Embed Size (px)

Citation preview

Lecture 2Mechanics of Trading

Primary Texts

Edwards and Ma: Chapter 2

CME: Chapters 2 & 3

Mechanics of Trading Futures Contracts

Futures Commission Merchants (FCM) Exchanges Floor Brokers Clearinghouse The Order Flow Liquidation or settling a futures position The performance bond Various Types of Futures Orders

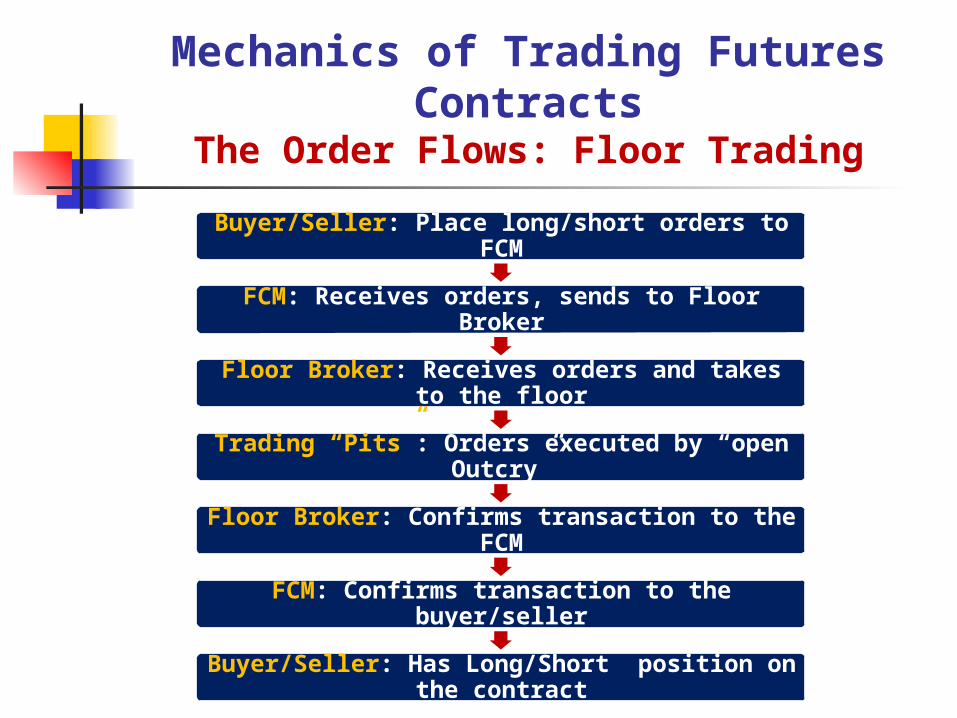

Mechanics of Trading Futures ContractsThe Order Flows: Floor Trading

Buyer/Seller: Place long/short orders to FCM

FCM: Receives orders, sends to Floor Broker

Floor Broker: Receives orders and takes to the floor

Trading “Pits”: Orders executed by “open Outcry”

Floor Broker: Confirms transaction to the FCM

FCM: Confirms transaction to the buyer/seller

Buyer/Seller: Has Long/Short position on the contract

Mechanics of Trading Futures ContractsFutures Commission Merchants (FCM)

The FCM is a central institution in the futures industry, that performs functions similar to a brokerage house in the securities industry. FCMs are regulated by Commodity Futures Trading Commission (CFTC) under the Commodity Exchange Act (CEA).

Futures traders first have to open an account at a FCM Futures traders with FCM accounts give their trading orders to an

account executive employed at the FCM The FCM executives give customer orders to floor brokers to

execute the orders on the floor of an exchange The FCM collects margin balance from the customers (traders),

maintains customer money balance, and records and reports all trading activity of its customers

Mechanics of Trading Futures ContractsMargins or Performance Bonds

Before trading a futures contract, the prospective trader must deposit funds with an FCM – the deposit serves as a performance bond and is referred to as initial margin.

The requirements are not set as a percentage of contract value. Instead they are a function of the price volatility of the commodity. A common method is to set initial margin (IPF) equal to μ + 3σ

An initial margin is a deposit to cover losses the trader may incur on a futures contract as it is marked-to-market.

A maintenance margin is a minimum amount of money that must be maintained on deposit in a trader’s account. Maintenance margin is a lesser amount than the initial margin - typically 75% of the initial margin

A margin call is a demand for an additional deposit to bring a trader’s account up to the initial margin (performance bond) level.

Traders post the funds for performance bond with their FCMs

Mechanics of Trading Futures ContractsInitial Margin

Initial Margin- An Example Each Gold futures contract is for 100 ounces of gold Assume that the current market price of gold is $400 an ounce The average daily absolute price change over the last 4 weeks is $10 an

ounce μ = $10 × 100 = $1,000

The standard deviation of the last 4 weeks’ daily absolute price change is $3 an ounce

σ = $3 × 100 = $300 Thus, the initial margin for 1 gold futures contract will be

μ + 3σ = $1,000 + 3 × $300 = $1,900 For most futures contracts, the initial margin may be 5 percent or less of the

contract’s face value.

