Embed Size (px)

Citation preview

Applying IFRS

New Venezuelan currency regime - same accounting and reporting considerations

June 2015

1 June 2015 New Venezuelan currency regime – same accounting and reporting considerations

Contents

Overview .................................................................................... 21. Background .......................................................................... 2 1.1 Looking back at 2014 ....................................................... 32. Recent developments and outlook for 2015 ............................. 4 2.1 Cap on profits earned in Venezuela .................................... 63. Foreign currency accounting considerations ............................. 6 3.1 Functional currency ......................................................... 6 3.2 Foreign currency transactions ........................................... 7 3.3 Translation of a foreign operation ...................................... 74. Other accounting and financial reporting considerations ............ 85. Disclosures ........................................................................... 9

�What you need to know• The new currency exchange system requires companies with operations in

Venezuela to reconsider again the exchange rate(s) they use to translateVenezuelan foreign operations and to translate their Venezuelanbolivar-denominated monetary assets and liabilities and related revenuesand expenses.

• Entities will need to consider their specific transactions and their ability totransact through the various exchange mechanisms to determine whichexchange rate(s) to use.

• Economic conditions in Venezuela and changes in the currency exchangemechanisms also raise a number of other financial reporting issues.

• Entities with significant operations in Venezuela should consider providingadditional disclosure about their exposure to Venezuela, including howthey are affected by recent developments.

June 2015 New Venezuelan currency regime – same accounting and reporting considerations 2

OverviewNow that Venezuela has revamped its foreign currency exchange system,companies with operations in Venezuela should reconsider the exchange rate(s)they use to translate their bolivar-denominated monetary assets and liabilitiesand related revenues and expenses. Entities should also consider supplementingtheir disclosures to reflect their consideration of recent events.

In February 2015, the Venezuelan Government (the Government) announcedthat it merged its two supplementary foreign currency exchange systems(i.e., Sistema Complementario de Administración de Divisas, or SICAD 1, andSistema Cambiario Alternativo de Divisas, or SICAD 2) into a single mechanismcalled SICAD. The Government also introduced the Sistema Marginal de Divisas(Marginal Currency System, or SIMADI) to compete with the unofficial parallelcurrency exchange market (the black market). As a result, companies will needto consider whether to use the new SIMADI rate of approximately 198 bolivars(Bs) per US dollar (USD) as of 4 June 2015, the new SICAD rate of Bs12 per USdollar or the official rate of Bs6.3 per US dollar.

To determine which rate(s) to use to translate Venezuelan foreign operationsand to translate specific bolivar-denominated monetary assets and liabilities,a company should consider: (1) its legal ability to convert currency or to settletransactions using a specific rate and (2) its intent to use a particularmechanism, including whether the rate available through that mechanism ispublished or readily determinable. The second criterion is important becauseentities can use different exchange mechanisms with different rates for manytransactions.

Determining the appropriate exchange rate(s) for financial reporting purposeswill depend on a company’s individual facts and circumstances. Complicatingthis determination is the increasing lack of exchangeability across all exchangemechanisms. Many questions remain about whether Venezuela’s supply ofUS dollars will be sufficient to meet demand and how exchanges will be handledunder the new currency exchange system.

This publication addresses the IFRS requirements for translating foreigncurrency transactions and translation of foreign operations- and some of thefactors companies need to consider when determining the appropriateexchange rate or rates to use. Other accounting and disclosure considerationsare also discussed.

1. BackgroundThe Government has maintained currency controls and a fixed officialexchange rate since February 2003. Since 2010, the Venezuelan economyhas been considered highly inflationary under IAS 29 Financial Reportingin Hyperinflationary Economies. For years, the Government has limited acompany’s ability to repatriate profits (i.e., pay dividends) and obtainUS dollars to pay for imported goods and services.

Determining theappropriate exchangerate(s) for financialreporting purposes willdepend on an entity’sindividual facts andcircumstances.

