Embed Size (px)

Citation preview

MIE 754 - Class #6 MIE 754 - Class #6 Manufacturing & Engineering Manufacturing & Engineering

EconomicsEconomics

• Concerns and QuestionsConcerns and Questions• Quick Recap of Previous ClassQuick Recap of Previous Class• Today’s Focus:Today’s Focus:

– Chap 4 Finish Rate of Return Chap 4 Finish Rate of Return MethodsMethods

– Chap 4, Appendix 4B - Payback Chap 4, Appendix 4B - Payback Period Method and LiquidityPeriod Method and Liquidity

– Chapter 6 - Depreciation MethodsChapter 6 - Depreciation Methods

Concerns and Questions?Concerns and Questions?

Quick Recap of Previous ClassQuick Recap of Previous Class

Useful Life versus Study PeriodUseful Life versus Study Period Internal Rate of ReturnInternal Rate of Return

• Single AlternativeSingle Alternative

• Comparing AlternativesComparing Alternatives

Comparing Mutually Exclusive Comparing Mutually Exclusive Alternatives (MEAs) with RR MethodsAlternatives (MEAs) with RR Methods

Fundamental Purpose of Capital Fundamental Purpose of Capital Investment:Investment:• Obtain Obtain at leastat least the MARR for every dollar the MARR for every dollar

invested.invested.

Basic Rule:Basic Rule:• Spend the least amount of capital possible Spend the least amount of capital possible

unlessunless the extra capital can be justified by the the extra capital can be justified by the extra savings or benefits.extra savings or benefits.(i.e., any increment of capital spent above the (i.e., any increment of capital spent above the minimum must be able to pay its own way) minimum must be able to pay its own way)

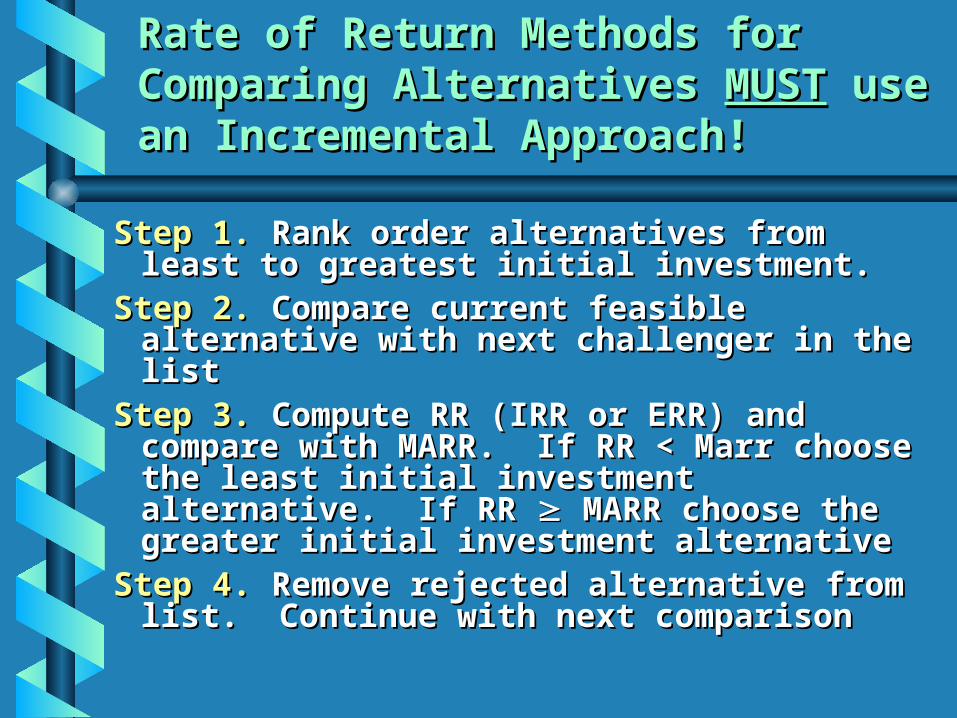

Rate of Return Methods for Comparing Rate of Return Methods for Comparing Alternatives Alternatives MUSTMUST use an Incremental use an Incremental Approach!Approach!

Step 1.Step 1. Rank order alternatives from least Rank order alternatives from least to greatest initial investment.to greatest initial investment.

Step 2.Step 2. Compare current feasible Compare current feasible alternative with next challenger in the alternative with next challenger in the listlist

Step 3.Step 3. Compute RR (IRR or ERR) and Compute RR (IRR or ERR) and compare with MARR. If RR < Marr compare with MARR. If RR < Marr choose the least initial investment choose the least initial investment alternative. If RR alternative. If RR MARR choose the MARR choose the greater initial investment alternativegreater initial investment alternative

Step 4.Step 4. Remove rejected alternative from Remove rejected alternative from list. Continue with next comparisonlist. Continue with next comparison

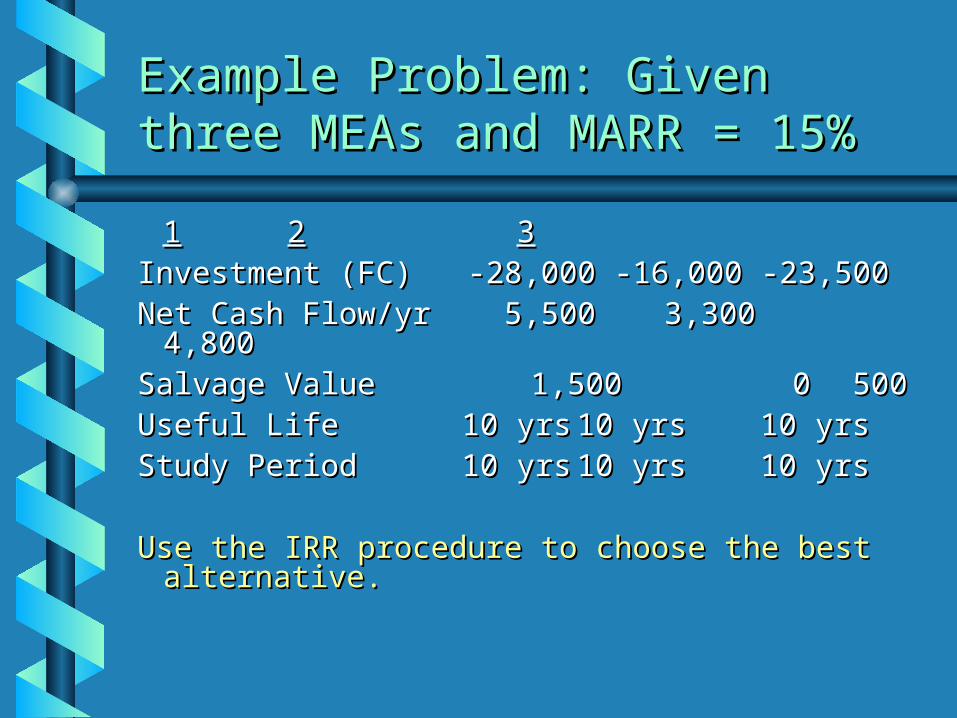

Example Problem: Example Problem: Given three Given three MEAs and MARR = 15%MEAs and MARR = 15%

11 22 33Investment (FC) -28,000 -16,000 -23,500Investment (FC) -28,000 -16,000 -23,500Net Cash Flow/yr 5,500Net Cash Flow/yr 5,500 3,300 4,800 3,300 4,800Salvage ValueSalvage Value 1,500 1,500 0 0 500500Useful LifeUseful Life 10 yrs 10 yrs 10 yrs 10 yrs10 yrs 10 yrsStudy PeriodStudy Period 10 yrs 10 yrs 10 yrs 10 yrs10 yrs 10 yrs

Use the IRR procedure to choose the best Use the IRR procedure to choose the best alternative.alternative.

