Embed Size (px)

Citation preview

Romanian financial system – recent developments and perspectives

Liviu Voinea Deputy Governor

Bucharest, 9 March 2016

2

Romania made significant progress over the past years…

• GDP growth accelerated, output gap expected to turn positive in 2016

• Inflation is very low (negative rates) mainly due to fiscal measures,

domestic consumption is strong

• Strong fiscal consolidation

• MTO reached in 2014

• All nominal convergence criteria have been met since second half of 2014

• Transmission of monetary policy improved

• Lower contagion risk in the banking sector

• NPLs substantially reduced

• Romania exit the EDP in 2013 and the MIP in 2016

…This progress has been achieved with the support of EC and IMF…

…but there is an increasing risk of policy reversal by unwarranted legislative

proposals and pro-cyclical fiscal measures

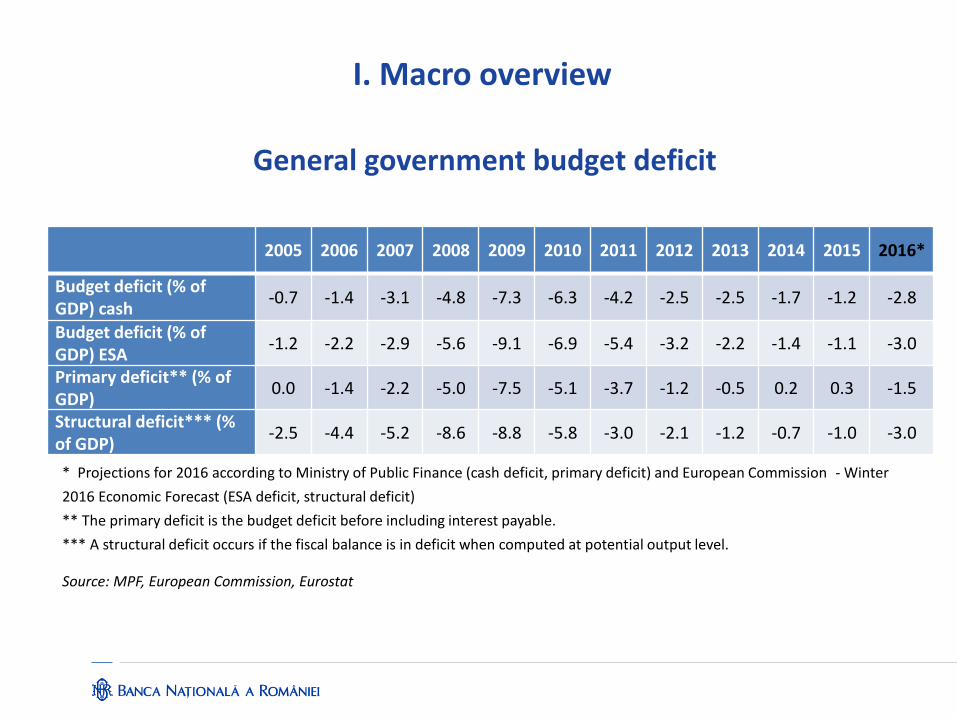

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Budget deficit (% of GDP) cash

-0.7 -1.4 -3.1 -4.8 -7.3 -6.3 -4.2 -2.5 -2.5 -1.7 -1.2 -2.8

Budget deficit (% of GDP) ESA

-1.2 -2.2 -2.9 -5.6 -9.1 -6.9 -5.4 -3.2 -2.2 -1.4 -1.1 -3.0

Primary deficit** (% of GDP)

0.0 -1.4 -2.2 -5.0 -7.5 -5.1 -3.7 -1.2 -0.5 0.2 0.3 -1.5

Structural deficit*** (% of GDP)

-2.5 -4.4 -5.2 -8.6 -8.8 -5.8 -3.0 -2.1 -1.2 -0.7 -1.0 -3.0

* Projections for 2016 according to Ministry of Public Finance (cash deficit, primary deficit) and European Commission - Winter

2016 Economic Forecast (ESA deficit, structural deficit)

** The primary deficit is the budget deficit before including interest payable.

*** A structural deficit occurs if the fiscal balance is in deficit when computed at potential output level.

Source: MPF, European Commission, Eurostat

General government budget deficit

I. Macro overview

External balance improved

The current account deficit narrowed significantly since 2009, but resumed growth in 2015 as domestic

consumption expands

The surplus for trade in services widen over the past years, driven by transport and IT

Current account balance

Source: NBR

4

-25

-20

-15

-10

-5

0

5

10

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Goods Services Income Current account/GDP

balance, EUR billions/ percent

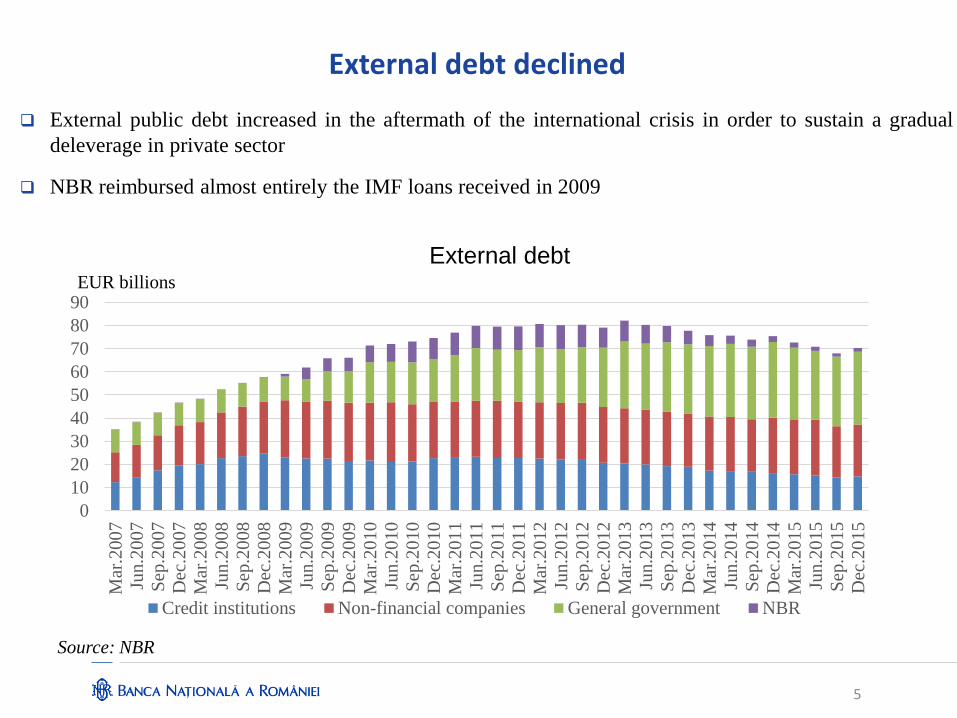

External debt declined

External public debt increased in the aftermath of the international crisis in order to sustain a gradual

