Embed Size (px)

Citation preview

July 18, 2013

RICK PORTER – DIRECTORNATURAL GAS REGULATORY ADVISORY SERVICES

Issues For An Expanding Energy Market Energy Bar Association – Houston ChapterJuly Luncheon

CAPITA

L, CONVE

RGEN

CE, C

APAC

ITY

– WHILE THE INDUSTRY IS OPTIMISTIC, CHALLENGES EXIST

2

4.57

4.22

4.21

4.21

4.13

4.08

4.01

3.94

3.80

3.74

Safety

Economic growth

Gas supply reliability

Rate and regulatory certainty

Capital access and cost

Aging infrastructure

Gas price stability

Electric‐gas interdependency

Environmental activism

Aging work force

On a scale of 1 to 5, rate the most important long‐term issues to the gas industry.

No Impact

SignificantImpact

Capital, Capacity

Convergence, Capital, Capacity

Convergence, Capital, Capacity

Convergence, Capital, Capacity

Convergence, Capital, Capacity

Convergence, Capital, Capacity

Convergence, Capital, Capacity

Convergence, Capital, Capacity

Convergence, Capital, Capacity

Capital

Source: 2012 Black & Veatch Strategic Directions in the US Natural Gas Industry

Thesemarketissuesrequireregulatorystrategies

3

3.44

3.43

3.23

3.22

3.10

3.10

Ability to recover operating costs and provide satisfactory earnings

Costs associated with maintaining satisfactory regulatory compliance

Level of investment made by your company in the natural gas industry

Predictability of natural gas prices

Level of natural gas prices to consumers

Stability of service pricing

– CAPITAL: HOW WILL UNCERTAINTY AFFECT EXPANSION AND MAINTENANCE INVESTMENTS

B&V Survey Question: To what extent do you believe regulatory uncertainty (at either the federal or state level) has an impact on the following issues?

No Impact

SignificantImpact

CAPIT

AL

4

CAPIT

AL– MAJORITY OF PIPELINE ARE EARNING LESS THAN

ALLOWED RETURNS ON EQUITY

‐40% ‐30% ‐20% ‐10% 0% 10% 20% 30% 40%

StingrayHIOS

PanhandleSea Robin

REXEl Paso Pipeline

ANRTennesseeTrunkline

Texas EasternTransco

Nothern NaturalColumbia Gas

VikingNorthern BorderColumbia Gulf

Return on Equity

Interstate Pipeline ‐ 2012 Return on Equity (Based on FERC Form 2 Data)

AverageEquityReturn:7.1%MedianEquityReturn:9.5%

Estimated FERC Allowed ROE

5

– CAPITAL: WILL REGULATORY UNCERTAINTY INHIBIT MIDSTREAM INVESTMENTS?

CAPIT

AL

Source: INGAA Foundation Study

• US and Canada capital spendincludes:

• Over 35,000 miles of transmission mainline

• 414,000 miles of gathering

• 304,000 miles of laterals to power plants

• 589 Bcf of Working Gas Capacity

• 32.5 Bcf/d of Processing Capacity

• Projected NGL and Oil expenditures expected to total $46 Billion over the same period

Bakken

Utica

Marcellus

Eagle Ford

Barnett‐Woodford Barnett Haynesville

Granite Wash

Woodford

Fayetteville

Cummulative US Capital Spend (2011‐2035)

Billions (2012$)

Gas Transmission Mainline $103.7Laterals $31.0Gathering Line $43.4Gas Pipeline Compression $9.5Gas Storage Fields $5.0Gas Processing Capacity $23.0

