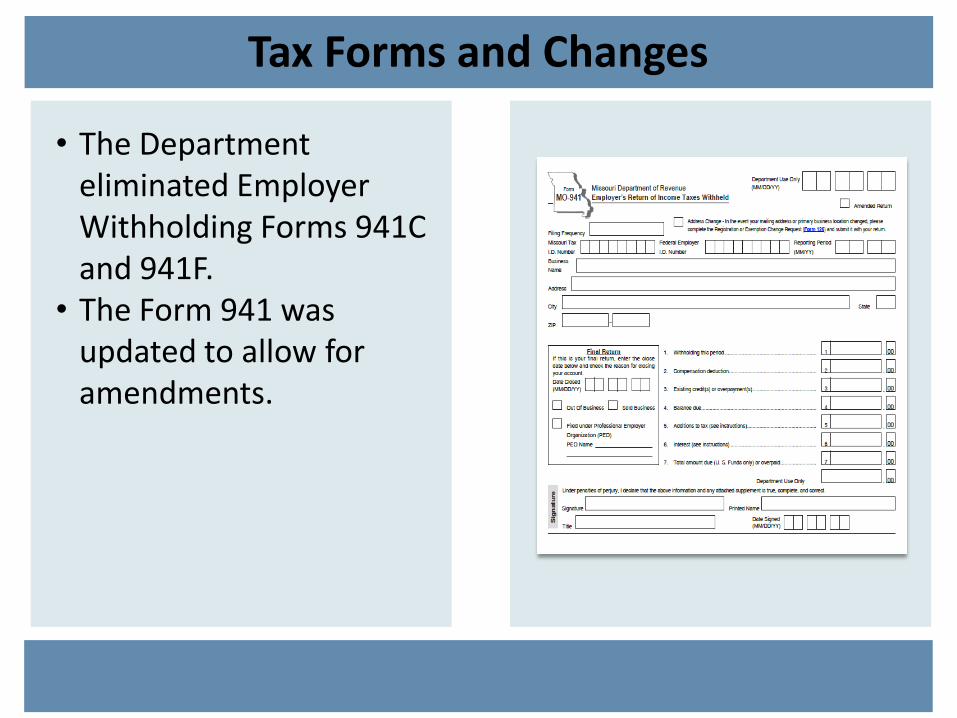

• The Department eliminated Employer Withholding Forms 941C and 941F.

• The Form 941 was updated to allow for amendments.

Tax Forms and Changes

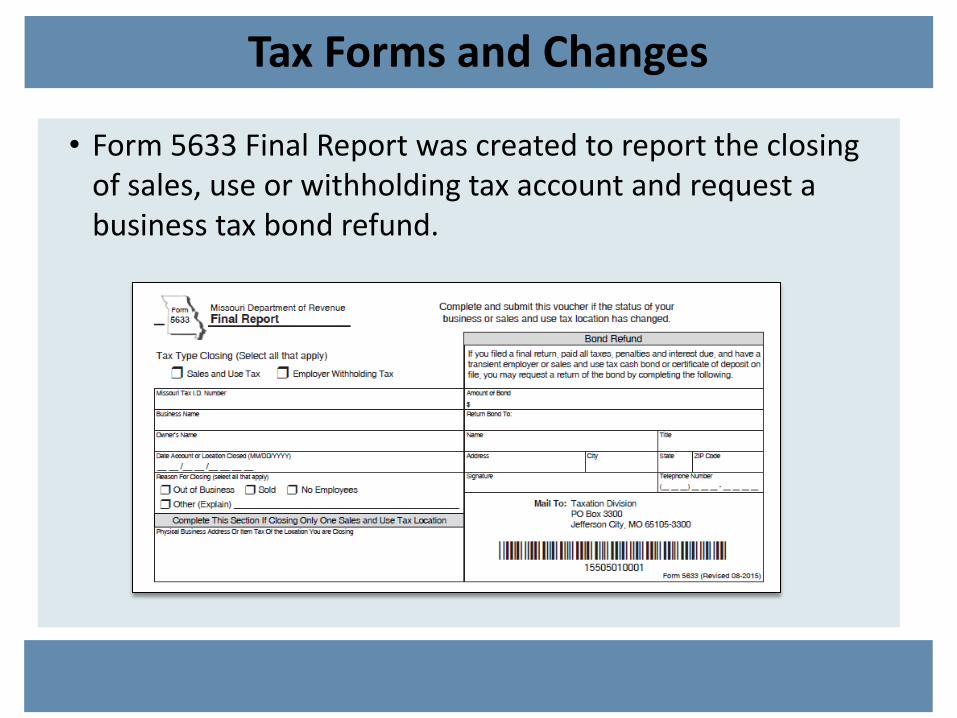

• Form 5633 Final Report was created to report the closing of sales, use or withholding tax account and request a business tax bond refund.

