Embed Size (px)

Citation preview

Indonesia’s Challenges toward Industrial Upgrading

11 August 2017

Yuri Sato

Executive Vice President

Institute of Developing Economies

Japan External Trade Organization

(IDE-JETRO)

Indonesia = Japan 2nd Industrial DialogueJICA mission @ Bappenas

1. Indonesia’s Advantages

2. Challenges Facing Indonesia

- From Deindustrialization

to Reindustrialization

- Weak Productivity

- Weak Financial Intermediation

3. Assessing Economic Reform Policies

4. Conclusion

2

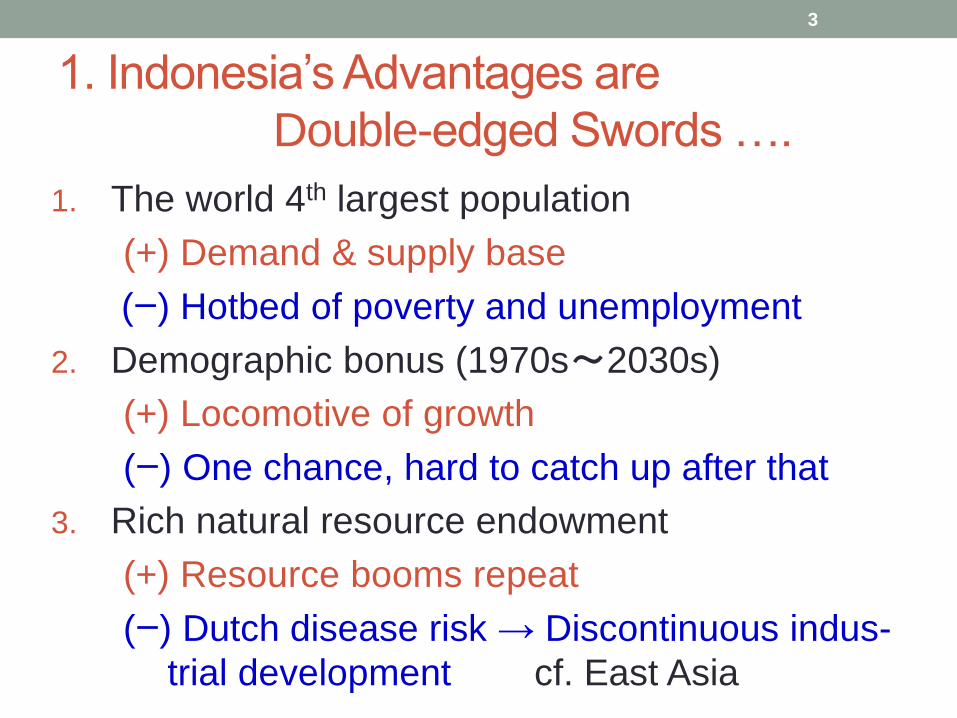

1. Indonesia’s Advantages are

Double-edged Swords ….