Example Problem Cont.Example Problem Cont.

Step 1.Step 1. DN -> 2 -> 3 -> 1 DN -> 2 -> 3 -> 1Step 2.Step 2. Compare DN -> 2 Compare DN -> 2

cash flowscash flows InvestmentInvestment -16,000 - 0 = -16,000-16,000 - 0 = -16,000 Annual ReceiptsAnnual Receipts 3,300 - 0 = 3,300 3,300 - 0 = 3,300 Salvage ValueSalvage Value 0 - 0 = 0 - 0 = 0 0

Compute Compute IRR IRRDN->2DN->2

PW(PW(i') = 0 = -16,000 + 3,300(P|A, i') = 0 = -16,000 + 3,300(P|A, i'%, 10)i'%, 10)i'i'DN->2DN->2 15.9% 15.9%

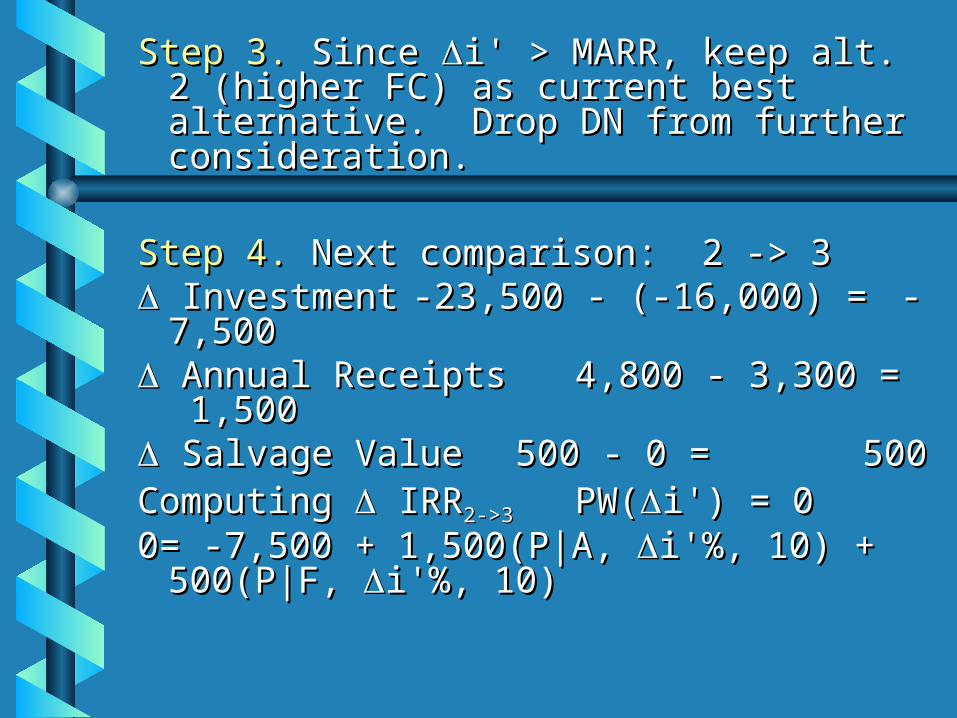

Step 3.Step 3. Since Since i' > MARR, keep alt. 2 i' > MARR, keep alt. 2 (higher FC) as current best alternative. (higher FC) as current best alternative. Drop DN from further consideration. Drop DN from further consideration.

Step 4.Step 4. Next comparison: 2 -> 3 Next comparison: 2 -> 3 InvestmentInvestment -23,500 - (-16,000) = -23,500 - (-16,000) = --

7,5007,500 Annual ReceiptsAnnual Receipts 4,800 - 3,300 = 4,800 - 3,300 =

1,5001,500 Salvage ValueSalvage Value 500 - 0 = 500 - 0 =

500 500Computing Computing IRR IRR2->32->3 PW(PW(i') = 0 i') = 0 0= -7,500 + 1,500(P|A, 0= -7,500 + 1,500(P|A, i'%, 10) + i'%, 10) +

500(P|F, 500(P|F, i'%, 10)i'%, 10)

i'i'2->32->3 15.5% 15.5%Since Since i' > MARR, keep Alt. 3 (higher FC) i' > MARR, keep Alt. 3 (higher FC) as current best alternative. Drop Alt. 2 as current best alternative. Drop Alt. 2 from further consideration. from further consideration.

Next comparison: 3 -> 1Next comparison: 3 -> 1 cash flows cash flows InvestmentInvestment -28,000 - (-23,500) = -28,000 - (-23,500) = --

4,5004,500 Annual ReceiptsAnnual Receipts 5,500 - 4,800 = 5,500 - 4,800 = 700700 Salvage Value 1,500 - 500 = Salvage Value 1,500 - 500 =

1,0001,000

Compute Compute IRR IRR3->13->1 PW(PW(i') = 0 i') = 0 0= -4,500 + 700(P|A, 0= -4,500 + 700(P|A, i'%, 10) + 1,000(P|i'%, 10) + 1,000(P|

F, F, i'%, 10)i'%, 10)i'i'3->13->1 10.9% 10.9%

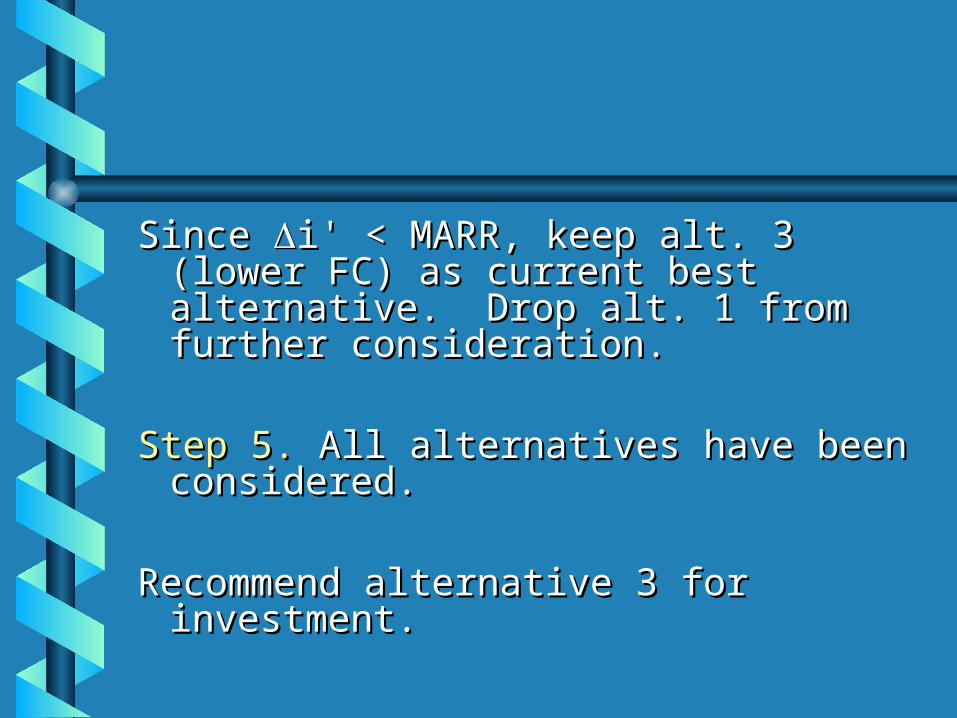

Since Since i' < MARR, keep alt. 3 (lower i' < MARR, keep alt. 3 (lower FC) as current best alternative. Drop FC) as current best alternative. Drop alt. 1 from further consideration. alt. 1 from further consideration.