deleverage in private sector

NBR reimbursed almost entirely the IMF loans received in 2009

Source: NBR

0

10

20

30

40

50

60

70

80

90

Mar

.200

7

Jun.2

007

Sep

.2007

Dec

.20

07

Mar

.200

8

Jun.2

008

Sep

.2008

Dec

.20

08

Mar

.200

9

Jun.2

009

Sep

.2009

Dec

.20

09

Mar

.201

0

Jun.2

010

Sep

.2010

Dec

.20

10

Mar

.201

1Ju

n.2

011

Sep

.2011

Dec

.20

11

Mar

.201

2Ju

n.2

012

Sep

.2012

Dec

.20

12

Mar

.201

3Ju

n.2

013

Sep

.2013

Dec

.20

13

Mar

.201

4

Jun.2

014

Sep

.2014

Dec

.20

14

Mar

.201

5

Jun.2

015

Sep

.2015

Dec

.20

15

Credit institutions Non-financial companies General government NBR

EUR billions

External debt

5

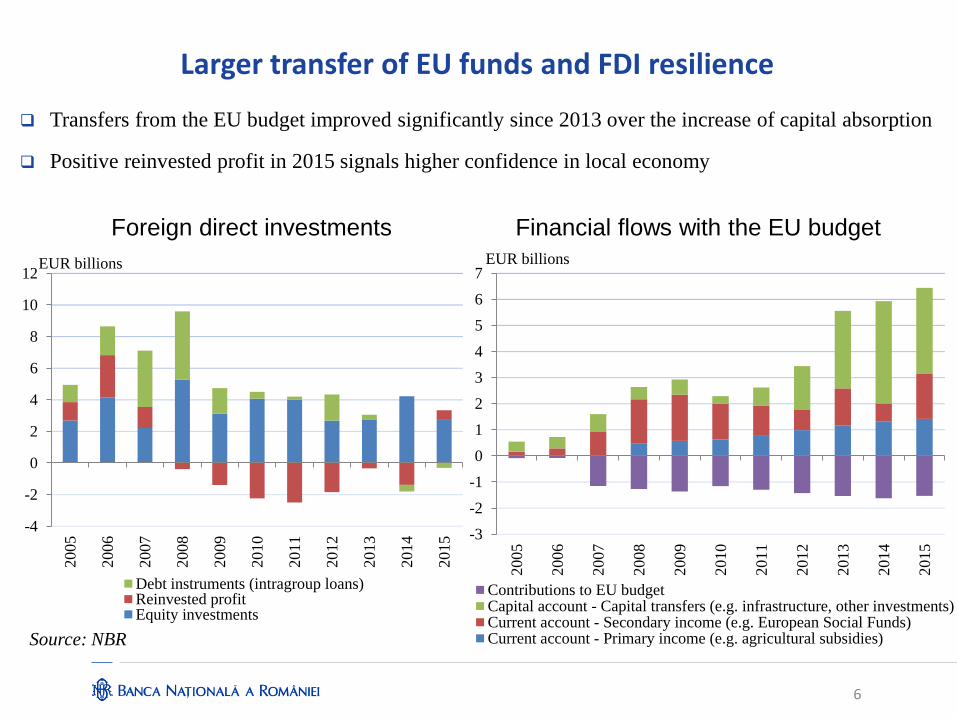

Larger transfer of EU funds and FDI resilience

Transfers from the EU budget improved significantly since 2013 over the increase of capital absorption

Positive reinvested profit in 2015 signals higher confidence in local economy

Foreign direct investments Financial flows with the EU budget

Source: NBR

-4

-2

0

2

4

6

8

10

12

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Debt instruments (intragroup loans)Reinvested profitEquity investments

EUR billions

-3

-2

-1

0

1

2

3

4

5

6

7

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Contributions to EU budgetCapital account - Capital transfers (e.g. infrastructure, other investments)Current account - Secondary income (e.g. European Social Funds)Current account - Primary income (e.g. agricultural subsidies)

EUR billions

6

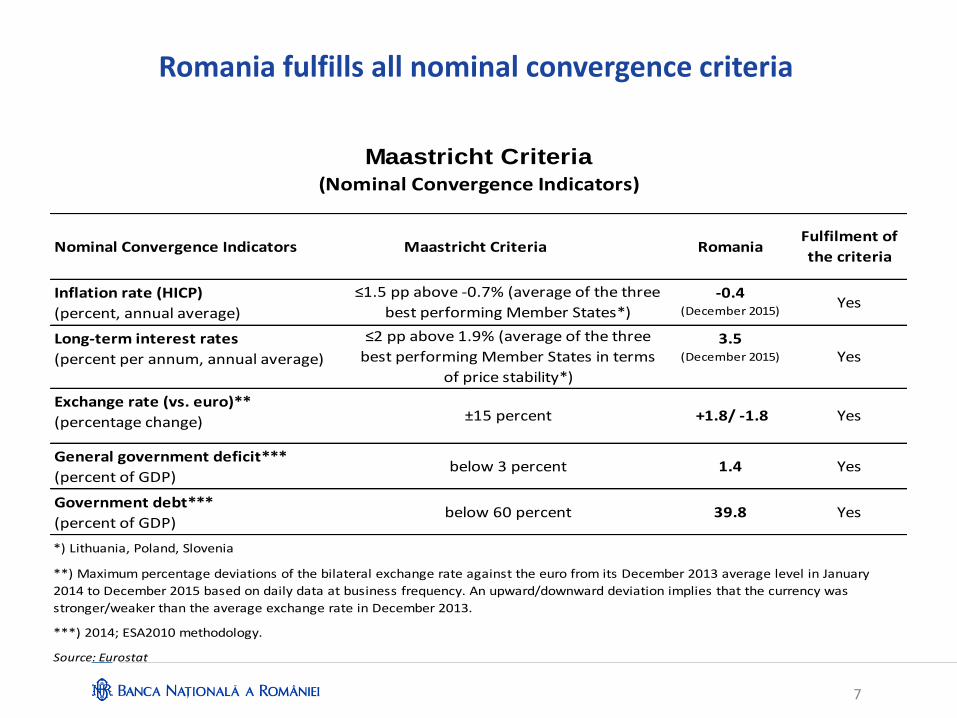

Romania fulfills all nominal convergence criteria

7

Inflation rate (HICP) -0.4

(percent, annual average) (December 2015)

Long-term interest rates 3.5

(percent per annum, annual average) (December 2015)

Exchange rate (vs. euro)**

(percentage change)

General government deficit***

(percent of GDP)

Government debt***

(percent of GDP)

Source: Eurostat

Maastricht Criteria

(Nominal Convergence Indicators)

Nominal Convergence Indicators Maastricht Criteria RomaniaFulfilment of

the criteria

≤1.5 pp above -0.7% (average of the three

best performing Member States*) Yes

≤2 pp above 1.9% (average of the three

best performing Member States in terms

of price stability*)

Yes

±15 percent +1.8/ -1.8 Yes

below 3 percent 1.4 Yes

**) Maximum percentage deviations of the bilateral exchange rate against the euro from its December 2013 average level in January

2014 to December 2015 based on daily data at business frequency. An upward/downward deviation implies that the currency was

stronger/weaker than the average exchange rate in December 2013.