3 June 2015 New Venezuelan currency regime – same accounting and reporting considerations

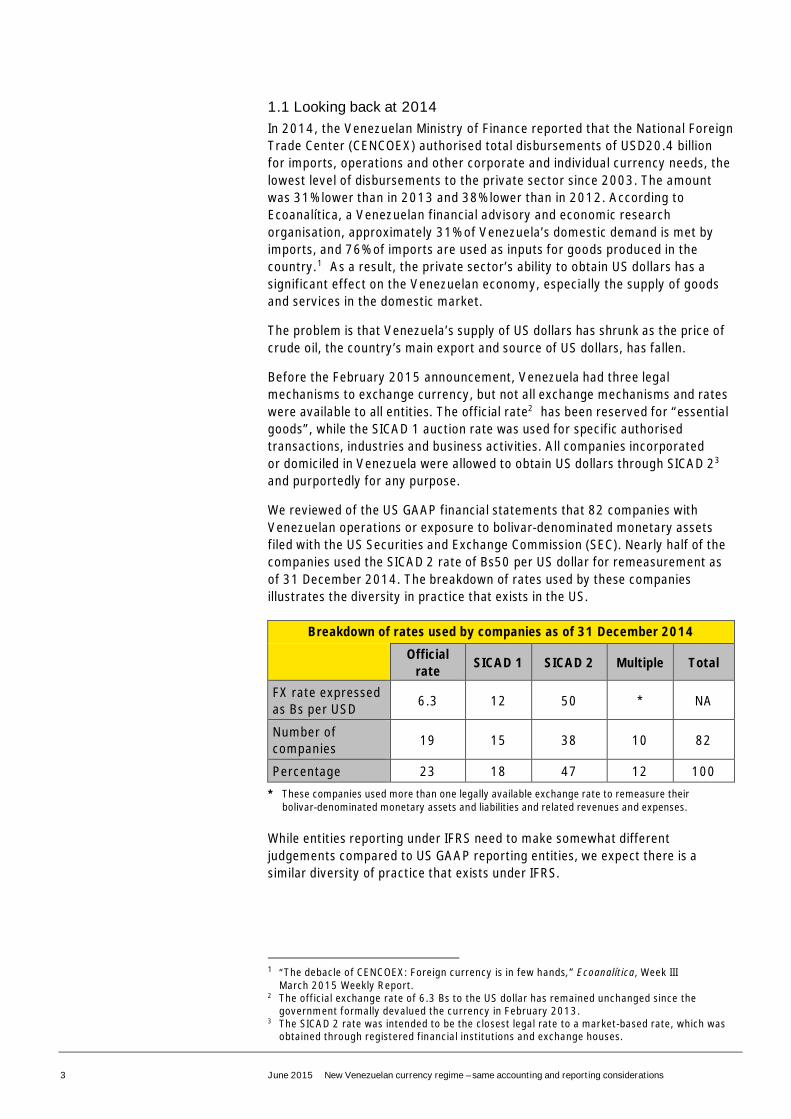

1.1 Looking back at 2014In 2014, the Venezuelan Ministry of Finance reported that the National ForeignTrade Center (CENCOEX) authorised total disbursements of USD20.4 billionfor imports, operations and other corporate and individual currency needs, thelowest level of disbursements to the private sector since 2003. The amountwas 31% lower than in 2013 and 38% lower than in 2012. According toEcoanalítica, a Venezuelan financial advisory and economic researchorganisation, approximately 31% of Venezuela’s domestic demand is met byimports, and 76% of imports are used as inputs for goods produced in thecountry.1 As a result, the private sector’s ability to obtain US dollars has asignificant effect on the Venezuelan economy, especially the supply of goodsand services in the domestic market.

The problem is that Venezuela’s supply of US dollars has shrunk as the price ofcrude oil, the country’s main export and source of US dollars, has fallen.

Before the February 2015 announcement, Venezuela had three legalmechanisms to exchange currency, but not all exchange mechanisms and rateswere available to all entities. The official rate2 has been reserved for “essentialgoods”, while the SICAD 1 auction rate was used for specific authorisedtransactions, industries and business activities. All companies incorporatedor domiciled in Venezuela were allowed to obtain US dollars through SICAD 23

and purportedly for any purpose.

We reviewed of the US GAAP financial statements that 82 companies withVenezuelan operations or exposure to bolivar-denominated monetary assetsfiled with the US Securities and Exchange Commission (SEC). Nearly half of thecompanies used the SICAD 2 rate of Bs50 per US dollar for remeasurement asof 31 December 2014. The breakdown of rates used by these companiesillustrates the diversity in practice that exists in the US.

Breakdown of rates used by companies as of 31 December 2014

Officialrate SICAD 1 SICAD 2 Multiple Total

FX rate expressedas Bs per USD 6.3 12 50 * NA

Number ofcompanies 19 15 38 10 82

Percentage 23 18 47 12 100* These companies used more than one legally available exchange rate to remeasure their

bolivar-denominated monetary assets and liabilities and related revenues and expenses.

