Embed Size (px)

Citation preview

Liquidity requirements according to Basel III/CRD IVA survey concerning Liquidity Coverage Ratio (LCR)and Net Stable Funding Ratio (NSFR)

On behalf of Bankenfachverband e. V.

Management summary

A SURVEY ON BASEL III/CRD IV LIQUIDITY REQUIREMENTS

Contacts

Bankenfachverband e. V. Michael Somma Head of Economic Affairs Littenstr. 10 10179 Berlin Tel. +49 30 2462 596 16 [email protected] Ernst & Young GmbH Wirtschaftsprüfungsgesellschaft EMEIA Advisory/Financial Services – Quality & Risk Management Dr. Karsten Füser Mittlerer Pfad 15 70499 Stuttgart Tel. +49 711 9881 14497 [email protected]

A SURVEY ON BASEL III/CRD IV LIQUIDITY REQUIREMENTS

E 1

Management Summary

Due to the general decline of mutual trust within the financial markets that came along with the general eco-nomic crisis, many banks have suffered from liquidity shortages despite adequate economic capital buffers. Consequently, in the wake of the crisis, liquidity risk and its appropriate governance have moved into the focus of regulators and market participants.

Basel III has introduced two liquidity ratios to enforce a quantitative governance of liquidity risk: Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR). The short-term liquidity ratio LCR is meant to make sure that financial institutions are able to satisfy their need for liquidity within a defined liquidity stress scena-rio using a 30 calendar day time horizon. The structural liquidity ratio NSFR, on the other hand, should guaran-tee a matched maturity refinancing of a financial institution over a time period of one year. The Capital Re-quirements Regulation further details necessary computations and data collection with respect to both ratios at a European level.

In order to counter the general uncertainties related to the introduction of both the LCR and the NSFR, the Bankenfachverband e. V. has resolved to conduct a survey among its German member institutions. The survey is intended to administer a comprehensive and reliable overview over the present liquidity situations of the German member institutions and hence to possibly sharpen their awareness for possible problems. The Bank-enfachverband has entrusted Ernst & Young with the conception, conduction and evaluation of the associated research.

In total, 37 members of the Bankenfachverband in Germany have participated in the survey. These banks dis-play a wide variety of core business areas and portfolio sizes, which in turn significantly influences the band-width of values of the liquidity ratios captured in the survey.

LCR and NSFR above regulatory minimum re-quirements

5 institutions

Need for action w.r.t. LCR 10 institutions

Need for action w.r.t. NSFR 4 institutions

Need for action w.r.t. LCR and NSFR 18 institutions

Figure 1: Overview of the results with respect to LCR and NSFR

Our analysis has shown that for the majority of the institutions, both present LCR and present NSFR values indicate that corrective actions should be taken. Only five institutions were able to comply with the planned regulatory minimum values of 100 % for both LCR and NSFR at the reference date of the survey. 14 institutions are facing a need for action with respect to at least one of the two liquidity ratios (among these is one bank, for which the NSFR could not be determined during the research period). 18 institutions are below the planned regulatory threshold of 100 % for both of the liquidity ratios.

