Embed Size (px)

Citation preview

Emission allowance origination and trading: How does it affect ABB and its Group Treasury Operations?

Jonas Lindqvist Linus Lund

Production Economics

Master’s Thesis Department of Management and Engineering

LIU-IEI-TEK-A--09/00537--SE

This page is intentionally left blank.

Emission allowance origination and

trading – How does it affect ABB and its Group Treasury

Operations?

Master’s Thesis carried out at the

Department of Management and Engineering,

Linköping Institute of Technology

and at ABB

by

Jonas Lindqvist and

Linus Lund

LIU‐IEI‐TEK‐A‐‐09/00537‐‐SE

Supervisors

Peter Hultman (IPE)

Pawel Skala (ABB)

This page is intentionally left blank.

Abstract The purpose of the thesis is to determine how ABB’s treasury department (GTO) should respond to an increasing awareness and interest in the carbon credit markets. Emission caps have been introduced on national levels and also for certain industries in Europe as a consequence of the Kyoto Protocol. This allows for trading of certain carbon credits as well as for the creation of new credits. ABB is a company which has many solutions for efficient energy use; solutions that aim to reduce electricity cost and in the prolongation also emissions. The awareness of the carbon market is growing within ABB, but no carbon credit generating projects have been completed and the initiatives are scattered.

The thesis describes the Kyoto Protocol and its implementation within EU, the markets available for trading by companies as well as what instruments and derivatives exist. With the underlying regulations described an empirical study of ABB’s involvement is conducted. The study shows that ABB has few installations with emissions caps and that the potential for generating new credits as a way to increase profit is quite big. However, there have been no carbon generating projects registered up to this point and there are many barriers to overcome before ABB receives any carbon credits.

To ensure a thorough analysis, a model of factors affecting ABB’s carbon credit involvement is formed. The model is based on the available literature on the subjects organizational performance, transfer pricing, project‐ and financial risk and risk management.

GTO’s immediate response should be to set up a pool to which subsidiaries with compliance requirements are to send their carbon credits. The pool will then redistribute the credits so that each subsidiary’s needs are fulfilled and finally settle the net remainder on the open market. A unit independent of GTO, called Group Carbon Operations (GCO) in the thesis, should be formed in the near future with responsibility to actively follow the progress of CDM pilot projects and to facilitate their implementation.

Depending on the outcome of these pilot‐projects ABB can then either, in case of a negative outcome, quickly end the direct CDM involvement and reach closure or, in case of a positive outcome, further develop the GCO department to profit from ABBs involvement in the CDM market. In case of a positive outcome, the GTO should be further involved regarding risk handling and internal pricing.

Sammanfattning Syftet med denna studie är att avgöra hur ABBs treasuryavdelning (GTO) bör reagera på den allt större medvetenheten och potentialen i utsläppsrättsmarknaden. Utsläppstak har introducerats för länder runt om i världen och även för vissa industrier i främst Europa som en konsekvens av Kyoto Protokollet. Detta skapar möjligheter att handla med utgivna utsläppsrätter och derivat på dessa samtidigt som nya utsläppsrätter kan generereras genom utsläppsreducerande projekt. ABB är ett företag vars produktportfölj till stor del utgörs av energieffektiva lösningar vars syfte ofta är att reducera energianvändning och i förlängningen därmed även utsläppen. Medvetenheten om utsläppsrättsmarknaden växer inom ABB, men ännu har inga utsläppsrättsgenererande projekt färdigställts och initativen som är tagna är spridda inom organisationen.

Denna studie beskriver Kyoto Protokollet och dess implikationer, främst inom EU, samt de tillgängliga marknaderna, instrumenten och derivaten. Efter att denna underliggande information inhämtas följer en grundläggande empirisk studie av ABBs involvering i utsläppsrättsmarknaden. Studien visar att ABB har några få installationer med utsläppsregleringar och att potentialen för generering av nya utsläpprätter via utsläppsreducerande projekt är stor. Inga projekt har ännu ej registrerats för utsläppsrättsgenerering och det finns ett flertal barriärer som måste övervinnas innan ABB får nya utsläpprsätter i sin ägo.

För att säkerställa att analysen av frågeställningen blir uttömanade skapas en analysmodell innehållande de faktorer som påverkar ABBs involvering på utsläppsrättsmarknaden. Modellen baseseras på tillgänglig litteratur i ämnena organisation, internprissättning, projekt‐ och finansiell risk samt riskhantering.

GTOs direkta respons bör vara att skapa en utsläppsrättspool, till vilken de installationer med utsläppstak ska överföra sina tilldelade utsläppsrätter. Via poolen kommer sedan utsläppsrätterna distribueras så att alla installationer kan möta utsläppstaken och kvarstoden kan sedan köpas eller säljas på marknaden.

Dessutom bör en av GTO organisatorisk oberoende enhet, kallad Group Carbon Operations (GCO) i uppsatsen, skapas som aktivt ska följa utvecklingen av CDM pilotprojekten och underlätta deras genomförande.

Om pilotprojekten visar att CDM potentialen är låg kan ABB lägga ner GCO och därmed snabbt avsluta CDM involveringen och nå ett, för hela företaget, tydligt avslut. Om potentialen däremot visar sig vara hög bör GCO vidareutvecklas för att ytterligare förbättra ABBs möjlighet att profitera på en CDM involvering. I detta fall bör även GTO vidareutveckla sitt erbjudande till dotterbolagen så att det täcker både en övergripande riskhantering och möjligheten att internprissätta utsläppsrätter.

Table of content 1 INTRODUCTION............................................................................................................................................... 1

1.1 GLOBAL WARMING – THE BACKGROUND OF THE THESIS................................................................................ 1 1.2 ABB – A COMPANY DESCRIPTION.................................................................................................................. 1

1.2.1 ABB Group Treasury Operations............................................................................................................. 2 1.3 PURPOSE........................................................................................................................................................ 2 1.4 THE ROAD TO A CONCLUSION – A METHODOLOGY DISCUSSION ..................................................................... 3

1.4.1 The orientation of the study...................................................................................................................... 4 1.4.2 Study approach......................................................................................................................................... 5 1.4.3 Primary and secondary sources ............................................................................................................... 6 1.4.4 Analysis .................................................................................................................................................... 8 1.4.5 Method criticism....................................................................................................................................... 8

1.5 DELIMITATION .............................................................................................................................................. 9 2 CARBON CREDITS AND EMISSION TRADING....................................................................................... 11

2.1 THE GREENHOUSE EFFECT AND GLOBAL WARMING ..................................................................................... 11 2.2 THE UNFCCC............................................................................................................................................. 11 2.3 THE KYOTO PROTOCOL............................................................................................................................... 12 2.4 KYOTO MECHANISMS AND KYOTO UNITS .................................................................................................... 12

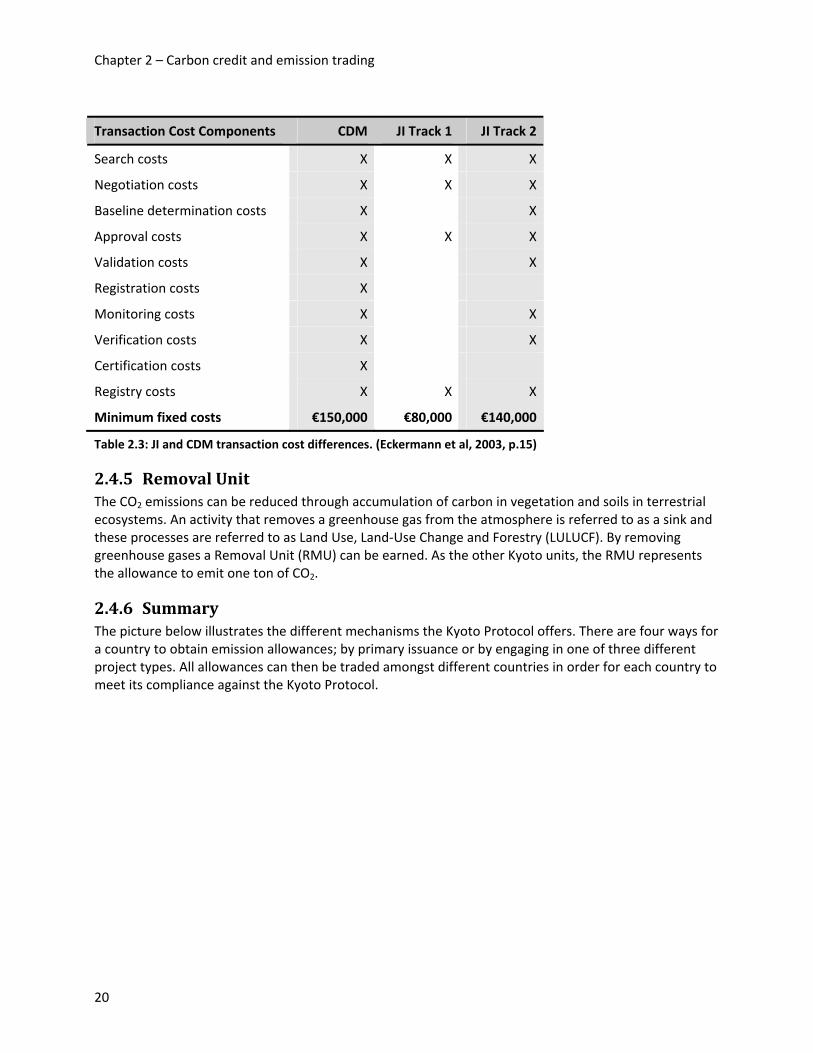

2.4.1 Assigned Amount Unit............................................................................................................................ 13 2.4.2 Emission Trading Mechanism................................................................................................................ 13 2.4.3 Clean Development Mechanism and Certified Emission Reduction ...................................................... 13 2.4.4 Joint Implementation and Emission Reduction Units............................................................................. 18 2.4.5 Removal Unit.......................................................................................................................................... 20 2.4.6 Summary................................................................................................................................................. 20

2.5 THE EUROPEAN UNION EMISSION TRADING SCHEME.................................................................................. 21 2.5.1 Phase I.................................................................................................................................................... 22 2.5.2 Phase II .................................................................................................................................................. 22 2.5.3 Summary................................................................................................................................................. 23

2.6 POST 2012 EMISSION RESTRICTIONS ............................................................................................................ 23 2.6.1 Future of the EU ETS............................................................................................................................. 23

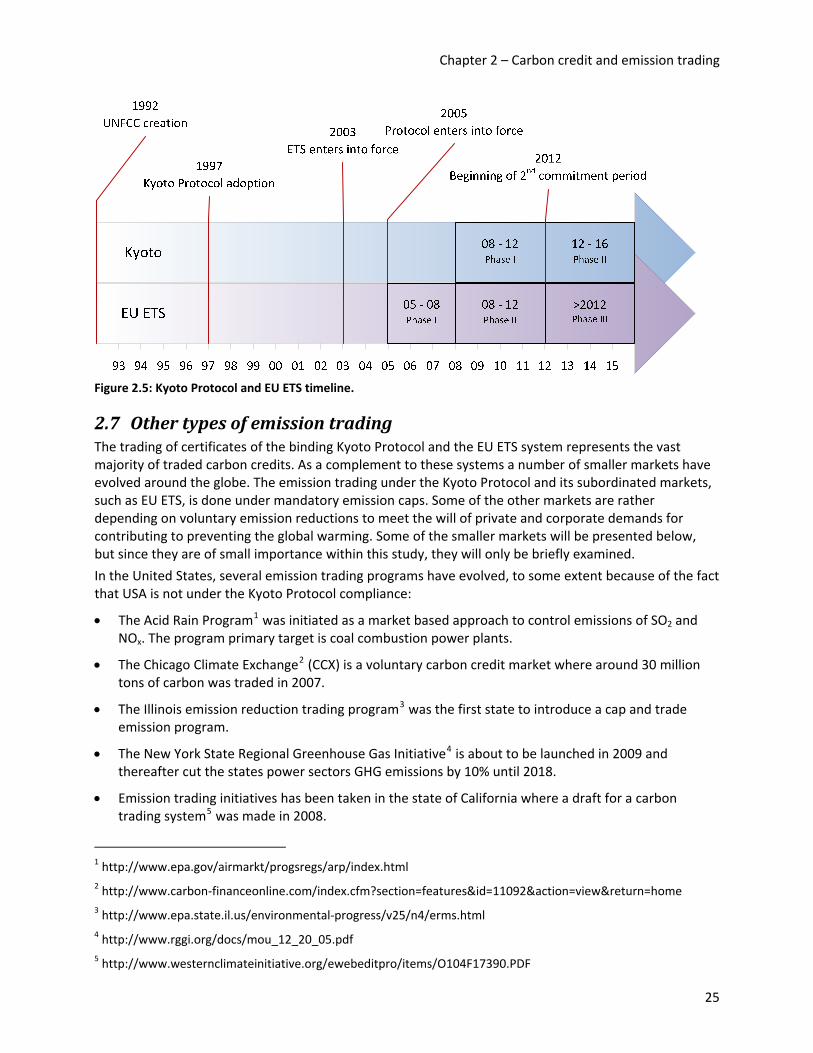

2.7 OTHER TYPES OF EMISSION TRADING........................................................................................................... 25 2.8 THE CARBON CREDIT MARKET..................................................................................................................... 26

2.8.1 Carbon market characteristics............................................................................................................... 28 2.8.2 Practical implications of carbon credit trading..................................................................................... 30 2.8.3 Instruments............................................................................................................................................. 31

