Embed Size (px)

Citation preview

NWOSU CHUKWUBUZO JERRY PG/MBA/08/47498

ANALYSIS OF THE NEW CONTRIBUTORY PENSION SCHEME IN THE NIGERIA PUBLIC SECTOR: ISSUES, PROBLEMS AND

PROSPECTS

Management

A THESIS SUBMITTED TO THE DEPARTMENT OF MANAGEMENT, FACULTY OF

BUSINESS ADMINISTRATION, UNIVERSITY OF NIGERIA ENUGU CAMPUS

Webmaster Digitally Signed by Webmaster’s Name

DN : CN = Webmaster’s name O= University of Nigeria, Nsukka

OU = Innovation Centre

2010

UNIVERSITY OF NIGERIA

ANALYSIS OF THE NEW CONTRIBUTORY

PENSION SCHEME IN THE NIGERIA PUBLIC SECTOR:

ISSUES, PROBLEMS AND PROSPECTS

NWOSU CHUKWUBUZO JERRY

PG/MBA/08/47498

DEPARTMENT OF MANAGEMENT

FACULTY OF BUSINESS ADMINSITRATION

UNIVERSITY OF NIGERIA

ENUGU CAMPUS

MARCH, 2010

CERTIFICATION

I Nwosu Chukeubuzo Jerr, a postgraduate students of the

Department of Management with Registration Number

PG/MBA/08/47498 has satisfactorily completed the

requirements of the course and research work for the award of

Masters Degree in (MBA) in Management, Faculty of Business

Administration

The work embodied in this project report is original and has

not been submitted in part of full for any Diploma or Degree of

this in any other university.

---------------------------------------- Nwosu Chukwubuzo Jerr

PG/MBA/08/47498

----------------------------------- ---------------------------- Prof. U.J.F. Ewurum Prof U.J.F Ewurum Supervisor Head of Department

DEDICATION

This project work is dedicated to Almighty God, author and

finisher our faith, our help in ages past. And to our late

Nationalists and good leaders who contributed in one way or

the other to the development of this nation.

ACKNOWLEDGEMENT

It is obvious that a project of this nature must definitely

require the contribution and support of other person.

Therefore I remain grateful in the course of the research.

My profound appreciation goes to my project supervisor Prof.

U.J.F Ewurum for his genuine advice and guidance that help

towards the accomplishment of this project. I am grateful to

the Head of Department of Management, Prof. U.J.F Ewurum

for his fatherly advice, and all the staff of department of

management.

I am sincerely grateful to my family members for their moral

and financial support and encouragement in the course of my

study. My special thanks go my lovely wife. Above all, I am

highly grateful to Almighty God, for providing me with the

knowledge and inspiration that is required for this project.

To God be the Glory.