1. The world 4th largest population

(+) Demand & supply base

(ー) Hotbed of poverty and unemployment

2. Demographic bonus (1970s~2030s)

(+) Locomotive of growth

(ー) One chance, hard to catch up after that

3. Rich natural resource endowment

(+) Resource booms repeat

(ー) Dutch disease risk → Discontinuous indus-

trial development cf. East Asia

3

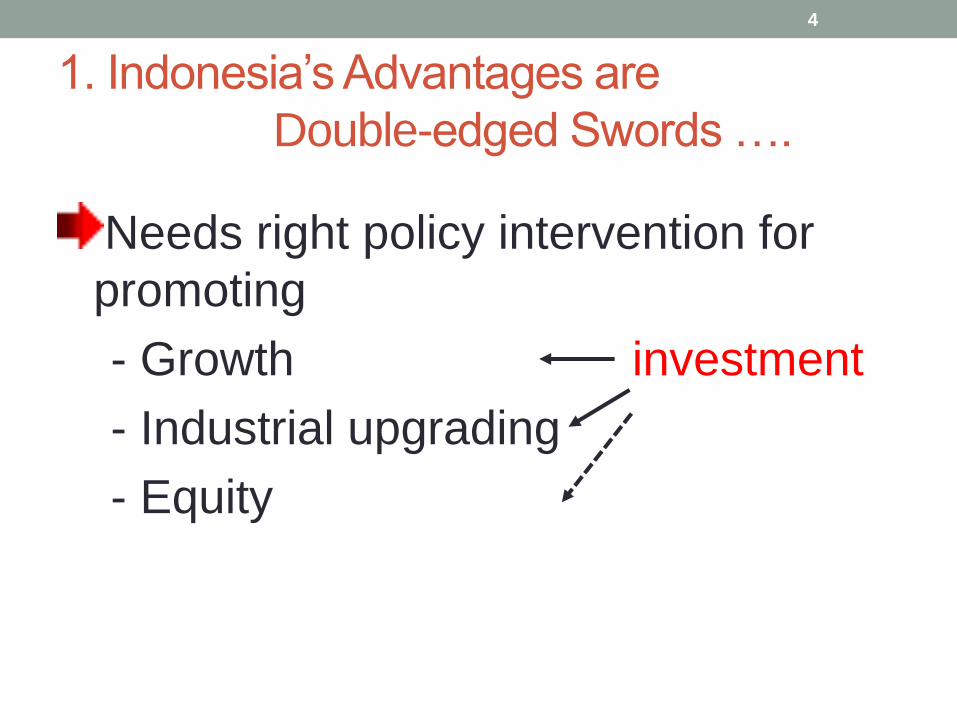

1. Indonesia’s Advantages are

Double-edged Swords ….

Needs right policy intervention for

promoting

- Growth investment

- Industrial upgrading

- Equity

4

0

10

20

30

40

50

19

70

19

73

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

20

06

20

09

20

12

20

15

Authoritarian Developmental Regime (Soeharto Regime)

(%)

Agriculture, Fishery, Forestry

Mining

Manufacturing

Democracy

Service industries

Transition period

Commodity boomOil boom

2. Challenges Facing Indonesia

Rise and Fall of Manufacturing Share

5

• Under the authoritarian

developmental regime, the

manufacturing share

constantly increased, even

in the oil booms.

• “Full-set industrialization”

(resource-based +

labor- intensive +

capital-intensive industries)

progressed.

• However, In the 2000s

commodity boom,

Indonesia moved to

deindustrialization.Note: Base year of GDP is 2000 up to 2012, and 2010 after 2013.

Source: BPS Indonesia (Central Agency of Statistics).

Shares in GDP (1970-2016)

