Embed Size (px)

Citation preview

Industries, �rms and brands:

a view on Multinationals

Vanessa Alviarez

Sauder Business School

University of British Columbia

OECD workshopNovember, 2018

Alviarez (UBC) Multinationals

Multinationals shape:

I Countries' comparative advantage.

I Cross-country propagation of aggregate shocks.

I Market concentration.

Alviarez (UBC) Multinationals

Multinational Production and

Comparative Advantage

Alviarez (UBC) Multinationals

Multinational Production (MP) shapes

countries' patterns of production

I Oftentimes, countries host large foreign multinationals in sectorswhere they lack major local �rms.

I In other sectors, large local companies dominate, deterring the

operations of foreign a�liates in their market.

I Spain is the world's 8th-largest producer of cars under theleadership of foreign a�liates of Daimler AG, Ford,Peugeot, GM, Nissan, Renault, and Volkswagen.

I In Italy, however, prominent home-based companies, suchas Ferrari or Fiat, capture a dominant share of the market.

=⇒ Country's comparative advantage is jointly determined bythe productivities of local producers and MP in the economy.

=⇒ By altering sectoral productivities, MP shapes thecross-country trade and cross-border patterns of production.

Alviarez (UBC) Multinationals

Relevance for Policy

I Undertanding this relationship help us to asses the responses of

trade and multinational production (MP) to shocks a�ecting the

level of cross borders production frictions

I Policies strengthening investor-state dispute settlementprovisions and fortify intellectually property rights.

I Role of MP frictions and the sectoral structure of local

producers' capabilities in explaining cross-country di�erences in:

I Industrial composition of inward MP.I Pool of investing countries that each economy hosts.

Alviarez (UBC) Multinationals

Stylized Fact

I Sectoral di�erences in MP shares are stronglycorrelated with Ricardian productivitydi�erences.

I Observed shares of inward MP are larger in sectorswhere local producers are relatively less productive

I Productivity enhancement is uneven and biasedtowards sectors in which locals exhibit comparativedisadvantage.

Alviarez (UBC) Multinationals

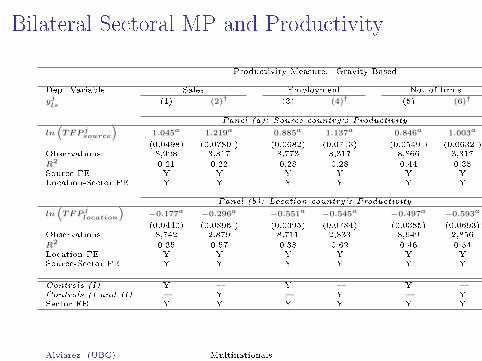

Bilateral Sectoral MP and Productivity

Productivity Measure: Gravity Based

Dep. Variable Sales Employment No. of �rms

yjls

(1) (2)† (3) (4)† (5) (6)†

Panel (a): Source country's Productivity

ln(TFP jsource

)1.045a 1.219a 0.885a 1.137a 0.846a 1.003a

(0.0498) (0.0780 ) (0.0682) (0.0713) (0.0549 ) (0.0632 )Observations 8,928 3,317 8,773 3,317 8,866 3,317

R2 0.21 0.22 0.28 0.28 0.44 0.35Source FE Y Y Y Y Y YLocation-Sector FE Y Y Y Y Y Y

Panel (b): Location country's Productivity

ln(TFP

jlocation

)−0.177a −0.296a −0.551a −0.545a −0.497a −0.593a

(0.0440) (0.0896 ) (0.0395) (0.0784) (0.0385) (0.0693)Observations 8,742 2,879 8,711 2,833 8,649 2,856

R2 0.35 0.57 0.38 0.62 0.46 0.54Location FE Y Y Y Y Y YSource-Sector FE Y Y Y Y Y Y

Controls (I) Y � Y � Y �Controls (I and II) � Y � Y � YSector FE Y Y Y Y Y Y

Alviarez (UBC) Multinationals

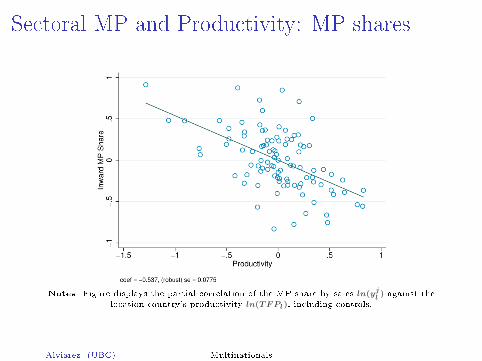

Sectoral MP and Productivity: MP shares

Notes: Figure displays the partial correlation of the MP share by sales ln(yjl) against the

location country's productivity ln(TFPl), including controls.