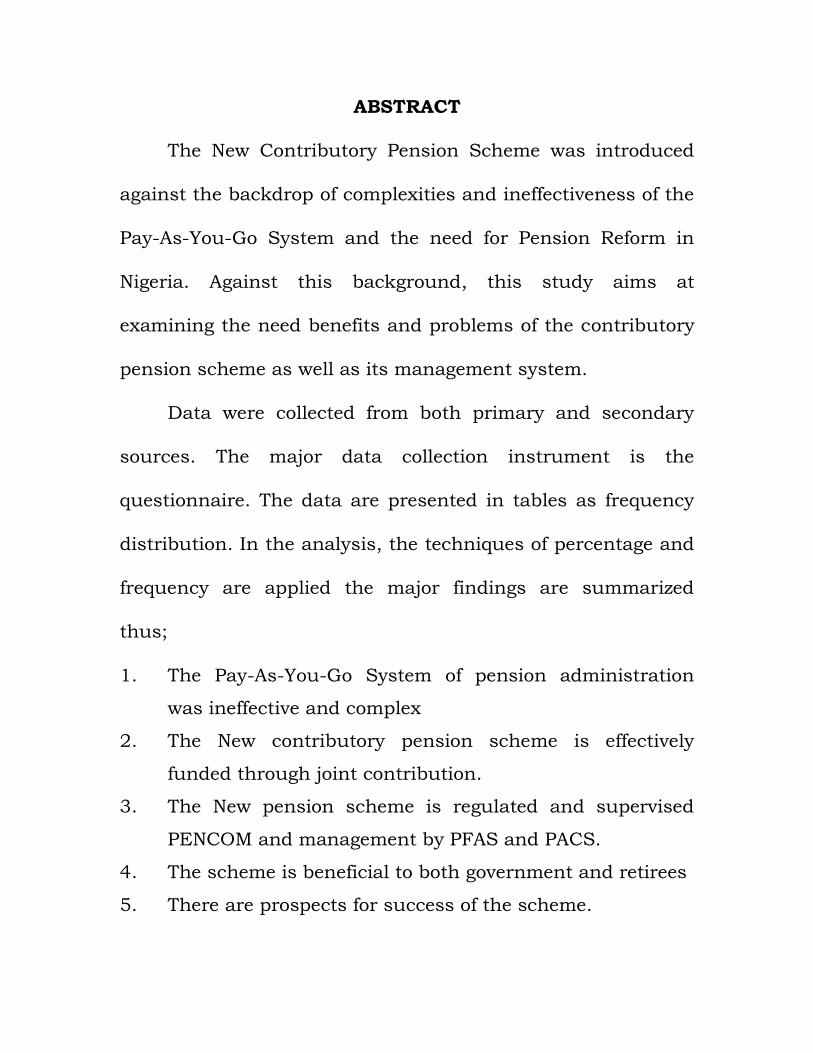

ABSTRACT

The New Contributory Pension Scheme was introduced

against the backdrop of complexities and ineffectiveness of the

Pay-As-You-Go System and the need for Pension Reform in

Nigeria. Against this background, this study aims at

examining the need benefits and problems of the contributory

pension scheme as well as its management system.

Data were collected from both primary and secondary

sources. The major data collection instrument is the

questionnaire. The data are presented in tables as frequency

distribution. In the analysis, the techniques of percentage and

frequency are applied the major findings are summarized

thus;

1. The Pay-As-You-Go System of pension administration

was ineffective and complex

2. The New contributory pension scheme is effectively

funded through joint contribution.

3. The New pension scheme is regulated and supervised

PENCOM and management by PFAS and PACS.

4. The scheme is beneficial to both government and retirees

5. There are prospects for success of the scheme.

It is the existence of these factors that pose serious challenges

to the management of the new contributory pension scheme.

1.3 OBJECTIVES OF THE STUDY

The objectives of the study are:

1. To examine the rationale for the introduction of the

contributory pension scheme.

2. To examine how the new pension scheme is regulated

and supervised.

3. To find out how the scheme is funded.

4. To find out how the scheme is administered.

5. To highlight the problems and prospects of the scheme.

1.4 RESEARCH QUESTIONS

The following questions will be addressed in this study:

1. What is the rationale for the introduction of the new

contributory pension scheme?

2. How is the new pension scheme regulated and

supervised?

3. What are the sources of funds for the new contributory

pension scheme?

4. What are the problems and prospects of the new pension

scheme?

1.5 Formulation of hypotheses

1. There is no rationale for the introduction of the

contributory pension scheme.

2. There is no regulation and supervision of new pension

scheme

3. The sources of funds does not contribute effectively to

pension scheme.

4. There is no relationship between the problems and

prospects of the new pension scheme

1.6 SIGNIFICANCE OF THE STUDY

The significance of the study derives from its usefulness to

employers, workers, pension fund administrators and

custodians as well as PENCOM and students. This is as

follows:

1. Government

The perceived problems of the new pension scheme will be

highlighted in this study. And, it will provide such useful

information that will enable the government to take remedial

measures through its recommendations.

2. Corporate Bodies

Corporate bodies in the organized private sector as well as

local and state government of immense benefit. It will highlight

the benefit of contributory person schemes unknown to them.

This may carry enough appeal as to make them adopt the

scheme.

3. Workers

Many workers are still not well informed about the scheme

and its virtue. This study will provide adequate information

about this to workers and make then understand the scheme

and its benefits fully.

CHAPTER FOUR

DATA PRESENTATION AND ANALYSIS

In this chapter, the researcher presents and analyses the

data collected from the respondents.

