Embed Size (px)

Citation preview

June 2009

Investor Presentation

Aston SwiftVP Investor Relations

For further information contact:

[email protected]+44 (0)20 7396 3400

Intertek Head Office25 Savile RowLondon W1S 2ES

www.intertek.com 30/06/2009

Cautionary statement regarding forward-looking statements

This presentation contains certain forward-looking statements with respect to the financial condition, results, operations and business of Intertek Group plc. These statements and forecasts involve risk and uncertainty because they relate to events and depend upon circumstances that will occur in the future. There are a number of factors that could cause actual results or developments to differ materially from those expressed or implied by these forward-looking statements and forecasts. Nothing in this presentation should be construed as a profit forecast.

June 2009

2

www.intertek.com 30/06/2009

Profile

• Origins of company go back to 1885

• Floated May 2002 on London Stock Exchange

• Entered FTSE 100 in March 2009

• Network of laboratories and offices in 110 countries

• Over 23,000 people

• ITRK.L; ITRK.LN

3

www.intertek.com 30/06/2009

What we do and what we provide our customers

4

• A leading international provider of quality and safety solutions

• Strengthen customers’ competitive position through:• Improved products• Reduced costs

• Across a balanced portfolio of industries

DivisionalRevenue

RegionalRevenue

Asia Pacific 36%Americas 34%EMEA 30%

Oil, Chemical & Agri 31%Consumer Goods 25%Commercial & Electrical 20%Analytical Services 12%Government Services 5%Minerals 4%Industrial Services 3%

Source 2008 Revenue figures

www.intertek.com 30/06/2009

Our industries

5

Supporting our customers in their global tradeOur organisation The industries we operate in What we doOur organisation What we doThe industries we operate in

Our organisation Industries we operate in What we doOur organisation Industries we operate in What we do

Testing

Inspection

Certification

Auditing

Outsourcing

Advisory

Quality Assurance

Consumer Goods

Industrial

Analytical

Commercial & Electrical

Oil, Chemical Agri

Minerals

Aerospace & AutomotiveBuilding ProductsChemicalConsumer Goods & RetailersElectrical & ElectronicEnergyFood & AgricultureGovernment & InstitutionsIT & TelecomIndustrialMedical & PharmaceuticalPetroleumToys, Games & HardlinesTextile, Apparel & Footwear

