Embed Size (px)

Citation preview

1

In Pari Delicto: What Are the Recent Cases Saying?

ABA Business Bankruptcy CommitteeWebinar and Teleconference

December 10, 2010

2

Panelists

Kit Weitnauer Alston & Bird LLP (Atlanta)

David M. Stern Klee, Tuchin, Bogdanoff & Stern LLP (Los Angeles)

Debbie J. McComasHaynes and Boone LLP (Dallas)

Eric D. Madden Diamond McCarthy LLP (Dallas)

3

What is in pari delicto?

Meaning – “in equal fault”

Purpose – to deter illegality and to keep courts from serving as a “referee between thieves”

Affirmative defense versus standing doctrine– Majority rule: defense– Wagoner rule: standing

4

Imputation General rule – agent’s actions are imputed to the

company

Adverse interest exception – no imputation if agent was acting adversely to company’s interest– Standard: total abandonment– Looting is the classic example– Fraud for the company vs. against the company

Sole actor rule – imputation still applies if agent and company are “one and the same”

5

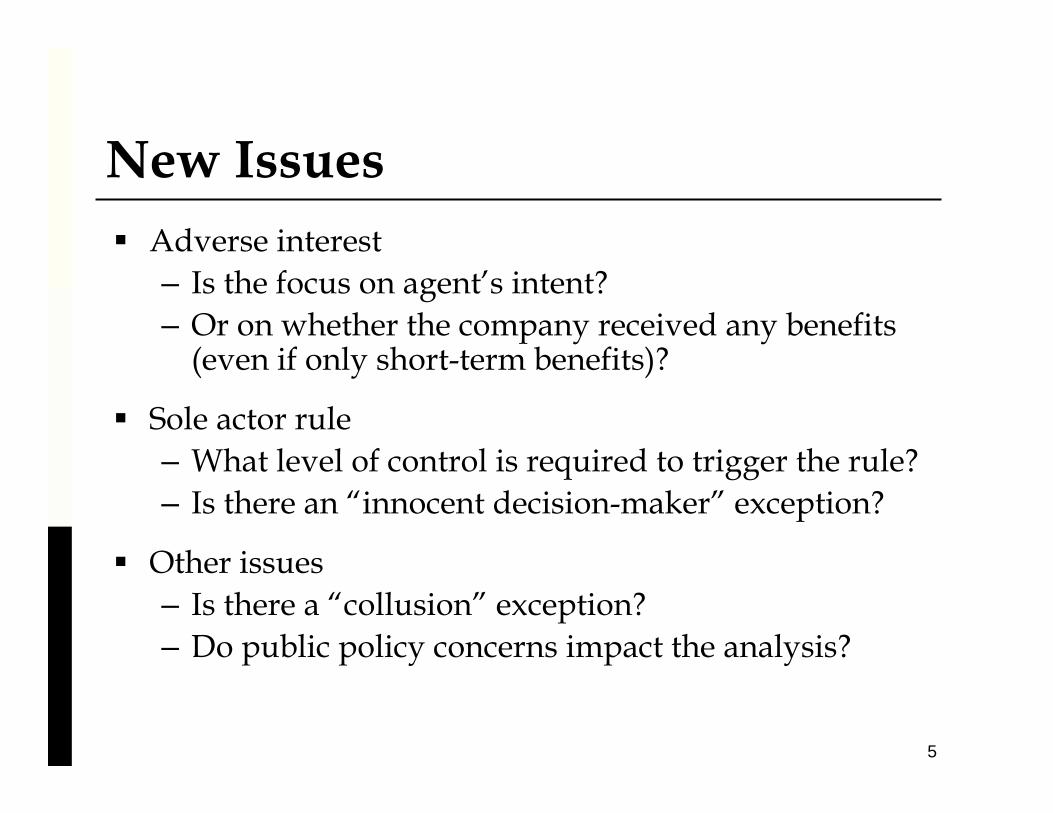

New Issues Adverse interest

– Is the focus on agent’s intent?– Or on whether the company received any benefits

(even if only short-term benefits)?

