Embed Size (px)

DESCRIPTION

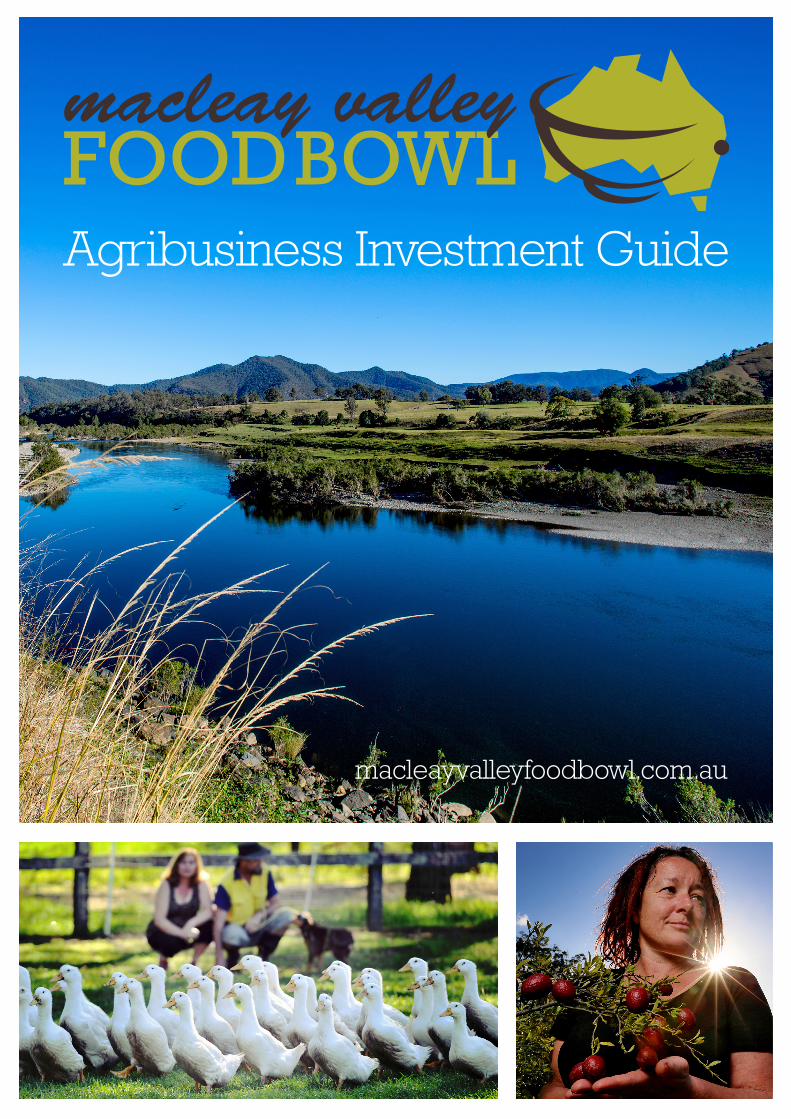

Macleay Valley Foodbowl Agribusiness Investment Guide

Citation preview

Agribusiness Investment Guide

macleayvalleyfoodbowl.com.au

1 Message from the Council 1

2 Why invest in the

Macleay Valley Food Bowl? 2

3 The Macleay Valley Food Bowl Region 3

Regionalsnapshot 3

Location&transport 4

Servicesavailabletonewbusinesses&people 4

4 Commercial information 6

Landavailability,propertysizes&value 6

Infrastructurecapability 8

Marketinformation 9

5 Land suitability 11

Sub-regions 11

Landcapability&soiltypes 11

Climate 14

Wateravailability 15

Topography 15

6 Key investment opportunities

– overview 16

7 Key aspects of selected investment

opportunities 19

7.1 Grazing-redmeatproductionfrombeef 19

7.2Animalhusbandry–poultry,meatchickens 22

7.3Animalhusbandry–pigs 26

7.4Dairy 26

7.5Buffalos 27

7.6Goat&sheepmilkproduction 27

7.7Cropping 27

7.8Perennialhorticulture–fruit,nuts,flowers, &specialitycrops 28

7.9Annualhorticulturecrops–vegetables,

herbs&spices 29

7.10Otherpotentialopportunities 29

8 Getting started 30

9 Further information 33

Appendix 1: Maps 34

Contents

PreparedbyRMCG,publishedJuly2016

KempseyShireCouncilacknowledgesthesupportofNSWDepartmentofIndustry.

Coverimages(mainimage):TheMacleay’scleanandgreenenvironment,combinedwithitssubtropicalweather,makeitidealforgrowingawiderangeofproduce.

Bottomleft:BurrawangGaianFarmnorthofKempseyproducesducksthatarehighlysoughtbysomeofthecountry’sleadingchefs,includingKylieKwong.

Bottomright:PipersCreekGroveproducersshowcasetheircropofBloodLimes.

OrganicgarlicfromSweetWaterFarm

BlueberryGreensproducerCaitlinWilliamsinspectshercrop

Whenitcomestoinvestment,timingiskey,along

withhavingaqualityproduct,strongmarketdemand,

asupportiveenvironment,professionalnetworksand

solidrelationships.TheMacleayValleyisalready

thelocationofchoiceforsomeofAustralia’smost

recognisedproductsandbrands.LegendaryAkubra

hatshasmanufacturedfromitsKempseyplantfor

thepast40years,whileNestle’siconicMilobrand

wasinventedatthevillageofSmithtown80years

agoandisstillproducedheretoday.

TheMacleayisalsohometoagrowingindustry

ofhighvaluefoodproducers,atrendKempsey

ShireCouncilproudlysupports,inpartnershipwith

industry,throughtheMacleayValleyFoodBowl

brandanditsAgribusinessInvestmentProject.

Theregion’sclean,greenenvironment,includingits

soilsandclimate,producestopqualityproducethat,

putsimply,tastessensational.

Ourhistoryofbeef,dairyandtimberproductionhas

todaygivenrisetoavibrantnewgenerationofhigh

valueandvalue-addedprimaryproduction.From

ourprosperousorganicsindustry,tonativebush

foods,intensivehorticulture,highgradebeef,dairy

andpasture-raisedpoultry,theMacleayValleyiswell

suitedtoabroadrangeofagribusinessventures.

Allinvestmentcarriesadegreeofrisk,butthe

MacleayValleyofferssomeuniquecharacteristics

toincreaseyourchanceofsuccess.Firstly,your

up-frontcostsarelower,withpropertypricessome

ofthemostaffordableontheNSWeastcoast.

Secondly,youwillhaveaccesstoareadyworkforce.

Thirdly,youwillbecomepartofastrongandvibrant

MacleayValleyFoodBowlnetworkofproducers

whoenjoythecompetitiveadvantageofabranded

destinationwithareputationforthebestproduce

moneycanbuy.Fourthly,ourhighwaytransport

linkstomajormarketsarefirstrateandwillcontinue

toimproveasupgradesarecompleted,further

reducingtraveltimes.Andfinally,theMacleay’s

pristineandpicturesquehinterland-to-coast

environmentoffersabeautifulplacetoliveandbuild

yourdreamhomeandbusiness.

KempseyShireCouncil,withsupportfromNSW

DepartmentofIndustry,hasinvestedinproducing

thisInvestmentGuidebecausetheresearchtells

usthereisasignificantopportunityforinvestment.

Thisviewissharedbythosealreadyinvestingand

isevidencedbytheunprecedentedmarketdemand

forMacleayValleyFoodBowlproduce.

Thereisnobettertimeoropportunitytoinvestright

here,rightnow,intheMacleayValley.

CrLizCampbell

Mayor,KempseyShireCouncil

1 Message from the Council

1CrescentHeadeastofKempseyisanationallyrecognisedSurfReserveandagrowinghubforhighqualityproduceanddiningexperiences.

TheMacleayValleyisontheMidNorthCoastof

NSW,mid-waybetweenSydneyandBrisbaneand

onlyanhourineitherdirectiontotheregional

centresofPortMacquarieandCoffsHarbour.

TheMacleayissuitableforawiderangeof

agriculturalproductsassociatedwithanimal

husbandryandcropproduction,withmany

naturalandstrategicfactorsbenefitingtheregion

comparedtoneighbouringareasontheMidNorth

CoastandotherproductiveareasaroundAustralia.

Theseinclude:

High quality agricultural land

Highqualitylandcanbefoundontherichalluvial

plains,upriverofKempseyoutsideofthealluvial

plains,andinthesurroundinghinterland.This

geographicdiversityprovidesopportunitiesacross

multipleagriculturalactivities.

Affordable land values

Agriculturallandistypicallypricedatadiscount

of20%ormorecomparedtosimilarlandin

neighbouringareas.

A sub-tropical climate

Amildandlargelyfrost-freecoastalclimatewithfew

extremelyhotdaysmakestheMacleayValleywell

suitedtoawiderangeofagriculturalenterprises,

andprovidesopportunityforcounter-seasonal

supplyofagriculturalproducts.

High rainfall and abundant water supplies

TheMacleayValleyhashighandconsistentrainfall,

positioningtheregionwellforbothrainfedand

irrigatedsystems.

Strategic location

Locatedhalf-wayalongtheSydney-Brisbane

corridor,primaryproducersintheregioncan

easilyaccessbothlocalregionalmarketsatPort

MacquarieandCoffsHarbour,aswellaslarger

marketsinSydneyandBrisbane.

Excellent infrastructure and services

RecentupgradestothePacificHighwayhave

reducedroadtransporttimestomajormarkets.

Bothnearbyregionalcentresofferregular

commercialpassengerandfreightairservices.

Theregionisalsohometoanabattoir,apublicly

availablecommercialkitchen,transportservicesand

agronomicservices.

Enviable lifestyle

TheMacleayValleyoffersaqualitylifestylewith

communityinfrastructurethatincludesarecently

upgradedhospital,schoolsandTAFE,anduniversity

campusesinCoffsHarbour,PortMacquarieand

Armidale.Asatouristdestinationtheregionis

well-knownforthelaidbackmixofcoastaland

hinterlandexperiences.

KempseyShireCouncilisstronglysupportiveof

agriculturalinnovationandhasledthedevelopment

oftheMacleayValleyFoodBowl,seekingtoprovide

tangiblesupporttheMacleay’sagribusinessindustry.

Already,theMacleayValleyFoodBowlbrandis

becomingwellknownintheSydney,Melbourne

andBrisbanemarkets,wheretheregion’sproduce

isbeingsoughtbyleadingchefsandgourmet

retailers.1

RisingexportdemandfromChinaforAustralian

milkproducts,includingthosefromNorco,whichall

dairyfarmersintheMacleayValleysupplyto,isalso

resultinginrenewedinvestmentinthelocaldairy

sector.

Nomatterwhatyourinterestorareaofagricultural

expertise,opportunitiesexistforyouintheMacleay

Valley.ThisGuidehasbeenpreparedtooutlinewhat

theregionhastooffer,andtohelpyouidentifywhat

opportunitiesmightsuityou.

2 Why invest in the Macleay Valley Food Bowl?

1 Forfurtherinformationsee:macleayvalleyfoodbowl.com.au 2

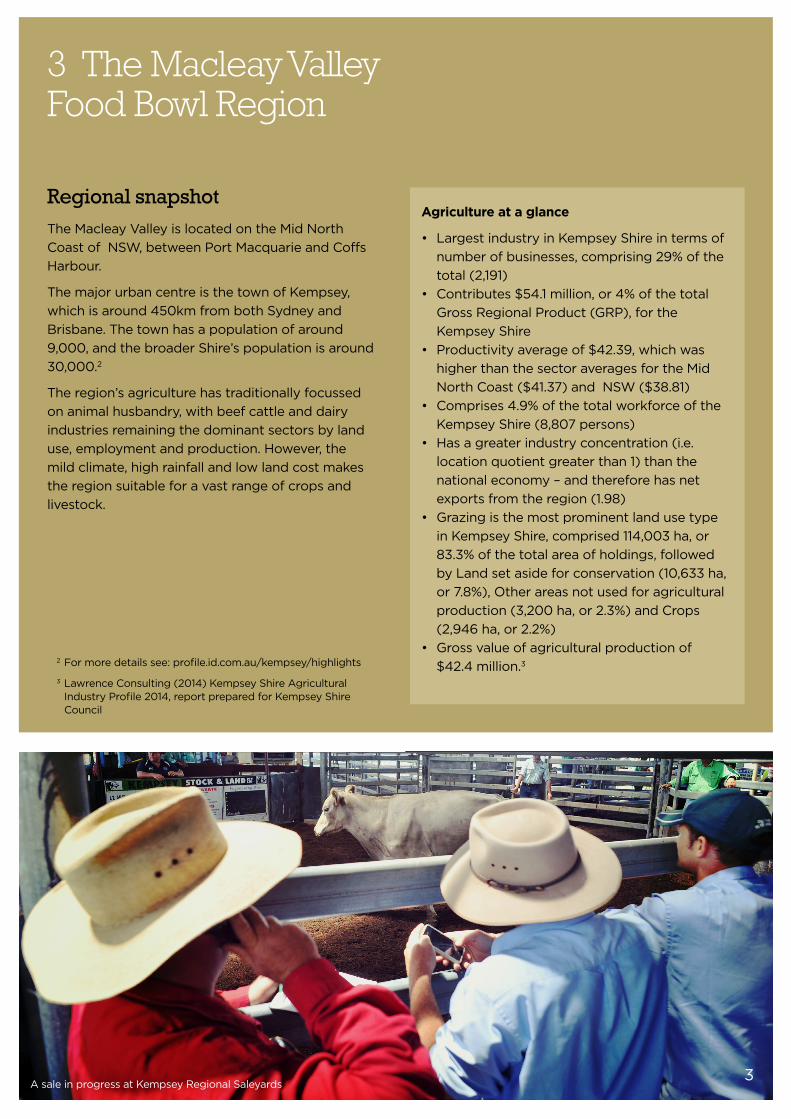

Regional snapshotTheMacleayValleyislocatedontheMidNorth

CoastofNSW,betweenPortMacquarieandCoffs

Harbour.

ThemajorurbancentreisthetownofKempsey,

whichisaround450kmfrombothSydneyand

Brisbane.Thetownhasapopulationofaround

9,000,andthebroaderShire’spopulationisaround

30,000.2

Theregion’sagriculturehastraditionallyfocussed

onanimalhusbandry,withbeefcattleanddairy

industriesremainingthedominantsectorsbyland

use,employmentandproduction.However,the

mildclimate,highrainfallandlowlandcostmakes

theregionsuitableforavastrangeofcropsand

livestock.

Agriculture at a glance

• LargestindustryinKempseyShireintermsof

numberofbusinesses,comprising29%ofthe

total(2,191)

• Contributes$54.1million,or4%ofthetotal

GrossRegionalProduct(GRP),forthe

KempseyShire

• Productivityaverageof$42.39,whichwas

higherthanthesectoraveragesfortheMid

NorthCoast($41.37)andNSW($38.81)

• Comprises4.9%ofthetotalworkforceofthe

KempseyShire(8,807persons)

• Hasagreaterindustryconcentration(i.e.

locationquotientgreaterthan1)thanthe

nationaleconomy–andthereforehasnet

exportsfromtheregion(1.98)

• Grazingisthemostprominentlandusetype

inKempseyShire,comprised114,003ha,or

83.3%ofthetotalareaofholdings,followed

byLandsetasideforconservation(10,633ha,

or7.8%),Otherareasnotusedforagricultural

production(3,200ha,or2.3%)andCrops

(2,946ha,or2.2%)

• Grossvalueofagriculturalproductionof

$42.4million.3

3 The Macleay Valley Food Bowl Region

2Formoredetailssee:profile.id.com.au/kempsey/highlights

3LawrenceConsulting(2014)KempseyShireAgriculturalIndustryProfile2014,reportpreparedforKempseyShireCouncil

3AsaleinprogressatKempseyRegionalSaleyards

Location and transport Road

ThePacificHighwaypassesthroughtheShireonthe

outskirtsofKempsey,connectingtheMacleayValley

toneighbouringtowns,aswellastoSydneyand

Brisbane:

• 35minutes’drivesouthtoPortMacquarie

(49kmsviathePacificHighway)

• 1.5hours’drivenorthtoCoffsHarbour

(112kmsviathePacificHighway)

• 4.5hours’drivetosouthSydney

(428kmsviathePacificHighway)

• 6hours’drivetonorthBrisbane

(538kmsviaPacificHighway).