Step 5.Step 5. All alternatives have been All alternatives have been considered.considered.

Recommend alternative 3 for Recommend alternative 3 for investment. investment.

Graphical Interpretation of ExampleGraphical Interpretation of Example

Measures of LiquidityMeasures of Liquidity

Simple Payback Period (Simple Payback Period ()) - how - how many years it takes to recover the many years it takes to recover the investment (ignoring the time investment (ignoring the time value of money). value of money).

Discounted Payback Period (Discounted Payback Period (')') - how many years it takes to - how many years it takes to recover the investment (including recover the investment (including the time value of money). the time value of money).

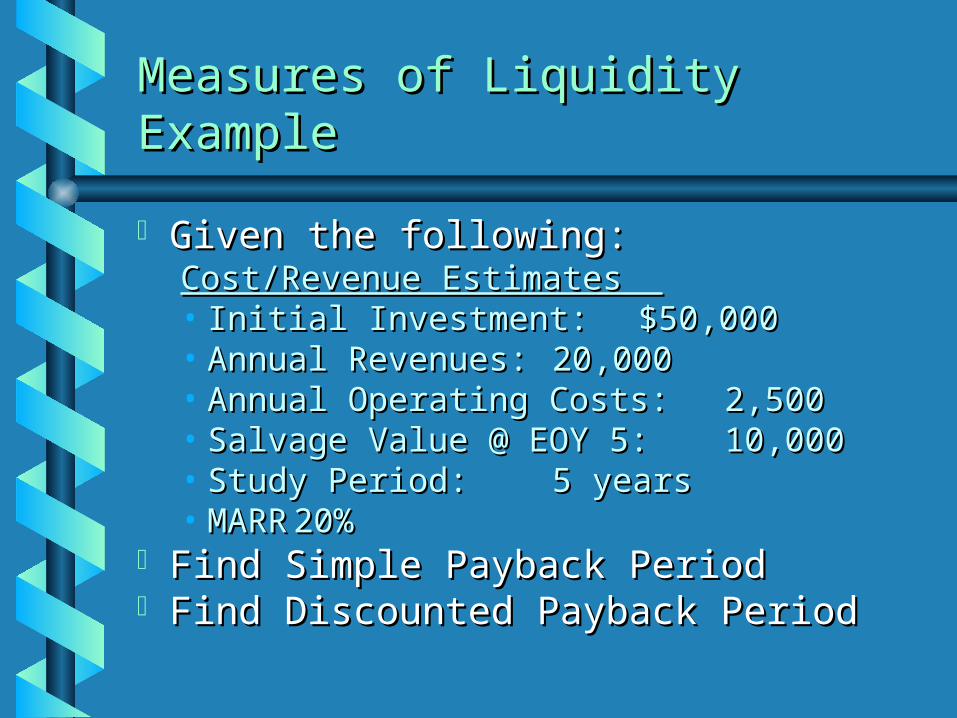

Measures of Liquidity ExampleMeasures of Liquidity Example

Given the following:Given the following:Cost/Revenue Estimates Cost/Revenue Estimates • Initial Investment:Initial Investment: $50,000$50,000• Annual Revenues:Annual Revenues: 20,00020,000• Annual Operating Costs:Annual Operating Costs: 2,5002,500• Salvage Value @ EOY 5:Salvage Value @ EOY 5: 10,00010,000• Study Period: Study Period: 5 years5 years• MARRMARR 20%20%

Find Simple Payback PeriodFind Simple Payback Period Find Discounted Payback PeriodFind Discounted Payback Period

ExampleExample

Simple PaybackSimple Payback Discounted PaybackDiscounted Payback(Cumulative PW) (Cumulative PW) (Cumulative PW)(Cumulative PW)EOYEOY (i = 0%)(i = 0%) (i = MARR = 20%)(i = MARR = 20%)00 -$50,000-$50,000 -$50,000-$50,00011 -32,500 -32,500 -35,417 -35,41722 -15,000 -15,000 -23,264 -23,26433 +2,500 +2,500 -13,137 -13,13744 +20,000 +20,000 -4,697 -4,69755 +47,500 +47,500 +6,354.50 +6,354.50

= 3 years= 3 years '' = 5 years = 5 years

Chapter 6 - Consideration of Chapter 6 - Consideration of Depreciation and TaxesDepreciation and Taxes

Why consider taxes in economic Why consider taxes in economic analysis?analysis?

BTCF versus ATCF?BTCF versus ATCF?

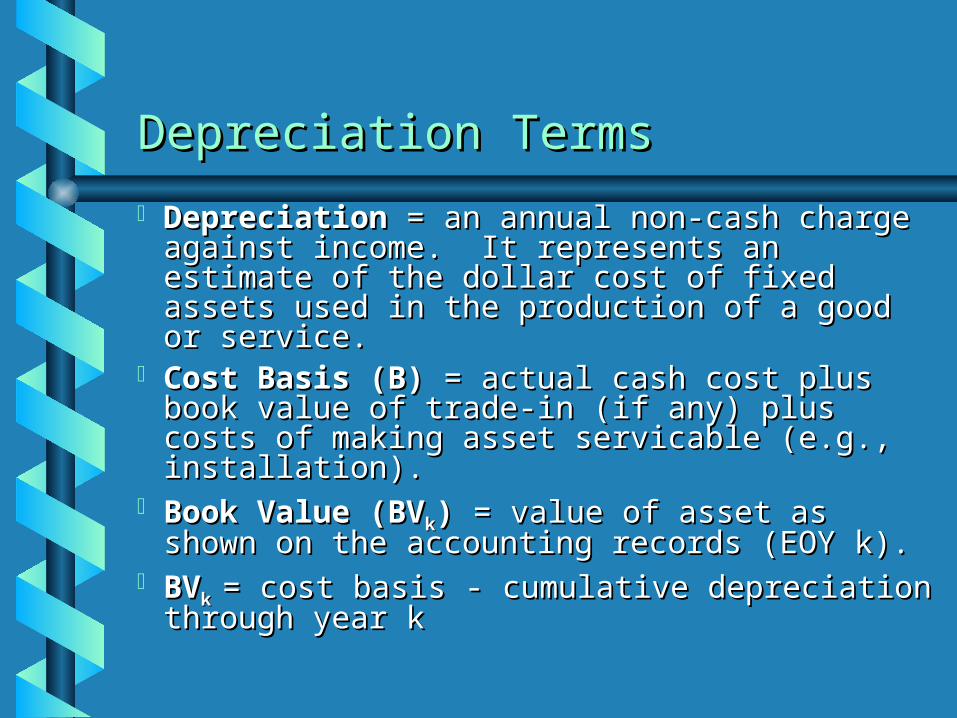

Depreciation TermsDepreciation Terms

DepreciationDepreciation = an annual non-cash = an annual non-cash charge against income. It represents an charge against income. It represents an estimate of the dollar cost of fixed assets estimate of the dollar cost of fixed assets used in the production of a good or service.used in the production of a good or service.

Cost Basis (B)Cost Basis (B) = actual cash cost plus = actual cash cost plus book value of trade-in (if any) plus costs of book value of trade-in (if any) plus costs of making asset servicable (e.g., installation). making asset servicable (e.g., installation).

