Embed Size (px)

Citation preview

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 1 of 137

IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLORADO

Civil Action No. 1:12-cv-00292-WJM-KMT

In re MOLYCORP, INC. SECURITIES LITIGATION.

PLAINTIFFS’ CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF FEDERAL SECURITIES LAWS

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 2 of 137

TABLE OF CONTENTS

Page

NATUREOF THE ACTION ..........................................................................................................1

JURISDICTIONAND VENUE ......................................................................................................4

PARTIES.........................................................................................................................................4

Plaintiffs...............................................................................................................................4

The1934 Act Defendants ....................................................................................................6

The 1933 Act Defendants ..................................................................................................18

Control Person/Group Published Information Allegations................................................27

SUBSTANTIVE ALLEGATIONS ...............................................................................................29

Background........................................................................................................................29

Molycorp’s Modernization and Expansion Plan for Mountain Pass: “Project Phoenix”.................................................................................................................30

Defendants’ Unlawful Scheme ..........................................................................................31

SUMMARY OF SCIENTER ALLEGATIONS............................................................................36

Defendants’ Knowledge or Reckless Disregard of Materially Adverse Non-Public Facts.......................................................................................................................36

DEFENDANTS WERE MOTIVATED TO COMMIT FRAUD..................................................40

Motivation to Commit Securities Fraud: Insider Trading..................................................40

Motivation: Acquisition of Silmet Grupp..........................................................................42

Motivation: Molycorp’s Convertible Senior Note Offering..............................................44

MATERIALLY FALSE AND MISLEADING STATEMENTS DURING THE CLASS PERIOD.............................................................................................................................44

POST CLASS-PERIOD EVENTS ................................................................................................71

LOSS CAUSATION/ECONOMIC LOSS ....................................................................................74

- i -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 3 of 137

Page

FRAUD-ON-THE-MARKET PRESUMPTION OF RELIANCE................................................76

NOSAFE HARBOR .....................................................................................................................77

CLASS ACTION ALLEGATIONS ..............................................................................................78

FIRST CLAIM FOR RELIEF ...........................................................................................80

For Violations of §10(b) of the 1934 Act and Rule 10b-5 Against Defendants Molycorp, Smith, KMSMITH, Allen, Ashburn, Bhappu, Burba, Cogut, Pegasus, Dolan, RCF, Kristoff, T-II Holdings, Henry and Thompson................................................................80

SECOND CLAIM FOR RELIEF ......................................................................................83

For Violations of §20(a) of the 1934 Act Against Defendants Molycorp, Smith, KMSMITH, Allen, Ashburn, Bhappu, Burba, Cogut, Pegasus, Dolan, RCF, Kristoff, T-II Holdings, Henry and Thompson..................................................................................................83

THIRD CLAIM FOR RELIEF..........................................................................................85

For Violations of §20A(a) of the 1934 Act Against Defendants RCF and Bhappu.......................................................................................................85

FOURTH CLAIM FOR RELIEF ......................................................................................86

For Violations of §20A(b) of the 1934 Act Against Defendants Bhappu AndDolan..................................................................................................86

FIFTH CLAIM FOR RELIEF ...........................................................................................87

For Violations of §20A(c) of the 1934 Act Against Defendants Bhappu andDolan...................................................................................................87

SIXTH CLAIM FOR RELIEF...........................................................................................88

For Violations of §20A(a) of the 1934 Act Against Defendants Pegasus, Cogutand Kristoff .....................................................................................88

SEVENTH CLAIM FOR RELIEF....................................................................................89

- ii -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 4 of 137

Page

For Violations of §20A(b) of the 1934 Act Against Defendants Cogut and Kristoff.......................................................................................................89

EIGHTH CLAIM FOR RELIEF .......................................................................................90

For Violations of §20A(c) of the 1934 Act Against Defendants Cogut and Kristoff.......................................................................................................90

NINTH CLAIM FOR RELIEF..........................................................................................92

For Violations of §20A(a) of the 1934 Act Against Defendants T-II Holdings, Cogut and Kristoff.....................................................................92

TENTH CLAIM FOR RELIEF .........................................................................................93

For Violations of §20A(b) of the 1934 Act Against Defendants Cogut and Kristoff.......................................................................................................93

ELEVENTH CLAIM FOR RELIEF .................................................................................94

For Violations of §20A(c) of the 1934 Act Against Defendants Cogut and Kristoff.......................................................................................................94

TWELFTH CLAIM FOR RELIEF....................................................................................95

For Violations of §20A(a) of the 1934 Act Against Defendants KMSMITH and Smith ...............................................................................95

THIRTEENTH CLAIM FOR RELIEF .............................................................................96

For Violations of §20A(b) of the 1934 Act Against Defendant Smith..................96

FOURTEENTH CLAIM FOR RELIEF............................................................................97

For Violations of §20A(c) of the 1934 Act Against Defendant Smith..................97

FIFTEENTH CLAIM FOR RELIEF.................................................................................99

For Violations of §20A(a) of the 1934 Act Against Defendants Ashburn, Burbaand Thompson.................................................................................99

ALLEGATIONS SPECIFIC TO THE 1933 ACT ACTION ......................................................100

- iii -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 5 of 137

Page

MATERIALLY FALSE AND MISLEADING STATEMENTS IN THE OFFERING DOCUMENTS.................................................................................................................101

The February 11, 2011 Offering......................................................................................101

The June 10, 2011 Offering .............................................................................................102

FIRST CLAIM FOR RELIEF .........................................................................................104

For Violations of §11 of the 1933 Act in Connection with the Offering of Securities Against Defendants Molycorp, Smith, Allen, Ashburn, Ball, Bhappu, Cogut, Dolan, Kristoff, Machiels, Henry and Thompson................................................................................................104

SECOND CLAIM FOR RELIEF ....................................................................................106

For Violations of §12(a)(2) of the 1933 Act Against Defendants Smith, Allen, Ashburn, Ball, Bhappu, Cogut, Dolan, Kristoff, Machiels, Henry, Thompson, Morgan Stanley, J.P. Morgan, Knight, Dahlman, Stifel, BNP, CIBC, Piper Jaffray and RBS.............................106

THIRD CLAIM FOR RELIEF........................................................................................107

Violations of §15 of the 1933 Act Against All Defendants.................................107

PRAYER FOR RELIEF ..............................................................................................................108

JURY TRIAL DEMANDED.......................................................................................................109

- iv -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 6 of 137

NATURE OF THE ACTION

1. Lead Plaintiffs Randall Duck (“Duck”), Jerry W. Jewell (“Jewell”), Philip Marner

(“Marner”) and Donald E. McAlpin (“McAlpin”), and representative plaintiffs Iron Workers Mid-

South Pension Fund (the “Iron Workers”), Joseph Martiny (“Martiny”), Jayne McCarthy

(“McCarthy”), Robert Grabowski (“Grabowski”), Marjorine Dowd (“Dowd”), Kyle Hare (“Hare”),

Robert DeStefano (“DeStefano”) and Eugene R. Salmon (“Salmon”) (collectively, “plaintiffs”) bring

this action on their own behalf and on behalf of all other persons similarly situated, allege the

following based upon personal knowledge as to themselves and their own acts, information and

belief as to all other matters, based upon, inter alia , the investigation conducted by and through their

attorneys.

2. This is a class action for violations of the federal securities laws on behalf of all

purchasers or acquirers of Molycorp, Inc. (“Molycorp” or the “Company”) securities from February

11, 2011 through November 10, 2011 (the “Class Period”), including all persons who purchased or

acquired Molycorp 5.50% Series A Mandatory Convertible Preferred Stock (“Preferred Stock”)

pursuant to the February 11, 2011 initial public offering (“Preferred Stock IPO”) and all persons who

purchased or acquired Molycorp common stock pursuant to the June 10, 2011 secondary offering

(“Secondary Offering”), and who were damaged thereby (the “Class”).

3. This action concerns defendants’ false and/or misleading statements and omissions

regarding the capabilities of the Company’s mine, known as Mountain Pass, located in San

Bernardino County, California. Specifically, throughout the Class Period, defendants falsely assured

investors that the Mountain Pass ore body contained commercial quantities of highly-valued “heavy

- 1 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 7 of 137

rare earth elements” (“HREEs”) and that users of “light rare earth elements” (“LREEs”) were not

switching to viable substitutes as the prices for LREEs skyrocketed during 2010 and 2011.