UpgradestothePacificHighwaywillfurtherreduce

traveltimetomajorcentres,withthemajortown

ofKempseybypassedin2013andadditional

upgradestothesouthandnorthscheduledfor

completionin2016and2017.Theformerhighwayis

beingprogressivelyupgradedtodualcarriageway.

CompletionofthePacificHighwaywillreducetravel

timefromBrisbanetoSydneyby2hours.

Air

KempseyAirportisaregisteredairportwithan

airstripcapableofhandlingcommercialairline

services,althoughnocommercialservicescurrently

operatefromtheairport.Ithasrecentlyundergone

a$2.5millionupgradetocreateanewAviation

BusinessParkandishometoamajorinternational

pilottrainingschool.

PortMacquarieAirportlocated35minutessouth

ofKempseyreceivesdailyflightsfromSydney,

BrisbaneandCanberrawithQantasandVirgin.

Rail

TheKempseyRailwayStationconnectstheregion

byrailtoBrisbaneandSydneyalongtheNorth

CoastLine.

Transportation companies

Multipletransportationcompaniesandestablished

networksoperatewithinthevalleyincluding

MacleayValleyTransport.

Services available to new businesses and peopleCouncil services

KempseyShireCouncil’sEconomicSustainability

Unitisresponsibleforeconomicdevelopment,

tourismandcommercialassetmanagement.The

ESUteamisavailableasafirstpointofcontactfor

newandexistingbusinesseskeenforinformation

aboutthelocaleconomyandbusinessenvironment,

oradvicefromCouncil’splanningteam.

Overview of general services

TheKempseyregionhasanumberofservicesthat

supportavibrantagriculturalsector.4

Table 3-1: Overview of general services in the Kempsey region

Service Description

Sale

yard

s TheCouncilownedKempseyRegionalSaleyardshavebeenupgradedandaccreditedundertheNationalSaleyardsQualityAssuranceProgramsince2001.Kempseyisoneof22saleyardswithfullaccreditation.Approximately40salesareheldannuallyandattractvendorsandbuyersofallformsoflivestockthroughouttheMidNorthCoast.

Ab

att

oir

s EversonsFoodProcessorsisanabattoirandmeatpackerbasedinFrederickton,northofKempsey,thatservicesthelocalarea.Itisamultispeciesabattoirprocessinglamb,sheep,cattle,pigsandgoats.

Ed

ucati

on

TheregionhasastrongeducationsectorwithTAFE,theUniversityofNewEnglandatArmidale,SouthernCrossUniversityatCoffsHarbourandLismore,andCharlesSturtUniversityandtheUniversityofNewcastleatPortMacquarie.

Healt

h KempseyHospital’s$80millionupgradewascompletedin2016andtheregionalsooffersnumerousprivately-ownedmedicalpractices.

Co

mm

un

ity Sportsgroundsandrecreationalfacilities

•11licensedclubs•4publicswimmingpools•10registeredclubs•4golfcourses•Horseandgreyhoundracingtracks•Indoorcricketandtenpinbowling•14tenniscourtcomplexesand3

squashcomplexes•ServiceclubsincludingRotary,Lions,

Apex,Quota,ProbusandViewClubs.

Sh

op

pin

g ShoppingcentresandstoresincludingBigW,CountryTarget,Woolworths,Coles,IGA,Aldiandmanyspecialtyandgiftretailers.TheKempseytowncentrehasrecentlyundergonea$3.6millionupgradefeaturingnewpaving,lighting,plantingsandstreetfurniture.4ForfurtherinformationseetheMacleayValleyWelcomepack

2015-2016:kempsey.nsw.gov.au/econodev/pubs/macleay-valley-welcome-pack-2015-2016.pdf 4

Agricultural production advice

Adviceandsupportforarangeofindustriesis

providedbyLocalLandServices(lls.nsw.gov.au).

Forregionalsupport,contactNorthCoastLocal

LandServiceson1300795299or0265636700,

orPOBox108NSW2440.Theofficeislocatedat

83BelgraveStreetKempsey.

NSWFarmers(nswfarmers.org.au/home)canalso

beofassistance.

Council,MacleayValleyBusinessChamberandNorth

CoastLocalLandservicesareabletoputnewcomers

totheregionintouchwithlocalproducergroups,

includingfordairy,beef,organicsorotherspecialist

producerslocatedwithintheMacleayValleyFood

Bowl.Council’smacleayvalleyfoodbowl.com.au

websitecontainsacomprehensiveandup-to-date

localproducercontactlist.

TheMacleayLandcareNetworkisactiveinthe

regionandwelcomesnewcomers.Joininga

Landcaregroupcanbeagoodwaytomeetlike-

mindedpeople,learnaboutopportunitiesandover-

comechallenges.MacleayLandcarehasaResource

KitforRuralLandholders:macleaylandcare.org.

au/#!farming-and-soil-health/c12ae.

Fee-for-serviceagronomicadviceisavailablefrom

severalagribusinessserviceprovidersandrural

producestoresinthearea.Currently,thereisgreater

expertiseinlivestockproductionwithspecialiststaff

focussingmoresoonbeefanddairycattlethanin

horticulture.Forthisreason,specifichorticultural

expertisemayneedtobesourcedfromoutsideof

theimmediateareainadjacentregionssuchasCoffs

Harbour.

Business support

Generalinformationisavailablefromthe

DepartmentofIndustry,InnovationandScience

(business.gov.au).Thisincludesguidanceon

starting,runningandexitingabusiness,aswellas

grantsandassistance,advisoryservicesandevents.

EnterpriseConnectcanalsoofferadviceand

supporttoeligibleAustraliansmallandmedium-

sizedbusinesses,includingacomprehensive,

confidentialandindependentBusinessReviewat

nocharge.(businesscentre.com.au/item/enterprise-

connect)

Smallbusinesssupportservicesareavailablein

theKempseyarea,alongwithallmajorAustralian

bankingservices.Informationisavailablefrom

KempseyBusinessChamber(macleayvalleychamber.

com),SouthWestRocksChamberofCommerce

(southwestrocks.org.au)andKempseyShireCouncil

(kempsey.nsw.gov.au).

TheNSWDepartmentofIndustry,throughthe

OfficeofRegionalDevelopmentandOfficeof

SmallBusiness,offersregionalbusinesssupport

andadvice,includingadviceonfundingprograms,

andhasaregionalofficeatnearbyPortMacquarie

(industry.nsw.gov.au).

AusIndustryalsoprovidesadviceonarangeof

business,employment,finance,insurance,taxand

exportmatters,withregionalofficersservicingthe

KempseyareafromtheNewcastle,Tamworthand

Sydneyoffices(business.gov.au).

Otherkeyindustrycontactsareavailableonthe

MacleayValleyFoodbowlwebsiteunder‘Links’.

5Kempsey’sCBDhasrecentlyundergoneamajormulti-milliondollarupgrade

KempseyShireCouncil’splanningstaffareavailabletoprovideadviceallthewaythroughtheplanningapprovalprocess

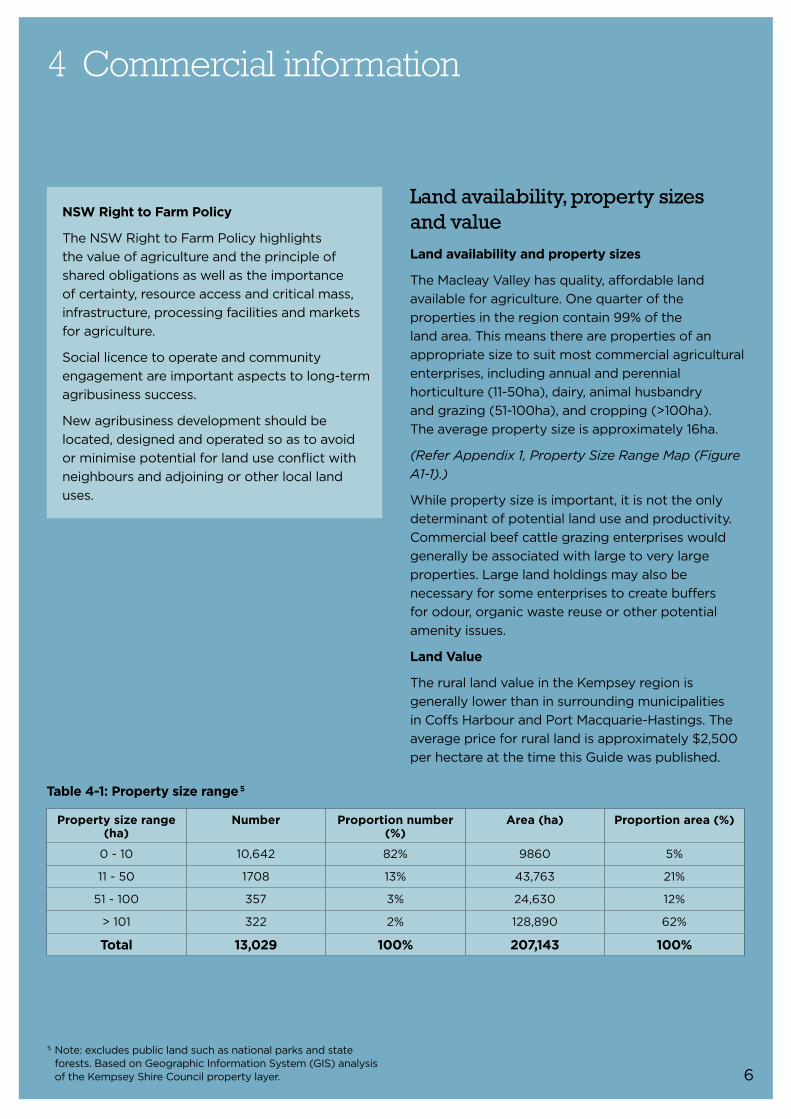

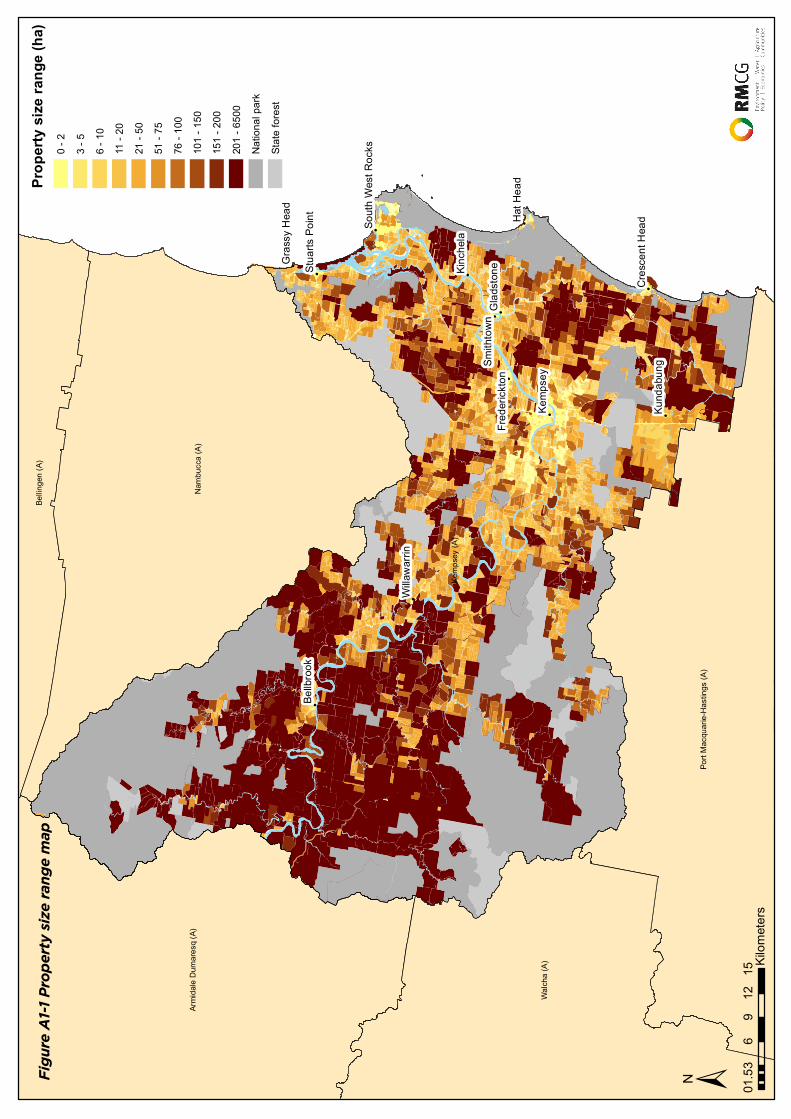

Table 4-1: Property size range 5

Property size range (ha)

Number Proportion number (%)

Area (ha) Proportion area (%)

0-10 10,642 82% 9860 5%

11-50 1708 13% 43,763 21%

51-100 357 3% 24,630 12%

>101 322 2% 128,890 62%

Total 13,029 100% 207,143 100%

NSW Right to Farm Policy

TheNSWRighttoFarmPolicyhighlights

thevalueofagricultureandtheprincipleof

sharedobligationsaswellastheimportance

ofcertainty,resourceaccessandcriticalmass,

infrastructure,processingfacilitiesandmarkets

foragriculture.

Sociallicencetooperateandcommunity

engagementareimportantaspectstolong-term

agribusinesssuccess.

Newagribusinessdevelopmentshouldbe

located,designedandoperatedsoastoavoid

orminimisepotentialforlanduseconflictwith

neighboursandadjoiningorotherlocalland

uses.

Land availability, property sizes and valueLand availability and property sizes

TheMacleayValleyhasquality,affordableland

availableforagriculture.Onequarterofthe

propertiesintheregioncontain99%ofthe

landarea.Thismeanstherearepropertiesofan

appropriatesizetosuitmostcommercialagricultural

enterprises,includingannualandperennial

horticulture(11-50ha),dairy,animalhusbandry

andgrazing(51-100ha),andcropping(>100ha).

Theaveragepropertysizeisapproximately16ha.

(Refer Appendix 1, Property Size Range Map (Figure

A1-1).)

Whilepropertysizeisimportant,itisnottheonly

determinantofpotentiallanduseandproductivity.

Commercialbeefcattlegrazingenterpriseswould

generallybeassociatedwithlargetoverylarge

properties.Largelandholdingsmayalsobe

necessaryforsomeenterprisestocreatebuffers

forodour,organicwastereuseorotherpotential

amenityissues.

Land Value

TherurallandvalueintheKempseyregionis

generallylowerthaninsurroundingmunicipalities

inCoffsHarbourandPortMacquarie-Hastings.The

averagepriceforrurallandisapproximately$2,500

perhectareatthetimethisGuidewaspublished.