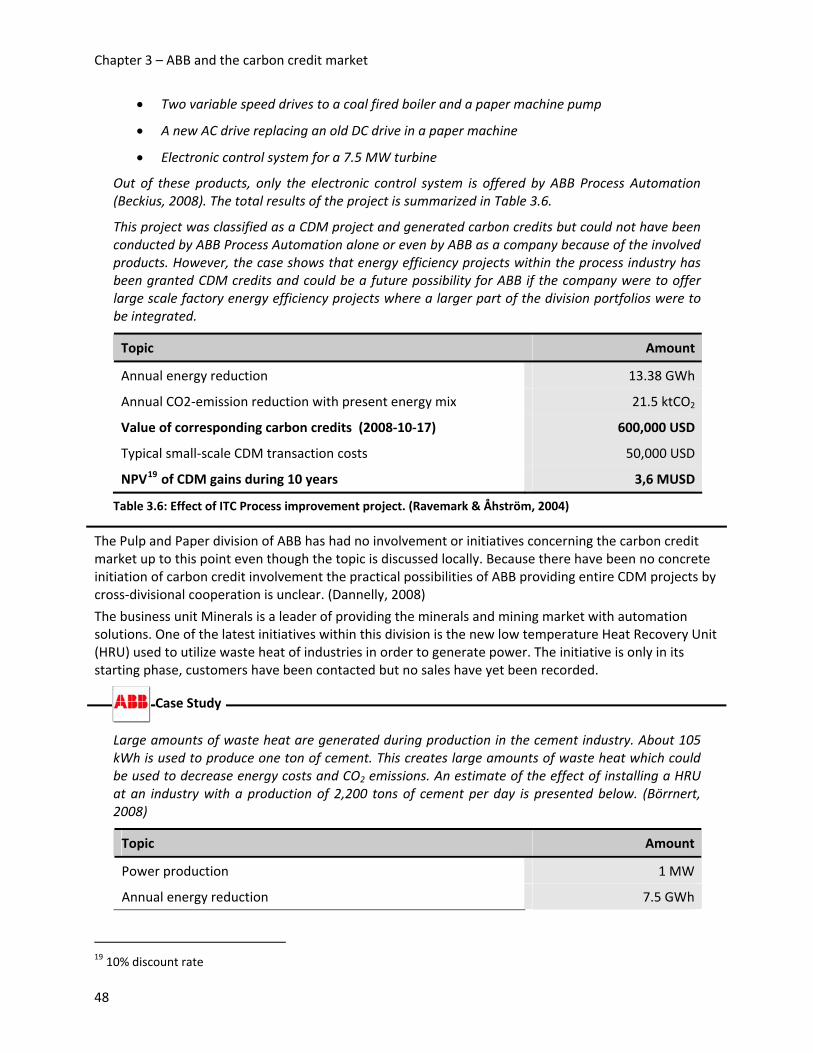

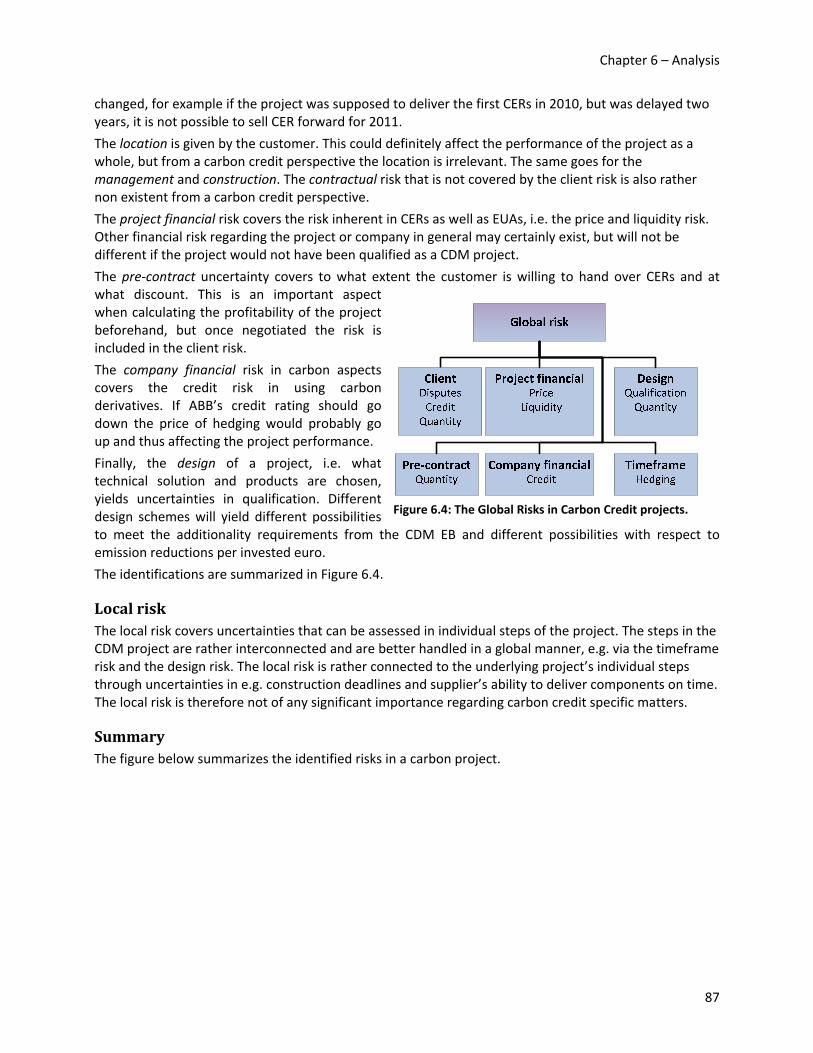

3 ABB AND THE CARBON CREDIT MARKET ............................................................................................ 35 3.1 ABB AND CARBON CREDIT SUPPLY ............................................................................................................. 35

3.1.1 Flexible mechanism projects.................................................................................................................. 36 3.1.2 Emission reduction as a sales argument ................................................................................................ 36 3.1.3 Power Products...................................................................................................................................... 37 3.1.4 Power Systems........................................................................................................................................ 38 3.1.5 Automation Products.............................................................................................................................. 45 3.1.6 Process Automation ............................................................................................................................... 47 3.1.7 Cross-divisional cooperation ................................................................................................................. 49 3.1.8 Carbon credit supply barriers................................................................................................................ 49

3.2 ABB AND CARBON CREDIT DEMAND ........................................................................................................... 51 3.2.1 ABB Figeholm ........................................................................................................................................ 53 3.2.2 ABB Fastighet ........................................................................................................................................ 53 3.2.3 ABB Service............................................................................................................................................ 53 3.2.4 ABB Pucaro............................................................................................................................................ 54

3.3 PREVIOUS INVOLVEMENT IN THE CARBON CREDIT MARKET ........................................................................ 54 3.4 SUMMARY ................................................................................................................................................... 54

i

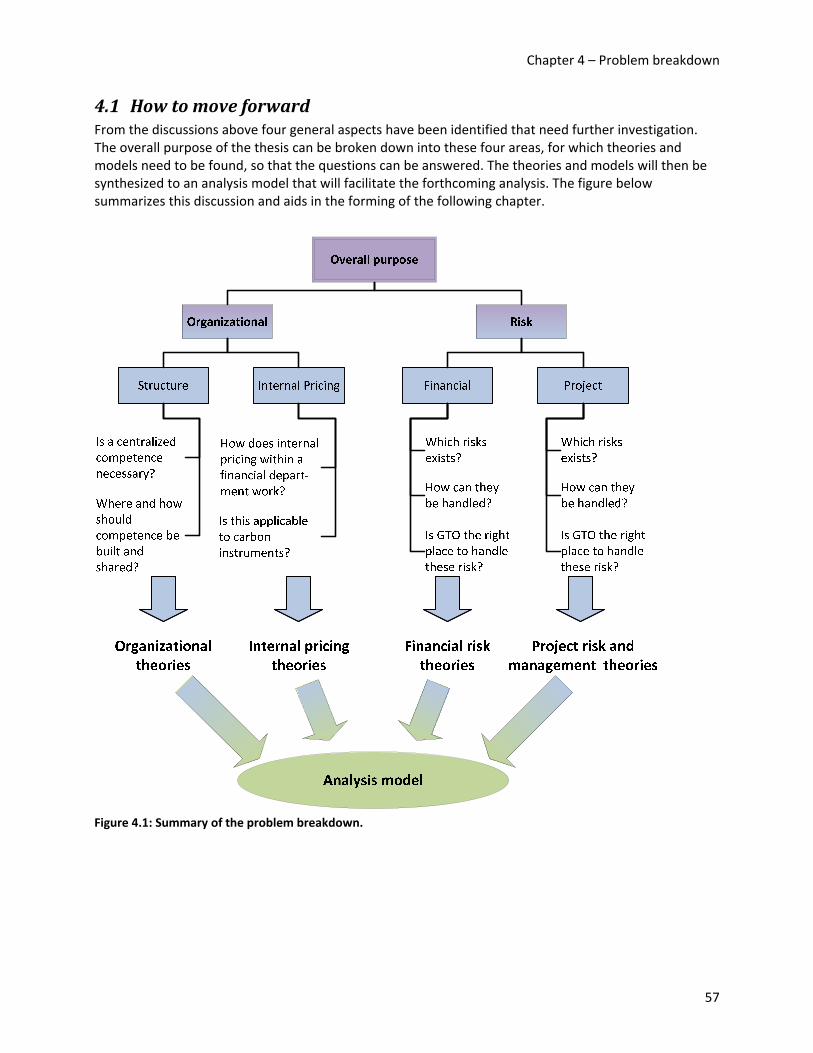

4 PROBLEM BREAKDOWN............................................................................................................................. 56 4.1 HOW TO MOVE FORWARD............................................................................................................................ 57

5 THEORETICAL FRAME OF REFERENCE................................................................................................ 58 5.1 ORGANIZATION ........................................................................................................................................... 58

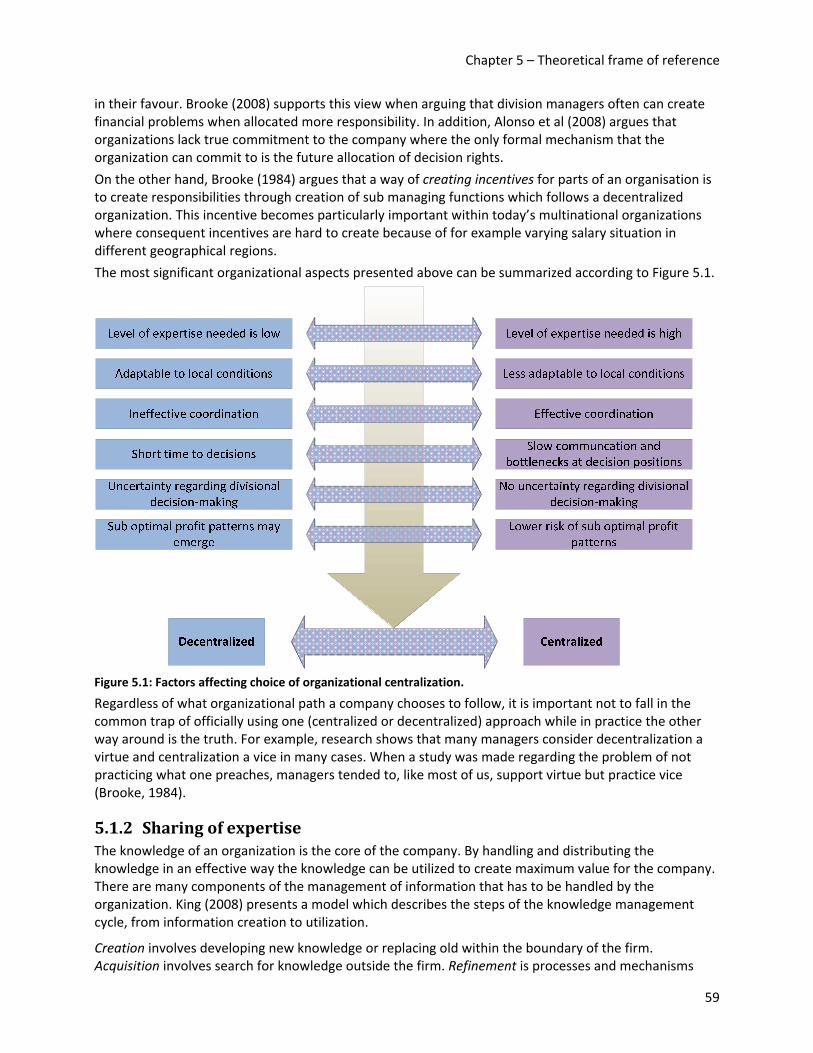

5.1.1 Centralization versus decentralization................................................................................................... 58 5.1.2 Sharing of expertise................................................................................................................................ 59 5.1.3 Outsourcing............................................................................................................................................ 62

5.2 TRANSFER PRICING WITHIN A TREASURY DEPARTMENT............................................................................... 64 5.2.1 Financial services .................................................................................................................................. 65

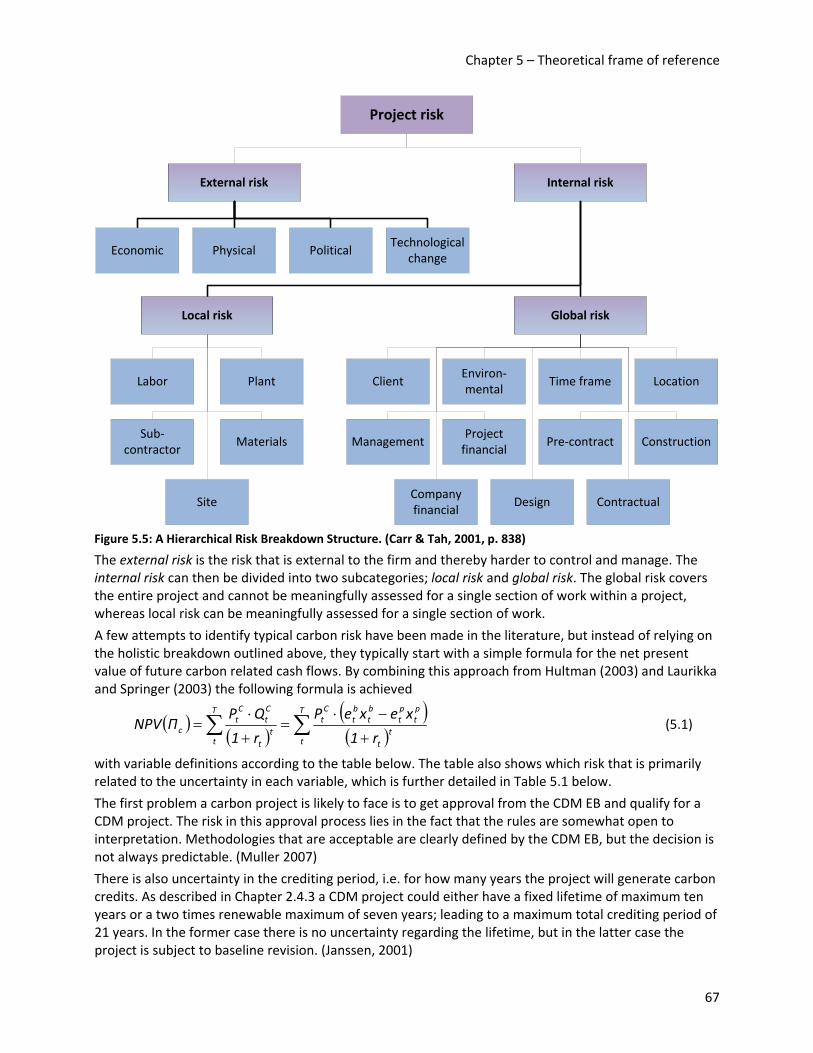

5.3 PROJECT RISK AND RISK MANAGEMENT....................................................................................................... 66 5.3.1 Risk identification................................................................................................................................... 66 5.3.2 Risk quantification and analysis............................................................................................................. 69 5.3.3 Risk response control ............................................................................................................................. 69

5.4 FINANCIAL RISK AND RISK MANAGEMENT ................................................................................................... 70 5.4.1 Financial risk management techniques.................................................................................................. 72 5.4.2 Financial risk management in practice.................................................................................................. 76

5.5 ANALYSIS MODEL........................................................................................................................................ 76 6 ANALYSIS......................................................................................................................................................... 79

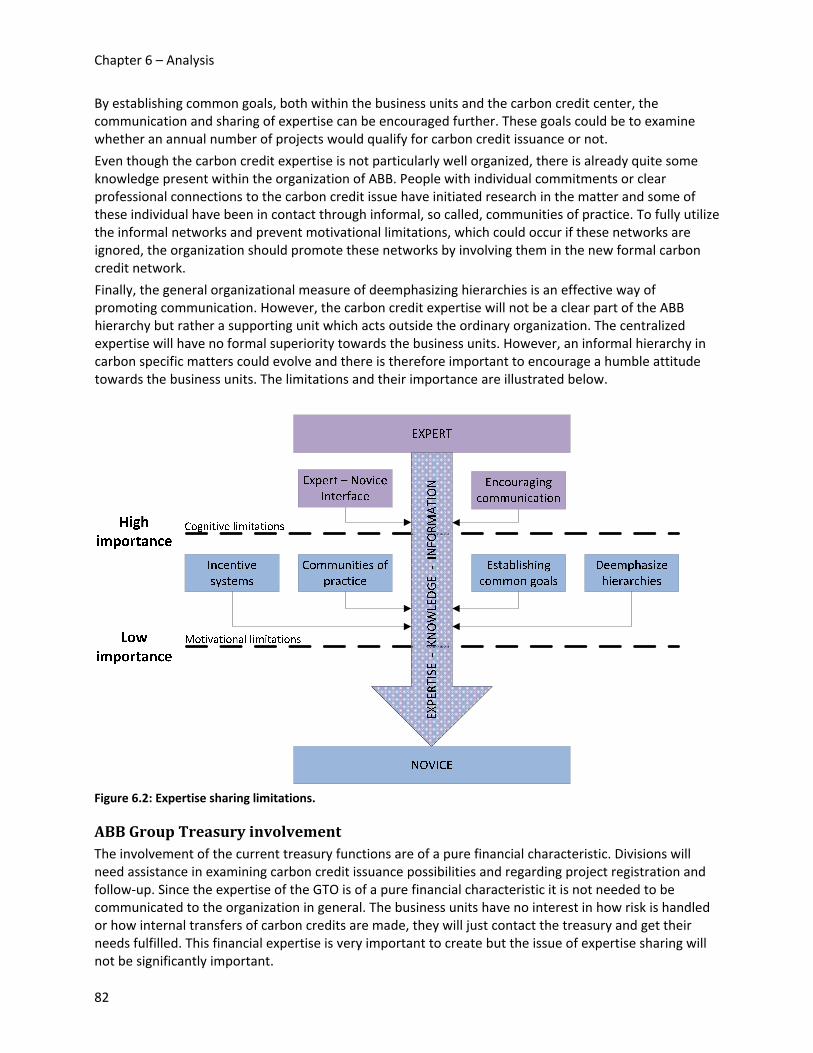

6.1 ORGANIZATIONAL OUTCOME ...................................................................................................................... 79 6.1.1 The centralization – decentralization trade-off ...................................................................................... 79 6.1.2 Efficient sharing of expertise.................................................................................................................. 81 6.1.3 Outsourcing versus In-house.................................................................................................................. 83 6.1.4 Internal pricing ...................................................................................................................................... 84