Book Value (BVBook Value (BVkk)) = value of asset as = value of asset as shown on the accounting records (EOY k).shown on the accounting records (EOY k).

BVBVkk = cost basis - cumulative depreciation = cost basis - cumulative depreciation through year kthrough year k

Depreciation TermsDepreciation Terms

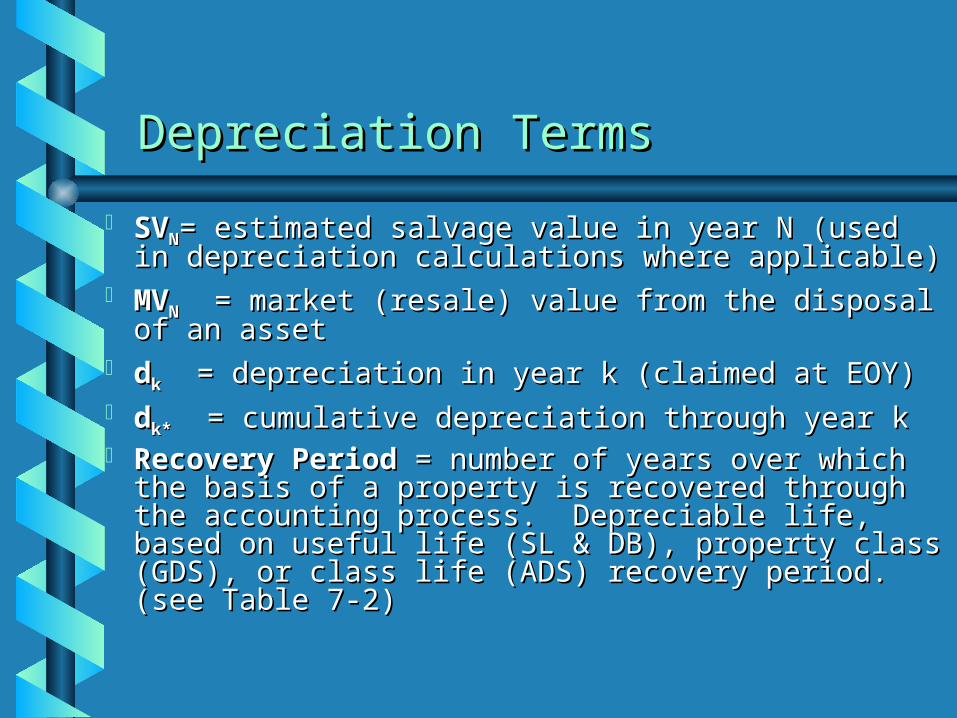

SVSVNN= estimated salvage value in year N (used = estimated salvage value in year N (used in depreciation calculations where applicable)in depreciation calculations where applicable)

MVMVNN = market (resale) value from the disposal = market (resale) value from the disposal of an assetof an asset

ddkk = depreciation in year k (claimed at EOY) = depreciation in year k (claimed at EOY) ddk*k* = cumulative depreciation through year k = cumulative depreciation through year k Recovery PeriodRecovery Period = number of years over = number of years over

which the basis of a property is recovered which the basis of a property is recovered through the accounting process. Depreciable through the accounting process. Depreciable life, based on useful life (SL & DB), property life, based on useful life (SL & DB), property class (GDS), or class life (ADS) recovery period. class (GDS), or class life (ADS) recovery period. (see Table 7-2)(see Table 7-2)

What is Depreciable?What is Depreciable?

1.1. Must be used in business or Must be used in business or held to produce income.held to produce income.

2.2. Must have a determinable life Must have a determinable life greater than one year.greater than one year.

3.3. Must wear out or get used up Must wear out or get used up over time. over time.

4.4. Is not inventory, stock in Is not inventory, stock in trade, or investment property. trade, or investment property.

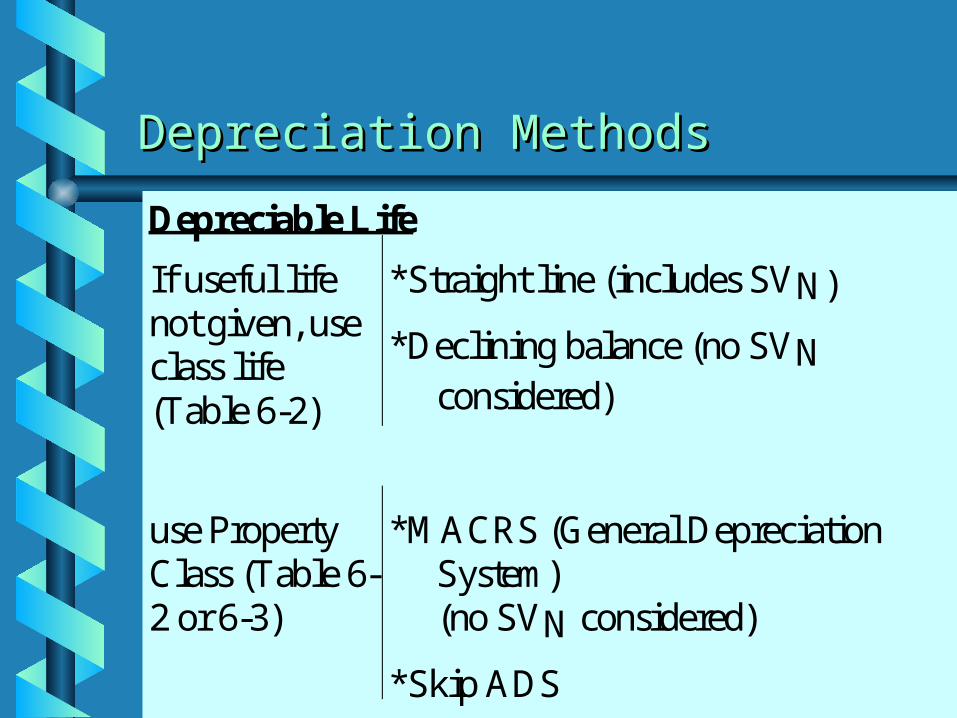

Depreciation MethodsDepreciation Methods

Depreciable Life

If useful lifenot given, useclass life(Table 6-2)

*Straight line (includes SVN)

*Declining balance (no SVNconsidered)

use PropertyClass (Table 6-2 or 6-3)

*MACRS (General DepreciationSystem)(no SVN considered)