4 Commercial information

5Note:excludespubliclandsuchasnationalparksandstateforests.BasedonGeographicInformationSystem(GIS)analysisoftheKempseyShireCouncilpropertylayer. 6

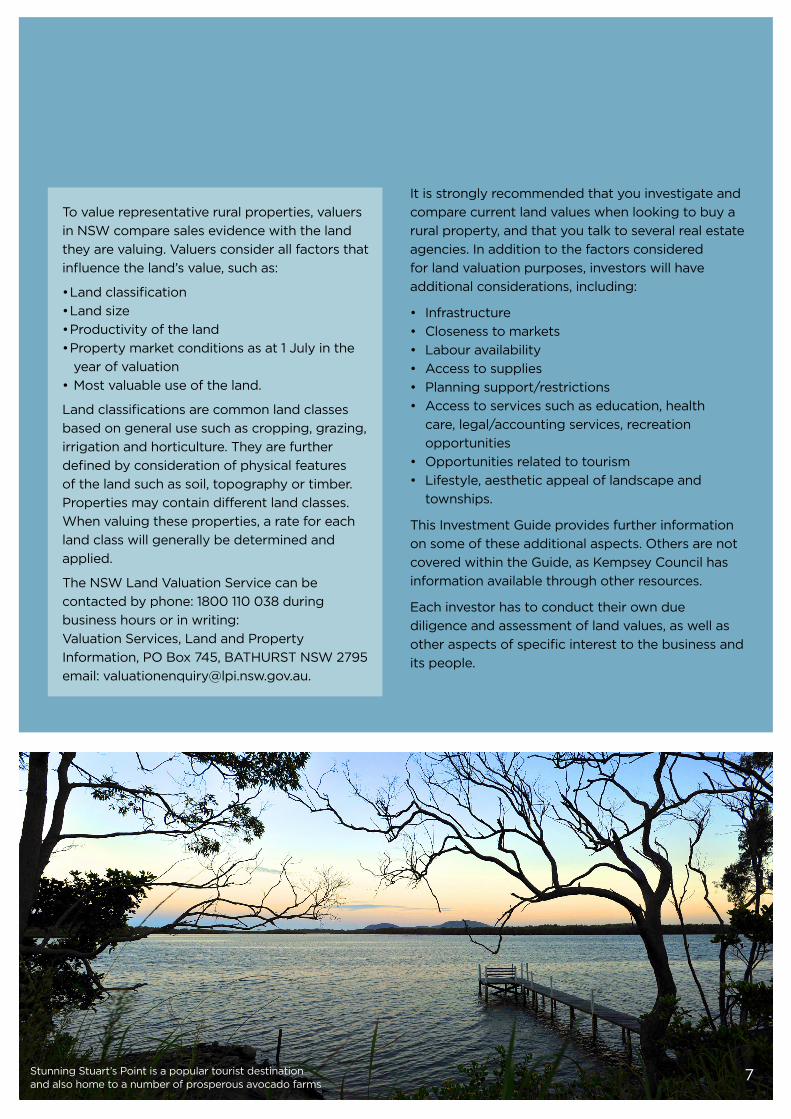

Tovaluerepresentativeruralproperties,valuers

inNSWcomparesalesevidencewiththeland

theyarevaluing.Valuersconsiderallfactorsthat

influencetheland’svalue,suchas:

•Landclassification

•Landsize

•Productivityoftheland

•Propertymarketconditionsasat1Julyinthe

yearofvaluation

•Mostvaluableuseoftheland.

Landclassificationsarecommonlandclasses

basedongeneralusesuchascropping,grazing,

irrigationandhorticulture.Theyarefurther

definedbyconsiderationofphysicalfeatures

ofthelandsuchassoil,topographyortimber.

Propertiesmaycontaindifferentlandclasses.

Whenvaluingtheseproperties,arateforeach

landclasswillgenerallybedeterminedand

applied.

TheNSWLandValuationServicecanbe

contactedbyphone:1800110038during

businesshoursorinwriting:

ValuationServices,LandandProperty

Information,POBox745,BATHURSTNSW2795

email:[email protected].

Itisstronglyrecommendedthatyouinvestigateand

comparecurrentlandvalueswhenlookingtobuya

ruralproperty,andthatyoutalktoseveralrealestate

agencies.Inadditiontothefactorsconsidered

forlandvaluationpurposes,investorswillhave

additionalconsiderations,including:

• Infrastructure

• Closenesstomarkets

• Labouravailability

• Accesstosupplies

• Planningsupport/restrictions

• Accesstoservicessuchaseducation,health

care,legal/accountingservices,recreation

opportunities

• Opportunitiesrelatedtotourism

• Lifestyle,aestheticappealoflandscapeand

townships.

ThisInvestmentGuideprovidesfurtherinformation

onsomeoftheseadditionalaspects.Othersarenot

coveredwithintheGuide,asKempseyCouncilhas

informationavailablethroughotherresources.

Eachinvestorhastoconducttheirowndue

diligenceandassessmentoflandvalues,aswellas

otheraspectsofspecificinteresttothebusinessand

itspeople.

7StunningStuart’sPointisapopulartouristdestinationandalsohometoanumberofprosperousavocadofarms

Infrastructure capabilityTransport services

Anumberoffreightserviceprovidersoperatein

thearea,takingproducetoregionalmarketsas

wellastoSydney,BrisbaneandMelbourne.

AirfreightcanbesentfromPortMacquarie

Airport,whichhasdailyservicestoSydney.

Other infrastructure

ACouncil-ownedcommercialkitchenisavailable

forhireforfoodproduction.Thekitchenoffers

twocommercialovensandgascooktopsand

largerangehood.Equipmentincludesafridge

andfreezer,pots,pansandcookwaretogether

withadishwasher.

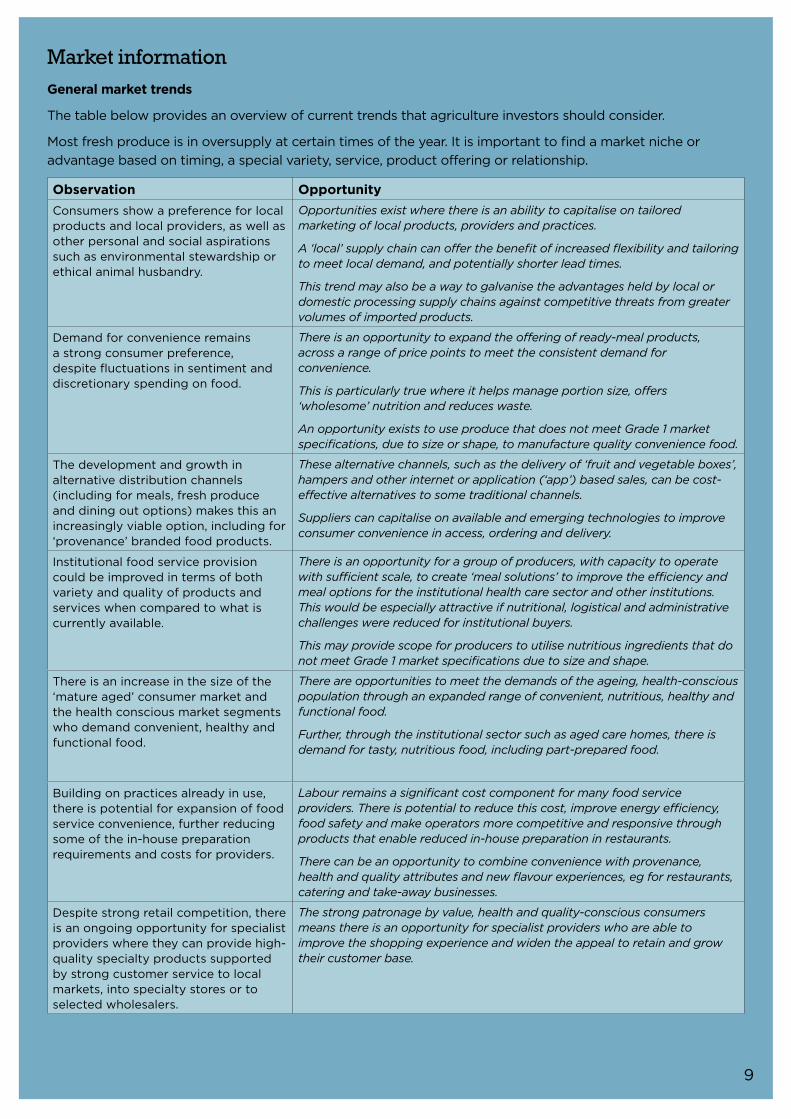

Localorregionalmarketsforproducecanbe

foundinthefollowingcentres:

• Gladstone:GladstoneQualityMarkets,Kinchela

Street,Gladstone

• Kempsey:MarketatRiversidePark,Kempsey,

withnumerousothermarketsdetailedat

macleayvalleycoast.com.au

• PortMacquarie:HastingsFarmersMarket

atPortMacquarieWestportPark,Port

Macquarie:growersmarket.net.au,orWauchope

MarketsWauchopeShowgroundHighStreet:

wauchopefarmersmarket.com.au

• CoffsHarbour:CoffsCoastGrowers’Market

CitySquareHarbourDrive,CoffsHarbour

• Bellingen:GrowersMarket,cornerofHammond

St&BlackSt,Bellingen.

Informationongrowersmarketsnationallycanbe

foundatmarkethere.com.au.

Freshhorticulturalproduce(fruit,vegetables,

herbs,flowers)wholesalemarketsexistinallmajor

centres:

• Sydney:sydneymarkets.com.au

• Newcastle:newcastlemarkets.com.au

• Brisbane:brisbanemarkets.com.au

• Melbourne:melbournemarkets.com.au

• Adelaide:saproducemarket.com.au

• Perth:perthmarket.com.au/wholesale-markets.

Informationtoassistinexportconsiderationscan

befoundinthefollowingresources:

• NSWGovernmentexportassistance

• NSWGovernmentExportAcceleratorToolkit

• Austradeguidetoexporting

• ExportCouncilofAustraliamarketresearch

advice

• AUSVEGexportreadinesschecklist.

8

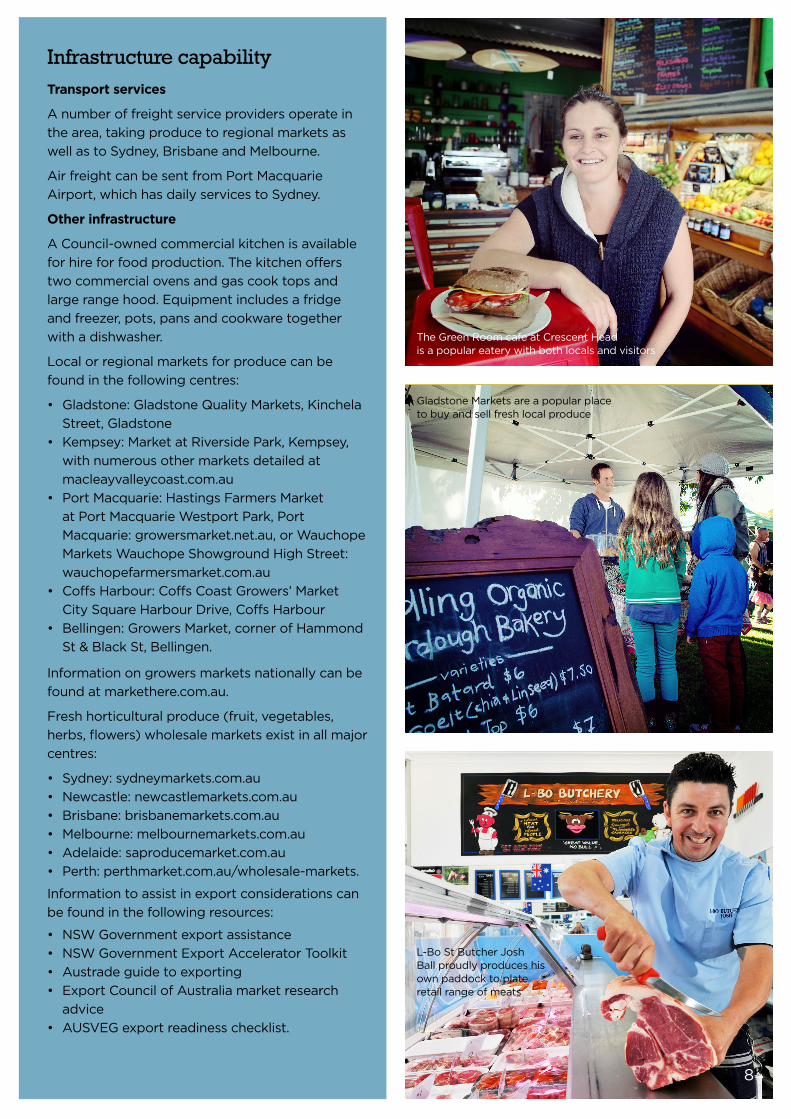

TheGreenRoomcafeatCrescentHeadisapopulareaterywithbothlocalsandvisitors

GladstoneMarketsareapopularplacetobuyandsellfreshlocalproduce

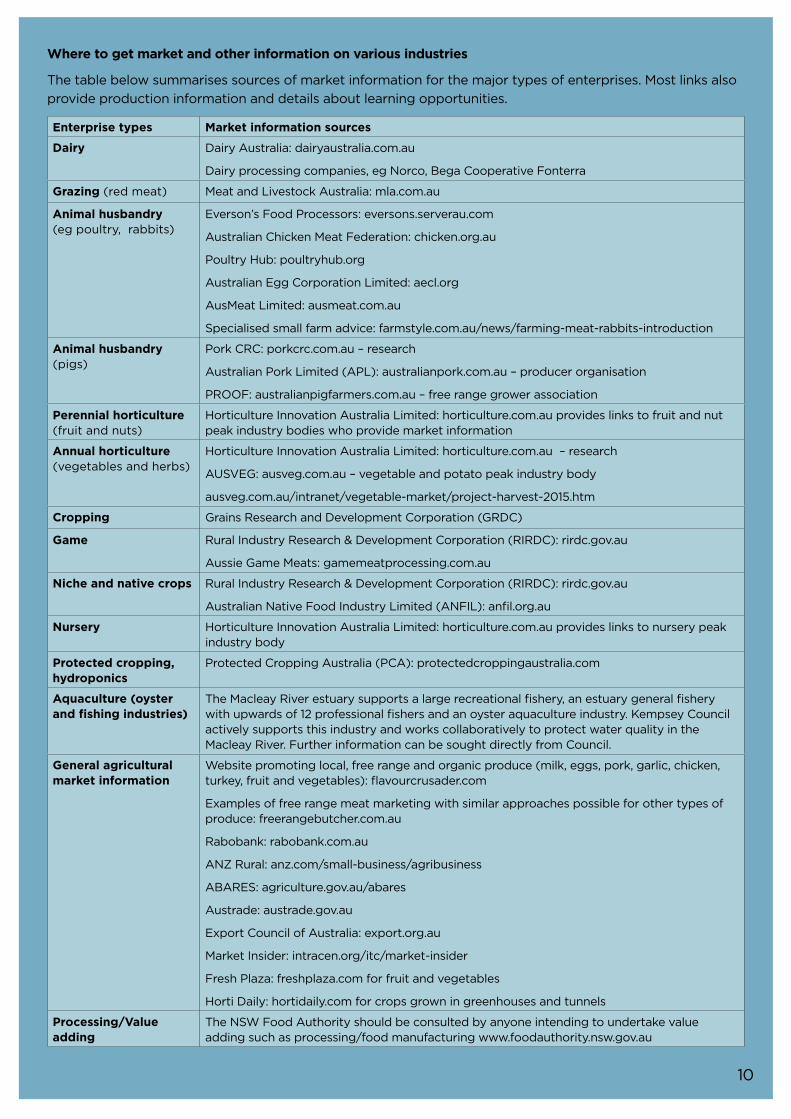

L-BoStButcherJoshBallproudlyproduceshisownpaddocktoplateretailrangeofmeats

Market informationGeneral market trends

Thetablebelowprovidesanoverviewofcurrenttrendsthatagricultureinvestorsshouldconsider.

Mostfreshproduceisinoversupplyatcertaintimesoftheyear.Itisimportanttofindamarketnicheor

advantagebasedontiming,aspecialvariety,service,productofferingorrelationship.

Observation Opportunity

Consumersshowapreferenceforlocalproductsandlocalproviders,aswellasotherpersonalandsocialaspirationssuchasenvironmentalstewardshiporethicalanimalhusbandry.

Opportunities exist where there is an ability to capitalise on tailored marketing of local products, providers and practices.

A ‘local’ supply chain can offer the benefit of increased flexibility and tailoring to meet local demand, and potentially shorter lead times.

This trend may also be a way to galvanise the advantages held by local or domestic processing supply chains against competitive threats from greater volumes of imported products.

Demandforconvenienceremainsastrongconsumerpreference,despitefluctuationsinsentimentanddiscretionaryspendingonfood.

There is an opportunity to expand the offering of ready-meal products, across a range of price points to meet the consistent demand for convenience.

This is particularly true where it helps manage portion size, offers ‘wholesome’ nutrition and reduces waste.

An opportunity exists to use produce that does not meet Grade 1 market specifications, due to size or shape, to manufacture quality convenience food.

