Embed Size (px)

Citation preview

INNOVATION

PROFESSIONALISM

INTEGRITY

CUSTOMER FOCUSED

TEAMWORK

ELEVATINGPROGRESS

TO NEW LEVELSANNUAL REPORT 2016

In an ever-evolving market environment, consumers need change. At MSIG, we understand this. Thus, we constantly strive to maintain our customer’s satisfaction through innovative services and products that cater to both personal and business needs. Powered by the values we hold dear: Customer Focused, Integrity, Teamwork, Innovation and Professionalism, our focus is to constantly move ahead by keeping up with the needs of today whilst also anticipating the needs of tomorrow.

ANNUAL REPORT 2016 3CONTENTS

Board of Directors

Directors’ Profile

Corporate Information

Senior Management

Financial Highlights

Chairman’s Statement

Directors’ Report

Statement of Financial Position

Statement of Profit or Loss and Other Comprehensive Income

Statement of Changes in Equity

Statement of Cash Flows

Notes to the Financial Statements

Statement by Directors

Statutory Declaration

Independent Auditors’ Report

04

05

09

10

12

14

21

33

34

35

36

37

89

90

91

4 ANNUAL REPORT 2016 BOARD OF DIRECTORS

BACK ROW (LEFT TO RIGHT) Hitoshi Kitagawa, Alan John Wilson, Chua Seck Guan, Datuk Seri Dr Nik Norzrul Thani bin N Hassan Thani.

FRONT ROW (LEFT TO RIGHT) Loh Guat Lan, Dato’ Mohd. Sallehuddin bin Othman, Pearl Chan Siew Cheng.

ANNUAL REPORT 2016 5

Dato’ Mohd. Sallehuddin bin Othman

Dato’ Mohd. Sallehuddin bin Othman joined MSIG Insurance (Malaysia) Bhd as an Independent Non-Executive Director in 2005 and was appointed the Chairman of the Board in March 2014. He holds professional accounting qualifi cations from the Association of Chartered and Certifi ed Accountants (ACCA) and Chartered Institute of Management Accountants (CIMA), United Kingdom. He also graduated with a Master’s Degree from City University, London in 1975. He has been registered as a Chartered Accountant with the Malaysian Institute of Accountants since 1981 and became a Fellow member of ACCA in 1983.

Dato’ Mohd. Sallehuddin began his career with brief stints at various audit fi rms in Malaysia and the United Kingdom, a statutory body and a major Government-linked company in Malaysia, before joining the Asian Development Bank based in Manila, Philippines from 1981 to 1986. Upon his return to Malaysia in 1986, Dato’ Mohd. Sallehuddin joined Permodalan Nasional Berhad, working in senior positions in corporate services and human resources until 1994. From mid-1994 to 2000, Dato’ Mohd. Sallehuddin was with UMW Holdings Berhad, initially as Executive Director, and subsequently as Group Managing Director. From 2001 until his retirement in 2006, he served as Group Managing Director of Malaysian Industrial Finance Berhad.

Post retirement, Dato’ Mohd. Sallehuddin has served as an Independent Non-Executive Director of a few companies including a foreign Islamic bank. In addition to MSIG Insurance (Malaysia) Bhd, he is currently an Independent Director of a number of companies, notably Axa Affi n Life Insurance Berhad and Bank of Tokyo-Mitsubishi UFJ (M) Berhad.

DIRECTORS’ PROFILE

6 ANNUAL REPORT 2016

Datuk Seri Dr Nik Norzrul Thani bin N Hassan Thani

Datuk Seri Dr Nik Norzrul Thani bin N Hassan Thani was appointed Director of MSIG Insurance (Malaysia) Bhd on 16 March 2009. He holds a Ph.D in Law from the School of Oriental and African Studies (SOAS), University of London and a Masters in Law from Queen Mary College, University of London. He read law at the University of Buckingham, United Kingdom. Datuk Seri Dr Nik also holds a Post-Graduate Diploma in Syariah Law and Practice (with distinction) from the International Islamic University Malaysia. A Barrister of Lincoln’s Inn and an Advocate and Solicitor of the High Court of Malaya, he was called to the Bar of England and Wales in 1985 and to the Malaysian Bar in 1986. He was previously a Visiting Fulbright Scholar, Harvard Law School and a Chevening Fellow at the Oxford Centre of Islamic Studies. Datuk Seri Dr Nik is a Fellow of the Financial Services Institute of Australasia (FINSIA). Currently, Datuk Seri Dr Nik is the Chairman and Senior Partner of Zaid Ibrahim & Co. Prior to joining Zaid Ibrahim & Co., Datuk Seri Dr Nik was with Baker & McKenzie (International Lawyers), Singapore. He is also a Director of Fraser & Neave Holdings Bhd, Al Rajhi Banking & Investment Corporation (Malaysia) Bhd, UMW Holdings Bhd, T7 Global Berhad, Ranhill Holdings Bhd, Chin Hin Group Berhad and Amanah Saham Nasional Berhad.

Hitoshi Kitagawa

Mr Hitoshi Kitagawa joined the Board of MSIG Insurance (Malaysia) Bhd as an Independent Non-Executive Director on 18 March 2014. He is currently the Managing Director of Toyota Tsusho (Malaysia) Sdn Bhd. Prior to this, he had been the Group Leader of the Techno Park Management Group of Toyota Tsusho Corporation. A graduate of Meiji University, Japan, Mr Kitagawa joined Toyota Tsusho Corporation in Japan in 1981. He has gained over 35 years of working experience in the machinery, global logistics and auto parts manufacturing global operations in his time with the company. His previous overseas posting was to Bangkok, Thailand where he worked from 2005 to 2011.

ANNUAL REPORT 2016 7

Pearl Chan Siew Cheng

Ms Pearl Chan Siew Cheng joined the Board of MSIG Insurance (Malaysia) Bhd on 18 March 2014 as an Independent Non-Executive Director. She has 31 years of experience in the Malaysian fund management industry, having managed institutional money such as government funds, insurance funds, pension funds, charitable foundations and unit trust funds throughout her career. Prior to her retirement in January 2008, Ms Chan was the Deputy Chief Executive Offi cer of CIMB Principal Asset Management for one year, after a merger between CIMB and the Southern Bank Group. Before that, she pioneered SBB Asset Management, a wholly-owned subsidiary of the Southern Bank Group, which became the fi rst commercial bank in Malaysia to have an asset management arm. She held the position of CEO for 17 years, and CEO/Chief Investment Offi cer for the fi rst 14 years, leading a team of equity and fi xed income fund managers. Before setting up SBB Asset Management, she was General Manager of Rashid Hussain Asset Management and a fund manager with Bumiputra Merchant Bankers Berhad for a total of 13 years. During her career, she also spearheaded two major corporate integration exercises in 2003 and 2007, where she successfully completed the entire integration process, involving organisation and governance structures, human resources, administration and technical systems. Ms Chan is a graduate in Economics from the University of Nottingham, England.

Loh Guat Lan

Ms Loh Guat Lan joined the Board of MSIG Insurance (Malaysia) Bhd as a Non-Independent Non-Executive Director on 1 October 2010. She is currently the Group Managing Director / Chief Executive Offi cer of Hong Leong Assurance Berhad (HLA), a subsidiary of HLA Holdings Sdn Bhd (HLAH) wholly-owned by Hong Leong Financial Group Berhad (HLFG), the fi nancial services arm of Hong Leong Group Malaysia. She is also a director of Hong Leong MSIG Takaful Berhad. Ms Loh holds a Bachelor’s degree in Nutrition Science and is a Fellow member of Life Management Institute (FLMI), Customer Service Management (CSM) and Life Offi ce Management (LOMA). She is also a Certifi ed Financial Planner (CFP) and Registered Financial Planner (RFP). Her last role prior to joining HLA as the Chief Operating Offi cer (Life Division) was Vice President & Senior Director of Agency (Malaysia). Ms Loh has over 27 years of experience in the insurance industry.

8 ANNUAL REPORT 2016

Alan John Wilson

Mr Alan Wilson has helmed the Singapore-based Asia regional holding office of Mitsui Sumitomo Insurance Company (MSIG) as Regional CEO since 2008. In his capacity as Regional CEO, he also serves as Chairman or Director (or equivalent) on the boards of 13 MSIG companies around the region. Under Mr Wilson’s leadership, the MSIG network in Asia has now expanded to 17 markets. In April 2015, Mr Wilson was honoured to be appointed as the first foreign Executive Officer, Mitsui Sumitomo Insurance Co Ltd (Japan). Mr Wilson has a sound executive management track record and has over 30 years of experience in the general insurance industry.

Prior to joining MSIG Asia, Mr Wilson was the Asia CEO at Allianz from 1999. He assumed overall responsibility for managing over 20 general, life and health insurance operations across 14 countries and later served on several boards for Allianz and for other groups such as Parkway in Asia. Mr Wilson joined Allianz from Guardian Royal Exchange Assurance Group where he was Asia Managing Director. Over the course of his 21 years there, he held various senior positions with progressive responsibilities, where he managed general and life insurance business in 11 countries.

A British national and a Singaporean Permanent Resident, Mr Wilson has lived and worked in Asia since 1982 in various places, including Hong Kong, Indonesia, Pakistan and Singapore.

Mr Wilson is also Chairman of MSIG Berhad.

