Embed Size (px)

Citation preview

Monopolistic Competition and Oligopoly

Chapter 11

McGraw-Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Objectives

• Characteristics of monopolistic competition

• Normal profit in the long run• Characteristics of oligopoly• The oligopolist’s kinked demand

curve• Collusion among oligopolists• The effects of advertising

11-2

Monopolistic Competition• Monopolistic competition is

characterized by a relatively large number of sellers who offer similar but not identical products–Each firm has a small

percentage of the total market–Collusion (working together to

establish a price every firm agrees upon) is nearly impossible with so many firms

–Firms act independently, the actions of one firm are ignored by the other firms in the industry

11-3

Monopolistic Competition

• Product differentiation and other types of nonprice competition give the individual firm some degree of monopoly power–Product differentiation may be physical–There may be special services and

conditions that go along with the product

–Brand names and packaging may be different

–Product differentiation allow producers to have some control over the prices of their products

Monopolistic Competition

• The monopolistic firm’s demand curve is highly elastic, but not perfectly so–This relatively high elasticity means

that increases in price result in a significant loss of customers

–The seller has many rivals producing close substitutes

– It is less elastic than in pure competition because the seller’s product is differentiated from its rivals, so that the firm has some control over price

Monopolistic Competition

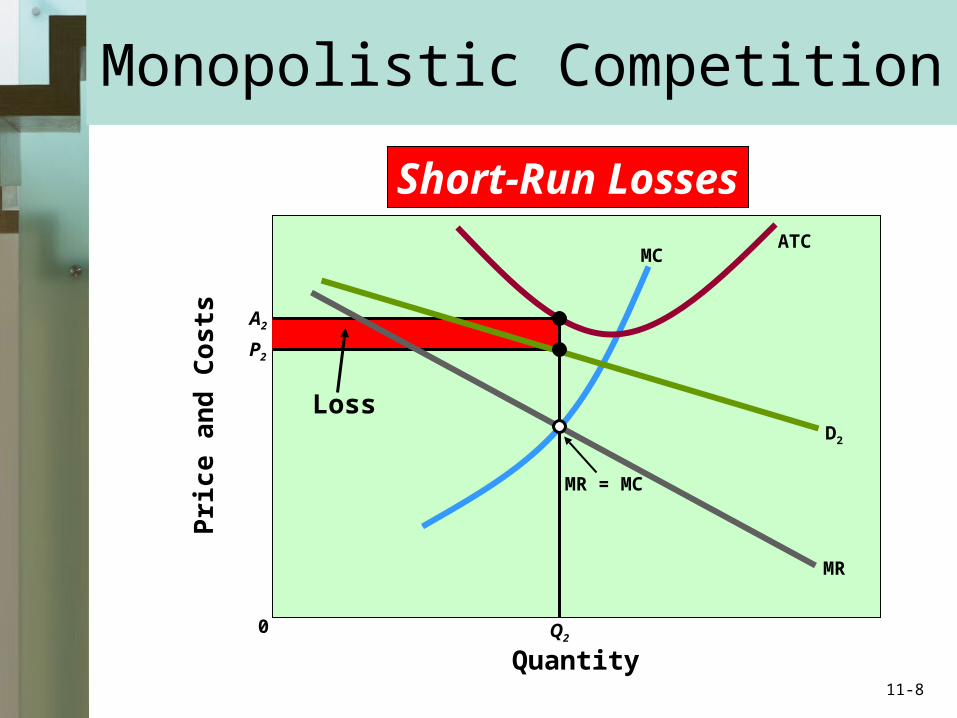

• In the short-run situation, the firm will maximize profits or minimizes losses by producing where MC = MR, as in both pure competition and monopoly