Thedevelopmentandgrowthinalternativedistributionchannels(includingformeals,freshproduceanddiningoutoptions)makesthisanincreasinglyviableoption,includingfor‘provenance’brandedfoodproducts.

These alternative channels, such as the delivery of ‘fruit and vegetable boxes’, hampers and other internet or application (‘app’) based sales, can be cost-effective alternatives to some traditional channels.

Suppliers can capitalise on available and emerging technologies to improve consumer convenience in access, ordering and delivery.

Institutionalfoodserviceprovisioncouldbeimprovedintermsofbothvarietyandqualityofproductsandserviceswhencomparedtowhatiscurrentlyavailable.

There is an opportunity for a group of producers, with capacity to operate with sufficient scale, to create ‘meal solutions’ to improve the efficiency and meal options for the institutional health care sector and other institutions. This would be especially attractive if nutritional, logistical and administrative challenges were reduced for institutional buyers.

This may provide scope for producers to utilise nutritious ingredients that do not meet Grade 1 market specifications due to size and shape.

Thereisanincreaseinthesizeofthe‘matureaged’consumermarketandthehealthconsciousmarketsegmentswhodemandconvenient,healthyandfunctionalfood.

There are opportunities to meet the demands of the ageing, health-conscious population through an expanded range of convenient, nutritious, healthy and functional food.

Further, through the institutional sector such as aged care homes, there is demand for tasty, nutritious food, including part-prepared food.

Buildingonpracticesalreadyinuse,thereispotentialforexpansionoffoodserviceconvenience,furtherreducingsomeofthein-housepreparationrequirementsandcostsforproviders.

Labour remains a significant cost component for many food service providers. There is potential to reduce this cost, improve energy efficiency, food safety and make operators more competitive and responsive through products that enable reduced in-house preparation in restaurants.

There can be an opportunity to combine convenience with provenance, health and quality attributes and new flavour experiences, eg for restaurants, catering and take-away businesses.

Despitestrongretailcompetition,thereisanongoingopportunityforspecialistproviderswheretheycanprovidehigh-qualityspecialtyproductssupportedbystrongcustomerservicetolocalmarkets,intospecialtystoresortoselectedwholesalers.

The strong patronage by value, health and quality-conscious consumers means there is an opportunity for specialist providers who are able to improve the shopping experience and widen the appeal to retain and grow their customer base.

9

Where to get market and other information on various industries

Thetablebelowsummarisessourcesofmarketinformationforthemajortypesofenterprises.Mostlinksalso

provideproductioninformationanddetailsaboutlearningopportunities.

Enterprise types Market information sources

Dairy DairyAustralia:dairyaustralia.com.au

Dairyprocessingcompanies,egNorco,BegaCooperativeFonterra

Grazing(redmeat) MeatandLivestockAustralia:mla.com.au

Animal husbandry(egpoultry,rabbits)

Everson’sFoodProcessors:eversons.serverau.com

AustralianChickenMeatFederation:chicken.org.au

PoultryHub:poultryhub.org

AustralianEggCorporationLimited:aecl.org

AusMeatLimited:ausmeat.com.au

Specialisedsmallfarmadvice:farmstyle.com.au/news/farming-meat-rabbits-introduction

Animal husbandry(pigs)

PorkCRC:porkcrc.com.au–research

AustralianPorkLimited(APL):australianpork.com.au–producerorganisation

PROOF:australianpigfarmers.com.au–freerangegrowerassociation

Perennial horticulture(fruitandnuts)

HorticultureInnovationAustraliaLimited:horticulture.com.auprovideslinkstofruitandnutpeakindustrybodieswhoprovidemarketinformation

Annual horticulture(vegetablesandherbs)

HorticultureInnovationAustraliaLimited:horticulture.com.au–research

AUSVEG:ausveg.com.au–vegetableandpotatopeakindustrybody

ausveg.com.au/intranet/vegetable-market/project-harvest-2015.htm

Cropping GrainsResearchandDevelopmentCorporation(GRDC)

Game RuralIndustryResearch&DevelopmentCorporation(RIRDC):rirdc.gov.au

AussieGameMeats:gamemeatprocessing.com.au

Niche and native crops RuralIndustryResearch&DevelopmentCorporation(RIRDC):rirdc.gov.au

AustralianNativeFoodIndustryLimited(ANFIL):anfil.org.au

Nursery HorticultureInnovationAustraliaLimited:horticulture.com.auprovideslinkstonurserypeakindustrybody

Protected cropping, hydroponics

ProtectedCroppingAustralia(PCA):protectedcroppingaustralia.com

Aquaculture (oyster and fishing industries)

TheMacleayRiverestuarysupportsalargerecreationalfishery,anestuarygeneralfisherywithupwardsof12professionalfishersandanoysteraquacultureindustry.KempseyCouncilactivelysupportsthisindustryandworkscollaborativelytoprotectwaterqualityintheMacleayRiver.FurtherinformationcanbesoughtdirectlyfromCouncil.

General agricultural market information

Websitepromotinglocal,freerangeandorganicproduce(milk,eggs,pork,garlic,chicken,turkey,fruitandvegetables):flavourcrusader.com

Examplesoffreerangemeatmarketingwithsimilarapproachespossibleforothertypesofproduce:freerangebutcher.com.au

Rabobank:rabobank.com.au

ANZRural:anz.com/small-business/agribusiness

ABARES:agriculture.gov.au/abares

Austrade:austrade.gov.au

ExportCouncilofAustralia:export.org.au

MarketInsider:intracen.org/itc/market-insider

FreshPlaza:freshplaza.comforfruitandvegetables

HortiDaily:hortidaily.comforcropsgrowningreenhousesandtunnels

Processing/Value adding

TheNSWFoodAuthorityshouldbeconsultedbyanyoneintendingtoundertakevalueaddingsuchasprocessing/foodmanufacturingwww.foodauthority.nsw.gov.au

10

Sub-regions TheMacleayValleyisextremelydiverseand

offerssomethingforeveryone.Itscompetitive

advantages,includingaccesstonaturalresources

suchaswater,aswellasitsfavourablesoil

andclimate,combinetosupportarangeof

agriculturalenterprises.Theseconditionsvary

acrossthreedistinctsub-regions:

1. AlluvialplainseastofKempseytothemouthof

theMacleayRiver

2.UpriverwestofKempseytoWillawarrin

3.HillcountryfromWillawarrinwesttotheshire

boundary.

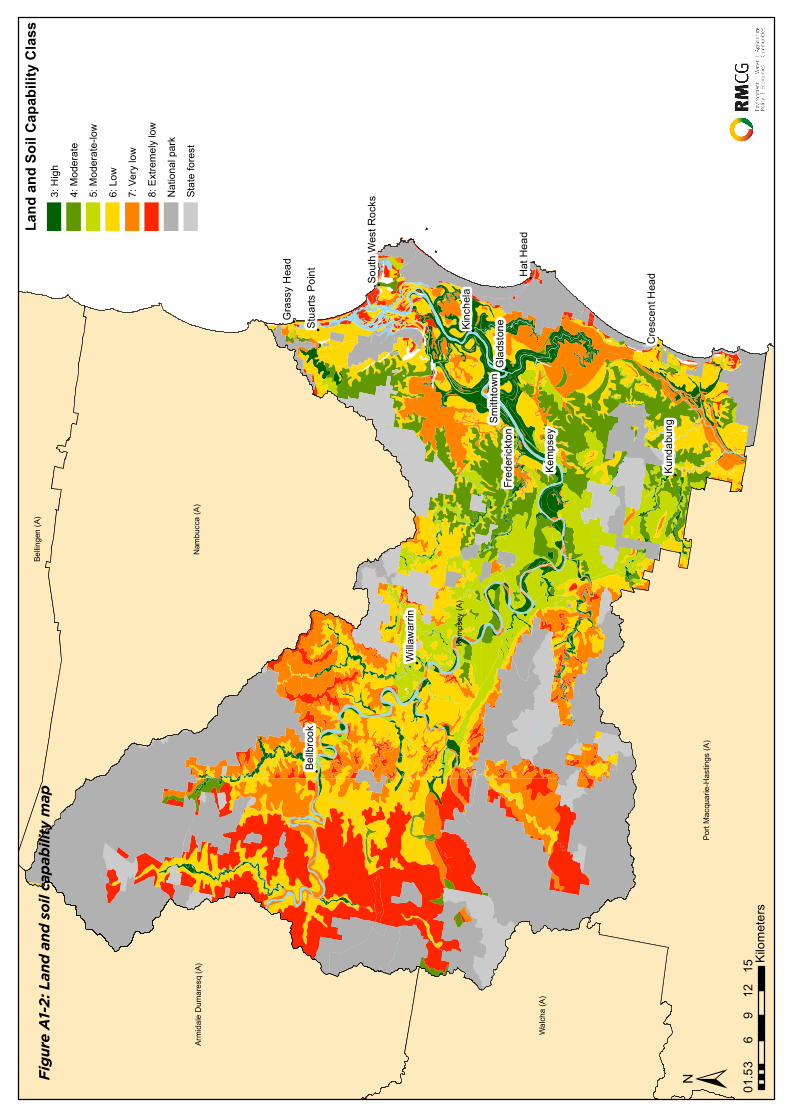

Land capability and soil typesAlandscapemapofKempseybylandcapability

canbefoundinAppendix1(FigureA1-2).

TheKempseyregionhasalargeareaofhigh

(Class3)andmoderate(Class4)landcapability

capableofsupportingarangeofagricultural

enterprises.

Landcapabilityisdefinedastheinherentphysical

capacityofthelandtosustainarangeofland

usesandmanagementpracticesinthelong-

term,withoutdegradingsoil,land,airandwater

resources.TheLandandSoilCapability(LSC)

assessmentschemeusesthebiophysicalfeatures

ofthelandandsoil,includinglandformposition,

slopegradient,drainage,climate,soiltypeand

soilcharacteristics,toderivedetailedratingtables

forarangeoflandandsoilhazards.Class1isthe

bestandhighestcapabilityland,whileClass8is

theworstorlowestcapabilityland.6Thedifferent

Classes,areasandindicativesoiltypesforthe

regionareshowninTable5-1onthenextpage.

ThereisnoClass1or2landintheregion,whichis

notunusual.

5 Land suitability

6OfficerofEnvironmentandHeritage(2013)Thelandandsoilcapabilityassessmentscheme;Secondapproximation;AgeneralrurallandevaluationsystemforNewSouthWales,NSWGovernment,Sydney 11

AcropoforganicgarlicthrivesatSweetWaterFarm,located10minuteswestofKempsey

TheMacleayValleyisproudofitsstrongagriculturalhistory

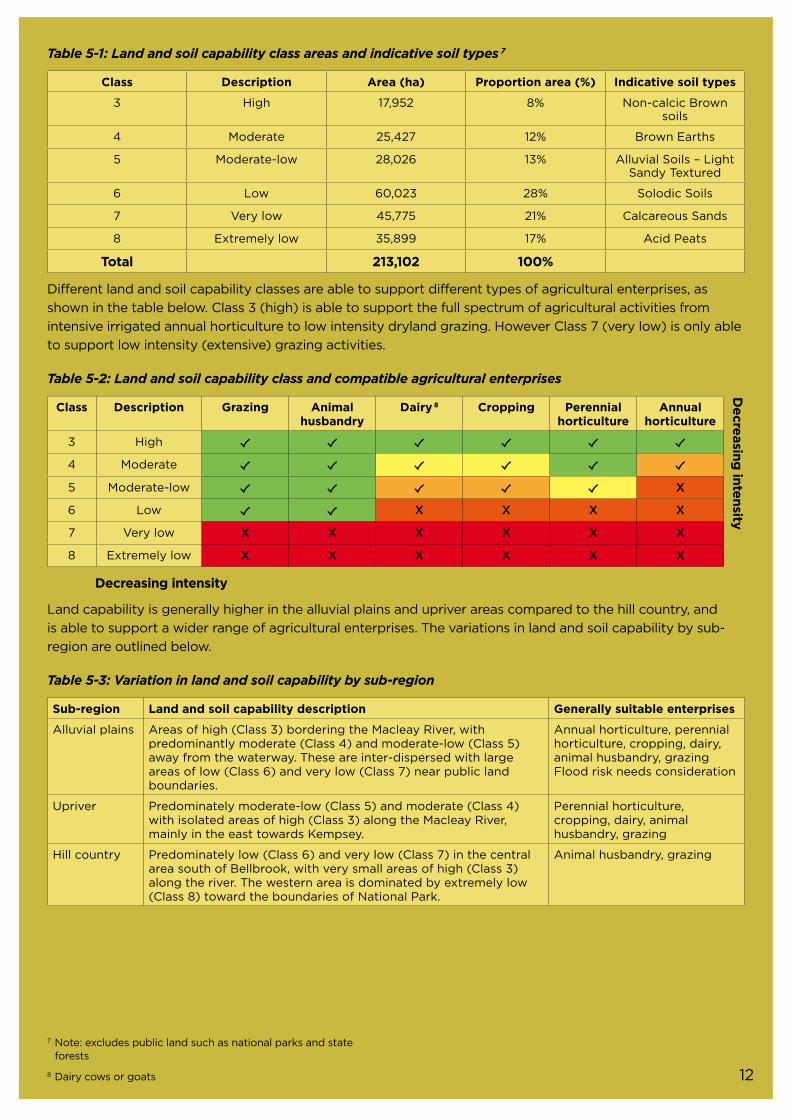

Table 5-1: Land and soil capability class areas and indicative soil types 7

Class Description Area (ha) Proportion area (%) Indicative soil types

3 High 17,952 8% Non-calcicBrownsoils

4 Moderate 25,427 12% BrownEarths

5 Moderate-low 28,026 13% AlluvialSoils–LightSandyTextured

6 Low 60,023 28% SolodicSoils

7 Verylow 45,775 21% CalcareousSands

8 Extremelylow 35,899 17% AcidPeats

Total 213,102 100%

Differentlandandsoilcapabilityclassesareabletosupportdifferenttypesofagriculturalenterprises,as

showninthetablebelow.Class3(high)isabletosupportthefullspectrumofagriculturalactivitiesfrom

intensiveirrigatedannualhorticulturetolowintensitydrylandgrazing.HoweverClass7(verylow)isonlyable

tosupportlowintensity(extensive)grazingactivities.

Table 5-2: Land and soil capability class and compatible agricultural enterprises

Class Description Grazing Animal husbandry

Dairy 8 Cropping Perennial horticulture

Annual horticulture

3 High

4 Moderate

5 Moderate-low X

6 Low X X X X

7 Verylow X X X X X X

8 Extremelylow X X X X X X

Decreasing intensity

Landcapabilityisgenerallyhigherinthealluvialplainsandupriverareascomparedtothehillcountry,and

isabletosupportawiderrangeofagriculturalenterprises.Thevariationsinlandandsoilcapabilitybysub-

regionareoutlinedbelow.

Table 5-3: Variation in land and soil capability by sub-region

Sub-region Land and soil capability description Generally suitable enterprises

Alluvialplains Areasofhigh(Class3)borderingtheMacleayRiver,withpredominantlymoderate(Class4)andmoderate-low(Class5)awayfromthewaterway.Theseareinter-dispersedwithlargeareasoflow(Class6)andverylow(Class7)nearpubliclandboundaries.

Annualhorticulture,perennialhorticulture,cropping,dairy,animalhusbandry,grazingFloodriskneedsconsideration

Upriver Predominatelymoderate-low(Class5)andmoderate(Class4)withisolatedareasofhigh(Class3)alongtheMacleayRiver,mainlyintheeasttowardsKempsey.

Perennialhorticulture,cropping,dairy,animalhusbandry,grazing

Hillcountry Predominatelylow(Class6)andverylow(Class7)inthecentralareasouthofBellbrook,withverysmallareasofhigh(Class3)alongtheriver.Thewesternareaisdominatedbyextremelylow(Class8)towardtheboundariesofNationalPark.

