Embed Size (px)

Citation preview

Moody’s Analytics WebinarThe Value of Granular Risk Rating Models for CECL

November 15, 2016

2The Value of Granular Risk Rating Models for CECL

2

Independent provider of credit rating opinions

and related information for over 100 years

Models, data, software and research for

financial risk analysis and related

professional services

A unit of Moody’s Corporation, Moody’s Analytics provides risk solutions and thought leadership to the financial services industry

Leading global provider of credit rating opinions, insight and

tools for credit risk measurement and management

3The Value of Granular Risk Rating Models for CECL

Today’s Speakers

Senior Director | Enterprise Risk Solutions

Chris Henkel leads the risk measurement advisory team throughout the Americas and is an experienced credit practitioner.

Having spent most of his career in commercial banking, Chris has a unique blend of business and academic experience

across the financial services industry - including expertise in commercial credit and financial analysis, portfolio management,

asset quality, loan loss reserve methodologies, stress testing, credit administration, process redesign, safety & soundness

examinations, and credit risk modeling.

He received his master’s and undergraduate degree from the University of Texas and graduated Valedictorian from the

Southwestern Graduate School of Banking at Southern Methodist University.

Team Lead | Impairment, Capital Planning, and Stress Testing

Anna Krayn is a Senior Director and Team Lead, responsible for solution structuring across Moody’s Analytics products and

services focusing on impairment, stress testing and capital planning solutions. Her clients include a variety of financial

services institutions, including those in the banking and insurance sectors across Americas. Prior to her current role, she was

with Enterprise Risk Solutions as engagement manager leading projects with financial institutions across Americas in loss

estimation, enhancements in internal risk rating capabilities and counterparty credit risk management.

Anna holds a B.S. and MBA from Stern School of Business at New York University.

Presenters

Chris Henkel

Moderator

Anna Krayn

Managing Director | Economic Research

Tony Hughes oversees the company's credit analysis consulting projects for global lending institutions. An expert applied

econometrician, Dr. Hughes manages the Moody’s CreditCycle and CreditForecast.com products. He has helped develop

approaches to stress testing and loss forecasting in retail, C&I, and commercial real estate portfolios. Lately he has introduced

a methodology for stress-testing a bank’s deposit book. Currently he is developing ways to streamline the economic scenario

building process and exploring ways to simulate economic paths more effectively.

A native Australian, Dr. Hughes was formerly the lead Asia-Pacific economist for Moody’s Analytics, before which he held

academic positions at the University of Adelaide, the University of New South Wales, and Vanderbilt University. He has been

published in leading statistics and economics journals as well as several major industry publications. He received his PhD in

econometrics from Monash University in Melbourne, Australia.Tony Hughes

4The Value of Granular Risk Rating Models for CECL

In June 2016, the FASB issued an Accounting Standards Update (ASU), commonly known as “CECL”

Who does it apply to?

» The new accounting standard applies to all banks, savings associations, credit unions, and financial institution holding

companies, regardless of asset size

» Entities holding financial assets and net investment in leases that are not accounted for at fair value through net income

» Includes: Loans, debt securities, trade receivables, net investments in leases, off-balance-sheet credit exposures,

reinsurance receivables, etc.

» The standard requires organizations to immediately record the full amount of credit losses that are expected in their financial

assets held at amortized cost

Topic 326: Financial Instruments – Credit Losses:

Measurement of Credit Losses on Financial Instruments

When does it go into effect?

» FY 2019 (after 12/15/19) for public business entities that are SEC filers, including interim periods within those fiscal years

» FY 2020 (after 12/15/20) for all other public business entities, including interim periods within those fiscal years

» FY 2021 (after 12/15/21) for all other entities, and interim periods within fiscal years beginning after December 15, 2021

» All entities may early adopt beginning after December 15, 2018, including interim periods within those fiscal years

5The Value of Granular Risk Rating Models for CECL

Bank loans are among the largest asset class to be affected by the new accounting standard update

C&I21%

CRE22%

SFR21%Credit Card

8%

Auto5%

Consumer -Other

8% Other15%

Loan Portfolio Composition including all

FDIC Insured institutions (total ~$9 trillion)