Table 4.1 Questionnaire Administration

Questionnaires No %

a) Distributed 101 100

b) Returned 101 100

c) Not Returned - -

d) Discarded - -

e) Analysed 101 100

The table above shows that all the questionnaires

distributed were returned and analysed. This implies that

none was discarded.

Table 4.2 Sex Distribution of Respondents

Sex No %

a) Males 56 55.4

b) Females 45 55.6

Total 101 100

This shows that 55.4% of the respondents are males

while 44.6% are females. This implies that more males were

randomly selected for this study.

Table 4.3 Age Distribution of Respondents

Age Group (yrs) No %

a) Under 30 19 18.8

b) 30-40 30 29.7

c) 41-50 34 33.7

d) 51-60 18 17.8

Total 101 100

From the table above, it can be seen that 18.8% are

below 30 years old. 29.7% are within 30-40 years age range.

33.7% are within 41-50 years of age while 51-60 years age b

racket. This implies that a greater segment of the respondents

are within 30-50 age bracket.

Table 4.4 Marital Distribution of Respondents

Marital Status No %

a) Single 40 39.6

b) Married 49 48.5

c) Others 12 11.9

Total 101 100

The table shows that 39.6% are single while 48.5% are

married. Widows, widowers and divorcees constituted 11.9%.

This implies that most of the respondents are married.

Table 4.5 Educational Qualification of Respondents

Qualification No %

a) FSLC - -

b) WASC/GCE 18 17.8

c) NCE/OND 21 20.8

d) BSC/HND/Equiv 32 31.7

e) MSc/ MBA/Equiv. 18 17.8

f) Others 12 11.9

Total 101 100

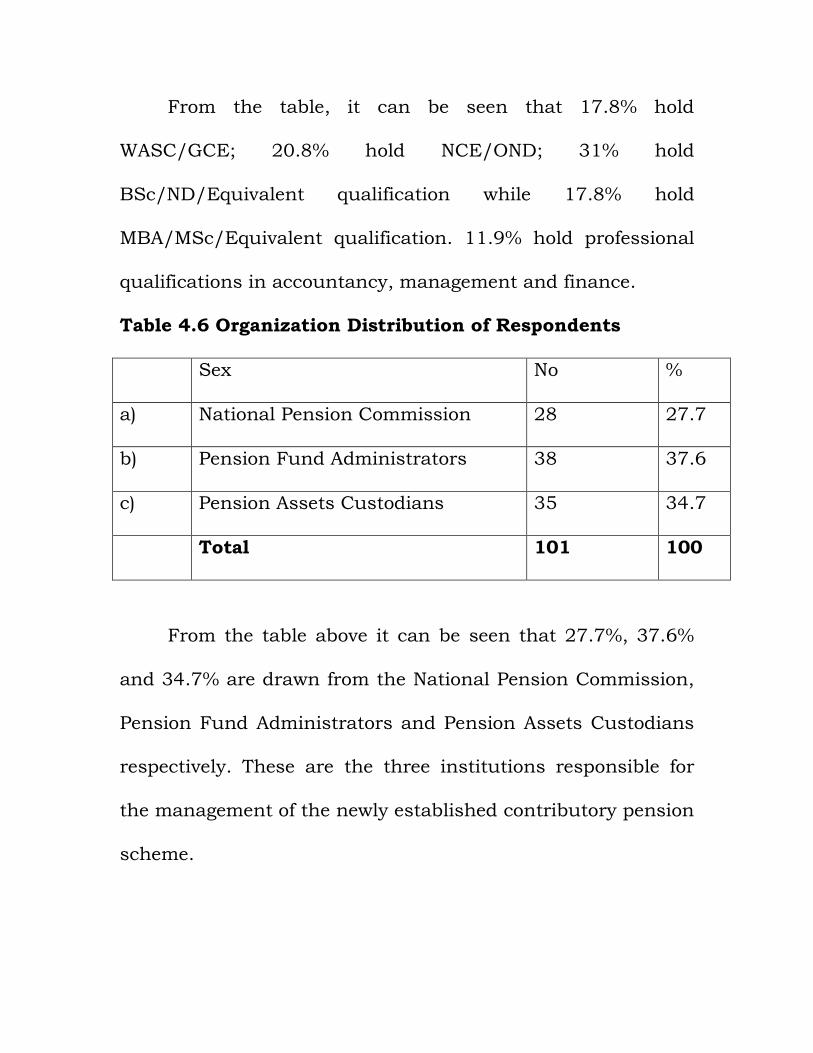

From the table, it can be seen that 17.8% hold

WASC/GCE; 20.8% hold NCE/OND; 31% hold

BSc/ND/Equivalent qualification while 17.8% hold

MBA/MSc/Equivalent qualification. 11.9% hold professional

qualifications in accountancy, management and finance.