Animalhusbandry,grazing

Decre

asin

g in

ten

sity

7Note:excludespubliclandsuchasnationalparksandstateforests

8Dairycowsorgoats 12

Specific considerations relating to soils and land capability

Soils

Individualsiteslocatedwithinotherwisesuitable

areasoftheMacleayValleymayhavemorelimited

landusesduetoparticularaspectswithspecific

managementrequirements.Theseinclude,for

instance,potentialacidsulphatesoilsinthelower

lyingpartsofthealluvialplains.

Manyoftheregion’ssoilsthathavenotbeen

intensivelyusedarelikelytobeacidicandthis,

alongwithlowinherentfertility,isatypicalfeature

ofAustraliansoils.Plantsotherthannatives,such

asblueberries,wouldrequireaninitialinvestmentin

soilimprovement.Thiscouldincludelimingandthe

additionoffertiliserstoreachtherequiredpHand

fertilitystatusfortheselectedcroporpasture.Organic

soilamendmentsmayalsobebeneficialinsomecases.

Itisimportantthatyouseekoutexpertadvicewhen

selectingaspecificsiteforaparticularlanduse

(referSection3.3,Services).

Soilonsteeperhillslopescanbeshallowandeasily

eroded.Itisnotadvisabletoclearslopesbymore

than15%forcroppingorgrazingpurposesonnorth-

facingslopes,evenifpermissible.

FurtherinformationisavailablefromtheResource

KitforRuralLandholdersintheNambucca,Macleay

andHastingsValleys,2008Landcare,DAFF,

NRCMA.

Land capability

Class5landissuitableforcroppinganddairying,

withsomespecificconsiderations.Thelandneeds

tobemanagedcarefullyandinasite-specific

mannertopreventsoildegradation,forexample

viacompaction,organicmatterlossorerosion.

Generally,thismeansthatcroppingrequiring

intensivetillagewouldonlybepracticalonceor

twicewithineightyears,unlesssoilsareameliorated

andmanagedwithcare,forexampleviasuitablesoil

amendments,drainageasrequiredandminimum

tillage,controlledtraffic,covercroppinganderosion

control.Rockysoilsareusuallynotsuitablefor

conventionalcropping.

Dairyingmayrequiredrainage,higherinputsthanon

betterclassland,orlowerstockingratestoprevent

soildegradation.Animalsshouldnotbegrazed

onwaterloggedpastures.Goatsareespecially

susceptibletofootdiseasesifkeptonwetground.

However,smalleranimalscouldbeeasilykept.

Perennialcropswouldbeeasiertomanagebut

wouldstillrequiregoodsoilpreparationtothemain

rootingdepth,whichcouldincludea1-yearcover

croptostartwith.

Floodrisksneedtobeconsideredwithinthevicinity

oftheriverandestuary,withpermanentstructures

tobebuiltandpositionedaccordingly.Perennial

cropsarenotrecommended,andanimalsmay

requirestandoffareasorshiftingtohigherground.

Higherlabourinputsareusuallyrequiredonsloping

land.

Adequateskillsandknowledgearerequiredto

manageClass4andespeciallyClass5land,as

indicatedinTable5-3.

13

GreenLeafFarmatClybuccaisasignificantnewagribusinessintheMacleayValley

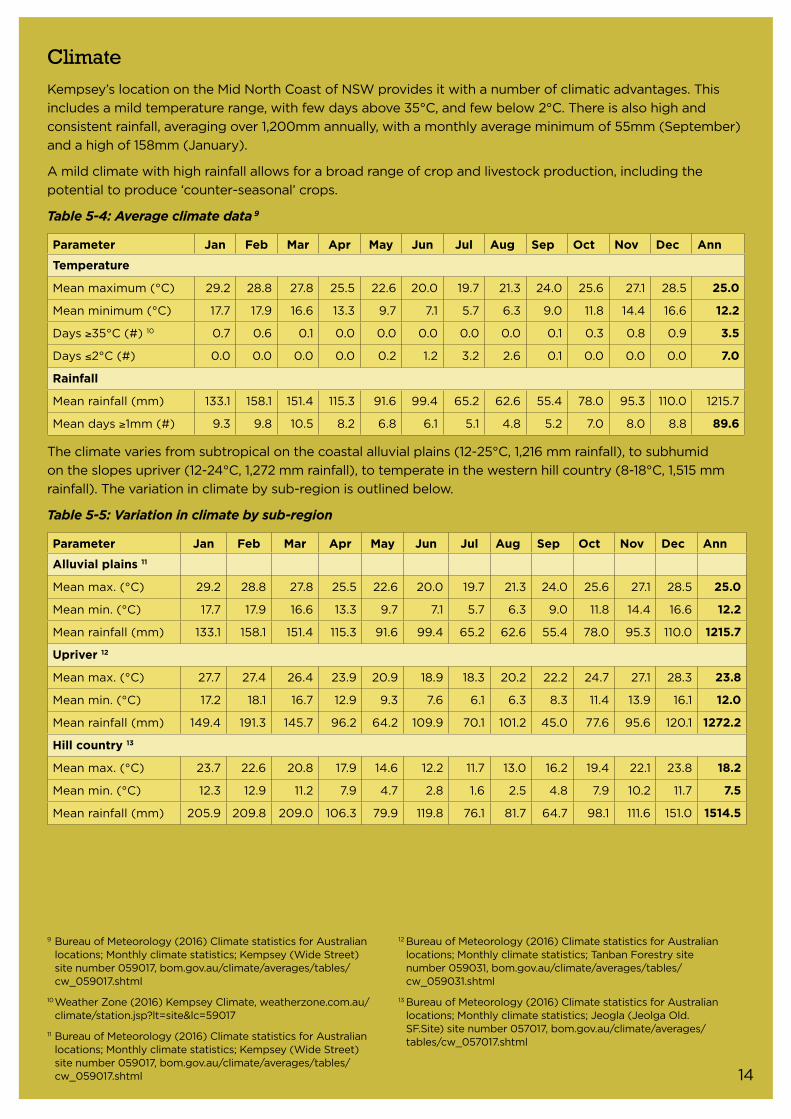

Climate Kempsey’slocationontheMidNorthCoastofNSWprovidesitwithanumberofclimaticadvantages.This

includesamildtemperaturerange,withfewdaysabove35°C,andfewbelow2°C.Thereisalsohighand

consistentrainfall,averagingover1,200mmannually,withamonthlyaverageminimumof55mm(September)

andahighof158mm(January).

Amildclimatewithhighrainfallallowsforabroadrangeofcropandlivestockproduction,includingthe

potentialtoproduce‘counter-seasonal’crops.

Table 5-4: Average climate data 9

Parameter Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Ann

Temperature

Meanmaximum(°C) 29.2 28.8 27.8 25.5 22.6 20.0 19.7 21.3 24.0 25.6 27.1 28.5 25.0

Meanminimum(°C) 17.7 17.9 16.6 13.3 9.7 7.1 5.7 6.3 9.0 11.8 14.4 16.6 12.2

Days≥35°C(#)10 0.7 0.6 0.1 0.0 0.0 0.0 0.0 0.0 0.1 0.3 0.8 0.9 3.5

Days≤2°C(#) 0.0 0.0 0.0 0.0 0.2 1.2 3.2 2.6 0.1 0.0 0.0 0.0 7.0

Rainfall

Meanrainfall(mm) 133.1 158.1 151.4 115.3 91.6 99.4 65.2 62.6 55.4 78.0 95.3 110.0 1215.7

Meandays≥1mm(#) 9.3 9.8 10.5 8.2 6.8 6.1 5.1 4.8 5.2 7.0 8.0 8.8 89.6

Theclimatevariesfromsubtropicalonthecoastalalluvialplains(12-25°C,1,216mmrainfall),tosubhumid

ontheslopesupriver(12-24°C,1,272mmrainfall),totemperateinthewesternhillcountry(8-18°C,1,515mm

rainfall).Thevariationinclimatebysub-regionisoutlinedbelow.

Table 5-5: Variation in climate by sub-region

Parameter Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Ann

Alluvial plains 11

Meanmax.(°C) 29.2 28.8 27.8 25.5 22.6 20.0 19.7 21.3 24.0 25.6 27.1 28.5 25.0

Meanmin.(°C) 17.7 17.9 16.6 13.3 9.7 7.1 5.7 6.3 9.0 11.8 14.4 16.6 12.2

Meanrainfall(mm) 133.1 158.1 151.4 115.3 91.6 99.4 65.2 62.6 55.4 78.0 95.3 110.0 1215.7

Upriver 12

Meanmax.(°C) 27.7 27.4 26.4 23.9 20.9 18.9 18.3 20.2 22.2 24.7 27.1 28.3 23.8

Meanmin.(°C) 17.2 18.1 16.7 12.9 9.3 7.6 6.1 6.3 8.3 11.4 13.9 16.1 12.0

Meanrainfall(mm) 149.4 191.3 145.7 96.2 64.2 109.9 70.1 101.2 45.0 77.6 95.6 120.1 1272.2

Hill country 13

Meanmax.(°C) 23.7 22.6 20.8 17.9 14.6 12.2 11.7 13.0 16.2 19.4 22.1 23.8 18.2

Meanmin.(°C) 12.3 12.9 11.2 7.9 4.7 2.8 1.6 2.5 4.8 7.9 10.2 11.7 7.5

Meanrainfall(mm) 205.9 209.8 209.0 106.3 79.9 119.8 76.1 81.7 64.7 98.1 111.6 151.0 1514.5

9BureauofMeteorology(2016)ClimatestatisticsforAustralianlocations;Monthlyclimatestatistics;Kempsey(WideStreet)sitenumber059017,bom.gov.au/climate/averages/tables/cw_059017.shtml

10WeatherZone(2016)KempseyClimate,weatherzone.com.au/climate/station.jsp?lt=site&lc=59017

11 BureauofMeteorology(2016)ClimatestatisticsforAustralianlocations;Monthlyclimatestatistics;Kempsey(WideStreet)sitenumber059017,bom.gov.au/climate/averages/tables/cw_059017.shtml

12BureauofMeteorology(2016)ClimatestatisticsforAustralianlocations;Monthlyclimatestatistics;TanbanForestrysitenumber059031,bom.gov.au/climate/averages/tables/cw_059031.shtml

13BureauofMeteorology(2016)ClimatestatisticsforAustralianlocations;Monthlyclimatestatistics;Jeogla(JeolgaOld.SF.Site)sitenumber057017,bom.gov.au/climate/averages/tables/cw_057017.shtml

14

Water availability WateravailabilityintheMacleayValleyislessofachallengethansomeotherproductiveregionsinAustralia,

duetohighrainfall,availabilityofbothsurfacewaterandgroundwaterentitlements,andcatchmentinon-

farmdams.

SurfaceandgroundwaterextractionisgovernedbyWaterSharingPlans(WSP)inNSW.AnupdatedWater

SharingPlanfortheMacleayValleyisexpectedinmid-2016,withthefollowingfeatures:

• Almost3,500mlofsurfacewaterentitlementintheMacleayValley(noadditionalentitlementavailable)

• Noadditionalgroundwaterallocationforcommercialuse,howevermanypropertiesalreadyhave

groundwaterentitlementinuse.

ThenewWSPseparateslandandwaterrights,facilitatingtradeofentitlementwithintheValley,andalso

upstreamfromthebroaderExtractionManagementUnit(afurther20,000mlofentitlement).Thiswill

increasethepotentialpoolofsurfacewaterentitlementavailableforuseintheMacleayValley.

Manyfarmssourcewaterfromon-farmdamswhichdonotrequirealicenceifsizedaccordingtoitsmaximum

harvestableright.

Itshouldbenoted,particularlyforirrigationuse,thatsurfacewaterdownstreamofthetownofKempsey

canbeaffectedbysalinity.Whilewateravailabilityisnotanissue,floodrisksneedtobeconsideredforland

locatedwithinthevicinityoftheriverandestuary.

TheNSWOfficeofWaterhasanofficeinKempseyandcanprovidefurtherinformationonwater

infrastructureandwateravailabilityforirrigation.

TopographyThemajorityoftheKempseyregionisflat(0%slope)orslightlyundulating(1-2%or3-5%slope),makingit

idealforagriculturallanduse(ReferAppendix1,FigureA1-3).Topographyisimportanttoconsider,asthis

determinestheriskofsoilerosion,nutrientandsedimentrunoff,andtheabilitytosafelyfarmthelandwith

machineryandavoidpotentialoff-siteimpacts.

Slopegenerallyneedstobelessthanorequalto15%forsustainableagriculturallanduse,howeverthisvaries

dependingontheenterprise.Itispreferableforannualhorticulturetobeundertakenonslopeslessthan,or

equalto,5%.Croppingandpasturefordairy,animalhusbandryandgrazingisbestundertakenonslopesless

than,orequalto,10%,whileperennialhorticulturecanbeundertakenonslopesofupto15%.

Landisflattestinthealluvialplainssub-region,followedbyslightlyslopinglandupriver.Landbecomesmore

undulatingandsteeperfurtherwestinthehillcountry.Thevariationinslopebysub-regionisoutlinedbelow.

Table 5-6: Variation in slope by sub-region

Sub-region Slope description Most suitable enterprises

Alluvialplains Predominatelyflat(0%)ontheareassurroundingtheMacleayRiver,withsmallareasofslightlyundulatingland(3-5%)aroundGrassyHeadinthenorthandCrescentHeadinthesouth.Verysmallisolatedareaofsteeperland(6-10%)onthemunicipalboundaryinthenorth.

Annualhorticulture,perennialhorticulture,cropping,dairy,animalhusbandry,grazing

Upriver Concentratedareasofflatland(0%)closetotheriver,increasinginslopewestwardstowardsWillawarrin(1-2%and3-5%).Smallareasofsteeperland(6-10%)inthenorthandsouthawayfromthevalley.

Perennialhorticulture,cropping,dairy,animalhusbandry,grazing

Hillcountry Undulatingland,primarily3-5%inter-dispersedwithsteeper(6-10%)andflatter(1-2%)land.Moderateareasofsteep(11-15%)andverysteep(16-20%and21-25%)landsouthwestofBellbrooktowardsthenationalparkboundaries,withisolatedareasextremelysteep(26-40%).

Perennialhorticulture,animalhusbandry,grazing

15

Thetableonthefollowingpagesummarises

investmentopportunitiesbyenterprisetype

andMacleayValleysub-region,outliningthe

competitiveadvantagesandkeyconsiderations

foreach.Furtherdetailsaboutopportunities

foreachtypeofenterprise,alongwithmarket

considerations,areprovidedinSection7.

Whenitcomestopracticaldecision-makingfor

specificinvestments,keyopportunitieswillbe

foundwherethereisadequatelandcapability

andpropertysizetosupportyourparticular

agriculturalcommodityofinterest.Thisisshown

ataregionalscaleinTable6-1,withfurther

analysisprovidedinTable6-2.Forexample,

thiscouldincludehighervalue(Class3)land

on11-50hapropertiesforannualhorticulture

andspecialitycrops,ormoderate(Class4)

landonpropertiesgreaterthan100hafor

grazingpurposes.Indooranimalhusbandryand

hydroponicproductionmaybeplacedonpoorer

qualityland.