Alviarez (UBC) Multinationals

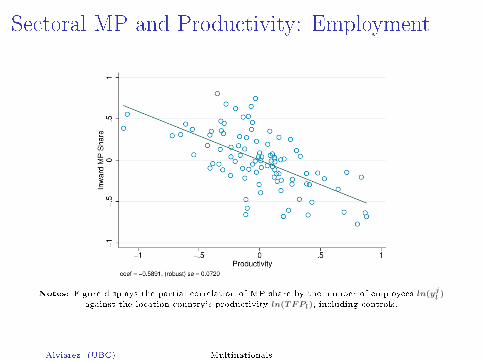

Sectoral MP and Productivity: Employment

Notes: Figure displays the partial correlation of MP share by the number of employees ln(yjl)

against the location country's productivity ln(TFPl), including controls.

Alviarez (UBC) Multinationals

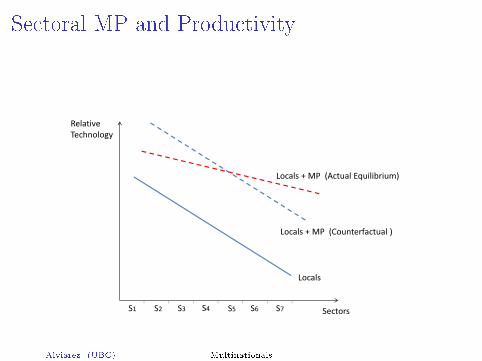

Sectoral MP and Productivity

��������

������ �

�������������������������������

�������� �� �� �� �� �� ��

�����

����������� �������� �������

Alviarez (UBC) Multinationals

Gains from trade GT

I GT can be decomposed into two multiplicative terms:

I Aggregate domestic trade shareI Dispersion of domestic trade shares across sectors.

GTl =W lg>0,d>0

W lg>0,d→∞

= (πll)− 1θ︸ ︷︷ ︸

aggregate domestictrade share

× (1−Aπll)− 1θ︸ ︷︷ ︸

dispersion ofdomestic trade shares

I GT increase with the dispersion of domestic trade shares, Aπll ,and decrease in aggregate domestic shares, πll.

Alviarez (UBC) Multinationals

A Multi-Sector Model of Trade and MP

I Develops a multi-sector extension of the benchmarkRicardian model of trade and multinational production(Ramondo & Rodríguez-Clare, 2013).

I Model nests fundamental and e�ective comparativeadvantage in a uni�ed framework

I Incorporating multiple sectors and multiple factors ofproduction (Levchenko & Zhang, 2016);

I Allows for export platformsI Asymmetric and sector speci�c MP barriers;I Heterogeneous preferences;I Di�erences in factor and intermediate input intensities

across sectors: input-output inter-linkages, inter- andintra-sectoral trade; and

I A non-tradable sector.

Alviarez (UBC) Multinationals

E�ective and Fundamental Productivities

Alviarez (UBC) Multinationals

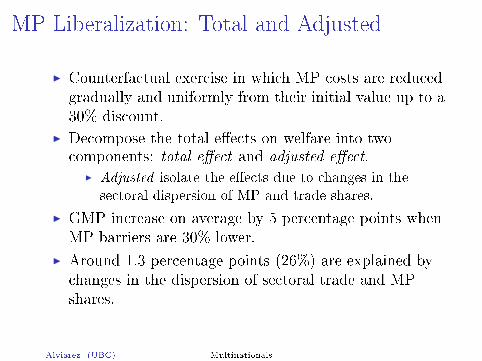

MP Liberalization: Total and Adjusted

I Counterfactual exercise in which MP costs are reducedgradually and uniformly from their initial value up to a30% discount.

I Decompose the total e�ects on welfare into twocomponents: total e�ect and adjusted e�ect.

I Adjusted isolate the e�ects due to changes in thesectoral dispersion of MP and trade shares.

I GMP increase on average by 5 percentage points whenMP barriers are 30% lower.

