Embed Size (px)

Citation preview

Macquarie Adviser Services

Are TTR pensions viable for the under 60s?

David Barrett & Curtis Dowel

Macquarie Adviser ServicesNovember 2012

Macquarie Adviser Services3

Agenda

1. Do TTR pension strategies still make sense for under 60s?

2. Further practical considerations in commencing a TTR pension

Macquarie Adviser Services

Do TTR pension strategies still make sense for under 60s?

David Barrett

Macquarie Adviser Services5

TTR pensions for under 60s?

Recent impacts on the TTR / salary sacrifice strategy

• CC cap reduction – over 50s:

• $100k 1 July 2007 to 30 June 2009

• $50k 1 July 2009 to 30 Jun 2012

• $25k 1 July 2012 to ...

(1 July 2014 proposed re $500k threshold test)

Macquarie Adviser Services6

TTR pensions for under 60s?

Recent impacts on the TTR / salary sacrifice strategy

• Tax on death benefits in pension phase:

• TR 2011/D3 – tax applicable from date of death unless dependent beneficiary is automatically entitled to an income stream

• Govt announcement 22 October 2012 in MYEFO – law to be amended from 1 July 2012 to allow tax exemption until death benefit paid

Macquarie Adviser Services7

TTR pensions for under 60s?

Recent impacts on the TTR / salary sacrifice strategy

• Taxation of pension payments:

• ATO – election re form of super benefit for tax purposes not constrained by character of benefit for SIS purposes

• TTR benefits can be elected to be received as LS without causing them to be commutations for SIS purposes

• Tax Act pension phase tax exemption considerations

Macquarie Adviser Services8

1. Purpose of TTR pension?

2. CC cap already full utilised? No…

$1,000 salary

Net rec’d$535

Tax at 46.5%$465

$1,000 CC

$850Accum

Acct

Pension Acct

$781

Tax $150

Tax at 46.5% less 15% = $246

Net rec’d $535

Net $69, plus

earnings tax benefit

$25k CC constraintfrom 2012/13

TTR pensions for under 60s?

Macquarie Adviser Services9

$850 $803 $189 $614 $46

$850 $815 $155 $660 $35

$850 $841 $46 $795 $9

• 30% conts tax for $300k+ income – impact?

MTR$1,000 salary after tax

46.5% $535

38.5% $615

34.0% $660

20.5% $795

$1,000 CC

after tax

TTR pension payment

Tax on pension payment

(15% rebate)

Net pension

rec’d

Benefit of TTR / sal sacrifice strategy *

$850 $781 $246 $535 $69

* plus impact of tax free earnings on TTR pension account balance

TTR pensions for under 60s?

Macquarie Adviser Services10

• 30% conts tax impact?

$1,000 salary

Net rec’d$535

Tax at 46.5%$465

$1,000 CC

$700Accum

Acct

Pension Acct

$781

Tax $300

Tax at 46.5% less 15% = $246

Net rec’d $535

Net -$81, plus

earnings tax benefit

TTR pensions for under 60s?

0% tax freecomponent

(break even at 25.2% tax free)

Macquarie Adviser Services11

3. CC cap already full utilised? Case 1:

Accum Acct

$500k

Pension Acct

$0

Earnings taxed:• Effective tax rate?• CGT 0%, 10%?• Asset turnover

rate?• Income/gains mix

Tax based on MAStech return assumptions (7.36% p.a.)= $2,454*

Accum Acct$0

Pension Acct

$500k

$15k pmt

Earnings tax exempt

Tax at 46.5% less 15%: $4,725

Fund member$10,275

Re-cont$10,275

NCC

0% tax free

TTR pensions for under 60s?

* See Appendix 1 for return assumptions

Macquarie Adviser Services12

Accum Acct

$500k

Pension Acct

$0

Accum Acct$0

Pension Acct

$500k

$15k pmt

Tax at 46.5% less 15%: $1,890

Fund member$13,110

Re-cont$13,110

NCC

60% tax free

TTR pensions for under 60s?