Chua Seck Guan

Mr Chua Seck Guan was appointed as the Chief Executive Officer and Executive Director of MSIG Insurance (Malaysia) Bhd on 1 April 2010. A Senior Associate and Certified Insurance Professional from the Australian and New Zealand Institute of Insurance and Finance, he has vast experience in general insurance operations having served 34 years with the company. He provides the leadership and plays key strategic and operational roles in charting the company’s growth to its current revenue and profit level, and has positioned MSIG as one of the leaders in the industry. He was also instrumental in leading MSIG to be the General Insurance Company of The Year 2015, a recognition awarded by the Asia Insurance Review.

He is currently the Deputy Chairman of PIAM Management Committee and sits on the boards of Malaysia Rating Corporation Berhad (MARC), and MSIG Berhad.

ANNUAL REPORT 2016 9

BOARD NOMINATIONS COMMITTEE Chairman: Pearl Chan Siew Cheng

Members: Dato’ Mohd. Sallehuddin bin Othman

Datuk Seri Dr Nik Norzrul Thani bin N Hassan Thani Hitoshi Kitagawa Alan John Wilson

BOARD COMPLIANCE & RISK MANAGEMENT COMMITTEE

Chairman: Datuk Seri Dr Nik Norzrul Thani bin N Hassan Thani

Members: Dato’ Mohd. Sallehuddin bin Othman Hitoshi Kitagawa Pearl Chan Siew Cheng

BOARD INVESTMENT COMMITTEE

Chairman: Pearl Chan Siew Cheng

Members: Dato’ Mohd. Sallehuddin bin Othman Loh Guat Lan Chua Seck Guan Koichi Nagase

COMPANY SECRETARIES

Lee Wai Ngan(LS00184)Chan Toye Ying(LS00185)

REGISTERED OFFICE

Plaza 138,Suite 18.03, 18th Floor,138, Jalan Ampang50450 Kuala Lumpur.

BOARD REMUNERATION COMMITTEE

Chairman: Hitoshi Kitagawa

Members: Dato’ Mohd. Sallehuddin bin Othman Datuk Seri Dr Nik Norzrul Thani bin N Hassan Thani

BOARD AUDIT COMMITTEE

Chairman: Datuk Seri Dr Nik Norzrul Thani bin N Hassan Thani

Members: Dato’ Mohd. Sallehuddin bin Othman Hitoshi Kitagawa Pearl Chan Siew Cheng

SHARE REGISTRAR

System Associates Sdn. Bhd.Plaza 138,Suite 18.03, 18th Floor,138 Jalan Ampang,50450 Kuala Lumpur.

EXTERNAL AUDITOR

KPMG PLT

TECHNICAL ADVISORS

Tetsunori ShojiBachelor of Business Adminstration

Nobuhiro OjioBachelor of Commerce

Kensuke HiraiBachelor of Laws

Yusuke TakamuraBachelor of Laws

Yoshihiro ShibuyaBachelor of LawsYu OiBachelor of Economics

CORPORATE INFORMATION

10 ANNUAL REPORT 2016

CHIEF EXECUTIVE OFFICERChua Seck GuanANZIIF (Snr Assoc)

DEPUTY CHIEF EXECUTIVE OFFICERKoichi NagaseBachelor of Laws

TECHNICAL ADVISORTetsunori ShojiBachelor of Business Administration

CHIEF OPERATING OFFICERJennifer Hsu Chin FenLLB (Hons)

SENIOR VICE PRESIDENTCompliance & EnterpriseRisk ManagementChin Kong MengCA (M), FCPA (Aust), CFP

EXECUTIVE VICE PRESIDENTFinance, Planning & ActuarialSoh Lai SimCA (M), CPA, FCTIM

SENIOR VICE PRESIDENTIT, Digital, E-Commerce & Business IntelligenceChin Jee GwanBSc (Hons), MSc

SENIOR MANAGEMENT

ANNUAL REPORT 2016 11

VICE PRESIDENTBrokingAng Yien ChiaB.Sc (BA), DMII

VICE PRESIDENTFranchise & Direct CorporateVictor Chen Fan LoanANZIIF (Assoc) CIP, DMII

SENIOR VICE PRESIDENTClaims & ReinsuranceLoke Phaik PohFCII, FMII, Chartered Insurer

SENIOR VICE PRESIDENTBranch Operations Support, PSD & AdministrationJessica Teh Siew Kheng

SENIOR VICE PRESIDENTAgencyTeoh Guan HuatMBA, ANZIIF (Snr Assoc) CIP, DMII

SENIOR VICE PRESIDENTUnderwriting & BancassuranceTan Poh SuatB.Sc (Hons), ACII, AMII, Chartered Insurer

12 ANNUAL REPORT 2016

Composition of 2016 Gross Premium Total: RM1.5 Billion

2000 400 600 800 1000 1200 1400 1600

26% 43% 8% 23%

23%7%25% 45%

2016

2015

2014

2013

2012

RM (million)

Fire Motor Marine, Aviation & Transit Miscellaneous

Year Ended 31 December

Paid-up Share Capital

Total Equity

Total Assets

Gross Premium

Net Premium

Underwriting Surplus

Investment & Other Income

Profit Before Taxation

Profit After Taxation

Earning Per Share (RM)

NTA Per Share (RM)

Total Workforce

333,143

2,071,236

3,960,331

1,326,297

1,037,183

135,709

96,396

232,105

182,103

0.55

2.79

1,115

333,143

2,189,496

4,194,057

1,425,924

1,119,674

168,492

88,325

256,817

203,851

0.61

3.15

1,119

333,143

2,298,400

4,344,034

1,486,662

1,203,263

193,165

85,209

278,374

214,960

0.65

3.47

1,133

333,143

2,401,381

4,632,954

1,535,370

1,233,630

173,536

88,299

261,835

200,100

0.60

3.78

1,149

333,143

2,547,953

4,612,182

1,522,503

1,227,640

206,749

106,801

313,550

248,800

0.75

4.22

1,160

2012RM’000

2013RM’000

2014RM’000

2015RM’000

2016RM’000

FINANCIAL HIGHLIGHTS

6%45%26% 23%

7%25% 45% 23%

23%7%27% 44%

ANNUAL REPORT 2016 13

2012 2013 2014 2015 2016

PROFIT BEFORE TAXATIONINVESTMENT & OTHER INCOME

TOTAL EQUITY TOTAL ASSET

RM (million)RM (million)

RM (million) RM (million)

275

300

325

25090

225

200

2700

2400

4800

2100

4200

175

1800

3600

150

15003000

125

12002400

100

900 1800

75

600 1200

50

25

300 600

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

2012 2013 2014 2015 2016

UNDERWRITING SURPLUSRM (million)

220

200

180

160

140

120

100

80

60

40

20

0

GROSS PREMIUMRM (million)

1540

1400

1260

1120

980

840

700

560

420

280

140

0

0

110

100

80

70

60

50

40

30

20

10

0

0 0

CHAIRMAN’S STATEMENT14 ANNUAL REPORT 2016

“On Behalf Of The Board Of Directors, It Is My Pleasure To Present The Annual Report And Financial Statements Of The Company For The Year Ended 31 December 2016.

“Dato’ Mohd. Sallehuddin bin Othman

Chairman

Bagi Pihak Lembaga Pengarah, Saya Dengan Sukacitanya Mengemukakan Laporan Tahunan Serta Penyata Kewangan Syarikat Bagi Tahun Berakhir 31 Disember 2016.

ANNUAL REPORT 2016 15

FINANCIAL REVIEW

The 2016 financial year recorded a Gross Written Premium of RM1.52 billion against RM1.54 billion in the previous year. This contraction of RM12.9 million (0.8%) can be attributed primarily to the Motor Class which experienced a significant reduction in vehicle sales of 13% year-on-year, continued rate softening and intense competition as insurers strive for larger market share ahead of the Motor Insurance Liberalisation in July 2017. Weak consumer sentiment and sluggish external trade amidst growing uncertainties in the global environment also affected the market.

Despite the decrease in GWP, Underwriting Surplus was up by RM33.2 million (19.1%) from RM173.5 million in 2015 to RM206.7 million, with a Combined Operating Ratio of 83.8%. The Underwriting Surplus, the highest in 5 years, marks a milestone for surpassing the RM200 million and is underpinned by diligent underwriting discipline and robust claims management.

The Company’s total investment size amounted to RM2.7 billion. Investment Income of RM104.3 million registered a double-digit increase of 13.3%, translating into a RM12.3 million increase over 2015. This is another record, crossing the RM100 million level for the first time.

Realised investment profit was also higher at RM9.5 million compared to RM3.8 million in the previous year. However, this gain was negated by the provision for impairment loss on investments amounting to RM7.6 million from equities.

The Profit Before Tax of RM313.6 million and Profit After Tax of RM248.8 million reflect a net earnings per share of 74.7 cents.

A final dividend of RM99.9 million for financial year 2015 was declared in June 2016.

As at end 2016, the Company’s Total Assets, including Goodwill, was RM4.6 billion.