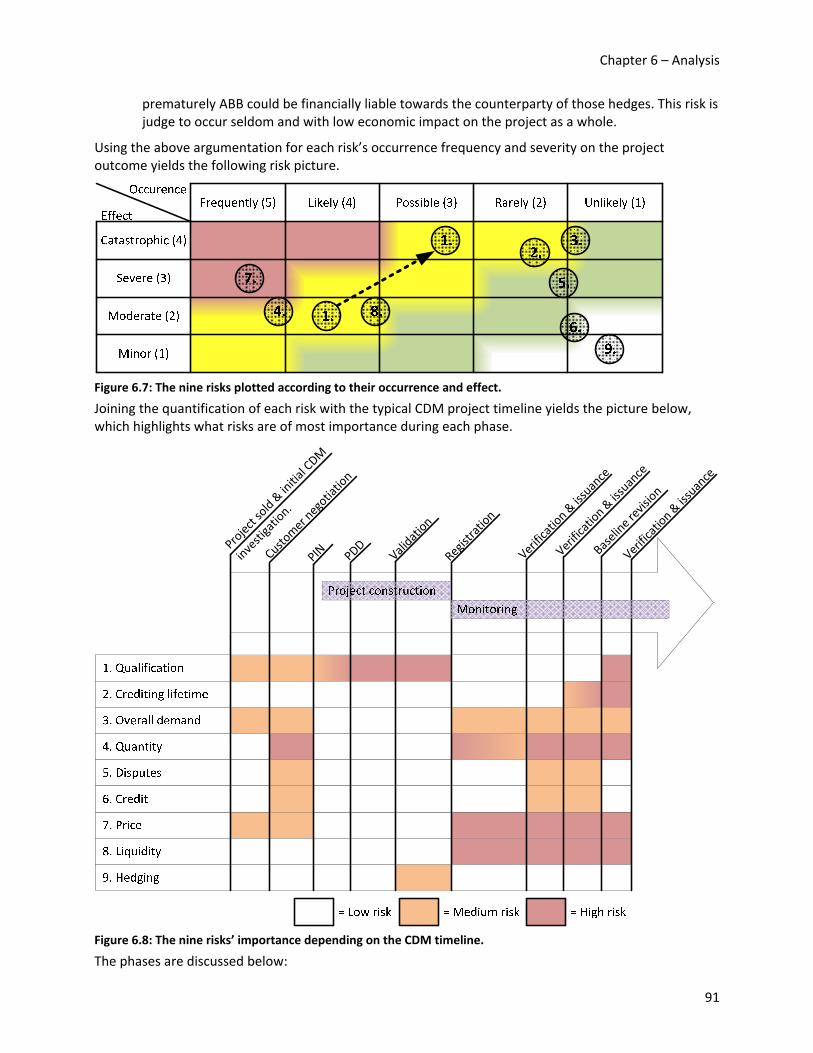

6.2 RISK MANAGEMENT .................................................................................................................................... 85 6.2.1 Risk identification................................................................................................................................... 85 6.2.2 Risk quantification ................................................................................................................................. 88 6.2.3 Risk response control ............................................................................................................................. 92

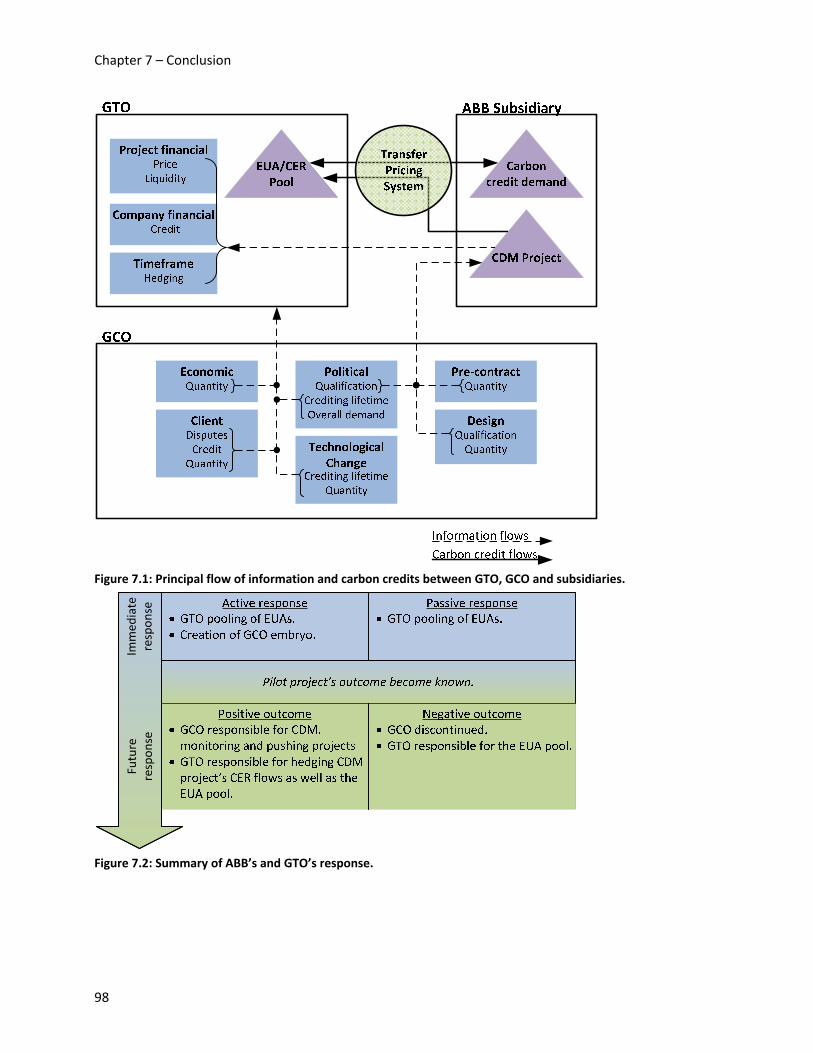

7 CONCLUSION.................................................................................................................................................. 95 7.1 IMMEDIATE RESPONSE................................................................................................................................. 95

7.1.1 Preparation for future CDM involvement .............................................................................................. 95 7.2 FUTURE RESPONSE ...................................................................................................................................... 96

7.2.1 Negative outcome ................................................................................................................................... 96 7.2.2 Positive outcome .................................................................................................................................... 97

REFERENCES........................................................................................................................................................... 99 APPENDIX A– ABB ORGANIZATION SCHEME............................................................................................. 106 APPENDIX B– HOW TO COMPLY..................................................................................................................... 107 APPENDIX C– FACTORS AFFECTING ORGANIZATIONAL PERFORMANCE...................................... 109

ii

List of figures FIGURE 1.1: PROPORTIONS OF REVENUE PER DIVISON. (ABB, 2007) ............................................................ 2 FIGURE 1.2: THE PHASES AND STEPS IN THE THESIS WORK. ......................................................................... 3 FIGURE 1.3: THE INFORMATION FLOW BETWEEN ALL PHASES AND STEPS IN THE THESIS WORK. ... 4 FIGURE 1.4: THE MAIN ORIENTATION OF THE FIRST THREE STEPS IN THE THESIS WORK.................... 5 FIGURE 1.5: THE MAIN ORIENTATION, DATA TYPE AND APPROACH OF THE FIRST THREE STEPS IN

THE THESIS WORK. .......................................................................................................................................... 6 FIGURE 1.6: THE MAIN ORIENTATION, DATA TYPE, APPROACH AND SOURCES OF THE FIRST THREE

STEPS IN THE THESIS WORK.......................................................................................................................... 6 FIGURE 1.7: THE DIFFERENCES BETWEEN THE ANALYTICAL APPROACHES. (HÖRTE, 1999, P.8) ......... 8 FIGURE 1.8: ALL METHODOLOGICAL CHOICES OF ALL STEPS AND PHASES IN THE THESIS WORK. .. 8 FIGURE 2.1: SCHEMATIC DESCRIPTION OF ADDITIONALITY DETERMINATION. (UNFCC, 2008E)....... 14 FIGURE 2.2: CDM TRANSACTION COSTS. (HODES, 2007, P.10)....................................................................... 18 FIGURE 2.3: THE KYOTO PROTOCOL’S MECHANISMS AND EMISSION ALLOWANCE UNITS. .............. 21 FIGURE 2.4: THE EU ETS’ MECHANISMS AND EMISSION ALLOWANCE UNITS. ....................................... 23 FIGURE 2.5: KYOTO PROTOCOL AND EU ETS TIMELINE................................................................................ 25 FIGURE 2.6: THE MECHANISMS AND ALLOWANCES AVAILABLE FOR THE OTHER MARKETS........... 26 FIGURE 2.7: SCHEMATIC OVERVIEW OF THE CARBON CREDIT MARKET................................................. 27 FIGURE 2.8: CDM MARKET DEVELOPMENT IN MTCO2E (WORLD BANK 2008, P.20) ................................ 29 FIGURE 2.9: LOCATION OF CDM PROJECTS, AS SHARE OF VOLUME SUPPLIED IN 2007. (WORLD

BANK, 2008, P. 27) ............................................................................................................................................ 29 FIGURE 2.10: THE CURRENT REGISTRY STRUCTURE AS OF SEPTEMBER 2008. (UNFCCC, 2008B) ....... 30 FIGURE 2.11: THE REGISTRY STRUCTURE AFTER THE CONNECTION OF THE CITL AND THE ITL.

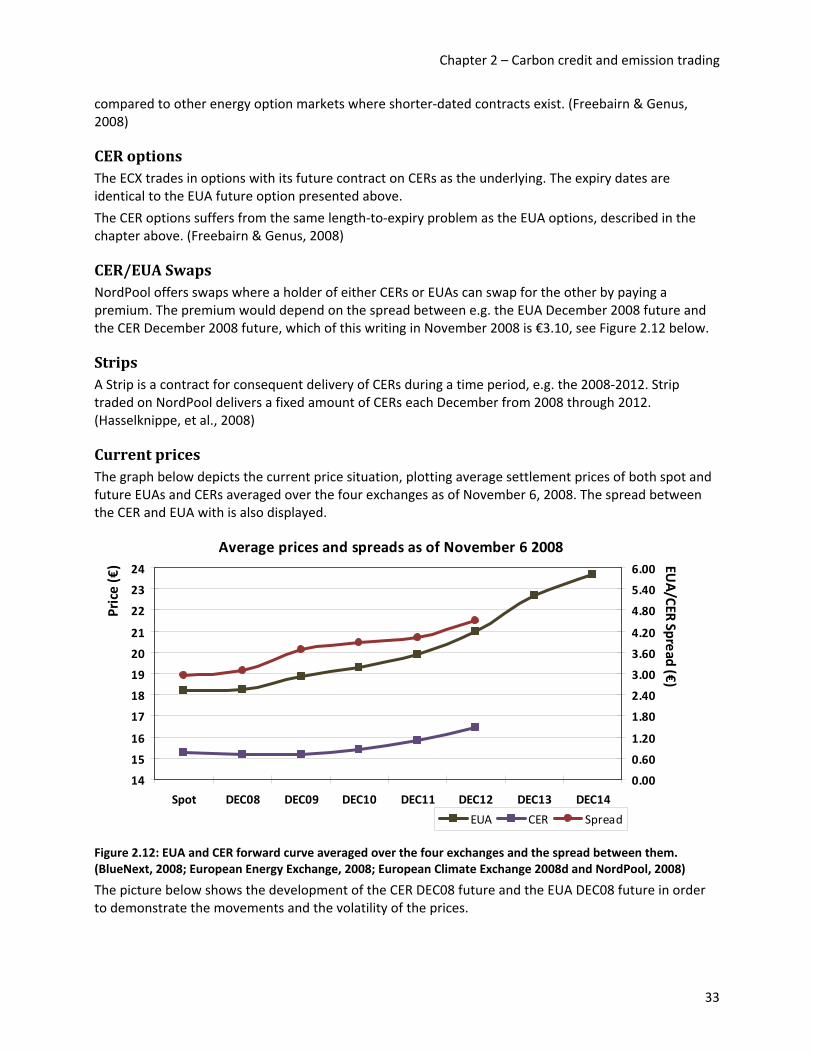

(UNFCCC, 2008D) ............................................................................................................................................. 31 FIGURE 2.12: EUA AND CER FORWARD CURVE AVERAGED OVER THE FOUR EXCHANGES AND THE

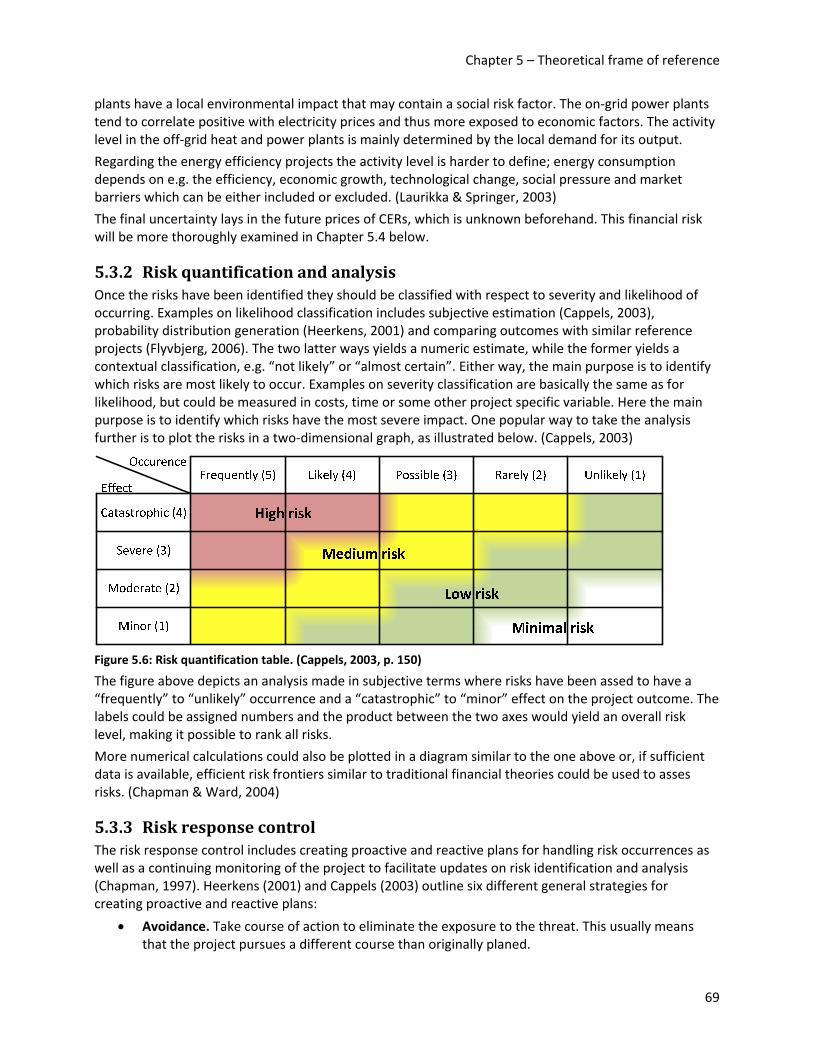

SPREAD BETWEEN THEM. (BLUENEXT, 2008; EUROPEAN ENERGY EXCHANGE, 2008; EUROPEAN CLIMATE EXCHANGE 2008D AND NORDPOOL, 2008)....................................................... 33

