Embed Size (px)

Citation preview

Monthly Commodities Report

July 2016

Monthly Commodities Report 2 Monday, 02 August 2016

Contents

1. Inflation Review

2. Weather Update

3. Kharif Crops Sowing Progress

4. Price Volatility in Agricultural Commodities (June 2016 – July 2016)

5. Price Movement in Major Internationally traded Agricultural Commodities

6. Markets and Trade Analysis of major Exchange Traded Commodities

A. Cereals : Maize , Wheat, Barley

B. Pulses: Chana

C. Oilseeds: Soybean, Rapeseed-Mustard seed

D. Spices: Coriander

E. Edible Oils: Soy oil

F. Manufactured Commodities : Sugar

G. Fibres: Cotton

Monthly Commodities Report 3 Monday, 02 August 2016

Inflation

Table 1: Food Articles – Classification and Weightage

Table 2: Non-Food Articles – Classification and Weightage

Commodity Classification

Weightage in

WPI

Total Number of Commodities in

the Group

Number of Commodities

Traded on NCDEX

Commodities Traded on NCDEX

Weightage of NCDEX traded Commodities

Fibre 0.877 6 1 Raw Cotton 0.705

Oil Seeds 1.780 11 2 Soybean, RM Seed

0.709

Other Non-Food

Articles 1.386 9 1 Guar seed, 0.048

Flowers 0.213 3 0 - 0

Total 4.257 29 4 1.462

Table 3: Manufactured Products - Classification and Weightage

Commodity Classification

Weightage in

WPI

Total Number of Commodities in

the Group

Number of Commodities

Traded on NCDEX

Commodities Traded on NCDEX

Weightage of NCDEX traded Commodities

Edible oils 3.042 10 2 Soy oil , Palm oil

0.780

Sugar, Khandsari, Gur

2.088 6 1 Sugar 1.737

Oil cakes 0.494 5 1 Cotton seed

oilcake 0.129

Total 5.625 21 4 2.646

Commodity Classification

Weightage in

WPI

Total Number of Commodities

in the Group

Number of Commodities

Traded on NCDEX

Commodities Traded on NCDEX

Weightage of NCDEX traded

Commodities

Cereals 3.373 7 3 Barley,

Wheat, Maize 1.350

Pulses 0.716 5 1 Gram 0.335

Vegetables 1.735 11 0 - 0

Fruits 2.107 13 0 - 0

Milk 3.238 1 0 - 0

Eggs, Meat & Fish 2.413 7 0 - 0

Condiments &

Spices 0.569 9 4

Turmeric, Chilli,

Coriander, Cumin 0.302

Other Food Articles 0.183 2 0 - 0

Total 14.337 55 8 1.987

Monthly Commodities Report 4 Monday, 02 August 2016

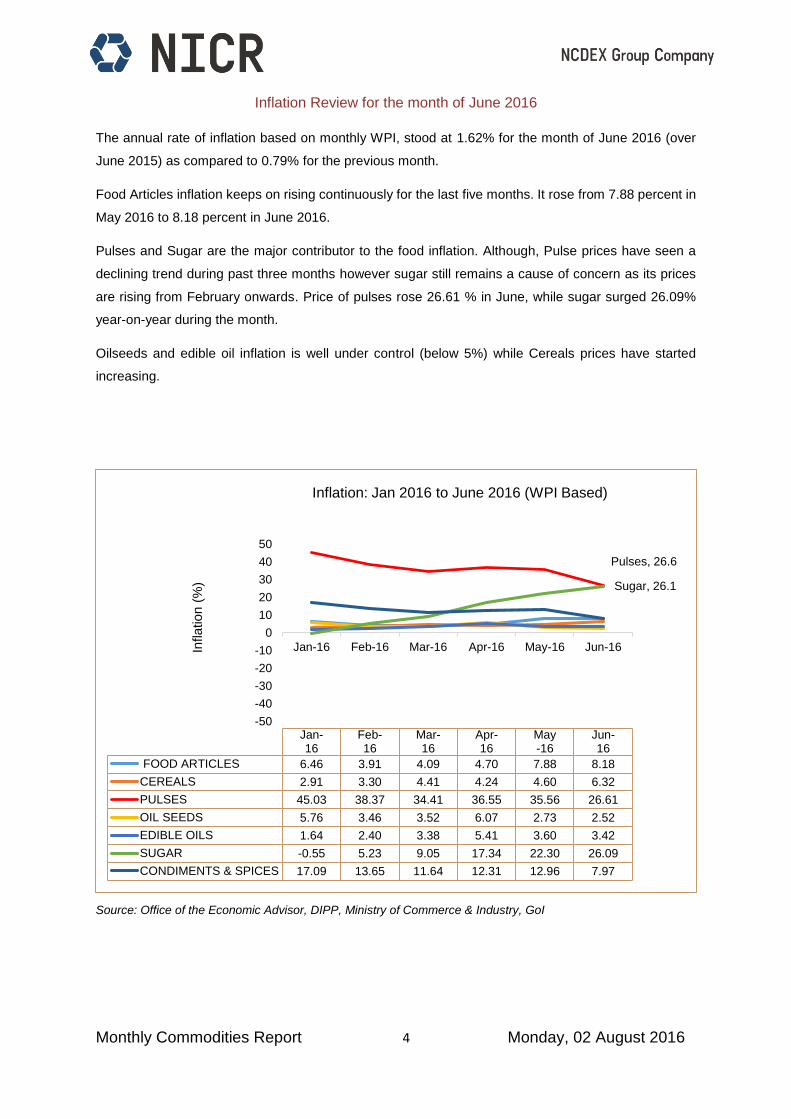

Inflation Review for the month of June 2016

The annual rate of inflation based on monthly WPI, stood at 1.62% for the month of June 2016 (over

June 2015) as compared to 0.79% for the previous month.

Food Articles inflation keeps on rising continuously for the last five months. It rose from 7.88 percent in

May 2016 to 8.18 percent in June 2016.

Pulses and Sugar are the major contributor to the food inflation. Although, Pulse prices have seen a

declining trend during past three months however sugar still remains a cause of concern as its prices

are rising from February onwards. Price of pulses rose 26.61 % in June, while sugar surged 26.09%

year-on-year during the month.

Oilseeds and edible oil inflation is well under control (below 5%) while Cereals prices have started

increasing.

Source: Office of the Economic Advisor, DIPP, Ministry of Commerce & Industry, GoI

Pulses, 26.6

Sugar, 26.1

-50

-40

-30

-20

-10

0

10

20

30

40

50

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16Inflation (

%)

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

FOOD ARTICLES 6.46 3.91 4.09 4.70 7.88 8.18

CEREALS 2.91 3.30 4.41 4.24 4.60 6.32

PULSES 45.03 38.37 34.41 36.55 35.56 26.61

OIL SEEDS 5.76 3.46 3.52 6.07 2.73 2.52

EDIBLE OILS 1.64 2.40 3.38 5.41 3.60 3.42

SUGAR -0.55 5.23 9.05 17.34 22.30 26.09

CONDIMENTS & SPICES 17.09 13.65 11.64 12.31 12.96 7.97

Inflation: Jan 2016 to June 2016 (WPI Based)

Monthly Commodities Report 5 Monday, 02 August 2016

Major Commodities Contributing to Inflation during June 2016

Pulses : Urad, Gram and Tur Sugar : Marked price rise is seen Cereals : Barley, Maize and Wheat

All India Inflation rates (on point to point basis i.e. current month over same month of last year, i.e.,

June 2016 over June 2015), based on monthly WPI are presented below of major agricultural

commodities.

Trend of Rate of Inflation for Important Agricultural Commodities

COMMODITIES Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

FOOD ARTICLES 6.46 3.91 4.09 4.70 7.88 8.18

CEREALS 2.91 3.30 4.41 4.24 4.60 6.32

Barley 2.27 4.84 4.86 18.78 22.00 25.54

Maize 11.43 12.49 8.95 9.24 13.48 16.66

Wheat 5.54 6.03 5.89 5.00 3.85 6.83

PULSES 45.03 38.37 34.41 36.55 35.56 26.61

Urad 66.87 61.51 59.82 59.01 64.92 59.12

Gram 48.06 40.58 34.78 38.50 35.71 33.01

Arhar (Tur) 70.40 56.27 45.08 45.38 41.16 22.79

Masur 23.70 17.49 12.16 15.68 15.35 0.82

Moong 3.80 2.82 7.04 9.00 7.05 -6.50

Sugar -0.55 5.23 9.05 17.34 22.30 26.09

CONDIMENTS & SPICES 17.09 13.65 11.64 12.31 12.96 7.97

Chillies(Dry) 23.61 29.89 29.91 34.93 32.73 26.37

Black Pepper -5.00 -3.13 6.35 9.63 11.65 7.10

Cumin 16.12 9.74 2.61 5.75 8.20 4.50

Turmeric 6.90 2.70 2.42 0.66 -0.08 -0.08

Coriander -9.09 -2.63 4.44 -1.05 -9.11 -17.41

OIL SEEDS 5.76 3.46 3.52 6.07 2.73 2.52

Soybean 2.71 4.21 7.14 13.19 -3.38 2.99

Rape & Mustard Seed 11.99 10.54 12.01 10.15 8.00 1.98

EDIBLE OILS 1.64 2.40 3.38 5.41 3.60 3.42

Mustard & Rapeseed Oil 11.99 10.54 12.01 10.15 8.00 1.98

Soybean Oil -2.14 -1.70 -0.53 2.07 2.47 3.28

Palm Oil -4.21 -2.40 -1.12 0.56 -0.08 1.78

Others

Raw Cotton 2.75 4.23 0.79 -2.68 -3.10 9.03

Cotton Seed Oil Cake 22.01 22.87 25.58 23.50 12.76 10.98

Guar Seed -27.23 -21.64 -24.34 -24.96 -30.40 -31.76

Source: Office of the Economic Advisor, DIPP, Ministry of Commerce & Industry, GoI

Monthly Commodities Report 6 Monday, 02 August 2016

Weather Update

June and July rainfall activities have so far remained satisfactory. Monsoon rainfall in the last two

months has been normal to excess in 25 out of 36 meteorological subdivisions. Gujarat still remains a

rainfall deficient state however by and large other states have seen normal rainfall activities.

Some important regions which contribute a major proportion of kharif season crop production namely

Maharashtra, Rajasthan and Madhya Pradesh have received ample rainfall to boost agricultural

activities. However, in some patches near to above normal rainfall was seen which may cause some

damage to the crop. At the same time, the crops in the Gujarat regions are water stressed thus the crop

growth may be adversely affected if monsoon rainfall activities do not improve in coming weeks.

Normal monsoon rainfall is seen at all India Level. The country received a cumulative seasonal rainfall

of 445.7 mm against a normal of 443.9 mm since 01 June – 30 July, 2016 (Departure: 0% from Long

Period Average) indicating a normal rainfall activity. Some states have received lesser rainfall however

majority of the states have received normal to excess rainfall.

The July rainfall over the country as whole has been 107% above the Long Period Average (LPA). The

rainfall during August is likely to be 104 ± 9% of LPA as was forecasted in June. Rainfall over the country

as a whole during second half of southwest monsoon season (August to September) is most likely to

be above normal (>106% of LPA) with a probability of 55%. Quantitatively, monsoon season rainfall for

the country as a whole is likely to be 106% of the long period average with a model error of ±4% as was

forecasted in June by IMD.

Region wise, the season rainfall is likely to be 108% of LPA over North-West India, 113% of LPA over

Central India, 113% of LPA over South Peninsula and 94% of LPA over North-East India all with a

model error of ± 8 %.