While entities reporting under IFRS need to make somewhat differentjudgements compared to US GAAP reporting entities, we expect there is asimilar diversity of practice that exists under IFRS.

1 “The debacle of CENCOEX: Foreign currency is in few hands,” Ecoanalítica, Week IIIMarch 2015 Weekly Report.

2 The official exchange rate of 6.3 Bs to the US dollar has remained unchanged since thegovernment formally devalued the currency in February 2013.

3 The SICAD 2 rate was intended to be the closest legal rate to a market-based rate, which wasobtained through registered financial institutions and exchange houses.

June 2015 New Venezuelan currency regime – same accounting and reporting considerations 4

2. Recent developments and outlook for 2015In February 2015, the Venezuelan Government said it merged its SICAD 1 andSICAD 2 foreign currency exchange systems and issued Exchange AgreementNo. 33 establishing regulations for foreign exchange transactions conductedthrough the new SIMADI system.

How we see itAn entity’s decision to use a particular exchange rate or rates should bebased on careful consideration of the various exchange mechanisms andentity-specific facts and circumstances. Absent a change in facts andcircumstances, a company that previously concluded that it was not eligibleto transact at either the official rate or the SICAD 1 rate would generally beexpected to use the SIMADI rate, now that the SICAD 2 system no longerexists.

SIMADI is intended to compete with the black market by establishing a legaltrading system based on supply and demand. It’s available to individuals andboth public and private companies, except for banks and other financialinstitutions that are authorised to facilitate exchanges through SIMADI.These financial institutions are prohibited from accessing SIMADI for theirown accounts.

The Government has said that both the official rate and the new SICAD ratewould be available to entities importing essential goods (e.g., certain food,medicine, raw materials), with the majority of such imports being settled at themost favourable rate of Bs6.3 per US dollar. However, the Government has notpublished any new rules or regulations that clarify exactly which activities,industries or transactions will be eligible to transact at these rates. Allowingcertain entities to transact at the two most favourable exchange rates, subjectto the country’s profit cap laws, is intended to make many necessities affordablefor Venezuelan citizens.

Since its inception, the SIMADI system reportedly has not been able to meet thedemand from the private sector due to a lack of supply of US dollars andcomplex rules, among other reasons. As a result, the bolivar continues to bedevalued. For example, on the first day of operation, the SIMADI exchange ratewas approximately Bs172 per US dollar, compared with approximately Bs177per US dollar on the black market. As of the date of this publication, the SIMADIrate was approximately Bs198 per US dollar, compared with approximatelyBs4284 per USD on the black market.

The following exchange mechanisms and rates were legally available, dependingon facts and circumstances, as of 31 March 2015:

• Through CENCOEX at the official rate of 6.3

• Through CENCOEX at the new SICAD rate of 12

• Through the SIMADI system at the negotiated rate of approximately 193

4 Dolartoday.com.

5 June 2015 New Venezuelan currency regime – same accounting and reporting considerations

We understand that the new SICAD rate will be established through periodicauctions regulated by the Government in a process similar to the one theGovernment previously used to set the SICAD 1 rate. However, there havebeen no public auctions since October 2014, which is why the SICAD rate hasremained unchanged at Bs12 per USD. Until auctions resume, any currencyexchanged at the SICAD rate will be through CENCOEX.

In January 2014, when use of the SICAD 1 exchange rate was significantlyexpanded through Exchange Agreement No. 25, the Venezuelan governmentannounced that the published exchange rate resulting from the latest SICADauction would be used for the following transactions and activities:

• Foreign investments and payments of royalties; use and exploitation ofpatents, trademarks, licences and franchises; as well as contracts fortechnology import and technical assistance

• International public air transportation service for passengers, cargo andmail duly authorised by the Government

• Operations inherent in insurance activity

• Contracts for leasing and services; use and exploitation of patents,trademarks, licences and franchises, as well as import of intangiblegoods; payment of network rental agreements and installation; repair andmaintenance of imported machinery, equipment or software of thetelecommunications sector

• Cash for travelling abroad, including payment of purchases with creditcards while travelling abroad and of electronic commerce transactionswith suppliers abroad

• Remittances to relatives living abroad

• Payments for operations inherent in national civil aviation

It is unclear whether the new SICAD rate will apply to these types oftransactions and activities. It is also unclear whether companies that interpretedthe term “foreign investments” in Exchange Agreement No. 25 to meanthat future dividend remittances would be transacted at the exchange rateestablished through the SICAD auction process will be able to continue to makethat assertion. Entities may need to change the rate they use to translate theirnet monetary assets, depending on what the Government says about how thenew SICAD rate can be used.