Sole actor rule– What level of control is required to trigger the rule?– Is there an “innocent decision-maker” exception?

Other issues– Is there a “collusion” exception?– Do public policy concerns impact the analysis?

6

Leading Cases Cenco Inc. v. Seidman & Seidman, 686 F.2d 449

(7th Cir. 1982) Schacht v. Brown, 711 F.2d 1343 (7th Cir. 1983) Shearson Lehman Hutton, Inc. v. Wagoner, 944 F.2d 114

(2d Cir. 1991) Bankruptcy Services, Inc. v. Ernst & Young (In re CBI

Holding Co.), 529 F.3d 432 (2d Cir. 2008) NCP Litigation Trust v. KPMG LLP, 187 N.J. 353 (NJ 2006) Thabault v. Chait, 541 F.3d 512 (3d Cir. 2008)

7

AHERF: Issues Certified What is the proper test under Pennsylvania law for determining

whether an agent’s fraud should be imputed to the principal when it is an allegedly non-innocent third-party that seeks to invoke the law of imputation to shield itself from liability?

Does the doctrine of in pari delicto prevent a corporation from recovering against its accountants for breach of contract, professional negligence or aiding and abetting a breach of fiduciary duty if those accountants conspired with officers of the corporation to misstate the corporation’s finances to the corporation’s ultimate detriment?

Official Cttee. of Unsecured Creditors of Allegheny Health Ed. & Research Foundation v. PWC, 2008 U.S. App. LEXIS 18823 (3rd Cir. July 1, 2008)

8

AHERF: When In Pari DelictoApplies In pari delicto applies if “Plaintiff is an active, voluntary

participant in the wrongful conduct or transactions for which it seeks redress and bears substantially equal or greater responsibility for the illegality.”

AHERF v. PWC, 989 A.2d 313 (Pa. 2010)

9

AHERF: The Proper Test Under Pennsylvania Law Policy considerations to be taken into account in novel

settings Application of the defense in the corporate auditing

context “Here, we have not been presented with sufficient

information concerning all relevant factors to lend our support to any general rule which would uniquely disable auditors, as a class, from asserting an in pari delicto defense.

10

AHERF: Imputation Acknowledges general principle Adverse interest exception

good faith/negligence – liberal test for corporate benefit

collusive or fraudulent activity – no benefit as a matter of law

benefit determined in light of a reasonable third party in its dealings with the agent

11

APPLICATION OF AHERFSTANDARD

AHERF v. PWC, 607 F.3d 346 (3rd Cir. 2010)

Adelphia Recovery Trust v. Bank of America, 2010 U.S. App. LEXIS 90836 (S.D.N.Y. Sept. 1, 2010)

12

The Second Circuit Perspective 2nd Circuit (Kirshner v. KPMG) and Delaware

Chancery Court (In re American International Group, Inc., 998 A.2d 280 (Del. 2010)) certified questions to the New York Court of Appeals.

New York Court of Appeals issued a 4-3 decision favoring defendants.

13

Second Circuit: Adverse Interest –Insider’s State of Mind

District Court: The Wagoner rule addresses the question of who has a claim for relief, which, in the context of fraud, means who has been harmed and who has benefitted by the fraudulent conduct alleged ... [The question is] not ... the perpetrators’ ... motives.

Because we considered New York law and our own language in CBI to create some uncertainty as to the significance of the insiders' intent, one question that we ... asked [was], “Whether the adverse interest exception is satisfied by showing that the insiders intended to benefit themselves by their misconduct?” ... The Court of Appeals answered, “No.”