State Rainfall Map (1 June -30 July)

Source: IMD, New Delhi

Monthly Commodities Report 7 Monday, 02 August 2016

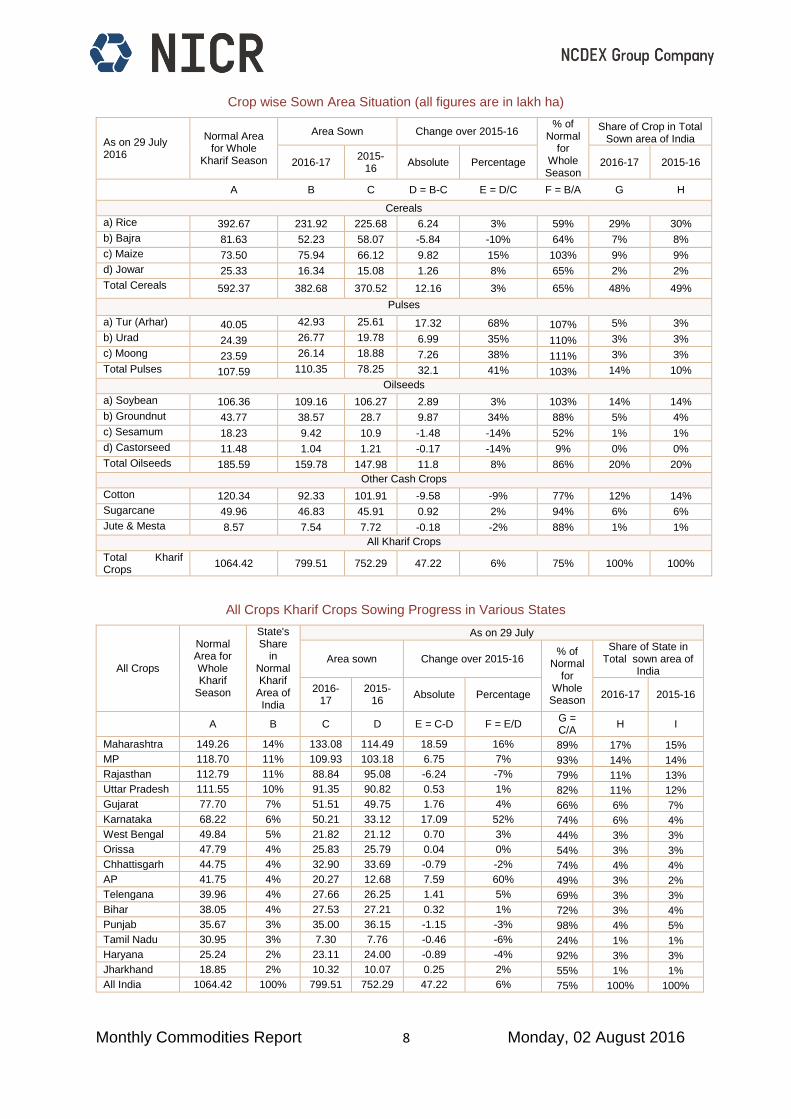

Kharif Crops Sowing Progress

Kharif sowing process is in full swing. About 75% of the normal sown area under kharif season is sown

till 29 July. As compared to last year, sowing is ahead by 6%. The total sown area at all India level as

on 29 July, 2016 stands at 799.51 lakh hectare as compared to 752.29 lakh hectare at this time last

year.

Sowing in the states like Andhra Pradesh, Karnataka, Maharashtra, Madhya Pradesh and Telengana

is running ahead while Rajasthan, Tamil Nadu, Haryana, Punjab and Chhattisgarh are lagging behind

from the previous year’s figures.

In terms of proportionate increase in sown area, pulse are running far ahead from other competing crop

registering about 41% increment in sown area compared to same period last year followed by oilseed

(8%). Cotton sowing is less by 9% this year compared to last year.

Pulses have been sown on 103% of the normal sown area. Sugarcane sowing is about 94% complete

of the normal area. Oilseeds have been sown on 86% of the normal sown area.

Guarseed sown area in Rajasthan has fallen by 43% as compared to the sown area during same period

last year. Only 35% of the normal sown area under Guarseed in Rajasthan is sown till 25 July 2016. In

Gujarat Guarseed sowing is less by 30% compared to last year.

In Telengana, as per market sources, the significant amount of cotton area is diverted towards soybean

and Moong (Green Gram).

All India Sowing Progress as on 29 July 2016 (all figures are in lakh ha)

As on 29 July 2016

Normal Area for Whole Kharif

Season

Share of

Crop in Normal

Area

Area sown Change over 2015-16 % of

Normal for

Whole Season

Share of Crop in Total Sown area of

India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

Total Cereals

592.37 56% 382.68 370.52 12.16 3% 65% 48% 49%

Total Oilseeds

185.59 17% 159.78 147.98 11.8 8% 86% 20% 20%

Total Pulses

107.59 10% 110.35 78.25 32.1 41% 103% 14% 10%

Cotton 120.34 11% 92.33 101.91 -9.58 -9% 77% 12% 14%

Sugarcane 49.96 5% 46.83 45.91 0.92 2% 94% 6% 6%

All Crops 1064.42 100% 799.51 752.29 47.22 6% 75% 100% 100% *Normal Area: it is the average of actual sown area of last 5 Years.

Data Source: MoAFW, GoI,

Major crops grown during Kharif Season

(i) Cereals : Paddy, Jowar, Bajra, Maize, Ragi

(ii) Pulses : Tur (Arhar), Moong, Urad

(iii) Oilseeds : Groundnut, Soybean, Sunflowerseed, Sesamum, Nigerseed, Castor seed

(iv) Cotton

(v) Guarseed

(vi) Sugarcane

(vii) Spices : Chilli and Turmeric

Monthly Commodities Report 8 Monday, 02 August 2016

Crop wise Sown Area Situation (all figures are in lakh ha)

As on 29 July 2016

Normal Area for Whole

Kharif Season

Area Sown Change over 2015-16 % of

Normal for

Whole Season

Share of Crop in Total Sown area of India

2016-17 2015-

16 Absolute Percentage 2016-17 2015-16

A B C D = B-C E = D/C F = B/A G H

Cereals

a) Rice 392.67 231.92 225.68 6.24 3% 59% 29% 30%

b) Bajra 81.63 52.23 58.07 -5.84 -10% 64% 7% 8%

c) Maize 73.50 75.94 66.12 9.82 15% 103% 9% 9%

d) Jowar 25.33 16.34 15.08 1.26 8% 65% 2% 2%

Total Cereals 592.37 382.68 370.52 12.16 3% 65% 48% 49%

Pulses

a) Tur (Arhar) 40.05 42.93 25.61 17.32 68% 107% 5% 3%

b) Urad 24.39 26.77 19.78 6.99 35% 110% 3% 3%

c) Moong 23.59 26.14 18.88 7.26 38% 111% 3% 3%

Total Pulses 107.59 110.35 78.25 32.1 41% 103% 14% 10%

Oilseeds

a) Soybean 106.36 109.16 106.27 2.89 3% 103% 14% 14%

b) Groundnut 43.77 38.57 28.7 9.87 34% 88% 5% 4%

c) Sesamum 18.23 9.42 10.9 -1.48 -14% 52% 1% 1%

d) Castorseed 11.48 1.04 1.21 -0.17 -14% 9% 0% 0%

Total Oilseeds 185.59 159.78 147.98 11.8 8% 86% 20% 20%

Other Cash Crops

Cotton 120.34 92.33 101.91 -9.58 -9% 77% 12% 14%

Sugarcane 49.96 46.83 45.91 0.92 2% 94% 6% 6%

Jute & Mesta 8.57 7.54 7.72 -0.18 -2% 88% 1% 1%

All Kharif Crops

Total Kharif Crops

1064.42 799.51 752.29 47.22 6% 75% 100% 100%

All Crops Kharif Crops Sowing Progress in Various States

All Crops

Normal Area for Whole Kharif

Season

State's Share

in Normal Kharif

Area of India

As on 29 July

Area sown Change over 2015-16 % of

Normal for

Whole Season

Share of State in Total sown area of

India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A

H I

Maharashtra 149.26 14% 133.08 114.49 18.59 16% 89% 17% 15%

MP 118.70 11% 109.93 103.18 6.75 7% 93% 14% 14%

Rajasthan 112.79 11% 88.84 95.08 -6.24 -7% 79% 11% 13%

Uttar Pradesh 111.55 10% 91.35 90.82 0.53 1% 82% 11% 12%

Gujarat 77.70 7% 51.51 49.75 1.76 4% 66% 6% 7%

Karnataka 68.22 6% 50.21 33.12 17.09 52% 74% 6% 4%

West Bengal 49.84 5% 21.82 21.12 0.70 3% 44% 3% 3%

Orissa 47.79 4% 25.83 25.79 0.04 0% 54% 3% 3%

Chhattisgarh 44.75 4% 32.90 33.69 -0.79 -2% 74% 4% 4%

AP 41.75 4% 20.27 12.68 7.59 60% 49% 3% 2%

Telengana 39.96 4% 27.66 26.25 1.41 5% 69% 3% 3%

Bihar 38.05 4% 27.53 27.21 0.32 1% 72% 3% 4%

Punjab 35.67 3% 35.00 36.15 -1.15 -3% 98% 4% 5%

Tamil Nadu 30.95 3% 7.30 7.76 -0.46 -6% 24% 1% 1%

Haryana 25.24 2% 23.11 24.00 -0.89 -4% 92% 3% 3%

Jharkhand 18.85 2% 10.32 10.07 0.25 2% 55% 1% 1%

All India 1064.42 100% 799.51 752.29 47.22 6% 75% 100% 100%

Monthly Commodities Report 9 Monday, 02 August 2016

Crop wise Kharif Sowing Progress in various States ((all figures are in lakh ha)

Cereals

Rice

Normal Rice Area for

Whole Kharif Season

State's Share in Normal Kharif Rice

Area of India

As on 29 July

Area sown Change over 2015-16 % of

Normal for

Whole Season

Share of State in Total Rice sown

area of India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

Uttar Pradesh

58.40 15% 44.19 43.82 0.37 1% 76% 19% 19%

West Bengal 40.63 10% 15.71 14.74 0.97 7% 39% 7% 7%

Orissa 38.39 10% 17.21 17.49 -0.28 -2% 45% 7% 8%

Chhattisgarh 37.74 10% 27.65 28.24 -0.59 -2% 73% 12% 13%

Bihar 30.82 8% 18.80 18.89 -0.09 0% 61% 8% 8%

Punjab 28.48 7% 29.71 29.30 0.41 1% 104% 13% 13%

Assam 21.10 5% 13.13 13.93 -0.80 -6% 62% 6% 6%

Madhya Pradesh

18.46 5% 13.81 10.23 3.58 35% 75% 6% 5%

Andhra Pradesh

16.48 4% 4.48 3.81 0.67 18% 27% 2% 2%

Tamil Nadu 16.14 4% 2.15 1.94 0.21 11% 13% 1% 1%

Maharashtra 15.21 4% 6.35 4.68 1.67 36% 42% 3% 2%

Jharkhand 12.72 3% 5.04 5.46 -0.42 -8% 40% 2% 2%

Haryana 12.42 3% 10.18 11.74 -1.56 -13% 82% 4% 5%

Telengana 10.50 3% 1.91 1.19 0.72 61% 18% 1% 1%

All India 392.67 100% 231.92 225.68 6.24 3% 59% 100% 100%

Maize

Normal Maize Area for

Whole Kharif Season

State's Share in Normal Kharif Maize

Area of India

As on 29 July

Area sown Change over 2015-16 % of

Normal for

Whole Season

Share of State in Total Maize sown

area of India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

Karnataka 11.93 16% 11.00 7.80 3.20 41% 92% 14% 12%

Rajasthan 9.94 14% 9.45 8.36 1.09 13% 95% 12% 13%

Madhya Pradesh

9.08 12% 12.14 10.43 1.71 16% 134% 16% 16%

Maharashtra 7.41 10% 8.03 6.66 1.37 21% 108% 11% 10%

Uttar Pradesh

7.06 10% 6.74 7.15 -0.41 -6% 95% 9% 11%

Telengana 4.62 6% 5.10 3.49 1.61 46% 110% 7% 5%

Gujarat 3.63 5% 3.05 2.80 0.25 9% 84% 4% 4%

Jammu & Kashmir

3.06 4% 1.98 2.07 -0.09 -4% 65% 3% 3%

Himachal Pradesh

2.94 4% 2.97 2.95 0.02 1% 101% 4% 4%

Bihar 2.62 4% 4.18 3.95 0.23 6% 160% 6% 6%

Jharkhand 2.35 3% 2.47 2.35 0.12 5% 105% 3% 4%

Tamil Nadu 1.74 2% 0.08 0.10 -0.02 -20% 5% 0% 0%

Punjab 1.29 2% 1.45 1.46 -0.01 -1% 112% 2% 2%

Chhattisgarh 1.09 1% 1.76 1.71 0.05 3% 161% 2% 3%

Orissa 0.97 1% 1.91 1.84 0.07 4% 197% 3% 3%

Andhra Pradesh

0.83 1% 0.54 0.40 0.14 35% 65% 1% 1%

All India 73.5 100% 75.94 66.12 9.82 15% 103% 100% 100%

Monthly Commodities Report 10 Monday, 02 August 2016

Pulses (all figures are in lakh ha)