TINJAUAN KEWANGAN

Tahun kewangan 2016 mencatatkan Premium Bertulis Kasar (PBK) sebanyak RM1.52 bilion berbanding laporan tahun lepas sebanyak RM1.54 bilion. Faktor-faktor utama susutan sebanyak RM12.9 juta (0.8%) adalah disebabkan oleh Kelas Motor yang mengalami kadar pengurangan ketara sebanyak 13% dalam penjualan kenderaan semasa, kadar mendatar yang berterusan, serta persaingan sengit di mana syarikat-syarikat insurans lebih menumpukan kepada pasaran yang lebih besar ke arah Liberalisasi Insurans Motor pada Julai 2017. Sentimen pengguna yang lemah serta dagangan luar yang perlahan dengan keadaan global yang tidak menentu juga mempengaruhi keadaan pasaran.

Biarpun terdapat penyusutan dalam PBK, Lebihan Taja Jamin meningkat sebanyak RM33.2 juta (19.1%) dari RM173.5 juta pada 2015, ke RM206.7 juta dengan Kadar Kendalian Digabungkan sebanyak 83.8%. Lebihan Taja Jamin pada 2016 sebanyak RM206.7 juta merupakan rekod tertinggi sepanjang 5 tahun dan merupakan sebuah pencapaian positif, melepasi tanda aras RM200 juta.Kejayaan ini tentu sekali berjaya dicapai melalui penajajaminan yang berdisiplin serta pengurusan tuntutan yang cekap.

Saiz jumlah pelaburan Syarikat berkembang sebanyak RM2.7 bilion manakala Pendapatan Pelaburan sebanyak RM104.3 juta mencatatkan kenaikan sebanyak 13.3%, iaitu RM12.3 juta berbanding tahun 2015. Sekali lagi mencatatkan rekod, melepasi aras RM100 juta untuk kali pertama.

Keuntungan pelaburan terealis juga mencatat angka yang lebih tinggi dengan RM9.5 juta berbanding RM3.8 juta pada tahun lepas. Walau bagaimanapun, peningkatan ini disangkalkan akibat daripada peruntukan untuk kerugian ke atas kemerosotan nilai pelaburan yang bernilai sebanyak RM7.6 juta daripada ekuiti.

Keuntungan Sebelum Cukai sebanyak RM313.6 juta dan Keuntungan Selepas Cukai sebanyak RM248.8 juta menjanakan perolehan bersih setiap saham dengan nilai 74.7 sen.

Dividen akhir sebanyak RM99.9 juta bagi tahun kewangan 2015 diisytiharkan pada Jun 2016.

Akhir 2016, Jumlah Aset Syarikat, termasuk Muhibah bernilai sebanyak RM4.6 bilion.

16 ANNUAL REPORT 2016

OPERATIONAL REVIEW

Customer Focused InnovationWe were honoured to have our Prime PA product,

launched in 2015, awarded 2nd place in the Regional Innovation Award organised by our Regional Office. To continue with our focus on product innovation and improvement, the year in review witnessed the launch of Out-of-Pocket Expenses Insurance (OOPS) to cover Inconvenience Allowances for Flood and Vehicle laid-up for repairs, a common pain point for consumers when their cars are under repair. We also reinforced our Travel Insurance with enhanced benefits such as Adventurous Activity to reflect the trend of participating in adventurous past-times like bungee jumping, hot air balloon rides and other activities as part of the travel experience. This saw our Travel product register a RM2.6 million growth for 2016.

Innovation was also the focus of our Customer Contact Centre which receives 7,000 calls per month for all classes of products and distribution channels. The implementation of a Process Innovation programme resulted in a 66% improvement in productivity, improved calls pick-up rate to 80%, a customer satisfaction rate of 93% and an impressive 83% of customers surveyed willing to be a MSIG brand “ambassador” by introducing MSIG to their family and friends.

In addition, we continued our Digitalisation journey with the introduction of two new systems during the year in review :

n Business Management System – streamlining and automating processes across key functions and lines of business to improve efficiency and to enable the business to quickly respond to changing market needs, competitive forces, growth initiatives and customer demands.n Risk Survey Application – digitalising the pre-acceptance risk survey process on mobile devices for risk surveyors to use out in the field and thus, bring about speedier turnaround time and increased productivity.

TINJAUAN OPERASI

Inovasi Yang Menumpukan Kepada PelangganKami merasa amat bangga dengan produk Prime PA

kami yang telah dilancarkan pada 2015 berjaya merangkul tempat kedua dalam Anugerah Inovasi Peringkat Serantau oleh Pejabat Serantau kami. Bagi meneruskan kecemerlangan proses inovasi dan penambahbaikan produk, Insurans Belanja Tunai Langsung (OOPS) telah dilancarkan pada 2016 untuk memberikan Elaun Kesulitan untuk Banjir dan Kenderaan yang sedang diselenggarakan di bengkel, yang mana menjadi satu keperluan bagi pihak pelanggan setiap kali kenderaan mereka dibaiki akibat kemalangan. Kami juga turut memperkenalkan Insurans Perjalanan yang telah dipertingkatkan dengan manfaat untuk Aktiviti Yang Mencabar bagi memenuhi trend pelanggan yang mengambil bahagian dalam aktiviti-aktiviti mencabar seperti melompat bungee, menaiki belon panas dan pelbagai lagi aktiviti lain yang mereka nikmati ketika melancong. Dengan ini, produk Insurans Perjalanan kami telah mencatatkan peningkatan jualan sebanyak RM2.6 juta pada tahun 2016.

Inovasi juga adalah fokus Pusat Panggilan Pelanggan kami yang menerima 7,000 panggilan setiap bulan untuk semua kelas produk serta saluran edaran. Pelaksanaan program Proses Inovasi berjaya menghasilkan peningkatan produktiviti sebanyak 66%, peningkatan kadar menjawab panggilan sebanyak 80% serta kadar kepuasan pelanggan sebanyak 93% dan melalui kaji selidik, sebanyak 83% pelanggan bersetuju untuk memperkenalkan MSIG kepada keluarga dan rakan-rakan mereka.

Di samping itu, perjalanan Digital kami diteruskan dengan pengenalan 2 sistem baru seperti berikut:

n Sistem Pengurusan Perniagaan – menyelaraskan dan mengautomatikkan proses bagi fungsi-fungsi utama dan aliran perniagaan bagi mempertingkatkan kadar kecekapan dan membolehkan perniagaan bertindak pantas terhadap perubahan mengikut kehendak pasaran, daya saing, inisiatif pertumbuhan dan permintaan pelanggan.

n Aplikasi Tinjauan Risiko – Pendigitalan proses pra-penerimaan tinjauan risiko pada peranti mudah alih untuk digunakan oleh jurunilai risiko, dapat mencapai putaran kerja lebih pantas dan meningkatkan produktiviti.

ANNUAL REPORT 2016 17

Corporate Social Responsibility

On a daily basis, much of the food that we throw away can still be consumed. To help reduce wastage whilst simultaneously doing our bit for the underprivileged and the environment, MSIG embarked on a partnership with Food Aid Foundation which saw staff and intermediaries connect with local communities in transforming excess food to feed the needy. Every alternate Saturday from March to July 2016, 213 staff volunteered, cooked excess food, packed and distributed to 1,300 children and senior citizens in 20 underprivileged homes.

Our CSR outreach programme also included talks by NGOs such as St John Ambulance, UNICEF and The National Autism Society of Malaysia to staff and agents.

Preparation for Liberalisation

Following the release by Bank Negara Malaysia (BNM) of the Phased Liberalisation for Motor and Fire Policy Document outlining the framework, timelines and expectations of BNM when the industry moves from the current tariff environment to risk based pricing on 1 July 2017, plans and strategies pertaining to pricing, products, systems, people, sales and distribution were effected in preparation for this major industry change.

Liberalisation will also provide opportunities for Insurers to offer innovative products from the current restrictive tariff environment.

The Board provided guidance and support to the Management in the setup of the various committees and projects, and overall liberalisation plan.

Tanggungjawab Sosial Korporat

Ramai yang masih tidak sedar bahawa kebanyakan sisa makanan yang kita buang setiap hari masih boleh dimakan. Bagi mengelakkan aktiviti pembaziran terus berlaku sambil menyumbang kepada penduduk yang tidak berkemampuan serta alam sekitar, MSIG telah berkerjasama dengan Food Aid Foundation bagi menghubungkan kakitangan dan pengantara kami kepada komuniti tempatan dengan menyalurkan makanan lebihan kepada mereka yang memerlukan. Seramai 213 staf secara sukarela menyumbangkan bantuan pada setiap selang Sabtu dari Mac hingga Julai 2016 dengan memasak, membungkus dan mengagihkan makanan kepada 20 rumah kebajikan yang menempatkan 1,300 orang kanak-kanak dan warga emas.

Program ‘CSR’ kami juga termasuk ceramah-ceramah oleh ‘NGO’ seperti St John Ambulance, UNICEF dan The National Autism Society of Malaysia bagi kakitangan dan ejen-ejen.

Persediaan Menghadapi Liberalisasi

Terbitan Dokumen Polisi Fasa Liberalisasi bagi Motor dan Kebakaran oleh Bank Negara Malaysia (BNM) yang merangkumi rangka kerja, garis masa dan jangkaan BNM apabila industri berubah dari keadaan tarif semasa hinggalah harga berdasarkan risiko yang bermula pada 1 Julai 2017, memberi kesan kepada pelan-pelan dan strategi-strategi berkaitan harga, produk, sistem, tenaga kerja, jualan dan edaran dalam persediaan menghadapi perubahan besar industri ini.

Liberalisasi juga membuka peluang kepada syarikat-syarikat Insurans untuk menawarkan produk-produk inovatif berbanding dengan keadaan tarif semasa.