2. Challenges Facing Indonesia

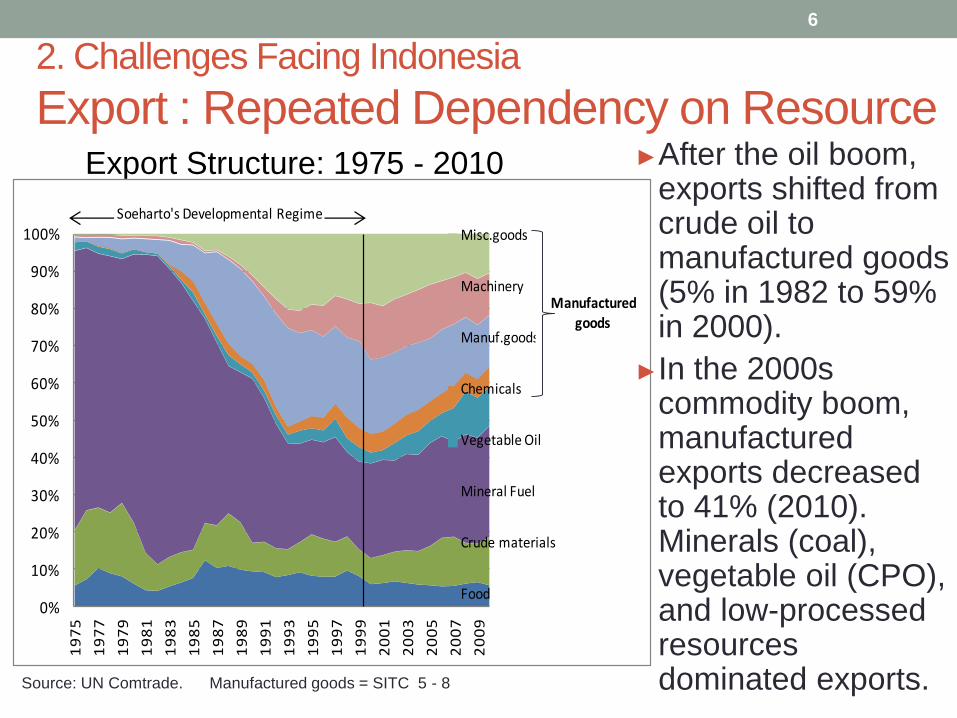

Export : Repeated Dependency on Resource

6

Export Structure: 1975 - 2010

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

Misc.goods

Machinery

Manuf.goods

Chemicals

Vegetable Oil

Mineral Fuel

Crude materials

Food

Soeharto's Developmental Regime

Manufactured goods

Source: UN Comtrade. Manufactured goods = SITC 5 - 8

►After the oil boom, exports shifted from crude oil to manufactured goods (5% in 1982 to 59% in 2000).

►In the 2000s commodity boom, manufactured exports decreased to 41% (2010). Minerals (coal), vegetable oil (CPO), and low-processed resources dominated exports.

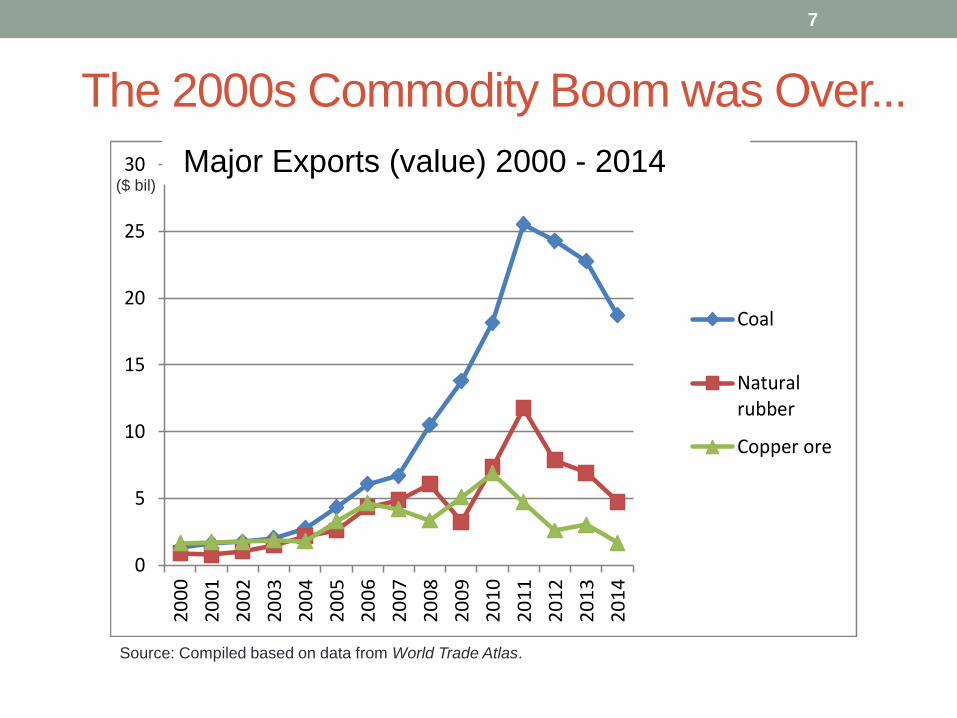

The 2000s Commodity Boom was Over...

0

5

10

15

20

25

302

00

0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Coal

Naturalrubber

Copper ore

7

Source: Compiled based on data from World Trade Atlas.

($ bil)Major Exports (value) 2000 - 2014

Some Manufactured Exports Picking Up

0.0

0.5

1.0

1.5

2.0

2.5

3.02

00

0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Motor cars

Plywood

Fattyacid/alcoholFootwear

8

Source: Compiled based on data from World Trade Atlas.