Pulses

Normal Pulse Area for

Whole Kharif Season

State's Share in Normal Kharif Pulse

Area of India

As on 29 July

Area sown Change over 2015-16 % of

Normal for

Whole Season

Share of State in Total Pulse sown

area of India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

Rajasthan 24.21 23% 22.95 19.00 3.95 21% 95% 21% 24%

Maharashtra 21.02 20% 23.38 14.91 8.47 57% 111% 21% 19%

Karnataka 13.48 13% 15.32 7.74 7.58 98% 114% 14% 10%

Madhya Pradesh

12.72 12% 17.80 13.23 4.57 35% 140% 16% 17%

Uttar Pradesh

8.82 8% 7.17 6.89 6.28 91% 81% 6% 9%

Gujarat 5.06 5% 3.87 2.45 2.04 83% 76% 4% 3%

Orissa 4.70 4% 3.40 3.04 0.36 12% 72% 3% 4%

Telengana 4.51 4% 5.58 3.16 2.42 77% 124% 5% 4%

Jharkhand 3.15 3% 2.73 2.08 0.65 31% 87% 2% 3%

Andhra Pradesh

2.62 2% 2.38 0.66 1.72 261% 91% 2% 1%

Tamil Nadu 2.16 2% 0.89 0.86 0.03 3% 41% 1% 1%

Chhattisgarh 2.11 2% 1.46 1.63 -0.17 -10% 69% 1% 2%

All India 107.59 100% 110.35 78.25 32.1 41% 103% 100% 100%

Tur (Arhar)

Normal Tur Area for

Whole Kharif Season

State's Share in Normal Kharif

Tur Area of India

As on 29 July

Area sown Change over 2015-16 % of

Normal area for Whole Season

Share of State in Total Tur Sown

area of India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

Maharashtra 12.13 30% 13.94 8.53 5.41 63% 115% 32% 33%

Karnataka 7.74 19% 10.01 3.34 6.67 200% 129% 23% 13%

Madhya Pradesh

5.08 13% 6.03 4.53 1.50 33% 119% 14% 18%

UP 3.13 8% 2.26 2.47 -0.21 -9% 72% 5% 10%

Telengana 2.80 7% 3.77 1.88 1.89 101% 135% 9% 7%

Gujarat 2.35 6% 2.42 1.64 0.78 48% 103% 6% 6%

Andhra Pradesh

2.04 5% 1.71 0.42 1.29 307% 84% 4% 2%

Jharkhand 1.61 4% 0.00 0.00 0.00 #DIV/0! 0% 0% 0%

Orissa 1.39 3% 0.95 1.01 -0.06 -6% 68% 2% 4%

All India 40.05 100% 42.93 25.61 17.32 68% 107% 100% 100%

Monthly Commodities Report 11 Monday, 02 August 2016

Urad

Normal Urad Area for

Whole Kharif Season

State's Share in Normal Kharif Urad

Area of India

As on 29 July

Area sown Change over 2015-16 % of

Normal for

Whole Season

Share of State in Total Urad Sown

area of India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

Madhya Pradesh

6.45 26% 9.72 7.49 2.23 30% 151% 36% 38%

UP 5.21 21% 4.51 4.07 0.44 11% 87% 17% 21%

Maharashtra 3.63 15% 4.11 2.35 1.76 75% 113% 15% 12%

Rajasthan 2.00 8% 3.51 2.07 1.44 70% 176% 13% 10%

Orissa 1.00 4% 0.94 0.74 0.20 27% 94% 4% 4%

Chhattisgarh 0.97 4% 0.53 0.66 -0.13 -20% 55% 2% 3%

Karnataka 0.93 4% 0.77 0.70 0.07 10% 83% 3% 4%

Jharkhand 0.93 4% 0.00 0.00 0.00 #DIV/0! 0% 0% 0%

Gujarat 0.90 4% 0.97 0.54 0.43 80% 108% 4% 3%

Tamil Nadu 0.53 2% 0.34 0.20 0.14 70% 64% 1% 1%

Andhra Pradesh

0.19 1% 0.33 0.04 0.29 725% 174% 1% 0%

All India 24.39 100% 26.77 19.78 6.99 35% 110% 100% 100%

Moong

Normal Moong Area

for Whole Kharif

Season

State's Share in Normal Kharif Moong Area of India

As on 29 July

Area sown Change over 2015-16 % of Normal

for Whole Season

Share of State in Total Moong Sown

area of India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

Rajasthan 10.05 41% 11.97 8.73 3.24 37% 119% 46% 46%

Maharashtra 4.33 18% 4.70 3.23 1.47 46% 109% 18% 17%

Karnataka 2.83 12% 3.74 2.76 0.98 36% 132% 14% 15%

Gujarat 1.36 6% 0.38 0.21 0.17 81% 28% 1% 1%

Telengana 1.29 5% 1.39 1.01 0.38 38% 108% 5% 5%

Orissa 1.05 4% 1.05 0.81 0.24 30% 100% 4% 4%

MP 1.02 4% 1.71 1.12 0.59 53% 168% 7% 6%

UP 0.48 2% 0.40 0.35 0.05 14% 83% 2% 2%

Andhra Pradesh

0.26 1% 0.28 0.15 0.13 87% 108% 1% 1%

All India 23.59 97% 26.14 18.88 7.26 38% 111% 100% 100%

Monthly Commodities Report 12 Monday, 02 August 2016

Oilseeds (all figures are in lakh ha)

Oilseeds

Normal Oilseeds Area for

Whole Kharif Season

State's Share in Normal Kharif

Oilseeds Area of India

As on 29 July

Area sown Change over 2015-16 % of Normal

for Whole Season

Share of State in Total oilseeds

sown area of India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

MP 64.34 35% 56.21 59.44 -3.23 -5% 87% 35% 40%

Maharashtra 36.01 19% 39.21 34.19 5.02 15% 109% 25% 23%

Gujarat 24.67 13% 17.08 14.39 2.69 19% 69% 11% 10%

Rajasthan 20.35 11% 17.18 18.59 -1.41 -8% 84% 11% 13%

AP 12.95 7% 7.94 3.54 4.40 124% 61% 5% 2%

Karnataka 9.85 5% 8.66 5.47 3.19 58% 88% 5% 4%

UP 4.45 2% 4.12 4.49 -0.37 -8% 93% 3% 3%

Tamil Nadu 2.92 2% 1.05 1.16 -0.11 -9% 36% 1% 1%

Telengana 2.73 1% 3.34 2.84 0.50 18% 122% 2% 2%

Chhattisgarh 2.18 1% 1.85 1.91 -0.06 -3% 85% 1% 1%

All India 185.59 100% 159.78 147.98 11.8 8% 86% 100% 100%

Groundnut

Normal Groundnut

Area for Whole Kharif

Season

State's Share in Normal Kharif

Groundnut Area of India

As on 29 July

Area sown Change over 2015-16 % of

Normal for

Whole Season

Share of State in Total Groundnut

sown area of India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

Gujarat 14.92 34% 15.02 12.62 2.40 19% 101% 39% 44%

AP 10.57 24% 7.39 3.22 4.17 130% 70% 19% 11%

Karnataka 5.05 12% 4.11 1.84 2.27 123% 81% 11% 6%

Rajasthan 4.24 10% 4.06 4.31 -0.25 -6% 96% 11% 15%

Maharashtra 2.48 6% 1.87 1.61 0.26 16% 75% 5% 6%

Tamil Nadu 2.32 5% 1.00 1.05 -0.05 -5% 43% 3% 4%

MP 2.12 5% 2.06 1.92 0.14 7% 97% 5% 7%

UP 0.93 2% 0.87 0.83 0.04 5% 94% 2% 3%

Chhattisgarh 0.27 1% 0.43 0.42 0.01 2% 159% 1% 1%

Telengana 0.21 0% 0.07 0.05 0.02 40% 33% 0% 0%

All India 43.77 100% 38.57 28.7 9.87 34% 88% 100% 100%

Soybean

Normal Soybean Area for

Whole Kharif Season

State's Share in Normal Kharif

Soybean Area of India

As on 29 July

Area sown Change over 2015-16 % of

Normal for Whole Season

Share of State in Total Soybean

sown area of India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

MP 58.30 55% 52.58 55.46 -2.88 -5% 90% 48% 52%

Maharashtra 32.24 30% 36.81 32.20 4.61 14% 114% 34% 30%

Rajasthan 9.60 9% 10.25 10.66 -0.41 -4% 107% 9% 10%

Karnataka 2.01 2% 3.05 2.66 0.39 15% 152% 3% 3%

Telengana 1.31 1% 2.86 2.42 0.44 18% 218% 3% 2%

Chhattisgarh 1.05 1% 1.32 1.35 -0.03 -2% 126% 1% 1%

Gujarat 0.58 1% 1.24 0.83 0.41 49% 214% 1% 1%

AP 0.50 0% 0.01 0.00 0.01 #DIV/0! 2% 0% 0%

UP 0.24 0% 0.35 0.31 0.04 13% 146% 0% 0%

All India 106.36 100% 109.16 106.27 2.89 3% 103% 100% 100%

Monthly Commodities Report 13 Monday, 02 August 2016

Other Commercial Crops (all figures are in lakh ha)

Cotton

Normal Cotton Area for Whole

Kharif Season

State's Share in Normal Kharif Cotton Area of India

As on 29 July

Area sown Change over 2015-16 % of

Normal for

Whole Season

Share of State in Total Cotton sown

area of India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

Maharashtra 41.19 34% 36.27 36.10 0.17 0% 88% 39% 35%

Gujarat 26.77 22% 20.38 23.48 -3.10 -13% 76% 22% 23%

Telengana 16.32 14% 11.22 15.21 -3.99 -26% 69% 12% 15%

Karnataka 6.24 5% 3.60 3.69 -0.09 -2% 58% 4% 4%

Madhya Pradesh

6.05 5% 5.27 5.42 -0.15 -3% 87% 6% 5%

Haryana 5.86 5% 4.98 5.81 -0.83 -14% 85% 5% 6%

Andhra Pradesh

5.84 5% 2.85 2.78 0.07 3% 49% 3% 3%

Punjab 4.87 4% 2.56 4.50 -1.94 -43% 53% 3% 4%

Rajasthan 4.27 4% 3.74 3.49 0.25 7% 88% 4% 3%

Tamil Nadu 1.44 1% 0.03 0.03 0.00 0% 2% 0% 0%

Orissa 1.09 1% 1.26 1.19 0.07 6% 116% 1% 1%

All India 120.34 100% 92.33 101.91 -9.58 -9% 77% 100% 100%

Sugarcane

Normal Sugarcane

Area for Whole Kharif

Season

State's Share in Normal Kharif

Sugarcane Area of India

As on 29 July

Area sown Change over 2015-16 % of

Normal for

Whole Season

Share of State in Total Kharif

Sugarcane sown area of India

2016-17

2015-16

Absolute Percentage 2016-17 2015-16

A B C D E = C-D F = E/D G = C/A H I

Uttar Pradesh

21.74 44% 21.79 20.52 1.27 6% 100% 47% 45%

Maharashtra 9.77 20% 7.62 8.21 -0.59 -7% 78% 16% 18%

Karnataka 4.36 9% 4.44 3.96 0.48 12% 102% 9% 9%

Tamil Nadu 3.17 6% 2.68 2.94 -0.26 -9% 85% 6% 6%

Bihar 2.46 5% 2.52 2.50 0.02 1% 102% 5% 5%

Gujarat 1.90 4% 1.87 2.03 -0.16 -8% 98% 4% 4%

Andhra Pradesh

1.52 3% 1.40 1.17 0.23 20% 92% 3% 3%

Uttrakhand 1.06 2% 0.86 0.90 -0.04 -4% 81% 2% 2%

Haryana 0.96 2% 1.13 1.13 0.00 0% 118% 2% 2%

Punjab 0.83 2% 0.94 0.70 0.24 34% 113% 2% 2%

All India 49.96 100% 46.83 45.91 0.92 2% 94% 100% 100%

Guarseed Normal Gaur

Area for Whole Kharif Season

As on 29 July

Area sown Change over 2015-16 % of Normal for Whole Season 2016-17 2015-16 Absolute Percentage