***) 2014; ESA2010 methodology.

below 60 percent 39.8 Yes

*) Lithuania, Poland, Slovenia

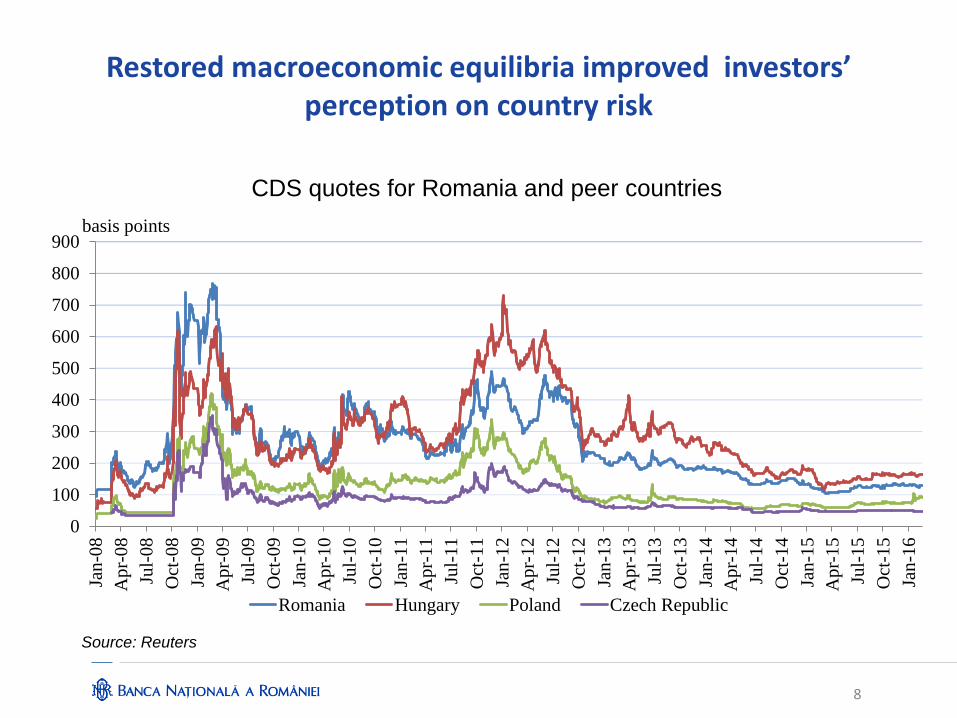

Restored macroeconomic equilibria improved investors’ perception on country risk

8

CDS quotes for Romania and peer countries

Source: Reuters

0

100

200

300

400

500

600

700

800

900

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Romania Hungary Poland Czech Republic

basis points

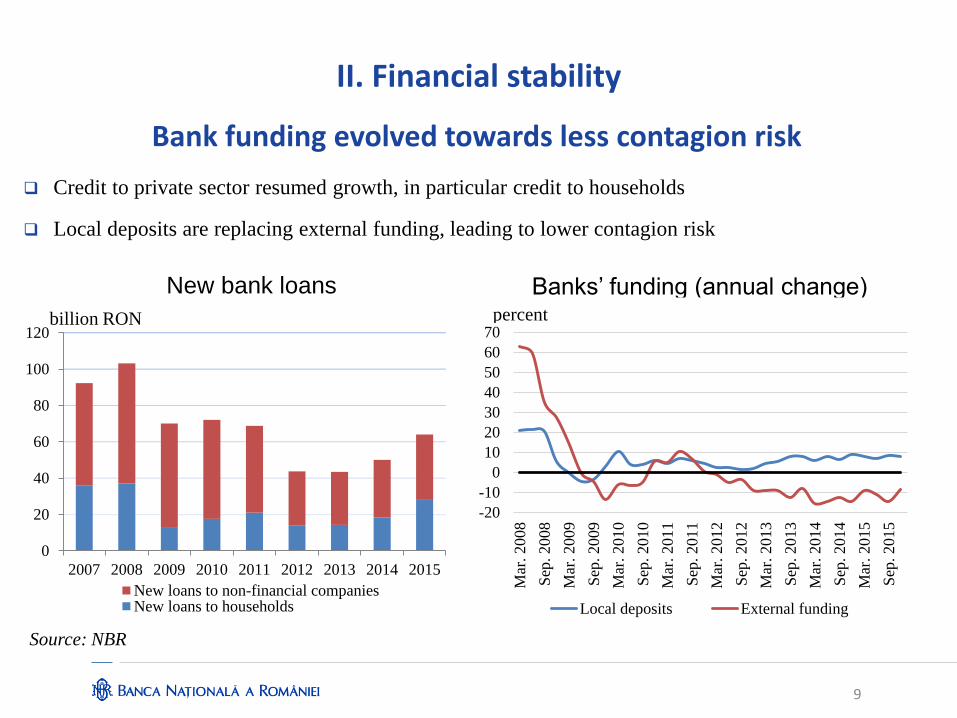

Bank funding evolved towards less contagion risk

Credit to private sector resumed growth, in particular credit to households

Local deposits are replacing external funding, leading to lower contagion risk

New bank loans Banks’ funding (annual change)

Source: NBR

9

II. Financial stability

0

20

40

60

80

100

120

2007 2008 2009 2010 2011 2012 2013 2014 2015

New loans to non-financial companiesNew loans to households

billion RON

-20

-10

0

10

20

30

40

50

60

70

Mar

. 2008

Sep

. 2008

Mar

. 2009

Sep

. 2009

Mar

. 2010

Sep

. 2010

Mar

. 2011

Sep

. 2011

Mar

. 2012

Sep

. 2012

Mar

. 2013

Sep

. 2013

Mar

. 2014

Sep

. 2014

Mar

. 2

015

Sep

. 2015

Local deposits External funding

percent

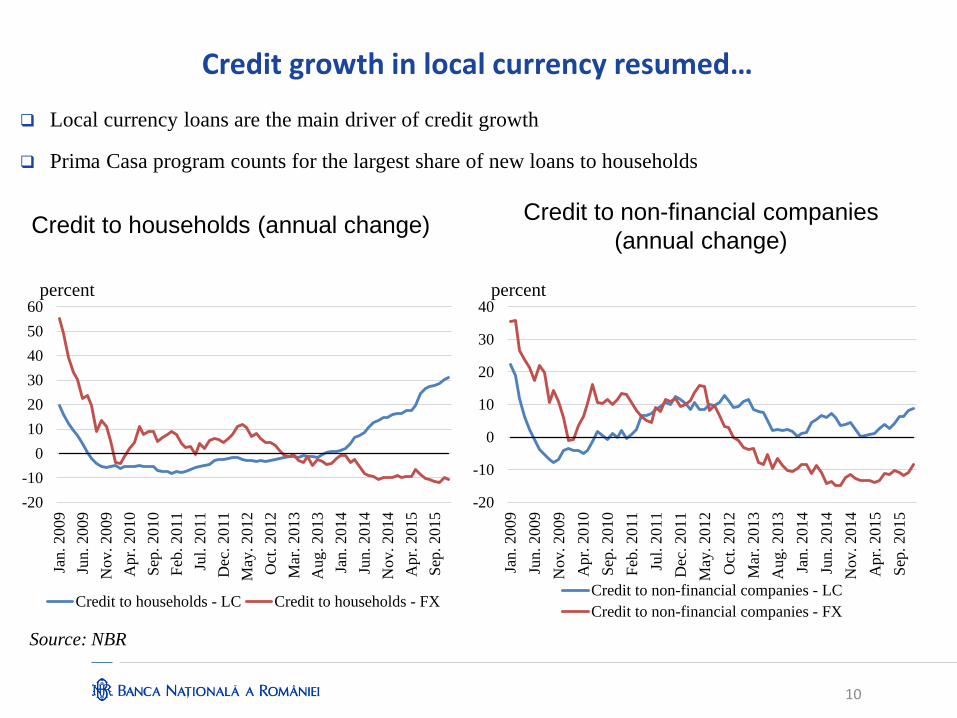

Credit growth in local currency resumed…

Local currency loans are the main driver of credit growth

Prima Casa program counts for the largest share of new loans to households

Credit to households (annual change) Credit to non-financial companies

(annual change)

Source: NBR

10

-20

-10

0

10

20

30

40

50

60

Jan.