Short-Run Profits

Quantity

Pri

ce

an

d C

os

ts

MR = MC

MC

MR

D1

ATC

EconomicProfit

Q1

A1

P1

0

Monopolistic Competition

11-7

Short-Run Losses

Quantity

Pri

ce

an

d C

os

ts

MR = MC

MC

MR

D2

ATC

Loss

Q2

A2

P2

0

Monopolistic Competition

11-8

Long-run Situation

• In the long-run situation, the firm will tend to earn a normal profit only, that it, it will break even– Firms can enter the industry easily and will when an

economic profit can be made– As firms enter the industry, this decreases the

demand curve facing an individual firm as buyers shift some demand to new firms

– The demand curve will shift until the firm just breaks even

– If the demand shifts below the break-even point, some firms will leave the industry in the long run

– When firms leave the industry, the demand curve facing each firm will be raised (fewer substitutes for buyers) and the break-even point (normal profits) will be reached

Long-Run Equilibrium

Quantity

Pri

ce

an

d C

os

ts

MR = MC

MC

MR

D3

ATC

Q3

P3= A3

0

Monopolistic Competition

11-10

Exceptions to long-run normal profit scenario

• The products of some firms may become so differentiated that they are not easily duplicated by rivals– These firms may enjoy economic profits in

the long-run

• Some restrictions to entry in the industry such as financial barriers may exist, especially for small firms

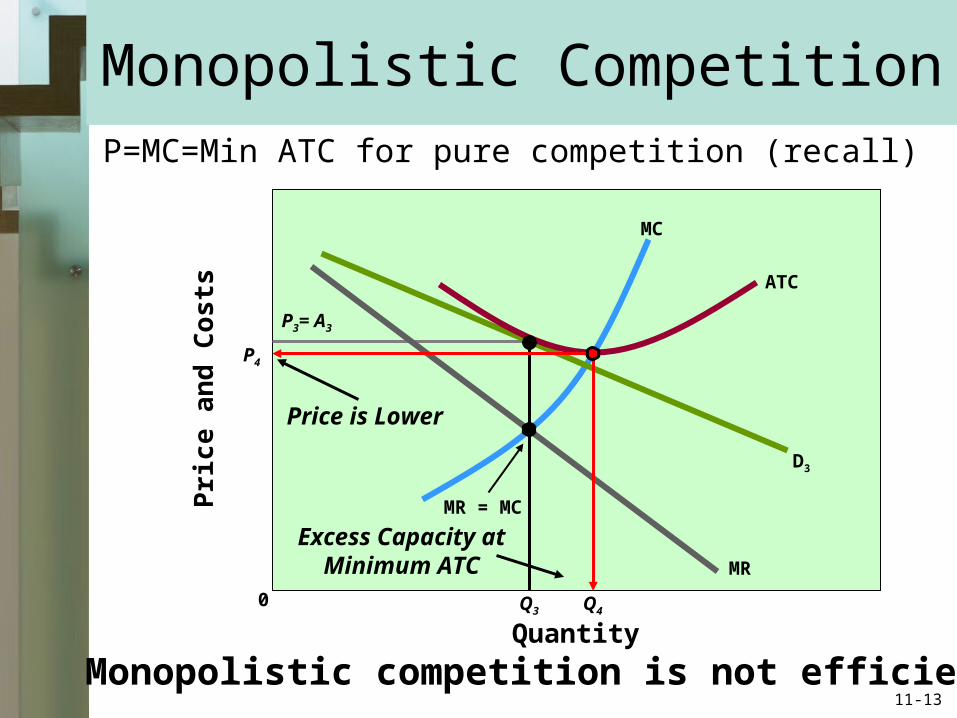

Economics Efficiency

• Monopolistic firms do not have allocative or productive efficiency– Allocative efficiency occurs when price =

marginal cost; i.e., the right amount of resources are allocated to the product

– Productive efficiency occurs when price = minimum average total cost; where production occurs using the least-cost combination of resources

– The gap between price and marginal cost for each firm creates a loss in efficiency

Quantity

Pri

ce

an

d C

os

ts

MR = MC

MC

MR

D3

ATC

Q30

P3= A3

P=MC=Min ATC for pure competition (recall)

P4

Q4

Price is Lower

Excess Capacity atMinimum ATC

Monopolistic competition is not efficient

Monopolistic Competition

11-13

Oligopoly• Oligopoly exists where a few

large firms that produce either a homogeneous (almost identical) or differentiated product dominate the market

• There are few enough firms in the industry that firms are mutually interdependent

• Because there are so few firms in the industry, oligopolists have considerabe control over their prices

11-14

–Some oligopolistic industries produce standardized products such as steel and cement, while others produce differentiated products such as automobiles

–They must consider the reactions of their business rivals when ever they change prices, output, or advertise.