A C D E = C-D F = E/D G = C/A

Rajasthan 40.60 14.27 25.18 -10.91 -43% 35%

Gujarat 37.88 5.30 7.60 -2.30 -30% 14%

Monthly Commodities Report 14 Monday, 02 August 2016

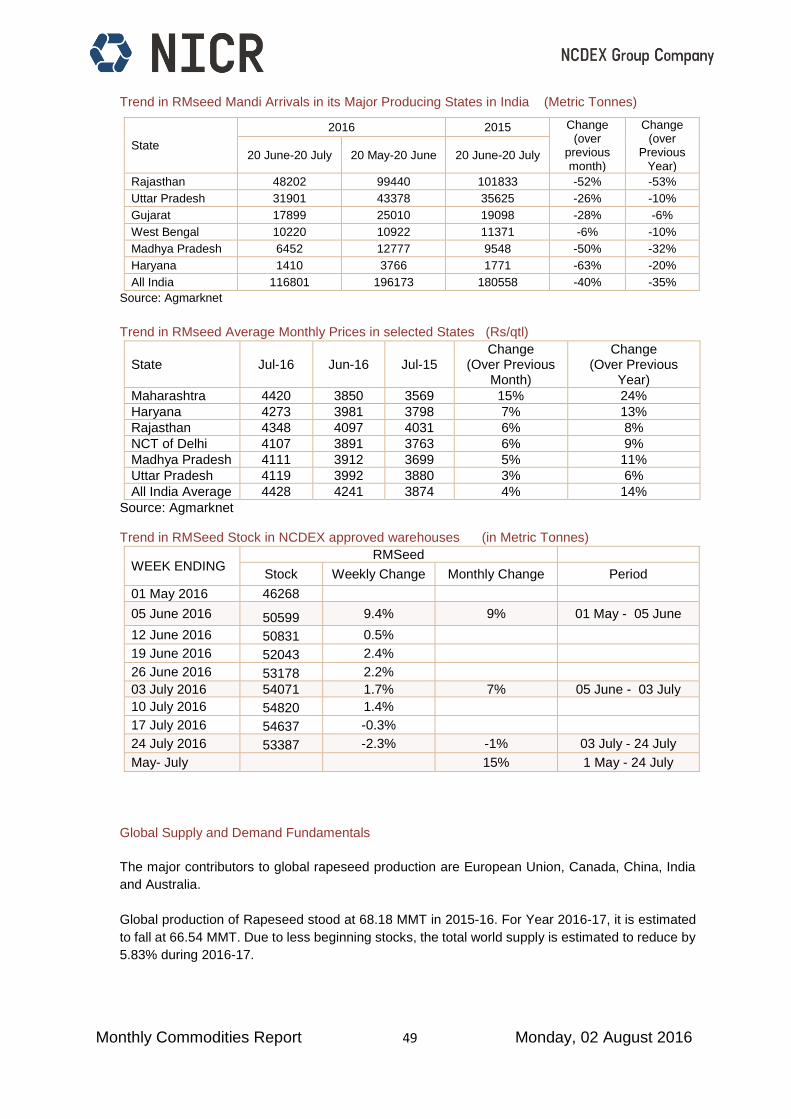

Price Volatility in Agricultural Commodities Review Period: 20 June – 20 July, 2016

Spot and Futures Prices:

A comparative price change in the major agricultural commodities during the current month and the

last month is presented below.

Commodity

Current Month Same Period Last Month

20 June - 20 July, 2016 20 May - 20 June, 2016

Near Month Futures

Spot Near Month

Futures Spot

Chana 31% 27% 20% 14%

Guar gum 31% 35% 3% 4%

Guar seed 10 21% 23% -2% -2%

Coriander 19% 15% -3% -2%

Kapas 12% - 3% -

Cotton cake 10% 10% 12% 10%

Turmeric 7% 1% 0% -2%

Jeera 6% 11% 6% 2%

Rmseed 5% 8% 5% 6%

Cpo 2% 3% -6% -5%

Barley 0% 0% 1% 2%

Sugar -1% 0% 1% 1%

Chilli -1% 0% 5%

Soya oil -2% 0% -1% 1%

Wheat -4% -2% 7% 7%

Maize rabi -4% 1% 10% 18%

Soybean -6% -2% -5% -4%

Price rise in Spot and futures market was seen in Chana, Guar gum, Guar seed, Coriander, Kapas

Cotton cake, Turmeric, Jeera and Rmseed. However other commodities like soybean, Maize and What

witnessed a price fall during the period from 20-06-2016 to 20-07-2016. No significant change was

observed in sugar, CPO and Chilli Prices.

Significant price rise was observed in Chana, Guarseed, Guar gum, Coriander, Kapas and Cotton cake

in spot as well as futures market. Considerable price fall was seen in Soybean, Maize Rabi and Wheat

prices.

Firm consumption demand amidst tight supply kept Chana prices up. Sharp decline in sown area under

Cotton and Guar seed in during current kharif season fuelled the market sentiments of these two crops.

Weakness was seen in the Soybean and Maize prices due to overall good sowing progress in their

major growing states. Soy oil and CPO sentiments also remained steady due to increased imports in to

India.

Monthly Commodities Report 15 Monday, 02 August 2016

A table summarizing the movement in spot and futures prices of major agricultural commodities during

the period from 20 June, 2016 to 20 July, 2016 is presented below:

Commodity Expiry Date

Futures Price Spot Price

20-06-2016 20-07-2016 %

Change 20-06-2016 20-07-2016

% Change

BARLEY Jul-16 1,591.50 1,595.00 0.22%

1,627.95 1,626.80 -0.07% BARLEY Aug-16 1,623.50 1,622.00 -0.09%

BARLEY Sep-16 1,649.50 1,653.50 0.24%

BARLEY Oct-16 1,675.50 1,685.00 0.57%

CHANA Jul-16 6,870.00 9,033.00 31.48%

6,937.00 8,842.10 27.46% CHANA Aug-16 6,764.00 8,893.00 31.48%

CHANA Sep-16 6,614.00 8,946.00 35.26%

CHANA Oct-16 6,398.00 8,599.00 34.40%

CHILLI Jul-16 12,976.00 12,882.00 -0.72%

12,900.00

12,866.65 -0.26% CHILLI Aug-16 13,050.00 12,940.00 -0.84%

CHILLI Sep-16 13,130.00 13,018.00 -0.85%

CHILLI Oct-16 13,206.00 13,092.00 -0.86%

CORIANDER Jul-16 7,007.00 8,338.00 19.00%

7,189.55

8,303.15

15.49% CORIANDER Aug-16 7,074.00 7,832.00 10.72%

CORIANDER Sep-16 7,141.00 7,832.00 9.68%

CORIANDER Oct-16 7,208.00 8,007.00 11.08%

COTTON_CAKE Jul-16 2,486.00 2,740.00 10.22%

2,531.35

2,773.75

9.58% COTTON_CAKE Aug-16 2,531.00 2,700.00 6.68%

COTTON_CAKE Sep-16 2,583.00 2,782.00 7.70%

COTTON_CAKE Dec-16 2,058.00 2,261.00 9.86%

CPO Jul-16 513.90 525.00 2.16%

510.00

524.05

2.75% CPO Aug-16 517.10 528.20 2.15%

CPO Sep-16 520.10 531.20 2.13%

CPO Oct-16 522.90 534.00 2.12%

GUAR_GUM Jul-16 5,340.00 6,980.00 30.71%

5,357.20

7,221.20

34.79% GUAR_GUM Oct-16 5,700.00 7,310.00 28.25%

GUAR_GUM 5 Nov-16 6,060.00 7,483.00 23.48%

GUAR_GUM 5 Dec-16 6,420.00 7,709.00 20.08%

GUAR_SEED_10 Jul-16 3,047.00 3,673.00 20.54%

3,090.50

3,800.00

22.96% GUAR_SEED_10 Oct-16 3,162.00 3,871.00 22.42%

GUAR_SEED_10 Nov-16 3,198.00 3,922.00 22.64%

GUAR_SEED_10 Dec-16 3,234.00 3,989.00 23.35%

JEERA Jul-16 17,755.00 18,905.00 6.48%

17,419.25

19,273.10

10.64% JEERA Aug-16 17,970.00 19,280.00 7.29%

JEERA Sep-16 18,065.00 19,585.00 8.41%

JEERA Oct-16 18,160.00 19,795.00 9.00%

KAPAS Apr-17 914.00 1,027.50 12.42% # #

Monthly Commodities Report 16 Monday, 02 August 2016

Commodity Expiry Date

Futures Price Spot Price

20-06-2016 20-07-2016 %

Change 20-06-2016 20-07-2016

% Change

MAIZE RABI Jul-16 1,584.00 1,520.00 -4.04%

1,514.35

1,530.70 1.08% MAIZE RABI Aug-16 1,612.00 1,533.00 -4.90%

MAIZE RABI Sep-16 1,626.00 1,548.00 -4.80%

MAIZE KHARIF Oct-16 1,488.00 1,404.00

-5.65%

1,640.00

1,744.35 6.36%

RMSEED Jul-16 4,710.00 4,956.00 5.22%

4,750.00

5,150.00

8.42% RMSEED Aug-16 4,783.00 5,002.00 4.58%

RMSEED Sep-16 4,846.00 5,072.00 4.66%

RMSEED Oct-16 4,931.00 5,179.00 5.03%

SOYBEAN Jul-16 3,827.00 3,596.00 -6.04%

3,911.00

3,803.00

-2.76%

SOYBEAN Oct-16 3,692.00 3,739.00 1.27%

SOYBEAN Nov-16 3,665.00 3,711.00 1.26%

SOYBEAN Dec-16 3,713.00 3,760.00 1.27%

SOYBEAN Jan-17 3,789.00 3,814.00 0.66%

SOYA_OIL Jul-16 646.10 631.10 -2.32%

634.15

633.80

-0.06%

SOYA_OIL Aug-16 650.45 644.85 -0.86%

SOYA_OIL Sep-2016

652.15 644.95 -1.10%

SOYA_OIL Oct-16 645.00 642.50 -0.39%

SOYA_OIL Nov-16 645.45 637.10 -1.29%

SOYA_OIL Dec-16 648.45 639.10 -1.44%

SOYA_OIL Jan-17 652.35 645.20 -1.10%

SUGAR Jul-16 3,631.00 3,610.00 -0.58%

3,646.00

3,656.25

0.28%

SUGAR Oct-16 3,760.00 3,824.00 1.70%

SUGAR Dec-16 3,700.00 3,814.00 3.08%

SUGAR Mar-17 3,842.00 3,880.00 0.99%

SUGAR May-17 3,984.00 3,946.00 -0.95%

SUGAR Jul-17 4,126.00 4,012.00 -2.76%

SUGAR Oct-17 4,045.00 4,285.00 5.93%

SUGAR Dec-17 4,095.00 4,270.00 4.27%

TURMERIC Jul-16 8,068.00 8,618.00 6.82%

8,380.95

8,464.45

1.00% TURMERIC Aug-16 8,106.00 8,322.00 2.66%

TURMERIC Sep-16 8,144.00 8,330.00 2.28%

TURMERIC Oct-16 8,182.00 8,400.00 2.66%

WHEAT Jul-16 1,790.00 1,725.00 -3.63%

1,825.00

1,782.50

-2.33% WHEAT Aug-16 1,814.00 1,738.00 -4.19%

WHEAT Sep-16 1,845.00 1,764.00 -4.39%

WHEAT Oct-16 1,864.00 1,791.00 -3.92%

NOTE: # Kapas spot price will be available from Feb 2017 onwards.