6 Key investment opportunities - Overview

16

BloodLimes,picturedatPipersCreekGrovefarmatDondingalong

KempseyFarmersMarketsinBelgraveSt,Kempsey

TheMacleayValleyhasarichagriculturalheritage

Table 6-1: Key investment opportunities by enterprise type and Macleay Valley sub-region

Enterprise Alluvial plains

Upriver Hill country Competitive advantage

Key considerations for production

Grazing (red meat)

Yescattle

Yes,mainlycattle

Yes •Beefisawellestablished,predominantindustryandahistoricagriculturallanduseintheregion

•Networksorcooperationwithotherproducerspossible

•Localdomesticabattoir

•Landmanagementonsteeperhillcountry

•Standoffareasorsomehigherlyinglandneededduetofloodriskonalluvialplains

•Theclimateisnotsuitableforlargerscalesheepandgoatproductioninlowerlyingareas(wetsoils,humidity)

•Shelterandriparianfencingrecommended

Animal husbandry (poultry, pigs)

Yes Yes Yes •Favourableclimaticconditions

•Smallersizepropertiesavailable

•Localdomesticabattoir

•Landmanagementonsteeperhillcountry

•Effluentandmanuremanagementifanimalsarehousedoronsmallareaswithlittlerotation

•Farmingrabbitshasbecomeexpensiveduetovirusvaccinationneeds

•Shelterneededforfreerangeanimals

Dairy Yes Mainlysmallerscale,Heifers

Limitationsinmostareas-refertolandcapability

•Establishedindustryandprocessor

•Goodpastureandfodderproductioncountry

•Scale,agistmentpotential•Effluentandmanuremanagement•Wateravailabilityforanimalsand

pastures•Technology,egmilkingshed,

electricitygeneration•Processingchoice•Standoffareasorsomehigherlying

landneededduetofloodriskonalluvialplains

•Shelterandriparianfencingrecommended

Cropping Innon-floodingareas

Smallscale

No •Goodgrowingseason•Rainfall•Mildclimate

•Floodriskonalluvialplains•Landmanagementonundulating

uprivercountry•Smallfarmsizesandlandformsmay

belimiting•Profitablecroprotationsneeded•Seedcrops(pasture,grain,vegetables)

growninisolationfromcommercialcropscouldbeexplored

Perennial horticulture (fruit and nuts)

Innon-floodingareas

Yes Suitablecropsonverysmallscale

•Potentialtogrowawiderangeofsubtropicalmildtemperate/Mediterraneanandnativecrops

•Accesstogoodqualitywaterforirrigation

•Floodriskonalluvialplains•Irrigationwateravailability•Highrainfallcandamagecrops

duringharvest•Windprotectionneeded•Limitationsposedbyundulating

country•Productgrading,packingandcool

storageneeds•Cooltransportavailabilityandcosts

Annual horticulture (vegetables, herbs)

Innon-floodingareas

Yes Suitablecropsonverysmallscale

•Potentialtogrowawiderangeofsubtropicalandmildtemperate(Mediterranean)crops

•Accesstogoodqualitywaterforirrigation

•Protectedcroppingpossibleincoolerareas(e.g.tunnels)

•Floodriskonalluvialplains•Irrigationwateravailability•Erosionriskonslopesdueto

exposedsoil•Profitablecroprotationsneeded•Productgrading,packingandcool

storageneeds•Cooltransportavailabilityandcosts•Greenhousesortunnelsshouldbe

onflatareasandwellventilated•Windprotectionrecommended

Nursery, turf & ornamentals

Innon-floodingareas

Somesites,notturf

Suitablenativeplantsinlimitedsmallareas

•SupplytoBrisbaneandSydney

•Greenhousesortunnelsshouldbeonflatareasandwellventilated

•Windprotectionrecommended

17

Table 6-2: Guidance on key opportunities considering land capability and property size for a commercially viable operation 1

Enterprise Land capability (LSC)

Property size (ha)

Considerations

Grazing (red meat)

•3-5suitable •Mediumtolargesize

•HigherLandandSoilCapability(LSC)requiredtogrowfoddercrops,hayandsilage

•SheepandgoatscanbegrazedonlowerLSCland,eghillcountry

•Adjuststockingratestopastureproductivity,whichdeclineswithincreasingLSCnumber

Animal husbandry (pigs)

•3-5suitable•6,dependingon

locationandtypeofenterprise

•Mediumsizepreferableforpigs

•Pigsareverydestructivetosoilstructureifmanagedfreerange,sosufficientareaisneededtorotatethemandreinvigoratepastures

•Ifpigsarehoused,lowerLSCisacceptableiflandisflat.Sufficientproductivelandisneededtodealwithpiggeryeffluent,forexampleviairrigationormanureuse

Animal husbandry (poultry)

•3-5suitable•LSC6depending

onlocationandtypeofenterprise

•Smalltomediumsizesuitable

•Poultrymaybedestructivetothesoilifmanagedfreerange,sosufficientareaisneededtorotatethemandreinvigoratepastures

•Ifpoultryishoused,lowerLSCisacceptableiflandisflat.Sufficientproductivelandisneededtodealwithmanure

Dairy •3-5suitable •Mediumtolargesize

•HigherLSCrequiredtogrowfoddercrops,hayandsilage

•Adjuststockingratestopastureproductivity,whichdeclineswithincreasingLSCnumber.This,andpotentlyhigherinputs,arelikelytopreventeconomicallyviabledairyproduction,especiallyforconventionalmilkprocessorsonLSC4&particularlyLSC5

Cropping •3-4suitable •Mediumtolargesize

•Lowermargincropsrequirelargerareas•Highervaluecropssuchasseedcrops(pasture,grain,

vegetables)maybeproducedprofitablyonsmallersizeproperties

Perennial horticulture

•3-4,some5mayalsobesuitable

•Medium •Productionsystems,treesizesandcropvaluesvaryandshouldbewellresearchedtodetermineoptimumpropertysize

Annual horticulture

•3-4,lowerLSClandforgreenhouses

•Dependingoncroptype

•Intensive,highvalueproductioningreenhousestructuresrequireslesslandthan,forexample,vegetableproductionoreasilygrown,lowervaluecrops

Nursery, turf & ornamentals

•3-5,lowerLSClandforgreenhouses

•Smalltomedium

•Accesstohighqualitywaterintegral•Lowsalinesoilsanecessaryrequirement

1Lifestylefarmshavingoff-farmincomemaybesmallerthanindicatedinTable6-2. 18

7 Key aspects of selected investment opportunities

Teninvestmentopportunitiesareoutlinedinthis

section,including:

7.1 Grazing-redmeatproductionfrombeef

7.2 Animalhusbandry–poultry,meatchickens

7.3 Animalhusbandry–pigs

7.4 Dairy

7.5 Buffalos

7.6 Goatandsheepmilkproduction

7.7 Cropping

7.8 Perennialhorticulture

7.9 Annualhorticulturecrops

7.10 Otherpotentialopportunities

7.1 Grazing - red meat production from beefBeefcattlehavetraditionallybeenproducedinthe

MacleayValley.Itisawell-suitedenterpriseforthe

regionandanyscaleofproduction.Opportunities

existtodevelopalocal,highqualitybeefbrand.

Current industry context

AsatJune30,2012,Australia’snationalcattleherd

stoodat28.5millionhead,ofwhich13.6millionwere

beefcowsandheifers.Thesecattlewererunon

77,164cattlepropertiesacrossAustralia.Australia

producedaround2.2milliontonnesofbeefand

vealin2012-13,ofwhich67%wasexportedto

morethan100countriesatavalueofoverAU$5

billion.Australiaistheworld’sseventhlargestbeef

producer,producing4%oftheworld’sbeefsupply

andisthethirdlargestbeefexporter.Australia’s

largestbeefexportmarketisJapan,followedbythe

USandSouthKorea.

Beefindustrybodiesinclude:

• Meat&LivestockAustralia(MLA)

• CattleCouncilofAustralia(CCA)

• AustralianMeatIndustryCouncil(AMIC)

• AustralianMeatProcessorCorporationLtd

(AMPC)

• AustralianLivestockExportCorporationLtd

(LiveCorp)

• AustralianLotFeedersAssociation(ALFA)

• RedMeatAdvisoryCouncilLimited(RMAC).

Competitive advantage

Nearlyyearroundrainfallmeanstheremaybelittle

needtobuyinfeed,providingthatpastures,fodder

cropsandstockingrates,andgrazingarewell

managedthroughouttheyear.Whenproduction

isbasedontraditionalimprovedpasturesystems,

basedonintroducedtropicalandsubtropicalwarm

seasondominantperennialgrasses,theareahas

asignificantwinter/springfeedgapduetolow

pastureproductivityandfeedquality.

Specificwintergrowingpasturessuchasryeand

otherfoddercropswouldhavetobeplanted.Low

winterrainfallmeansthatannualwintergrowing

speciesmayberequired.Therainfalldistribution

maymakemaintaininglegumesinmixedpastures

challenging.NSWDepartmentofPrimaryIndustries

hasconductedresearchonwinterfoddercrops.

Informationcanalsobyfoundatfuturebeef.com.

au/knowledge-centre/pastures-and-forage-crops/

aswellasfromresourcesproducedbyMeatand

LivestockAustralia(MLA).

Thedevelopmentofsuitable,productivepasture

basedsystemsmaybechallengingbutworthwhile

fortheregion.Thereisamarketforqualitypasture-

fedbeefandtheMacleayValleymaybesuitedto

developinganew,localbeefbrandthatisbasedon

MSAgradingandprovenance.

Asalways,beforeinvestinginbeefproduction,

seekoutadvicefrompeoplewiththerequired

experience.

19

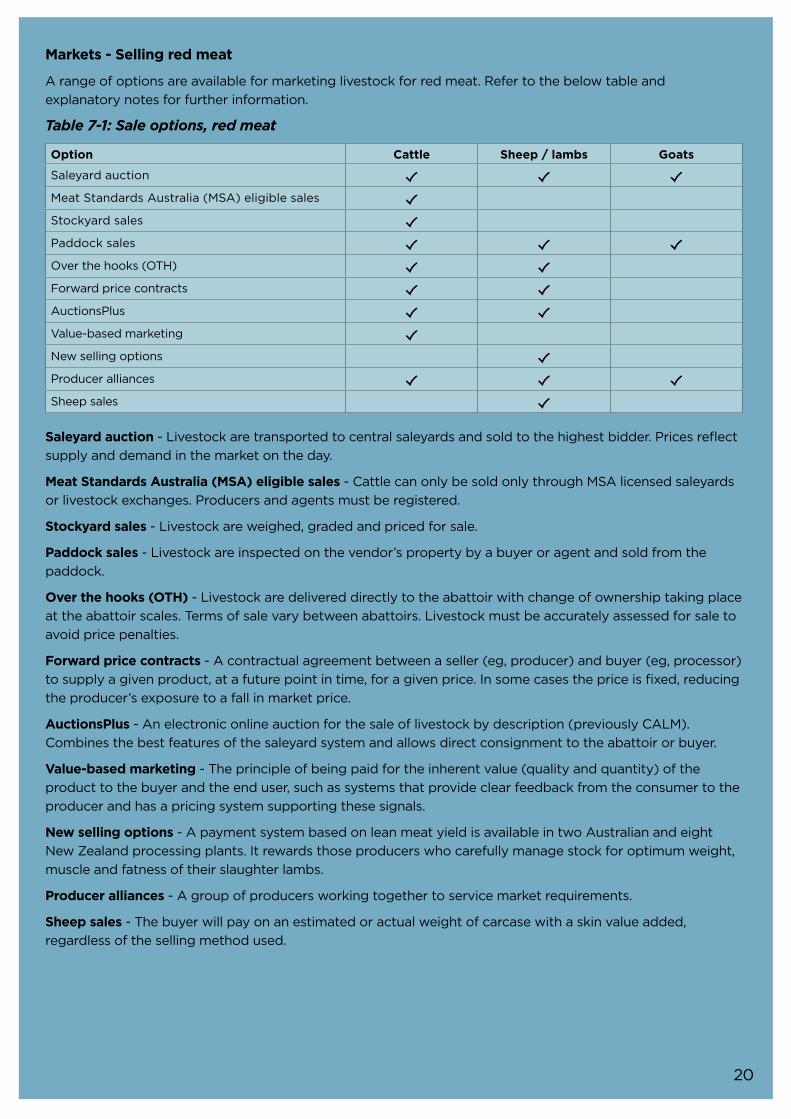

Markets - Selling red meat

Arangeofoptionsareavailableformarketinglivestockforredmeat.Refertothebelowtableand

explanatorynotesforfurtherinformation.

Table 7-1: Sale options, red meat

Option Cattle Sheep / lambs Goats

Saleyardauction

MeatStandardsAustralia(MSA)eligiblesales

Stockyardsales

Paddocksales

Overthehooks(OTH)

Forwardpricecontracts

AuctionsPlus

Value-basedmarketing

Newsellingoptions

Produceralliances

Sheepsales

Saleyard auction-Livestockaretransportedtocentralsaleyardsandsoldtothehighestbidder.Pricesreflect

supplyanddemandinthemarketontheday.

Meat Standards Australia (MSA) eligible sales-CattlecanonlybesoldonlythroughMSAlicensedsaleyards

orlivestockexchanges.Producersandagentsmustberegistered.

Stockyard sales-Livestockareweighed,gradedandpricedforsale.

Paddock sales-Livestockareinspectedonthevendor’spropertybyabuyeroragentandsoldfromthe

paddock.

Over the hooks (OTH)-Livestockaredelivereddirectlytotheabattoirwithchangeofownershiptakingplace

attheabattoirscales.Termsofsalevarybetweenabattoirs.Livestockmustbeaccuratelyassessedforsaleto

avoidpricepenalties.

Forward price contracts-Acontractualagreementbetweenaseller(eg,producer)andbuyer(eg,processor)

tosupplyagivenproduct,atafuturepointintime,foragivenprice.Insomecasesthepriceisfixed,reducing

theproducer’sexposuretoafallinmarketprice.

AuctionsPlus-Anelectroniconlineauctionforthesaleoflivestockbydescription(previouslyCALM).

Combinesthebestfeaturesofthesaleyardsystemandallowsdirectconsignmenttotheabattoirorbuyer.

Value-based marketing-Theprincipleofbeingpaidfortheinherentvalue(qualityandquantity)ofthe

producttothebuyerandtheenduser,suchassystemsthatprovideclearfeedbackfromtheconsumertothe

producerandhasapricingsystemsupportingthesesignals.

New selling options-ApaymentsystembasedonleanmeatyieldisavailableintwoAustralianandeight

NewZealandprocessingplants.Itrewardsthoseproducerswhocarefullymanagestockforoptimumweight,

muscleandfatnessoftheirslaughterlambs.

Producer alliances-Agroupofproducersworkingtogethertoservicemarketrequirements.

Sheep sales-Thebuyerwillpayonanestimatedoractualweightofcarcasewithaskinvalueadded,

regardlessofthesellingmethodused.

20

Key considerations

Initialinvestment,infrastructurerequirementsand

timetobreakevenareallimportantconsiderations

wheninvestinginorexpandinganagribusiness

enterprise.Whenyoupurchaseagrazingproperty,

lookforgoodexistinginfrastructure,especially

fencing,torotategrazingandprovidecattlewith

wateraccessotherthanallowingcattletoaccess

streams.

Regulatoryconsiderations

Requirementsexistinrelationtovarious

regulationsrelatingtoanimalwelfare,on-farm

animalwelfare,requirementsinfeedlotsand

animaltransportation.Theregulationsapplyto

bothdomesticandliveexportanimals.Meat&

LivestockAustralia’sAnimalWelfarepageprovides

furtherinformationontheseregulations.

Thebeefindustryhasalsoinitiatednumerous

supplychainmeasurestoensuremeatsafetyand

traceability.Thesemeasuresareessentialtoensure

consumerscontinuetodemandAustralia’sred

meatproducts.

Future outlook

Likeanyprimaryproductionenterprise,thereare

arangeofrisksassociatedwiththecommercial

productionofbeefcattle.Theseincludethelossof

vitalexportmarkets,weather,diseaseandpests,

inputpricesandsaleprices.Whilemostofthese

arebeyondtheproducer’scontrol,therearea

rangeoftoolsthatcanassistyoutomanagethe

risks.

Forcurrentinformationonmarketsandprices,

refertotheindustrybodiesandorganisations

listedinthisGuide.

21

CattlegrazingintheMacleayHinterland

KempseyRegionalSaleyardsofferregularsalesforbuyersandsellers

LBoStreetButchery

7.2 Animal husbandry – poultry, meat chickensCurrent industry context

About560millionchickensareproducedand

processedannuallyforchickenmeatinAustralia,

whichequatestomorethanonebillionkilogramsof

chickenmeat.Thegrossvalueofpoultrymeatatthe

timeofslaughterwasAU$2.2billionin2013.Chicken

meatisthemostpopularformofmeatprotein

consumedinAustralia,withpercapitaconsumption

averagingmorethan44kg/year.Chickenmeathas

arelativelysmallenvironmentalfootprintcompared

withotherland-basedmeatproteinsources.