Lembaga Pengarah telah memberikan panduan dan menyokong Pihak Pengurusan dalam penubuhan pelbagai komiti dan projek, serta pelan liberalisasi secara keseluruhannya.

18 ANNUAL REPORT 2016

OUTLOOK

Looking ahead, 2017 remains challenging amidst global economic uncertainties, an impending increase in US interest rates and the weakening Ringgit. On the local front, the government has projected a 4% to 5% GDP growth, which augurs well for the industry.

Despite the subdued outlook, there are sectors which are expected to spur growth, e.g. transportation-related Infrastructure projects, new Foreign Direct Investments and a recovery in commodity prices, and which are likely to benefit the Property, Engineering, Marine and Liability classes of our Business. There are also opportunities arising from new emerging risks such as cyber activities, ridesharing, terrorism and the deployment of disruptive technologies (Fintech and Insurtech).

Another possible game-changer for the general insurance industry is changing consumer attitude towards online purchases with the foreseeable future likely to see the inevitable arrival of similar purchasing trends. The recent growth of insurance aggregators or motor pricing comparison sites, online platforms, customer choices and conveniences is an indication that Millennials and Gen Y users will be the drivers of such behavioural change and MSIG needs to rise up to these consumers’ changing trends.

Notwithstanding the above challenges, I am confident 2017 and beyond will be exciting and rewarding with our continued focus on the Company’s core values of Customer Focused, Integrity, Teamwork, Innovation and Professionalism.

ACKNOWLEDGEMENT

On behalf of the Board, I would like to express my gratitude and appreciation to our valued intermediaries, clients and business partners for their strong support in making 2016 another outstanding year.

We also wish to extend our appreciation to the Senior Management Team and our staff for their dedication and commitment to continuous improvements in line with the Company’s core values.

The Board would also like to thank Bank Negara Malaysia and the relevant Regulatory Authorities for their guidance and advice.

Lastly, I would like to thank my fellow Directors for their valuable inputs and contributions.

Dato’ Mohd. Sallehuddin bin Othman Chairman

MELANGKAH KE HADAPAN

Melihat ke hadapan, 2017 pastinya merupakan tahun yang mencabar pada ketika keadaan ekonomi yang tidak menentu, peningkatan kadar faedah AS yang bakal berlaku dan Ringgit yang semakin rendah. Kerajaan telah menjangkakan pertumbuhan KDNK sebanyak 4% hingga 5% yang merupakan satu tanda baik buat industri.

Walaupun masa hadapan yang tidak menjaminkan, terdapat juga sektor-sektor yang dijangka berkembang pesat, contohnya projek infrastruktur berkaitan kenderaan, Pelaburan Langsung Asing yang baru dan harga komoditi yang kian pulih yang mana akan membantu sektor perniagaan insurans seperti kelas Hartanah, Kejuruteraan, Marin dan Liabiliti. Terdapat juga peluang-peluang dari kemunculan risiko baru seperti aktiviti siber, berkongsi kenderaan (ridesharing), keganasan dan perkembangan teknologi-teknologi disruptif (Fintech dan Insurtech).

Satu lagi faktor yang menyumbang kepada perubahan ketara dalam industri insurans am adalah sikap pelanggan yang kini lebih menjurus ke arah pembelian atas talian yang mana bakal menyaksikan trend yang serupa dalam industri ini. Perkembangan laman pengumpulan data (aggregator) insurans atau perbandingan harga insurans motor, platform online, pilihan dan kemudahan pelanggan jelas menunjukkan pengguna Milennial dan Gen Y bakal menjadi penggerak dalam perubahan ini. Oleh itu, MSIG perlu meningkatkan usaha untuk memenuhi trend perubahan keperluan pelanggan ini.

Walaupun terdapat pelbagai rintangan seperti yang disebutkan, saya yakin tahun 2017 dan seterusnya bakal menjanjikan pengalaman yang menarik dan memberi ganjaran seiring dengan fokus terhadap nilai-nilai utama Syarikat iaitu Tumpuan terhadap Pelanggan, Integriti, Kerjasama Berpasukan, Inovasi dan Profesionalisme.

PENGHARGAANBagi pihak Lembaga Pengarah, saya ingin mengucapkan

terima kasih dan menyampaikan penghargaan kepada para perantara, pelanggan dan rakan niaga kami yang amat dihargai atas sokongan padu mereka menjadikan tahun 2016 satu lagi tahun yang cemerlang.

Kami juga ingin menyampaikan penghargaan kepada Kumpulan Pengurusan Kanan dan pekerja atas dedikasi dan komitmen mereka yang berterusan seiring dengan nilai-nilai teras syarikat.

Lembaga Pengarah juga ingin mengucapkan terima kasih kepada Bank Negara Malaysia dan Pihak Berkuasa yang berkenaan atas panduan dan nasihat mereka.

Akhir kata, saya ingin mengucapkan ribuan terima kasih kepada rakan-rakan Pengarah saya di atas nasihat dan sumbangan mereka yang berharga.

Dato’ Mohd. Sallehuddin bin Othman Pengerusi

Financial Statements

ANNUAL REPORT 2016 21

for the year ended 31 December 2016

DIRECTORS’ REPORT

The Directors have pleasure in submitting their report together with the annual audited financial statements of the Company for the financial year ended 31 December 2016.

Principal activities

The Company is principally engaged in the underwriting of all classes of general insurance business. There has been no significant change in the nature of these activities during the financial year.

Ultimate holding company

The Company is a subsidiary of Mitsui Sumitomo Insurance Co., Ltd. and MS&AD Insurance Group Holdings, Inc. is parent company of Mitsui Sumitomo Insurance Co., Ltd., both companies are incorporated in Japan. MS&AD Insurance Group Holdings, Inc. is regarded by the Directors as the Company’s ultimate holding company, during the financial year and until the date of this report.

Financial results RM’000Profit for the year 248,800

Dividends

Since the end of the previous financial year, the Company paid a final dividend of 30 sen per ordinary share totalling RM99,943,000 in respect of the year ended 31 December 2015 on 5 July 2016.

The final ordinary dividends recommended by the Directors in respect of the financial year ended 31 December 2016 is 25 sen per ordinary share totalling RM83,286,000. Such dividend, if approved, will be accounted for in the shareholders’ equity as an appropriation of retained earnings during financial year ending 31 December 2017.

Directors of the Company

Directors who served during the financial year until the date of this report are:

Dato’ Mohd. Sallehuddin bin Othman Datuk Seri Dr Nik Norzrul Thani bin N Hassan Thani Mr Hitoshi Kitagawa Ms Pearl Chan Siew Cheng Ms Loh Guat Lan Mr Alan John Wilson Mr Chua Seck Guan

Directors’ interests in shares

The interests and deemed interests in the shares of the Company and of its related corporations of those who were Directors at financial year end (including the interests of the spouses or children of the Directors who themselves are not Directors of the Company) as recorded in the Register of Directors’ Shareholdings are as follows:

Number of ordinary shares At At 1.1.2016 Bought Sold 31.12.2016Shareholdings in which Director has direct interest

Related companies: BPI/MS Insurance Corporation Mr Alan John Wilson 1 - - 1 Ueang Mai Co Ltd Mr Alan John Wilson 1 - - 1 Yardhimar Company Ltd Mr Alan John Wilson 1 - - 1

None of the other Directors holding office at the end of the financial year had any interest in the ordinary shares of the Company or its related corporations during the financial year.

22 ANNUAL REPORT 2016

Directors’ benefits

Since the end of the previous financial year, no Director of the Company has received nor become entitled to receive any benefit (other than a benefit included in the aggregate amount of remuneration received or due and receivable by Directors as shown in the financial statements or the fixed salary of a full time employee of the Company or of related corporations) by reason of a contract made by the Company or a related corporation with the Director or with a firm of which the Director is a member, or with a company in which the Director has a substantial financial interest.

There were no arrangements during and at the end of the financial year which had the object of enabling Directors of the Company to acquire benefits by means of the acquisition of shares in or debentures of the Company or any other body corporate.

Issue of shares

There was no change in the authorised, issued and paid-up capital of the Company during the financial year.

Options granted over unissued shares and debentures

No options were granted to any person to take up unissued shares or debentures of the Company during the financial year.

Reserves and provisions

There were no material transfers to or from reserves and provisions during the financial year under review except as disclosed in the financial statements.

Provision for insurance liabilities

Before the statement of profit or loss and other comprehensive income and statement of financial position of the Company were made out, the Directors took reasonable steps to ascertain that there was adequate provision for its insurance liabilities in accordance with the valuation basis specified in Part D of the Risk-Based Capital Framework for Insurers.

Impaired debts

Before the statement of profit or loss and other comprehensive income and statement of financial position of the Company were made out, the Directors took reasonable steps to ascertain that action had been taken in relation to the writing off of impaired debts and the making of impairment allowance for impaired debts and satisfied themselves that all known impaired debts had been written off and adequate impairment allowance had been made for impaired debts.

At the date of this report, the Directors are not aware of any circumstances that would render the amount written off for impaired debts or the amount of the impairment of allowance for impaired debts in the financial statements of the Company inadequate to any substantial extent.

Current assets

Before the statement of profit or loss and other comprehensive income and statement of financial position of the Company were made out, the Directors took reasonable steps to ascertain that any current assets, other than debts, which were unlikely to be realised in the ordinary course of business, at their values as shown in the accounting records of the Company have been written down to an amount which they might be expected so to realise.

