Embed Size (px)

Citation preview

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 1/84

1

Pricing Strategy and its Success of Automobile Manufacturers in India

Prepared by

Pratyusha

Submitted to

Date Submitted

Word Count

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 2/84

2

Contents

Abstract 4

1: Introduction 4

1.1 Background to the research 4

1.2 Relevance of the topic for management study 5

1.3 Purpose of Research and Aims 6

1.4 Structure of the Rest of the Report 6

2: Literature Review 6

2.1 Theory 7

2.2 Results of Various Empirical Researches 14

Chapter 3: Economy 16

3.1: Indian Economy & Auto Sector 17

3.2: Indian Auto Industry 24

Chapter 4: Methodology 25

4.1 Types of Research 25

4.2: The Research Problem & Style Chosen 25

4.3 Hypothesis 26

4.4 Research Question 26

4.5 methods of Analysis 26

4.6 Data Sources 28

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 3/84

3

5. Analysis and Findings 28

5.1 Critical Appraisal of Literature 28

5.2 Study through Statistical analysis (Analysis of Data)

Graphical Appreciation 32

5.3: 5.3: Study through theoretical models 46

6. Discussion 47

6.1 Interpretation of results and answer to the research question 50

6.2 Evaluation of answer with existing

theory and previous empirical research 51

7. Conclusion 52

7.1 Conclusion, evaluation of hypothesis 53

7.2 Reflection on the work 55

7.3 Limitations of Current Research 55

7.4 Recommendations for the further work 56

8. Appendices 57

8. List of References 82

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 4/84

4

Abstract:

The problem that is addressed in this paper is about profitability of Indian auto market and

the way the firms are framing a pricing strategy as well as the products to maintain profits.

The paper explores the growth and changes in Indian auto market as well as in componentindustry that made the automobile manufacturing more local than in the past. The literature

review finds the changes that made Indian Auto market capable of producing and selling

more thus breaking the thresholds of the past. The financial performance of five companies

in five years starting from 2005 to 2009 is used to find the performance of the firms and the

demand in Indian market. This needed a solution because, the Indian market is price sensitive

and the pricing strategies of the firms are important in marketing as well as production. The

proposed achievement is to establish the linkage between prices, production, marketing as

well as supply chain as these aspects decide the course of pricing strategy of the company

regarding its products. Ratio analysis and correlation are used to obtain the details of

profitability and financial performance of different companies and the correlation between

profits for five years for each company are used to decide the profitability even in the period

of decrease of sales for the companies like Hindustan Motors. The result of the paper is to

know the pricing strategy is crucial as well as the design of the product and target customers

for an automobile company to increase its performance as well as profitability.

Chapter 1: Introduction

1.1 Background to the Research

The current interest in the problem mentioned in this paper is due to price sensitiveness

of Indian market, which has large customer base that consider price before trying a car.

Coming to the commercial activities in a developing country in India, there are activities

that offer large profits as well as small margins. The customers who afford for luxury

vehicles are also present but less in number. However, both economy and luxury models

find market but the strategy of targeting the customers in luxury models and pricing the

products and offering margins to the dealers is crucial in the context of economy models.

The more retail counters the more the sales and the more servicing centers, the more the

reputation and increase of sales in the future. These aspects of more retain counters and

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 5/84

5

servicing centers and the way Maruti and Tata Motors used to increase their sales and

thus profitability are reviewed. This complex background that makes the strategic

thinking of automobile firms a complex activity is a reason to select this aspect for the

research. The aspect that finds relevance for management study is the review of the

emergence of automobile market in India, which is full of management strategies used by

Multinational Companies to produce their cars in Indian Market. These strategies served

as background for the managements’ designing capabilities so that they can produce

small cars and light commercial vehicles for Indian Auto Market. Though the pricing

strategy is paramount for Indian automobile companies to find success in the market,

Tata Motors did not overcome Maruti’s sales even with the cheapest car in the world;

Nano. However, Maruti’s cars are not costly but still the company offers different models

and more service points than any other company. Even in this context of competition

from Maruti, the way Tata Motors dominates the overall Indian Automobile Market with

the diversity in its products ranging from small cars via LCVs to heavy automobiles is

also suitable for study that gives information about success strategies in auto market like

country in India.

1.2 Relevance of the topic for management study

The topic being studied is related to the management subject because; the management of automobile firms should integrate production, marketing and designing activities before

deciding the price of the product. The efficient management of supply chain of the

company also is crucial and this whole aspect receives the attention necessary as a

management subject. The ratio analysis in the paper indicates the profitability and the

capability of the Indian automobile companies in using their assets to increase sales. The

topics relevant to management in this aspect are about managing assets to increase sales

without decrease in profit. Though the profit margin is less, the management aspect in

this context is to increase the magnitude of sales to get more magnitude of profit, even in

the presence of lesser margins.

Purpose of the research and aims

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 6/84

6

As the pricing strategy is important in Indian automobile market, the success of different

pricing strategies can be explored even in the presence of cheaper and cheapest cars in

the market. The presence of diversified customer base also provides a complex situation

to study. The aim is to find the effect of pricing strategy on the performance of the firm

and its profitability. The aspects like reducing the capacity of the car to minimize the

price for Indian market and the plans of Maruti and Tata Motors regarding that aspect are

discussed. The aim of this review and discussion is to evaluate the way the Indian

automobile manufacturers are using their capabilities to offer four wheelers at affordable

price to middle class customers. The purpose of the research is to analyze and evaluate

the financial and sales activities in order to find the extent of profitability the Indian

automobile companies are achieving.

1.3 Structure of the rest of the report

The further structure of the paper is as follows:

Chapter 2: Reviews the literature linking the relation.

Chapter 3: Economy

Chapter 4: Methodology

Chapter 5: Analysis of Findings

Chapter 6: Discussion

Chapter 7: Conclusion

Chapter 2: Literature Review

Chapter 8: References.

The paper deals with profitability and pricing strategy of Indian Auto Market. The literature

review starts with reviewing the role of cost effective nature of purchasing activities as well as

supply chain management in auto industry. This is because; the collaboration between

automotive manufacturers and auto parts supplies is necessary in auto industry to produce

automotives.

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 7/84

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 8/84

8

collaborative relationship forever. They have to select the behavior models to maintain that

relationship. The cost effective nature of these activities affect profitability. Regarding this,

authors quote Gordon and Laura (1991) about profit centre strategy. One such strategy is to

invest in new technologies of production. The existence of competition between suppliers

decides the minimization effect of transaction cost. However, if the firms are leading in their

technology and quality, may not give more importance to pricing strategy as they do not give

much importance to transaction cost. Even then, the supplier management in automotive industry

demonstrates the aspects that affect the transaction cost. Hence, it is important for automotive

companies to select appropriate partners in supply chain. The transaction costs and pricing

strategy can be affected seriously by supplies in the presence of exists oligopoly market. In this

context, the considerations of contracts can stabilize price and preserves long term market for

both suppliers and firms. However, if the market is monopolistic, there exists no competition and

the aspect depends on production behavior (Chia-MinWei., Chia-Yon Chen, 2008, p.973-980).

While considering the production behavior, it is crucial to consider the significant component of

Indian economy that turned global from 1991. The auto industry also found demand in the global

market by supplying components to the countries in Asia and Africa thus increasing the

prospects of profitability. Regarding this aspect Singh, Garg, Deshmukh (2008, p.24) mention

the business environment that depends more on knowledge rather than the tangible resources.

The industry does not deny the necessity of tangible resources, but the knowledge base it is

highly relying guides the industry in making optimal use of them. As the topic of review is auto

industry, the component industry finding place in domestic as well as global market affects the

firms in India. The better quality components produced by the component manufacturing firms in

India are capable of producing quality automotives in India thus increasing the export

opportunities. Though the constraints for growth and lack of support from government stay, but

the demand from the domestic and global market is driving the Indian auto industry. In the

environment of only minimal support from the side of government, the strategies of manufacturers are important. The authors quote the value of components shipped from India at

$177 million in 2002 and that is far less than Mexico and Brazil as well as China. Though there

is much to achieve in exporting, the present exports are better than before. The component and

automotive manufacturers in India are investing more money in research to develop the

knowledge base. This will be helpful in competing with the quality of competitors in

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 9/84

9

international market. One such area the manufacturers have to concentrate is on identity niches

that happen by the development of new products. The new products should have quality

standards also more than the international and domestic competitors. While doing this, it is

essential for the manufacturers to have a two pronged strategy. One is for the domestic market

and the other for international market. As the domestic market is price sensitive, the components

as well as the automotives also should attract customers with competitive prices. This

competitive pricing strategy will be useful for the developing countries like India in Asia and

Africa. Regarding the other prong of the strategy, it is important to concentrate on quality aspect,

even the price is not competitive. In this strategy, the establishment of identity niche is

necessary. The quality also important for Indian auto components industry as the countries like

US made clear that they consider the quality of the products while importing them. As US is the

biggest business partner for India to which the country is exporting majority of its exports, it is

crucial for the Indian government to encourage the manufacturers to concentrate on quality. This

increases international business for the auto industry thus increasing the profitability. The

increase in the quality reduces the rate of rejection and the authors quote Munial Shows Ltd.,

which produces shockers for Hero Honda and Maruti that set the target of reducing the rejection

rate from 1000ppm to 500ppm. In a similar manner, when the remaining companies also do the

same thing, the auto industry gets two benefits. The first one is that the domestic automotive

manufacturers get the spares at the cheaper rate than before and the component manufacturerscan bag export opportunities due to their quality in their products (Rajesh K. Singh, Suresh K.

Garg and S.G. Deshmukh, 2008, p.24-25).

While considering the effect and development of component industry in India, it is crucial to

consider its beginning as it is after 1960.The short history of development is filled with the needs

of the indigenous vehicle assembly, which is not in line with the international competition.

However, the changes after 1991, which comprise of abolishment of licensing requirements as

well as promotion of exports also resulted in relaxation of MRTP and liberalization of economy.Regarding this aspect, Rajesh K Singh, Suresh K Garg and S.G. Deshmukh (2007, p.286) quotes

the collaborations of the component sectors with the foreign companies for growth. The

liberalized economy and collaboration with foreign companies resulted in growth of domestic

market by 26.5 percent and the international market by 11 percent for Indian component

industry. However, the bulk of exports are targeted at Asia and Africa but not to developed

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 10/84

10

countries in Europe or to USA. Even then, this can be considered as the remarkable development

for Indian component sector when compared to its sluggish growth in past. However, the

component sector also eyed the market in developed countries and the companies like Sundaram

Fasteners are supplying radiator caps to GM, Caterpillar and others. The castings used in Lucas

Industries in Germany are supplied by Brakes India. The shock absorbers used by Yamaha-SOQI

are from Gabriel India. The Rockwell Company imports axle systems from Bharat forge. These

suppliers have entered into market of development countries by developing quality in their

products. Along with this, the component industry concentrated on volume capacities to make

the production cost effective. Even then the component industry as well as automotive industry

in India is small in turnover and production when compared to global firms. For example, the

component industry is smaller than the annual turnover of Visteon, whose global revenue is US

$20 billion in 2002. Moreover, the Indian auto component manufacturing firms can be

considered as SMEs when compared to global level component manufacturers. However, the

liberalization of economies at global level offered opportunities to Indian component Industry as

the companies like Ford, GM, Suzuki, Honda, Mercedes, and Daewoo in car segment and

Piaggio, Suzuki, Honda, Yamana, Kawasaki in motorcycle segment have started procurement of

spares through international operations. Though these operations offered large customer base in

which Indian component vendors can rely on; the research and development, testing and

validation involved in the supplies to the international automotive makers made it difficult tothem to grab the opportunity. The reason is that the domestic manufacturers used to give them

the specifications of the spares necessary for them. Hence, the R&D part of the work used to be

carried by the automotive assembling companies. There is very little pressure on component

sector to do so in the past. However, the international market that is luring the Indian component

sector is putting the responsibilities of research, development and validation of the products on

vendors. They international companies want full service suppliers, whom they term as FSS at

lowest cost. This is in sharp contrast to the market they faced in the past, which required only the

manufacturers. As a result, the Indian component manufacturers are forced to develop forward

strategies with the above challenges in mind. In this context, the strategies of competitiveness

need to be more polished. The production activities of the component manufacturers are

demanding more knowledge intensive strategies that are complex in an uncertain environment.

The uncertainty can be reduced or minimized with high quality in components speedy delivery of

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 11/84

11

them to the companies, low price and bigger volume as well as product flexibility. The important

of all these things are knowledge and technology regarding manufacturing of components.

Consequently, in sustaining competitiveness in the uncertain and competitive market, the Indian

component manufacturers faced pressures and constraints due to their limited resources to

knowledge and technology as they are not used up to research and development. Hence, the

strategies that nullify the negative effects of changing environment are being delayed and this

hampers growth of the sector. However the growth of Indian automotive industry is offering

enough resources to overcome the just mentioned constraints to some extent (Rajesh K. Singh,

Suresh K. Garg and S.G. Deshmukh, 2007, p. 285-287).