14

Second Circuit: Harm to DebtorDistrict Court: “the Trustee must allege that the corporation was

harmed by the scheme, rather than being one of its beneficiaries.”Here, “the gravamen of the Trustee's allegations is not that the insiders

stole assets from Refco, but rather that the insiders' fraudulent scheme was to steal for Refco - to inflate the value of Refco's interests on behalf of Refco itself by maintaining the illusion that Refco was fast-growing, highly profitable, and able to satisfy its substantial working capital needs without having to borrow money.”

The District Court considered the argument that the debtor was injured “when it incurred $1.4 billion in new LBO debt and was no longer able to repay the funds diverted from affiliates ....” He rejected this “harm,” pointing out that “[i]t is a basic principle of corporate finance that extending credit to a distressed entity in itself does the entity no harm.”

15

Second Circuit: Harm to Debtor Because the Trustee had argued on appeal to this Court

that the adverse interest exception does not require an allegation of harm to the corporation, and because we considered New York law and our own language in CBIto create some uncertainty as to whether the adverse interest exception required harm to the corporation, another question asked, “Whether the exception is available only where the insiders' misconduct has harmed the corporation?” The Court of Appeals answered, “Yes.”

16

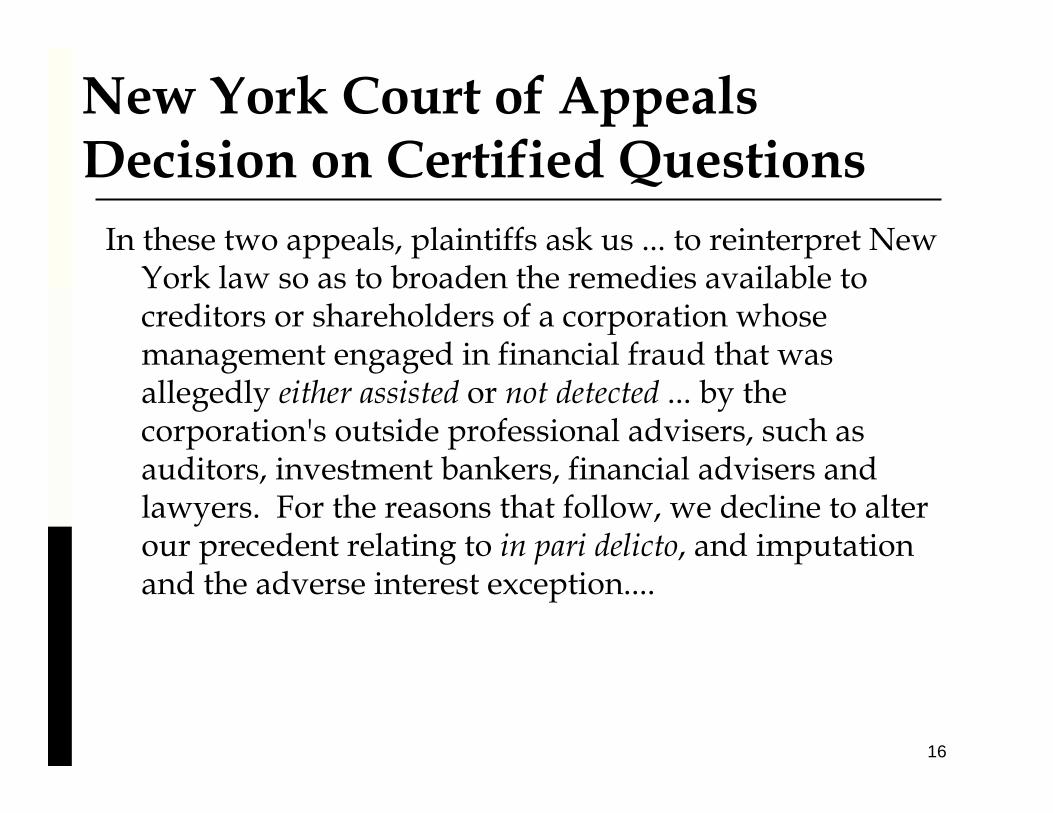

New York Court of Appeals Decision on Certified Questions

In these two appeals, plaintiffs ask us ... to reinterpret New York law so as to broaden the remedies available to creditors or shareholders of a corporation whose management engaged in financial fraud that was allegedly either assisted or not detected ... by the corporation's outside professional advisers, such as auditors, investment bankers, financial advisers and lawyers. For the reasons that follow, we decline to alter our precedent relating to in pari delicto, and imputation and the adverse interest exception....