FIGURE 2.13: HISTORICAL PRICES OF EUA AND CER FUTURES WITH DELIVERY IN DECEMBER 2008. (JPMORGAN, 2008B, P. 1, MODIFIED)........................................................................................................... 34

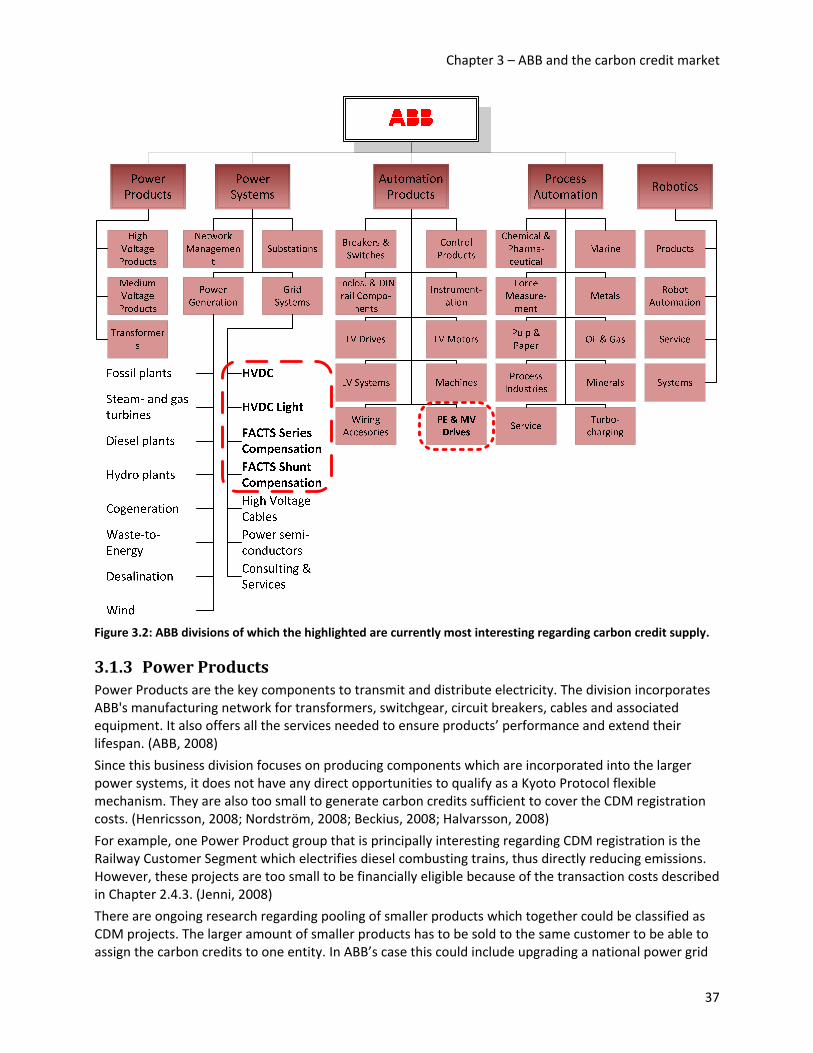

FIGURE 3.1: ABB GROUP FUNCTIONS. ................................................................................................................ 35 FIGURE 3.2: ABB DIVISIONS OF WHICH THE HIGHLIGHTED ARE CURRENTLY MOST INTERESTING

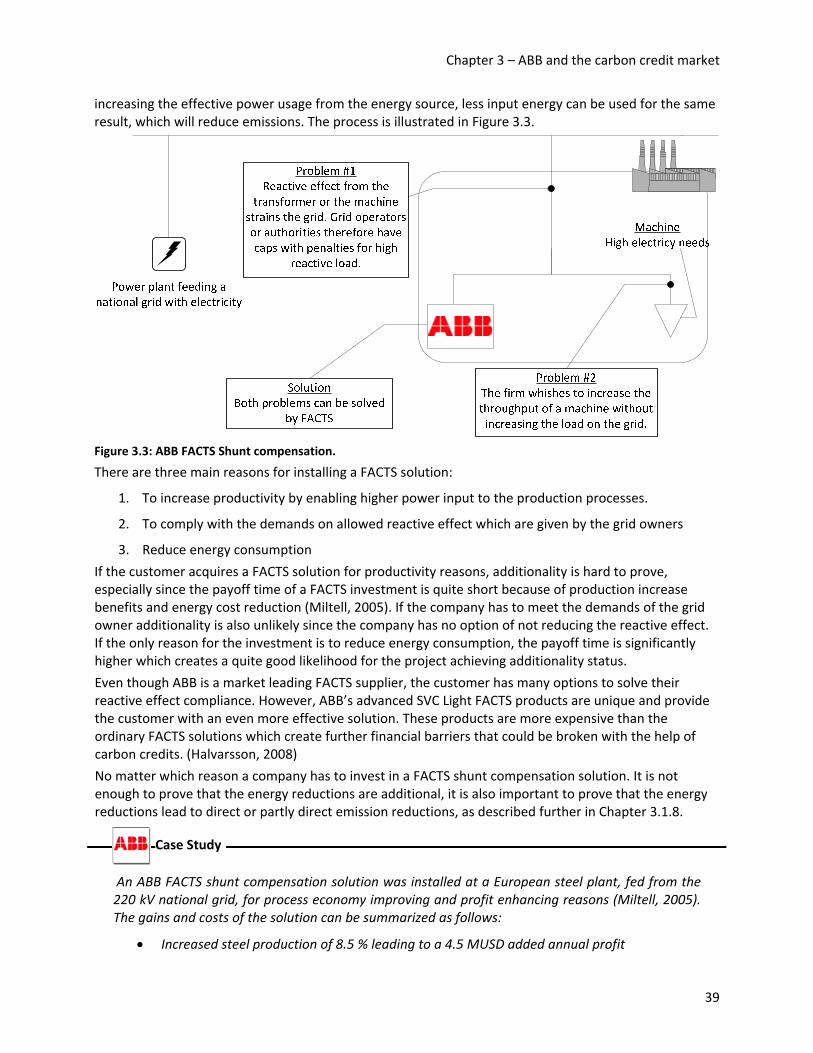

REGARDING CARBON CREDIT SUPPLY..................................................................................................... 37 FIGURE 3.3: ABB FACTS SHUNT COMPENSATION. .......................................................................................... 39 FIGURE 3.4: POSSIBLE PROFIT INCREASES DUE TO INSTALLATION OF A FACTS SHUNT

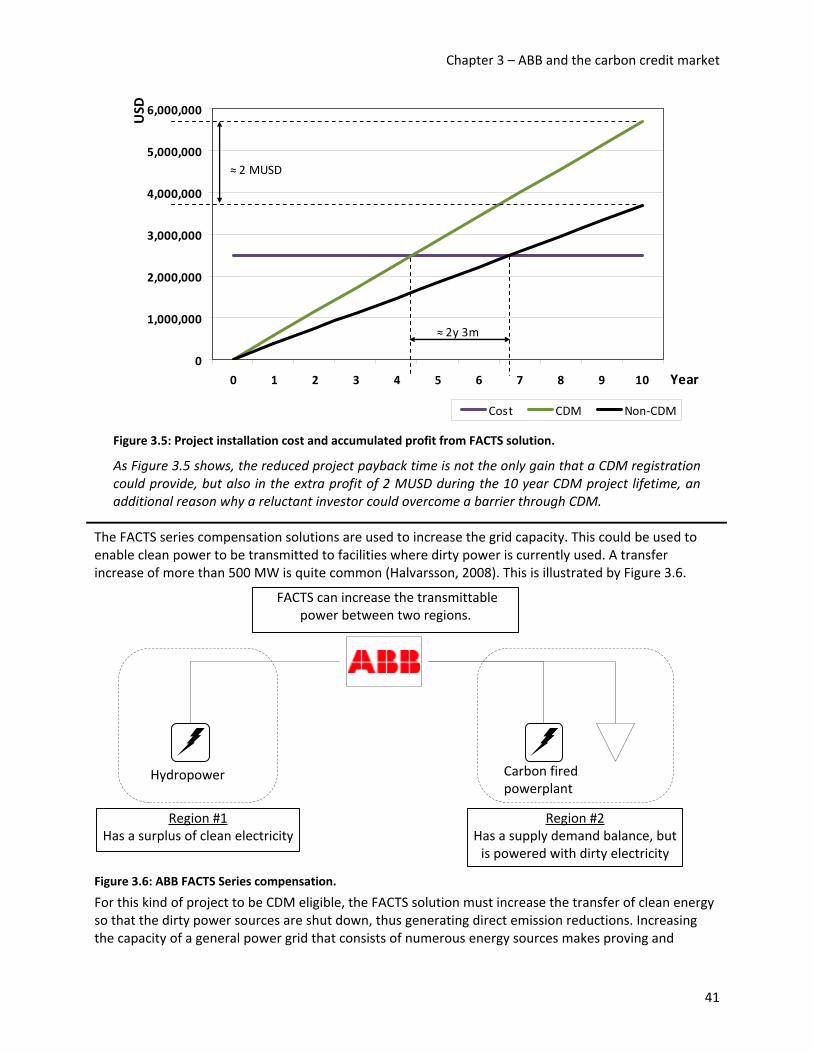

COMPENSATION SOLUTION......................................................................................................................... 40 FIGURE 3.5: PROJECT INSTALLATION COST AND ACCUMULATED PROFIT FROM FACTS SOLUTION.

............................................................................................................................................................................. 41 FIGURE 3.6: ABB FACTS SERIES COMPENSATION. .......................................................................................... 41 FIGURE 3.7: TRANSMISSION LOSSES FOR VARIOUS TYPES OF TRANSMISSIONS. (MACHAREY ET AL,

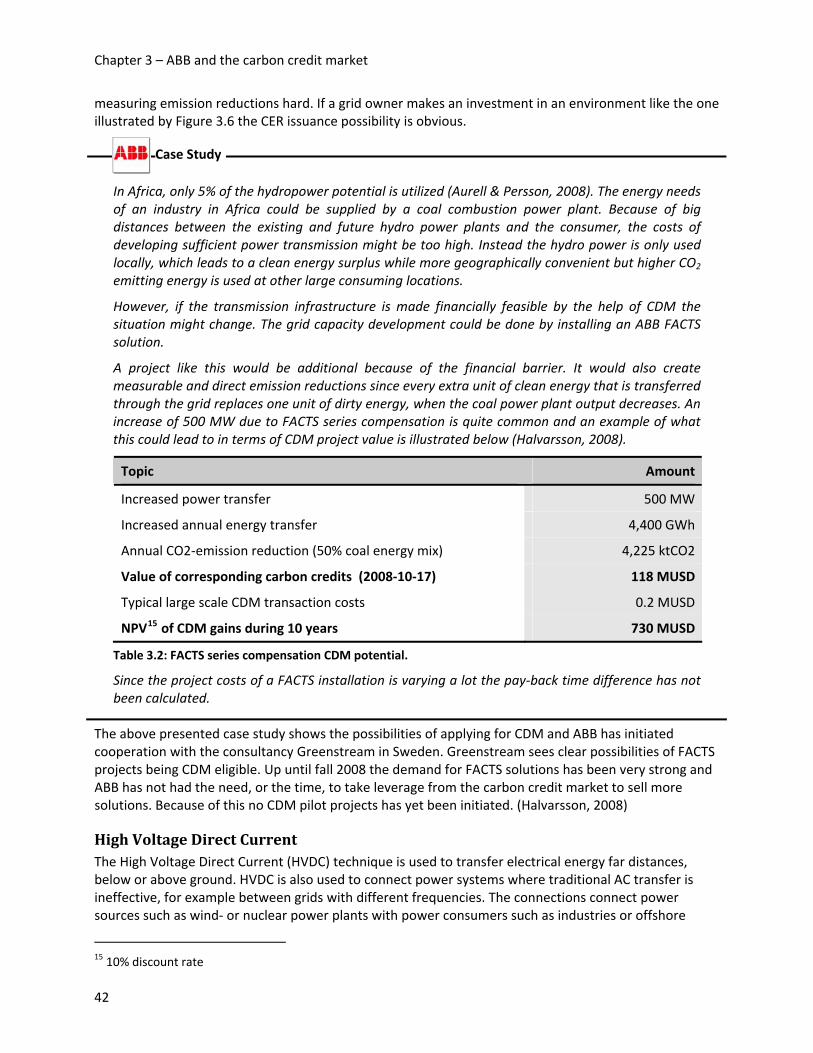

2007) ................................................................................................................................................................... 43 FIGURE 4.1: SUMMARY OF THE PROBLEM BREAKDOWN. ............................................................................ 57 FIGURE 5.1: FACTORS AFFECTING CHOICE OF ORGANIZATIONAL CENTRALIZATION......................... 59 FIGURE 5.2: THE KNOWLEDGE MANAGEMENT CYCLE (KING, 2008).......................................................... 60 FIGURE 5.3: OVERCOMING EXPERTISE SHARING LIMITATIONS. ................................................................ 62 FIGURE 5.4: FACTORS AFFECTING THE OUTSOURCING DECISION AND ITS OUTCOME........................ 64 FIGURE 5.5: A HIERARCHICAL RISK BREAKDOWN STRUCTURE. (CARR & TAH, 2001, P. 838) .............. 67 FIGURE 5.6: RISK QUANTIFICATION TABLE. (CAPPELS, 2003, P. 150).......................................................... 69 FIGURE 5.7: ILLUSTRATION OF THE VAR MEASURE. ..................................................................................... 73 FIGURE 5.8: PAYOFFS FROM FORWARD AND FUTURES CONTRACT, DEPENDENT ON DELIVERY

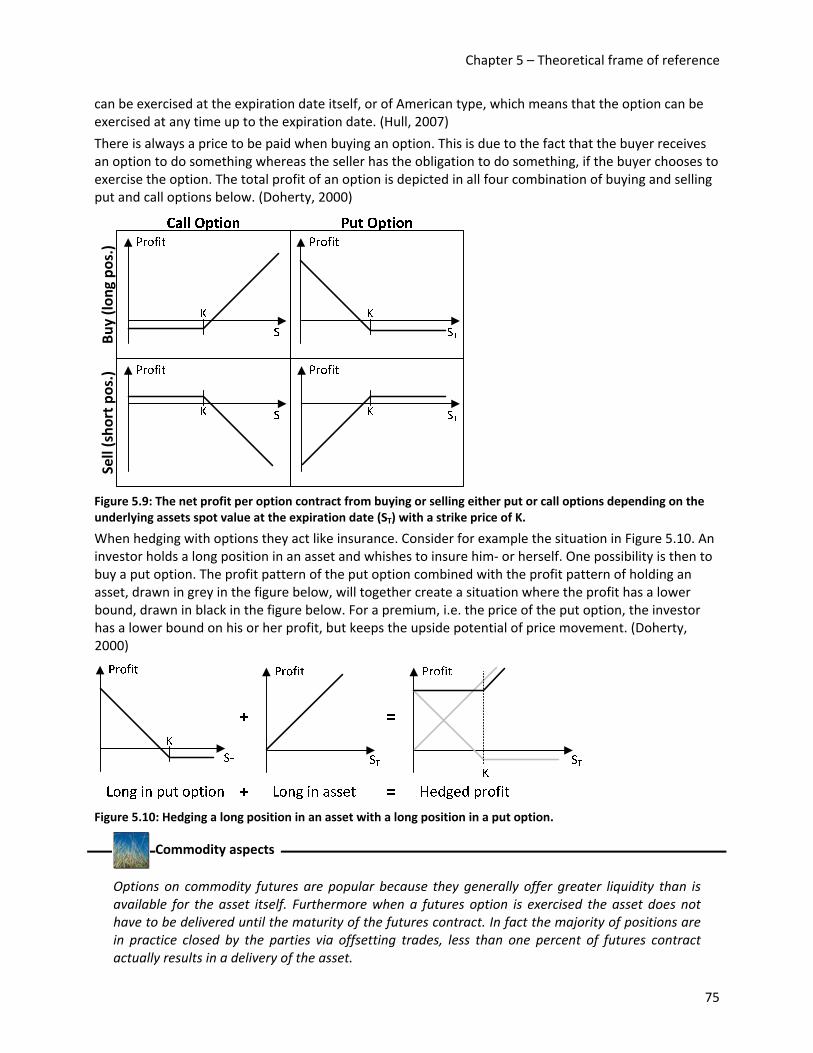

PRICE, K, AND SPOT PRICE AT TIME OF DELIVERY, ST. ......................................................................... 73 FIGURE 5.9: THE NET PROFIT PER OPTION CONTRACT FROM BUYING OR SELLING EITHER PUT OR