www.intertek.com 30/06/2009

0.0

0.5

1.0

1.5

2.0

2.5

SGS BVDek

ra

TUV Sud

Intertek

DNV

TUV Rheinlan

d

TUV Nord

Lloyd's

regist

er

Apave UL

Eurofin

s

ApplusGL

Core Lab

s NV

£bn

The TIC industry by revenue

www.intertek.com 30/06/2009

Intertek’s Target Market

In Trade Local Infrastructure

TIC industry

www.intertek.com 30/06/2009

0.0

0.5

1.0

1.5

2.0

2.5

SGS Intertek BV TUV Sud Dekra

£bn

Intertek target market

www.intertek.com 30/06/2009

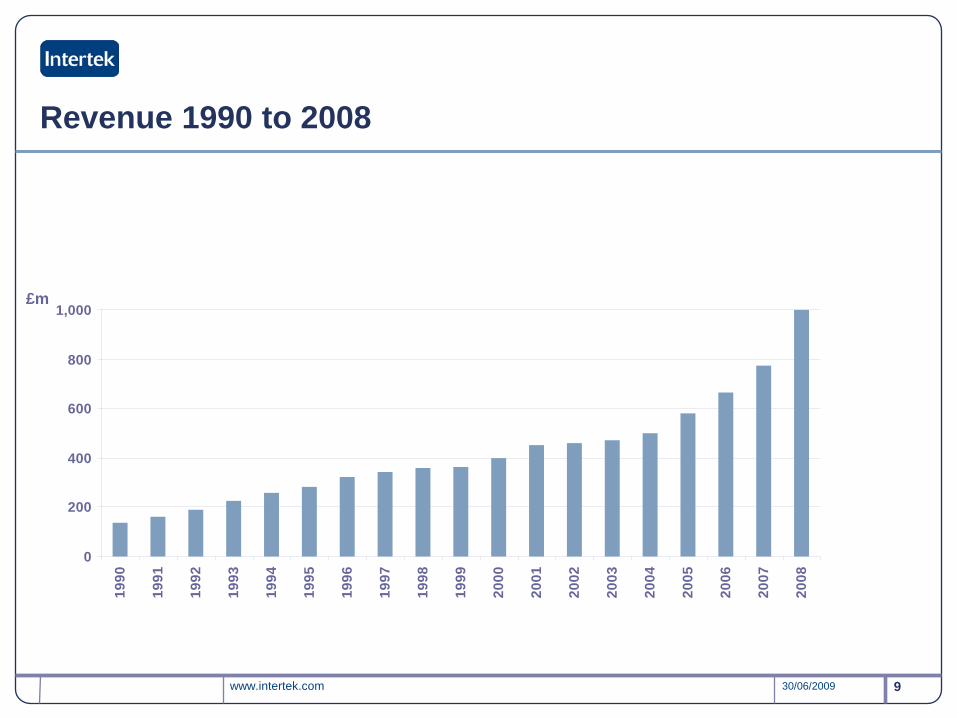

Revenue 1990 to 2008

9

0

200

400

600

800

1,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

£m

www.intertek.com 30/06/2009

Financial highlights

For the twelve months to 31 December 2008

1. Operating profit before amortisation of acquisition intangibles, goodwill impairment and non-recurring costs

Operating profit margin

Revenue

Operating profit 1 £164.7m

£1,003.5m

16.4%

+35.4% at actual

+21.2% at constant +14.8% at constant organic

+29.4% at actual

+18.7% at constant+12.3% at constant organic

+70 bps at actual

+30 bps at constant +40 bps at constant organic

10

www.intertek.com 30/06/2009

Highlights continued

Diluted adjusted EPS 2

Operating cash flow 1

Profit before tax £138.6m

£194.0m

Up 31.0%

Up 30.1%

67.1p Up 37.5%

11

1. Operating cash flow is before capital expenditure

2. Diluted adjusted earnings per share based on operating profit before amortisation of acquisition intangibles, goodwill impairment and non-recurring costs

www.intertek.com 30/06/2009

Interim management statement: 15 May 2009

Total revenue growth 42%

• 7% organic at constant exchange rates

• 5% from acquisitions

• 30% from currency

12

Expect to maintain a stable margin at prior year levels and to grow well for remainder of 2009

Drivers remain robust and are expected to continue to produce good organic revenue growth throughout the year

