Embed Size (px)

Citation preview

UNIVERSITEIT GENT

FACULTEIT ECONOMIE EN BEDRIJFSKUNDE

ACADEMIEJAAR 2012 – 2013

MACROECONOMIC CONSENSUS DATA AND FINANCIAL MARKETS

Masterproef voorgedragen tot het bekomen van de graad van

Master of Science in de Toegepaste Economische Wetenschappen: Handelsingenieur

Mathias Wambeke

onder leiding van

Prof. Dr. William De Vijlder

UNIVERSITEIT GENT

FACULTEIT ECONOMIE EN BEDRIJFSKUNDE

ACADEMIEJAAR 2012 – 2013

MACROECONOMIC CONSENSUS DATA AND FINANCIAL MARKETS

Masterproef voorgedragen tot het bekomen van de graad van

Master of Science in de Toegepaste Economische Wetenschappen: Handelsingenieur

Mathias Wambeke

onder leiding van

Prof. Dr. William De Vijlder

I

PERMISSION

The undersigned declares that the content of this thesis can be consulted and/or reproduced, subject

to acknowledgement of sources.

Mathias Wambeke

II

PREFACE

When writing this thesis, I had help from multiple sources. First of all, I would like to thank Prof. Dr.

William De Vijlder for his ongoing advice and support with this subject. Also, a word of thanks to

Kristjan Kasikov (foreign exchange quantitative analyst at Citigroup) for providing me with additional

data.

III

TABLE OF CONTENTS

PREFACE .................................................................................................................................................. II

TABLE OF CONTENTS .............................................................................................................................. III

ABBREVIATIONS ....................................................................................................................................... V

LIST OF TABLES ........................................................................................................................................ V

LIST OF FIGURES ..................................................................................................................................... VI

I. INTRODUCTION ............................................................................................................................... 1

II. MACROECONOMIC SURPRISES........................................................................................................ 3

II.1. Current literature ......................................................................................................................... 3

II.1.1. Research on the macroeconomic fundamentals of asset returns ........................................ 3

II.1.2. Research on macro surprises and asset returns ................................................................... 7

II.1.3. Surprise indices.................................................................................................................... 13

II.2. Data and descriptive analysis ..................................................................................................... 14

II.2.1. Data ..................................................................................................................................... 14

II.2.2. Descriptive analysis ............................................................................................................. 16

II.3. Method and results .................................................................................................................... 20

II.3.1. Surprise indices and long term government bond returns ................................................. 21

II.3.2. Timing government bond portfolios ................................................................................... 22

II.4. Conclusion .................................................................................................................................. 26

III. DISPERSION & CONSENSUS DATA ............................................................................................. 28

III.1. Current literature ...................................................................................................................... 28

III.1.1. Dispersion of micro consensus data ................................................................................... 28

III.1.2. Dispersion of macro consensus data .................................................................................. 31

III.1.3. Pricing models and the dispersion – asset return relationship .......................................... 35

III.1.4. Gaps in current research .................................................................................................... 36

III.2. Data ........................................................................................................................................... 38

III.3. Method and results ................................................................................................................... 42

III.3.1. Stock returns and macro dispersion ................................................................................... 42

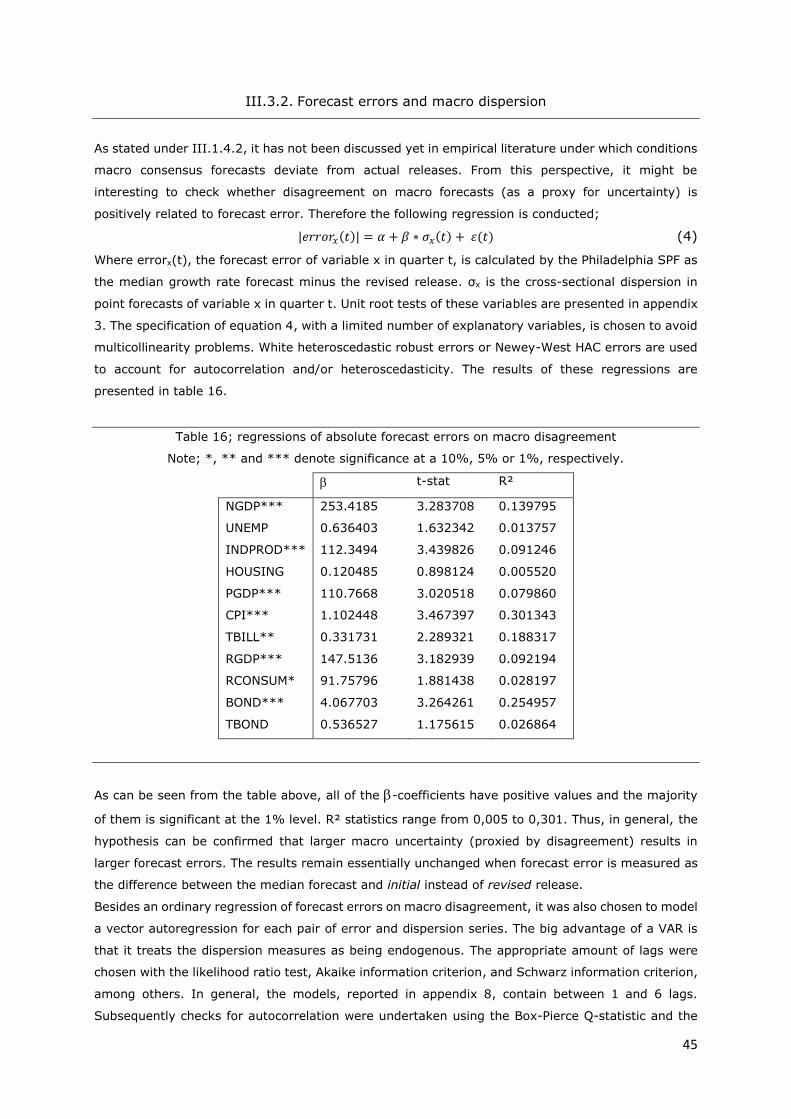

III.3.2. Forecast errors and macro dispersion ................................................................................ 45

III.3.3. Default premia and macro dispersion ................................................................................ 47

III.3.4. Preliminary conclusion ....................................................................................................... 50

III.4. Conclusion ................................................................................................................................. 51

REFERENCES .......................................................................................................................................... VII

IV

APPENDIX ............................................................................................................................................. XIII

Appendix 1 - Out of sample bond timing returns for different derivatives ................................. XIII

Appendix 2 –Bond timing strategy based on US and domestic surprise index derivatives ......... XVI

Appendix 3 - Unit root tests ........................................................................................................ XVII

Appendix 4 –Bond timing strategy based on surprise index levels ............................................ XVIII

Appendix 5 – Chow breakpoint tests ........................................................................................... XIX

Appendix 6 – Market timing for the S&P500 based on macro dispersion .................................... XX

Appendix 7 – Plot of disagreement on TBOND and 6 month S&P500 returns ............................ XXI

Appendix 8 – Granger causality tests ........................................................................................... XXI

Appendix 9 – Market timing for the default premium based on macro dispersion ................... XXII

Appendix 10 – Plot of disagreement on CPI and the 1 month default spread change .............. XXIII

Appendix 11 – Nederlandse samenvatting ................................................................................ XXIV

V

ABBREVIATIONS

ADS Aruoba – Diebold - Scotti index

CESI Citi Economic Surprise Index

CESICAD Canada Citi Economic Surprise Index

CESIEUR EMU area Citi Economic Surprise Index

CESIGBP UK Citi Economic Surprise Index

CESIJPY Japan Citi Economic Surprise Index

CESIUSD USA Citi Economic Surprise Index

ECB European Central Bank

HML High Minus Low – book to market factor

SMB Small Minus Big – size factor

SPF Survey of Professional Forecasters

UMD Up Minus Down – momentum factor

LIST OF TABLES

Table 1; Early studies on asset returns and macroeconomic variables .................................................. 3

Table 2; macroeconomic surprises and stock returns............................................................................. 8

Table 3; macroeconomic surprises and foreign exchange returns ......................................................... 9

Table 4; macroeconomic surprises and fixed income returns .............................................................. 11

Table 5; correlations between Citi Economic Surprise Indices ............................................................. 15

Table 6; long term government bond portfolios ................................................................................... 15

Table 7; money market rates ................................................................................................................ 16

Table 8; correlations between 3 month % forex returns and surprise indices ..................................... 18

Table 9; correlations between surprise indices and 3 month % returns of long term government

bonds ..................................................................................................................................................... 20

Table 10; Regressions of bond returns on surprise indices ................................................................... 21

Table 11; Market timing statistics ......................................................................................................... 25