At the date of this report, the Directors are not aware of any circumstances which would render the values attributed to the current assets in the financial statements of the Company misleading.

Valuation methods

At the date of this report, the Directors are not aware of any circumstances which have arisen which render adherence to the existing method of valuation of assets or liabilities of the Company misleading or inappropriate.

ANNUAL REPORT 2016 23

Contingent and other liabilities

At the date of this report, there does not exist:

(i) any charge on the assets of the Company that has arisen since the end of the financial year and which secures the liabilities of any other person; or

(ii) any contingent liability in respect of the Company that has arisen since the end of the financial year, except as disclosed in Note 37 of the financial statements.

No contingent liability or other liability has become enforceable, or is likely to become enforceable within the period of twelve months after the end of the financial year which, in the opinion of the Directors, will or may substantially affect the ability of the Company to meet its obligations as and when they fall due.

For the purpose of this paragraph, contingent liability or other liabilities do not include liabilities arising from contracts of insurance underwritten in the ordinary course of business of the Company.

Change of circumstances

At the date of this report, the Directors are not aware of any circumstances not otherwise dealt with in this report or the financial statements of the Company, which would render any amount stated in the financial statements of the Company misleading.

Items of an unusual nature

The results of the operations of the Company for the financial year were not, in the opinion of the Directors, substantially affected by any item, transaction or event of a material and unusual nature.

There has not arisen in the interval between the end of the financial year and the date of this report any item, transaction or event of a material and unusual nature likely, in the opinion of the Directors, to affect substantially the results of the operations of the Company for the year in which this report is made.

Indemnity and insurance costs

During the financial year, the Company incurred a premium expense of approximately RM25,000 in respect of the Directors and Officers Liability insurance effected for all the Directors and senior management of the Company.

24 ANNUAL REPORT 2016B

oard

of

Dir

ecto

rsM

emb

ersh

ip a

nd

mee

tin

gs

of t

he

Com

mit

tees

The

com

posi

tion

of

the

Boa

rd a

nd B

oard

Com

mit

tees

, num

ber

of m

eeti

ngs

held

dur

ing

the

fina

ncia

l yea

r en

ded

31

Dec

embe

r 2

016

, inc

ludi

ng n

umbe

r of

mee

ting

s co

nven

ed

by t

he B

oard

and

eac

h B

oard

Com

mit

tee

wit

h th

e at

tend

ance

of

each

mem

ber

are

as f

ollo

ws:

Boa

rd C

omp

lian

ce

B

oard

B

oard

B

oard

&

Ris

k

Boa

rd

Au

dit

N

omin

atio

ns

Rem

un

erat

ion

M

anag

emen

t In

vest

men

t

B

oard

Co

mm

itte

e Co

mm

itte

e Co

mm

itte

e Co

mm

itte

e Co

mm

itte

e

(A

tten

danc

e /

Num

ber

of M

eeti

ngs)

Dat

o’ M

ohd.

Sal

lehu

ddin

bin

Oth

man

(C

hair

man

)

(Inde

pend

ent

Non

-Exe

cutiv

e D

irect

or)

6/6

4

/4

4/4

2

/2

4/4

6

/6

Dat

uk S

eri D

r N

ik N

orzr

ul T

hani

bin

N H

assa

n T

hani

(Cha

irm

an)

(Cha

irm

an)

(Inde

pend

ent

Non

-Exe

cutiv

e D

irect

or)

6/6

3

/4

4/4

1

/1

4/4

-

Mr

Hit

oshi

Kit

agaw

a

(Cha

irm

an)

(Inde

pend

ent

Non

-Exe

cutiv

e D

irect

or)

5/6

2

/4

4/4

2

/2

3/4

-

Ms

Pea

rl C

han

Siew

Che

ng

(Cha

irm

an)

(C

hair

man

)

(Inde

pend

ent

Non

-Exe

cutiv

e D

irect

or)

6/6

4

/4

4/4

-

4/4

6

/6

Ms

Loh

Gua

t La

n

(Non

-Ind

epen

dent

Non

-Exe

cutiv

e D

irect

or)

6/6

-

- -

- 6

/6

Mr

Ala

n Jo

hn W

ilson

(Exe

cutiv

e D

irect

or)

6/6

-

4/4

1

/1

- -

Mr

Chua

Sec

k G

uan

(Chi

ef E

xecu

tive

Offi

cer/

Exec

utiv

e D

irect

or)

6

/6

- -

- -

6/6

Mr

Koi

chi N

agas

e(D

eput

y Ch

ief E

xecu

tive

Offi

cer)

- -

- -

- 5

/6

ANNUAL REPORT 2016 25

Board of Directors (continued)

Profiles of Directors

The profiles of the Directors of the Company are as follows:

Dato’ Mohd. Sallehuddin bin Othman(Chairman / Independent Non-Executive Director)

Dato’ Mohd. Sallehuddin bin Othman joined MSIG Insurance (Malaysia) Bhd as an Independent Non-Executive Director in 2005 and was appointed as the Chairman of the Board in March 2014. He holds professional accounting qualifications in Association of Chartered and Certified Accountants (ACCA) and Chartered Institute of Management Accountants (CIMA), United Kingdom. He also graduated with a Master’s Degree from City University, London in 1975. He is registered as a Chartered Accountant with Malaysia Institute of Accountants in 1981 and became a Fellow member of ACCA in 1983.

Dato’ Mohd. Sallehuddin bin Othman began his career with brief stints in various audit firms in Malaysia and United Kingdom, a statutory body and a major Government linked company in Malaysia before joining the Asian Development Bank based in Manila, Philippines from 1981 to 1986.

Upon returning to Malaysia in 1986, he joined Permodalan Nasional Berhad in senior positions doing corporate services and human resources until 1994. From mid-1994 to 2000, Dato’ Mohd. Sallehuddin was with UMW Holdings Berhad initially as Executive Director and subsequently as Group Managing Director. From 2001 until his retirement in 2006, he served as Group Managing Director of Malaysian Industrial Finance Berhad.

Post retirement, Dato’ Mohd. Sallehuddin has served as an Independent Non-Executive Director of a few companies including a foreign Islamic bank. Currently, apart from MSIG Insurance (Malaysia) Bhd, he is an Independent Director of a number of companies, notably Axa Affin Life Insurance Berhad and Bank of Tokyo-Mitsubishi UFJ (M) Berhad.

Datuk Seri Dr Nik Norzrul Thani bin N Hassan Thani(Independent Non-Executive Director)

Datuk Seri Dr Nik Norzrul Thani bin N Hassan Thani was appointed as Director of MSIG Insurance (Malaysia) Bhd on 16 March 2009.

He holds a Ph.D in Law from the School of Oriental and African Studies (SOAS), University of London and a Masters in Law from Queen Mary College, University of London. He read law at the University of Buckingham, United Kingdom.

Datuk Seri Dr Nik also holds a Post-Graduate Diploma in Syariah Law and Practice (with distinction) from the International Islamic University Malaysia. A Barrister of Lincoln’s Inn and an Advocate and Solicitor of the High Court of Malaya, he was called to the Bar of England and Wales in 1985 and to the Malaysian Bar in 1986. He was previously a Visiting Fulbright Scholar, Harvard Law School and a Chevening Fellow at the Oxford Centre of Islamic Studies. Datuk Seri Dr Nik is a Fellow of the Financial Services Institute of Australasia (FINSIA).

Currently, Datuk Seri Dr Nik is the Chairman and Senior Partner of Zaid Ibrahim & Co. Prior to joining Zaid Ibrahim & Co., Datuk Seri Dr Nik was with Baker & McKenzie (International Lawyers), Singapore.

His directorships in other companies are as Director of Fraser & Neave Holdings Bhd, Al Rajhi Banking & Investment Corporation (Malaysia) Bhd, UMW Holdings Bhd, T7 Global Berhad, Ranhill Holdings Bhd, Chin Hin Group Berhad and Amanah Saham Nasional Berhad.

Mr Hitoshi Kitagawa(Independent Non-Executive Director)

Mr Hitoshi Kitagawa joined the Board of MSIG Insurance (Malaysia) Bhd as an Independent Non-Executive Director on 18 March 2014. Mr Kitagawa is currently the Managing Director of Toyota Tsusho (Malaysia) Sdn Bhd. Prior to this, he was the Group Leader of Techno Park Management Group of Toyota Tsusho Corporation since 2011.

As a graduate from Meiji University Japan, he joined Toyota Tsusho Corporation, Japan in 1981. Mr Kitagawa has more than 35 years of working experience in the machinery, global logistics and assisting the auto parts manufacturers’ global operation during his tenure in Toyota Tsusho Corporation. He also had an overseas posting where he worked in Thailand Office in Bangkok from 2005 to 2011.

26 ANNUAL REPORT 2016

Board of Directors (continued)Profiles of Directors (continued)

Ms Pearl Chan Siew Cheng (Independent Non-Executive Director)

Pearl Chan Siew Cheng joined the Board of MSIG Insurance (Malaysia) Bhd on 18 March 2014 as an Independent Non-Executive Director. She has 31 years of experience in the Malaysian fund management industry, having managed institutional money such as government funds, insurance funds, pension funds, charitable foundations and unit trust funds throughout her career.