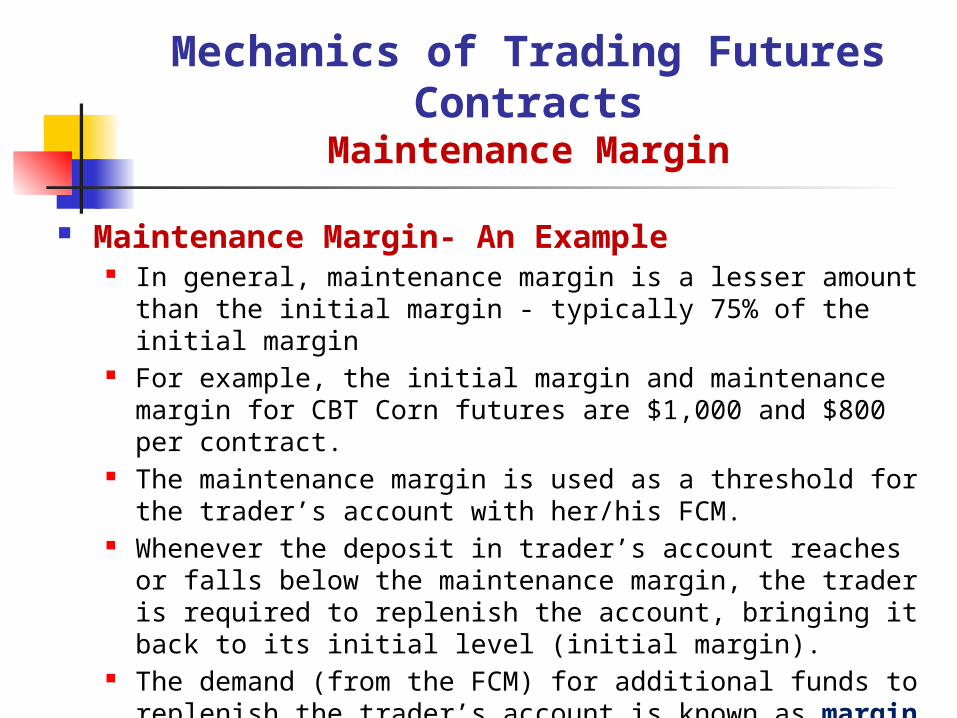

Mechanics of Trading Futures ContractsMaintenance Margin

Maintenance Margin- An Example In general, maintenance margin is a lesser amount than the initial margin

- typically 75% of the initial margin For example, the initial margin and maintenance margin for CBT Corn

futures are $1,000 and $800 per contract. The maintenance margin is used as a threshold for the trader’s account

with her/his FCM. Whenever the deposit in trader’s account reaches or falls below the

maintenance margin, the trader is required to replenish the account, bringing it back to its initial level (initial margin).

The demand (from the FCM) for additional funds to replenish the trader’s account is known as margin call.

Mechanics of Trading Futures ContractsVariation Margin

To maintain customer deposits at the level of the initial margin (or at the maintenance margin level), clearinghouses require the member FCMs to make daily adjustments to customer accounts in response to changes in the value of customer positions.

To maintain initial margin levels, FCMs require customers to make daily payments equal to the losses on their futures positions, while FCMs in turn pay to customers the gains on their positions.

These daily payments are calculated by marking-to-market customer accounts – revaluing accounts based on daily settlement prices

These daily payments are called variation margins, and must generally be made before the market opens on the next trading day.

For example, if a trader losses (gains) $150 after marking-to-market, the amount will be subtracted (deposited) to the trader’s account.

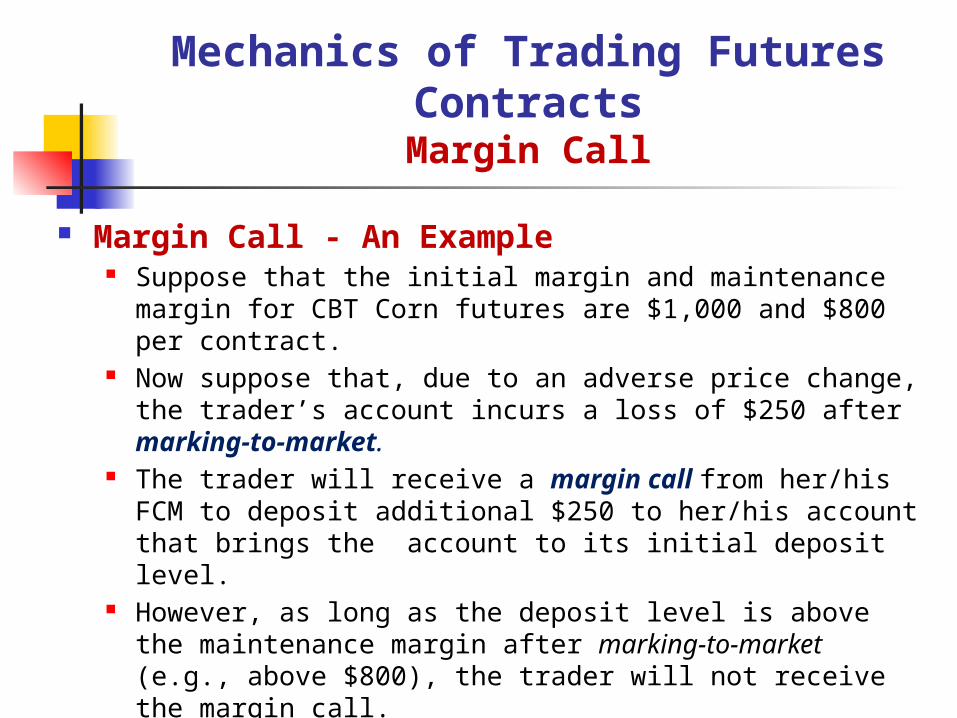

Mechanics of Trading Futures ContractsMargin Call

Margin Call - An Example Suppose that the initial margin and maintenance margin for CBT Corn