17

New York Court of Appeals Decision on Certified Questions: In Pari DelictoThe doctrine of in pari delicto mandates that the courts will

not intercede to resolve a dispute between two wrongdoers. This principle has been wrought in the inmost texture of our common law for at least two centuries.... The doctrine survives because it serves important public policy purposes. First, denying judicial relief to an admitted wrongdoer deters illegality. Second, in pari delicto avoids entangling courts in disputes between wrongdoers. ... “[N]o court should be required to serve as paymaster of the wages of crime, or referee between thieves. Therefore, the law will not extend its aid to either of the parties or listen to their complaints against each other, but will leave them where their own acts have placed them.”

18

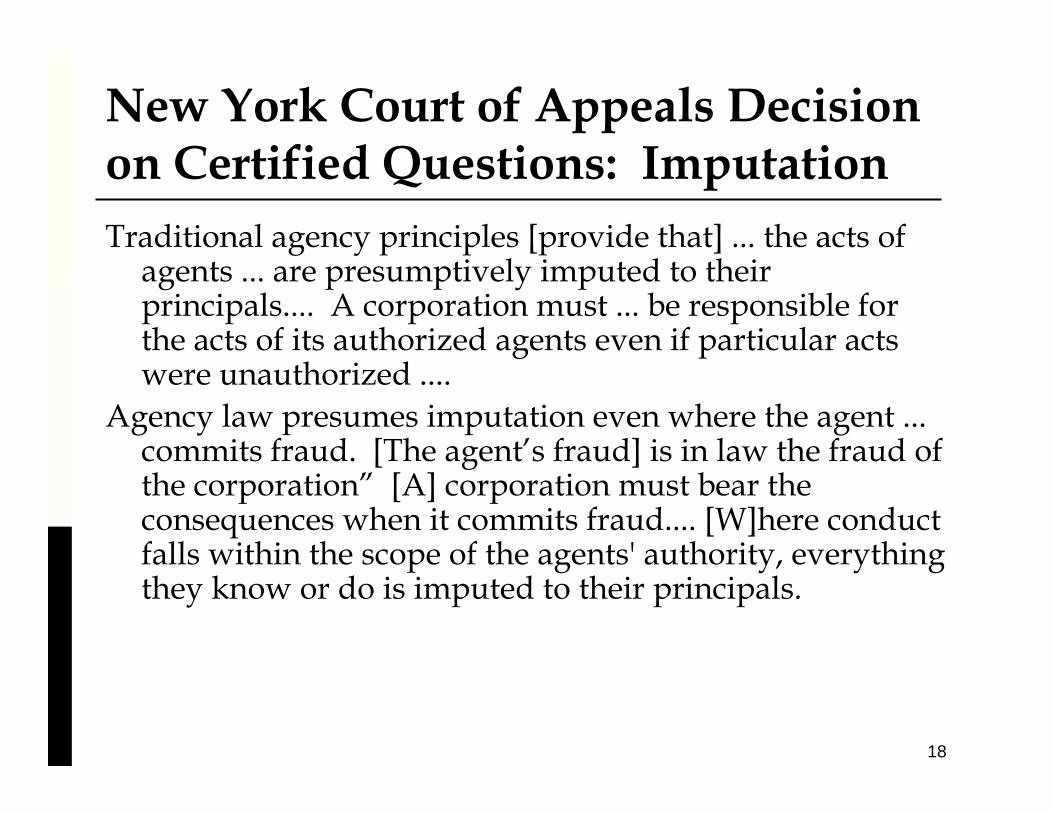

New York Court of Appeals Decision on Certified Questions: ImputationTraditional agency principles [provide that] ... the acts of

agents ... are presumptively imputed to their principals.... A corporation must ... be responsible for the acts of its authorized agents even if particular acts were unauthorized ....