Identity Theft Victim Reporting

Report the incident by completing Form 5593:

• Send scanned copy/documentation to [email protected] or

• Mail to: Missouri Department of Revenue Attn: Identity Theft PO Box 3366 Jefferson City, Missouri 65105-3366 Telephone: 573-751-3505 Fax: 573-522-4848 Email: [email protected]

http://dor.mo.gov/personal/individual/identity_theft.php

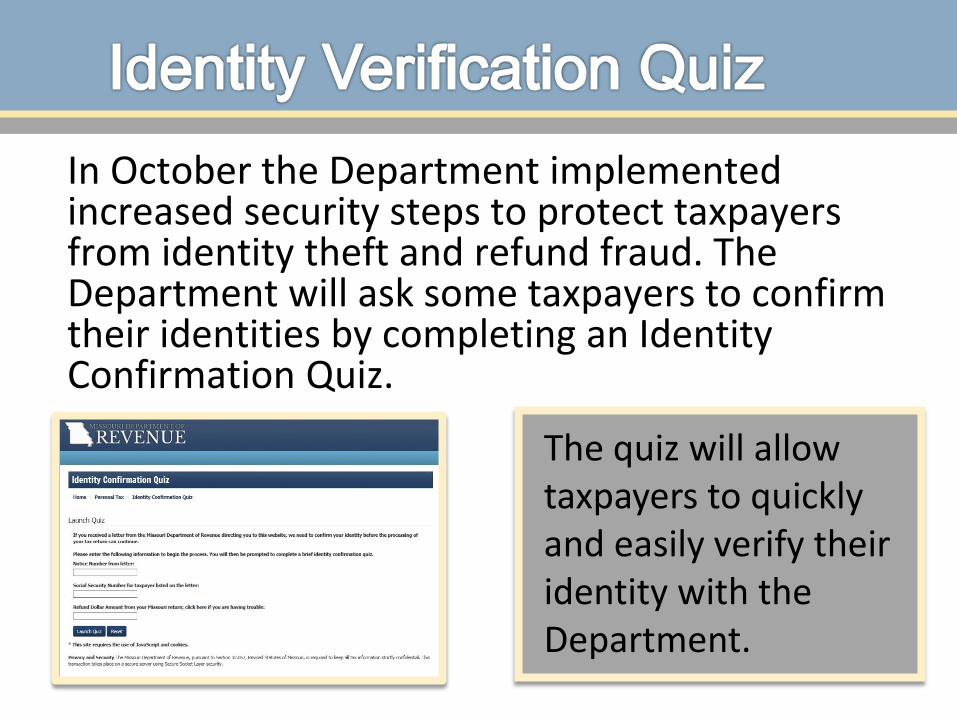

In October the Department implemented increased security steps to protect taxpayers from identity theft and refund fraud. The Department will ask some taxpayers to confirm their identities by completing an Identity Confirmation Quiz.

The quiz will allow taxpayers to quickly and easily verify their identity with the Department.

Taxpayers selected to take the quiz will receive a letter from the Department of Revenue following the submission of their tax return. The quiz is taken on a secure website and should only take a few minutes to complete.

If a taxpayer receives an identity confirmation letter and they did not file an income tax return with Missouri, they should contact the Department at [email protected]

The Department has updated our website with information on the new Identity Confirmation Quiz, created a short video and FAQ’s to assist individuals through the new process.

http://dor.mo.gov/personal/individual/identity_theft.php

Identity Verification Quiz

To login and complete the Identity Confirmation Quiz, taxpayers will need the following information: • Notice Number from the

Quiz letter. • Social Security Number of

the person on the quiz letter.

• Requested refund amount from the Missouri tax return.

What happens after the taxpayer successfully logs in to start the quiz?

• Answer a short four question quiz.

• Taxpayers have five minutes to take the quiz.