*Skip ADS

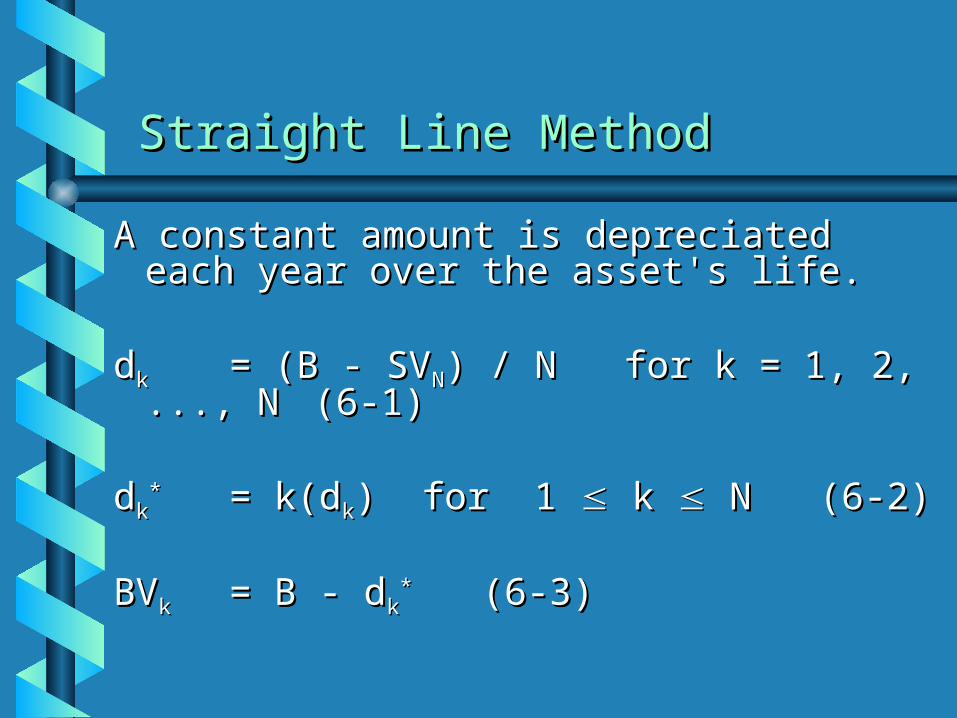

Straight Line MethodStraight Line Method

A constant amount is depreciated each A constant amount is depreciated each year over the asset's life. year over the asset's life.

ddkk= (B - SV= (B - SVNN) / N for k = 1, 2, ..., N) / N for k = 1, 2, ..., N (6-1)(6-1)

ddkk** = k(d= k(dkk) for 1 ) for 1 k k N N(6-2)(6-2)

BVBVkk = B - d= B - dkk** (6-3)(6-3)

Declining Balance MethodDeclining Balance Method

Annual depreciation is a constant percentage of the asset's Annual depreciation is a constant percentage of the asset's value at the BOY. value at the BOY.

dd11= B(R)= B(R) (6-4)(6-4)ddkk = B(1-R)= B(1-R)k-1k-1(R) = BV(R) = BVk-1k-1(R)(R) (6-5)(6-5)ddkk

** = B[1 - (1 - R)= B[1 - (1 - R)kk]] (6-6)(6-6)BVBVkk = B(1 - R)= B(1 - R)kk (6-7)(6-7)BVBVNN = B(1 - R)= B(1 - R)NN (6-8)(6-8)R = 2/NR = 2/N 200% declining balance, or200% declining balance, orR = 1.5/NR = 1.5/N 150% declining balance150% declining balance Uses the useful life (or class life) for NUses the useful life (or class life) for N Does not consider SVDoes not consider SVNN

SL and DB ExampleSL and DB Example

A computer was purchased for $20,000 A computer was purchased for $20,000 and $2,000 was spent installing it. The and $2,000 was spent installing it. The computer has an estimated salvage computer has an estimated salvage value of $4,000 at the end of its class value of $4,000 at the end of its class life. Compute the depreciation life. Compute the depreciation deduction in year 3 and the book value deduction in year 3 and the book value at the end of year 6 using:at the end of year 6 using:

a)a) straight-line methodstraight-line methodb)b) 200% declining balance 200% declining balance

methodmethod

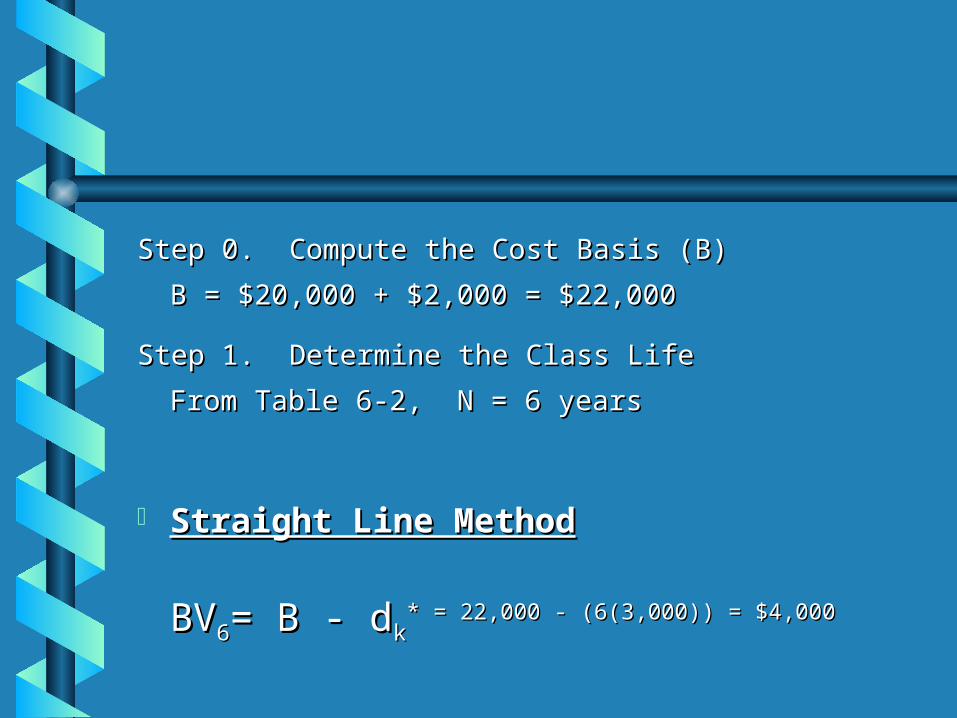

Step 0. Compute the Cost Basis (B) Step 0. Compute the Cost Basis (B)

B = $20,000 + $2,000 = $22,000B = $20,000 + $2,000 = $22,000

Step 1. Determine the Class LifeStep 1. Determine the Class Life

From Table 6-2, N = 6 yearsFrom Table 6-2, N = 6 years

Straight Line MethodStraight Line Method

BVBV66= B - d= B - dkk* = 22,000 - (6(3,000)) = $4,000* = 22,000 - (6(3,000)) = $4,000

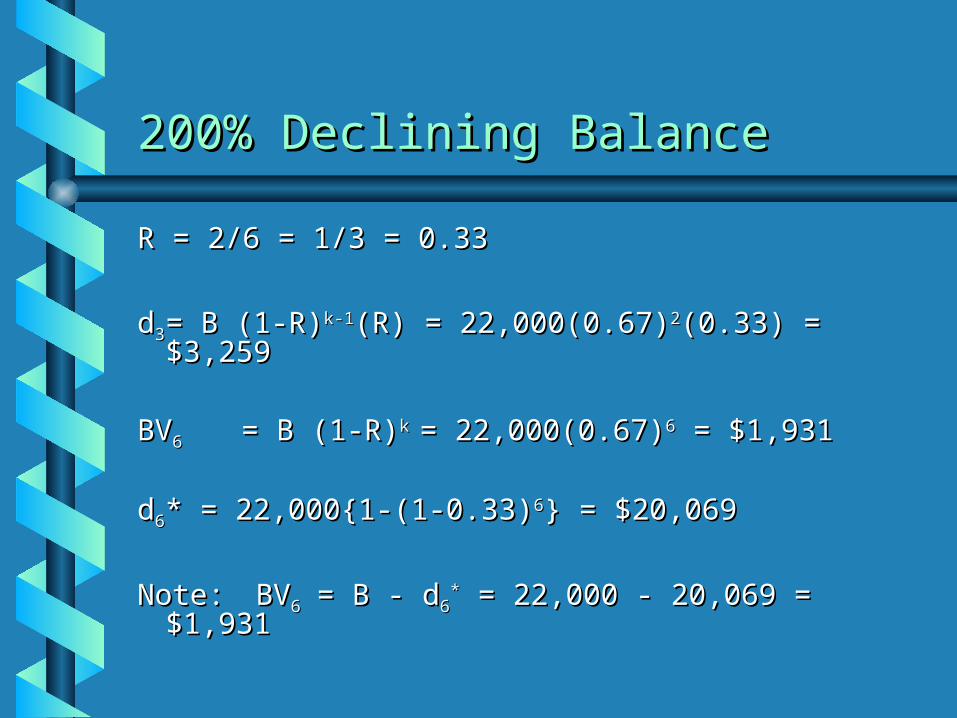

200% Declining Balance200% Declining Balance

R = 2/6 = 1/3 = 0.33R = 2/6 = 1/3 = 0.33

dd33 = B (1-R)= B (1-R)k-1k-1(R)(R) = 22,000(0.67)= 22,000(0.67)22(0.33) = $3,259(0.33) = $3,259