futures are $1,000 and $800 per contract. Now suppose that, due to an adverse price change, the trader’s account

incurs a loss of $250 after marking-to-market. The trader will receive a margin call from her/his FCM to deposit

additional $250 to her/his account that brings the account to its initial deposit level.

However, as long as the deposit level is above the maintenance margin after marking-to-market (e.g., above $800), the trader will not receive the margin call.

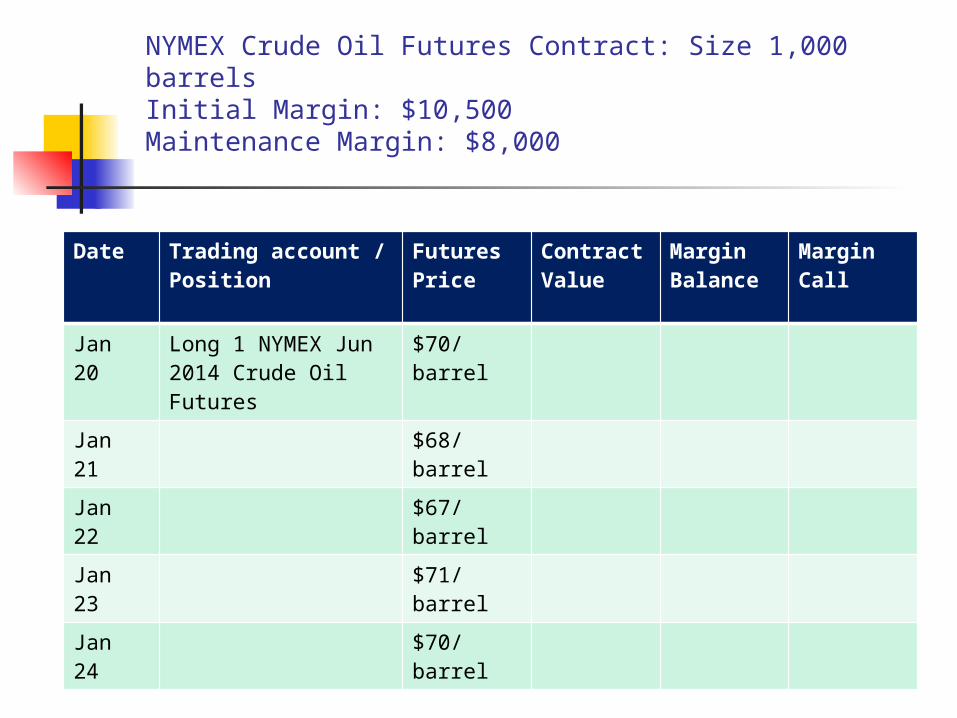

NYMEX Crude Oil Futures Contract: Size 1,000 barrelsInitial Margin: $10,500Maintenance Margin: $8,000

Date Trading account / Position

Futures Price

Contract Value

Margin Balance

Margin Call

Jan 20 Long 1 NYMEX Jun 2014 Crude Oil Futures

$70/barrel

Jan 21 $68/barrel

Jan 22 $67/barrel

Jan 23 $71/barrel

Jan 24 $70/barrel

Mechanics of Trading Futures ContractsExchanges

In order to execute customer orders, FCMs must transmit such orders to an exchange (or contract market)

Exchanges perform three functions: Provide and maintain a physical marketplace – the floor Police and enforce financial and ethical standards Promote the business interests of members

Exchanges are membership organizations whose members are either individuals or business organizations

Membership is limited to a specified number of seats – the seat price rises with the trading volume

Members receive the right to trade on the floor of the exchange, without having to pay FCM commissions