($ bil)

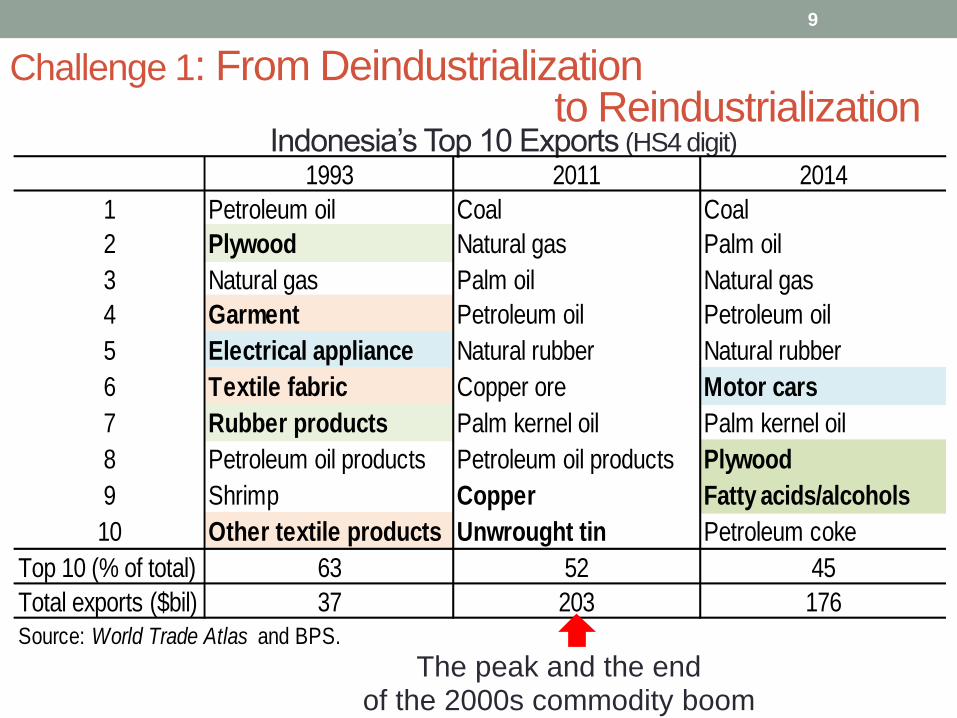

The peak and the end of the 2000s commodity boom

Indonesia’s Top 10 Exports (HS4 digit)

9

1993 2011 2014

1 Petroleum oil Coal Coal

2 Plywood Natural gas Palm oil

3 Natural gas Palm oil Natural gas

4 Garment Petroleum oil Petroleum oil

5 Electrical appliance Natural rubber Natural rubber

6 Textile fabric Copper ore Motor cars

7 Rubber products Palm kernel oil Palm kernel oil

8 Petroleum oil products Petroleum oil products Plywood

9 Shrimp Copper Fatty acids/alcohols

10 Other textile products Unwrought tin Petroleum coke

Top 10 (% of total) 63 52 45

Total exports ($bil) 37 203 176

Source: World Trade Atlas and BPS.