Australiaproducesaround1%oftheworld’schicken

meat,withtheUSA,ChinaandBrazilbeingthe

largestchickenmeatproducingcountries.Thereare

anumberofwayschickensarerearedandmarketed

inAustralia,butthemostcommonareconventional,

freerangeandorganic.

Australiahasstricttradepoliciesandbiosecurity

measuresinplacetoensurethecountry,andits

domesticpoultryindustries,areprotectedfrom

diseasesnotusuallyfoundinAustralia.Importsof

chickenmeataresubjecttostringentconditions,

resultinginverylimitedimportsofprocessed

chickenmeatandnoimportsoffreshchicken

meat.Thismeansvirtuallyallchickenmeateaten

inAustraliaisgrowninAustralia.Also,almostall

chickenmeatproducedinAustraliaisconsumed

locally,withlessthan5%beingexported.90%of

thepopulationeatschickenmeatatleastoncea

week,andathirdeatitthreeormoretimesaweek.

Percapita,consumptionofpoultrymeathassoared

from10.5kg(1969–70)to44.6kg(2012-13).

Conventionalchickenfarming

Unlikeotheranimalhusbandryindustries,the

chickenmeatindustryismostlyverticallyintegrated.

Typically,thismeansindividualcompaniesown

almostallaspectsofproduction,includingbreeding

farms,multiplicationfarms,hatcheries,feedmills,

somebroilergrowingfarms,andprocessingplants.

Twolargeintegratednationalcompaniessupply

morethan70%ofAustralia’sbroilerchickens.They

areBaiada(withbrandsLilydaleandSteggles)and

Inghams(ownedbyUS-basedTPGCapital),with

enterprisesinall6states.Themajorityof834,000

tonne-a-yearchickenmeatissoldonsupermarket

shelves.

Anothersixmedium-sized,privatelyownedcompanies

supplythebalanceofthemarket,witheachsupplying

betweenapproximately3-9%ofthenationalmarket.

Thereareamyriadofothersmallerprocessors.

Processingcompaniesgenerallycontractgrowers

togrowbroilerchickens,fromday-oldchicksto

thedayofprocessing.Approximately800growers

produceabout80%ofAustralia’smeatchickens

underthesecontracts.Othermeatchickensare

producedonlargecompanyfarms,oronfarms

ownedandmanagedby‘intermediary’companies.

Thesecompaniesownanumberoffarms,each

managedbyafarmmanager,andenterinto

contractswithprocessingcompaniestogrowout

chickensonalargerscale.

22

BurrawangGaianFarm’sproduceisproudlycertified‘HumaneChoice’

BurrawangGaianFarm’sHayden&BethMcMillanathome

Freerangechickenfarming

Thereisanichemarketforfreerangechickens,with

someconsumershappytopaymoreforfreerange

birds.Freerangebirdsarematuredforanextra

10-12daysandhavelessfatthanconventionally

farmedbirds.Examplesofniche,highvaluepoultry

productionalreadyexistintheMacleayValley

(seetheMacleayValleyFoodBowlwebsitefor

informationonBurrawongGaianpoultryfarm).

Organicchickenfarming

Certifiedorganicchickenfarmingmustfollowthe

rulesoforganiccertificationbodies.

Gamebirds

Gamebirdsincludespeciesofbirdstraditionally

huntedinvariouspartsoftheworldforfoodorsport.

Theyincludepheasants,partridges,guineafowl,

quail,geeseandpigeons(squab).

Opportunitiesmayexisttoproducegamebirdsfor

specialtymarkets,includingrestaurantsorbutchers.

Competitive advantage

ThemainadvantageoftheMacleayValleyregion

forchickenmeatproductionisthemildclimateand

accesstomajormarketsforthosewhodonotwant

togrowundercontractforthemajorproducers.

Markets - selling chicken meat

Ifyoudonotwanttogothroughthemajorchicken

meatproducersandsupermarkets,trytolinkwith

localproducersandproducergroups.Oneoption

istolistyourfarmathttp://flavourcrusader.com/

orwithsimilarorganisations.Trytocollaborate

withexistinglocalproducerstogetstarted.Inthe

Macleay,thereisstrongmarketdemandforHumane

Choiceaccreditedchicken,withtheownersof

BurrawongGaianpoultryfarmatBarraganyatti

willingtotrainothersinhowtoraisepasture-raised,

HumaneChoiceaccreditedbirds.

Key considerations

Ifyouareconsideringgettingintochicken

production,besureyouconsideryourinitial

investmentcosts,infrastructurerequirementsand

timetobreakeven.

Growingmeatchickensundercontracttoa

processorcanprovidearegularincomecompared

tomanyothertypesofagriculturalenterprises,butit

doesrequireahighlevelofinitialcapitalinvestment.

Emergencyandotherdiseasespresentsome

risks,particularlyasitisnotpossibletocontrolthe

movementsofwildbirds,whichcanoftenbethe

hostsofdiseaseagents.However,adherenceto

acceptedindustrybiosecuritymeasuressignificantly

mitigatesthisrisk.

Approvalforapoultryfarmdevelopmentneeds

tobeobtainedfromKempseyShireCounciland

DevelopmentApplicationsinvariablyneedtobe

supportedbyastrongcasethattheenvironment

(includingfortheneighbouringhumanpopulation)

willnotbesignificantlyadverselyimpacted.Notall

siteswillbesuitableforapoultryfarmdevelopment.

Aconsultantcanbeengagedtoassistinthe

preparationofaDA(includinganEnvironmental

ImpactStudy).Thecostsofthiswillneedtobetaken

intoaccountwhencalculatingyouroperationset-up

costs.

23

FresheggsfromBurrawangGaianFarm Pasture-raisedpoultryatBurrawangGaianFarm

Itisstronglyrecommendedthatanyoneinterested

inestablishingameatchickenfarmcontacttheir

closestchickenprocessing/marketingcompaniesto

findoutwhatopportunitiesexistforgrowingand

supplying,aswellasanyadditionaladviceonthe

bestwaytoproceed.

Regulatoryconsiderations

Poultryfarming,aswithanyintensiveanimal

farming,canonlybeundertakenindesignated

zones.Newfarmswillnormallyneedbothplanning

approvalfromKempseyShireCouncilaswellas

environmentalapprovalfromlocalgovernment,the

StateEnvironmentProtectionAuthority(EPA)or

theStateagriculturedepartmentorequivalent.

Statedepartmentsresponsibleforagriculture

canassistnewentrantstounderstandthevarious

regulatoryrequirementsthatneedtobemetby

chickenfarms(suchasplanningandenvironmental)

togainapprovaltooperate.Theycanalsoprovide

guidanceastootherregulatoryrequirements

thatneedtobemetoncethefarmisoperational

(suchasbirdwelfarestandardsandfoodsafety

requirements).

Further information

TheDepartmentofPrimaryIndustries(DPI)NSW

providessupporttothepoultryindustrythrough

itsextensionofficers,researchscientists,diagnostic

laboratories,publications,poultrykeepingcourses

andregulatoryservices(referto:dpi.nsw.gov.au/

agriculture/livestock/poultry).

DPINSWpublishedapracticalAgGuidehandbook

“Gettingstartedinfreerangepoultry”.Toorder,

visit:dpi.nsw.gov.au/aboutus/resources/bookshop/

poultry-agguide-free-range

Alsocheckout:PoultryHub:poultryhub.organd

www.chicken.org.au.

Theindustrybodiesare:

• AustralianChickenMeatFederationInc.

• AustralianChickenGrowersCouncil.

Future outlook

Forecastscurrentlyuniformlypredictcontinued

steadygrowthinbothproductionanddomestic

consumptionofchickenmeat.Onedriverfor

increasedconsumptionisthefactthatchicken

meathascontinuedtogetcheapercomparedto

othermeat.Thisisduetoimprovedbreedsandbird

management.Chickenmeatexportsareprojected

toremainrelativelylow,withmostproduction

consumeddomestically.

Thepositiveoutlookfortheindustryandpotential

increaseddemandforfreerangepoultrymay

provideopportunitiesforthosewhowanttoruna

hatcheryorgrowmeatchickens.

Up-to-dateinformationonmarketsandprices

shouldbeobtainedfromtheorganisations

suggestedinthisGuide,includingindustrybodies.

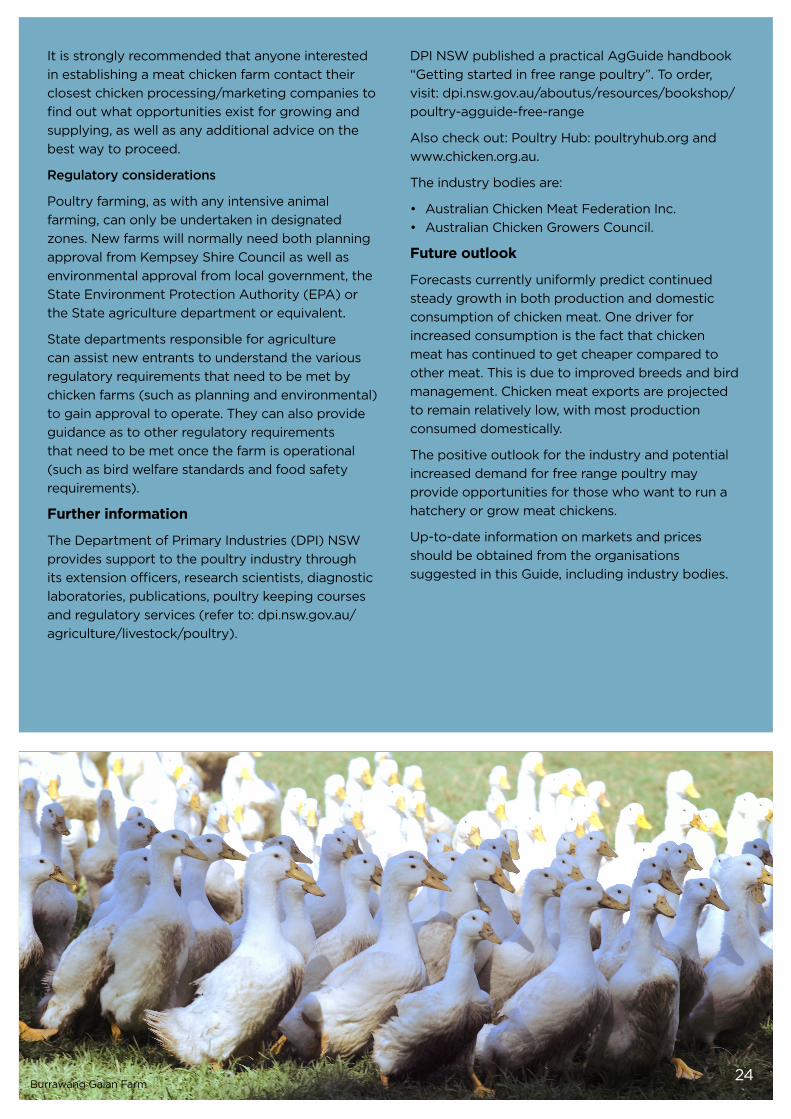

24BurrawangGaianFarm

Poultry egg production (layers)

Thebestwaytoobtaininformationonopportunities

andrequirementsforpoultryeggproduction

istoobtainacopyofthe2015NSWPoultry

EggIndustryOverview,publishedbytheNSW

DepartmentofPrimaryIndustries(NSWDPI).It

canbeobtainedat:dpi.nsw.gov.au/__data/assets/

pdf_file/0010/578422/poultry-egg-industry-

overview-2015.pdf

NSWDPIhasalsopublishedinformationspecifically

forsmallholders,whichcanbefoundat:dpi.nsw.

gov.au/content/agriculture/livestock/poultry/

production-small-scale.

25BurrawangGaianFarm

7.3 Animal husbandry – pigsOpportunitiesmayexisttoproducefree-range

pigsforspecialtymarkets,includingrestaurantsor

butchers.

DownloadafreecopyofthePROOFe-book,

‘GettingStartedinFreeRangePigs’at:

australianpigfarmers.com.au.

7.4 Dairy ThedairyindustryiswellestablishedintheMacleay

Valleyregion,withgoodnetworks,supportand

apathtomarket.Anopportunitymayexistto

producelocallybrandedspecialtycheeses.There

arealreadyanumberofsmall-scale,nichemarket

dairyoperatorsintheareatothesouthofthe

Macleay,withEwetopiaandComboyneCultureboth

producingcheesesandotherdairyproducts.

Otherexamplesofthistypeofdevelopmentinclude

KingIslandCheesesorAshgroveCheese,Tasmania.

Current industry context

About40%ofAustralianmilkproductionisexported

toAsia,predominantlyJapanandGreaterChina.

CurrentlymilkistransportedoutsidetheMacleay

regionforprocessing.

Awell-establishedprocessor,Norco,supports

growersintheregionandexploresmarket

opportunities.Strongnetworksexist.DairyNSWand

DairyAustraliaprovidestrategicdirection,research,

developmentandextensionsupporttothelocal

dairyindustry.

Competitive advantage and opportunities

• Climateandalluvialsoilssupportrain-fedpastures

• Growingconditionsforfoddercropsaregood

• Goodagronomyandsupportnetworksexist

• Localmanufacturingofbrandedspecialitymilk

productshaspotential.

Markets for milk

ThedairyindustryinAustraliaislargelyvertically

integrated.Processorscontractdairyfarmersto

producecertainvolumesofmilk.Takingthisroute

tomarketsuitspeoplewhodonotwanttoprocess

andmarkettheirownproduce.Thebestwaytoget

informationonthesupplychainistotalktolocal

producers,advisersandaNorcorepresentative,as

theyareregionallylocated.

Key considerations

Majorconsiderationsincludemarkets,initial

investment,infrastructurerequirementsandtimeto

breakeven.Globally,productionexceedsdemand

mostofthetime,whilecurrentexporttrade

agreementsarefavouringcompetitors.Fluctuations

inkeyinputpricescanoccur,especiallyforfertiliser

andfodder,whichcanaffectprofitability.Still,

specialitycheesesandothermilkproductswitha

provenancebrandmaybeabletowithstandmarket

fluctuations.Existingregionaloperatorsshouldbe

consultedtoconfirmthis.

Future outlook

TheAustralianBureauofAgriculturalandResource

EconomicsandSciences(ABARES)predictionisfor

short-termimprovementduetoincreasingdemand,

butdecliningrealtermmilkpricesinthemedium

termduetocompetitionfromotherexporting

nations(Source:ABCRural,4March2015).

26

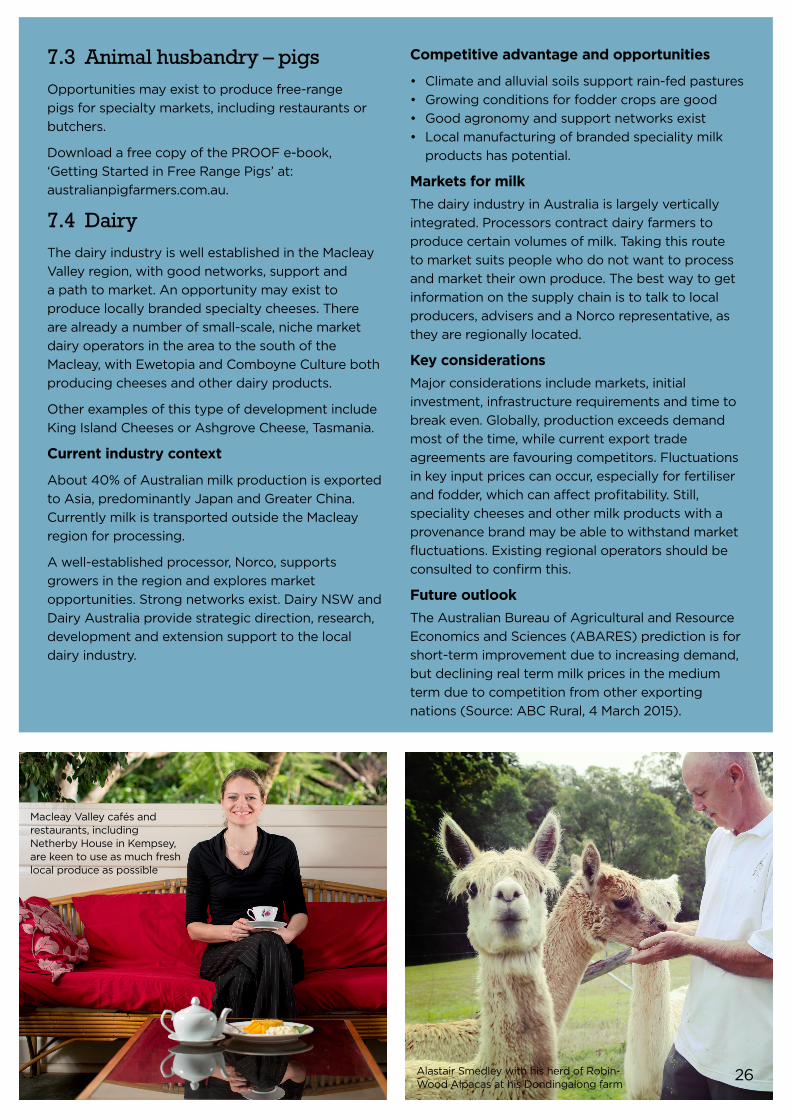

MacleayValleycafésandrestaurants,includingNetherbyHouseinKempsey,arekeentouseasmuchfreshlocalproduceaspossible

AlastairSmedleywithhisherdofRobin-WoodAlpacasathisDondingalongfarm

7.5 Buffalos Buffalosareprimarilydairyanimals,butcanalso

beasourceofmeatandleather.Farmingbuffalo

requiresapermitorlicenceinallstatesand

territoriesexcepttheNorthernTerritoryandfarming

isbannedinsomelocations,suchastheKimberley

inWesternAustralia.