Prior to her retirement in January 2008, she was the Deputy Chief Executive Officer of CIMB Principal Asset Management for one year, after a merger between CIMB and the Southern Bank Group. Before that, she pioneered SBB Asset Management, a wholly-owned subsidiary of the Southern Bank Group, which became the first commercial bank in Malaysia to have an asset management arm. She held the position of CEO for 17 years, and CEO/Chief Investment Officer for the first 14 years, leading a team of equity and fixed income fund managers. Before setting up SBB Asset Management, she was General Manager of Rashid Hussain Asset Management and fund manager with Bumiputra Merchant Bankers Berhad for a total of 13 years.

During her career, she also spearheaded two major corporate integration exercises in 2003 & 2007, where she successfully completed the entire integration process, involving organisation and governance structures, human resources, administrative and technical systems. She is a graduate in Economics from the University of Nottingham, England.

Ms Loh Guat Lan(Non-Independent Non-Executive Director)

Loh Guat Lan joined the Board of MSIG Insurance (Malaysia) Bhd as Non-Independent Non-Executive Director on 1 October 2010. She is currently the Group Managing Director / Chief Executive Officer of Hong Leong Assurance Berhad (HLA), a subsidiary of HLA Holdings Sdn Bhd (HLAH) wholly-owned by Hong Leong Financial Group Berhad (HLFG), the financial services arm of Hong Leong Group Malaysia. She is also a director of Hong Leong MSIG Takaful Berhad.

She was appointed to the position on 1 September 2009. She holds a Bachelor’s Degree in Nutrition Science and is a fellow member of Life Management Institute (FLMI), Customer Service Management (CSM) and Life Office Management (LOMA). She is also a Certified Financial Planner (CFP) and Registered Financial Planner (RFP).

Her last role prior to joining HLA as the Chief Operating Officer (Life Division) was Vice President & Senior Director of Agency (Malaysia). She has over 26 years of experience in the insurance industry.

Mr Alan John Wilson(Executive Director)

Mr Alan Wilson has helmed the Singapore-based Asia regional holding office of Mitsui Sumitomo Insurance Company (MSIG) as Regional CEO since 2008. In his capacity as Regional CEO, he also serves as Chairman or Director (or equivalent) on the Boards of 13 MSIG companies around the region. Under Mr Wilson’s leadership, the MSIG network in Asia has now expanded to 17 markets. In April 2015, Mr Wilson was honoured to be appointed as the first foreign Executive Officer, Mitsui Sumitomo Insurance Co Ltd (Japan). Mr Wilson has a sound executive management track record and has over 30 years of experience in the general insurance industry.

Prior to joining MSIG Asia, Mr Wilson was the Asia CEO at Allianz from 1999. He assumed overall responsibility for managing over 20 general, life and health insurance operations across 14 countries and later served on several Boards for Allianz and for other groups such as Parkway in Asia. Mr Wilson joined Allianz from Guardian Royal Exchange Assurance Group where he was Asia Managing Director. Over the course of his 21 years there, he held various senior positions with progressive responsibilities, where he managed general and life insurance business in 11 countries.

A British national and a Singaporean Permanent Resident, Mr Wilson has lived and worked in Asia since 1982 in various places, including Hong Kong, Indonesia, Pakistan and Singapore.

Mr Wilson is also Chairman of MSIG Berhad.

Mr Chua Seck Guan(Chief Executive Officer/Executive Director)

Mr Chua Seck Guan was appointed as the Chief Executive Officer and Executive Director of MSIG Insurance (Malaysia) Bhd on 1 April 2010. A Senior Associate and Certified Insurance Professional from the Australian and New Zealand Institute of Insurance and Finance, he has vast experience in General Insurance operations having served 34 years with the Company. He provides the leadership and played key strategic and operational roles in charting the Company’s growth to its current revenue and profit level, and positioned MSIG as one of the leaders in the industry. He was also instrumental in leading MSIG to be the General Insurance Company of The Year 2015, awarded by the Asia Insurance Review.

He is currently the Deputy Chairman of PIAM Management Committee and sits in the Board of Malaysia Rating Corporation Berhad (MARC), Ombudsman for Financial Services and MSIG Berhad.

ANNUAL REPORT 2016 27

Board of Directors (continued)

Trainings attendedThe trainings attended by the Directors are as follows:-

• A dialogue on “The New and Revised Auditor Reporting Standards: Implications to Financial Institutions”• Special Invitation to Industry Briefing on Directors Register Implementation• 3rd BNM - FIDE FORUM Annual Dialogue with the Governor of Bank Negara• Launch of FIDE Forum’s Directors Register• FIDE Core Programme Module B – Insurance• FinTech: Business Opportunity or Disruptor by Markus Gnirck and Veiverne Yuen• Technology-based Innovation that Counts by Steven Lewis, Patrick Menard and Shankar Kanabiran, Ernst & Young• MSIG In-House Directors’ Training

Responsibilities of the Board and Board Committees (A) The roles and responsibilities of the Board are as follows:

(i) Approve the risk appetite, business plans and other initiatives which would, singularly or cumulatively, have a material impact on the Company’s risk profile.

(ii) Oversee the selection, performance, remuneration and succession plans of the CEO, control function heads and other members of senior management, such that the Board is satisfied with the collective competence of senior management to effectively lead the operations of the Company.

(iii) Oversee the implementation of the Company’s governance framework and internal control framework, and periodically review whether these remain appropriate in light of material changes to the size, nature and complexity of the Company’s operations.

(iv) Promote, together with senior management, a sound corporate culture within the Company which reinforces ethical, prudent and professional behavior.

(v) Promote sustainability through appropriate environmental, social and governance considerations in the Company’s business strategies.

(vi) Oversee and approve the recovery and resolution as well as business continuity plans for the Company to restore its financial strength, and maintain or preserve critical operations and critical services when it comes under stress.

(vii) Promote timely and effective communication between the Company and Bank Negara Malaysia on matters affecting or that may affect the safety and soundness of the Company.

(B) The roles and responsibilities of the Board Committees are as follows:

Board Audit CommitteeThe Board Audit Committee’s primary role is to support the Board in ensuring that there is a reliable and transparent financial reporting process within the Company. In addition, providing oversight over the external auditor to foster a quality audit. In fulfilling this role, the Board Audit Committee must:

(i) Review and approve the audit plan including its scope, procedures and frequency.

(ii) Review and approve the Audit Charter and budget of the Internal Audit Department and to ensure that the Internal Audit Department is distinct and has the appropriate status within the overall Company structure for the internal auditors to achieve their audit objectives.

(iii) Review key audit reports and ensure that Senior Management is taking necessary corrective actions in a timely manner to address control weaknesses, non-compliance with laws, regulatory requirements, policies and other problems identified by the Internal Audit and other control functions.

(iv) Note any significant disagreements between the Chief Internal Auditor and the rest of the Senior Management, irrespective of whether these have been resolved, in order to identify any impact that the disagreements may have on the audit process or findings.

(v) Advice on the appointment, remuneration, performance, evaluation, removal and redeployment of the Chief Internal Auditor and senior officers of the internal audit functions.

(vi) Establishing a mechanism to assess the performance and effectiveness of the internal audit function.

(vii) Make recommendations to the Board on the appointment, removal and remuneration of the external auditor.

(viii) Monitor and assess the independence of the external auditor including approving the provision of non-audit services by the external auditor.

28 ANNUAL REPORT 2016

Responsibilities of the Board and Board Committees (continued)

Board Audit Committee (continued)

(ix) Monitor and assess the effectiveness of the external audit, including by meeting with the external auditor without the presence of senior management at least annually.

(x) Maintain regular, timely, open and honest communication with the external auditor, and requiring the external auditor to report to the Board Audit Committee on significant matters.

(xi) Ensure that Senior Management is taking necessary corrective actions in a timely manner to address external audit findings and recommendations.

(xii) Review and update the Board on all related party transactions.

(xiii) Review the accuracy and adequacy of the Chairman’s statement in the directors’ report, corporate governance disclosure, interim financial reports and preliminary announcements in relation to the preparation of financial statements.

(xiv) Monitor compliance with the Board’s conflicts of interest policy.

(xv) Review third-party opinions on the design and effectiveness of the Company’s internal control framework.

(xvi) Other functions as may be determined by the Board.

Board Nominations Committee

(i) To establish minimum requirements for the Board of Directors and the Chief Executive Officer to perform their responsibilities effectively as well as to oversee the overall composition of the Board in terms of the appropriate size and mix of skills, the balance between Executive, Non-Executive and Independent Directors and other core competencies required.

(ii) To assess and recommend the nominees for Board and Board Committees, as well as nominees for the position of Chief Executive Officer. This includes assessing Directors and the Chief Executive Officer proposed for re-appointment, before an application for approval is submitted to Bank Negara Malaysia.

(iii) To establish a mechanism for formal assessment on the effectiveness of the Board as a whole, the contribution by each Director to the effectiveness of the Board, the contribution of the Board Committees and the performance of the Chief Executive Officer. The assessments should also include ascertaining that the Director is not disqualified under the relevant law and fulfill the “fit and proper” criteria.

(iv) To recommend to the Board on the removal of a Director / Chief Executive Officer if he is ineffective, errant or negligent in discharging his responsibilities.

(v) To ensure that all Directors undergo appropriate induction programmes and receive continuous trainings.

(vi) To oversee the appointment, management succession planning and performance evaluation of Senior Management and recommend to the Board on the removal of Senior Management if they are ineffective, errant or negligent in discharging their responsibilities.

(vii) To ensure that processes are in place to facilitate and monitor the effective transfer of knowledge and expertise from expatriates employed in Senior Management and specialist positions to the staff of the Company as well as the industry generally.

(viii) To ensure all Key Responsible Persons fulfill the “fit and proper” criteria and conducting assessment of the fitness and propriety of Key Responsible Persons and the Company Secretary.

Board Remuneration Committee

(i) To recommend a framework for the remuneration of Directors and Senior Management.

(ii) To recommend specific remuneration packages for Directors and Senior Management.

(iii) To ensure compliance with BNM Risk Governance Policy Document (Principle 10) which states that the Executive remuneration must be aligned with prudent risk-taking and appropriately adjusted for risks.

ANNUAL REPORT 2016 29

Responsibilities of the Board and Board Committees (continued)

Board Compliance & Risk Management Committee

Compliance

(i) Promoting a positive, open and consistent Compliance culture and monitoring the overall compliance with applicable laws, rules and regulations as well as operational manuals.

(ii) Reviewing and assessing the adequacy and effectiveness of the Compliance policies and processes through an appropriate and clear framework of accountability, reporting and controls, including ensuring adequate infrastructure, resources and systems are in place.

(iii) Reviewing and recommending the Company’s Compliance Policy, Compliance Manual and Compliance Program for the Board of Directors’ approval.

(iv) Reviewing and assessment of Compliance with Bank Negara Malaysia (“BNM”) / Persatuan Insurans Am Malaysia (“PIAM”) guidelines / circulars and MSIG Policies in pursuant to Financial Services Act, 2013 requirements.

(v) Reviewing the Management’s periodic Compliance reports and checklists, including Risk Treatment Plans (RTP), Complaint reporting as well as disclosure in regard to Compliance activities in the Company’s Annual Report.

Risk Management

(i) Ensuring effective implementation of expectations in pursuant to Policies for Risk Governance under BNM/ RH/GL/013-5.

(ii) Reviewing and recommending Risk Management strategies, policies and risk tolerance levels for the Board’s approval.

(iii) Reviewing and assessing the adequacy of the Risk Management policies and framework for identifying, measuring, monitoring and controlling risks as well as the extent to which these are operating effectively.

(iv) Ensuring that adequate infrastructure, resources and systems are in place for effective Risk Management e.g. ensuring that the staff responsible for implementing Risk Management systems perform those duties independently of the Company’s risk taking activities.

(v) Reviewing the periodic reports on risk exposure, risk portfolio composition, independent assessment and Risk Management activities, including disclosure in regard to Risk Management activities in the Company’s Annual Report.

(vi) Reviewing activities as well as Risk Appetite Statement, Individual Target Capital Level (“ITCL”) Review Report and Capital Management Plan (A.k.a. ICAAP Report) regularly as required under BNM/RH/GL/003-29.

(vii) Reviewing the Stress Testing progress and corrective action plan to comply with BNM/RH/GL/003-23.

(viii) Reviewing activities and reports in regard to the Risk Management Framework on Outsourcing in compliance with BNM/RH/GL/003-4.

(ix) Reviewing and providing direction on the Internal Control Program (ICP).

The Board Compliance & Risk Management Committee is supported by the Compliance & Risk Management Working Committee comprising the Chief Executive Officer, Deputy Chief Executive Officer and Senior Management Team. To effect a more focused attention on management of compliance risks as prescribed by the BNM Policy Document on Compliance, and on enterprise risk management at the management level, the Board Committee endorsed at the last meeting two management committees, namely the Compliance Committee and the Enterprise Risk Management Committee in supporting the Board Committee.

Board Investment Committee

(i) Review and advise on Investment strategies and policies with a view to optimise investment performance in line with MSIG’s Investments Risk Appetite Statement.

(ii) Review and monitor the Investment Assets Allocation within the risk and limit permitted under the Investment Policy, BNM Guidelines and RBC framework, at least on an annual basis.

(iii) Review and approve the exposure limits for counterparties for Deposits placements.

(iv) Manage and monitor risks associated with investment activities with a view to strengthening the Capital Adequacy Ratio whilst optimising risk adjusted returns.

(v) Ensure proper execution and monitoring of investments by having adequate internal controls for investment assets management, including approval of counterparty limits.

30 ANNUAL REPORT 2016

Responsibilities of the Board and Board Committees (continued)

Board Investment Committee (continued)

(vi) Review and approve the Investment Plan.

(vii) Set Performance Standards for external Fund Managers and review their actual performance on a regular basis.

(viii) Review and approve the appointment / termination of external Fund Managers, including the Custodians for safekeeping of assets.

(ix) Ensure compliance with the Regional Investment Policy, BNM’s requirements, as well as in compliance with legal, accounting, prudential and liquidity requirements.

Internal control framework• The Company has established an Internal Control Programme (“ICP”) comprising of Company Level Control and

Process Level Control Documentation to ensure Internal Controls on significant key risk areas in regard to Financial Reporting are adequately designed, documented and functioning effectively at all times.

• ICP is an annual exercise entailing review and update of the ICP documentation of the Company’s operational processes and controls that include compliance with the requirement of relevant laws and regulations.

• It is subject to independent Testing of Design and Operating Effectiveness on annual basis for the evaluation on Internal Control Over Financial Reporting (“ICOFR”) to provide assurance on reliability of Financial Reporting.

• The internal control requirement on the key risk areas and compliance with relevant laws and regulations will be embedded in the Company’s new Business Process Management system.

• The Risk Management Independent Risk Assessment focusing on the business units’ risk management and governance is performed annually.

• The Company’s outsourcing arrangements and Outsourcing Policy & Procedures are reviewed periodically to ensure compliance with the Guidelines on Outsourcing for Insurers issued by Bank Negara and its effectiveness in managing the Company’s outsourcing activities.

• Besides the framework for internal controls and procedures, the Company puts in place an organisation structure that clearly defines the segregation of roles, responsibilities and authority in the Company.

RemunerationRemuneration Policy

The Company adopts a fair and competitive Remuneration Policy where rewards commensurate with position responsibilities and individual performance of the job, and to avoid directors and employees from engaging in excessive or inappropriate risk taking.

It is also guided by equal opportunities principles and principles to balance risk and incentives associated with remuneration in order to ensure a sound and appropriate design and operation of the remuneration framework.

Performance and job sizes will be assessed by the consistent application of an objective process to establish job weight and its relative value in the organisation, taking into account the incumbent’s experience, performance and the positions’ potential risk exposure, ensuring equitable remuneration practices for both existing and new employees.

Remuneration Policy’s Key Objectives

1. Success of the organisation is built on a true performance culture. Individual contributions must be recognized and rightfully rewarded to enable the organisation to continue to attract and retain quality staff that will support the Company’s operations.

2. The Company believes that an equitable and competitive Remuneration Policy, balanced with the appropriate management of risk exposure will establish the Company as a sustainable and preferred employer, helping us to recruit and motivate employees to deliver business success and build a performance culture.

3. The policy provides a consistent framework to develop the Company’s pay policy within the context of statutory requirements, market conditions and business challenges.

ANNUAL REPORT 2016 31

Remuneration (continued)

Scope of Remuneration Policy

Scope covers all members of staff (including but not limited to permanent employee, contract and temporary staff).

The policy however excludes expatriates assigned to the Company.

Senior Management members comprises of:

1. Chief Executive Officer

2. Executive Vice President – HR, L&D, Marketing, Business Excellence, Accident & Health Underwriting

3. Senior Vice President – Finance, Planning & Actuarial

4. Senior Vice President – Underwriting (Commercial Lines), Claims & Reinsurance

5. Senior Vice President – IT, E Commerce & Business Intelligence

6. Senior Vice President – Compliance & Enterprise Risk Management

7. Senior Vice President – Agency & Motor Franchise

8. Senior Vice President – Branch Operations Support, PSD, Motor Underwriting & Administration

Risk Governance

In compliance with Bank Negara Malaysia Policy Document on Risk Governance, the Company has also incorporated the Principle 10 into its remuneration structure where executive remuneration is aligned with prudent-risk taking and appropriately adjusted for risks.

A guided performance management process is in place to ensure that the payments of variable remuneration are conducted in accordance with the Remuneration Policy.

At this juncture, the Company is satisfied with the existing remuneration structure and performance management process to meet the objectives of the Company’s Remuneration Policy. The Company will review the remuneration framework to ensure it continues to meet the Company’s long term objectives.

Remuneration for employees in control functions are structured in a way that is principally based on the achievement of their control objectives and does not compromise their independence.

Pay structure is designed to consider all types of risks and long-term benefits of the Company. Specifically such structure is determined by using market data for the level of remuneration that is sourced from external consultants and by taking into account conditions (such as business structure, organisation, legal system, employment / pay structure / practices), financial position of the entity, existing and potential risks, and the roles and tasks of the jobs.

The Company’s key risks are identified through the Risk Management Framework and the Company’s 3 year Business Plan, which includes actions plans. Such actions are incorporated into the performance measurements of employees to enforce the performance and competencies through remuneration measures.

In 2016, there were no specific changes to the nature and type of measures.