Table 12; Philadelphia SPF macroeconomic estimates ......................................................................... 38

Table 13; correlations between dispersion measures .......................................................................... 41

Table 14; regressions of excess stock returns on macro disagreement ............................................... 42

Table 15; market timing for the S&P500 based on macro dispersion .................................................. 44

Table 16; regressions of absolute forecast errors on macro disagreement ......................................... 45

Table 17; regressions of absolute forecast errors on NBER recessions and macro disagreement ....... 46

Table 18; regressions of default premia on GDP growth, VIX and macro disagreement...................... 47

Table 19; default premium regressed on its macro determinants ....................................................... 49

Table 20; market timing for the default spread based on macro dispersion ........................................ 50

VI

LIST OF FIGURES

Figure 1; CESIUSD and S&P500 returns ................................................................................................. 17

Figure 2; CESIUSD and Euro Stoxx 50 returns ....................................................................................... 17

Figure 3; CESIEUR-CESIUSD and EURUSD returns ................................................................................. 18

Figure 4; CESIUSD-CESIJPY and USDJPY returns .................................................................................... 18

Figure 5; CESIUSD and 3 month log returns of a 30 year T bond portfolio ........................................... 19

Figure 6; CESIUSD and 3 month log returns of a 30 year EMU bond portfolio ..................................... 19

Figure 7; different measures of dispersion. .......................................................................................... 32

1

I. INTRODUCTION

Macroeconomic consensus data are pooled estimates or predictions on variables that have the

potential to determine the current state of the economy. These predictions are provided by banks or

forecasting departments of large industrial companies, and aggregated trough services such as

Bloomberg.

Although decent macro consensus data were almost non-existent about twenty years ago, they have

now gained considerable importance in financial markets and academic research. The reason for this

is quite straightforward; raw macro releases do not provide enough information to trade, as financial

markets only react to unexpected components of news. Therefore, it will be the difference between

macro releases and the corresponding consensus that will be determinant on the reaction of

investors. Indeed, simple macroeconomic releases do provide insight into the overall state of the

economy, but they aren’t useful for financial markets unless they are considered simultaneously with

their respective consensus estimates.

The increasing interest of financial market actors in macro consensus estimates is clearly linked to

the wide availability of this type of data. For example, Bloomberg now provides a large set of pooled

USA macro estimates, ranging from GDP growth rates and nonfarm payrolls to unit labor costs.

Reviews dedicated solely to macro consensus data have emerged, e.g. ConsensusEconomics®.

Central banks are also clearly interested in macro estimates; both the ECB and the Federal Reserve

Bank of Philadelphia now manage their own Survey of Professional Forecasters (SPF).

Literature dealing with the effect of macroeconomic surprises1 on asset markets has become quite

mature over time. Numerous studies have shown that financial markets (including stock markets,

fixed income and forex) react to the surprise of macro releases. These researches often apply

sophisticated econometric models (see for example Andersen, Bollerslev, Diebold and Vega, 2003)

and managed to get, over time, some agreement on which macro surprises affect asset markets

under which conditions (cf. supra).

Another interesting application of macro consensus data resides in its potential to proxy for

uncertainty. Arnold and Vrugt (2008) and Glansbeek and Ivo (2011) use the dispersion of macro

estimates to establish a link between volatility in financial markets and macroeconomic uncertainty.

Furthermore, Dopke and Fritsche (2006) find that macro uncertainty is particularly high before and

during recessions.

In this thesis, multiple gaps in current literature on macro consensus data are identified. First of all,

the market timing potential of macro surprise indices will be assessed. These indices aggregate the

surprises of multiple macroeconomic series into a comprehensive surprise measure. Although this

1 defined as the standardized difference between a macro release and the corresponding consensus

estimate

2

type of data provides an interesting way of dealing with the surprise of macro consensus estimates,

it has hardly been discussed in literature so far.

A second gap in extant research is the application of macroeconomic uncertainty in relationship to

stock returns. The past use of dispersion in macro consensus data was limited to assessing its impact

on asset volatility or other more descriptive approaches. In thesis, it will be verified whether this

macro uncertainty is a measure of non-diversifiable risk, and whether it is therefore linked to

innovations in stock markets. Furthermore, dispersion in macro estimates will be used in two other

domains; we will check how dispersion and macro surprises are related, and whether macro

uncertainty can explain default premia.

The structure of this thesis is as follows; the first part will deal with macro surprises and starts with

an overview of current literature about the effect of macro variables, macro surprises and macro

surprise indices on asset prices. Subsequently, data and descriptive analysis are provided, followed

by market timing models for government bonds based on macro surprise indices. Next, the results

and preliminary conclusion are given.

The second part of this thesis will deal with the dispersion of consensus estimates. It starts with an

overview of related literature on micro and macro consensus data, after which multiple gaps in

current research are identified. Subsequently information is provided on consensus forecasts

obtained from the Philadelphia SPF. The following section describes our econometric models and

provides the results; the last part concludes.

In the next pages, this thesis will present that macro surprise indices have the potential of

determining a profitable market timing strategy for long term government bonds, though to a limited

extent. Also documented is a clear effect of macro dispersion on subsequent surprises and default

premia. However, the dispersion of macroeconomic consensus data does not appear to have a clear

relationship to stock returns, nor can it be used for a stock market timing or default premium timing

strategy.

3

II. MACROECONOMIC SURPRISES

II.1. Current literature

This literature overview starts with some early studies on the link between asset returns and macro

fundamentals. Next, a review of papers studying the effect of macro surprises on stock, forex and

bond returns is provided. The section ends with some notes on macro surprise indices. Unless

mentioned otherwise, results are reported for US markets and US macro variables.

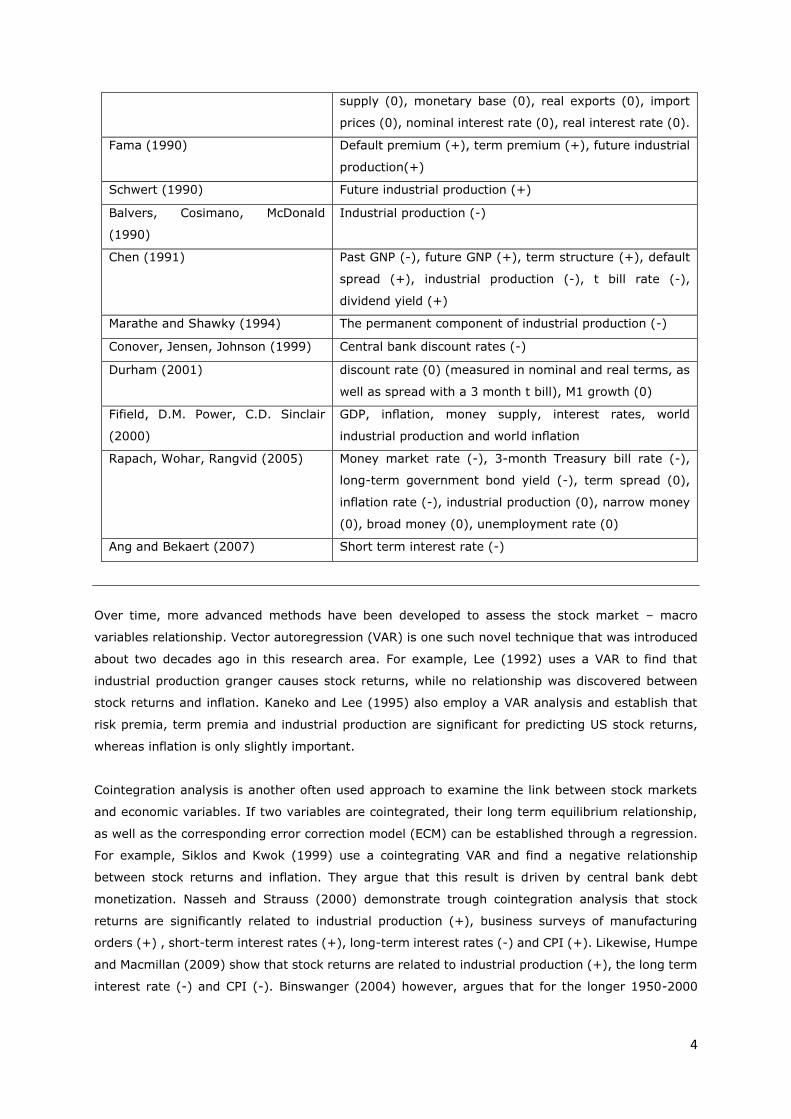

II.1.1. Research on the macroeconomic fundamentals of asset returns

II.1.1.1. Stock markets

The first articles on the link between stock returns and macro variables were published around the

year 1980. These early studies simply used regressions of asset returns on current, lagged or future

innovations of macro variables. There is a large discrepancy in the conclusions of the researches

applying this method, with some authors revealing significant coefficients for macro variables (e.g.