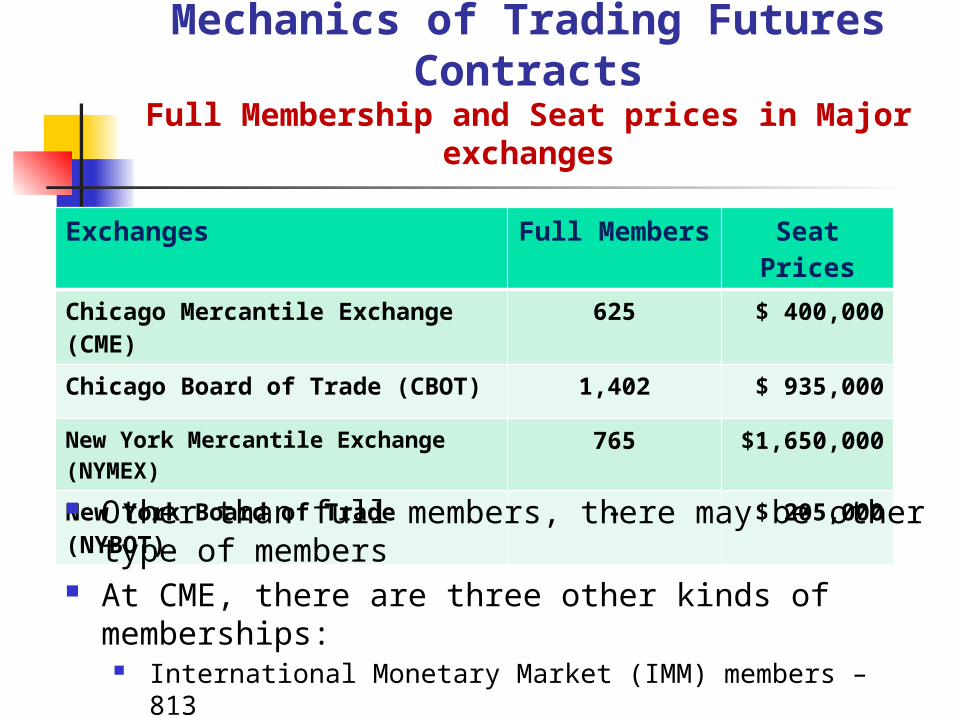

Mechanics of Trading Futures ContractsFull Membership and Seat prices in Major exchanges

Exchanges Full Members Seat Prices

Chicago Mercantile Exchange (CME) 625 $ 400,000

Chicago Board of Trade (CBOT) 1,402 $ 935,000

New York Mercantile Exchange (NYMEX) 765 $1,650,000

New York Board of Trade (NYBOT) - $ 205,000

Other than full members, there may be other type of members At CME, there are three other kinds of memberships:

International Monetary Market (IMM) members – 813 Index and Option Market (IOM) members – 1,278 Growth and Emerging Markets (GEM) members – 413

Mechanics of Trading Futures ContractsFloor Brokers

Floor brokers take the responsibility for executing the orders to trade futures contracts that are accepted by FCMs.

Self-employed individual members of the exchange who act as agents for FCMs and other exchange members

May trade customer accounts as well as their own accounts – Dual trading

Floor brokers specialize in particular commodities Floor brokers are subject to CFTC regulations

Exchange floors are organized into several different pits (physical locations), where different futures contracts are traded.

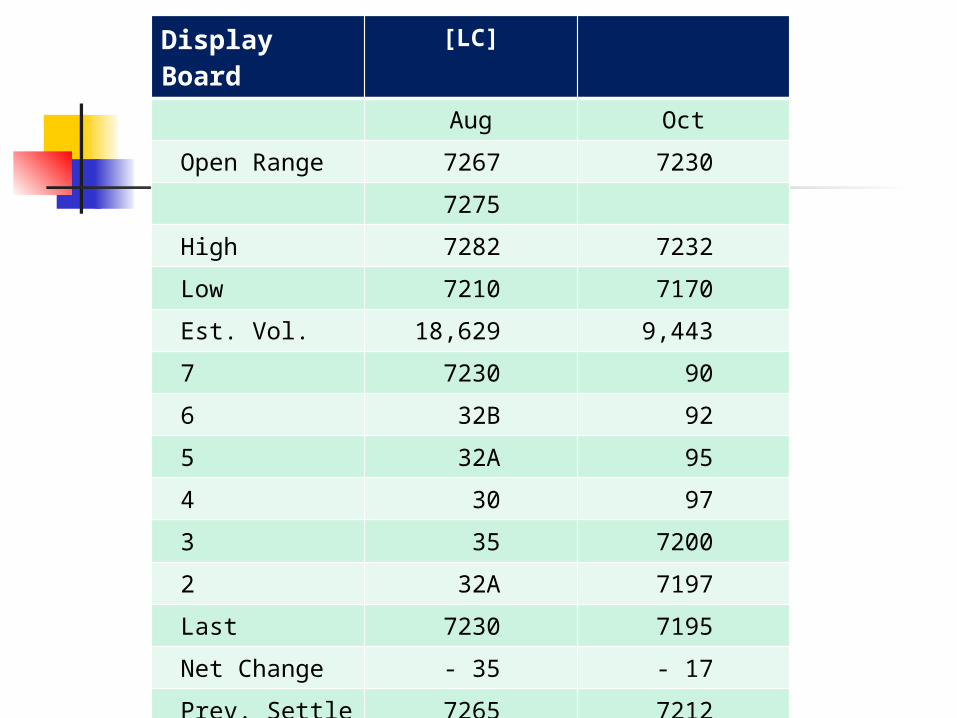

Display Board [LC]