It is unclear which typesof transactions andactivities will be subjectto the new SICAD rate.

June 2015 New Venezuelan currency regime – same accounting and reporting considerations 6

How we see itWith slumping crude oil prices and significant debt payments coming duelater this year, the Government has fewer US dollar reserves available tomeet the private sector’s demands this year. As a result, entities may have aharder time obtaining US dollars this year than at any time since currencycontrols were first implemented.

In its Week III March 2015 Weekly Report, Ecoanalítica said, “the drop in oilprices implies a drop of 48.0% in the country’s foreign currency revenuesand a deficit of US$25.58 billion, which, given the lack of financing options,will have to be offset by an adjustment in demand and, as always, privatesector imports are the first on the list when it comes to implementing cuts.”

If Ecoanalítica and other analysts are correct, entities doing business inVenezuela may experience less exchangeability in 2015 unless oil pricesrecover significantly and Venezuela changes its monetary policy. Currencyexchanges at either the official or SICAD rate to pay dividends remainunlikely for the foreseeable future. Such capital outflows likely will occur onlythrough the new SIMADI system, assuming liquidity in that market improvesand other operational challenges are addressed. According to theVenezuelan Central Bank, during the first six weeks of the new system’soperation, only 1.4% of all authorised foreign exchange transactionsoccurred through SIMADI compared with initial estimates of 5% to 7%.

2.1 Cap on profits earned in VenezuelaIt is our understanding that an entity’s compliance with Venezuela’s profit caplaw,5 which was enacted in January 2014, will continue to be a prerequisite toobtain US dollars through any of the exchange mechanisms controlled by theGovernment.

The law limits profit margins by product and service and sets a cap of 30%above the cost structure (as defined) of the good or service. The NationalSuperintendence for Defense of Socioeconomic Rights is in charge of itsenforcement and monitors compliance by importers, producers, suppliers andretailers. Some entities have been required to demonstrate their compliancewith this law by furnishing performance certificates, which are subject togovernment audit.

3. Foreign currency accounting considerations3.1 Functional currencyIAS 21 The Effects of Changes in Foreign Exchange Rates defines the functionalcurrency of an entity as the currency of the primary economic environment inwhich the entity operates. Whilst judgement may sometimes be required todetermine the functional currency, it is a matter of fact, not an accountingpolicy choice.

5 Decree No. 600 with Rank, Value and Force of Master Law of Fair Prices in Official GazetteNo. 40,340.

7 June 2015 New Venezuelan currency regime – same accounting and reporting considerations

As the Venezuelan economy is hyperinflationary, IAS 29 must first be applied.IAS 29 requires a restatement approach, whereby financial informationrecorded in the hyperinflationary currency is adjusted by applying a generalprice index and expressed in the measuring unit (the hyperinflationary currency)current at the end of the reporting period. The alternative approach whereby anentity selects a stable currency as its unit of accounting is prohibited under IFRSif that currency is not the entity's functional currency as defined under IAS 21.

3.2 Foreign currency transactionsIAS 21 requires each foreign currency transaction to be recorded in thefunctional currency of the reporting entity at the date it is recognised, usingthe spot exchange rate in effect at that date.

Under IAS 21, when several exchange rates are available, the rate used is thatat which the future cash flows represented by the transaction or balance couldhave been settled, if those cash flows had occurred at the measurement date.If more than one exchange mechanism is legally available, an entity shouldgenerally base its decision on its intention to use a particular mechanism tosettle the specified transaction and whether the rate available through thatmechanism is published or readily determinable at the reporting date. Theprobability of transacting through a particular mechanism should also beconsidered (i.e., whether the volume and frequency of exchange activitythrough a particular mechanism will support the entity’s currency needs). Ifexchangeability is lacking across all exchange mechanisms, an entity shoulduse the published rate for the legally available exchange mechanism that mostfaithfully reflects the economics of the company’s business activity. Theexchange rate an entity uses for translation may vary by transaction type,based on the entity’s legal ability to convert currency or to settle transactionsusing the specified rate. Determining which currency exchange mechanisms andrates are legally available to a reporting entity in Venezuela requires carefulconsideration of Exchange Agreements used. The assistance of legal counselor Venezuelan regulatory authorities (such as CENCOEX) may be required.