A SURVEY ON BASEL III/CRD IV LIQUIDITY REQUIREMENTS

2 E

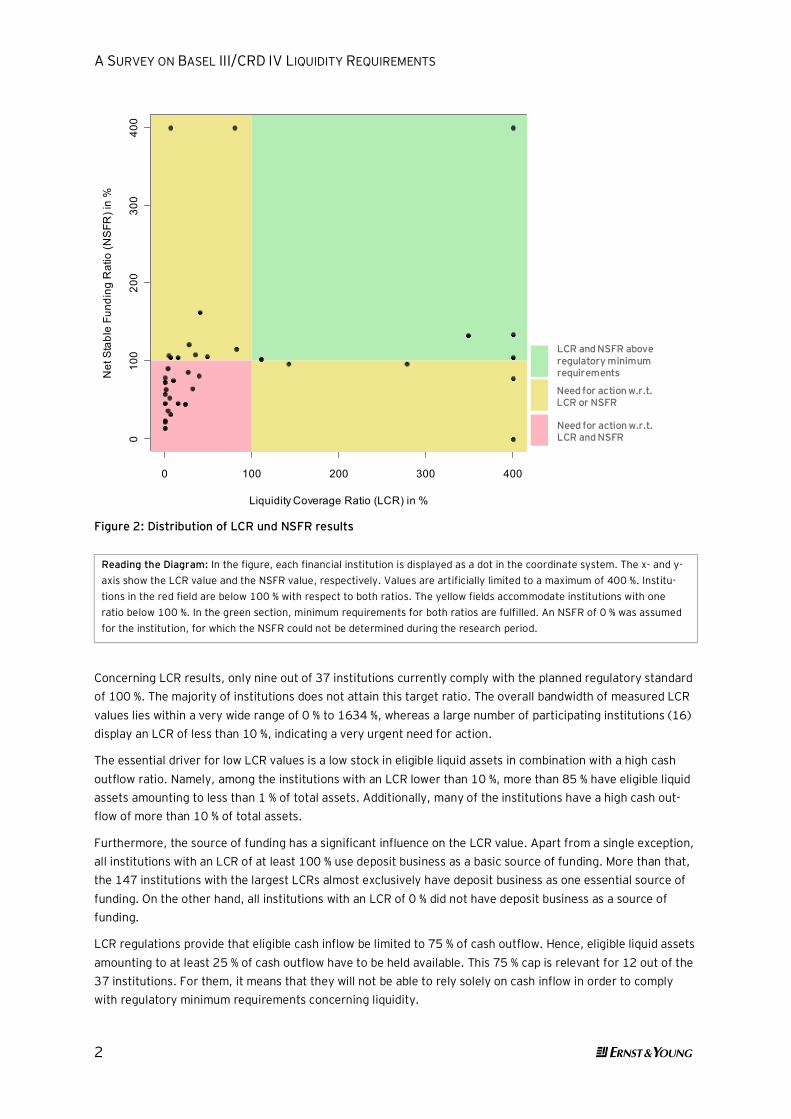

Figure 2: Distribution of LCR und NSFR results

Reading the Diagram: In the figure, each financial institution is displayed as a dot in the coordinate system. The x- and y-axis show the LCR value and the NSFR value, respectively. Values are artificially limited to a maximum of 400 %. Institu-tions in the red field are below 100 % with respect to both ratios. The yellow fields accommodate institutions with one ratio below 100 %. In the green section, minimum requirements for both ratios are fulfilled. An NSFR of 0 % was assumed for the institution, for which the NSFR could not be determined during the research period.

Concerning LCR results, only nine out of 37 institutions currently comply with the planned regulatory standard of 100 %. The majority of institutions does not attain this target ratio. The overall bandwidth of measured LCR values lies within a very wide range of 0 % to 1634 %, whereas a large number of participating institutions (16) display an LCR of less than 10 %, indicating a very urgent need for action.

The essential driver for low LCR values is a low stock in eligible liquid assets in combination with a high cash outflow ratio. Namely, among the institutions with an LCR lower than 10 %, more than 85 % have eligible liquid assets amounting to less than 1 % of total assets. Additionally, many of the institutions have a high cash out-flow of more than 10 % of total assets.

Furthermore, the source of funding has a significant influence on the LCR value. Apart from a single exception, all institutions with an LCR of at least 100 % use deposit business as a basic source of funding. More than that, the 147 institutions with the largest LCRs almost exclusively have deposit business as one essential source of funding. On the other hand, all institutions with an LCR of 0 % did not have deposit business as a source of funding.

LCR regulations provide that eligible cash inflow be limited to 75 % of cash outflow. Hence, eligible liquid assets amounting to at least 25 % of cash outflow have to be held available. This 75 % cap is relevant for 12 out of the 37 institutions. For them, it means that they will not be able to rely solely on cash inflow in order to comply with regulatory minimum requirements concerning liquidity.

LCR and NSFR above regulatory minimum requirements

Need for action w.r.t.LCR or NSFR

Need for action w.r.t. LCR and NSFR

0 100 200 300 400

010

020

030

040

0

Liquidity Coverage Ratio (LCR) in %

Net

Sta

ble

Fund

ing

Rat

io (N

SFR

) in

%

A SURVEY ON BASEL III/CRD IV LIQUIDITY REQUIREMENTS

E 3

Participating institutions would have to invest 5.6 bn EUR if they wanted to stock up on eligible liquid assets until compliance with the regulatory target was reached. On average this means that those institutions will have to invest more than 13 % of their total assets into eligible liquid assets.

NSFR results do paint a much brighter picture. All in all, 15 out of 36 institutions feature an NSFR of 100 % or higher (for one bank, the relevant data delivery was not sufficient to compute NSFR). Actual NSFR values range from 14 % to 651 %, displaying far less variance than for LCR.

Again, institutions with deposit business as a primary or significant source of funding performed better con-cerning NSFR values. In particular, deposit business is an essential source of funding for 80 % of the institutions which feature an NSFR of more than 100 %.

In terms of a summary, the survey indicates significant and overall need for action across participating finan-cial institutions. Particularly, LCR results are quite visibly below the regulatory target value of 100 % for many institutions and portend notable pressure towards adjustments. On the one hand, these adjustments will mate-rialize in the necessary acquisition of a portfolio of eligible liquid assets. For many, primarily smaller, institu-tions, this also means an investment into a new asset class, and entails the conduction of a new products process, and the establishment of corresponding business- and risk management processes in accordance with the minimum requirements for risk management (MaRisk). More than this, there will be consequences for the profitability of institutions, in case profit margins within the portfolio of eligible liquid assets are significantly below the margins of the institutions usual business.

However, compliance with the minimum requirements will not always be attainable solely by the investment into a portfolio of eligible liquid assets. In many cases, there will be repercussions on the strategic orientation of the business and hence, on cash in- and outflows. For instance, institutions with a high cash outflow (indica-ting short term refinancing practices) will have to reassess their funding strategy.