• Quiz questions are based on information associated with taxpayer on quiz letter.

At end of quiz, taxpayer will see confirmation of pass or fail of the quiz.

• Taxpayers who fail the quiz the first time can take the quiz a second time with different questions.

• If the taxpayer fails the second attempt they will be directed to mail documentation to the Department confirming their identity.

What if the taxpayer fails the quiz?

Processing of the tax return will not resume until a quiz is passed or

requested documentation is processed.

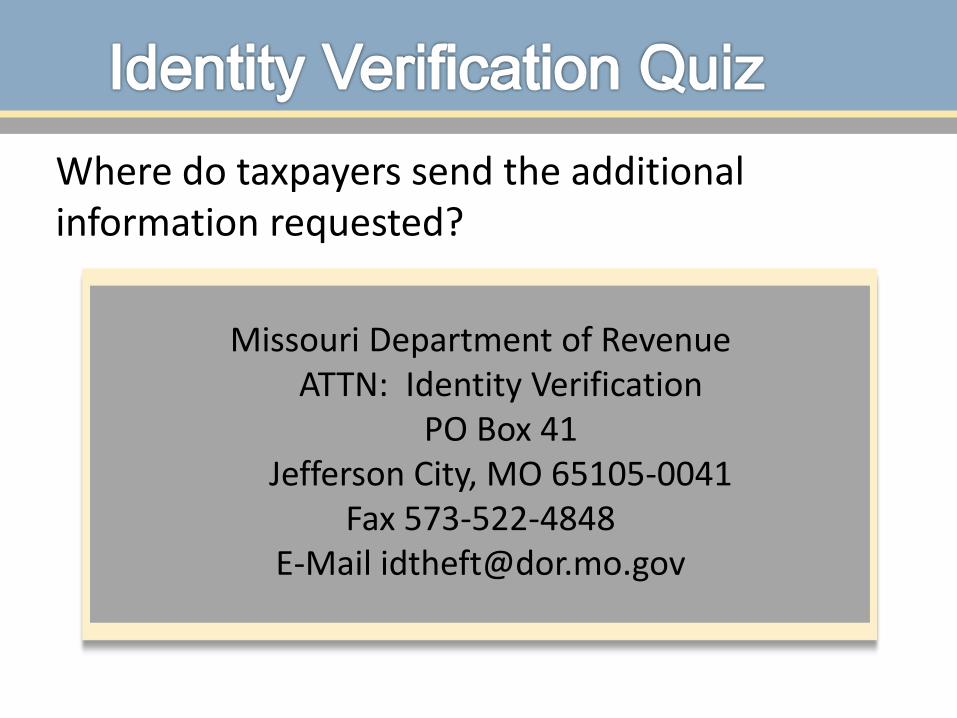

Missouri Department of Revenue ATTN: Identity Verification

PO Box 41 Jefferson City, MO 65105-0041

Fax 573-522-4848 E-Mail [email protected]

Where do taxpayers send the additional information requested?

Department Website: http://dor.mo.gov

Resolve Delinquent Accounts: (573) 751-7200

General Income Tax Questions/Refunds: (573)751-3505

Listing of all Mailing Addresses and Phone Numbers

http://dor.mo.gov/contact.htm

Electronic Filing: (573) 751-8150 [email protected]

Cindy Doss, Manager, Collections and Tax Assistance 301 West High Street Jefferson City, Missouri 65105 Telephone 573-751-3958 Fax 573-522-3218

![Printed at Chennai Micro Print Pvt Ltd....AKHIL AWASTHI [w.e.f. January 28,2016] S. RADHAKRISHNAN EVA MARIA ROSA SCHORK [w.e.f January 28,2016] AMIT DIXIT [Until July 29,2015] MANAGING](https://img.dokumen.tips/doc/110x75/5f2e25027503dd5861527d30/printed-at-chennai-micro-print-pvt-ltd-akhil-awasthi-wef-january-282016.jpg)

![Ecologie territoriale et indicateurs pour un développement ......Audrain, Cordier et al. — Indicateurs pour un Développement Durable de la Métropole Parisienne — Page [3] FONDaTERRA](https://img.dokumen.tips/doc/110x75/60212f941e2c012ef614648e/ecologie-territoriale-et-indicateurs-pour-un-dveloppement-audrain-cordier.jpg)