Monthly Commodities Report 17 Monday, 02 August 2016

Price Movement in Major Internationally traded Agricultural Commodities

Cotton prices in the international market rose by 11.74%. Commodities like Corn, Wheat, Soymeal, and

Soybean observed sharp fall in prices. Moderate price fall was seen in CPO and Soy oil prices.

A table summarizing the movement in futures prices of major internationally traded agricultural

commodities during the period from 20 June to 20 July, 2016 is presented below:

Commodity Exchange Price Unit

Price as on

Price as on

Change Major Specification

20-Jun-16 20-Jul-16

Cotton ICE Cents/Pound 64.39 71.95 11.74% Cotton No. 2 Futures, Strict Low Middling Staple Length:

1 2/32nd inc

Sugar LIFFE Dollar/MT 536.4 535.9 -0.09% No. 5- Refined Sugar

CPO BMD Ringgit/MT 2443 2387 -2.29% Crude Palm Kernel Oil in bulk unbleached of good

merchantable quality.

Soy Oil CBOT Cents/lb 31.64 30.71 -2.94% Crude soybean oil meeting

exchange -approved grades-expeller pressed

Soybean CBOT Cents/Bushel 1143.5 1027 -10.19% No.2- Yellow Soybean

Soy meal CBOT Dollar and Cents/short ton

402.7 352 -12.59% 48% Protein soybean meal

Wheat CBOT Cents/Bushel 473 413 -12.68% No. 2 Soft Red Winter

Corn CBOT Cents/Bushel 421.25 337.5 -19.88% No. 2 Yellow Maize

Note:

CBOT: Chicago Board of Trade (US), ICE: Intercontinental Exchange (US) LIFFE: The London International Financial Futures and Options Exchange (UK) BMD: Bursa Malaysia Derivatives (Malaysia); previously known as KLSE i.e. Kuala Lumpur Stock Exchange

Monthly Commodities Report 18 Monday, 02 August 2016

Markets and Trade Analysis of major Exchange Traded Commodities

Cereals

Maize

Introduction

Maize (Corn) is one of the most important cereal crops in the world. In India, maize is the third most

important food crops after rice and wheat. The importance of maize is due to its wide diversity of

uses. It is used both as food for human and feed for animals. Maize is nearly directly consumed as

feed and as an edible table vegetable. Maize is converted in to a variety of foods such as popped

snack food, green cobs, sweet corn, baby corn, popcorn etc. Maize is a major source of starch.

Maize is used as feed meal in poultry and livestock and as an industrial ingredient to thousands of

industrial products that includes starch, edible oil, protein, alcoholic beverages, food sweeteners,

pharmaceutical, cosmetic, film, textile, gum, package, paper industries and ethanol, etc.

Cultivation Pattern

Maize in grown during both Kharif and Rabi season but around 70-75% of the total production

comes from Kharif season crop. Kharif Maize is sown in India between May and June and is

harvested in September-October. Rabi Maize is sown in October-November and is harvested in

April-May.

Production

India’s Maize production is estimated to fall by nearly 13% for the crop Year 2015-16. According to

the Indian Government’s 3rd advance estimates for 2015-16, India’s Maize production is estimated

at 21.02 million metric tonnes (MMT). Maize. Karnataka, Andhra Pradesh, Bihar and Maharashtra

are the major producers of maize in India.

State wise Maize Production (in MMT)

States 2001-02 2010-11 2011-12 2012-13 2013-14 2014-15*

Andhra Pradesh 1.46 3.96 3.66 4.86 4.86 3.94

Karnataka 1.45 4.44 4.09 3.48 3.98 3.85

Bihar 1.49 1.44 1.61 2.48 2.11 2.17

Maharashtra 0.59 2.60 2.43 1.82 2.73 2.04

Madhya Pradesh 1.68 1.05 1.29 1.51 1.53 1.88

Tamil Nadu 0.12 1.03 1.70 0.95 1.86 1.82

Rajasthan 1.48 2.05 1.67 1.76 1.50 1.57

Uttar Pradesh 1.52 1.11 1.31 1.23 1.31 1.33

Himachal Pradesh 0.77 0.67 0.72 0.66 0.65 0.72

Others 2.61 3.37 3.30 3.52 3.72 3.66

India 13.16 21.73 21.76 22.26 24.26 22.97

Source: Indiastat.com

Monthly Commodities Report 19 Monday, 02 August 2016

Global Supply and Demand Fundamentals In 2015-16, global production of corn is estimated to remain at 960 MMT which is around 5% less

as compared to Year 2014-15. Despite ample beginning stocks, the total supplies are estimated to

remain low as compared to last year. However the world corn supply projections for 2016-17 are

quite encouraging. The world corn production is anticipated to increase by 5.31%.

World Corn Supply & Demand Estimates (in MMT)

Attribute 2014-15 2015-16

(Estimates) 2016-17

(Projections)

Change in 2015-16 over

2014-15

Change in 2016-17

over 2015-16

Beginning Stocks 176 209 207 19% -0.77%

Production 1013 960 1011 -5% 5.31%

Imports 125 135 127 8% -5.95%

Total Supply 1314 1303 1344 -1% 3.17%

Exports 142 119 133 -16% 11.72%

Total Consumption 964 977 1002 1% 2.65%

Ending Stocks 208 207 208 -1% 0.72% Source: United State Department of Agriculture (USDA), As on 25 July 2016

India is the 8th largest producer, 6th largest consumer and 15th largest exporter of corn. Top 10 world

leaders in corn production, consumption, exports and imports are presented below.

Leading Corn Producers in World, 2015-16 Leading Corn Consumers in World, 2015-16

Top Producers Production

(in MMT)

Country's Share in

World Total

Top Consumers Consumption

(in MMT)

Country's Share in

World Total

United States 345.49 36% United States 301.25 31%

China 224.58 23% China 217.50 22%

Brazil 77.50 8% European Union 74.01 8%

European Union 57.98 6% Brazil 58.00 6%

Argentina 27.00 3% Mexico 35.80 4%

Mexico 25.00 3% India 22.20 2%

Ukraine 23.33 2% Egypt 14.75 2%

India 21.00 2% Japan 14.60 1%

Canada 13.60 1% Canada 13.40 1%

Russia 13.17 1% Indonesia 12.80 1%

Other 137.72 14% Other 216.67 22%

World 966.37 100% World 980.99 100%

Leading Corn Exporters in World, 2015-16 Leading Corn Importers in World, 2015-16

Top Exporters Export

(in MMT)

Country's Share in

World Total

Top Importers Import

(in MMT)

Country's Share in

World Total

United States 46.36 38% Japan 14.70 11%

Brazil 22.50 19% European Union 14.50 11%

Argentina 18.00 15% Mexico 12.50 9%

Ukraine 16.00 13% Korea, South 10.00 8%

Russia 4.40 4% Egypt 8.50 6%

Paraguay 2.30 2% Vietnam 7.30 5%

Serbia 1.70 1% Iran 5.50 4%

European Union 1.60 1% Colombia 4.50 3%

Mexico 1.00 1% Taiwan 4.20 3%

Canada 1.00 1% Algeria 4.10 3%

Other 5.77 5% Other 47.49 36%

World 120.62 100% World 133.29 100%

Source: USDA, as on 22 June 2016,

Monthly Commodities Report 20 Monday, 02 August 2016

Spot and Futures Price Chart

0

200

400

600

800

1000

1200

1400

1600

1800

Ap

r-11

Jul-

11

Oct-

11

Jan

-12

Ap

r-12

Jul-

12

Oct-

12

Jan

-13

Ap

r-13

Jul-

13

Oct-

13

Jan

-14

Ap

r-14

Jul-

14

Oct-

14

Jan

-15

Ap

r-15

Jul-

15

Oct-

15

Jan

-16

Ap

r-16

Jul-

16

Rs./

Qu

inta

lMaize Long Term Price Trend

Spot Price Futures Prices

1,300

1,400

1,500

1,600

1,700

1,800

20-J

un-1

6

21-J

un-1

6

22-J

un-1

6

23-J

un-1

6

24-J

un-1

6

25-J

un-1

6

26-J

un-1

6

27-J

un-1

6

28-J

un-1

6

29-J

un-1

6

30-J

un-1

6

01-J

ul-1

6

02-J

ul-1

6

03-J

ul-1

6

04-J

ul-1

6

05-J

ul-1

6

06-J

ul-1

6

07-J

ul-1

6

08-J

ul-1

6

09-J

ul-1

6

10-J

ul-1

6

11-J

ul-1

6

12-J

ul-1

6

13-J

ul-1

6

14-J

ul-1

6

15-J

ul-1

6

16-J

ul-1

6

17-J

ul-1

6

18-J

ul-1

6

19-J

ul-1

6

20-J

ul-1

6

Rs./

Qu

inta

l

Maize Price Trend : 20 June - 20 July, 2016

Spot Price Jul-2016 Aug-2016 Sep-2016

Monthly Commodities Report 21 Monday, 02 August 2016

Production during last 3 years

Year Production

(Million MT)

2013-14 24.26

2014-15 24.17

2015-16 (3rd Advance Estimates) 21.02

Average Spot Prices

Financial Year Average Price

(Rs/ Quintal) Y-O-Y

Price Variation

2013-14 1355

2014-15 1216 -10.25%

2015-16 1382 13.65%

2016-17 1349 -2.41%

Month-wise Price Volatility

*Maize (Rabi)

Average Open Interest, Stocks in approved warehouses and deliveries

Financial Year Average

Open Interest (MT)

Stocks in approved warehouses

(MT)

Deliveries during the year

(MT)

2013-14 61423 14604 28760

2014-15 38267 28332 57180

2015-16 18276 22975 48130

2016-17 31074 10876 4980

Stocks = Maximum stocks on the day of expiry during respective financial year

Deliveries = Total deliveries during the respective financial year

Trend in Maize Stock in NCDEX approved warehouses (in Metric Tonnes)

WEEK ENDING MAIZE

Stock Weekly Change Monthly Change Period

01-May-16 3989

05-Jun-16 5058 27% 27% 01 May - 05 June

12-Jun-16 6894 36%

19-Jun-16 5645 -18%

26-Jun-16 6200 10%

03-Jul-16 8005 29% 58% 05 June - 03 July

10-Jul-16 10325 29%

17-Jul-16 10806 5%

24-Jul-16 11334 5% 42% 03 July - 24 July

May- July 184% 1 May - 24 July

Note: Stock includes valid stocks + in process stock

Month Volatility

Jan-16 5.89%

Feb-16 16.61%

Mar-16 59.76%

April-16 34.00%

May -16 10.83%

June -16 27.57%

July-16 (Till 20 July) 12.38%

*Spot Price Volatility during January to July Period 31.39%

Monthly Commodities Report 22 Monday, 02 August 2016

Markets and Trade

Weakness is seen in Maize domestic as well international prices during the period under review (20

June-20 July 2016).

Domestic Spot market prices fell by 2% while near month futures declined by 4%.

In international market (CBOT) Corn price fell by 19.88% during the period under review.

Kharif season Maize sown area has seen increment this year. The sown area at all India level is

increased by 9% as compared to previous year. Karnataka, Rajasthan and Madhya Pradesh have

witnessed an area increase by 32, 19 and 20% respectively by 22 July 2016.

Better sowing prospects in India and weak international markets have remained one of the most

important factors behind the weakness in the Maize prices during period under review.

Maize stocks at the NCDEX approved warehouses have shown increment of about 184% during

last three months. This has also resulted in to weakness in the market prices.

Arrivals have also declined amidst subdued demand.

As per 3rd Advance Estimate for 2015-16, maize production is estimated to be around 21.02 million

tonnes in 2015-16 as against 24.17 million tonnes produced in 2014-15 (down by 13%).