BVBV66 = B (1-R)= B (1-R)k k = 22,000(0.67)= 22,000(0.67)66 = $1,931 = $1,931

dd66* = 22,000{1-(1-0.33)* = 22,000{1-(1-0.33)66} = $20,069} = $20,069

Note:Note: BVBV66 = B - d= B - d66** = 22,000 - 20,069 = $1,931 = 22,000 - 20,069 = $1,931

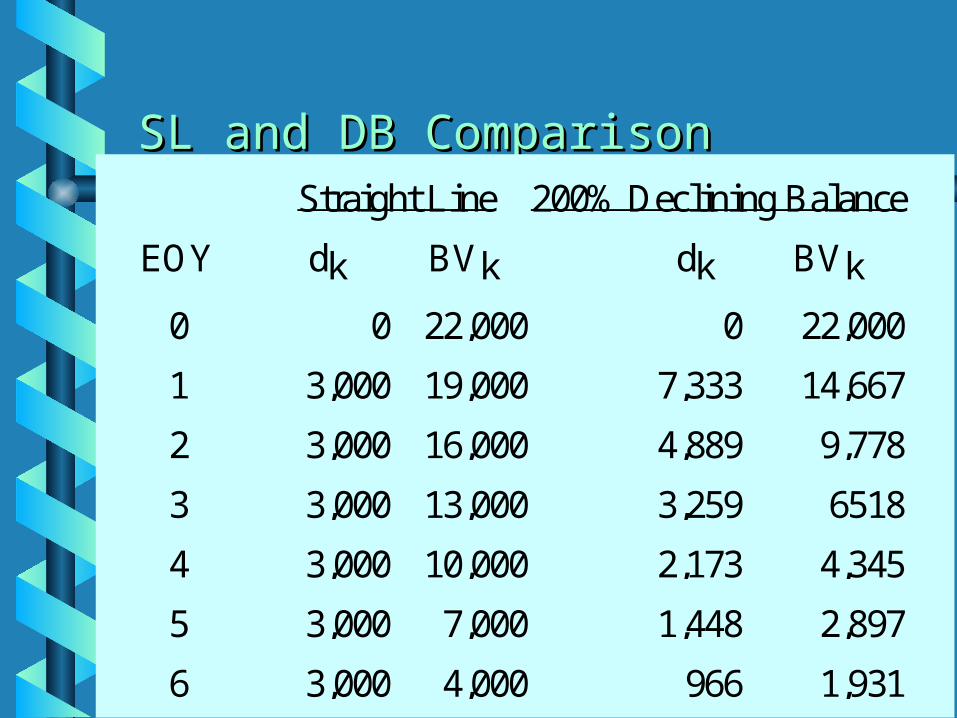

SL and DB ComparisonSL and DB Comparison Straight Line 200% Declining Balance

EOY dk BVk dk BVk

0 0 22,000 0 22,000

1 3,000 19,000 7,333 14,667

2 3,000 16,000 4,889 9,778

3 3,000 13,000 3,259 6518

4 3,000 10,000 2,173 4,345

5 3,000 7,000 1,448 2,897

6 3,000 4,000 966 1,931

MACRS (GDS) METHODMACRS (GDS) METHOD

Annual depreciation is a fixed percentage of the Annual depreciation is a fixed percentage of the cost basis (percentage specified by the IRS). cost basis (percentage specified by the IRS). Mandatory for most assets. Mandatory for most assets.

ddkk = r = rkkBB

Step 1.Step 1. Determine the property class (recovery period) from Determine the property class (recovery period) from Table 6-2 or Table 6-3Table 6-2 or Table 6-3

Step 2.Step 2. Use Table 6-4 to obtain GDS rates, r Use Table 6-4 to obtain GDS rates, rkk

Step 3.Step 3. Compute depreciation deduction in year k by Compute depreciation deduction in year k by multiplying the asset’s cost basis by the appropriate multiplying the asset’s cost basis by the appropriate recovery rate, rrecovery rate, rkk..

MACRS over N + 1 years due to half-year MACRS over N + 1 years due to half-year conventionconvention

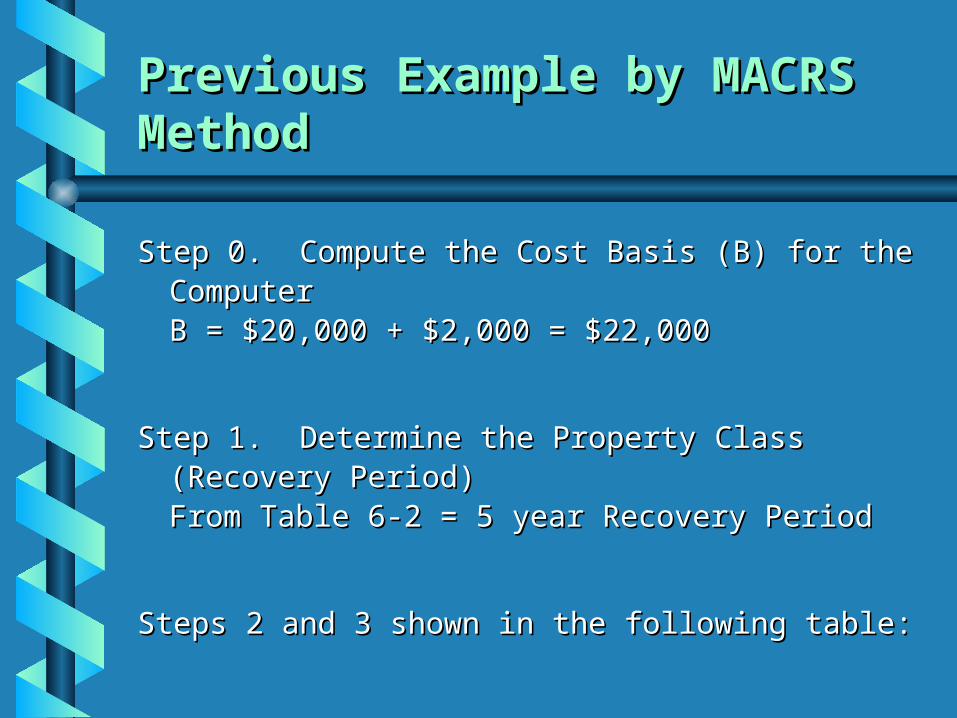

Previous Example by MACRS MethodPrevious Example by MACRS Method

Step 0. Compute the Cost Basis (B) for the Step 0. Compute the Cost Basis (B) for the ComputerComputer

B = $20,000 + $2,000 = $22,000B = $20,000 + $2,000 = $22,000

Step 1. Determine the Property Class (Recovery Step 1. Determine the Property Class (Recovery Period)Period)