Source: FDIC:

6The Value of Granular Risk Rating Models for CECL

Collective (“Pool”) Evaluation

» Required for financial assets when similar

risk characteristic(s) exists

Individual Evaluation

» Required when a financial asset does not

share risk characteristics with its other

financial assets

The ASU requires entities to apply one of two approaches to evaluate expected credit losses

» Internal or external credit score

» Risk ratings or classification

» Financial asset type

» Collateral type

» Size

Examples of Shared Risk Characteristics

» Effective interest rate

» Term

» Geographical location

» Industry of the borrower

» Vintage

7The Value of Granular Risk Rating Models for CECL

The concept is really quite simple

Example of a CRE Portfolio

Historical Loss Rate 2.00%

Impact of Decline in RE Values 0.50%

Impact of Increase in Unemployment Rate 0.25%

Expected Loss Rate 2.75%

Portfolio Value (Amortized Cost Basis) $10,000,000

Allowance for Expected Credit Losses $275,000

8The Value of Granular Risk Rating Models for CECL

In the context of credit risk modeling, collective evaluation could be at varying levels of granularity

C&I Loan Portfolio

Region (Geography)

Sector

Size (Total Assets)

Credit Risk Models / Scorecards

Should we segment here?

…perhaps here?

…or here?

9The Value of Granular Risk Rating Models for CECL

The right answer…?

Is our primary objective accuracy in the ECL estimate?

…It depends

If a less granular model is more accurate, how can we use it for

portfolio management decisions?

Do we have the required data to run a more granular model?

How homogenous is the portfolio?

10The Value of Granular Risk Rating Models for CECL

Treating all C&I loans the same, for example, would ignore obvious differences in the level of risk across sectors

Percentage of loans with bank-assigned adverse regulatory ratings, by industry

Source: Moody’s Analytics

11The Value of Granular Risk Rating Models for CECL

Model Coefficients

(Sensitivity to

Macroeconomic Variables)

Credit Risk (e.g., PD)

Sector

Within C&I loan portfolios, Sector and Credit Risk are two factors with different sensitivities to economic variables

0.25% (Loan 1)

1.00% (Loan 2)

2.00% (Loan 3)

5.00% (Loan 4)

10.00% (Loan 5)

Sector: Trade (All Loans)

C&I Loan Example

Macroeconomic Variables:» Unemployment

» Equity Prices

» Interest Rates

» Credit Spreads

» …

12The Value of Granular Risk Rating Models for CECL

Granular models also allow you to capture the different sensitivities to current conditions and forecasts

0.05% 0.08% 0.10%0.20% 0.25% 0.26%0.40% 0.44% 0.40%

1.00%0.93%

0.76%

2.00%

1.64%

1.20%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

Q0 Q1 Q2 Q3 Q4 Q5 Q6 Q7 Q8

ECL Forecast (S0: Baseline Scenario)

Loan 1 Loan 2 Loan 3 Loan 4 Loan 5

Sept. ‘16

Exp

ecte

d C

red

it L

oss (

PD

x L

GD

) Sept. ‘17 Sept. ‘18Loan Q4/Q1 Q8/Q1

Loan 1 1.54 2.06

Loan 2 1.27 1.32

Loan 3 1.09 1.01

Loan 4 0.93 0.76

Loan 5 0.82 0.60

Change In ECL

Case Study Assumptions: » C&I loan portfolio (five loan sample)

» Moody’s Analytics Baseline Scenario (S0)

» PD/LGD approach; LGD constant at 20%

» 1 year remaining to maturity

(10% x 20%)

13The Value of Granular Risk Rating Models for CECL

Case Study: Auto Loans

Source: Lexus.com

14The Value of Granular Risk Rating Models for CECL

Forecasting Used Car Prices

» Applications for loans (LGD) and leases (residual risk).

» Potential applications to CECL and loss provisioning.

» Portfolios are often heterogenous – Camrys, Hummers and Bugatis – so

granular forecasts are desired.