Indian state-run trading company PEC Ltd has floated a new international tender to buy and import

200,000 tonnes of non-GMO yellow corn (maize). Shipment is sought between Dec. 15, 2016 and

Jan. 31, 2017. Earlier, PEC received only one offer in a tender to import 120,000 tonnes of GMO-

free corn. The sole tender participant offered only 25,000 tonnes of corn due to difficulties in sourcing

non-GMO corn as it is grown by only few countries in the world. It is to be learnt that Indian

government has asked state trading houses to import an extra half a million tonnes of GMO-free

corn to curve rising prices and ease domestic supplies.

International

International corn prices at CBOT has also seen sharp fall (19.88%) during the period under review.

In 2015-16, global production of corn is estimated to remain at 960 MMT which is around 5% less

as compared to Year 2014-15. Despite ample beginning stocks, the total supplies are estimated to

remain low as compared to last year. However the world corn supply projections for 2016-17 are

quite encouraging. The world corn production is anticipated to increase by 5.31%.

Brazil corn production for 2015-16 is lowered 7.5 MMT. Argentina corn production for 2015-16 is

raised 1.0 MMT based on harvest data reported to date. Global 2016-17 coarse grain consumption

is lowered 3.3 MMT mainly due to reduction in corn feeding, mostly reflecting for the United States,

Brazil, China, EU, South Korea, and Indonesia.

EU corn imports are lowered for 2015-16 and 2016-17 with greater wheat and barley feeding.

Brazil corn exports are lowered for 2015-16 and 2016-17, down 4.0 MMT and 1.0 MMT,

respectively. Global 2016-17 corn ending stocks are projected 3.3 MMT higher mostly on a 2.1-

million-tonnes increase for China. Outside of China, corn stocks are 1.2 MMT higher with larger

stocks for the United States and Indonesia more than offsetting reductions for Brazil, Japan, and

Canada.

(Source: USDA)

Monthly Commodities Report 23 Monday, 02 August 2016

Wheat

Introduction

In India, wheat is the second most important food crop after rice. Wheat grain is a staple food used

to make flour for steamed breads, biscuits, cookies, cakes, breakfast cereal, pasta, noodles, and

for fermentation to make beer, other alcoholic beverages or biofuel. The principal parts of wheat

flour are gluten and starch. The by-products of milling whole grain are bran and germ. The whole

grain is a concentrated source of vitamins, minerals, and protein, while the refined grain is mostly

starch. Wheat starch is an important commercial product of wheat, but second in economic value

to wheat gluten.

Cultivation Pattern

Wheat is a major Rabi crop in India. Sowing takes place between October and November. The

maturity period ranges from 110-140 days depending on the variety and location. Harvesting takes

place between April and May.

State wise Production

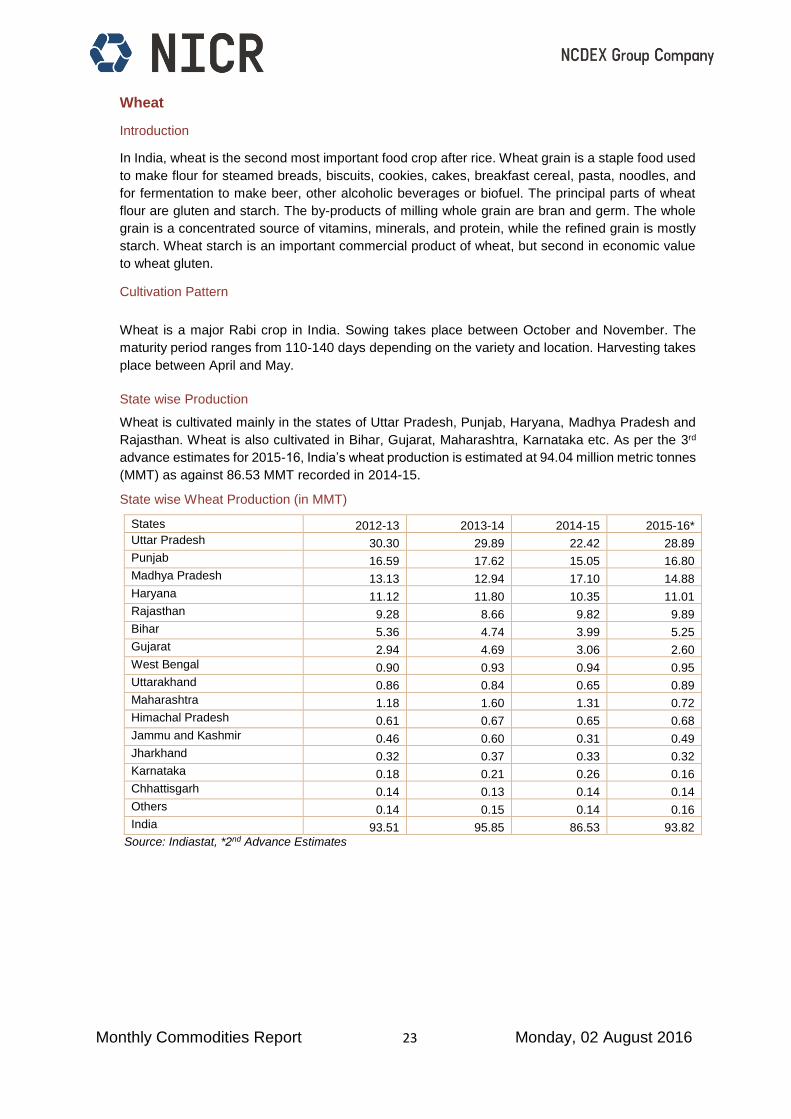

Wheat is cultivated mainly in the states of Uttar Pradesh, Punjab, Haryana, Madhya Pradesh and

Rajasthan. Wheat is also cultivated in Bihar, Gujarat, Maharashtra, Karnataka etc. As per the 3rd

advance estimates for 2015-16, India’s wheat production is estimated at 94.04 million metric tonnes

(MMT) as against 86.53 MMT recorded in 2014-15.

State wise Wheat Production (in MMT)

States 2012-13 2013-14 2014-15 2015-16*

Uttar Pradesh 30.30 29.89 22.42 28.89

Punjab 16.59 17.62 15.05 16.80

Madhya Pradesh 13.13 12.94 17.10 14.88

Haryana 11.12 11.80 10.35 11.01

Rajasthan 9.28 8.66 9.82 9.89

Bihar 5.36 4.74 3.99 5.25

Gujarat 2.94 4.69 3.06 2.60

West Bengal 0.90 0.93 0.94 0.95

Uttarakhand 0.86 0.84 0.65 0.89

Maharashtra 1.18 1.60 1.31 0.72

Himachal Pradesh 0.61 0.67 0.65 0.68

Jammu and Kashmir 0.46 0.60 0.31 0.49

Jharkhand 0.32 0.37 0.33 0.32

Karnataka 0.18 0.21 0.26 0.16

Chhattisgarh 0.14 0.13 0.14 0.14

Others 0.14 0.15 0.14 0.16

India 93.51 95.85 86.53 93.82

Source: Indiastat, *2nd Advance Estimates

Monthly Commodities Report 24 Monday, 02 August 2016

Trend in Wheat Average Monthly Prices in important Producing States (Rs/qtl)

State *Jul-16 Jun-16 Jul-15 Change

(Over Previous Month)

Change (Over Previous

Year)

Madhya Pradesh 1728 1730 1473 0% 17%

Haryana 1584 1513 1360 5% 16%

Rajasthan 1705 1683 1482 1% 15%

Uttar Pradesh 1628 1588 1440 3% 13%

Punjab 1573 1528 1525 3% 3%

All India Average 1778 1773 1649 0% 8% Source: Agmarknet, July-16 prices are till 25 July, 2016

Trend in Wheat Mandi Arrivals in its Major Producing States in India (Metric Tonnes)

State

2016 2015 Change (over previous

month)

Change (Over Previous

Year) 20 June- 20 July

20 May- 20 June

20 June- 20 July

Uttar Pradesh 312741 550577 413788 -43% -24%

Madhya Pradesh 280171 673587 384530 -58% -27%

Rajasthan 54085 170348 221570 -68% -76%

Gujarat 34007 71091 72212 -52% -53%

Maharashtra 17230 31965 10973 -46% 57%

NCT of Delhi 2226 5839 19398 -62% -89%

All India 741441 1590362 1164965 -53% -36%

Source: Agmarknet

Trend in Wheat Stock in NCDEX approved warehouses (in Metric Tonnes)

WEEK ENDING Wheat

Stock Weekly Change Monthly Change Period

01 May 2016 15605

05 June 2016 21390 37.1% 37% 01 May - 05 June

12 June 2016 21410 0.1%

19 June 2016 21008 -1.9%

26 June 2016 18892 -10.1%

03 July 2016 18902 0.1% -12% 05 June - 03 July

10 July 2016 18941 0.2%

17 July 2016 18639 -1.6%

24 July 2016 15967 -14.3% -16% 03 July - 24 July

May- July 2% 1 May - 24 July

Monthly Commodities Report 25 Monday, 02 August 2016

Progressive procurement of Wheat as on June 30, 2016 (Lakh tonnes)

States 2016-17 2015-16 Change in %

Punjab 106.5 103.5 3%

Haryana 67.2 66.9 0%

Uttar Pradesh 8.0 20.0 -60%

Madhya Pradesh 39.9 72.0 -45%

Rajasthan 7.6 12.7 -40%

Chandigarh 0.1 0.1 -36%

All-India 229.3 275.8 -17% Source: Ministry of Agriculture

Status of Wheat Stocks with Central Pool (in Lakh tonnes)

Months Stock Norms

Stock in Central Pool

Stock as % of Norms

Stock in Central Pool

Stock as % of Norms

2016 2015

Jan 138.0 237.9 172% 251.1 182% Feb 138.0 203.4 147% 220.1 160%

March 138.0 168.7 122% 195.3 141% April 74.6 145.4 195% 172.2 231% May 74.6 314.5 422% 341.3 457% June 74.6 326.4 438% 403.5 541%

July 275.8 301.8 109% 386.8 140% Aug 275.8 367.8 133%

Sep 275.8 344.7 125%

Oct 205.2 324.5 158% Nov 205.2 299.1 146%

Dec 205.2 268.8 131% Source: Food Corporation of India

Indian Trade Policy in Wheat

Export Policy: Export of wheat is free under the extant export policy of Government of India.

Import Policy: Import of seeds is restricted. Whereas, import of wheat for human consumption is

permitted through State Trading Enterprises

Wheat Import Policy of India

HS Code Item Description Import Policy Standard

Duty Bound Duty

Applied Duty

10011100 Durum Wheat: Of seed Quality Restricted 100 100 100%

10011900 Other Durum Wheat Free* 100 100 25%**

10019100 Other: Wheat of Seed Quality Restricted 100 100 25%**

10019910 Other Wheat Free* 100 100 25%**

10019920 Meslin State Trading Enterprises

100 100 100%

Source: MoAFW, Commodity Profile

Note: *Import of Wheat (HS Code 10011900 and 10019910) made free till further order vide DGFT's Notification No. 35 Dated 8 October 2007 ** Import duty on Wheat has been increased from 10% to 25% vide Notification No. 51/2015, Customs dated 19 October 2015 till March 2016. The said 25% duty has been further extended without any time limit vide notification dated 17 June 2016.

Monthly Commodities Report 26 Monday, 02 August 2016

Production during last 3 years

Year Production

(Million MT)

2013-14 95.85

2014-15 86.53

2015-16 (3rd Advance Estimates) 94.04

Average Spot Prices

Financial Year Average Price

(Rs./Quintal) YOY

Price Variation

2013-14 1599

2014-15 1605 0.38%

2015-16 1631 1.62%

2016-17 1719 5.38%

Month-wise Price Volatility

Average Open Interest, Stocks in approved warehouses and deliveries

Year Average

Open Interest (MT) Stocks in approved warehouses (MT)

Deliveries during the year (MT)

2013-14 17383 16444 28560

2014-15 12437 8207 13210

2015-16 15226 49477 63660

2016-17 25941 21008 15601

Stocks = Maximum stocks on the day of expiry during respective financial year

Deliveries = Total deliveries during the respective financial year

Global Supply and Demand Fundamentals

India is the third largest producer and consumer of wheat in the world after European Union and

China. India accounts for about 13% of world’s wheat production in 2014-15. Other major producers

of wheat in the world include Russia, USA, Canada, Pakistan, Ukraine etc. Major exporters of wheat

are European Union, USA, Canada, Russia, Australia, etc. Major importers are Egypt, Indonesia,

Algeria, Iran, Brazil, etc.