I Around 1.3 percentage points (26%) are explained bychanges in the dispersion of sectoral trade and MPshares.

Alviarez (UBC) Multinationals

Counterfactuals: Removing Fundamental

Comparative Advantage

Alviarez (UBC) Multinationals

Impact of MP on E�ective Productivities

I Scenario in which MP only a�ects the average productivity ofthe economy, while keeping the same comparative advantage oflocal producers.

I GT are 12% higher if MP only enhances aggregate productivitywithout eroding host country's comparative advantage.

Alviarez (UBC) Multinationals

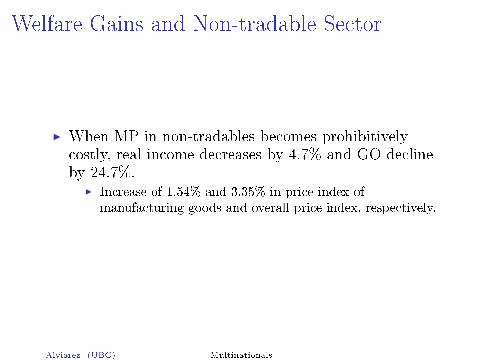

Welfare Gains and Non-tradable Sector

I When MP in non-tradables becomes prohibitivelycostly, real income decreases by 4.7% and GO declineby 24.7%.

I Increase of 1.54% and 3.35% in price index ofmanufacturing goods and overall price index, respectively.

Alviarez (UBC) Multinationals

The growth of multinational �rms in the

Great Recession (with Javier Cravino

and Andrei A. Levchenko)

Alviarez (UBC) Multinationals

MotivationI Rapid economic integration between 1980-2007

I Trade, FDI, capital �ows

I Pattern reversed during the Great Recession

1. 'Great Trade Collapse'2. Large drop in �nancial �ows

I Large literature on two related questions

1. Why did cross-border capital and trade �ows declined?2. Did this contribute to the crisis?

I Not much attention to multinational �rms'performance

What happened to multinationals during the crisis?

Alviarez (UBC) Multinationals

MotivationI Rapid economic integration between 1980-2007

I Trade, FDI, capital �ows

I Pattern reversed during the Great Recession

1. 'Great Trade Collapse'2. Large drop in �nancial �ows

I Large literature on two related questions

1. Why did cross-border capital and trade �ows declined?2. Did this contribute to the crisis?

I Not much attention to multinational �rms'performance

What happened to multinationals during the crisis?

Alviarez (UBC) Multinationals

Imports and manufacturing FMN sales relative

to GDP.7

.8.9

1

.85

.9.9

51

1.05

.81

1.2

.8.9

11.

1

.8.9

11.

11.

2

.9.9

51

1.05

1.1

.8.9

11.

11.

2

.8.9

11.

1

.6.7

.8.9

12005 2007 2009 2011 2005 2007 2009 2011 2005 2007 2009 2011

United States Austria France

Germany Netherlands United Kingdom

Spain Italy Japan

Imports/GDP Foreign Affiliate Sales/GDP

Source: OECD statisticsAlviarez (UBC) Multinationals

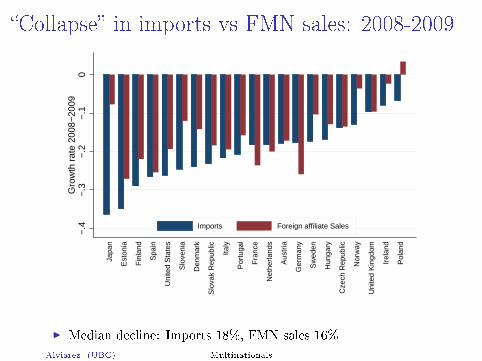

�Collapse� in imports vs FMN sales: 2008-2009

−.4

−.3

−.2

−.1

0G

row

th r

ate

2008

−20

09

Japa

n

Est

onia

Fin

land

Spa

in

Uni

ted

Sta

tes

Slo

veni

a

Den

mar

k

Slo

vak

Rep

ublic

Italy

Por

tuga

l

Fra

nce

Net

herla

nds

Aus

tria

Ger

man

y

Sw

eden

Hun

gary

Cze

ch R

epub

lic

Nor

way

Uni

ted

Kin

gdom

Irel

and

Pol

and

Imports Foreign affiliate Sales

I Median decline: Imports 18%, FMN sales 16%

Alviarez (UBC) Multinationals

Preview of results

I Sectoral and size di�erences account for most of theFMN decline

I FMNs performance varies widely depending on FMNssource country

I Implication: Multinationals will have a di�erentialimpact on aggregate output across destinationcountries hosting FMNs from di�erent sources