CALL OPTIONS DEPENDING ON THE UNDERLYING ASSETS SPOT VALUE AT THE EXPIRATION DATE (ST) WITH A STRIKE PRICE OF K. ..................................................................................................... 75

FIGURE 5.10: HEDGING A LONG POSITION IN AN ASSET WITH A LONG POSITION IN A PUT OPTION.............................................................................................................................................................................. 75

iii

FIGURE 5.11: THE ANALYSIS MODEL.................................................................................................................. 77 FIGURE 5.12: THE FIRST PART OF THE MODEL................................................................................................. 77 FIGURE 5.13: THE SECOND PART OF THE MODEL. .......................................................................................... 78 FIGURE 6.1: ORGANIZATIONAL ASPECTS, WHICH IMPORTANCE IS ILLUSTRATED BY THE GREY

ARROWS............................................................................................................................................................ 80 FIGURE 6.2: EXPERTISE SHARING LIMITATIONS............................................................................................. 82 FIGURE 6.3: THE EXTERNAL RISKS IN CARBON CREDIT PROJECTS. .......................................................... 86 FIGURE 6.4: THE GLOBAL RISKS IN CARBON CREDIT PROJECTS. ............................................................... 87 FIGURE 6.5: RISKS IN CARBON CREDIT PROJECTS.......................................................................................... 88 FIGURE 6.6: A TYPICAL CDM PROJECT TIMELINE........................................................................................... 88 FIGURE 6.7: THE NINE RISKS PLOTTED ACCORDING TO THEIR OCCURRENCE AND EFFECT.............. 91 FIGURE 6.8: THE NINE RISKS’ IMPORTANCE DEPENDING ON THE CDM TIMELINE................................ 91 FIGURE 7.1: PRINCIPAL FLOW OF INFORMATION AND CARBON CREDITS BETWEEN GTO, GCO AND

SUBSIDIARIES.................................................................................................................................................. 98 FIGURE 7.2: SUMMARY OF ABB’S AND GTO’S RESPONSE............................................................................. 98

iv

List of tables TABLE 2.1: CDM REGISTRATION TRANSACTION COSTS. (PIN, 2005) .......................................................... 17 TABLE 2.2: PROPOSED CDM REGISTRATION FEES. (PIN, 2005) ..................................................................... 17 TABLE 2.3: JI AND CDM TRANSACTION COST DIFFERENCES. (ECKERMANN ET AL, 2003, P.15).......... 20 TABLE 2.4: ANNUAL VOLUMES AND VALUES OF TRANSACTIONS ON THE MAIN ALLOWANCE

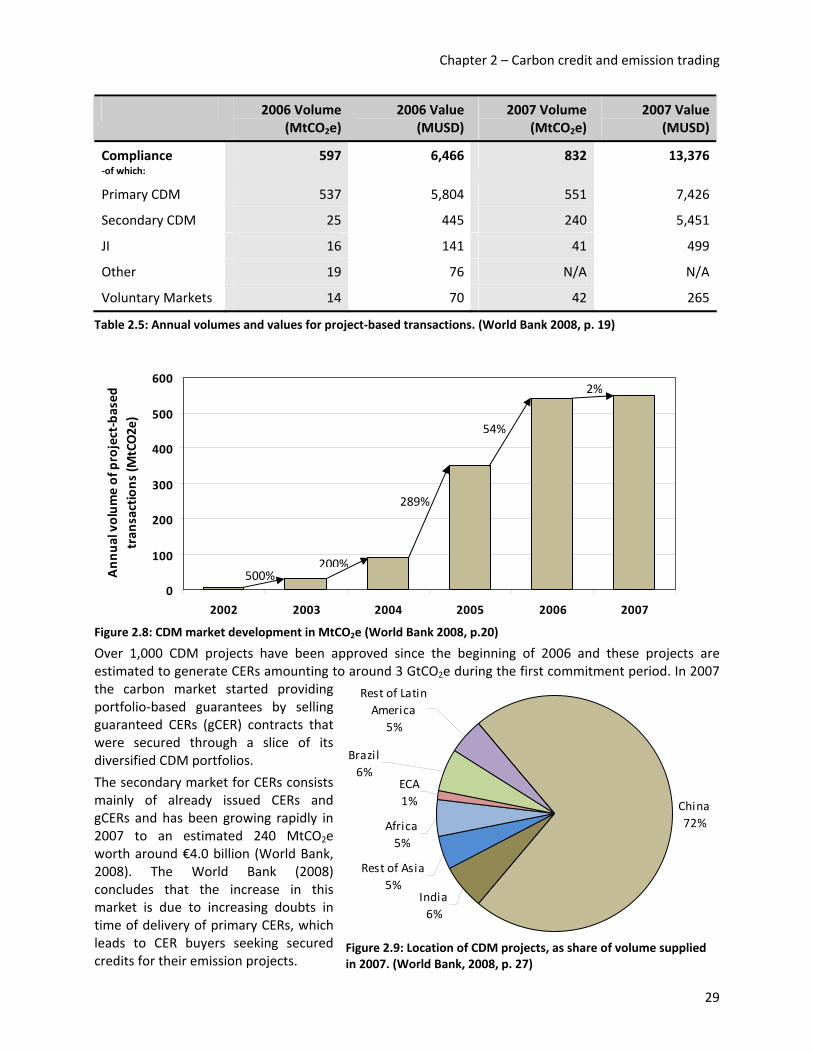

MARKETS. (WORLD BANK, 2008, P. 7) ........................................................................................................ 28 TABLE 2.5: ANNUAL VOLUMES AND VALUES FOR PROJECT-BASED TRANSACTIONS. (WORLD BANK

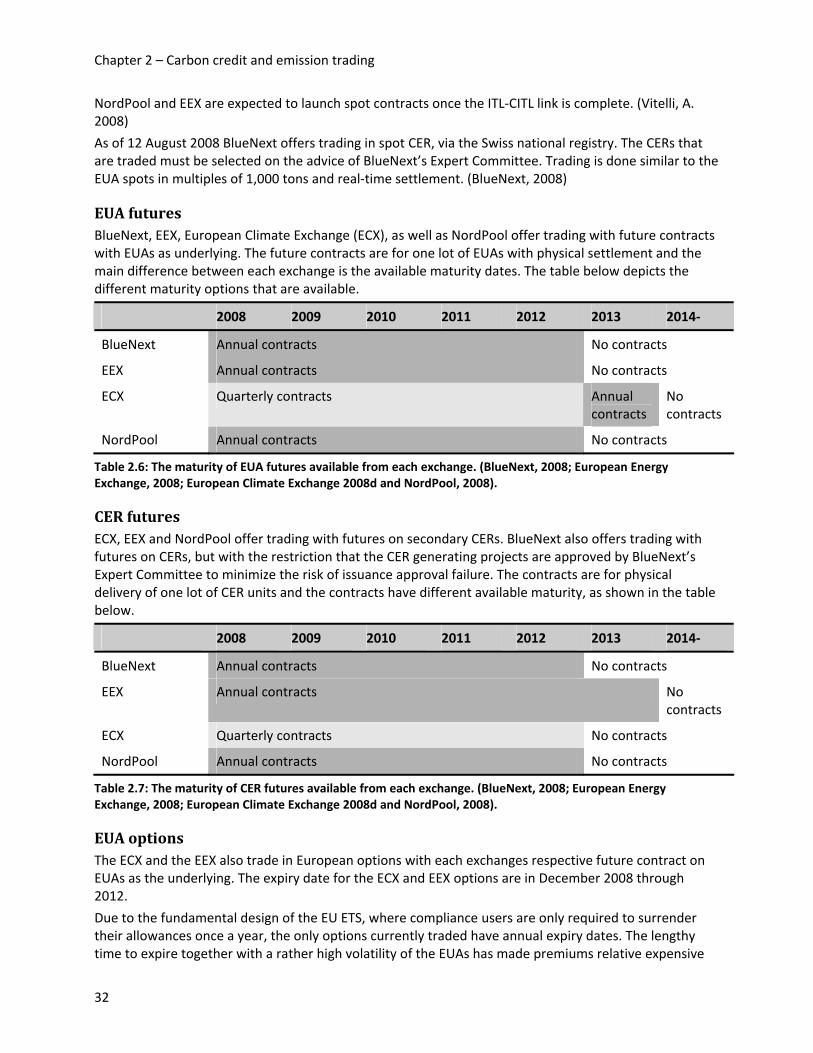

2008, P. 19) ......................................................................................................................................................... 29 TABLE 2.6: THE MATURITY OF EUA FUTURES AVAILABLE FROM EACH EXCHANGE. (BLUENEXT,

2008; EUROPEAN ENERGY EXCHANGE, 2008; EUROPEAN CLIMATE EXCHANGE 2008D AND NORDPOOL, 2008)............................................................................................................................................ 32

TABLE 2.7: THE MATURITY OF CER FUTURES AVAILABLE FROM EACH EXCHANGE. (BLUENEXT, 2008; EUROPEAN ENERGY EXCHANGE, 2008; EUROPEAN CLIMATE EXCHANGE 2008D AND NORDPOOL, 2008)............................................................................................................................................ 32

TABLE 3.1: FACTS SHUNT COMPENSATION CDM POTENTIAL. .................................................................... 40 TABLE 3.2: FACTS SERIES COMPENSATION CDM POTENTIAL. .................................................................... 42 TABLE 3.3: HVDC LINK CDM POTENTIAL. ......................................................................................................... 44 TABLE 3.4: EFFECT OF VALHALLA HVDC PROJECT........................................................................................ 45 TABLE 3.5: MVD PROJECT EXAMPLES. (BACH & WIKSTRÖM, 2006) ........................................................... 46 TABLE 3.6: EFFECT OF ITC PROCESS IMPROVEMENT PROJECT. (RAVEMARK & ÅHSTRÖM, 2004) ..... 48 TABLE 3.7: EFFECT OF A HEAT RECOVERY UNIT INSTALLED AT A CEMENT PRODUCTION PLANT.

(BÖRRNERT, 2008)........................................................................................................................................... 49 TABLE 3.8: ABB CARBON CREDIT DEMAND DURING EU ETS PHASE I. (RÅDSTEDT, 2008;

JOHANSSON, 2008; RABE, 2008; MECKES, 2008)........................................................................................ 52 TABLE 3.9: ABB CARBON CREDIT DEMAND DURING EU ETS PHASE II. (RÅDSTEDT, 2008;

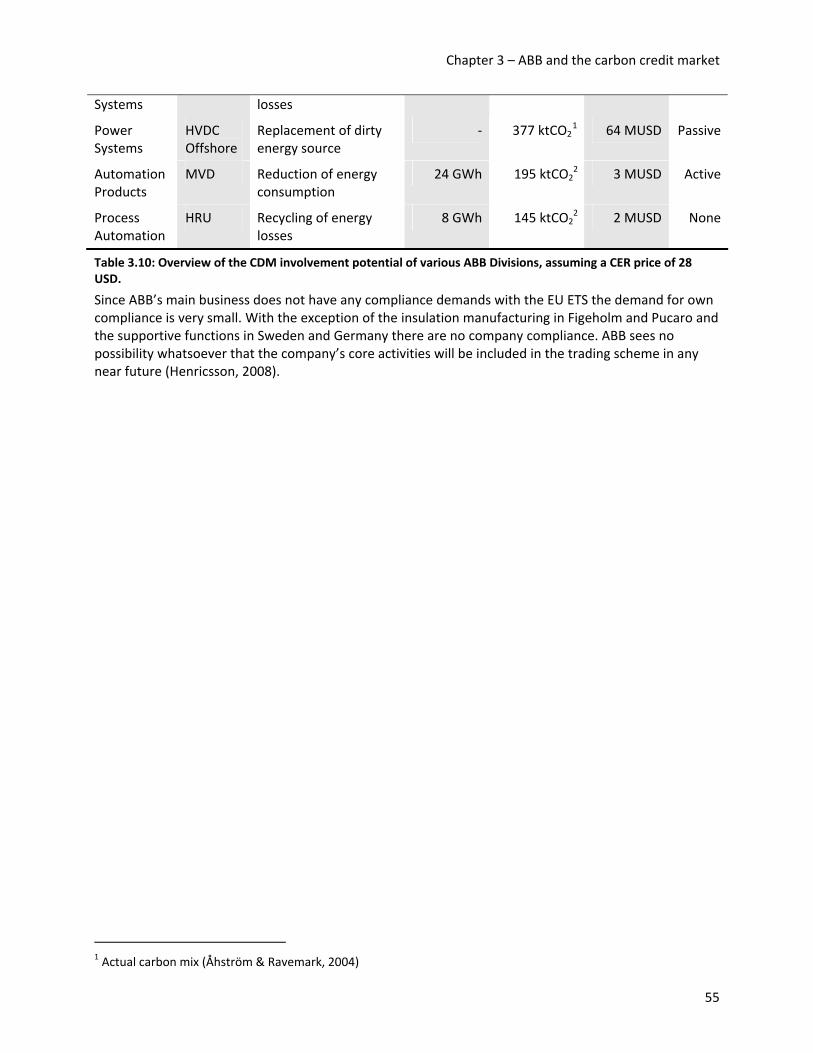

JOHANSSON, 2008; RABE, 2008; MECKES, 2008)........................................................................................ 53 TABLE 3.10: OVERVIEW OF THE CDM INVOLVEMENT POTENTIAL OF VARIOUS ABB DIVISIONS,

ASSUMING A CER PRICE OF 28 USD. .......................................................................................................... 55 TABLE 5.1: VARIABLE DEFINITION AND RELATED RISK. (HULTMAN, 2003; LAURIKKA & SPRINGER,

2003) ................................................................................................................................................................... 68 TABLE 5.2: RISK FACTORS REGARDING THE PROJECT ACTIVITY LEVEL. (LAURIKKA & SPRINGER,

2003) ................................................................................................................................................................... 68 TABLE 6.1: HOW TO INTERPRET THE DIFFERENT CATEGORIES OF THE RISK QUANTIFICATION

MATRIX. ............................................................................................................................................................ 89

v

Abbreviations AAU Assigned Amount Unit

BPO Business Process Outsourcing

CDM Clean Development Mechanism

CDM EB CDM Executive Board

CER Certified Emission Reduction

CO2e Carbon dioxide equivalent

ERU Emission Reduction Unit

EU ETS European Union Emission Trading Scheme

EUA EU Emission Allowance

FACTS Flexible Alternating Current Transmission System

GCO Group Carbon Operations

GF‐SA Group Function Sustainability Affairs

GHG Greenhouse Gases

GTO Group Treasury Operations

HVDC High Voltage Direct Current

JI Joint Implementation

LULUCF Land Use, Land Use Change and Forestry

MVD Medium Voltage Drive

NAP National Allocation Plan

RMU Removal Unit

UNFCCC United Nations Framework Convention on Climate Change

VaR Value‐at‐Risk

vi

1 Introduction The introduction presents the background to the thesis along with a brief description of ABB and ABB Group Treasury Operations (GTO). The overall purpose is then presented and a methodological discussion describes how the work intends to progress and what flaws may be introduced as a consequence of the selected method. Finally, general delimitations are made in order to make the timeframe realistic.