Global 2015-16 wheat supplies are raised by 4% primarily on increased beginning stocks and

increase in production. World production is estimated at a record 734.62 MMT. World exports are

raised to 169.23 MMT (+3%). World wheat consumption for 2015-16 is estimated at 705.45 MMT

which is well below the available supplies. Ending stocks are estimated at 244.52 MMT for 2015-

16 which are around 12% higher than the ending stock of the Year 2014-15. For 2016-17 too, the

world supply is expected to stay above the demand.

Month Volatility

Jan-16 2.19%

Feb-16 5.01%

Mar-16 10.67%

April-16 15.26%

May-16 13.20%

June -16 11.41%

July-16 (Till 20 July) 6.00%

Spot Price Volatility during January to July Period 10.41%

Monthly Commodities Report 27 Monday, 02 August 2016

World Wheat Supply & Demand Estimates (in MMT)

Attributes 2014-15 2015-16

(Estimates) 2016-17

(Projections)

Change in 2015-16 over

2014-15

Projected Change in

2016-17 over 2015-16

Beginning Stocks 194.18 217.40 244.52 12% 12%

Production 727.85 734.62 738.51 1% 1%

MY Imports 158.84 167.18 164.20 5% -2%

Total Supply 1080.87 1119.20 1147.23 4% 3%

MY Exports 164.14 169.23 168.43 3% 0%

Total Consumption 699.32 705.45 725.11 1% 3%

Ending Stocks 217.40 244.52 253.70 12% 4%

Source: USDA, as on 25 July 2016,

India is the 3rd largest producer as well as consumer of Wheat. However it is neither a big exporter

nor a big importer of Wheat.

Leading Wheat Producers in World, 2015-16 Leading Wheat Consumers in World, 2015-16

Country Production

(MMT) Country's Share

in World Total

Country Consumption

(MMT)

Country's Share in

World Total

European Union 160.01 22% European Union 128.80 18%

China 130.19 18% China 112.00 16%

India 86.53 12% India 88.64 13%

Russia 61.04 8% Russia 37.00 5%

United States 55.84 8% United States 31.74 4%

Canada 27.60 4% Pakistan 24.40 3%

Ukraine 27.27 4% Egypt 19.20 3%

Pakistan 25.10 3% Turkey 18.00 3%

Australia 24.50 3% Iran 18.00 3%

Turkey 19.50 3% Ukraine 12.50 2%

Other 116.66 16% Other 215.15 30%

World 734.24 100% World 705.43 100%

Leading Wheat Exporters in World, 2015-16 Leading Wheat Importers in World, 2015-16

Country Export (MMT)

Country's Share in World Total

Country Import (MMT)

Country's Share in

World Total

European Union 33.00 20% Egypt 11.50 7%

Russia 24.50 15% Indonesia 9.10 5%

Canada 22.50 13% Algeria 8.10 5%

United States 21.09 13% European Union 6.70 4%

Australia 16.50 10% Brazil 6.00 4%

Ukraine 15.80 9% Japan 5.70 3%

Argentina 9.00 5% Morocco 4.70 3%

Kazakhstan 7.50 4% Thailand 4.50 3%

Turkey 5.50 3% Philippines 4.50 3%

Mexico 1.30 1% Mexico 4.50 3%

Other 11.59 7% Other 100.64 61%

World 168.28 100% World 165.94 100%

Source: USDA, June 2016

Monthly Commodities Report 28 Monday, 02 August 2016

Spot and Futures Price Chart

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Ap

r-11

Jul-

11

Oct-

11

Jan

-12

Ap

r-12

Jul-

12

Oct-

12

Jan

-13

Ap

r-13

Jul-

13

Oct-

13

Jan

-14

Ap

r-14

Jul-

14

Oct-

14

Jan

-15

Ap

r-15

Jul-

15

Oct-

15

Jan

-16

Ap

r-16

Jul-

16

Rs./

Qu

inta

l

Wheat Long Term Price Trend

Spot Price Futures Price

1,600

1,650

1,700

1,750

1,800

1,850

1,900

1,950

20-J

un-1

6

21-J

un-1

6

22-J

un-1

6

23-J

un-1

6

24-J

un-1

6

25-J

un-1

6

26-J

un-1

6

27-J

un-1

6

28-J

un-1

6

29-J

un-1

6

30-J

un-1

6

01-J

ul-1

6

02-J

ul-1

6

03-J

ul-1

6

04-J

ul-1

6

05-J

ul-1

6

06-J

ul-1

6

07-J

ul-1

6

08-J

ul-1

6

09-J

ul-1

6

10-J

ul-1

6

11-J

ul-1

6

12-J

ul-1

6

13-J

ul-1

6

14-J

ul-1

6

15-J

ul-1

6

16-J

ul-1

6

17-J

ul-1

6

18-J

ul-1

6

19-J

ul-1

6

20-J

ul-1

6

Rs./

Qu

inta

l

Wheat Price Trend : 20 June - 20 July, 2016

Spot Price Jul-2016 Aug-2016 Sep-2016 Oct-2016 Nov-2016

Monthly Commodities Report 29 Monday, 02 August 2016

Markets and Trade

Wheat spot as well as near month futures prices fell by around 2 and 4 % respectively during the

period under review (20 June-20 July 2016). Wheat prices at CBOT fell by 12.68%.

Baring Madhya Pradesh, all other major wheat producing states like Rajasthan, Uttar Pradesh,

Punjab and Haryana witnessed slight increase in Wheat prices. But the wheat prices are higher

by more than 10% in most of the major wheat producing states. In Madhya Pradesh, the wheat

prices are higher by 17% compared to corresponding period last year. The prevailing mandi prices

are higher than MSP in these states.

Mandi Arrivals have declined by more than 50% in all these states as compared to previous

month, however the arrivals are around 30% low at all India basis compared to corresponding

period last year.

There has been continuous declines in the stock in the NCDEX approved warehouses in the past

two months due to withdrawal by the market participants reflecting that demand has remained

firm during previous months.

The Wheat stock in the July month with the central pool is about 109% of the prescribed norms for

the July-September quarter. However during 2015-16, it was about 140% of the prescribed norms.

It is to be noted that market get signals from the stock availability with the government and its time

to time disposal in the open market. This year Indian government missed the set wheat

procurement targets for 2016-17. The Wheat stock in the Central Pool as on 1 July 2016 was 301.8

lakh tonnes as against the stocking norms for Central Pool (Buffer Norms) of 275.8 lakh tonnes for

the quarter July-September. The annual requirement under National Food Security Act (NFSA) is

around 240 lakh tonnes.

Wheat procurement by the government agencies, has been down by 17% to around 229.3 lakh

tonnes during April- June 30, 2016 over the corresponding period of the last year. It must be noted

that government set the target of 280 lakh tonnes for wheat procurement for the wheat marketing

season 2016-17. The contribution of states like UP, Rajasthan and Madhya Pradesh in

Government procurement has reduced drastically in the range of 40-60% compared to last year’s

contribution.

The private agencies are also believed to procure about 60-65 lakh tonnes of wheat in Indian.

Production has fallen during 2015-16. Market estimates nearly 85 million metric tonnes (MMT)

however India government estimates wheat production to remain at 94.04 MMT as against 86.53

MMT recorded in 2014-15.

Unchanged import duty structure too has supported prices. Government has extended a 25% duty

on wheat imports in the month of June without specifying any time line to help curb cheap

shipments into the country in a surplus year. The Government in March 2016 had extended the

25% import duty on wheat by three months to June 30. The basic customs duty had been raised

to 25% from 10% in October 2015.

India may import the most wheat in a decade as output declines in the world’s second biggest

producer. Imports may total 5 million metric tonnes in 2016-17, the most since 200607, according

to the median estimate of seven traders surveyed by Bloomberg. Declining supply is prompting

flour millers in non-wheat growing states to buy grain from Food Corp. of India and some

processors have contracted to import from Australia and France. As much as 1 million metric

tonnes from the two countries have been contracted for import, sources said (Source: Live Mint,

21 June 2016)

Monthly Commodities Report 30 Monday, 02 August 2016

International

International wheat prices fell significantly by 12.68% during the period under review due to ample

supplies and better production outlook.

As per the Wheat Outlook report, USDA published in July 2016

The Global 2015-16 wheat supplies are raised by 4% primarily on increased beginning stocks and

increase in production. World production is estimated at a record 734.62 MMT. World exports are

raised to 169.23 MMT (+3%). World wheat consumption for 2015-16 is estimated at 705.45 MMT

which is well below the available supplies. Ending stocks are estimated at 244.52 MMT for 2015-

16 which are around 12% higher than the ending stock of the Year 2014-15. For 2016-17 too, the

world supply is expected to stay above the demand.

Projected 2016-17 world wheat production beats last year’s record this month. Increases for

exporting countries, coupled with some declines for importers, boost world wheat trade prospects.

Lower wheat quality and competitive prices encourage wheat feeding and raise projected global

consumption. Ending foreign stocks decline while U.S. stocks are projected substantially-higher.

Wheat growing conditions are almost perfect, with abundant precipitation boosting yields in most

countries across the globe, while temperatures are often beneficially cooler than usual.

On the European continent, higher wheat output is projected for Russia and Ukraine and the

countries of the south-eastern part of the continental European Union (EU). Wheat output in

Serbia, which is not part of the EU and borders it in the southeast, is expected to harvest a record-

high crop.

In North America, both the United States and Canada are benefitting from very good growing

conditions.

In the Southern Hemisphere, timely rains in Australia, where winter wheat planting has just been

completed, boosted yield prospects,

Higher wheat area in Argentina, where planting is still underway, is expected to underpin higher

output.

Wheat quality is also expected to be low this year in China. Strong rains in April and May in many

key producing regions (Anhui, Henan, Hubei, and Jiangsu,) during the crop grain fill and heavy

rains in June during the harvest reduced wheat quality in the country, expanding the share of feed

quality in wheat output. The wheat damaged by fusarium fungus, mold, or germination is not

suitable for milling purposes for human consumption, and will have to be sold at a big discount to

feed mills.

The combined 2016-17 output by the major foreign wheat exporters—EU, Canada, Australia,

Argentina, Russia, and Ukraine—is projected to increase by 2.5 million tonnes this month and by

4.4 million tonnes compared to last year. This will maintain ample exportable supplies buttressed

by 1.5-million-ton larger beginning stocks.

Australian wheat production is forecast to rise by 5 per cent in 2016–17 to 25.4 million tonnes,

mainly as a result of an expected increase in yields. The area planted to wheat is forecast to decline

by almost 1 per cent in 2016–17, reflecting higher expected returns from growing other crops such

as canola, oats and some pulses. The previous estimate in March was 24.5 million tonnes.

(Source: Australian Bureau of Agricultural and Resource Economics and Sciences -ABARES)

Monthly Commodities Report 31 Monday, 02 August 2016

Barley

Introduction

Barley is an annual cereal crop consumed as a major food and feed. Basically a grass crop, it

belongs to the family of Poaceae, and is considered to be the fourth most-important crop in the

world after wheat, maize and rice. This crop has been commercially grown for 10,000 years now.

The crop originated in the Middle East and in the lands of modern-day Ethiopia. As a wild grass it

was used as feed for animals during early periods, but with the progress of civilization it was

domesticated. Currently, it is used as food, feed and for the preparation of alcoholic beverages.

Seasonality

Barley is planted as a winter or summer crop in different countries. In the colder regions, barley is

planted in April or May as a summer crop; in the warmer regions, barley is planted between mid-

September to November. In India, it is cultivated as a Rabi crop. Sowing normally takes place

between October and December and harvested from March to April. The market arrivals start from

March onwards. In India, the crop duration of barley is around 120-150 days.