Agency law presumes imputation even where the agent ... commits fraud. [The agent’s fraud] is in law the fraud of the corporation” [A] corporation must bear the consequences when it commits fraud.... [W]here conduct falls within the scope of the agents' authority, everything they know or do is imputed to their principals.

19

New York Court of Appeals Decision on Certified Questions: Imputation[T]he presumption that agents communicate information to

their principals ... is a legal presumption that governs in every case, except where the corporation is actually the agent's intended victim. Where the agent is defrauding someone else on the corporation's behalf, the presumption of full communication remains in full force and effect.

[T]here are strong considerations of public policy underlying this precedent: imputation fosters an incentive for a principal to select honest agents and delegate duties with care.

20

New York Court of Appeals Decision on Certified Questions: Adverse InterestTo come within the [adverse interest] exception, the agent

must have totally abandoned his principal's interests and be acting entirely for his own or another's purposes. This rule ... reserves this most narrow of exceptions for those cases - outright theft or looting or embezzlement -where the insider's misconduct benefits only himself or a third party....

Fraud on behalf of a corporation is not the same thing as fraud against it... So long as the corporate wrongdoer's fraudulent conduct enables the business to survive ... this testis not met....

21

New York Court of Appeals Decision on Certified Questions: Adverse Interest

[A]ny harm from the discovery of the fraud ... does not bear on whether the adverse interest exception applies. The disclosure of corporate fraud nearly always injures the corporation. If that harm could be taken into account, a corporation would be able to invoke the adverse interest exception and disclaim virtually every corporate fraud ... as soon as it was discovered and no longer helping the company. Generally, a fraud will suit the interests of both a company and its insiders for as long as it remains a secret ..., and leads to negative consequences for both when disclosed.

22

New York Court of Appeals Decision on Certified Questions: Intent and Illusory Benefits

[T]he Litigation Trustee asks us to make ... the adverse interest exception depend upon whether “corporate insiders ... intended to benefit themselves personally and actually received personal benefits and/or that the company received only short term benefits but suffered long term harms” (emphasis added). [This] ... would “explode” the exception .... This is so because fraudsters are presumably not, as a general rule, motivated by charitable impulses, and a company victimized by fraud is always likely to suffer long-term harm once the fraud becomes known. The Trustee's proposed rule would limit imputation to fraudsters so inept they gain no personal benefit and unexposed frauds, which is another way of saying the adverse interest exception would become a dead letter ....

23

NCP and AHERF Rules

Alternatively, the Litigation Trustee urges us to take the approach to in pari delicto and imputation adopted by ... NCP ... or ... AHERF.

24

... NCP[In NCP] ... the New Jersey Supreme Court held that “when an auditor is negligent within the scope of its engagement, the imputation doctrine does not prevent corporate shareholders from seeking to recover”. These corporate shareholders must be “innocent,” though: an auditor may still assert the “imputation defense” against those shareholders who engaged in the fraud; or who, by way of their role in the company, should have been aware of the fraud; or who owned large blocks of stock and therefore arguably possessed some ability to oversee the company's operations. Thus, the New Jersey rule calls for the relative faults of the company/shareholders and auditors to be sorted out by the fact finder as matters of comparative negligence and apportionment.

25

... AHERF[In AHERF] the Pennsylvania Supreme Court first rejected the approach taken by New Jersey, concluding that “the best course ... for Pennsylvania common law [was] to continue to recognize the availability of the in pari delicto defense ..., via the necessary imputation, in the negligent-auditor context” where the plaintiff's culpability was equal to or greater than the defendant's. But as to the issue of auditor collusion..., the court took a different view, holding that imputation ... was unavailable where an auditor had not proceeded in material good faith.