Table 4.6 Organization Distribution of Respondents

Sex No %

a) National Pension Commission 28 27.7

b) Pension Fund Administrators 38 37.6

c) Pension Assets Custodians 35 34.7

Total 101 100

From the table above it can be seen that 27.7%, 37.6%

and 34.7% are drawn from the National Pension Commission,

Pension Fund Administrators and Pension Assets Custodians

respectively. These are the three institutions responsible for

the management of the newly established contributory pension

scheme.

Table 4.7 Rationale for the new Contributory Pension

Scheme Options

Options No %

a) Inadequate funding of the old pension scheme 23 22.8

b) Complex procedures in processing pension

benefits.

12 11.9

c) Delays in paying pension benefits 18 17.8

d) Ignorance and apathy of pension fund trustees 6 5.9

e) Diversion and misappropriations 20 19.8

f) All of the above 22 21.8

Total 101 100

The table shows that 22.8, 11.9 and 17.8% indicate that

the rationale for the introduction of the new contributory

pension scheme is inadequate funding of the old pension

scheme, complex procedures in processing pension benefits

and delays in paying pension benefits respectively. 5.9 and

19.8% indicate that it is the ignorance and apathy of pension

fund trustees and diversion and misappropriation of pension

funds respectively. 21.8% indicate all of the above.

This implies that the introduction of the new contributory

pension scheme was necessitated by administrative and

management problems of the old pension scheme which made

it ineffective.

Table 4.8 Regulatory and Supervisory body for the Scheme

Options No %

a) National Pension Commission 101 100

b) Pension Fund Administrators - -

c) Pension Assets Custodians - -

Total 101 100

The table shows that all the respondents indicate that

the regulatory and supervisory body for the new contributory

pension scheme is the National Pension Commission

(PENCOM). This body was established by the Pension Act,

2004.

Table 4.9 Regulation and Supervision of the New

Contributory Pension Scheme

Options No %

a) The regulatory and supervisory body

establishes standards rules and

operational guidelines

14

13.9

b) The body approves and appoints PFAs

and PACs.

10

9.8

c) It enlightens the public about the new

pension scheme

5

4.9

d) It receives and investigates complaints

against PFAs and PACs

10

9.8

e) It sanctions all erring PFAs and PACs 9 8.9

f) All of the above 53 52.7

Total 101 100

On how the new pension scheme is regulated and

supervised 13.9, 9.8 and 4.9% indicate that the regulatory and

supervisory body establishes standards, rules and operational

guidelines; approves and appoints PFAs and PACs and

enlightens the public on the new pension scheme respectively.

9.8 and 8.9% indicate that the body receives and investigates

complaints against PFAs and PACs and sanctions erring PFAs

and PACS respectively. 52.7% indicate all of the above.

This implies that PENCOM regulates, monitors and

controls the activities of all registered PFAs and PACs and

ensures that their activities comply with the provisions of the

new Pension Act.