4. Specifically, and as described in detail at ¶¶94-95 below, according to former

Molycorp employees, including a mining equipment operator, analytical chemist and geologist, there

were not commercially significant volumes of HREEs in the Mountain Pass ore body or in the

Molycorp stockpiles. In addition, and as described in detail at ¶¶96-98 below, according to a leading

industry expert with extensive and long-term experience in the total rare earth supply chain who

personally visited the Mountain Pass mine prior to and during the Class Period, Molycorp will never

produce commercially significant volumes of HREE from the Mountain Pass ore body. The industry

expert has personal knowledge that Molycorp, prior to and during the Class Period, in desperate

efforts to purchase companies with proven deposits of commercial volumes and recoverable levels of

HREEs because Molycorp’s Mountain Pass mine ore body does not have commercially viable

amounts of HREEs. In fact, shortly before June 2009, the industry expert personally viewed a

Molycorp internal report authored by a Molycorp Vice President, which indicated that the Mountain

Pass ore body did not have commercially viable amounts of HREEs.

5. Defendants’ Class Period false and/or misleading statements and omissions

artificially inflated Molycorp’s security prices, allowed the insider selling defendants to unload, in

less than four months, the staggering sum of more than $1.5 billion of their personal holdings of

Company stock. In addition, it allowed the Company to complete a $207 million Preferred Stock

IPO, a $586.5 million Secondary Offering of common stock and facilitated the acquisition of

Aktsiaselts Silmet Grupp (“Silmet Grupp”) for the purpose of creating the illusion that Molycorp

would be producing HREEs in commercial quantities. As the truth about defendants’ false and/or

- 2 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 8 of 137

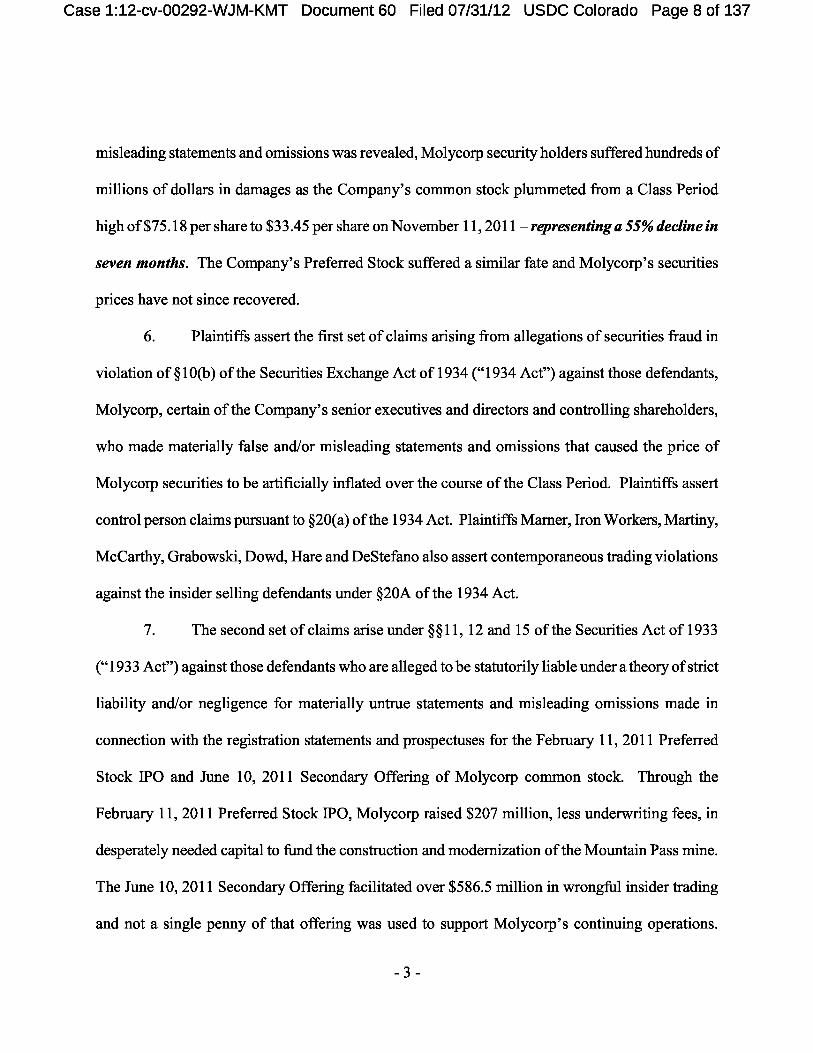

misleading statements and omissions was revealed, Molycorp security holders suffered hundreds of

millions of dollars in damages as the Company’s common stock plummeted from a Class Period

high of $75.18 per share to $33.45 per share on November 11, 2011 – representing a 55% decline in

seven months . The Company’s Preferred Stock suffered a similar fate and Molycorp’s securities

prices have not since recovered.

6. Plaintiffs assert the first set of claims arising from allegations of securities fraud in

violation of §10(b) of the Securities Exchange Act of 1934 (“1934 Act”) against those defendants,

Molycorp, certain of the Company’s senior executives and directors and controlling shareholders,

who made materially false and/or misleading statements and omissions that caused the price of

Molycorp securities to be artificially inflated over the course of the Class Period. Plaintiffs assert

control person claims pursuant to §20(a) of the 1934 Act. Plaintiffs Marner, Iron Workers, Martiny,

McCarthy, Grabowski, Dowd, Hare and DeStefano also assert contemporaneous trading violations

against the insider selling defendants under §20A of the 1934 Act.

7. The second set of claims arise under §§11, 12 and 15 of the Securities Act of 1933

(“1933 Act”) against those defendants who are alleged to be statutorily liable under a theory of strict

liability and/or negligence for materially untrue statements and misleading omissions made in

connection with the registration statements and prospectuses for the February 11, 2011 Preferred

Stock IPO and June 10, 2011 Secondary Offering of Molycorp common stock. Through the

February 11, 2011 Preferred Stock IPO, Molycorp raised $207 million, less underwriting fees, in

desperately needed capital to fund the construction and modernization of the Mountain Pass mine.

The June 10, 2011 Secondary Offering facilitated over $586.5 million in wrongful insider trading

and not a single penny of that offering was used to support Molycorp’s continuing operations.

- 3 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 9 of 137

Plaintiffs also assert control person claims pursuant to §15 of the 1933 Act. Consistent with the

Tenth Circuit’s decision in Schwartz v. Celestial Seasonings , 124 F.3d 1246, 1251-52 (10th Cir.

1997), and recent court decisions within the Tenth Circuit, plaintiffs’ non-fraud allegations in

support of the 1933 Act claims are pled as separate, stand-alone claims under the notice pleading

standards of Fed. R. Civ. P. 8(a).

JURISDICTION AND VENUE

8. The claims asserted herein arise under §§11, 12(a)(2) and 15 of the 1933 Act (15

U.S.C. §§77k, 77l and 77o) and under §§10(b), 20(a) and 20A of the 1934 Act (15 U.S.C. §§78j(b),

78t(a) and 78t-1) and Rule 10b-5 (17 C.F.R. §240.10b-5) promulgated thereunder by the Securities

and Exchange Commission (“SEC”). Jurisdiction is conferred by §22 of the 1933 Act (15 U.S.C.

§77v) and §27 of the 1934 Act (15 U.S.C. §78aa). Venue is proper pursuant to §22 of the 1933 Act

and §27 of the 1934 Act. Molycorp’s headquarters are located in Greenwood Village, Colorado and

many of the acts and transactions constituting the violations of the securities laws alleged herein

occurred in this District.

9. In connection with the acts and conduct alleged herein, defendants, directly and

indirectly, used the means and instrumentalities of interstate commerce, including, but not limited to,

the United States mails, interstate telephone communications and the facilities of the national

securities exchanges and markets.