26

... considerations of EquityThe NCP and AHERF decisions were both animated by considerationsof equity - the notion that although the plaintiffs stood in the shoes of the principal malefactors, any recovery they achieved from the defendant[s] - which were alleged to have been either negligent or complicit - would, in fact, only benefit innocent shareholders or unsecured creditors and so should not be barred by in pari delicto. The Pennsylvania Supreme Court reflected this sentiment when it said that it would be “ill-advised, if not perverse ... [to] apply ... imputation as against AHERF” because that “would result in the corporation being charged with knowledge as against a third party whose agents actively and intentionally prevented those in AHERF's governing structure who were non -participants in the fraud from acquiring such knowledge.”

27

... public policy

We are not persuaded ... that the equities are quite so obvious. ... Why should the interests of innocent stakeholders of corporate fraudsters trump those of innocent stakeholders of the outside professionals who are the defendants in these cases? ...... plaintiffs' proposals [create] a double standard whereby theinnocent stakeholders of the corporation's outside professionals are held responsible for the sins of their errant agents while the innocent stakeholders of the corporation itself are not charged with knowledge of their wrongdoing agents. And, of course, the corporation's agents would almost invariably play the dominant role in the fraud and therefore would be more culpable than the outside professional's agents who allegedly aided and abetted the insiders or did not detect the fraud at all or soon enough.

28

... public policy... outside professionals ... already are at risk for large settlements and judgments in the litigation that inevitably follows the collapse of an Enron ... type scandal.... It is not evident that expanding the adverse interest exception or loosening imputation principles under New York law would result in any greater disincentive for professional malfeasance or negligence than already exists. Yet the approachadvocated by the Litigation Trustee and the derivative plaintiffs would allow the creditors and shareholders of the company that employs miscreant agents to enjoy the benefit of their misconduct without suffering the harm.The principles of in pari delicto and imputation, with its narrow adverse interest exception, which are embedded in New York law, remain sound. The speculative public policy benefits advanced ... do not ... outweigh the important public policies that undergird our precedents in this area or the importance of maintaining the “stability and fair measure of certainty which are prime requisites in any body of law.”

29

Adverse Interest and exceptions in other jurisdictions

Kirschner is the last word but not the only word. It essentially holds that imputation in the normal principal/agent context is sufficient, expressly rejecting the holdings in NCP and AHERF.

Our sister states fashioned carve-outs from traditional agency law in cases of corporate fraud so as to deny the in pari delictodefense to negligent or otherwise culpable outside auditors (New Jersey) and collusive outside professionals (Pennsylvania).

The NY Court of Appeals rejected, without citation, a variety ofother articulations of the adverse interest exception, including some in the 2nd Circuit, which may well reappear in cases in other jurisdictions.

30

Adverse Interest – other jurisdictions

Schact: Rejecting the “seriously flawed assumption … that the fraudulent prolongation of a corporation's life beyond insolvency is automatically to be considered a benefit to the corporation's interests.”711 F.2d at 1343 (also questioning whether “wrongdoing … to conceal the true condition of the corporation” can ever be beneficial).

Notably, Schact is from the same court, the 7th Circuit, that had originated the concept, relied upon in Kirschner, that “[f]raud on behalf of a corporation is not the same thing as fraud against it.” 686 F.2d at 456.

Thabault: A 3rd circuit decision rejecting a pure imputation test as well as a black letter rule “that the ‘adverse interest’ exception does not apply [where the wrongdoer] was not stealing from the company.”Agreeing with Schact, Court holds that adverse interest exception is available if wrongdoer’s “conduct allowed [company] to continue past the point of insolvency.” 541 F.3d at 528-29

31

CBI: Although clearly no longer the law in New York, and maybe in the 2nd Circuit, CBI affirmed a bankruptcy court judgment because “the evidence showed that the fraud was perpetrated for the purpose of obtaining a bigger bonus for Castello, and to preserve Castello's personal control over the company [with the result that] management's knowledge should not be imputed to CBI.” 529 F.3d at 443. This formulation was plainly rejected in both the New York Court of Appeals’ decision and the Second Circuit’s follow-on decision in Kirschner, but it may still be citable in other jurisdictions.