Fama, 1990), while others admit having discovered no relationship at all (e.g. Cutler, Poterba, and

Summers, 1989). Many authors discern a significant negative relationship between inflation, interest

rates and stock returns, while evidence for real activity measures (industrial production, GNP) is

mixed at best. The table below provides a short overview of these early publications.

Table 1; Early studies on asset returns and macroeconomic variables

Note; (+) indicates a positive relationship with stock returns, (-) indicates a negative relationship,

(0) indicates no relationship

Author (year of publication) Coefficients evaluated

C.R. Nelson (1976) Inflation (-)

Fama, G.W. Schwert (1977) Inflation (-)

Fama (1981) Inflation (-), future capital expenditures (+), future

industrial production (+), future real GNP (+)

Solnick (1984) Interest rates (-)

Kaul (1987) Inflation (-), M1 (-),industrial production (+), real GDP (+)

Asprem (1989) Employment (-), imports (-), inflation (-) interest rates (-

), future industrial production (+), capital expenditures

(0)), measures for money supply (+) and the U.S. yield

curve (+), consumption (0)

Fama and French (1989) Default premium (+), term premium (+)

Cutler, Poterba, Summers, 1989 Industrial production (0), CPI (0), M1 (0), long-term

interest rates (0), 3 month t bill rate (0)

Wasserfallen (1989) Real GNP (0), Industrial production (0), real consumption

(0), real investment (0), consumer prices (0), money

4

supply (0), monetary base (0), real exports (0), import

prices (0), nominal interest rate (0), real interest rate (0).

Fama (1990) Default premium (+), term premium (+), future industrial

production(+)

Schwert (1990) Future industrial production (+)

Balvers, Cosimano, McDonald

(1990)

Industrial production (-)

Chen (1991) Past GNP (-), future GNP (+), term structure (+), default

spread (+), industrial production (-), t bill rate (-),

dividend yield (+)

Marathe and Shawky (1994) The permanent component of industrial production (-)

Conover, Jensen, Johnson (1999) Central bank discount rates (-)

Durham (2001) discount rate (0) (measured in nominal and real terms, as

well as spread with a 3 month t bill), M1 growth (0)

Fifield, D.M. Power, C.D. Sinclair

(2000)

GDP, inflation, money supply, interest rates, world

industrial production and world inflation

Rapach, Wohar, Rangvid (2005) Money market rate (-), 3-month Treasury bill rate (-),

long-term government bond yield (-), term spread (0),

inflation rate (-), industrial production (0), narrow money

(0), broad money (0), unemployment rate (0)

Ang and Bekaert (2007) Short term interest rate (-)

Over time, more advanced methods have been developed to assess the stock market – macro

variables relationship. Vector autoregression (VAR) is one such novel technique that was introduced

about two decades ago in this research area. For example, Lee (1992) uses a VAR to find that

industrial production granger causes stock returns, while no relationship was discovered between

stock returns and inflation. Kaneko and Lee (1995) also employ a VAR analysis and establish that

risk premia, term premia and industrial production are significant for predicting US stock returns,

whereas inflation is only slightly important.

Cointegration analysis is another often used approach to examine the link between stock markets

and economic variables. If two variables are cointegrated, their long term equilibrium relationship,

as well as the corresponding error correction model (ECM) can be established through a regression.

For example, Siklos and Kwok (1999) use a cointegrating VAR and find a negative relationship

between stock returns and inflation. They argue that this result is driven by central bank debt

monetization. Nasseh and Strauss (2000) demonstrate trough cointegration analysis that stock

returns are significantly related to industrial production (+), business surveys of manufacturing

orders (+) , short-term interest rates (+), long-term interest rates (-) and CPI (+). Likewise, Humpe

and Macmillan (2009) show that stock returns are related to industrial production (+), the long term

interest rate (-) and CPI (-). Binswanger (2004) however, argues that for the longer 1950-2000

5

period, no clear cointegrating relationship can be found in G-7 countries for real GDP, industrial

production, and stock returns.

A recent strand in literature searches for regime dependent macro effects on stock returns. An often

used approach is to construct a two state Markov model for stock returns, which in practice almost

always results in a high return – low variance and a low return – high variance regime. Next, the

influence of macro variables on stock returns is assessed for each of the two regimes, (potentially)

together with the effect of macro variables on transition probabilities. For example, Perez-Quiros and

Timmermann (2000) find a significant influence of the 1 month t bill rate (-) and default premium

(+) during the low return – high variance regime, while these variables don’t affect stock returns

during high return – low variance periods. Similarly, Chang (2009) finds that the 3 month t bill rate

(-) and default premium (+) significantly affects stock markets during the low return – high volatility

regime, but not so for high return – low volatility periods. Chen (2007) shows that M2 growth (+),

the federal funds rate (-) and discount rate (-) significantly affect stock markets, but this relationship

appears to be stronger during bear market regimes. Furthermore, it is shown that decreasing

discount rates lead to a higher probability of switching to a bear-market period.

In summary, there is a vast amount of literature available on the link between macroeconomic factors

and stock market returns. Although multiple authors find a significant relationship between inflation

(-), interest rates (-) and stock returns, results for measures of real economic activity (industrial

production, GDP, employment etc.) are mixed at best. It could be argued that this lack of clarity is

partially due to the fact that only a limited number of papers take into account time varying

coefficients for macro variables. Moreover, all of the above papers ignore the existence of consensus

data. This seems problematic, as classic investment theory states that asset prices only respond to

the unexpected component of (macroeconomic) news. Therefore, only taking into account macro

series without their respective consensus estimates seems like an invalid measure of macroeconomic

influences, therefore making spurious data mining results likely. The next section (II.1.2) will thus

pay considerable attention to researches that do take into account macro surprises, not just raw

macroeconomic announcements.

II.1.1.2. Foreign exchange

Most of the research about macroeconomic effects on forex rates has focused on the so-called

fundamental models. These include (i) the flexible price monetary model, (ii) sticky price monetary

model, (iii) the productivity differential model and (iv) models based on the Taylor rule.

The flexible price (Frenkel-Bilson) model defines an exchange rate as the relative price resulting from

the demand and supply for two moneys. Other key assumptions made by this model include that (1)

domestic and foreign assets are perfect substitutes; (2) purchasing power parity (PPP) holds at all

times; and (3) the uncovered interest parity (UIP) holds at all times. The resulting model is given

by;

s = a0 + a1*(m-mf) + a2(y-yf) + a3*(rs-rsf) + u

6

where s is the logarithm of the domestic price of foreign currency, m is the logarithm of money

supply, y is the logarithm of real income, rs is the short-term interest rate, and u is an error term.

The subscript f indicates foreign variables.

The sticky-price (Dornbusch-Frankel) model does not assume the PPP to hold continuously; the goods

market prices are presumed to be sticky, at least in the short run. Exchange rates and interest rates

therefore have to compensate for this price stickiness, and thus exchange rates can “overshoot” their

long-run equilibrium rates. The resulting equation is given by;

s = a0 + a1*(m-mf) + a2(y-yf) + a3*(rs-rsf) + a4*(e-ef) + u

wheree is the expected long-run inflation.

The alternative sticky price (Hooper-Merton) model also allows the long-run real exchange rate to

fluctuate. These real exchange rate changes are presumed to be caused by unanticipated trade

balance shocks. The resulting equation is;

s = a0 + a1*(m-mf) + a2(y-yf) + a3*(rs-rsf) + a4*(e-ef) + a5*TB + a6*TBf + u

where TB is the cumulated trade balance.

A third type of fundamental models accords a central role to productivity differentials in explaining

real exchange rate fluctuations. These Balassa–Samuelson models hypothesize that PPP only holds for

tradable goods, whereas non-tradables are a function of productivity differentials (z). In other words,

the Balassa-Samuelson model holds if (1) the productivity differential between traded and non-traded

sectors are positively correlated to relative prices; (2) the ratio of traded versus non-traded good prices

increases with per capita GDP; (3) real exchange rate are positively correlated to relative prices of non-

tradables. A generic version of this model is thus given by;

s = a0 + a1*(m-mf) + a2(y-yf) + a3*(rs-rsf) + a4*(z) + u

A final type of fundamental model is based on the Taylor rule. Assuming that the UIP holds, this

model gives;

s = a0 + a1* - a2*f + a3*y – a4*yf + a5*q + a6*rs – a7*rsf + u

where q is the real exchange rate.