I Model: Multinationals contributed 0.24 percent to thedecline in growth in the median country

I Composition across sources is important for individualcountries, decline in growth ranges from 0 to 0.5 pctpoints

Alviarez (UBC) Multinationals

Firm level Data

I ORBIS (Bureau van Dijk)

I Data from business registries and annual reports

I Both publicly listed and private �rms

I Manufacturing and non-manufacturing

I 2004-2012

I Cross-�rm ownership data

I Multinationals >50% ownership

I Sample: 34 countries with good coverage sample

I Europe (Euro Area and periphery) + AUS, JPN,KOR, MEX, SGP

I Average country: 180K �rms

Alviarez (UBC) Multinationals

Observation 1

The a�liates of foreign multinationals grew faster than

domestic �rms in every year between 2004-2008 and

2009-2012. This pattern was reversed in 2008-2009.

Alviarez (UBC) Multinationals

FMN vs. domestic �rms growthFirm level evidence

(1) (2)Dep. Var.: γin,t(f)I{f∈FMN} 0.0207 0.0184

(0.0042) (0.0009)

I{f∈FMN} × I{t=2009} -0.0326 -0.0297(0.0093) (0.0023)

No. of Observations 31,521,858 31,521,858No. of Firms 6,639,262 6,639,262No. of Multinationals 214,851 214,851R2 0.0110 0.0240

Year Yes No

Dest×Year No Yes

Notes: Standard errors clustered at the source-destination level.

Alviarez (UBC) Multinationals

FMN vs. domestic �rms growth

−.0

20

.02

.04

For

eign

Affi

liate

Gro

wth

Diff

eren

tial

2005 2006 2007 2008 2009 2010 2011 2012Year

Alviarez (UBC) Multinationals

Observation 2

Within sectors, the a�liates of foreign multinational �rms

grew faster than similarly-sized domestic �rms in every

year between 2004-2012.

Much of the aggregate relative slowdown of multinational

�rms in 2008-2009 is accounted for by observable

di�erences in �rm size and by di�erences in the sectors in

which multinational �rms operate.

Alviarez (UBC) Multinationals

Understanding the collapse in multinationals

sales(1) (2) (3) (4)

Dep. Var.: γin,t(f)I{f∈FMN} 0.0207 0.0184 0.0177 0.0205

(0.0042) (0.0009) (0.0009) (0.0010)

I{f∈FMN} × I{t=2009} -0.0326 -0.0297 -0.0177 -0.0012(0.0093) (0.0023) (0.0020) (0.0017)

No. of Observations 31,521,858 31,521,858 31,302,684 31,302,216No. of Firms 6,639,262 6,639,262 6,563,480 6,563,408No. of Multinationals 214,851 214,851 212,988 212,981R2 0.0110 0.0240 0.0333 0.0422

Year Yes No No No

Dest×Year No Yes No No

Dest×Sect×Year No No Yes No

Dest×Sect×Quart×Year No No No Yes

Notes: Standard errors clustered at the source-destination level.

Alviarez (UBC) Multinationals

Propensity Score Matching

Alviarez (UBC) Multinationals

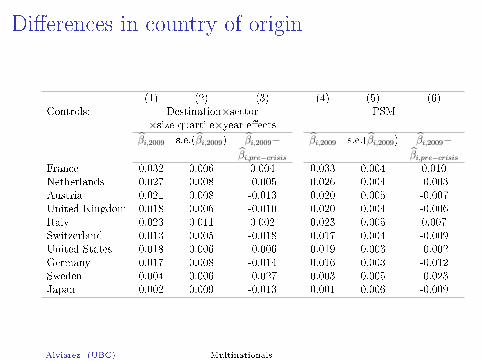

Observation 3

Multinationals from di�erent source countries fared

di�erently in the crisis

Implication: Impact of FMN decline will di�er acrosscountries hosting FMN from di�erent source countries