» Forecasts have other uses, for which granularity is also a desired

attribute.

15The Value of Granular Risk Rating Models for CECL

Form of the (Assumed) Champion Model

The model is actually made up of several sub-components, each of which

serves a different key function.

Model layers are all developed at the Make, Model, Year, Trim level or

below:

» A VIN level model captures relativity between different vehicles under

different underlying economic conditions.

– This model rank orders the cars. Tells us which car will be worth more (given

economic conditions) in relative terms

– Cars can “leap-frog” over other cars under different economic scenarios.

– For example, under baseline a 2009 BMW 328 with 78k miles may be worth

slightly more than a 2011 Kia Rio with 16k on the clock.

– These vehicles may then “flip” positions in a recession!

16The Value of Granular Risk Rating Models for CECL

Form of the Model (Cont.)

» A quantile model shows and allows us to project how the distribution of

vehicles changes over time.

– This model allows us to map individual relativities into the aggregate distribution

– We can consider forecasts for different vehicles with different levels of

condition.

– For two identical cars with the same trim and mileage, the 10th percentile

projection pertains to a poorly maintained car, the 90th percentile to a very well

maintained car.

» A fleet level, forecasting model that captures the effect of the economy

on the entire segment in question.

– This model “anchors” the more detailed projections, allowing the effect of the

economy to be correctly rendered.

– Importantly, this model allows prediction of future model years.

17The Value of Granular Risk Rating Models for CECL

Form of the (Assumed) Challenger Model

» This model just uses the VIN level model (Step 1) without the application

of the calibration methods used in the (assumed) champion.