PARTIES

Plaintiffs

10. Plaintiff Duck purchased Molycorp common stock during the Class Period, as set

forth in the certification accompanying the Motion to Appoint the Molycorp Shareholder Group as

- 4 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 10 of 137

Lead Plaintiff, and was damaged as a result of defendants’ conduct as alleged herein. See Dkt. No.

29-2.

11. Plaintiff Jewell purchased Molycorp common stock during the Class Period, as set

forth in the certification accompanying the Motion to Appoint the Molycorp Shareholder Group as

Lead Plaintiff, and was damaged as a result of defendants’ conduct as alleged herein. See Dkt. No.

29-2.

12. Plaintiff Marner purchased Molycorp common stock during the Class Period, as set

forth in the certification accompanying the Motion to Appoint the Molycorp Shareholder Group as

Lead Plaintiff, and was damaged as a result of defendants’ conduct as alleged herein. See Dkt. No.

29-2.

13. Plaintiff McAlpin purchased Molycorp common stock during the Class Period, as set

forth in the certification accompanying the Motion to Appoint the Molycorp Shareholder Group as

Lead Plaintiff, and was damaged as a result of defendants’ conduct as alleged herein. See Dkt. No.

29-2.

14. Representative plaintiff Iron Workers purchased Molycorp common stock during the

Class Period, as set forth in the certification attached hereto, and was damaged as a result of

defendants’ conduct as alleged herein.

15. Representative plaintiff Martiny purchased Molycorp common stock during the Class

Period, as set forth in the certification attached hereto, and was damaged as a result of defendants’

conduct as alleged herein.

- 5 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 11 of 137

16. Representative plaintiff McCarthy purchased Molycorp common stock during the

Class Period, as set forth in the certification attached hereto, and was damaged as a result of

defendants’ conduct as alleged herein.

17. Representative plaintiff Grabowski purchased Molycorp common stock during the

Class Period, as set forth in the certification attached hereto, and was damaged as a result of

defendants’ conduct as alleged herein.

18. Representative plaintiff Dowd purchased Molycorp common stock during the Class

Period, as set forth in the certification attached hereto, and was damaged as a result of defendants’

conduct as alleged herein.

19. Representative plaintiff Hare purchased Molycorp common stock during the Class

Period, as set forth in the certification attached hereto, and was damaged as a result of defendants’

conduct as alleged herein.

20. Representative plaintiff DeStefano purchased Molycorp common stock during the

Class Period, as set forth in the certification attached hereto, and was damaged as a result of

defendants’ conduct as alleged herein.

21. Representative plaintiff Salmon purchased Molycorp preferred stock in connection

with the Company’s February 2011 Preferred Stock IPO, as set forth in the certification attached

hereto, and was damaged as a result of defendants’ conduct as alleged herein.

The 1934 Act Defendants

22. Defendant Molycorp is a rare earth element (‘REE”) mining business, engaged in the

production and sale of rare earth oxides in the western hemisphere. The Company’s products

include rare earth oxides, metals, alloys and magnets for various inputs in existing and emerging

- 6 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 12 of 137

applications and water treatment technology. The Company owns and operates the Mountain Pass

facility, an open-pit mine located in San Bernardino County, California. Molycorp maintains its

corporate headquarters at 5619 Denver Tech Center Parkway, Suite 1000, Greenwood Village,

Colorado.

23. Defendant Mark A. Smith (“Smith”) was, at all relevant times, Chief Executive

Officer (“CEO”), President and a Director of Molycorp. During the Class Period, Smith participated

in the issuance of false and/or materially misleading statements and omissions and failed to disclose

the true facts about the capabilities of the Mountain Pass mine. In addition to issuing statements

throughout the Class Period, Smith continuously had the opportunity to correct misstatements and

omissions by and on behalf of Molycorp, but failed to do so. During the Class Period, Smith

reported indirect and direct sales of 259,260 shares of the Molycorp common stock for proceeds of

$13.1 million . These insider sales amounted to more than 21% of Smith’s total Class Period

holdings of Molycorp common stock.

24. As CEO, President and a Director, Smith was responsible for directing Molycorp’s

financial and business affairs. During conference calls and meetings with analysts and investors,

Smith repeatedly held himself out as knowledgeable about the Company’s operating and financial

condition, including, specifically, the characteristics of the ore body at Mountain Pass. Further, in

conjunction with each of the Company’s Class Period financial reports filed with the SEC, Smith

assured investors that he, together with defendant James S. Allen was “responsible for . . .

maintaining disclosure controls and . . . [d]esigned such disclosure controls and procedures . . . to

ensure that material information relating to [Molycorp], including it consolidated subsidiaries, is

made known to us by others within [Molycorp].” At no time during the Class Period did Smith or

- 7 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 13 of 137

any other defendant assert that they were not aware of material aspects of Molycorp’s mining

operations.

25. Reinforcing the claim that Smith, along with other Molycorp senior executives, was

aware of material adverse information concerning the Mountain Pass mine, the Company’s SEC

filings stated “Smith[] [has] broad experience in the rare earths mining industry and [a] deep

understanding of the operations at our Mountain Pass facility.” In addition, Smith has been involved

with the operation and development of the Mountain Pass mine for over 24 years.

26. Further reinforcing the claim that Smith, along with other Molycorp senior

executives, monitored and was aware of material information regarding the existence, or lack

thereof, of HREEs at the Mountain Pass mine, the Company’s SEC filings stated that Smith’s

incentive compensation during the Class Period was primarily based upon “achieving various

financial objectives, such as ensuring full funding of Project Phoenix” (10% weighting) and

“successful completion of various [Project Phoenix] milestones related to our business

modernization and expansion plans, such as meeting schedule and cost targets, submitting

applications and securing all required [] permits” (40% weighting). Defendants and the market

understood Project Phoenix to be a reference to the Mountain Pass mine modernization project. For

2011, Smith was awarded $742,910 in incentive compensation in connection with his monitoring

and achievement of Project Phoenix milestones.

27. Defendant KMSMITH LLC (“KMSMITH”) was, at all relevant times, a Delaware

limited liability company having a registered agent located at 1811 Silverside Road, Wilmington,

Delaware and listing its address in SEC filings as c/o Molycorp, Inc., 5619 Denver Tech Center

Parkway, Suite 1000, Greenwood Village, Colorado, Attention: Mark A. Smith. At the times

- 8 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 14 of 137

specified herein, KMSMITH, through its employees or agents, engaged in inside trading in violation

of §§10(b) and 20A of the 1934 Act (15 U.S.C. §§78j(b) and 78t(1)) and Rules 10b-5 and 10b5-1

promulgated thereunder by the SEC (17 C.F.R. §240.10b-5) at the direction of, and/or based on

material, adverse, non-public information provided by Smith, who had the power to control, and did

control, KMSMITH. Smith is married to Kimberly Smith, who purportedly has sole voting and

investment power with respect to KMSMITH. During the Class Period, KMSMITH reported sales

of 148,301 shares of Molycorp common stock for proceeds of $7.5 million . These insider sales

amounted to 49% of KMSMITH’s total Class Period holdings of Molycorp common stock.

28. Defendant James S. Allen (“Allen”) was, at all relevant times, Chief Financial Officer

(“CFO”) and Treasurer of Molycorp. During the Class Period, Allen participated in the issuance of

false and/or materially misleading statements and omissions and failed to disclose the true facts

about the capabilities of the Mountain Pass mine. In addition to issuing statements throughout the

Class Period, Allen continuously had the opportunity to correct misstatements and omissions by and

on behalf of Molycorp.

29. As CFO and Treasurer, Allen was responsible for directing Molycorp’s financial and

business affairs. During conference calls and meetings with analysts and investors, Allen repeatedly

held himself out as knowledgeable about the Company’s operating and financial condition, including

the capabilities of the Mountain Pass mine. Further, in conjunction with each of the Company’s

Class Period financial reports filed with the SEC, Allen assured investors that he, together with

defendant Smith, was “responsible for . . . maintaining disclosure controls and . . . [d]esigned such

disclosure controls and procedures . . . to ensure that material information relating to [Molycorp],

including its consolidated subsidiaries, is made known to us by others within [Molycorp].” At no

- 9 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 15 of 137

time during the Class Period did Allen or any other defendant assert that they were not aware of

material aspects of Molycorp’s mining operations.