Alviarez (UBC) Multinationals

Di�erences in country of origin

(1) (2) (3) (4) (5) (6)Controls: Destination×sector PSM

×size quartile×year e�ectsβ̂i,2009 s.e.(β̂i,2009) β̂i,2009− β̂i,2009 s.e.(β̂i,2009) β̂i,2009−

β̂i,pre−crisis β̂i,pre−crisisFrance 0.032 0.006 0.004 0.033 0.004 0.010Netherlands 0.027 0.008 -0.005 0.026 0.004 -0.003Austria 0.021 0.008 -0.013 0.020 0.005 -0.007United Kingdom 0.018 0.006 -0.010 0.020 0.004 -0.006Italy 0.023 0.011 0.002 0.023 0.005 0.007Switzerland 0.013 0.005 -0.018 0.017 0.004 -0.009United States 0.018 0.006 -0.006 0.019 0.003 -0.002Germany 0.017 0.008 -0.014 0.016 0.003 -0.012Sweden 0.004 0.006 -0.027 0.003 0.005 -0.023Japan 0.002 0.009 -0.013 0.001 0.006 -0.009

Alviarez (UBC) Multinationals

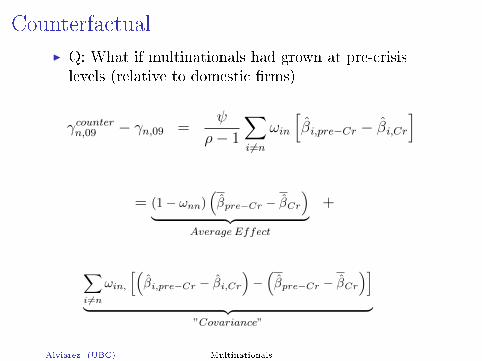

Counterfactual

I Q: What if multinationals had grown at pre-crisislevels (relative to domestic �rms)

γcountern,09 − γn,09 =ψ

ρ− 1

∑i 6=n

ωin

[β̂i,pre−Cr − β̂i,Cr

]

= (1− ωnn)(β̂pre−Cr − β̂Cr

)︸ ︷︷ ︸

Average Effect

+

∑i 6=n

ωin,

[(β̂i,pre−Cr − β̂i,Cr

)−(β̂pre−Cr − β̂Cr

)]︸ ︷︷ ︸

”Covariance”

Alviarez (UBC) Multinationals

Counterfactual

I Growth rates would have been 0.12 pp higher for the meancountry in the sample.

I And 0.18 pp on average in the top 10 destination countries

I MNCs contributed 0.5 pp s to the reduction in output inLithuania. The largest single source of foreignmulti-nationals in Lithuania is Poland, whose foreigna�liates did quite poorly in the crisis, with the growthdi�erential of -4.3% relative to the pre-crisis times.

I Estonia and Latvia were also among the countries mostnegatively a�ected. Sweden and Finland are the largestsources of foreign a�liates in these countries.

Alviarez (UBC) Multinationals

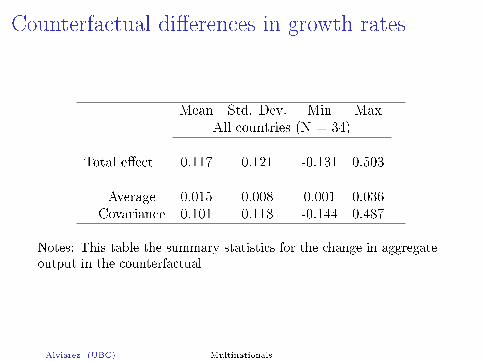

Counterfactual di�erences in growth rates

Mean Std. Dev. Min MaxAll countries (N = 34)

Total e�ect 0.117 0.121 -0.131 0.503

Average 0.015 0.008 0.001 0.036Covariance 0.101 0.118 -0.144 0.487

Notes: This table the summary statistics for the change in aggregateoutput in the counterfactual

Alviarez (UBC) Multinationals

Local Origin, Foreign Ownership:

Multinational amalgamation of brands

(with Thierry Mayer and Keith Head)

(Preliminary)

Alviarez (UBC) Multinationals

Rising concentration and brand amalgamation

I A feature of modern market economies is the dominance ofenormous multinational corporations (MNCs).

I Under the traditional view MNCs become so large byachieving economies of scale in a set of core productsdeveloped at headquarters.

I A lesser discussed route is the amalgamation of brandsdeveloped in multiple countries through cross-borderacquisitions.