Table 4.10 Funding of the Scheme

Options No %

a) Contribution by Government - -

b) Contribution by workers - -

c) Joint contributions of government

and workers

101

100

Total 101 100

The table shows that all the respondents indicate that

the new pension scheme is funded through joint contributions

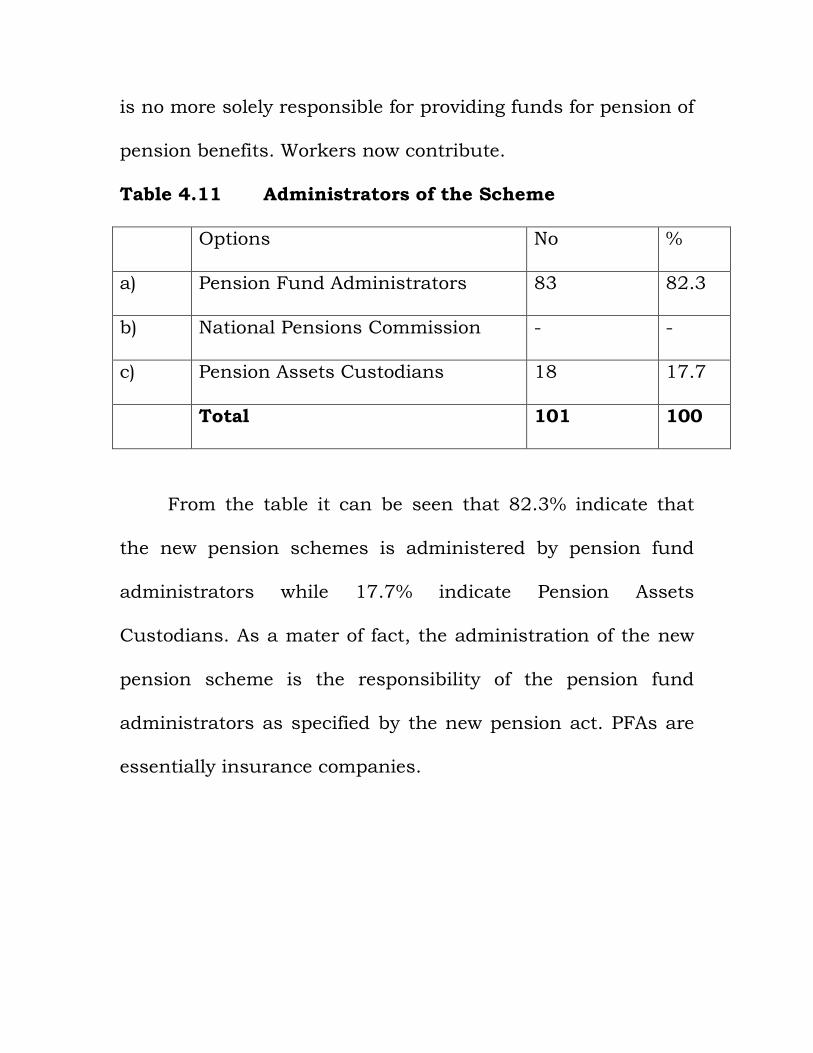

by the government and workers. This implies that government

is no more solely responsible for providing funds for pension of

pension benefits. Workers now contribute.

Table 4.11 Administrators of the Scheme

Options No %

a) Pension Fund Administrators 83 82.3

b) National Pensions Commission - -

c) Pension Assets Custodians 18 17.7

Total 101 100

From the table it can be seen that 82.3% indicate that

the new pension schemes is administered by pension fund

administrators while 17.7% indicate Pension Assets

Custodians. As a mater of fact, the administration of the new

pension scheme is the responsibility of the pension fund

administrators as specified by the new pension act. PFAs are

essentially insurance companies.

Table 4.12 Responsibilities of the PFAs.

Options No %

a) Computation of employees

retirement benefits

7

6.9

b) Opening of retirement savings

accounts for employees

9

8.9

c) Causing retirement benefits to be

paid into the account

8

7.9

d) Investing and managing pension

funds

- -

e) Maintaining books of accounts for

retirees

7

6.9

f) Providing customer services and

relevant information for employees

6

5.9

g) All of the above 56 55.6

Total 101 100

With respect to responsibilities of the Pension Fund

Administrators, the table shows that 6.9, 8.9 and 7.9%

indicate computation of employees retirement benefit, opening

of retirement savings accounts for employees and causing

retirement benefits to be paid into the account respectively.

6.9, 7.9 and 5.9% indicate investing and managing pension

funds, maintaining books of accounts and providing customer

services and relevant information for employees respectively.

55.6% indicate all the above as the role of PFAs.

This implies that the PFAs in the new contributory

pension scheme has taken over the role of the board of

trustees in the old pension scheme.