30. Reinforcing the claim that Allen, along with other Molycorp senior executives,

monitored and was aware of material information regarding the existence, or lack thereof, of HREEs

at the Mountain Pass mine, the Company’s SEC filings stated that Allen’s incentive compensation

during the Class Period was primarily based upon “achieving various financial objectives, such as

ensuring full funding of Project Phoenix” (10% weighting) and “successful completion of various

[Project Phoenix] milestones related to our business modernization and expansion plans, such as

meeting schedule and cost targets, submitting applications and securing all required [] permits” (40%

weighting). For 2011, Allen was awarded $258,282 in incentive compensation in connection with

his monitoring and achievement of Project Phoenix milestones.

31. Defendant John F. Ashburn, Jr. (“Ashburn”) was, at all relevant times Executive Vice

President and General Counsel of Molycorp. During the Class Period, Ashburn participated in the

issuance of false and/or materially misleading statements and omissions and failed to disclose the

true facts about the capabilities of the Mountain Pass mine. In addition to issuing statements

throughout the Class Period, Ashburn continuously had the opportunity to correct misstatements and

omissions by and on behalf of Molycorp, but failed to do so. During the Class Period, Ashburn

reported direct sales of 95,184 shares of Molycorp common stock for proceeds of $4.8 million .

These insider sales amounted to 34% of Ashburn’s total Class Period holdings of Molycorp common

stock.

32. Prior to joining Molycorp, Ashburn was Senior Counsel of Chevron Mining, Inc., a

wholly-owned subsidiary of Chevron Corporation. Prior to joining Chevron Mining, Inc., Ashburn

- 10 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 16 of 137

was Senior Counsel of Unocal Corporation. Ashburn was involved in various aspects of the

Mountain Pass mine, in his capacity as Senior Counsel with Chevron Mining, Inc. and Unocal

Corporation, since the mid-1990s. All told, Ashburn has nearly 20 years combined service with

various companies that owned and/or operated the Mountain Pass mine, including, Chevron Mining,

Inc., Unocal Corporation and, finally, Molycorp.

33. Reinforcing the claim that Ashburn, along with other Molycorp senior executives,

monitored and was aware of material information regarding the existence, or lack thereof, of HREEs

at the Mountain Pass mine, the Company’s SEC filings stated that Ashburn’s incentive

compensation during the Class Period was primarily based upon “achieving various financial

objectives, such as ensuring full funding of Project Phoenix” (10% weighting) and “successful

completion of various [Project Phoenix] milestones related to our business modernization and

expansion plans, such as meeting schedule and cost targets, submitting applications and securing all

required [] permits” (40% weighting). For 2011, Ashburn was awarded $258,282 in incentive

compensation in connection with his monitoring and achievement of Project Phoenix milestones.

34. Defendant Ross R. Bhappu (“Bhappu”) was, at all relevant times, the Chairman of the

Board of Molycorp. During the Class Period, Bhappu participated in the issuance of false and/or

materially misleading statements and omissions and failed to disclose the true facts about the

capabilities of the Mountain Pass mine. In addition to issuing statements throughout the Class

Period, Bhappu repeatedly had the opportunity to correct misstatements and omissions by and on

behalf of Molycorp, but failed to do so. According to the Company’s SEC filings, Bhappu has been

associated with the mining industry for over 25 years and has a background in metallurgical

engineering and mining project finance. Bhappu was previously employed by Newmont Mining,

- 11 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 17 of 137

GTN Copper Corporation and Cyprus Minerals. According to the Company’s SEC filings, with

Bhappu’s “comprehensive knowledge of the mining industry . . ., [he] is a key member of [the

Company’s] Board of Directors.” Since 2005, Bhappu has been a partner of Resource Capital

Funds. Resource Capital Funds, along with the Traxys Group and Pegasus Capital Advisors, L.P.

(“Pegasus”) (discussed below), was a principal investor in connection with the acquisition of the

Mountain Pass mine from Chevron Mining, Inc. in 2008. During the Class Period, Bhappu reported

indirect sales of 13,769,319 shares of Molycorp common stock for proceeds of $694.2 million .

These insider sales amounted to 49.8% of Bhappu’s total Class Period holdings of Molycorp

common stock.

35. Defendant John L. Burba (“Burba”) was, at all relevant times, Executive Vice

President and Chief Technology Officer of Molycorp. During the Class Period, Burba participated

in the issuance of false and/or materially misleading statements and omissions and failed to disclose

the true facts about the capabilities of the Mountain Pass mine. In addition to issuing statements

during the Class Period, Burba continuously had the opportunity to correct misstatements and

omissions by and on behalf of Molycorp, including through his reported sale of 118,982 shares of

Molycorp common stock for proceeds of $6.0 million . These insider sales amounted to 34.7% of

Burba’s total Class Period holdings of Molycorp common stock.

36. Reinforcing the claim that Burba, along with other Molycorp senior executives,

monitored and was aware of material information regarding the existence, or lack thereof, of HREEs

at the Mountain Pass mine, the Company’s SEC filings stated that Burba’s incentive compensation

during the Class Period was primarily based upon “achieving various financial objectives, such as

ensuring full funding of Project Phoenix” (10% weighting) and “successful completion of various

- 12 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 18 of 137

[Project Phoenix] milestones related to our business modernization and expansion plans, such as

meeting schedule and cost targets, submitting applications and securing all required [] permits” (40%

weighting). For 2011, Burba was awarded $258,282 in incentive compensation in connection with

his monitoring and achievement of Project Phoenix milestones.

37. Defendant Craig M. Cogut (“Cogut”) was, at all relevant times, a managing director

at Pegasus Capital LLC, which controls Molycorp LLC, the entity that was formed to acquire the

Mountain Pass mine from Chevron Mining, Inc. During the Class Period, Cogut participated in the

issuance of false and/or materially misleading statements and omissions and failed to disclose the

true facts about the capabilities of the Mountain Pass mine. In addition to issuing statements

throughout the Class Period, Cogut continuously had the opportunity to correct misstatements and

omissions by and on behalf of Molycorp, but failed to do so. During the Class Period, Cogut

reported indirect sales of 12,270,073 shares of Molycorp common stock for proceeds of $618.7

million . These insider sales amounted to 50.1% of Cogut’s total Class Period holdings of Molycorp

common stock. Cogut is the founder and a partner of Pegasus. Pegasus, along with the Traxys

Group and Resource Capital Funds, was a principal investor in connection with the acquisition of the

Mountain Pass mine from Chevron Mining, Inc. in 2008. During the Class Period, Cogut and the

entities he controlled were beneficial owners of more than 5% of the outstanding common stock of

Molycorp.

38. Defendant Pegasus was, at all relevant times, a Delaware limited partnership with

offices at 505 Park Avenue, 21st floor, New York, New York. At the times specified herein,

Pegasus, through its owners, employees or agents, or the owners, employees or agents of its general

partners, limited partners and/or affiliates Pegasus Capital Advisors IV GP, LLC; Pegasus Capital

- 13 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 19 of 137

Advisors IV, L.P.; MP IH Holdings 1, LLC; MP IH Holdings 2, LLC; Pegasus Capital LLC;

Pegasus Investors IV GP, LLC; Pegasus Investors IV, L.P.; Pegasus Partners IV, L.P.; PP IV

Mountain Pass II, LLC; Pegasus Partners IV (AIV), L.P.; PP IV MP AIV 1, LLC; PP IV MP AIV 2,

LLC; PP IV MP AIV 3, LLC; and/or T-II Holdings, LLC; engaged in inside trading in violation of

§§10(b) and 20A of the 1934 Act (15 U.S.C. §§78j(b) and 78t(1)) and Rules 10b-5 and 10b5-1

promulgated thereunder by the SEC (17 C.F.R. §240.10b-5) at the direction of, and/or based on

material, adverse, non-public information provided by, Cogut who is the founder and managing

partner of Pegasus and/or defendant Mark Kristoff who is the CEO of T-II Holdings, LLC (both

discussed below). Moreover, Cogut had the power to control, and did control, Pegasus. During the

Class Period, Pegasus reported sales of 12,270,073 shares of Molycorp common stock for proceeds

of $618.7 million . These insider sales amounted to 50.1% of Pegasus’ total Class Period holdings of

Molycorp common stock.