An elaborate strand in literature investigates whether these fundamental models have out-of-sample

explanatory or predictive power. In a well-known paper, Meese and Rogoff (1983) find that a random

walk performs as well as the Frenkel-Bilson, Dornbusch-Frankel and Hooper-Morton models in terms

of out-of-sample forecasting accuracy, even when including future realized values of explanatory

variables.

In the more recent literature, multiple researchers have found significant out-of-sample predictability

for fundamental models, though mainly in the long run. These researchers include Chinn and Meese

(1995), who find some predictive power at a 3 year horizon for the Frenkel-Bilson, Dornbush-Frankel

and Balassa–Samuelson model. Kim and Mo (1995) corroborate these findings, while MacDonald and

Taylor (1994), Mark (1995) and Mark and Sul (2001) use the Frenkel-Bilson model to conclude that

it has predictive ability for the short run (1 month) as well as the long run (up to 4 years).

7

Recent literature has also found some significant short term out-of-sample predictive ability for

fundamental models based on the Taylor rule. Molodtsova, Nikolsko and Papell (2008) come to this

conclusion by using the USD/DM exchange rate, while Molodtsova and Papell (2009) confirm these

findings for 11 different currencies (out of 12 tested) vis-à-vis the U.S. dollar. Molodtsova, Nikolsko

and Papell (2008) also find evidence of short-term predictability using the EUR/USD rate.

However, these findings on significant predictability have not remained without criticism. Berben and

van Dijik (1998), for example, casts doubt on the “stylized fact” that predictability increases for

longer horizons. While the cointegration is generally assumed in papers about forex fundamentals,

it can be shown that alternative critical values under the null of no cointegration can counter classic

findings of significant long-run predictability. These results are corroborated by Berkowitz and

Giorgianni (2001). Kilian (1999) emphasizes biases due to small-samples and spurious regression

fits; he develops a novel bootstrap method to account for small-sample inference, and consequently

finds no long-run forex predictability using this new technique. Nikolsko-Rzhevskyy and Prodan

(2012) argue that the alleged predictive ability of fundamental models is partly due to the inclusion

of constant drift terms. He models this drift term as a Markov switching model and finds robust

evidence for short term as well as long-run (1 year) forex predictive ability. Lastly, Cheung, Chinn,

and Pascual (2005) don’t find any predictive power for the PPP, Dornbusch-Frankel, Balassa–

Samuelson or composite model at horizons ranging from 1 up to 20 quarters. Just like Meese and

Rogoff (1983), they conclude that no fundamental model is consistently superior to a normal random

walk.

Research on the Balassa-Samuelson (B-S) hypothesis also produced mixed results. For example,

Solanes, Portero and Flores (2008) do find that productivity differentials between traded and non-

traded sectors are positively correlated to relative prices, but they cannot prove that inter-country

productivities are linked to real exchange rate innovations, and therefore find no evidence in favor

of the B-S model. These findings hold for new as well as old member states of the EU. Drine and

Rault (2005) on the other hand, confirm the B-S hypothesis for 8 out of 12 OECD countries, similar

to Chong, Jorda and Taylor (2012), who confirm the B-S model for 21 OECD member states, although

they find a substantial variation in results across countries. Lastly, Dumrongrittikul (2012) found

that, for 17 developing countries, in favor of the B-S model, higher productivity for traded goods

leads to real forex rate appreciation, while opposite results hold for 16 developed countries.

It can be concluded that the results for these fundamental models, relating forex rates to

macroeconomic fundamentals, are mixed at best. As Meese and Rogoff (1983) already pointed out,

this might be due to not properly taking into account expectations of explanatory variables. Again,

the argument is that looking for a macro surprise effect on short term forex rates might be a

fundamentally better way of searching for link between forex and macro variables.

II.1.2. Research on macro surprises and asset returns

The disappointing results from conventional regressions denoted in the previous part have made

academics look for more advanced methods for research on the link between macro variables and

asset returns. Literature using macroeconomic surprises (defined as the standardized difference

8

between a macro release and the corresponding consensus estimate) is becoming more and more

common practice. This type of research often uses high frequency returns to reduce the potential

effect of other, non-macroeconomic variables. The econometric models of this approach have become

quite mature over time, with the regressions including GARCH terms to account for conditional

heteroscedasticity of daily returns, calendar effects to account for intraday patterns of volatilities etc.

Results are also often controlled for different states of the economy, as it could be that, e.g.

unemployment news has a time-varying effect on asset returns, dependent on whether the current

state is defined as a recession or expansion. These different economic states can be determined

based on several indices or variables, such as the trend of industrial production, Aruoba-Diebold-

Scotti (ADS) index or the NBER classification of economic states.

The following section will briefly examine the main results of the prevailing literature concerning the

effect of macro surprises on stock markets, foreign exchange and bond markets.

II.1.2.1. Stock markets

An overview of literature (see table 2) reveals some consistent results on the macro variable – stock

return relationship; CPI, PPI and money supply have an overall negative effect on stock returns,

nonfarm payrolls have a negative effect on stock markets during economic expansion and a positive

effect on stock returns during recession, while the opposite holds for unemployment.

A lot of variables that are commonly used to proxy for economic activity, such as industrial

production, GDP, retail sales etc. do not show any relationship with stock returns.

Table 2; macroeconomic surprises and stock returns

Note; (+) indicates a positive relationship with stock returns, (-) indicates a negative relationship,

(0) indicates no relationship

Author Surprise coefficients evaluated

Pearce and Roley

(1983)

Money supply (-).

Pearce and Roley

(1985)

Money supply (-), discount rate (-), PPI (-). CPI (0), industrial production

(0), unemployment (0).

McQueen and Roley

(1993)

Money supply (-) and PPI (-), not conditional on the state of the economy.

Industrial Production (- during expansions) Merchandise trade deficit (-

during expansions), CPI (- in medium state), unemployment (+during

expansions). Nonfarm payrolls (0), discount rate (0).

Flannery and

Protopapadakis (2002)

CPI (-), PPI (-), M1 (-). Several of the lagged conditioning variables also

have significant coefficients in the expected returns equation; the value-

weighted market index (+), 3 month treasury bill rate (-), treasury term

premium (-), and the dividend-price ratio (+).

Balance of trade (0), consumer credit (0), construction spending (0),

nonfarm payrolls (0), unemployment, new home sales (0), housing starts

(0), industrial production (0), leading indicators (0), M2 (0), personal

consumption (0), personal income (0), Real GDP (0), retail sales (0).

9

Kim, McKenzie & Faff

(2004)

CPI (-) and PPI (-).

Balance of trade (0), GDP (0), unemployment (0), retail sales (0).

Adams, McQueen and

Wood (2004)

PPI (-) CPI (-).

Poitras (2004) Nonfarm payrolls (- during expansions, + during recessions), CPI (-), PPI

(-), and the discount rate(-).

Industrial production (0), unemployment rate (0), M1 (0).

Boyd et al. (2005) Unemployment (+ during expansions, - during contractions).

Andersen et al. (2007) Nonfarm payrolls (- during expansions, + during contractions), durable

goods orders (- during expansions, + during contractions), initial

unemployment claims (0 during expansions, - during recessions), PPI (-

during expansions, 0 during contractions).

Cenesizoglu (2011) Nonfarm Payrolls (- during expansions, 0 during recessions), hourly

earnings (-), trade Balance (+), export price index (-) and core CPI (-),

fed funds target rate (-).

Real GDP (0), unemployment rate (0), retail sales (0), industrial

production (0), personal income (0), consumer credit (0), new home

sales (0), PCE (0), construction spending (0), import price index (0), PPI

(0), core PPI (0), CPI (0), housing starts (0), leading indicators (0).

II.1.2.2. Foreign exchange

Compared to research on forex fundamental models, an approach using surprises allows assessment

of a much wider array of macro variables. Whereas fundamental models are generally limited to

money supply, inflation, interest rates, real income and trade balances, the surprise approach does

not a priori exclude any macroeconomic release. Theoretically, it is expected that positive domestic

economic surprises will increase the domestic interest rates, leading to an appreciation of the

exchange rate. The main results show that foreign exchange markets react to macro surprises as

expected a priori (see table 3). Although this literature overview shows some variability with respect

to which macro variables have a significant effect on forex rates, it is clear that these inconsistencies

are mainly due to the length of the data series employed or other irregularities in the measurement

of returns or surprises. For example, Kim, McKenzie and Faff (2004) use daily returns instead of high

frequency returns, leading to a large amount of insignificant surprise coefficients. In general, foreign

exchange markets react significantly to surprises of economic activity (GDP, industrial production,

retail sales, durable goods orders), nonfarm payrolls, unemployment, balance of trade and the

federal funds rate. These consistent results for a large number of macroeconomic releases clearly

show the value of using consensus data in this type of research.