1.1 Global warming – the background of the thesis The global warming is the ultimate background of this thesis. Most scientists now agree that the changing climate is a direct effect of mankind’s emissions of so called greenhouse gases (GHG). In order to try to turn the trend of a climbing average temperature the UN called for an agreement with reduction of GHG all over the world as the goal. The agreement came to be known as the Kyoto Protocol and contains clear targets on emission cuts for all industrialized countries that have ratified the protocol. In order to make the reductions as cost efficient as possible a cap‐and‐trade system was created. With clear caps on allowable emissions of GHG, measured in CO2 equivalents (CO2e), and a possibility to trade these allowances between firms and even to originate new allowances from investing in emission reducing projects in the developing world, the goal is to create a sustainable environment.

ABB is a company which specializes in power transfer and automation within the whole chain of energy distribution, from generators at waterfalls to efficient production equipment. This competence is sought by ABB’s customers, regardless if they wish to reduce energy costs or if they wish to save emission allowances. This puts ABB in a possible central position with respect to the new market of emission allowances, or carbon credits.

An increasing awareness of this potential position within ABB has raised the question if and how ABB’s treasury department could assist. Today the department lacks knowledge about the carbon market and whether ABB’s subsidiaries are involved in it. To be able to make an informed decision on the appropriate response, the treasury department took the chance to investigate these matters through this master’s thesis.

1.2 ABB – a company description The history of ABB begun in 1883 with the establishment of Elektriska Aktiebolaget in Stockholm, a company manufacturing electrical lightning and generators. Only seven years later the firm merges with another, creating Allmänna Svenska Elektriska Aktiebolaget, later shortened to Asea. Around the same time Brown, Boveri & Cie (BBC) is created in Baden, Switzerland, a company that shortly afterwards is the first to transmit high‐voltage power.

The two firms’ history run in parallel for almost 100 years, until they merge in 1989 forming Asea Brown Boveri or ABB for short. During these 100 years Asea has played a big part in the electrification of Sweden, examples include building the first high voltage direct current (HVDC) transmission line in 1952 and the construction of Sweden’s nuclear power plants with the first one in 1970. In 1978 Asea also invents and launches one of the first industrial robots in the world. Meanwhile BBC has become a leader within power systems, creating the first combined heat and power plant in 1893, the first combustion gas turbine in 1939 and the world’s most powerful transformer in 1973. Both firms started their expansion abroad in the early 1900’s.

The newly formed ABB continued the expansion into eastern and central Europe upon the collapse of the iron curtain in 1990 and into USA, finally making ABB currently present in approximately 100 countries. The 1990’s was also colored by a number of strategic moves where ABB started to focus on its core competence. (ABB, 2008) This change accelerated during the early 2000’s due to a financial crisis

1

Chapter 1 – Introduction

where an economy in downturn, large claims from asbestos related law suits in USA and too much accumulated debt from the aggressive expansion during the 1990’s made ABB’s future prospects unclear.

Nuclear power, power generation and rail businesses were divested and in 2002 the organizational structure was streamlined to focus on two core areas; power technologies and automation technologies. The divestments solved the immediate debt problems and the reorganization helped ABB to focus on its

core competence. Leaving three years of net losses behind, 2004 became a profitable year, marking the end of the financial crisis. (Economist, 2002)

Automation Products 27%

Process Automation

20%

Robotics 4% Power Products 31%

Power Systems 18%

Figure 1.1: Proportions of revenue per divison. (ABB, 2007)

In 2008 ABB is a leader in power and automation technologies, having a turnover of approximately 34 billion USD with the help of 112,000 employees. The ultimate parent company of the ABB Group, which consists of 323 consolidated operating and holding subsidiaries, is ABB Ltd., Switzerland. Its organizational structure is enclosed in Appendix A, showing that ABB is organized in five different divisions along with a number of divisional transboundary group functions reporting directly to a member of the executive committee. The divisions’ proportion of revenue is depicted in Figure 1.1. (ABB, 2007)

The division’s main operations and markets are described respectively below:

• Power Products incorporates ABB’s manufacturing network for transformers, switchgear, circuit breakers, cables and associated equipment. Approximately 32,000 employees serve customers primarily in utilities, transportation and power‐generation industries.

• Power Systems offers turnkey systems and services for power transmissions, distribution grids and power plants. Other solutions provided by Power Systems include automation control and protection systems for power transmissions. The main customers are in utilities and power generation industries and approximately 14,000 employees helped serve them during 2007.

• Automation Products helps customers improve their productivity via a product portfolio containing circa 170,000 products, such as drives, motors, generators, instrumentation and power electronics. Approximately 33,000 employees worked within Automation Products in 2007, serving mainly industrial applications.

• Process Automation provides its customer with integrated solutions for control, plant optimization and industry‐specific application knowledge. 26,000 employees helped customers in primarily oil and gas, metals, minerals, pulp and paper, chemical and pharmaceuticals with their needs.

• Robotics offers robots, services and modular manufacturing solutions. Around 5,000 employees served customers in manufacturing, foundry, packaging and material handling industries.

1.2.1 ABB Group Treasury Operations GTO consists of the main office in Zurich, where we are placed, and two branches in Singapore and USA. The description will therefore only cover GTO, Zurich.

2

Chapter 1 – Introduction

GTO is ABB’s internal bank, providing the ABB Group companies with professional treasury management services that cover interest rates, foreign exchange, commodities and cash management. The department is internally organized similar to an external bank, with a trading floor, a risk control and a back office as well as with its own IT support and accounting functions. The main services provided by GTO are described below:

Interest rates. ABB policies state that both liquidity surplus and debt financing must be done with GTO except legally impossible or prohibited. GTO applies credit ratings for Group companies and quotes them market interest rates for lending and borrowing.

Foreign exchange. Group companies must hedge contracted exposures as soon as the sales order is received or the purchase order is placed. Companies with sales of standard product must hedge at least 50% of their forecasted foreign currencies sales for a maximum of 12 months. All FX transactions must be executed using GTO if legally possible. GTO manages FX risk within approved limits.

Commodities. ABB policies require that all companies must hedge risks related to forecast demand of raw materials fabricated from primary aluminum, copper and crude oil. The hedging transactions must be done by GTO, if this is not legally impossible, and the policies also states that allowable derivatives for this hedging are swaps and futures.

Other services. Include funding of working capital, internal and external payments, management of cash pools and investing the liquidity of the Group. (ABB, 2008)

1.3 Purpose The assignment from ABB is to determine whether ABB’s treasury department should take a centralized role in the handling of carbon credits spawning from projects that the ABB group companies are involved in. This leads to the purpose of the thesis being:

How should GTO respond to ABB’s involvement in carbon credit related issues?

To answer this main purpose a number of sub‐purposes evolves:

• to examine the underlying functions and mechanisms of the carbon credit market.

• to determine ABB’s current exposure to the carbon credit market and what future possibilities that lies ahead.

• to determine how carbon credit related issues are handled by ABB today.

• to determine how the GTO can get involved in the handling of carbon credits.

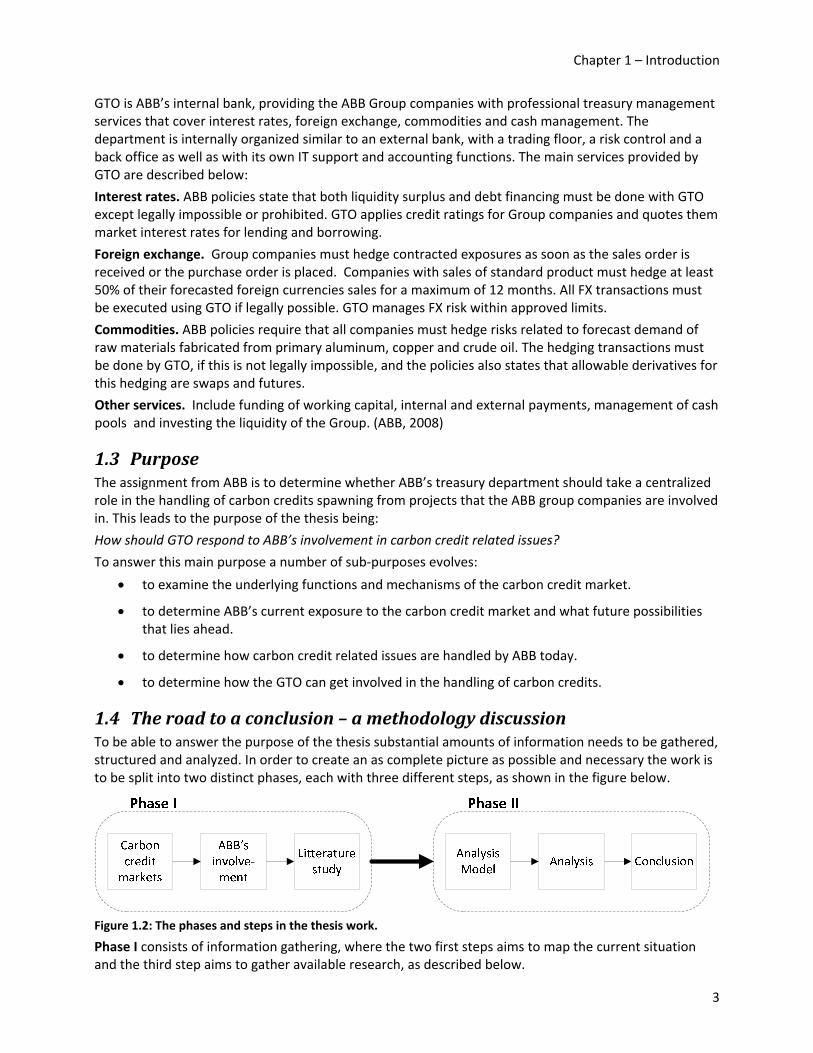

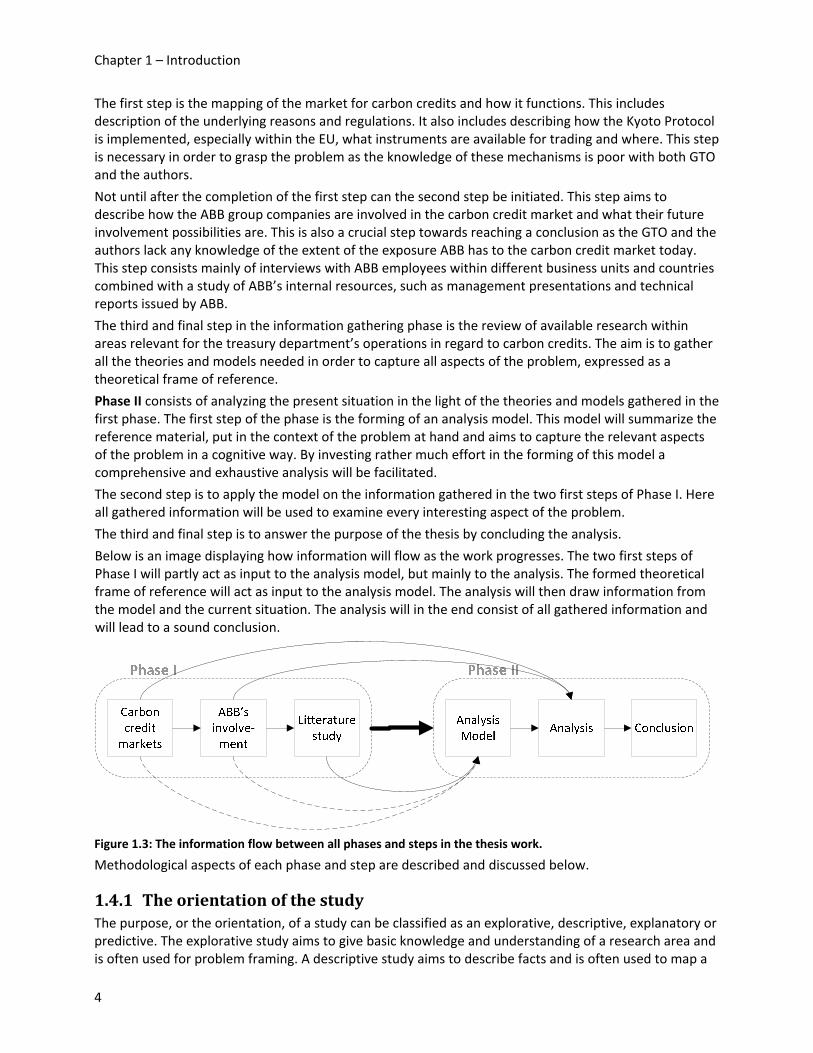

1.4 The road to a conclusion – a methodology discussion To be able to answer the purpose of the thesis substantial amounts of information needs to be gathered, structured and analyzed. In order to create an as complete picture as possible and necessary the work is to be split into two distinct phases, each with three different steps, as shown in the figure below.

Figure 1.2: The phases and steps in the thesis work.

Phase I consists of information gathering, where the two first steps aims to map the current situation and the third step aims to gather available research, as described below.

3

Chapter 1 – Introduction

The first step is the mapping of the market for carbon credits and how it functions. This includes description of the underlying reasons and regulations. It also includes describing how the Kyoto Protocol is implemented, especially within the EU, what instruments are available for trading and where. This step is necessary in order to grasp the problem as the knowledge of these mechanisms is poor with both GTO and the authors.

Not until after the completion of the first step can the second step be initiated. This step aims to describe how the ABB group companies are involved in the carbon credit market and what their future involvement possibilities are. This is also a crucial step towards reaching a conclusion as the GTO and the authors lack any knowledge of the extent of the exposure ABB has to the carbon credit market today. This step consists mainly of interviews with ABB employees within different business units and countries combined with a study of ABB’s internal resources, such as management presentations and technical reports issued by ABB.

The third and final step in the information gathering phase is the review of available research within areas relevant for the treasury department’s operations in regard to carbon credits. The aim is to gather all the theories and models needed in order to capture all aspects of the problem, expressed as a theoretical frame of reference.

Phase II consists of analyzing the present situation in the light of the theories and models gathered in the first phase. The first step of the phase is the forming of an analysis model. This model will summarize the reference material, put in the context of the problem at hand and aims to capture the relevant aspects of the problem in a cognitive way. By investing rather much effort in the forming of this model a comprehensive and exhaustive analysis will be facilitated.

The second step is to apply the model on the information gathered in the two first steps of Phase I. Here all gathered information will be used to examine every interesting aspect of the problem.

The third and final step is to answer the purpose of the thesis by concluding the analysis.

Below is an image displaying how information will flow as the work progresses. The two first steps of Phase I will partly act as input to the analysis model, but mainly to the analysis. The formed theoretical frame of reference will act as input to the analysis model. The analysis will then draw information from the model and the current situation. The analysis will in the end consist of all gathered information and will lead to a sound conclusion.

Figure 1.3: The information flow between all phases and steps in the thesis work.

Methodological aspects of each phase and step are described and discussed below.

1.4.1 The orientation of the study The purpose, or the orientation, of a study can be classified as an explorative, descriptive, explanatory or predictive. The explorative study aims to give basic knowledge and understanding of a research area and is often used for problem framing. A descriptive study aims to describe facts and is often used to map a

4

Chapter 1 – Introduction

situation or a problem. Its aim is to describe how it looks rather than try to explain the underlying reasons. An explanatory study takes one step further compared to the descriptive study and tries to clarify causality. A study with a predictive orientation goes yet another step further and aims to give a forecast or prediction about e.g. the future development of a phenomenon. A study is seldom of one pure orientation, rather it experiences influences from two or three, but is focused around one.

The level of ambition regarding the information in the results of the study is increasing from the explorative to the predictive orientation. There is also an implicit causality between the steps, such that in order to perform a predictive study one has to have an explanatory understanding of the problem. (Lekvall & Wahlbin, 2001)

It is only Phase I that concerns information gathering, each step in Phase II uses this information as inputs in order to perform analysis and conclusions. Therefore it is only reasonable to talk about a study’s orientation for the steps within Phase I.