Aug Oct

Open Range 7267 7230

7275

High 7282 7232

Low 7210 7170

Est. Vol. 18,629 9,443

7 7230 90

6 32B 92

5 32A 95

4 30 97

3 35 7200

2 32A 7197

Last 7230 7195

Net Change - 35 - 17

Prev. Settle 7265 7212

Year High 7490 7505

Year Low 6580 6250

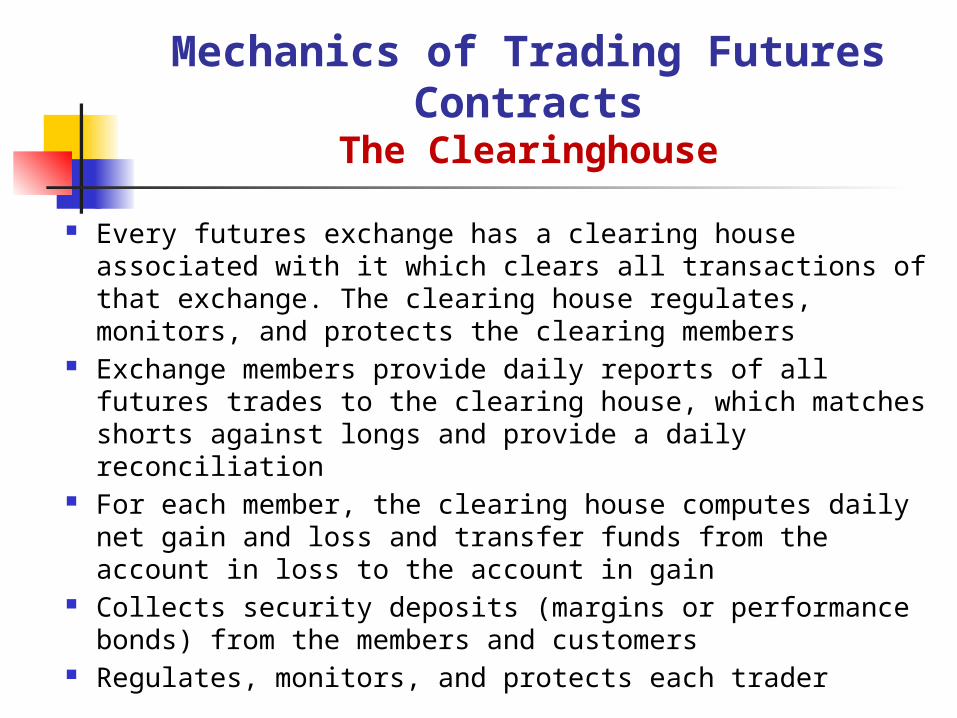

Mechanics of Trading Futures ContractsThe Clearinghouse

Every futures exchange has a clearing house associated with it which clears all transactions of that exchange. The clearing house regulates, monitors, and protects the clearing members

Exchange members provide daily reports of all futures trades to the clearing house, which matches shorts against longs and provide a daily reconciliation

For each member, the clearing house computes daily net gain and loss and transfer funds from the account in loss to the account in gain

Collects security deposits (margins or performance bonds) from the members and customers

Regulates, monitors, and protects each trader

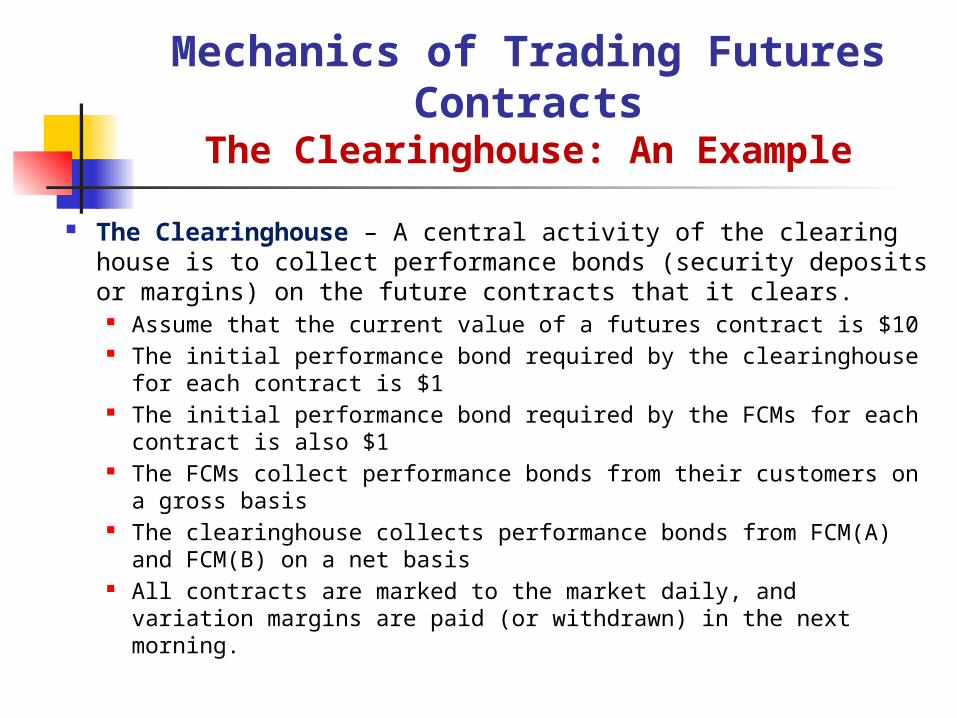

Mechanics of Trading Futures ContractsThe Clearinghouse: An Example

Nine parties: 1 Clearinghouse 2 clearing member FCMs – FCM(A) and FCM(B) 1 non-clearing FCM(C) – Omnibus Account 5 individual customers (future traders)

2 are members of FCM(A) 1 is member of FCM(B) 2 are members of FCM(C)