Challenge 1: From Deindustrialization to Reindustrialization

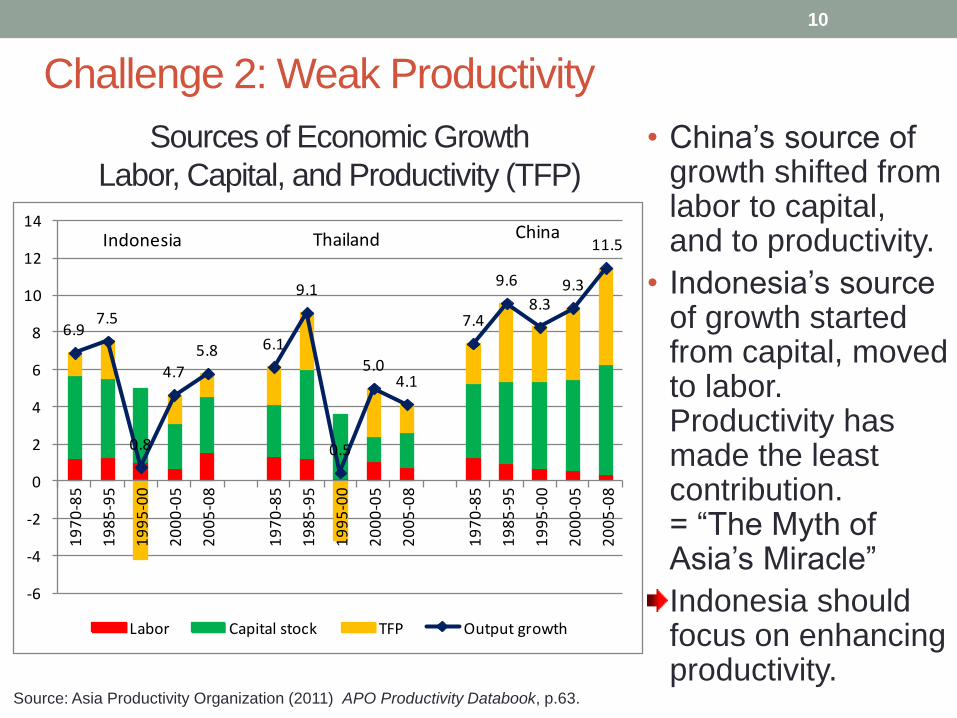

Sources of Economic Growth

Labor, Capital, and Productivity (TFP)

10

• China’s source of growth shifted from labor to capital, and to productivity.

• Indonesia’s source of growth started from capital, moved to labor. Productivity has made the least contribution. = “The Myth of Asia’s Miracle”

Indonesia shouldfocus on enhancing productivity.

Source: Asia Productivity Organization (2011) APO Productivity Databook, p.63.