When choosing among possible actions to be taken towards the end of, e.g., an LCR optimization, possible ef-fects on NSFR must be taken into account. For example, switching from overnight money to time deposits with a maturity of 60 days in refinancing would positively influence LCR, but leave NSFR quite unimpressed.

Last but not least, regulatory uncertainties need to be taken into account at present. According to the press release of the Group of Governors and Heads of Supervision (GHOS) as of January 8th, 2012, no essential changes in the Basel III regulation for the liquidity ratios are to be expected. However, modifications may be impending for some key aspects such as the composition of the portfolio of eligible liquid assets and the cali-bration of the net cash outflows. At a European level, the European Banking Authority (EBA) will establish cer-tain so called Technical Standards. Here, to make an example, an extended eligibility of mortgage bonds or of asset backed securities is being discussed.

A SURVEY ON BASEL III/CRD IV LIQUIDITY REQUIREMENTS

4 E

List of members of Bankenfachverband

The members of Bankenfachverband e. V. are listed below (in alphabetical order): (source: homepage of Bankenfachverband, www.bfach.de):

abcbank GmbH

akf bank GmbH & Co KG

AKTIVBANK AG

Allgemeine Beamten Kasse Kreditbank AG

AUMA KREDITBANK GmbH & CO.KG - Bank für Finanzierungen

Bank Deutsches Kraftfahrzeuggewerbe AG

Bank11 für Privatkunden und Handel GmbH

Banque PSA FINANCE S.A. Niederlassung Deutschland

Barclaycard Barclays Bank PLC

BMW Bank GmbH

BNP PARIBAS LEASE GROUP S.A. Zweigniederlassung Deutschland

Brühler Bank eG

C&A Bank GmbH

CB Bank GmbH

Commerz Finanz GmbH

Credit Europe Bank N.V. Niederlassung Deutschland

CreditPlus Bank AG

CRONBANK Aktiengesellschaft

Deutsche Kreditbank Aktiengesellschaft

Deutsche Leasing Finance GmbH

Deutsche Postbank AG

DZB BANK GmbH

FFS Bank GmbH

FGA BANK Germany GmbH

Ford Bank Niederlassung der FCE Bank plc

GE Capital Bank AG

GE Money Bank AG (Schweiz)

GEFA Gesellschaft für Absatzfinanzierung mbH

GMAC Bank GmbH

A SURVEY ON BASEL III/CRD IV LIQUIDITY REQUIREMENTS

E 5

Hanseatic Bank GmbH & Co KG

Honda Bank GmbH

IBM Deutschland Kreditbank GmbH

Ikano Bank GmbH

ING-DiBa AG

Iveco Finance GmbH

Mercedes-Benz Bank AG

MKB Mittelrheinische Bank GmbH

MKG Bank Zweigniederlassung der MCE Bank GmbH

netbank AG

NordFinanz Bank Aktiengesellschaft

norisbank GmbH

RCI Banque S.A. Niederlassung Deutschland

readybank ag

S-Kreditpartner GmbH

Santander Consumer Bank AG

SKG BANK AG

Standard Chartered Bank Germany Branch

Süd-West-Kreditbank Finanzierung GmbH

TARGOBANK AG & Co. KGaA

TeamBank AG Nürnberg

TEBA Kreditbank GmbH & Co. KG

TOYOTA KREDITBANK GMBH

UniCredit Family Financing Bank (Niederlassung der UniCredit S.p.A.)

UniCredit Leasing Finance GmbH

Valovis Bank AG

Volkswagen Bank GmbH

Volvo Auto Bank Deutschland GmbH

VON ESSEN GmbH & Co. KG Bankgesellschaft

VR DISKONTBANK GmbH

Ernst & Young

Assurance | Tax | Transactions | Advisory

About the global Ernst & Young organization The global Ernst & Young organization is a leader in assurance, tax, transaction and advisory services. It makes a difference by helping its people, its clients and its wider communities achieve their potential. Worldwide, 152,000 people are united by shared values and an unwavering commitment to quality.

The global Ernst & Young organization refers to all member firms of Ernst & Young Global Limited (EYG). Each EYG member firm is a separate legal entity and has no liability for another such entity’s acts or omissions. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information, please visit www.de.ey.com

In Germany, Ernst & Young comprises some 7,000 people at 22 locations. In this publication, “Ernst & Young” and “we” refer to all German member firms of Ernst & Young Global Limited.

© 2012 Ernst & Young GmbH Wirtschaftsprüfungsgesellschaft All Rights Reserved.

HFI 0212

This publication contains information in summary form and is therefore intended for general guidance only. Although prepared with utmost care this publication is not intended to be a substitute for detailed research or the exercise of professional judgment. Therefore no liability for correctness, completeness and/or currentness will be assumed. It is solely the responsibility of the readers to decide whether and in what form the information made available is relevant for their purposes. Neither Ernst & Young GmbH Wirtschaftsprüfungsgesellschaft nor any other member of the global Ernst & Young organization can accept any responsibility. On any specific matter, reference should be made to the appropriate advisor.