In the first step the problem knowledge is poor, we need to gain insights into the carbon credit market in order to be able to proceed and examine whether ABB is exposed to this market. But as the main sources needed to extend the problem knowledge is of such a regulatory and legislative nature the main orientation is best described as a descriptive one. However as we proceed into Step II the orientation shifts to an exploratory one. This is due to that we have no prior knowledge of the problems before entering this step and there are no standardized sources we can use. Instead here we need to be open‐minded and try to gain a basic understanding of how the ABB divisions are involved in the carbon credit market. In Step III the problem knowledge has increased and the orientation shifts back to a descriptive one.

The figure below summarized the different orientations within the first three steps.

Figure 1.4: The main orientation of the first three steps in the thesis work.

1.4.2 Study approach First one can make a distinction between a qualitative and a quantitative study. The difference between the two is how data is expressed and how the initial analysis is performed. A qualitative study is characterized by data that cannot be quantified meaningfully and an initial analysis in terms of verbal reasoning. A quantitative study on the other hand is characterized by data coded in number form and an initial analysis in terms of calculations and statistical measures.

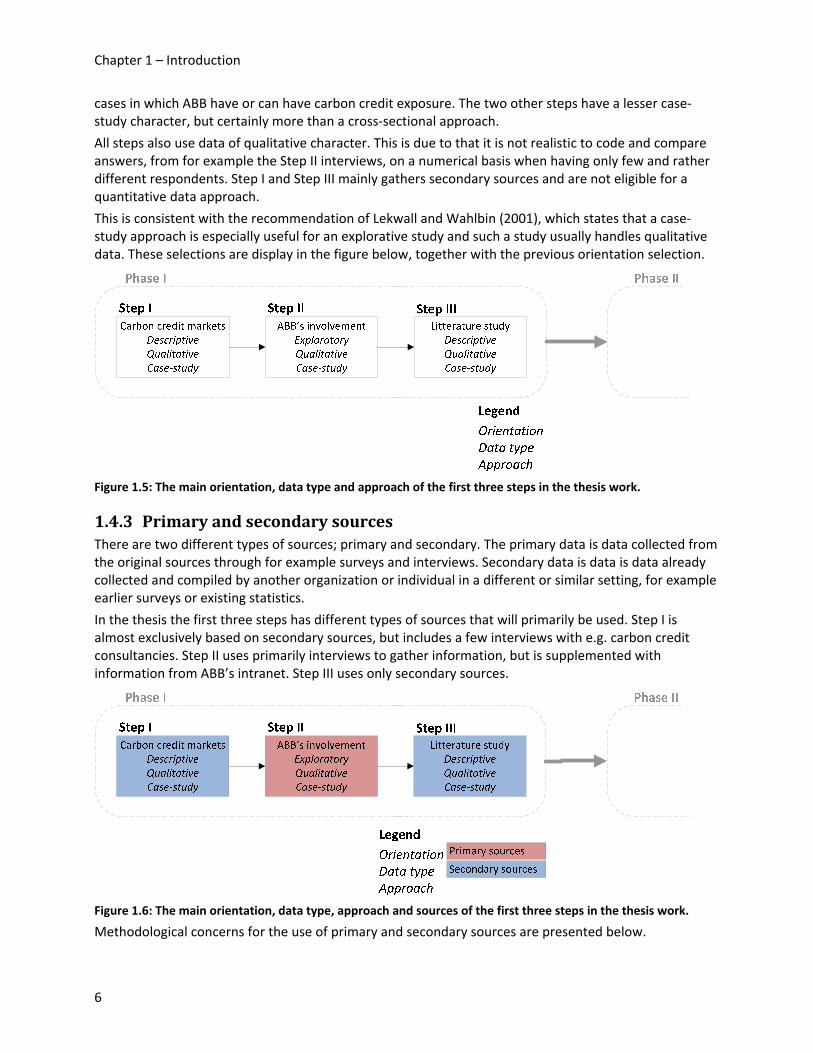

Secondly one can also make a distinction between a case‐study approach and a cross‐sectional approach. In a case‐study approach the researcher is interested in profound description and analysis of few cases. The researcher is not aiming to make conclusions of how the studied cases are related to some underlying population. A cross‐sectional approach measures a number of relations determined before the study and the aim is to generalize the findings to an underlying population. (Lekwall & Wahlbin, 2001)

All steps in Phase I are of either exploratory or descriptive orientation. It is therefore not appropriate to approach the study as a cross‐sectional study; instead the case‐study approach is selected. It is most apparent in Step II, where we will examine specific business units with certain products and formulate

5

Chapter 1 – Introduction

cases in which ABB have or can have carbon credit exposure. The two other steps have a lesser case‐study character, but certainly more than a cross‐sectional approach.

All steps also use data of qualitative character. This is due to that it is not realistic to code and compare answers, from for example the Step II interviews, on a numerical basis when having only few and rather different respondents. Step I and Step III mainly gathers secondary sources and are not eligible for a quantitative data approach.

This is consistent with the recommendation of Lekwall and Wahlbin (2001), which states that a case‐study approach is especially useful for an explorative study and such a study usually handles qualitative data. These selections are display in the figure below, together with the previous orientation selection.

Figure 1.5: The main orientation, data type and approach of the first three steps in the thesis work.

1.4.3 Primary and secondary sources There are two different types of sources; primary and secondary. The primary data is data collected from the original sources through for example surveys and interviews. Secondary data is data is data already collected and compiled by another organization or individual in a different or similar setting, for example earlier surveys or existing statistics.

In the thesis the first three steps has different types of sources that will primarily be used. Step I is almost exclusively based on secondary sources, but includes a few interviews with e.g. carbon credit consultancies. Step II uses primarily interviews to gather information, but is supplemented with information from ABB’s intranet. Step III uses only secondary sources.

Figure 1.6: The main orientation, data type, approach and sources of the first three steps in the thesis work.

Methodological concerns for the use of primary and secondary sources are presented below.

6

Chapter 1 – Introduction

Primary sources – Interviews As described above the thesis will have a case‐study approach, which implies that the primary data is collected through interviews. An interview can take the form of a fully structured interview, where the interviewer has a number of pre‐formulated questions and strictly defined answering alternatives, an open‐ended interview, where the interviewer and the interviewee discusses a subject with no preplanning, or any combination of the two. In Step II the purpose is rather clear, to clarify the present situation, which creates a good base for what kind of questions to explore. To encourage the interviewee to express him‐ or herself freely and to perhaps discover issues not considered beforehand a semi‐structured approach is selected. (Lekvall & Wahlbin, 2001)

The selection of who to interview differs between the steps. As Step II is of explorative character a top‐down approach is used. Persons holding rather high positions within the different business units or group companies are initially interviewed. If they do not hold the information sought, they are simply asked to refer to the most relevant person available. This could of course introduce some bias into study, but limitations in time and the explorative nature of the study makes this solution the only feasible. Step I is more of a descriptive character and the available interviewees are much smaller – only a few consultancies have had previous contact with ABB. The aim is therefore to interview everyone within this group.

The goal is to perform as many interviews as possible in person. This will be particularly tough in Step II, due to the number of persons that needs to be interviewed and due to the working load allocated to persons high up in the hierarchy. Where possible, telephone interviews will be performed and as last resort questions will be asked via email. The general form, i.e. semi‐structured interviews, will be used in all cases. It is important to recognize that, particularly in the email case, a semi‐structured interview may fail to capture additional information. We will try to contact each mail‐interviewee in person whenever we suspect that the person holds more relevant information.

Regarding practical aspects notes will be taken during the entire interview and be compared and discussed as fast as possible after each interview. A discussion on what have been said will take place and additional or clarifying questions to the interviewee will be asked via phone or email if needed. Every interview has also been pre‐booked in order to not catch the interviewee at a bad time where he or she is stressed or otherwise suspected to be unable to give satisfying answers.

Secondary sources The main sources used in step one are the actual Kyoto Protocol and the legislative and regulative documents of the commitments made by the EU countries. However, as the authors lack any deeper juridical education and experience, sources summarizing these documents will also be used. In order to preserve the integrity of the thesis all such sources will, whenever possible, be checked against other summarizing sources and/or the normative documents.

The second step will use ABB internal presentations and technical reports in order to capture ongoing work within the company with respect to carbon credit markets. We will use the internal search engine to locate relevant sources and we expect to receive relevant material from our mentors and interviewees.

In the third step we will use database search engines to locate books and journal articles covering the subject we identify in the problem breakdown chapter. We will start broad, searching on general keywords to get a grasp of the subject. We will then proceed to more specific sources handling interesting questions. References of the material will be checked, to see if a publication relies too much on one source and from what publications the sources have been taken.

7

Chapter 1 – Introduction

1.4.4 Analysis How an analysis and a reasoning is built up can be described by three main approaches; induction, deduction and abduction. They all contain the same three components, but are organized differently. One component is the way one interprets how the world is structured and how it works, here called the model. Another component is something that has been empirically observed, named the empirics. The last component, named the result, is the result one gets when relating the empirical observations to the model. (Hörte, 1999)

Figure 1.7: The differences between the analytical approaches. (Hörte, 1999, p.8)

As shown in the figure above the difference between the analytical approaches is in the starting point. In a deductive approach the researcher goes from a model, applies them on empirical data in order to reach a result. An inductive approach starts in empirical data, using them as results in order to conclude general theories and models. Finally, an abductive approach starts with a situation, i.e. the result, and attempts to explain the situation using a model with support from empirical findings. (Hörte, 1999)

The analysis and reasoning approach used in this thesis will resemble the deductive approach the most. We will start with a set of theories to which we apply empirics in order to reach result.

1.4.5 Method criticism This part presents criticism to the selected methodological approaches. Its purpose is to demonstrate that the authors are aware that the method will have flaws. By being aware of these flaws their effect could be managed. The methodological choices are summarized in the figure below and its criticism further below.

Figure 1.8: All methodological choices of all steps and phases in the thesis work.

8

Chapter 1 – Introduction

Phase I – Primary sources Two factors affect the quality of the study, its reliability and its validity. The reliability concerns the measuring method’s ability to resist influence of different disturbing moments. If different respondents give different answers to the same question, or if one respondent gives different answers to the same question asked on different times, the reliability of the study is low. (Lekvall & Wahlbin, 2001) To heighten the reliability the same questions will be asked to different persons within the same business unit to compare the answers. As mentioned above interviews will be pre‐booked in order to avoid disturbances such as stressed or tired interviewees. Clarifying questions will be asked in case of unclarity regarding what has been said or if the answer is hard to interpret. The fact that an individual’s view or knowledge of a situation is not necessarily the true one is something that cannot be avoided, but taking the measures described above is an insurance that the used information is the best available.

The validity of a study concerns the measuring method’s ability to actually measure the property it intends to measure. To ensure that a study has a high validity is generally rather difficult. (Lekvall & Wahlbin, 2001) The face validity, i.e. that the respondent agrees that the questions asked are relevant for the study’s purpose, for the first phase is considered to be rather good, since most of the interviews are conducted within ABB which will encourage an less formal discussion climate where questions easily can be altered so that all involved parties are satisfied.

Phase II – Secondary sources Step I is heavily based on legislative and regulatory documents. This may introduce bias and misinterpretation due to the lack of juridical education and experience with the authors. We will try to minimize this by cross‐reading the official documentation against other summarizing sources to increase the integrity of this part.

The internal material used in Step II has varying purposes and may therefore be biased. We will try to stay objective to our cause when reading this material by being aware of the publications purpose and how this may reflect on the content.

In Step III we are affected by time limitations; we cannot cover all research available and we cannot go through all available databases. This is a rather natural limitation, but may nevertheless affect the frame of reference. However, the method introduced above follows the recommendations of Lekvall and Wahlbin (2001) and we will try to as objective as possible when choosing what literature to include in the thesis.

Phase II – Analysis Even though our general analysis approach will be of a deductive character it is not possible to form a pure and complete logical chain of events leading to a conclusion. Assumptions, delimitations and introduced simplifications will affect the conclusion and must be chosen carefully. We will rely on our own judgment and common sense to do this and this may obviously introduce bias. But, as Gummesson (2006) suggests:

It [research] includes objectivity, intersubjectivity and subjectivity. Instead of being ashamed of subjectivity elements, we should let them out of the closet and use them as assets.

(Gummesson, 2006, p.178)

1.5 Delimitation The study will not focus on technical aspects of carbon credits, such as how to properly price different instruments, what hedge ratios should be used when cross‐hedging or specific risk management techniques. The study will rather focus on general descriptions of the instruments and general risk

9

Chapter 1 – Introduction

management techniques. This is partly due to the lack of proper time series but mainly due to the focus of the thesis being of a more strategic nature.

The case descriptions will only highlight future potential of cash flows related to carbon credits. They will not be thoroughly investigated with respect to CDM acceptance probabilities or customer involvement probabilities.

ABB has used and are using carbon credits indirectly through sales arguments. Another master thesis that investigates how voluntary carbon credits and carbon certifications can be used to enhance, among other things, the sales arguments is being conducted in parallel within the MVD division in Switzerland. Therefore this thesis will not go in very deep on these subjects, but rather assume that these mechanisms work satisfactory today.

The carbon credit markets are developing rapidly compared to more mature financial markets, which have introduced issues regarding timing. We will therefore handle certain issues with respect to a fixed point in time. It is clearly marked in the thesis whenever this limitation has been used.

10

2 Carbon credits and emission trading Carbon credits and the emission trading market are the underlying mechanisms of this study. In order to give the reader an understanding of these mechanisms, this initial chapter will explain the issue of global warming and the measures that are being taken in order to meet associated future threats. Unless otherwise stated, the information in this chapter originates from the United Nations Framework Convention on Climate Change (UNFCC, 2008a) and the European Commission (European Commission, 2008).

2.1 The greenhouse effect and global warming One of the most important conditions for life on earth is maintaining a stable temperature that enables inhabitance. The atmosphere of the earth preserves greenhouse gases (GHG) which in turn preserves the solar heat that enters the atmosphere as radiation. Without this so called greenhouse effect, the temperature of the earth would not reach sufficient levels.

GHG are gaseous constituents of the atmosphere that absorb and emit radiation at certain wavelengths within the infrared radiation spectrum emitted by the Earth. The most important greenhouse gases are water vapor, carbon dioxide, methane, nitrous oxide and ozone.

In the last century, the greenhouse effect became considerable larger, thus raising the average temperature of earth about 0.75 °C (IPCC, 2007). A vast majority of the world climate experts deduct this increase of temperature to the increase of GHG due to human activities. This temperature increase due to a larger greenhouse effect is referred to as global warming.

The Intergovernmental Panel on Climate Change (IPCC) concludes that Most of the observed increase in global average temperatures since the mid‐20th century is very likely due to the observed increase in anthropogenic greenhouse gas concentrations.

(IPCC, 2007, p.10)

IPCC forecasts that the temperature increases will be considerably larger during the 21st century if substantial measures to reduce the emission of greenhouse gases are not carried out.

2.2 The UNFCCC With the warnings of IPCC and other climate experts in mind, a majority of the countries in the world joined an international treaty called the United Nations Framework Convention on Climate Change (UNFCCC) which was created 1992. The treaty was made in order to initiate considerations of what could be done to cope with increasing global temperatures. The treaty was created without setting any binding GHG emission limits and is therefore not considered to be legally binding.

The convention divides countries into three main groups according to differing commitments:

• The Annex I parties consist of industrialized countries that were members of the Organization for Economic Cooperation and Development (OECD) at the time of convention creation. Countries with economies in transition, such as Russia, the Baltic States and several other Eastern‐ and Central European States are also included. Today, Annex I consists of 41 countries. These countries agreed to establish national policies to reduce climate change and limit anthropogenic greenhouse gas. The Annex I countries committed to reduce their emissions to 1990’s levels by the year of 2000, either by reducing their own emissions or through joint efforts.

• The Annex II parties are a subgroup of the Annex I parties, namely the OECD members. These countries are not only committed to reduce their own emissions but also to provide financial resources to developing countries to undertake emission reducing activities.