39. Defendant Brian T. Dolan (“Dolan”) was, at all relevant times, a Director of

Molycorp. During the Class Period, Dolan participated in the issuance of false and/or materially

misleading statements and omissions and failed to disclose the true facts about the capabilities of the

Mountain Pass mine. In addition to issuing statements throughout the Class Period, Dolan

continuously had the opportunity to correct misstatements and omissions by and on behalf of

Molycorp, but failed to do so. During the Class Period, Dolan provided RCF Management, LLC

(“RCF”) (discussed below) with material, adverse, non-public information concerning Molycorp,

upon which it, directly, and Bhappu, indirectly, executed direct sales of 13,769,319 shares of

Molycorp common stock for proceeds of $694.2 million . These insider sales amounted to 49.8% of

RCF’s total Class Period holdings of Molycorp common stock.

- 14 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 20 of 137

40. Defendant RCF, was, at all relevant times, a Delaware limited liability corporation

doing business as Resource Capital Funds, with offices in this District at 1400 Sixteenth Street, Suite

200, Denver, Colorado. At the times specified herein, RCF, through its owners, employees or

agents, or the owners, employees or agents of its general partners, limited partners and/or affiliates

Resource Capital Associates IV, LP; Resource Capital Fund IV, LP; RCA IV GP, LLC; Resource

Capital Associates V, LP; Resource Capital Fund V, LP; RCA V GP, Ltd.; and/or RCF US

Holdings, L.P.; engaged in inside trading in violation of §§10(b) and 20A of the 1934 Act (15 U.S.C.

§§78j(b) and 78t(1)) and Rules 10b-5 and 10b5-1 promulgated thereunder by the SEC (17 C.F.R.

§240.10b-5) at the direction of, and/or based on material, adverse, non-public information provided

by, defendant Bhappu who is a partner at RCF and serves on RCF’s investment committee and

defendant Dolan who served as counsel for RCF from its inception until December 31, 2011.

Moreover, Bhappu had the power to control, and did control, RCF. During the Class Period, RCF

reported direct sales of 13,769,319 shares of Molycorp common stock for proceeds of $694.2

million . These insider sales amounted to 49.8% of RCF’s total Class Period holdings of Molycorp

common stock.

41. Defendant Mark Kristoff (“Kristoff”) was, at all relevant times, a Director of

Molycorp. Kristoff has been the CEO of the Traxys Group since April 2005, which is a global

trading, marketing and distribution concern. During the Class Period, Kristoff participated in the

issuance of false and/or materially misleading statements and omissions and failed to disclose the

true facts about the capabilities of the Mountain Pass mine. In addition to issuing statements

throughout the Class Period, Kristoff continuously had the opportunity to correct misstatements and

omissions by and on behalf of Molycorp, but failed to do so. During the Class Period, Kristoff

- 15 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 21 of 137

reported direct and indirect sales of 4,774,448 shares of Molycorp common stock for proceeds of

$240.7 million . These insider sales amounted to 52% of Kristoff’s total direct and indirect Class

Period holdings of Molycorp common stock. According to the Company’s SEC filings, “Kristoff’s

experience in global trading, financing, supply chain management, and distribution of metals and

[rare earth elements] provides valuable insight to [Molycorp’s] Board of Directors regarding existing

and potential opportunities in the rare earths markets.” The Traxys Group, along with Pegasus and

Resource Capital Funds, was a principal investor in connection with the acquisition of the Mountain

Pass mine from Chevron Mining, Inc. in 2008.

42. Defendant T-II Holdings, LLC (“T-II Holdings”), was, at all relevant times, an

Anguillan limited liability corporation with offices at 825 Third Avenue, 9th Floor, New York, New

York. At the times specified herein, T-II Holdings, through its owners, employees or agents, or the

owners, employees or agents of its wholly owned companies, subsidiaries and/or affiliates Pegasus,

TNA Moly Group LLC (“TNA Moly”); Traxys S.a.r.l. (“Traxys S”); and Traxys North America,

LLC (“Traxys”); engaged in inside trading in violation of §§10(b) and 20A of the 1934 Act (15

U.S.C. §§78j(b) and 78t(1)) and Rules 10b-5 and 10b5-1 promulgated thereunder by the SEC (17

C.F.R. §240.10b-5) at the direction of, and/or based on material, adverse, non-public information

provided by, defendant Kristoff who is the CEO of T-II Holdings, TNA Moly, Traxys S and Traxys

and/or defendant Cogut who is the founder and managing partner of Pegasus. During the Class

Period, T-II Holdings reported sales of 4,584,710 shares of Molycorp common stock for proceeds of

over $230 million . These insider sales amounted to 52% of T-II Holdings’ total Class Period

holdings of Molycorp common stock.

- 16 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 22 of 137

43. Defendant Charles R. Henry (“Henry”) was, at all relevant times, a Director of

Molycorp. During the Class Period, Henry participated in the issuance of false and/or materially

misleading statements and omissions and failed to disclose the true facts about the capabilities of the

Mountain Pass mine. In addition to issuing statements throughout the Class Period, Henry

continuously had the opportunity to correct misstatements and omissions by and on behalf of

Molycorp, but failed to do so. During the Class Period, Henry reported direct sales of 69,000 shares

of Molycorp common stock for proceeds of $3.5 million . These insider sales amounted to 51% of

Henry’s total Class Period holdings of Molycorp common stock. According to the Company’s SEC

filings, Henry’s “strong background in management . . . brings significant organizational acumen to

[Molycorp’s] Board of Directors.”

44. Defendant Jack E. Thompson (“Thompson”) was, at all relevant times, a Director of

Molycorp. During the Class Period, Thompson participated in the issuance of false and/or materially

misleading statements and omissions and failed to disclose the true facts about the capabilities of the

Mountain Pass mine. In addition to issuing statements throughout the Class Period, Thompson

continuously had the opportunity to correct misstatements and omissions by and on behalf of

Molycorp, but failed to do so. During the Class Period, Thompson reported direct sales of 63,706

shares of Molycorp common stock for proceeds of $3.2 million . These insider sales amounted to

47.9% of Thompson’s total Class Period holdings of Molycorp common stock. According to the

Company’s SEC filings, Thompson served on a number of board of directors of mining companies

and “brings extensive knowledge of the mining industry and broad management experience to [the

Company’s] Board of Directors.”

- 17 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 23 of 137

45. Defendants Molycorp, Smith, KMSMITH, Allen, Ashburn, Bhappu, Dolan, RCF,

Burba, Cogut, Pegasus, Kristoff, T-II Holdings, Henry and Thompson are referred to herein

collectively as the “1934 Act Defendants.”

46. Defendants Smith, KMSMITH, Allen, Ashburn, Bhappu, Dolan, RCF, Burba, Cogut,

Pegasus, Kristoff, T-II Holdings, Henry and Thompson are referred to herein collectively as the

“Insider Selling Defendants.”

The 1933 Act Defendants

47. On February 11, 2011, Molycorp issued 2.07 million shares of Preferred Stock to

trade under the symbol “MCP-PA.” The registration statements for the Preferred Stock IPO were

signed and filed with the SEC on or about February 7 and February 10, 2011. Molycorp is

statutorily liable under §§11 and 12 of the 1933 Act for the materially untrue statements incorporated

and contained in the Preferred Stock IPO offering documents. Molycorp also was responsible for

the issuance of the materially untrue statements incorporated in the June 10, 2011 Secondary

Offering of its common stock and, therefore, is liable under §§11 and 12 of the 1933 Act for the

materially untrue statements incorporated and contained in the Secondary Offering documents. The

registration statement for the Secondary Offering was filed with the SEC on June 7, 2011.