2009

Jun. 2009

Nov. 2009

Apr.

2010

Sep

. 2010

Feb

. 2011

Jul.

2011

Dec

. 2011

May

. 2012

Oct

. 2012

Mar

. 2013

Aug. 2013

Jan.

2014

Jun. 2014

Nov. 2014

Apr.

2015

Sep

. 2015

Credit to households - LC Credit to households - FX

percent

-20

-10

0

10

20

30

40

Jan.

2009

Jun. 2009

Nov. 2009

Apr.

2010

Sep

. 2010

Feb

. 2011

Jul.

2011

Dec

. 2011

May

. 2012

Oct

. 2012

Mar

. 2013

Aug. 2013

Jan.

2014

Jun. 2014

Nov. 2014

Ap

r. 2

015

Sep

. 2015

Credit to non-financial companies - LC

Credit to non-financial companies - FX

percent

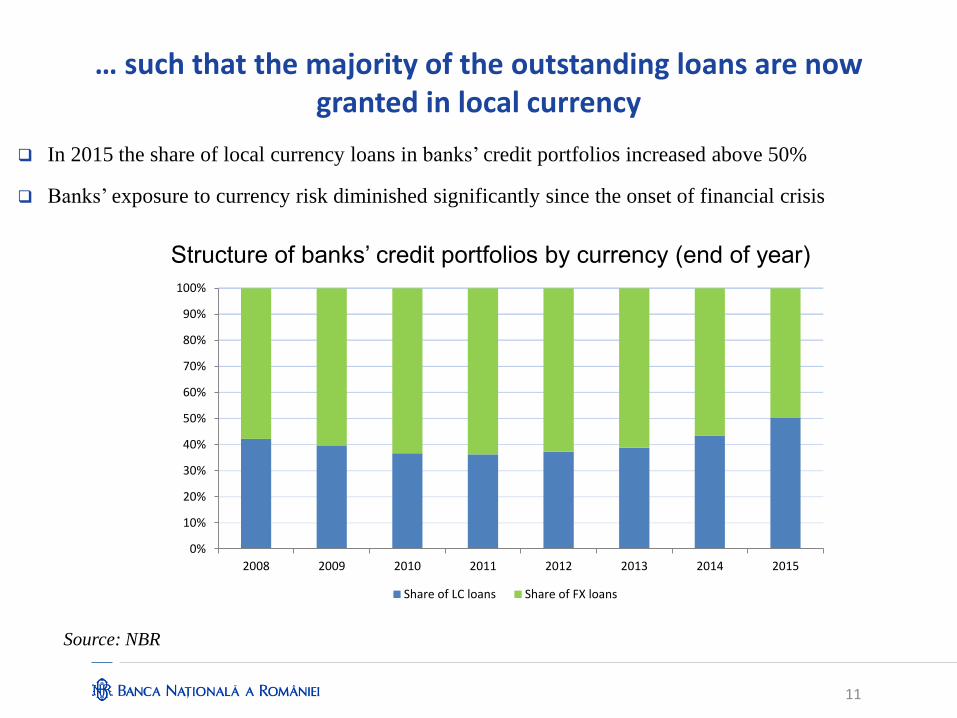

… such that the majority of the outstanding loans are now granted in local currency

In 2015 the share of local currency loans in banks’ credit portfolios increased above 50%

Banks’ exposure to currency risk diminished significantly since the onset of financial crisis

Structure of banks’ credit portfolios by currency (end of year)

Source: NBR

11

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015

Share of LC loans Share of FX loans

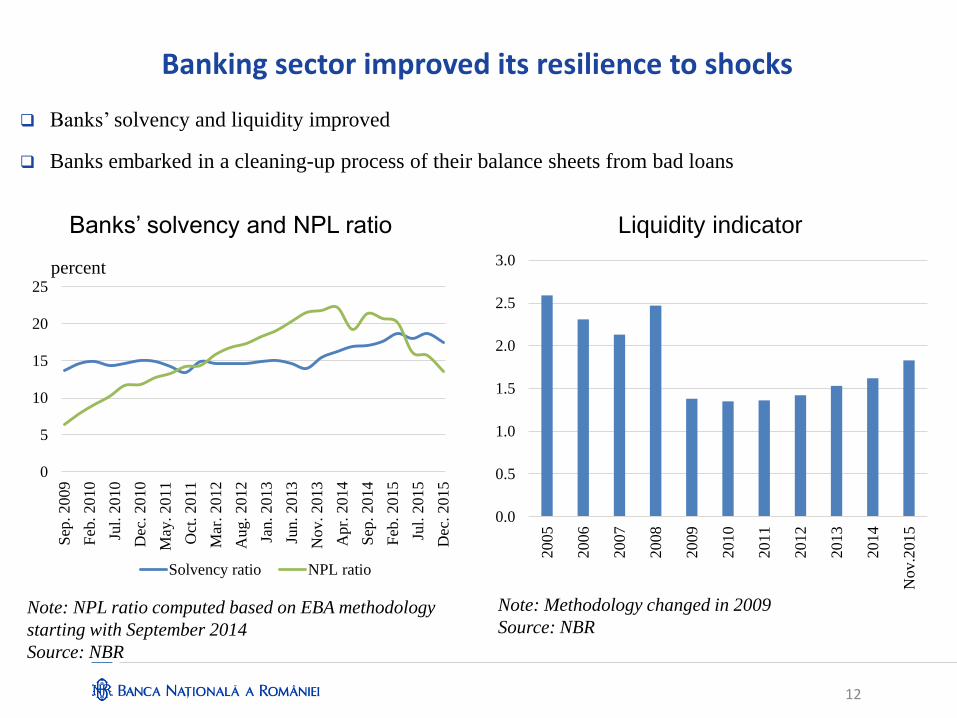

Banking sector improved its resilience to shocks

Banks’ solvency and liquidity improved

Banks embarked in a cleaning-up process of their balance sheets from bad loans

Banks’ solvency and NPL ratio Liquidity indicator

Note: NPL ratio computed based on EBA methodology

starting with September 2014

Source: NBR

0.0

0.5

1.0

1.5

2.0

2.5

3.0

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Nov.2

015

12

0

5

10

15

20

25

Sep

. 2009

Feb

. 2010

Jul.

2010

Dec

. 2010

May

. 2011

Oct

. 2011

Mar

. 2012

Aug. 2012

Jan. 2013

Jun. 2013

Nov. 2013

Apr.

2014

Sep

. 2014

Feb

. 2015

Jul.