11

Chapter 2 – Carbon credit and emission trading

• Non‐Annex I parties mainly consist of developing countries. These countries are not subject to the same emission reductions for economic or geographical reasons but they need to report their emission status. The convention emphasizes activities such as investments and technology transfers by developed countries to meet the undeveloped countries needs. The 49 least developed countries (LDCs) are given special consideration because of their limited capacity to respond to climate change.

2.3 The Kyoto Protocol The UNFCCC encourages emission reductions but in order to make binding commitments a linked addition to the convention has been signed, the Kyoto Protocol.

The general implications of the Kyoto Protocol is the establishment of legally binding targets for emission of greenhouse gases for 36 industrialized countries plus the European Union which is considered as one entity.

The protocol was adopted in 1997 and was open for signing from March 1998 to March 1999 and thereafter entered into force on 16 February 2005. By the final signing date, the protocol was signed by 84 countries. The parties that had not yet signed have been able to do this later and today a majority of the world countries have signed the protocol. The only country that has signed the protocol but not ratified it is the United States.

The average reduction target for the countries bound to reduce their emissions is 5.2% in relation to the 1990 emission levels. This reduction should be carried out during the first commitment period from 2008 to 2012. Though, separate emission reduction targets have been created for individual regions depending on the current emissions and the effort needed to reduce emissions. For example, the European Union are bound to reach emission levels of 8% below the 1990 levels while some countries, such as Australia, are permitted increases in its emissions. The individual emission targets of the Kyoto Protocol are stated in the protocols Annex B. The Annex B countries are almost identical to the Annex I countries, though certain Annex I countries such as Turkey were not included in Annex B since they were not parties to the convention when the protocol was adopted.

The emission targets are quantified as CO2 equivalents (CO2e) but include the six main greenhouse gases which are presented in Annex A of the Kyoto Protocol:

• Carbon dioxide – CO2

• Methane – CH4

• Nitrous oxide – N2O

• Hydroflourocarbons – HFCs

• Perflourocarbons – PFCs

• Sulphur hexaflouride – SF6

The Kyoto Protocol compliance is carried out through an enforcement branch. If any Annex B country fails to meet its Kyoto emission restrictions they are subject to penalties. Except for making up for the difference between the assigned emission amount and the actual emission amount during the second commitment period (after 2012), the penalized country will get a 30% decrease of the second commitment period emission targets.

2.4 Kyoto mechanisms and Kyoto units The parties included by the Kyoto Protocol are bound to meet their emission targets, which can be done through domestic measures such as investing in new technology, introducing emission taxes or

12

Chapter 2 – Carbon credit and emission trading

subventions. As a complement to these domestic measures, the Kyoto protocol offers three market based mechanisms; Emission Trading, Clean Development Mechanism and Joint Implementation, to manage the four Kyoto carbon credit units, Assigned Amount Unit, Certified Emission Reduction, Emission Reduction Unit and Removal Unit. These market based mechanisms will be in the focus of this chapter.

2.4.1 Assigned Amount Unit To quantify the assigned emission limits of each Kyoto Protocol party, the total allowed emissions were divided into Assigned Amount Units (AAU) which was distributed among participating countries. One AAU represents a permission to emit one ton of CO2e.

2.4.2 Emission Trading Mechanism Emission trading allows countries which manage to reduce their emissions more than required, thus creating excessive carbon credits, to sell these to countries who cannot reach their targets. Carbon credits are now traded like all other commodities at a market known as the carbon market. New carbon credits are issued at the primary market, but the emission trading system also allows these credits to be traded amongst their owners on a secondary market.

The advantage of emission trading, compared to for example emission tax, is that it sets a controllable cap of emissions. It also creates an environment where emissions will be reduced at lowest possible cost. For example it might cost company A 100€ to reduce emissions representing one AAU while it would cost company B only 50€ to achieve the same reduction, due to the nature of the companies businesses. If an AAU unit would cost 75€ it would make more sense for company A to buy one AAU rather than reducing their emissions internally and vice versa for company B.

Except for the fixed amount of AAU distributed amongst the major part of the Annex I countries there are three other instruments issued and traded at the global market, namely the CERs, ERUs and RMUs which are described below.

2.4.3 Clean Development Mechanism and Certified Emission Reduction The Clean Development Mechanisms (CDM) enables a country with an emission limitation (Annex B) commitment under the Kyoto Protocol to carry out an emission reducing project in a developing country that lacks a binding emission limit. By doing this, a project can earn Certified Emission Reduction (CER) credits which is a tradable instrument that gives the owner the right to emit one ton of CO2. The CDM system enables industrial countries to be more flexible in the way that they can meet their emission targets. A CDM project is not bound to governments and may involve both private and public entities.

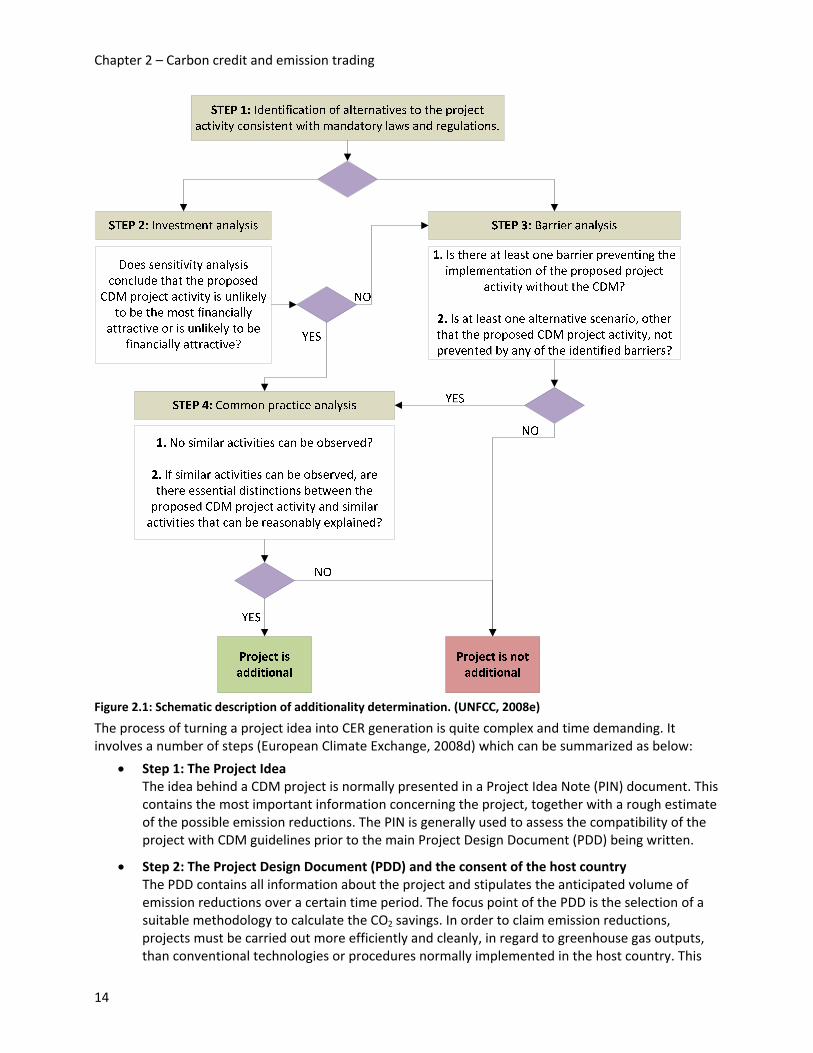

In order for an Annex B country to carry out a CDM project in a developing country, the country hosting the project must agree on the fact that the project will provide a sustainable emission reduction. To qualify as a CDM project the project must also provide emission reductions that are additional to what otherwise would have occurred ‐ the project must supply emission reductions compared to the current state, must not be financially feasible without the support of carbon credits or need the support of carbon credits to overcome project barriers. These barriers could for example be economical, technological, political or local resistance. The additionality of a project is overseen by the CDM Executive Board (EB) and is illustrated schematically in Figure 2.1.

13

Chapter 2 – Carbon credit and emission trading

Figure 2.1: Schematic description of additionality determination. (UNFCC, 2008e)

The process of turning a project idea into CER generation is quite complex and time demanding. It involves a number of steps (European Climate Exchange, 2008d) which can be summarized as below:

• Step 1: The Project Idea The idea behind a CDM project is normally presented in a Project Idea Note (PIN) document. This contains the most important information concerning the project, together with a rough estimate of the possible emission reductions. The PIN is generally used to assess the compatibility of the project with CDM guidelines prior to the main Project Design Document (PDD) being written.

• Step 2: The Project Design Document (PDD) and the consent of the host country The PDD contains all information about the project and stipulates the anticipated volume of emission reductions over a certain time period. The focus point of the PDD is the selection of a suitable methodology to calculate the CO2 savings. In order to claim emission reductions, projects must be carried out more efficiently and cleanly, in regard to greenhouse gas outputs, than conventional technologies or procedures normally implemented in the host country. This

14

Chapter 2 – Carbon credit and emission trading

hypothetical reference scenario forms the so‐called baseline. The PDD, and thus the suggested CDM project, must be authorized through the responsible authorities in the developing country, i.e. its Designated National Authority (DNA). Attention is focused on the contribution of the project to the sustainable development of the country.

• Step 3: Validation In addition, the PDD must be checked by a United Nations accredited organization, called a Designated Operational Entity (DOE). The validation process of the project is usually carried out by certification institutions such as SGS, TUV or DNV. Validation includes an inspection of the PDD, with focal point on the methods used in order to comply with baseline principles, as well as the calculation and monitoring of emission reductions. Everyone is allowed to comment on a project during the validation process, and the PDD is open to debate for a period of 30 days on the UNFCCC website.

• Step 4: Registration Once validated, the project developer makes an application to register the project with the CDM EB. This Executive Board has the last word, as it is the executive organ of the United Nations in all CDM matters. Once the board agrees, the project is officially registered and CERs can be generated.

• Step 5: Monitoring It is far from over with the registration of the project under the CDM. After all, the PDD only depicts the intentional performance of a project toward emission reductions over a certain time. The project developer must prove whether this performance is actually generated over the credit period of the project. Monitoring reports, in which features of the project are reported, assist here. The reported information permits the precise calculation of the emission reductions in relationship to the selected baseline.

• Step 6: Verification Despite the monitoring reports, accredited organizations keep a close eye on project developers. This process is called Verification and is normally carried out on a yearly basis. After inspection, the independent Verifier goes on to make a statement concerning the integrity and accuracy of the information provided in the monitoring report.

• Step 7: Issuing of the CERs Provided that the monitoring reports are approved without objection during the verification, the CDM Executive Board is allowed to issue the generated CERs.

The crediting period is the period for which the CDM Program Activity (CPA) generates emission reductions from the baseline case. There are certain rules (Baker&McKenzie, 2008) which have to be taken into account when determining the period for which the CDM project will generate CERs:

• The crediting period for a CPA must not extend beyond the operational lifetime of the CPA.

• The crediting period cannot exceed the end date of the program of activities to which the CPA belongs.

• The crediting period of a CPA is limited to 7 years with the option to renew it twice, to a total maximum of 21 years, or to 10 years without the renewal option.

The exploding growth of the CDM market, described in Chapter 0, has lead to significant delays due to the overloading of the of the CER issue administration. These bottlenecks have put pressure of the CDM to deliver sufficient CER on time.

15

Chapter 2 – Carbon credit and emission trading

For example, of the 3,188 projects currently in pipeline a vast majority, 2,022 projects, are at the validation stage. Further on, market participants report that it is taking up to six months to engage a DOE just to reach the CDM pipeline (step 4 above). Upon initiation of registration, projects experience an average wait time of 80 days until registration completion. Because of the following monitoring processes (step 5 and 6 above), projects need an average time of one to two years to reach CER issuance from the time they enter the pipeline. That sums up to a total time of 1.5 to 2.5 years to reach issuance from the point where the project idea is generated. (World Bank, 2008)

Besides experiencing problems due to the rigorous administration processes DOEs have been reporting staffing shortages. The shortages have different reasons, such as lack of candidates with proper language knowledge or the post 2012 uncertainty presented in Chapter 0.

There are certain simplifications to the CDM registration rules that can be made according to a directive of simplified modalities and procedures for small‐scale CDM projects. The major conclusion from this directive is that a project can be considered a small‐scale project if it has a capacity below 15 MW, if it saves up to 15 GWh per year or if the project emits less than 15 ktCO2. If classified as a small‐scale project the project will be subject to less rigorous registration processes. (UNFCC, 2008f) It will also lead to CDM related transaction costs being reduced up to 70% (Yapp, 2006).

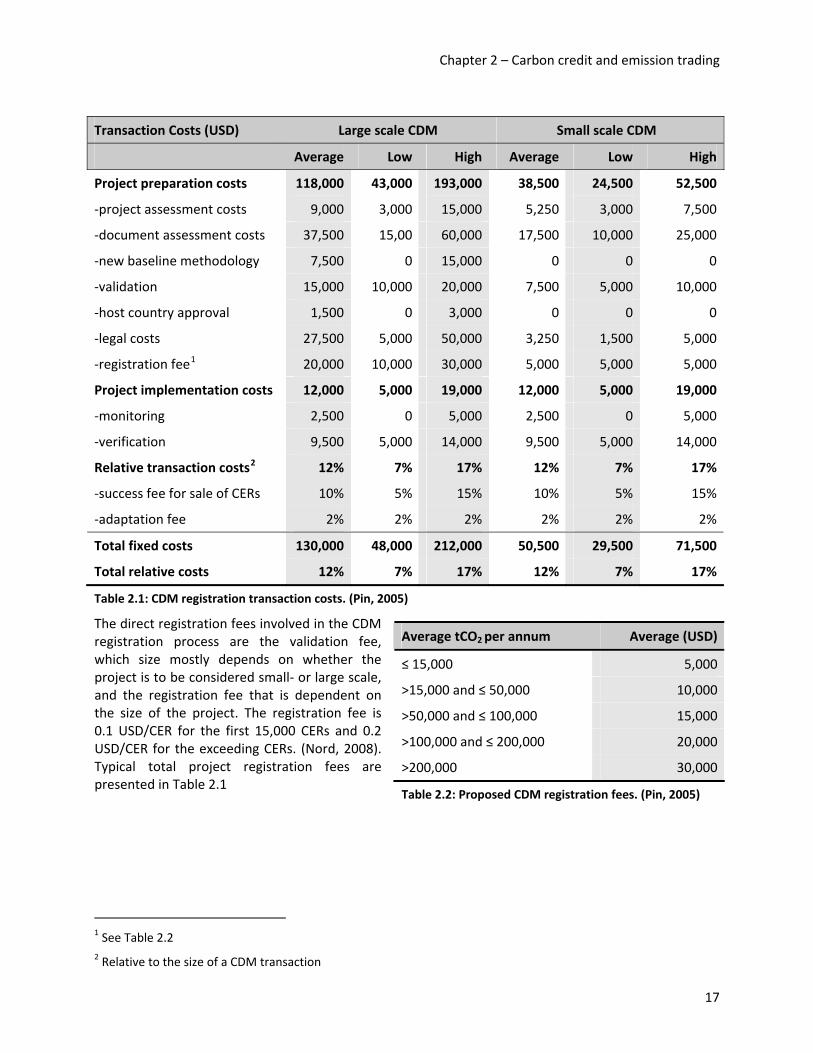

CDM transaction costs The flexible mechanism project registration is not only complex and time demanding, it also generates significant costs. Except for the indirect costs connected to the personnel involvement there are many direct registration and monitoring costs. The total transaction costs for a normal CDM project is about USD 200,000 while the transaction costs for the small‐scale CDM projects are significantly lower at about 60,000 (Yapp, 2006; Nilsson 2008).

The transaction costs are dependant of the size of the project, the demands of the hosting country, what type of project that is performed and who is conducting the project. If the registration process is handled by an inexperienced group the costs can be significantly higher than 200,000 USD. (Nilsson, 2008) Transaction costs can be divided into three major categories as follows (Pin, 2008):

• Project preparation costs

• Project implementation costs

• Relative transaction costs

The transaction cost structure is presented in Table 2.1 and Table 2.2 and illustrated by Figure 2.2.

16