www.intertek.com 30/06/2009

Confident of continuing growth overall

www.intertek.com 30/06/2009

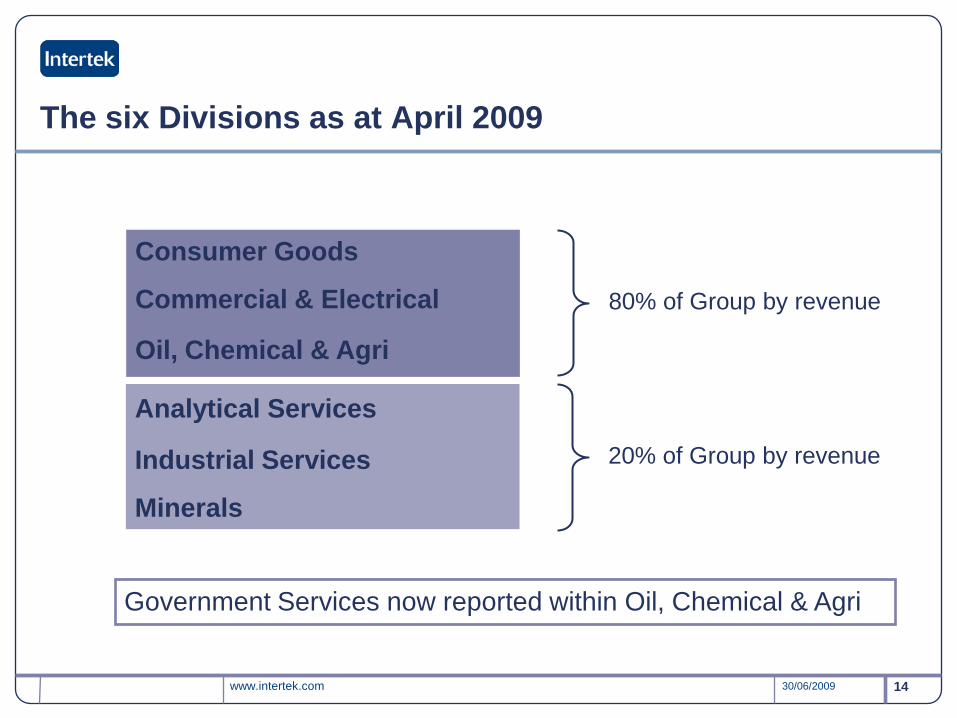

The six Divisions as at April 2009

14

Consumer Goods

Commercial & Electrical

Oil, Chemical & Agri

Analytical Services

Industrial Services

Minerals

Government Services now reported within Oil, Chemical & Agri

80% of Group by revenue

20% of Group by revenue

www.intertek.com 30/06/2009

Consumer Goods

25.0%of Group Revenue

46.0%of Group

Profit

15

Industries:

Textiles, Toys, Footwear, Hardlines, Food and Retail

Paul YaoSource 2008 Revenue & Adjusted Operating Profit

www.intertek.com 30/06/2009

£m @ constant exchange rates £m Change Organic

change

Revenue 250.4 24.1% 20.3%

Operating profit 75.7 27.9% 25.3%

Margin 30.2% +90 bps +120 bps

Results Consumer Goods

Four months to 30 April 2009:

Excellent organic revenue growth of 18%

Twelve months to 31 December 2008:

www.intertek.com 30/06/2009

Commercial & Electrical

17

20.2%of Group Revenue

17.7%of Group

Profit

Industries: Home Appliances, Lighting, Medical, Building, Industrial, IT & Telecom, HVAC/R (Heating, Ventilation, Air Conditioning & Refrigeration) and Automotive