2015

Dec

. 2015

Solvency ratio NPL ratio

percent

Note: Methodology changed in 2009

Source: NBR

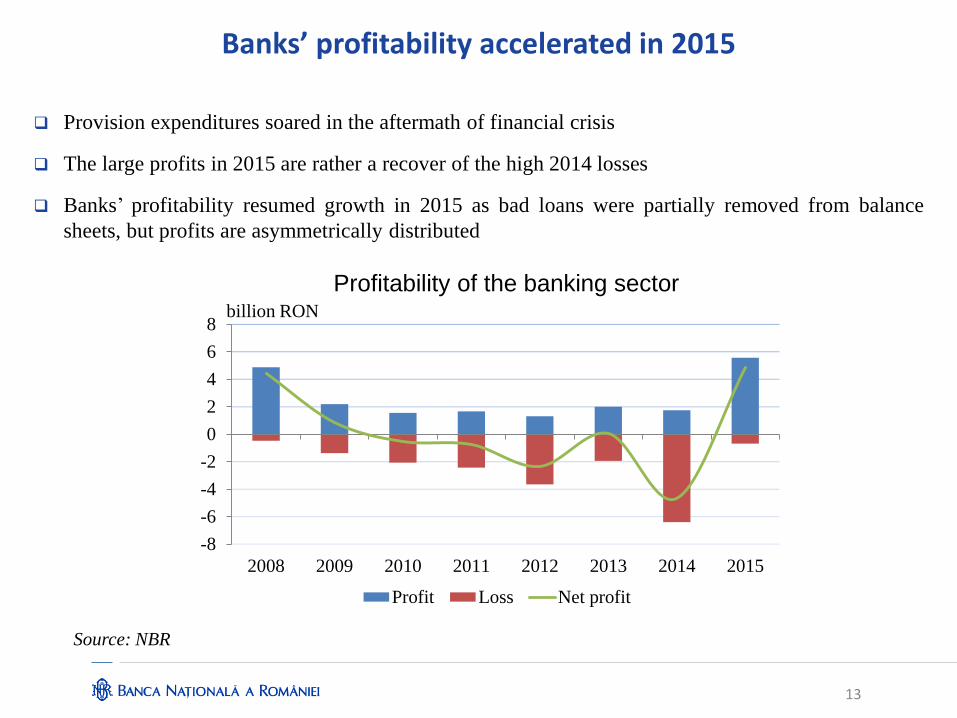

Banks’ profitability accelerated in 2015

Provision expenditures soared in the aftermath of financial crisis

The large profits in 2015 are rather a recover of the high 2014 losses

Banks’ profitability resumed growth in 2015 as bad loans were partially removed from balance

sheets, but profits are asymmetrically distributed

Profitability of the banking sector

Source: NBR

13

-8

-6

-4

-2

0

2

4

6

8

2008 2009 2010 2011 2012 2013 2014 2015

Profit Loss Net profit

billion RON

Main threat to financial stability: legislative

initiatives leading to uncertainty

• BNR defends price stability, financial stability, exchange rate stability

• Some legislative initiatives are aimed at changing terms of contracts already signed, creating instability and uncertainty.

• “Datio in solutum” law was approved by Parliament – then the President sent it to reexamination.

• The European Central Bank and the European Commission warned of threats to financial stability if this law is passed in its original form.

• BNR intervenes in this debate because it answers to the requests from the Presidency and Parliament.

• We are making proposals with the aim to answer the requests of the Presidency.

14

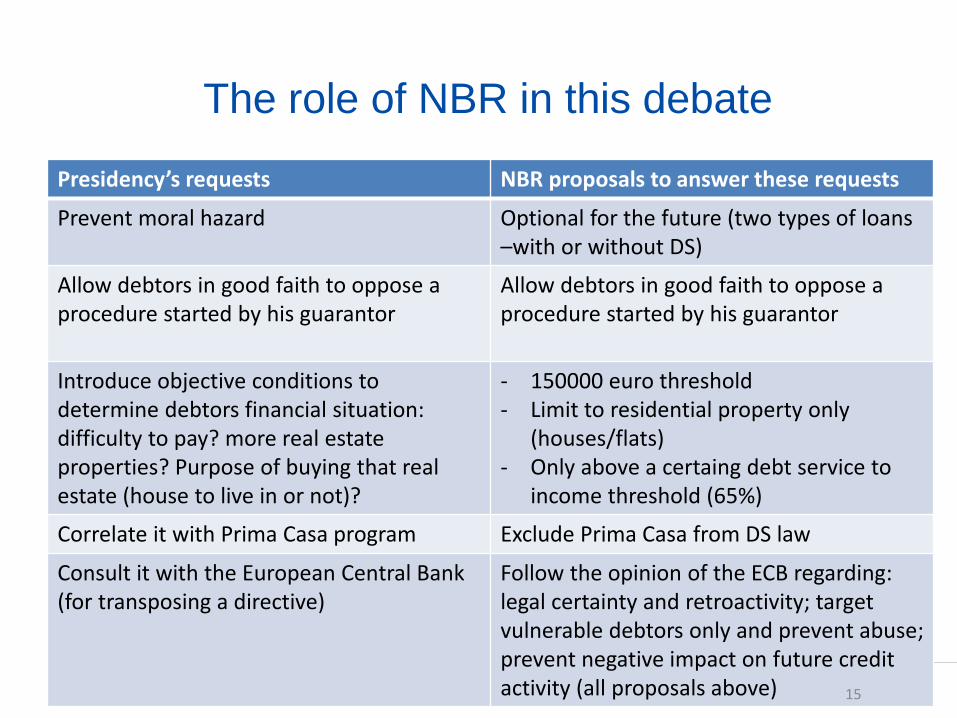

The role of NBR in this debate

Presidency’s requests NBR proposals to answer these requests

Prevent moral hazard Optional for the future (two types of loans –with or without DS)

Allow debtors in good faith to oppose a procedure started by his guarantor

Allow debtors in good faith to oppose a procedure started by his guarantor

Introduce objective conditions to determine debtors financial situation: difficulty to pay? more real estate properties? Purpose of buying that real estate (house to live in or not)?

- 150000 euro threshold - Limit to residential property only

(houses/flats) - Only above a certaing debt service to

income threshold (65%)

Correlate it with Prima Casa program Exclude Prima Casa from DS law

Consult it with the European Central Bank (for transposing a directive)

Follow the opinion of the ECB regarding: legal certainty and retroactivity; target vulnerable debtors only and prevent abuse; prevent negative impact on future credit activity (all proposals above) 15