Table 4.13 Responsibilities of PACs

Options No %

a) Receipt of all remittances on behalf

of PFAs

16

15.8

b) Keeping in safe custody all funds

and assets

15

14.9

c) Effecting payments to beneficiaries 15 14.9

d) Rendition of reports and returns

on investment to PENCOM and

PFAz

13

12.9

e) All of the above 42 41.5

Total 101 100

In respect of responsibilities of PACs, the table shows

that 15.8 and 14.9% indicate receipt of all remittances on

behalf of the PFAs and keeping in safe custody the funds and

assets of the scheme respectively. 14.9 and 12.9% indicate

effecting payments to retirees and rendition of reports and

returns on investment to PENCOM and PFAs respectively.

41.5% indicate all the above.

This implies that PACs are bankers to the PFAs and

PENCOM.

Table 4.14 Benefits of the Scheme

Options No %

a) Reduction of Pension liability

burden for the government

13

12.9

b) Effective Funding of the Pension

scheme

12

11.9

c) Effective management of Pension

Fund

12

11.9

d) Timely Payment of Pension

benefits

10

9.9

e) All of the above 54 53.4

Total 101 100

On the benefits of the pension scheme, the tables shows

that 12.9 and 11.9% indicate reduction of pension liabilities

burden for the government and effective funding of the

pension scheme respectively. 11.9 and 9.9% indicate effective

management of pension fund and timely payment of pension

benefits respectively. 53.4% indicate all of the above.

This implies that both the government and

employees/retirees benefit from the new contributory Pension.

Table 4.15 Problems of the Scheme

Options No %

a) Delays in remitting deductions to

PFAs

28

27.7

b) Inadequate skilled personnel for

PFAs

10

9.9

c) Encroachment by old pension

scheme managers

9

8.9

d) Shallow capital market for

investing funds

33

32.7

e) All of the above 21 20.8

Total 101 100

From the table, it can be seen that 27.7% identify the

problem of the scheme as delays in remitting deductions to

PFAs. 9.9, 8.9 and 32.7% identify the problems as inadequate

skilled personnel for the PFAs, encroachment by old pension

scheme managers and shallow capital market for investing

funds. 20.8% identify all the above problems.

This implies that most of the respondents identify delays

in remitting deductions to PFAs and shallow capital market as

the most pronounced problems of the pension scheme.

It is alleged that establishments do not remit workers’

contributions deducted at source to the Pension Fund

Administrators. This, in turn, has caused some problems in

crediting the accounts of the contributors.

Besides, the PFA’s of not have adequate competent staff

to facilitate the processing of documents and crediting of

accounts as well as rendition of reports to PENCOM on time.

This has tempted old managers of this scheme to encroach in

the new scheme to perform one function or the other.

The new pension scheme is considered effective because it is

designed to have all funds unused immediately invested in the

capital market. But it is being expressed that the Nigerian

capital market is too shallow and does not have the capacity to

absorb all the funds being raised under the scheme. This

poses the danger of fund diversion and misappropriation by

fund managers.

On the prospects of the scheme the respondents highlights

the following:

- Increasing contributions by government and workers

- Viability of bonds issued to retirees.

- Improving Nigerian economy for investment.

- Increasing capacity building of the Pension Fund

Administrators

- Increasing emphasis on SERVICOM which will facilitate

service delivery in remitting deductions to PFAs by

government establishments.

CHAPTER FIVE

SUMMARY, CONCLUSION AND RECOMMENDATIONS

5.1 SUMMARY OF FINDINGS

The following are the major findings of the study;

- The rationale for the new contributory pension scheme

include inadequate funding of the old pension scheme,

complex procedures in processing pension benefits,

delays in paying pension benefits, ignorance and apathy

of pension fund trustees and diversion and

misappropriation of pension funds.

- The National Pension Commission is the regulatory body.

Its regulatory and supervisory responsibilities include

establishing standards, rules and operational guidelines,

approving and appointing Pension Funds administrators

and custodians, receiving and investigating complaints

against PEAs and PACs and sanctioning erring PEAs and

PACs.

- The pension fund is financed through joint contributions

by the government and workers.

- The scheme is administered by the PEAs. The

responsibilities of the PEAs include computation of

retirement benefits, opening of Retirement Saving

account, causing retirement benefits to be paid to

retirees, investigating and managing pension funds,

maintaining books of account for retirees and providing

customer services and relevant information for

employees.