All transactions are assumed to be on the same futures contract The FCMs collect performance bonds on a gross basis The clearinghouse collects performance bond on a net basis The clearinghouse always has a balanced position All contracts are marked to the market daily, and variation margins are

paid (withdrawn) the next morning

Mechanics of Trading Futures ContractsThe Clearinghouse: An Example

FCM (A) – 250 Long and 230 Short – Net 20 Long Trader 1 – Member of FCM(A) – 100 Long Trader 2 – Member of FCM(A) – 90 Short FCM(C) – Member of FCM(A) – 150 Long and 140 Short

Trader 3 – Member of FCM(C) – 150 Long Trader 4 – Member of FCM(C) – 140 Short

FCM (B) – 0 Long and 20 Short – Net 20 Short Trader 5 – Member of FCM(B) – 20 Short

The Clearinghouse – 2 Members: FCM(A) and FCM(B) FCM(A) – 20 Long FCM(B) – 20 Short

Mechanics of Trading Futures ContractsThe Clearinghouse: An Example

The Clearinghouse – A central activity of the clearing house is to collect performance bonds (security deposits or margins) on the future contracts that it clears.

Assume that the current value of a futures contract is $10 The initial performance bond required by the clearinghouse for each

contract is $1 The initial performance bond required by the FCMs for each contract is

also $1 The FCMs collect performance bonds from their customers on a gross

basis The clearinghouse collects performance bonds from FCM(A) and

FCM(B) on a net basis All contracts are marked to the market daily, and variation margins are

paid (or withdrawn) in the next morning.

Mechanics of Trading Futures ContractsThe Clearinghouse: An Example

The Clearinghouse – Collects a total of $40 as initial performance bonds FCM(A) – deposits $20 for net 20 long contracts FCM(B) – deposits $20 for net 20 short contracts

FCM (A) – Collects $480 as initial performance bond – $250 from the longs and $230 from the shorts

Trader 1 –100 Long – deposits $100 for 100 long positions Trader 2 – 90 Short – deposits $90 for 90 short positions FCM(C) – Collects $290 from Traders 3 and 4 and deposits to FCM(A)

Trader 3 – 150 Long – deposits $150 for 150 long positions Trader 4 – 140 Short – deposits $140 for 140 short positions

FCM (B) –Collects $20 as initial performance bond Trader 5 –20 Short – deposits $20 for 20 short positions

Mechanics of Trading Futures ContractsThe Clearinghouse: An Example

Suppose that the market value of the futures contract increases by $1 during the same day (changes from $10 to $11). As a result,

the longs will have a profit of $1 on each contract, and The shorts will have a loss of $1 on each contract

Thus, FCMs will require a variation margin of $1 from each of their customers holding short positions

FCM(A) will require additional $230: $90 from Trader 2 and $140 from FCM© FCM(B) will require additional $20 from Trader 5

The collected funds will be passed through to customers holding long positions FCM(A) will transfer $100 to the account of Trader 1 holding 100 long positions FCM(A) will transfer $150 to the account of Trader 3 holding 150 longs through FCM© FCM(B) will transfer $20 to the clearinghouse, which in turn will transfer the fund to FCM(A)

Thus, the original level of total deposit is maintained.

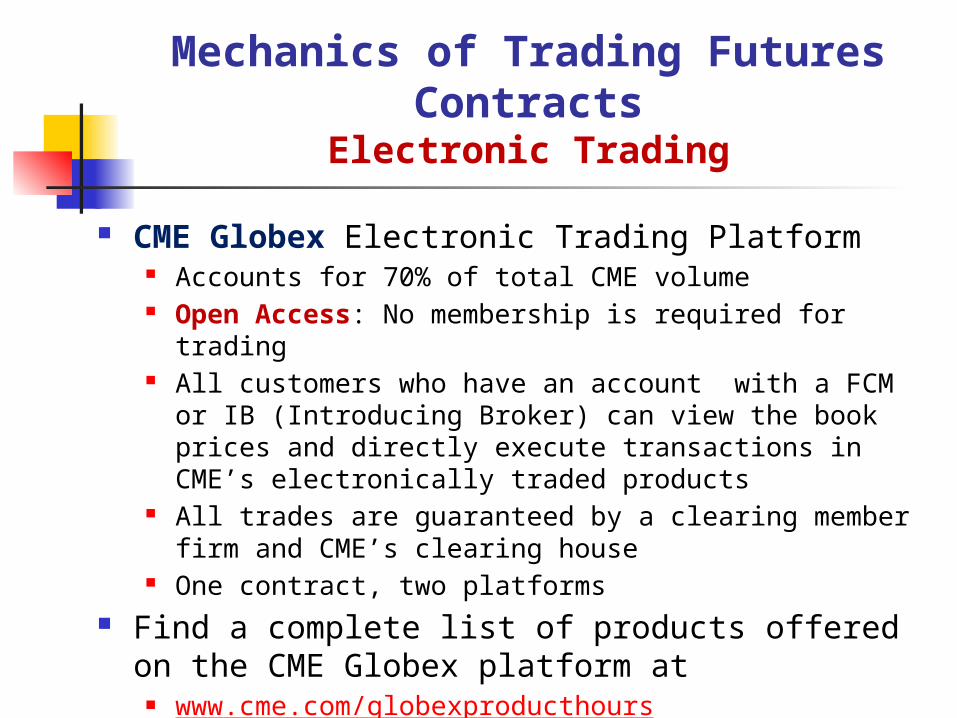

Mechanics of Trading Futures ContractsElectronic Trading

CME Globex Electronic Trading Platform Accounts for 70% of total CME volume Open Access: No membership is required for trading All customers who have an account with a FCM or IB (Introducing