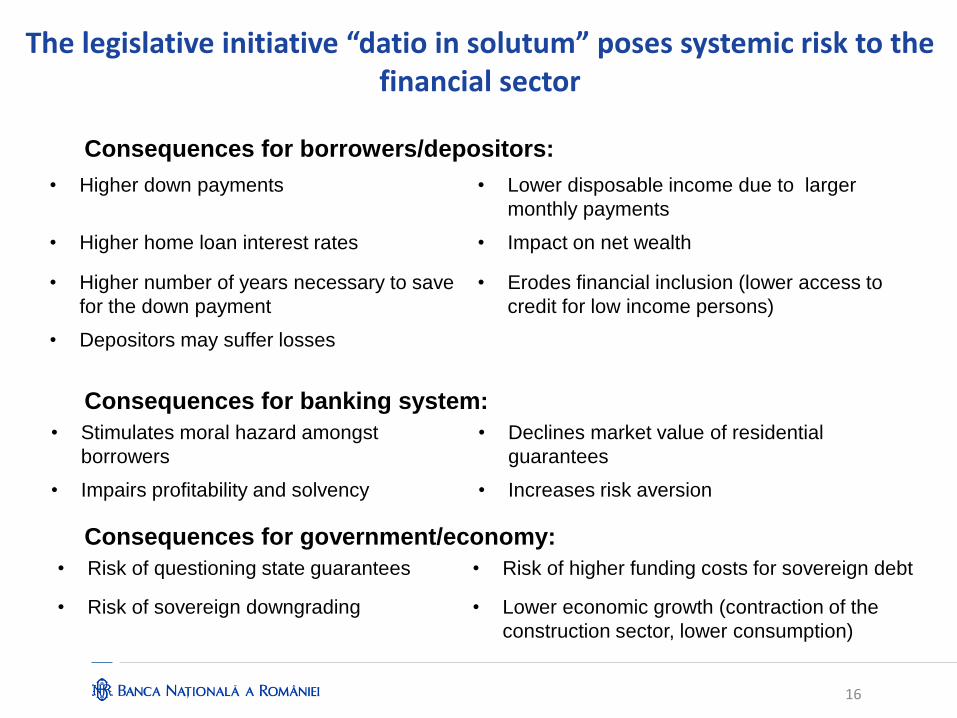

The legislative initiative “datio in solutum” poses systemic risk to the financial sector

Consequences for borrowers/depositors:

Consequences for banking system:

Consequences for government/economy:

• Higher down payments • Lower disposable income due to larger

monthly payments

• Higher home loan interest rates • Impact on net wealth

• Higher number of years necessary to save

for the down payment

• Erodes financial inclusion (lower access to

credit for low income persons)

• Depositors may suffer losses

• Stimulates moral hazard amongst

borrowers

• Declines market value of residential

guarantees

• Impairs profitability and solvency • Increases risk aversion

• Risk of questioning state guarantees • Risk of higher funding costs for sovereign debt

• Risk of sovereign downgrading • Lower economic growth (contraction of the

construction sector, lower consumption)

16

European Commission’s position

• Country Report Romania (26.2.2016) - risks from unwarranted legislative developments - DS: Not transposing Directive 17/2014 (voluntary vs. mandatory) - Major concern on retroactive applicability - Concern on wide applicability - Several provisions of the draft law, if applied without further

amendments, are likely to undermine payment discipline and investor sentiment going forward

- Impacts credit activity - Generate systemic risk - Challenge to financial stability • Communication from the Commission to European Parliament, Council,

ECB and Eurogroup (8.3.2016): - Banking sector is now well capitalized and liquid but several currently discussed legislative initiatives pose a risk to its stability.

17

The legislative initiative “datio in solutum” will deteriorate the access to credit

Number of years necessary to save

for the down payment Increase of monthly payments

Source: NBR

1.3

3.8

7.9

0

1

2

3

4

5

6

7

8

9

Prima Casa, down

payment=15%

Mortgage loan, down

payment=15%

Mortgage loan, down

payment=35%

number of years

679

807

978

1142

0

200

400

600

800

1000

1200

RON EUR RON EUR

Before After

RON

Note: results obtained for 2 person household, average

income, saving ratio=25%, house value=EUR 60,000,

residential price decline=10%

Note: results obtained for average loans, maturity=30

years, interest rate increase=150 b.p., maturity

decline=10 years

Source: NBR

18

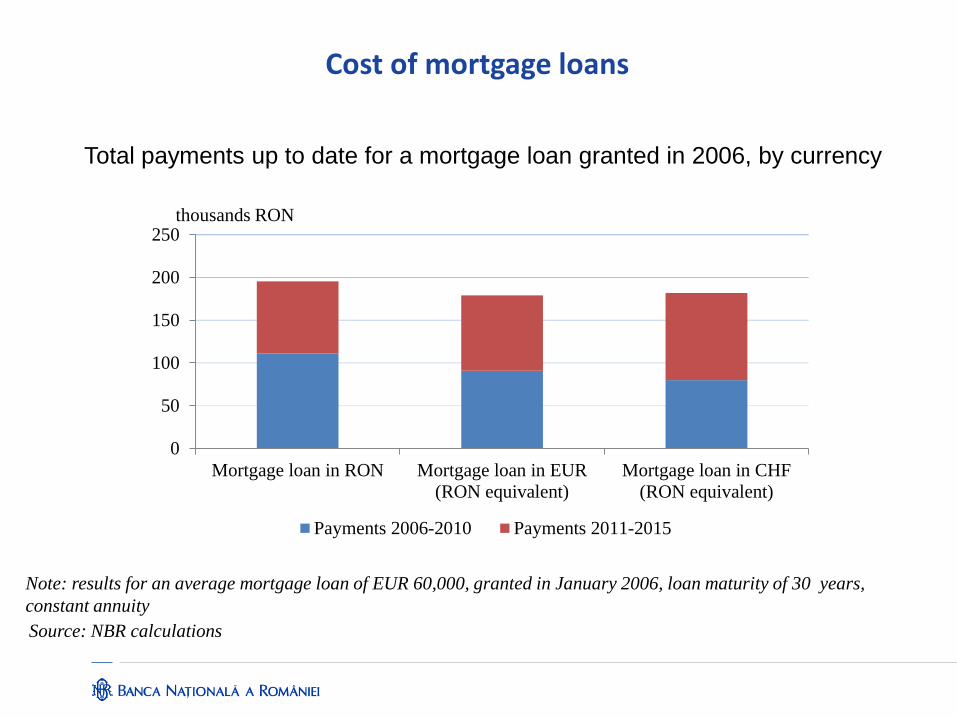

Total payments up to date for a mortgage loan granted in 2006, by currency

Note: results for an average mortgage loan of EUR 60,000, granted in January 2006, loan maturity of 30 years,

constant annuity

Cost of mortgage loans

Source: NBR calculations

0

50

100

150

200

250

Mortgage loan in RON Mortgage loan in EUR

(RON equivalent)

Mortgage loan in CHF

(RON equivalent)