- PACs are the bankers of the scheme. Their

responsibilities include receiving all remittances from

government and its establishments on behalf of the PFAs,

keeping all funds and assets in safe custody, effecting

payments to retirees and rendition of reports/returns to

PENCOM and PFAs.

- The benefits of the new pension scheme include

reduction of pension liability for the government, effective

funding of the pension scheme, effective management of

pension scheme and timely payment of pension benefits.

- The inherent problems of the new pension scheme

include delays in remitting deductions to PFAs,

inadequate skilled personnel for PEAs, encroachment by

old pension scheme managers and shallow capital

market for investment of pension funds.

- The prospects of the new pension scheme include

increasing joint contributions, viability of issued bonds,

improving Nigerian economy for investment, increasing

capacity building of PFAs and increasing emphasis on

SERVICECOM.

5.2 CONCLUSION

The introduction of the new contributory pension was against

the backdrop of ineffective pension management in Nigeria.

The shifting of management of pension to private sector

institution makes for efficiency in the new scheme. The

rationale for the scheme is justified by the benefits of the

contributory pension scheme.

Joint contributions by workers and government guarantee

adequate funding of this scheme. Given the improving

investment and business environment in Nigeria and viability

of bonds issued to retirees, there is no doubt that there are

prospects for the success and effectiveness of the new

contributory pension scheme.

5.3 RECOMMENDATIONS

1. The Government and PENCOM should increase their

efforts to make the scheme by ensuring that all

contributions are promptly remitted to the PFAs.

2. The PFAs should intensify their capacity building effort if

they must cope with the scheme. More competent

professional managers should be employed while current

personnel should be given continuous training.

3. Adequate information communication technology should

be procured by all PEAs to facilitate processing and

computation of benefits of retirees.

4. PACs should make prompt payments to retirees as soon

as they receive information from PEAs. They should also

make monthly benefits regular and prompt.

5. Diversion and misappropriation of Pension Funds should

receive imprisonment terms without optiuons.

BIBLIOGRAPHY Amadi, S. (2006) “Benefits of the contributory Pension scheme” Service News. Nov/Dec. Amalu, K. (2005) “Gains In The New Pension Scheme” The Vanguard, Tue. Sept. 25. Awuzie, J. (2003) “Pension Regulations and Management in Nigeria” Business Times Mon. June 6. Dike, C. (2006) Understanding the New Contributory Pension Scheme. Enugu: Providence Press. Ebegbunam P. (1999) “Management of Pension Schemes in Nigeria” A Paper delivered at a training workshop for officers in Directorial Cadre in Lagos. Eke, R. (2003) “Agenda for Reform And Effective Pension Administration In Nigeria” Text of A Lecture Delivered At The 2nd Pensions National Sumit on Contributory Pension held in Enugu. Eze, D. (2003) “Rationale For the Contributory Pension Scheme” A Paper Delivered in a Seminar held for Public Servants held in Enugu. Meribole, B. (2006) “Workers Welfare with the New Contributory Pension Scheme” Service News. Nov/Dec. Nnadi, P. (2005:45) “Angenda for Pension Reform In Nigeria” The Source. October 16. Odion, F. (2004) Management of Pension Funds In The Public Sector; The Nigerian Perspective. Lagos: Hugotek Press. Oke, H. (2006) “Origin of Pension Scheme In Nigeria” The Vanguard Feb. 28. Ola, G. (2005:24) “Pension Reform; A Good Development “The Guardian. Inc. Sept. 10.

Oladele, M. (1999:32) “Keeping Refirees Alive Through Pension Reform: I” The Herald. July, 20. Omoragbon, B. (2000:10) quoted in Dike, C. (2006:13) Op. Cit. Ugbaja, C.O. (2004:46) “Need For Pension Reform In Nigeria” The Vanguard. Feb. 28. Uzoma, K. (2005:13) Public Service Reforms; the Case For Vension Administration And Management. Lagos: Intel.

Department of Management Faculty of Business Administration School of Post-Graduate Studies UNEC March, 2008.