From Table 6-2 = 5 year Recovery PeriodFrom Table 6-2 = 5 year Recovery Period

Steps 2 and 3 shown in the following table: Steps 2 and 3 shown in the following table:

Previous Example with MARCSPrevious Example with MARCS

EOY rate, rk dk BVk

0 $22,000

1 0.2000 $4,400 17,600

2 0.3200 7,040 10,560

3 0.1920 4,224 6,336

4 0.1152 2,534 3,802

5 0.1152 2,534 1,268

6 0.0576 1,268 0

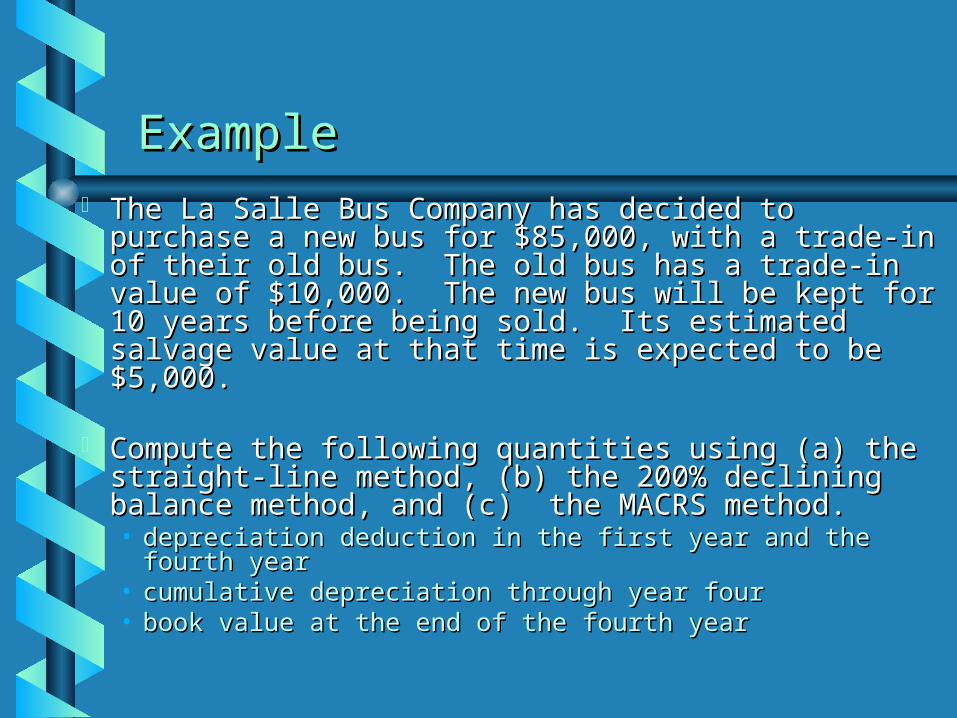

ExampleExample The La Salle Bus Company has decided to purchase a The La Salle Bus Company has decided to purchase a

new bus for $85,000, with a trade-in of their old bus. The new bus for $85,000, with a trade-in of their old bus. The old bus has a trade-in value of $10,000. The new bus will old bus has a trade-in value of $10,000. The new bus will be kept for 10 years before being sold. Its estimated be kept for 10 years before being sold. Its estimated salvage value at that time is expected to be $5,000.salvage value at that time is expected to be $5,000.

Compute the following quantities using (a) the straight-Compute the following quantities using (a) the straight-line method, (b) the 200% declining balance method, and line method, (b) the 200% declining balance method, and (c) the MACRS method.(c) the MACRS method.• depreciation deduction in the first year and the fourth yeardepreciation deduction in the first year and the fourth year• cumulative depreciation through year fourcumulative depreciation through year four• book value at the end of the fourth yearbook value at the end of the fourth year

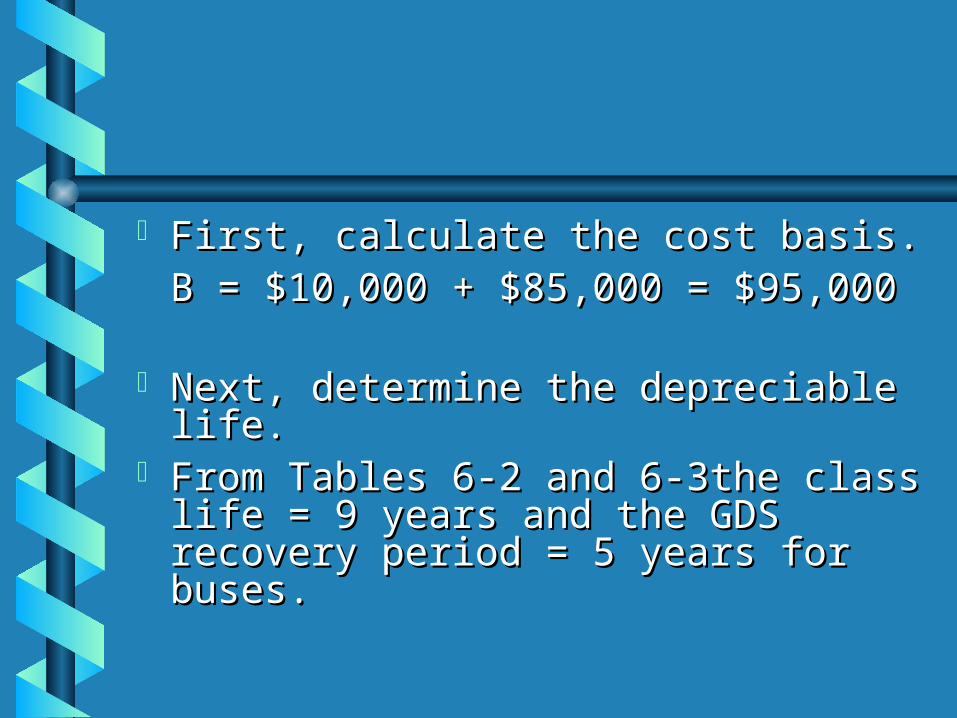

First, calculate the cost basis.First, calculate the cost basis.B = $10,000 + $85,000 = B = $10,000 + $85,000 =

$95,000$95,000

Next, determine the depreciable life.Next, determine the depreciable life. From Tables 6-2 and 6-3the class life From Tables 6-2 and 6-3the class life

= 9 years and the GDS recovery = 9 years and the GDS recovery period = 5 years for buses.period = 5 years for buses.