Asat2011–12,therewere65buffalofarmsin

Australiaandthenationalherdwas12,000.In2014

anaerialsurveyofArnhemLandintheNorthern

Territoryestimatedaminimumof100,000headof

free-rangebuffalo.Abuffalodairyexistsjustnorth

ofKempseyatEungaiCreekBuffalo,withnumerous

handcraftedgourmetdairyproductsbeingmade

onsite.

Australiancommercialbuffaloaretheswampand

riverinetypesofwaterbuffalo(Bubalusbubalis),or

variouscrossesofboth.Thefarmingofbuffalois

verysimilartofarmingbeefanddairycattle,except

thatbuffaloaremoreefficientatconvertingpoor

feedtoenergy.

Whilegoodmarketsexistforliveexportandbuffalo

milk,meatproductionislimitedbythelackof

abattoirfacilitieswillingtoslaughterbuffalo.Buffalo

areconsideredapestspeciesinsomestatesandon-

farmanimalsmustberegisteredannually.Alltrade

oflivestockrequiresStateGovernmentpermits.

7.6 Goat and sheep milk production Goodinformationaboutfarmingandmarketing

goatandsheepmilkproductscanbeobtainedvia

theRIRDCPublicationNo08/207availablethrough

https://rirdc.infoservices.com.au/downloads/08-207

orcontactingRIRDCvia0262714160,or

TheNSWbranchoftheDairyGoatSocietyof

Australiacanprovideregionallyrelevantinformation.

Findinformationviadairygoatnsw.com.auorcontact

thebranchvia(02)98261371orwritetobyerst@

nswfarmers.org.au.

7.7 CroppingDuetoitsclimate,theMacleayiscapableof

producingabroadrangeofcrops.Thetwo

variablesthatyouneedtoresearcharemarket

opportunitiesandtheavailabilityofsuitableland.

Soils,microclimateandlandparcelinformation

containedinthisGuideprovidessomedirectionon

thesuitabilityofspecificlocationsforwheat,barley,

grainsorghum,maize,chickpeas,lentils,favabeans,

sweetsorghumandsoybeans.

Typicalbroadacrecropsrequirescaleofproduction

andmostcurrentfarmsizesintheMacleaydonot

providetherequiredscale.Specialtymarketsfor

organicgrainsmayexistandshouldbeexploredon

anindividual,case-by-casebasis.

27BushtuckergrownatWigayFarminKempseyisapopulartouristattraction

Localbananasarerenownedfortheirsizeandsweettaste

7.8 Perennial horticulture – fruit, nuts, flowers, and speciality crops Basedontheregion’sclimate

andsoiltypes,therearea

numberofperennialcrops

thatcanbegrownonsuitable

farmsintheMacleayValley.

Marketopportunitiesshould

beidentifiedonacase-by-case

basis.Soils,landcapability,

andmicroclimateinformation

fromthisGuidecanbeusedfor

initialdirectiononthesuitability

ofspecificlocations.Details

onthespecificproduction

requirementsforeachof

thecropslistedbelowcan

beundertakenbydoinga

comprehensiveinternetsearch,

beginningwiththeorganisations

suggestedinthisGuide.It

isrecommendedthatyou

followupyourdeskresearch

withsitevisits,advicefrom

thelocalandindustryservice

providerslistedinthisGuide

andsuggestedbyKempsey

ShireCouncil.Forsomecrops,

financialinformationisavailable

online.However,itisessential

togetindividualadvicefroma

registeredfinancialadviser.

Suitablefruitcrops• Avocado

• Blueberry

• Cacao

• Citrus,eg

–Nativecitrustypes

–Grapefruit

–Lime

• Custardapple

• Dragonfruit(Pitaya)

• NativeDavidsonplum

• Fig

• Grape

• Kiwifruit

• Lychee

• Melon

• Persimmon

• Pawpaw/papaya

• Pomegranate

• Raspberry

• Riberry

• Tomato(fieldorhydroponic)

• Nativebushtomato

• Arangeofexoticsubtropical

fruitfromaroundtheworld

couldbegrownifplanting

stockisavailableinAustralia

Suitablenutcrops• Almond

• Chestnut

• Hazelnut

• Macadamianut

• Pecan

• Pistachio

• Walnut

Suitableornamentalcrops/flowers• Banksia

• Eucalyptusfoliage

• FlannelFlower

• Kangaroopaw

• Waratah

• Waxflower

• Leucospermum

• Leucadendron

Suitablespecialitycrops• Coffee

• NativeAniseMyrtle

• Blacktea

• Ginger

• Lavenderoil

• Lemonmyrtle(Myrtlerust

freeareas)

• Teatreeoil

28

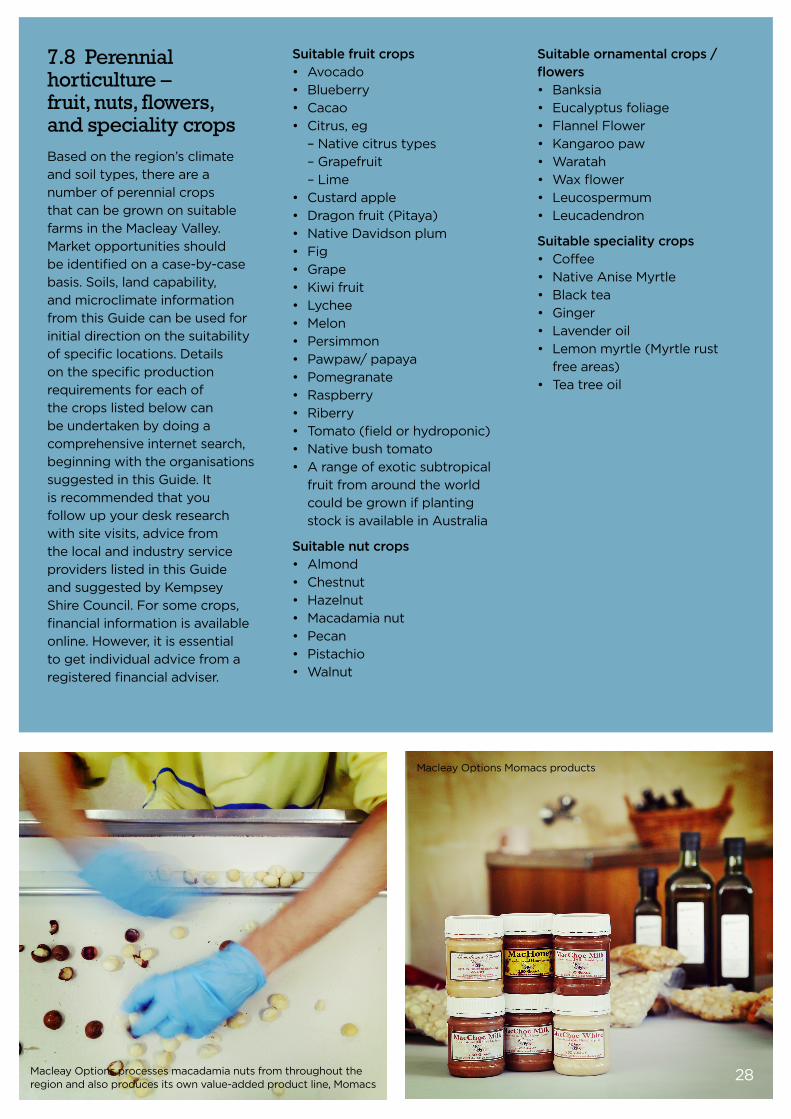

MacleayOptionsMomacsproducts

MacleayOptionsprocessesmacadamianutsfromthroughouttheregionandalsoproducesitsownvalue-addedproductline,Momacs

7.9 Annual horticulture crops – vegetables, herbs and spicesThefollowingvegetableand

herbcropscouldbegrownin

suitablelocationsintheMacleay

Valleyifmarketopportunities

havebeenidentified.Similar

toperennialhorticulturecrops,

thesoilsandmicroclimate

informationfromthisGuide

canbeusedfordirection

onthesuitabilityofspecific

locations.Detailsonthespecific

productionrequirementsof

eachcroplistedbelowcanbe

obtainedviaacomprehensive

internetsearch,startingwith

theorganisationssuggested

intheGuide.Forsomecrops,

financialinformationisavailable

online.However,itisessential

togetindividualadvicefroma

registeredfinancialadviser.

• Asianleafygreens

• Bittermelon

• Culinarybambooshoots

• Jerusalemartichoke

• Artichoke

• GreenSnakebean

• Capsicum-fieldor

hydroponic

• Chilli

• Cucumber-fieldor

hydroponic

• Eggplant

• Okra

• Pumpkin

• Taro

• Zucchini

7.10 Other potential opportunities• Nursery,turfandornamentals

• Industrialhemp

• Widerangeofleafyherbsor

spices

–Turmeric(fresh)

–Garlic(fresh)

–Ginger(fresh)

–Seeds(sesame,sunflower

etc)

–Wattleseed

–Nativepepperberries

–Aniseedmyrtle

–Seedsprouts-hydroponic

• Mushrooms

• Timber(CalifornianRedwood,

RiverSheoak,SpottedGum,

BlackWalnut,RedCedar,

Sandalwood,RedIronbark,

SilkyOak)

• Organics(localorganics

producersarestrongly

supportedbythelocally

basedOrganicMarketing

Company).

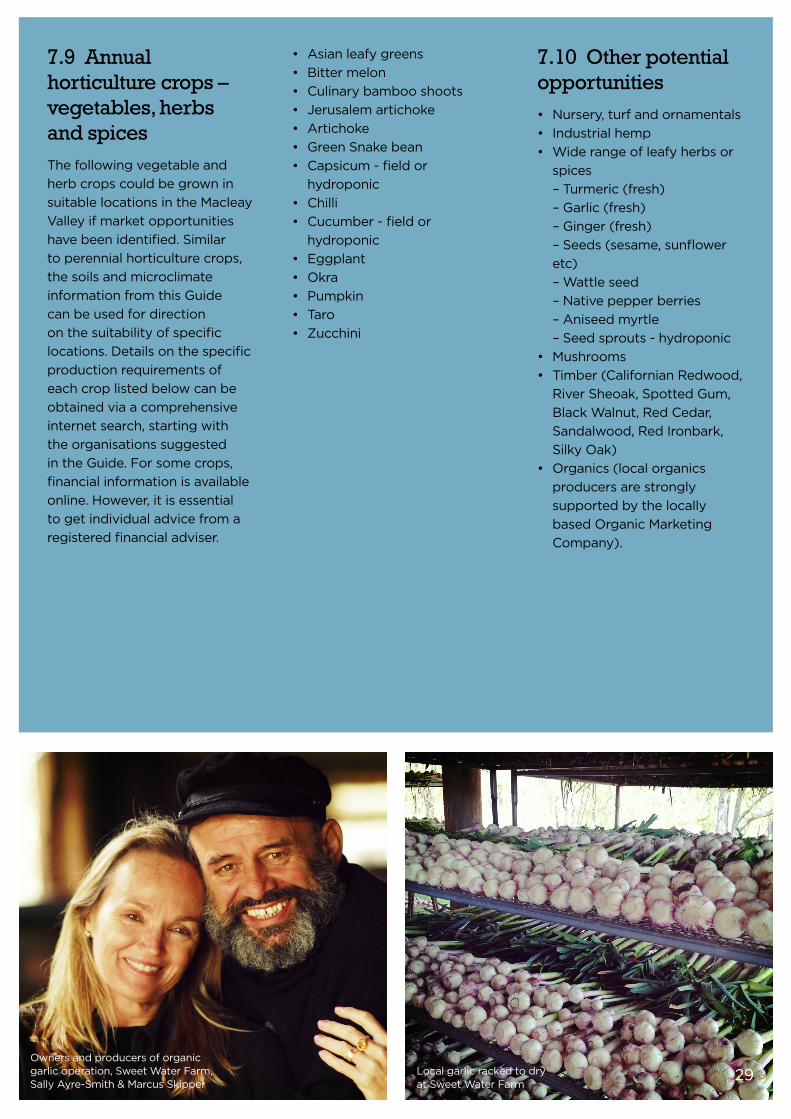

29Ownersandproducersoforganicgarlicoperation,SweetWaterFarm,SallyAyre-Smith&MarcusSkipper

LocalgarlicrackedtodryatSweetWaterFarm

8 Getting started

Beforeyoustartdiversifyingyourfarm,orsetting

upanewagribusiness,takeafewminutestoanswer

thesequestions1:

Canyoudescribetheproposedendproducttobe

sold?

Ifyoucandescribetheproduct/saccurately,

andidentifythemarketsfortheproduct/s,then

someofthehardworkmaybedone.Ifyouare

unabletodescribetheproduct/saccurately,then

itsmarketabilitymaynotyetbedetermined.

Althoughtherangeofpossibleproductsfromanew

enterprisemaybeexciting,ifthereisnoestablished

demandormarket,orthepathwaytomarketis

unclear,thensubstantialworkmayneedtobedone

tocultivatethesemarkets.Thiscantakeyears,

financialinvestmentandpersonalcommitment.

Isthereanestablishedmarketordemandforthe

proposedproduct?

Researchingandunderstandingthemarketsfor

anewenterpriseisessential.Ifthemarketisnot

established,youmayneedtodevelopdemandfor

yourproductinordertosellit.Ifitisanestablished

market,youwillneedtounderstandanyregulations,

suchasproductstandards,thatgovernthetrading

oftheproduct.Somequestionsthatcanhelpguide

yourmarketresearchinclude:

• Whoisthecustomer(agent,wholesaler,retailer,

consumer)?

• Istheproductcurrentlytradedhereoroverseas?

• Wherearetheexistingmarketsfortheproduct?

• Whattypeofmarketsarethese,intermsofsize?

• Whereisthetargetmarketfortheintendednew

product?

• Arethereanylimitationsimposedbythemarket?

• Whatistheproductusedfor,leadingto

identificationofsubstitutesfortheproductand

thenatureofthesubstitution?

• Whatistheestimatedmarketprice(pricepoint)

thatisrequiredfortheventuretobeviable,taking

intoaccountthecostofproduction,possible

pricesofsubstitutes,andimport/exportprices?Is

thepricepointachievableandsustainable?

• Whatpackagingisrequiredandistherea

distributionmechanismavailable?

• Whatistheestimatedfuturedemand(takinginto

accounteconomicanddemographicfactorsand

factorswhichmayaffectthisdemand)?

• Arethereexistingandaccessiblesupplychains

fortheproposedproduct?

• Whatmarketingand/orpromotionalstrategies