Dear Respondent, I am a student in the above —named Institution carrying out a study on the new contributory Pension Scheme In The Nigerian Public Sector. I want you to study this questionnaire carefully and, then; respond to the questions in it. The study is being carried out for academic purpose. And so the information you provide will be treated with strict confidentiality. Thanks for your co-operation.

I am,

Yours faithfully

Okeke, V. N.

QUESTIONNAIRE

INSTRUCTION; Please, tick (I) in the box that indicates

your of answer. Otherwise, answer the question where

necessary.

Q1. Name-----------------------------------------------------------------------

Q2. Sex (a) Males [ ] (b) Females [ ]

Q3. Age (a) Under 30 years [ ] (b) 30-4oyears [ ]

(c) 41-50 years [ ] (d) 51 -60 years [ ]

Q4. Marital status (a) Single [ ] (b) Married [ ]

(c) Others specify [ ]

Q5. Indicate your educational qualification

(a) FSLC [ ] (b) WASC/GCE [ ]

(c) NCE/OND [ ] (d) B.Sc./HND/Equiv.

(e) M.Sc/MBA/EqLliv. [ ]

(f) Others (Specify) [

Q6. Indicate your establishment

(a) National Pension Commission [ ]

(b) Pension Fund Administrator [ ]

(c) Pension Assets Custodian [ ]

Q7. What is the rationale for the new contributory pension

scheme recently introduced?

(a) Inadequate funding of the old pension scheme [ ]

(b) Complex procedures in processing pension benefits [ ]

(c) Delays in paying pension benefits [ ]

(d) Ignorance and apathy of pension fund trustees [ ]

(e) Diversion and misappropriation of pension funds [ ]

(f) All of the above [ ]

Q8. Which of the following bodies regulates and supervises

the new contributory pension scheme?

(a) National pension commission [ ]

(b) Pension fund administrators [ ]

(c) Pension assets custodians [ ]

Q9. How is the new pension scheme regulated and

supervised?

(a) The regulatory body establishes standards, rules

and operational guidelines [ ]

(b) The body approves and appoints pension fund

administrators and custodians [ ]

(c) It enlightens the public on the new pension

scheme [ ]

(d) It receives and investigates complaints against PFAs

and PACs [ ]

(e) It sanctions erring PFAs and PACs [ ]

(f) All of the above [ ]

Q1O. How is the scheme funded?

(a) Contribution by government [ ]

(b) Contribution by employees [ ]

(c) Joint contribution by government and employees [ ]

Q11. Which of the underlisted bodies administers the scheme?

(a) National Pension Commission [ ]

(b) Pension fund administrators [ ]

(c) Pension assets custodians [ ]

Q12. What are the responsibilities of the pension fund

administrators?

(a) Computation of employees retirement benefits [ ]

(b) Opening of retirement savings accounts for

employees [ ]

(c) Causing retirement benefits to be paid into the

account [ ]

(d) Investing and managing pension funds [ ]

(e) Maintaining books of accounts for retirees {J

(f) Providing customer services and relevant information

for employees [ ]

(g) All of the above [ ]

Q13. What are the responsibilities of the pension assets

custodians?

(a) Receipt of all remittances on behalf of the PEAs [ ]

(b) Keeping custody of all funds and assets [ ]

(c) Effecting payments of benefits to retirees [ ]

(d) Rendition of reports and returns on investment to

PENCOM and PFAs

(e) All of the above [ ]

Q14. In your opinion, what are the benefits of the scheme?

(a) Reduction of pension liability burden for the

government [ ]

(b) Effective funding of pension scheme [ ]

(c) Effective management of pension fund [ ]

(d) Timely payment of pension benefits [ ]

(e) All of the above [ ]

Q15. Identify the current problems of the new pension

scheme?

(a) Delays in remitting deductions to PEAs [ ]

(b) Inadequate skilled personnel for PFAs [ j

(c) Encroachment by old pension scheme management [ ]

(d) Shallow capital market for investment of

pension funds [ ]

(e) All of the above [ ]

Q16. Highlight the prospects of the scheme?

----------------------------------------------------------------------

----------------------------------------------------------------------

----------------------------------------------------------------------

----------------------------------------------------------------------

----------------------------------------------------------------------

----------------------------------------------------------------------