Oligopoly

• There are barriers to entry by new firms– Economies of scale may exist due to technology

and market share– Capital investment requirements may be very

large– Other barriers may exist such as patents, control

of raw materials, retaliatory pricing, large advertising budgets, and brand loyality

• While some firms have become oligopolists through growth of the business, others have acquired the status through mergers and acquistions

Three Oligopoly Models

• Because of the diversity in oligopolistic firms, there are three models used to explain the price-output behavior–Kinked-demand curve–Collusive pricing–Price leadership

11-17

The kinked-demand Model

• Assumes firms do not act together in a collusive manner

• Each firm believes the other firm will match any price cuts– Because of that, they do not want to lower prices

since total revenue will fall when demand is inelastic

• However, they do not believe any other firm would raise prices if they did– With a price raise, the demand would be elastic;

revenue would decrease

• This analysis is one explanation of the fact that prices tend to be inflexible in oligopolistic industries

The kinked-demand Model

• Movement of the demand curve will depend upon whether there is a price cut or a price increase involved, and the response of the other rival firms

• If firm A cuts their price, its sales increase only a little because business rivals will also cut their price to prevent firm A from gaining an advantage over them– The small increase in sales that firm A receives is

from other firms in the industry– Firm A probably wouldn’t raise their prices, and

lose market share

The kinked-demand Model

• Other firms might choose to ignore the price changes by firm A– If firm A lowers price and its rivals do not, firm

A will gain significantly at the expense of its rivals

– If the firm raises its price, and its rivals do not, firm A will lose customers to its rivals because it will be undersold

– However, even if firm A raises its price, it will not be totally priced out of the market because of product loyalty.

Pri

ce

Pri

ce a

nd

Co

sts

Quantity Quantity

0 0

P0

MR2

D2

D1

MR1

e

f

g

Rivals IgnorePrice Increase

Rivals MatchPrice Decrease

Q0

Competitor and rivals strategize versus each otherConsumers effectively have 2 partial demand curves

and each part has its own marginal revenue part

MR2

D2

D1

MR1Q0

MC1

MC2

P0

Resulting in a kinked-demand curve to the consumer – price and output

are optimized at the kink

e

f

g

Kinked-Demand Curve

11-21

Collusions

• Collusion between firms reduces uncertainty, increases profits, and may prohibit the entry of new rivals

• A cartel is a group of producers that sign formal agreements as to how each may produce and charge (such as OPEC)– Assuming each member had identical cost,

demand, and marginal-revenue data, the resulting cartel would behave economically as if they were made up of a single monopoly