6.97.5

0.8

4.7

5.8 6.1

9.1

0.5

5.04.1

7.4

9.6

8.39.3

11.5

-6

-4

-2

0

2

4

6

8

10

12

14

19

70

-85

19

85

-95

19

95

-00

20

00

-05

20

05

-08

19

70

-85

19

85

-95

19

95

-00

20

00

-05

20

05

-08

19

70

-85

19

85

-95

19

95

-00

20

00

-05

20

05

-08

Labor Capital stock TFP Output growth

Indonesia Thailand China

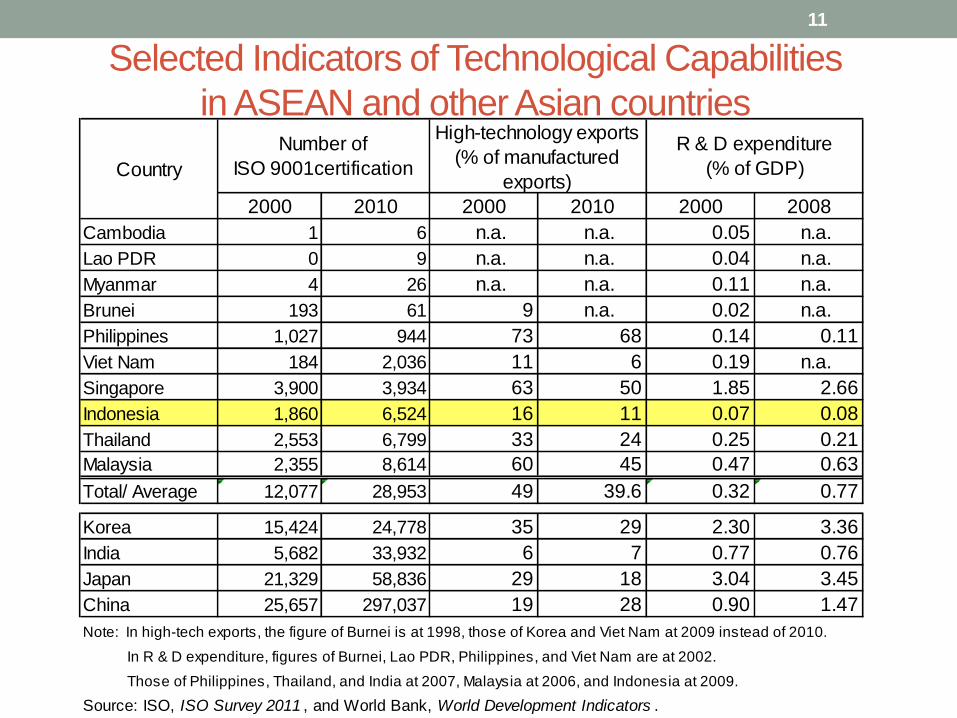

Challenge 2: Weak Productivity

Selected Indicators of Technological Capabilities

in ASEAN and other Asian countries

11

2000 2010 2000 2010 2000 2008

Cambodia 1 6 n.a. n.a. 0.05 n.a.

Lao PDR 0 9 n.a. n.a. 0.04 n.a.

Myanmar 4 26 n.a. n.a. 0.11 n.a.

Brunei 193 61 9 n.a. 0.02 n.a.

Philippines 1,027 944 73 68 0.14 0.11

Viet Nam 184 2,036 11 6 0.19 n.a.

Singapore 3,900 3,934 63 50 1.85 2.66

Indonesia 1,860 6,524 16 11 0.07 0.08

Thailand 2,553 6,799 33 24 0.25 0.21

Malaysia 2,355 8,614 60 45 0.47 0.63

Total/ Average 12,077 28,953 49 39.6 0.32 0.77

Korea 15,424 24,778 35 29 2.30 3.36

India 5,682 33,932 6 7 0.77 0.76

Japan 21,329 58,836 29 18 3.04 3.45

China 25,657 297,037 19 28 0.90 1.47

Note: In high-tech exports, the figure of Burnei is at 1998, those of Korea and Viet Nam at 2009 instead of 2010.

In R & D expenditure, figures of Burnei, Lao PDR, Philippines, and Viet Nam are at 2002.

Those of Philippines, Thailand, and India at 2007, Malaysia at 2006, and Indonesia at 2009.

Source: ISO, ISO Survey 2011 , and World Bank, World Development Indicators .

Country

Number of

ISO 9001certification

High-technology exports

(% of manufactured

exports)

R & D expenditure

(% of GDP)

0

20

40

60

80

100

120

140

160

180

200

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

China

Malaysia

Thailand

Vietnam

India

Indonesia

(%)