Table 3; macroeconomic surprises and foreign exchange returns

Author (year) Surprise variable with theoretically

expected coefficient

Surprise variable with

insignificant coefficient

10

Andersen, Bollerslev,

Diebold, and Vega

(2003)

GDP (advance and preliminary),

nonfarm payrolls, retail sales,

industrial production, durable goods

orders, construction spending, factory

orders, trade balance, PPI, CPI,

consumer confidence index, NAPM

index, housing starts, target federal

funds rate, initial unemployment

claims, M1, M2 and M3.

Capacity utilization, personal

income, consumer credit,

personal consumption

expenditures, new home sales

business inventories,

government budget deficit,

index of leading indicators.

Kim, McKenzie, Faff

(2004)

Balance of trade. GDP, unemployment, retail

sales, PPI, CPI.

Andersen, Bollerslev,

Diebold and Vega

(2007)

Nonfarm payrolls, durable goods

orders, initial unemployment claims.

PPI.

Faust, Rogers, Wang,

and Wright, (2007)

Federal funds rate, GDP, initial

unemployment claims, nonfarm

payrolls, retail sales, trade balance

and unemployment

CPI, PPI, housing starts.

II.1.2.3. Fixed income

From a theoretical perspective, it is expected that “good” economic surprises (i.e. macro

announcements indicating a stronger than expected economy) will increase interest rates, and

therefore reduce bond and bill prices. An overview of the macro surprise effect on fixed income

returns (see table 4) largely confirms this theoretical viewpoint; in general surprises denoting “good”

news indeed increase fixed income rates. The variables that generally support this empirical finding

include GDP, industrial production, nonfarm payrolls, initial jobless claims, unemployment, retail

sales, factory orders, durable goods orders, consumer confidence, the NAPM index, housing starts,

money supply, CPI, and PPI. The only macro variables which are consistently categorized as

insignificant are business inventories, the balance of trade and balance of trade proxies.

A priori we don’t expect to see any time-varying effects of macro surprises on interest rates. Only a

few papers report research on whether the state of the economy could influence the macro surprise

– interest rate relationship; McQueen and Roley (1993) and Andersen, Bollerslev, Diebold and Vega

(2007) find constant effects of surprises on interest rates, regardless of the state of the business

cycle. On the other hand, Boyd et al. (2005) find that unemployment surprises have a negative effect

on interest rates in expansions, but no effect during economic contractions.

The papers listed in table 4 report returns of long term bonds as well as short term bills. In general,

all maturities (from 3 month bills up to 30 year bonds) react significantly to surprise in macro

announcements. However, the term structure of US (and foreign) interest rates doesn’t simply move

vertically in response to macroeconomic news; McQueen and Roley (1993) and Faust, Rogers, Wang,

and Wright (2007) show that short and medium term interest rates are more sensitive to macro

surprises than long term rates, or as Faust et al. (2007, p. 1057) put it; “the effect is hump shaped

11

with a maximum effect at about 2 years”. Even though long term rates are less sensitive to macro

surprises, it is clear that, due to their higher duration, prices of long term bond portfolios will react

more strongly than short term bills. This is clearly shown by Balduzzi, Elton, and Green (2001), who

compare prices of 3 month bills, 2 and 10 year notes and 30 year bonds.

It is interesting to note that the effect of US macro surprises reported in table 4 holds for US as well

as EMU fixed income markets; indeed, different authors such as Ehrmann and Fratzscher (2005),

Andersson, Overby and Sebestyen (2009) and Andersen, Bollerslev, Diebold and Vega (2007) find

that Euro area bonds react significantly to US macro surprises, and that this effect is stronger than

for the equivalent euro area surprises. As Ehrmann and Fratzscher (2005, p. 928) put it; “In recent

years certain US macroeconomic news affect euro area money markets and have become good

leading indicators for the euro area”. Similarly, Andersson et al. (2009) find that German government

bond futures react more strongly to US macro surprises compared to German and euro area

announcements. They find that the effect of US releases has become more important during the

period considered (’99-’05).

Finally, it should be noted that two papers in table 4 found a rather high number of insignificant

surprise coefficients; this is notably the case for Kim, McKenzie and Faff (2004) and Ehrmann and

Fratzscher (2005). This is mainly because these two papers use daily return data, whereas other

papers generally use high-frequency returns.

Table 4; macroeconomic surprises and fixed income returns

Author (year) Surprise variables with a theoretically

expected coefficient

Surprise variable with an

insignificant coefficient

McQueen and

Roley (1993)

Industrial production, unemployment,

nonfarm payrolls, PPI, CPI, M1, fed funds

discount rate.

Merchandise trade deficit.

Balduzzi, Elton,

and Green

(2001)

Durable goods orders, housing starts, initial

jobless claims, nonfarm payrolls, PPI, CPI,

consumer confidence, NAPM index, new home

sales, unemployment, retail sales, capacity

utilization, industrial production, factory

orders, M2.

Leading indicators,

merchandise trade balance,

US imports, US exports,

business inventories,

construction spending,

personal consumption,

personal income, treasury

budget, M1, M3.

Hautsch and

Hess (2002)

Nonfarm payrolls, unemployment, hourly

earnings, NAPM index, overall CPI, core CPI,

housing starts, M2, Retail Sales.

Kim, McKenzie,

Faff (2004)

Retail sales, PPI and CPI. Balance of trade, GDP,

unemployment

Boyd et al.

(2005)

Unemployment news in expansions Unemployment news in

contraction

12

Ehrmann and

Fratzscher

(2005)

Feral funds target rate, NAPM index, nonfarm

payrolls, consumer confidence, retail sales.

Industrial production, GDP,

CPI, unemployment rate, PPI,

housing starts, trade balance.

Andersen,

Bollerslev,

Diebold and Vega

(2007)

Durable goods orders, nonfarm payrolls, initial

jobless claims, PPI.

Faust, Rogers,

Wang, and

Wright (2007)

GDP, retail sales, housing starts, initial jobless

claims, unemployment, nonfarm payrolls, PPI,

CPI, trade balance, Federal funds rate.

Andersson,

Overby,

Sebestyen

(2009)

GDP, industrial production, nonfarm payrolls,

initial jobless claims, retail sales, factory

orders, durable goods orders, University of

Michigan consumer sentiment index, Chicago

PMI, consumer confidence, Philadelphia Fed

Business Outlook Survey, ISM non-

manufacturing confidence, CPI, PPI.

Business inventories.

From the discussion above, it is clear that the use of consensus data and the corresponding macro

surprises is a relevant way of searching for the macro variable – asset return relationship. Whereas

previous literature was generally not able to link asset prices to their macro fundamentals, the novel

papers combining consensus data and high frequency returns have provided more consistent findings.

This holds for stock markets, forex as well as bond returns. Andersen, Bollerslev, Diebold and Vega

(2007, p. 251), who search for the effect of macro surprises on different asset classes, conclude; “We

find that news produces conditional mean jumps; hence high-frequency stock, bond and exchange rate

dynamics are linked to fundamentals”.

However, this approach using macro surprises to explain high frequency returns entails some

downsides;

- The interaction or aggregation of macro surprises has hardly been discussed in literature so far.

For example, Andersen et al. (2003, 2007) only consider the joint effect of macro surprises if the

corresponding announcements are released at the same time.

- Macro expectations often show long periods of too optimistic forecasts, followed by long periods

of too pessimistic forecasts (cf. supra). This effect is ignored by the papers listed above.

- High frequency returns provide, per definition, only very limited and short term insight into the

evolution of asset prices. The results from these papers can hardly be used for an asset allocation

or market timing strategy.

Surprise indices, discussed in the next paragraphs, are a novel way of searching for a macro surprise –

asset return relationship, and potentially can surpass some of the shortcomings listed above.

13

II.1.3. Surprise indices

Surprise indices allow to track the performance of economic forecasts by aggregating past

macroeconomic surprises into a comprehensive index. The first surprise indices emerged some 15

years ago, and often have been quoted in popular press2 ever since. The popularity of surprise indices

is also clearly denoted by the large number of banks who have now created their own surprise index.

The best known examples include the Citigroup Economic Surprise index (CESI), Bloomberg

Economic Surprise index, HSBC US activity index, Schroders’ index, and the JP Morgan Economic

Activity Surprise Index (EASI). In a recent press release3, JP Morgan claimed that; “Almost all large

dollar drops in recent years have coincided with phases of pessimism as defined by the EASI, (…)

and trading EASI signals would have delivered annual returns of 8.2%”.