18The Value of Granular Risk Rating Models for CECL

Autocycle 2.0 Backtesting Results

Model N R-Square ME MAE RMSE

In Sample Challenger 30,069,965 0.88 -0.004 0.0615 0.083

Champion 30,146,120 0.90 -0.001 0.055 0.075

Out of

Sample Challenger 6,417,497 0.86* -0.006 0.0608 0.0836

Champion 6,417,497 0.84* 0.034 0.066 0.089

Sources: NADA, Moody’s Analytics

19The Value of Granular Risk Rating Models for CECL

Autocycle 2.0 Backtesting Results

Model N R-Square ME MAE RMSE

In Sample Champion 30,069,965 0.88 -0.004 0.0615 0.083

Challenger 30,146,120 0.90 -0.001 0.055 0.075

Out of

Sample Champion 6,417,497 0.86* -0.006 0.0608 0.0836

Challenger 6,417,497 0.84* 0.034 0.066 0.089

Sources: NADA, Moody’s Analytics

20The Value of Granular Risk Rating Models for CECL

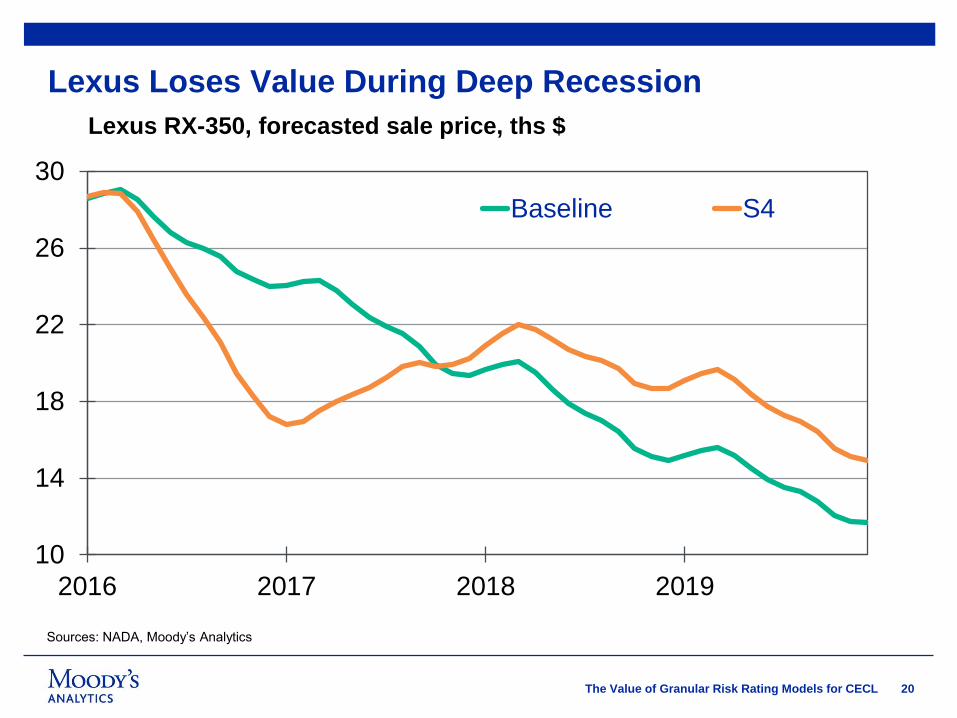

Lexus Loses Value During Deep Recession

10

14

18

22

26

30

2016 2017 2018 2019

Baseline S4

Lexus RX-350, forecasted sale price, ths $

Sources: NADA, Moody’s Analytics

21

Moody’s CECL Councils: Collaborating with the Industry

Activities

» Discuss key implementation challenges

» Share best practices regarding implementation

timelines, governance structure, and modeling

methodologies

» Deep dives into current provision calculation practices

and gaps relative to CECL requirements

Three Groups to “Right” Size CECL Implementation

Community Banks Regional Banks Large Banks

High-Level Timelines

Q1 2017 TBD

Form

CouncilsMeeting #1 Other Meetings

Current point

Benefits for Participants

» Network with leading impairment accounting

practitioners

» Define specific impairment calculation methods for

different asset classes and different-sized institutions

» Help shape design of your and our loss estimation tools

If you would like to participate, please email us at [email protected]

23The Value of Granular Risk Rating Models for CECL

moodysanalytics.com

Contact Us

Chris Henkel

Senior Director, Enterprise Risk Solutions

Moody’s Analytics

Tony Hughes

Managing Director, Economic Research

Moody’s Analytics

Anna Krayn

Senior Director, Business Development

Moody’s Analytics

24The Value of Granular Risk Rating Models for CECL

© 2016 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors

and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES

(“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES,

CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND

RESEARCH PUBLICATIONS PUBLISHED BY MOODY’S (“MOODY’S PUBLICATIONS”) MAY INCLUDE

MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT

COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE

RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY

COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS

DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET

VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN

MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S

PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK

AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT

RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR

FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT

PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES.

NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN

INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND

PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH

INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY

THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE

BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL

INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN

INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER

PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO,

COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE

REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED,

REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN

WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY

PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and

reliable. Because of the possibility of human or mechanical error as well as other factors, however, all

information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary

measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources

MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,

MOODY’S is not an auditor and cannot in every instance independently verify or validate information received

in the rating process or in preparing the Moody’s Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives,

licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or

incidental losses or damages whatsoever arising from or in connection with the information contained herein

or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers,

employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such

losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or

damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned

by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives,

licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any

person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any

other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any

contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,

representatives, licensors or suppliers, arising from or in connection with the information contained herein or

the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS,

MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR

OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER

WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation

(“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds,

debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have,

prior to assignment of any rating, agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating

services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain

policies and procedures to address the independence of MIS’s ratings and rating processes. Information

regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities

who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more

than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate

Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian

Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399

657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as

applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section

761G of the Corporations Act 2001. By continuing to access this document from within Australia, you

represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale

client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or

its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001.

MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the

equity securities of the issuer or any form of security that is available to retail investors. It would be reckless

and inappropriate for retail investors to use MOODY’S credit ratings or publications when making an

investment decision. If in doubt you should contact your financial or other professional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency

subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’s Overseas Holdings Inc., a

wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency

subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”).

Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings

are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not qualify for

certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the

Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2

and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and

municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MJKK or MSFJ (as

applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for

appraisal and rating services rendered by it fees ranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.