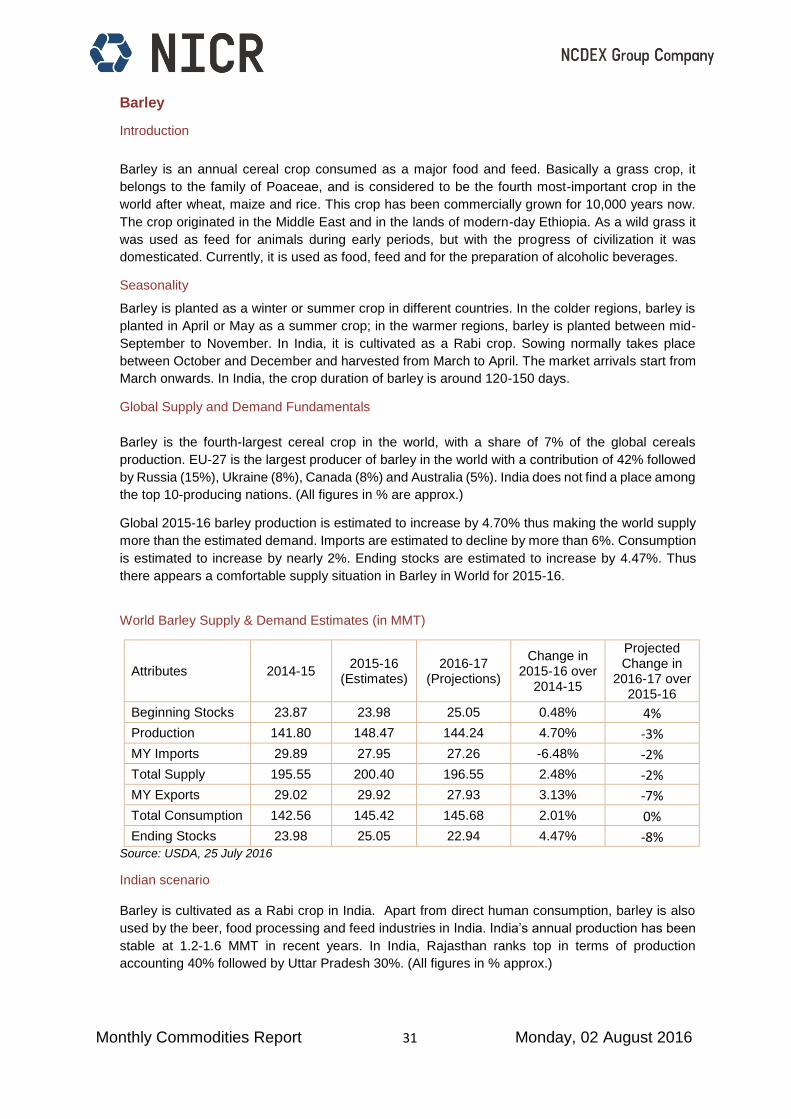

Global Supply and Demand Fundamentals

Barley is the fourth-largest cereal crop in the world, with a share of 7% of the global cereals

production. EU-27 is the largest producer of barley in the world with a contribution of 42% followed

by Russia (15%), Ukraine (8%), Canada (8%) and Australia (5%). India does not find a place among

the top 10-producing nations. (All figures in % are approx.)

Global 2015-16 barley production is estimated to increase by 4.70% thus making the world supply

more than the estimated demand. Imports are estimated to decline by more than 6%. Consumption

is estimated to increase by nearly 2%. Ending stocks are estimated to increase by 4.47%. Thus

there appears a comfortable supply situation in Barley in World for 2015-16.

World Barley Supply & Demand Estimates (in MMT)

Attributes 2014-15 2015-16

(Estimates) 2016-17

(Projections)

Change in 2015-16 over

2014-15

Projected Change in

2016-17 over 2015-16

Beginning Stocks 23.87 23.98 25.05 0.48% 4%

Production 141.80 148.47 144.24 4.70% -3%

MY Imports 29.89 27.95 27.26 -6.48% -2%

Total Supply 195.55 200.40 196.55 2.48% -2%

MY Exports 29.02 29.92 27.93 3.13% -7%

Total Consumption 142.56 145.42 145.68 2.01% 0%

Ending Stocks 23.98 25.05 22.94 4.47% -8% Source: USDA, 25 July 2016

Indian scenario

Barley is cultivated as a Rabi crop in India. Apart from direct human consumption, barley is also

used by the beer, food processing and feed industries in India. India’s annual production has been

stable at 1.2-1.6 MMT in recent years. In India, Rajasthan ranks top in terms of production

accounting 40% followed by Uttar Pradesh 30%. (All figures in % approx.)

Monthly Commodities Report 32 Monday, 02 August 2016

State wise Production (in MMT)

States 2012-13 2013-14 2014-15

Rajasthan 0.85 0.94 0.80

Uttar Pradesh 0.45 0.45 0.46

Madhya Pradesh 0.14 0.15 0.21

Haryana 0.17 0.15 0.14

Punjab 0.05 0.05 0.06

Uttarakhand 0.03 0.03 0.03

Himachal Pradesh 0.04 0.03 0.03

Bihar 0.02 0.01 0.01

Others 0.01 0.02 0.01

India 1.75 1.83 1.77#

Source: Indiastat, #As per Indian government 3rd advance estimates the production for 2014-15 is 1.61 MMT.

Trend in Barley Mandi Arrivals in its Major Producing States in India (Metric Tonnes)

State

2016 2015 Change (over

previous month)

Change (Over

Previous Year)

20 June-20 July 20 May-20 June 20 June-20 July

Uttar Pradesh 6601 9648 9687 -32% -32%

Madhya Pradesh 2311 2184 2137 6% 8%

Rajasthan 1119 4860 9587 -77% -88%

All India 10318 17289 22728 -40% -55%

Source: Agmarknet

Trend in Barley Average Monthly Prices in Selected States (Rs/qtl)

State *Jul-16 Jun-16 Jul-15 Change

(Over Previous Month)

Change (Over Previous

Year)

Uttar Pradesh 1607 1582 1324 2% 21%

Rajasthan 1555 1544 1117 1% 39%

Madhya Pradesh 1519 1518 1158 0% 31%

All India 1513 1566 1196 -3% 26%

Source: Agmarknet, *July 2016 Average price is Till 26 July 2016

Monthly Commodities Report 33 Monday, 02 August 2016

Spot and Futures Price Chart

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Ap

r-11

Jul-

11

Oct-

11

Jan

-12

Ap

r-12

Jul-

12

Oct-

12

Jan

-13

Ap

r-13

Jul-

13

Oct-

13

Jan

-14

Ap

r-14

Jul-

14

Oct-

14

Jan

-15

Ap

r-15

Jul-

15

Oct-

15

Jan

-16

Ap

r-16

Jul-

16

Rs./

Qu

inta

lBarley Long Term Price Trend

Spot Price Futures Price

1,400

1,450

1,500

1,550

1,600

1,650

1,700

1,750

20-J

un-1

6

21-J

un-1

6

22-J

un-1

6

23-J

un-1

6

24-J

un-1

6

25-J

un-1

6

26-J

un-1

6

27-J

un-1

6

28-J

un-1

6

29-J

un-1

6

30-J

un-1

6

01-J

ul-1

6

02-J

ul-1

6

03-J

ul-1

6

04-J

ul-1

6

05-J

ul-1

6

06-J

ul-1

6

07-J

ul-1

6

08-J

ul-1

6

09-J

ul-1

6

10-J

ul-1

6

11-J

ul-1

6

12-J

ul-1

6

13-J

ul-1

6

14-J

ul-1

6

15-J

ul-1

6

16-J

ul-1

6

17-J

ul-1

6

18-J

ul-1

6

19-J

ul-1

6

20-J

ul-1

6

Rs./

Qu

inta

l

Barley Price Trend : 20 June - 20 July, 2016

Spot Price Jul-2016 Aug-2016 Sep-2016 Oct-2016 Nov-2016

Monthly Commodities Report 34 Monday, 02 August 2016

Production during last 3 years

Year Production

(Million MT)

2013-14 1.83

2014-15 1.61

2015-16 (3rd Advance Estimates) 1.62

Average Spot Prices

Financial Year Average prices

(Rs/Quintal) YOY

Price Variation

2013-14 1344

2014-15 1448 7.74%

2015-16 1356 -6.53%

2016-17 1600 17.99%

Month-wise Price Volatility

Average Open Interest, Stocks in approved warehouses and deliveries

Year Open Interest

(MT)

Stocks in approved warehouses

(MT)

Deliveries during the year

(MT)

2013-14 11497 30166 41280

2014-15 12248 10514 13220

2015-16 20897 15988 36690

2016-17 18267 12545 10190

Stocks = Maximum stocks on the day of expiry during respective financial year

Deliveries = Total deliveries during the respective financial year

Month Volatility

Jan-16 10.44%

Feb-16 10.52%

Mar-16 14.92%

April-16 10.93%

May-16 7.53%

June -16 11.28%

July-16 (Till 20 July) 6.59%

Spot Price Volatility during January to July Period 11.33%

Monthly Commodities Report 35 Monday, 02 August 2016

Markets and Trade

A very narrow range bound trade is observed in Barley prices during the period under review.

No significant change was observed in the spot and futures prices during 20 June-20 July

period.

The demand in the physical market is steady. Although mandi arrivals have declined

substantially but could not affect the prices due to steady demand. Further there is talk in the

market that the prices of imported Barley is almost same to that of physical market prices. Due

to which market prices are unable to go up.

As per the 3rd advance estimate for 2015-16 released by Ministry of Agriculture on May 09,

2016 Barley production is estimated to be around 1.62 MMT. Production stood at 1.61 MMT in

2014-15.

Winter Barley all over Ukraine is at the stage of complete ripeness. Crop condition is mostly

good. Rains and strong winds caused some crops lodging in the fields, which impeded field

works and further works with harvested grain. Ukraine Barley prices have also seen decline

both in export and domestic markets due to new crop good supply prospects. The average

grain productivity of Ukraine is 11% higher than last year.

India is likely to import a record high of 125,000 tonnes of barley in 2016-17 (April-March) from

Argentina, Australia and France due to a smaller domestic crop, industry officials said. India

imports around 10,000 tonnes of barley every year, but the purchase is seen nearly 12.5 fold

higher this year. The imports would be mainly carried out by the malt industry, which is facing

a shortage of the commodity in domestic markets. Two shipments of 50,000 tonnes each from

Australia are expected to reach Indian shores in two months. The deals for barley imports are

struck at $195 per tonne ( Rs. 13,217) free on board, way cheaper than the domestic prices

of Rs. 15,000-16,000 a tonne. (Source: The Hindu Business Line, 30 June 2016)

World 2015-16 barley production is estimated to increase by 4.70% thus making the world

supply more than the estimated demand. Imports are estimated to decline by more than 6%.

Consumption is estimated to increase by nearly 2%. Ending stocks are estimated to increase

by 4.47%. Thus there appears a comfortable supply situation in Barley in World for 2015-16.

The NCDEX has revised value at risk (VaR)-based initial margins for select commodities

including Barley. VaR-based initial margins are part of the exchange's risk management

framework. The exchange has also decided to have margin period of risk (MPOR) of two days

as a measure of underlying liquidity. This means the exchange will cover margins required for

two days and that will be based on liquidity. Commodities that are part of the revised margin

are sensitive commodities, such as sugar and chana or those having limited production or

marketable surplus such as barley, chilli, coriander, guar, jeera, turmeric, etc. These changes

are with effect from July 29, 2016.

Monthly Commodities Report 36 Monday, 02 August 2016

Pulses

Chana

Introduction

Chana or chickpea is an important pulse crop of India and is a rich source of protein and used as edible

seed and also for making flour. It is highly nutritious and ranks third amongst important legumes after

dry bean and peas. The two main types of Chana are desi and kabuli (also known as dollar Chana).

Among the total Chana production in the world, desi type contributes to 80% while rest is of kabuli type.

India is the largest producer of Chana contributing around 70% to the total global production. Desi

Chana is mainly grown in India and they are brown split peas and are relatively small in size with a

relatively thick seed coat while kabuli Chana are creamy whitish in color and bigger in size compare to

desi Chana with thin seed coat.

Cultivation Pattern