Alviarez (UBC) Multinationals

Brand amalgamation: Beer

Alviarez (UBC) Multinationals

Why MNCs acquire foreign brands

I What the MNC wants:I Bypass the home bias that limits MNCs ability to sellit's existing roster of (foreign) brands.

I Acquire superstar brands that have multi-marketpotential.

I Why the MNC can outbid local owners:I The MNC has other brands that it can sell throughthe local target's distribution channels.

I The MNC has distribution assets in other marketsthat can be exploited to sell the targeted brand morewidely.

Alviarez (UBC) Multinationals

Examples of brand amalgamation

I US-based snack foods maker Mondelez (spun o� fromKraft), is the 2nd largest chocolate seller in the world.

I 81% of its chocolate sales via brands originating in Britain(Cadbury), Belgium (Cote d'Or), Switzerland (Toblerone,Milka), Norway (Freia, Marabou), and Greece (Lacta).

I Flagship brands are important, but represent a smallershare of big brewers' world sales:

I AB-Inbev: Budweiser 12.3%, Stella 4.2%.I Heineken brand: 27.3%.I Carlsberg brand: 17.8%

I Diageo, owner of Johnnie Walker, Smirno�,Tanqueray.I Had a market share of less than two percent in India before

it bought the local Group United Breweries, and now it hasa 39% market share.

Alviarez (UBC) Multinationals

This paper

I Documents the international expansion of MNCs throughthe acquisition of brands created in other countries.

I Quanti�es the impact of acquired brands on brand and�rm size heterogeneity.

I Uses a CES oligopoly multi-product model in order to inferbrand's appeal and delivered marginal cost, and estimatehow changes in brand's corporate headquarters a�ectconsumers' demand and �rms' costs.

I Constructs a counterfactual evaluating the impact ofchanges in brands' ownership matrix across countries onmarket concentration.

Alviarez (UBC) Multinationals

Dataset

I Unique dataset of sales value and/or volume for over83,000 brands owned by 46,000 companies, across 153product categories, in 79 countries (Global MarketInformation Dataset (GMID))

I Track national and cross-border changes in ownershipat the brand level occurred over 2006�2016.

I Apply classi�cation algorithm using Wikipedia, USPTO,and WIPO, to identify each brand's country of origin.

I Separate headquarter country of current owner from thecountry in which the brand was originally created.

I The headquarter country of each company in the dataset isobtained by name matching Orbis, Lexis Nexis and SDCplatinum database

Alviarez (UBC) Multinationals

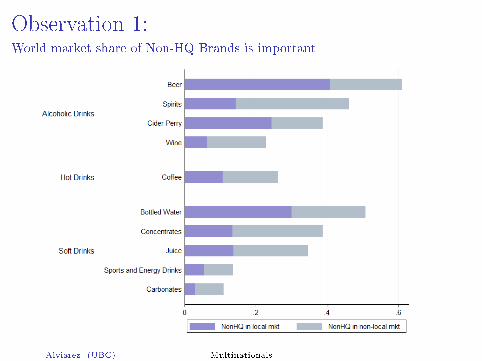

Observation 1:World market share of Non-HQ Brands is important

Alviarez (UBC) Multinationals

10 largest companies: Beer

Alviarez (UBC) Multinationals

Observation 2:NonHQ brands signi�cantly contribute to market concentration

Category CR4 CR4 (Non HQ)

Beer 0.86 0.56Bottled Water 0.71 0.37Carbonates 0.89 0.13Cider Perry 0.82 0.34Co�ee 0.82 0.25Concentrates 0.71 0.32Juice 0.63 0.35Spirits 0.60 0.32Sports and Energy Drinks 0.83 0.17Wine 0.55 0.19

Alviarez (UBC) Multinationals

Observation 3-5

I Observation 3: HQ brands�on average�are available inmore markets compare to NonHQ brands.

I Observation 4: Acquisition of NonHq brands is 18.5% morelikely the lower the market share of �agship brands.

I Observation 5: On average the price of acquired brandsincreases by 1.7%, and market share decreases by 2.3%after acquisition takes place.

Alviarez (UBC) Multinationals

A quantitative framework

We interpret the data from the lens of a quantitative frameworkin order to:

I Understand the role of the acquired portfolio of brands inexplaining the observed level of �rm heterogeneity.