3.3 Translation of a foreign operationWhere the results and financial position of a foreign operation are translatedinto the presentation currency of the reporting entity, IAS 21 requires thatthe financial statements are first restated in accordance with IAS 29 forhyperinflationary economies. Once restated, IAS 21 requires all current periodamounts to be translated at the closing rate at the reporting date.

When the presentation currency of the reporting entity is not USD, the entitymay also need to determine the USD to presentation currency exchange rate totranslate the financial statements of its Venezuelan operations. This is becauseall three of the exchange rates legally available in Venezuela are based solely onthe Bolivar to US dollar conversion.

June 2015 New Venezuelan currency regime – same accounting and reporting considerations 8

4. Other accounting and financial reportingconsiderations

The Government reported a contraction in gross domestic product (GDP) in2014 and an inflation rate of 68.5%. Some analysts are projecting a furthercontraction in GDP this year and an inflation rate of more than double the2014 rate. Venezuela’s deteriorating economy and its currency exchangecontrols and profit cap law raise a number of financial reporting issuesbeyond the foreign currency matters discussed above. These accountingand financial reporting considerations include:

• Consolidation: IFRS 10 Consolidated Financial Statements requires aninvestor to consolidate an investee that it controls. In determining whetherit has control, an entity considers (among other factors) whether it haspower over an investee, being existing rights that give it the current abilityto direct the relevant activities. In assessing its rights, the investorconsiders whether those rights are substantive, including whether thereare regulatory or legal requirements that prevent the holder from exercisingits rights6 (e.g., where a foreign investor is prohibited from exercisingits rights). While entities should consider their individual facts andcircumstances in determining whether to deconsolidate a foreign entity,generally, we do not believe that a lack of exchangeability in itself wouldresult in the deconsolidation of a Venezuelan subsidiary.

IFRS 12 Disclosure of Interests in Other Entities requires a company todisclose significant restrictions on its ability to access or use the assets andsettle the liabilities of the group (e.g., those that restrict the ability of aparent or its subsidiaries to transfer cash or other assets to (or from)other entities within the group7).

• Cash: IAS 7 Statement of Cash Flows requires an entity to disclose, togetherwith a management commentary, the amount of significant cash and cashequivalent balances held that are not available for use by the group. IAS 7states that examples include cash and cash equivalent balances held by asubsidiary that operates in a country where exchange controls or other legalrestrictions apply when the balances are not available for general use by theparent or other subsidiaries.8

How we see itThe nature of the restriction on the use of cash and cash equivalents mustalso be assessed to determine if the balance is ineligible for inclusion in cashequivalents because the restriction results in the investment ceasing to behighly liquid or readily convertible.

• Revenue: Pursuant to IAS 18 Revenue, revenue should be recognisedonly when it is probable that the economic benefits associated with thetransaction will flow to the entity. Lack of exchangeability, devaluation ofthe bolivar and deteriorating economic conditions in Venezuela all raisequestions about the collectability of an entity’s receivables from customerslocated in Venezuela. Revenue should only be recognised once theuncertainty about the collectability of the consideration is removed.

6 IFRS 10.B23(a)(vii)7 IFRS 12.13(a)(i)8 IAS 7.49

We do not believe that alack of exchangeabilityin itself would result inthe deconsolidation of aVenezuelan subsidiary.

9 June 2015 New Venezuelan currency regime – same accounting and reporting considerations

• Financial assets measured at amortised cost: Paragraph 58 of IAS 39Financial Instruments: Recognition and Measurement, requires an entity toassess, at each reporting period, whether there is any objective evidenceof impairment. Entities with amounts due (e.g., loans, trade receivables)from customers in Venezuela (including the Government) should considerwhether there is evidence of impairment and, if so, determine theimpairment loss.

• Investments in equity instruments: Paragraph 61 of IAS 39 explains that, inthe following circumstances, there is objective evidence of impairment of anequity investment:

• Information about significant changes with an adverse effect that havetaken place in the technological, market, economic or legal environmentin which the entity operates, and indicates that the cost of investmentmay not be recovered; or

• A significant or prolonged decline in the fair value of an investment insuch an instrument below its cost.