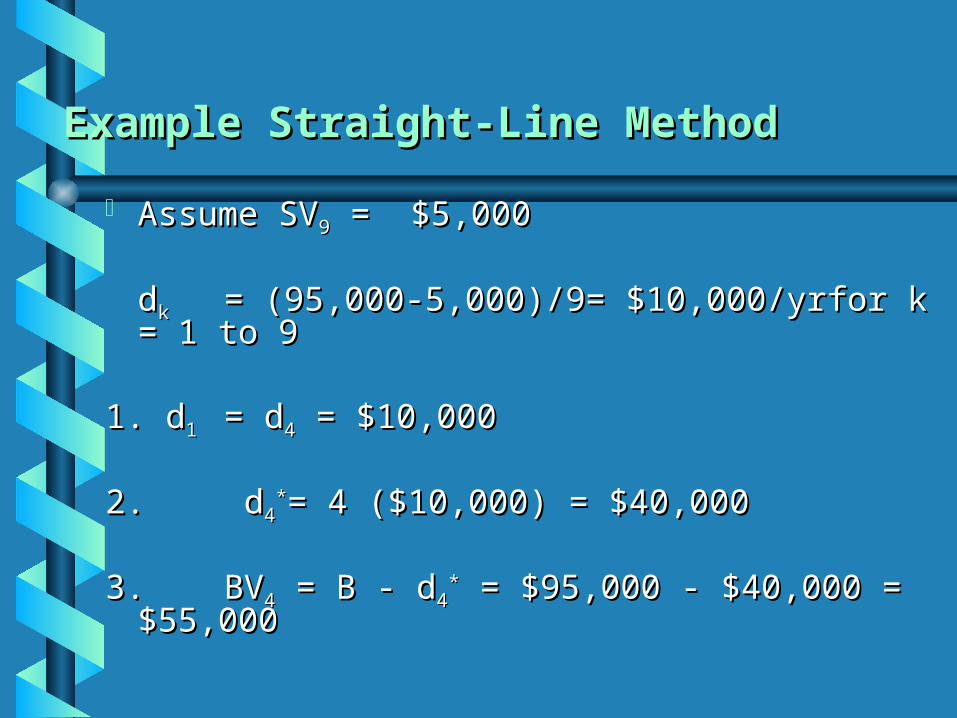

Assume SVAssume SV99 = $5,000 = $5,000

ddkk = (95,000-5,000)/9= $10,000/yr= (95,000-5,000)/9= $10,000/yr for k = 1 to 9for k = 1 to 9

1. d1. d11 = d= d44 = $10,000 = $10,000

2.2. d d44**= 4 ($10,000) = $40,000= 4 ($10,000) = $40,000

3.3. BVBV44 = B - d = B - d44** = $95,000 - $40,000 = $55,000 = $95,000 - $40,000 = $55,000

Example Straight-Line MethodExample Straight-Line Method

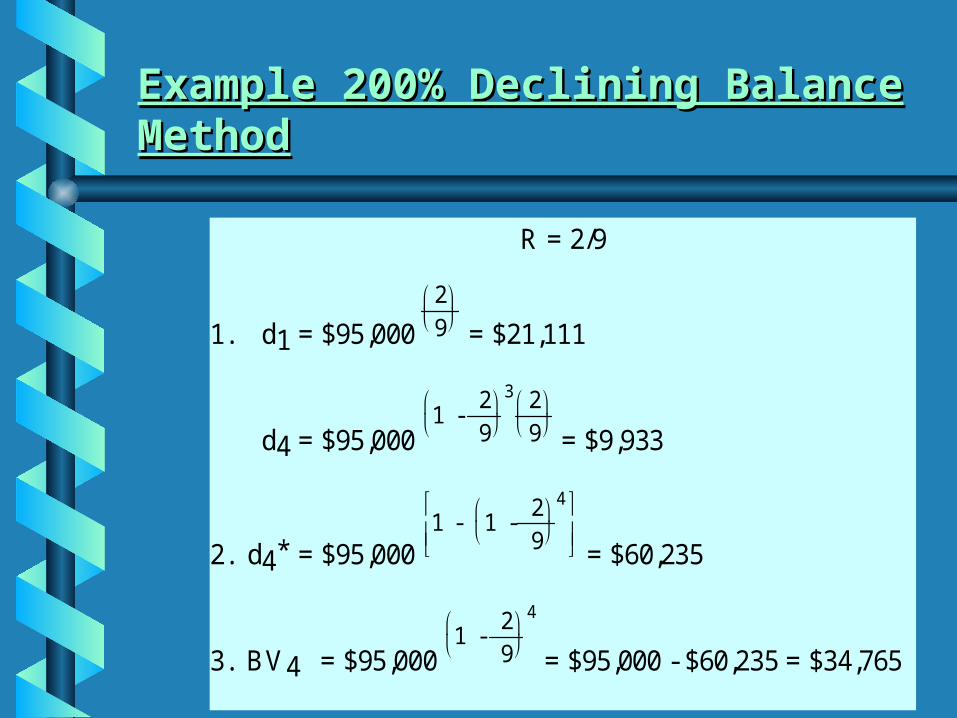

Example 200% Declining Balance MethodExample 200% Declining Balance Method

R = 2/9

1. d1 = $95,000 29

= $21,111

d4 = $95,000 1 -

29

3 29

= $9,933

2. d4* = $95,000 1 - 1 -

29

4

= $60,235

3. BV4 = $95,000 1 -

29

4

= $95,000 - $60,235 = $34,765

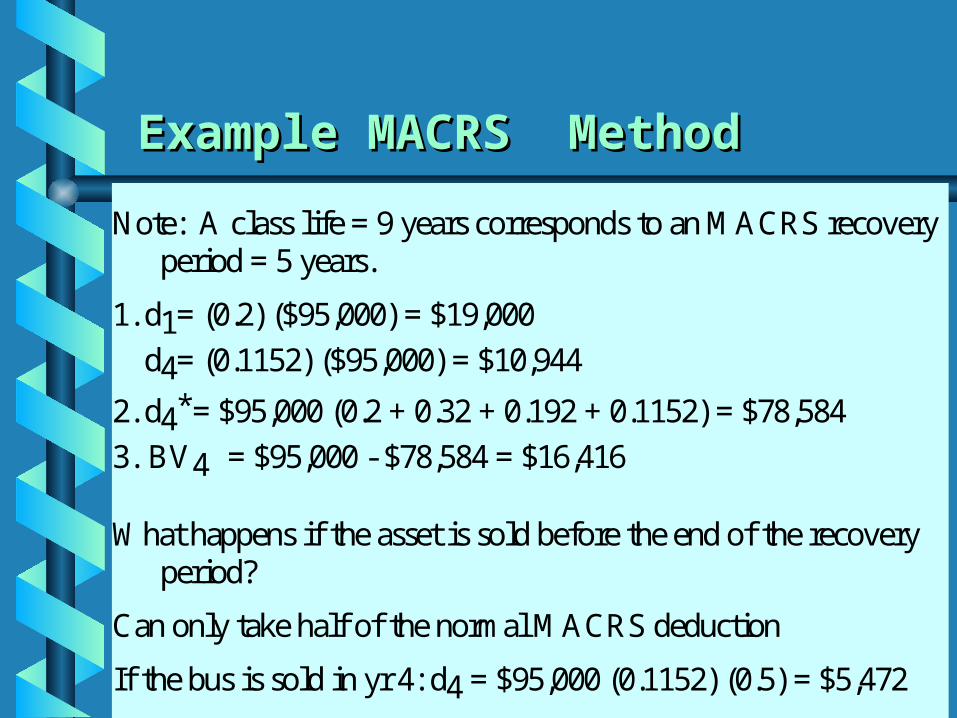

Example MACRS MethodExample MACRS Method

Note: A class life = 9 years corresponds to an MACRS recoveryperiod = 5 years.

1. d1= (0.2) ($95,000) = $19,000

d4= (0.1152) ($95,000) = $10,944

2. d4*= $95,000 (0.2 + 0.32 + 0.192 + 0.1152) = $78,584

3. BV4 = $95,000 - $78,584 = $16,416

What happens if the asset is sold before the end of the recoveryperiod?

Can only take half of the normal MACRS deduction

If the bus is sold in yr 4: d4 = $95,000 (0.1152) (0.5) = $5,472

![Today’s line-up Status reports Research article analysis – recap View sample project from previous class Project teams + project plan [due Tues Mar 4]](https://img.dokumen.tips/doc/110x75/56649f215503460f94c39987/todays-line-up-status-reports-research-article-analysis-recap-view-sample.jpg)