I Quantify the impact of �acquired appeal�.I Quantify the cost e�ect of acquired brands.

Alviarez (UBC) Multinationals

Contribution of �original� and �acquired� brands

∆c lnYft =

Firm's Appeal︷ ︸︸ ︷(σ − 1)

[∆c

(NOfb

NfblnϕOft

)]︸ ︷︷ ︸

Appeal of Original Brands

+ (σ − 1)

[∆c

(NAfb

NfblnϕAft

)]︸ ︷︷ ︸

Appeal of Acquired Brands

+ ∆c lnNft︸ ︷︷ ︸Scope

+

Firm's Marginal Cost︷ ︸︸ ︷(σ − 1)∆c ln

(1

c̃Oft

)︸ ︷︷ ︸MC Original Brands

+ (σ − 1)∆c ln

(1

c̃Aft

)︸ ︷︷ ︸MC Acquired Brands

+ ∆c ln

[1

Nft

∑b∈B

(c̃ftcbt

ϕbt

)σ−1]︸ ︷︷ ︸

Cost-appeal covariance

− (σ − 1)∆c lnµft︸ ︷︷ ︸Markup

Alviarez (UBC) Multinationals

Contribution of acquired brands to appeal

Alviarez (UBC) Multinationals

Decomposing e�ects of frictionsln sbn lnAbn ln cbn lnµbn

mkt. share Appeal Bertrand Cournot Bertrand Cournot

Brand originshome 0.980a 0.315a -0.179a -0.260a 0.051a 0.128a

(0.097) (0.068) (0.028) (0.031) (0.008) (0.017)ln dist -0.178a -0.052a 0.051a 0.058a -0.006b -0.014a

(0.027) (0.020) (0.011) (0.011) (0.003) (0.005)lang 0.163a 0.010 -0.071a -0.081a 0.005 0.011

(0.063) (0.051) (0.025) (0.026) (0.006) (0.011)Corporate Headquartershome 0.136c 0.024 -0.040 -0.065b 0.015b 0.040b

(0.077) (0.053) (0.026) (0.029) (0.007) (0.016)ln dist -0.033 -0.026 -0.000 0.003 -0.003 -0.008c

(0.022) (0.016) (0.009) (0.009) (0.002) (0.005)lang 0.066 0.062 0.021 0.028 -0.007 -0.012

(0.052) (0.042) (0.022) (0.024) (0.006) (0.012)Observations 142413 138153 138139 138139 144579 144579R2 0.717 0.642 0.986 0.984 0.888 0.846

Alviarez (UBC) Multinationals

Discussion of results

I While the pooled regressions hide cross-categoryheterogeneity, on average, home-origin brands have hugeadvantages: Since exp(0.98) ≈ 2.66, home increases marketshare by 166%.

I The largest impact comes on the taste side (home bias):Being a home brand raises demand equivalent to a 37%price change.

I Cost advantages of home brands are also substantial,especially under Cournot.

I Brands from nearby countries also have appeal and costadvantages.

I Brands sell somewhat better in their HQ country, evenholding brand origin constant, mainly a cost e�ect (4�7%advantage).

Alviarez (UBC) Multinationals

Forced divestiture of foreign-owned,

domestic-origin brandsCounterfactual

I What is the cumulative impact on concentration andconsumer surplus from all the brand acquisitions of MNCs?

I One way to answer this is to start from the status quo andimagine a policy compelling each foreign-owned �rm to sello� the brand it owns that originate in the local market.

I We do this by creating counterfactual owners for thesebrands.

I Then, we use the Bertrand and Cournot versions of theCES oligopoly model to predict market shares andmarkups in this counterfactual.

Alviarez (UBC) Multinationals

Divestitures of acquired local brands

Bertrand

0.0 0.2 0.4 0.6 0.8

010

0020

0030

0040

0050

0060

0070

00

Share of foreign−owned, domestic origin

Mar

ket c

once

ntra

tion

(Her

finda

hl in

dex)

US

CN

JP

BR

GB

DE

MXKR

ESAU

RU

CA

FR

ZA

IT

2016 dataCF divestment

(#) %change in price index

high concentration (EU guidelines)(−1)

(−1)

(0)

(−18)

(−1)

(0)

(−5)(−6)

(−3)(−5)

(−3)

(−9)(−4)

(−38)

(−1)

Alviarez (UBC) Multinationals