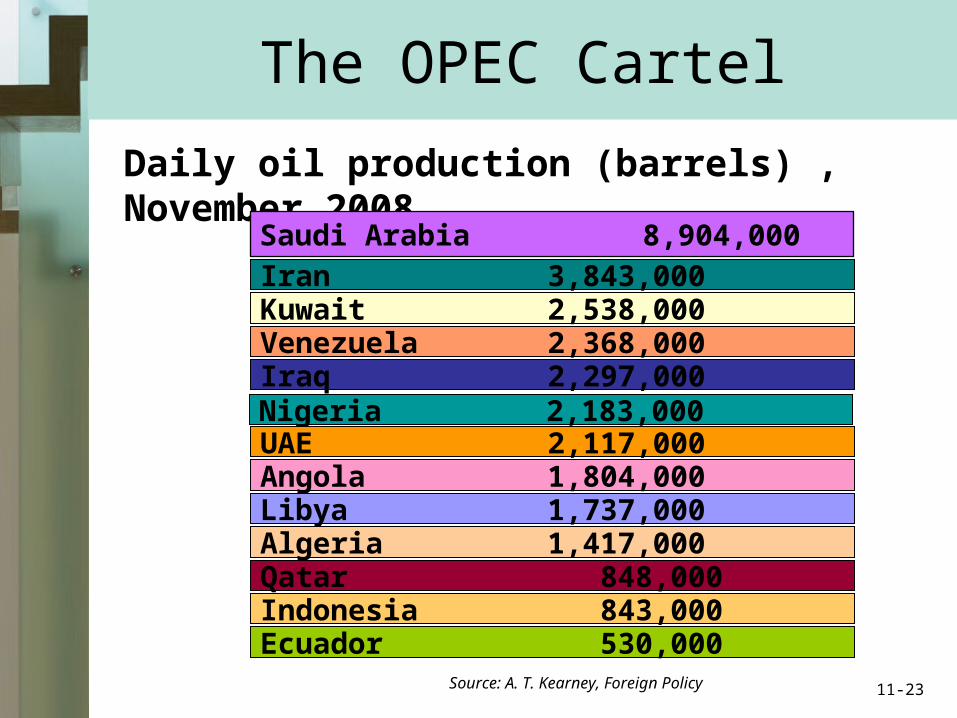

The OPEC Cartel

Source: A. T. Kearney, Foreign Policy

Iran 3,843,000Kuwait 2,538,000Venezuela 2,368,000Iraq 2,297,000Nigeria 2,183,000UAE 2,117,000Angola 1,804,000Libya 1,737,000Algeria 1,417,000Qatar 848,000Indonesia 843,000Ecuador 530,000

Daily oil production (barrels) , November 2008

Saudi Arabia 8,904,000

11-23

Cartels and Other Collusion• Covert collusion – not formalized

– Tacit understandings• Obstacles to collusion

– Demand and cost differences among firms

– Too many firms in the industry– An incentive to cheat– Recession with decreasing demand

and increasing average total costs– Potential entry when profits become

too high– Legal obstacles: antitrust law that

prohibit collusion

11-24

Price Leadership Model

• Price leadership is a type of gentleman’s agreement to coordinate their prices legally–No formal agreements–One firm, usually the largest,

changes the price first and then the other firms follow

11-25

Price Leadership Model

Several price leadership tactics are practiced by the leading firm

• Prices are changed only when cost and demand conditions have been significantly altered industry-wide

• Publicizing the “need to raise prices” through publications and speeches puts other firms on alert

• The new price may be below the short-run profit-maximizing level (an economic loss) to discourage new firms from entering the industry

• Price leadership in oligopoly occasionally breaks down and a price war may result

Oligopoly and AdvertisingThe Largest U.S. Advertisers, 2006

CompanyAdvertising Spending

Millions of $

Proctor and GambleAT&TGeneral MotorsTime WarnerVerizonFord MotorGlaxoSmithKlineWalt DisneyJohnson & JohnsonUnilever

$4898334532963089282225772444232022912098

Source: Advertising Age11-27

World’s Top 10 Brand Names, 2007

Source: Interbrand

Coca-ColaMicrosoftIBMGeneral ElectricNokiaToyotaIntelMcDonald’sDisneyMercedes-Benz

Oligopoly and Advertising

11-28

Oligopoly and Efficiency

• Not productively efficient• Not allocatively efficient• Tendency to share the monopoly

profit

11-29

Key Terms

• monopolistic competition

• product differentiation• nonprice competition• four-firm concentration

ratio• Herfindahl index• excess capacity• oligopoly• homogeneous

oligopoly• differentiated oligopoly

• strategic behavior• mutual interdependence• interindustry

competition• import competition• game theory• collusion• kinked-demand curve• price war• cartel• price leadership

11-30

Next Chapter Preview…

Technology, R&D,And Efficiency

11-31