Source 2008 Revenue & Adjusted Operating ProfitGregg Tiemann

www.intertek.com 30/06/2009

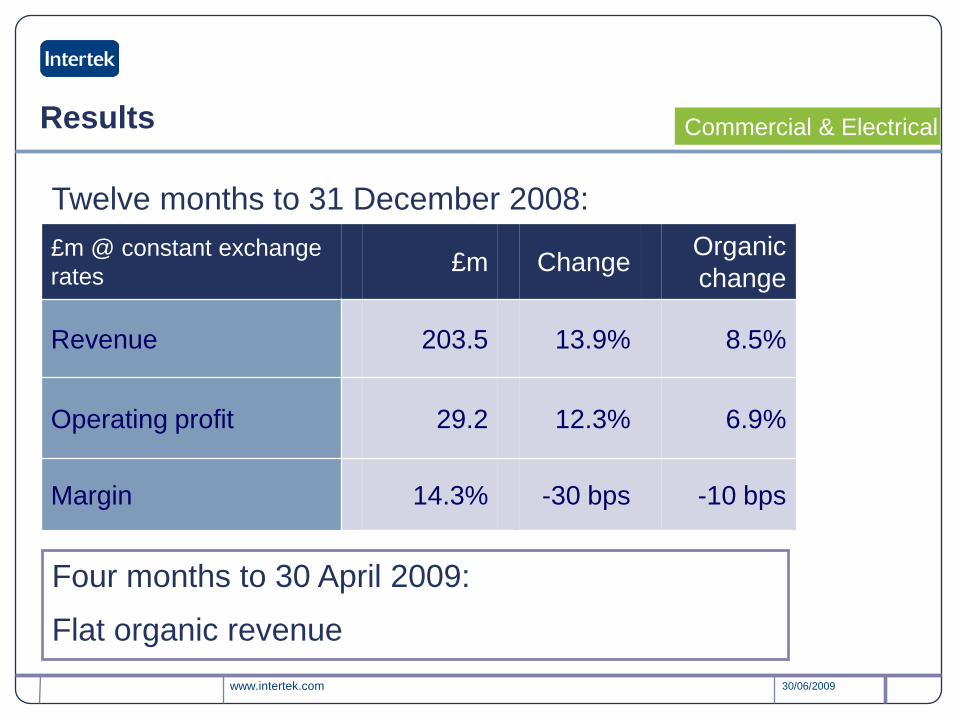

Results

£m @ constant exchange rates £m Change Organic

change

Revenue 203.5 13.9% 8.5%

Operating profit 29.2 12.3% 6.9%

Margin 14.3% -30 bps -10 bps

Commercial & Electrical

Twelve months to 31 December 2008:

Four months to 30 April 2009:

Flat organic revenue

www.intertek.com 30/06/2009

Oil, Chemical & Agri

30.7%of Group Revenue

20.3%of Group

Profit

19

Industries:

Energy, Petroleum, Chemical and Agricultural

Jay GutierrezSource 2008 Revenue & Adjusted Operating Profit

www.intertek.com 30/06/2009

Results

£m @ constant exchange rates £m Change Organic

change

Revenue 308.1 14.5% 13.3%

Operating profit 33.5 25.5% 23.0%

Margin 10.9% +100 bps +80 bps

Oil, Chemical & Agri

Twelve months to 31 December 2008:

Four months to 30 April 2009:

Started year well with 5% organic revenue growth

www.intertek.com 30/06/2009

Trading update 15 May 2009 New Divisions

• Analytical Services: 5% organic revenue growth

• Industrial Services: 15% organic revenue growth

• Minerals: 12% organic revenue growth

These division account for 20% of Group revenues

Appendix

Investor Presentation: June 2009

www.intertek.com 30/06/2009

Organic revenue growth in 2008

23

constant exchange rates 1H 2H Full Year

Consumer Goods 23.1% 18.3% 20.3%

Commercial & Electrical 9.3% 7.8% 8.5%

Oil, Chemical & Agri 15.2% 11.7% 13.3%

Government Services (6.9)% (0.4)% (3.5)%

Analytical Services (0.2)% 4.8% 2.4%

Industrial Services 6.0% 23.2% 14.9%

Minerals 58.3% 57.4% 57.8%

Sub-total New Divisions 4.5% 12.3% 8.6%

Total 12.6% 12.0% 12.3%

www.intertek.com 30/06/2009

CPSIA – 14 August 2008

Extensive new US legislation• Increase safety children’s products• Increase budget for enforcement• Increase fines and penalties• Increase whistleblower protections

Main provisions for Intertek• Mandatory third party testing before import• Lead in paint; lead in substrate• Phthalates in plastics (e.g. toys, pacifiers)

ASTM F-963 voluntary toy standard into law (choking, sharp edges, magnets, heavy metals, electrical)

Also new requirements for cribs, tracking labels, package labelling

Consumer Goods

www.intertek.com 30/06/2009

Growth through complementary expansion

2005/2006: average of £41m p.a.2007: £100m on 16 acquisitions2008: £80m on 14 acquisitions

• Food: Applica £3m, Eko Lab £3m, RQA £2m• Consumer: 4-Front £9m, Porst & Partner £2m• Upstream: CML Biotech £10m, EMIS £1m• Minerals: Philippines £3m, Ghana £2m• Ballistics: HP White £22m• Industrial: Hi-Cad £16m• Pharma: Bioclin £3m• Explosives: Epsilon £2m• Water: £2m

2009: £22m on two more Industrial acquisitions

In 2008 pro forma revenue is £1,020m

25