Despite the apparent popularity and usefulness of surprise indices, literature on this type of data is

almost nonexistent. The only noteworthy paper is by Scotti (2012), who compares the US Citigroup

Economic Surprise index with a self-created macro surprise index. In this paper, surprise indices are

used in an ordinary regression to explain foreign exchange returns. Although the R² of these

regressions are rather low (<0,05), the surprise indices are often significant and generally have the

right sign (a positive change in the US surprise index appreciating the US dollar and vice versa).

Because of the apparent lack of literature on surprise indices (except for the work of Scotti, 2012),

these indices will be subsequently discussed further in this thesis. More concretely, investigation will

be carried out as to whether these indices are linked to past asset returns, and whether they can

predict future returns. It will be researched whether it is possible to deduct an asset allocation

strategy from the evolution of a surprise index; specifically, checking whether these indices can be

used for the market timing of bond portfolios with a high duration.

By doing so, this thesis will be different from conventional macro surprise research (cf. infra II.1.2)

because;

- Individual surprises are aggregated into an all-inclusive surprise index. In such a setting,

individual surprises are not of interest anymore; on the contrary, this type of research investigates

whether it is the aggregation of surprises that contains additional information.

- High frequency returns are not used; rather it is assessed whether longer term asset returns

respond to aggregated surprises.

- This thesis is not limited to a descriptive approach; the aim is to look for an effective market

timing strategy.

2 See, for example, Friedman (2012) or Levkovich (2012). 3 JPMorgan, February 7, 2002, JPMorgan introduces the economic activity surprise index, URL; <http://investor.shareholder.com/jpmorganchase/releasedetail.cfm?releaseid=145456>

14

II.2. Data and descriptive analysis

This section starts with a brief description of the surprise indices and asset returns used in the

empirical models of this thesis. This is followed by a visual comparison of surprise indices and the

returns on different asset classes, and calculations of the corresponding correlations.

II.2.1. Data

The specific surprise index used in this thesis will be the Citigroup Economic Surprise Index (CESI).

Bloomberg provides the following definition; “The Citigroup Economic Surprise Indices are objective

and quantitative measures of economic news. They are defined as weighted historical standard

deviations of data surprises (actual releases vs Bloomberg survey median). A positive reading of the

Economic Surprise Index suggests that economic releases have on balance been beating consensus.

The indices are calculated daily in a rolling three-month window. The weights of economic indicators

are derived from relative high-frequency spot FX impacts of 1 standard deviation data surprises. The

indices also employ a time decay function to replicate the limited memory of markets.”

CESI series have been obtained for a total of 11 different regions (Australia, Canada, Switzerland,

Euro area, Japan, Norway, New Zealand, Sweden, United Kingdom, United States and the G10), with

daily data ranging from April 1998 until January 2013. Table 5 provides correlations between the

different indices. Except for the United States, most CESI indices have a rather poor coverage of

expectation surveys in the years 1998 until 2003. Therefore, interpretation of CESI indices in this

early period might be misleading.

The method of calculating CESI indices is also subject to criticism. As Citigroup calculates weights

based on reaction of forex markets to news surprises, it is depicted as subjective in the sense that it

might leave out otherwise important macro announcements. Scotti (2012, p. 19), on the other hand

calculates weights based on the contribution of the macro announcement to an unobserved common

factor, and therefore argues that this method “represents a more objective measure of deviation

from consensus expectations”. Alternatively, HSBC activity indices are simply calculated by the sum

of all economic surprises since the creation of the indices, which therefore allows visualization of runs

of surprises in little-watched data.

Despite this criticism, it was decided to continue with the CESI as it is the best known surprise index

and one of the only indices with publicly available data.

The government bond portfolio returns used in section II.3 are obtained from Datastream.

Specifically considered are bond portfolios with a high duration because, as demonstrated by Balduzzi

et al. (2001), long term bond portfolios have the strongest reaction to macro surprises. Table 6

provides an overview of the specific portfolios and their data range.

15

Table 5; correlations between Citi Economic Surprise Indices

CESI

CAD

CESI

EUR

CESI

G10

CESI

JPY

CESI

NZD

CESI

NOK

CESI

SEK

CESI

CHF

CESI

GBP

CESI

USD

CESI

AUD

CESICAD 1.0000

CESIEUR 0.1180 1.0000

CESIG10 0.2274 0.7241 1.0000

CESIJPY 0.0162 0.0784 0.2287 1.0000

CESINZD 0.1427 0.1001 -0.0078 -0.0615 1.0000

CESINOK -0.0144 -0.1033 -0.0521 -0.1542 -0.0816 1.0000

CESISEK -0.0756 0.1871 0.1472 -0.0787 -0.0827 0.0954 1.0000

CESICHF 0.3122 0.3352 0.3395 0.0703 0.0322 -0.1349 0.0633 1.0000

CESIGBP -0.0803 0.1641 0.3521 0.0093 -0.0448 -0.0259 0.1417 -0.1410 1.0000

CESIUSD 0.1271 0.1873 0.7874 0.0498 -0.1048 0.0197 0.0493 0.17026 0.2862 1.0000

CESIAUD 0.1797 -0.0141 0.1104 -0.0034 0.0054 0.1243 -0.0101 0.0352 0.0795 0.0950 1.0000

Table 6; long term government bond portfolios

Portfolio Datastream

mnemonic Data range

Canada 30 year government bond return

index BMCN30Y(RI) 1/4/’98 – 31/1/’13

EMU 30 year government bond return index BMEM30Y(RI) 1/1/’99 – 31/1/’13

Japan 30 year government bond return index BMJP30Y(RI) 31/12/’99 – 31/1/’13

UK 30 year government bond return index BMUK30Y(RI) 1/4/’98 – 31/1/’13

UK 50 year government bond return index BMUK50Y(RI) 31/5/’05 – 31/1/’13

USA 30 year government bond return index BMUS30Y(RI) 1/4/’98 – 31/1/’13

The return indices are calculated by the formula;

𝑅𝐼𝑡 = 𝑅𝐼𝑡−1 ∗ ∑ (𝑃𝑖,𝑡 + 𝐴𝑖,𝑡 + 𝐶𝑃𝑖,𝑡 + 𝐺𝑖,𝑡) ∗ 𝑁𝑖,𝑡−1𝑖

∑ (𝑃𝑖,𝑡−1 + 𝐴𝑖,𝑡−1 + 𝐶𝑃𝑖,𝑡−1) ∗ 𝑁𝑖,𝑡−1𝑖

Where P is the middle price of the bond, A is the accrued interest, Gi,t is the value of any coupon

payment received from the ith bond at time t since time t-1, N is the nominal value of the amount

outstanding, CP is the value equal to the next coupon payment in the ex-dividend period or 0 outside

the ex-dividend period.

The money market rates used in section II.3 are presented in table 7. The overnight currency

deposits are obtained from Bloomberg, while the Japanese overnight uncollateralized call money rate

is obtained from Datastream.

Other series used in section II.2.2 include the S&P500, Euro Stoxx 50, and USD exchange rates,

which are obtained from Bloomberg. Data ranges from April 1998 up to January 2013. Returns are

generally calculated using past 3 month percentages or natural log differences.

16

Table 7; money market rates

Portfolio Mnemonic Data range

CAD overnight deposit CDDR1T 1/4/’98 – 31/1/’13

EUR overnight deposit EUDR1T 1/1/’99 – 31/1/’13

Japan overnight uncollateralized call money rate JPCALLO(IR) 31/12/’99 – 31/1/’13

GBP overnight deposit BPDR1T 1/4/’98 – 31/1/’13

GBP overnight deposit BPDR1T 31/5/’05 – 31/1/’13

USD overnight deposit USDR1T 1/4/’98 – 31/1/’13

II.2.2. Descriptive analysis

This section provides graphs and correlation tables to show how surprise indices and asset returns

of the USA, as well as foreign markets are related. The discussion starts with stock markets, followed

by foreign exchange , and finally fixed income markets.

II.2.2.1. Stock markets

The figure below presents the USA Citigroup Economic Surprise Index (CESIUSD) together with the

S&P500 3 month % return. This long horizon for S&P returns has been modeled specifically because

the CESI indices are calculated using an aggregate of the past 3 month surprises, too. However,

mind that this definition of the CESI (aggregate of 3 month past surprises) and S&P returns (3 month

past returns) induces a form of autocorrelation; the value of a particular day will be very close to the

value on the previous day.

Drawing S&P500 returns with surprises of other regions (such as the CESI of the G10 or Euro area,

or a difference of these indices - not shown here), does not display a clear fit such as in figure 1. The

relationship between the CESIUSD and S&P500 returns is visibly dependent on the state of the

economy. When the economy is in clear expansion (mid-2004 up to the end of 2007), there is a

negative correlation between surprises and S&P500 returns. Otherwise (mid-1998 up to mid-2004

and 2008 up to now), the correlation is positive.