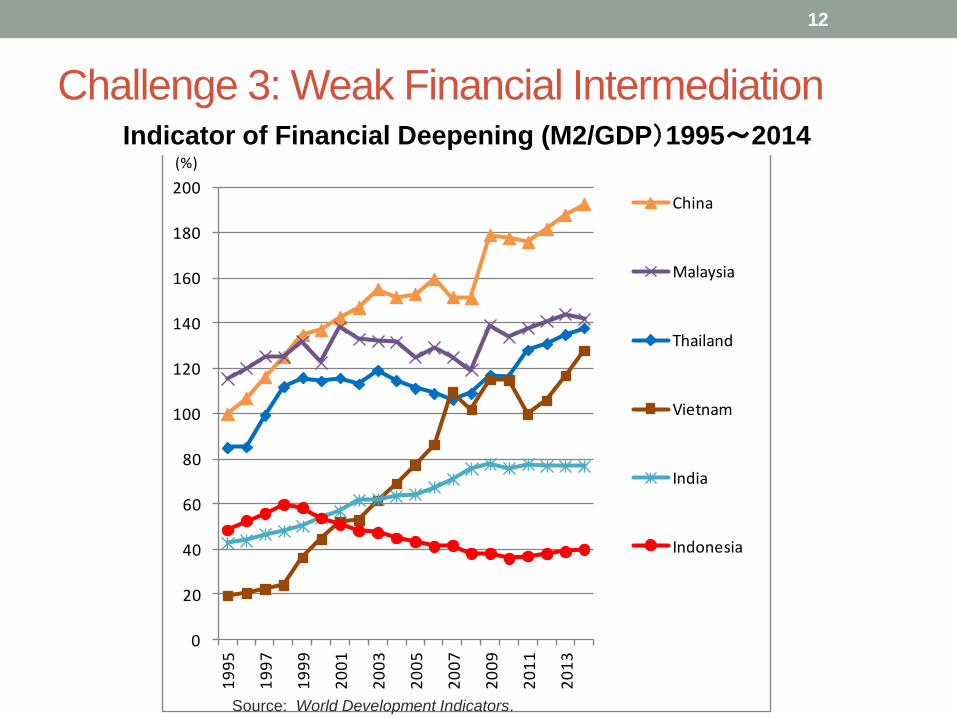

Challenge 3: Weak Financial Intermediation

12

Indicator of Financial Deepening (M2/GDP)1995~2014

Source: World Development Indicators.

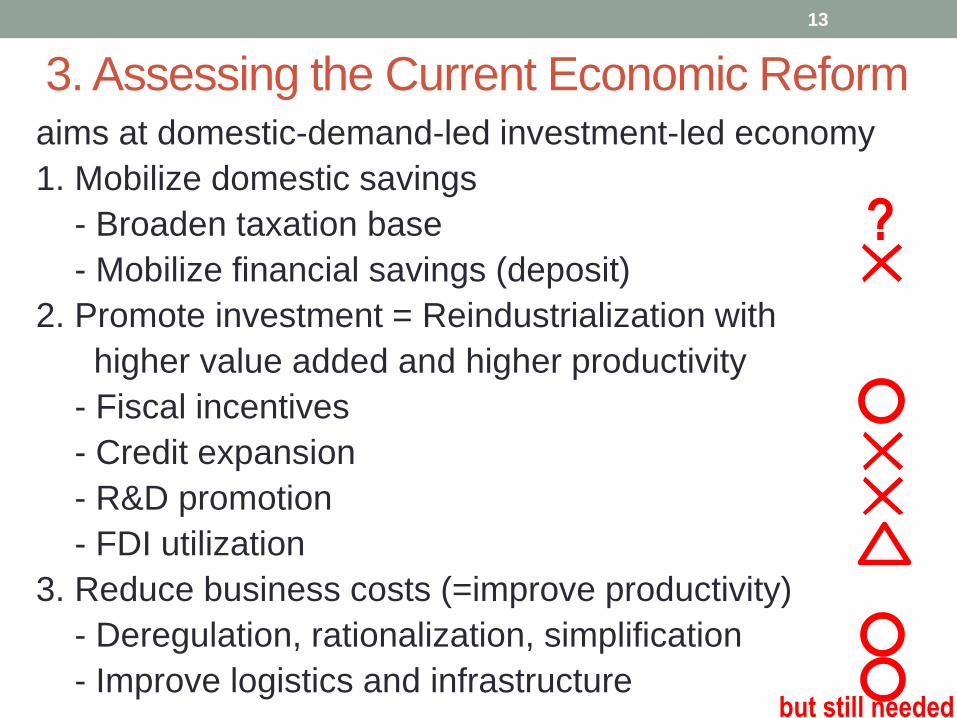

aims at domestic-demand-led investment-led economy

1. Mobilize domestic savings

- Broaden taxation base

- Mobilize financial savings (deposit)

2. Promote investment = Reindustrialization with

higher value added and higher productivity

- Fiscal incentives

- Credit expansion

- R&D promotion

- FDI utilization

3. Reduce business costs (=improve productivity)

- Deregulation, rationalization, simplification

- Improve logistics and infrastructure

3. Assessing the Current Economic Reform

13

but still needed

?

Conclusion

► Indonesia is amid the phase of critical importance,

an unrepeatable chance of demographic bonus.

► Higher growth accompanied with industrial

upgrading should be pursued. Reindustrialization

with higher value added and higher productivity

would be the key indicator.

► It is crucial to make smart policy intervention in

order to boost domestic-demand-led growth by

mobilizing savings, investing them toward

industrial upgrading, and reducing business costs.

Government efforts of economic reform need to be

more intensified.

14