Payments 2006-2010 Payments 2011-2015

thousands RON

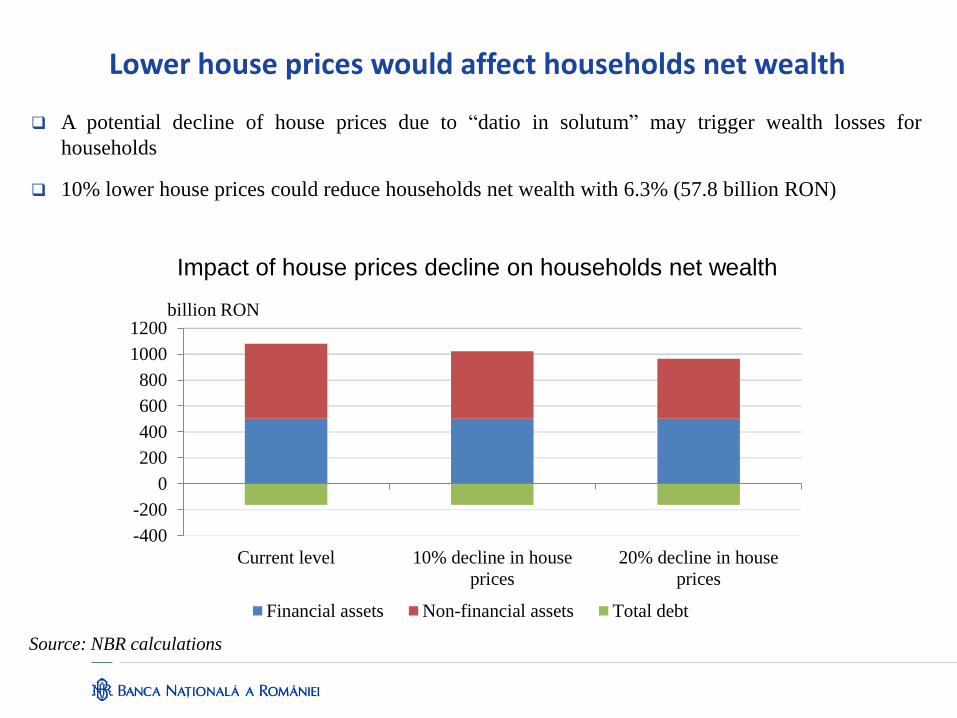

Impact of house prices decline on households net wealth

Lower house prices would affect households net wealth

Source: NBR calculations

-400

-200

0

200

400

600

800

1000

1200

Current level 10% decline in house

prices

20% decline in house

prices

Financial assets Non-financial assets Total debt

billion RON

A potential decline of house prices due to “datio in solutum” may trigger wealth losses for

households

10% lower house prices could reduce households net wealth with 6.3% (57.8 billion RON)

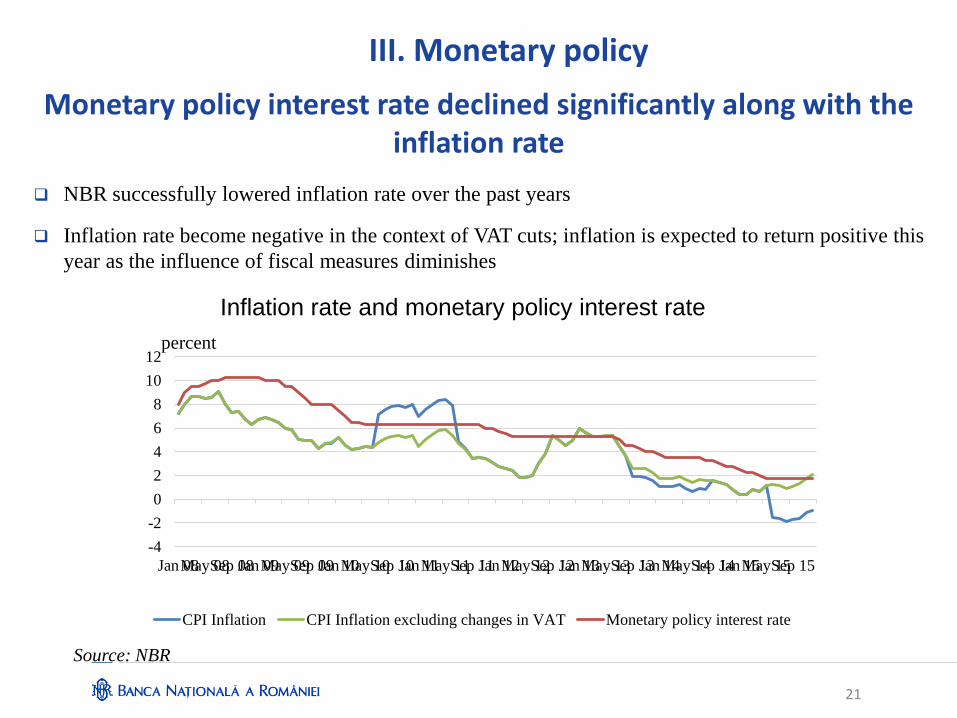

Monetary policy interest rate declined significantly along with the inflation rate

NBR successfully lowered inflation rate over the past years

Inflation rate become negative in the context of VAT cuts; inflation is expected to return positive this

year as the influence of fiscal measures diminishes

Inflation rate and monetary policy interest rate

Source: NBR

21

III. Monetary policy

-4

-2

0

2

4

6

8

10

12

Jan 08May 08Sep 08Jan 09May 09Sep 09Jan 10May 10Sep 10Jan 11May 11Sep 11Jan 12May 12Sep 12Jan 13May 13Sep 13Jan 14May 14Sep 14Jan 15May 15Sep 15

CPI Inflation CPI Inflation excluding changes in VAT Monetary policy interest rate

percent

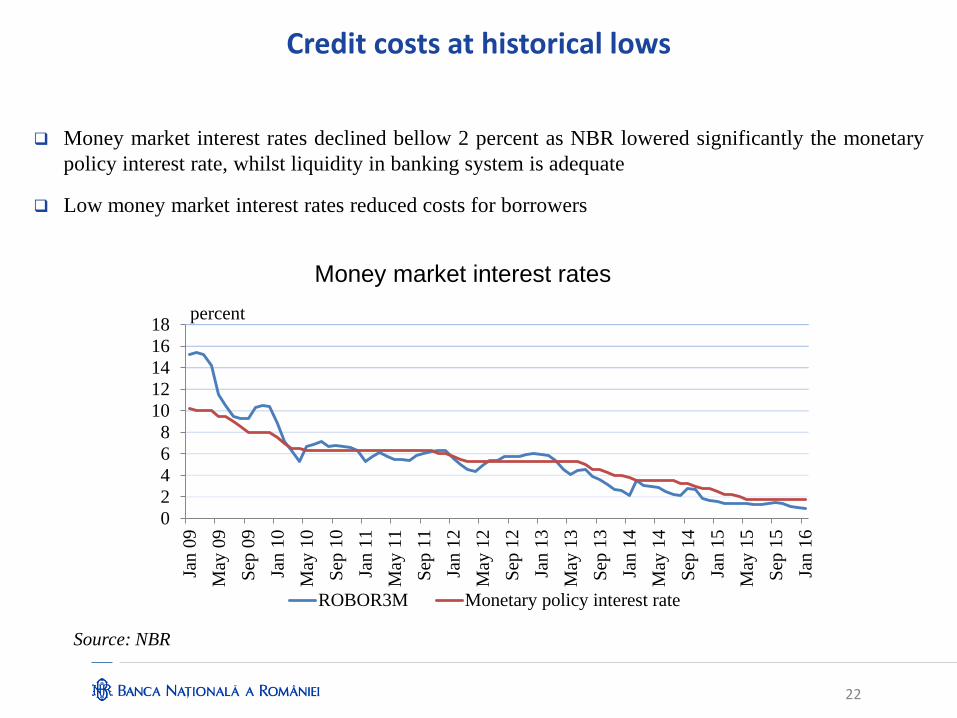

Credit costs at historical lows

Money market interest rates declined bellow 2 percent as NBR lowered significantly the monetary