Equity investments in Venezuelan entities are likely to be at high risk ofimpairment due to the economic conditions. Therefore, entities will needto assess whether there is objective evidence of impairment.

• Impairment of assets: IAS 36 prescribes the procedures that an entityapplies to ensure that its assets are carried at no more than theirrecoverable amount. An asset is carried at more than its recoverable amountif its carrying amount exceeds the amount to be recovered through use orsale of the asset. Entities should consider how recent economic and politicaldevelopments in Venezuela may affect their capital and operating strategiesand whether changes to those strategies will affect the recoverability of theirassets. Indefinite-lived intangible assets and goodwill are subject to annualimpairment tests as well as interim impairment tests if impairment indicatorsare present.

5. DisclosuresEntities with exposure to Venezuela should challenge the disclosures in theirfinancial statements. Where material, disclosures that entities should considerinclude:

• A discussion of an entity’s operations in Venezuela, including the nature andextent of business activities in that country

• A discussion that IAS 29 has been applied and the financial statements andthe corresponding figures for previous periods that have been restated forchanges in the general purchasing power of the functional currency

• IAS 29 also requires disclosure of whether the financial statements arebased on a historical or current cost approach and the identity and level ofthe price index at the end of the reporting period with disclosure of themovement in the index during the current and previous reporting periods

June 2015 New Venezuelan currency regime – same accounting and reporting considerations 10

• A discussion of exchange rates used to translate bolivar-denominatedforeign currency transactions and translation of foreign operations,including a discussion of the entity’s ability to actually transact at such rates:

• Whether items were translated at a different rate than in the previousperiod (e.g., items translated at the SIMADI rate in the current periodthat were translated at the SICAD 2 rate in the previous period)

• Whether multiple exchange rates are used and, if so: (1) the basis forapplying different rates; and (2) the limitations and uncertainties of eachselected rate (e.g., the amount of currency available at such rates, theentitiy’s ability to transact through specified exchange mechanisms andto realise the rates established through those mechanisms (bothhistorically and projected))

• The amount of bolivars pending Government approval for settlement ateach rate and the length of time pending

• The effect of exchange restrictions on the company’s cash flows availableto meet capital and short-term funding requirements, including: possiblechanges in profitability that may result from any additional expectedcurrency devaluation; change in exchange rates to be used for translationpurposes; or the existing law capping profits thatcan be earned in Venezuela

• Recognised impairments and debt covenant violations attributed to changesin exchange rates or other factors attributed to the entity’s operations inVenezuela

In July 2014, the IFRS Interpretations Committee considered a request forguidance on the translation and consolidation of the results and financialposition of foreign operations in Venezuela and the question which rateshould be used if there was a longer-term lack of exchangeability. The IFRSInterpretations Committee published it’s agenda decision on the application ofIAS 21 to foreign operations in Venezuela in November 2014, noting thatseveral exisiting disclosure requirements in IFRS would apply when the impactof foreign exchange controls is material:

• Disclosure of significant accounting policies and significant judgements inapplying those policies (paragraphs 117–124 of IAS 1)

• Disclosure of sources of estimation uncertainty that have a significant riskof resulting in a material adjustment to the carrying amounts of assets andliabilities within the next financial year, which may include a sensitivityanalysis (paragraphs 125–133 of IAS 1)

• Disclosure about the nature and extent of significant restrictions on anentity’s ability to access or use assets and to settle the liabilities of the group,or its joint ventures or associates (paragraphs 10, 13, 20 and 22 of IFRS 12)

Next stepsThe Venezuelan Government may issue more regulations or take other stepsthat may affect an entity’s decision on which exchange rate(s) to use forfinancial reporting purposes. Entities should continue to closely monitordevelopments in this area.

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s International Financial Reporting Standards GroupA global set of accounting standards provides the global economy with one measure to assess and compare the performance of companies. For companies applying or transitioning to International Financial Reporting Standards (IFRS), authoritative and timely guidance is essential as the standards continue to change. The impact stretches beyond accounting and reporting, to key business decisions you make. We have developed extensive global resources — people and knowledge — to support our clients applying IFRS and to help our client teams. Because we understand that you need a tailored service as much as consistent methodologies, we work to give you the benefit of our deep subject matter knowledge, our broad sector experience and the latest insights from our work worldwide.

© 2015 EYGM Limited. All Rights Reserved.

EYG No. AU3117ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com

EY | Assurance | Tax | Transactions | Advisory