In re Today’s Destiny, 388 B.R. 737 (Bankr. S.D. Tex. 2008): Although not expressly reaching the question of how adverse interest is determined in Texas, the Court holds that unless the plaintiff was guilty of unlawful acts, “pari delicto is not an automatic bar.” Id. at 749.

Of course there are courts that are equally adamant about the inapplicability of the adverse interest exception as long as the company “received some benefit [however temporary] from the Insiders’actions.” In re Scott Acquisition Corp., 2007 Bankr. LEXIS 643, *16 (Bankr. D. Del. Mar. 6, 2007).

Adverse Interest – other jurisdictions

32

Adverse Interest – comparative fault Today’s Destiny hints at another path to dealing with adverse interest and

pari delicto generally: comparative fault.

In Cenco, Judge Posner noted that state laws (or in some instances decisions) replacing contributory negligence with comparative negligence might suggest a similar treatment for in pari delicto. 686 F.2d at 453-54. He did not adopt proportionate responsibility because the Illinois statute at issue had an effective date after the commencement of trial in the case.

Subsequent cases have suggested proportionate responsibility might apply in the context of corporate wrongdoing and in pari delicto: NCP: “[B]enefit would not be a complete bar to liability but only a

factor in apportioning damages.” 901 A.2d at 888. Today’s Destiny: “Allowing contribution between joint tortfeasors for

liability arising from a single course of allegedly shared criminal conduct does not conflict with in pari delicto's policy goals.” 388 B.R. at 750.

Baird v. Jones, 27 Cal.Rptr.2d 232, 236 (Ct. App. 1993): “Consistent with the Supreme Court's view, we conclude comparative fault principles should be applied to intentional torts, at least to the extent that comparative equitable indemnification can be applied between concurrent intentional tortfeasors.”

33

Sole Actor: The Exception to the Exception In those jurisdictions where the adverse interest exception is viable, be

aware of the sole actor exception. As succinctly summarized in CBI, “the ‘sole actor’ rule [is] an exception to

the exception [that] imputes the agent's knowledge to the principal …where the principal and agent are one and the same or, in the corporate context, where the principal is a corporation and the agent is its sole shareholder.” 529 F.2d at 453 n.9.

This exception to an exception has been, at best, inconsistently applied. Cobalt Multifamily Investors I, LLC v. Shapiro, 2009 WL 2058530, * 8 n.13 (S.D.N.Y. July 15, 2009) (“the Court finds that the presence of the shareholders with the authority to remove the managers defeats the sole actor rule”); Official Comm. of Unsecured Creditors v. R.F. Lafferty & Co., 267 F.3d 340, 360 (3d Cir. 2001) (“[W]e reject the Committee's argument that the exception should not apply because several of the Debtors' directors merely acted negligently and did not perpetrate the fraud. The possible existence of any innocent independent directors does not alter the fact that the Shapiros controlled and dominated the Debtors.”).

34

Choice of Law

Internal affairs doctrine – law of the state of incorporation/formation

Choice-of-law principles – law of the state with most significant relationshipIn re Adelphia Communications Corp., 365 B.R. 24 (Bankr. S.D.N.Y. 2007)

In re Magnesium Corp. of Am., 399 B.R. 722 (Bankr. S.D.N.Y. 2009) In re Friedman’s Inc., 394 B.R. 623 (S.D. Ga. 2008) Collins & Aikman v. Stockman, 2010 WL 184074 (D. Del. 2010)

35

Question and Answer

This is the end of the presentation. There will be a brief opportunity for Question and Answer.