Figure 2 shows the relationship between the Euro Stoxx 50 and the CESIUSD. Drawing the Euro

Stoxx 50 together with other surprise indices (such as the CESI of the Euro area or other regions –

not shown here) does not display a clear fit such as in figure 2. Again, the correlation between these

two series is clearly dependent on the state of the economy; in the pre-2004 and post-2008 period,

the correlation is clearly positive, whereas in in the period between mid-2004 and the end of 2007,

the correlation turns negative.

17

Figure 1; CESIUSD and S&P500 returns

Figure 2; CESIUSD and Euro Stoxx 50 returns

II.2.2.2. Foreign exchange

A priori, it is expected that the EURUSD exchange rate should move in line with CESIEUR-CESIUSD

innovations; when CESIEUR is higher than its American counterpart, the EURUSD should appreciate.

Figure 3 shows that this relationship holds, although there appears to be a lot of noise in the data.

In general, the relationship between forex returns and their respective surprise indices is not as clear

as for the EURUSD case. Table 8 provides correlations for some important exchange rates. It appears

from this table that for the EURUSD exchange rate, the relationship with its surprise indices is quite

strong, while this is rarely the case for other foreign exchange returns.

-0,5

-0,4

-0,3

-0,2

-0,1

0

0,1

0,2

0,3

0,4

0,5 CESIUSD/500 S&P500 3 month % return

-0,4

-0,3

-0,2

-0,1

0

0,1

0,2

0,3

0,4

0,5

0,6 CESIUSD/500 Euro Stoxx 50 3 month % returns

18

Figure 3; CESIEUR-CESIUSD and EURUSD returns

Table 8; correlations between 3 month % forex returns and surprise indices

Exchange rate EURUSD USDJPY USDCAD GBPUSD AUDUSD

Surprise indices CESIEUR-CESIUSD

CESIUSD-CESIJPY

CESIUSD-CESICAD

CESIGBP-CESIUSD

CESIAUD-CESIUSD

Correlation 0,2917 0,2203 -0,1099 -0,0276 -0,0474

Exchange rate USDCHF USDSEK NZDUSD USDNOK

Surprise indices CESIUSD-CESICHF

CESIUSD-CESISEK

CESINZD-CESIUSD

CESIUSD-CESINOK

Correlation 0,2111 -0,1112 0,0749 -0,1056

As an illustration, provided is a figure of 3 month USDJPY returns together with the surprise index

CESIUSD-CESIJPY. It appears from this figure that the relationship between the two series is rather

unclear.

Figure 4; CESIUSD-CESIJPY and USDJPY returns

-0,3

-0,25

-0,2

-0,15

-0,1

-0,05

0

0,05

0,1

0,15

0,2 (CESIEUR-CESIUSD)/1000 EURUSD 3 month log return

-200

-150

-100

-50

0

50

100

150

200

-0,25

-0,2

-0,15

-0,1

-0,05

0

0,05

0,1

0,15 USDJPY3 month % return CESIUSD-CESIJPY

19

II.2.2.3. Fixed income

A priori, a strong relation is expected between surprise indices and fixed income returns; positive

surprises should result in higher interest rates and therefore lower prices of bond portfolios. As

previous research (cf. II.1.2.3) already demonstrated a strong effect of macro surprises on interest

rates, it is expected that also surprise indices should have a strong relationship with bond returns.

Figure 5 compares the CESIUSD with the return on a portfolio of 30 year US government bonds;

visibly, the link between these two series is very strong.

Figure 5; CESIUSD and 3 month log returns of a 30 year T bond portfolio

As explained in section II.1.2.3, Euro area bonds have a stronger link with USA surprises compared

to domestic news. Figure 6 therefore compares the returns of 30 year EMU bonds with an index of

USA surprises. Obviously, the relationship is not as good as in figure 5, but it is still clear that the

CESIUSD index can explain a considerable part of the innovations in the 30 year EMU government

bond portfolio. Visibly, the link between the two series has become stronger over time; this has

already been documented by Andersson et al. (2009), who also find that the reaction of German

bond markets to US releases has become more significant during the period 1999-2005.

Figure 6; CESIUSD and 3 month log returns of a 30 year EMU bond portfolio

-0,3

-0,2

-0,1

0

0,1

0,2

0,3

0,4 CESIUSD/500 (inverted) 3 month log return

-0,3

-0,2

-0,1

0

0,1

0,2

0,3

0,4 CESIUSD/500 (inverted) 3 month log return

20

The table below provides a complete overview of the correlations between surprise indices and

returns on the long term government bond portfolios which will be used in section 3.

Table 9; correlations between surprise indices and 3 month % returns of long term government

bonds

Bond portfolio Canada 30Y

EMU 30Y Japan 30Y UK 30Y UK 50Y USA 30Y

Surprise index CESICAD CESIEUR CESIJPY CESIGBP CESIGBP CESIUSD

Correlation -0,1805 -0,2647 -0,3065 -0,0707 -0,0364 -0,4688

Bond portfolio Canada 30Y

EMU 30Y Japan 30Y UK 30Y UK 50Y USA 30Y

Surprise index CESIUSD CESIUSD CESIUSD CESIUSD CESIUSD CESIUSD

Correlation -0,3362 -0,3848 -0,3843 -0,2793 -0,2405 -0,4688

It appears from this table that, as expected, bond portfolio returns have high (absolute) correlations

with surprise indices. It is apparent that these portfolios have consistently higher correlations with

US surprises compared to their respective domestic surprise indices. This finding is in line with

Ehrmann and Fratzscher (2005) and Andersson et al. (2009), who both comment on high spillover

effects from US news on foreign bond markets.

II.2.2.4. Concluding notes

Looking at the three asset classes discussed above, it can be stated that there is overall a clearly

visible relationship between the Citi Economic Surprise Indices and asset returns. Again, this is

evidence that asset returns are linked to macro fundamentals. The CESI has an apparent relationship

with stock indices for different regions. Consistent with other research, it was found that this

relationship is dependent on the state of the economy. The link between foreign exchange rates and

surprise indices is often not that clear, although the correlation between the EURUSD and CESIEUR-

CESIUSD is quite high. This high correlation specifically for the EURUSD is not a coincidence; after

all, this is the most liquid currency pair with the highest volume in the forex market4. Consistent with

the findings of Andersen et al. (2007), it was found that fixed income markets react most strongly

to macroeconomic surprises. Just like previous research, it is shown that interest rates are more

related to the USA surprises than domestic surprise indices.

II.3. Method and results

The previous section has shown that, of all asset classes considered, the fixed income market has

the clearest relationship with surprise indices. Specifically, it was decided to make use of long term

bonds in our models. Although Faust et al. (2007) have shown that long term interest rates have a

4 The Foreign Exchange Committee, October 2012, FX volume survey, URL; <http://www.newyorkfed.org/FXC/volumesurvey/>

21

comparatively small reaction to macro surprises, Balduzzi et al. (2011) reported that the price

reaction of long term bonds, due to their high duration, is relatively bigger compared to shorter

maturities. Therefore, long term bonds should also have the clearest reaction to changes in surprise

indices. In section 3.1, the relationship between high duration government bond portfolios and

surprise indices will be formalized. Section 3.2. will explain how surprise indices can potentially be

used to actually time the fixed income market. To end is the simulation of a market timing strategy

for six different bond portfolios.

II.3.1. Surprise indices and long term government bond returns

Previous literature has already shown a clear effect of macro surprises on high frequency bond

returns (cf. 1.2.3). In line with the descriptive statistics in section 2, the intention is to formally test

whether the effect on bond returns is also significant for macro surprise indices. To this end, we

regress the following equation;

𝑟(𝑡) = 𝛼 + 𝛽𝑟(𝑡 − 1) + 𝛾1∆𝐶𝐸𝑆𝐼𝑈𝑆𝐷(𝑡) + 𝛾2∆𝐶𝐸𝑆𝐼𝐷𝑜𝑚𝑒𝑠𝑡𝑖𝑐(𝑡) + 𝜀(𝑡)

With r(t) the daily return, measured as the first difference of natural logarithms, of a long term

government bond portfolio. This return is regressed on its lagged value, together with the first

difference of the CESIUSD index and, when applicable, the first difference of the domestic CESI

index. We use White heteroscedastic robust errors to account for heterogeneity. In general, no

autocorrelation is found, nor was an important degree of multicollinearity detected. Normality for the

error terms is generally rejected, but does not seem problematic due to the large sample size (>2000

observations). Table 10 shows the results;

Table 10; Regressions of bond returns on surprise indices

Note; numbers in parentheses are t-statistics. *, ** and *** denote significance at a 10%, 5% or

1%, respectively.