Broker) can view the book prices and directly execute transactions in CME’s electronically traded products

All trades are guaranteed by a clearing member firm and CME’s clearing house

One contract, two platforms Find a complete list of products offered on the CME Globex

platform at www.cme.com/globexproducthours

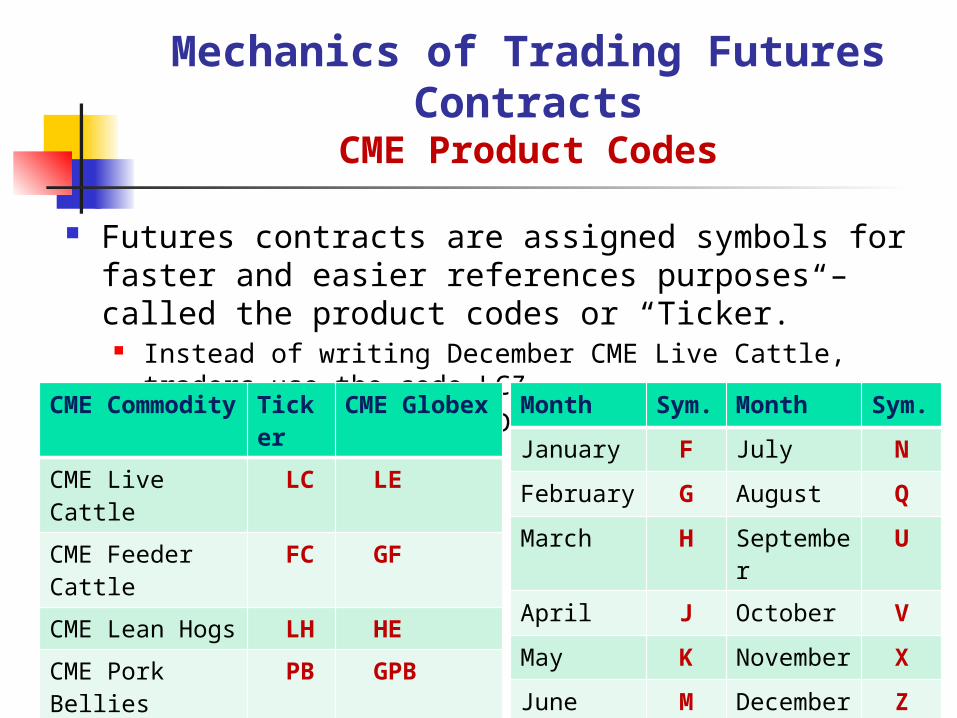

Mechanics of Trading Futures ContractsCME Product Codes

Futures contracts are assigned symbols for faster and easier references purposes – called the product codes or “Ticker.”

Instead of writing December CME Live Cattle, traders use the code LCZ LC – Live Cattle, Z - December

CME Commodity Ticker CME Globex

CME Live Cattle LC LE

CME Feeder Cattle FC GF

CME Lean Hogs LH HE

CME Pork Bellies PB GPB

CME Corn C GC

CME Wheat W ZW

CME Soybeans S ZS

Month Sym. Month Sym.

January F July N

February G August Q

March H September U

April J October V

May K November X

June M December Z

Mechanics of Trading Futures ContractsTypes of Futures Orders

A futures order refers to a set of instructions given to a FCM (or introducing broker) by a customer requesting that the broker take certain actions in the futures market on behalf of the customer.

Most frequently used orders: Market Order (MKT) – “BUY 1 Oct 2009 Live Cattle MKT”

An order placed to buy or sell at the market means that the order should be executed at the best possible price immediately following the time it is received by the floor broker on the trading floor.

In this case, the customer is less concerned about the price s/he will receive, and more concerned with the speed of execution.