48. As alleged above, defendant Smith was, at all relevant times, CEO, President and a

Director of Molycorp. Smith signed the Company’s February 7 and February 10, 2011 registration

statements for the February 11, 2011 Preferred Stock IPO and the June 7, 2011 registration statement

for the June 10, 2011 Secondary Offering of common stock, which were then incorporated into the

preferred stock and common stock offering prospectuses. Smith was a member of the Board of

Directors at the time of the offerings. Smith is statutorily liable under §§11, 12 and/or 15 of the

- 18 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 24 of 137

1933 Act for the materially untrue statements incorporated and contained in the offering documents.

Smith failed to perform adequate due diligence and/or did not possess reasonable grounds for the

belief that the statements contained in and incorporated in the offering documents were true and

without omissions of any material facts and were not misleading.

49. As alleged above, defendant Allen was, at all relevant times, CFO and Treasurer of

Molycorp. Allen signed the Company’s February 7 and February 10, 2011 registration statements

for the February 11, 2011 Preferred Stock IPO and the June 7, 2011 registration statement for the

June 10, 2011 Secondary Offering of common stock, which were then incorporated into the

preferred stock and common stock offering prospectuses. Allen is statutorily liable under §§11, 12

and/or 15 of the 1933 Act for the materially untrue statements incorporated and contained in the

offering documents. Allen failed to perform adequate due diligence and/or did not possess

reasonable grounds for the belief that the statements contained in and incorporated in the offering

documents were true and without omissions of any material facts and were not misleading.

50. As alleged above, defendant Ashburn was, at all relevant times Executive Vice

President and General Counsel of Molycorp. Ashburn signed the Company’s February 7 and

February 10, 2011 registration statements for the February 11, 2011 Preferred Stock IPO and the

June 7, 2011 registration statement for the June 10, 2011 Secondary Offering of common stock,

which were then incorporated into the preferred stock and common stock offering prospectuses.

Ashburn is statutorily liable under §§11, 12 and/or 15 of the 1933 Act for the materially untrue

statements incorporated and contained in the offering documents. Ashburn failed to perform

adequate due diligence and/or did not possess reasonable grounds for the belief that the statements

- 19 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 25 of 137

contained in and incorporated in the offering documents were true and without omissions of any

material facts and were not misleading.

51. Defendant Russell D. Ball (“Ball”) was, at all relevant times, a Director of Molycorp.

According to the Company’s SEC filings, “Ball brings a unique and important understanding of

finance and accounting in the international mining industry to our Board of Directors.” Ball signed

the Company’s February 7 and February 10, 2011 registration statements for the February 11, 2011

Preferred Stock IPO and the June 7, 2011 registration statement for the June 10, 2011 Secondary

Offering of common stock, which were then incorporated into the preferred stock and common stock

offering prospectuses. Ball is statutorily liable under §§11, 12 and/or 15 of the 1933 Act for the

materially untrue statements incorporated and contained in the offering documents. Ball failed to

perform adequate due diligence and/or did not possess reasonable grounds for the belief that the

statements contained in and incorporated in the offering documents were true and without omissions

of any material facts and were not misleading.

52. As alleged above, defendant Bhappu, was at all relevant times, the Chairman of the

Board of Molycorp. Bhappu signed the Company’s February 7 and February 10, 2011 registration

statements for the February 11, 2011 Preferred Stock IPO and the June 7, 2011 registration statement

for June 10, 2011 Secondary Offering of common stock, which were then incorporated into the

preferred stock and common stock offering prospectuses. Bhappu is statutorily liable under §§11, 12

and/or 15 of the 1933 Act for the materially untrue statements incorporated and contained in the

offering documents. Bhappu failed to perform adequate due diligence and/or did not possess

reasonable grounds for the belief that the statements contained in and incorporated in the offering

documents were true and without omissions of any material facts and were not misleading.

- 20 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 26 of 137

53. As alleged above, defendant Cogut was a controlling shareholder of Molycorp.

Cogut signed the Company’s February 7 and February 10, 2011 registration statements for the

February 11, 2011 Preferred Stock IPO and the June 7, 2011 registration statement for the June 10,

2011 Secondary Offering of common stock, which were then incorporated into the preferred stock

and common stock offering prospectuses. Cogut is statutorily liable under §§11, 12 and/or 15 of the

1933 Act for the materially untrue statements incorporated and contained in the offering documents.

Cogut failed to perform adequate due diligence and/or did not possess reasonable grounds for the

belief that the statements contained in and incorporated in the offering documents were true and

without omissions of any material facts and were not misleading.

54. As alleged above, defendant Dolan was, at all relevant times, a Director of Molycorp.

Dolan signed the Company’s February 7 and February 10, 2011 registration statements for the

February 11, 2011 Preferred Stock IPO and the June 7, 2011 registration statement for the June 10,

2011 Secondary Offering of common stock, which were then incorporated into the preferred stock

and common stock offering prospectuses. Dolan is statutorily liable under §§11, 12 and/or 15 of the

1933 Act for the materially untrue statements incorporated and contained in the offering documents.

Dolan failed to perform adequate due diligence and/or did not possess reasonable grounds for the

belief that the statements contained in and incorporated in the offering documents were true and

without omissions of any material facts and were not misleading.

55. As alleged above, defendant Kristoff was, at all relevant times, a Director of

Molycorp. Kristoff signed the Company’s February 7 and February 10, 2011 registration statements

for the February 11, 2011 Preferred Stock IPO and the June 7, 2011 registration statement for the

June 10, 2011 Secondary Offering of common stock, which were then incorporated into the

- 21 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 27 of 137

preferred stock and common stock offering prospectuses. Kristoff is statutorily liable under §§11,

12 and/or 15 of the 1933 Act for the materially untrue statements incorporated and contained in the

offering documents. Kristoff failed to perform adequate due diligence and/or did not possess

reasonable grounds for the belief that the statements contained in and incorporated in the offering

documents were true and without omissions of any material facts and were not misleading.

56. Defendant Alec Machiels (“Machiels”) was, at all relevant times, a Director of

Molycorp. According to the Company’s SEC filings, Machiels’ “strong background in financial

management and investment in commodity-related businesses provides [the Company’s] Board of

Directors with a valuable perspective on strategic, financial and capital raising matters.” Machiels

signed the Company’s February 7 and February 10, 2011 registration statements for the February 11,

2011 Preferred Stock IPO and the June 7, 2011 registration statement for the June 10, 2011

Secondary Offering, which were then incorporated into the preferred stock and common stock

offering prospectuses. Machiels is statutorily liable under §§11, 12 and/or 15 of the 1933 Act for the

materially untrue statements incorporated and contained in the offering documents. Machiels failed

to perform adequate due diligence and/or did not possess reasonable grounds for the belief that the

statements contained in and incorporated in the offering documents were true and without omissions

of any material facts and were not misleading.

57. As alleged above, defendant Henry was, at all relevant times, a Director of Molycorp.

Henry signed the Company’s February 7 and February 10, 2011 registration statements for the

February 11, 2011 Preferred Stock IPO and the June 7, 2011 registration statement for the June 10,

2011 Secondary Offering of common stock, which were then incorporated into the preferred stock

and common stock offering prospectuses. Henry is statutorily liable under §§11, 12 and/or 15 of the

- 22 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 28 of 137

1933 Act for the materially untrue statements incorporated and contained in the offering documents.

Henry failed to perform adequate due diligence and/or did not possess reasonable grounds for the

belief that the statements contained in and incorporated in the offering documents were true and

without omissions of any material facts and were not misleading.

58. As alleged above, defendant Thompson was, at all relevant times, a Director of

Molycorp. Thompson signed the Company’s February 7 and February 10, 2011 registration

statements for the February 11, 2011 Preferred Stock IPO and the June 7, 2011 registration statement

for the June 10, 2011 Secondary Offering of common stock, which were then incorporated into the

preferred stock and common stock offering prospectuses. Thompson is statutorily liable under §§11,

12 and/or 15 of the 1933 Act for the materially untrue statements incorporated and contained in the

offering documents. Thompson failed to perform adequate due diligence and/or did not possess

reasonable grounds for the belief that the statements contained in and incorporated in the offering

documents were true and without omissions of any material facts and were not misleading.