policy interest rate, whilst liquidity in banking system is adequate

Low money market interest rates reduced costs for borrowers

Money market interest rates

Source: NBR

22

0

2

4

6

8

10

12

14

16

18

Jan

09

May

09

Sep

09

Jan

10

May

10

Sep

10

Jan

11

May

11

Sep

11

Jan

12

May

12

Sep

12

Jan

13

May

13

Sep

13

Jan

14

May

14

Sep

14

Jan

15

May

15

Sep

15

Jan

16

ROBOR3M Monetary policy interest rate

percent

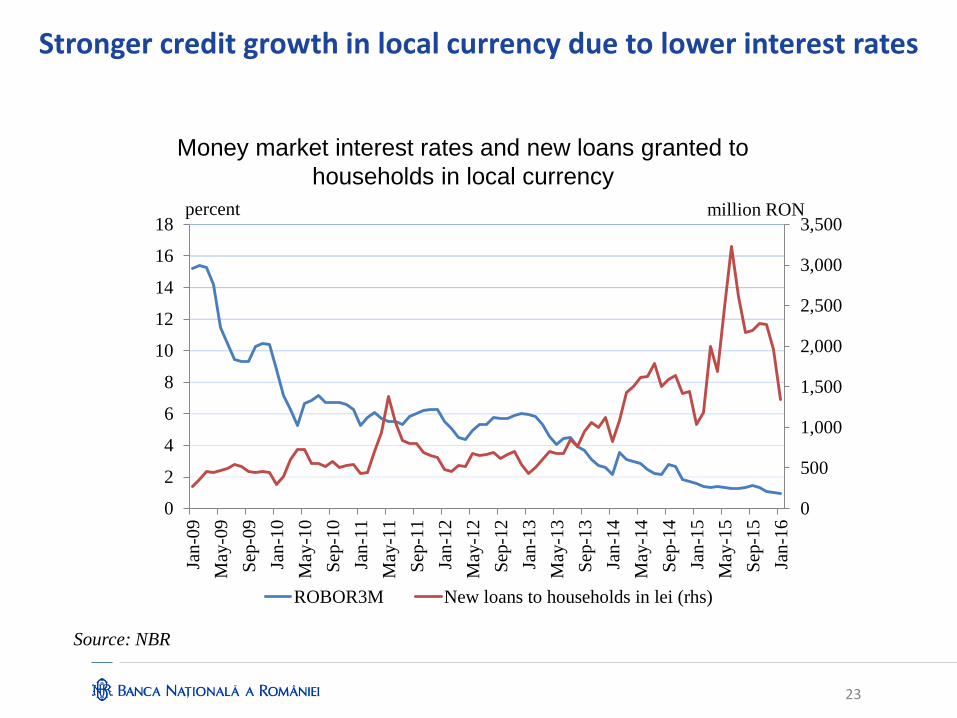

Stronger credit growth in local currency due to lower interest rates

Money market interest rates and new loans granted to

households in local currency

Source: NBR

23

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

2

4

6

8

10

12

14

16

18

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

Jan

-16

ROBOR3M New loans to households in lei (rhs)

percent million RON

24

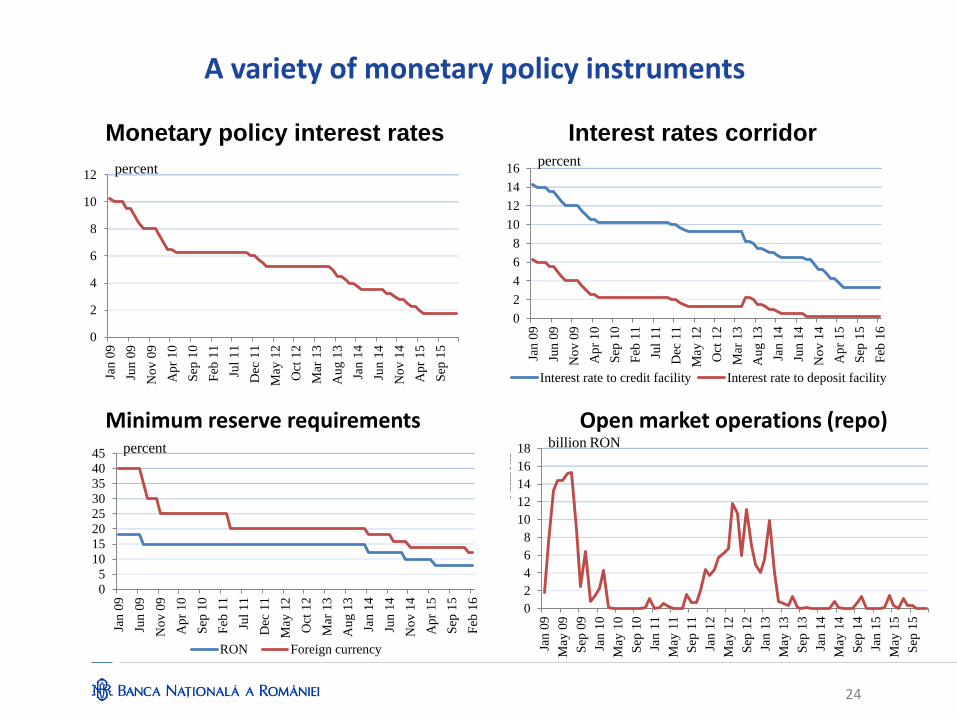

A variety of monetary policy instruments

Monetary policy interest rates

Interest rates corridor

Minimum reserve requirements

Open market operations (repo)

0

2

4

6

8

10

12

Jan

09

Jun

09

No

v 0

9

Ap

r 1

0

Sep

10

Feb

11

Jul

11

Dec

11

May

12

Oct

12

Mar

13

Au

g 1

3

Jan

14

Jun

14

No

v 1

4

Ap

r 1

5

Sep

15

percent

0

2

4

6

8

10

12

14

16

Jan

09

Jun

09

No

v 0

9

Ap

r 1

0

Sep

10

Feb

11

Jul

11

Dec

11

May

12

Oct

12

Mar

13

Au

g 1

3

Jan

14

Jun

14

No

v 1

4

Ap

r 1

5

Sep

15

Feb

16

Interest rate to credit facility Interest rate to deposit facility

percent

0

5

10

15

20

25

30

35

40

45

Jan

09

Jun

09

No

v 0

9

Ap

r 1

0

Sep

10

Feb

11

Jul

11

Dec

11

May

12

Oct

12

Mar

13

Au

g 1

3

Jan

14

Jun

14

No

v 1

4

Ap

r 1

5

Sep

15

Feb

16

RON Foreign currency

percent

0

2

4

6

8

10

12

14

16

18

Jan

09

May

09

Sep

09

Jan

10

May

10

Sep

10

Jan

11

May

11

Sep

11

Jan

12

May

12

Sep

12

Jan

13

May

13

Sep

13

Jan

14

May

14

Sep

14

Jan

15

May

15

Sep

15

Mil

lio

ns

billion RON

25

Challenges ahead

External challenges

• Brexit, refugees crisis and sluggish economic growth in the euro area increase

uncertainty in the EU

• Divergent monetary policy in the United States and the euro area pose risks to

emerging markets

• Low commodity prices: assimetric consequences for companies, households and

commodity producers

Domestic challenges

• Risk of policy reversal by pro-cyclical fiscal measures

• Legislative unpredictability

Thank you