Mechanics of Trading Futures ContractsTypes of Futures Orders

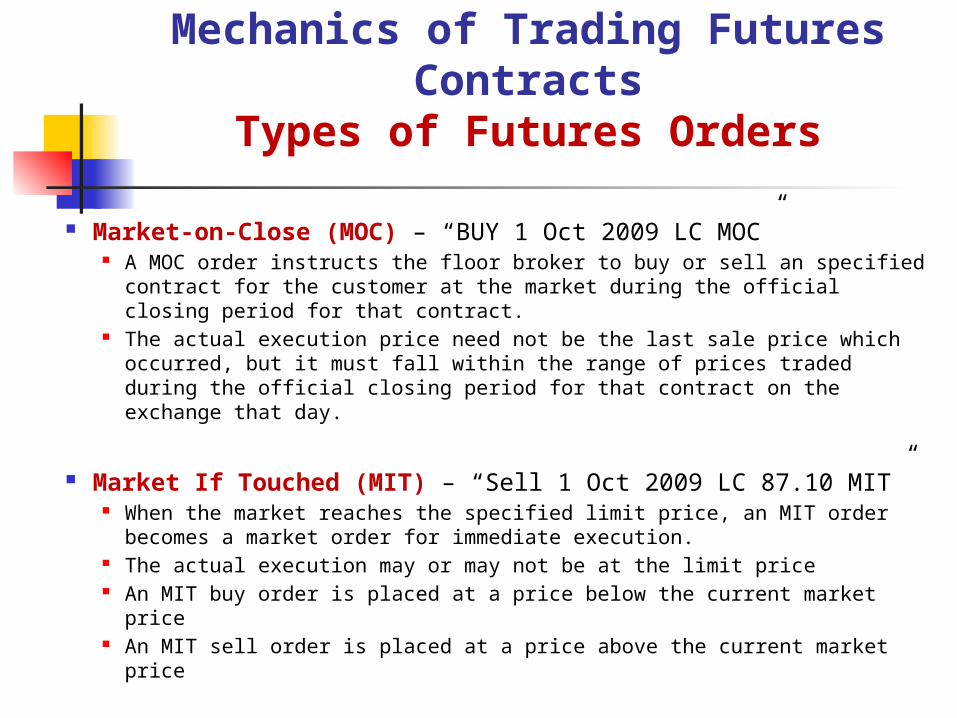

Market-on-Close (MOC) – “BUY 1 Oct 2009 LC MOC” A MOC order instructs the floor broker to buy or sell an specified contract

for the customer at the market during the official closing period for that contract.

The actual execution price need not be the last sale price which occurred, but it must fall within the range of prices traded during the official closing period for that contract on the exchange that day.

Market If Touched (MIT) – “Sell 1 Oct 2009 LC 87.10 MIT” When the market reaches the specified limit price, an MIT order becomes a

market order for immediate execution. The actual execution may or may not be at the limit price An MIT buy order is placed at a price below the current market price An MIT sell order is placed at a price above the current market price

Mechanics of Trading Futures ContractsTypes of Futures Orders

Limit Orders – “BUY 1 Oct 2009 Live Cattle at 86.50”

“Sell 1 Oct 2009 Live Cattle at 87.10”

A limit order is used when the customer wants to buy (sell) at a specified price below (above) the current market price.

The order must be filled either at the price specified on the order or at a better price.

The advantage of a limit order is that a trader knows the worst price he will receive if his order is executed.

However, the trader is not assured of execution, as with a market order.

Mechanics of Trading Futures ContractsTypes of Futures Orders

Stop Order – “Buy 1 Oct 2009 Live Cattle 86.50 Stop”

“Sell 1 Oct 2009 Live Cattle 87.10 Stop” In contrast to limit orders, a buy-stop order is placed at a price above the

current market price, and a sell-stop order is placed at a price below the current market price

Stop orders become market orders when the designated price limit is reached

The execution of simple stop orders, however, is not restricted to the designated limit price

They may be executed at any price subsequent to the designated stop order price being touched

Stop orders are often used to limit losses on open futures positions.

Mechanics of Trading Futures ContractsTypes of Futures Orders

Stop-Limit Order – “BUY 1 Oct 2009 LC 86.50 Stop Limit”

“SELL 1 Oct 2009 LC 87.10 Stop Limit”

A stop-limit order is similar to a regular stop order except that its execution is limited to the specified limit price or “better”

A broker may not be able to execute a stop-limit order in a fast market, because of the restrictions placed on the execution price.

Spread Order – “Spread BUY 1 Oct 2009 LC SELL 1 Dec 2009 LC, Oct 10 cents premium”

A spread order directs the broker to buy and sell simultaneously two different futures contracts, either at the market or at a specified spread premium.

It is necessary to specify the order as “Spread” at the beginning, and it is customary to write BUY side of each spread order first.

Mechanics of Trading Futures ContractsLiquidating or Settling a Futures Position

Three ways to close a futures position Physical delivery or cash settlement Offset or reversing trade Exchange-for-Physicals (EFP) or ex-pit transaction

Physical Delivery Physical delivery takes place at certain locations at certain times under

rules specified by a futures exchange. Imposes certain costs to traders

Storage costs Insurance costs Shipping cost, and Brokerage fees

Mechanics of Trading Futures ContractsLiquidating or Settling a Futures Position

Cash Settlement Instead of making physical delivery, traders make/receive payments at

the expiration of the contract to settle any gains or losses. At the close of trading in a futures contract, the difference between

the cash price of the underlying commodity at that time and the buying/selling price is debited/credited to the account of the long/short trader, via the clearing house and FCMs.

Available only for futures contracts that specifically designate cash settlement as the settlement procedure

Most financial futures contracts allows completion through cash settlement

Cash settlement avoids the problem of temporary shortage of supply It also makes it difficult for traders to manipulate or influence futures

prices by causing an artificial shortage of the underlying commodity

Mechanics of Trading Futures ContractsLiquidating or Settling a Futures Position

Offsetting The most common way of liquidating an open futures position The initial buyer (long) liquidates his position by selling (short) an

identical futures contract (same commodity and same delivery month) The initial seller (short) liquidates his position by buying (long) an

identical futures contract (same commodity and same delivery month) The clearinghouse plays a vital role in facilitating settlement by offset Offsetting entails only the usual brokerage costs.

Exchange-for-Physicals (EFP) A form of physical delivery that may occur prior to contract maturity An EFP transaction involves the sale of a commodity off the exchange

by the holder of the short contracts to the holder of long contracts, if they can identify each other and strike a deal.