R²

Canada 30 years 0.0002*** 0.0477** -0.0001*** -0,00004*** 0.0229

(3.1171)*** (2.3344)** (-6.5786)*** (-3.8958)***

EMU 30 years 0.0002** 0.1288*** -0.0001*** -0,00004*** 0.0281

(2.0879)** (5.9755)*** (-5.6319)*** (-2.9038)***

Japan 30 years 0.0001 0.1167*** -0,00003** -0,00002 0.0155

(1.0730) (4.3276)*** (-1.9622)** (-1.1914)

UK 30 years 0.0002** 0.0715*** -0.0001*** -0,00004*** 0.0163

(2.0585)** (2.9957)*** (-5.3528)*** (-2.9823)***

UK 50 years 0.0002 0.0800** -0.0001*** -0,00006*** 0.0175

(1.0319) (2.3779)** (-3.2647)*** (-2.7211)***

USA 30 years 0.0002* 0.0147 -0.0002*** 0.0251

(1.7391)* (0.6959) (-9.1413)***

22

Whereas previous literature has already shown that bond markets react significantly to macro

surprises, the results in table 10 now also confirm that bond returns are significantly connected to

macro surprise indices. The coefficients 1 and 2 are negative, as a priori expected, and often

significant at the 1% level. Similar to previous literature on macro surprises, R² statistics are quite

low (<0,029).

For all bond portfolios, it appears that the coefficients of the CESIUSD index are bigger (in absolute

value) and more significant than their respective domestic CESI counterparts. Again, this is in line

with the research of Ehrmann and Fratzscher (2005) and Andersson et al. (2009), who both find high

spillover effects from US surprises on foreign bond markets.

II.3.2. Timing government bond portfolios

II.3.2.1. Market timing strategy

Now that the relationship between bond returns and the CESI has been formally established, it could

be asked whether these surprise indices can be used for market timing purposes. The logic behind

the timing strategy is as follows; when the derivative of a CESI index is high, this means that recently

some positive macro news has been published. This is a sign of an economy in expansion, which

should result in higher interest rates, and therefore lower the return on a bond portfolio. As

graphically illustrated in section II.2.2, surprise indices are generally persistent, in the sense that

long periods of rising surprise indices (overly optimistic forecasts) are visible, followed by long periods

of declining surprise indices (overly pessimistic forecasts). This finding is useful for market timing,

as this could mean that a rising surprise index (implying rising interest rates) is a signal to sell long

term bond portfolios in the favor of cash or other money market instruments. This reasoning will be

empirically validated in the next paragraphs.

For this market timing strategy, an investor is modeled who has the choice between investing either

in long term government bonds of one specific country, or overnight money market deposits of the

same currency. The portfolio can be adapted every day. Although government bond returns of 5

different regions are available, the investor will only look at the CESIUSD index (and not the domestic

CESI index). Indeed, section II.2.2. has shown the correlations between USA surprises and

government bond returns to be higher compared to domestic surprises. When the first derivative of

the CESIUSD index is high (low), the investor will invest 100% in overnight currency deposits (a long

term government bond portfolio).

For most government bond portfolios, data is available from 1998 until 2013. This range will be

divided into an in-sample and out-of-sample period. Looking at other research on market timing,

e.g. Resnick & Shoesmith (2002) use an in sample period of 1/4 of the total data range , Rapach et

al. (2005) use an in sample period of 3/5 of the total data range, and Chen (2009) uses an in sample

period of 1/5 of the total data range. In this thesis, an in-sample period of 3 years is chosen compared

to an out-of-sample period of 12 years.

The in-sample period serves for two purposes. First of all, a precise definition of “derivative” will be

determined; the derivative of a surprise index can be measured as difference in levels between two

subsequent days, 3 subsequent days, 10 subsequent days etc. It is clear that, when a derivative is

23

defined as a short term (e.g. 2 day) difference of the level of a surprise index, the investor will

rebalance his portfolio more frequently compared to when the derivative is defined as a long term

(e.g. 20 day) difference in the level of the CESI. The in-sample period will determine the definition

of “derivative” which is the most profitable for market timing. Second, a threshold has to be

determined for when a derivative is categorized is “high”. In the in-sample period, the percentile of

derivatives will be calculated for which the corresponding threshold leads to the highest profitability

for our market timing strategy. These definitions of the derivative and threshold level are continued

throughout the remaining years of the out-of-sample period.

Afterwards, the profitability of this market timing strategy is compared with a buy and hold of the

corresponding long term government bond portfolio and overnight currency deposits.

In order to assess whether the market timing ability of our model is statistically significant, the

Pesaran and Timmermann nonparametric test is conducted. As Pesaran and Timmermann (1992, p.

461) state, this test is particularly useful when “the focus of the analysis is on the correct prediction

of the direction of change in the variable under consideration”, as is the case in this model. This test

does not a priori restrict the distribution of variables, and holds as long as the government bond

portfolio returns and the first derivative of the CESIUSD are symmetrically distributed around 0.

Another advantage of this test is that, contrary to risk based measures such as the Sharpe ratio,

Jensen’s alpha or the two beta model of Hendriksson and Merton, the nonparametric test of Pesaran

and Timmermann does not require the definition of a market and risk free portfolio. This test statistic

is defined as follows;

𝑆 =𝑝 − 𝑝 ∗

√𝜎𝑝2 − 𝜎𝑝∗

2 ~𝑁(0,1)

Where p is the proportion of times that the sign of yt is predicted correctly; p* = pypx + (1-py)(1-px);

py = Pr(yt>0); px = Pr(xt>0); s2p = n-1p*(1-p*); s2

p* = n-1(2py-1)2px(1-px) + n-1(2px-1)2py(1-py) +

4n-2pypx(1-py)(1-px); xt is the CESIUSD, yt is the daily return of a long term government bond

portfolio minus the overnight rate on a currency deposit.

Lastly, transaction costs must be accounted for. As it is not clear what the average cost would be of

buying or selling portfolios of government bonds, the number of transactions are simply counted

over the period under consideration and a theoretical transaction cost (in % of total portfolio value)

that would make the return of our market timing strategy equal to the bond benchmark is calculated.

II.3.2.2. Market timing results

The results of the market timing strategy are presented in table 11. For 5 out of 6 bond portfolios,

the out-of-sample return of the market timing strategy clearly outperforms the respective

benchmarks. Likewise, the Peseran and Timmermann test is significant at a 5% level for all portfolios.

Keep in mind that all six of the investment strategies are based on the CESIUSD Index. From that

perspective, it is remarkable that this strategy works equally well for US government bonds as well

as most foreign bond portfolios. Market timing does not seem to work for 30 year Canadian

government bonds, although the Pesaran Timmerman statistic is still significant (p-value of 0,0342).

The disappointing out of sample return of Canadian government bonds might be due to their

relatively low volatility. After all, it is more difficult to apply a market timing model to a bond portfolio

with nearly continuously rising prices, compared to a region with much more volatile bond returns.

Table 9 therefore also presents the volatility of the different bond portfolios, measured as the

24

standard deviation of weekly natural log returns. It clearly appears from this table that the portfolio

of 30 year Canadian government bonds is the least volatile.

The yearly returns presented in table 11 don’t take into account transaction costs. The last row of

table 11 therefore shows the theoretical transaction cost (in % of the portfolio value) that would

make the return of our market timing strategy equal to the bond benchmark. These transaction costs

are often quite low (0,086% or smaller), which casts doubt on the ability of this market timing

strategy to yield above benchmark returns in the real world.

A consistent finding emerges from the table below; for most bond portfolios, 5 and 6 day CESIUSD

derivatives appear to provide the best trading strategies. The market timing strategy for US T-bonds

seems to diverge from other bond portfolios with an optimal strategy for 25 day CESIUSD derivatives;

however, keep in mind that this derivative is chosen based on a rather short in-sample period of

about three years. Over the full sample (15 years), a five day strategy seems optimal, anyway.

An important cautionary note is necessary when measuring derivatives over such a short 5 day or 6

day interval; not only will a short interval entail considerable transaction costs, but also such a short

time period will only contain one or two macro releases. This entails that this market timing method

is not very different from conventional research which looks at the effect of a single macro surprise

on asset returns. As an illustration, appendix 1 graphically presents out of sample returns for different

derivative definitions. This is shown for the 70th and 75th percentile strategies for all of the six bond

portfolios. It appears from these figures that, in general, 5 day derivatives are associated with a peak

in out of sample return, while strategies based on longer derivatives are unprofitable.