Performance Management System

The Company uses a comprehensive performance measurement framework that incorporates both financial and non-financial performance in determining the size and allocation of the variable remuneration under the Company’s Short Term Incentive Plan (STI).

The financial matrix links the STI to the profits, revenue and other performance measurements of the Company as a whole, and the contributions of the employee in deciding the quantum.

The non-financial matrix captures the performance of the qualitative aspects such as the compliance of Risk Management Policy, adherence to legal, regulatory and other ethical standards, customer’s satisfaction, effectiveness and efficiency of support functions.

The overall assessment of the Individual is a combination of Individual Performance and Competencies. The overall scores will be given a weightage which falls into a structured performance banding ranging from Outstanding Performance, Strong Performance, Effective Performance, Marginal Performance and Unsatisfactory Performance. This ensures the employees are appropriately assessed and compensated at the level corresponding to the performance.

For Unsatisfactory Performance, this would impact the salary / bonus of the affected employees and in certain circumstances the Company would not grant bonus or increase in salary.

32 ANNUAL REPORT 2016

Remuneration (continued)

Remuneration Structure

The Company’s Remuneration Policy is limited to cash and benefits-in-kind which commensurate with the position of the officers. There are no shares and/or share-linked instruments, deferring or vesting as part of its remuneration framework.

The Company’s Remuneration Policy does not accord the following:-

1. Deferral and/or vesting of variable remuneration.

2. Deferred remuneration with claw-back arrangements.

The breakdowns of the total amount of remuneration awards to the Senior Management for the financial year are as follows:

Total Value of Remuneration Awards for the Financial Year

UnrestrictedRM

DeferredRM

Fixed remuneration

• Cash-based 4,507,611 Nil

• Shares and share-linked instruments Nil Nil

• Others Nil Nil

Variable remuneration

• Cash-based 991,252 Nil

• Shares and share-linked instruments Nil Nil

• Others Nil Nil

TOTAL 5,498,863 Nil

Auditors

The auditors, KPMG PLT (converted from a conventional partnership, KPMG, on 27 December 2016), have indicated their willingness to accept re-appointment.

The auditors’ remuneration is disclosed in note 25 to financial statements.

Signed on behalf of the Board of Directors in accordance with a resolution of the Directors:

……………………………………….........................................………………… Dato’ Mohd. Sallehuddin bin Othman

……………………………………….........................................………………… Chua Seck Guan

Kuala Lumpur,Date: 21 March 2017

ANNUAL REPORT 2016 33

as at 31 December 2016Statement of financial position

Note 2016 2015 RM’000 RM’000Assets

Plant and equipment 3 23,272 18,036Investment property 4 141 146Goodwill 5 1,141,224 1,141,224Available-for-sale financial assets 6 1,342,506 1,277,800Deferred tax assets 7 12,292 9,664Reinsurance assets 8 440,744 547,902Loans and receivables, excluding insurance receivables 9 1,209,716 1,205,228Insurance receivables 10 194,259 217,613Deferred acquisition costs 11 74,414 77,191Cash and cash equivalents 12 173,614 138,150

Total assets 4,612,182 4,632,954

Equity and liabilities Share capital 13 333,143 333,143Reserves 2,214,810 2,068,238

Total equity 2,547,953 2,401,381

Insurance contract liabilities 15 1,848,749 1,975,730Other financial liabilities 16 20,374 30,281Insurance payables 17 117,974 152,525Other payables 18 62,707 61,098Tax payable 14,425 11,939

Total liabilities 2,064,229 2,231,573

Total equity and liabilities 4,612,182 4,632,954

The notes on pages 37 to 88 are an integral part of the financial statements.

34 ANNUAL REPORT 2016

Note 2016 2015 RM’000 RM’000

Operating revenue 19 1,638,304 1,566,567

Gross written premiums 15.2 1,522,503 1,535,370Change in unearned premiums provision 19,062 (54,088)

Gross earned premiums 1,541,565 1,481,282

Gross written premiums ceded to reinsurers 15.2 (294,863) (301,740)Change in unearned premiums provision (1,723) 8,874

Premiums ceded to reinsurers (296,586) (292,866)

Net earned premiums 1,244,979 1,188,416

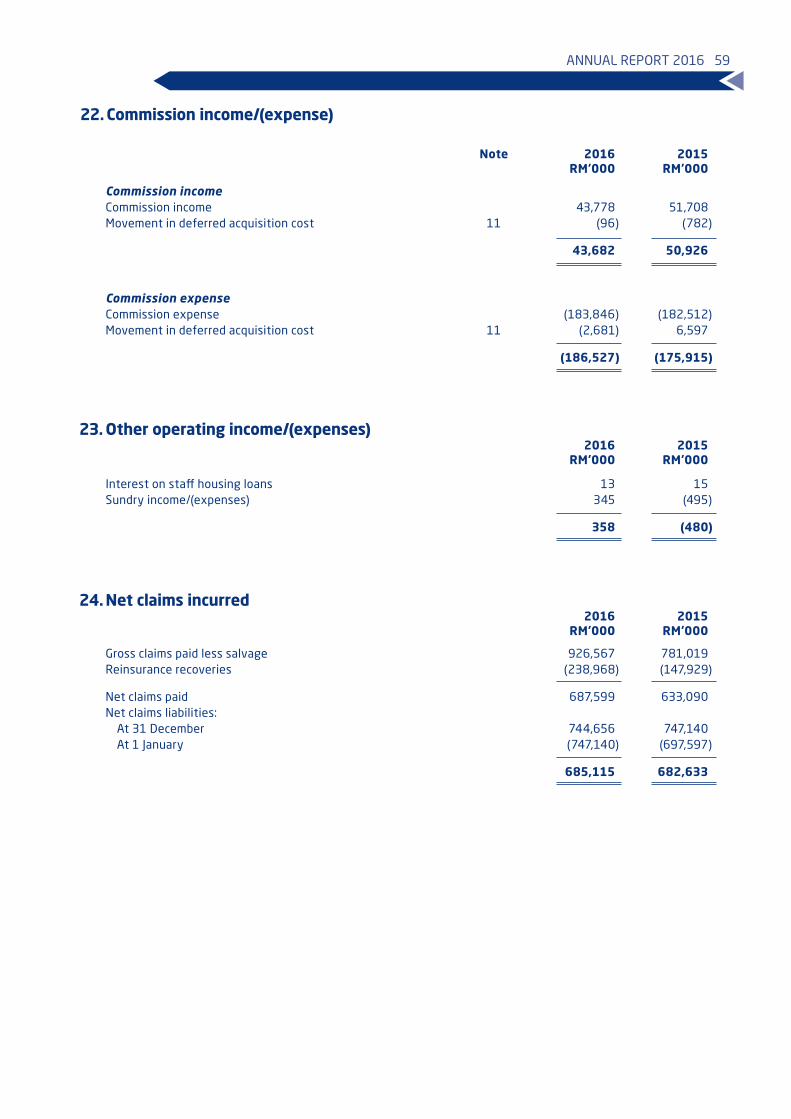

Investment income 20 96,739 85,285Realised gains and losses 21 9,704 3,494Commission income 22 43,682 50,926Other operating income/(expenses) 23 358 (480)

Other income 150,483 139,225

Gross claims paid 15.1 (926,567) (781,019)Claims ceded to reinsurers 15.1 238,968 147,929Gross change in contract liabilities 107,919 (99,253)Change in contract liabilities ceded to reinsurers (105,435) 49,710

Net claims incurred 24 (685,115) (682,633)

Commission expense 22 (186,527) (175,915)Management expenses 25 (210,270) (207,258)

Other expenses (396,797) (383,173)

Profit before tax 313,550 261,835Tax expense 27 (64,750) (61,735)

Profit for the year 248,800 200,100

Other comprehensive income Items that may be reclassified subsequently to profit or loss

Net (loss)/gain on fair value of available-for-sale financial assets (3,017) 3,764Tax effect 07 732 (940)

Other comprehensive (loss)/income for the year, net of tax (2,285) 2,824 Total comprehensive income for the year 246,515 202,924 Basic earnings per share (sen) 28 74.7 60.1

The notes on pages 37 to 88 are an integral part of the financial statements.

for the year ended 31 December 2016Statement of profit or loss and other comprehensive income

ANNUAL REPORT 2016 35

for

the

year

end

ed 3

1 D

ecem

ber

201

6St

atem

ent

of c

hang

es in

equ

ity

Shar

e Sh

are

Fair

val

ue

R

etai

ned

To

tal

cap

ital

p

rem

ium

re

serv

e ea

rnin

gs

equ

ity

N

ote

RM

’00

0

RM

’00

0

RM

’00

0

RM

’00

0

RM

’00

0

At

1 Ja

nu

ary

20

15

333

,143

1

,17

8,4

03

(2

,23

5)

78

9,0

89

2

,29

8,4

00

Fair

val

ue o

f av

aila

ble-

for-

sale

fina

ncia

l ass

ets

-

- 2

,824

-

2,8

24

Tota

l oth

er c

ompr

ehen

sive

inco

me

for

the

year

- -

2,8

24

- 2

,824

Pro

fit

for

the

year

- -

- 2

00

,10

0

20

0,1

00

Tota

l com

preh

ensi

ve in

com

e fo

r th

e ye

ar

-

- 2

,824

2

00

,10

0

20

2,9

24D

ivid

ends

pai

d du

ring

the

yea

r 2

9

- -

- (9

9,9