Total Gas Capital Requirement $215.6

GROWING GAS FIRED GENERATION REQUIRES ENHANCED PIPELINE CAPACITY AND SERVICES

6Source: Black & Veatch Energy Market Perspective

CONVERGENCE

The market share of natural gas is expected to increase ~25%

Total GWh: 4,223,743 Total GWh: 5,637,829

Coal 1,109,662 19.6%

Natural Gas 2,914,779 51.6%

Nuclear 716,514 12.7%

Hydro 285,262 5.0%

Renewable 552,339 9.8%

IGCC Coal 59,273 1.0% Other 11,372

0.2%

2037

Coal 1,578,941 37.3%

Natural Gas 1,061,906 25.1%

Nuclear 988,128 23.3%

Hydro 339,534 8.0%

Renewable 248,292 5.9%

IGCC Coal 6,942 0.2% Other 12,254

0.3%

2013

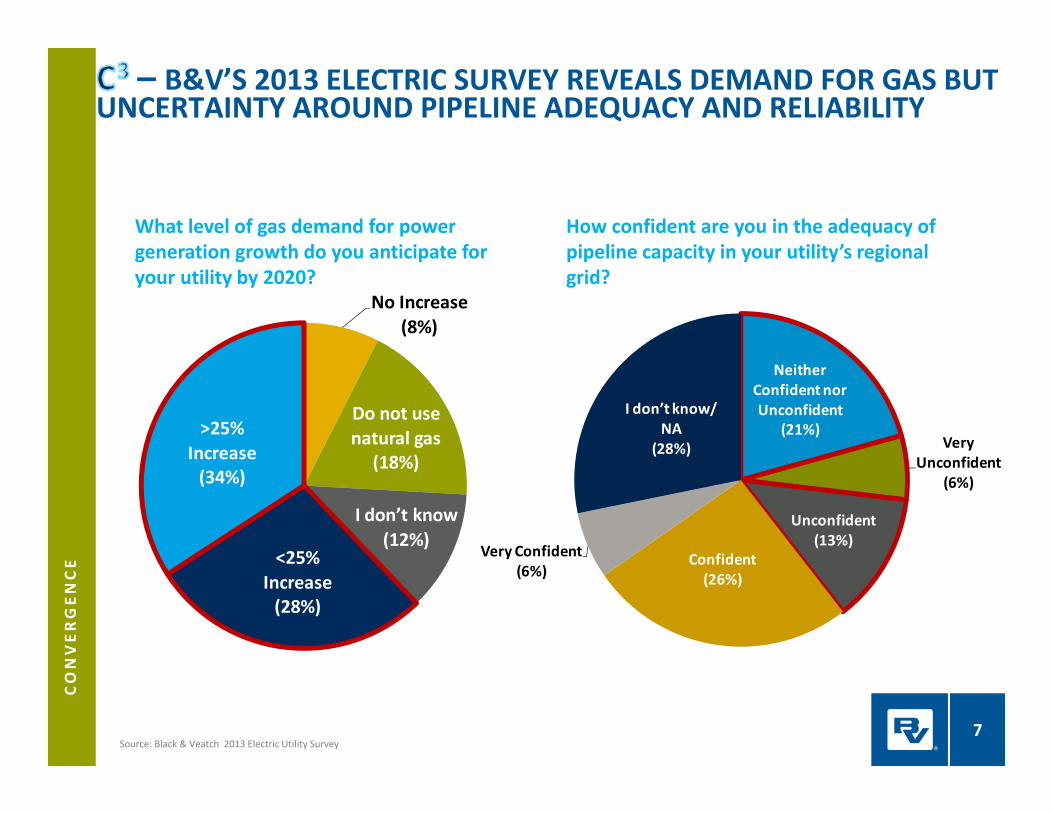

– B&V’S 2013 ELECTRIC SURVEY REVEALS DEMAND FOR GAS BUT UNCERTAINTY AROUND PIPELINE ADEQUACY AND RELIABILITY

7

CONVERGENCE

What level of gas demand for power generation growth do you anticipate for your utility by 2020?

How confident are you in the adequacy of pipeline capacity in your utility’s regional grid?

Source: Black & Veatch 2013 Electric Utility Survey

No Increase(8%)

Do not use natural gas

(18%)

I don’t know(12%)

<25% Increase(28%)

>25% Increase(34%)

Neither Confident nor Unconfident

(21%)Very

Unconfident(6%)

Unconfident(13%)

Confident(26%)

Very Confident(6%)

I don’t know/ NA

(28%)

Moreoptionssupportsgas/electricconvergence.

• Requirement 2 of Order 1000 creates opportunities for gas pipelines

• Implementation plans are not complete;

• RTOs should ask “What is the appropriate placement and relationship of new electric and gas facilities that will promote the most cost efficient delivery of energy to consumers and industry?”

– CONVERGENCE: INCREASED CHOICES FOR OPTIMIZING REGIONAL ENERGY GRIDS

8

Major PipelinesElectric TransmissionNortheast U.S.

CONVERGENCE

– COMMUNICATION AND SCHEDULING COORDINATION IS VALUABLE, HOWEVER…

Source:ISONewEnglandNUCPUCSymposium

9

CONVERGENCE

Beginwithanother'stoendwithyourown.‐BaltasarGracián

• Guidelines for new service design:• Use existing FERC designs as a point of departure;• Recognize the operational characteristics of the pipeline;• Understand the cost implications for the pipeline;• Redefine the value of the capacity – Don’t let basis or spreads establish price

• Don’t try to be all things to all shippers, group services according to their needs;

• Test the design when possible and let it evolve.

• An Evolving Flexible Rate Design• Gulfstream – Docket No.CP00‐6;• ANR Pipeline – Docket No.RP00‐332;• Kinetica Energy Express – Docket No.CP12‐49

– …SO IS GAS PIPELINE FLEXIBILITY.

10

CONVERGENCE

2012‐2022 Flows Increase2012‐2022 Flows Decrease2012‐2022 Flows StableNatural Gas Pipelines

11

– SHIFTING SUPPLY BASINS REDEFINE ALL MARKETS

Source: Black & Veatch Energy Market Perspective Analysis

CAPACIT

Y

Emerging Shale2012 2022

Marcellus Shale 5.4 16.8Haynesville Shale 7.5 10.4Eagle Ford Shale 3.8 6.0Barnett Shale 4.9 4.5Utica Shale 0.4 3.7

Projected Production (Bcf/d)

– DRAMATIC CAPACITY REALIGNMENTS CALL FOR RETHINKING MARKETS AND SERVICES

12

CAPACIT

Y

WillGulfCoastLNGExportsReviveLong‐Haulpipelinecapacity?

Sabine Pass

CameronGolden Pass Lake Charles

Bakken

UticaMarcellus

Eagle Ford

Barnett‐Woodford

Barnett Haynesville

Granite Wash Woodford

Fayetteville

Lake Charles

CameronGolden Pass

Sabine Pass

– MANAGE UNCERTAINTY, DON’T LET IT MANAGE YOU

13Ifthehighestaimofacaptainweretopreservehisship,hewouldkeepitinportforever.‐ ThomasAquinas

www.bv.com