59. Defendant Morgan Stanley & Co. Incorporated acted as a lead underwriter of the IPO

of 2.07 million shares of Molycorp Preferred Stock in February 2011. Morgan Stanley & Co. LLC

acted as a lead underwriter of the Secondary Offering of 11.5 million shares of Molycorp common

stock in June 2011. Morgan Stanley & Co. Incorporated and Morgan Stanley & Co. LLC are

collectively referred to herein as “Morgan Stanley”. Morgan Stanley is statutorily liable under §§12

and/or 15 of the 1933 Act for the materially untrue statements incorporated and contained in the

offering documents. Morgan Stanley failed to perform adequate due diligence and/or did not possess

reasonable grounds for the belief that the statements contained in and incorporated in the offering

documents were true and without omissions of any material facts and were not misleading.

- 23 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 29 of 137

60. Defendant J.P. Morgan Securities LLC (“J.P. Morgan”) acted as a lead underwriter of

the IPO of 2.07 million shares of Molycorp Preferred Stock in February 2011. J.P. Morgan also

acted as a lead underwriter of the Secondary Offering of 11.5 million shares of Molycorp common

stock in June 2011. J.P. Morgan is statutorily liable under §§12 and/or 15 of the 1933 Act for the

materially untrue statements incorporated and contained in the offering documents. J.P. Morgan

failed to perform adequate due diligence and/or did not possess reasonable grounds for the belief that

the statements contained in and incorporated in the offering documents were true and without

omissions of any material facts and were not misleading.

61. Defendant Knight Capital Americas, L.P. (“Knight”) acted as an additional

underwriter of the Secondary Offering of 11.5 million shares of Molycorp common stock in June

2011. Knight is statutorily liable under §§12 and/or 15 of the 1933 Act for the materially untrue

statements incorporated and contained in the offering documents. Knight failed to perform adequate

due diligence and/or did not possess reasonable grounds for the belief that the statements contained

in and incorporated in the offering documents were true and without omissions of any material facts

and were not misleading.

62. Defendant Dahlman Rose & Company, LLC (“Dahlman”) acted as an additional

underwriter of the Secondary Offering of 11.5 million shares of Molycorp common stock in June

2011. Dahlman is statutorily liable under §§12 and/or 15 of the 1933 Act for the materially untrue

statements incorporated and contained in the offering documents. Dahlman failed to perform

adequate due diligence and/or did not possess reasonable grounds for the belief that the statements

contained in and incorporated in the offering documents were true and without omissions of any

material facts and were not misleading.

- 24 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 30 of 137

63. Defendant Stifel, Nicolaus & Company Incorporated (“Stifel”) acted as an additional

underwriter of the Secondary Offering of 11.5 million shares of Molycorp common stock in June

2011. Stifel is statutorily liable under §§12 and/or 15 of the 1933 Act for the materially untrue

statements incorporated and contained in the offering documents. Stifel failed to perform adequate

due diligence and/or did not possess reasonable grounds for the belief that the statements contained

in and incorporated in the offering documents were true and without omissions of any material facts

and were not misleading.

64. Defendant BNP Paribas Securities Corp. (“BNP”) acted as an additional underwriter

of the Secondary Offering of 11.5 million shares of Molycorp common stock in June 2011. BNP is

statutorily liable under §§12 and/or 15 of the 1933 Act for the materially untrue statements

incorporated and contained in the offering documents. BNP failed to perform adequate due

diligence and/or did not possess reasonable grounds for the belief that the statements contained in

and incorporated in the offering documents were true and without omissions of any material facts

and were not misleading.

65. Defendant CIBC World Markets Corp. (“CIBC”) acted as an additional underwriter

of the Secondary Offering of 11.5 million shares of Molycorp common stock in June 2011. CIBC is

statutorily liable under §§12 and/or 15 of the 1933 Act for the materially untrue statements

incorporated and contained in the offering documents. CIBC failed to perform adequate due

diligence and/or did not possess reasonable grounds for the belief that the statements contained in

and incorporated in the offering documents were true and without omissions of any material facts

and were not misleading.

- 25 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 31 of 137

66. Defendant Piper Jaffray & Co. (“Piper Jaffray”) acted as an additional underwriter of

the Secondary Offering of 11.5 million shares of Molycorp common stock in June 2011. Piper

Jaffray is statutorily liable under §§12 and/or 15 of the 1933 Act for the materially untrue statements

incorporated and contained in the offering documents. Piper Jaffray failed to perform adequate due

diligence and/or did not possess reasonable grounds for the belief that the statements contained in

and incorporated in the offering documents were true and without omissions of any material facts

and were not misleading.

67. Defendant RBS Securities Inc. (“RBS”) acted as an additional underwriter of the

Secondary Offering of 11.5 million shares of Molycorp common stock in June 2011. RBS is

statutorily liable under §§12 and/or 15 of the 1933 Act for the materially untrue statements

incorporated and contained in the offering documents. RBS failed to perform adequate due diligence

and/or did not possess reasonable grounds for the belief that the statements contained in and

incorporated in the offering documents were true and without omissions of any material facts and

were not misleading.

68. Defendants Morgan Stanley, J.P. Morgan, Knight, Dahlman, Stifel, BNP, CIBC,

Piper Jaffray and RBS are collectively referred to herein as the “Underwriter Defendants.” The

Underwriter Defendants shared $5.9 million and $20.4 million in underwriting fees in connection

with the February 2011 Preferred Stock IPO and the June 2011 common stock Secondary Offering,

respectively.

69. Defendants Molycorp, Smith, Allen, Ashburn, Ball, Bhappu, Cogut, Dolan, Kristoff,

Machiels, Henry, Thompson, Morgan Stanley, J.P. Morgan, Knight, Dahlman, Stifel, BNP, CIBC,

Piper Jaffray and RBS are collectively referred to herein as the “1933 Act Defendants.”

- 26 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 32 of 137

Control Person/Group Published Information Allegations

70. It is appropriate to treat the 1934 Act Defendants, except Molycorp, collectively as a

group for pleading purposes and to presume that the materially false, misleading and incomplete

information conveyed in the Company’s public filings, press releases and public statements, as

alleged herein was the result of the collective actions of the 1934 Act Defendants identified above.

The 1934 Act Defendants, by virtue of their high-level positions within the Company, directly

participated in the management of the Company, were directly involved in the day-to-day operations

of the Company at the highest levels and were privy to confidential proprietary information

concerning the Company and its business, operations, prospects, growth, finances and financial

condition, as alleged herein.

71. The 1934 Act Defendants were involved in drafting, producing, reviewing, approving

and/or disseminating the materially false and misleading statements and information alleged herein,

were aware of or recklessly disregarded the fact that materially false and misleading statements were

being issued regarding the Company, and approved or ratified these statements, in violation of

securities laws.

72. As officers and controlling persons of a publicly-held company whose common stock

was, and is, registered with the SEC pursuant to the 1934 Act, and was traded on the New York

Stock Exchange (“NYSE”), and governed by the provisions of the federal securities laws, the 1934

Act Defendants each had a duty to promptly disseminate accurate and truthful information with

respect to the Company’s financial condition and performance, growth, operations, financial

statements, business, markets, management, earnings, present and future business prospects, and to

correct any previously issued statements that had become materially misleading or untrue, so that the

- 27 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 33 of 137

market price of the Company’s publicly-traded securities would be based upon truthful and accurate

information. The 1934 Act Defendants’ material misrepresentations and omissions during the Class

Period violated these specific requirements and obligations.

73. The 1934 Act Defendants, by virtue of their positions of control and authority as

officers and/or directors of Molycorp, were able to and did control the content of the various SEC

filings, press releases and other public statements pertaining to the Company during the Class

Period. As such, the 1934 Act Defendants were controlling persons of Molycorp within the meaning

of §20(a) of the 1934 Act. Further, the 1934 Act Defendants were provided with copies of the

documents alleged herein to be misleading prior to or shortly after their issuance and/or had the

ability and/or opportunity to prevent their issuance or cause them to be corrected. Accordingly, they

are responsible for the accuracy of the public reports and releases detailed herein.

74. With respect to the 1934 Act claims, each of the 1934 Act Defendants is liable as a

participant in a scheme, plan and course of conduct that operated as a fraud and deceit on Class

Period purchasers of the Company’s securities. Throughout the Class Period, defendants

disseminated materially false and misleading statements and suppressed material adverse facts about

the Company.