Hence, need of the Indian automotive component manufacturers is to capture a value for their

product in international market. They have to offer a wide array of products to diverse industrial

applications, so that they can act as facilitating goods that enable the quality outcome for the end

product. The first aspect is to achieve quality along with substantial plant load factor, so that

large batches can be delivered when manufacturers are satisfied. The achievement of quality and

plant load factor by the component supplier should be supported by good logistic support by the

administration to transport the goods to customers. Before exploring these two activities of

quality-plant load factor and logistics, the company has to study its market to decide the nature

of the product it can supply. Regarding this aspect, Paul Matthyssens, Koen Vandenbempt,

Caroline Goubau (2007, p.57) quotes an European based firm that supplies materials to

automobiles, service centers, packaging, construction industries. However, the component

suppliers from India, whom the paper mentioned till now are not producing the materials of such

a wide array. This implies that their technological knowledge base is limited and that may result

in hampering the business. The first task of the Indian auto component manufacturers is to

manufacture two or more types of automotive spares, so that the automotive manufacturers

prefer them. In this context, it is essential for the component manufacturers to keep in view the

types of applications of their spares that decide the pricing level, which eventually decides the profit. They have to offer tactical or opportunistic pricing in the international market, when there

is presence of new customer in the market. First of all, they have to enter the market with

penetration price and impress the automotive manufacturers with their quality. When the

customer’s product depends on the supplier’s spares, then the component manufacturer can

decide the price that offers higher profit than in the past. However, the component manufacturers

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 12/84

12

need to consider the competition in international market, which decides the price leverage of the

component manufacturer and automotive assembler. The point that is being emphasized here is

that the component manufacturer should enter into the group of the suppliers who are capable of

deciding the value-based pricing. As there is not straight forward method to decide the value of

the component manufactured, the acceptance of the automotive assembler is crucial here.

However, the review emphasizes the regional nature of Indian automotive manufacturers that is

confined to India and such developing countries. Hence, in this context, it is realistic to mention

the regional nature of different parts of the world. Regarding this regional nature, Alain Verbeke

& Paul Brugman (2005, p.97) cites Rugman’s demonstration about vast majority of the world

that is regional in nature. Hence, as per Rugman’s conclusion, there is no global automotive firm

and the companies entered into Indian auto market realized that aspect and collaborated with

Indian companies to manufacture vehicles according to the needs and affordability of Indian

customers. Hence, the MNCs that entered into Indian auto market acted as ‘the regional

multinationals’ mentioned by Rugman. The reason is that the firms tried to find a region to

expand their business without disturbing their businesses in their respective countries. Hence, a

separate management entity is necessary that can act according to the regional conditions in

India. This resulted in selecting a partner in Indian automobile market so that the partner can take

care of design of the products as well as its marketing. The MNCs have offered technological

advances and helped in supply chain management as the Indian companies need to import some

components. However, the entry of MNCs into Indian market has also developed the component

industry in India so that the necessity of importing them has decreased for Indian automobile

manufacturers. This resulted in inter-regional expansion for all the companies and this further

resulted in inter-regional completion thus decreasing prices of the vehicles in Indian market.

However, the competition in Indian market is not as strong as it is in North America, Europe and

Japan and there are investment opportunities as well. Hence, the Indian automotive

manufacturers have concentrated on pricing strategies to capture the auto market in the country.The reason is that though the prices are less in the Indian auto market, the companies are

adopting lean manufacturing technologies that are even reducing the capacities of the vehicles

according to the affordability of the targeted customer base. However, the strategy has paid

dividends to the Indian automobile companies that are collaborated with the foreign ones as they

have sold large number of vehicles (Alain Verbeke & Paul Brugman, 2005, p. 97-113). In

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 13/84

13

contrast to that the company Hindustan Motors is not able to get profits as it failed to increase its

sales by decreasing the prices as well as the capacities of the vehicles. Hence, it is crucial to have

components at lesser prices to manufacture vehicles and get profit in Indian profit as HM did not

concentrate on that aspect. Regarding this aspect, it will be germane to mention the state of Guru

Prakash Prabhakar (2010, p. 1010-1011) that what is right in France may not click in India and

vice versa. The reason is cultural differences and in the context of automotives, the reason may

be the price and model of the cars and other vehicles. The research concludes that the pricing

strategy is crucial in India due to the emergence of middle class population and it was taped by

Tata, Maruti and Mahindra. Tata Motors even launched the world’s cheapest car for Rs. 1,00,000

(approx $2600) to capture the customer base of middle class. Hence, the common type of

pressure that is encountered by the automotive firms in India is about pricing and then the design

that enables the affordable price for the customer. Regarding this aspect the author cites the fact

that the company Fiat, which is successful in Western countries is facing stiff competition from

Maruti and Tata as well as Mahindra as these companies are releasing vehicles with lesser price

and they designed them so. However, the companies like Fiat are not successful in doing so and

failed to attract the middle class customer base in India (Guru Prakash Prabhakar, 2010, p. 1010-

1020). However, there is potentiality in Indian market even in the context of low pricing.

Carmaker Renault entered into the Indian market with the product ‘Logan’ with a price of

$10,000 (5,000 GBP). Though the price is less when compared to the prices in Westerncountries, the company with its Indian partner is planning to release still cheaper version.

Though there is chance of decreasing profit for a single vehicle, the forecasting of increase of

Indian auto market by 50 percent by 2010 prompted that company to release the cheaper

products. Hence, the Indian automobile manufacturers are planning to sell low price and low

profitable vehicles more in number to get a huge profit. In this context, The Company might be

prompted from the words of Tata Motors MD Ravi Kant who says that the company releases

Nano for the people who carry their families on two wheelers. Hence, Renault-Nissan is still far

away from the strategies of Tata Motors coming to the point of designing the cheapest

automobiles and planning the pricing strategies in that manner. However, the foreign companies

are not giving up and there is news that Toyota is planning an even more low cost car that

reflects the changes in design as well as sourcing and production. These companies are framing

strategies regarding design and pricing mixed with supply chain management keeping in view

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 14/84

14

the emerging markets in countries like India. Hence, the review of empirical researches

regarding India can help in further research for the paper.

2.2: Results of Various Empirical Researches

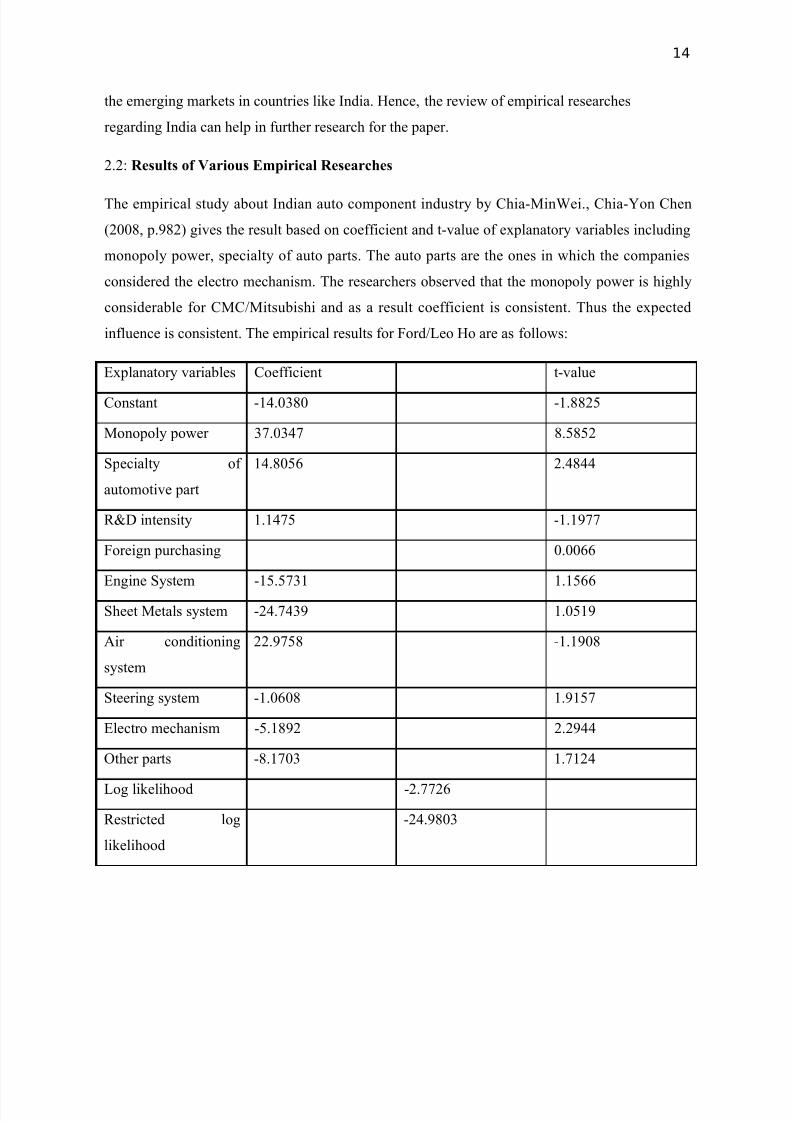

The empirical study about Indian auto component industry by Chia-MinWei., Chia-Yon Chen

(2008, p.982) gives the result based on coefficient and t-value of explanatory variables including

monopoly power, specialty of auto parts. The auto parts are the ones in which the companies

considered the electro mechanism. The researchers observed that the monopoly power is highly

considerable for CMC/Mitsubishi and as a result coefficient is consistent. Thus the expected

influence is consistent. The empirical results for Ford/Leo Ho are as follows:

Explanatory variables Coefficient t-value

Constant -14.0380 -1.8825

Monopoly power 37.0347 8.5852

Specialty of

automotive part

14.8056 2.4844

R&D intensity 1.1475 -1.1977

Foreign purchasing 0.0066

Engine System -15.5731 1.1566

Sheet Metals system -24.7439 1.0519

Air conditioning

system

22.9758 -1.1908

Steering system -1.0608 1.9157

Electro mechanism -5.1892 2.2944

Other parts -8.1703 1.7124Log likelihood -2.7726

Restricted log

likelihood

-24.9803

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 15/84

15

The above table is adapted from Chia-MinWei., Chia-Yon Chen. (2008). “An Empirical Study of

Purchasing Strategy in Automotive Industry” in Industrial Management & Data Systems, 108(7).

Pp.982.

Similarly the empirical results for CMC/Mitsubishi are as follows

Explanatory variables Coefficient t-value

Constant -9.2675 -1.1032

Monopoly power 27.4959 9.1305

Specialty of

automotive part

7.4472 0.8679

R&D intensity 1.2176 0.0966Foreign purchasing -10.1223 -0.5724

Engine System -10.8786 0.6246

Sheet Metals system -10.7870 1.2949

Air conditioning

system

-11.7589 -1.3189

Steering system -0.4683 1.2183

Electro mechanism -0.6369 1.7039

Other parts -0.6833 1.4180

Log likelihood -3.9894

Restricted log

likelihood

-28.1134

The above table is adapted from Chia-MinWei., Chia-Yon Chen. (2008). “An Empirical Study of

Purchasing Strategy in Automotive Industry” in Industrial Management & Data Systems, 108(7).

Pp.982.

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 16/84

16

It is clear from the tables that the Leo Ho/Ford has significance in electro mechanism spares and

CMC/Mitsubishi has highly significant monopoly variable.

Chapter 3: Economy

The economy that finds consideration in this paper is a large developing economy and it has

increasing market for automotives. In that economy there is necessity for auto industries as well

as the firms that produce components for the domestic and foreign automotive companies. This

needs a good supply chain management as the markets in developing economies are price

sensitive. Though the country considered in this paper is resource based, the technology

intensive suppliers are necessary. The automotive industry can gain from exports when they

contain more quality than their competitors. The developing country like India needs technology

intensive suppliers for its automotive firms and knowledge based companies that rely on quality.

However, when concentrating on domestic market, the supply chain is also important make the

production cost effective. Hence, a structural change is necessary for the Indian economy,

particularly to automotive industry. The automotive firms need to have the components suppliers

to be situated nearby areas to reduce the supply costs from components to suppliers. It is

essential for a developing economy like India to build technological capabilities and to spread

them to various activities in economy. However, it is not simple and is a complex process. The

technological capabilities of the companies refer to their resources in terms of knowledgeregarding the technology they need. To gain it, some automotive companies in India entered into

collaboration with the foreign companies and launched vehicles into Indian Market. The best

example of them is ‘Maruti’. Some other companies are taking help from other companies in

their research activities, but still are manufacturing the automotives on their own. In place of

collaboration, they are trying to acquire the companies that had the required technology. The best

example for this type of companies is ‘Tata Motors’ (Carlos Torres-Fuchslocher, 2010, p.269).

3.1: Indian Economy & Auto Sector

The restrictions of Indian economy on industries have been relaxed in the last two decades. This

resulted in removing the technical inefficiency existed in era of restricted production. The reason

is due to the increase of competitive pressure and freedom in production and marketing activities

of automobile and component manufacturers. This resulted in adoption of best practice

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 17/84

17

technology as there is more number of ways available for the manufacturers regarding the

technology and the spares. The product lines, capital stocks and imports of goods as well as

technology changed rapidly paving the way for the development of production and increasing of

market for every sector and industry. This resulted in increase of levels of output that resulted in

decreasing the cost of any product thus resulting in attracting more customers as the products and

services are available at competitive price than in the past. This resulted in productivity gains

making them profitable. The restructuring of manufacturing resulted in estimation of long run

cost function that maintained the long run equilibrium levels of the stocks. The reforms made a

change in the structure of Indian economy as it is moribund in the era of pre-liberalization and

government used to regulate the production and imports. The reforms resulted in flow of foreign

exchange into the domestic market paving the way for imports and this further resulted in

strategies of joint venture firms formed by domestic and international players in India, which

made Indian industry competitive of producing products on larger scale. This is made possible

by removing the technical inefficiencies with the introduction of technology that is new for

Indian market as well as for the markets of developing countries like India. Thus after the

liberalization of trade the capital in Indian auto market entered as a regressor in the short run cost

function. Hence, it is evident that there exists the reason for the success of this capital to result in

profits. For this, the firms used the input usage according to the expected output levels. Hence,

the overall effect of capital in the liberalization era in Indian market is according to the scale of the investment in the industry. Previously, the return to scale used to be low, but after the

liberalization of trade restrictions, the production restrictions on the firms are relaxed and this

resulted in increase of return to scale, though the percentage of profit is decreased. This implies

that the magnitude of overall profit due to the increase of production happened in Indian market

after the liberalization of the restrictions on imports and exports. However, the firms recognized

that the returns will be sustained for long term strategies as the market in India is in growing

stage and short term strategies may result in situations for any company to lose the future market

share. Even in short run there should be some profits that make possible the long term growth.

The competition in the liberalized market is making the firms to hire inputs in expectation for

achieving growth in future. Hence, the investments in establishment of plants and providing

equipments are on increasing spree to increase production of various models. Consequently,

there exists a situation to transport and store the produced goods according to the marketing

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 18/84

18

needs (Brian Fikkert., Rana Hasan, 1998: 51-62). Hence, the industrial firms in developing

countries like India should compete with a freight transportation system that is not cost effective.

According to Sumila Gulyani (2001, p.1157) the reason is weak physical infrastructure. The

ports, airports and road as well as rail networks are not well connected or not much useful to the

industry to make its supply chain management a well structured network. The weak

infrastructure makes the public as well as private sector transport operators to exhibit limited

range of expertise in transportation. Consequently, though the automotive industries are able to

compete on domestic market, they are not capable to compete with the firms in industrialized

countries. To remove this weakness, it is crucial for the administrations in developing countries

to focus on quality linkages between transportation infrastructures. Gulyani (2001, p. 1158)

quotes the logistics costs borne by India’s largest auto assembler ‘Maruti’ to analyze the

transport solutions put forth by Maruti as well as the companies like Ford. The analysis finds that

though the transportation in India is not much expensive, but the poor transportation system

results in damages incurred in transit and that increases the cost of inventories of the assemblers.

Though the analysis of the Gulyani (2001) quantified the firm specific costs of transportation, the

transportation created costs are beyond a particular organization and cannot be generalized. Thus

the quantification of transportation costs in Indian auto market do not shed light on the way

individual firms’ perceptions about transportation problems. In this type of situation it is

essential for the auto assemblers in Indian market to frame strategies that reduce the impacts of poor transportation. As a result Indian auto Industry moved towards lean production, which is

cost effective. However, this is helpful after Indian government deregulated its economy after

1993 and allowed auto components with reduced import tariffs. Thus it resulted in entry of

internationally competitive assemblers into the Indian passenger car market. The Indian market

contains 12 world class firms that include Ford, General Motors, Hyundai, Daewoo, Honda,

Toyota, Fiat and Mercedes-Benz. Even then Maruti is still India’s largest car assembler by

holding 63 percent of Indian car market. This is due to the presence of its service centers in

abundance all over India. The competition between these firms resulted in production exceeding

the demand for cars in the country. It further resulted in restructuring to cut costs and enhance

quality of passenger cars assembled by them. One of the important aspects of that restructuring is

lean assembling or manufacturing. The manufacturers who follow lean manufacturing ask their

suppliers to deliver several times a day with accurate schedule (Sumila Gulyani, 2001, p.1160).

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 19/84

19

Hence, the suppliers who are component manufacturers have growth opportunities along with

their customers who are automotive manufacturers. Hence, both automotive manufacturers and

component supplies for them are the ones who have substantial growth opportunities. According

to Rajesh K. Pillania (2008, p.1453), Indian component sector dominated by SMEs, though far

lesser than world class firms of similar type registered a growth rate of 17 percent in the period

1998-2003. In addition to that the author quotes that the Auto Components Manufacturing

Association (ACMA) forecasted 15 percent growth per annum till 2012. This is in line with

growing exports at the rate of 24 percent. Hence, knowledge management is necessary in SMEs

of automotive industry, which are component manufacturing units. As these SMEs are less

mature in the use of knowledge regarding mechanical aspects of the technology, the knowledge

management needs categorization. As knowledge is about know-how and there is difference

between tacit and explicit knowledge, the categorization is crucial. In this context, Rajesh K.

Pillania (2008, p.1454) quotes that the categorization of tacit and explicit knowledge as know-

how and know-that. Regarding explicit knowledge, the organization of information about

customers is essential as it helps not only in marketing the product but also in product designing.

The Indian component manufacturers of automotives do not have this categorization till the

liberalization of automobile trade activities. Hence, it resulted in a situation of depending on the

research and development activities of automotive manufacturers, so that they decide the

parameters of the components. The dependence is necessary for them as long as they create aknowledge base and get that quality for their products, so that the manufacturers design their

vehicles accordingly. To act according to the needs of the manufacturers, component

manufacturers should have enough research and development on their own, independent to that

of the automotive manufacturers. It is essential to get the position of supplying the same

component to more than one manufacturer, if an auto component firm wants to transform into a

world class one. This situation demands innovation that is recognized by CEOs Indian

Automobile companies. According to knowledge management, a national caliber of converting

knowledge into wealth and social utility is key for its future and innovation plays a crucial role in

that aspect. Hence, along with research and development the Indian auto component

manufacturers need innovative and motivation provocative mechanisms to use the knowledge

provided by R&D units according to the profitability of the company. The emphasis on

innovation is because, the Rajesh K. Pillania (2008, p.1455) quotes that India is not only lagging

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 20/84

20

behind in innovation when compared to US, Germany and Japan but also with Brazil, China and

Russia in various parameters when focused on big firms. The difference is that even SMEs in

Europe spend on R&D despite their limited budgets, but that is not the same in case of India. In

this regard, the author quotes small businesses in Taiwan, which consider R&D as grass roots for

development. The R&D activities of Taiwanese SMEs are regarding increasing quality and

productivity of the product. This is due to the fact the company with technological advantage

gains over the competitors in the presence of ever changing market. Coming to the Indian studies

regarding the knowledge of the auto component industry, various researches in India state that

the post liberalization era has witnessed the decrease of innovation output barring a small

number of exceptions. The author cites PRDC (1999), which states that the high level of

innovation and IPR management associated with strategic manufacturing as well as aggressive

marketing strategies are necessary for the growth of industry in India. It can be understood that

some exceptional companies mentioned above about the innovation follow this rule to be

innovative in producing quality products. The reason for lack of innovation and knowledge base

is due to the absence of institutional ecosystem for creation in India. The eco system results in

lack of acquisition as well of assimilation of knowledge by SMEs (Rajesh K. Pillania (2008, p.

1452-1455).

As a result, it is important to cite Alain Verbeke and Paul Brugman (2005-p.97-98), regarding he

firm specific and region specific advantages and differences and the strategies that need to follow

for performance of the organizations. Regarding these differences, the authors cite Kenichi

Ohmae (1985) who released a classic ‘Triad Power’ for international business activities.

According to that book, the world is not global and it is instead regional triad comprising of

United States, Europe and Japan as the powers. The same thing has been recognized by Rugman

as he identified the fact that the majority of trade and business has been and is being taking place

in North America, European countries rather instead of being international. Hence, the authors

quote Rugman’s ‘The End of Globalization’ that states that there is no global firms and all thefirms that are termed as global are in fact regional. These include automotive firms also. While

explaining the regional nature of the firms, the authors cite Rugman (2005) about the issues that

are related to regional sales distribution in the automotive industry. These issues are linked with

the performance of the firm that is under consideration. However, the authors disagree with

Rugman regarding sales regional nature of the automotive firms is having probability to turn

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 21/84

21

really global in the near future. To explain this, authors bring to the fore the argument that the

profit for a single unit needs consideration rather than overall sales and that depends on the

regional factors and may change from place to place. Hence, if the company is having different

profits in different regions per single unit of its product, still having profit in total revenues, then

the global or regional nature of the firm can be appraised on the basis of sales. The restructuring

of Indian automobile industry is due to introduction of capital and technology of Japanese

industries that shaped the structure of the industry. The first step in that direction is formation of

Maruthi Udyog Limited (MUL), which is a joint venture between Suzuki Motors and the

Government of India. The structuring of the Indian Automobile industry continued when the

local manufacturers in India resorted to collaboration with other foreign companies who can

provide matching technology. This happened due to the dismantling of the regulations regarding

automobile business in India. Further this restructuring is in line with the restructuring and value

capturing of component industry and that resulted in growth of automobile as well as component

sectors that resulted in mutual sustenance of the development. This resulted in increase of

consumer choice in the automobile market, particularly in passenger car market. However, the

just mentioned restructuring did not result in substantial increase of production in volumes of

manufacturing and market fragmentation continued. According to Anthony P. D’Costa. (1995,

486), the involvement of middle class as the customer base is important for growth of any

industry including automobile. The situation in India post liberalization of economy resulted inthe same situation that increased the purchasing capacity of middle class. This resulted in

increased customer base prompting the companies to produce more and to compete in domestic

as well as international market. However, in the course of these happenings, the private

investments wanted protection from international environment and that situation is comprised of

bailouts for public sector, which are a resultant of being sick due to competition from private

industries. Further restricting is about manufacturing of different models of vehicles by a same

manufacturer introducing the concept of broad banding that is a different form, which offers a

choice of models for the customers. This situation has been made possible as the component

manufacturers responded in the same way as the automobile manufacturers due to assistance in

capital and technology from foreign investors. For example, a vehicle manufacturer produced

three wheelers, four wheelers, two wheelers thus demanding wide range of components from the

suppliers. The lack of certain components in domestic market has been compensated as the

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 22/84

22

government of India allowed the vehicle manufacturers to import the required components. This

is due to the availability of foreign exchange, which is not available in the past and the imports

are restricted due to that reason. This resulted in upgrading of technology of component

manufacturers as well as automobile companies as the imports and exports resulted in exchange

of technology along with capital. Thus the internationalization of the production and marketing

of automobile industry resulted in restructuring. The main components of the restructuring are

due to change in activities of production, collaboration and market shares. In this context, again

the joint venture of Suzuki Motors Corporation (SMC) with Maruti Udyog Limited comes to the

fore as it is first transnational company and paved way for other such ventures. Taking cue from

this venture, the Indian companies like TELCO, Ashok-Leyland and Bajaj increased the

production of commercial vehicles as MUL increased the profit by producing more. Taking the

same tempo into the future, the Japanese companies Toyota, Nissan, Mitsubishi and Mazda in

collaboration with the domestic companies in India, increased the production light commercial

vehicles thus bringing down the price of LCVs. The increase of production of the LCVs can be

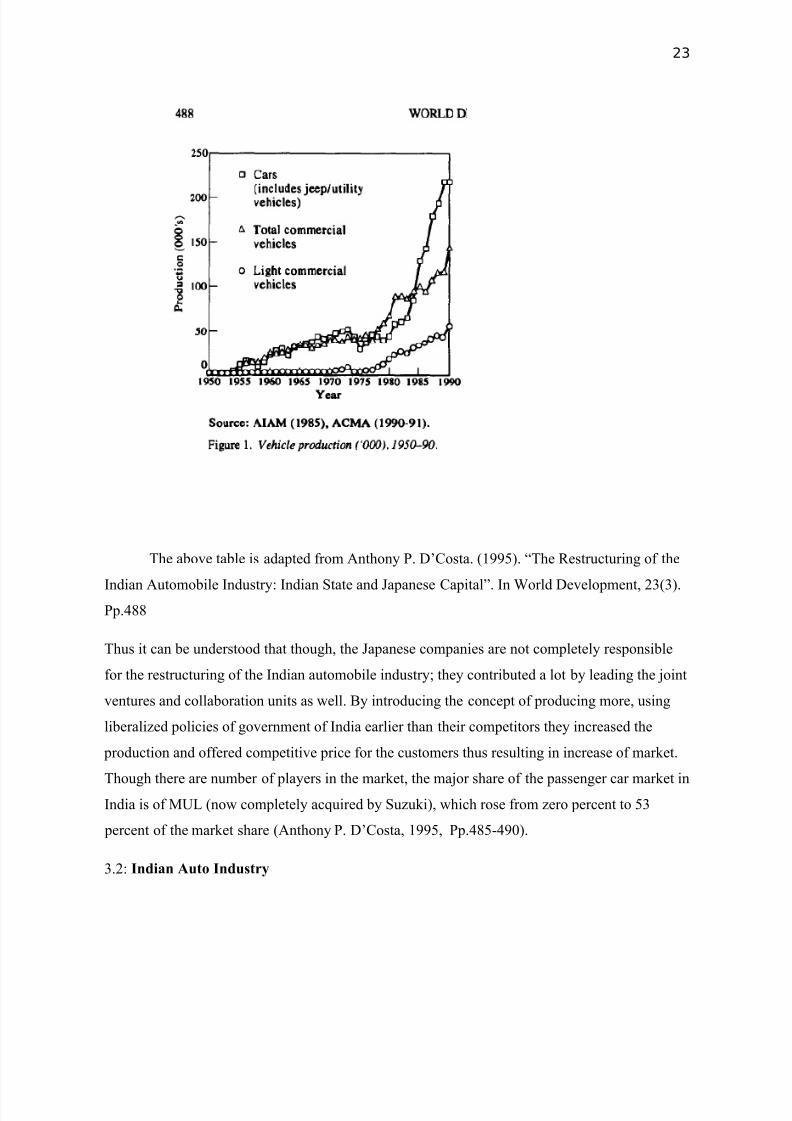

observed from the following table.

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 23/84

23

The above table is adapted from Anthony P. D’Costa. (1995). “The Restructuring of the

Indian Automobile Industry: Indian State and Japanese Capital”. In World Development, 23(3).

Pp.488

Thus it can be understood that though, the Japanese companies are not completely responsible

for the restructuring of the Indian automobile industry; they contributed a lot by leading the joint

ventures and collaboration units as well. By introducing the concept of producing more, using

liberalized policies of government of India earlier than their competitors they increased the

production and offered competitive price for the customers thus resulting in increase of market.

Though there are number of players in the market, the major share of the passenger car market in

India is of MUL (now completely acquired by Suzuki), which rose from zero percent to 53

percent of the market share (Anthony P. D’Costa, 1995, Pp.485-490).

3.2: Indian Auto Industry

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 24/84

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 25/84

25

as well as the customers of the companies considered are used to compare the pricing strategy

and profitability of the firms. The important points that are followed in this research are: 1. The

importance of topic and question and its meaning in commercial and market conditions, 2. The

findings in literature review are used in analysis, 3. Finding appropriate persons to interview, 4.

Framing relevant questions to interview the concerned persons, 5. Conducting person-to-person

interviews if necessary, 6. Organizing and analyzing the data (Clark E. Moustakas, 1994:103-

105).

4.1.2 The second type of research followed in the paper is about deductive research and this has

been done according to the theory followed for pricing strategy and profitability. The literature

review and discussion in the paper finds this type of research, which involves theory before

research.

4.2: The Research Problem & Style Chosen

The research problem involved in this research paper is how the pricing strategies of the Indian

Automobile companies are resulting in profitability for them. The style of analysis is a mix of

qualitative and quantitative analysis as ratio analysis and correlation between different ratio

values of companies help analyzing their performance.

4.3:Hypothesis

Price is the most important element in strategy for the profits of the company.

The appropriate pricing strategy that works on the target customers results in profitability when

that strategy is relevant to the customers’ needs as well as the production strategies. The pricing

strategies of Indian Automobile Companies are connected to their profitability in domestic and

international markets. Thus the pricing strategy will be different for various companies

depending on the target customers and the production strategies. Hence the pricing strategy

depends on the models the automobile companies make and sell as they decide the target

customers. However, again the emphasis will be on pricing strategy as that decides the model

that manufacturer intend to make. When the manufacturer intends to remove the restrictions on

price, then the firm can proceed to make a luxury model of the car. If the manufacturer’s

intention is to produce different models from basic to luxury cars, the pricing strategy is

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 26/84

26

significant and in turn it is related with profitability. The number of models and the vastness of

the customer base the company targets decides the course of pricing strategy of an automobile

manufacturer. The success and efficiency of pricing strategy also depends on supply chain of the

company as it helps in cost effective production as well as timely delivery. The influence of the

company on the retailers and the network of the company regarding the services it offers to its

customers further decide the company’s extent of freedom in fixing a price a little more than its

competitors. Thus the paper establishes the relation of pricing strategy with various aspects like

production, profitability, marketing and supply chain management of the company and the way

they affect the strategy.

4.4: Research Question

How important is pricing strategy for Indian Automobile Companies, when profitability and

marketing of the product is concerned?

4.5: Methods of Analysis

The methods of analysis followed in this paper are inductive and deductive methods.

Inductive Method:

As inductive method is referred to scientific methods that use observations, it has been followed

in this paper to decide the performance and profitability of Indian automobile companies. The

observations gathered here are regarding five years from 2005 to 2009 and the period is 2006-10

for Hindustan Motors (HM). Based on the values and information given by the firms in their

annual reports, various rations are calculated that decide the performance and profitability of the

company as well as the benefits for the investors who are shareholders of the companies. The

observations found in the analysis are used to generalization of the research topic and the theory

in it. The qualitative analysis in the paper inherently have inductive research and explicit

deductive research.

Deductive Method:

In addition to inductive research, the deductive research is used as data from the operations of

the companies is used to support the theory involved in research question about pricing strategy.

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 27/84

27

The annual reports of five companies are used to draw the data to support the theory involved in

supporting the significance of pricing strategy in a country like India. The statistical analysis that

involves rations and correlation is used to deduce the hypothesis. Normally the deductive

methods begin with a general concept or rule intending to move towards a particular conclusion.

However, in some circumstances the research may result in the conclusion that is opposite in

nature. In this paper, the conclusion is the same as the hypothesis as Indian automobile

companies are successful in earning more profits with narrow margins on each unit by selling

more number of units. As the deductive reasoning is method of reaching conclusion that is

supposed before the research, the outcome depends on the evidence we collected. In this paper,

the evidence collected, supported the hypothesis that pricing strategy is crucial for Indian auto

market. Hence, the statistical evidence and findings of analysis are used to conclude that the

companies who follow a definite pricing strategy for Indian auto market in the era of removal of

licenses on production are successful. This conclusion has been deduced by analyzing the

evidence qualitatively. In this case according to the evidence and the prices of products of

different companies, the conclusion has been drawn.

4.6: Data Sources

The fundamental sources for data are the annual reports of the companies involved and the

relevant literature about Indian auto industry and its techniques about production. The other datasources involve different researches conducted on the topic of the paper.

Chapter 5: Analysis and Findings

The correlation is used to calculate the relation between the data in the annual reports and the

findings are analyzed according to the pricing strategies and profitability in Indian market. The

profitability will be analyzed separately if the companies are selling their automobiles in both

domestic and international markets. The difference in pricing strategies and profitability of the

companies in domestic and international markets will be a part of the analysis and findings.

5.1: Critical Appraisal of Literature

From the annual report of MUL in 2006 one can find that the company is ahead of its

competitors by its introduction of premium car model ‘Swift’. The growth is significant as the

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 28/84

28

company achieved it despite the decline in automobile market. This indicates the company’s

decision making about timely intervention of the various car models. Normally, the overall

demand for passenger cars decrease when there is decrease in demand for basic models and mid

range cars. The demand for premium models may not suffer much for minor decreases in

demand for passenger cars. Keeping in view this aspect, the company released the premium

model ‘Swift’. The network of service centers of the company and the comparatively cheaper

price with other premium models may be the reason for the success of the model in 2006 (Maruti

Udyog Limited, 2006: 20).

MUL is now Maruti Suzuki India Limited increased its sales and profitability by the end of 2008

by 23.4 percent and 20.9 percent. This indicates that though the profitability increased with the

increase of sales it is not proportionate to the increase of sales as the rate of profit is lesser than

the rate of sales growth. However, as the company is maintaining a regular growth in both sales

and profit. The small changes are not affecting the company’s performance.

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 29/84

29

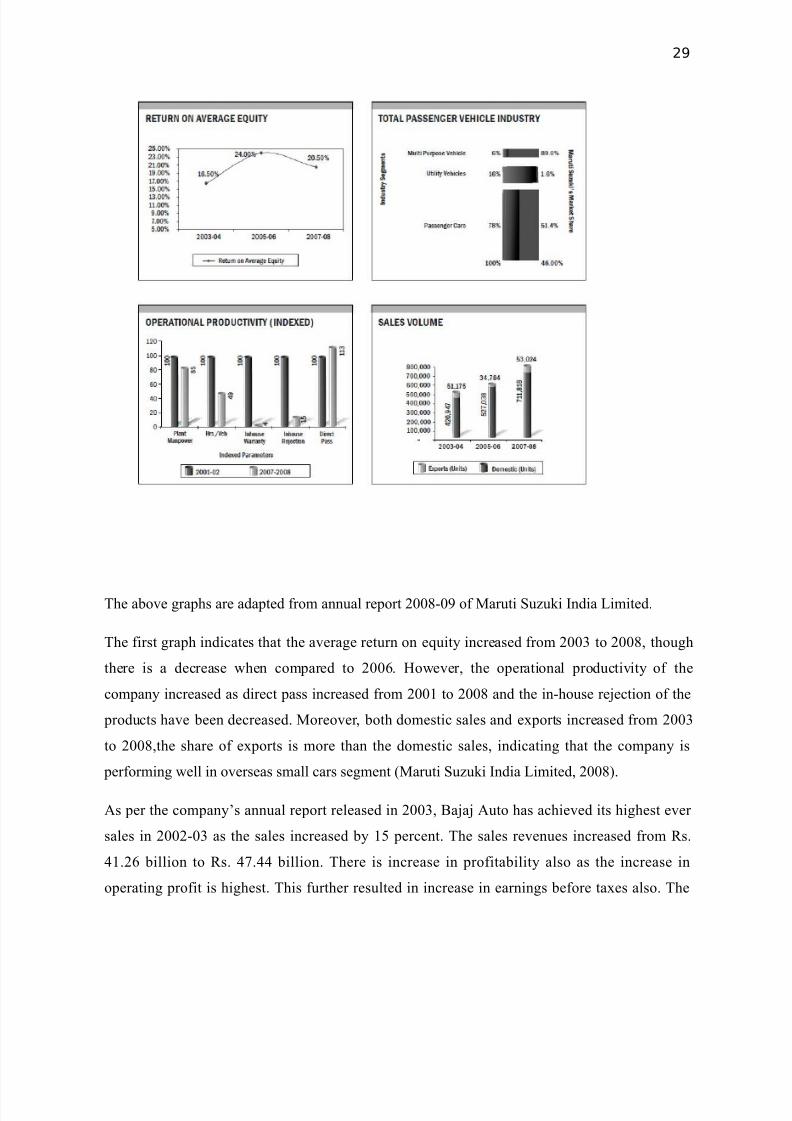

The above graphs are adapted from annual report 2008-09 of Maruti Suzuki India Limited.

The first graph indicates that the average return on equity increased from 2003 to 2008, though

there is a decrease when compared to 2006. However, the operational productivity of the

company increased as direct pass increased from 2001 to 2008 and the in-house rejection of the

products have been decreased. Moreover, both domestic sales and exports increased from 2003

to 2008,the share of exports is more than the domestic sales, indicating that the company is

performing well in overseas small cars segment (Maruti Suzuki India Limited, 2008).

As per the company’s annual report released in 2003, Bajaj Auto has achieved its highest ever

sales in 2002-03 as the sales increased by 15 percent. The sales revenues increased from Rs.

41.26 billion to Rs. 47.44 billion. There is increase in profitability also as the increase in

operating profit is highest. This further resulted in increase in earnings before taxes also. The

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 30/84

30

company is capable of increasing EBITDA margins from 9.8 to 16.8 percent, which is a sign of

increase of profitability. The increase of pre tax returns indicates the healthy economic status of

the company. These changes are sign for the positive results that are shown by the bajaj auto

company’s change it has shown in its products. The company changed its products from scooters

to bikes and these two wheelers contribute major revenues for the company. The company’s

annual report indicates that the company’s sales grew continuously from 1994 to 2003.

Moreover, the company increased the sales of motorcycles, which is less when compared to the

all two wheelers in 1994. This change indicates that the company is successful in understanding

the aspirations of the customers and is changing accordingly to manufacture more motorbikes. In

1994, the share of motorbikes is 21.6 percent in the overall sales of the company. When it comes

to 2003, the share increased to 74.3 percent thus indicating the change in production as well as

marketing strategies of the company. As the prices of bajaj motorbikes are lesser than their

competitors and even the profitability is increasing the pricing strategy can be analyzed while

doing the ratio analysis. Moreover, the basic models are priced at a maximum price of Rs. 37,000

and their premium category bikes are priced at a maximum of Rs. 45,000. This resulted in

attracting the middle class customers. As middle class customers are more in number in India,

when compared to remaining class, it can be understood that the company’s strategies are

successful in attracting the customer base, which are in larger number in the country (Bajaj Auto,

2003).

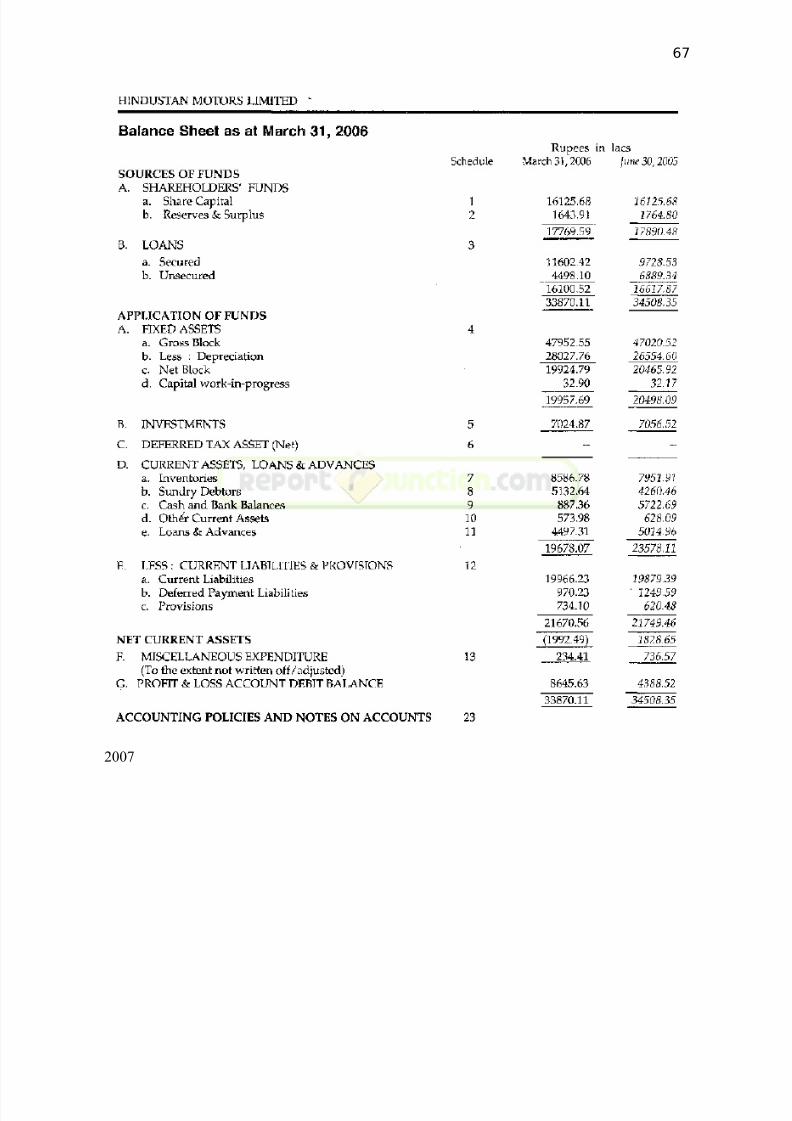

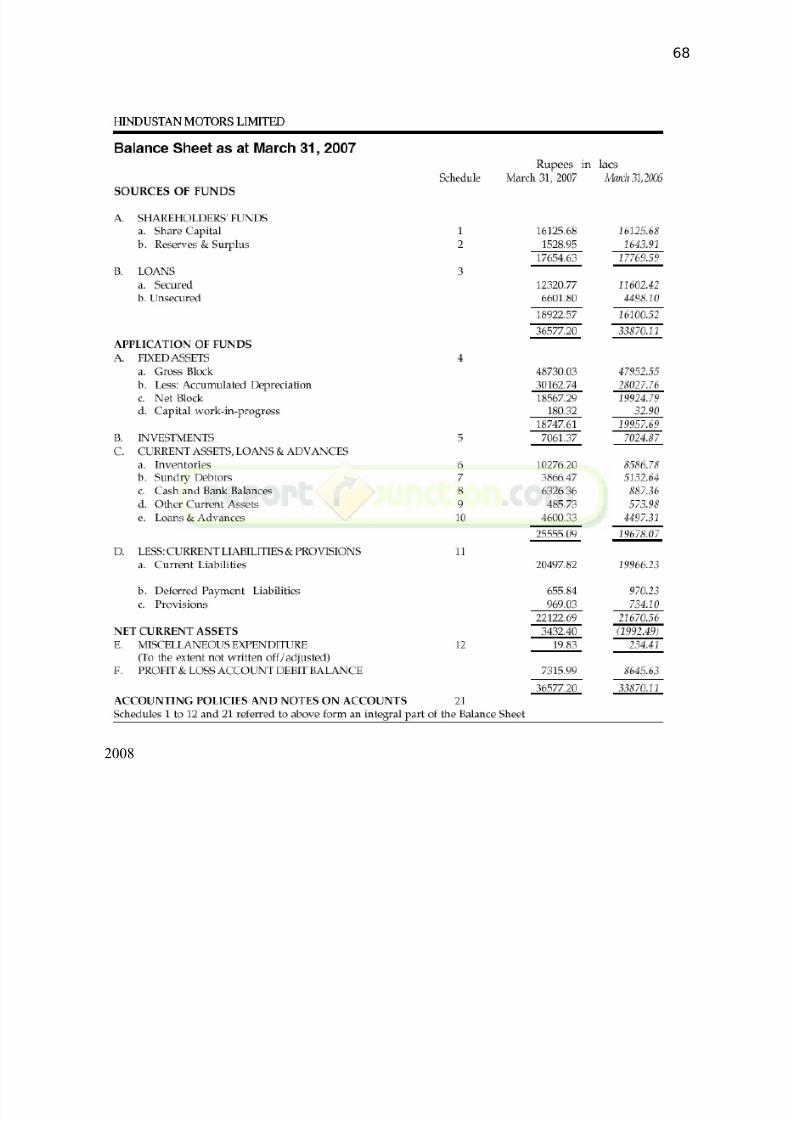

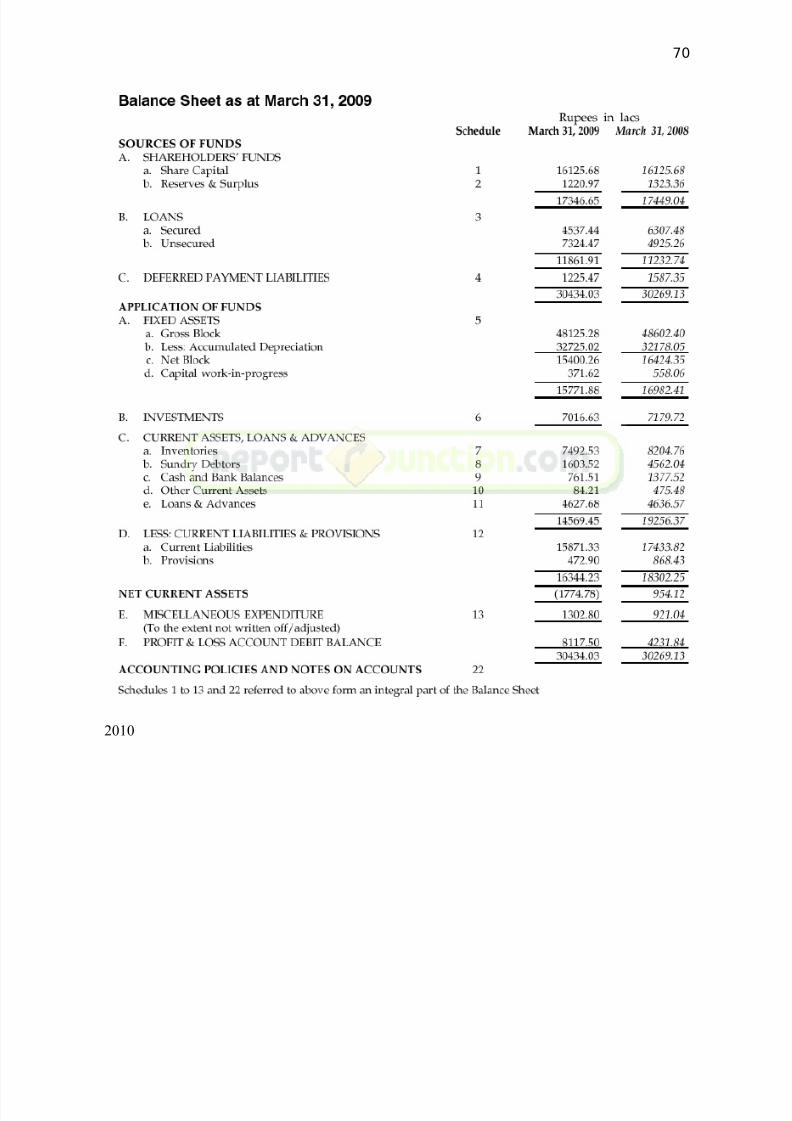

Regarding the annual report of HM, the one released in 2010 is 68 th report and it reveals that the

company’s revenue increased from 736 crores to Rs. 771 crores. There is no profit after taxation

this year and the loss stood at Rs. 51.10 crores. If the debt balance of previous years is added to

the present year’s loss, the total loss stands at Rs. 132.28 crores. The company finds that its 50%

of its net worth has been eroded in the last four financial years and it informs that it takes

necessary steps to prevent further erosion. However, the situation of the company is to inform

the Board of Industrial and Financial Reconstruction in India as it is a sick unit according tosection 23 of the sick industrial companies act 1985. Hence, when we compare the information

from the competitors like Maruti Suzuki, Bajaj, Mahindra and Tata Motors, the HM is not in par

with their growth and the reason is that the company has not changed according to the need of

the hour. All the other companies in Indian Market have changed their products according to the

need of the customers and framed pricing strategy accordingly to attract more number of

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 31/84

31

customers and recorded growth in both sales and profits. However, these strategies are not

followed by HM and thus resulted in the company losing its net worth and turning to be a sick

unit. However, as the company is focusing on automobile as well as auto component business,

there is a chance of reviving its growth and profitability. The company is focusing on forgings,

castings and stampings for other automobile companies and for the vehicles like Ambassador,

Lancer, Cedia, SUVs like Pajero, Montero and Outlander. However, if the company is successful

in recording the growth in sales of above mentioned vehicles, the profitability can be revived

(HM, 2010).

After critical appraisal of the automobile manufacturers’ details of performance, the overall

pricing strategy necessary for the market comes to the fore. The companies decide the pricing

strategy according to the interactions among automakers, dealers and buyers. The important

question is about the dealer margins that deal with sales and profits of the new car market.

Regarding this, Pinelopi Koujianou Goldberg (1996, p.623) cites Bresnahan and Reiss (1985)

about the questions related to the rent distribution between dealers and automakers. However, the

disappearance of monopoly model in Indian auto market, the explaining the dealer markups and

differential treatment received by buyers from the dealers is important. Hence, in this context,

the authors cite Ayres (1991) and Ayres and Siegelman (1995) that focus on relationship

between dealer prices and buyer attitudes as well as the other attributes like the type of the

customer base. As the Indian market is price sensitive, the customers wait for the quality

products that are available at competitive prices. Hence, price discrimination depends on

consumer characteristics and companies need to consider that aspect while describing the

markups associated with realized purchases. However, the environment in which the company

sells its automobiles is not controlled one in the existence of enough competition. Even in the

presence of competition, the availability of diverse range of customers offer Indian automobile

companies to bank on different products ranging from basic models to luxury models. The

pricing strategy for basic models or economy models considers profit for the dealer as well as the price offered to the customer. In contrast the customers of luxury models may prefer quality and

in this context the manufacturer has to consider only the profit of the dealer and the price offered

to the customer depends on the quality and the price offered by the competitor, but not as much

as in the case of the price of economy models. In addition to that the estimations of mean

discount distribution that is necessary to compete with the strategies of the competitors are

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 32/84

32

important while framing pricing strategy. Hence, while framing pricing strategies, the price

decided should be in a manner to offer discounts when competitors offer competitive prices than

expected. However, the capability of the dealer to negotiate also decides the attraction of

customer groups and when the company wants to sell more vehicles with less margin, the dealers

should be offered reasonable profit percentage so that they work for marketing the products in

their area. Hence, the company should offer the dealer a variety of models of vehicles, so that

when they sell a vehicle for lesser margin, they have to be confident that they can get it in

another model. Hence, while choosing the retail counters or getting the dealers, the company

should have diversified products from economy models to luxury vehicles (Pinelopi Koujianou

Goldberg, 1996. pp.622-630).

While considering the automobile market, the market base for bikes cannot be ignored and the

present situation in India resulted in almost disappearance of scooters and the motorbikes

replaced them. Though there are some vehicles that are named as scooties, the motorcycles are

dominant products in two wheeler markets. Not only in the four wheeler segment, has even the

segment of motor cycles offered diversity in products for the customers. However, this does not

resulted in fall of prices as it was the case of the prices of economy models in four wheelers.

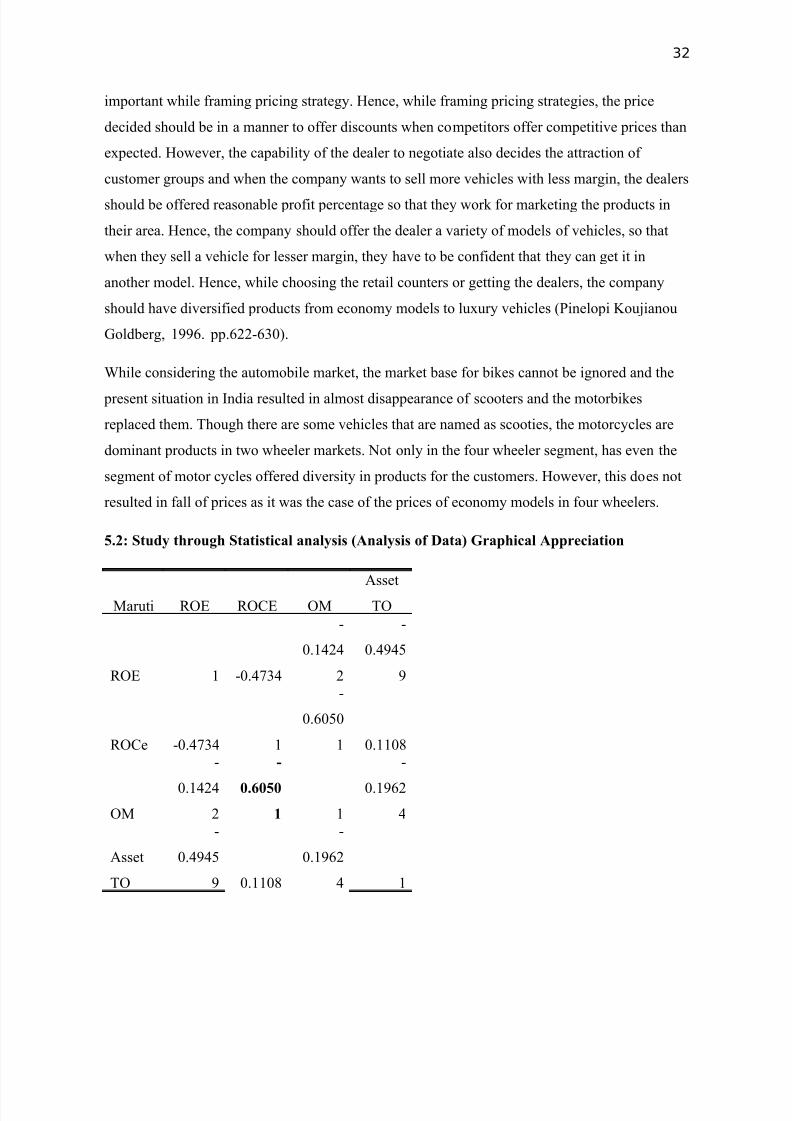

5.2: Study through Statistical analysis (Analysis of Data) Graphical Appreciation

Maruti ROE ROCE OM

Asset

TO

ROE 1 -0.4734

-

0.1424

2

-

0.4945

9

ROCe -0.4734 1

-

0.6050

1 0.1108

OM

-0.1424

2

-0.6050

1 1

-0.1962

4

Asset

TO

-

0.4945

9 0.1108

-

0.1962

4 1

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 33/84

33

-0.6-0.4-0.2

00.20.40.60.8

1

ROE ROCE OM AssetTO

ROE

ROCE

OM

Asset TO

The negative relationship between ROE and ROCE indicates that the debts of the company affect

profitability. Though the relation is same type between ROE and OM it is better when compared

to that exists between ROE and ROCE. That means the profit is increasing with increase of sales.

The negative relationship between ROE and Asset Turnover indicates that the company’s

efficiency does not match with the assets it possesses. Though the company’s profit is increasing

with sales, it is not up to the standards of the assets it have. However, the positive relationship

between ROCE and Asset Turnover indicates the presence of relationship between sales and

operating profit.

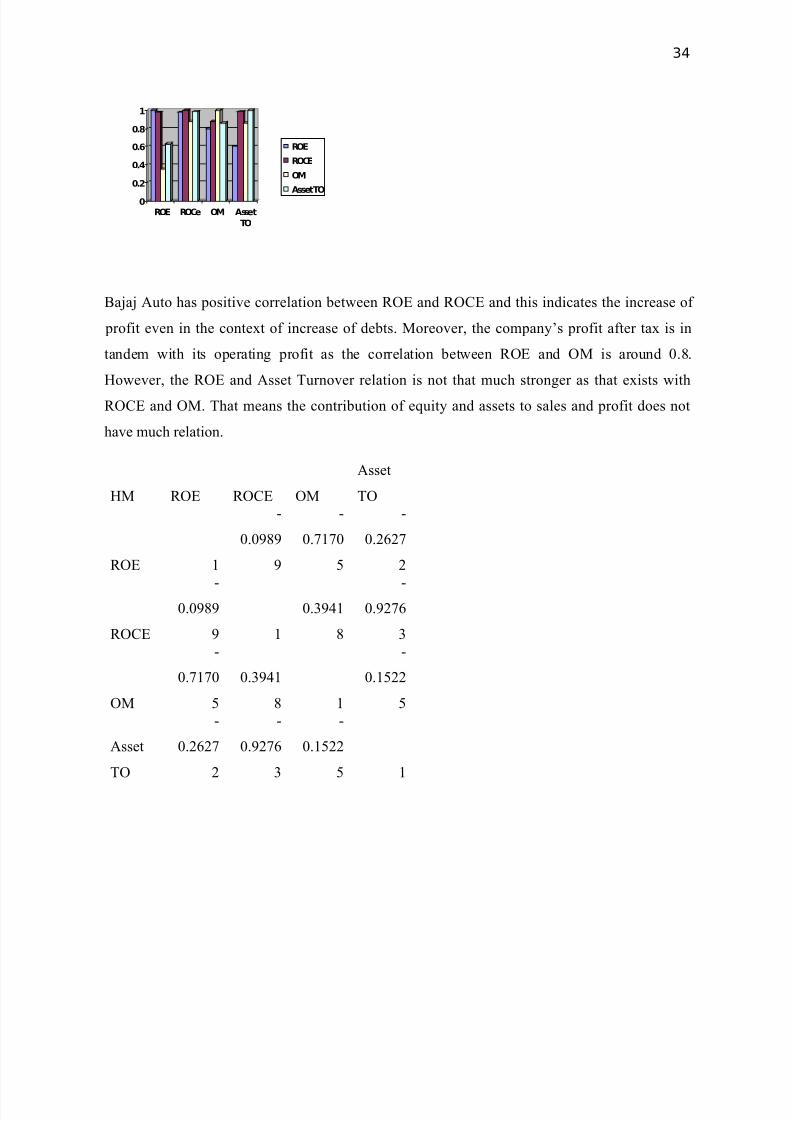

Bajaj ROE ROCE OM

Asset

TO

ROE 1 0.9869

0.8056

3

0.6351

6ROCE 0.9869 1 0.8844 0.9993OM 0.3577 0.8841 1 0.868Asset

TO 0.6351 0.9983 0.868 1

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 34/84

34

0

0.2

0.4

0.6

0.8

1

ROE ROCe OM AssetTO

ROE

ROCE

OM

Asset TO

Bajaj Auto has positive correlation between ROE and ROCE and this indicates the increase of

profit even in the context of increase of debts. Moreover, the company’s profit after tax is in

tandem with its operating profit as the correlation between ROE and OM is around 0.8.

However, the ROE and Asset Turnover relation is not that much stronger as that exists withROCE and OM. That means the contribution of equity and assets to sales and profit does not

have much relation.

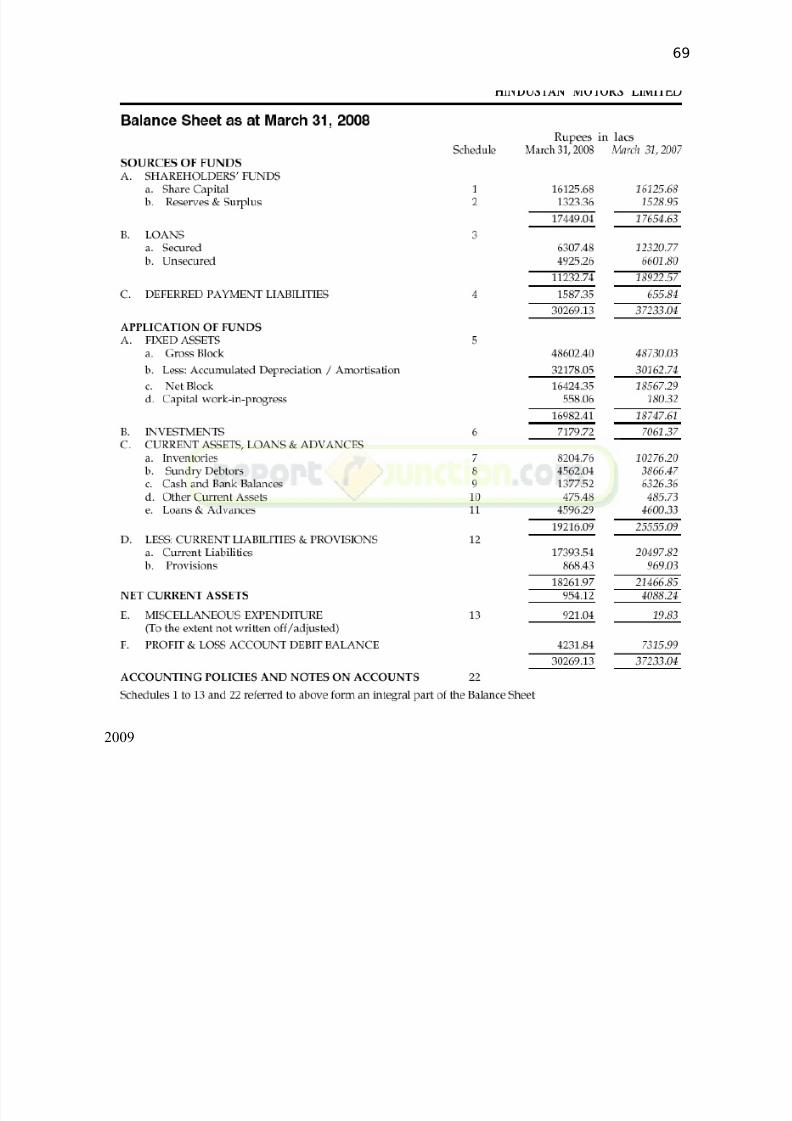

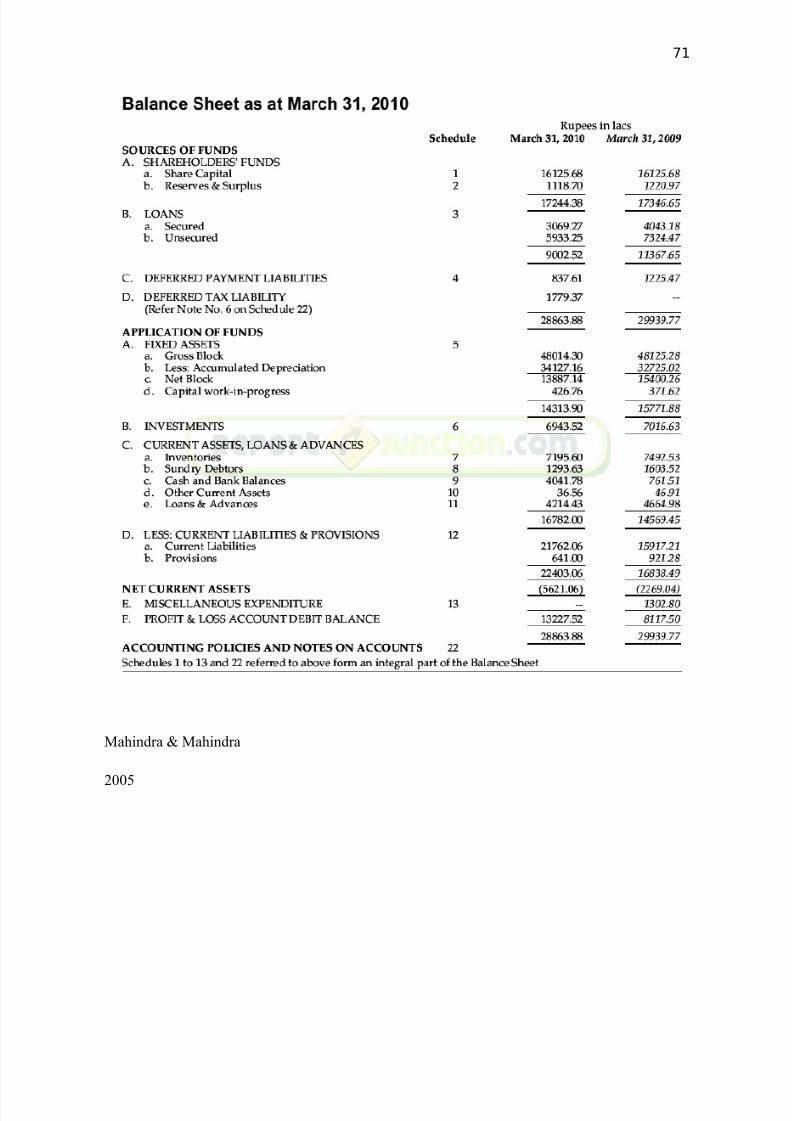

HM ROE ROCE OM

Asset

TO

ROE 1

-

0.0989

9

-

0.7170

5

-

0.2627

2

ROCE

-

0.0989

9 1

0.3941

8

-

0.9276

3

OM

-

0.7170

5

0.3941

8 1

-

0.1522

5

Asset

TO

-

0.2627

2

-

0.9276

3

-

0.1522

5 1

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 35/84

35

0

0.2

0.4

0.6

0.8

1

ROE ROCE OM Asset

TO

ROE

ROCE

OM

Asset TO

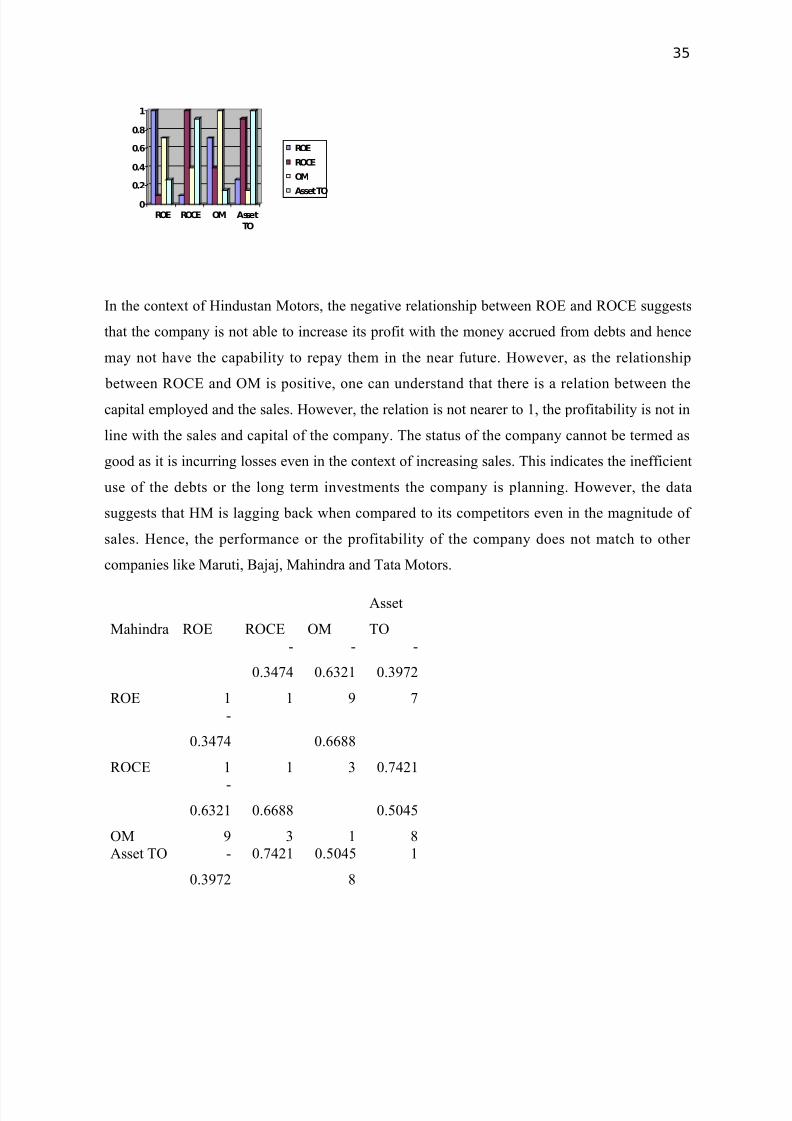

In the context of Hindustan Motors, the negative relationship between ROE and ROCE suggests

that the company is not able to increase its profit with the money accrued from debts and hence

may not have the capability to repay them in the near future. However, as the relationship

between ROCE and OM is positive, one can understand that there is a relation between thecapital employed and the sales. However, the relation is not nearer to 1, the profitability is not in

line with the sales and capital of the company. The status of the company cannot be termed as

good as it is incurring losses even in the context of increasing sales. This indicates the inefficient

use of the debts or the long term investments the company is planning. However, the data

suggests that HM is lagging back when compared to its competitors even in the magnitude of

sales. Hence, the performance or the profitability of the company does not match to other

companies like Maruti, Bajaj, Mahindra and Tata Motors.

Mahindra ROE ROCE OM

Asset

TO

ROE 1

-

0.3474

1

-

0.6321

9

-

0.3972

7

ROCE

-

0.3474

1 1

0.6688

3 0.7421

OM

-

0.6321

9

0.6688

3 1

0.5045

8Asset TO -

0.3972

0.7421 0.5045

8

1

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 36/84

36

7

0

0.2

0.4

0.6

0.8

1

ROE ROCe Om Asset

TO

ROE

ROCE

OM

Asset TO

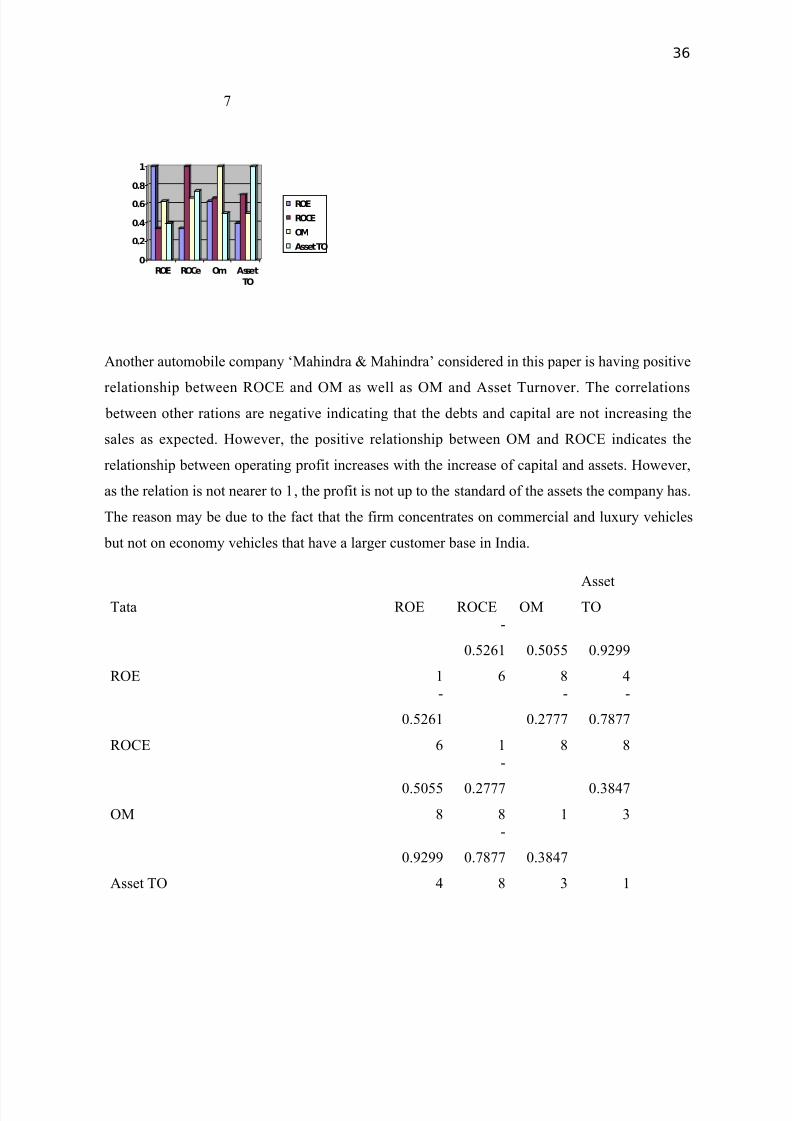

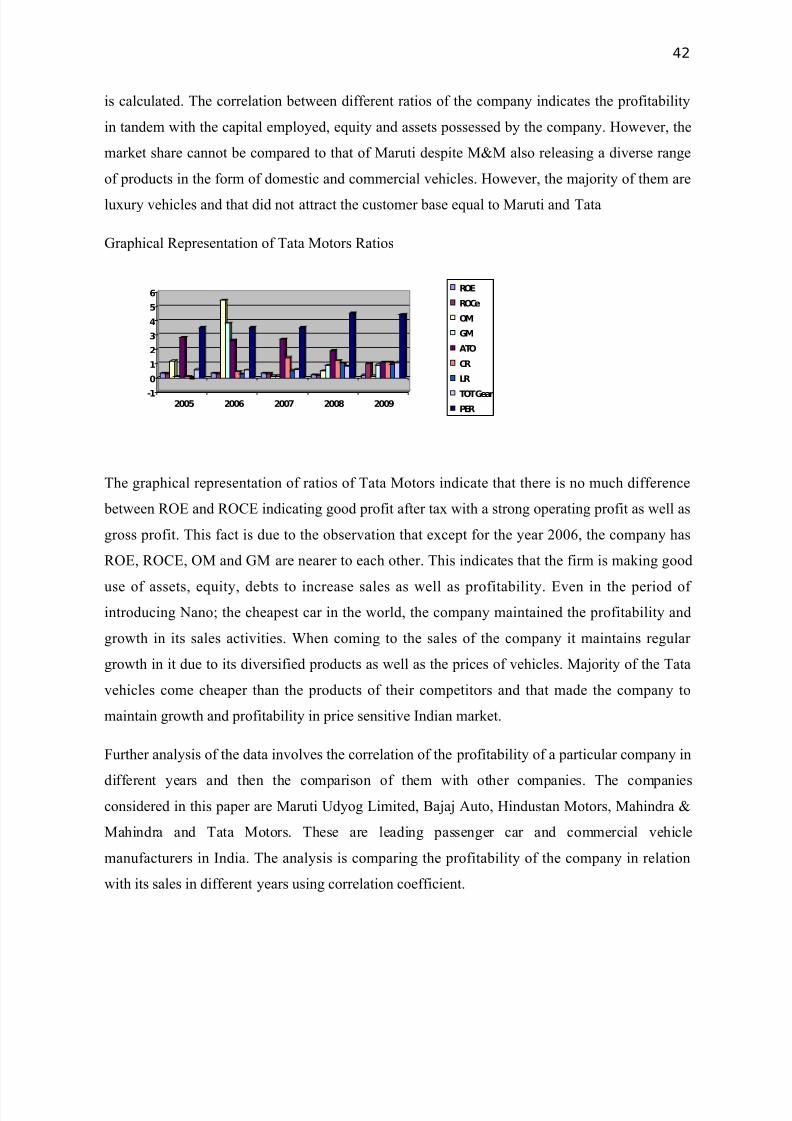

Another automobile company ‘Mahindra & Mahindra’ considered in this paper is having positive

relationship between ROCE and OM as well as OM and Asset Turnover. The correlations

between other rations are negative indicating that the debts and capital are not increasing the

sales as expected. However, the positive relationship between OM and ROCE indicates the

relationship between operating profit increases with the increase of capital and assets. However,

as the relation is not nearer to 1, the profit is not up to the standard of the assets the company has.

The reason may be due to the fact that the firm concentrates on commercial and luxury vehicles

but not on economy vehicles that have a larger customer base in India.

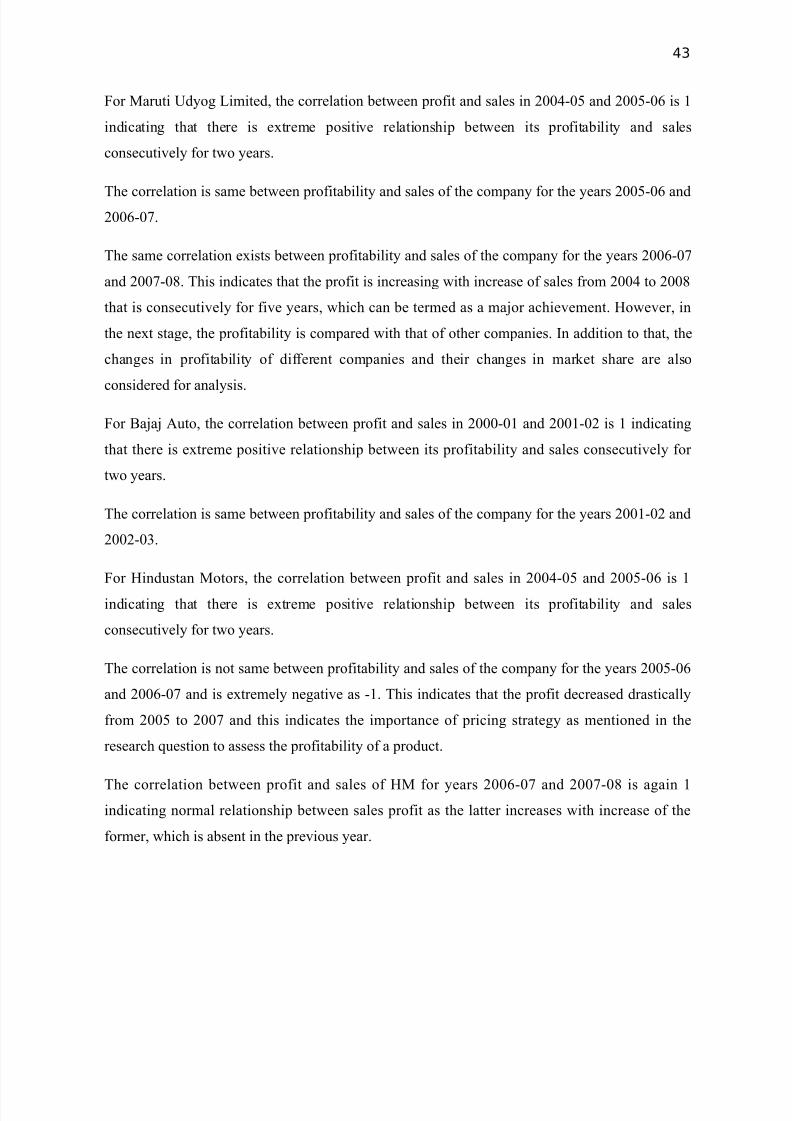

Tata ROE ROCE OM

Asset

TO

ROE 1

-

0.5261

6

0.5055

8

0.9299

4

ROCE

-

0.5261

6 1

-

0.2777

8

-

0.7877

8

OM

0.5055

8

-0.2777

8 1

0.3847

3

Asset TO

0.9299

4

-

0.7877

8

0.3847

3 1

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 37/84

37

0

0.2

0.4

0.6

0.8

1

ROE ROCE OM Asset

TO

ROE

ROCE

OM

Asset TO

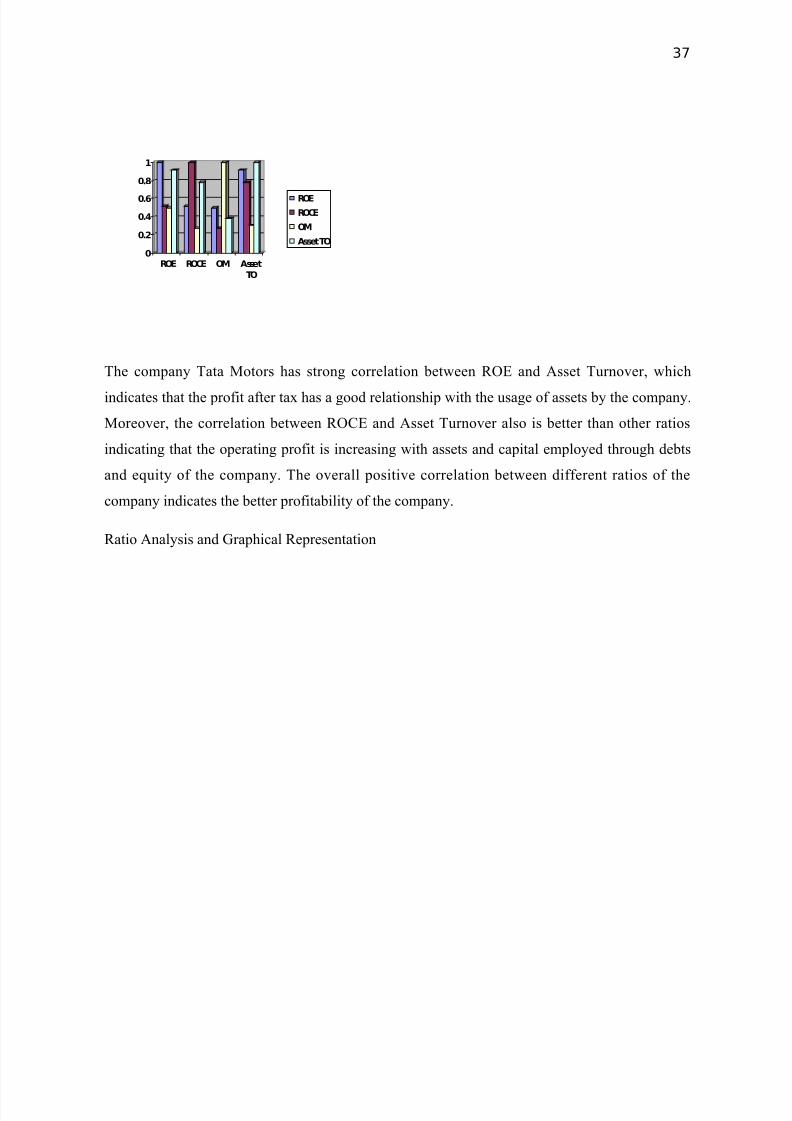

The company Tata Motors has strong correlation between ROE and Asset Turnover, which

indicates that the profit after tax has a good relationship with the usage of assets by the company.

Moreover, the correlation between ROCE and Asset Turnover also is better than other ratios

indicating that the operating profit is increasing with assets and capital employed through debts

and equity of the company. The overall positive correlation between different ratios of the

company indicates the better profitability of the company.

Ratio Analysis and Graphical Representation

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 38/84

38

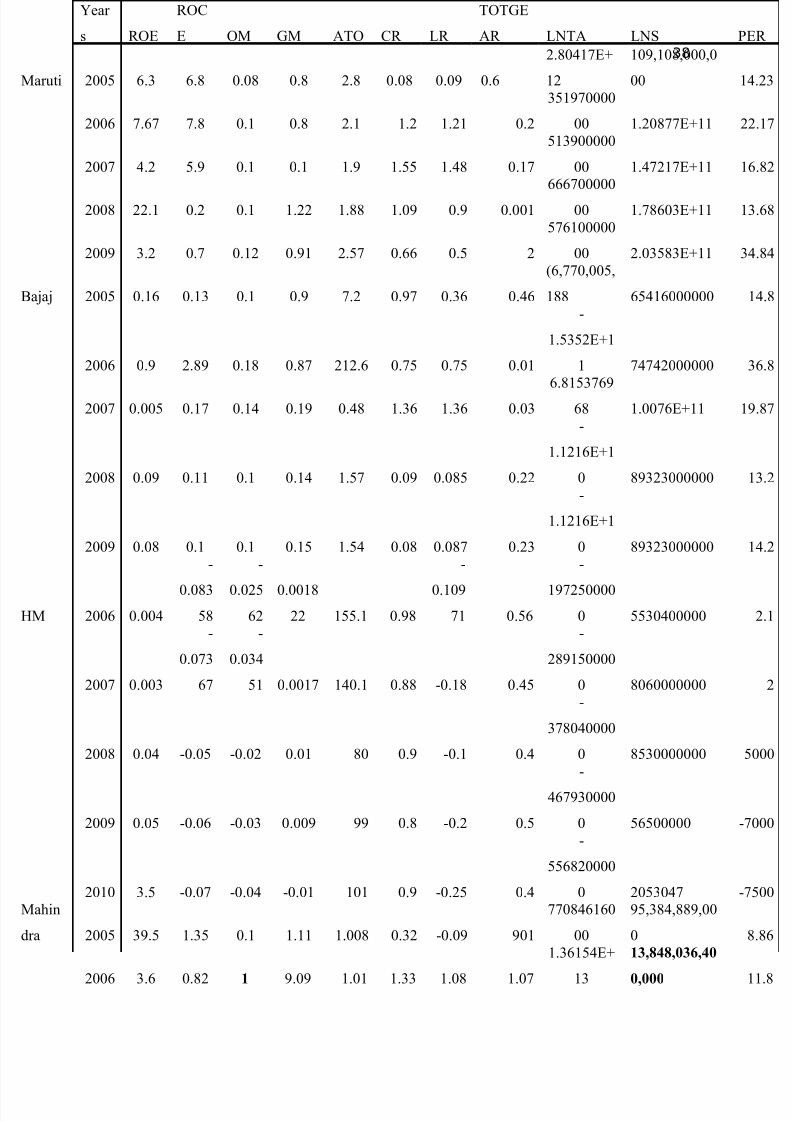

Year

s ROE

ROC

E OM GM ATO CR LR

TOTGE

AR LNTA LNS

ruti 2005 6.3 6.8 0.08 0.8 2.8 0.08 0.09 0.6

2.80417E+

12

109,108,000,0

00

2006 7.67 7.8 0.1 0.8 2.1 1.2 1.21 0.2

351970000

00 1.20877E+11

2007 4.2 5.9 0.1 0.1 1.9 1.55 1.48 0.17

513900000

00 1.47217E+11

2008 22.1 0.2 0.1 1.22 1.88 1.09 0.9 0.001666700000

00 1.78603E+11

2009 3.2 0.7 0.12 0.91 2.57 0.66 0.5 2

576100000

00 2.03583E+11

aj 2005 0.16 0.13 0.1 0.9 7.2 0.97 0.36 0.46

(6,770,005,

188 65416000000

2006 0.9 2.89 0.18 0.87 212.6 0.75 0.75 0.01

-

1.5352E+1

1 74742000000

2007 0.005 0.17 0.14 0.19 0.48 1.36 1.36 0.036.8153769

68 1.0076E+11

2008 0.09 0.11 0.1 0.14 1.57 0.09 0.085 0.22

-

1.1216E+1

0 89323000000

2009 0.08 0.1 0.1 0.15 1.54 0.08 0.087 0.23

-

1.1216E+1

0 89323000000

2006 0.004

-

0.083

58

-

0.025

62

0.0018

22 155.1 0.98

-

0.109

71 0.56

-

197250000

0 5530400000

2007 0.003

-

0.073

67

-

0.034

51 0.0017 140.1 0.88 -0.18 0.45

-

289150000

0 8060000000

2008 0.04 -0.05 -0.02 0.01 80 0.9 -0.1 0.4

-

378040000

0 8530000000

2009 0.05 -0.06 -0.03 0.009 99 0.8 -0.2 0.5

-

467930000

0 56500000

2010 3.5 -0.07 -0.04 -0.01 101 0.9 -0.25 0.4

-

556820000

0 2053047hin

2005 39.5 1.35 0.1 1.11 1.008 0.32 -0.09 901

770846160

00

95,384,889,00

0

2006 3.6 0.82 1 9.09 1.01 1.33 1.08 1.071.36154E+

1313,848,036,400,000

8/8/2019 Indian Auto Marekt_II

http://slidepdf.com/reader/full/indian-auto-marektii 39/84

39

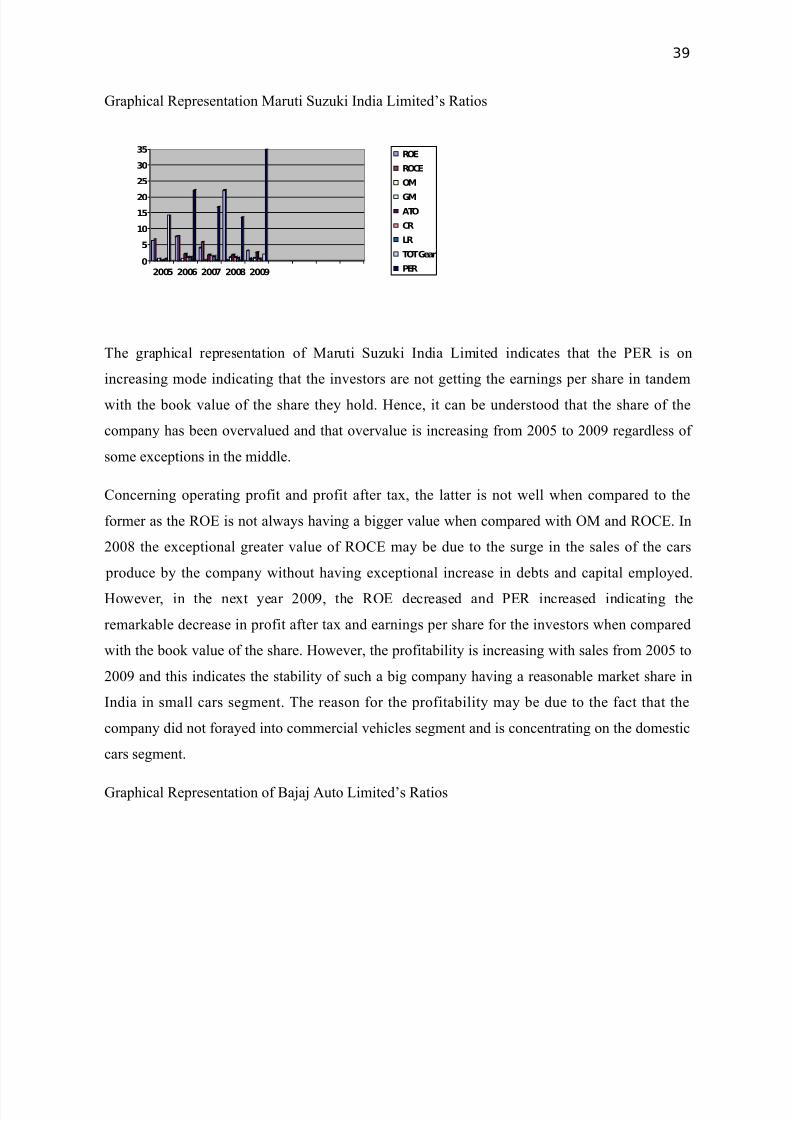

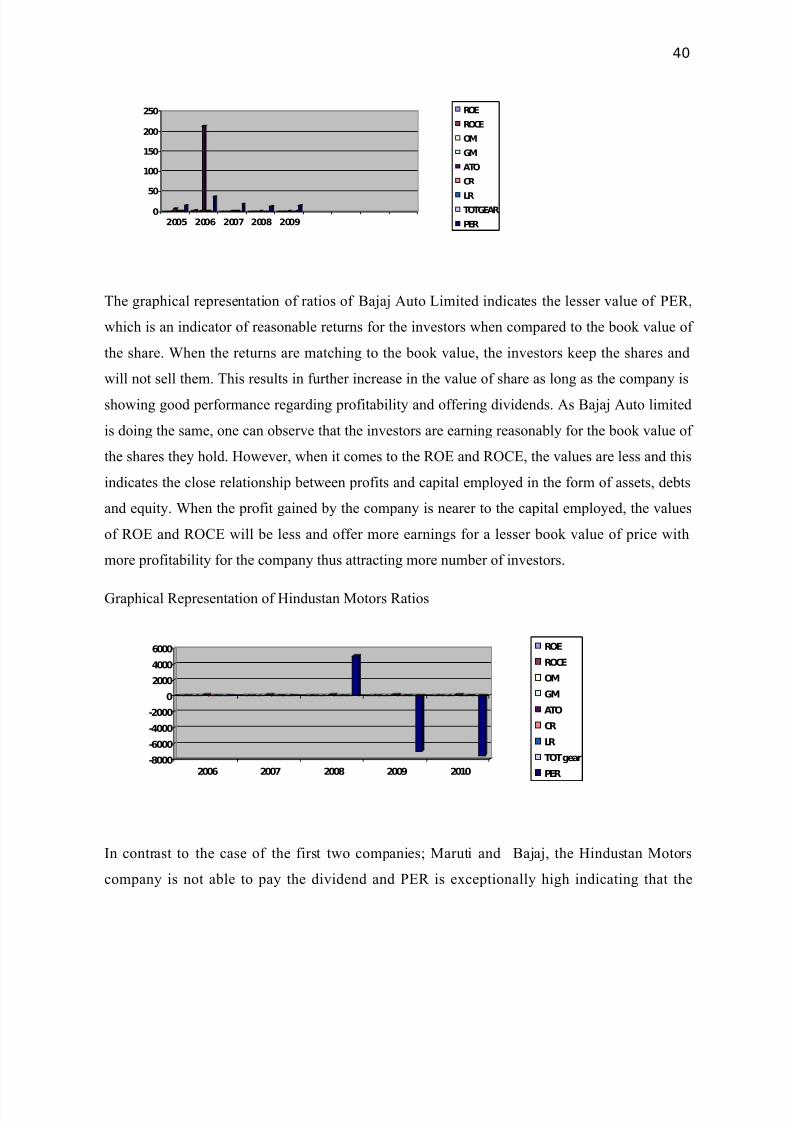

Graphical Representation Maruti Suzuki India Limited’s Ratios

0

5

10

15

20

25

30

35

2005 2006 2007 2008 2009

ROE

ROCE

OM

GM

ATO

CR

LR

TOT Gear

PER

The graphical representation of Maruti Suzuki India Limited indicates that the PER is on

increasing mode indicating that the investors are not getting the earnings per share in tandemwith the book value of the share they hold. Hence, it can be understood that the share of the

company has been overvalued and that overvalue is increasing from 2005 to 2009 regardless of

some exceptions in the middle.

Concerning operating profit and profit after tax, the latter is not well when compared to the

former as the ROE is not always having a bigger value when compared with OM and ROCE. In