* See Appendix 1 for return assumptions

Tax based on MAStech return assumptions (7.36% p.a.)= $2,454*

Difference $564.Note: Breakeven tax free is 48.1%

over 1 year

3. CC cap already full utilised? Case 2:

Macquarie Adviser Services13

Accumulation vs TTR/re-cont strategy comparison

• Identify break-even point by varying:

1. % tax free component, and

2. gross return (after fees)

3. for each marginal tax rate: 20.5%, 34.0%, 38.5%, 46.5%

TTR pensions for under 60s?

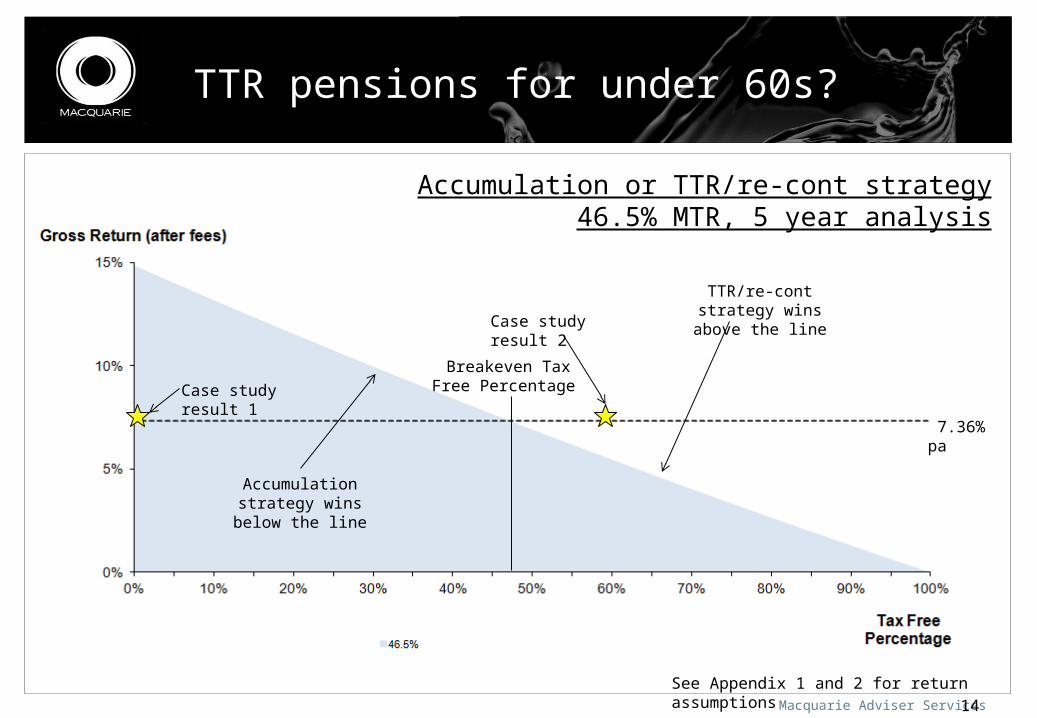

Macquarie Adviser Services14

7.36% pa

Breakeven Tax Free Percentage

TTR/re-cont strategy wins above the line

Accumulation strategy wins below

the line

Accumulation or TTR/re-cont strategy46.5% MTR, 5 year analysis

See Appendix 1 and 2 for return assumptions

TTR pensions for under 60s?

Case study result 1

Case study result 2

Macquarie Adviser Services15

7.36% pa

Breakeven Tax Free Percentage for 38.5% MTR

TTR/re-cont strategy wins above the line

Accumulation strategy wins below

the line

Breakeven Tax Free Percentage for 34.0% MTR

See Appendix 1 for return assumptions

TTR pensions for under 60s?

Accumulation or TTR/re-cont strategyVarious MTRs, 5 year analysis

Macquarie Adviser Services16

Summary:

TTR pensions may still make sense for:

1. original policy purpose – i.e. phasing into retirement

2. TTR / salary sacrifice strategies to CC cap (if 15% conts tax applies)

• (if 30% conts tax applies, reliant on TFC and earnings tax break)

3. TTR / re-cont strategies depending on:

• level of tax free component

• investment return rate

• recipient’s marginal tax rate

• Consider also upfront & ongoing costs, and issues of commencing a TTR pension...

TTR pensions for under 60s?

Macquarie Adviser Services

Practical considerations of implementing a TTR strategy

Curtis DowelOutplanMacquarie Adviser ServicesNovember 2012

Macquarie Adviser Services18

Practical considerations for TTRs

• What to consider:

– The products

– The client

– Contributions

– The employer

Macquarie Adviser Services19

Practical considerations for TTRs

• Things to watch out for:

– Product minimums & fees

– Exit fees

– Frozen assets

– Ability to refresh the pension

Products

• Minimum cash requirements

Macquarie Adviser Services20

Practical considerations for TTRs

• Macquarie Wrap – pension refresh

Products

· No account details change· Account history remains· Pension re-commences for

SIS purposes

Macquarie Adviser Services21

Practical considerations for TTRs

• Macquarie Wrap fee comparison – example 1

Products

Estimated fee: $4,100

Minimum fee: $369

Estimated fee: $4,018

Macquarie Adviser Services22

Practical considerations for TTRs

• Macquarie Wrap fee comparison – example 2

Products

Estimated fee: $4,100

Estimated fee: $36

Estimated fee: $4,059

Macquarie Adviser Services23

Practical considerations for TTRs

• SMSFs– Generally, product fees are minimised

– Administrator/accountant fees

– Audit certificates

– Segregation

– Meeting minutes & investment strategy

Products

Macquarie Adviser Services24

Practical considerations for TTRs

• SMSFs – fee example– From our example earlier, we save around $564 in tax – BUT:

• $400-$800 for pension commencement paperwork• $300-$400 pa audit certificate

– An extra cost in the first year!– Savings in subsequent years reduced by $300-$400

Products

Macquarie Adviser Services25

Practical considerations for TTRs

• Responsiveness

• Pay cycles

• The NCCs

Clients

Macquarie Adviser Services26

Practical considerations for TTRs

• Contribution caps

• SG payments

• Existing salary sacrifice

• ‘Catch-up’ payments

Contributions

The 27 Fortnight year• eg: salary of $120k pa• SG = $10,800 pa• Recommend sal sac of

$14,200 to maximise cap• BUT if there are 27 pay

periods in the year: • SG $415.38 pf x 27• Sal sac $546.15 pf x 27• Total concessional

contributions of $25,961.31!!

Bring-forward trap• Make a $150k NCC this FY• Accidentally breach CC• Make $450,000 NCC in

2014/15• Breach of NCC cap!!

• 46.5% tax

Macquarie Adviser Services27

Practical considerations for TTRs

• Treatment of salary• Where should contributions be made?

Employers

Defined benefits? Extra contributions? Employer funded insurance?

‘Matched’ contributions?

Macquarie Adviser Services

Outplan

Curtis DowelOutplanMacquarie Adviser ServicesNovember 2012

Macquarie Adviser Services29

Outplan – who we are

• Small team of dedicated paraplanners

• Professional, presentable SoAs

• Fast turnaround

• Quality focused

• Fixed, transparent fees

Macquarie Adviser Services30

Outplan – the process

Client meeting

Client presentation

Macquarie Adviser Services31

Outplan – the process

Receive & analyse request

Macquarie Adviser Services32

Why outsource your SoAs?

• You focus on what you do best

• We do what we do best

• Fixed vs variable costs

• Flexibility

• Opportunity for a 2nd opinion

• More time more clients

Macquarie Adviser Services

Are TTR pensions viable for the under 60s?

David Barrett & Curtis Dowel

Macquarie Adviser ServicesNovember 2012