75. Among other actionable conduct detailed herein, the 1934 Act Defendants, inter alia ,

failed to timely disclose that the Mountain Pass mine would not produce commercially viable

amounts of HREE, particularly dysprosium and terbium as daily analyses of 20 to 30 samples of

Mountain Pass ore revealed that these elements could not be obtained in commercially significant

quantities from the mine. During investigations of float tests, which is a process that physically

separates particles of different REEs based on the ability of air bubble to selectively adhere to

- 28 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 34 of 137

mineral surfaces in a mineral/water slurry, of Mountain Pass ore conducted during the Class Period,

the Company failed to identify commercially significant quantities of HREE at Mountain Pass.

Further, internal reports dated as far back as 2009 indicated that HREE did not exist at Mountain

Pass mine and that lack of HREEs at Mountain Pass mine were recorded in lab notebooks and

reported in Molycorp’s computerized Laboratory Information Management System (known

internally at Molycorp as “LIMS”), which was widely accessible to the Company personnel,

including Company management.

SUBSTANTIVE ALLEGATIONS

Background

76. In 1949, REEs were discovered at the Mountain Pass mine, which is located just

north of the unincorporated community of Mountain Pass, California. The next year, Molybdenum

Corporation of America acquired the mining claims at Mountain Pass. In 1952, production of

certain LREEs first began under the auspices of Molybdenum Corporation of America.

77. During the 1960s and through the 1980s, the Mountain Pass mine was the world’s

dominant source of rare earth oxides. The increase of the Company’s production during that time

period was driven by the Company’s low-cost production and the rapid rise in demand for LREEs,

particularly europium for use in television and computer monitors, and cerium for glass polishing.

By 2000, however, virtually all such LREEs were imported from China. Due to the huge supply of

LREEs in China and a series of environmental/regulator problems ( e.g. , a pipeline spill of

contaminated water), production of REEs ceased at the Mountain Pass mine in 2002. Since 2002,

the U.S. has lost virtually all of its capacity in the global rare earth supply chain.

- 29 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 35 of 137

78. At the time Mountain Pass ceased producing REEs in 2002, Unocal Corporation

owned the mine and, in 2005, sold the facility to Chevron Mining, Inc. Molycorp Minerals, LLC,

was formed in June 12, 2008 to purchase the Mountain Pass mine from Chevron Mining, Inc.

Thereafter, Molycorp Minerals, LLC embarked on a campaign to return Mountain Pass to the

position of a dominant global player in the REE market – versus a dormant strip mining property –

through what was known as the “mine-to-magnets” strategy. In March 2010, Molycorp was formed

for the purpose of taking the Company public.

79. On July 29, 2010, Molycorp became a publicly-traded firm through the IPO of 28.1

million shares at $14.00 per share. The Company’s common stock trades under the ticker symbol

“MCP” on the NYSE.

Molycorp’s Modernization and Expansion Plan for Mountain Pass: “Project Phoenix”

80. In view of purported “strong industry fundamentals” and “reduced Chinese supply

and strong price increases” for REEs, beginning in 2010, the Company began the process of

recommencing mining operations at Mountain Pass and planning for the modernization and

expansion of the facility. One of the purposes underlying the modernization and expansion plan of

Mountain Pass was to achieve the Company’s “mine-to-magnets” strategy, which would purportedly

make Molycorp the only vertically integrated producer of high-performance permanent rare earth

magnets that would incorporate the use of highly-valued HREEs such as dysprosium and terbium.

Repeatedly through the Class Period, defendants assured investors that demand for these products

was expected to increase in a range between 10%-15% annually through 2015. The defendants

continually piqued investors’ interest in the Company by stressing that China now produced virtually

all REEs globally, was restricting its exports to the rest of the world, while China’s internal

- 30 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 36 of 137

consumption continued to expand. Indeed, Molycorp was to be the answer to Chinese dominance,

particularly as it related to HREEs.

81. During the Class Period, the Company’s modernization and expansion plan for

Mountain Pass was referred to by defendants as “Project Phoenix.” Phase I of Project Phoenix

envisions the production rate of 19,500 metric tons of REE oxides from Mountain Pass by no later

than the end of 2012. Phase II of Project Phoenix, which largely requires the completion of

advanced mechanical mining operations at Mountain Pass, envisions the production of 40,000 metric

tons of REE oxides as early as mid-2013.

82. According to the Company’s public filings with the SEC and various presentations

made to investors, not only would Molycorp produce HREEs during Phase I and II of Project

Phoenix, but the Company would transport dysprosium and terbium mined from Mountain Pass to

off-site facilities to produce rare earth metals and alloys. The Company’s public filings also claimed

that, the metal and alloy production would occur at Mountain Pass. The Company’s public filings

with the SEC specifically stated that defendants Smith, Allen, Ashburn and Burba’s compensation

during the Class Period was directly tied to their ability to hit specific Project Phoenix completion

milestones. As such, throughout the Class Period, defendants Smith, Allen, Ashburn and Burba had

intimate knowledge of the status of Project Phoenix, as well as knowledge of whether commercial

volume of HREEs, particularly dysprosium and terbium, existed at Mountain Pass at all.

Defendants’ Unlawful Scheme

83. Just like the “gold-rush” days of the 19th century, defendants assured eager investors

that the development of the Mountain Pass mine was a sure-bet to meet growing global demand for

REEs, as well as to address global scarcity. For example, defendants repeatedly informed investors:

- 31 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 37 of 137

China has dominated the global supply of [rare earth oxides or “REOs”] for the last ten years and, according to IMCOA, accounted for approximately 97% of global REO production in 2008. Even with our planned production, global supply is expected by analysts to remain tight due to the combined effects of growing demand and actions taken by the Chinese government to restrict exports. . . . China’s internal consumption of rare earths is expected to continue to grow, leaving the Rest of World with less supply during a period of projected increasing global demand.

* * *

IMCOA estimates there is a [sic] currently a global deficit in REO supply, which anticipated [sic] to continue without the advent of production from new projects, such as Mountain Pass. Limits on rare earth exports from China and the lack of available substitutes make the development of new sources of REEs essential to meet the growing demand for existing and emerging technologies . . . .

84. Further, with respect to valuable, highly-valued HREEs, such as dysprosium and

terbium, defendants misleadingly informed investors that the Mountain Pass mine would be a

commercially significant source of supply. For instance, defendants stated: “ [w]e’ll be producing 10

different rare earth elements as part of Phase 1 and as part of Phase 2 [of ‘Project Phoenix’], and

that will be . . . Dysprosium [and] Terbium ”; “we look at these [heavy] rare earth elements that

[Molycorp will] be producing in commercial quantities ”; “[w]e intend to transport . . . dysprosium

[and] terbium . . . from our Mountain Pass facility to Molycorp Silmet AS and MMA to produce

rare earth metals and alloys ”; “[t]hat’s all from the Mountain Pass rare earth ore body” ; and

“what it does is it really makes it sound as if – the deposit like that Mountain Pass deposits is

disadvantaged on that [HREE] side and, in fact, what it’s really saying is, is that we have a very

high ore grade .” Defendants also falsely assured investors during the Class Period that the

Mountain Pass mine was particularly crucial given the “ lack of available substitutes ” for rare earth

oxides at a time of a “global deficit” in supply. Further, defendants maintained their rouse by failing

to inform investors that in August 2011, joint-venture discussions with Hitachi Metals to

- 32 -

Case 1:12-cv-00292-WJM-KMT Document 60 Filed 07/31/12 USDC Colorado Page 38 of 137

manufacture magnets utilizing HREEs – pursuant to the Company’s purported “mine-to-magnets”

strategy – collapsed because Hitachi Metals had concluded that there were not commercial volumes

of HREEs at Mountain Pass.

85. Defendants’ Class Period statements regarding the Mountain Pass mine being a

source of commercial quantities of HREEs were critical to investors and their investment decisions.

For instance, the U.S. Department of Energy (“DOE”) has concluded that between 2011 and 2015,

dysprosium and terbium will be crucial to the clean energy industry and the elements would suffer

critically high supply shortages for the foreseeable future. The 2011 DOE report made several

critical conclusions in this regard: